Capital structure analysis for nrb bearings

19

CAPITAL STRUCTURE ANALYSIS PREPARED BY : SUMIT KR SINGH

-

Upload

sumit-kr-singh -

Category

Data & Analytics

-

view

79 -

download

3

Transcript of Capital structure analysis for nrb bearings

CAPITAL STRUCTURE ANALYSIS

PREPARED BY : SUMIT KR SINGH

COMPANY’S PROFILE

Date of Establishment 30-06 1965

Revenue 94.5557 ( USD in Millions )

Market Cap 11252.71386 ( Rs. in Millions )

Corporate Address Dhannur,15 Sir P M Road ,Fort Mumbai-400001,

Maharashtra

www.nrbbearings.com

Management Details Chairperson - Trilochan Singh Sahney

MD -

Directors - Ashank Desai, Devesh S Sahney, Aslesha A

Gowariker, S B (Ravi) Pandit, Uday Khanna, Tashwinder

Singh, Harshbeena S Zaveri

Business Operation Bearings

Background NRB Bearing was incorporated in 1965 as an Indo-French

venture with Nadella, pioneering the production of needle

roller bearings in India. NRB acquired SNL Bearings in

June 2000. Over the years NRB has expanded to five

modern manufacturing facilities producing needle,

spherical, cylindrical, wide-inner ring bearings, tapered

roller bearings and ball bearings. The TUV Managements

services (Gmbh), internatio

Company Secretary Satish C Rangani

Bankers DBS Bank, Citi Bank, BNP Paribas

Auditors Deloitte Haskins & Sells

Our Vision

To be a recognized leader in the Design and Production of

Customized Friction Solutions, with a presence in every vehicle in

the World.

Our Mission

To create a culture that fosters innovation and rewards out-of the-

box thinking which leads to quantum improvements

To supply products of high quality at optimal cost, leading us to be

the preferred business partner

To cultivate team spirit and a sense of ownership, empowering

each individual to measurably impact the quality of our

organizational results

To recognize individuals who respect and communicate our values

and are consistently ethical

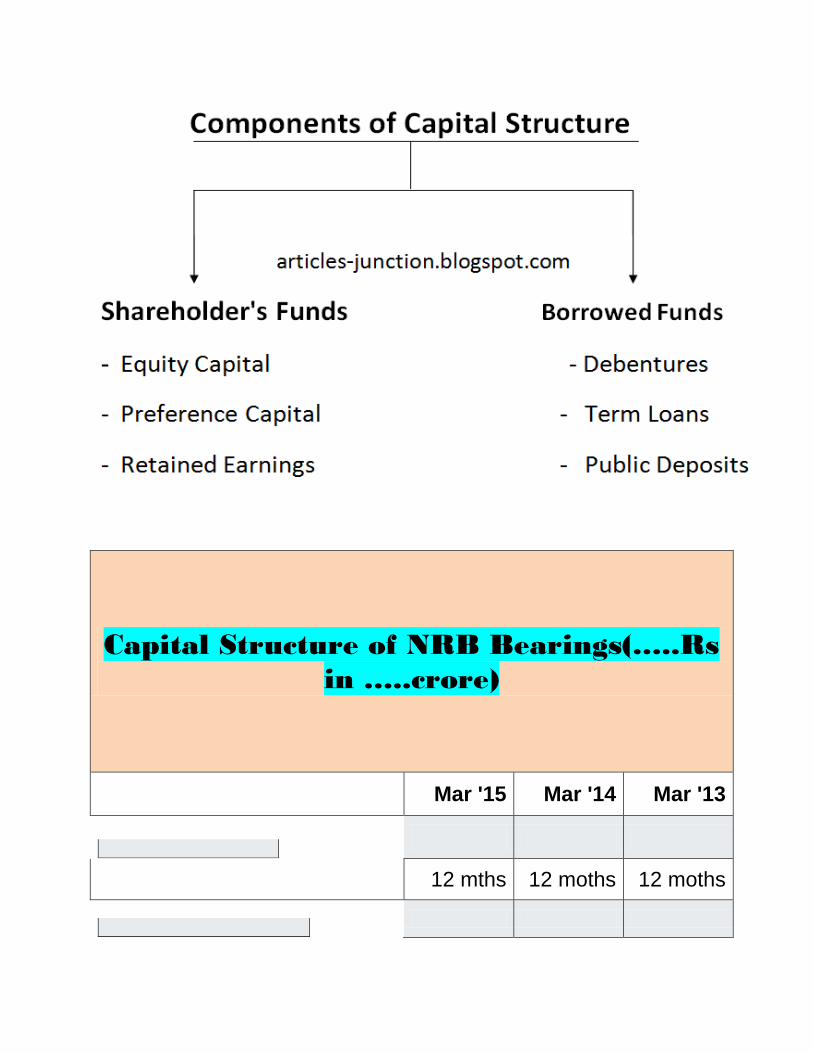

What is a 'Capital Structure'

