Business insurance Marketing guide

24

Life 674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 This Producer Guide is designed to provide introductory information in regard to the subject matter covered. It is general in nature and not comprehensive, the applicable laws may change and the strategies suggested may not be suitable for everyone. This material does not constitute tax, legal or accounting advice and neither Midland National nor any of its producers, employees or registered representatives are in the business of offering such advice. It was not intended or written for use and cannot be used by any taxpayer for the purpose of avoiding any IRS penalty. It was written to support the marketing of the transactions or topics addressed. Comments on taxation are based on Midland National’s understanding of current tax law, which is subject to change. Anyone interested in these transactions or topics should seek advice based on his or her particular circumstances from their own independent legal and tax advisors. Business insurance Marketing guide Expand your market

Transcript of Business insurance Marketing guide

Life

674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20

This Producer Guide is designed to provide introductory information in regard to the subject matter covered. It is general in nature and not comprehensive, the applicable laws may change and the strategies suggested may not be suitable for everyone. This material does not constitute tax, legal or accounting advice and neither Midland National nor any of its producers, employees or registered representatives are in the business of offering such advice. It was not intended or written for use and cannot be used by any taxpayer for the purpose of avoiding any IRS penalty. It was written to support the marketing of the transactions or topics addressed. Comments on taxation are based on Midland National’s understanding of current tax law, which is subject to change. Anyone interested in these transactions or topics should seek advice based on his or her particular circumstances from their own independent legal and tax advisors.

Business insuranceMarketing guideExpand your market

2674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

Business insurance marketing guide

For The Life Of Your Business®

A life insurance death benefit can help ensure that if the unthinkable happens, a closely held business can continue to be

successful.

The success of a business is largely dependent on strategy, planning and - of course - hard work. But there are a few

areas that can sometimes get overlooked. For business owners, these areas usually concern protecting and rewarding key

employees or successfully transferring a business to surviving family members or partners. Business insurance can help

ensure that all the effort and money invested in a business doesn’t disappear when things don’t go as planned.

This Producer Guide is designed to help you tap into the business insurance market...for the life of your client’s business

and the life of your business.

Table of ContentsThe Business Insurance Market ...........................................................................................................................4

Selecting the Right Product ......................................................................................................................................................................................... 4

Sponsorship........................................................................................................................................................................................................................... 4

Marketing Materials .......................................................................................................................................................................................................... 5

Underwriting ......................................................................................................................................................................................................................... 5

Key Employee Insurance ........................................................................................................................................6How it Works .......................................................................................................................................................................................................................6

Details ........................................................................................................................................................................................................................................7

Prospects ................................................................................................................................................................................................................................8

Tax Treatment ......................................................................................................................................................................................................................8

3674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

Executive Bonus Plan ..............................................................................................................................................9How it Works ........................................................................................................................................................................................................................9

Details ...................................................................................................................................................................................................................................... 10

Prospects .................................................................................................................................................................................................................................11

Tax Treatment .......................................................................................................................................................................................................................11

Supplemental Executive Retirement Plan (SERP) .........................................................................................12How it Works .......................................................................................................................................................................................................................12

Details .......................................................................................................................................................................................................................................13

Prospects ............................................................................................................................................................................................................................... 14

Tax Treatment ..................................................................................................................................................................................................................... 14

Buy-Sell Agreements ..............................................................................................................................................15Choosing the Type of Buy-Sell Agreement ........................................................................................................................................................15

Step Up in Cost Basis .......................................................................................................................................................................................................15

How an Entity-Purchase Agreement Works ...................................................................................................................................................... 16

- Entity-Purchase Example .......................................................................................................................................................................................... 16

Details of an Entity-Purchase Agreement ............................................................................................................................................................17

How a Cross-Purchase Agreement Works .......................................................................................................................................................... 18

- Cross-Purchase Example ........................................................................................................................................................................................... 18

Details of a Cross-Purchase Agreement ............................................................................................................................................................... 19

Prospects for Buy-Sell Agreements .......................................................................................................................................................................20

Tax Treatment of Buy-Sell Agreements ..............................................................................................................................................................20

One-Way Buy-Sell Agreement ............................................................................................................................21How it Works ..................................................................................................................................................................................................................... 22

Details ......................................................................................................................................................................................................................................23

Prospects ...............................................................................................................................................................................................................................23

Tax-Treatment ....................................................................................................................................................................................................................23

Appendix ..................................................................................................................................................................24Additional Resources ..................................................................................................................................................................................................... 24

InsMark Illustration System ........................................................................................................................................................................................ 24

Footnotes and Disclosures ..................................................................................................................................24

4674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

The Business Insurance MarketIt seems like common sense. Regardless of what new technologies develop, or what new efficiencies are attained, we know that it is the people that truly make a business profitable. But, do we act on that common sense? We insure certain business assets to protect against loss. But what about key employees, top executives, and business owners? Loss of a key employee can be devastating to a business.

Here are a few reasons why you may want to consider the business life insurance market:

1. There is a compelling need for business life insurance. A building may never burn, but every human being will eventually die. As a matter of fact, in most cases the need for business life insurance is as great as the need for personal life insurance. Many business owners have put their “all” into their businesses, and failure would be disastrous to their personal estates as well as to their businesses.

2. It’s the human life that matters. People generate profits – not machines. The need for insurance to offset the loss of key people is self-evident.

3. The business life insurance premium dollar may be comparatively easier to get. It is often easier to ask for a business check than it is for a personal check.

4. Business life insurance is an effective approach. Business owners who “live and breathe” their businesses may be indifferent to an approach based on personal insurance, but may become very interested when the subject is changed to the future of their business.

5. You may be better able to approach these prospects during normal business hours because the subject is business (not personal).

Business life insurance is a field of opportunity that no agent should overlook. If you prepare yourself for this market, you can not only increase your commission

income substantially, but also earn the gratitude, respect and loyalty of your clients for years to come. After your prospect is a business client, the door to his or her personal insurance planning may be open as well.

Selecting the Right ProductBusiness insurance marketing concepts are not tied to any particular product. For example, you may recommend term life insurance for some situations, such as Key Employee Insurance and Buy-Sell plans, or you could recommend universal life insurance using a minimum premium. When a business insurance plan requires cash value accumulation, such as an Executive Bonus Plan or a SERP, you’ll want to consider universal life and indexed universal life. Midland National offers a range of highly competitive products in each category. Some of our products emphasize a guaranteed death benefit, others emphasize early cash value accumulation, and still others focus on long-term cash value accumulation. You’ll be sure to find a strong product that meets your client’s need.

SponsorshipBusiness insurance usually involves some degree of employer sponsorship, whether the employer is the premium payer, policyowner or beneficiary. Each business insurance concept varies in the degree of required employer sponsorship. The concepts discussed here are selective executive benefits. If properly implemented, IRS pre-approval is not needed.

5674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

Marketing MaterialsWe’ve developed our marketing materials with two ends in mind: 1) to introduce the idea of business insurance to your client, and 2) to help you explain some of the intricacies of each business concept to your client. In addition to a general business insurance mailer, each business insurance concept has its own consumer brochure. Each brochure contains the same flowchart you’ll see in this guide. Use the brochure to help explain the concept to your client.

