Bumrungrad Hospital Public Company Limitedbh.listedcompany.com/misc/PRESN/20160518-bh... ·...

29

Bumrungrad Hospital Public Company Limited Analyst Meeting No. 2/2016 (1Q16 Results Update) Wednesday 18 May 2016

Transcript of Bumrungrad Hospital Public Company Limitedbh.listedcompany.com/misc/PRESN/20160518-bh... ·...

PG.1

Bumrungrad Hospital Public Company Limited

Analyst Meeting No. 2/2016 (1Q16 Results Update)

Wednesday 18 May 2016

PG.2

Disclaimer • The information contained in this presentation is for information purposes only and does not constitute an offer or invitation to sell or

the solicitation of an offer or invitation to purchase or subscribe for any securities of Bumrungrad Hospital Public Company Limited (the

"Company") in any jurisdiction nor should it or any part of it form the basis of, or be relied upon in connection with, any contract or

commitment whatsoever.

• This presentation is being communicated only to persons who have professional experience in matters relating to investments and/or

to persons to whom it is lawful to communicate it under the laws of applicable jurisdictions. Other persons should not rely or act upon

this presentation or any of its contents.

• Certain information and statements made in this presentation contain the Company's forward-looking statements. All forward-looking

statements are the Company's current expectation of future events and are subject to a number of factors that could cause actual

results to differ materially from those described in the forward-looking statements. Prospective investors should take care with respect

to such statements and should not place undue reliance on any such forward-looking statements.

• This presentation has been prepared by the Company solely for the use at this presentation. The information in this presentation has

not been independently verified. No representation, warranty, express or implied, is made as to, and no reliance should be placed on,

the fairness, accuracy, completeness or correctness of the information and opinions in this presentation. None of the Company, any of

its affiliates or any of their respective agents, advisors or representatives, shall have any liability (in negligence or otherwise) for any

loss or damage howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this

presentation. The information presented or contained in this presentation is current as of the date hereof and is subject to change

without notice and its accuracy is not guaranteed. None of the Company, any of its affiliates or any of their respective agents, advisors

or representatives, makes any undertaking to update any such information subsequent to the date hereof.

• This presentation should not be construed as legal, tax, investment or other advice. No part of this presentation shall be relied upon

directly or indirectly for any investment decision-making or for any other purposes. Prospective investors should undertake their own

assessment with regard to any investment and should obtain independent advice on any such investment’s suitability, inherent risks

and merits and any tax, legal and accounting implications which it may have for them.

• Certain data in this presentation were obtained from various external data sources, and none of the Company, any of its affiliates or

any of their respective agents, advisors or representatives have verified such data with independent sources. Accordingly, the Company

makes no representation as to the accuracy or completeness of those data, and such data involve risks and uncertainties and are

subject to change based on various factors.

PG.3

Corporate CEO Retirement

Dennis Brown, Corporate CEO of Bumrungrad Hospital PCL. will be retired on July 31st, 2016.

PG.4

Ronald s. Lavater, MPA, Fache

Ron is serving as the CEO for Al Noor Hospitals Group, Plc. since October 2014. Ron is a Fellow with the American College of Healthcare Executives (ACHE) and recently completed a two-year term as president of the Middle East & North Africa ACHE group.

EDUCATION

Master of Public Administration and Policy, concentration in Healthcare Administration and Policy Florida State University, 1992 • City of Tallahassee, Intern, City Manager’s Office, 1991 – 1992

PROFESSIONAL EXPERIENCE

• Al Noor Hospitals Group, Plc. Abu Dhabi, UAE, 2014 – Present * Chief Executive Officer and Executive Director of the Board

• Johns Hopkins Medicine International (JHI), Baltimore, Maryland, 2009 - 2014

* Chief Executive Officer, Corniche Hospital, 2009 – 2013 • Hospital Corporation of America (HCA), Nashville, Tennessee, 1996 – 2007 * Chief Executive Officer, Palms West Hospital, Florida, 2005 – 2007 • Blue Cross and Blue Shield of Florida, Jacksonville, Florida, 1993 – 1995

PG.5

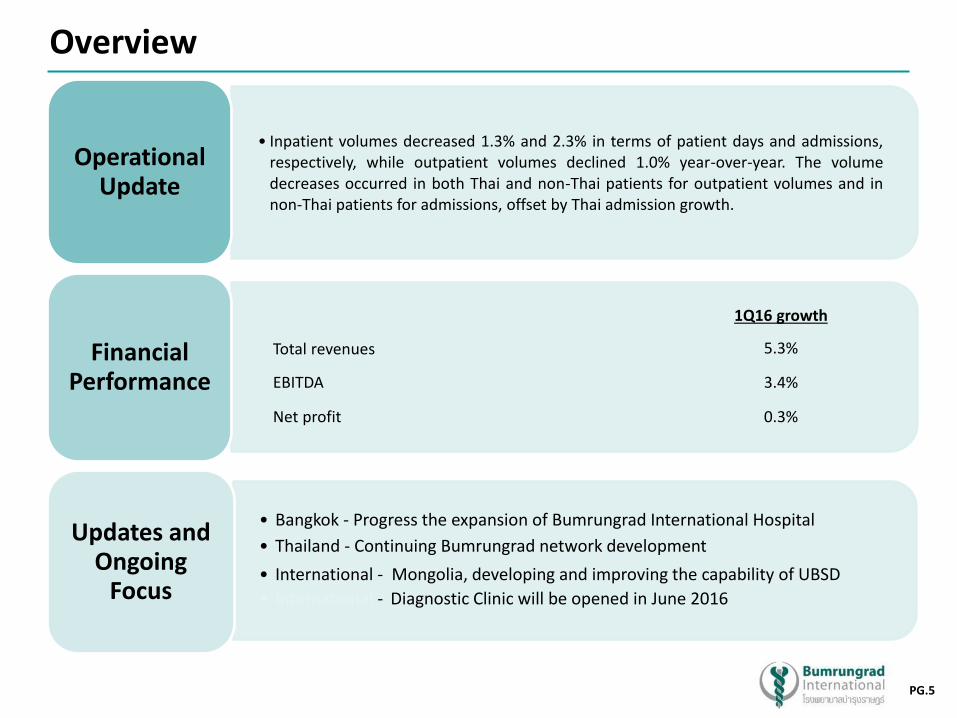

Overview

• Inpatient volumes decreased 1.3% and 2.3% in terms of patient days and admissions, respectively, while outpatient volumes declined 1.0% year-over-year. The volume decreases occurred in both Thai and non-Thai patients for outpatient volumes and in non-Thai patients for admissions, offset by Thai admission growth.

