CANBACK INTRODUCTION AND CELLULAR OPERATOR ANALYSIS … · CANBACK INTRODUCTION AND CELLULAR...

19

PREDICTIVE ANALYTICS INTEGRATORS EIU CANBACK Boston, Massachusetts www.canback.com +1-617-399-1300 CANBACK INTRODUCTION AND CELLULAR OPERATOR ANALYSIS TOOL October 2014

Transcript of CANBACK INTRODUCTION AND CELLULAR OPERATOR ANALYSIS … · CANBACK INTRODUCTION AND CELLULAR...

PREDICTIVE ANALYTICS

INTEGRATORS

EIU CANBACKBoston, Massachusetts

www.canback.com+1-617-399-1300

CANBACK INTRODUCTION ANDCELLULAR OPERATOR ANALYSIS TOOL

October 2014

2

Contents

Introduction to Canback

Cellular operator analysis tool (COAT)

3

Canback is the world’s leading manage-ment

consulting firm leveraging predictive analytics

for strategic purposes.

We operate globally with the world’s largest

companies as clients. This has taken us to

more than 50 countries since our founding in

2004.

We also offer analytic services with the

Canback Global Income Distribution Database

(C-GIDD) as our flagship product.

Canback is a subsidiary of The Economist

Intelligence Unit since 2015.

4

Pe

rfo

rma

nce

Time1900 1960 1990

Traditional

management

consulting

Predictive

analytics

2016

A new paradigm

with higher

performance

Few, if any, break-

throughs since the

early 1990s

- Conceptually based

problem-solving

- Experience preferred

over hard analysis

- Datasets at the

center of problem-

solving

- Repeatability and

scalability for

efficiency

Canback prefers fundamental analysis of primary data over conceptual frameworks, achieving

greater accuracy in problem solving at a lower cost

“The future is already here, it is just unevenly distributed”

MANAGEMENT CONSULTING INDUSTRY S-CURVE

5

Canback is often cited in the press, research reports, annual reports, and investor presentations by

some of the largest companies and organizations in the world

Quarterly divisional seminar: Africa (2015)

Quarterly divisional seminar: South Africa (2014)

Quarterly divisional seminar: Asia-Pacific (2013)

Mapping the Path to Future Prosperity: Emerging Markets Growth Index (2014)

Abuja +12: Shaping the Future of Health in Africa (2013)

Africans Open Fuller Wallets to the Future (2014)

The Shifting Urban Economic Landscape: What Does it Mean for Cities? (2013)

Annual Results Presentation (2013)

Africa's Middle Class: Few and Far Between (2015)

Hot spots: Benchmarking Global City

Competitiveness (2012)

Why are Africans Either Very Rich, or

Very Poor (2015)

Consolidated Annual Report (2012)

The Future of Retailer Brands (2010)

The War for Nigeria (2013)

Nigeria - A Nation Divided (2012)

6

We have worked on the ground in over 50 countries, helping clients draw reliable, fact-based

conclusions through data-driven analyses

PROJECT COMPOSITION

Global projects: 14%

United States: 7%

South America: 30%

Mid America: 11%

Europe: 7%

Africa: 24%

Asia: 8%

Core office

Satellite office

Country projects

Consultants work travel

7

Canback works mainly in four consumer-facing sectors where we have distinct competitive

advantages based on methods and experience

CONSUMER GOODS

Capturing exciting but hard to understand opportunities for durable and

non-durable goods, such as assessing new category potential in Asia or

developing a market entry strategy in Africa

RETAIL

Predicting trends in retailing to inform strategic decisions, for example

choosing store formats in Latin America and forecasting the evolution of

modern trade in the Philippines

FINANCIAL

SERVICES

Optimizing credit card, retail banking and consumer finance operations,

including creating a pricing strategy for credit cards in Europe and defining

optimal mix of ATM and retail branches for bank in sub-Saharan Africa

INFORMATION &

COMMUNICATIONS

TECHNOLOGY

Assessing future demand in global markets, such as predicting new

subscriber growth in Central America and analyzing profitability prospects

for a third market entrant in China

8

Canback is diversified across functional areas. Strategy development is our largest practice.

