‘Business Profits’ under Tax Treaties - The Chamber of … · · 2017-09-08‘Business...

26

‘Business Profits’ under Tax Treaties Sanjay Sanghvi Workshop on Taxation of Foreign Remittances | Mumbai | 22 January 2016

Transcript of ‘Business Profits’ under Tax Treaties - The Chamber of … · · 2017-09-08‘Business...

‘Business Profits’under Tax Treaties

Sanjay Sanghvi

Workshop on Taxation of Foreign Remittances

| Mumbai | 22 January 2016

Copyright © Khaitan & Co 2016 | 2

Business Profits | Broad Framework Governing Provisions

– Domestic law – Section 9 (1)(i) of the Income-tax Act (Act) read with Rule 10 of the Income-tax Rules

– Tax Treaty – Article 7 read with Article 5 of the Tax Treaties

Income in the nature of ‘business profits’ is taxable in India – subject to constitution of a business connection (BC)/ permanent establishment (PE) in India.

– PE is the sine qua non for taxability of business profits

‘Business Profits’ not defined – Intended to cover income from any trade or business (US Model Commentary [2006])

Only those profits which are attributable to PE in India are taxable

Characterisation of income important

– Absence of PE – unless income is in the nature of royalty, interest, or FTS- not taxable in source state

– In case of PE – even royalty, interest, FTS attributable to PE is taxable as business profit

Copyright © Khaitan & Co 2016 | 3

Business Profits | Broad Framework

Taxation Provision Threshold for Taxation Quantum of Taxable Profits

Domestic Law Existence of Business Connection

Reasonably attributable to operations in India

Tax Treaties Existence of Permanent Establishment

Attributable to PE (directly or indirectly – Force of attraction under certain tax treaties, see India-US DTAA or India-UK DTAA)

Taxation of ‘business profits’ of a non-resident in India (i.e. the Source State)

Beneficial provisions of the Act or the Tax Treaty can be applied

Copyright © Khaitan & Co 2016 | 4

Taxation of Business Profits

Country of residence has a tax treaty with India & NR eligible to access treaty

• Analysis as per tax treaty• Permanent Establishment (PE)

test• Art. 5, e.g., Fixed Place PE,

Service PE, Agency PE

Country of residence does not have a tax treaty with India or

where NR is not eligible to access treaty

• Analysis as per Act• Business Connection (BC) test • Section 9, Act ‘real and intimate

connection’

Business Profits | Broad Framework

Copyright © Khaitan & Co 2016 | 5

Decisive condition for taxation of income from business activities

PE is a fixed place of business through which the business of a foreign enterprise is wholly or partly carried on in India

PE is a term defined in tax treaties to determine when a non-resident enterprise is taxable in source country

Section 9(1)(i) of the Act deems taxability of all income accruing or arising directly or indirectly through or from any ‘business connection’ in India

It defines the requisite level of nexus in a country to support taxation of income at source

‘Business connection’ not defined but much wider than PE as determined by judicial precedents (SC decision in RD Agarwal & Co):

– Existence of ‘business’ & ‘connection’ – must be real and intimate– an element of continuity between the Non resident’s (NR) business and

activity in India– ‘facilitation of & assistance to’ the NR’s business in India based on facts of

case Star Cruise India Travel Services Pvt Ltd (ITAT Mumbai) - mere canvassing for business of

the non-resident principal by an agent in India is out of the scope of business connection

Significance of ‘Business Connection’ / ‘Permanent Establishment’

Copyright © Khaitan & Co 2016 | 6

Fixed place PE

– Excludes inter alia: place of business for carrying out preparatory & auxiliary activities

Service PE (UN Model)

Construction/ installation PE

Agency PE

– Dependent v independent agents

– Legal and economic independence

Various forms of PE

Copyright © Khaitan & Co 2016 | 7

Various forms of PE

Fixed Place PE

This term is not defined in the OECD MC, UN MC or tax treaties or in the Act

Determination is factual – any form of presence of a foreign enterprise (physical office or through employees/ representatives) could be treated as a fixed place of business

Agency PE

‘Agency’ describes a relationship by which one person (Agent) has the authority to legally bind another person (Principal) in dealing with third parties

Under UN MC and the OECD MC, generally an agency relationship can constitute a PE only if the agent is a ‘dependent agent’

An agent catering to a number of clients in its usual course of business who is not financially, managerially or otherwise dependent on or controlled by a single principal - an ‘independent agent’ (not a PE)

Copyright © Khaitan & Co 2016 | 8

Various forms of PE

Service PE

Under UN MC, Service PE of an enterprise is constituted if:

–Services are furnished by the enterprise within the Source State–The services are furnished by the foreign enterprise through its employees or other personnel–The period of furnishing of services exceeds the specified threshold period

Indian tax treaties which include Service PE clause are based on UN MC clause with / without variations in threshold period, etc.