Operational Update

Financial Performance

• Bangkok - Progress the expansion of Bumrungrad International Hospital

• Thailand - Continuing Bumrungrad network development

• International - Mongolia, developing and improving the capability of UBSD

• International - Diagnostic Clinic will be opened in June 2016

Updates and Ongoing

Focus

1Q16 growth

Total revenues 5.3%

EBITDA 3.4%

Net profit 0.3%

PG.6

Agenda

Strategy

Operational Update

Financial Performance

PG.7

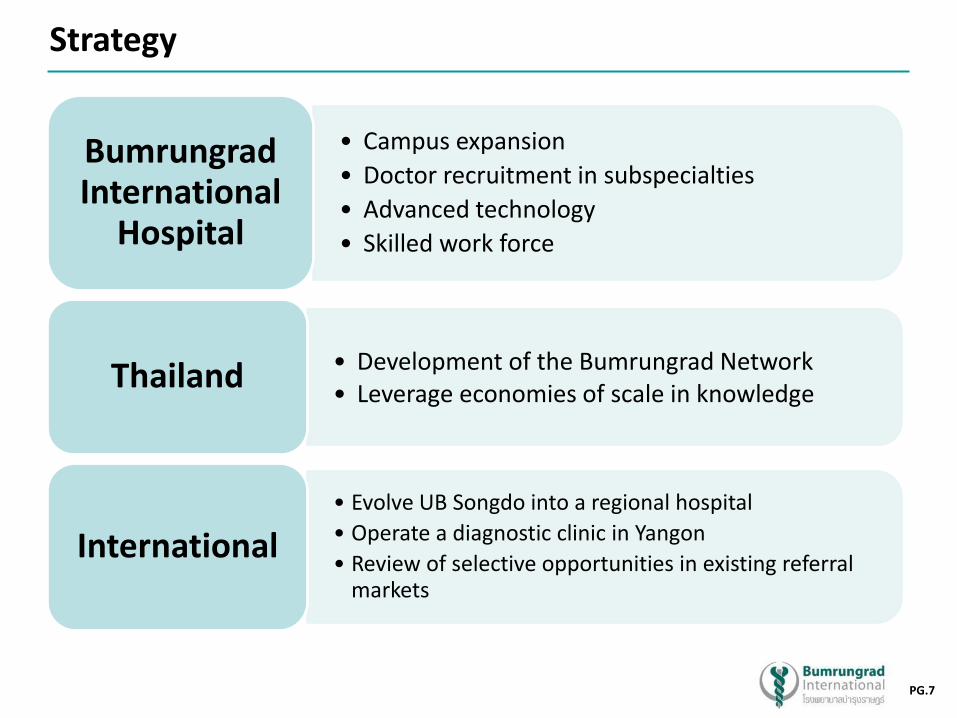

Strategy

• Campus expansion

• Doctor recruitment in subspecialties

• Advanced technology

• Skilled work force

Bumrungrad International

Hospital

• Development of the Bumrungrad Network • Leverage economies of scale in knowledge

Thailand

• Evolve UB Songdo into a regional hospital

• Operate a diagnostic clinic in Yangon

• Review of selective opportunities in existing referral markets

International

PG.8

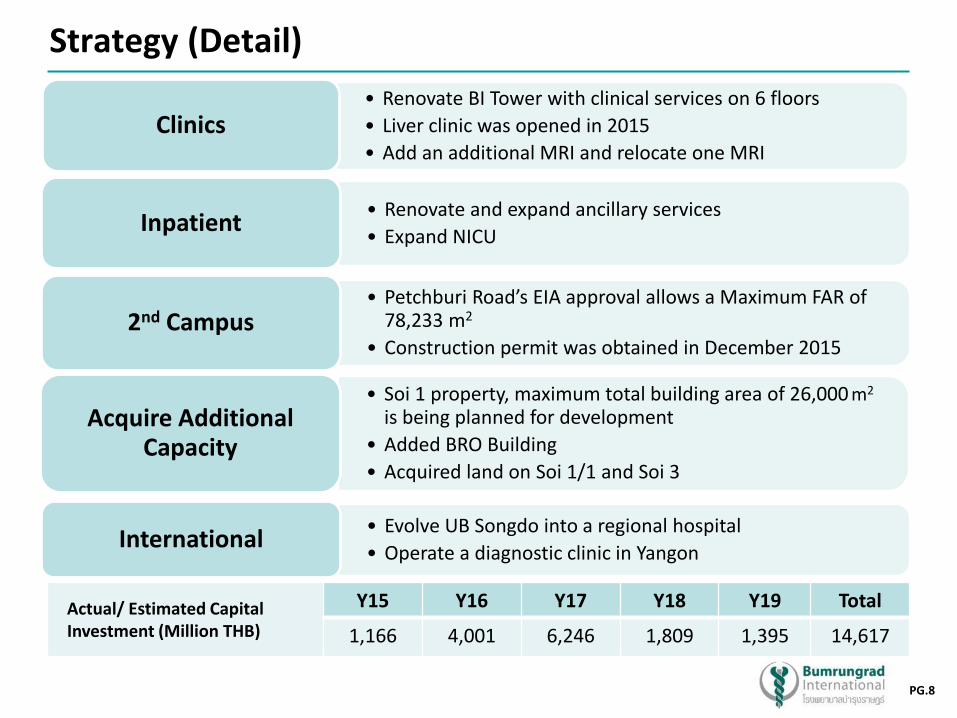

Strategy (Detail)

• Renovate BI Tower with clinical services on 6 floors

• Liver clinic was opened in 2015

• Add an additional MRI and relocate one MRI Clinics

• Renovate and expand ancillary services

• Expand NICU Inpatient

• Petchburi Road’s EIA approval allows a Maximum FAR of 78,233 m2

• Construction permit was obtained in December 2015 2nd Campus

• Soi 1 property, maximum total building area of 26,000 m2 is being planned for development

• Added BRO Building

• Acquired land on Soi 1/1 and Soi 3

Acquire Additional Capacity

• Evolve UB Songdo into a regional hospital

• Operate a diagnostic clinic in Yangon International

Actual/ Estimated Capital Investment (Million THB)

Y15 Y16 Y17 Y18 Y19 Total

1,166 4,001 6,246 1,809 1,395 14,617

PG.9

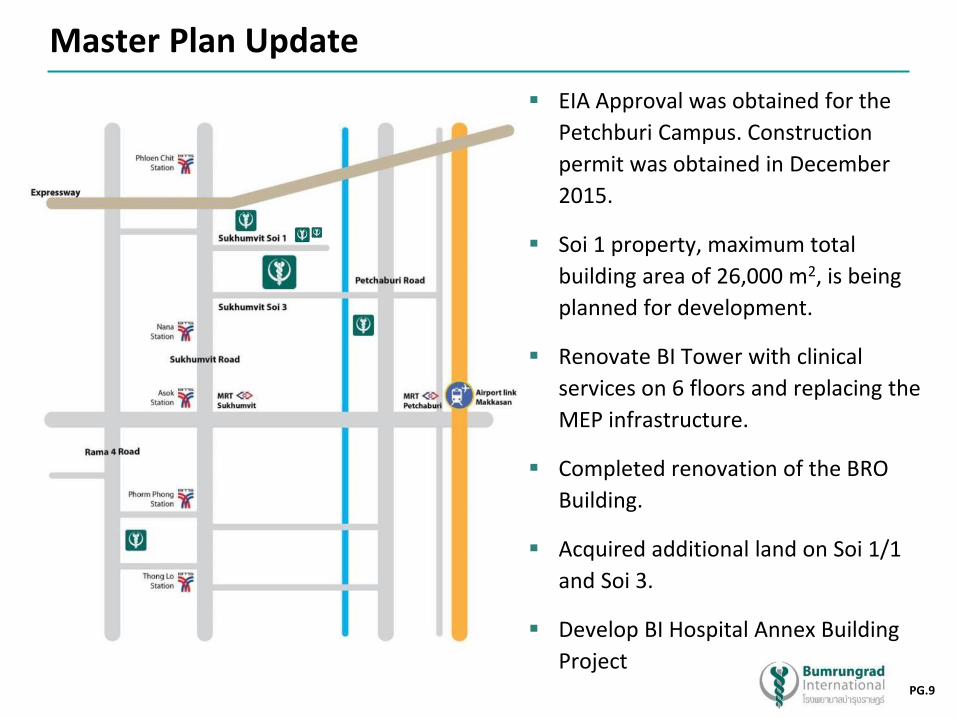

Master Plan Update

EIA Approval was obtained for the

Petchburi Campus. Construction

permit was obtained in December

2015.

