Building and Sustaining the Business Manager’s Relationship with Board Members Luann Mathis,...

80

Building and Sustaining the Business Manager’s Relationship with Board Members Luann Mathis, Business Manager, Prospect Heights ESD 23 Lauri Calabrese, Asst. Superintendent of Finance, LaGrange ESD 102 Ann Williams, Director of Business & Ops, Bradley-Bourbonnais HSD 307

-

Upload

judith-liliana-hamilton -

Category

Documents

-

view

215 -

download

0

Transcript of Building and Sustaining the Business Manager’s Relationship with Board Members Luann Mathis,...

Building and Sustaining the Business Manager’s Relationship

with Board Members

Luann Mathis, Business Manager, Prospect Heights ESD 23Lauri Calabrese, Asst. Superintendent of Finance, LaGrange ESD 102

Ann Williams, Director of Business & Ops, Bradley-Bourbonnais HSD 307

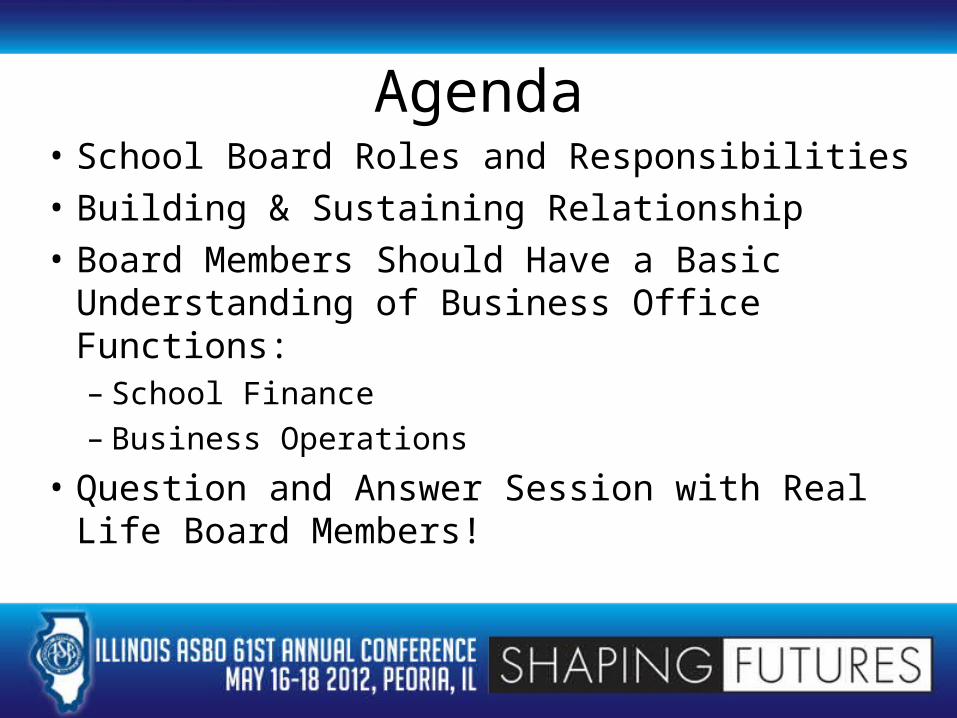

Agenda• School Board Roles and Responsibilities• Building & Sustaining Relationship• Board Members Should Have a Basic

Understanding of Business Office Functions:– School Finance– Business Operations

• Question and Answer Session with Real Life Board Members!

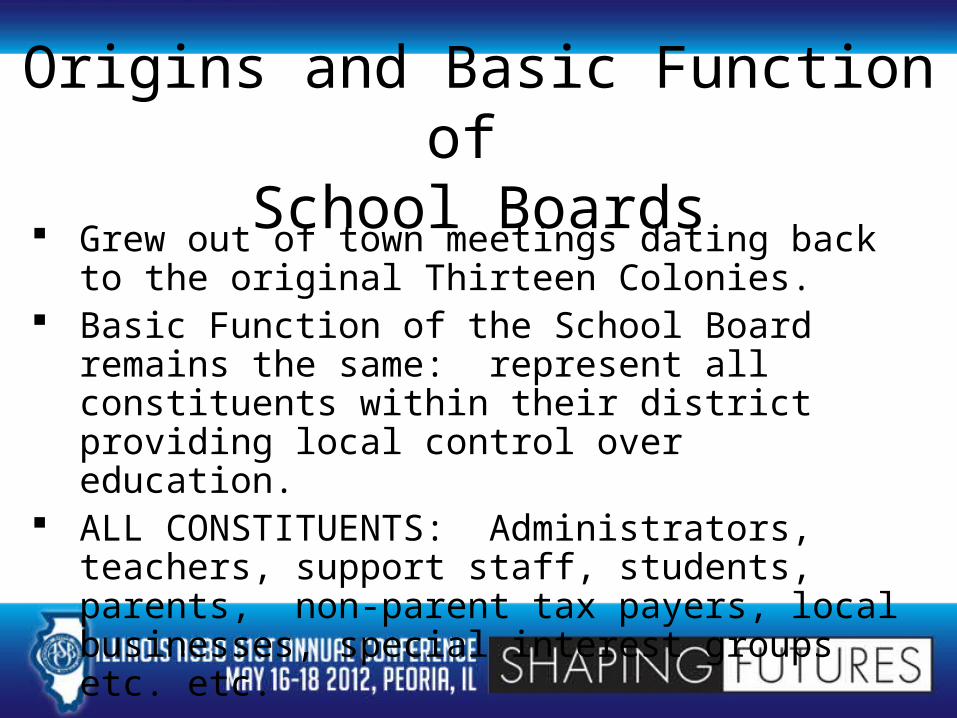

Origins and Basic Function of School Boards

Grew out of town meetings dating back to the original Thirteen Colonies.

Basic Function of the School Board remains the same: represent all constituents within their district providing local control over education.

ALL CONSTITUENTS: Administrators, teachers, support staff, students, parents, non-parent tax payers, local businesses, special interest groups etc. etc.

