2 Corporation tax – trading profits · 2.4 business tax (Finance Act 2014) tutorial. corporation...

26

In this chapter we provide a brief review of the Corporation Tax computation, and examine the step by step procedures for compiling the computation, before concentrating on the calculation of adjusted trading profits. We examine in detail how to adjust the data provided in an income statement so that it is valid for tax purposes. This involves adjusting income and expenditure. We will note the main types of expenditure that cannot be set against trading income, as well as specific examples of expenditure that is allowable. There will be opportunities to practice adjusting accounts that have been prepared for internal purposes, as well as using published accounts. We will then see how to deal with the situation when accounts have been prepared for a long period and need to be split into two Chargeable Accounting Periods. Finally, we will learn the rather complex rules about the options that are available to companies to offset any trade losses that they incur. Corporation tax – trading profits 2 this chapter covers...

Transcript of 2 Corporation tax – trading profits · 2.4 business tax (Finance Act 2014) tutorial. corporation...

In this chapter we provide a brief review of the Corporation Tax computation, andexamine the step by step procedures for compiling the computation, beforeconcentrating on the calculation of adjusted trading profits.We examine in detail how to adjust the data provided in an income statement so that itis valid for tax purposes. This involves adjusting income and expenditure. We will notethe main types of expenditure that cannot be set against trading income, as well asspecific examples of expenditure that is allowable.There will be opportunities to practice adjusting accounts that have been prepared forinternal purposes, as well as using published accounts.We will then see how to deal with the situation when accounts have been prepared fora long period and need to be split into two Chargeable Accounting Periods. Finally, we will learn the rather complex rules about the options that are available tocompanies to offset any trade losses that they incur.

Corporation tax –trading profits

2

this chapter covers...

calculate Corporation Tax liability based on taxable total profits

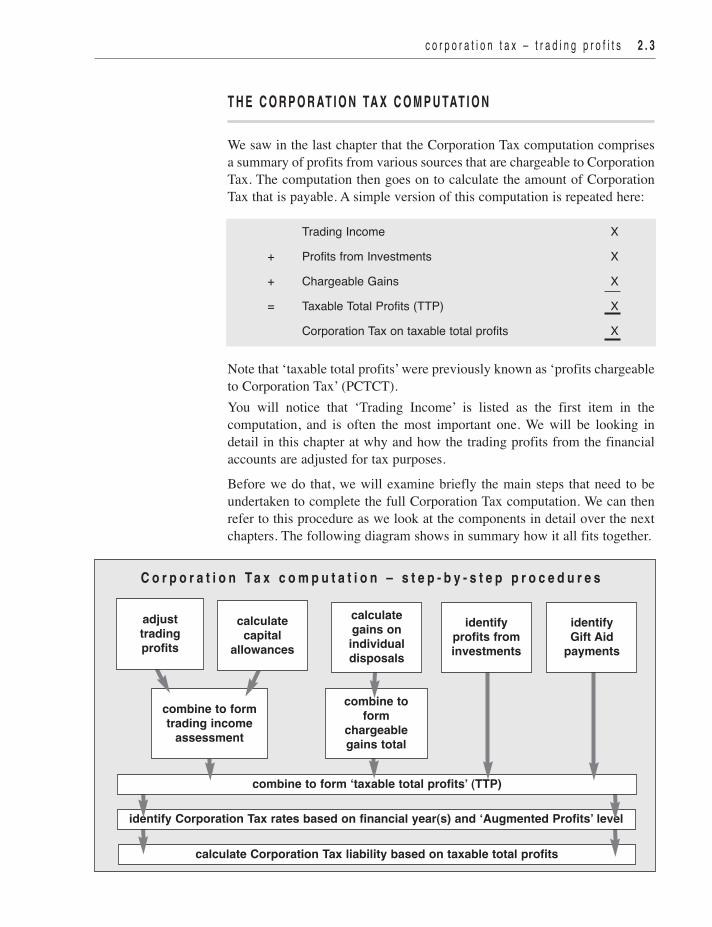

T H E C O R P O R AT I O N TA X C O M P U TAT I O N

We saw in the last chapter that the Corporation Tax computation comprisesa summary of profits from various sources that are chargeable to CorporationTax. The computation then goes on to calculate the amount of CorporationTax that is payable. A simple version of this computation is repeated here:

Trading Income X

+ Profits from Investments X

+ Chargeable Gains X

= Taxable Total Profits (TTP) X

Corporation Tax on taxable total profits X

Note that ‘taxable total profits’ were previously known as ‘profits chargeableto Corporation Tax’ (PCTCT). You will notice that ‘Trading Income’ is listed as the first item in thecomputation, and is often the most important one. We will be looking indetail in this chapter at why and how the trading profits from the financialaccounts are adjusted for tax purposes.

Before we do that, we will examine briefly the main steps that need to beundertaken to complete the full Corporation Tax computation. We can thenrefer to this procedure as we look at the components in detail over the nextchapters. The following diagram shows in summary how it all fits together.

c o r p o r a t i o n t a x – t r a d i n g p r o f i t s 2 . 3

C o r p o r a t i o n T a x c o m p u t a t i o n – s t e p - b y - s t e p p r o c e d u r e s

identify Corporation Tax rates based on financial year(s) and ‘Augmented Profits’ level

combine to form ‘taxable total profits’ (TTP)

identifyprofits frominvestments

identify Gift Aid

payments

combine toform

chargeablegains total

calculategains onindividualdisposals

combine to formtrading income

assessment

adjusttradingprofits

calculatecapital

allowances

In this chapter we are going to learn how to adjust the trading profit (the topleft-hand box in the diagram). We will also see how trade losses can be setagainst profits to reduce total taxable profits. In Chapter Three we will see how to calculate capital allowances so that wecan incorporate the result into the trading income assessment. In Chapter Four we will examine chargeable gains and then we will see howit all fits together.In Chapter Five we will explain how to calculate the Corporation Taxliability.

A D J U S T M E N T O F P R O F I T S

The starting point for the calculation of trading profits is the statement ofprofit or loss (income statement) that has been prepared by the company.Whether you are asked to work from a set of accounts prepared for internaluse, or in published format, the process is the same.

The ‘basis of assessment’ for trading profits is the tax-adjusted tradingprofits of the chargeable accounting period, prepared on an accruals basis.In this section of the book we will start by using accounts that have beenprepared for the chargeable accounting period (ie no more than 12 months).We will see later how we deal with accounts that have been prepared for alonger period. Since the financial accounts that will be our starting point willalways have been prepared on an accruals basis, that aspect should not causeus any problems.

The reason that accounts need to be adjusted for tax purposes is not becausethey are wrong, but because Corporation Tax does not use exactly the samerules as financial accounting. We need to arrive at a profit figure that is basedon the tax rules! For example, there are some costs that although quitelegitimate from an accounting point of view are not allowable as a deductionin arriving at the profit figure for tax purposes.

The object of adjusting the financial accounts is to make sure that:n the only income that is credited is trading incomen the only expenditure that is deducted is allowable trading expenditure

When we adjust profits, we will start with the profit from the financialaccounts, andn deduct any income that is not trading income, andn add back any expenditure that has already been deducted but is not allowable

This approach is much more convenient than re-writing the whole profit andloss account based on tax rules. It is quite logical, because it effectivelycancels out income and expenditure that is not relevant for tax purposes.

2 . 4 b u s i n e s s t a x ( F i n a n c e A c t 2 0 1 4 ) t u t o r i a l

c o r p o r a t i o n t a x – t r a d i n g p r o f i t s 2 . 5

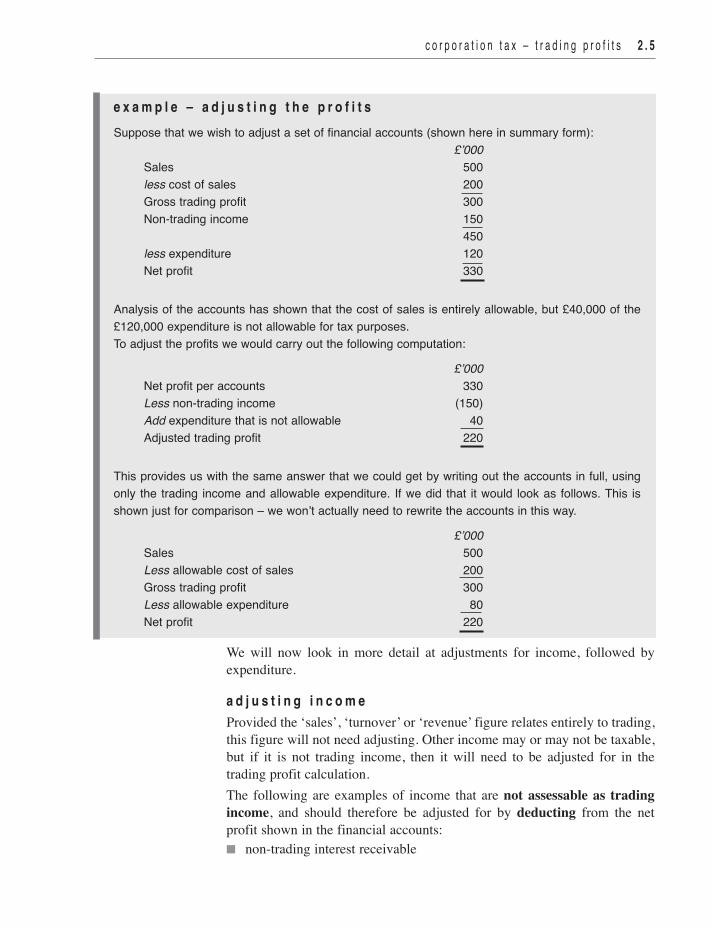

e x a m p l e – a d j u s t i n g t h e p r o f i t sSuppose that we wish to adjust a set of financial accounts (shown here in summary form):

£’000Sales 500less cost of sales 200Gross trading profit 300Non-trading income 150

450less expenditure 120Net profit 330

Analysis of the accounts has shown that the cost of sales is entirely allowable, but £40,000 of the£120,000 expenditure is not allowable for tax purposes.To adjust the profits we would carry out the following computation:

£’000Net profit per accounts 330Less non-trading income (150)Add expenditure that is not allowable 40Adjusted trading profit 220

This provides us with the same answer that we could get by writing out the accounts in full, usingonly the trading income and allowable expenditure. If we did that it would look as follows. This isshown just for comparison – we won’t actually need to rewrite the accounts in this way.

