Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

71

Budget PLUS 2012 Key features of India’s Union Budget 2012 -13

-

Upload

mayank-purohit -

Category

Documents

-

view

216 -

download

0

Transcript of Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 1/71

Budget PLUS 2012Key features of India’s Union Budget 2012-13

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 2/71

March 2012 Budget PLUS 2012Page 2

Presenters

Pranav has been

rated as one of the leading

tax advisors

in India by International

Tax Review & by the

Legal Media Group Guide

to the World’s Leading

Tax Advisers. His area of expertise lies in

international

tax matters, cross border

and domestic mergers,

acquisitions & joint

ventures

Direct Tax

Pranav Sayta

Harishanker (Hari) is

a licensed customs broker.

His domain

of expertise lies in advising

companies

on resolution of

import pricing at

arm’s length on customsspecial valuation

representations, export

incentive programs, cross

border transactions, tax

structuring, and

tax efficient supply chains

Indirect Tax

Harishanker

Subramaniam

Ajay Lalvani is a

Chartered Accountant with

over 25 years of industry

experience. Currently, he

is the Head of Taxation

with Hindustan Unilever

Ltd. responsible for both

Direct and Indirect taxes. Ajay is a regular speaker

on tax & policy issues and

has represented industry

bodies at various

platforms

Industry

Ajay Lalvani

Sudhir has a rich

experience of more than

two decades in advising

multinational companies in

inbound investment

strategies and domestic

companies in relation to

their outbound investmentstrategies, including tax

efficient supply chain and

transfer pricing

Moderator

Sudhir Kapadia

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 3/71

1. Budget backdrop

2. Budget Snapshot

3. Budget 2012

► Key policy

announcements

► Direct Tax proposals

► Indirect Tax proposals

B u

d g e t P L U

S 2

0 1 2Contents

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 4/71

B u

d g e t P L U

S 2

0 1 2

Budget backdrop

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 5/71

March 2012 Budget PLUS 2012Page 5

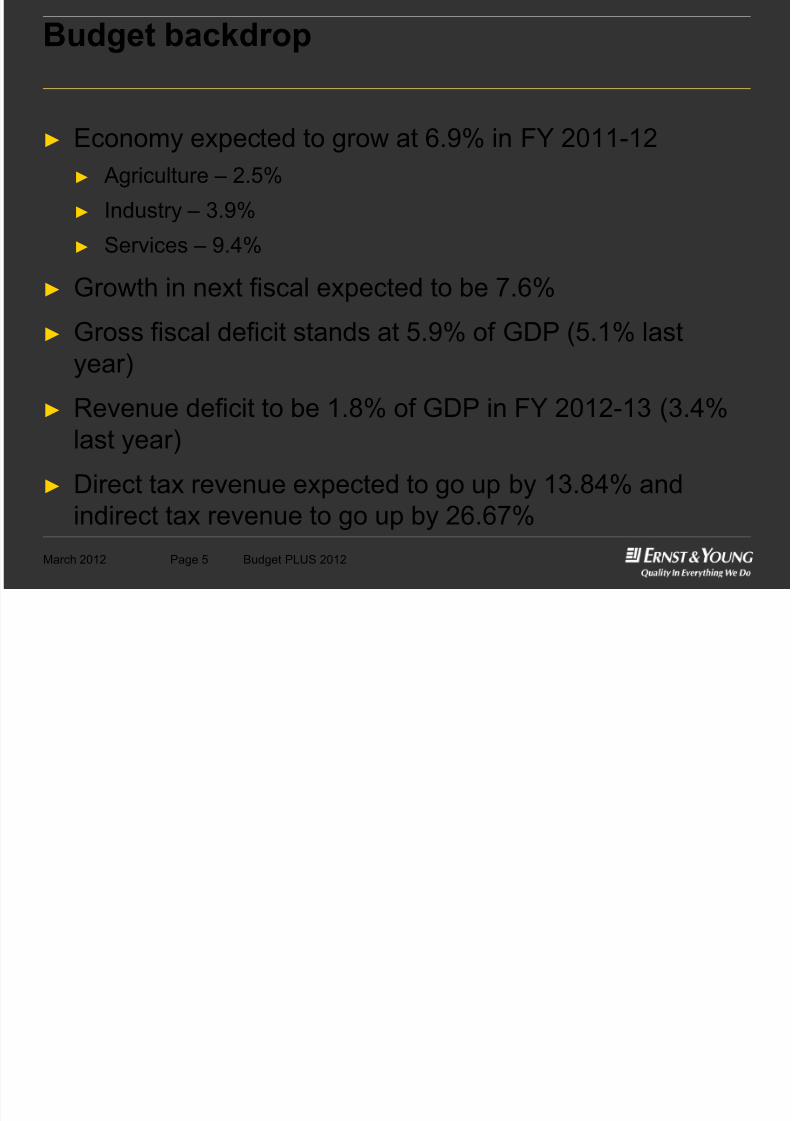

Budget backdrop

► Economy expected to grow at 6.9% in FY 2011-12► Agriculture – 2.5%

► Industry – 3.9%

► Services – 9.4%

► Growth in next fiscal expected to be 7.6%

► Gross fiscal deficit stands at 5.9% of GDP (5.1% last

year)

► Revenue deficit to be 1.8% of GDP in FY 2012-13 (3.4%last year)

► Direct tax revenue expected to go up by 13.84% and

indirect tax revenue to go up by 26.67%

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 6/71

B u

d g e t P L U

S 2

0 1 2

Budget snapshot

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 7/71

March 2012 Budget PLUS 2012Page 7

Budget snapshot

Particulars BEFY 2011-12

REFY 2011-12

BEFY 2012-13

Variance(%)

Particulars (a) (b) (c) of (c)

over (b)

Total Tax Revenues 932,440 901,664 1,077,611 19.51

- Direct Tax Receipts 534,624 502,968 572,567 13.84

- Indirect Tax Receipts 397,816 398,696 505,044 26.67

Non-tax revenues 125,435 124,737 164,614 31.97

Total Expenditure 1,257,729 1,318,720 1,490,925 13.06

- Plan expenditure 441,547 426,604 521,025 22.13- Non-plan expenditure 816,182 892,116 969,900 8.72

