Business Law - PIIMT "Private International Institute Of...

69

Transcript of Business Law - PIIMT "Private International Institute Of...

• Module 1: Business Entities

Step 1: Review Module lesson Step 2: In-class lecture and PPT Step 3: Answer Module questions Step 4: Complete Drafting Exercise (where assigned) Step 5: Go to next module

Introduction to Business

Organizations

• The way that a business is set up is

often as important as how it is run and

the choice of business entity often has a

huge influence on the eventual success

or failure of that business.

Sole Proprietorships

• Sole proprietorships are both the oldest,

and simplest, form of business

structure.

• In a sole proprietorship, there is a single

individual who conducts all aspects of

the business.

Legal Liability of Sole

Proprietors

• If a sole proprietor is sued because of

some business disagreement, his

personal assets are in danger.

• This is true because there is no legal

boundary between a sole proprietor’s

business assets and personal assets.

The Advantages of a Sole

Proprietorship

• One of the most obvious advantages to

a sole proprietorship is the freedom

given to the owner to make business

decisions.

Tax Consequences of Sole

Proprietorship

• One of the major advantages of a sole

proprietorship concerns income taxes.

• When a sole proprietor sustains a major

income loss during the year, he can

pass this loss through on his personal

income tax return.

The Disadvantages of a Sole

Proprietorship

• Because the business is so closely

associated with a single person, the

death or incapacity of that person

causes the business to fail. There is

usually no way for the business to

continue without the owner.

• Sole proprietors also frequently suffer

from undercapitalization.

• With only their personal credit and

financial resources to rely on, many sole

proprietors find it difficult to expand their

businesses or to pay unexpected bills.

General Partnerships

• A partnership consists of two or more

people working together in a joint

business venture.

Forming a General

Partnership

• The partners simply agree to be bound

to one another in a business and to

pledge their financial assets for the

business.

• Although many partners write out a

General Partnership Agreement, in

most situations it is not required.

Advantages of General

Partnerships

• The advantages of a partnership are

obvious: with two or more people, the

business can expand and serve more

customers.

• Partners can also contribute more

financial resources than a single

individual.

Disadvantages of General

Partnerships

• A general partner’s personal assets

could be seized to pay a judgment,

sometimes putting the general

partnership in a precarious situation.

Limited Partnerships

• In a limited partnership, there are two

classifications of partners. There are

general partners and limited partners

• General partners are responsible for the

day-to-day management of the business

in the same way that general partners

are in a regular partnership

arrangement.

• Limited partners, on the other hand,

have no right to control day-to-day

operations, but they also enjoy a

protection that the general partners do

not.

Limited Liability

• Limited partners are protected by

limited liability.

• This means that the extent of their

financial loss in the business is limited

to the extent of their financial

contribution.