£’000Sales 500Less allowable cost of sales 200Gross trading profit 300Less allowable expenditure 80Net profit 220

We will now look in more detail at adjustments for income, followed byexpenditure.

a d j u s t i n g i n c o m eProvided the ‘sales’, ‘turnover’ or ‘revenue’ figure relates entirely to trading,this figure will not need adjusting. Other income may or may not be taxable,but if it is not trading income, then it will need to be adjusted for in thetrading profit calculation. The following are examples of income that are not assessable as tradingincome, and should therefore be adjusted for by deducting from the netprofit shown in the financial accounts:n non-trading interest receivable

2 . 6 b u s i n e s s t a x ( F i n a n c e A c t 2 0 1 4 ) t u t o r i a l

n rent receivablen gains on the disposal of non-current assets (fixed assets)n dividends receivedAll these examples should be adjusted by simply deducting the amount thatwas credited to the financial accounts. There is no need to worry aboutexactly how the figure was originally calculated. We will then have arrivedat what the profit would have been if these items had not been includedoriginally. Items that originate from the trade (eg discounts received) aretaxable as part of trading income, and therefore need no adjustment.Non-trading interest and rent received will reappear in the taxable totalprofits (TTP) computation as investment income and property incomerespectively. Throughout the examples in this book you can assume that anyinterest received is non-trading and is therefore dealt with as outlined hereunless stated otherwise. Gains on the disposal of non-current assets could result in chargeable gains.These gains need to be calculated according to special rules before beingincorporated into the taxable total profits as we will see in Chapter 4. Dividendsreceived from UK companies are not assessable under Corporation Tax at all(since they have been paid out of another company’s taxed income), although,as we will see later, they can have an impact on the rate of tax applied.

a d j u s t i n g e x p e n d i t u r eWe will only need to adjust for any expenditure accounted for in the financialaccounts profit if it is not allowable. We do this by adding it back to thefinancial accounts profit. Expenditure that is allowable can be left unadjustedin the accounts. Although this may seem obvious, it is easy to get confused.

The general rule for expenditure to be allowable in a trading incomecomputation is that it must be:n revenue rather than capital in nature, andn ‘wholly and exclusively’ for the purpose of the tradeAlthough we will look at how to deal with various specific types ofexpenditure shortly, these rules are fundamental, and should always be usedto guide you in the absence of more precise information. This part of the unitwill require a good deal of study, since it is quite complex, and the rules andexamples that follow will need to be remembered. The best way to approachthis is to continually revise the topic and practice lots of examples.

e x p e n d i t u r e t h a t i s n o t a l l o w a b l eThe following are examples of expenditure that is not allowable, andtherefore require adjustment. Some clearly follow the rules outlined above,while others may have arisen from specific regulations, or court casesforming precedents (case law).

c o r p o r a t i o n t a x – t r a d i n g p r o f i t s 2 . 7

n any capital expenditureThis follows the normal financial accounting use of the term, to meanexpenditure on assets that will have a value to the business overseveral accounting periods. Capital expenditure includes expenditureto improve non-current assets, and installation costs and legalexpenses in connection with acquiring non-current assets.

n depreciation of non-current assetsThis is because capital allowances are allowable instead, as HMRevenue & Customs alternative to depreciation, as we will see in thenext chapter. Even where there are no capital allowances available,depreciation is still not allowed. Other items which are similar todepreciation (eg amortisation of certain assets, and losses on disposalof non-current assets) are also not allowable.

n part of lease rental payments for high emission carsWhen a car with an emission level of more than 130g/km of CO2 isleased for over 45 days through an operating lease, 15% of the leaserental payment is disallowed, leaving an allowable expenditure of85% of the payment. If the car has emission levels lower than this thenall of the lease rental payment is allowable.

n entertaining expenditureThis relates to business entertaining of customers or suppliers.Entertaining of the businesses’ own staff is however allowable (seepage 2.9).

n gifts to customersVirtually all gifts made to customers are not allowable. There is anexception for some low-value items, as we will see shortly.

n increases in general bad debt provisionsAny such increase (that is debited to the income statement) must beadded back in the computation, and decreases in general provisionsadjusted for by deducting from profits. A general provision could bebased on a lump sum, or a percentage of total trade receivables(debtors). Increases in specific provisions and the actual write-off ofbad debts are however allowable. Where accounts have been preparedusing ‘impairment’ as a means of calculating the bad debt provision,the provision will be treated in the same way as a specific bad debtprovision. This applies as long as objective evidence was used tocalculate the amount of impairment. This situation could arise if, forexample, the accounts are prepared under International AccountingStandards. See also the additional note on page 2.9.

n charitable paymentsThese items can be deducted from the total profits of the company inthe taxable total profits (TTP) calculation as Gift Aid payments.Where this occurs the expenditure cannot also be deducted in the

calculation of trading profits. We will look a little more closely at giftaid payments in Chapter 5.

n fines for law breakingFines imposed on the company itself for lawbreaking (e.g. for breachesof health & safety legislation) are not allowable, nor are the associatedlegal costs. The costs of tax appeals are also not allowable. Fines forminor motoring offences incurred by employees whilst on business areallowable, but not if the employee is a Director of the company.

n certain legal expenses Legal expenses incurred on forming a company or acquiring newleases (both long and short leases).

n illegal payments For example bribes, or payments made in response to threats.

n donations to political partiesThese are not for the purpose of ‘the trade’ and so are not allowable.

n writing off non-trade loansFor example, loans to employees or directors (unless they wereincurred in the normal course of trade).

n dividends payableThe payment of dividends is not an allowable expense. However ifthese occur in the accounts after the net profit that we have used as thestarting point for our calculation, there will be no need for an adjustment.

n Corporation Tax Logically, the tax payment itself is not tax deductible!

e x p e n d i t u r e t h a t i s a l l o w a b l eAs already stated, revenue expenditure that is ‘wholly and exclusively’ forthe purpose of the trade is allowable. We will now list some illustrativeexamples, a few of which were referred to above.n normal cost of salesn normal business expenditure, for example:

- distribution costs- administration- salaries and wages, and employers’ NIC- rent, rates and insurance- repairs- advertising- business travel and subsistence- accountancy services- research & development expenditure

2 . 8 b u s i n e s s t a x ( F i n a n c e A c t 2 0 1 4 ) t u t o r i a l

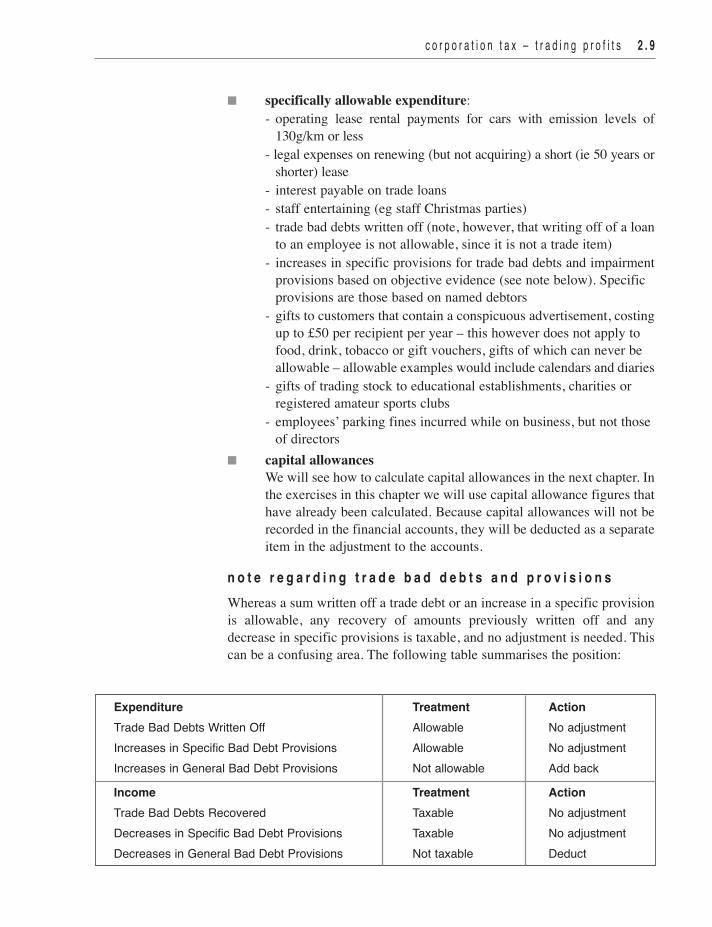

n specifically allowable expenditure:- operating lease rental payments for cars with emission levels of 130g/km or less

- legal expenses on renewing (but not acquiring) a short (ie 50 years orshorter) lease

- interest payable on trade loans- staff entertaining (eg staff Christmas parties)- trade bad debts written off (note, however, that writing off of a loanto an employee is not allowable, since it is not a trade item)

- increases in specific provisions for trade bad debts and impairmentprovisions based on objective evidence (see note below). Specific provisions are those based on named debtors

- gifts to customers that contain a conspicuous advertisement, costingup to £50 per recipient per year – this however does not apply to food, drink, tobacco or gift vouchers, gifts of which can never be allowable – allowable examples would include calendars and diaries

- gifts of trading stock to educational establishments, charities or registered amateur sports clubs

- employees’ parking fines incurred while on business, but not those of directors

n capital allowancesWe will see how to calculate capital allowances in the next chapter. Inthe exercises in this chapter we will use capital allowance figures thathave already been calculated. Because capital allowances will not berecorded in the financial accounts, they will be deducted as a separateitem in the adjustment to the accounts.

n o t e r e g a r d i n g t r a d e b a d d e b t s a n d p r o v i s i o n sWhereas a sum written off a trade debt or an increase in a specific provisionis allowable, any recovery of amounts previously written off and anydecrease in specific provisions is taxable, and no adjustment is needed. Thiscan be a confusing area. The following table summarises the position:

c o r p o r a t i o n t a x – t r a d i n g p r o f i t s 2 . 9

Expenditure Treatment ActionTrade Bad Debts Written Off Allowable No adjustmentIncreases in Specific Bad Debt Provisions Allowable No adjustmentIncreases in General Bad Debt Provisions Not allowable Add back

Income Treatment ActionTrade Bad Debts Recovered Taxable No adjustmentDecreases in Specific Bad Debt Provisions Taxable No adjustmentDecreases in General Bad Debt Provisions Not taxable Deduct

