HDFC - Marketing - Insurance Sector

180

PROJECT REPORT ON MARKETING RESEARCH ABOUT COMPETITION IN INSURANCE INDUSTRY & APPOINTMENT OF FC’S [EMPHASIS ON LIFE INSURANCE] Respect Yourself Submitted for the partial fulfillment towards the award of the degree in MASTER OF BUSINESS ADMINISTRATION of U.P. Technical University, Lucknow (Session : 2006-2008) UNDER THE SUPERVISION OF MR. FAIZ KHAN (Sales Development Manager, HDFC SLIC) SUBMITTED TO SUBMITTED BY DR. K.N. SINGH ANSHUL CHAURASIA

-

Upload

kritika-dwivedi -

Category

Documents

-

view

68 -

download

1

Transcript of HDFC - Marketing - Insurance Sector

PROJECT REPORT

ON

MARKETING RESEARCH ABOUT COMPETITION IN

INSURANCE INDUSTRY & APPOINTMENT OF FC’S

[EMPHASIS ON LIFE INSURANCE]

Respect Yourself

Submitted for the partial fulfillment towards the award of the degree in MASTER OF BUSINESS ADMINISTRATION

of U.P. Technical University, Lucknow(Session : 2006-2008)

UNDER THE SUPERVISION OFMR. FAIZ KHAN

(Sales Development Manager, HDFC SLIC)

SUBMITTED TO SUBMITTED BY

DR. K.N. SINGHFaculty (MBA)

ANSHUL CHAURASIAMBA (IIIrd Sem)Roll No.: 0614970010

CENTER FOR MANAGEMENT TECHNOLOGY25, 27, 28, KNOWLEDGE PARK, PHASE-I, GREATER NOIDA

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

STUDENT DECLARATION

I, hereby certify that the Survey data collection and analysis work

related to research project report on ‘Marketing Research about

Competition in Insurance Industry & Appointment of FC’s’ has

been carried out exclusively on my own effort under the supervision

of Mr. FAIZ KHAN (Sales Development Manager, HDFC, SLIC)

is my research guide and Dr. K.N. Singh, Faculty Guide.

2

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

ACKNOWLEDGEMENT

First of all I would like expressing my gratitude to my Mentor, who guided me with his

knowledge and skill and helped me in successful completion of the work.

I gratefully acknowledge my project guide Dr. K.N. Singh, Faculty Guide, and

Supervision of Mr. Faiz Khan (Sales Development Manager, HDFC, SLIC). They

have been fully support and guide that was provided to me by various individuals that

led to the successful completion of this project. Their vision of the problem gave me

enough direction to bring out a meaningful result.

I am grateful to their great support and help all throughout the project. I am thankful

to them for taking out time and pointing out the multitudinous aspects of customer

service and helping me increase my learning out of the project.

I would heartily thank all the respondents of the survey without whose support &

valuable inputs this project would not have been completed.

ANSHUL CHAURASIA

MBA (IIIrd Sem)

3

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

TABLE OF CONTENTS

COMPANY PROFILE

INTRODUCTION

IMPORTANCE OF STUDY

SCOPE OF STUDY

LITERATURE REVIEW

RESEARCH DESIGN

RESEACH ANALYSIS

RESERCH OBJECTIVE

DATA COLLECTION

DATA ANALSYIS/INTERPRETATION

CONCLUSION

RECOMMENDATION

FURTHER SCOPE OF STUDY

APENDIX

QUESTIONNAIRE

BIBLIOGRAPHY

4

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

COMPANY PROFILE

5

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

ABOUT HDFC

• Incorporated in 1977 as a public limited company

• To specialize in provision of housing finance to

individuals, co-operative societies & the corporate sector

• First private sector retail housing finance company

• HDFC is listed on both BSE and NSE

• Market capitalisation (June 2002) - Rs. 79 billion (US $ 1.6

bn)

Strengths of HDFC

6

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

• Strong Brand

• Customer base of over 2 million

• Stable and experienced management

• High service standards

• High quality loan portfolio

• Provision for contingencies

• Constant technological upgradation of systems

• One of the best capital adequacy ratio

7

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

BACKGROUND

HDFC was incorporated in 1977 with the primary objective of meeting a social need – that of promoting home ownership by providing long-term finance to households for their housing needs. HDFC was promoted with an initial share capital of Rs. 100 million.

Business Objectives

The primary objective of HDFC is to enhance residential housing stock in the country through the provision of housing finance in a systematic and professional manner, and to promote home ownership. Another objective is to increase the flow of resources to the housing sector by integrating the housing finance sector with the overall domestic financial markets...

Organizational Goals

HDFC’s main goals are to a) develop close relationships with individual households, b) maintain its position as the premier housing finance institution in the country, c) transform ideas into viable and creative solutions, d) provide consistently high returns to shareholders, and e) to grow through diversification by leveraging off the existing client base.

HDFC is a professionally managed organization with a board of directors consisting of eminent persons who represent various fields including finance, taxation, construction and urban policy & development. The board primarily focuses on strategy formulation, policy and control, designed to deliver increasing value to shareholders.

Board of Directors

Mr. D S Parekh - Chairman Mr. Keshub Mahindra - Vice Chairman Ms. Renu S. Karnad - Executive Director Mr. K M Mistry - Managing Director Mr. D M Sukthankar Mr. D N Ghosh Mr. S Venkitaramanan

Dr. Ram S Tarneja Mr. N M Munjee Mr. D M Satwalekar Mr. Shirish B Patel Mr. Bansi S Mehta Dr. S A Dave

8

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

HDFC has a staff strength of 1029, which includes professionals from the fields of finance, law, accountancy, engineering and marketing.

Consultancy Services

HDFC is a unique example of a housing finance company which has demonstrated the viability of market-oriented housing finance in a developing country. It is viewed as an innovative institution and a market leader in the housing finance sector in India. The World Bank considers HDFC a model private sector housing finance company in developing countries and a provider of technical assistance for new and existing institutions, in India and abroad. HDFC’s executives have undertaken consultancy assignments related to housing finance and urban development on behalf of multilateral agencies all over the world.

HDFC has also served as consultant to international agencies such as World Bank, United States’ Agency for International Development (USAID), Asian Development Bank, United Nations’ Center for Human Settlements, Commonwealth Development Corporation (CDC) and United Nations’ Development Programme (UNDP). HDFC has also undertaken assignments for the United Nations’ Capital Development Fund in Ethiopia, for the UNCHS in Nairobi, for USAID in Russia and Bulgaria, and projects of the World Bank in Indonesia and Ghana.

At the national level, HDFC executives have played a key role in formulating national housing policies and strategies. Recognizing HDFC’s expertise, the Government of India has invited HDFC’s executives to join a number of committees and task forces related to housing finance, urban development and capital markets.

Consultancy assignments undertaken:

Project Title Project Country

Agency

State Mortgage Investment Bank Russia USAID

Review of Operations of Bank Tabunga Negara

Indonesia World Bank

Detailed Analysis of Housing Situation Bhutan Govt. of Bhutan

Study of Housing Finance Sector Ghana Govt. of Ghana

Management and Operations Audit Thailand C D C

Technical Assistance for Alliance Housing Oman Direct

9

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

Bank

Feasibility of Establishing New Mortgage Finance Comp

Mauritius C D C

Feasibility Study for a Second Building Society

Malawi Direct

Workshop on ‘Housing Finance & Managerial Effectiveness’ for Housing Professionals

Ghana World Bank

Review of Nepal Housing Development Finance Company Limited (NHDFC)

Nepal USAID & UNDP

Evaluation of an investment proposal of Commonwealth Development Corporation in Turks & Caicos Islands

Turks & Caicos Islands

C D C

Evaluation of Caribbean Housing Finance Corporation Limited, Jamaica

Jamaica C D C

Review of Mortgage Underwriting and Servicing Manuals developed for Bulgaria

Bulgaria The Urban Institute

Workshop on Credit Appraisal & Loan Recovery

Philippines Asian Coalition

Development of Mortgage Servicing Manual Russia Abt. Associates

Over the past two decades, HDFC has been making inroads into varied spheres of development, while retaining a focus on low-income housing and related issues. During this year, HDFC further consolidated its operations as a wholesaler in micro-finance and weaker section housing, while advancing the reconstruction activities at Gujarat into an intensive phase. In addition, HDFC has been engaged in some specific micro-finance initiatives involving for e.g. policy frameworks and developing case studies; these have been captured in a separate section below.