A capital structure is a mix of a company's long-term debt, specific short-term

debt, common equity and preferred equity. The capital structure is how a

firm finances its overall operations and growth by using different sources of

funds.

Debt comes in the form of bond issues or long-term notes payable, while

equity is classified as common stock, preferred stock or retained

earnings. Short-term debt such as working capital requirements is also

considered to be part of the capital structure.

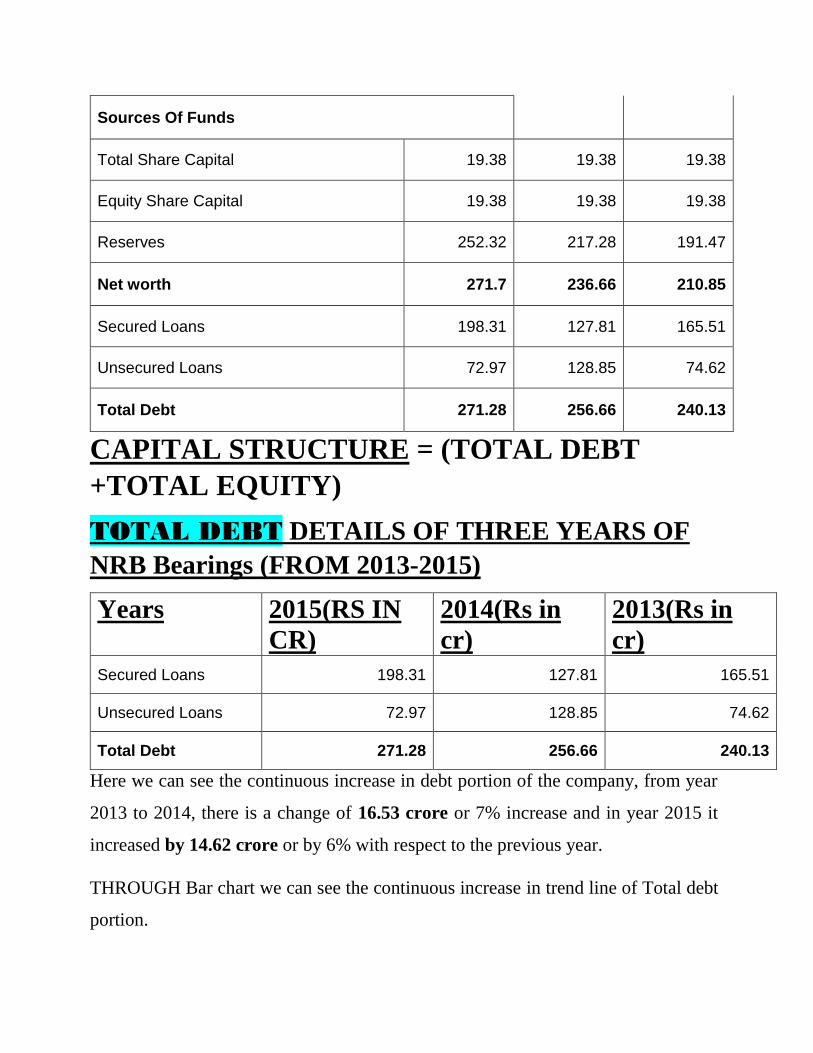

Capital Structure of NRB Bearings(…..Rs

in …..crore)

Mar '15 Mar '14 Mar '13

12 mths 12 moths 12 moths

Sources Of Funds

Total Share Capital 19.38 19.38 19.38

Equity Share Capital 19.38 19.38 19.38

Reserves 252.32 217.28 191.47

Net worth 271.7 236.66 210.85

Secured Loans 198.31 127.81 165.51

Unsecured Loans 72.97 128.85 74.62

Total Debt 271.28 256.66 240.13

CAPITAL STRUCTURE = (TOTAL DEBT

+TOTAL EQUITY)

TOTAL DEBT DETAILS OF THREE YEARS OF

NRB Bearings (FROM 2013-2015)

Years 2015(RS IN

CR)

2014(Rs in

cr)

2013(Rs in

cr)

Secured Loans 198.31 127.81 165.51

Unsecured Loans 72.97 128.85 74.62

Total Debt 271.28 256.66 240.13

Here we can see the continuous increase in debt portion of the company, from year

2013 to 2014, there is a change of 16.53 crore or 7% increase and in year 2015 it

increased by 14.62 crore or by 6% with respect to the previous year.