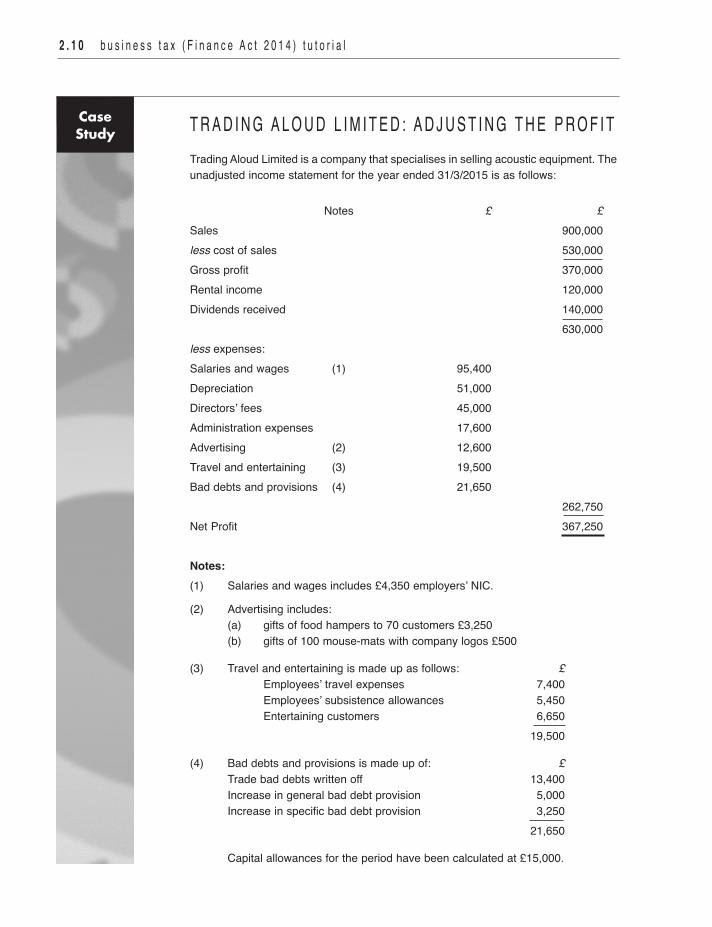

T R A D I N G A L O U D L I M I T E D : A D J U S T I N G T H E P R O F I TTrading Aloud Limited is a company that specialises in selling acoustic equipment. Theunadjusted income statement for the year ended 31/3/2015 is as follows:

Notes £ £Sales 900,000less cost of sales 530,000Gross profit 370,000Rental income 120,000Dividends received 140,000

630,000less expenses:Salaries and wages (1) 95,400Depreciation 51,000Directors’ fees 45,000Administration expenses 17,600Advertising (2) 12,600Travel and entertaining (3) 19,500Bad debts and provisions (4) 21,650

262,750Net Profit 367,250

Notes:(1) Salaries and wages includes £4,350 employers’ NIC.

(2) Advertising includes:(a) gifts of food hampers to 70 customers £3,250(b) gifts of 100 mouse-mats with company logos £500

(3) Travel and entertaining is made up as follows: £Employees’ travel expenses 7,400Employees’ subsistence allowances 5,450Entertaining customers 6,650

19,500

(4) Bad debts and provisions is made up of: £Trade bad debts written off 13,400Increase in general bad debt provision 5,000Increase in specific bad debt provision 3,250

21,650

Capital allowances for the period have been calculated at £15,000.

CaseStudy

2 . 1 0 b u s i n e s s t a x ( F i n a n c e A c t 2 0 1 4 ) t u t o r i a l

c o r p o r a t i o n t a x – t r a d i n g p r o f i t s 2 . 1 1

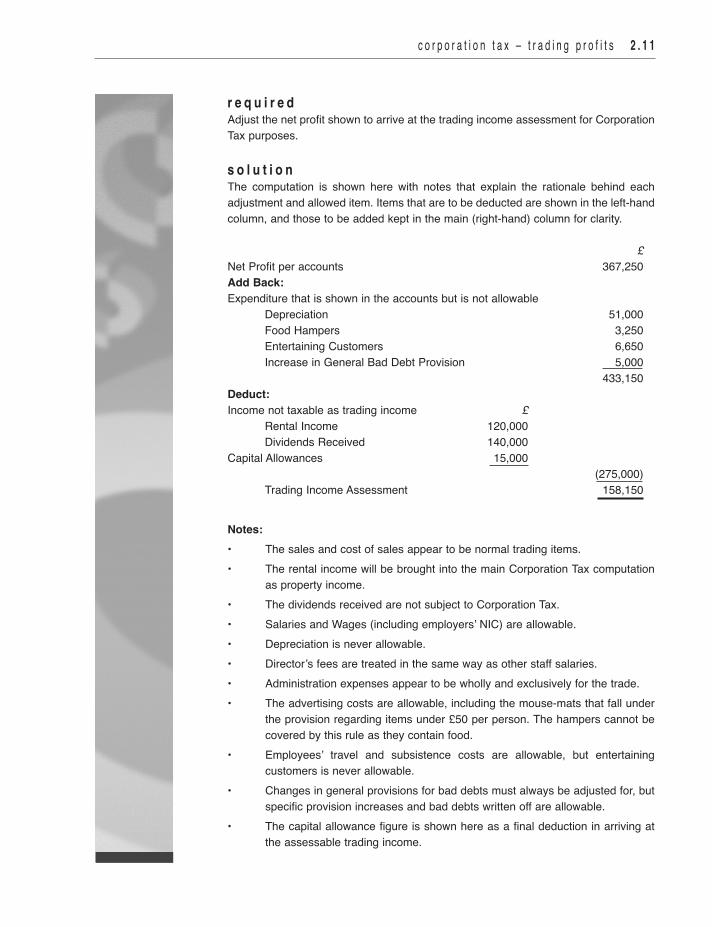

r e q u i r e dAdjust the net profit shown to arrive at the trading income assessment for CorporationTax purposes.

s o l u t i o nThe computation is shown here with notes that explain the rationale behind eachadjustment and allowed item. Items that are to be deducted are shown in the left-handcolumn, and those to be added kept in the main (right-hand) column for clarity.

£Net Profit per accounts 367,250Add Back:Expenditure that is shown in the accounts but is not allowable

Depreciation 51,000Food Hampers 3,250Entertaining Customers 6,650Increase in General Bad Debt Provision 5,000

433,150Deduct:Income not taxable as trading income £

Rental Income 120,000Dividends Received 140,000

Capital Allowances 15,000(275,000)

Trading Income Assessment 158,150

Notes:• The sales and cost of sales appear to be normal trading items.• The rental income will be brought into the main Corporation Tax computation

as property income.• The dividends received are not subject to Corporation Tax.• Salaries and Wages (including employers’ NIC) are allowable.• Depreciation is never allowable.• Director’s fees are treated in the same way as other staff salaries.• Administration expenses appear to be wholly and exclusively for the trade.• The advertising costs are allowable, including the mouse-mats that fall under

the provision regarding items under £50 per person. The hampers cannot becovered by this rule as they contain food.

• Employees’ travel and subsistence costs are allowable, but entertainingcustomers is never allowable.

• Changes in general provisions for bad debts must always be adjusted for, butspecific provision increases and bad debts written off are allowable.

• The capital allowance figure is shown here as a final deduction in arriving atthe assessable trading income.

2 . 1 2 b u s i n e s s t a x ( F i n a n c e A c t 2 0 1 4 ) t u t o r i a l

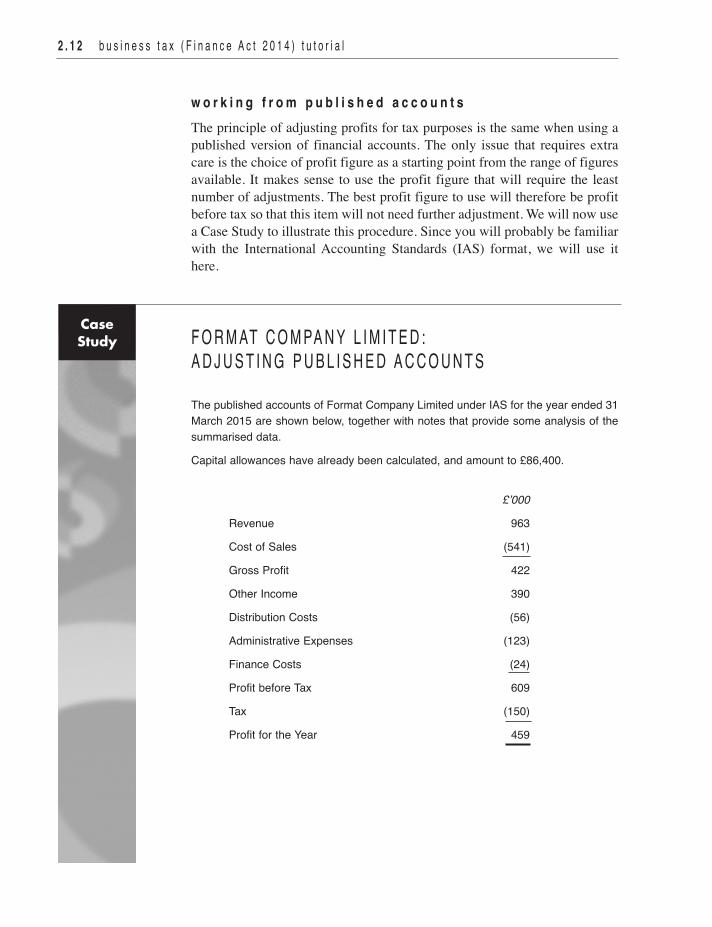

w o r k i n g f r o m p u b l i s h e d a c c o u n t sThe principle of adjusting profits for tax purposes is the same when using apublished version of financial accounts. The only issue that requires extracare is the choice of profit figure as a starting point from the range of figuresavailable. It makes sense to use the profit figure that will require the leastnumber of adjustments. The best profit figure to use will therefore be profitbefore tax so that this item will not need further adjustment. We will now usea Case Study to illustrate this procedure. Since you will probably be familiarwith the International Accounting Standards (IAS) format, we will use ithere.