Lending Operations in Weaker-Section Housing

HDFC continued to utilize the Kreditanstalt für Wiederaufbau (KfW) lines (HDFC II and HDFC III) by making loans to Non Governmental Organisation (NGO) intermediaries and state government agencies towards low-cost rural and urban EWS housing projects. Under the second line comprising DM 30 million as grant (HDFC II), HDFC has drawn the full amount from KfW (INR equivalent Rs. 67.98 crore) and all sub-projects have now reached completion. This includes loan disbursements in the amount of Rs. 56.91 crore and the balance has been released as grant funds towards rehabilitation housing projects in response to natural calamities.

The third line, also a grant of DM 30 million is split into two components – the smaller component of Euro 6 million is

10

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

towards the micro-enterprise Finance Facility (MFF), whereas Euro 9.34 million have been earmarked towards the EWS housing component. The cumulative loan approvals, disbursements and related information for the housing projects under HDFC II and III are furnished in Table I.

The KfW has recently reviewed the progress under HDFC II and III and they have gathered that the borrowers were generally in control of their housing process, leading to optimal use of available resources, and good construction quality. The cost ceiling for housing construction has been increased to Rs. 60,000 per housing unit, as a consequence of which the end-borrower loan size has increased from the current level of Rs. 45,000 to Rs. 54,000 (upto 90% of cost).

MFF Lending and KfW Lines for Micro-Finance

During the year, HDFC has approved 11 income-generation projects under the Micro-enterprise Finance Facility i.e. MFF component of HDFC III. On a cumulative basis, HDFC has approved 51 livelihood projects with a disbursement of Rs. 12.16 crore. The borrowing agencies, which act as social and financial intermediaries, range from professional micro-finance institutions (MFIs) to development NGOs to self-help group (SHG) federations. Until March 31, 2003, HDFC has covered over 35,000 EWS households, so far, and HDFC has experienced near 100% recoveries under the scheme.

Under the National Renewal Fund — Self Employed Women's Association (NRF — SEWA) component comprising a special grant of DM 2.4 million from KfW towards micro-enterprise development (Sanjivani Project), HDFC has disbursed as at March 31, 2003, a cumulative amount of Rs. 4.37 crore to SEWA Bank, Ahmedabad. The SEWA Bank has utilized the funds in disbursing 2470 loans to their women members, covering a variety of livelihood activities. The bank's cumulative disbursements under this project stood at Rs. 4.15 crore, with an average loan size of Rs. 17,000.

During the year KfW conducted an appraisal of the proposed Microfinance Refinance Facility (HDFC V, fifth line). As an outcome of which, bilateral funding of Euro 10 million has been committed, which includes a loan of Euro 9 million and the balance as a grant towards technical assistance (TA) and capacity building measures. In the first round of MFI selection,

11

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

out of the eight detailed appraisals carried out, four prominent Indian MFIs have been identified viz. Bharatiya Samruddhi Finance Ltd., Friends of

A woman’s World Banking, DHAN Foundation and the Indian Association for Savings and Credit (IASC). HDFC may include more MFIs in the program at a later stage. The Ministry of Economic Cooperation (BMZ), Federal Republic of Germany has also approved HDFC V; and the TA and capacity building measures are expected to commence shortly.

FUTURE

HDFC has always been market-oriented and dynamic with respect to resource mobilization as well as its lending Programme. This renders it more than capable to meet the new challenges that have emerged. Over the years, HDFC has developed a vast client base of borrowers, depositors, shareholders and agents, and it hopes to capitalize on this loyal and satisfied client base for future growth. Internal systems have been developed to be robust and agile, to take into account changes in the volatile external environment.

HDFC has developed a network of institutions through partnerships with some of the best institutions in the world, for providing specialized financial services. Each institution is being fine-tuned for a specific market, while offering the entire HDFC customer base the highest standards of quality in product design, facilities and service.

AWARDS HDFC Ranked as ‘India’s Third Best Managed Company’

by Finance Asia – 2005 Mr. Deepak Parekh awarded the 'Hall of Fame' award by

Outlook Money magazine. HDFC receives the 'Dream Home' award for the best

Housing Finance company for 2004 from Outlook Money magazine

Awards galore by HDFC at the 44th ABCI Awards!!! 5th Best Company to work for in India, ranked by

Business Today in November 2004 Economic Times Corporate Citizen of the Year Award,

November 2004 Rated by Deutsche Bank as one of the top 5

banks/Financial Institutions in Asia in October 2004

12

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

Ranked among the Top 20 companies to deliver healthiest returns to shareholders, Outlook Money Magazine - September 2004

1st Prize at the New York Festival's Gold Midas Awards for Environmental Communication Ad in August 2004

Features in the Forbes list of Top 20 Leading Indian Companies in May 2004.

One of the Top 10 Investor Friendly Companies, ranked by Business Today in March 2004.

HDFC Ranked No. 3 - 'India's Best Managed Companies' by Finance Asia

Clean Sweep by HDFC at the 43rd ABCI Awards!!! National Award for Excellence In Corporate Governance

by The Institute of Company Secretaries of India 2nd Best Company for Corporate Governance in India by

The Asset magazine. The Economic Times Lifetime Achievement Award -

2003. (For Mr. Deepak Parekh - Chairman, HDFC Ltd.) One of the Top Ten - Most Admired Companies in India '

- 2003 by Business Barons One of the Top Ten - Most Admired CEOs in India ' -

2003 by Business Barons ( for Mr. Deepak Parekh ) India's Second Best Managed Company - 2003 by

Finance Asia. India's Biggest Wealth Creator in the banking and

financial series by the fourth Business Today - Stern Steward Survey.

One of the Top Ten - Most Respected Companies in India' by Business world.

Highest rating for ' Governance and Value Creation ' by CRISIL.

One among the top ten ' Company Leaders in India' by the Far Eastern Economic Review Survey.

Best Managed Financial Institution in India' by fox Pitt Survey.

13

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

HDFC GROUP

14

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

The Standard Life Insurance Assurance Company

• Founded in 1825• Mutual Life Insurance Company since 1925• Largest mutual life insurance company in Europe• Assets under management over Rs 707836 crores (£ 89.2

bn) Total assets under management : Rs. 707836 Crores• New premium income 2003 :Rs. 76277 Crores• AA2 rated by Standard & Poor’s and Moody’s

Financial Strengths of the company

• Total assets under management: Rs. 5, 81,000 Crores

• New premium income 2001:Rs. 58,000 Crores

• AA2 rated by Standard & Poor’s and Moody’s

About Standard Life

Standard Life has been looking after its customers for over 180 years, and currently over 7 million people rely on them for their financial needs. We have assets under management which are worth more than the combined market value of Shell, Reuters, Tesco, Cadbury Schweppes and Marks & Spencer.

Financial Security

Standard Life has the financial strength to remain secure and competitive. We aim to offer products that provide competitive returns to their customers while maintaining an adequate level of financial strength to ensure their security. Like most people, you want to know that your financial future is in good hands. Standard Life places a great deal of importance on getting your money to work hard for you; that's why we believe you can have confidence in us.