OECD MC currently does not have a Service PE clause.

Construction Installation PE

Under UN MC, a Construction/Installation PE of an enterprise is constituted if:–A building site, a construction, assembly or installation project or supervisory services in connection therewith;–Period of furnishing of services and/or the building site, construction, assembly or installation exceeds specified threshold period

OECD MC currently does not deem supervisory activities in connection with building site, construction etc. to create a PE

Copyright © Khaitan & Co 2016 | 9

Certain Issues In the absence of any threshold under the basic rule, how much presence creates a risk

– Golf in Dubai (AAR)

Specific PE v PE under the basic rule

– Will the presence of employees/ representatives be tested only under Service PE rule

– Is the test under the basic PE rule also relevant?

What sort of activities fall within the purview of ‘preparatory and auxiliary services’ – factual determination – for instance, activities typically undertaken by rep office/ Los (UAE Exchange –Delhi HC)

Online Marketplace (e-commerce) – Can a website be treated as a PE? Is location of the server determinative?

Under agency PE clause, would negotiations by an agent or a representative on behalf of a foreign principal trigger agency PE risk

– India’s reservation under the OECD – mere participation in negotiations is sufficient for PE conclusion

– In some treaties, ‘negotiations’ specifically included

Business profits v other income – In some treaties, ‘other income’ attributable to PE taxable in source state. In certain other treaties, taxable in source state whether or not attributable to PE.

Attribution of Profits to a PE

Copyright © Khaitan & Co 2016 | 11

Principles of Attribution | Domestic Law

No specific mechanism provided for attribution of profits

Transfer pricing rules can be applied to undertake arm’s length attribution

General Principles of Attribution

Profit attribution restricted to amount ‘reasonably attributable’ to operations in India [Clause (a) of Explanation 1 to section 9(1)(i)]

Exclusions From Attribution [Explanation 1 to section 9(1)(i)]

Operations confined to purchase of goods in India for the purpose of export

Collection of news & views in India for transmission out of India by news agency, etc

Operations confined to shooting of cinematograph film in India

Rule 10 of the Rules can be applied - determining income in the case of non-residents that are unable to definitely ascertain the income attributable to their India operations

Function / Asset / Risk analysis imperative to determine profit attribution – Morgan Stanley

Copyright © Khaitan & Co 2016 | 12

Principles of Attribution | Domestic Law

Prescribed Methods For Attribution [Rule 10]

If ascertainable, AO to determine actual profit

If AO thinks actual profit determination fails, he can ascertain profits by adopting:-

– a reasonable % of turnover

– global profit formulary approach; apply ratio of Indian receipts to Total (business) receipts

– such other manner as AO deems suitable

Over the last few years, judicial forums in India (ITAT and above) have espoused the TP – arm’s length approach i.e. if the PE has been remunerated at an ALP, then nothing further remains to be attributed (Morgan Stanley (SC), SET Satellite (Bom HC), BBC Worldwide Limited (ITAT, Delhi Bench))

Copyright © Khaitan & Co 2016 | 13

Article Key Provisions

Art 7(1) Basic Rule

Income Attributable to PE

Force of Attraction Rule (if any) or Indirect attribution

Art 7(2) Computation Hypothesis

As if PE is

– a distinct and independent enterprise

– engaged in same or similar activities

– under same or similar conditions Art 7(3)

Expense Deduction Actual Expense incurred, incl. reasonable allocation

of General & Admin Overheads

Whether in source state or in HO state

Subject to domestic law (Section 44C)

No deduction for HO payment (except reimbursement of actual expenses)

Others (varies from Treaty to Treaty)

Applying Apportionment method in case of difficulty (reasonable)

Methodology applied consistently Y-on-Y

Exception (Purchase activity)

Principles of Attribution | Tax Treaties

Copyright © Khaitan & Co 2016 | 14

Principles of Attribution | Tax Treaties

Article 7(1) | OECD Model Commentary

Profits of an enterprise of a Contracting State shall be taxable only in that State unless it carries on business in other Contracting State through a permanent establishment situated therein. If so, profits that are attributable to the permanent establishment in accordance with the provisions of paragraph 2 may be taxed in that other State

Key aspects:

– Existence of PE must for attribution - Only profits attributable to such PE are taxable in the source country

– Nothing attributable if activities are preparatory or auxiliary in nature e.g. purchasing of goods

Copyright © Khaitan & Co 2016 | 15

Principles of Attribution | Tax Treaties

Authorised OECD Approach (AOA)

Authorised OECD approach contains 2 steps:

– Conduct a functional and factual analysis to hypothesise the PE as a separate and distinct enterprise. Attribute to the PE functions, transactions / contracts with third parties, assets, risks, free capital.

