Capital Markets Day 2013 FINALm - PKC Group

50

Capital Markets Day 2013 April 3, 2013 in Helsinki 1

Transcript of Capital Markets Day 2013 FINALm - PKC Group

Capital Markets Day 2013

April 3, 2013 in Helsinki

1

Disclaimer

• The content of this presentation contains time-sensitive information that is accurate as of the time hereof.

• A number of forward-looking statements will be made during this presentation. Forward-looking statements are any statements that are not historical facts. These statements are based on current decisions and plans and currently known factors. They involve risks and uncertainties which may cause the actual results to materially differ from the results currently expected by PKC Group.

• If any portion of this presentation is rebroadcast, retransmitted or redistributed at a later date, PKC Group will not be reviewing or updating the material that is contained herein.

2April 3, 2013 Capital Markets Day

The Agenda

Capital Markets Day 2013

12.30 Opening wordsMatti Hyytiäinen, President & CEO

12.30 – 13.00 PKC’s StrategyMatti Hyytiäinen, President & CEO

13.00 – 13.20 Developing PKC Uniqueness further Jyrki Keronen, Senior Vice President, Business Development & APAC

13.20 – 13.40 Maximizing current PKC set-up Rico Mutone, Vice President, Sales and Engineering, North America

13.40 – 13.50 Coffee break

13.50 – 14.10 Penetrating into APACMatti Hyytiäinen, President & CEO

14.10 – 14.25 Exploring Opportunities to Expand within Transporta tion IndustryFrank Sovis, President, Wiring Systems, North America

14.25 – 14.45 FinancialsJuha Torniainen, CFO

14.45 – 15.00 Closing StatementMatti Hyytiäinen, President & CEO

3April 3, 2013 Capital Markets Day

4

Capital Markets Day

PKC Strategy

April 3, 2013

Matti HyytiäinenPresident & CEO

Definition: Electrical Distribution Systems

5

PKC delivers Nerve Systems

to vehicles

April 3, 2013 Capital Markets Day

Definition: PKC in Transportation Industry

6April 3, 2013 Capital Markets Day

Railway Vehicles Commercial Aircraft

Material Handling Vehicles

Mining Machinery

Potential Customer SegmentsCurrent Customer Segments

Light Commercial Vehicles (LCV)

Trucks & Buses (HCV & MCV)

Construction Equipment

EnginesAgriculture and Forestry

Recreational Vehicles

PKC Today

“Today, PKC is the Preferred Supplier for the main global Commercial Vehicle brands, supplying Electrical Distribution Systems.

The customer programs are typically 5-10 years long, which gives us a good view ahead. PKC is a critical partner in its customers’ value chain.

We see plenty of opportunities to grow our topline.”

7April 3, 2013 Capital Markets Day

PKC Uniqueness

“Our current position is based on PKC Uniqueness. That is how we call our unique know-how of managing complex processes of individually tailored products and thousands of product variants.

PKC Uniqueness makes us an asset to the customers because we can integrate into their processes, enabling our customers an unlimited product offering, with very short lead-times.

PKC Uniqueness is scalable and hard to copy, which gives us a significant competitive edge.”

8April 3, 2013 Capital Markets Day

PKC Capturing Growth

“We see interesting and above average growth possibilities in our current customer base, in penetrating into Asia and in expanding within the Transportation Industry globally.”

