Business models, strategyegy and internationalisation around the Telecom Crash What is the influence...

23

Business models, strategyegy and internationalisation around the Telecom Crash What is the influence of these strategic choices on the performance of telecom operator companies in the years 1998-2001 H.Ebbers, Nyenrode University and CEIBS Shanghai

-

date post

21-Dec-2015 -

Category

Documents

-

view

214 -

download

0

Transcript of Business models, strategyegy and internationalisation around the Telecom Crash What is the influence...

Business models, strategyegy and internationalisation around

the Telecom CrashWhat is the influence of these strategic choices on the

performance of telecom operator companies in the years 1998-2001

H.Ebbers, Nyenrode University and CEIBS Shanghai

Agenda• Introduction

• Earlier work about KPN

• Theory/ choices

• Research methods

• Results

• Conclusions

Introduction

• Work in progress

• Three students between May 2002 and February 2003

• Guidance of the Center for International Business, Nyenrode University

•Mobile telecommunication

•IP and data services

•Internet, call centre and media- services

•Fixed network

Emphasis is on the first three activities

Core Activities for KPN

Two strategically important joint ventures: KPN Orange (1998) and

BellSouth-KPN (1999)………

• Acquisition of E- plus (Germany) …seen as a growth market

• Acquisition of Orange-KPN Belgium

• Majority stakes in Central and Eastern Europe

KPN Mobile

• Arrangements with NTT- DoCoMo

– Technology sharing

– Minority holding: NTT- DoCoMo aquired a 15% stake in KPN

– UMTS biddings

International expansion

• Regional focus (CEE)

• Control over management

• Divestments driven by debt problems and the 2001 telecomcrash

KPN

Bell South

Orange (UK)

France Telecom

Pannon

UMC

Telkomsel

OTE/ BTC

Euroweb Corp

Telia

E-plus

Comsource

Slovak Telecom

Eirocom

Orange -KPN Belgium

Swisscom

SPT/ Cesky Telecom

Telsource

NTT Docomo

Hutchison #G

Tele Danmark

Join

t ve

ntur

e(50

%)

minority (17%)

majority

(51%)

minority (21%)

=Alliance at the endof 2002

=alliance which KPN is considering to end.

= sold non -core asset or ended alliance

KPN

Bell South

Orange (UK)

France Telecom

Pannon

UMC

Telkomsel

OTE/ BTC

Euroweb Corp

Telia

E-plus

Comsource

Slovak Telecom

Eirocom

Orange -KPN Belgium

Swisscom

SPT/ Cesky Telecom

Telsource

NTT Docomo

Hutchison #G

Tele Danmark

Join

t ve

ntur

e(50

%)

minority (17%)

majority

(51%)

minority (21%)

=Alliance at the endof 2002

=alliance which KPN is considering to end.

= sold non -core asset or ended alliance

KPN’s alliance network within mobile telecommunications

KPN

KPN-Qwest

Wipro/wipronet

DisneyBlast

KPN Belgium

InfonetServices Corporation

Lambda net

EurowebCorp

SchipholTelematics

CESECBEC

Jasz-Tel

AT &T-unisourceservices

Unisource

Telsource

Planet Internet

Telstra Satellite

Utel

=Alliance at the endof 2002

=alliance which KPN is considering to end.

= sold non-core asset or ended alliance

Nokia

Joint Venture

Fixed

IP/data/ICM

KPN

KPN-Qwest

Wipro/wipronet

DisneyBlast

KPN Belgium

InfonetServices Corporation

Lambda net

EurowebCorp

SchipholTelematics

CESECBEC

Jasz-Tel

AT &T-unisourceservices

Unisource

Telsource

Planet Internet

Telstra Satellite

Utel

=Alliance at the endof 2002

=alliance which KPN is considering to end.