15

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

Standard Life has been awarded the "Raising Standards" quality mark. This shows that we:

use clear language to describe their products on key documents,

have appropriate products and Provide a quality service for our customers.

The quality mark covers products bought by individuals including pensions, long-term savings and protection. We were independently tested against a number of rigorous standards. And we have to continue to pass these tests every year to keep using the quality mark.

Standard Life won the Money Marketing 'Company of the Year' award in March 2005 for the seventh year running. Other awards the Standard Life group has received include:

Money Marketing Awards Company of the Year every year from 1999 to 2005 Best Pension Provider 2004 and 2005 Best Group Pension Provider every year from 1998 to 2003 Best Personal Pension Provider every year since 1998 to

2003 Best Life Investment Product Provider 2003 and 2004 Gold Award in the Poster Campaign Category (Advertising)

2004

Money facts Investment, Life & Pensions Awards Best Pension Product 2003, 2004 and 2005 Best Pension Service 2003, 2004 and 2005

Bank hall Achievement Awards Pension Provider of the Year 2003 and 2004

Financial Adviser Provider Awards Overall Winner in 1999, 2000, 2001 and 2002 Pensions Provider of the Year 1999, 2000, 2001, 2002 and

2003 Pensions Company of the Year 2004 Individual Pensions Company of the Year 2004 Group Pensions Provider of the Year 2004 Health Insurance Company of the Year 2004

Financial Adviser Service Awards Company of the Year every year from 1997 to 2001

16

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

5 Star Life and Pensions Provider every year from 1996 to 2004

5 Star Investment Provider every year from 1996 to 2002 and 2004

Pensions Management Administration and Service Awards

Overall Winner - Personal Pensions 2003 Overall Winner - Stakeholder Pensions 2002 and 2003 Overall Winner - Group Personal Pensions 2002 and 2004 Member Communications - Personal Pensions, Group

Personal Pensions & Stakeholder Pensions 2003 Backup (branch office) - Personal Pensions 2003 Backup (head office technical support) - Personal Pensions

& Stakeholder Pensions 2003

Pensions Management Technology Awards Best extranet accessibility 2004

Guardian & Observer Consumer Finance Awards Overall Winner in Personal & Stakeholder Pension

Provider 2003

Professional Adviser Awards Best Product Provider Website (adviser zone) 2005

Online Finance Awards Best online Product Provider (ifazone) 2003 Best online Financial Adviser (ifazone) 2002

Head Office - Edinburgh, Scotland (UK)

Presence

United Kingdom: 31 branches

Canada 11 "

Ireland 7 "

Germany 1 "

Austria 1 sales office

Spain 31 branches

Hong Kong 1 representative office

17

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

China 2 representative office

Year Award

• 2003 Company of the Year• 2002 Company of the Year• 2001 Best Personal Pension Provider• 2000 Company of the Year• 1999 Company of the Decade• 1996-99 Company of the year• 1995 4 star service award• 1992-94 Overall best company• 1991 3 star service award• 1990 Best mortgage services

18

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

History of Joint Venture

• Discussions commenced - January 1995

• Joint venture agreement signed - October 1995• Joint venture agreement renewed - October 1998• Life Insurance project team established - January 2000

(Mumbai)• Company officially incorporated - 14th August 2000• First private sector Life Insurance company to be granted

a certificate of registration - 23 October 2000• Shareholding - HDFC 81.4 %

Standard Life 18.6 %

The Partnership:

HDFC and Standard Life first came together for a possible joint venture, to enter the Life Insurance market, in January 1995. It was clear from the outset that both companies shared similar values and beliefs and a strong relationship quickly formed. In October 1995 the companies signed a 3 year

Joint venture agreement

Around this time Standard Life purchased a 5% stake in HDFC, further strengthening the

Relations

19

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

The next three years were filled with uncertainty, due to changes in government and ongoing delays in getting the IRDA (Insurance Regulatory and Development authority) Act passed in parliament. Despite this both companies remained firmly committed to the venture.

In October 1998, the joint venture agreement was renewed and additional resource made available. Around this time Standard Life purchased 2% of Infrastructure Development Finance Company Ltd. (IDFC). Standard Life also started to use the services of the HDFC Treasury department to advise them upon their investments in India.

Towards the end of 1999, the opening of the market looked very promising and both companies agreed the time was right to move the operation to the next level. Therefore, in January 2000 an expert team from the UK joined a hand picked team from HDFC to form the core project team, based in Mumbai.

Around this time Standard Life purchased a further 5% stake in HDFC and a 5% stake in HDFC Bank.

In a further development Standard Life agreed to participate in the Asset Management Company promoted by HDFC to enter the mutual fund market. The Mutual Fund was launched on 20th July 2000.

Incorporation of HDFC Standard Life Insurance Company Limited:

The company was incorporated on 14th August 2000 under the name of HDFC Standard Life Insurance Company Limited.

Their ambition from as far back as October 1995 was to be the first private company to re-enter the life insurance market in India. On the 23rd of October 2000, this ambition was realized when HDFC Standard Life was the only life company to be granted a certificate of registration.

HDFC are the main shareholders in HDFC Standard Life, with 81.4%, while Standard Life owns 18.6%. Given Standard Life's existing investment in the HDFC Group, this is the maximum investment allowed under current regulations.

HDFC and Standard Life have a long and close relationship built upon shared values and trust. The ambition of HDFC Standard Life is to mirror the success of the parent companies and be the yardstick by which all other insurance company's in India are measured.

20

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

Their Mission:

They aim to be the top new life insurance company in the market.

This does not just mean being the largest or the most productive company in the market, rather it is a combination of several things like-

Customer service of the highest order Value for money for customers Professionalism in carrying out business Innovative products to cater to different needs of different

customers Use of technology to improve service standards Increasing market share

Their Values:

SECURITY: Providing long term financial security to policy holders will be their constant Endeavour. We will be doing this by offering life insurance and pension products.

TRUST: We appreciate the trust placed by their policy holders in us. Hence, we will aim to manage their investments very carefully and live up to this trust.

INNOVATION: Recognizing the different needs of their customers, we will be offering a range of innovative products to meet these needs.

Their mission is to be the best new life insurance company in India and these are the values that will guide us in this.

21

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

METHODOLOGY

Part- 1 Visiting Different Mutual Funds Companies, for the complete knowledge of Mutual Funds and all of their provisions

Part - 2 Visiting insurance companies and to compare their Unit linked plans as per HDFC plans and to make a final comparison with the Mutual Funds.

Part – 3 Conducting a Survey of various people

APPROACH

Study is divided into 3 parts:

Data collection

Survey

Comparative Study

DATA COLLECTION

PRIMARY DATA SOURCES

A visit was made to Mutual Funds companies and knowing their

investment plans. Visited the company as a customer and asked

for their good schemes and about their ROI.

The companies covered were:

HDFC Mutual Funds ICICI Mutual Funds India Bulls Franklin Templeton

Collected the Brochures from Four Insurance companies and

compared their Unit Linked endowment plans

22

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

The Companies covered are

o HDFC Standard Life

o ICICI prudential

o Birla Sun Life

o Max New York Life

A Survey was conducted in NCR region from 100 people and we asked about their interest in investment in mutual funds or unit linked plansThe survey said

o 62 percent people said that they want to invest in Unit Linked Policies

o 27 percent people said that they want to invest in Mutual Funds

o 8 percent people said they don’t want to invest in private companies they just want to go with LIC traditional Plans as they don’t want to bear risk.

o 3 percent people said they want to invest in both the companies as they want to invest small amounts in all companies.

SECONDARY DATA SOURCES:

Websites was the Secondary data source

1. www.investopedia.com 2. www.hdfcinsurance.com 3. www.valueresearchonline.com 4. www.mutualfundsindia.com 5. www.amfiindia.com 6. www.hdfcmutualfunds.com

23

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

CONCEPT OF INSURANCEInsurance is aimed at compensating the financial loss suffered on the happening of an insured event. Insurance cannot prevent the happening of the event; however it can protect a person from the financial losses he may suffer after the happening of the event.