9April 3, 2013 Capital Markets Day

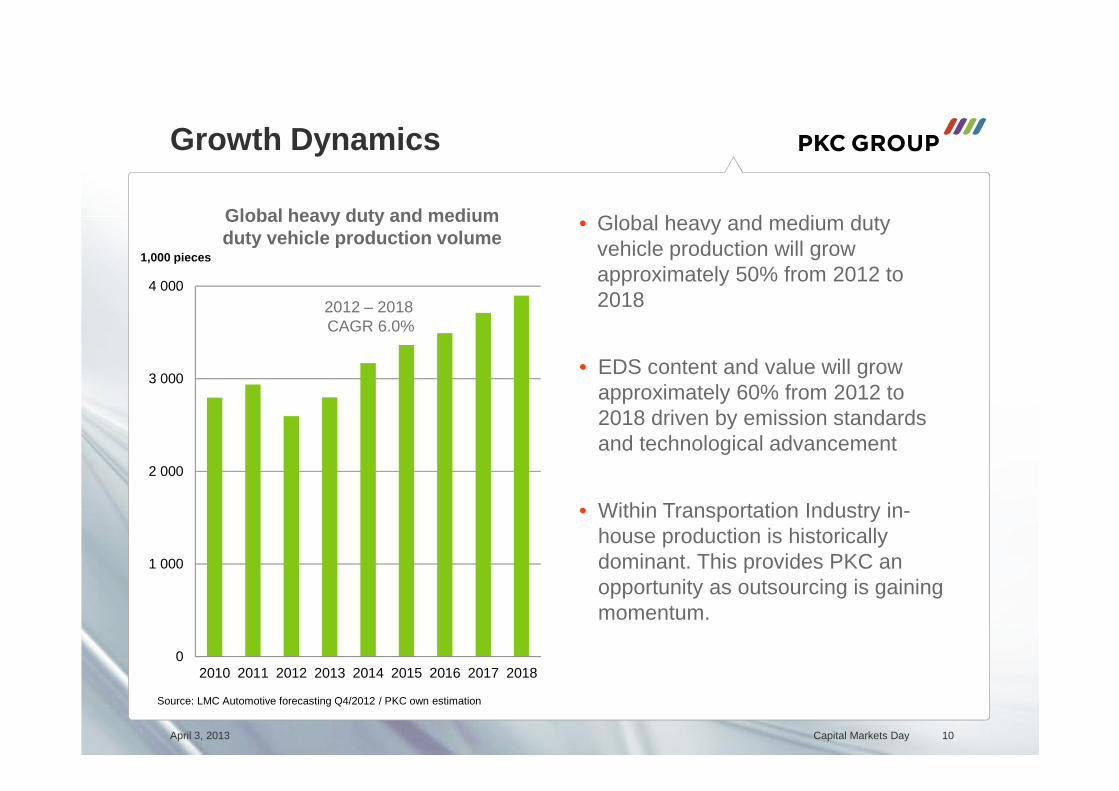

Growth Dynamics

0

1 000

2 000

3 000

4 000

2010 2011 2012 2013 2014 2015 2016 2017 2018

10

• Global heavy and medium duty vehicle production will grow approximately 50% from 2012 to 2018

• EDS content and value will grow approximately 60% from 2012 to 2018 driven by emission standards and technological advancement

• Within Transportation Industry in-house production is historically dominant. This provides PKC an opportunity as outsourcing is gaining momentum.

Global heavy duty and medium duty vehicle production volume

April 3, 2013 Capital Markets Day

1,000 pieces

Source: LMC Automotive forecasting Q4/2012 / PKC own estimation

2012 – 2018 CAGR 6.0%

PKC’s Financial Targets

“Financially we aim high. We target our topline to grow up to 1.4 billion euros by 2018, with EBITDA target >10% while maintaining healthy balance sheet.”

11April 3, 2013 Capital Markets Day

STRATEGIC INITIATIVES

PKC’s Strategy Captures Growth Opportunities

VISION 2020

PKC is the Preferred Supplier in Electrical Distribution Systems for Transportation Industry globally.