IASB Mission Statement

“The mission of the Illinois Association of School Boards is

Excellence in local school governance and support of public

education”

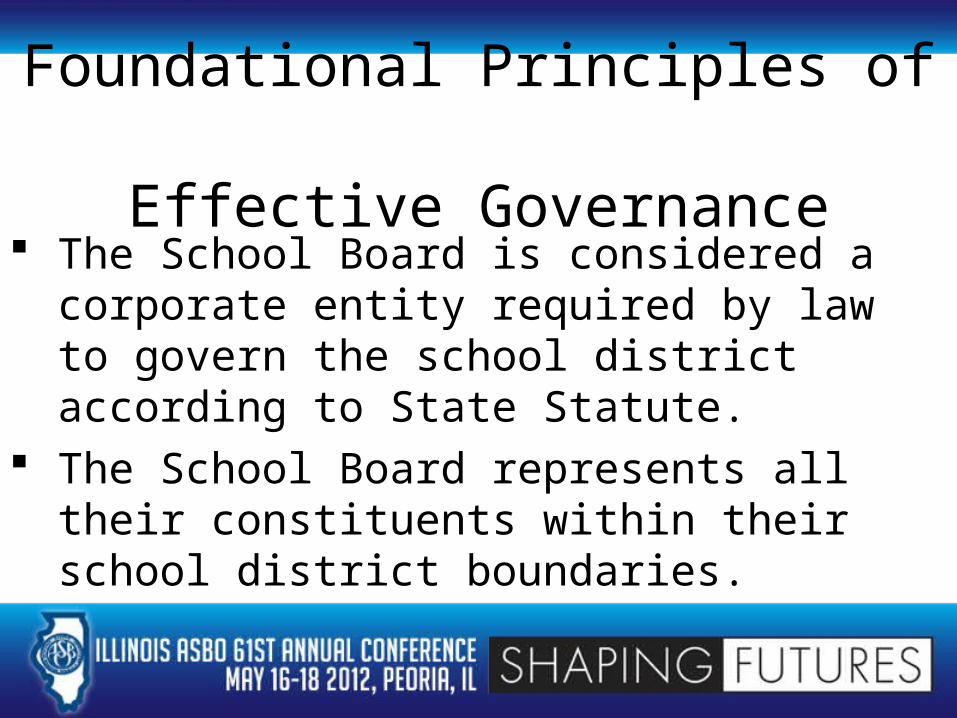

Foundational Principles of Effective Governance

The School Board is considered a corporate entity required by law to govern the school district according to State Statute.

The School Board represents all their constituents within their school district boundaries.

School Board Duties & Responsibilities IASB Defined Duties:

Employs a Superintendent Clarifies the District Purpose Connects with the Community Delegates Authority Monitors Performance Takes Responsibility for Itself

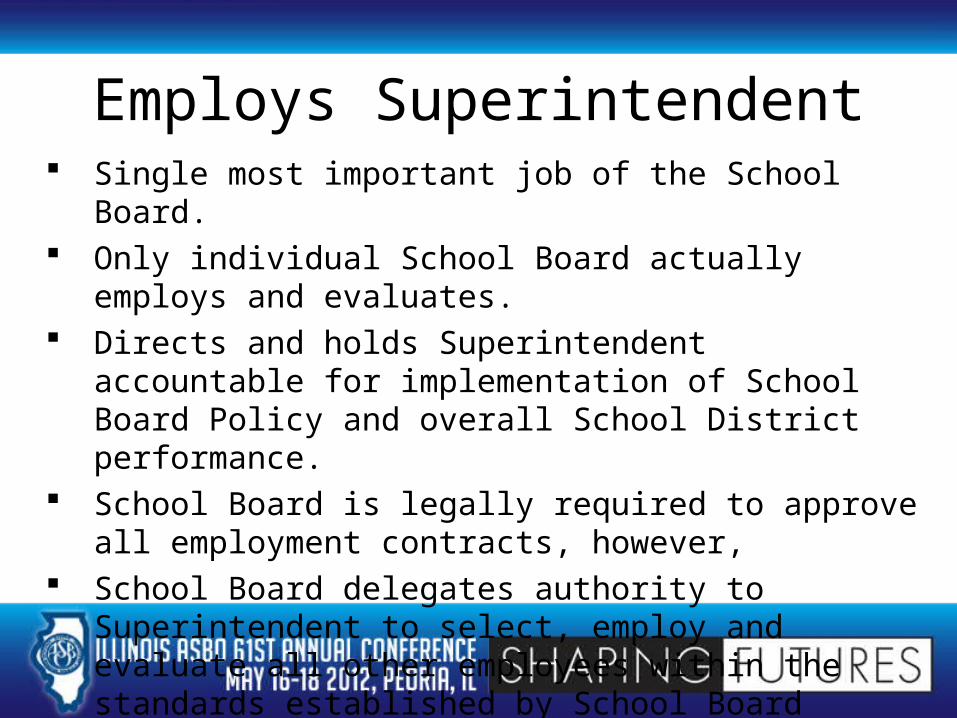

Employs Superintendent Single most important job of the School Board. Only individual School Board actually employs and evaluates. Directs and holds Superintendent accountable for

implementation of School Board Policy and overall School District performance.

School Board is legally required to approve all employment contracts, however,

School Board delegates authority to Superintendent to select, employ and evaluate all other employees within the standards established by School Board policy.

Clarifies the District Purpose Per IASB, “as its primary task, the School Board

continually defines, re-defines and articulates district ends to answer the recurring question – who gets what benefits for how much?”

As Steven Covey states: “Begin with the End in Mind”. Knowing where you want to be as a School District will help you to establish your mission, values and goals providing clear direction to all involved.

Clearly established goals allows the School Board to easily monitor the District performance holding the organization accountable.

Board Connects with the Community Per IASB “the purpose of the conversation is to

enable the Board to hear and understand the community’s educational aspirations and desires, to serve effectively as an advocate for district improvement and to inform the community of the district’s performance”.

How does your Board communicate? Comment time at meetings, web site, email, twitter,

face book, day/evening coffees, staff coffees, newsletters = transparency, transparency

Board Delegates Authority Difficult for some Board Members! Board is ultimately responsible for everything,

however the Board delegates authority to the Superintendent who delegates to many individuals within the District including the Business Manager.

Successful Boards are able to delegate and empower their Superintendent and staff.

Board Monitors Performance Per IASB “A School Board that pursues its ends

through the delegation of authority has a moral obligation to itself and the community to determine whether that authority is being used as intended”.

Board needs to have a basic understanding of data used within District, both student and financial based data.

Board Takes Responsibility for ItselfThe role the School Board fulfills as trustee

for their constituents cannot be filled by any other person or group – the Board is

ultimately responsible for the operations, success and compliance with State Laws.

Mandatory Board Training Open Meeting Act – Effective 1/1/2012 Board Members elected post 6/13/2011: Minimum 4 hours of professional development

inclusive of: education and labor law, financial oversight and accountability and fiduciary responsibilities.