• 669MM SERP Consumer Brochure

• 670MM Key Employee Consumer Brochure

• 671MM Executive Bonus Consumer Brochure

• 675MM Buy-Sell Consumer Brochure

UnderwritingBusiness insurance coverage is unique and the information you provide to us up-front can help speed along the underwriting process. In addition to the routine age/amount medical requirements please complete a Business Insurance Supplement. A cover letter explaining the purpose and how the amount of coverage was determined is recommended to help the underwriter fully understand the sale.

If the coverage is owned by the business be sure to obtain a Corporate-Owned Life Insurance (COLI) form at the time of the application.

No group underwriting, simplified or guaranteed issue is available.

6674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

Key Employee Life InsuranceHelp Safeguard the Continuity of Your Client’s BusinessAlmost every business has key employees who are essential to its overall success. A key employee can be anyone who, among other things, is responsible for management decisions, is highly paid or has a significant impact on sales. If a key employee passes unexpectedly, replacing his or her knowledge, experience and potential loss of earnings can be costly, time-consuming, and sometimes fatal to a business. A helpful solution to offer your clients is Key Employee Life Insurance.

How it works1. The employer purchases a life insurance policy on

the employee and is the owner, premium payer, and beneficiary of the policy.

2. If the employee’s death occurs, death benefits are paid to the employer. Death benefits are generally received free of federal income taxes1.

3. At the employee’s retirement, the employer may use the policy’s cash value, through policy loans and withdrawals2, to help supplement the employee’s retirement income. Income to the employee is taxable.

Key Employee Life Insurance

Upon Death of Key Employee

Upon Retirement of Key Employee

Life Insurance Company

Life Insurance Company

Life Insurance Company

Business

Business

Business

Recruit

RecruitKey Employee

Premiums

Policy of Key Employee

Death Benefit Proceeds

Funds to Recruit Replacement

Funds to Recruit

Replacement

Supplement Retirement Income

Withdrawals & Loans

7674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

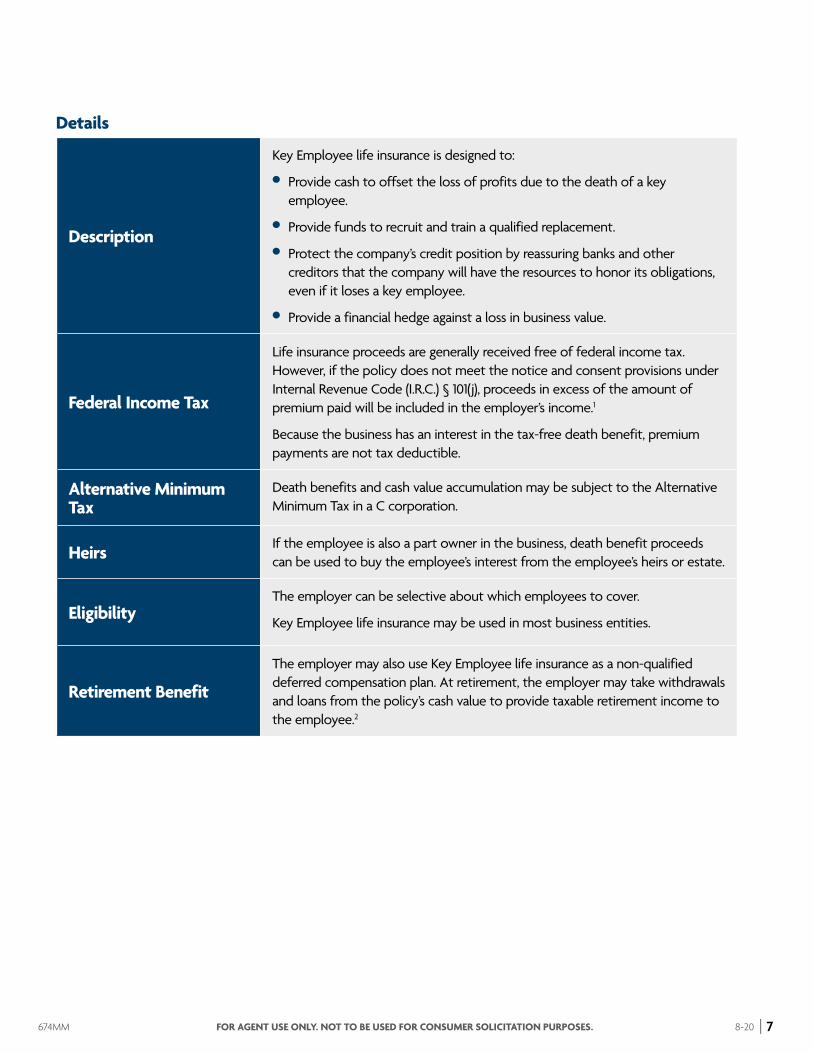

Details

Description

Key Employee life insurance is designed to:

• Provide cash to offset the loss of profits due to the death of a key employee.

• Provide funds to recruit and train a qualified replacement.

• Protect the company’s credit position by reassuring banks and other creditors that the company will have the resources to honor its obligations, even if it loses a key employee.

• Provide a financial hedge against a loss in business value.

Federal Income Tax

Life insurance proceeds are generally received free of federal income tax. However, if the policy does not meet the notice and consent provisions under Internal Revenue Code (I.R.C.) § 101(j), proceeds in excess of the amount of premium paid will be included in the employer’s income.1

Because the business has an interest in the tax-free death benefit, premium payments are not tax deductible.

Alternative Minimum Tax

Death benefits and cash value accumulation may be subject to the Alternative Minimum Tax in a C corporation.

Heirs If the employee is also a part owner in the business, death benefit proceeds can be used to buy the employee’s interest from the employee’s heirs or estate.

EligibilityThe employer can be selective about which employees to cover.

Key Employee life insurance may be used in most business entities.

Retirement Benefit

The employer may also use Key Employee life insurance as a non-qualified deferred compensation plan. At retirement, the employer may take withdrawals and loans from the policy’s cash value to provide taxable retirement income to the employee.2