12April 3, 2013 Capital Markets Day

Managing the Complexity

Developing PKC Uniqueness further

Maximizing currentPKC set-up

Penetrating into APAC

Exploring opportunities

to expand within Transportation

Industry

Developing Electronics business as a stand alone wi thin PKC Group

13

Capital Markets Day

Developing PKC Uniqueness further

April 3, 2013

Jyrki KeronenSenior Vice President, Business Development & APAC

Developing PKC Uniqueness further

April 3, 2013 Capital Markets Day 14

Managing the Complexity

Developing PKC

Uniqueness further

Maximizing currentPKC set-up

Penetrating into APAC

Exploring opportunities

to expand within Transportation

Industry

Complexity as a Trend will Prevail

April 3, 2013 Capital Markets Day 15

Urbanization

Transportationstandards,

special purpose vehicles

Emerging markets

APACSouth America

Green initiatives

Pollution, fuel efficiency

Mass Customization

High mix, low volumes, architecture platforms

Business evolution

TCO, Technology, Push to pull, Consolidation

Technology

Power & signal, consistency, reliability, light weight materials

Managing the Complexity is a global challenge

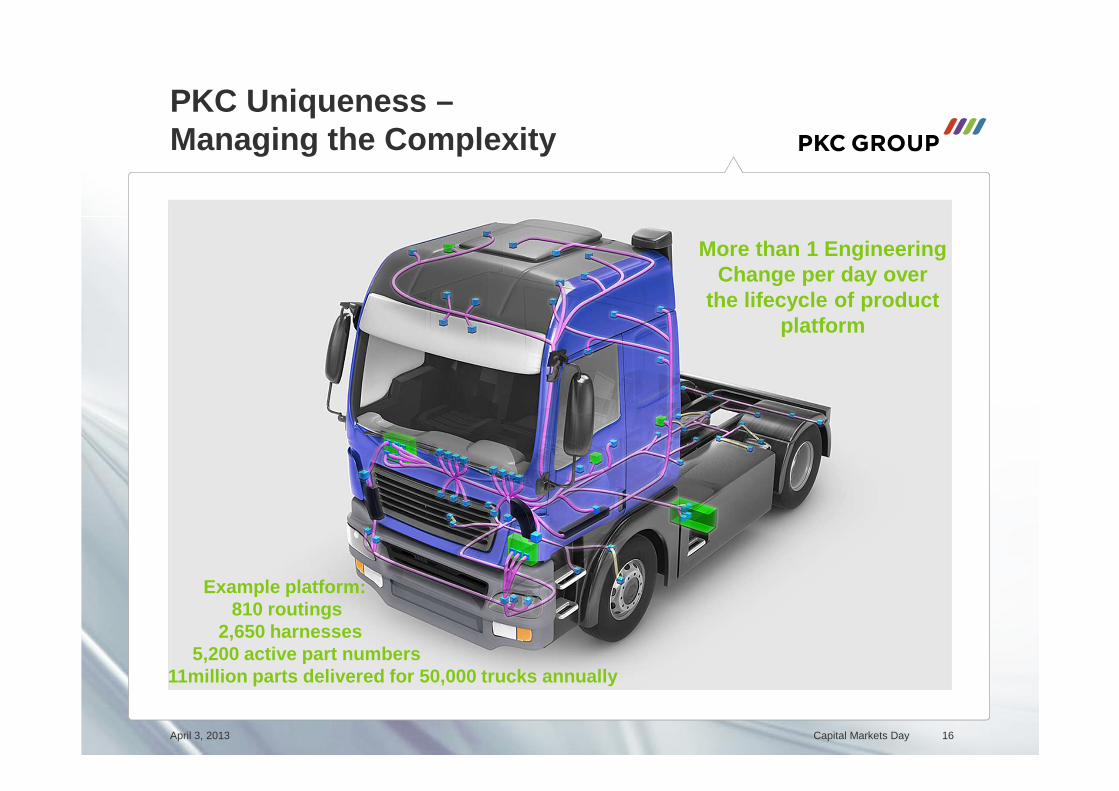

PKC Uniqueness –Managing the Complexity

April 3, 2013 Capital Markets Day 16

More than 1 Engineering Change per day over

the lifecycle of product platform

810 routings 2,650 harnesses

5,200 active part numbers11million parts delivered for 50,000 trucks annuall y

Example platform:

PKC Uniqueness – Key Elements

• PKC’s own developed data management process and tools enables seamless interface and data transfer from customer systems to PKC’s design and production

– PKC Data Management -process

• Special PKC COP and PKC LAD tools to support efficient manufacturing ensuring short lead time