This covers business planning, finding new market opportunities, developing corporate and

business unit strategies, and more

Canback

Management consulting

>65%

M&A due diligence

30%

Strategydevelopment

>35%

Predictive modeling

15%

Commercial databases

15%

Market/industry research

<5%

We pioneered, and are still the

world’s only supplier of GDP and

income data at the subdivision

and city level: C-GIDD

9

Canback strives to build partnerships that are long-term, collaborative, consistent and relevant to

every level of an organization

Long-term

At every level

Collaborative

Consistent

Enhancing client capabilities is a long-term endeavor. We strive to build

strategic partnerships that will be relevant in any market environment

Working alongside our clients, not in isolation, we maintain high levels of

transparency and communication throughout the course of any project

While our work is conducted globally, we centralize analysis in our core

offices to ensure consistency and quality of output

The structure of a global business is complex. We strive to build

relationships with both central teams as well as regional / local units

10

OUR GLOBAL OFFICES AND LEADERS

Canback has offices in twelve key international markets, allowing us direct access to vital

centers of economic growth

OUR CAPABILITIES

Office

Manage-

ment

Consulting

Predictive

AnalyticsC-GIDD

Market

Research

Boston

London

Beijing

Johannes-

burg

Chicago

Dubai

Shanghai

Singapore

Mexico City

Jakarta

Sao Paulo

Tokyo

Core office

Satellite office

11

The Canback Global Income Distribution Database (C-GIDD) is used to quantify market size and

demand drivers. C-GIDD is the only commercial database of its kind in the world

C-GIDD

benchmark

products and

services data

Internal to

Canback

C-GIDD

economic,

demographic,

social and

psychographic

data

Internal to

Canback

C-GIDD

income

distribution

data

Available as a

commercial

service at

cgidd.com

The world's only database with GDP, household

income and spending data for 213 countries, 696

subdivisions and 997 cities

Covers 2000 till 2025

Complemented with modules containing social,

demographic and psychographic data

Visit http://cgidd.com for more information

C-GIDD CONTENT

Quantify number of households at specific

income or socioeconomic levels

Compare consumer market sizes across

geographies in a uniform way

Merge with actual market data to spot new

or under-developed opportunities

0 0.25 0.5 0.75 1

Airline passengers

ATM machines

Bank deposits

Electricity consumption

Insurance premiums

Internet users

McDonald's restaurants

Milk consumption

Mobile phone subsribers

Oil consumption

Personal computers

Television sets

EXPLANATORY POWER OF C-GIDD

INCOME DISTRIBUTION DATA

FOR SELECT PRODUCTS AND SERVICESDemand variance explained by income above category-specific threshold

R2

12

Contents

Introduction to Canback

Cellular operator analysis tool (COAT)

13

The COAT database allows Canback to predict future winners and losers among cellular

operators around the world, and to understand what drives profitability and growth

Australia Lithuania

Canada Malaysia

China Mexico

Czech Republic Netherlands

Egypt Pakistan

Greece Philippines

Hong Kong Portugal

Hungary Russia

India South Africa

Ireland S. Korea

Italy Spain

Japan Sweden

OVERVIEW OF COAT (CELLULAR OPERATOR ANALYSIS TOOL) DATABASE

BACKGROUND

• Originally developed in 1999 to model

cellular profitability and 3rd entrant

probability of success in emerging

European markets

• Later expanded to a global dataset

• Builds on country and operator data

collected from annual reports, analysts,

regulators, and proprietary sources

• Uses pooled time series cross-sectional

analysis for the years 1999-2014

COUNTRY VARIABLES MARKET VARIABLES

* Countries and operators used for a particular effort. There are 12 additional countries and 28 operators in the total database.

OPERATORS*COUNTRIES*

Airtel (India)

Bell Canada (Canada)

Bitė (Lithuania)

Celcom (Malaysia)

China Mobile (China)

China Mobile(Hong

Kong)

China Unicom (China)

COSMOTE (Greece)

Globe Telecom

(Philippines)

Hutchison (Hong Kong)

IUSACELL (Mexico)

KPN (Netherlands)

KTF (S Korea)

Maxis (Malaysia)

Magyar Telekom

(Hungary)

Mobile TeleSystems

(Russia)

Mobilink (Pakistan)

Mobinil (Egypt)

MTN (S Africa)

NTT DoCoMo (Japan)