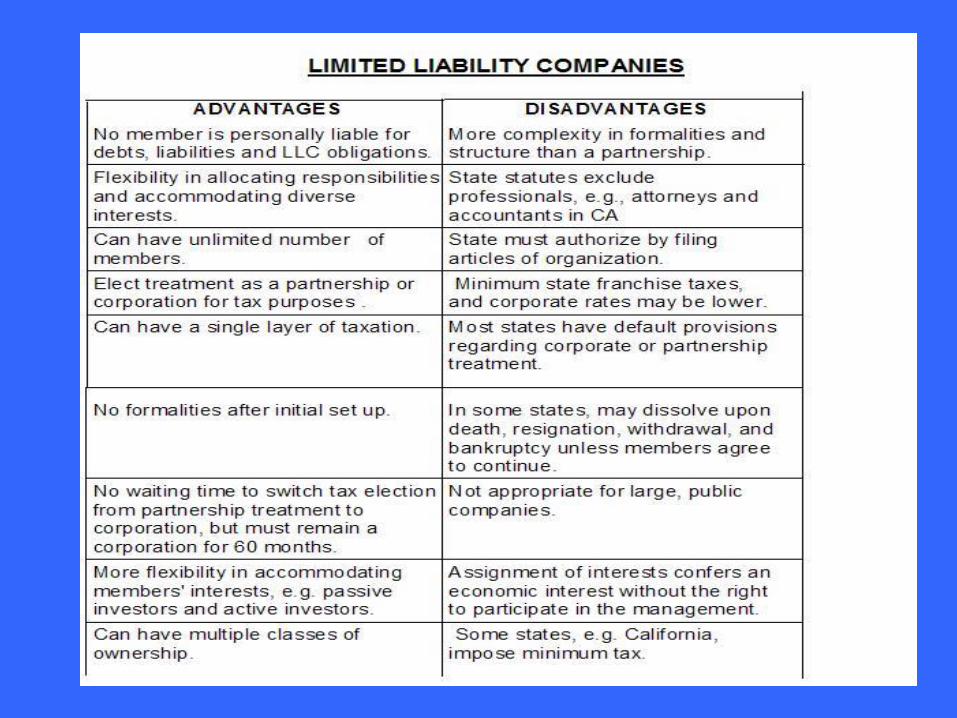

Limited Liability Companies

• A limited liability company is a cross

between partnership and a corporation

owned by members who may manage

the company directly or delegate to

officers or managers who are similar to

a corporation’s directors.

Forming a Limited Liability

Company

• In order to form a limited liability

company, a company must file several

documents with the state.

• One of the most important is the Articles

of Organization.

Articles of Organization

• This document contains the basic

information about the company,

including the company name, registered

agent and the names of the persons

forming the company.

Naming a Limited Liability

Company

• The name of a limited liability company

must contain the phrase "Limited

Liability Company" or some other easily

recognizable abbreviation, such as

“LLC.”

Advantages of Limited Liability

Companies

• LLCs can take advantage of the

protection of limited liability, as well as

enjoying some of the flexibility of a

partnership and the financial

advantages of spreading investment

over a larger pool of individuals.

• LLCs also allow individual owners to

pass through losses on their personal

income tax returns.

Organization of a Limited

Liability Company

• Individuals who own shares in limited

liability companies are referred to as

“members,” not partners or

shareholders.

• The day-to-day management of a

limited liability company is handled by

"managers.”

Corporations

• An organization that is formed under

state corporate law exists, for legal

purposes, as a separate being or an

"artificial person." The stockholders

have no liability for corporate debts

beyond the value of their stock.

Creating a Corporation

• A corporation is considered be an

artificial person

• Once created, a corporation continues

to exist separate and distinct from the

people that compose it.

Types of Corporations

• There is a wide range of corporation

types, ranging from small, privately held

corporations to huge, multinational

corporations with offices scattered

across the globe.

Corporate Shareholders

• The persons who own the corporation

are called shareholders.

• Shareholders are also entitled to an

annual payment, referred to as a

dividend, based on corporate profits.

Corporate Officers and

Directors

• Corporations have officers who manage

corporate affairs. These officers are

responsible for negotiating with

vendors, hiring and firing employees

and all of the other tasks that we would

associate with any business manager.

Corporate Directors

• Directors decide on long-term goals and

strategies for the corporation which they

then put into effect through the

corporate officers.

Disadvantages of

Corporations

• Shareholders do not enjoy the "pass

through" provisions for income tax

purposes that are seen in sole

proprietorships, general partnerships,

and other business structures that we

discussed in this chapter.

• A corporation pays its own income

taxes.

Advantages of Corporations

• As an artificial person, a corporation

may own property, negotiate contracts,

and, in many ways, enjoy a degree of

flexibility that resembles that seen in

sole proprietorships or partnerships.

Corporate Existence

• Corporations do not die.

• Although a corporation may cease to

exist because of bankruptcy or by

merger with another corporation, it does

not cease to exist when individual

shareholders, directors or officers die.

Transfer of Ownership

• Shares in corporations are bought and

sold by millions every day on the

various stock exchanges around the

world.

• Share ownership, in the form of stock

certificates, is a source of wealth for

millions of people.

Steps in Forming a

Corporation

• All states have rules about how a

corporation is formed.

• In most situations, parties form a

corporation by filing Articles of

Incorporation with the state.

Articles of Incorporation

• The articles of incorporation set out the

basic details of the corporate entity.

Articles of Incorporation

• The name of the corporation

• The number of shares the corporation is

authorized to issue

• The classes of stock issued

• The name and address of the

Registered Agent

• The names and addresses of the

principal incorporators

Corporate Organizational

Meeting

• This meeting, held among the people

who create the corporation, has several

purposes.

• The parties elect officers for the

corporation and then enact by-laws for

the day-to-day management of the

corporation.

Piercing the Corporate Veil

• This doctrine holds that when a person

uses corporate property

interchangeably with his private

property, the court may disregard the

existence of the corporation and seize

the person’s personal assets.