F O R M AT C O M PA N Y L I M I T E D : A D J U S T I N G P U B L I S H E D A C C O U N T S

The published accounts of Format Company Limited under IAS for the year ended 31March 2015 are shown below, together with notes that provide some analysis of thesummarised data.

Capital allowances have already been calculated, and amount to £86,400.

£’000

Revenue 963

Cost of Sales (541)

Gross Profit 422

Other Income 390

Distribution Costs (56)

Administrative Expenses (123)

Finance Costs (24)

Profit before Tax 609

Tax (150)

Profit for the Year 459

CaseStudy

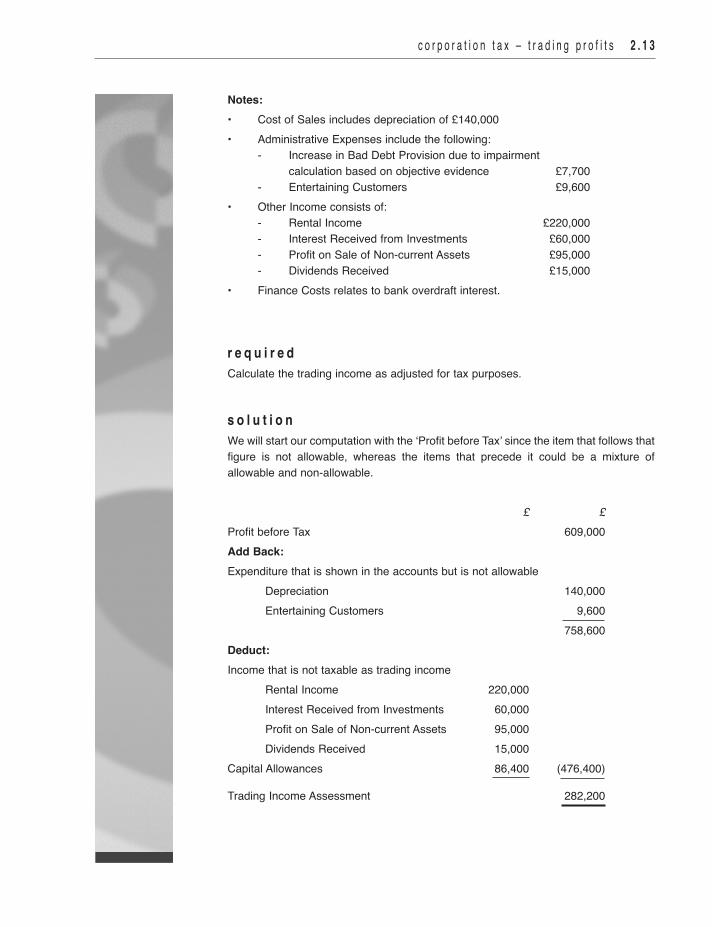

Notes:• Cost of Sales includes depreciation of £140,000• Administrative Expenses include the following:

- Increase in Bad Debt Provision due to impairmentcalculation based on objective evidence £7,700

- Entertaining Customers £9,600• Other Income consists of:

- Rental Income £220,000- Interest Received from Investments £60,000- Profit on Sale of Non-current Assets £95,000- Dividends Received £15,000

• Finance Costs relates to bank overdraft interest.

r e q u i r e dCalculate the trading income as adjusted for tax purposes.

s o l u t i o nWe will start our computation with the ‘Profit before Tax’ since the item that follows thatfigure is not allowable, whereas the items that precede it could be a mixture ofallowable and non-allowable.

£ £Profit before Tax 609,000Add Back:Expenditure that is shown in the accounts but is not allowable

Depreciation 140,000Entertaining Customers 9,600

758,600Deduct:Income that is not taxable as trading income

Rental Income 220,000Interest Received from Investments 60,000Profit on Sale of Non-current Assets 95,000Dividends Received 15,000

Capital Allowances 86,400 (476,400)

Trading Income Assessment 282,200

c o r p o r a t i o n t a x – t r a d i n g p r o f i t s 2 . 1 3

2 . 1 4 b u s i n e s s t a x ( F i n a n c e A c t 2 0 1 4 ) t u t o r i a l

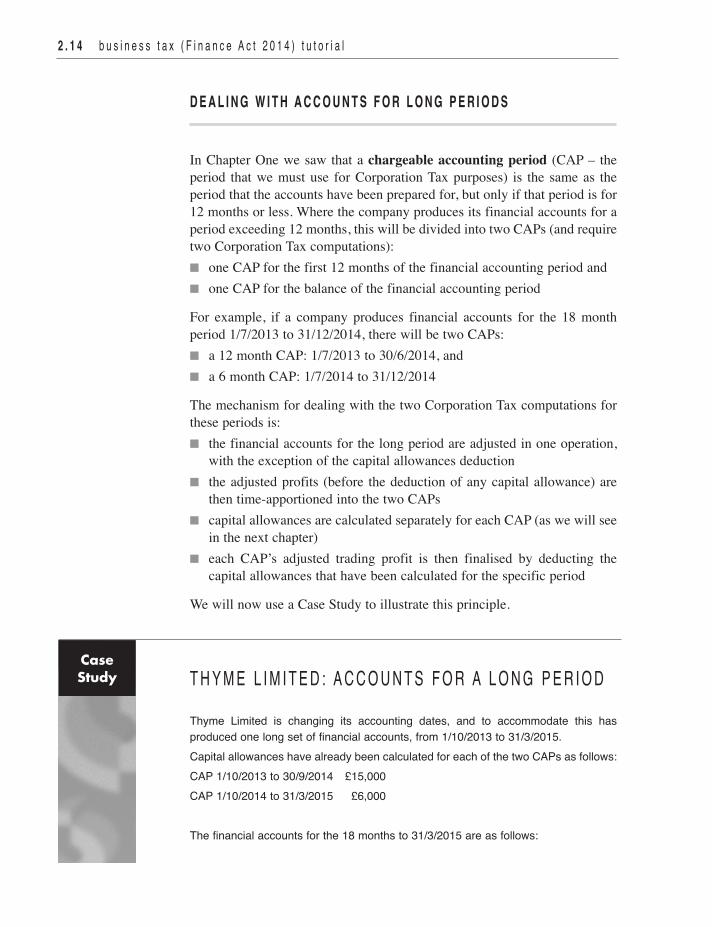

D E A L I N G W I T H A C C O U N T S F O R L O N G P E R I O D S

In Chapter One we saw that a chargeable accounting period (CAP – theperiod that we must use for Corporation Tax purposes) is the same as theperiod that the accounts have been prepared for, but only if that period is for12 months or less. Where the company produces its financial accounts for aperiod exceeding 12 months, this will be divided into two CAPs (and requiretwo Corporation Tax computations):n one CAP for the first 12 months of the financial accounting period andn one CAP for the balance of the financial accounting period

For example, if a company produces financial accounts for the 18 monthperiod 1/7/2013 to 31/12/2014, there will be two CAPs:n a 12 month CAP: 1/7/2013 to 30/6/2014, andn a 6 month CAP: 1/7/2014 to 31/12/2014

The mechanism for dealing with the two Corporation Tax computations forthese periods is:n the financial accounts for the long period are adjusted in one operation,with the exception of the capital allowances deduction

n the adjusted profits (before the deduction of any capital allowance) arethen time-apportioned into the two CAPs

n capital allowances are calculated separately for each CAP (as we will seein the next chapter)

n each CAP’s adjusted trading profit is then finalised by deducting thecapital allowances that have been calculated for the specific period

We will now use a Case Study to illustrate this principle.

T H Y M E L I M I T E D : A C C O U N T S F O R A L O N G P E R I O DThyme Limited is changing its accounting dates, and to accommodate this hasproduced one long set of financial accounts, from 1/10/2013 to 31/3/2015. Capital allowances have already been calculated for each of the two CAPs as follows:CAP 1/10/2013 to 30/9/2014 £15,000CAP 1/10/2014 to 31/3/2015 £6,000

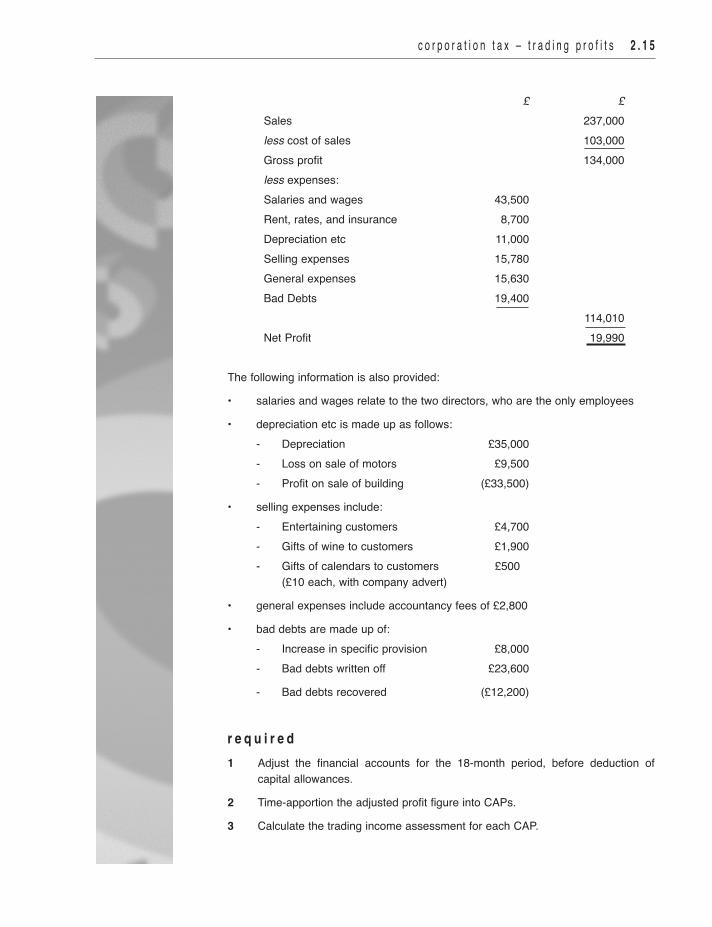

The financial accounts for the 18 months to 31/3/2015 are as follows:

CaseStudy

c o r p o r a t i o n t a x – t r a d i n g p r o f i t s 2 . 1 5

£ £Sales 237,000less cost of sales 103,000Gross profit 134,000less expenses:Salaries and wages 43,500Rent, rates, and insurance 8,700Depreciation etc 11,000Selling expenses 15,780General expenses 15,630Bad Debts 19,400

114,010Net Profit 19,990

The following information is also provided:

• salaries and wages relate to the two directors, who are the only employees

• depreciation etc is made up as follows:- Depreciation £35,000- Loss on sale of motors £9,500- Profit on sale of building (£33,500)

• selling expenses include:- Entertaining customers £4,700- Gifts of wine to customers £1,900- Gifts of calendars to customers £500

(£10 each, with company advert)

• general expenses include accountancy fees of £2,800

• bad debts are made up of:- Increase in specific provision £8,000- Bad debts written off £23,600

- Bad debts recovered (£12,200)

r e q u i r e d1 Adjust the financial accounts for the 18-month period, before deduction of

capital allowances.