8674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

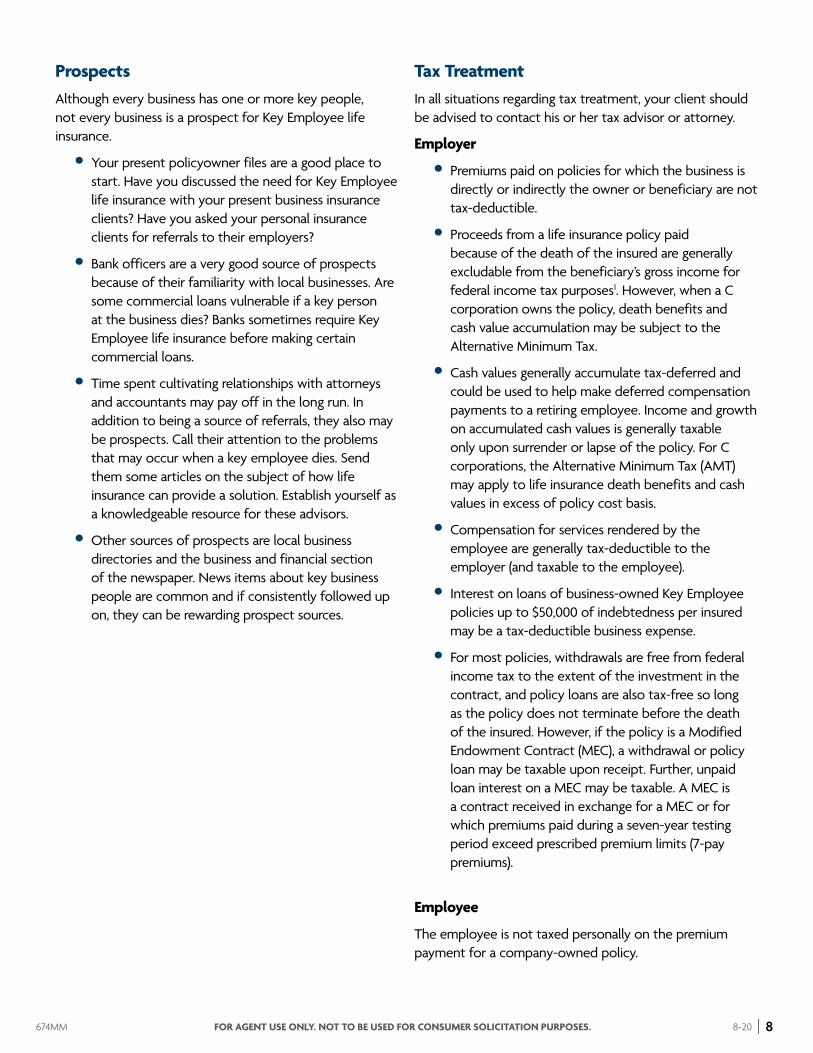

ProspectsAlthough every business has one or more key people, not every business is a prospect for Key Employee life insurance.

• Your present policyowner files are a good place to start. Have you discussed the need for Key Employee life insurance with your present business insurance clients? Have you asked your personal insurance clients for referrals to their employers?

• Bank officers are a very good source of prospects because of their familiarity with local businesses. Are some commercial loans vulnerable if a key person at the business dies? Banks sometimes require Key Employee life insurance before making certain commercial loans.

• Time spent cultivating relationships with attorneys and accountants may pay off in the long run. In addition to being a source of referrals, they also may be prospects. Call their attention to the problems that may occur when a key employee dies. Send them some articles on the subject of how life insurance can provide a solution. Establish yourself as a knowledgeable resource for these advisors.

• Other sources of prospects are local business directories and the business and financial section of the newspaper. News items about key business people are common and if consistently followed up on, they can be rewarding prospect sources.

Tax TreatmentIn all situations regarding tax treatment, your client should be advised to contact his or her tax advisor or attorney.

Employer

• Premiums paid on policies for which the business is directly or indirectly the owner or beneficiary are not tax-deductible.

• Proceeds from a life insurance policy paid because of the death of the insured are generally excludable from the beneficiary’s gross income for federal income tax purposes1. However, when a C corporation owns the policy, death benefits and cash value accumulation may be subject to the Alternative Minimum Tax.

• Cash values generally accumulate tax-deferred and could be used to help make deferred compensation payments to a retiring employee. Income and growth on accumulated cash values is generally taxable only upon surrender or lapse of the policy. For C corporations, the Alternative Minimum Tax (AMT) may apply to life insurance death benefits and cash values in excess of policy cost basis.

• Compensation for services rendered by the employee are generally tax-deductible to the employer (and taxable to the employee).

• Interest on loans of business-owned Key Employee policies up to $50,000 of indebtedness per insured may be a tax-deductible business expense.

• For most policies, withdrawals are free from federal income tax to the extent of the investment in the contract, and policy loans are also tax-free so long as the policy does not terminate before the death of the insured. However, if the policy is a Modified Endowment Contract (MEC), a withdrawal or policy loan may be taxable upon receipt. Further, unpaid loan interest on a MEC may be taxable. A MEC is a contract received in exchange for a MEC or for which premiums paid during a seven-year testing period exceed prescribed premium limits (7-pay premiums).

Employee

The employee is not taxed personally on the premium payment for a company-owned policy.

9674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

Executive Bonus Plan Help Your Clients Retain Talented EmployeesAttracting, retaining, and rewarding key employees can be challenging. If you have clients that are business owners, then you may know first hand just how hard it can be to hold on to top employees. But since they are vital to the life of every business, keeping them committed is essential. Loyal employees are hard to come by, and with recruiting and training costs on the rise, keeping reliable, quality employees is more important than ever. A helpful solution to offer your clients is an Executive Bonus arrangement.

How it works1. The employer selects an employee and the amount of

bonus to provide.

2. The employee applies for life insurance, which must be approved by the insurer before the Executive Bonus Plan takes effect.

3. The employer pays the life insurance premium on the employee’s behalf as a bonus.

4. Bonuses paid to the employee are generally tax-deductible to the employer and reportable as income to the employee. (The employer has the option to give the employee a Double Bonus to cover any taxes that may be due.)

5. At retirement, policy loans and withdrawals may be used to help supplement the employee’s retirement income2.

6. At the employee’s death, the death benefit proceeds are usually free from federal income tax to the beneficiary.

Executive Bonus Plan

Upon Death

Upon Retirement

Employer

Executive Bonus

Agreement

Life Insurance Company

Life Insurance Company

Life Insurance Company

Employee

Employee

Employee’s Beneficiary

IRS

Premiums

Insurance Policy

Death Benefit Proceeds

Withdrawals & Loans

10674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

Details

DescriptionUnder an Executive Bonus plan, the employer gives the selected employee a bonus, which the employee uses to buy a life insurance policy. The employee is the insured and owner and names his or her own beneficiary.

Single vs. Double Bonus

In a Single Bonus arrangement, the employer pays the life insurance premium on the employee’s behalf as a bonus. The employee is responsible for the income tax on the bonus.

In a Double Bonus arrangement, the bonus amount pays the premium, the tax on the premium, and the additional tax created by the bonus to minimize the tax effects for the employee.

Premiums

The employer pays the life insurance premium on the employee’s behalf.

The employee is able to purchase life insurance at a lower out of pocket expense — for Single Bonus arrangements, the income tax on the bonus is generally the employee’s only cost.

Federal Income Tax

The employee is responsible for income tax on the amount of the bonus.

The employee’s beneficiaries receive death benefit proceeds generally free of federal income tax.

For the business, the bonus may be a tax-deductible business expense.

Alternative Minimum Tax

Death benefits and cash value accumulation may be subject to the Alternative Minimum Tax in a C corporation.

Eligibility

The employer can be selective about which employees to cover.

When considering an Executive Bonus Plan for a business owner – the plan works best for businesses that are taxed separately from the person covered. For this reason, Executive Bonus does not work well for sole proprietors, partners in a partnership, stockholders in a Sub-S Corporation, or the members of some limited liability companies (LLCs).

CreditorsThe policies (and their cash values) are not subject to claims of the business’ creditors. The policies are not owned by the business so they are not business assets.

Retirement of the Employee

The employee could pay additional premium to grow the policy’s cash value and augment the cash value available to help supplement retirement income through withdrawals and policy loans2.