Amounts in crores of INR

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 8/71

B u

d g e t P L U

S 2

0 1 2

Budget 2012► Key policy announcements► Direct Tax proposals

► Indirect Tax proposals

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 9/71

B u

d g e t P L U

S 2

0 1 2

Budget 2012► Key policy announcements► Direct Tax proposals

► Indirect Tax proposals

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 10/71

March 2012 Budget PLUS 2012Page 10

Key policy announcements

► Tax reforms► Direct tax code to be enacted at the earliest

► Expeditious examination of the Parliamentary Standing Committee

report expected

► Plan to introduce GST on course

► Drafting of model legislation for Centre and State GST under progress

► Structure of GST IT enabled Network (GSTN) approved - GSTN will

be operational by August 2012

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 11/71

March 2012 Budget PLUS 2012Page 11

Key policy announcements

► Foreign Direct Investment reforms► Efforts to arrive on consensus on FDI in multi-brand retail trade

upto 51%

► Active consideration to allow foreign airlines to participate upto

49% in air transport

► ECB to be allowed for

► financing rupee debt of existing power projects

► capital expenditure for maintenance and operations of toll systems for

roads and highways

► working capital for airline industry► low cost affordable housing projects

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 12/71

March 2012 Budget PLUS 2012Page 12

Key policy announcements

► Financial reforms► Allowing QFIs to access Indian corporate bond market

► IPOs above INR 100 million to be mandatorily issued in electronic

form through stock exchanges

► Permitting two way fungibility in Indian Depository Receipts

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 13/71

March 2012 Budget PLUS 2012Page 13

Key policy announcements

► Other reforms► Amendments to the following bills to be moved during current

session

► Banking Laws (Amendment) Bill

► Insurance Laws (Amendment) Bill

► Following bills to be introduced shortly

► Micro Finance Institutions Bill

► Indian Stamp (Amendment) Bill

► White paper to tackle Black Money to be introduced

► Central KYC depository to be developed

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 14/71

B u

d g e t P L U

S 2

0 1 2

Budget 2012► Key policy announcements► Direct Tax proposals

► Indirect Tax proposals

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 15/71

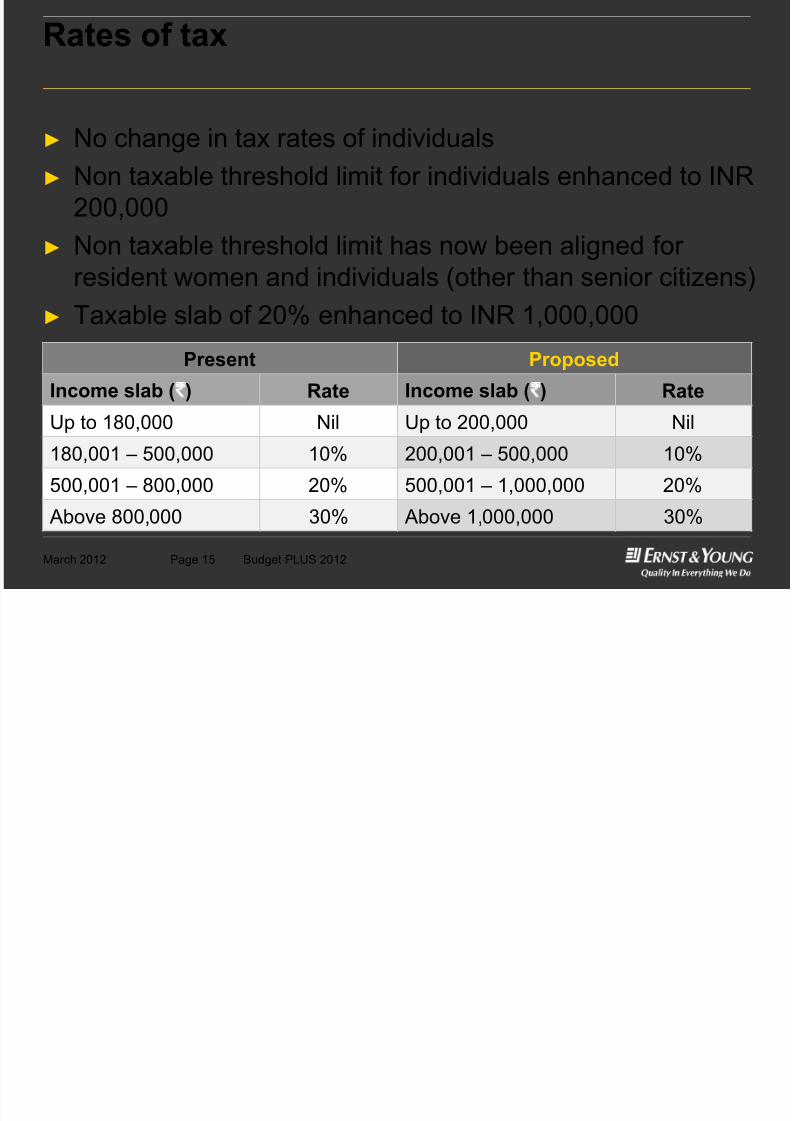

March 2012 Budget PLUS 2012Page 15

Rates of tax

► No change in tax rates of individuals► Non taxable threshold limit for individuals enhanced to INR

200,000

► Non taxable threshold limit has now been aligned for

resident women and individuals (other than senior citizens)► Taxable slab of 20% enhanced to INR 1,000,000