The above can be understood with the help of a simple example.

Example 1:In case a person has a car worth Rs 5, 00,000 and he insures the car for Rs 5, 00,000. In the event of a loss of Rs 1, 00,000 during the term of the insurance, he would be compensated the amount lost of Rs 1, 00,000. Although the insurance is for Rs 5, 00,000 the person cannot be paid more than Rs 1, 00,000 as this is the loss he has suffered. In case the insurance company pays more than the financial loss suffered by the policyholder then there is an incentive to the policyholder to make claims and make profits. This will increase in the premium amounts and in case all the policyholders claim losses then the insurance would be un-viable. Thus to protect the interests of all the group of policyholders the insurance offered is only to the extent of the financial loss suffered by the policyholder. Insurance is therefore only a compensation of a financial loss.

Example 2:In case a person has a car worth Rs 5, 00,000 and he insures the car for Rs 10, 00,000 (over insurance). In the event of a loss of Rs 1,00,000 during the term of the insurance the person cannot be compensated more than the amount of loss i.e. Rs 1,00,000 in this case.

In case the policyholder is paid double the amount lost because he has insured for double the value, then he would make a profit. Profit would act as an inducement for the person to go for over-insurance to a large extent. This would mean that the whole group of policyholders pays for the profits made by one policyholder. More the number of policyholders who make such profits the more un-viable the insurance would become. Hence in insurance it is an established principle that even in case of over-insurance the policyholder would not be paid more than the loss suffered by him.

24

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

Example 3In case a person has a car worth Rs 5, 00,000 and he insures the car for Rs 2, 50,000 (under-insurance). In the event of a loss of Rs 1, 00,000 during the term of the insurance, the person would be compensated an amount of Rs 50,000 only.Whenever a person buys a car he is on risk. Any event like a theft, fire, riot, and earthquake can happen and destroy the car or cause a financial loss to him. In case he is not insured then he has to bear the loss himself. The maximum amount of such loss that can occur to him is the value of the car, which in this case happens to be Rs 5, 00,000.When a person buys the insurance, he actually transfers the risk, which he possesses, to the insurance company. Once insurance is granted to him the insurance company would pay in the event of the loss. As seen above the maximum amount of risk the person possesses is the value of the car. In case he insures for less than the value, what the person actually does is that he transfers a portion of the risk to the insurance company. In the given example the person has chosen to transfer half the risk to the insurance company. Thus in the event of the loss the person would be compensated only half the amount of loss. The reason being he chose to insure only half of the risk to the insurance company.

Subject matter of insurance:When a person insurance his car the subject of the insurance is the car. What the insurance company guarantees is that in the event of a financial loss due arising due to an insured event then the company would compensate to the extent of the loss subject to the condition that the person has adequately insured the car.

In Life insurance what is the subject matter? Or what is covered in life insurance.

Surely it cannot be death because death cannot be compensated. It cannot be life either, as life too cannot be compensated.Life insurance aims to compensate the ‘Income Earning Capacity’ of the person. In this session we are only talking of pure insurance or Term Assurance and not of any savings, investment or retirement plan.

25

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

Events covered in life insuranceIn Life Insurance we cover the Income Earning Capacity. The loss of the Income Earning Capacity can be lost on the happening of the following events.

1. Death of the life assured2. Sickness of the life assured (critical illness)3. Accident of the life assured (death or permanent disability

due to accident)4. Retirement of the life assured

Death of the life assured can destroy the income earning capacity of the individual. When a person takes a life insurance (pure insurance) with the sum assured payable on death he protects his family from the loss of income earning capacity due to death. A Life Insurance company does not pay money to the family because the life assured has died, but because the family has lost the income earning capacity. Death itself is not covered. The loss of income earning capacity due to death is covered in life insurance.

It is often felt that life insurance means only death insurance. This is not true. Life insurance is insurance against the loss of the income earning capacity of the person. Sickness (critical illness only) can affect an income earning capacity of an individual. Life insurance offers protection for the loss of income earning capacity due to a sickness. Since minor ailments do not permanently destroy the income earning capacity of an individual the minor ailments are not covered in life insurance. Insurance against critical illnesses pay not because the person has contracted a critical illness, but because the person has lost his income earning capacity due to the critical illness.

Similar is the case with accident cover. All accidents are not covered only those accidents, which result in death or permanent disability of the life assured, are covered in life insurance. The payment is not made because the person has met with an accident, but the payment is made because a person has lost the income earning capacity due to an accident.

Retirement on the other hand is a certain event. A certain event cannot be insured at all. The only alternative left for the person is to save for retirement. All the lives assured would definitely retire hence insurance cannot be offered for retirement. Income earning capacity is affected on retirement. The retirement plans are therefore savings plans, which help a person, save for the retirement.

26

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

It is important that we understand some of the terms frequently used in Insurance. The following gives a brief description of what we mean by risk, peril and a hazard.

Risk It is a possibility of a loss. The loss may occur or may not occur if there is a possibility of a financial loss we can say that a risk exists. When a person has an income there is a risk of the loss of the income. Similarly in case a person owns a car there is a risk that the car may be destroyed or damaged by fire, riots, strike, lightening etc.

PerilIt is the cause of the loss. The income earning capacity may be destroyed by death. Death in this case is the peril. Similarly fire, theft, earthquake are perils in car insurance.

HazardThis is the condition that creates or increases the chance of the loss. An existing sickness is a condition that may cause death of the life assured at a future date. The existing sickness would be a hazard in life insurance.

Risk is not avoidable. In case a person has income then there is a risk of loss of that income. The person has the choice to deal with the risk in the following manner:1. Avoidance2. Reduction3. Retention4. Transfer5. Sharing

Insurance is a means of sharing of the risk. All the policyholders agree to share the losses suffered by a few of the unfortunate policyholders. Since who is going to suffer the loss is not known all the policyholders are protected in case they are the victims of the insured event.

All the risks cannot be insured. Only the risks, which satisfy the following criteria, can be insured. There has to be a large numbers of exposure units for the

risk to be insured The loss occurred due to the risk should be definite and

measurable The loss must be fortuitous The loss must not be catastrophic

27

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

The losses due to the risk should be on suffered by the group of policyholders on random

The risk cover should be economically viable

The following are the limitation of insurance All risks cannot be insured There must be insurable interest Insurance is limited to the financial value There must be large number of similar risks It must be possible to calculate the risk of loss Losses should not be catastrophic Losses must not be too small Losses must be reasonably unexpected Losses must be accidental It must be consistent with public policy

The following are the differences between life insurance and non-life insurance

Risk (possibility of a loss) is certain in life insurance. Every person who is insured is likely to die, and death would completely destroy the income earning capacity. In non-life insurance the risk is uncertain and the insured event may or may not result in the loss to the policyholder.

Life insurance is a long term contract while non-life insurance contracts are one year contracts.

Difficulty in determining value of human life in life insurance. In non-life insurance the value can be determined with much ease.

Life insurance is not a strict contract of indemnity. Non-Life insurance contracts are strict indemnity contracts.

28

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

WHY INSURANCE

Life Insurance has come a long way from the earlier days when it was originally conceived as a risk covering medium for short periods of time, covering temporary risk situations, such as sea voyages. As life insurance became more established, it was realized what a useful tool it was for a number of situations, including -

a) Temporary needs / threats:

The original purpose of life insurance remains an important element, namely providing for replacement of income on death etc.

b) Regular Savings:

Providing for one's family and oneself, as a medium to long term exercise (through a series of regular payment of premiums). This has become more relevant in recent times as people seek financial independence for their family.

c) Investment:

Put simply, the building up of savings while safeguarding it from the ravages of inflation. Unlike regular saving products, investment products are traditionally lump sum investments, where the individual makes a one off payment.

d) Retirement:

Provision for later years becomes increasingly necessary, especially in a changing cultural and social environment. One can buy a suitable insurance policy, which will provide periodical payments in one's old age.