PERA – Effective 6/13/2011

That’s All Great, But Where Does the Business Manager Fit in? – How do I Build and Sustain My

Relationship with My Board Members??

District’s Are Different! The First Step is to understand how your District

operates in terms of: Board Structure Communication with Board Board Policy Development Trust Between Board & Administrators Documents for the Board Board Involvement in Training & IASB

Don’t Forget CARDINAL RULE: UNDERSTAND clearly your

superintendent’s expectations of your relationship with Board Members!!

History of Relationship between Business Manager and Board Members New to the District - talk to your predecessor about their

relationship with Board. Take all discussions with a grain of salt – what worked for them, might not be your style – what can be changed, what needs to remain the same!

Have a basic understanding of your Board Members professional and personal backgrounds. Hot Buttons? Platforms? Agendas?

Board Structure This is not a cookie cutter approach! All Boards are

unique with their own personality! How Does your Board Operate:

Committee of the Whole? Board Committees with only Board members Board Committees plus community members Board Committees plus other administrators Board Committees plus community members & other

administrators, Etc., Etc., Etc.,!!!!!! Don’t forget – What authority do these committees have?

How Do You Communicate? Here is where having a clear understanding of your

superintendent’s expectations will come in handy! Again, possibilities are endless:

Individual Board member can email you questions: You respond only to that Board member, You forward question and your response to superintendent

who will respond to Board member(s), You respond only to that Board member and superintendent, You respond to entire Board and superintendent.

If not already established, early in your tenure, talk with your superintendent and possibly entire Board on their preferences for communication.

A Few Last Words on Communication Methods

Please Note in Ink!!! Established methods are subject to change!!!

New Superintendent – new methods New Board President – potential new methods.

And your mantra: Transparency, Transparency, Transparency!!

School Board Policy Development Well developed School Board Policy has been found to

make your life easier in some respects….. Does your Board just implement/approve policy

pushed out by IASB? Does your Board and superintendent allow you to

further develop policies unique to your district that are associated with finance and operations of the District?

What Exactly Do You Do All Day? Or, Why Does Our District Need You?

In meeting with new Board Members it is critical that they have a basic understanding of your role and responsibilities in the District!

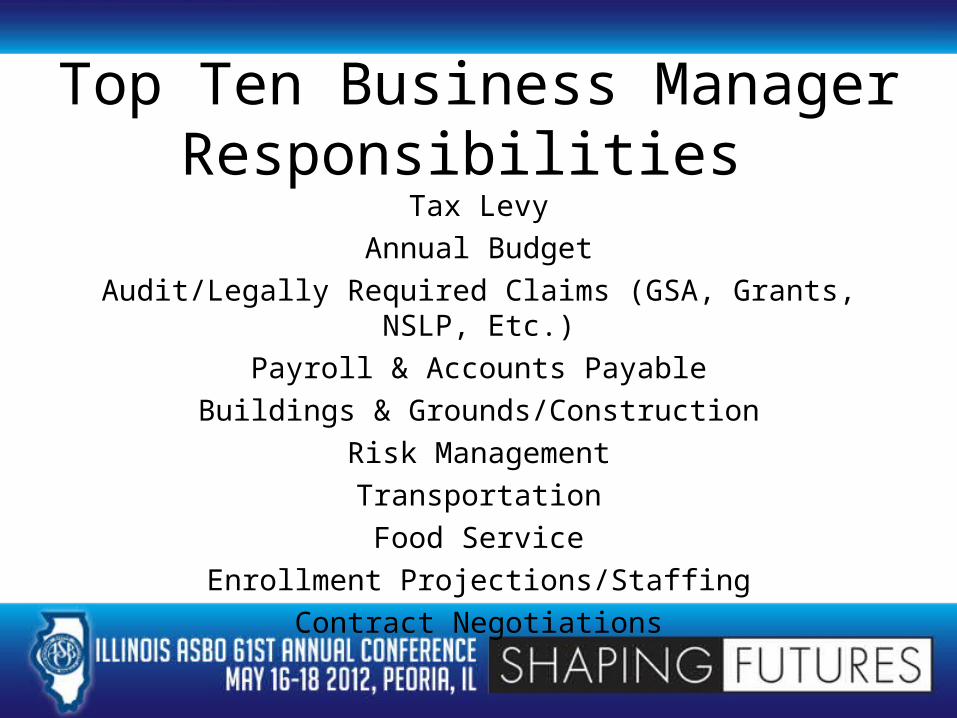

Top Ten Business Manager Responsibilities

Tax LevyAnnual Budget

Audit/Legally Required Claims (GSA, Grants, NSLP, Etc.)Payroll & Accounts Payable

Buildings & Grounds/ConstructionRisk Management

TransportationFood Service

Enrollment Projections/StaffingContract Negotiations

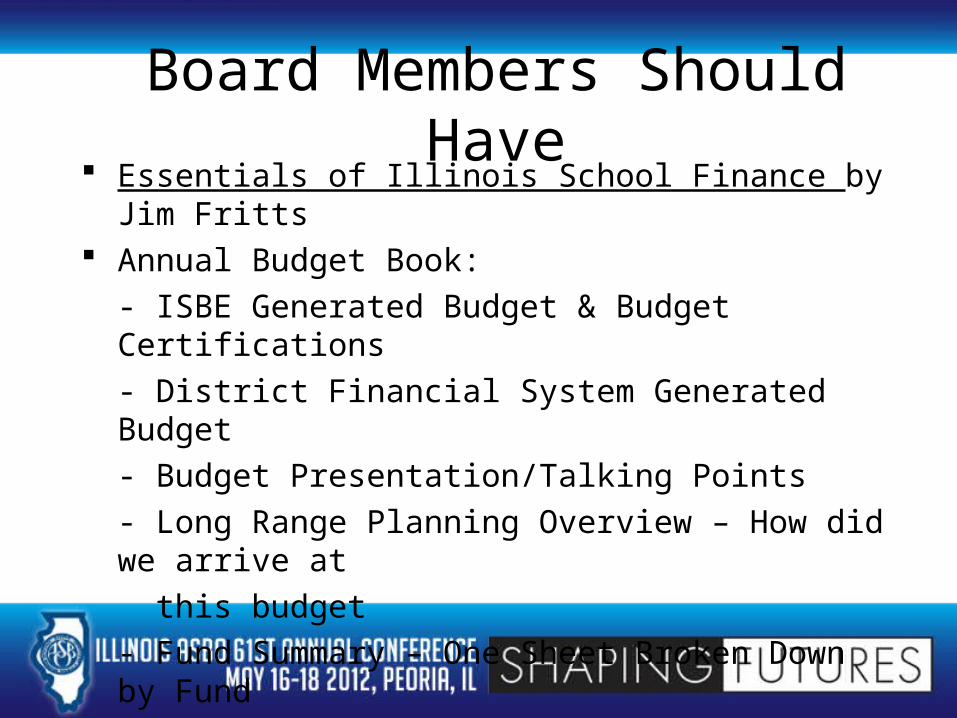

Board Members Should Have Essentials of Illinois School Finance by Jim Fritts Annual Budget Book:

- ISBE Generated Budget & Budget Certifications- District Financial System Generated Budget- Budget Presentation/Talking Points- Long Range Planning Overview – How did we arrive at this budget- Fund Summary – One Sheet Broken Down by Fund- Tax Levy- GSA Entitlement

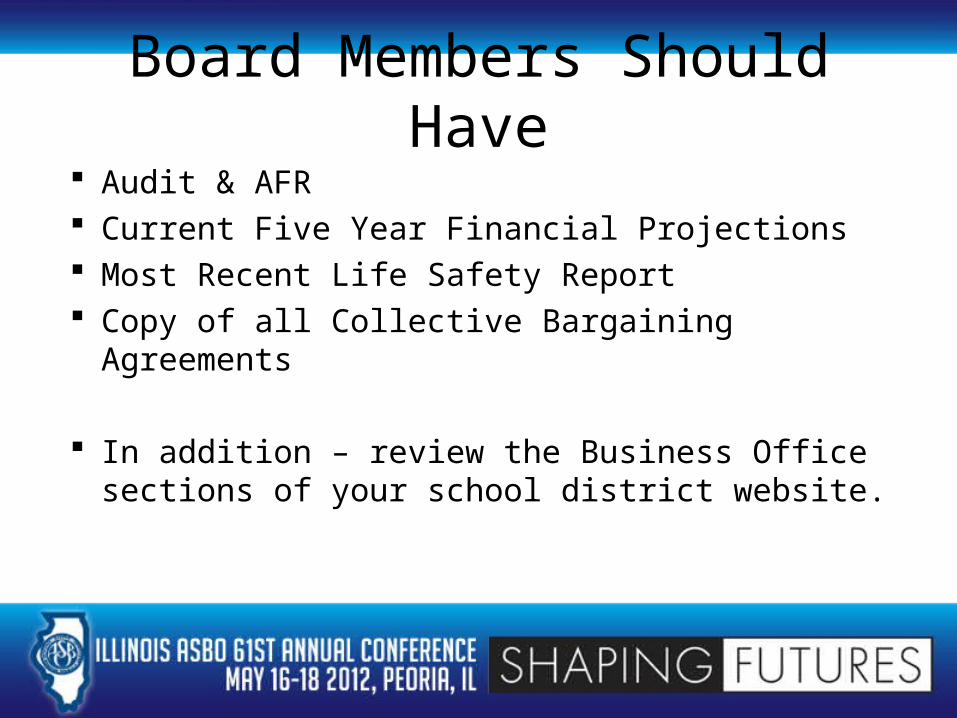

Board Members Should Have Audit & AFR Current Five Year Financial Projections Most Recent Life Safety Report Copy of all Collective Bargaining Agreements

In addition – review the Business Office sections of your school district website.

Finance Toolbox

Tools for the Business Manager to use with School Board Members in

Understanding School Finance

Simplify the High Level Concepts

Budget

Tax Levy

Investing

Borrowing

FUND ACCOUNTING

10 - Education 20 - Operations &

Maintenance 40 - Transportation 50 - IMRF/Social

Security 70 - Working Cash

OPERATING FUNDS OTHER FUNDS 30 - Debt Service 60 - Capital Projects 80 - Tort Immunity 90 - Health/Life Safety

A Good Resource

How is school income determined?

• Property Values

• Tax Rates

• State Appropriations & Federal Aid

• Pupil Enrollment

Revenue (Federal)• Block Grants - usually based on student

population and need. Focus resources on handicapped children, economically disadvantaged students and other targeted special purposes.

• National School Lunch Program

Revenue (State)• General State Aid - Unrestricted. The greater the

property value results in less General State Aid to the district per student. Based on average daily attendance.

• Categorical Aid - Restricted. Underwrites state required programs such as lunch program, transportation and special education.

• Grants - Restricted. Block and Matching

GSA & the Foundation Level (State)• The State Legislature increases General State Aid (GSA)

each year by increasing the foundation level.

• $6,119 in FY13 - $5,631?

• General assembly boasts that each school district will receive $X more per student

• GSA formula reduces foundation level by local “wealth”. Divide it!

Property Values

•Determines how much revenue the district is capable of raising from property taxes.

•Property value is set by the marketplace, the ability to access it is affected by the tax cap.

Tax Rate

•Maximum tax rates are established by the State of Illinois

•Can be raised above the maximum only with approval of voters.

•Tax cap keeps the tax rate lower than the approved level.

Revenue (Local)

Revenue (Local - Other)

•School Fees

•Lunch Fees

•Rental Income

Who decides how the district spends the money?

1. Determined by Board of Education based on recommendations from administrators through program decisions and negotiated contracts.

2. More and more budget decisions however are forced on boards by mandates beyond the board’s control (federal and state).

LaGrange School District 102

BUDGET PRESENTATION

FISCAL YEAR 2012

All Funds SummaryCHANGES FROM TENTATIVE TO FINAL BUDGET

• Final Stimulus Payment Received $187,945 • Added Retirement Penalty Budget $142,000• Salary & Benefits Increase $178,611 • Reduced Supply Budget $20,000• Construction Loan $2,000,000• Net Effect: $1,887,334

Operating Funds SummaryPRELIMINARY RESULTS FOR FY11:

• Operating Fund Balance $1.5m Favorable Variance• Deliberate Cost Savings Measures• Conservative Estimates• Teacher Contribution $660,000 over next two years

• State of Illinois Owed $1.1 Million from FY11• Promised by December• Will Receive Four Payments in FY12