Present Proposed

Income slab ( ) Rate Income slab ( ) Rate

Up to 180,000 Nil Up to 200,000 Nil

180,001 – 500,000 10% 200,001 – 500,000 10%

500,001 – 800,000 20% 500,001 – 1,000,000 20%

Above 800,000 30% Above 1,000,000 30%

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 16/71

March 2012 Budget PLUS 2012Page 16

Rates of tax

► No change in Corporate tax rates

► Securities Transaction Tax on delivery based transactions

of equity shares and mutual fund units reduced to 0.1%

from 0.125%

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 17/71

March 2012 Budget PLUS 2012Page 17

Rates of tax

► Dividend Distribution Tax (DDT)► DDT payable by holding company to be reduced by DDT paid by

subsidiary – now available in multi-tier corporate structure

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 18/71

March 2012 Budget PLUS 2012Page 18

Key international tax proposals

► Indirect transfers► Income deemed to accrue or arise in India ‘through’ transfer of a

capital asset situate in India to include, inter-alia:

► Income deemed to accrue or arise:

► ‘by means of’;

► ‘in consequence of’; or

► ‘by reason of’ transfer of that capital asset

► Share or interest in a company or entity registered or incorporated

outside India deemed to be situated in India

► If it derives its value, directly or indirectly, substantially from Indian

assets

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 19/71

March 2012 Budget PLUS 2012Page 19

Key international tax proposals

► Capital asset definition amended to include► Rights in or in relation to an Indian company, including rights of

management or control or any rights whatsoever

► Transfer definition proposed to be amended to include:

► Disposal of an asset or creating any rights therein

► Directly or indirectly

► Absolutely or conditionally

► Voluntarily or involuntarily

► By way of an agreement (whether entered into or outside India) or

otherwise

► Notwithstanding that the transfer of rights are characterized as beingeffected or dependent upon or flowing from transfer of shares of a

company registered or incorporated outside India

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 20/71

March 2012 Budget PLUS 2012Page 20

Key international tax proposals

► Validation clause proposed to be inserted► To validate all demands raised/ notices sent or purporting to have

been sent prior to coming into force of the validating clause

notwithstanding any judgment or decree of a court / tribunal / other

authority

► Amendments referred to as clarificatory and proposed

with retrospective effect from FY 1961-62

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 21/71

March 2012 Budget PLUS 2012Page 21

Key international tax proposals

► Obligation to withhold tax from payment to non residentsproposed to be made applicable to all persons, resident or

non-resident, irrespective of whether the non resident

payer has

► Residence or place of business or business connection in India;► Any other presence in any other manner whatsoever in India

► Amendments referred to as clarificatory and proposed

with retrospective effect from 1 April 1962

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 22/71

March 2012 Budget PLUS 2012Page 22

Key international tax proposals

► Foreign dividend► Beneficial tax rate of 15% on dividends declared, distributed or

paid by specified foreign company extended for one more year

► Tax Residency Certificate

► Submission of tax residency certificate made a mandatorycondition for availing benefits under any tax treaty

► Meaning of treaty terms

► Terms of treaty clarified through subsequent notifications deemed

to be effective retroactively from later of 1 October 2009 or cominginto force of the tax treaty

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 23/71

March 2012 Budget PLUS 2012Page 23

Key international tax proposals

► It is clarified with retrospective effect that DRP shall havepowers to enhance the variation on matters raised or not

by the assessee

► Direction of the DRP now appealable by the tax authority

with effect from 1 July 2012

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 24/71

March 2012 Budget PLUS 2012Page 24

Anti-avoidance measures

► General Anti-Avoidance Rule (GAAR) to be introduced todeal with aggressive tax planning involving use of

sophisticated structures

► Codification of anti-abuse rules which permit declaration

of an arrangement as an “impermissible avoidancearrangement”

► Impermissible avoidance arrangement is one where the main

purpose or one of the main purposes is to obtain a tax benefit and

satisfy atleast one of the following conditions

► Is not for bona fide business purpose

► Creates rights and obligations which are not normally created between

persons dealing at Arm’s Length Price (ALP)

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 25/71

March 2012 Budget PLUS 2012Page 25

Anti-avoidance measures

► Results, in misuse or abuse of the provisions of the tax law► Lacks commercial substance or is deemed to lack commercial

substance

► “Tax benefit” widely defined to mean

► A reduction, avoidance or deferral of tax, increase in refund of tax

(even if it as a result of a tax treaty), reduction, avoidance or

deferral of tax due to a tax treaty, reduction in tax bases including

increase in loss

► Illustrations of consequences if arrangement is held to be

impermissible avoidance arrangement provided for

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 26/71

March 2012 Budget PLUS 2012Page 26

Anti-avoidance measures

► Onus on the taxpayer to prove that obtaining tax benefit isnot the main purpose

► Tax treaty will not apply once GAAR applies

► Definition of “deemed to lack commercial substance”

introduced

► GAAR applicable prospectively

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 27/71

March 2012 Budget PLUS 2012Page 27

Anti-avoidance measures

If CIT is of the opinion

that GAAR provisions

to be invoked, he shall

refer matter to Approval

Panel

AO to make reference to

CITCIT to hear taxpayer

AO to determine

consequences of impermissible

avoidance arrangement

Approval Panel* shall

either declare the

arrangement to beimpermissible

avoidance arrangement

or otherwise

Final order invoking

GAAR to be passed by

AO after approval of CIT and such order is

appealable directly to

ITAT

* Approval Panel to dispose off the reference within 6 months from the end of the

month in which the reference was made by CIT

Proposed process of applying GAAR

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 28/71

March 2012 Budget PLUS 2012Page 28

Key transfer pricing provisions

► Advance Pricing Agreements (APA)

► APAs to be introduced with effect from 1 July 2012

► CBDT empowered to enter into an APA with any person,

determining the ALP or specifying the manner in which ALP is to

be determined in relation to an international transaction

► APA shall be binding on both the taxpayer and the tax authority for a period not exceeding five years except

► If there is a change in law or facts or where APA obtained by fraud or

misrepresentation

► Appropriate provisions made for modification of return,

assessment, extension of period of limitation, etc. consequent toconclusion of APA

► CBDT given the powers to prescribe a scheme specifying the

manner, form, procedure and any other matters in respect of APA

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 29/71

March 2012 Budget PLUS 2012Page 29

Key transfer pricing provisions

► Scope of transfer pricing provisions to be expanded with

effect from 1 April 2013 by including “specified domestictransaction” if aggregate value of such transactions

exceeds INR 50 million. Specific compliance provisions

introduced

►

International transactions to include transactions inrelation to tangible / intangible property, financing

including debt arising in course of business, provision of

services and business restructuring (irrespective whether

such restructuring has effect on income in year of the

transaction)► Intangible property widely defined to include intangibles in

relation to marketing, technology, artistic, data processing,

engineering, customer, contract, etc.