An example to understand the need for insurance:

Mr. Atul is 45 and self-employed. His wife Nandini, who is a housewife, looks after their two children aged 3 and 7 years. They stay in a rented accommodation, where the rent is 15,000 rupees per month. Mr. Atul has taken up a loan of Rs. 2 lakh. His monthly earnings on average are 40,000 rupees. Mr. Atul passes away in an unfortunate road accident. What are some of the financial implications of his death on his family?

29

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

There may be several financial implications on his family. Some of these are:

a) The monthly income, previously provided by Mr. Atul would stop.

b) His wife and children may have to seek financial assistance from other relatives.

c) His wife may not have enough money to pay back the loan of Rs. 2 lakhs.

d) The family may have to move into a cheaper accommodation.

e) His widow may have to take up work to earn money.

f) The education of his children may suffer.

This simple example illustrates the impact premature death can have on a family, where the main earner has no life cover.

Had Mr. Atul taken life cover, his family would not have faced such hardships in the event of his unfortunate death. A simple life insurance policy could have provided Mr. Atul's family with a lump sum that could have been invested to provide an income equal to all or part of his income.

In simple words, insurance protects against untimely losses. Insurance has been found useful in the lives of persons both in the short term and long term. Short term needs like sudden medical costs and long term needs like marriage expenses etc can be met with using life insurance.

Life Insurance ProductsTo understand the difference between life insurance products and insurance the analogy of medical science works well. The following points can be made while explaining the concepts of products and insurance.

The difference between an agent and a consultant can be brought about by an analogy of a chemist and a doctor. A chemist is interested in selling medicines but not qualified to advise. He knows the medicines but is not good at diagnosis and prescription.

A doctor on the other hand is a person qualified to advise and prescribe medicines. The doctor is not interested in selling medicines but is more interested in curing the client.

There is a difference in the training of the chemist and the doctor. A chemist studies chemistry and then studies the

30

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

composition of the medicines and knows the manufactures of the medicines. He has to ensure that he gives the right medicines, which is prescribed by the doctor.

On the other hand the doctor studies the human body and also studies the diseases. He has to understand the symptoms and then studies the effect of the medicines on the symptoms. He also knows the medicine and the compositions and is qualified to advice.

When you are sick you need to take medicines. However taking any medicine would not work. What is important is that you consume the medicine designed to cure the ailment you are suffering from. The medicines are also to be consumed taking into account the body constitutions. Hence different people have to take different medicines as per their body constitution.

There are certain limitations in medicines. One cannot consume medicines for the rest of one’s life. One medicine cannot cure all the diseases. Medicines can be administered in more then one methods. Medicines can be made attractive by sugar coatings but the sugar coatings do not improve the medicine but only increase the price of the medicine.

Products of life insurance are like medicine. Taking one policy is just not enough. It is important that the policy satisfies a need of the client. Life Insurance products are designed to satisfy a particular need of the client. When the product is sold as per the need of the client the product will be effective to satisfy the need of the client.

There is no one product that satisfies all the need of the client. What a consultant needs to do is to make a combination of products so that he can satisfy the need of the client. Besides the financial circumstances of the client may dictate the insurance plans that the client needs to take. A consultant should note the financial condition of the client and suggest a plan as per the need of the client.

The insurance needs of the clients keep on changing over a period of time and the consultant should help the client review his insurance needs periodically. Insurance is not a one-time affair. The consultant should build a relationship with the client and periodically help him review his insurance and suggest policies best suited to the needs of the client.

One insurance policy cannot satisfy all the insurance needs of the client. A combination of the insurance policies can offer the insurance that a client needs. Consultants should suggest the best combination for the clients after analyzing the needs of the client. Simply suggesting a combination of the plans without analyzing the needs of the client is not correct and not in the interest of the client or the consultant.

31

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

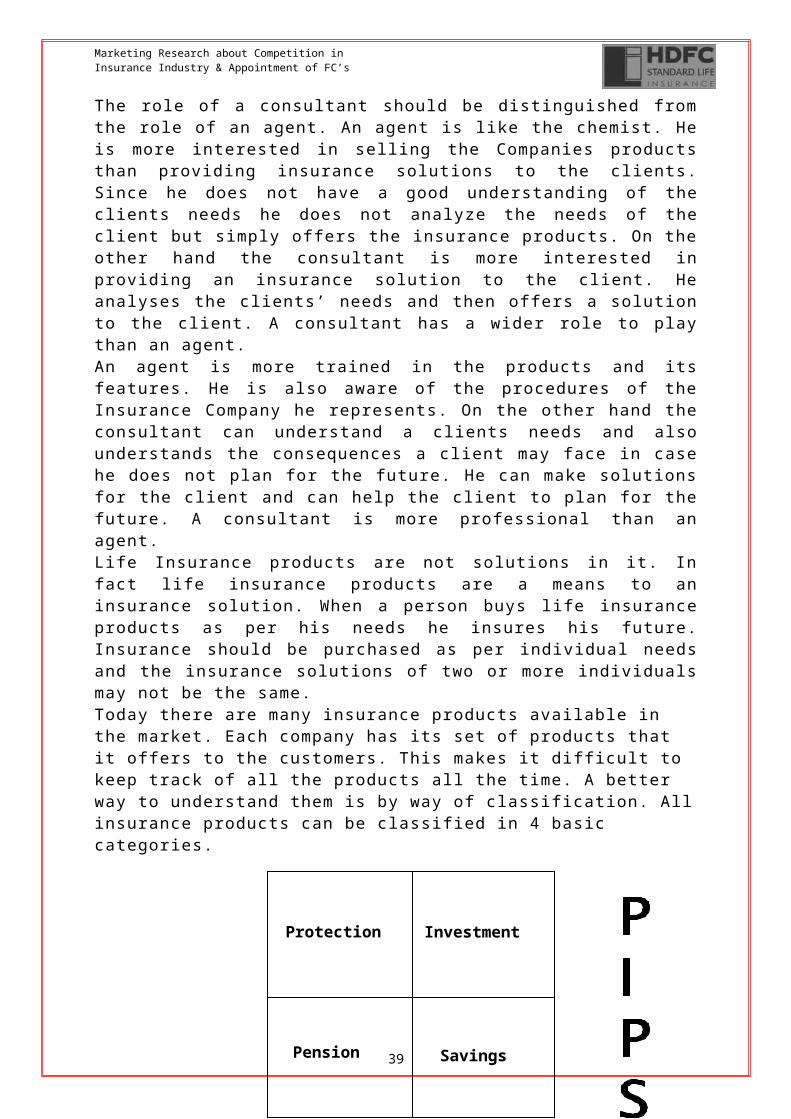

Additional features in an insurance product make the insurance product look attractive; however the features may be immaterial to the satisfaction of the clients needs. The client also has to pay a price for the additional feature as no feature in any insurance comes free. The consultant should bring this to the notice of the client in case the client is insisting on some additional feature.The role of a consultant should be distinguished from the role of an agent. An agent is like the chemist. He is more interested in selling the Companies products than providing insurance solutions to the clients. Since he does not have a good understanding of the clients needs he does not analyze the needs of the client but simply offers the insurance products. On the other hand the consultant is more interested in providing an insurance solution to the client. He analyses the clients’ needs and then offers a solution to the client. A consultant has a wider role to play than an agent.An agent is more trained in the products and its features. He is also aware of the procedures of the Insurance Company he represents. On the other hand the consultant can understand a clients needs and also understands the consequences a client may face in case he does not plan for the future. He can make solutions for the client and can help the client to plan for the future. A consultant is more professional than an agent.Life Insurance products are not solutions in it. In fact life insurance products are a means to an insurance solution. When a person buys life insurance products as per his needs he insures his future. Insurance should be purchased as per individual needs and the insurance solutions of two or more individuals may not be the same. Today there are many insurance products available in the market. Each company has its set of products that it offers to the customers. This makes it difficult to keep track of all the products all the time. A better way to understand them is by way of classification. All insurance products can be classified in 4 basic categories.