Soi 1 property, maximum total

building area of 26,000 m2, is being

planned for development.

Renovate BI Tower with clinical

services on 6 floors and replacing the

MEP infrastructure.

Completed renovation of the BRO

Building.

Acquired additional land on Soi 1/1

and Soi 3.

Develop BI Hospital Annex Building

Project

PG.10

New Land Acquisitions Surrounding Main Campus

Total Land Area 1,852 m2

Total Land Area 597 m2

Total Land Area 420 m2

SUKHUMVIT SOI 1

Total Land Area 138 m2

PG.11

Bumrungrad International Hospital (Main Campus)

3 Main Buildings

BI Clinic

BI Hospital

BI Tower

PG.12

BI Tower Building

Renovate BI Tower with clinical services on 6 floors, total space is about 8,100 m2

Renovation started in November 2015.

PG.13

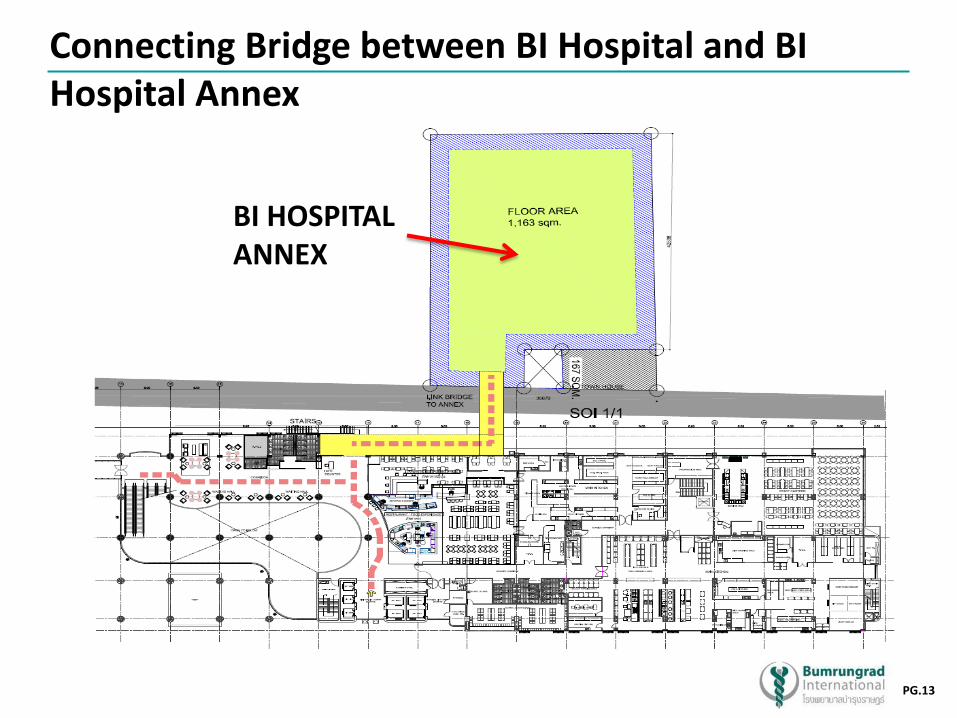

Connecting Bridge between BI Hospital and BI Hospital Annex

BI HOSPITAL ANNEX

PG.14

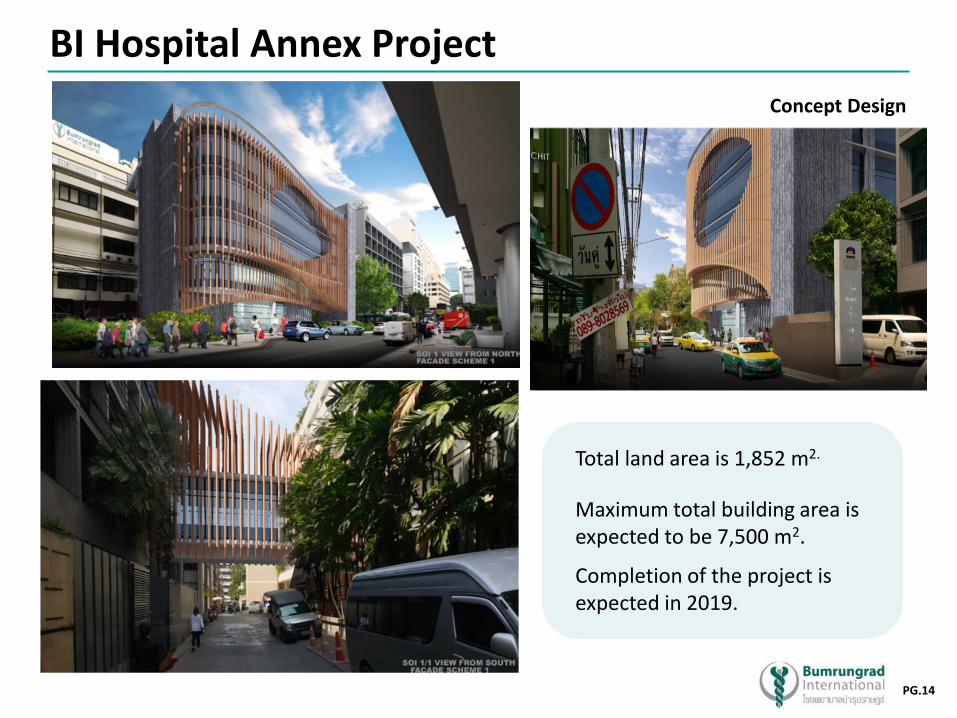

BI Hospital Annex Project

Concept Design

Total land area is 1,852 m2.

Maximum total building area is expected to be 7,500 m2.

Completion of the project is expected in 2019.