2 Time-apportion the adjusted profit figure into CAPs.

3 Calculate the trading income assessment for each CAP.

2 . 1 6 b u s i n e s s t a x ( F i n a n c e A c t 2 0 1 4 ) t u t o r i a l

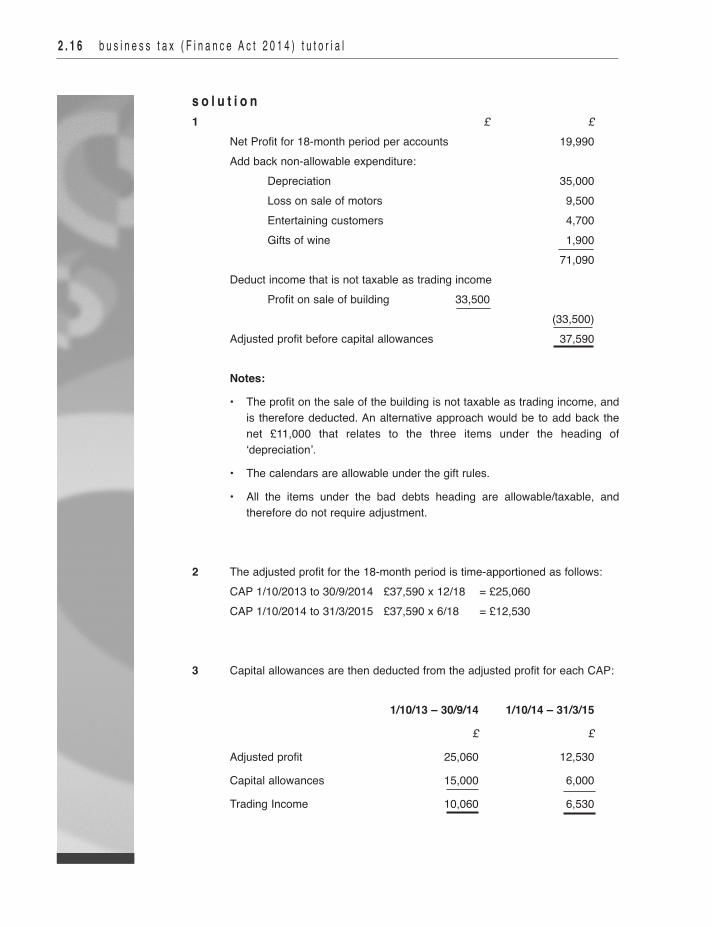

s o l u t i o n1 £ £

Net Profit for 18-month period per accounts 19,990Add back non-allowable expenditure:

Depreciation 35,000Loss on sale of motors 9,500Entertaining customers 4,700Gifts of wine 1,900

71,090Deduct income that is not taxable as trading income

Profit on sale of building 33,500(33,500)

Adjusted profit before capital allowances 37,590

Notes:

• The profit on the sale of the building is not taxable as trading income, andis therefore deducted. An alternative approach would be to add back thenet £11,000 that relates to the three items under the heading of‘depreciation’.

• The calendars are allowable under the gift rules.

• All the items under the bad debts heading are allowable/taxable, andtherefore do not require adjustment.

2 The adjusted profit for the 18-month period is time-apportioned as follows:CAP 1/10/2013 to 30/9/2014 £37,590 x 12/18 = £25,060CAP 1/10/2014 to 31/3/2015 £37,590 x 6/18 = £12,530

3 Capital allowances are then deducted from the adjusted profit for each CAP:

1/10/13 – 30/9/14 1/10/14 – 31/3/15

£ £

Adjusted profit 25,060 12,530

Capital allowances 15,000 6,000

Trading Income 10,060 6,530

c o r p o r a t i o n t a x – t r a d i n g p r o f i t s 2 . 1 7

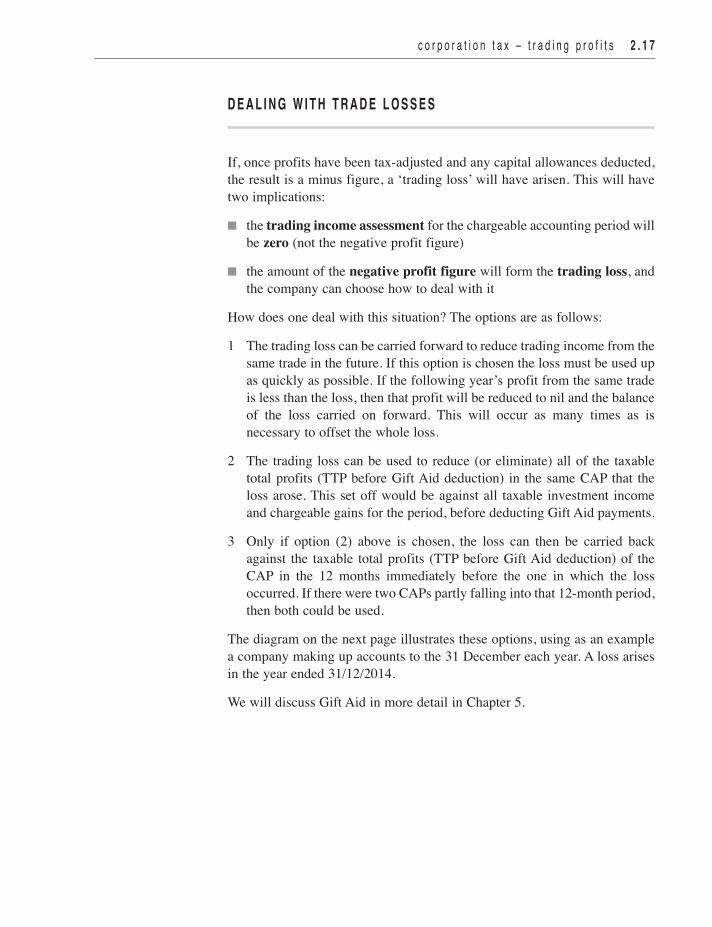

D E A L I N G W I T H T R A D E L O S S E S

If, once profits have been tax-adjusted and any capital allowances deducted,the result is a minus figure, a ‘trading loss’ will have arisen. This will havetwo implications:

n the trading income assessment for the chargeable accounting period willbe zero (not the negative profit figure)

n the amount of the negative profit figure will form the trading loss, andthe company can choose how to deal with it

How does one deal with this situation? The options are as follows:

1 The trading loss can be carried forward to reduce trading income from thesame trade in the future. If this option is chosen the loss must be used upas quickly as possible. If the following year’s profit from the same tradeis less than the loss, then that profit will be reduced to nil and the balanceof the loss carried on forward. This will occur as many times as isnecessary to offset the whole loss.

2 The trading loss can be used to reduce (or eliminate) all of the taxabletotal profits (TTP before Gift Aid deduction) in the same CAP that theloss arose. This set off would be against all taxable investment incomeand chargeable gains for the period, before deducting Gift Aid payments.

3 Only if option (2) above is chosen, the loss can then be carried backagainst the taxable total profits (TTP before Gift Aid deduction) of theCAP in the 12 months immediately before the one in which the lossoccurred. If there were two CAPs partly falling into that 12-month period,then both could be used.

The diagram on the next page illustrates these options, using as an examplea company making up accounts to the 31 December each year. A loss arisesin the year ended 31/12/2014.

We will discuss Gift Aid in more detail in Chapter 5.

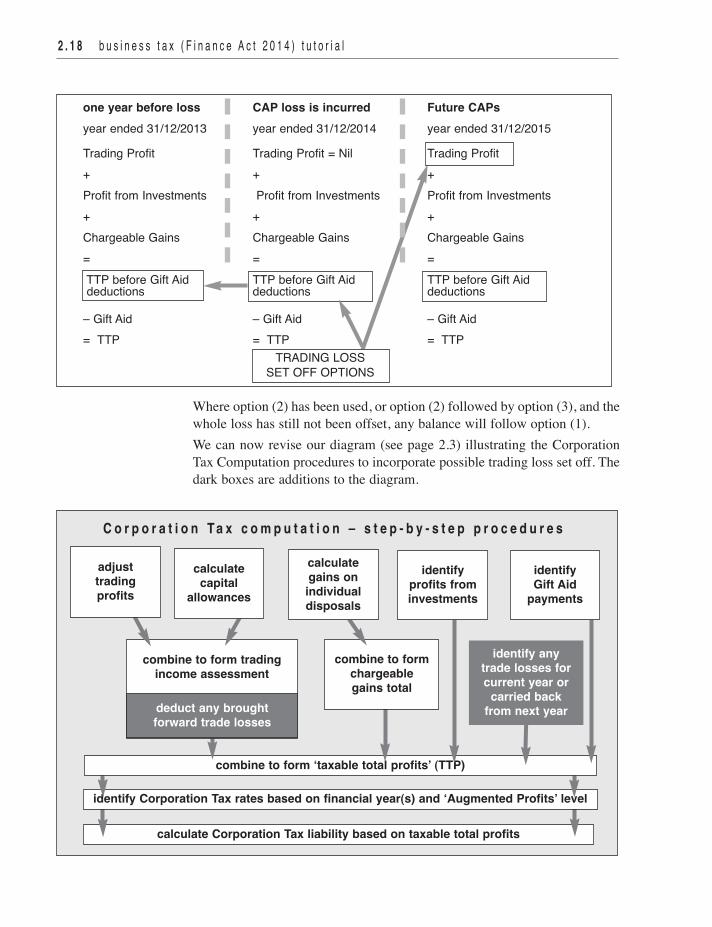

2 . 1 8 b u s i n e s s t a x ( F i n a n c e A c t 2 0 1 4 ) t u t o r i a l

calculate Corporation Tax liability based on taxable total profits

C o r p o r a t i o n T a x c o m p u t a t i o n – s t e p - b y - s t e p p r o c e d u r e s

identify Corporation Tax rates based on financial year(s) and ‘Augmented Profits’ level

combine to form ‘taxable total profits’ (TTP)

combine to formchargeablegains total

combine to form tradingincome assessment

deduct any broughtforward trade losses

identify anytrade losses forcurrent year or

carried backfrom next yeardeduct any brought

forward trade losses

Where option (2) has been used, or option (2) followed by option (3), and thewhole loss has still not been offset, any balance will follow option (1).We can now revise our diagram (see page 2.3) illustrating the CorporationTax Computation procedures to incorporate possible trading loss set off. Thedark boxes are additions to the diagram.