11674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

ProspectsThere may be times when your prospect is looking for a straightforward and uncomplicated solution to insurance needs in the business setting. At other times, the comptroller or accountant may challenge the tax treatment of an idea you’ve presented. For example, when discussing a Supplemental Executive Retirement Plan (SERP), an objection may be that employer premium payments are not income-tax-deductible. The owners are looking for a current, rather than delayed, tax advantage. Or when discussing a qualified retirement plan, the employer may object to the lack of selectivity among employees or the administrative costs.

One easily understood alternative is Executive Bonus. The employer uses generally tax deductible bonus payments to provide life insurance for selected employees with relatively little out-of-pocket tax cost to the employee.

Prime prospects are stockholder employees of closely held C corporations. Assuming the bonus amount is reasonable, the owners can do this for themselves – excluding all other employees if they wish. In a family business, even if the owners don’t want to participate, it can be used to pay premiums for insurance on children active in the business.

Other prime prospects are non-owner key employees. An Executive Bonus plan may serve as an alternative to giving an employee an ownership stake or a substantial salary increase.

Tax TreatmentIn all situations regarding tax treatment, your client should be advised to contact his or her tax advisor or attorney.

Employer

Premiums paid by the business may be deductible as long as they are reasonable in amount.

Employee

• The employee pays tax on the bonus.

• Death benefit proceeds from a life insurance policy paid because of the death of the insured are generally excludable from the beneficiary’s gross income for federal income tax purposes.

• Cash values grow tax-deferred. Income and growth on accumulated cash values are generally taxable only upon surrender or lapse.

• For most policies, withdrawals are free from federal income tax to the extent of the investment in the contract, and policy loans are also tax-free so long as the policy does not terminate before the death of the insured. However, if the policy is a Modified Endowment Contract (MEC), a withdrawal or policy loan may be taxable upon receipt. Further, unpaid loan interest on a MEC may be taxable. A MEC is a contract received in exchange for a MEC or for which premiums paid during a seven-year testing period exceed prescribed premium limits (7-pay premiums).

12674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

Supplemental Executive Retirement Plan (SERP) Help Your Clients Motivate Their Top ExecutivesA Supplemental Executive Retirement Plan is an incentive program designed to provide benefits to the employee upon retirement, or to their survivors upon the employee’s death. The employer puts money aside to fund its obligation, and usually purchases life insurance on the employee to help meet its responsibilities.

This type of plan can help attract, retain, motivate, and reward specific employees. Unlike other benefits, a SERP does not have to be offered to all employees, which may increase the value for the selected individuals.

How it works

1. The employer and employee enter into an agreement under which the employee will receive certain payments from the employer in the event of retirement or death.

2. The employer buys an insurance policy on the life of the employee to help the employer meet its obligations under the SERP plan.

3. The employer owns and pays the premium for the life insurance policy.

4. The cash value of the policy accumulates tax-deferred.3

5. At the employee’s retirement, the employer can use the policy’s cash value to help pay retirement benefits through policy loans and withdrawals2 which are generally free from federal income tax. Benefit payments to the employee may be a tax-deductible business expense to the employer. Retirement benefits paid by the employer to the employee will be taxable as income.

6. When the employee dies, the employer generally receives the death benefit proceeds free from federal income tax1 and can use the death benefit proceeds to provide survivor benefits to the employee’s heirs. Amounts paid to the heirs may be a tax-deductible business expense to the employer. Survivor benefits paid by the employer to the employee’s heirs will be taxable as income.

Supplemental Executive Retirement Plan

Upon Death

Upon Retirement

Employer

Employer

Employer

SERP Agreement

SERP Agreement

SERP Agreement

Life Insurance Company

Life Insurance Company

Life Insurance Company

Employee

Employee’s Beneficiary

Employee

IRS

IRS

Premiums

Income Tax

Income Tax

Death Benefit Proceeds

Withdrawals & Loans

Defined Benefit

Defined Benefit

Insurance Policy

13674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

Details

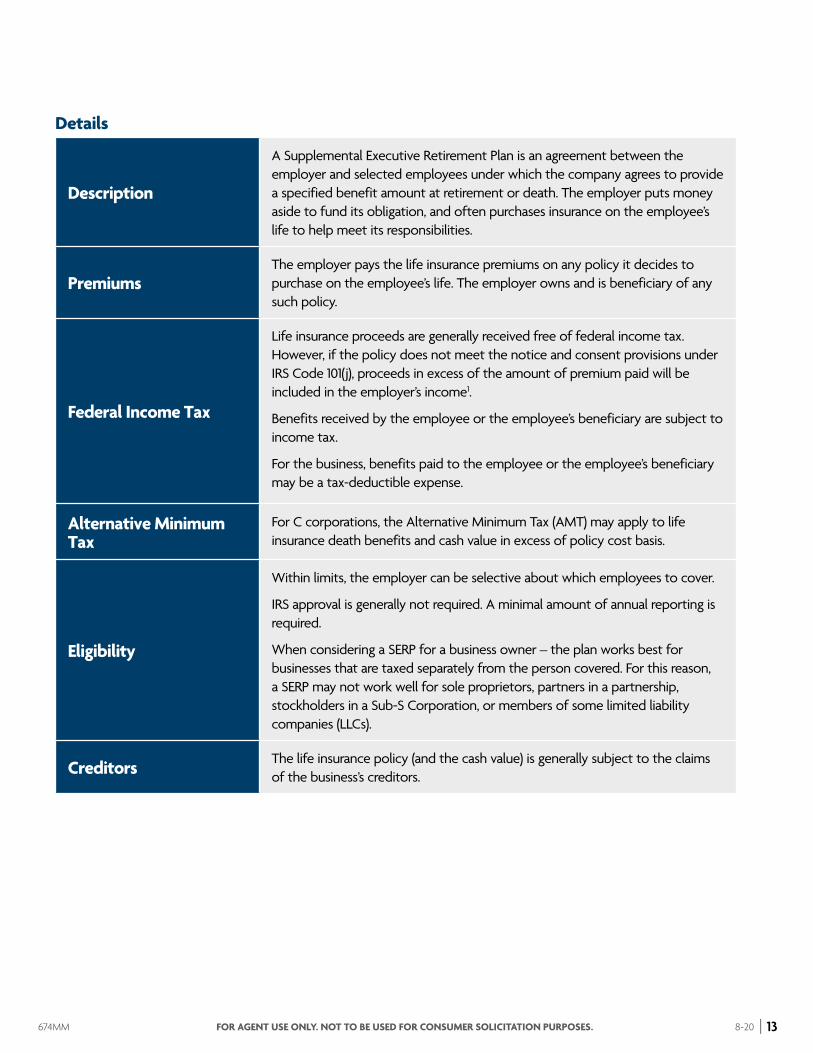

Description

A Supplemental Executive Retirement Plan is an agreement between the employer and selected employees under which the company agrees to provide a specified benefit amount at retirement or death. The employer puts money aside to fund its obligation, and often purchases insurance on the employee’s life to help meet its responsibilities.

PremiumsThe employer pays the life insurance premiums on any policy it decides to purchase on the employee’s life. The employer owns and is beneficiary of any such policy.

Federal Income Tax

Life insurance proceeds are generally received free of federal income tax. However, if the policy does not meet the notice and consent provisions under IRS Code 101(j), proceeds in excess of the amount of premium paid will be included in the employer’s income1.