– PKC Order Fulfilment -process

• PKC Safe Launch concept, efficient new product launch ramp-up tool

April 3, 2013 Capital Markets Day 17

PKC’s Own Data Management System

April 3, 2013 Capital Markets Day 18

CUSTOMER

Component libraryFunctionalities

3D wiring

CUSTOMER

Daily call-offsSequencing

Timing

CUSTOMER

To assembly lineSequencing

PKC

Data ProcessingMaster / Composite

PKC Data Management -process

PKC

Data ProcessingCutting, Crimping,

Assembly & Final Assembly,Testing, Shipping

PKC Order Fulfilment -process

• Key elements of PKC Uniqueness are developed further in NPI centres – Keila, Estonia

– Acuña, Mexico

– Curitiba, Brazil

• Development focus in– Methods

– MRP system

– Plant logistics / layout

– Production technology

– Processes

– Organization

NPI Centers Enable Continues Development of PKC Uniqueness

19April 3, 2013 Capital Markets Day

PKC Uniqueness - Benefits

• PKC Uniqueness - benefits for customers – Short lead time

– Unlimited customization

– Robust change management

– Fast and secured product launches and ramp-ups

– Competitive TCO (Total Cost of Ownership)

April 3, 2013 Capital Markets Day 20

21

Capital Markets Day

Maximizing Current PKC Set-up

April 3, 2013

Rico MutoneVice President, Sales and Engineering, North America

Maximizing C urrent PKC set-up

April 3, 2013 Capital Markets Day 22

Managing the Complexity

Developing PKC Uniqueness further

Maximizing current

PKC set-upPenetrating into

APAC

Exploring opportunities

to expand within Transportation

Industry

PKC Positioning in Value Chain

April 3, 2013 Capital Markets Day 23

Features

Vehicle Electrical Architecture

Software Hardware Data inputs & outputs

Power Distribution

Components

Wiring Harnesses

Vehicle Electronics

OEM’s

PKC and / orComponents

suppliers

PKC

Global Leader Position as a Target

• Current business relationship with all key western OEMs in commercial vehicle industry enable future growth

• Global leader position as a target

24

32 %

68 %

North America South AmericaEurope

Medium Commercial Vehicle

HeavyCommercialVehicle

PKCOtherSource: ACT report, January 2013, LMC Automotive forecasting Q4/2012. Note: Europe comprised of EU27 + Efta

April 3, 2013 Capital Markets Day

1 %

99 %

APAC

0 %

100 %

Maximizing PKC’s Current Set-up

• Globalizing relationships with our customers

• Expand manufacturing footprint to meet the growing market demand

• Participate future full range commercial light vehicle programs

April 3, 2013 Capital Markets Day 25

0

250

500

750

1 000

1 250

1 500

SouthAmerica

NorthAmerica

EU &Russia

Japan India China

2012 2018 Estimation

Heavy duty and medium duty commercial vehicle production Volume,

1,000 pieces

Source: LMC Automotive forecasting Q4/2012

26

Capital Markets Day

Penetrating into APAC

April 3, 2013

Matti HyytiäinenPresident & CEO

Penetrating into APAC

April 3, 2013 Capital Markets Day 27

Managing the Complexity

Developing PKC Uniqueness further

Maximizing currentPKC set-up

Penetrating into APAC

Exploring opportunities

to expand within Transportation

Industry

PKC Focus Countries in Asia-Pacific

28

• China is the biggest truck market in the world

– Total production 830,000 trucks in 2012

– Dominated by seven state-owned manufacturers

– Strong governmental influence

• India’s truck market grow steadily

– Total production 280,000 trucks in 2012

– Growth focus in light and medium duty

• Japan has mature market

– Total production 290,000 trucks in 2012

– Growth focus in medium duty

PKC

Current and potential customer

April 3, 2013 Capital Markets Day

APAC Market Dynamics

• Asia, especially China, is the world’s largest commercial vehicle market that is forecast to continue to grow significantly– PKC’s current global customers actively focus their growth into these markets

– In addition to market growth, Asian commercial vehicle markets are subject to a structural change

– New emission standards and customers’ need for uniquely optimized vehicles.