32

Protection Investment

Pension Savings

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

This classification is based on the needs of the customers. Accordingly each of these categories has an end need to be satisfied and all the products coming under that category aim to fulfil that need e.g. Products coming under Investment category aim to provide long term real growth over the period. Thus understanding these categories will not only help us to understand various products but also help us to position our products strongly in a competitive market. Let us take a look at the distinctive features of each category:

Protection type of products: A typical protection type of product aims at protecting income-earning capacity of the customers on happening of uncertain events mentioned above during the term of product. These are the pure risk products having no savings element. Naturally, these products don’t have any maturity benefits. High-risk cover at low costs is the unique feature of this type that makes this category most attractive for the prospects who want high insurance cover without spending much for it. Usually offered for a definite term, mainly the Term Assurances come under this type. Various riders offered by different companies are also a part of protection category. The claim is paid only if the stipulated event happens otherwise there are no maturity values at the end of the term. There are some variations in protection products with refund of premiums, where some part of the premium has a savings component.

6. Investment type of products: In investment type of products, the focus is on maximizing returns for the customer over a period time. In a way, it is opposite to Protection type where the focus is maximizing the risk cover. Here the risk cover is very low. The objective is to put maximum in investments. The underlying principle is to commit money for a certain period of time and get the benefits of real long-term growth. The products are usually single premium policies where the entire premium is collected in advance. Surrenders are discouraged and there is a commitment for certain minimum no of years. In death during the term, value of the investments is returned.

7. Pension products: Along with the risk of an untimely death or disability, we also have a risk of living too long – outliving our source of income. In other words, one needs to ensure that he gets a decent income even after his

33

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

retirement and continues to get it as long as he lives! This is where we have pension products addressing the need for a comfortable retirement. One can opt for an immediate pension or for pension at a future date (also called as deferred pension). There is a range of options that one can have when selecting a pension plan. There is a great amount of flexibility when it comes to selecting a pension product. The important point to be noted is that Pensions is a part of one’s present income that he reserves for future consumption. Every year that income is accumulated and invested. The lump sum accumulation then is used for purchasing pension on the vesting date.

8. Savings type products: People in India like to save. Our savings rate has been well above 20% of our GDP for last few years. We save for events like children’s’ marriage, education etc. Savings types of products aim to strike a good balance between risk cover as well as returns. It acts as a protection on savings. Sum assured is usually the targeted savings that one looks for. He gets that amount at the end of the term along with bonuses if it is a participating policy. On the protection side if any unfortunate event happens during the term, the sum assured (in other words the targeted savings) is still paid. So it encourages a person to save for an event at the same time ensures that his savings are protected. This is the unique advantage of savings through life insurance that no other savings product offers. We find very popular products like Endowment Assurance; Money Back plans in this category.

As stated earlier all the products come under these 4 broad categories. To understand a product, it is essential to find out the category of that product based on its features. Needless to say that it will not be possible to compare one category product to another. Each category is unique and caters to particular needs of the customer. The best approach is to find out what customer needs and then suggest a solution accordingly.

The products launched by HDFC Standard Life can be classified as follows

34

Term Assurance and Loan Cover Term Assurance

Single Premium Whole of Life

Insurance

Personal Pension Plan

Endowment Assurance

Money back PlansChildren’s Plan

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

Protection Products – Term Assurance and Loan Cover Term Assurance PlanInvestment Product – Single Premium Whole of Life Insurance PlanPension Product – Personal Pension PlanSavings Product – Endowment Assurance, Money Back Plan and Children’s Plan

1. ROI ROI is more in Mutual funds, if customer deals properly with the equity, and invest in good funds

ROI is not fixed but equivalent in all plans and this is approx figures, no one can assure for returns.

Comparasion of Mutual Funds and ULIP on 10% Return Basis

0

1000000

2000000

3000000

4000000

5000000

6000000

7000000

8000000

0 1 2 3 4 5 6 7 8 9 101112131415161718192021222324252627282930

Years

Rs HDFC SL

Mutual Funds

AS per the survey Conducted for the People who are interested in Mutual Funds or Unit Linked Insurance Plans. Most of the Customer said that they will prefer for the Unit Linked insurance Plans as they are provided with Risk Cover also and even they are having the same facilities as per the mutual funds, and in long runs they are successful. As ULIP are the plans by the insurance companies and they invest the funds in AAA rated companies only, And they provide some riders also which are very beneficial to the customers.

Now the Survey was conducted for 100 people where the Results Are

35

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

o 62 percent people said that they want to invest in Unit Linked Policies

o 27 percent people said that they want to invest in Mutual Funds

o 8 percent people said they don’t want to invest in private companies they just want to go with LIC traditional Plans as they don’t want to bear risk.

o 3 percent people said they want to invest in both the companies as they want to invest small amounts in all companies.

Start early, save moreEven if you invest less every month !

Rs3,00,000

Rs.12,23,459

Rs.3,75,000

Rs.7,33,107

When you invest Rs.10,000 annuallyfor 30 year period(from age 31 to 60)

When you invest Rs.25,000 annuallyfor 15 year period(from age 41 to 60)

If you invest early ! If you invest late !

Investment Retirement Savings

Market Factoid

1. The growth options of ULIP have recorded annualized returns of over 20 per cent.

2. Various charges amounting to approximately 25 per cent in the initial years in all the schemes.

3. Most companies normally allow customers to switch, a fixed number of times annually from one fund to other fund. Later, they charge approximately Rs.100 per switch.

36

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

4. Private insurance companies 50 per cent sales up because of ULIPs today.

5. Individuals availing tax exemption under section 88 of Income Tax Act.

6. New Schemes coming into the market, which covers life insurance and accident insurance.

37

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

SURVEY REPORT FOR THE CUSTOMER’S PERCEPTION FOR THEIR AWARENESS OF INSURANCE PRODUCTS (ULIP) AND MUTUAL FUNDS AND THE BUYING PREFERENCE.

As per the Questionnaire, I conducted a survey of 100 People and asked about their awareness of private insurance companies and the companies they know. So the form consisted of 6 companies’ option and each customer gave different views, now as per the survey reports…..

o ICICI Prudential 20%o Birla Sun Life 15%o HDFC Standard Life 15%o Bajaj Allianz Life 13%o Tata Aig Life 10%o Aviva Life 7%o Max New York Life 6%

HDFC SL

ICICI PRU

METLIFE

MNYL

TATA AIG

SBI LIFE

ROYAL SUNDARAM

AVIVA

ING VYSYA

BAJAJ ALLIANZ

BIRLA SUN LIFE

AMP SANMAR

OM KOTAK

SAHARA LIFE

People Aware about the Private Insurance Companies as per the conducted Survey

38

o ING Vysya 4%o SBI Life 4%o Metlife 2%o Om Kotak 2%o Royal Sundaram 1%o AMP Sanmar 1%o SAHARA Life 0%