PG.15

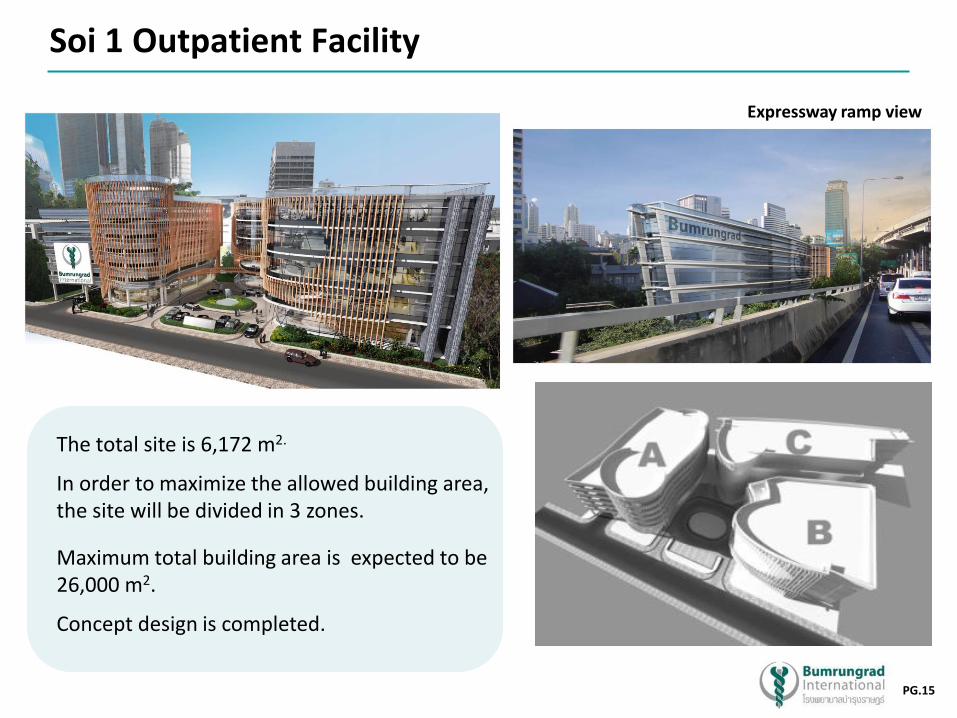

Soi 1 Outpatient Facility

Expressway ramp view

The total site is 6,172 m2.

In order to maximize the allowed building area, the site will be divided in 3 zones.

Maximum total building area is expected to be 26,000 m2.

Concept design is completed.

PG.16

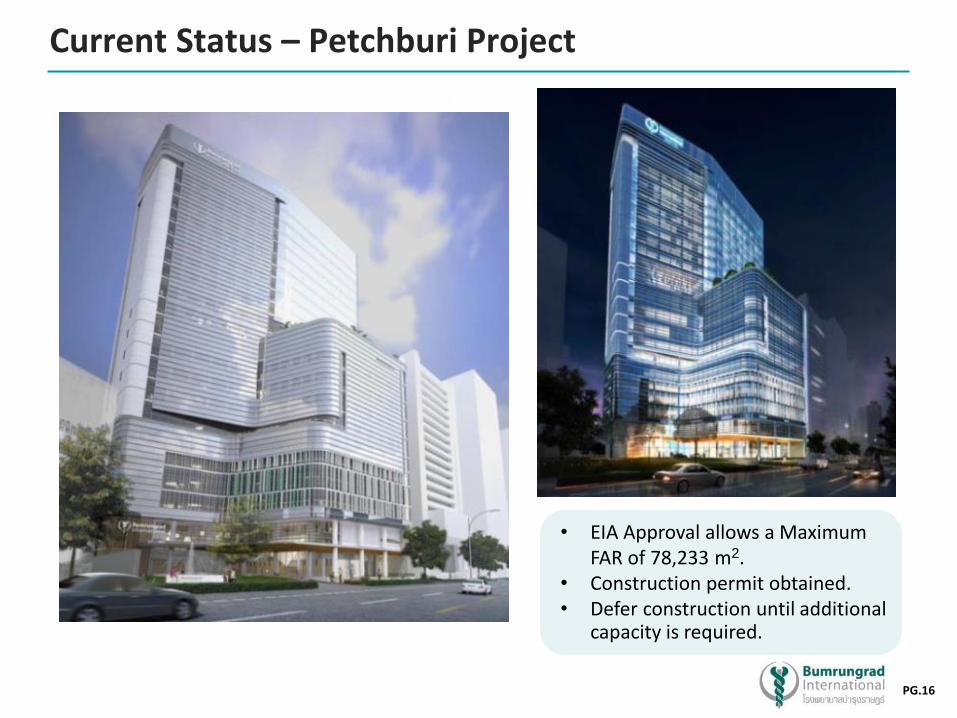

Current Status – Petchburi Project

• EIA Approval allows a Maximum FAR of 78,233 m2.

• Construction permit obtained. • Defer construction until additional

capacity is required.

PG.17

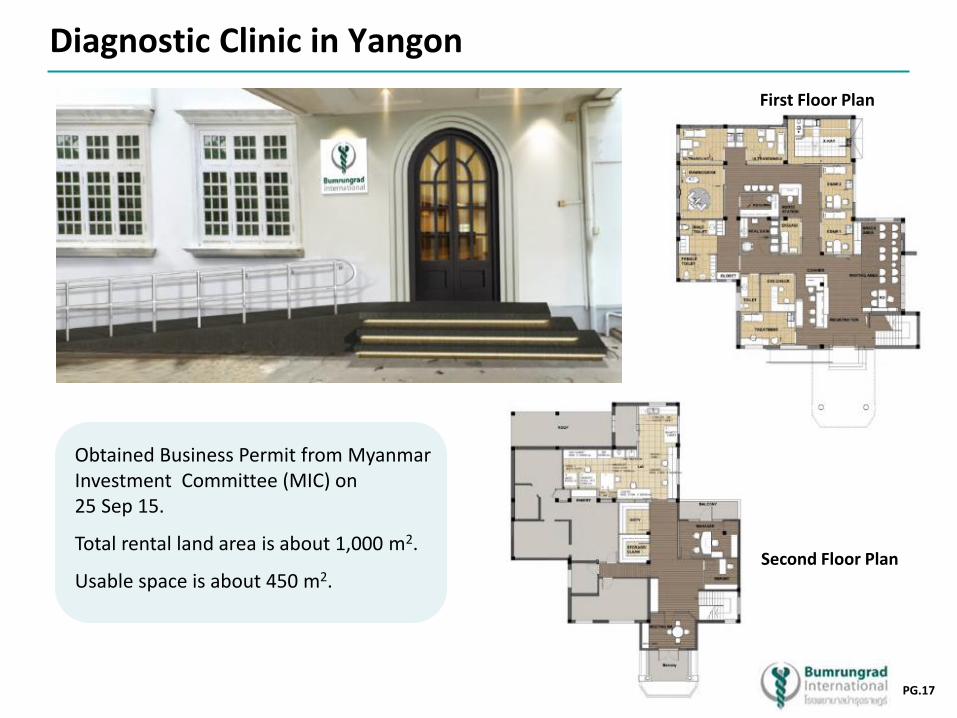

Diagnostic Clinic in Yangon

First Floor Plan

Obtained Business Permit from Myanmar Investment Committee (MIC) on 25 Sep 15.

Total rental land area is about 1,000 m2.