The Role of the Legal Team in

Creating a Business

• Business people often seek out legal

advice in both creating and running their

businesses.

• Legal professionals are often involved in

every step of business activities and

assist with the drafting and filing of

Articles of Incorporation to bankruptcy

actions if the business is not able to

stay afloat.

Licenses and Permits

• Local ordinances may require business

licenses or other permits to run specific

types of businesses.

• If the business will be run out of the

client’s home, there is also the issue of

zoning permits.

Critical Factors

• Limited Liability

• Management

• Tax-free conversion

• Eligibility

• Transferability of Interest

• Dissolution

• Taxation

Module 2: Business Basics

Understanding the Deal

Financing a Business 1. Debt vs. equity- Reflects the characterization of the

contribution of an investor. Affects priority in getting return, i.e. debt-repaid before return contribution or distribute profits but limited to amount owed plus interest; or equity-return on contribution plus a pro rata share of profits.

2. Retaining control vs. maximizing return via Preferences (priority in distribution), and Preemptive- right of first refusal. Preferences give the investor priority in distribution or first in line, e.g preferred shares. Preemptions allow the investor to restrict rights of other and protect against dilution. E.g. right of first refusal.

3. Leverage- use of other people’s money to purchase or invest. Cost of borrowing must be lower than interest earned in investing.

4. Marginal (tax rate from chart) vs. Effective tax (actual rate applied)

Contribution of Capital

• Partnerships: Any or no consideration is required

• LLC: Owners can contribute $, property, services rendered or binding obligation to contribute these so future services with a contract is OK.

• Closely corporation: Capital for a corp can be $, property, past services, debt securities. In Calif. no future services or promissory notes.

•

Characterization of

Contribution • Co. has interests different from individual

owners:

-Company usu. prefers more capital and less debt no obligation to repay so don’t spend your money on debt service; easier to leverage ‘cause it is not encumbered; better financial condition for lenders.

• Individual owners:

-Based upon risk tolerance, need to get money back, tax treatment, so may want more debt than capital ‘cause greater assurance for repayment, but low upside.

Module 3: Business Basics

Tax Planning

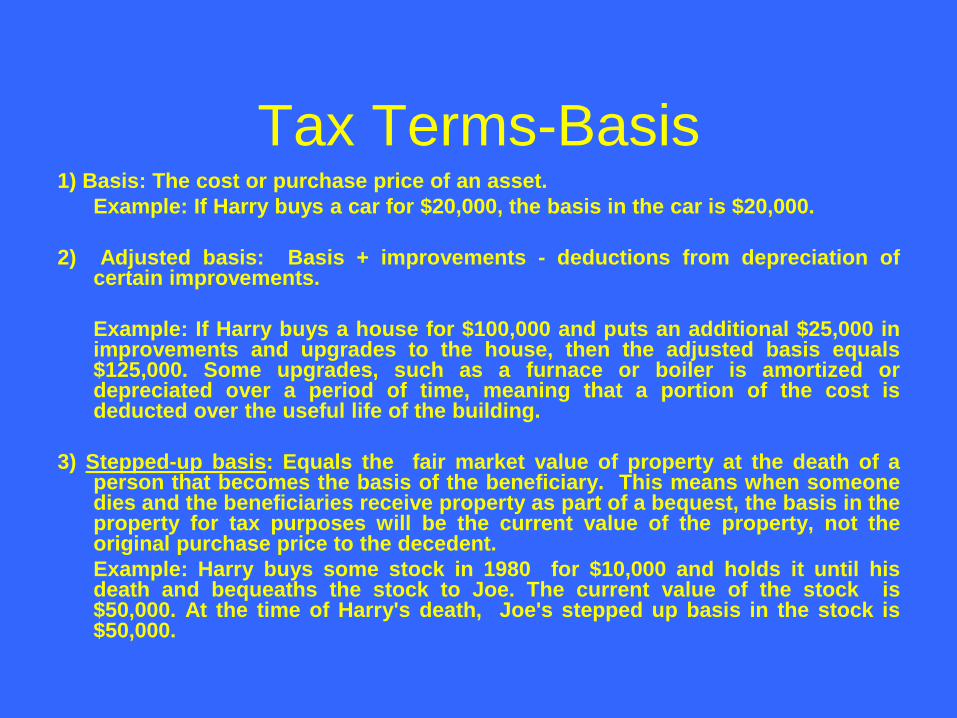

Tax Terms-Basis 1) Basis: The cost or purchase price of an asset.