TRADING LOSSSET OFF OPTIONS

identifyprofits frominvestments

identify Gift Aid

payments

calculategains onindividualdisposals

adjusttradingprofits

calculatecapital

allowances

one year before loss CAP loss is incurred Future CAPsyear ended 31/12/2013 year ended 31/12/2014 year ended 31/12/2015

Trading Profit Trading Profit = Nil Trading Profit+ + +Profit from Investments Profit from Investments Profit from Investments+ + +Chargeable Gains Chargeable Gains Chargeable Gains= = =TTP before Gift Aid TTP before Gift Aid TTP before Gift Aiddeductions deductions deductions

– Gift Aid – Gift Aid – Gift Aid= TTP = TTP = TTP

We will now use a Case Study to illustrate these options. We will also returnto this topic in later chapters when we have studied the build-up of thetaxable total profits (TTP) in more detail.

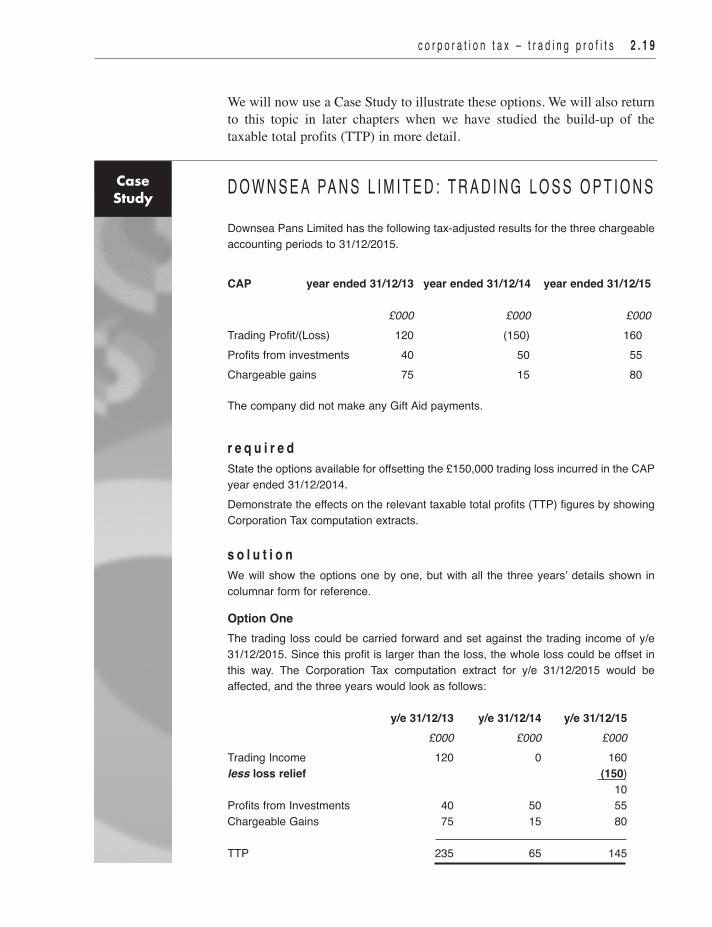

D O W N S E A PA N S L I M I T E D : T R A D I N G L O S S O P T I O N SDownsea Pans Limited has the following tax-adjusted results for the three chargeableaccounting periods to 31/12/2015.

CAP year ended 31/12/13 year ended 31/12/14 year ended 31/12/15

£000 £000 £000Trading Profit/(Loss) 120 (150) 160Profits from investments 40 50 55Chargeable gains 75 15 80

The company did not make any Gift Aid payments.

r e q u i r e dState the options available for offsetting the £150,000 trading loss incurred in the CAPyear ended 31/12/2014. Demonstrate the effects on the relevant taxable total profits (TTP) figures by showingCorporation Tax computation extracts.

s o l u t i o nWe will show the options one by one, but with all the three years’ details shown incolumnar form for reference.

Option OneThe trading loss could be carried forward and set against the trading income of y/e31/12/2015. Since this profit is larger than the loss, the whole loss could be offset inthis way. The Corporation Tax computation extract for y/e 31/12/2015 would beaffected, and the three years would look as follows:

y/e 31/12/13 y/e 31/12/14 y/e 31/12/15£000 £000 £000

Trading Income 120 0 160less loss relief (150)

10Profits from Investments 40 50 55Chargeable Gains 75 15 80

TTP 235 65 145

c o r p o r a t i o n t a x – t r a d i n g p r o f i t s 2 . 1 9

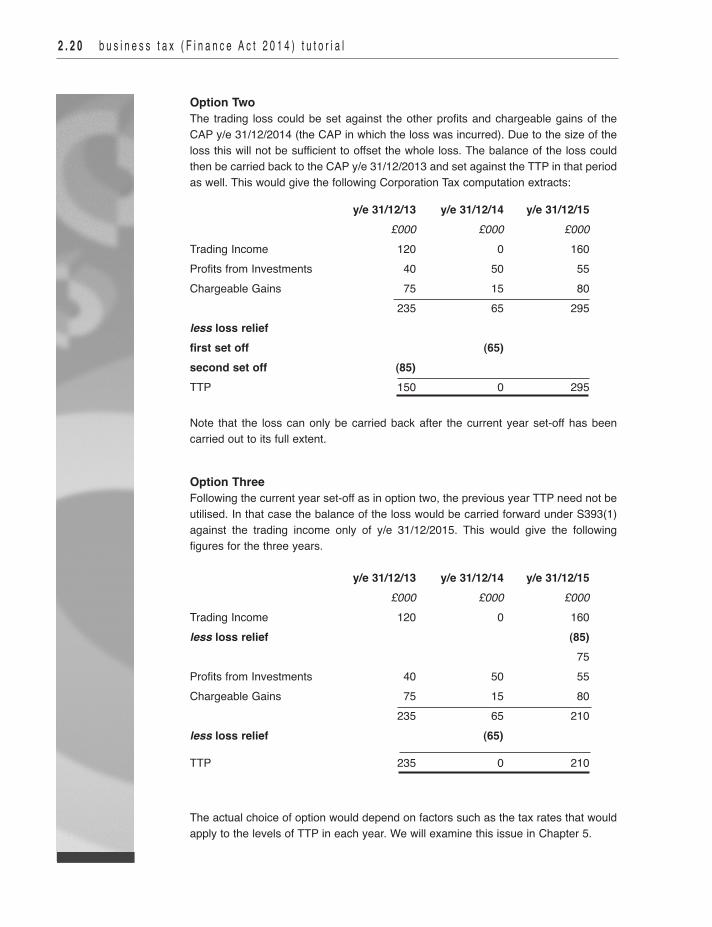

CaseStudy

Option TwoThe trading loss could be set against the other profits and chargeable gains of theCAP y/e 31/12/2014 (the CAP in which the loss was incurred). Due to the size of theloss this will not be sufficient to offset the whole loss. The balance of the loss couldthen be carried back to the CAP y/e 31/12/2013 and set against the TTP in that periodas well. This would give the following Corporation Tax computation extracts:

y/e 31/12/13 y/e 31/12/14 y/e 31/12/15£000 £000 £000

Trading Income 120 0 160Profits from Investments 40 50 55Chargeable Gains 75 15 80

235 65 295less loss relief first set off (65)second set off (85) TTP 150 0 295

Note that the loss can only be carried back after the current year set-off has beencarried out to its full extent.

Option ThreeFollowing the current year set-off as in option two, the previous year TTP need not beutilised. In that case the balance of the loss would be carried forward under S393(1)against the trading income only of y/e 31/12/2015. This would give the followingfigures for the three years.

y/e 31/12/13 y/e 31/12/14 y/e 31/12/15£000 £000 £000

Trading Income 120 0 160less loss relief (85)

75Profits from Investments 40 50 55Chargeable Gains 75 15 80

235 65 210less loss relief (65)

TTP 235 0 210

The actual choice of option would depend on factors such as the tax rates that wouldapply to the levels of TTP in each year. We will examine this issue in Chapter 5.

2 . 2 0 b u s i n e s s t a x ( F i n a n c e A c t 2 0 1 4 ) t u t o r i a l

n The ‘taxable total profits’ (TTP) include trading income, profits frominvestments, and chargeable gains. To arrive at the trading income, theprofits based on the financial accounts must be adjusted, and capitalallowances calculated and deducted from the adjusted profit figure.

n To adjust the profit based on the financial accounts, any income shown inthe accounts that is not taxable as trading income is deducted, and anyexpenditure that is not allowable is added. The capital allowances that willhave been calculated separately are then deducted to arrive at theassessable trading income.

n To be allowable, expenditure must be revenue (not capital), and wholly andexclusively for the purpose of the trade. There are also detailed rules aboutwhether certain items of expenditure are allowable.

n Where the financial accounts are prepared for a period exceeding twelvemonths, the period will form two chargeable accounting periods. One CAPwill be for the first twelve months, and the other for the balance of the financialaccounting period. To deal with this situation, the financial accounts areadjusted as a whole, apart from the capital allowances. The adjusted profit isthen time-apportioned into the two CAPs, and separate capital allowancefigures deducted from each to form two trading income assessments.

n Where the adjusted trading profits (after capital allowances) result in anegative figure, the trading income assessment is zero, and a trading lossis formed that can be relieved in several ways. It may be carried forwardand set off against the first available profits of the same trade. It mayalternatively be set against the taxable total profits (TTP before any Gift Aiddeductions) of the CAP in which the loss was incurred. Where this happensand not all the loss is used up, the balance can be carried back against thetaxable total profits (TTP before any Gift Aid deductions) arising in thepreceding twelve months.