04/19/23

Purchased Services

DESCRIPTION BUDGET

S/E Tuition to LEA's $650,000

S/E Transportation $517,011

Regular Transportation $341,662

Cleaning Service $279,046

Professional Development $189,501

Food Service $170,512

TRS Penalty/Bonus $142,000

Worker's Comp $132,749

Telephone $130,900

Property/Liability Ins. $110,536

Legal $110,000

Treasurer's Office Fee $107,000

DESCRIPTION BUDGET

Heating/Cooling $100,000

Grounds $72,000

Equipment Service $65,800

Copiers $62,649

Trash $61,500

Auditing $55,000

Technology Repairs $47,340

Substitute Custodians $44,472

Unemployment $43,360

Custodial Equipment $37,500

Water $28,250

Professional Services $24,726

Purchased Services

DESCRIPTION BUDGET

Travel $22,500

Plumbing $21,000

Postage $18,000

Discretionary $17,200

Software $17,115

Testing Services $17,000

S/E Diagnostics $15,000

Building Structure $13,000

Electrical $12,000

Printing $12,000

Miscellaneous (ED) $11,114

Miscellaneous (O&M) $10,300

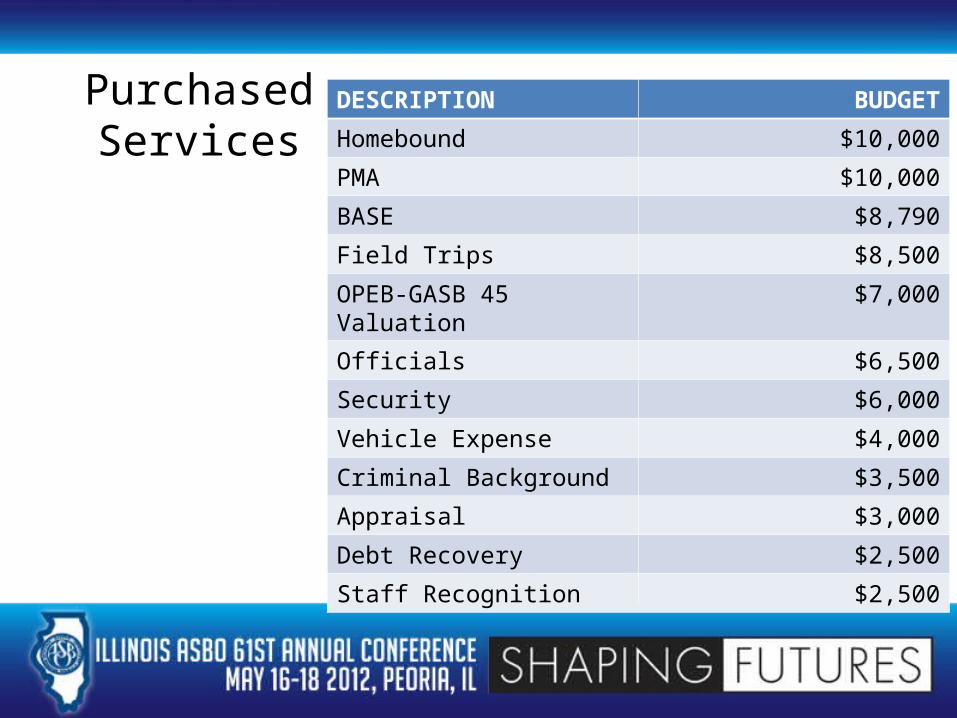

Purchased Services

DESCRIPTION BUDGET

Homebound $10,000

PMA $10,000

BASE $8,790

Field Trips $8,500

OPEB-GASB 45 Valuation $7,000

Officials $6,500

Security $6,000

Vehicle Expense $4,000

Criminal Background $3,500

Appraisal $3,000

Debt Recovery $2,500

Staff Recognition $2,500

Purchased Services

DESCRIPTION BUDGET

Storage $2,000

Graduation $1,500

Travel (O&M) $1,500

Exterminator $1,200

Total $3,788,233

Purchased Services

NON OPERATING FUNDSDebt Service Fund: Tentative Final Preliminary FY 2011

Beginning Fund Balance $1,455,351 $1,455,351 $1,556,281

Revenues $2,577,668 $2,577,668 $2,399,889

Expenditures $2,452,667 $2,452,667 $2,500,819

Ending Fund Balance $1,580,352 $1,580,352 $1,455,351

Capital Projects Fund

Beginning Fund Balance $60,513 $60,513 $1,463,446

Revenues/Loan Proceeds $10,000 $2,010,000 $10,618

Expenditures $1,520,000 $1,520,000 $1,534,217

Ending Fund Balance $1,570,153 $429,487 $60,513

Presented By: Lauri Calabrese

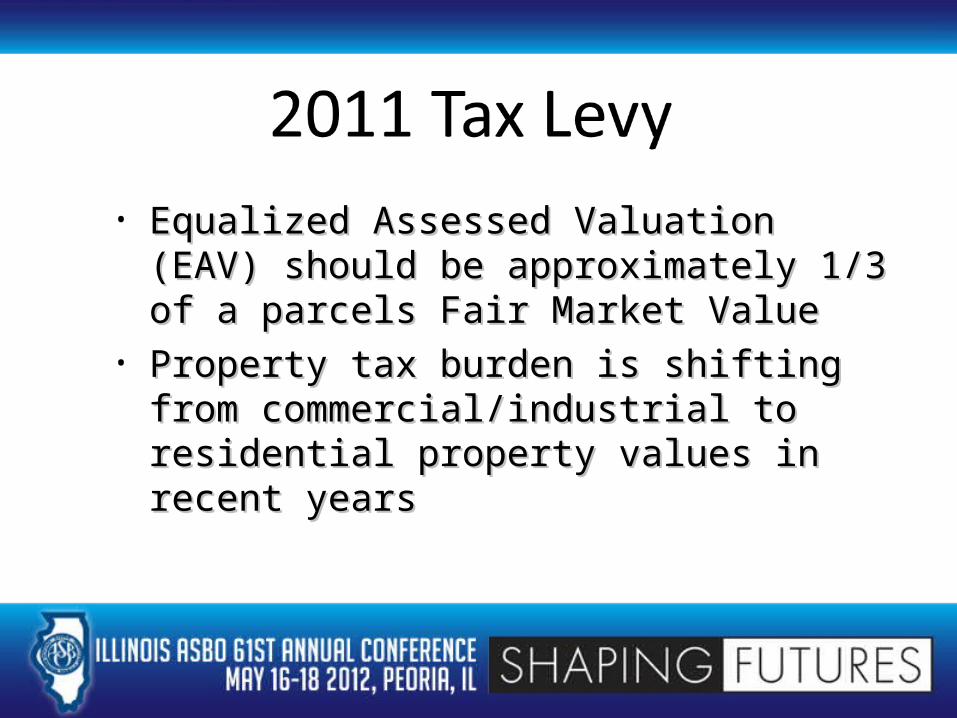

Timeline & Truth in Taxation Act• Tax levy must be estimated twenty days

prior to the adoption• If the proposed levy increase is more than

105%– Public notice must be given via local media – Public hearing must be held

• Tax Levy filed with Cook County by the last Tuesday in December

• Equalized Assessed Valuation (EAV) should be Equalized Assessed Valuation (EAV) should be approximately 1/3 of a parcels Fair Market Valueapproximately 1/3 of a parcels Fair Market Value