= sold non-core asset or ended alliance

Nokia

Joint Venture

Fixed

IP/data/ICM

Introduction

• Companies: Telecom Operators– SBC - KPN - France Telecom– Deutsche Telekom - Telia - Sonera– Vodafone - BT - AT&T – Colt - Cable & Wireless - Infonet– Sprint - MCI Worldcom - QWest

Telecom Content & Valueequipment Carriers/ Service Added Customersindustry Operators Providers Services

Theory• Business Models

– Mintzberg– Cushway & Lodge– Viscio & Pasternack

• Internationalisation• Strategies

– Boston Consulting Group matrix– Porter’s generic strategies– Ansoff’s product/market matrix– Equity and non equity based cooperative agreements

Business Models

V o ice D ata IP

C ab le & W ire less G lob a l

C arib b ean M id d le E as t M acau

C ab le & W ire less R eg ion a l

C ab le & W ire less G rou p

Traditional Model = 0 Emerging Model = 1 Score‘managing assets’ ‘managing resources’ 1998 1999 2000 2001

Businesses built around assets

Businesses built to leverage and develop resources (people, capabilities, knowledge) 0 0 0 0

Portfolio of businesses related in product-market terms

Portfolio of strategic capabilities based on knowledge created 0 0 0 0

Financial investment assigned business unit by business unit

Resource allocation (talent and capital) on a corporate-wide bases 0 0 0 0

Performance measured around assets (utilisation rates, profitability of single business units)

Performance measured on a corporate-wide level driven by knowledge creation and sharing 0 0 0 0

Accountability focussed on business unit financials often impeding and discouraging business interaction

accountability includes growth and best practices sharing 0 0 0 0

Total 0 0 0 0

InternationalisationC&W geographical revenue

US16%

UK41%Europe

6%

Japan9%

Caribbean22%

Asia3%

Rest 3%

more than 90% of revenue local: level 1 less than 90% but more than 50% of revenue local: level 2 less than 50% of revenue local but less than 25% of revenue outside its own continent: level 3 more than 25% but less than 50% of revenue outside its own continent: level 4 more than 50% of revenue outside its own continent: level 5

Strategieshigh

Question Mark Star

Market Growth Rate

Dog Cash Cow

lowlow Relative Market high

Share

Existing product New product

Existing Penetration Product develop-Market Strategies (90%) ment strategies (30%)

New Market development DiversificationMarket Strategies (30%) Strategies (10%)