Example: If Harry buys a car for $20,000, the basis in the car is $20,000.

2) Adjusted basis: Basis + improvements - deductions from depreciation of certain improvements.

Example: If Harry buys a house for $100,000 and puts an additional $25,000 in improvements and upgrades to the house, then the adjusted basis equals $125,000. Some upgrades, such as a furnace or boiler is amortized or depreciated over a period of time, meaning that a portion of the cost is deducted over the useful life of the building.

3) Stepped-up basis: Equals the fair market value of property at the death of a person that becomes the basis of the beneficiary. This means when someone dies and the beneficiaries receive property as part of a bequest, the basis in the property for tax purposes will be the current value of the property, not the original purchase price to the decedent.

Example: Harry buys some stock in 1980 for $10,000 and holds it until his death and bequeaths the stock to Joe. The current value of the stock is $50,000. At the time of Harry's death, Joe's stepped up basis in the stock is $50,000.

Profits & Losses

4) Amount realized, Gain or Profit: The cash received-adjusted basis upon sale or disposition of property; otherwise considered what is taxable as gain or profit.

Example: In our previous example, if Harry has an adjusted basis in a house for $125,000 and later sells it for $200,000, then the amount realized from the transaction is $75,000, or the difference between the adjusted basis and the sale price.

5) Loss: The amount lost if the sale price of property is less than the purchase price or adjusted basis. Losses are sometimes deductible, or can offset similar types of gains.

Example: In our previous example, if Harry has an adjusted basis in a house for $125,000 and later sells it for $75,000, then Harry will recognize a loss of $50,000 or the difference between the adjusted basis and the sale price.

Treatment of Assets/Income

6) Capital asset: An asset held for use in a business for more than 1 year, depending upon income, the maximum tax is 15%.

Example: Harry buys some equipment and holds it for 1 year. He actively uses the equipment in his business. If he sells it after 1 year, it will be considered a capital asset.

7) Passive income: Income earned from investments that are held for more than 1 year. Taxed at a maximum rate of 15%. Does not apply to income earned from an asset or activity in which the taxpayer is actively engaged in the business.

Example: Harry owns some stock worth $10,000 in a company in which he is not actively engaged. If he holds the stock for more than 1 year and then sells it for $15,000, the gain from the sale of the stock, or $15,000 will be taxed at a maximum rate of 15%.

Tax Treatment 8) Passive Loss: Income lost from investments that are held for more than 1 year. You

can offset passive income from passive losses to determine net passive income.

Example: Harry owns some stock worth $10,000 in a company in which he is not actively engaged. If he holds the stock for more than 1 year and then sells it for $7,500, the loss can be offset against other passive income he has realized.

9) Capital gains: Gain realized from profits earned from disposition of passive income. Passive income can be offset from passive losses. The current capital gains rate is a maximum rate of 15%.

Example: Harry owns some stock worth $10,000 in a company in which he is not actively engaged. If he holds the stock for more than 1 year and then sells it for $15,000, the gain from the sale of the stock, or $15,000 will be taxed at a maximum rate of 15%.

10) Short term gain: Income earned from investments held or activity engaged in for less than 1 year. Taxed as ordinary income.

Example: Harry earns $50,000 in profit from a business in which he is actively engaged. This is taxable income and will be taxed under the applicable tax rate.

Taxation Rules

• Individual taxation: Taxed on income less allowable deductions; Based upon Marginal rate or formula

• Partnership taxation: Partners taxed on pro rata share of earnings (profits); Partnership does not pay separate tax; Allocate according to Partnership agreement re percent of interest; not what actually distributed;

• Corporation: Taxed as entity and then salary and distributions taxed to individual. Since individual is a shareholder and employee, same pot of money is taxed twice, although the corporation can take a deduction as a expense for the salary.