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 30/71

March 2012 Budget PLUS 2012Page 30

Key transfer pricing provisions

► Determination of ALP

► Upper ceiling of 3% to apply to percentage of allowable variation

between the ALP and the transfer price

► New allowable variation is yet to be notified

► Earlier allowable variation of 5% to apply to all the assessment or

reassessment proceedings pending before assessing officer as on1 October 2009

► Clarified with retrospective effect that assessee not entitled to the

benefit of the earlier allowable variation of 5% as a standard

deduction

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 31/71

March 2012 Budget PLUS 2012Page 31

Key transfer pricing provisions

► With effect from 1 June 2002 TPO empowered to examineany international transaction whether or not referred by

the AO

► No reopening of any proceedings to be triggered only on account

of such adjustment

► Penalty @ 2% to apply for non-reporting of transactions in

accountants report in Form 3CEB

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 32/71

March 2012 Budget PLUS 2012Page 32

Widening of tax net

► Tax withholding on transfer of immovable properties► Tax to be withheld at the rate of 1% in case of transfer of

immovable property after 30 September 2012, if the consideration

exceeds

► INR 5 million for property in an urban agglomeration

► INR 2 million for property in any other area

► Stamp duty value to be deemed as consideration, if actual

consideration is lower

► Registration of transaction only after submission of proof of

payment of tax

f

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 33/71

March 2012 Budget PLUS 2012Page 33

Widening of tax net

► Definition of royalty expanded► Definition of royalty expanded to cover:

► right for use of or right to use a, computer software (including granting

of a licence) irrespective of the medium through which such right is

transferred

► right, property or information, whether or not (i) the possession or control of it is with the payer, or (ii) it is used directly by the payer, or

(iii) the location is in India

► transmission by satellite (including up-linking, amplification, conversion

for down-linking of any signal), cable, optic fibre or by any other similar

technology

Wid i f t t

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 34/71

March 2012 Budget PLUS 2012Page 34

Widening of tax net

► Scope of levy of Alternate Minimum Tax (AMT) of 18.5%extended to all persons other than companies (earlier

applicable only to Limited Liability Partnerships)

► AMT levy not applicable to individuals / HUFs whose

Adjusted Total Income does not exceed INR 2 million

Wid i f t t

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 35/71

March 2012 Budget PLUS 2012Page 35

Widening of tax net

► Minimum Alternate Tax (MAT)► On disposal of revalued asset, revaluation reserve taken directly to

general reserve to form part of book profits

► Financial accounts prepared by certain companies (for example

insurance, banking, electricity) as per the applicable regulatory

Acts to be taken as basis for computing book profits for MATpurpose

► Fair market value of asset to be taken as full value of

consideration where consideration for transfer of a capital

asset it not attributable or determinable

Wid i f t t

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 36/71

March 2012 Budget PLUS 2012Page 36

Widening of tax net

► Upward revision of daily tonnage income for qualifyingships

Qualifying ship having

net tonnage

Present Proposed

Up to 1,000 Rs 46 for each 100 tons Rs 70 for each 100 tons

1,001 to 10,000 Rs 460 plus Rs 35 for each

100 tons exceeding 1,000

Rs 700 plus Rs 53 for each

100 tons exceeding 1,000

10,001 to 25,000 Rs 3,610 plus Rs 28 for each

100 tons exceeding 10,000

Rs 5,470 plus Rs 42 for each

100 tons exceeding 10,000

Exceeding 25,000 Rs 7,810 plus Rs 19 for each

100 tons exceeding 25,000

Rs 11,770 plus Rs 29 for each

100 tons exceeding 25,000

E ti d d d ti

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 37/71

March 2012 Budget PLUS 2012Page 37

Exemptions and deductions

► Conversion of sole proprietorship/ partnership intocompany

► Cost of acquisition of assets in the hands of successor company

proposed to be that of sole proprietorship or firm in case of tax

exempt conversion with retrospective effect from 1 April 1999

► No requirement for the parent company to issue shares to

itself for amalgamation / demerger transaction to be tax

neutral

E ti d d d ti

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 38/71

March 2012 Budget PLUS 2012Page 38

Exemptions and deductions

► Investment –linked tax incentive of 100% deduction of capital expenditure (other than on land, goodwill and

financial instrument) also extended to :

► Setting up and operating an inland container depot or a container

freight station, a warehousing facility for storage of sugar

► Bee-keeping and production of honey and beeswax

► Incentive increased from 100% to 150% of capital expenditure :

► Setting up and operating a cold chain facility, a warehousing

facility for storage of agricultural produce, a hospital with at least

100 beds for patients

► Developing and building a housing project under a scheme for

affordable housing and Production of fertilizer in India

E ti d d d ti

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 39/71

March 2012 Budget PLUS 2012Page 39

Exemptions and deductions

► Relief from long term capital gains on transfer of residential property (house or plot of land) if

► invested in equity of new start up SME company in the

manufacturing sector ;

► the company utilizes the funds for purchase of new plant &

machinery and

► subject to fulfillment of other conditions

E ti d d d ti

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 40/71

March 2012 Budget PLUS 2012Page 40

Exemptions and deductions

► Weighted deduction benefit at 200% of expenditureincurred on approved in-house scientific research and

development facilities extended for a further period of 5

years i.e up to 31 March 2017

E ti d d d ti

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 41/71

March 2012 Budget PLUS 2012Page 41

Exemptions and deductions

► Exemption of income of SEBI registered Venture CapitalFund (VCF)/Venture Capital Company (VCC)