– Apply the arm’s length principle and Tranfer Pricing Guidelines by analogy to the “dealings” recognised between the PE and other parts of the enterprise it belongs to

– onus on the foreign enterprise to furnish a comprehensive transfer pricing study to the Revenue

– However, if the taxpayer is of the view that no profits are attributable to the PE – then onus is on the Revenue to demostrate that conditions of Article 7 (1) were fulfilled.

– Same principles must be applied to attribute losses

Copyright © Khaitan & Co 2016 | 16

UN Model – Article 7 (Also see US / UK Treaty)

Profits may be taxed but only so much of them as is attributable to-

– that PE,– sale of goods or merchandise of the same or similar kind as those sold through

that PE– other business activities carried on of the same or similar kind as those

effected through that PE Key Aspects

– FOA enlarges the scope of PE country taxation– If the above conditions are fulfilled, the profits attributable to such sale of goods

or the business activities would be taxable. The sale need not be conducted through PE nor have any connection / involvement with the PE (UN Commentary (2011) / Asst DIT v WNS North America )

Exemptions– Demonstrate that sale or business activities carried out other than through PE,

for legitimate business purpose and not to obtain treaty benefit– Sale by foreign principal through independent agents FOA present only in the UN Model and not the OECD Model No FOA Rules under the ITA- receipt basis of taxation

Force of Attraction Rule | UN Model Convention

Case Laws

Copyright © Khaitan & Co 2016 | 18

• Courts have held that attribution of profits is an exercise that would depend upon peculiar facts and circumstances of each case

• It should not be arbitrary but should be on a fair and rational basis and should meet the end of justices

• At the same time, any finding on the question of attribution will generally involve guesswork

• Endeavour could only be to approximate and there cannot be great precision and exactness

Attribution of Profits to PE | Case Laws

Copyright © Khaitan & Co 2016 | 19

Attribution of Profits to PE | Case Laws

Morgan Stanley and Co – Supreme Court

Activities outsourced by MS Co. to Indian group entity MSAS:– Equity / fixed income research– Account reconciliation; – IT enabled services, etc

MS Co. staff visited India for monitoring/quality control (stewardship)

MS Co. staff deputed to MSAS– MSAS reimburses salary cost to MS Co.– Employees deputed continue to be employed with MS Co., which pays

salary to the deputees outside India Service PE upheld

Profits of PE determined based on what an independent enterprise under similar circumstances might be expected to derive

Profits of MS Co. which have economic nexus with PE attributable

Associated Enterprise that constitutes PE and is remunerated on arms length basis taking into account all risk taking functions of the multinational enterprise – no further attribution

If TP analysis does not adequately reflect functions performed / risks assumed by the enterprise – there would be need to attribute profits for those functions / risks

Copyright © Khaitan & Co 2016 | 20

Attribution of Profits to PE | Case Laws

Convergys Customer Management Group Inc. - ITAT Ruling

CCMG, USA, was engaged in the business of providing Information Technology (IT) enabled customer management services to its clients outside India

CCM procured services from CIS on principal to principal basis :– IT enabled call centre services– Back office support services ; –CCM staff visited CIS for supervision/direction and control–CCM also provided certain hardware and software assets on free of cost basis to CISTax authorities held that CCMG had a PE in India in various forms viz-a-viz a fixed place PE, a service PE and a dependent agent PEThe Tribunal computed profits attributable to the PE in India by applying a formula. The global operating margin was applied to the revenues attributable to India. The excess of such profits attributable to India over profits earned by the Indian company were further attributed to the PE at the rate of 15% of such residuary profits

Copyright © Khaitan & Co 2016 | 21

Rolls Royce – ITAT Ruling

•Recently, the Delhi HC in the case of Rolls Royce UK and Rolls Royce Singapore, held that attribution of profits to a PE requires robust TP analysis

•The HC ruled that where the activities of the PE in India are remunerated at fair value and this has been taxed in India, there is no question of the taxpayer being taxed again on the same deemed income

•Remuneration paid to the PE could be reasonable and meet the ALP criteria if justified by a TP Study

Attribution of Profits to PE | Case Laws

Copyright © Khaitan & Co 2016 | 22

Attribution of Profits to PE | Issues

• Whether further attribution required when a robust TP analysis has been undertaken.