Usable space is about 450 m2. Second Floor Plan

PG.18

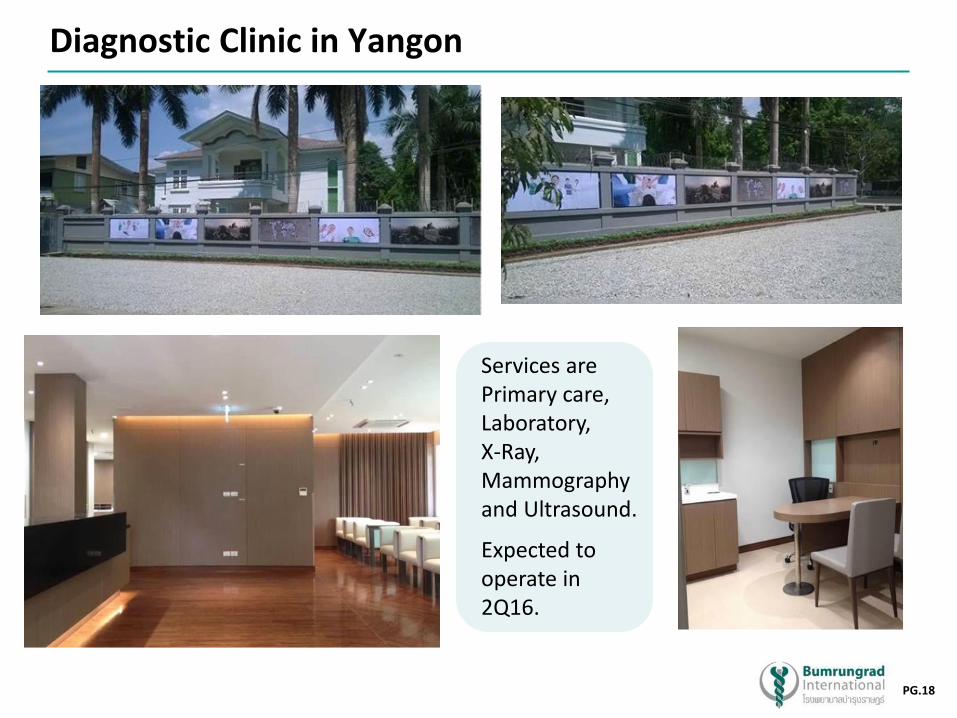

Diagnostic Clinic in Yangon

Services are Primary care, Laboratory, X-Ray, Mammography and Ultrasound.

Expected to operate in 2Q16.

PG.19

Strategy

Operational Update

Financial Performance

Agenda

PG.20

17.9%

2,820

3,348 3,424 3,397 3,325

3,264 3,249 3,269 3,325 3,255

0

1,000

2,000

3,000

4,000

1Q 2Q 3Q 4Q 1Q

2014 2015 2016

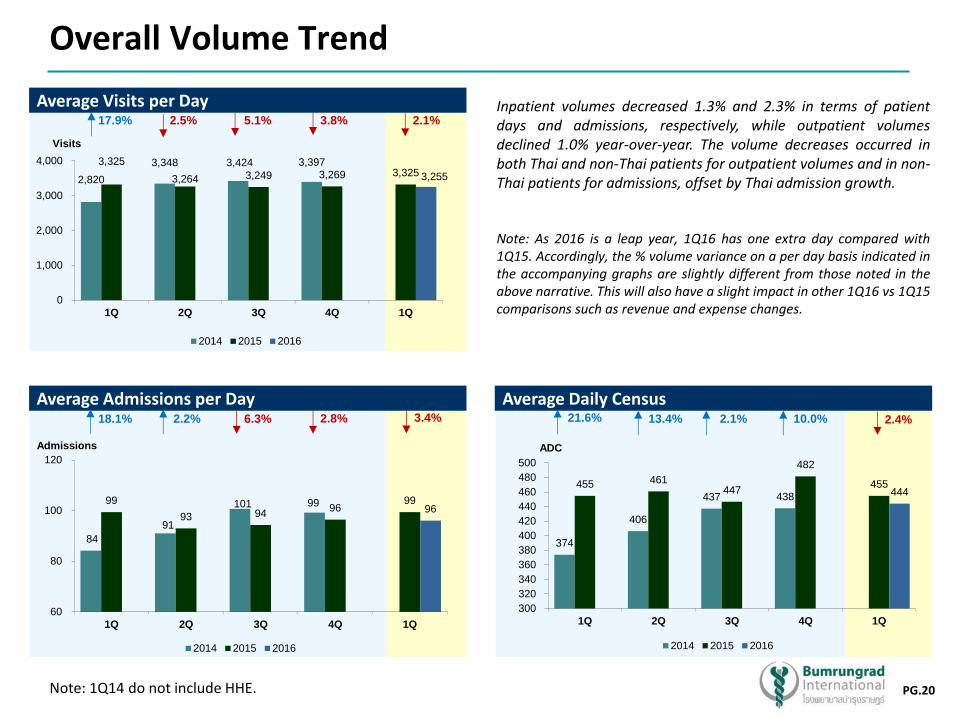

Overall Volume Trend

Visits

Average Visits per Day 2.5% 5.1% 3.8%

Note: 1Q14 do not include HHE.

Inpatient volumes decreased 1.3% and 2.3% in terms of patient days and admissions, respectively, while outpatient volumes declined 1.0% year-over-year. The volume decreases occurred in both Thai and non-Thai patients for outpatient volumes and in non-Thai patients for admissions, offset by Thai admission growth.

Note: As 2016 is a leap year, 1Q16 has one extra day compared with 1Q15. Accordingly, the % volume variance on a per day basis indicated in the accompanying graphs are slightly different from those noted in the above narrative. This will also have a slight impact in other 1Q16 vs 1Q15 comparisons such as revenue and expense changes.

84

91

101 99 99

93 94 96

99 96

60

80

100

120

1Q 2Q 3Q 4Q 1Q

2014 2015 2016

Admissions

Average Admissions per Day 18.1% 2.2% 6.3% 2.8%

ADC

Average Daily Census

374

406

437 438 455 461

447

482

455 444

300

320

340

360

380

400

420

440

460

480

500

1Q 2Q 3Q 4Q 1Q

2014 2015 2016

21.6%

2.1%

3.4% 13.4% 2.1% 10.0% 2.4%

PG.21

7,531

6,982

7,254 7,624

7,976 7,967 8,036 8,148 7,976

8,692

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1Q 2Q 3Q 4Q 1Q

2014 2015 2016

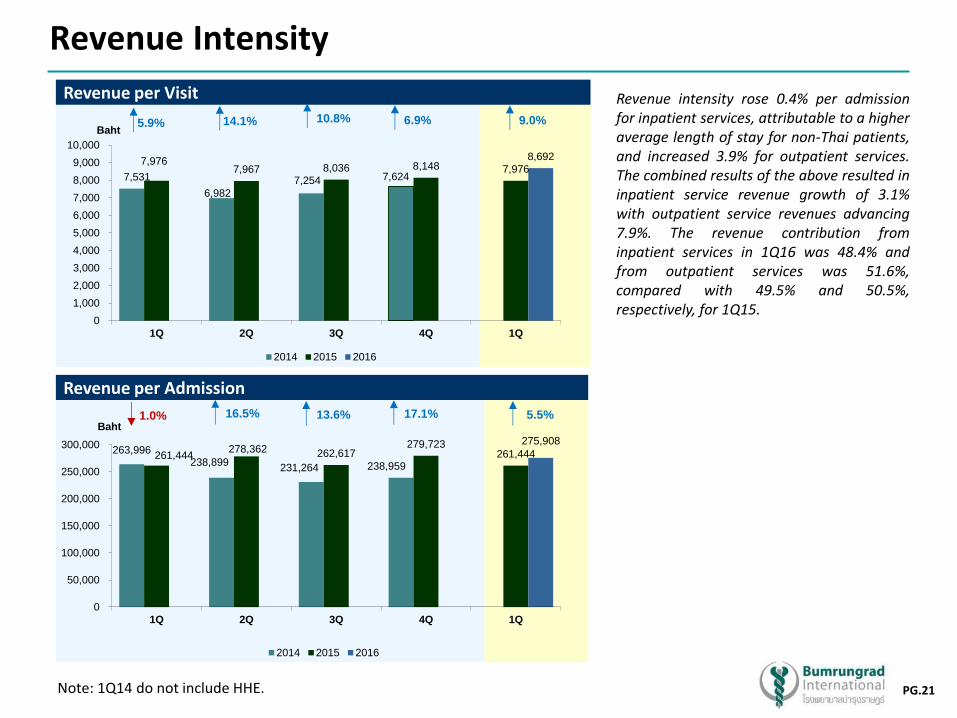

Revenue Intensity

Baht

Revenue per Visit

14.1% 10.8% 6.9%

263,996 238,899

231,264 238,959 261,444

278,362 262,617 279,723

261,444

275,908

0

50,000

100,000

150,000

200,000

250,000

300,000

1Q 2Q 3Q 4Q 1Q

2014 2015 2016

Baht

Revenue per Admission

16.5% 13.6% 5.5% 1.0%

Note: 1Q14 do not include HHE.