Benefits received by the employee or the employee’s beneficiary are subject to income tax.

For the business, benefits paid to the employee or the employee’s beneficiary may be a tax-deductible expense.

Alternative Minimum Tax

For C corporations, the Alternative Minimum Tax (AMT) may apply to life insurance death benefits and cash value in excess of policy cost basis.

Eligibility

Within limits, the employer can be selective about which employees to cover.

IRS approval is generally not required. A minimal amount of annual reporting is required.

When considering a SERP for a business owner – the plan works best for businesses that are taxed separately from the person covered. For this reason, a SERP may not work well for sole proprietors, partners in a partnership, stockholders in a Sub-S Corporation, or members of some limited liability companies (LLCs).

Creditors The life insurance policy (and the cash value) is generally subject to the claims of the business’s creditors.

14674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

ProspectsProspects for a Supplemental Executive Retirement Plan may be found in any business, regardless of whether it’s a closely held private company or a large public corporation. Examples include owner-employees, managers, key executives, and highly compensated sales people. Most businesses are generally looking to provide an extra “perk” to help ensure they retain key employees.

Tax TreatmentIn all situations regarding tax treatment, your client should be advised to contact his or her tax advisor or attorney. In particular, the client and his/her advisors should take great care to avoid special tax issues related to Section 409A of the Internal Revenue Code.

Employer

• Premiums paid on policies for which the business is directly or indirectly the owner or beneficiary are not tax-deductible.

• Benefit payments, when made to either the employee or his or her beneficiary because of death, are generally tax-deductible to the employer.

• Interest on loans for business-owned SERP policies up to $50,000 of indebtedness per person may be a tax-deductible business expense.

• Cash values generally grow tax-deferred3. Income and growth on accumulated cash values is generally taxable only upon surrender or lapse2.

• Death benefit proceeds from a life insurance policy paid to the employer because of the death of the insured are generally excludable from the employer’s gross income for income tax purposes. Death benefits and cash values may be subject to the Alternative Minimum Tax.

• For most policies, withdrawals are free from federal income tax to the extent of the investment in the contract, and policy loans are also tax-free so long as the policy does not terminate before the death of the insured. However, if the policy is a Modified Endowment Contract (MEC), a withdrawal or policy loan may be taxable upon receipt. Further, unpaid loan interest on a MEC may be taxable. A MEC is a contract received in exchange for a MEC or for which premiums paid during a seven-year testing period exceed prescribed premium limits (7-pay premiums).

Employee

• Income taxes are generally deferred until later years as long as the agreement is properly drafted and the plan is properly administered.

• When received by either the employee at retirement or the employee heirs at death, payments are reportable as income.

15674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

Buy-Sell Agreements Help Prepare Your Clients For Ownership TransferThe death of a business owner or partner can be an uncertain time for the life of a business. A Buy-Sell agreement can help protect your clients and their businesses from the effects of unintended or unwelcome transfers of ownership. It may also help protect your client’s heirs, by giving them an opportunity to turn shares into cash. In addition, it’s important to develop a plan to help surviving family members or owners fund the transfer of ownership of the business.

Choosing the Type of Buy-Sell AgreementIt is not unusual to encounter debate over whether a Buy-Sell plan in a corporation should be set up as an Entity-Purchase (a.k.a. stock redemption) or Cross-Purchase basis.

Entity-Purchase plans are considered simple because they require only one life policy per owner for funding. This simplicity can often be an important factor, especially where there are more than two or three owners. However, they suffer from some potential tax disadvantages that may be important to the owners.

• The surviving owners may not receive a full step-up in their cost basis when they purchase the interest of a deceased owner. The type of tax entity the business is (C corporation, S corporation or other) will affect the amount of this step-up in basis.

• Any asset backing the plan (such as life insurance) is subject to the claims of the business’ creditors, because the entity owns the asset.

• For C corporations, the alternative minimum tax may apply.

• There is no possibility for deducting the premiums of any life insurance used to fund the plan because it is owned by and payable to the business.

Cross-Purchase plans do not suffer from the listed disadvantages, but can become cumbersome to administer if there are multiple owners. Each owner must own a life insurance policy on each of the other owners to fund the purchase of that owner’s share. The surviving owners are the beneficiaries of the policy. A major advantage of this plan is that because each owner will be buying the other owner’s interest directly, there is a full step-up in cost basis on the purchased business interest. This can be a great tax advantage should any of the owners decide to sell their share of the business at a later date (before death).

Step Up in Cost BasisThe examples in the following pages show the importance of basis in considering which method of Buy-Sell arrangement may be preferable. There are other factors, however, to consider such as:

1. Likelihood of selling the business: If the business is not likely to ever be sold, the cost basis issue may be immaterial.

2. Creditor Claims: Under any entity-purchase plan, the business owns the life insurance policies so the cash values of those policies are available to the business and its creditors and are potentially exposed to the claims of the policyowner’s personal creditors. In contrast for a corporation, the cash values are not generally subject to the claims of the creditors for a cross-purchase plan, since the business does not own the life insurance policies. Keep in mind that state law may exempt cash values and death benefit proceeds from claims of personal creditors.

3. Equalization of Premium: In an entity purchase plan, for a C corporation, the corporation owns all the life insurance policies and pays all premiums. Younger stockholders may avoid paying the potentially higher premiums for older insured stockholders. Also, the stockholders who own less stock avoid paying premiums on a life insurance policy for an owner whose stock value is higher.

4. Taxes: In determining which funding method to use, remember that in either case, life insurance is an after-tax purchase. Premiums are not deductible.Death benefit proceeds are generally free from federal income tax1.

Note that in a closely held business, owners are often required by lenders to personally guarantee corporate debt. This may subject the owner’s assets, including life insurance cash values, to corporate creditors.

16674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

How an Entity-Purchase Agreement Works1. The business purchases life insurance on the lives of all

the owners and is the owner, beneficiary, and premium payer on the policies.

2. The amount of coverage on each owner is the value of the individual’s ownership in the business.

3. Upon the death of an owner, death benefit proceeds are paid to the business.

4. The death benefit proceeds are used to buy the deceased owner’s interest in the business from the deceased’s heirs or estate.

Entity-Purchase ExampleTwo individuals form a C corporation. Each has a 50% ownership interest and a $50,000 cost basis in their stock. They enter into an entity purchase agreement (a.k.a. stock redemption agreement). One partner dies when the agreed purchase price for the stock is $75,000. The corporation purchases the deceased owner’s stock for the agreed upon $75,000. The surviving partner now owns 100% of the business because they own all the outstanding stock, but their cost basis is still $50,000. If they subsequently sell their stock for $200,000, they will have a $150,000 taxable gain ($200,000 sale price less the $50,000 cost basis equals $150,000).

Entity Purchase: Two-Owner Business

At Death of Owner B

Entity Purchase

Agreement

Life Insurance Company

Life Insurance Company

Business Entity

Business Entity

Owner A

Owner B

Owner B’s Heirs

Policies on Each Other

Death Benefit Proceeds

Death Benefit Proceeds

Business Interest

17674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

Details of an Entity-Purchase Agreement

DescriptionAn Entity-Purchase Agreement is an arrangement between the business entity and individual business owners. The business buys a life insurance policy on each of the owners and is the beneficiary.