c o r p o r a t i o n t a x – t r a d i n g p r o f i t s 2 . 2 1

ChapterSummary

2 . 2 2 b u s i n e s s t a x ( F i n a n c e A c t 2 0 1 4 ) t u t o r i a l

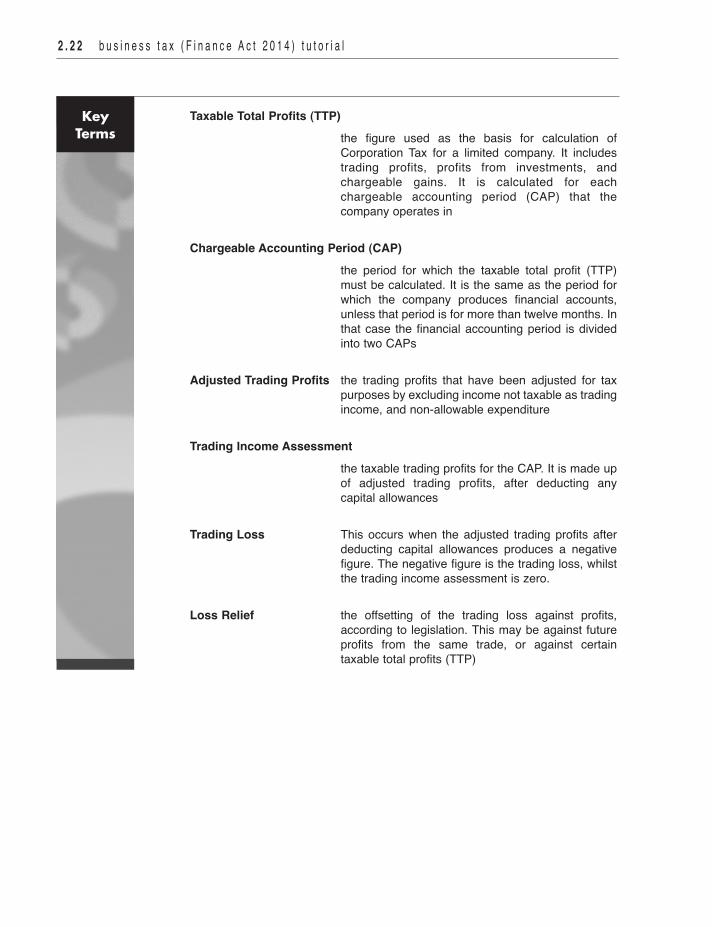

Taxable Total Profits (TTP)the figure used as the basis for calculation ofCorporation Tax for a limited company. It includestrading profits, profits from investments, andchargeable gains. It is calculated for eachchargeable accounting period (CAP) that thecompany operates in

Chargeable Accounting Period (CAP)the period for which the taxable total profit (TTP)must be calculated. It is the same as the period forwhich the company produces financial accounts,unless that period is for more than twelve months. Inthat case the financial accounting period is dividedinto two CAPs

Adjusted Trading Profits the trading profits that have been adjusted for taxpurposes by excluding income not taxable as tradingincome, and non-allowable expenditure

Trading Income Assessmentthe taxable trading profits for the CAP. It is made upof adjusted trading profits, after deducting anycapital allowances

Trading Loss This occurs when the adjusted trading profits afterdeducting capital allowances produces a negativefigure. The negative figure is the trading loss, whilstthe trading income assessment is zero.

Loss Relief the offsetting of the trading loss against profits,according to legislation. This may be against futureprofits from the same trade, or against certaintaxable total profits (TTP)

KeyTerms

c o r p o r a t i o n t a x – t r a d i n g p r o f i t s 2 . 2 3

2.1 The numbered items listed below appear in an income statement (before the net profit figure). If you are adjusting the trading profit for tax purposes, state whether each item should be: • added to the net profit• deducted from the net profit• ignored for adjustment purposes

1 accountancy fees payable

2 amortisation of lease

3 non–trade interest received

4 dividends received

5 employees’ travel expenses payable

6 gain on sale of non-current asset

7 decrease in specific provision for bad debts

8 gifts of cigars (with company adverts) to customers, costing £40 per recipient.

9 increase in general bad debt provision

10 donation to political party

11 employers’ National Insurance contributions

12 charitable donation under the Gift Aid scheme

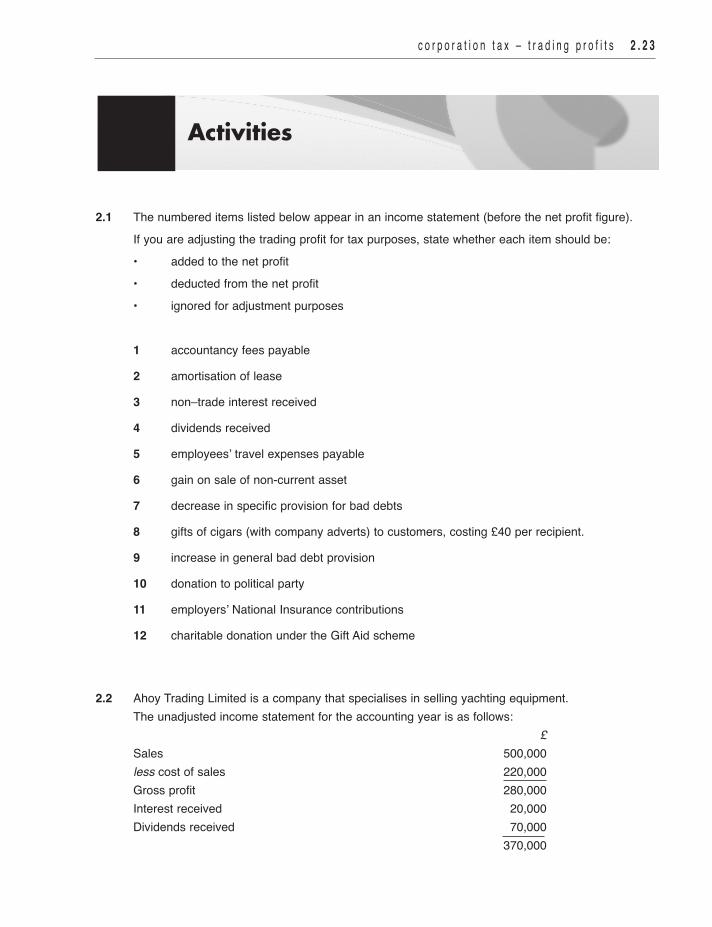

2.2 Ahoy Trading Limited is a company that specialises in selling yachting equipment. The unadjusted income statement for the accounting year is as follows:

£Sales 500,000less cost of sales 220,000Gross profit 280,000Interest received 20,000Dividends received 70,000

370,000

Activities

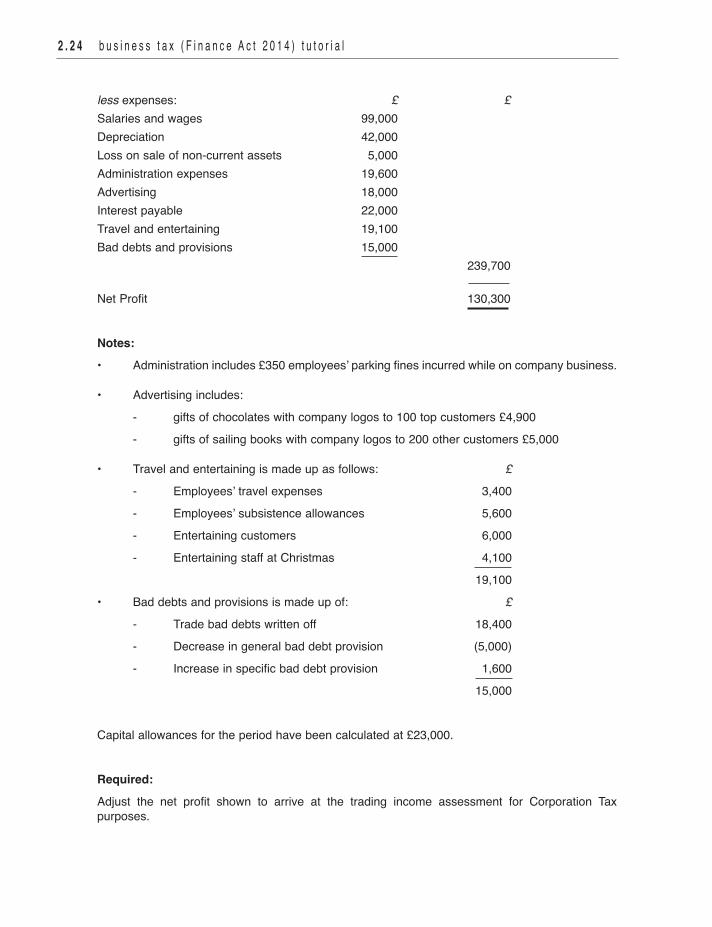

less expenses: £ £Salaries and wages 99,000Depreciation 42,000Loss on sale of non-current assets 5,000Administration expenses 19,600Advertising 18,000Interest payable 22,000Travel and entertaining 19,100Bad debts and provisions 15,000

239,700

Net Profit 130,300

Notes:• Administration includes £350 employees’ parking fines incurred while on company business.

• Advertising includes:- gifts of chocolates with company logos to 100 top customers £4,900- gifts of sailing books with company logos to 200 other customers £5,000

• Travel and entertaining is made up as follows: £- Employees’ travel expenses 3,400- Employees’ subsistence allowances 5,600- Entertaining customers 6,000- Entertaining staff at Christmas 4,100

19,100• Bad debts and provisions is made up of: £

- Trade bad debts written off 18,400- Decrease in general bad debt provision (5,000)- Increase in specific bad debt provision 1,600

15,000

Capital allowances for the period have been calculated at £23,000.

Required:Adjust the net profit shown to arrive at the trading income assessment for Corporation Taxpurposes.