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

Out of Hundred People the Profession of the people are as Follows

12

15

1927

5

7

15

Doctors

Engineers

Business Man

Service Class People

House Wife

Chartered Accountant

Misslenous

Income of People According to the Survey

0

5

10

15

20

25

30

35

40

Less Then 1,00,000 1,00,000 - 2,00,000 2,00,000 - 5,00,000 Above 5,00,000

INCOME

Status of insurance Cover for the Persons according to the Survey

39

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

US $

199419951996199719981999 2000200120022003

Years

World Life and Non Life Insurance Premiums

Nonlife

Life

Total

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

19%

10%

65%

6%

Only LIC Only Private Insurance Company

Both Insurance Companies No Policy

GLOBAL SCENARIO

WORLD LIFE AND NON LIFE INSURANCE PREMIUMS

Year Nonlife Life Total

1994 846,600 1,121,186 1,967,786

1995 906,781 1,236,627 2,143,408

1996 909,100 1,196,736 2,105,836

1997 896,873 1,231,798 2,128,671

1998 891,352 1,275,053 2,166,405

1999 912,749 1,424,203 2,336,952

2000 926,503 1,518,401 2,444,904

2001 969,945 1,445,776 2,415,721

2002 1,098,412 1,534,061 2,632,473

2003 1,268,157 1,672,514 2,940,671

40

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

41

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

The basic human trait is to be averse to the idea of taking risks. There is always an

urge to minimise the risks and take protection against possible failure. The risk

includes fire, death, accidents, etc. Any risk may be insured against at a premium

commensurate with the risk involved. Thus collective bearing of risk is insurance.

Insurance, whether life or non-life, provides people with a reasonable degree of

security and assurance that they will be protected in the event of a calamity or failure

of any sort.

Indian insurance sector is witnessing exciting challenges, forcing companies to

continuously innovate. Companies are under taking initiatives aimed at business

process re-engineering, enterprise resource planning, customer relationship,

breakdown of traditional organisational hierarchies besides introducing innovative,

customer oriented insurance products. Service is becoming the source of gaining and

retaining corporate leadership in the insurance business. Times have changed a lot

since Triton insurance company has, was the first general insurance company to be

established in India in 1850.

The liberalised business environment led to competition in insurance sector also,

which has helped ensure quality service to the customers besides spreading the

market share.

42

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

INSURANCE MARKET IN INDIA

By any yardstick, India, with about 300 million middle class households, presents a

huge untapped potential for players in the insurance industry. Saturation of markets

in many developed economies has made the Indian market even more attractive for

global insurance majors. (Table 1 in appendix reflects the low percentage and per

capita penetration of insurance in India compared to other developed and developing

countries.)

7

With the per capita income in India expected to grow at over 6% for the next 10 years

and with improvement in awareness levels, the demand for insurance is expected to

grow at an attractive rate in India. An independent consulting company, The Monitor

Group has estimated that the life insurance market will grow from Rs.218 billion in

1998 to Rs.1003 billion by 2008 (a compounded annual growth of 16.5%).

Winds of Change

Reforms have marked the entry of many of the global insurance majors into the

Indian market in the form of joint ventures with Indian companies. Some of the key

names are AIG, New York Life, Allianz, Prudential, Standard Life, Sun Life Canada

and Old Mutual. The entry of new players has rejuvenated the erstwhile monopoly

player LIC, which has responded to the competition in an admirable fashion by

launching new products and improving service standards.

The following are the key winds of change brought about by privatisation.

Market Expansion: There has been an overall expansion in the market. This has

been possible due to improved awareness levels thanks to the large number of

advertising campaigns launched by all the players. The scope for expansion is still

unlimited as virtually all the players are concentrating on large cities and towns -

except by LIC to an extent there was no significant attempt to tap the rural markets.

New Product Offerings: There has been a plethora of new and innovative products

offered by the new players, mainly from the stable of their international partners.

Customers have tremendous choice from a large variety of products from pure term

43

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

(risk) insurance to unit-linked investment products. Customers are offered unbundled

products with a variety of benefits as riders from which they can choose. More

customers are buying products and services based on their true needs and not just

traditional money-back policies, which is not considered very appropriate for long-

term protection and savings.

Customer Service: Not unexpectedly, this was one area that witnessed the most

significant change with the entry of new players. There is an attempt to bring in

international best practices in service and operational efficiency through use of latest

Technologies. Advice and need based selling is emerging through much better

trained sales force and advisors. There is improvement in response and turnaround

times in specific areas such as delivery of first policy receipt, policy document,

premium notice, final maturity payment, settlement of claims etc. However, there is a

long way to go and various customer surveys indicate that the standards are still

below customer expectation levels.

Channels of Distribution: Till three years back, the only mode of distribution of life

insurance products was through Agents. While agents continue to be the

predominant distribution channel, today a number of innovative alternative channels

are being offered to consumers. Some of them are banc assurance, brokers, the

internet and direct marketing. Though it is too early to predict, the wide spread of

bank branch network in India could lead to banc assurance emerging as a significant

distribution mechanism.

Though the market expansion has taken place, channel of distribution has increased

and customer service is becoming the priority but still much has to be done as

services are intangible, produced and consumed simultaneously and often less

standardized than goods. These unique characteristics present special challenges

and strategic marketing opportunities to the service marketers. The real competition

between the service marketers was set after globalisation of the Indian economy the

service marketing organisation has to adopt professional Management and its

marketers have to imbibe the qualities of professionalism in order to meet the

expectations of the customers.

44

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

Customers are now looking at insurance as complete financial solutions offering

stable returns coupled with total protection. Companies will need to constantly

innovate in terms of product development to meet ever changing consumer needs.

Understanding the customer better will enable insurance companies to design

appropriate products, determine price correctly and increase profitability. In the

present scenario, a key differentiated would be professional customer service in

terms of quality of advice on enhancing customer convenience.

According to one of the survey published in Indian Journal of marketing, 44 percent

Respondents buy insurance to avoid tax; their major source of awareness is from

friends. From the study it is observed that majority of the respondents are willing to

take new policies in new companies. This suggests that most respondents are not

happy with their existing company. Hence in this project study, an attempt has been

made to understand the marketing strategies that are prevalent now and suggestions

have been made to improve those strategies. Various factors that affect the

marketing of insurance services have also been touched.

45

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

EMERGENCE OF INSURANCE

Life insurance started in India about 200 years ago. The growth of the managing

agencies system has been ascribed to the life insurance companies set up by the

free merchants and the agency houses. Like insurance companies started in Calcutta

and catered largely to the civil and military officers and European merchants.

The Bombay Mutual Insurance society was started on immediate basis in the 1870s.

The Oriental government security life Insurance company grew into the largest in Life

Insurance Company. It was headed for many years by Sir Purshottam Das Thakur

Das, who held director shit in over 60 companies, and was the President of the East

India Cotton Exchange for many decades. Bharat Insurance was started in Lahore

and was controlled by Lala Harkishan Lal before it was taken over by the Dalmias in

1933. Lakshmi insurance company was all so Lahore - based and was started by

Lala Lajpat Rai. The Hindustan co-operative was pioneered by Sir NR Sircar in

Calcutta. Another large Calcutta - based company was the National Insurance

Company which was eventually taken over by a JK Singhania. The Birlas started new

Asiatic and Ruby. Till 1939, there was no restriction on life Insurance company

investments and the large business house is utilised their funds for the expansion

and diversification of their trading and industrial interest. The Tatas had founded the

New India Assurance Company in 1919.

The garment of India decided to nationalise life insurance and the life Insurance

Corporation (LIC) was set up in 1956. The second five - EA a plan had just started

and the nationalisation of the Imperial Bank of India and life Insurance Corporation

provided reforms for the large capital investment for the second plan investments.