O2 (Ireland)

Omnitel Vodafone (Italy)

Optus (Australia)

Oskar Mobil (Czech

Republic)

PLDT (Philippines)

Portugal Telecom

(Portugal)

Reliance Infocomm

(India)

Rogers (Canada)

SK Telecom (S. Korea)

SmarTone (Hong Kong)

SoftBank Mobile (Japan)

Tele2 (Lithuania)

Telefonica (Spain)

Telenor (Hungary)

TeliaSonera (Sweden)

Telstra (Australia)

T-Mobile (Czech Republic)

Ufone (Pakistan)

Vodacom (S Africa)

Vodafone (Greece)

Vodafone (Ireland)

Vodafone (Netherlands)

Vodafone Egypt (Egypt)

Vodafone Portugal

(Portugal)

Vodafone Spain (Spain)

WIND (Greece)

Cellular market size

Cellular penetration

Cellular revenue

Cellular revenue growth

GDP

GDP growth

Market age

Market concentration

Number of operators

Population

3G/4G/LTE network starting year

Cellular revenue

Cellular revenue growth

Country ARPU

Country cellular EBIT

Country cellular data usage

Entry order

Global capex

Global total EBIT

Global total revenue

Market share

Users

Years in market

14

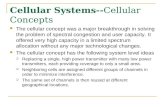

The COAT database is analyzed using a sophisticated structural equation model (SEM)

PARTIAL PATH DIAGRAM FOR PROFITS IN THE CELLULAR OPERATOR MARKET

Profit

ARPU relative to

GDP/capita

Market age

Market ARPU

Operator

market share

Number of

operators

Entry

positionGDP/capita

GDP growth

Market

penetration

Capital

expenditure

E1

E2

E3

E4E5

E6

.47.51

-.50

-.54

-.07

-.31

.31

.37

.00

.88

-.22

.20

.22

.71 -.34

.15

.13

-.14

.00.31

.15

-.21

.77

-.44

.17

.68

.61

.88 .25.80

.64

.68

Source: COAT, Canback analysis

15

This technical approach is converted into a set of simplified relationships, to understand and

explain the drivers of profitability (or growth—not shown here)

PATH DIAGRAM FOR CELLULAR OPERATOR

PROFITABILITY

PROFITABILITY

EBIT/Revenue

ARPU relative to

GDP/capita

Market age

Market ARPU

Operator

market share

Number of

operators

Entry

position

GDP/capita

GDP growth

Market penetration

MIN. IN SAMPLE MAX. IN SAMPLE

0.5 32

3 22

6 80

2 6

5% 90%

1 4

450 48,000

-1% +10%

11% 94%

Independent

variables

Dependent

variable

Note: EBIT/Revenue is the only profitability metric easy to collect for most operators

Source: COAT

16Source: COAT, Canback analysis

The analysis quantifies the importance of each profitability and/or growth driver

R R2

Standard

error of

the

estimate

Durbin-

Watson

0.78 0.61 0.12 2.0

MODEL SUMMARY

Variable t-stat

B Standard error

Constant 0.6019 0.2093

ARPU relative to GDP/capita 0.1170 0.0082 2.36

Market age 0.2239 0.0205 2.28

Market ARPU -0.0982 0.0057 -2.21

Number of operators -0.2281 0.0368 -1.67

Operator market share -0.3585 0.5282 -1.30

Entry position -0.1867 0.0825 -1.20

GDP/capita 0.0200 4.3E-06 0.57

GDP growth 0.4252 1.4244 0.51

Market penetration -0.0300 0.2346 -0.07

Unstandardized

coefficients

0.0 0.2 0.4 0.6 0.8 1.0

No statistical significance

Low

statistical

signifi-

cance

High

statistical

signifi-

cance

Significance

17

Operator

market share

The result is a detailed understanding of what drives growth and/or profitability, and how operators

can succeed in a given environment

* Based on a statistical (SEM) analysis of 46 operators in 24 countries between 2008 and 2013 (pooled time series cross-sectional analysis).

Source: COAT, Canback analysis

COMMENTS

The longer the cellular market has existed, the higher the profitability.

(This is true in most markets and industries.)

Profitability declines with the number of operators

Operators with high prices are less profitable.