– Technological contents of commercial vehicles increases which adds complexity

• PKC’s core competence is to be able to mass produce high quality uniquely tailored products with infinite variants with very fast turnaround time

– PKC has excellent competitive position to expand its business in Asia to current customers and the leading Asian and Chinese truck manufacturers

April 3, 2013 Capital Markets Day 29

Global Brands in Asia

• Global brands are penetrating into Asian markets with strategies adapted to each local market

– MAN• Sinotruck, China

• Force Motor, India

– Daimler• Fuso, Japan

• Foton, China

• BharatBenz, India

– Volvo • Nissan Diesel/UD Truck, Japan

• Dong Feng, China

• Eicher, India

• SDLG Construction Vehicles, China

– Navistar

• JAC, China

– Iveco

• SAIC, China

– Ford

• Jiangling Motor, China

30April 3, 2013 Capital Markets Day

EDS Base in Asia

• China: 90% of commercial vehicle EDS in-house production– Very limited customization

• Japan: outsourced locally– Cost pressure

• India: outsourced locally – Limited competition and

competence

April 3, 2013 Capital Markets Day 31

PKC’s Strategy in Asia

• Develop our Existing Business Framework– Expand the existing business as

we support our global key customers doing business in China, India and Japan

– Greenfield

• Explore Avenues for New Partnerships– Collaborate with market-leading

customers in China, India and Japan

– Outsourcing deals, joint ventures and acquisition

April 3, 2013 32Capital Markets Day

33

Capital Markets DayExploring Opportunities in Transportation Industry

April 3, 2013

Frank SovisPresident, Wiring Systems, North America

Developing PKC Uniqueness further

April 3, 2013 Capital Markets Day 34

Managing the Complexity

Exploring opportunities

to expand within

Transportation Industry

Maximizing currentPKC set-up

Penetrating into APAC

Developing PKC Uniqueness further

PKC Uniqueness as the Basis

PKC Uniqueness

A global leader in commercial vehicle electrical systems

Expert in Managing the Complexity

Understanding customers and their processes

April 3, 2013 Capital Markets Day 35

• OEMs in the transportation industry face similar challenges than OEM’s in commercial vehicle industry

• PKC specializes in managing these challenges

• PKC’s Uniqueness can be leveraged to add value to adjacent markets

Interesting Segments to Explore

36April 3, 2013 Capital Markets Day

Railway Vehicles Commercial Aircraft

Material Handling Vehicles

Mining Machinery

Potential Customer SegmentsCurrent Customer Segments

Light Commercial Vehicles (LCV)

Trucks & Buses (HCV & MCV)

Construction Equipment

EnginesAgriculture and Forestry

Recreational Vehicles

Interesting Segments to Explore

37April 3, 2013 Capital Markets Day

Railway Vehicles Commercial Aircraft

Material Handling Vehicles

Mining Machinery

Potential Customer Segments

• Sizeable market– Available total end market of

these four combined segments is the same as our current customer segments (excluding light commercial vehicles)

• Traditional Supply Chain– In-house production and

fragmented supply base

• Similar complexity as our current customer segments– Similar quality and reliability

demands

Market Expansion Rationale

April 3, 2013 Capital Markets Day 38

• PKC Uniqueness is scalable and it is not only commercial vehicle related knowhow

• PKC is actively seeking expansion opportunities within Transportation Industry– Study growth opportunities in selected

Transportation Industry Segments– Leverage PKC Uniqueness to provide

value to customers in adjacent markets– Increase economies of scale of purchased

materials

• Rationale for expanding within Transportation Industry– Utilizing the existing PKC knowhow– Better pricing/profit opportunity– Growth opportunities– Increase PKC’s market value