Module 4:

Problems

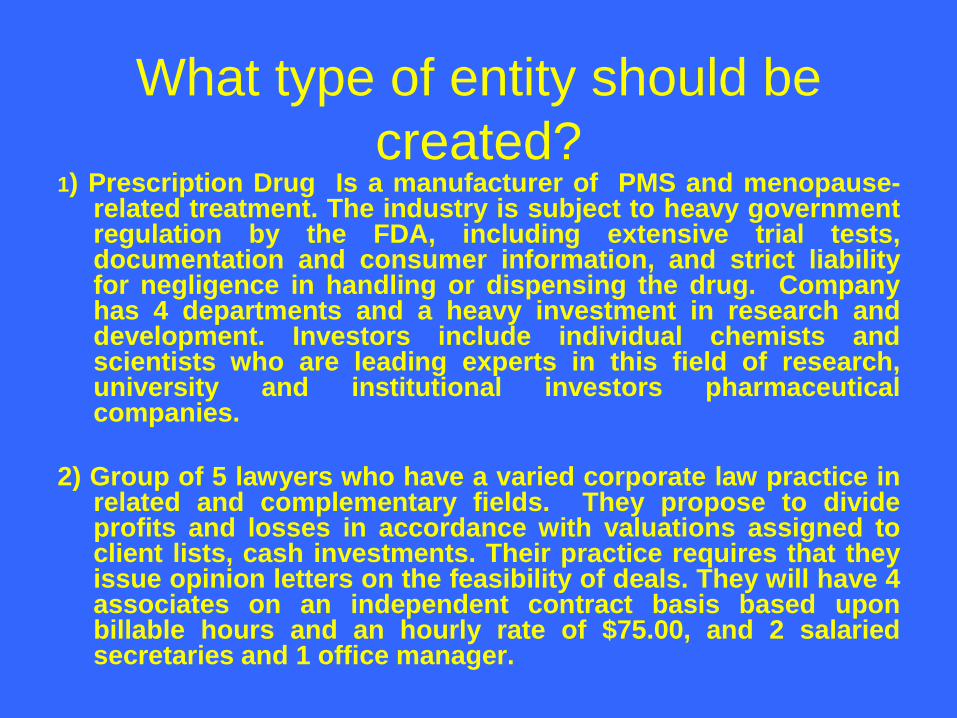

What type of entity should be

created? 1) Prescription Drug Is a manufacturer of PMS and menopause-

related treatment. The industry is subject to heavy government regulation by the FDA, including extensive trial tests, documentation and consumer information, and strict liability for negligence in handling or dispensing the drug. Company has 4 departments and a heavy investment in research and development. Investors include individual chemists and scientists who are leading experts in this field of research, university and institutional investors pharmaceutical companies.

2) Group of 5 lawyers who have a varied corporate law practice in related and complementary fields. They propose to divide profits and losses in accordance with valuations assigned to client lists, cash investments. Their practice requires that they issue opinion letters on the feasibility of deals. They will have 4 associates on an independent contract basis based upon billable hours and an hourly rate of $75.00, and 2 salaried secretaries and 1 office manager.

.

What type of entity should be

created? 3) A group of four college roommates decide to develop three

lots: one for commercial and two residential multi-family dwellings. Only two of the four roommates have any experience in real estate development, one as a marketing agent and the other working for an engineering firm. The other two have experience in banking, and retail sales and $10,000 each. They do not have enough money to develop all of the lots at the same time, so they will develop and finance them in stages. They propose to sell units to up to 90 passive investors total (30 investors per lot) who are looking to take the initial losses and profits from the business. Some investors want to invest in the commercial, but not the residential development. They are looking for an income stream. Banks will require personal guarantees of all of the roommates. Some of the investors may be foreign aliens. As part of closing, title insurance will be obtained and they intend to use bonded contractors.

What allocation of interest?

• What is the level of risk for A and B in

each of the following hypotheticals,

assuming A is contributing $100,000,

no additional contributions, veto power,

no salary; and B is contributing $10,000

plus sweat equity, salary of $5000/mo.,

no cash contribution, interest for cash,

past and future services.

Risk and Interest?

• a). ALT 1: A is a retired military who is

a widower. His contribution is his nest

egg. He relies on social security and

disability payments, owns 2 apartment

buildings. He is 60 years of age and in

fair health.