THROUGH Bar chart we can see the continuous increase in trend line of Total debt

portion.

TOTAL EQUITY DETAILS FOR THREE YEARS

NRB Bearings (FROM2013-2015)

YEARS 2015(Rs in cr) 2014(Rs in cr) 2013(Rs in cr)

Total Share Capital 19.38 19.38 19.38

Equity Share Capital 19.38 19.38 19.38

Reserves 252.32 217.28 191.47

Net worth 271.7 236.66 210.85

Here in case of equity share also we can see the continuous increase in equity portion

(from year 2013 to 2015 there is a change of 60.85 crore or 29%), but here company

is not increasing the further equity shareholdings, the main reason for increase in their

Mar '15 Mar '14 Mar '13

Secured Loans 198.31 127.81 165.51

Unsecured Loans 72.97 128.85 74.62

Total Debt 271.28 256.66 240.13

198.31

127.81

165.51

72.97

128.85

74.62

271.28256.66

240.13

0

50

100

150

200

250

300

rs in

cr

Axis Title

Chart showing Debt portion

Secured Loans Unsecured Loans Total Debt Linear (Total Debt)

equity portion is higher accumulation of reserves through profits, that’s the reason

we can see the continuous increase in reserve.

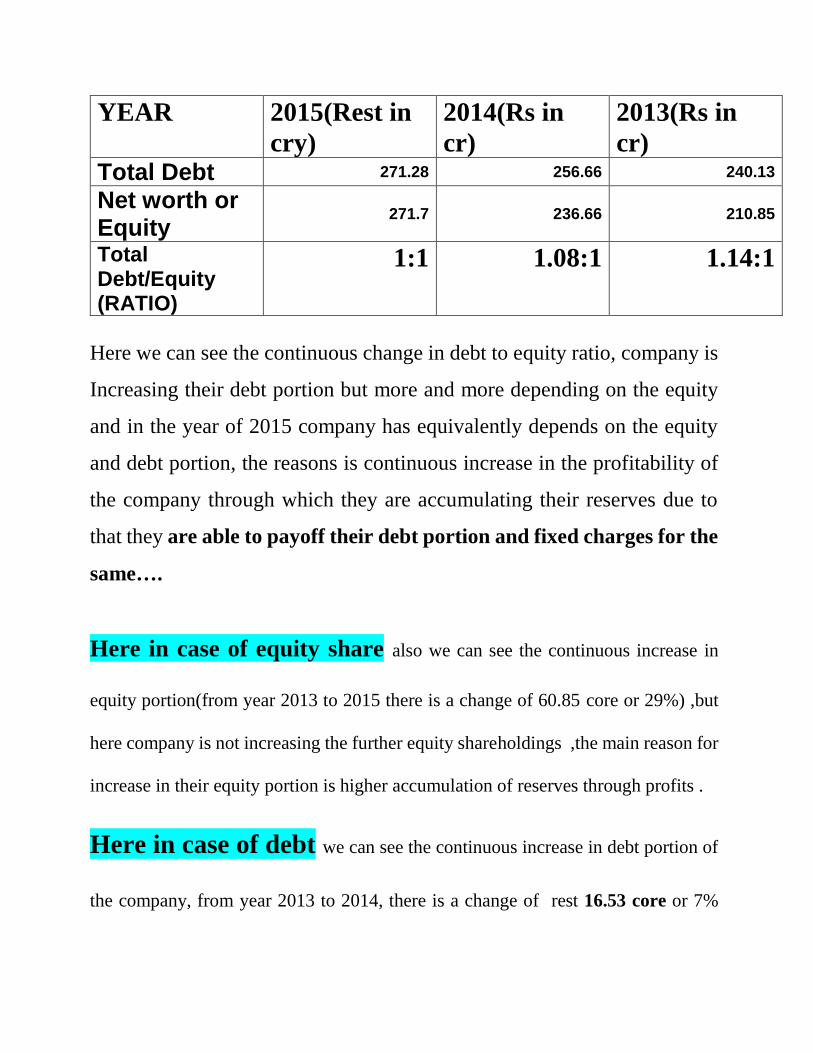

PROPORTION CHANGE IN DEBT AND

EQUITY DETAILS OF NRB Bearings for THREE

YEARS (2013-2015).