• Property tax burden is shifting from Property tax burden is shifting from commercial/industrial to residential property commercial/industrial to residential property values in recent years values in recent years

LEVY YEAR CPI COLLECTED:

2010 Levy 2.7% Spring 2011 FY11

2010 Levy 2.7% Fall 2011 FY12

2011 Levy 1.5% Spring 2012 FY12

2011 Levy 1.5% Fall 2012 FY13

Cook County collects and distributes property taxes as follows:Cook County collects and distributes property taxes as follows:

55% of prior year in the spring and the remainder in the fall55% of prior year in the spring and the remainder in the fall

TAX COLLECTION CYCLE TAX COLLECTION CYCLE

10-Year CPI History

1.5%

2.7%

0.1%

4.1%

2.5%

3.4%3.3%

1.9%2.4%

1.6%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Levy Year

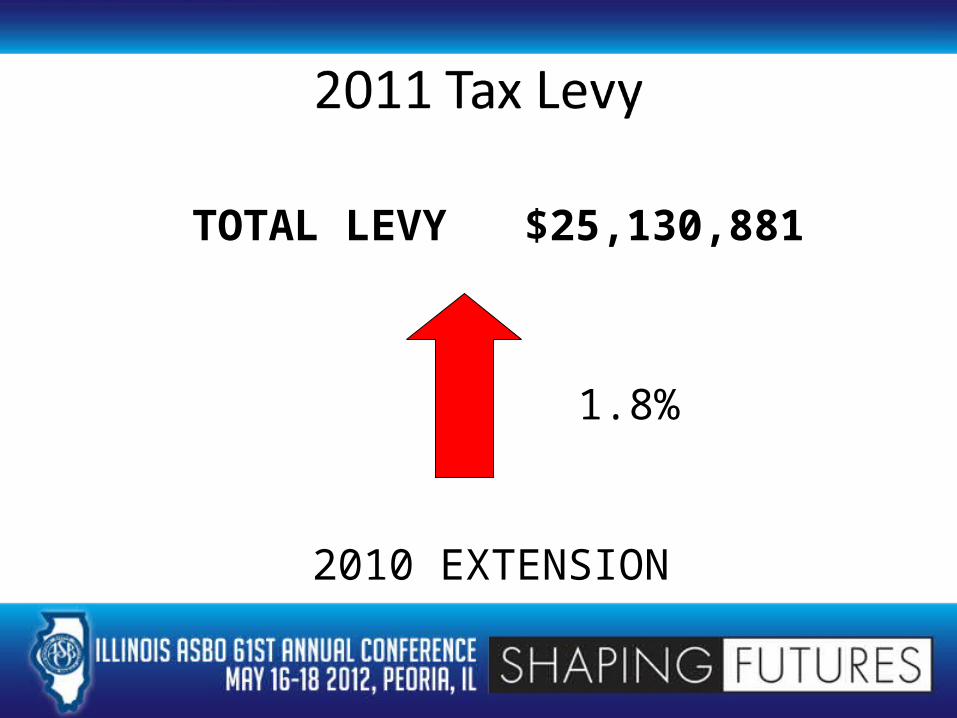

TOTAL LEVY $25,130,881

1.8%

2010 EXTENSION

• Limiting tax rate:– The calculated total allowable tax rate

for all operating funds.

• Bond and interest rate:– The rate for bond and interest payments

is in addition to the limiting rate, and OUTSIDE of the tax cap.

Step 1• Compute the limiting rate

Numerator: Multiply the previous years extension by the CPI

$24,680,171 * 101.5% = $25,050,374Denominator: Subtract the new construction from