► Restriction on business of Venture Capital Undertaking (VCU)

removed

► Definition of VCU aligned to SEBI definition

► Income accrual to VCF/VCC now taxable in hands of

investors on accrual basis

► Exemption from applicability of TDS on income paid by

VCF/VCC to investors withdrawn

E emptions and ded ctions

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 42/71

March 2012 Budget PLUS 2012Page 42

Exemptions and deductions

► Tax incentive for funding of certain Infrastructure sectors► Tax rate reduced to 5% for interest received by a non-resident

from companies engaged in the following sectors

► Construction of (i) dam, (ii) port (including inland port), (iii) road, toll

road or bridge, (iv) ships (in a shipyard)

► Operation of aircraft

► Manufacture or production of fertilizers

► Generation, transmission or distribution of power

► Developing an affordable housing project in accordance with the

notified scheme

► Loan should be in foreign currency and may be taken between 1

July 2012 to 1 July 2015 with the previous approval of the Central

Government

Exemptions and deductions

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 43/71

March 2012 Budget PLUS 2012Page 43

Exemptions and deductions

► Additional depreciation for power projects► Benefit of 20% additional initial depreciation extended to new

machinery or plant (other than ships and aircraft) acquired by

entities engaged in the business of generation or generation and

distribution of power

► Deduction in respect of generation, distribution and

transmission of power

► Sunset clause extended to 31 March 2013

►

Insurance policies issued after 1st April, 2012 whereinpremium payable exceeds 10% (formerly 20%) of “capital

sum assured” will not be eligible for deduction/exemption

Measures to counter unaccounted money

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 44/71

March 2012 Budget PLUS 2012Page 44

Measures to counter unaccounted money

► Cash credits► Share application money, share capital, share premium, or other

sum credited in the books of a closely held company to be taxed in

its hands unless the resident shareholder/ subscriber (other than a

registered venture capital fund) explains the nature and source of

the investment

► Taxation of cash credits, unexplained money and

investments, etc.

► Income of such nature to be taxed on a gross basis at the rate of

30%

Measures to counter unaccounted money

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 45/71

March 2012 Budget PLUS 2012Page 45

Measures to counter unaccounted money

► Consideration exceeding fair value of shares► Consideration in excess of fair value received by a closely held

company on issue of shares at a premium to a resident (other than

a registered venture capital fund) to be taxed as income from other

sources

► Fair value to be reckoned based on the higher of the value determinedas per a method to be prescribed or as substantiated by the company

to the assessing officer having regard to the value of the company’s

assets including intangible assets

► Mandatory tax return filing in relation to foreign assets

► Resident taxpayers having any asset (including any financial

interest in any entity) located outside India or signing authority in

any account located outside India mandatorily required to file a

return of income

Measures to counter unaccounted money

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 46/71

March 2012 Budget PLUS 2012Page 46

Measures to counter unaccounted money

► Time limitation for reassessment► Time limit for initiation of reassessment of income/ wealth in a

case where income/ wealth in relation to any asset (including

financial interest in any entity) located outside India has escaped

assessment extended to 17 years from the end of the relevant

financial year ► Provision to be effective retrospectively

Measures to counter unaccounted money

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 47/71

March 2012 Budget PLUS 2012Page 47

Measures to counter unaccounted money

► Penalty on undisclosed income found in search cases► Penalty on undisclosed income in a search initiated on or after

1 July 2012 revised as follows, subject to conditions:

► If undisclosed income is admitted during the search – 10%

► If undisclosed income is not admitted during the course of search but

disclosed in the return of income filed after the search – 20%

► In other cases - 30% to 90%

Rationalization of TDS/ TCS provisions

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 48/71

March 2012 Budget PLUS 2012Page 48

Rationalization of TDS/ TCS provisions

► Deemed date of payment of tax by the resident payee► W.e.f 1 July 2012, deductor who fails to deduct whole or any part

of the tax on payment to resident deductee shall not be deemed to

be an assessee in default if the resident deductee has:

► furnished his return of income under section 139

► taken into account such sum for computing his taxable income in histax return

► paid tax due on the above income

► Deductor to furnish a certificate from an accountant in the

prescribed form for the above

► Interest under section 201(1A) payable from the date on which tax

was deductible to the date of furnishing the tax return by the

resident deductee

Rationalization of TDS/ TCS provisions

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 49/71

March 2012 Budget PLUS 2012Page 49

Rationalization of TDS/ TCS provisions

► Similar amendments for TCS provisions to clarify the deemed dateof discharge of tax liablity by the buyer/ licensee/ lessee

► Date of furnishing tax return by the resident deductee

deemed to be the date of deduction and payment of tax

by the deductor for the purpose of allowance of business

expenditure under section 40(a)(ia) for the relevant FY

► Fee/ penalty for delay in furnishing TDS/TCS statement

and incorrect information enhanced/ introduced (with

effect from 1 July 2012)