5.9% 9.0%

17.1%

Revenue intensity rose 0.4% per admission for inpatient services, attributable to a higher average length of stay for non-Thai patients, and increased 3.9% for outpatient services. The combined results of the above resulted in inpatient service revenue growth of 3.1% with outpatient service revenues advancing 7.9%. The revenue contribution from inpatient services in 1Q16 was 48.4% and from outpatient services was 51.6%, compared with 49.5% and 50.5%, respectively, for 1Q15.

PG.22

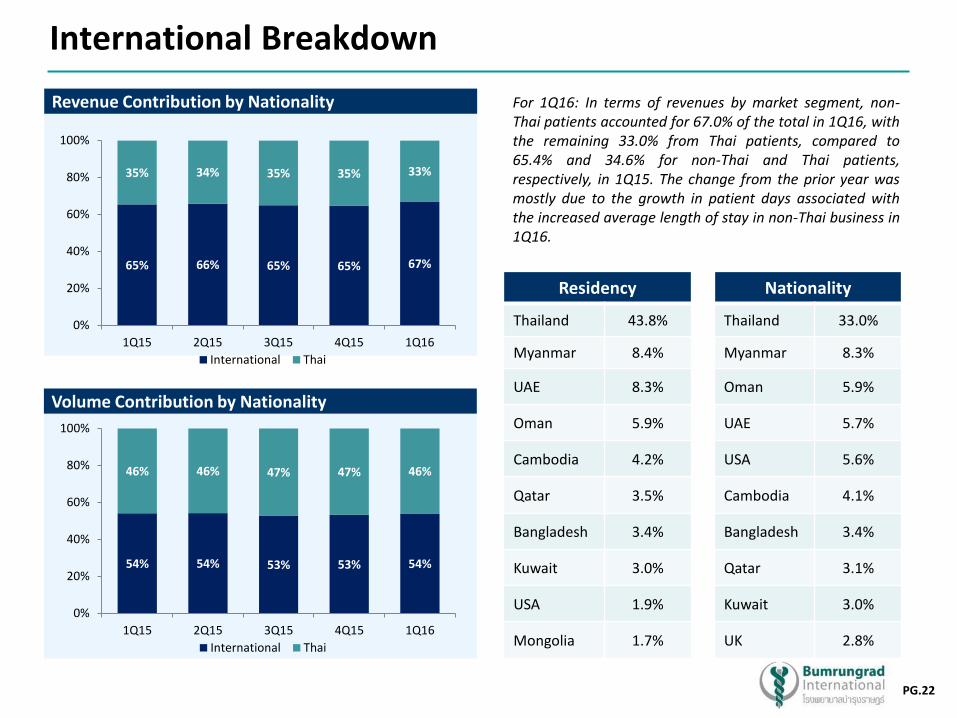

Volume Contribution by Nationality

Revenue Contribution by Nationality

International Breakdown

For 1Q16: In terms of revenues by market segment, non-Thai patients accounted for 67.0% of the total in 1Q16, with the remaining 33.0% from Thai patients, compared to 65.4% and 34.6% for non-Thai and Thai patients, respectively, in 1Q15. The change from the prior year was mostly due to the growth in patient days associated with the increased average length of stay in non-Thai business in 1Q16.

65% 66% 65% 65% 67%

35% 34% 35% 35% 33%

0%

20%

40%

60%

80%

100%

1Q15 2Q15 3Q15 4Q15 1Q16

International Thai

54% 54% 53% 53% 54%

46% 46% 47% 47% 46%

0%

20%

40%

60%

80%

100%

1Q15 2Q15 3Q15 4Q15 1Q16

International Thai

Nationality

Thailand 33.0%

Myanmar 8.3%

Oman 5.9%

UAE 5.7%

USA 5.6%

Cambodia 4.1%

Bangladesh 3.4%

Qatar 3.1%

Kuwait 3.0%

UK 2.8%

Residency

Thailand 43.8%

Myanmar 8.4%

UAE 8.3%

Oman 5.9%

Cambodia 4.2%

Qatar 3.5%

Bangladesh 3.4%

Kuwait 3.0%

USA 1.9%

Mongolia 1.7%

PG.23

Revenue Breakdown

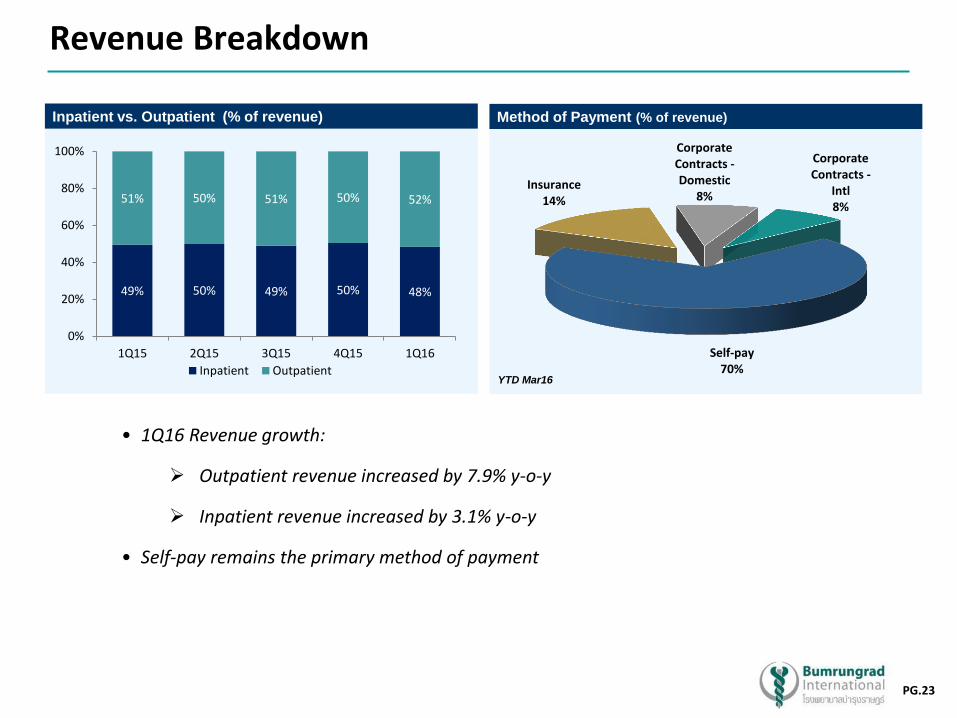

Inpatient vs. Outpatient (% of revenue) Method of Payment (% of revenue)

YTD Mar16

• 1Q16 Revenue growth:

Outpatient revenue increased by 7.9% y-o-y

Inpatient revenue increased by 3.1% y-o-y

• Self-pay remains the primary method of payment

49% 50% 49% 50% 48%

51% 50% 51% 50% 52%

0%

20%

40%

60%

80%

100%

1Q15 2Q15 3Q15 4Q15 1Q16

Inpatient Outpatient

Corporate Contracts - Domestic

8%

Corporate Contracts -

Intl 8%

Self-pay 70%

Insurance 14%

PG.24

Agenda

Strategy

Operational Update

Financial Performance

PG.25

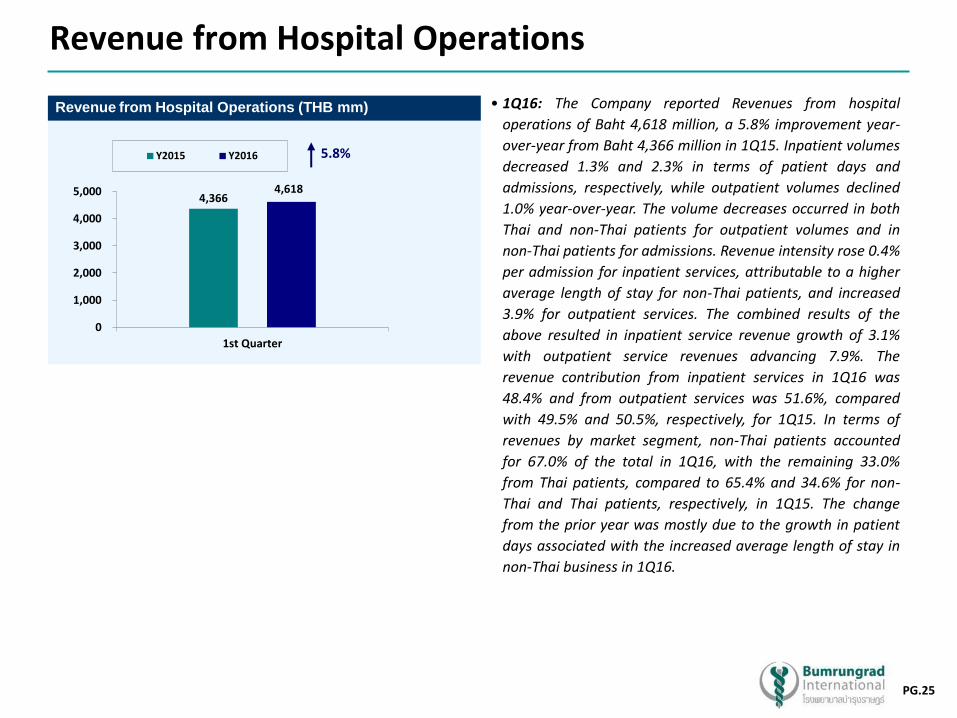

Revenue from Hospital Operations

Revenue from Hospital Operations (THB mm)

4,366 4,618

0

1,000

2,000

3,000

4,000

5,000

1st Quarter

Y2015 Y2016 5.8%

• 1Q16: The Company reported Revenues from hospital

operations of Baht 4,618 million, a 5.8% improvement year-

over-year from Baht 4,366 million in 1Q15. Inpatient volumes

decreased 1.3% and 2.3% in terms of patient days and

admissions, respectively, while outpatient volumes declined

1.0% year-over-year. The volume decreases occurred in both

Thai and non-Thai patients for outpatient volumes and in

non-Thai patients for admissions. Revenue intensity rose 0.4%

per admission for inpatient services, attributable to a higher

average length of stay for non-Thai patients, and increased

3.9% for outpatient services. The combined results of the

above resulted in inpatient service revenue growth of 3.1%

with outpatient service revenues advancing 7.9%. The

revenue contribution from inpatient services in 1Q16 was

48.4% and from outpatient services was 51.6%, compared

with 49.5% and 50.5%, respectively, for 1Q15. In terms of

revenues by market segment, non-Thai patients accounted

for 67.0% of the total in 1Q16, with the remaining 33.0%

from Thai patients, compared to 65.4% and 34.6% for non-

Thai and Thai patients, respectively, in 1Q15. The change

from the prior year was mostly due to the growth in patient

days associated with the increased average length of stay in

non-Thai business in 1Q16.

PG.26

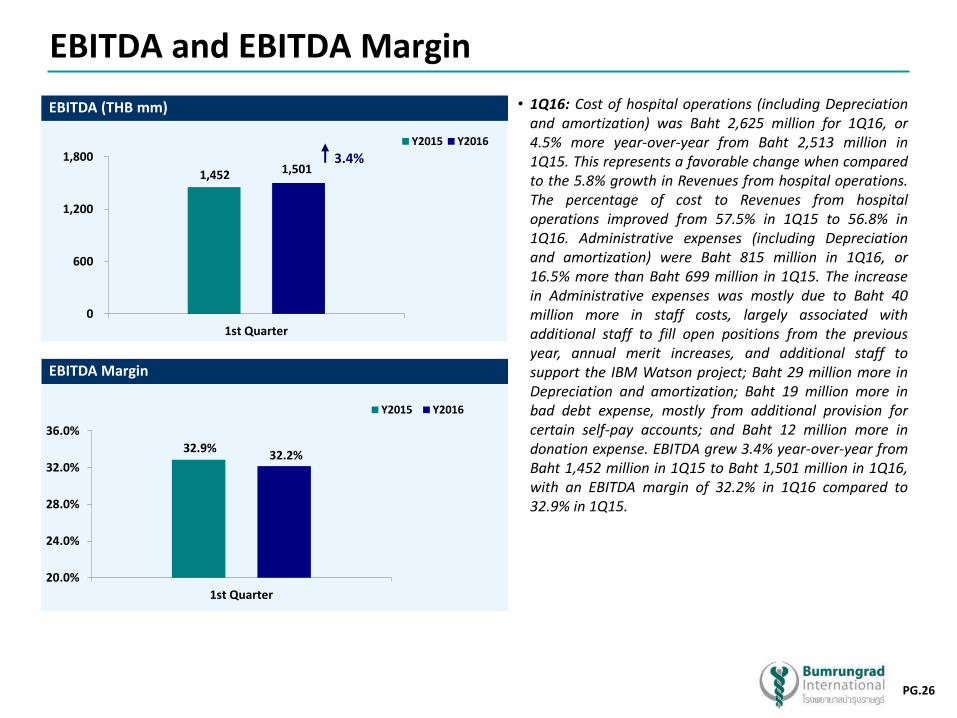

EBITDA and EBITDA Margin

EBITDA (THB mm)

EBITDA Margin

32.9% 32.2%

20.0%

24.0%

28.0%

32.0%

36.0%

1st Quarter

Y2015 Y2016

1,452 1,501

0

600

1,200

1,800

1st Quarter

Y2015 Y2016

3.4%

• 1Q16: Cost of hospital operations (including Depreciation and amortization) was Baht 2,625 million for 1Q16, or 4.5% more year-over-year from Baht 2,513 million in 1Q15. This represents a favorable change when compared to the 5.8% growth in Revenues from hospital operations. The percentage of cost to Revenues from hospital operations improved from 57.5% in 1Q15 to 56.8% in 1Q16. Administrative expenses (including Depreciation and amortization) were Baht 815 million in 1Q16, or 16.5% more than Baht 699 million in 1Q15. The increase in Administrative expenses was mostly due to Baht 40 million more in staff costs, largely associated with additional staff to fill open positions from the previous year, annual merit increases, and additional staff to support the IBM Watson project; Baht 29 million more in Depreciation and amortization; Baht 19 million more in bad debt expense, mostly from additional provision for certain self-pay accounts; and Baht 12 million more in donation expense. EBITDA grew 3.4% year-over-year from Baht 1,452 million in 1Q15 to Baht 1,501 million in 1Q16, with an EBITDA margin of 32.2% in 1Q16 compared to 32.9% in 1Q15.