Premiums The business pays the life insurance premiums.

Federal Income Tax

Life insurance proceeds are generally received free of federal income tax. However, if the policy does not meet the notice and consent provisions under IRS Code 101(j), proceeds in excess of the amount of premium paid will be included in the employer’s income1.

Because the business has an interest in the tax-free death benefit, premium payments are not tax deductible.

Estate Tax The agreement would be relevant to setting the value of the business interest for federal estate tax purposes.

Alternative Minimum Tax

For C corporations, the Alternative Minimum Tax (AMT) may apply to life insurance death benefits and cash value in excess of policy cost basis.

Creditors The life insurance policies (and their cash values) are subject to the business’ creditors.

Heirs Heirs receive a pre-determined price for the deceased’s share of the business.

Capital Gains

Surviving owners in a C corporation do not receive a full step-up in cost basis since the business purchases the interest and retires the purchased interest. This can result in a larger tax bill should surviving owners sell prior to their own deaths than under a Cross-Purchase plan. However, some pass-through types of business entities may receive a pro rata step-up in cost basis for their surviving owners when the life insurance death benefit is paid to the business prior to the stock purchase.

Sale of stock by an owner’s estate normally will be considered the sale of a capital asset and receive capital gains tax treatment. However, there usually is little or no capital gain to be recognized because of the step-up in basis of the business interest to its fair market value at the death of an owner.

Retirement of an Owner

The business could pay additional premium to grow the life insurance policy’s cash value. The business could potentially buy the retiring owner’s shares through withdrawals and policy loans2 from the policy’s cash value.

18674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

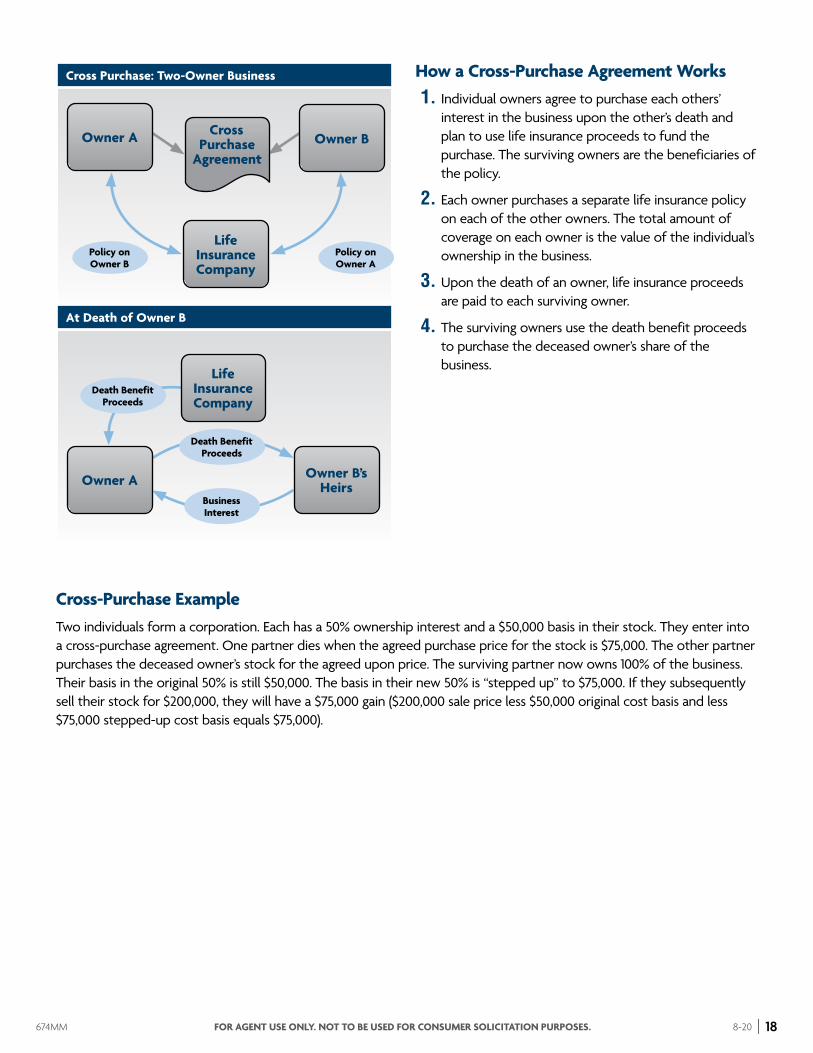

How a Cross-Purchase Agreement Works1. Individual owners agree to purchase each others’

interest in the business upon the other’s death and plan to use life insurance proceeds to fund the purchase. The surviving owners are the beneficiaries of the policy.

2. Each owner purchases a separate life insurance policy on each of the other owners. The total amount of coverage on each owner is the value of the individual’s ownership in the business.

3. Upon the death of an owner, life insurance proceeds are paid to each surviving owner.

4. The surviving owners use the death benefit proceeds to purchase the deceased owner’s share of the business.

Cross-Purchase ExampleTwo individuals form a corporation. Each has a 50% ownership interest and a $50,000 basis in their stock. They enter into a cross-purchase agreement. One partner dies when the agreed purchase price for the stock is $75,000. The other partner purchases the deceased owner’s stock for the agreed upon price. The surviving partner now owns 100% of the business. Their basis in the original 50% is still $50,000. The basis in their new 50% is “stepped up” to $75,000. If they subsequently sell their stock for $200,000, they will have a $75,000 gain ($200,000 sale price less $50,000 original cost basis and less $75,000 stepped-up cost basis equals $75,000).