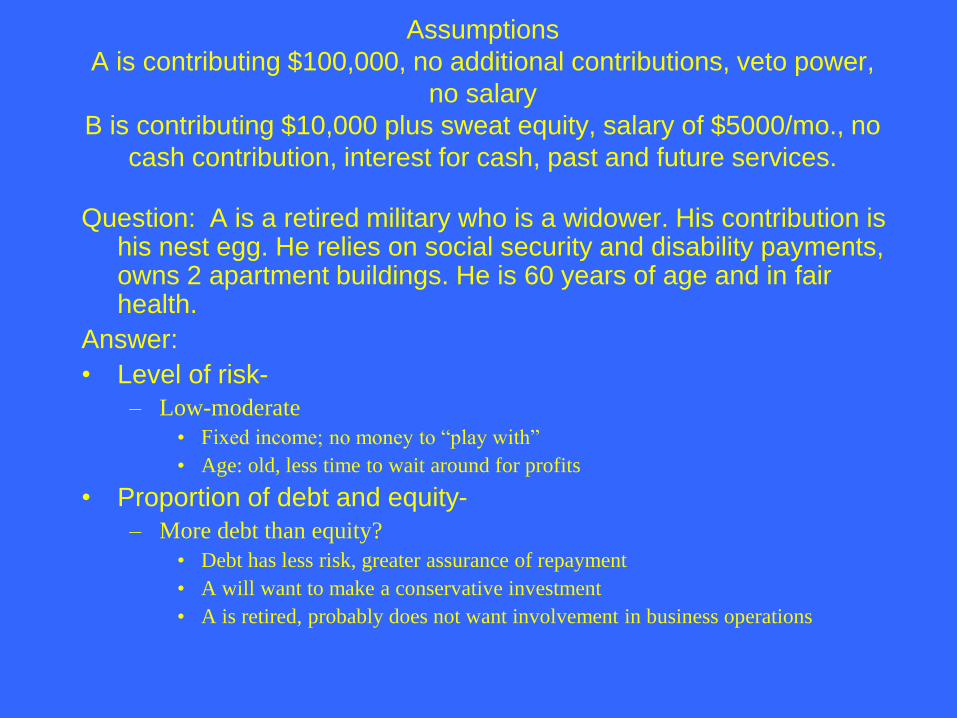

Assumptions

A is contributing $100,000, no additional contributions, veto power,

no salary

B is contributing $10,000 plus sweat equity, salary of $5000/mo., no

cash contribution, interest for cash, past and future services.

Question: A is a retired military who is a widower. His contribution is his nest egg. He relies on social security and disability payments, owns 2 apartment buildings. He is 60 years of age and in fair health.

Answer:

• Level of risk-

– Low-moderate

• Fixed income; no money to “play with”

• Age: old, less time to wait around for profits

• Proportion of debt and equity-

– More debt than equity?

• Debt has less risk, greater assurance of repayment

• A will want to make a conservative investment

• A is retired, probably does not want involvement in business operations

Risk and Interest?

b) ALT 2: A is a real estate attorney, with

a profitable practice from which he

receives a salary of $120,000. He has

other investments that bring in $10,000

a year, is 32 years of age, and is

looking to retire by the time he is 40

years of age.

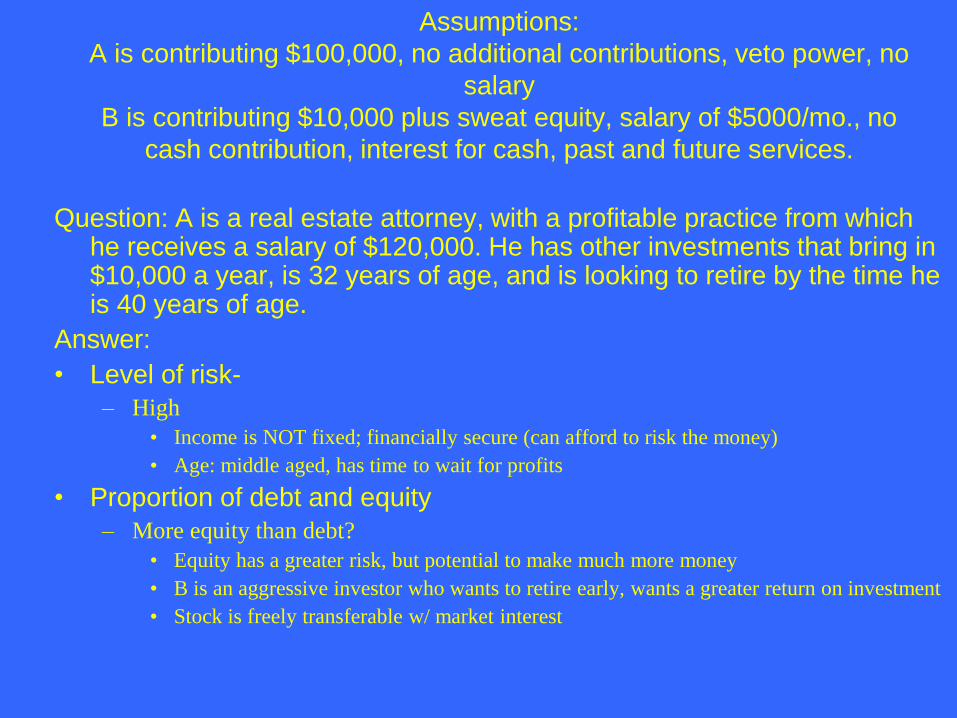

Assumptions:

A is contributing $100,000, no additional contributions, veto power, no

salary

B is contributing $10,000 plus sweat equity, salary of $5000/mo., no

cash contribution, interest for cash, past and future services.

Question: A is a real estate attorney, with a profitable practice from which he receives a salary of $120,000. He has other investments that bring in $10,000 a year, is 32 years of age, and is looking to retire by the time he is 40 years of age.

Answer:

• Level of risk-

– High

• Income is NOT fixed; financially secure (can afford to risk the money)

• Age: middle aged, has time to wait for profits

• Proportion of debt and equity

– More equity than debt?

• Equity has a greater risk, but potential to make much more money

• B is an aggressive investor who wants to retire early, wants a greater return on investment

• Stock is freely transferable w/ market interest

Risk and Interest?

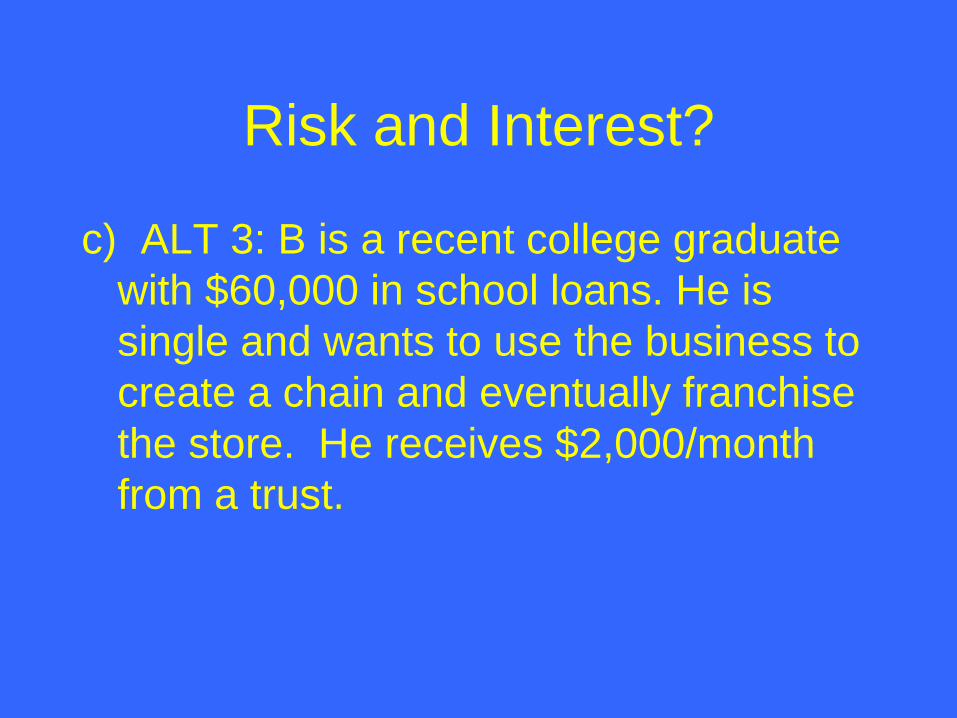

c) ALT 3: B is a recent college graduate

with $60,000 in school loans. He is

single and wants to use the business to

create a chain and eventually franchise

the store. He receives $2,000/month

from a trust.

Assumptions:

A is contributing $100,000, no additional contributions, veto power, no

salary.

B is contributing $10,000 plus sweat equity, salary of $5000/mo., no

cash contribution, interest for cash, past and future services.

Question: B is a recent college graduate with $60,000 in school loans.

He is single and wants to use the business to create a chain and

eventually franchise the store. He receives $2,000/month from a

trust.

Answer:

• Level of risk-

– Medium- High

• Low income, but wants to grow big via franchise

• Age: young and energy to work hard

• Proportion of debt and equity

– Equal proportion of debt and equity

• B wants to participate in the operation and control of the company, but is not in the

position to take a great financial risk