– Yes, refer NGC Network Asia LLC (ITAT Mumbai)

– Distinguished on facts from Morgan Stanley– ALP Certification + decision of various courts applicable only

where payments made by foreign enterprise to its Indian AE – Held – where foreign company receives money from India

and it is held to have a PE, then taxability to be examined under the provisions of the Act and Treaty

• When further attribution is not required to be done (based on the principle upheld in Morgan Stanley ruling and applied in various other rulings, what is the additional implication of a PE?

• Applicability of MAT – Taxable profits and book profits likely to be same and thus, tax may be payable under the normal provisions only

Copyright © Khaitan & Co 2016 | 23

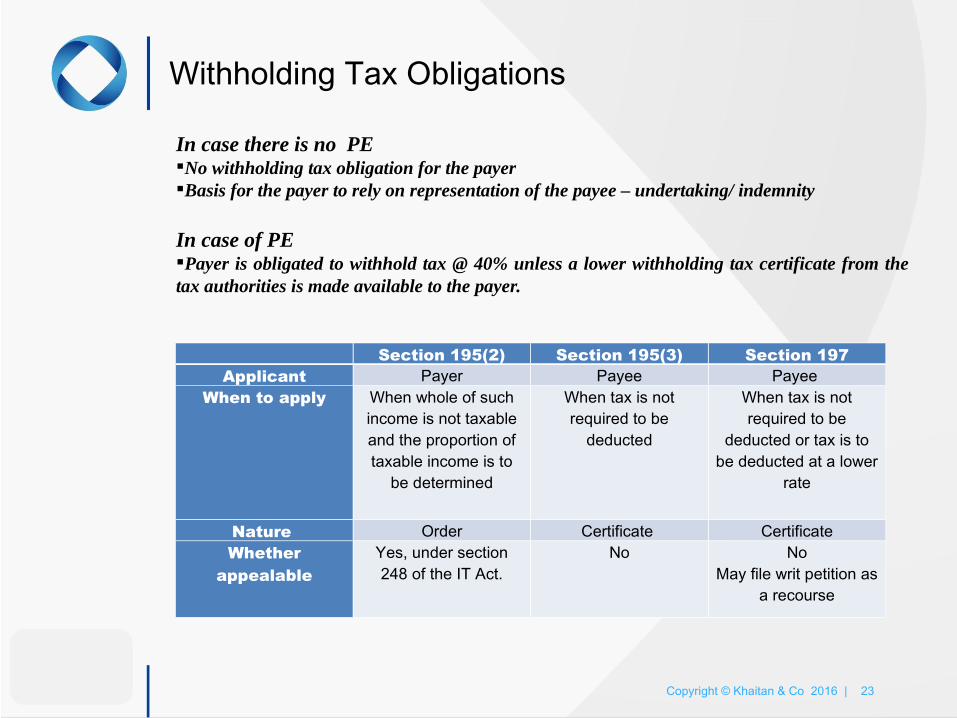

In case there is no PENo withholding tax obligation for the payerBasis for the payer to rely on representation of the payee – undertaking/ indemnity In case of PEPayer is obligated to withhold tax @ 40% unless a lower withholding tax certificate from the tax authorities is made available to the payer.

Withholding Tax Obligations

Section 195(2) Section 195(3) Section 197Applicant Payer Payee Payee

When to apply When whole of such income is not taxable and the proportion of taxable income is to

be determined

When tax is not required to be

deducted

When tax is not required to be

deducted or tax is to be deducted at a lower

rate

Nature Order Certificate CertificateWhether

appealableYes, under section 248 of the IT Act.

No NoMay file writ petition as

a recourse

Key Takeaways

Copyright © Khaitan & Co 2016 | 25

PE – a dynamic concept

Attribution – a complex and contentious exercise

Documenting functional analysis – key defense

On-going review of factual position

Attribution vis-à-vis arm’s length payments

Upfront planning desirable

Well documented Transfer pricing policy- Important to defend claims from revenue authorities

Advance Pricing Arrangements may be useful in reducing the uncertainty

Key Takeaways

www.khaitanco.com

![Interpreting Tax Treaties - Iowa Law ReviewA3_KYSAR.DOCX (DO NOT DELETE) 4/4/2016 12:09 PM 2016] INTERPRETING TAX TREATIES 1391 treaties is particularly sparse. 8 A central goal of](https://static.fdocuments.us/doc/165x107/5f4328fc6a02956bdc7c682f/interpreting-tax-treaties-iowa-law-review-a3kysardocx-do-not-delete-442016.jpg)