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 50/71

B u d g e t P L U S 2

0 1 2

Budget 2012► Key policy announcements► Direct Tax proposals

► Indirect Tax proposals

Service tax

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 51/71

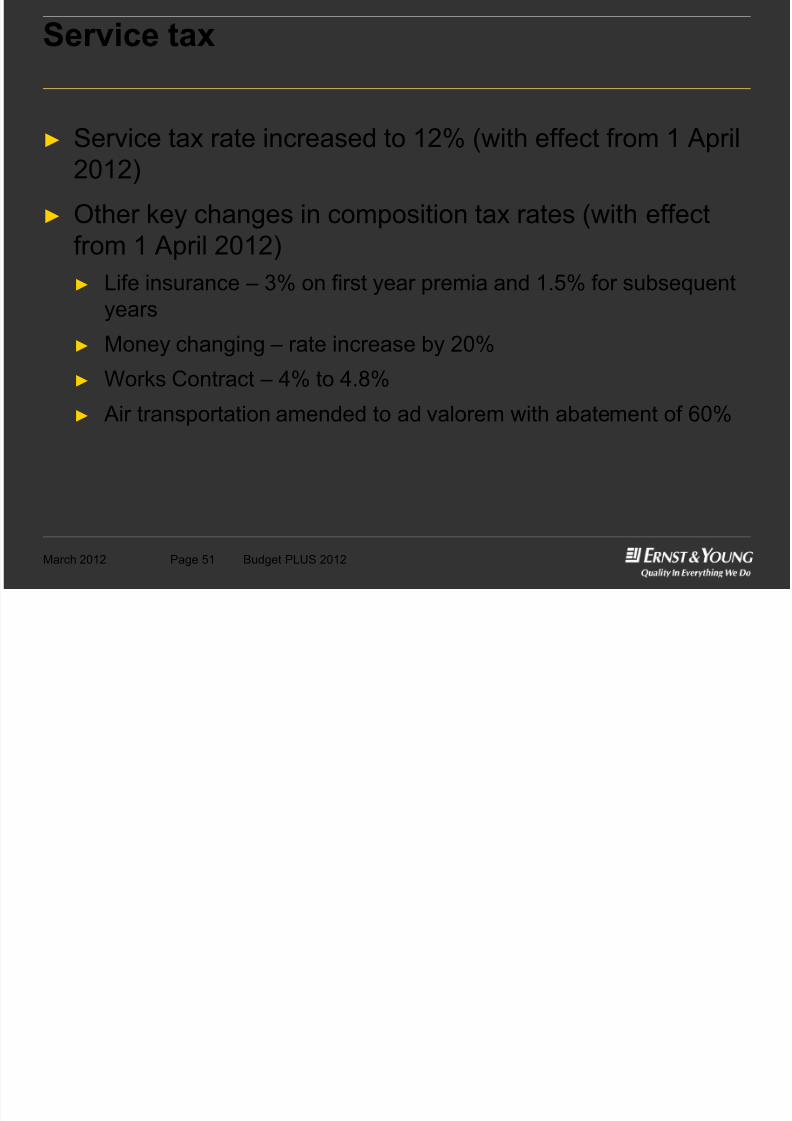

March 2012 Budget PLUS 2012Page 51

Service tax

► Service tax rate increased to 12% (with effect from 1 April2012)

► Other key changes in composition tax rates (with effect

from 1 April 2012)

► Life insurance – 3% on first year premia and 1.5% for subsequentyears

► Money changing – rate increase by 20%

► Works Contract – 4% to 4.8%

► Air transportation amended to ad valorem with abatement of 60%

Service tax

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 52/71

March 2012 Budget PLUS 2012Page 52

Service tax

► Proposal to introduce Negative List basis of levy of service tax► Any service now taxable unless included in Negative List or

exempt

► Deeming fiction – 9 declared services included such as renting of

immovable property, construction of complex, temporary transfer of IPR, agreeing to an obligation to refrain from an act or tolerate an act

► List of 17 services to be included in the Negative List, such as:

► Services provided by Government, RBI, local authority

► Trading of goods

► Services relating to agriculture► Process amounting to manufacture

► Selling of time and space for advertisements (other than radio/

television)

► Access to road/ bridge

Service tax

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 53/71

March 2012 Budget PLUS 2012Page 53

Service tax

► Admission to entertainment events or access to amusement facilities

► Renting of residential property

► Interest or discount on loans, advances and deposits

► Specific exemptions also proposed to be introduced, such as:

► Health care services

► Services provided by individual advocates and journalists

► Construction of specific infrastructure such as roads

► Copyright to cinematographic films

► Services of sports persons, folk and classical arts, etc.

► Rules of interpretation for determining taxability under NegativeList

► Existing exemptions to be removed (limited to 10)