current year EAV$931,924,834 - $3,000,000 = $928,924,834

Divide: $25,050,374 / $928,924,834 = 2.6967%

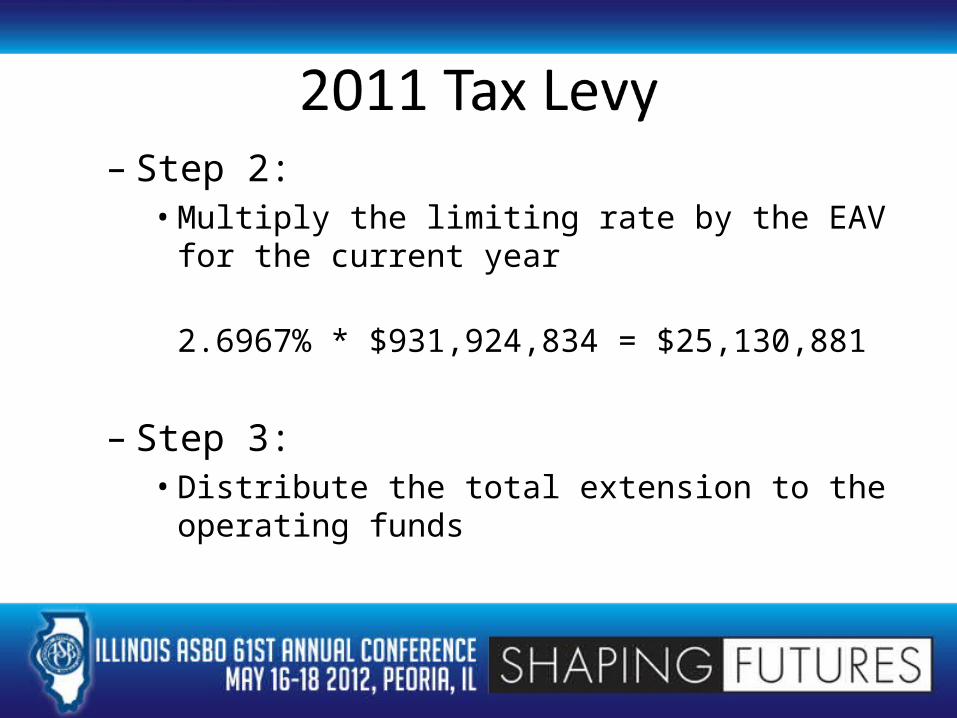

– Step 2:• Multiply the limiting rate by the EAV for the

current year

2.6967% * $931,924,834 = $25,130,881

– Step 3:• Distribute the total extension to the

operating funds

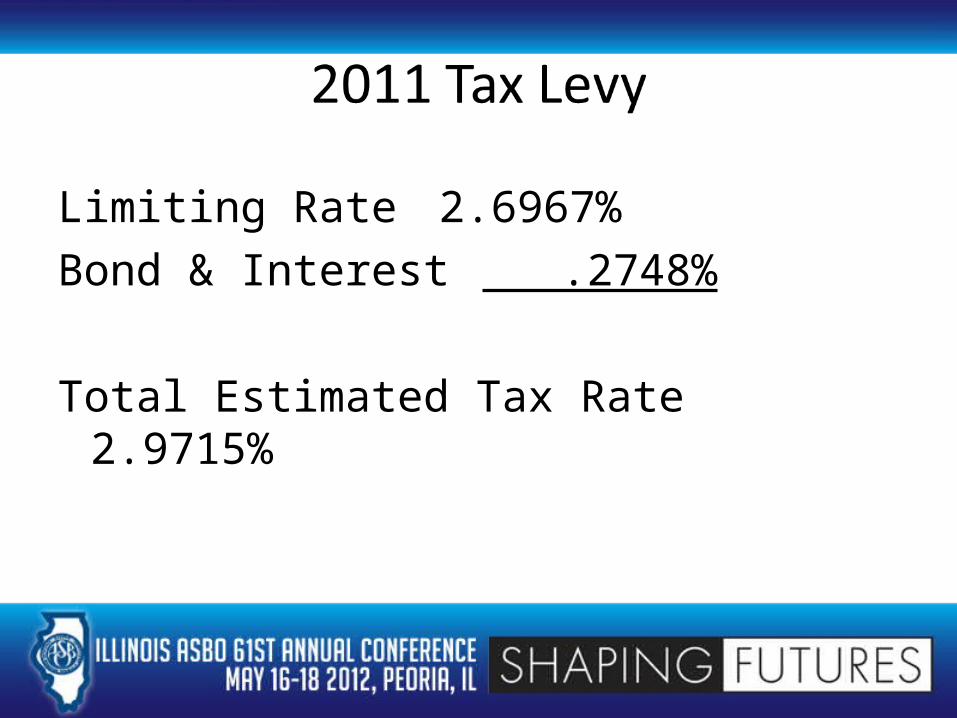

Limiting Rate 2.6967%Bond & Interest .2748%

Total Estimated Tax Rate 2.9715%

Seeking approval of the final Seeking approval of the final resolutions at the December resolutions at the December

8,2011 Board Meeting.8,2011 Board Meeting.

Thank You Thank You

2011Tax LevyNEW PROPERTY & TIFS

•When tax increment financing districts expire they are returned to the tax rolls as new property

•These tax dollars were already being collected, they were just redirected to the municipality for redevelopment projects

•This increase in EAV will not impact individual taxpayers

•Individual resident taxes will adjust based on the new EAV of their individual property and the Consumer Price Index (2.7%)

2011Tax LevyHow TIFs Work

A Tax Bill

3%

5%3%

23%

42%

4%

13%

1%3%

1%1%

Tax Bill-Village of Oak Lawn

Suburban TB Sanitarium

S Cook Mosquito Abatement

Water Reclamation Dist

Oak Lawn Park District

Moraine Valley College Dist

High School District 229

School District 123

Oak Lawn Library Fund

Village of Oak Lawn

Road and Bridge Worth

Worth General Assistance

Town of Worth

Forest Preserve District

County of Cook

Cook County Public Safety

Cook County Health Facil

State of School Funding from State of Illinois

Current Hot Topics:

•Pension Reform•General State Aid Funding •Transportation Funding

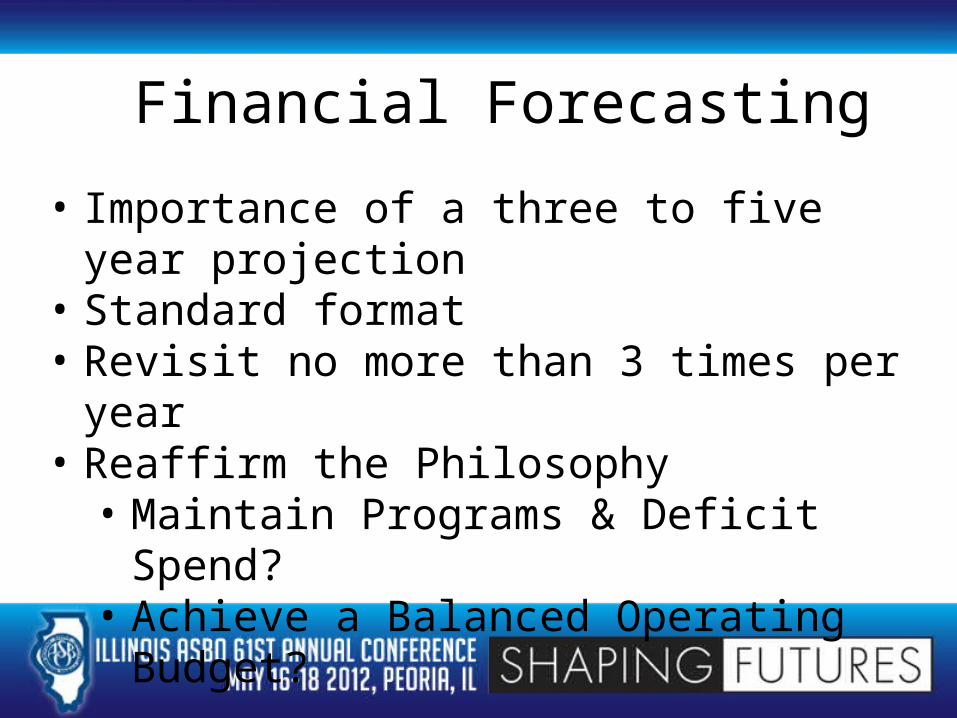

Financial Forecasting

• Importance of a three to five year projection• Standard format• Revisit no more than 3 times per year• Reaffirm the Philosophy

• Maintain Programs & Deficit Spend?• Achieve a Balanced Operating Budget?