In a given market, a high ARPU strategy leads to

higher profitability

Third entrants are perhaps slightly disadvantaged, but the statistical

significance is low, and disappears if 1st, 2nd, 3rd entrant groups are

tested separately

Operator market share has a slight negative impact on profitability

The level of market penetration does not affect profitability

Rich (OECD) markets are neither more or less profitable

than emerging markets

General GDP growth does not influence profitability

PATH DIAGRAM* FOR CELLULAR OPERATOR

PROFITABILITY

PROFITABILITY

EBIT/Revenue

61% of profitability

explained (R2)

ARPU relative to

GDP/capita

Market age

Market ARPU

Number of

operators

GDP/capita

GDP growth

Market penetration

-0.17

0.40

-0.40

-0.29

-0.12

n/m

n/m

n/m

0.60

High statistical significance

No statistical significance

Low statistical significance

Entry

position

1st entrant

2nd entrant

3rd entrant

18

The COAT database can used, for example, to predict the success of new market entrants or new

price strategies

Average for

comparison

countries

=17%

PROFITABILITY IN THE CHINESE CELLULAR OPERATOR MARKETEBIT/Revenue

PROFITABILITY SENSITIVITY ANALYSIS*2013

* Based on a statistical (SEM) analysis of 46 operators in 24 countries between 2008 and 2013 (pooled time series cross-sectional analysis)

** Data for US includes Cingular, Nextel and Verizon

*** High-ARPU strategy defined as 25% above China Mobile’s 2013 ARPU

Source: COAT, annual reports, Canback analysis

3 players

27%

2 players

26%

30%

22%4 players

30%

3 players

4 players

Total China:

Total China:

High-ARPU

strategy***:

35%

38%39%

32%

18%

30%

35%

38%

31%

2013

22%

US** 2013

15%

20122011

27%

2010

29%

Total ChinaChina UnicomChina Mobile

19

EIU Canback contact information

AMERICAS

Boston EIU Canback, Inc.

210 Broadway, Suite 303

Cambridge MA 02139

+1-617-399-1300

Irina Blinova

Mexico City Canback Mexico

Bosque de Ciruelos 194, PH3

Bosques de las Lomas

11700 Ciudad de México, D.F.

+52-55-4164-8500

+52-155-4354-9806

Francisco Maciel Morfin

Chicago EIU Canback USA

500 N. Michigan Ave.

Suite 1925

Chicago IL 60611

+1-312-853-3716 or 3823

Tom Andrews

Maureen Lanigan

Sao Paulo EIU Canback Brazil

Av. Brigadeiro Faria Lima, 3144

3º andar Jardim Paulistano

São Paulo, 01451-000

+55-11-3845 4767

Marcio Zanetti

EUROPE

London EIU Canback Europe

20 Cabot Square

London E14 4QW

+44-20-7576-8181

Chris Pearce

Asif Chaudhary

MIDDLE EAST AND AFRICA

Dubai EIU Canback MENA

Aurora Tower, 13th Floor

Office 1301A, PO Box 450056

Dubai Media City

+971-4433-4202

+971-52-269-8425

Paul Yata

Johannesburg EIU Canback Africa

First Floor, Building 8

Inanda Greens Office Park

55 Wierda Road East

Wierda Valley, Sandton

+27-83-786 2450

Arshad Abba

ASIA

Beijing EIU Canback China

Unit 1711, 17/F, Block 1

Taikang Financial Tower

38 East 3rd Ring Rd. North

Chaoyang District 100026

+86-10-8571-2188

Alex van [email protected]

Shanghai EIU Canback China

Rm 2508A, 25/F, Rui Jin Bldg

205 Mao Ming South Rd,

Shanghai 200020

+86-21-6473-7128

Seumas [email protected]

Singapore EIU Canback Southeast Asia

8 Cross St, #23-01 PWC Bldg.

Singapore 048424

+65-6534-5177

Vanny Dang

Tokyo EIU Canback Japan

Ginza Wall Building UCF 5F

6-13-16 Ginza

Chuo-ku, Tokyo 104-0061

+81-3-6338-0002

Shin Ito

Jakarta EIU Canback SE Asia

Jl. Tiang Bendera 5 no. 2A

DKI Jakarta 11230

+62-812-8743 7578

Teddy Purnomo