► Detailed guidance note on Negative List issued

Service tax

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 54/71

March 2012 Budget PLUS 2012Page 54

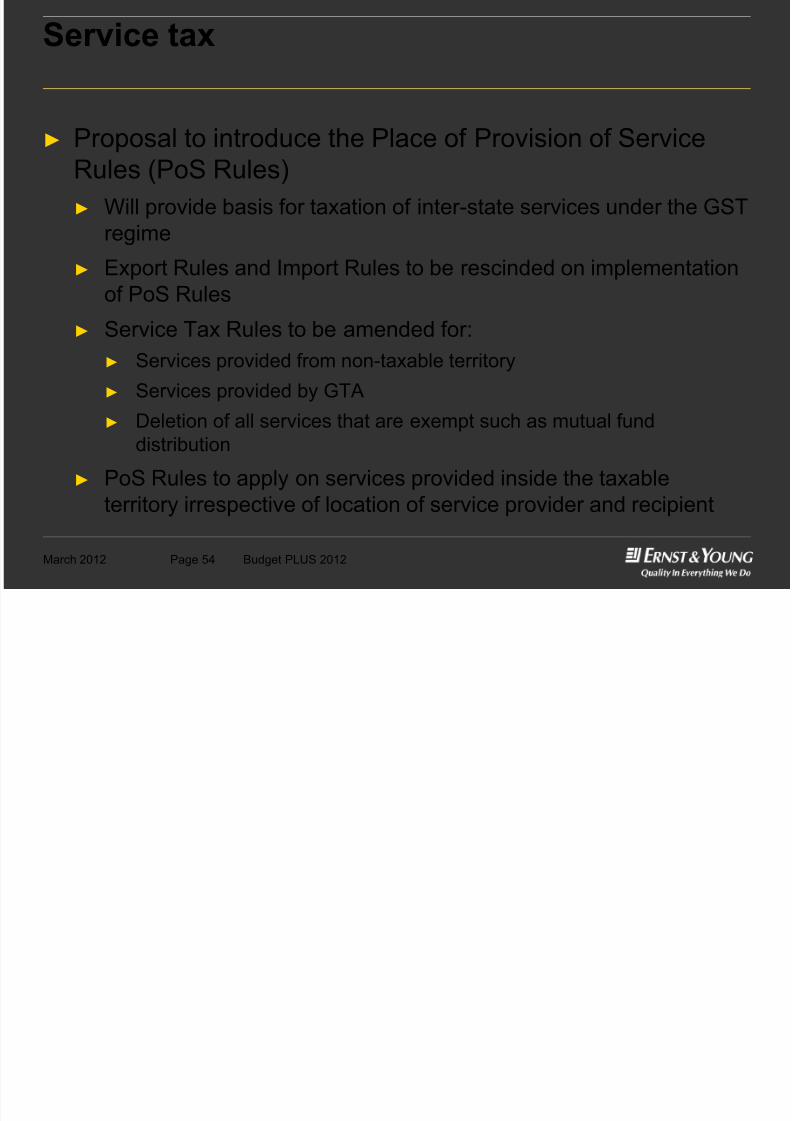

Service tax

► Proposal to introduce the Place of Provision of ServiceRules (PoS Rules)

► Will provide basis for taxation of inter-state services under the GST

regime

► Export Rules and Import Rules to be rescinded on implementation

of PoS Rules

► Service Tax Rules to be amended for:

► Services provided from non-taxable territory

► Services provided by GTA

► Deletion of all services that are exempt such as mutual funddistribution

► PoS Rules to apply on services provided inside the taxable

territory irrespective of location of service provider and recipient

Service tax

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 55/71

March 2012 Budget PLUS 2012Page 55

Service tax

► Impact on export of services on introduction of PoS Rules► Provisions relating to export to form part of Service Tax Rules

► Conditions of export

► Service provider located in taxable territory

► Service recipient located outside India

► Service not included in negative List

► PoS outside India

► Payment received in convertible foreign exchange

► To be notified from a date post assent of Finance Bill

Service tax

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 56/71

March 2012 Budget PLUS 2012Page 56

Service tax

► Impact on import of services on introduction of PoS Rules► Definition of taxable territory – services tax applicable on services

provided in taxable territory

► Jammu & Kashmir (J&K) excluded

► Services received from J&K into taxable territory taxable under reverse

charge

► For specified services the reverse charge liability to be shared by

service provider and service recipient

► Supply of manpower

► Works contract services

► Hiring of motor vehicles

► To be notified from a date post assent of Finance Bill

Service tax

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 57/71

March 2012 Budget PLUS 2012Page 57

Service tax

► Impact on Valuation Rules► New valuation rules for works contract services

► 40% original works i.e. new contructions and all types of additions/

alterations to make damaged structures workable

► 60% for other work contracts

► 25% for construction contracts where consideration received beforeconsideration

► Total value to include gross amount plus value of material supplied

under same or separate contract

► Credit on goods forming part of property not available

► New rates of abatement on services, such as:

► Coastal shipping (50%)

► Railway passengers (new levy – 70%)

► Outdoor catering (40%) and restaurant services (60%)

Service tax

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 58/71

March 2012 Budget PLUS 2012Page 58

Service tax

► Inclusions in the value of taxable service:► Any amounts realised for service beyond period originally

contracted such as demurrage

► Exclusions from value of taxable service:

► Interest on deposits and delayed payment (interest on loans to beexempt – credit available on actual basis in lieu of current adhoc

50%)

► Charges towards accidental damage due to unforseen actions not

relatable to the service

Service tax

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 59/71

March 2012 Budget PLUS 2012Page 59

Service tax

► Amendments to the Point of Taxation Rules, 2011 (PoTRules) (effective 1 April 2012)

► Time period for raising invoice extended to 30 days

► 45 day relaxation for banks and financial institutions

► PoT for exported services and 8 specified services provided by

individuals/ firms shifted to payment basis (up to turnover of INR 5

million)

► Amendment to definition of ‘continuous supply’

► Rationailisation of provision on rate of tax applicable on continuous

supply► Specific rule for determining PoT in case of proposed change in

rate with effect from 1 April 2012

► Provision to determine PoT based on best judgment introduced

Service tax

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 60/71

March 2012 Budget PLUS 2012Page 60

Service tax

► Amendments to Service Tax Rules, 1994► Alignment of service tax and excise procedures (with effect from

from date to be notified)

► Common PAN based tax code

► Common registration format

► Common returns

► Simplification of return format (Form EST-1)

► Monthly service tax returns for large assessees

► Adjustment of excess service tax paid allowed without limits (with

effect from 1 April 2012)

Service tax

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 61/71

March 2012 Budget PLUS 2012Page 61

Service tax

► Amendments to assessment procedures► Special audit provisions proposed

► Time period to issue notice increased 18 months (from 12 months)

► Limitation period for appeals aligned with central excise

► Provisions relating to settlement commission introduced

► Provisions for revision mechanism introduced in alignment

with central excise

Service tax

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 62/71

March 2012 Budget PLUS 2012Page 62

Service tax

► Amnesty from 100% penalty for renting of immovableproperty services (enactment of Finance Bill)

► If tax along with interest up to 6 March 2012 paid within 6 months

from enactment of the Finance Bill

► Retrospective effect to exemption notifications (enactmentof Finance Bill)

► Repair of roads with effect from 16 June 2005 (earlier from July

2009)

► Management, maintenance or repair of non-commercial

Government building with effect from 16 June 2005 (tillintroduction of Negative List)