Broad

1. Cost Leadership 2. Differentiation

Strategic targetMarket

3A. Cost Focus 3B. Differentiation Focus

Narrow/NicheLow-cost Strategic Advantage Uniqueness/

Differentiation

BCG

Porter

Ansoff

Research methods• detailed company analyses

– performance– business models– internationalisation– strategies

Results: Telecom Crash

Return On Equity

-25%

0%

25%

50%

2001200019991998

ROE market

• Market performanceDebt/Equity ratios

50%

100%

150%

2001200019991998

debt equity market

Net profit margin

-25%

0%

25%

2001200019991998

net profit Market

Stock price evolution compared to previous Year

0%

50%

100%

150%

200%

2001200019991998

Market

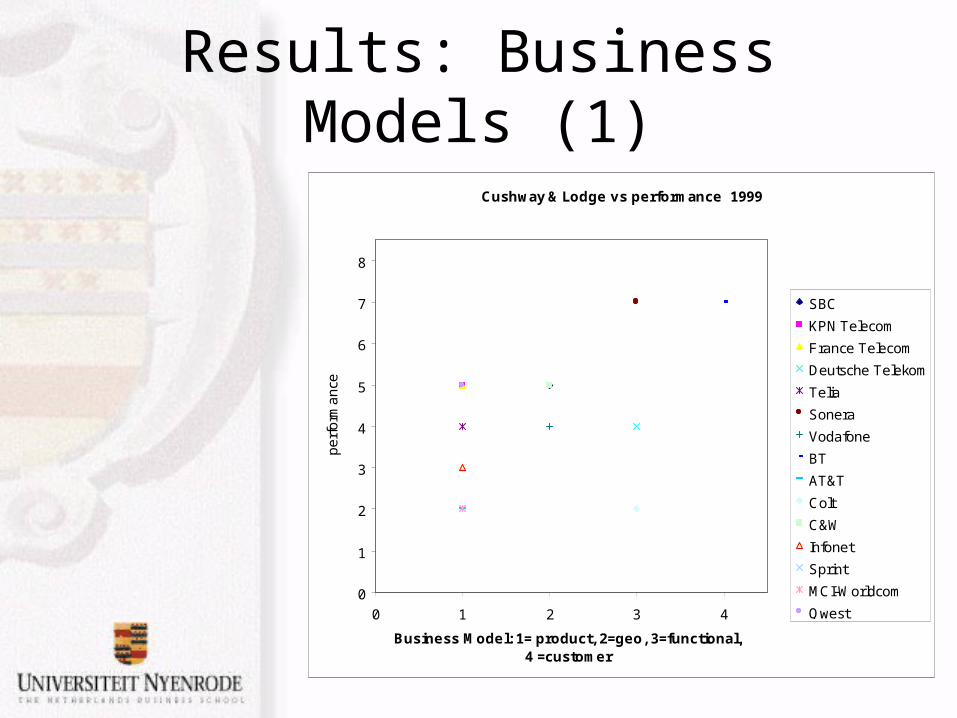

Results: Business Models (1)

Cushway & Lodge vs performance 1999

0

1

2

3

4

5

6

7

8

0 1 2 3 4

Business Model: 1= product, 2=geo, 3=functional,4 =customer

pe

rfo

rma

nce

SBC

KPN Telecom

France Telecom

Deutsche Telekom

Telia

Sonera

Vodafone

BT

AT&T

Colt

C&W

Infonet

Sprint

MCI-Worldcom

Qwest

Results: Business Models (2)

Viscio and Pasternack score vs performance 2000

0

1

2

3

4

5

6

7

8

0 1 2 3 4 5

Viscio and Pasternack score

pe

rfo

rma

nce

SBC

KPN Telecom

France Telecom

Deutsche Telekom

Telia

Sonera

Vodafone

BT

AT&T

Colt

C&W

Infonet

Sprint

MCI-Worldcom

Qwest

Results: Internationalisation

Internationalisation vs performance 1998

0

1

2

3

4

5

6

7

8

0 1 2 3 4 5

Internationalisation level

pe

rfo

rma

nce

SBC 1998

KPN Telecom 1998

France Telecom 1998

Deutsche Telekom 1998

Telia 1998

Sonera 1998

Vodafone 1998

BT 1998

AT&T 1998

Colt 1998

C&W 1998

Infonet 1998

Sprint 1998

MCI-Worldcom 1998

Results: Strategies

Porter vs performance 2000

0

1

2

3

4

5

6

7

8

0 1 2 3

Porter: 1= Cost Leader, 2=Differentiation, 3= Focus

perf

orm

ance

SBC

KPN Telecom

France Telecom

Deutsche Telekom

Telia

Sonera

Vodafone

BT

AT&T

Colt

C&W

Infonet

Sprint

MCI-Worldcom

Qwest

Results: Performance

Debt/Equity ratio vs performance 1998

0

1

2

3

4

5

6

7

8

0% 100% 200% 300% 400%

Debt/Equity ratio in %

pe

rfo

rma

nce

SBC

KPN Telecom

France Telecom

Deutsche Telekom

Telia

Sonera

Vodafone

BT

AT&T

Colt

C&W

Infonet

Sprint

MCI-Worldcom

Qwest

Conclusions (1)

• Generally a limited correlation between company performance and business models, internationalisation and strategy

• Telecom Crash has little impact on business models, internationalisation and strategy

• Low debt/equity ratio has positive impact on performance both before and after the Telecom Crash

Conclusions (2)• Business Models

• Lack of significant correlation– Customer oriented (Cushway & Lodge) – High Viscio & Pasternack Score

• Internationalisation• Little correlation in 1998, no correlation in other

years

• Strategy• Porter: correlation changes before & after crash• BCG: stars are performing well• Ansoff: move towards penetration after crash