39

Capital Markets Day

Financials

April 3, 2013

Juha TorniainenCFO

40

Delivering Growth

40

66 84 114 129 125 134 146 178 199 229289 312

202

316

550

928

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012Net Sales, EUR million

CAGR 19% during 1997-2012

1997 1998 2000 2002 2003 2005 2006 2007 2008 2009

� Brazilian factory was opened

� Acquisition of electronics business

� Acquisition of Estonian production

� Operations started in China

� PK Cables listed in the Helsinki Stock Exchange

� Acquisition of Russian production

� Acquisition of Electro Canada in Canada, the USA and Mexico

� Acquisition of MAN business in Poland

2010 2011

� Acquisition of SEGU in Germany, Poland and Ukraine

� Acquisition of AEES in North America, Brazil and Ireland

April 3, 2013 Capital Markets Day

Delivering Profitability

38

16

42

60

83

30

7

34

49

65

0

2

4

6

8

10

12

14

0

10

20

30

40

50

60

70

80

90

2008 2009 2010 2011 2012

EBITDA (adjusted*) EBITA (adjusted**) EBITDA* % EBITA** %

41

EUR million %

* excluding non-recurring items in EBITDA ** excluding non-recurring items and PPA depreciation and amortization in EBIT

April 3, 2013 Capital Markets Day

Strong Cash Flow over the Cycles

25

42

23

40

76

-10-4 -8 -11 -13

-22

0

0

-80

0

-6

38

15

-50

64

-100

-80

-60

-40

-20

0

20

40

60

80

100

2008 2009 2010 2011 2012

Cash from operations Net capex (organic)Acquisitions Free cash flowCash after net capex

42

EUR million

April 3, 2013 Capital Markets Day

Earnings, Cash Flow and Dividend per Share

43

0,310,13

1,09 1,16 1,120,87

2,32

0,82

1,46

2,97

0,150,40

0,55 0,60 0,70

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

2008 2009 2010 2011 2012

Earnings per share

Free cash flow (excl. acquisitions) per share

Dividend per share

EUR

April 3, 2013 Capital Markets Day

Improving Net Working Capital

44

6244

58

125106

5236

58

111

88

-33 -34

-55

-135-121

26

31

17

15

9,3

0

5

10

15

20

25

30

35

-150

-100

-50

0

50

100

150

2008 2009 2010 2011 2012

Receivables Inventories Payables NWC* % of net sales

EUR million %

* Average of beginning and end of the year

April 3, 2013 Capital Markets Day

Solid Balance Sheet and Returns

45

42

49

57

3034

0

10

20

30

40

50

60

2008 2009 2010 2011 2012

Equity ratio, %

76

36

-2

73

34

-100

1020304050607080

2008 2009 2010 2011 2012

Gearing, %

60

28

-2

111

57

-20

0

20

40

60

80

100

120

2008 2009 2010 2011 2012

Net debt

7

3

1917

15

21

6

26

1917

0

5

10

15

20

25

30

2008 2009 2010 2011 2012

ROE, % ROI, %

%%

EUR million%

April 3, 2013 Capital Markets Day

Funding Structure

46

68

8 8 8

47

0

10

20

30

40

50

60

70

80

2013 2014 2015 2016 2017

Loan maturities (excl. leases)EUR million, Dec 31, 2012

Long-term loans from banks 71.8Long-term financial leases 2.8Short-term loans from banks 68.6Short-term financial leases 0.6Total borrowings 143.8Cash 87.2Net debt 56.6

Un-utilized credit facility 30.0

April 3, 2013 Capital Markets Day

Long-Term Financial Targets

Annual Revenue EUR 1.4 Billion by 2018

EBITDA > 10%

Gearing < 75%

Dividends 30 – 60% of Free Cash Flow

Annual Revenue EUR 1.4 Billion by 2018

EBITDA > 10%

Gearing < 75%

Dividends 30 – 60% of Free Cash Flow

Developing PKC Uniqueness

further

Developing PKC Uniqueness

further

Maximizing current PKC set-up

Maximizing current PKC set-up

Penetrating into APAC

Penetrating into APAC

Exploring opportunities

to expand within Transportation

Industry

Exploring opportunities

to expand within Transportation

Industry

47April 3, 2013 Capital Markets Day

48

Capital Markets Day

Closing Statement

April 3, 2013

Matti HyytiäinenPresident & CEO

PKC is an Excellent Investment Opportunity

• PKC is a growth-driven company

• PKC has unique technological capabilities that deliver major benefits to our customers

• Solid financial position

April 3, 2013 Capital Markets Day 49

Managing the Complexity

www.pkcgroup.com

50

April 3, 2013 Capital Markets Day