The relation of the proportionate change in debt-equity, we can understand

through debt –equity ratio.

CALCULATION OF DEBT EQUITY RATIO

FORMULA = TOTAL LIABILITY or TOTAL DEBT TOTAL SHAREHOLDERS EQUITY

0

50

100

150

200

250

300

Mar '15 Mar '14 Mar '13

RS

IN c

r

Axis Title

NET WORTH OR EQUITY

Total Share Capital Equity Share Capital Reserves

Networth or equity Linear (Networth or equity)

YEAR 2015(Rest in

cry)

2014(Rs in

cr)

2013(Rs in

cr) Total Debt 271.28 256.66 240.13

Net worth or Equity

271.7 236.66 210.85

Total Debt/Equity (RATIO)

1:1 1.08:1 1.14:1

Here we can see the continuous change in debt to equity ratio, company is

Increasing their debt portion but more and more depending on the equity

and in the year of 2015 company has equivalently depends on the equity

and debt portion, the reasons is continuous increase in the profitability of

the company through which they are accumulating their reserves due to

that they are able to payoff their debt portion and fixed charges for the

same….

Here in case of equity share also we can see the continuous increase in

equity portion(from year 2013 to 2015 there is a change of 60.85 core or 29%) ,but

here company is not increasing the further equity shareholdings ,the main reason for

increase in their equity portion is higher accumulation of reserves through profits .

Here in case of debt we can see the continuous increase in debt portion of

the company, from year 2013 to 2014, there is a change of rest 16.53 core or 7%

increase and in year 2015 it increased by rs 14.62 crore or by 6% with respect to the

previous year.

The entire change in the debt equity portion has an effects on the financial

leverage, earning per share, Interest obligation and the dividend policy of

the company.

That will be further analyzed.

INTEREST OBLIGATIONS DUE TO DEBT STRUCTURE

Year 2015 2014 2013

Operating Profit

114.75

114.75

100.61

PBDIT

118.37

105.18

102.33

Interest

15.85 17.19 17.31

Chart shows the trend of Interest obligations.

Here we can see that after continuous increase in debt also interest obligation is

decreasing it may be because of the lower cost of debt in continuous years debt

financing, due to change in the debt proportion of the company, the actual change or

decrease in interest payable from 2013 to 2015 is RS 1.44 crore and decrease in %

change by 8%.