PG.27

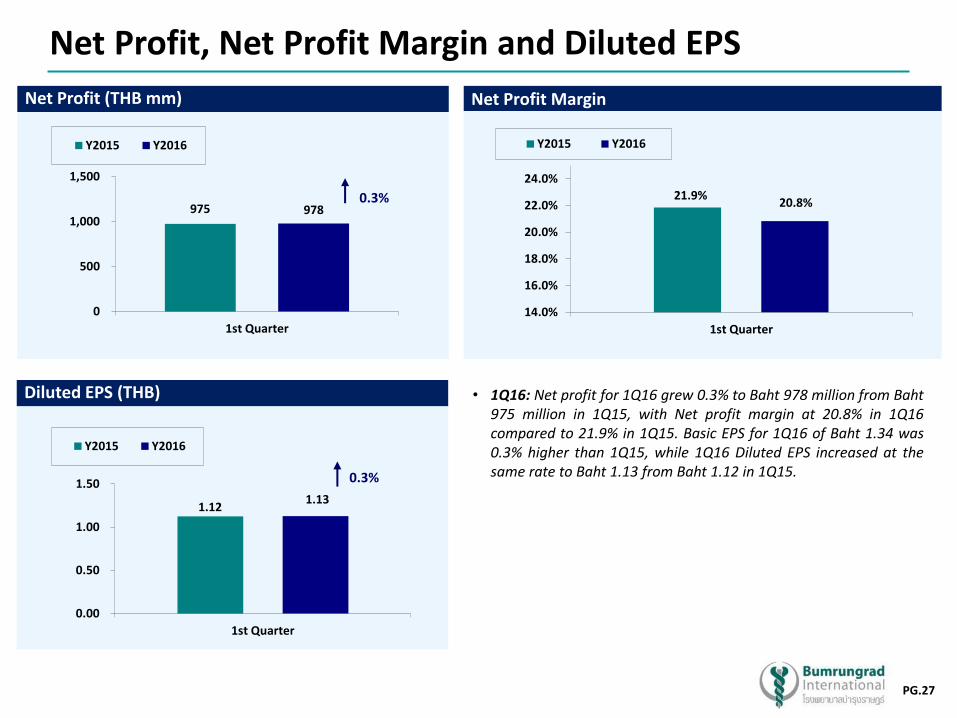

Net Profit (THB mm)

Diluted EPS (THB)

Net Profit Margin

Net Profit, Net Profit Margin and Diluted EPS

21.9% 20.8%

14.0%

16.0%

18.0%

20.0%

22.0%

24.0%

1st Quarter

Y2015 Y2016

• 1Q16: Net profit for 1Q16 grew 0.3% to Baht 978 million from Baht 975 million in 1Q15, with Net profit margin at 20.8% in 1Q16 compared to 21.9% in 1Q15. Basic EPS for 1Q16 of Baht 1.34 was 0.3% higher than 1Q15, while 1Q16 Diluted EPS increased at the same rate to Baht 1.13 from Baht 1.12 in 1Q15.

975 978

0

500

1,000

1,500

1st Quarter

Y2015 Y2016

0.3%

1.12 1.13

0.00

0.50

1.00

1.50

1st Quarter

Y2015 Y2016

0.3%

PG.28

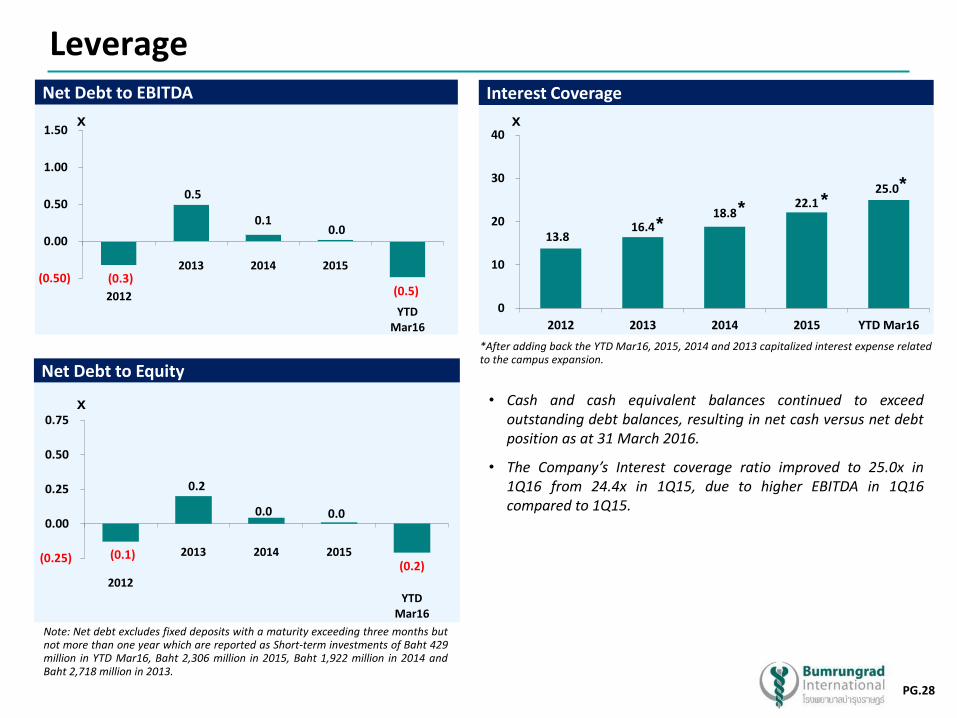

Leverage x Interest Coverage

x

Net Debt to EBITDA

x

Net Debt to Equity

x

(0.1)

0.2

0.0 0.0

(0.2) (0.25)

0.00

0.25

0.50

0.75

2012

2013 2014 2015

YTDMar16

(0.3)

0.5

0.1 0.0

(0.5) (0.50)

0.00

0.50

1.00

1.50

2012

2013 2014 2015

YTDMar16

13.8 16.4

18.8 22.1

25.0

0

10

20

30

40

2012 2013 2014 2015 YTD Mar16

Note: Net debt excludes fixed deposits with a maturity exceeding three months but not more than one year which are reported as Short-term investments of Baht 429 million in YTD Mar16, Baht 2,306 million in 2015, Baht 1,922 million in 2014 and Baht 2,718 million in 2013.

* * *

*

*After adding back the YTD Mar16, 2015, 2014 and 2013 capitalized interest expense related to the campus expansion.

• Cash and cash equivalent balances continued to exceed outstanding debt balances, resulting in net cash versus net debt position as at 31 March 2016.

• The Company’s Interest coverage ratio improved to 25.0x in 1Q16 from 24.4x in 1Q15, due to higher EBITDA in 1Q16 compared to 1Q15.

PG.29

Q & A