Cross Purchase: Two-Owner Business

At Death of Owner B

Life Insurance Company

Cross Purchase

AgreementOwner A Owner B

Policy on Owner B

Policy on Owner A

Life Insurance Company

Owner A Owner B’s Heirs

Death Benefit Proceeds

Death Benefit Proceeds

Business Interest

19674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

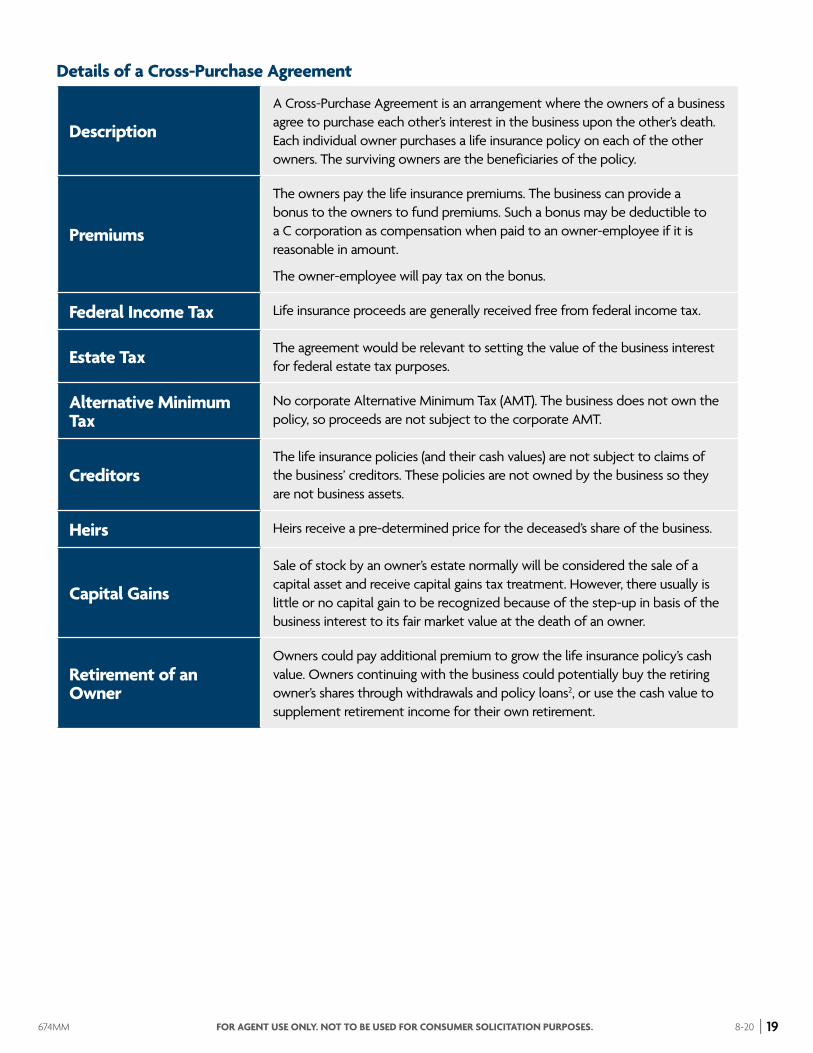

Details of a Cross-Purchase Agreement

Description

A Cross-Purchase Agreement is an arrangement where the owners of a business agree to purchase each other’s interest in the business upon the other’s death. Each individual owner purchases a life insurance policy on each of the other owners. The surviving owners are the beneficiaries of the policy.

Premiums

The owners pay the life insurance premiums. The business can provide a bonus to the owners to fund premiums. Such a bonus may be deductible to a C corporation as compensation when paid to an owner-employee if it is reasonable in amount.

The owner-employee will pay tax on the bonus.

Federal Income Tax Life insurance proceeds are generally received free from federal income tax.

Estate Tax The agreement would be relevant to setting the value of the business interest for federal estate tax purposes.

Alternative Minimum Tax

No corporate Alternative Minimum Tax (AMT). The business does not own the policy, so proceeds are not subject to the corporate AMT.

CreditorsThe life insurance policies (and their cash values) are not subject to claims of the business’ creditors. These policies are not owned by the business so they are not business assets.

Heirs Heirs receive a pre-determined price for the deceased’s share of the business.

Capital Gains

Sale of stock by an owner’s estate normally will be considered the sale of a capital asset and receive capital gains tax treatment. However, there usually is little or no capital gain to be recognized because of the step-up in basis of the business interest to its fair market value at the death of an owner.

Retirement of an Owner

Owners could pay additional premium to grow the life insurance policy’s cash value. Owners continuing with the business could potentially buy the retiring owner’s shares through withdrawals and policy loans2, or use the cash value to supplement retirement income for their own retirement.

20674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

Prospects for Buy-Sell AgreementsAny owner in a closely held private company is a good prospect for a buy-sell agreement. Many business owners assume that their business will continue regardless of who in the business dies. This assumption can create a false sense of security. They may not realize that while the death of an owner in a closely held business may leave its legal structure intact, it may alter the business’s vital management structure, and it may create problems for the heirs of the deceased.

With most closely held businesses, the ownership is generally concentrated in a few employee owners.

Tax Treatment of Buy-Sell AgreementsIn all situations regarding tax treatment, your client should be advised to contact his or her tax advisor or attorney.

• Premiums paid are not tax-deductible, whether paid by the business or the individual owners. However, in a Cross-Purchase buy out, a C corporation may pay a tax deductible bonus to owners to cover premiums on their individually owned life insurance policies.

• Interest on loans of business-owned life insurance policies up to $50,000 of indebtedness per person may be a tax-deductible business expense. Loan interest on a policy related to a Cross-Purchase buy-sell is generally not deductible on personal income taxes.

• Cash values grow tax-deferred3. Income and growth on accumulated cash values is generally taxable only upon surrender or lapse. For C corporations, the Alternative Minimum Tax (AMT) may apply to life insurance proceeds in excess of policy cost basis.

• Death benefit proceeds are generally received free from federal income tax.

• Stock generally receives a stepped-up basis in the hands of the survivors. Stock appreciation could therefore escape capital gains tax.

• For most policies, withdrawals are free from federal income tax to the extent of the investment in the contract, and policy loans are also tax-free so long as the policy does not terminate before the death of the insured. However, if the policy is a Modified Endowment Contract (MEC), a withdrawal or policy loan may be taxable upon receipt. Further, unpaid loan interest on a MEC may be taxable. A MEC is a contract received in exchange for a MEC or for which premiums paid during a seven-year testing period exceed prescribed premium limits (7-pay premiums).

21674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

One-Way Buy-Sell AgreementTo close a proprietorship at the death of the owner, the executor must bring the business to a conclusion in order to settle the estate. Without an agreement and the money to continue, the business may have to be sold at a discount in a forced liquidation. Employees may lose their jobs and the sole proprietor’s family may be left with no income. A buyout agreement using a life insurance policy may eliminate these devastating results.

In a One-Way Buy-Sell Agreement, the sole owner and a purchaser agree to transfer the business interest at a certain value (or method for determining value) upon the occurrence of a specified event. The event can include a number of options such as the owner’s death, disability, or retirement. A One-Way Buy-Sell Agreement is most often used with a Sole Proprietorship, but can also be used effectively with single-owner corporations and Limited Liability Companies (LLCs).

A properly drafted buyout agreement should also address the contingencies of the owner’s disability or retirement. In a buyout plan fully funded with permanent life insurance, the policy’s cash values can provide all or part of the money needed to accomplish the buyout at disability or retirement. The disability buyout would be similar to a buyout at death in that a triggering event (in this case, the owner’s inability to work because of illness or accident) obligates the owner to sell and the buyer to purchase the business at the price and terms in the agreement.

For a retirement buyout, the owner and buyer likewise agree to the purchase price and terms of purchase; the buyout may be accomplished with either a lump-sum payment or a series of payments over time.

22674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

How it Works1. An agreement is drafted obligating a key employee

or third-party buyer to purchase the business for a stipulated price in the event of the owner’s death (or disability or retirement).

2. The third party is the owner, beneficiary, and premium payer on a life insurance policy on the owner.

3. Premiums are not tax deductible to the business, but death benefit proceeds paid to the employer or third party are generally received free from federal income tax. When the third-party buyer is an employee, the employer may pay a tax deductible bonus if reasonable in amount to the employee to help pay premiums. The employee will pay tax on the bonus.

4. The life insurance provides the key employee or third party with the money to buy the business from the deceased owner’s heirs or estate.

5. If the employer retires or becomes disabled, the third party or employee may borrow against the life insurance policy’s cash value to purchase the business2.