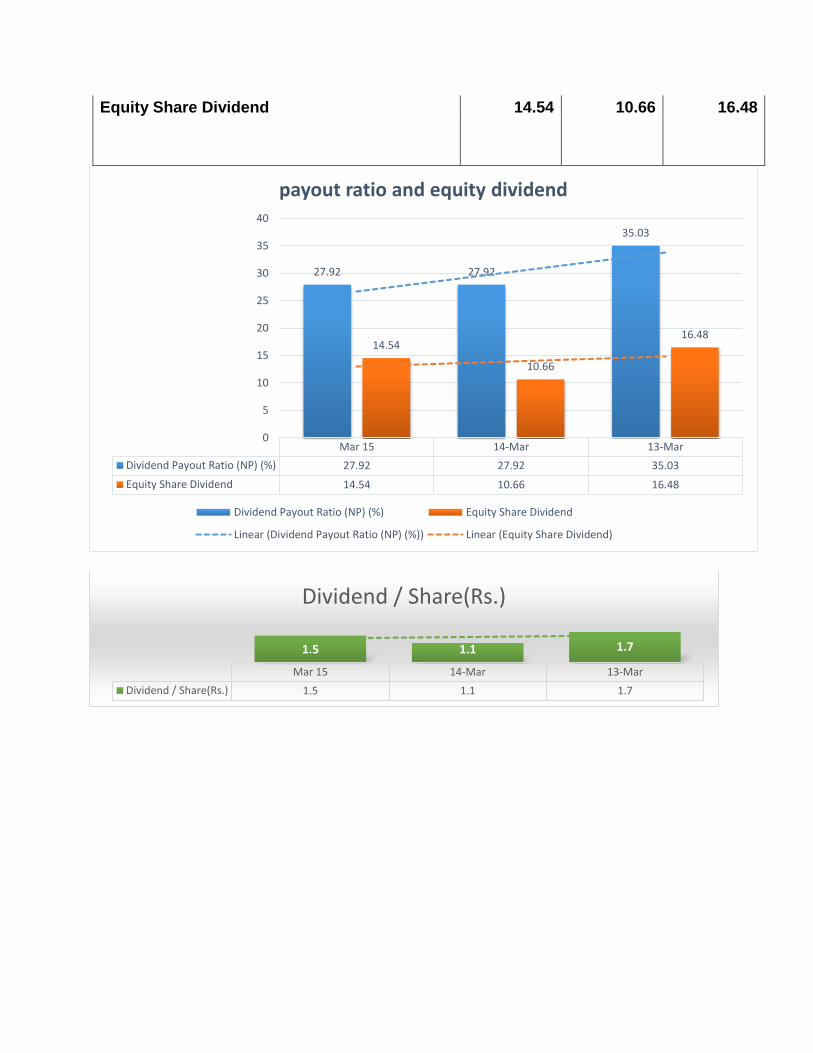

DIVIDEND DETAILS AND PAYOUT RATIO

Financial Ratios of NRB Bearings

Per Share Ratios Mar 15 14-Mar 13-Mar

Dividend / Share(Rs.) 1.5 1.1 1.7

Dividend Payout Ratio (NP) (%) 27.92 27.92 35.03

Dividend Payout Ratio (CP) (%) 18.08 14.92 21.39

Mar '15 Mar '14 Mar '13

Interest 15.87 17.19 17.31

15

15.5

16

16.5

17

17.5

18

Rs

in c

r

Axis Title

Interest Obligations

Interest Linear (Interest)

Equity Share Dividend 14.54 10.66 16.48

Mar 15 14-Mar 13-Mar

Dividend Payout Ratio (NP) (%) 27.92 27.92 35.03

Equity Share Dividend 14.54 10.66 16.48

27.92 27.92

35.03

14.54

10.66

16.48

0

5

10

15

20

25

30

35

40

payout ratio and equity dividend

Dividend Payout Ratio (NP) (%) Equity Share Dividend

Linear (Dividend Payout Ratio (NP) (%)) Linear (Equity Share Dividend)

Mar 15 14-Mar 13-Mar

Dividend / Share(Rs.) 1.5 1.1 1.7

1.5 1.1 1.7

Dividend / Share(Rs.)

Here we can see the relationship between dividend per share, payout ratio

and the equity dividend available to shareholders because all are varying

because of the profitability proportion of the firm.

Here we can directly see company is changing their payout policy, in year

2013 company pays 35.03% of total earnings of the firm but in successive

years company reduced payout ratio to 27.92%, it may be because of

reduction in debt and future investment purpose of the firm.so firm decided

to reduce the dividend rate and started accumulating reserves for

investments and debt payout purpose.

DIVIDEND POLICY OF YEAR 2013 AND 2015

1.5 1.1 1.7

27.92 27.92

35.03

14.54

10.66

16.48

0

5

10

15

20

25

30

35

40

Mar 15 14-Mar 13-Mar

dividend policy

Dividend / Share(Rs.) Dividend Payout Ratio (NP) (%)

Equity Share Dividend Linear (Dividend Payout Ratio (NP) (%))

Dividend (2013)

Directors recommend dividend of Rs.1.70/- per equity share of Rs.2/- (Rs.2.00 per

share for previous year) payable to members/beneficial owners as per the Register of

Members as applicable aggregating Rs.1647.68 lacs.

Dividend (2015)

Directors recommend dividend of Rs.1.50/-per equity share of Rs.2/-

(Rs.1.10 per share for previous year) payable to members/beneficial

Owners as per the Register of Members as applicable aggregating Rest.

1453.84 lacs.

LEVERAGE

The degree to which an investor or business is utilizing

borrowed money. Companies that are highly leveraged may be at risk of bankruptcy if they

are unable to make payments on their debt; they may also be unable to find new lenders in

The future.

The ability of the company to pay the fixed charges or cost.