Analyze Revenues & Expenses

How are we doing?• Quarterly Benchmarking• Monthly Cost Center Reporting• Dashboards• Monthly Board Run

Financial Profile Score

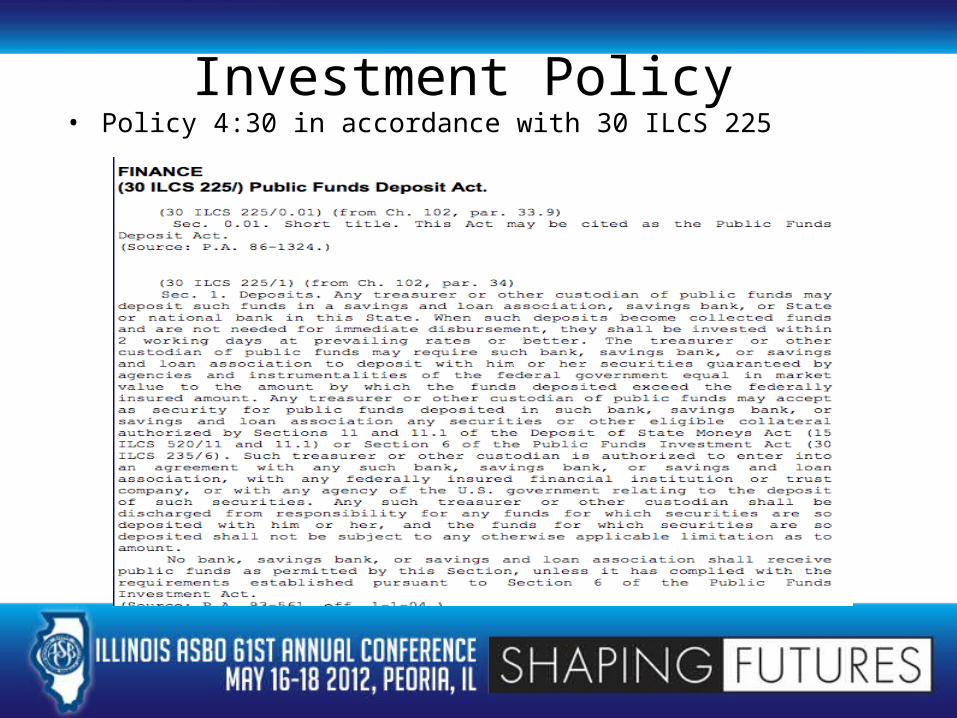

Investment Policy• Policy 4:30 in accordance with 30 ILCS 225

Borrowing• General limit:

– Separate Elementary & H.S. Districts 6.9% EAV– Unit Districts 13.8%

EAV

• Rating Agencies– Long Term Borrowing for Operations

• EAV Changes– & Bond Levy – Be Aware…

Collective bargaining agreements• Review current environment

– How many years is the current agreement?– Is there language that we need to focus on modifying

or removing?– During negotiations what will be our focus?

• Salary schedule• Benefit plan• Language changes

– What is the current relationship with the union?

Operations

Purchasing– Purchasing Official– Purchase Orders– Request for Proposals– Bidding

• Expenses over $25k must be bid ($50k relating to Operations & Maintenance)

• Bids should be awarded to the lowest responsible bidder who conforms in all material aspects to the requirements and criteria set for in the invitation to bid

– In house services– Contracted services– Vendor relations

• Gift ban act

Purchasing-Bidding• Specifications• Vendor selection• Bid opening• Public notice 10 days before• All bids must be sealed• All bids must be opened during a public bid opening where the contents

are announced• Bid analysis

• Low, responsive, responsible• Bids should be awarded to the lowest responsible bidder who

conforms in all material aspects to the requirements and criteria set for in the invitation to bid

• Board approval

Facilities• Describe current environment

– Custodial and Maintenance • Cleaning schedule• Summer/spring/holiday break schedules

– Intergovernmental agreements• An agreement between two or more government to cooperate in

some specific way– Facility planning

• Facility committee• Long range facility plan• Facility inspection schedule

– Life safety• Life safety fund• 10 year life safety survey

Food Service• Describe current environment

– In house or contracted out– Services provided

• Lunch– Free/Reduced participation– National School Lunch Program

• Breakfast• Snack

– Before and after school programs• Milk

– Preschool and kindergarten programs– Nutritional requirements for grant funded programs

Transportation• Describe current environment

– In house• Own or leased bus fleet

– outsourced– Special ed transportation

• Parent concerns often come from this service-be knowledgeable!• Service must be provided for students living 1.5+ miles from the

school• Distances under 1.5 miles may be approved as “serious safety

hazards”• Business Manager or Transportation Director files an annual claim for

reimbursement

Technology• Current environment

– Hardware– Software– Replacement schedule– Telephone system– Copier/printer management– Security

• E-rate program

Risk Management• Lines of Insurance

– Property– General liability– Board legal liability– Student accident insurance– Workers’ compensation

• Insurance Cooperatives– Medical/Dental– Workers’ Compensation– Risk Management

• Unemployment Compensation

School Board Member calendarWhen to do what you do

• July 1st – First day of fiscal year• July/August – Prepare Tentative Budget OR

Hold Public Hearing on the Final Budget (105 ILCS 5/17-1)

• September 30 –last day to adopt the annual budget (105 ILCS 5/17-1).

• October 15 – Annual Financial Report (ISBE 50-35) due

• November IASB, IASA, & IASBO Joint Annual Conference in Chicago

• November 30 – Annual Statement of Affairs due• Last Tuesday in December (December 27) –

Certificate of Tax Levy (ISBE 50-02) due

• December 30 – Last day for the school board to adopt a resolutions putting policy questions on the ballot at the March 20, 2012 General Primary Election. (10 ILCS5/28-2).

• March – Approve Staffing Plan for next fiscal year and release certified staff (if needed) at the March Board Meeting.

• April 1 – School Board must give written notice and reason of intent not to renew Superintendent’s expiring contract (105 ILCS 5/10-21.4)

• May 1 – Statement of Economic Interests: Completed form filed with county clerk (5 ILCS 420/4A-105)

• June 30 – Last day of the fiscal year for most Illinois school districts.

In summary…

• As the Business Official you need to:– Understand the Board Member’s Role– Communicate and work with your Board

Members to help them understand your role as the Business Official.

– Last Piece of Advice – Remember!! Superintendent is the Orchestra Leader! Follow their lead in developing your relationship with your Board of Education.