2 . 2 4 b u s i n e s s t a x ( F i n a n c e A c t 2 0 1 4 ) t u t o r i a l

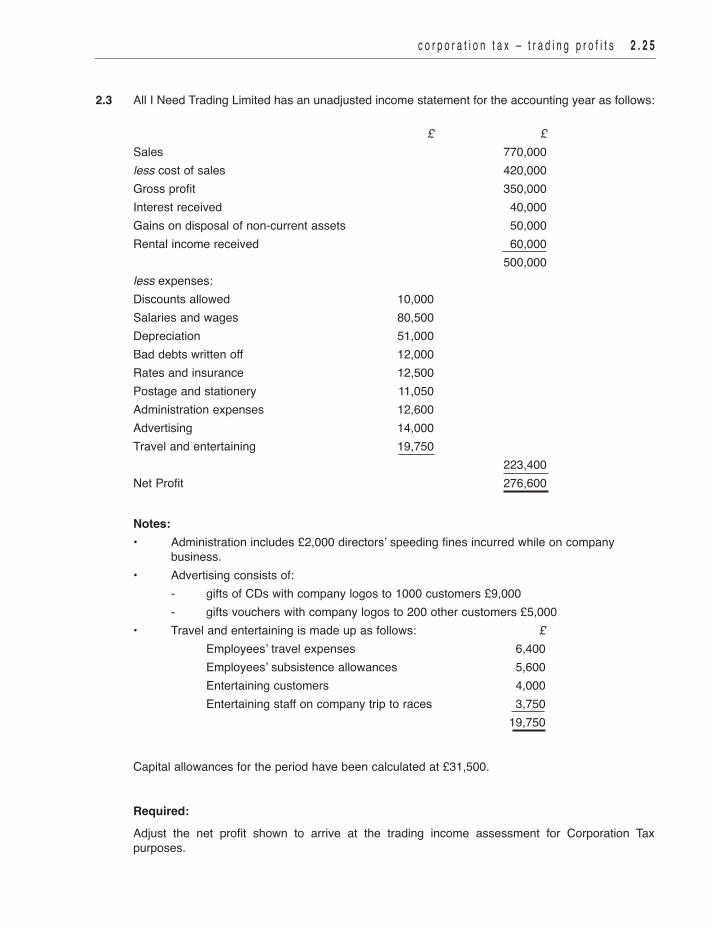

2.3 All I Need Trading Limited has an unadjusted income statement for the accounting year as follows:

£ £Sales 770,000less cost of sales 420,000Gross profit 350,000Interest received 40,000Gains on disposal of non-current assets 50,000Rental income received 60,000

500,000less expenses:Discounts allowed 10,000Salaries and wages 80,500Depreciation 51,000Bad debts written off 12,000Rates and insurance 12,500Postage and stationery 11,050Administration expenses 12,600Advertising 14,000Travel and entertaining 19,750

223,400Net Profit 276,600

Notes:• Administration includes £2,000 directors’ speeding fines incurred while on company

business.• Advertising consists of:

- gifts of CDs with company logos to 1000 customers £9,000- gifts vouchers with company logos to 200 other customers £5,000

• Travel and entertaining is made up as follows: £Employees’ travel expenses 6,400Employees’ subsistence allowances 5,600Entertaining customers 4,000Entertaining staff on company trip to races 3,750

19,750

Capital allowances for the period have been calculated at £31,500.

Required:Adjust the net profit shown to arrive at the trading income assessment for Corporation Taxpurposes.

c o r p o r a t i o n t a x – t r a d i n g p r o f i t s 2 . 2 5

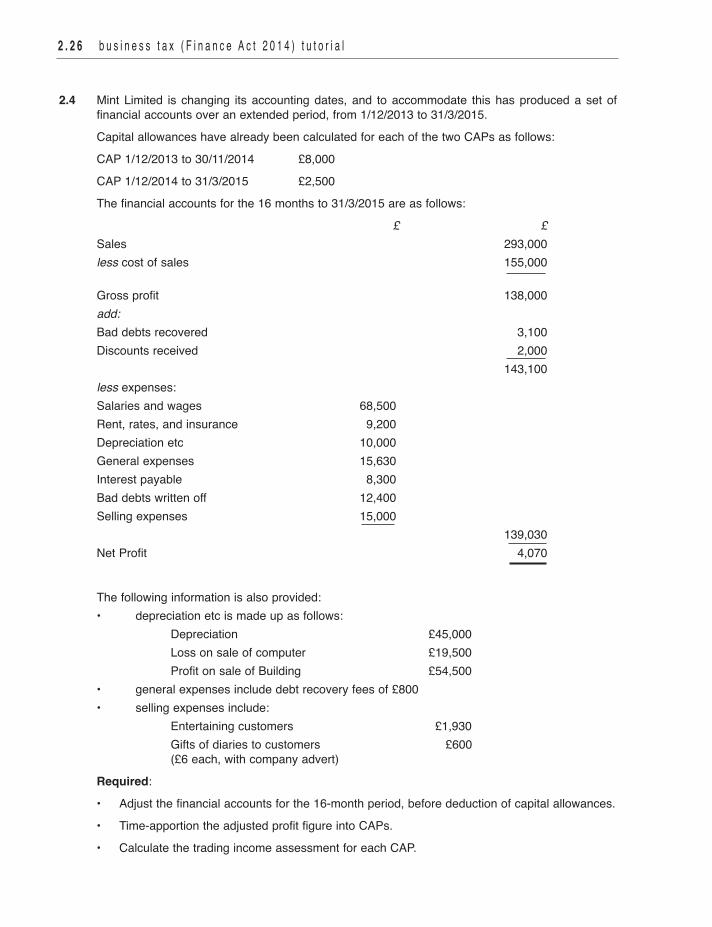

2.4 Mint Limited is changing its accounting dates, and to accommodate this has produced a set offinancial accounts over an extended period, from 1/12/2013 to 31/3/2015. Capital allowances have already been calculated for each of the two CAPs as follows:CAP 1/12/2013 to 30/11/2014 £8,000CAP 1/12/2014 to 31/3/2015 £2,500The financial accounts for the 16 months to 31/3/2015 are as follows:

£ £Sales 293,000less cost of sales 155,000

Gross profit 138,000add:Bad debts recovered 3,100Discounts received 2,000

143,100less expenses:Salaries and wages 68,500Rent, rates, and insurance 9,200Depreciation etc 10,000General expenses 15,630Interest payable 8,300Bad debts written off 12,400Selling expenses 15,000

139,030Net Profit 4,070

The following information is also provided:• depreciation etc is made up as follows:

Depreciation £45,000Loss on sale of computer £19,500Profit on sale of Building £54,500

• general expenses include debt recovery fees of £800• selling expenses include:

Entertaining customers £1,930Gifts of diaries to customers £600 (£6 each, with company advert)

Required:• Adjust the financial accounts for the 16-month period, before deduction of capital allowances.• Time-apportion the adjusted profit figure into CAPs.• Calculate the trading income assessment for each CAP.

2 . 2 6 b u s i n e s s t a x ( F i n a n c e A c t 2 0 1 4 ) t u t o r i a l

c o r p o r a t i o n t a x – t r a d i n g p r o f i t s 2 . 2 7

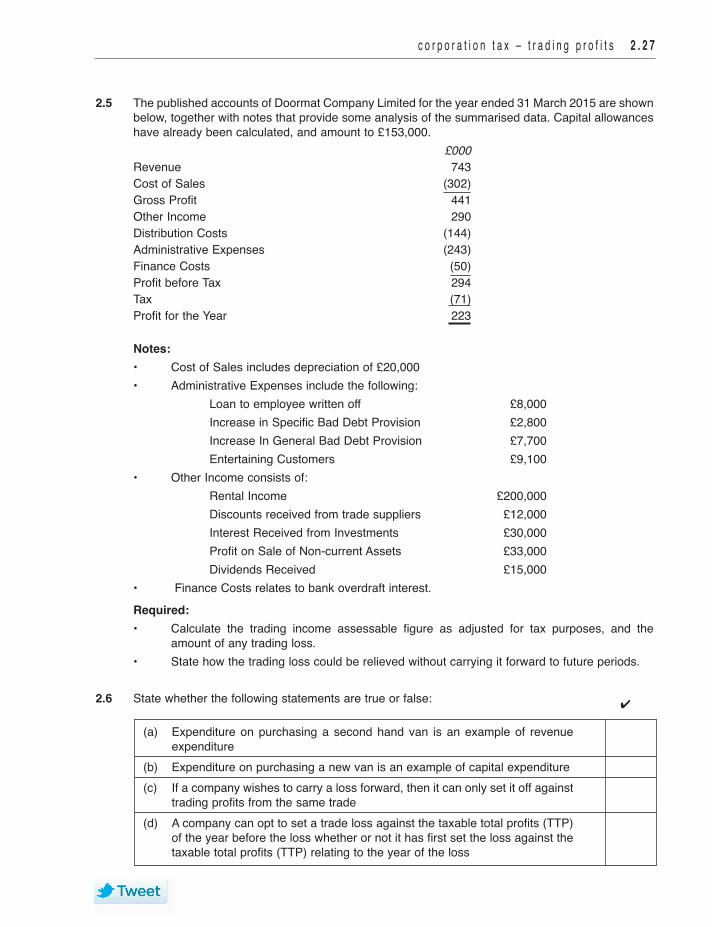

2.5 The published accounts of Doormat Company Limited for the year ended 31 March 2015 are shownbelow, together with notes that provide some analysis of the summarised data. Capital allowanceshave already been calculated, and amount to £153,000.

£000Revenue 743Cost of Sales (302)Gross Profit 441Other Income 290Distribution Costs (144)Administrative Expenses (243)Finance Costs (50)Profit before Tax 294Tax (71)Profit for the Year 223

Notes:• Cost of Sales includes depreciation of £20,000• Administrative Expenses include the following:

Loan to employee written off £8,000Increase in Specific Bad Debt Provision £2,800Increase In General Bad Debt Provision £7,700Entertaining Customers £9,100

• Other Income consists of:Rental Income £200,000Discounts received from trade suppliers £12,000Interest Received from Investments £30,000Profit on Sale of Non-current Assets £33,000Dividends Received £15,000

• Finance Costs relates to bank overdraft interest.Required:• Calculate the trading income assessable figure as adjusted for tax purposes, and the

amount of any trading loss.• State how the trading loss could be relieved without carrying it forward to future periods.

2.6 State whether the following statements are true or false:

(a) Expenditure on purchasing a second hand van is an example of revenueexpenditure

(b) Expenditure on purchasing a new van is an example of capital expenditure(c) If a company wishes to carry a loss forward, then it can only set it off against

trading profits from the same trade(d) A company can opt to set a trade loss against the taxable total profits (TTP)

of the year before the loss whether or not it has first set the loss against thetaxable total profits (TTP) relating to the year of the loss

4