TYPES OF LEVERAGE

FINANCIAL LEVERAGE OPERATING LEVERAGE

FINANCIAL LEVERAGE

Financial leverage can be aptly described as the extent to which a business or

investor is using the borrowed money. Business companies with high leverage are

considered to be at risk of bankruptcy if, in case, they are not able to repay the debts,

it might lead to difficulties in getting new lenders in future. It is not that financial

leverage is always bad. However, it can lead to an increased shareholders’ return on

investment. Also, very often, there are tax advantages related with borrowing, also

known as leverage.

FORMULA = EBIT (Earnings before interest and taxes)

EBT (Earning Before Tax)

CALCULATION OF EBIT AND EBT

Mar 15 14-Mar 13-Mar

PBDIT 118.37 105.18 102.33

Less: depreciation 28.31 33.27 29.97

EBIT 90.06 71.91 72.36 LESS: Interest 15.87 17.19 17.31

EBT 74.19 54.72 55.05

CALCULATION OF FINANCIAL LEVERAGE (FL)

YEAR 2015 2014 2013

EBIT 90.06 71.91 72.36 EBT 74.19 54.72 55.05 FINANCIAL

LEVERAGE)

1.214 1.314 1.314

Here we can see on the base of financial leverage risk proportion has reduced ,in year

2013 risk proportion was high because of high financial leverage and it has reduced

from 1.314 to 1.214 in year 2015 and firm risk element has reduced due to low

financial Leverage.

Definition of Degree of Financial Leverage

The degree of financial leverage (DFL) is the leverage ratio that sums up the effect

of an amount of financial leverage on the earning per share of a company. The degree

of financial leverage or DFL makes use of fixed cost to provide finance to the firm

and also includes the expenses before interest and taxes. If the Degree of Financial

Leverage is high, the Earnings per Share or EPS would be more unpredictable while

all other factors would remain the same.

CALCULATION OF DDEGREE OF FINANCIAL LEVERAGE

FORMULA= %Change in EPS

%Change in EBIT

CALCULATION OF %CHANGE IN EBITAND EPS

Mar 15 14-Mar 13-Mar

PBDIT 118.37 105.18 102.33

Less: depreciation 28.31 33.27 29.97

EBIT 90.06 71.91 72.36

LESS: Interest 15.87 17.19 17.31

EBT 74.19 54.72 55.05 Earnings Per Share (Rs) 5.37 3.94 4.85

% CHANGE IN EPS 36% 19% 3%

%CHANGE IN EBIT 20% 1% 10%

DOFL (DEGREE OF FINANCIAL LEVERAGE)

YEAR 2015 2014 2013

% CHANGE IN EPS 36% 19% 3%

%CHANGE IN EBIT 20% 1% 10% DEGREE OF FINANCIAL

LEVERAGE 1.8 19 .3

The ratio shows that the higher the degree of financial leverage, the more volatile is

EPS. Since interest is a fixed expense, leverage magnifies returns and EPS, which is

good when operating income is rising, but it can be a problem during tough economic

times when operating income is under pressure.

If the DOFL IS EQUAL TO 1 than company is operating well and there is not

such volatility in earning potential of the firm. But here DOFL is changing by

huge % and it shows the high level of risk element for EPS.

OVERALL ANALYSIS

1. On the base of debt equity portion we can see the dramatic increase in debt, debt

equity ratio is continuous decreasing, and the earning potential of the firm is

increasing, that can be seen through the EPS of the firm.

TAX SHIELD ALSO PLAYS IMPORTANT ROLE IN INCREASE IN EPS

2. The prime reason for increase in the profit and EPS and also the market value of

share is high level of accumulation of profit through lowest dividend payout policy

of the firm that reflects through reserves.

3. Here there is no increase in the share value of the firm, increase in the net worth

due to increased profit and the high reserves.

4. On the base of degree of financial leverage we can say that the risk element of the

firm has reduced through successive years because of low financial leverage.

5.But DOFL shows that the volatility into the earning capacity of the firm

irrespective of increased earning ,that is reflected through the EPS .WHICH SHOWS

The high volatility into the fixed charges of the firm that reflected through the DOFL.

FUTURE PROSPECT OF THE COMPANY IS GOOD AND COMPANY

CONTINOUSLY MAKING HIGHER PROFITS AND MAKING LESS DEBT

PROPORTION TO GET THE HIGH MARKET PRICE AND EPS.