About 75 percent of the life Insurance Corporation (LIC) funds are invested in the

public sector. A sizeable amount is also invested in foreign countries, in government

securities, debentures and share has and loans to public bodies. Since 1955, with a

marked fall in mortality, there has been a persistent demand for a reduction in the

46

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

premium rates. The Morarka committee's recommendations resulted in a slight

Reduction in the premium rates for without profit policies and some increase in

bonus; the expense ratio remains very high and the rates for policies with profits are

largely unchanged. The service has deteriorated; now there was a move to spread

the corporation into a number of zonal companies. The Insurance regulatory Act

provided for 26 percent foreign participation in life and general insurance area has

now. A number of leading foreign insurance companies, both life and general or

setting up joint ventures with some of the leading Indian houses to enter the

insurance field which holds good growth potential. The life Insurance Corporation is

the biggest investor in the country. Its total investment in 1978 - 79 amounted to

Rs.7, 386.2 million and has grown several fold in the 1980 s and 1990 s.

The General Insurance Corporation (GIC) was formed after the nationalisation or

General Insurance in 1971. The activities other than allegiance Corporation and its

subsidiaries cover all kinds of insurance (except of human life). It has integrated

Annan's seven private companies into just four subsidiaries, viz., National Insurance

company, Calcutta's; New India Assurance, Mumbai; Oriental fire and General

Insurance, New Delhi; and United India Insurance, Chennai. In January 1979, the

Corporation announced a premium relief of over rupees 280 million, which resulted

from a reduction of 20 percent in the premium rates for fire insurance.

OPENING OF INSURANCE SECTOR

In line with the economic reforms that were ushered in India in early nineties, the

Government set up a Committee on Reforms (popularly called the Malhotra

Committee) in April 1993 to suggest reforms in the insurance sector. The Committee

recommended throwing open the sector to private players to usher in competition

and bring more choice to the consumer. The objective was to improve the

penetration of insurance as a percentage of GDP, which remains low in India even

compared to some developing countries in Asia.

47

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

Reforms were initiated with the passage of Insurance Regulatory and Development

Authority (IRDA) Bill in 1999. IRDA was set up as an independent regulatory

authority, which has put in place regulations in line with global norms. So far in the

private sector, 12 life insurance companies and 9 general insurance companies have

been registered.

Rationale for opening of insurance sector

A thriving insurance sector is of vital importance to every modern economy. First

because it encourages the savings habit, second because it provides a safety net to

rural and urban enterprises and productive individuals. And perhaps most importantly

it generates long-term investible funds for infrastructure building. The nature of the

insurance business is such that the cash inflow of insurance companies is constant

while the payout is deferred and contingency related.

Malhotra Committee appointed by the government of India for conducting a study on

insurance is bullish on insurance sector potential. The poor reach of insurance in the

country and the sheer numbers make India a market with tremendous potential.

Some important recommendations of this committee were:

The private sector to be allowed to enter insurance business

An Insurance regulatory Authority to be set up to regulate, promote and

ensure orderly growth of the insurance industry in India.

Foreign insurance companies to be permitted on a selective basis, they may

should be required to float an Indian company for the purpose preferably in a

joint venture with a Indian partners.

the quality of agents recruited needs to be improve, the minimum level of

business to be written by them to be reviewed, institutional channels like

cooperative societies, NGOs need to be harnessed as distribution channel

48

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

Entry of private sector in insurance has been the hall mark of the emerging scenario.

Consequent to establishing IRDA were a good number of companies being given

licences to start insurance business in India.

SWOT Analysis of Insurance Sector in India

The aim of liberalisation of this sector was to provide better Services to the

customers, to provide innovativeness and need based products at reasonable

premium rates and provide satisfactory returns.

The figures of the basic parameters of the Industry's performance viz. insurance

density and insurance penetration also are evident of the hither to existing low yield

Indian market conditions.

The figure of premium vis-à-vis the GDP of 2000 today at 0.54 percent for non-life

insurance business and 1.39 percent for the life insurance business.

The term "insurance density" reflects the insurance purchasing power. The premium

per capita in India amounted to US $2.40 for non-life Insurance and US $ 6.10 for life

insurance in 2000.

According to 2000 - 01 figures, the per capita insurance premium in India was only

$8 as compared to $4,800 in Japan, $1,000 in South Korea, $887 in Singapore, $823

in Hong Kong and $144 in Malaysia. India's share in total insurance premium

worldwide was only 0.3 percent, though it was second most populous country in the

world while Japan's share was 31 percent, EU 25 percent, South Africa 2.3 percent

and Canada 1.7 percent.

The total insurance premium in India is two percent of our GDP, which is far below

the world average of 7.8 percent. India's Share in the world insurance market is only

0.39 percent as against 34.17 percent of US, 21.02 percent of and 8.4 percent of

UK .

49

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

STRENGTHS

high growth rate of insurance sector;

government's dependence on this sector for long range low cost funds

for infrastructure development;

huge contribution towards foreign exchange reserves by Re insurance ;

high level of employment generation;

Very big middle class (consuming class).

WEAKNESSES

low per capita insurance premium;

low penetration /reach;

society's perception for saving ends at gold or house;

Low faith of people in foreign companies for depositing hard earned

savings;

huge paper work/ time lag in settling claims;

Rampant corruption in nationalised insurers;

Low literacy rate.

OPPORTUNITIES

huge potential to be tapped ;

with coming of foreign insurance companies, their innovative insurance

products and marketing expertise will also flow ;

use of IT as service provider .

50

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

THREATS

Insurance (life) is a long term business and it is not feasible to predict the

interest rates over long tenures;

insurance is susceptible to vagaries of nature i.e. floods, earthquakes,

etc which can make insurance companies bankrupt ;

Wrong commitments / communication by insurance agents (on behalf of

company) to the gullible consumers.

51

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

MARKETING MIX IN THE INSURANCE SERVICES

PRODUCT

‘life insurance’ is a contract for payment of a sum of money to the person assured (or

failing him/ her, to the person entitled to receive the same) on the happening of the

event insured against.' usually the insurance contract provides for the payment of an

amount of on the date of maturity or at specified rates at periodic intervals or at

unfortunate death if it occurs earlier. Obviously, there is a price to be paid for this

benefit. Among other things, the contract also provides for the payment of premiums

by the assured.

‘life Insurance’ is universally acknowledged as a tool to eliminate risk, substitute

certainly for uncertainty and ensure timely aid for the family in the unfortunate event

of the death of the breadwinner. In other words, it is the civilised world's partial

solution to the problems caused by death. In a nutshell, life Insurance helps in two

ways: dealing with the premature death, which leads to dependent families to fend for

themselves and old age without visible means of support.

Product benefits

Superior to any other savings plan:

Unlike any other savings plan, a life insurance policy affords full protection

against risk of death of the policy holder; the insurance company makes

available the full sum assured to the policyholders' near and dear ones. In

comparison, any other savings plan would amount to only the total savings

accumulated till date. If the death occurs prematurely, such savings can be

much less than the sum assured which means that the potential financial loss

to the family is sizeable.

52

Marketing Research about Competition in Insurance Industry & Appointment of FC’s

Encourages and forces thrift:

A savings deposit can easily be with drawn. The payment of life insurance

premiums, however, is conceded sacrosanct and is viewed with the same

seriousness as the payment of interest on a mortgage. Thus, a life insurance

policy in effect brings about compulsory savings.

Easy settlement and protection against creditors:

A life insurance policy is the only financial instrument the proceeds of which

can be protected against the claims of the creditor of the assured by effecting

a valid assignment of the policy.

Administering the legacy for beneficiaries:

Speculative or unwise expenses can quickly cause the proceeds to be

squandered. Several policies have foreseen this possibility and provide for

payments over period of years or in a combination of instalments and lump

sum amounts.

Ready marketability and suitability for quick borrowing:

A life insurance policy can, after a certain time period be surrendered for a

cash value. The policy is also acceptable as a security for a commercial loan,

for example, a student loan. It is particularly advisable for housing loans when

an acceptable LIC policy may also cause the lending institution to give loan at

lower interest rates.

Disability benefits:

Death is not the only hazard that is insured; many policies also include