At Death of Owner

At Retirement or Disability of Owner

Single Owner

Life Insurance Company

Life Insurance Company

Life Insurance Company

Owner

Owner

Owner’s

Heirs

Third Party

Third Party

Third Party

Death Benefit Proceeds

Policy on Owner

Death Benefit Proceeds

Business Interest

Business Interest

Withdrawals & Loans

Withdrawals & Loans

Cross Purchase

Agreement

23674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20 |

Details

Description

A One-Way Buy-Sell Agreement is an arrangement where the sole owner and a third party (such as a key employee) agree to a buy-out plan in the case of death, disability, or retirement. To fund the buy-out, the third party purchases and owns life insurance on the owner.

Premiums The third party pays the life insurance premiums.

Federal Income Tax Life Insurance proceeds are generally received free of federal income tax.

Estate Tax The agreement would be relevant to setting the value of the business interest for federal estate tax purposes.

Alternative Minimum Tax

No corporate Alternative Minimum Tax (AMT). The business owner does not own the life insurance policy, so death benefit proceeds are not subject to the corporate AMT.

CreditorsThe life insurance policy (and its cash value) is not subject to claims of the business’ creditors. This policy is not owned by the business so it is not a business asset.

Heirs Heirs receive a pre-determined price for the deceased’s share of the business.

Capital Gains

Sale of stock by an owner’s estate normally will be considered the sale of a capital asset and receive capital gains tax treatment. However, there usually is little or no capital gain to be recognized because of the step-up in basis of the business interest to its fair market value at the death of an owner.

Retirement or Disability of the Sole Proprietor

The third party may pay additional premium to grow the life insurance policy’s cash value. The third party could potentially buy the owner’s shares through withdrawals and policy loans2.

Prospects The prospects for One-Way Buy-Sell plan are obviously individually owned small businesses with a limited number of employees. Your sources for prospects are often the same as for Key Employee insurance, because a key employee or other willing buyer must be identified to become the business owner at the proprietor’s death, disability or retirement.

Tax TreatmentIn all situations regarding tax treatment, your client should be advised to contact his or her tax advisor or attorney.

• Premiums are not tax-deductible unless paid by bonus plan.

• Proceeds from a life insurance policy paid because of the death of the insured are generally excludable from the beneficiary’s gross income for income tax purposes.

• For most policies, withdrawals are free from federal income tax to the extent of the investment in the contract, and policy loans are also tax-free so long as the policy does not terminate before the death of the insured. However, if the policy is a Modified Endowment Contract (MEC), a withdrawal or policy loan may be taxable upon receipt. Further, unpaid loan interest on a MEC may be taxable. A MEC is a contract received in exchange for a MEC or for which premiums paid during a seven-year testing period exceed prescribed premium limits (7-pay premiums).

Administrative OfficeOne Sammons PlazaSioux Falls, South Dakota MidlandNational.com

674MM FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. 8-20

AppendixThis Producer Guide is designed to provide introductory information in regard to the subject matter covered. It is general in nature and not comprehensive, the applicable laws may change and the strategies suggested may not be suitable for everyone. This material does not constitute tax, legal or accounting advice and neither Midland National nor any of its producers, employees or registered representatives are in the business of offering such advice. It was not intended or written for use and cannot be used by any taxpayer for the purpose of avoiding any IRS penalty. It was written to support the marketing of the transactions or topics addressed. Comments on taxation are based on Midland National’s understanding of current tax law, which is subject to change. Anyone interested in these transactions or topics should seek advice based on his or her particular circumstances from their own independent legal and tax advisors.

Other Potential ResourcesAdvanced Underwriting Consultants (AUC)AUC provides customized advanced sales support to life insurance professionals including telephone and e-mail consultation, proposal support, and sample documents.

www.advancedunderwriting.com [email protected] 1-888-556-8650

AUC only provides general tax and technical information for the information of Midland National employees and producers. AUC is not providing legal or tax advice on which a prospective or current customer can rely, nor should AUC materials be used for such purposes. If legal or tax advice is needed by prospective or current customers, an independent legal counsel or tax advisor should be sought. AUC materials are not for use with, or disclosure to, any Midland National prospective or current insurance customers. Midland National and its agents do not give legal or tax advice.

The American CollegeThe American College is an accredited non-profit educational institution providing training and development for financial services professionals.

Textbooks available through The American College at www.theamericancollege.edu.

InsMark Illustration SystemThe InsMark Illustration System allows you to effectively illustrate advanced market concepts using Midland National products and ExactIllustrations, Midland National’s web-based illustration software. For more information about how you can download a copy of the InsMark Illustrations System, look under the Marketing/Sales tab on LifeSupport.

The InsMark Illustration System is third-party software that provides supplemental illustrations for presenting advanced markets concepts. A Midland National illustration must accompany the InsMark supplemental illustration. InsMark, Inc., 2400 Camino Ramon, Suite 150, San Ramon, CA 94583.

The National Underwriter CompanyThe National Underwriter Company publishes print, web and software products for the insurance and financial services industries. TaxFacts Online resources are available through the National Underwriter Company at pro.nuco.com.

Footnotes and Disclosures1. See section 101(a) of the Internal Revenue Code. The exclusion for the death benefit is limited in a number of circumstances. In particular, if a policy is owned by the employer of the insured person, federal income tax is imposed on the death benefit to the extent the death benefit exceeds premiums previously paid for the policy, unless certain notice and consent requirements are satisfied. See section 101(j) of the Code. Notice – Before the policy is issued, the employer must provide written notice to the employee of the employer’s intention to purchase the policy, of the maximum possible face amount, and that the employer will be the beneficiary of the policy’s death benefit.Consent – Before the policy is issued, the employee must provide written consent to being insured under the policy and to the fact that such coverage may continue after he or she terminates employment. If these notice and consent requirements are met, the exclusion under section 101(a) will be available (1) for death benefits paid on an insured who was an employee at any time during the 12-month period before the insured’s death, and (2) for death benefits paid on an insured who, at the time the policy was issued, was a director or was a highly compensated employee or highly compensated individual (within the meaning of section 101(j)(2)(A)(ii)).The client may use Midland National form 7516 to fulfill the Notice and Consent requirements.2. In some situations loans and withdrawals may be subject to federal taxes. Midland National does not give tax or legal advice. Clients should be instructed to consult with and rely on their own tax advisor or attorney for advice on their specific situation.Income and growth on accumulated cash values is generally taxable only upon withdrawal. Adverse tax consequences may result if withdrawals exceed premiums paid into the policy. Withdrawals or surrenders made during a Surrender Charge period will be subject to surrender charges and may reduce the ultimate death benefit and cash value. Surrender charges vary by product, issue age, sex, underwriting class, and policy year.3. The tax-deferred feature of the universal life policy is not necessary for a tax-qualified plan. In such instances, your client should consider whether other features, such as the death benefit and optional riders make the policy appropriate for your client’s needs. Before purchasing this policy, your client should obtain competent tax advice both as to the tax treatment of the policy and the suitability of the product.Neither Midland National nor its agents give tax advice. Please advise your customers to consult with and rely on a qualified legal or tax advisor before entering into or paying additional premiums with respect to such arrangements.Sammons FinancialSM is the marketing name for Sammons® Financial Group, Inc.’s member companies, including Midland National® Life Insurance Company. Annuities and life insurance are issued by, and product guarantees are solely the responsibility of, Midland National Life Insurance Company.