Customs duty

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 63/71

March 2012 Budget PLUS 2012Page 63

Customs duty

► Rates effective from 17 March 2012► Peak rate maintained at 10%

► CVD enhanced from 10% to 12% due to increase in central excise

levy

► Education Cess and Secondary and Higher Education Cess on

CVD exempted

► Effective peak rate of customs duty enhanced to 28.85%

from 26.85%

► Duty free baggage allowances enhanced► Adults - INR 25000 to INR 35000

► Children (upto 10 years) – INR 12000 to INR 15000

Customs duty – effective 17 March 2012

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 64/71

March 2012 Budget PLUS 2012Page 64

Customs duty effective 17 March 2012

► BCD increased on certain products such asPresent Proposed

Products Rate Rate

Large cars, MUVs, SUVs 60% 75%

Flat rolled products of non-alloy steel 5% 7.5%

Cut and polished coloured gems NIL 2%

Digital Still Cameras NIL 10%

Standard gold / platinum bars 2% 4%

► BCD reduced on certain products such asPresent Proposed

Products Rate Rate

Isolated soya protein 15% 10%

Specified life saving drugs/ vaccines

and their bulk drugs

10% 5%

Customs duty – effective 17 March 2012

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 65/71

March 2012 Budget PLUS 2012Page 65

Custo s duty e ect e a c 0

► BCD fully exempted on certain products such as► Initial setting up and substantial expansion of fertilizer projects –

valid till 31 March 2015

► Steam Coal – valid till 31 March 2014

► Natural gas / LNG imported for power generation by a power

generating company► Equipment imported for road construction projects awarded by

Metropolitan Development Authorities

► Goods for Coal mining under Project Imports

► Parts of aircraft and testing equipment imported for maintenance

and repair of aircraft by third party MRO units► CVD exempted on foreign going vessels imported into

India subject to payment of duty if converted for coastal

run

Customs duty

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 66/71

March 2012 Budget PLUS 2012Page 66

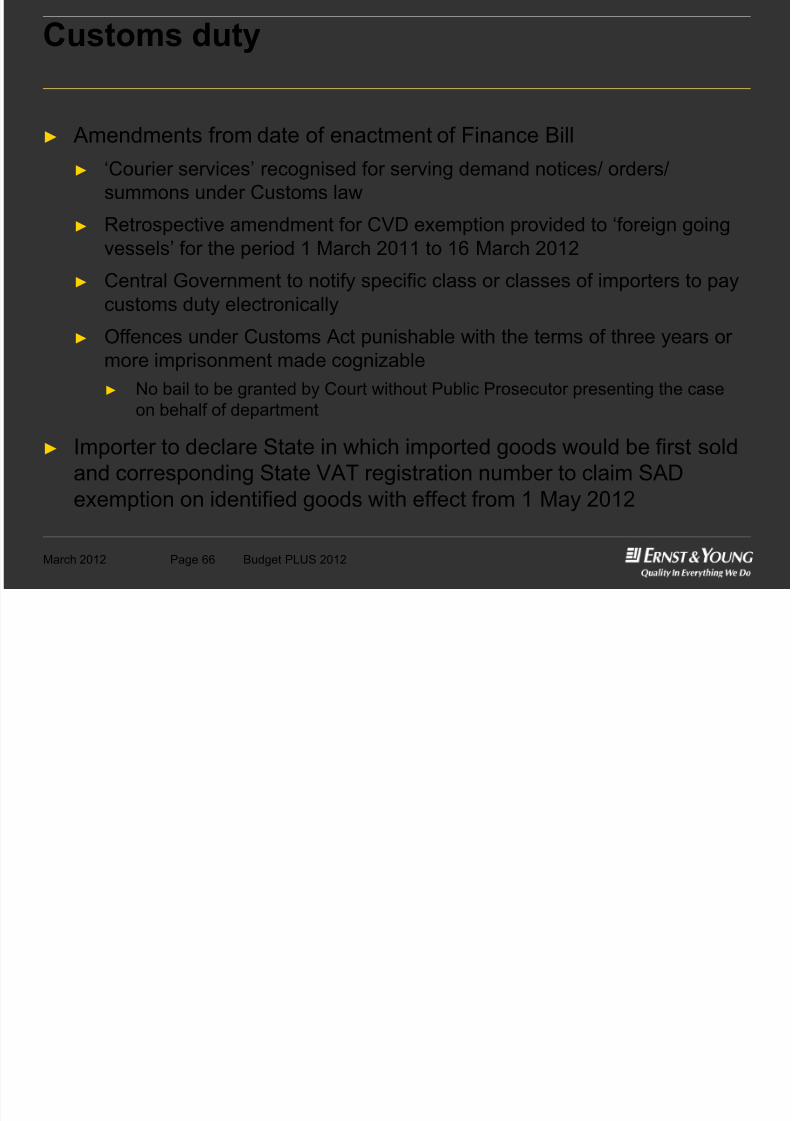

y

► Amendments from date of enactment of Finance Bill

► ‘Courier services’ recognised for serving demand notices/ orders/

summons under Customs law

► Retrospective amendment for CVD exemption provided to ‘foreign going

vessels’ for the period 1 March 2011 to 16 March 2012

► Central Government to notify specific class or classes of importers to paycustoms duty electronically

► Offences under Customs Act punishable with the terms of three years or

more imprisonment made cognizable

► No bail to be granted by Court without Public Prosecutor presenting the case

on behalf of department

► Importer to declare State in which imported goods would be first sold

and corresponding State VAT registration number to claim SAD

exemption on identified goods with effect from 1 May 2012

Cenvat credit

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 67/71

March 2012 Budget PLUS 2012Page 67

► Input credit allowed for excise duty/ CVD on specifiedmotor vehicles

► Refund scheme for service exporters simplified

► Rules to determine the manner of distribution of credit by

Input Service distributors specified

► Manufacturer entitled to transfer the unutilized credit of

SAD to other premises on a quarterly basis

► Interest payable only on wrong utilisation of credit

Central excise

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 68/71

March 2012 Budget PLUS 2012Page 68

► Median rate of Central Excise Duty enhanced from 10.3%to 12.36% with effect from 17 March 2012

► Duty increases across the board, including products liable

to lower rates (1 to 2%, 5 to 6%)

► Key products being cars, foodstuff, computer parts,foreign going vessels, etc.

► Cess on indigenous crude increased to Rs 4500 per tonne

► Excise duty reduced on branded textile articles, parts of

hybrid vehicles, memory cards, etc.

► Offences punishable for more than 3 years imprisonment

to be cognizable

Goods and Service Tax (GST) and Central

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 69/71

March 2012 Budget PLUS 2012Page 69

( )Sales Tax (CST)

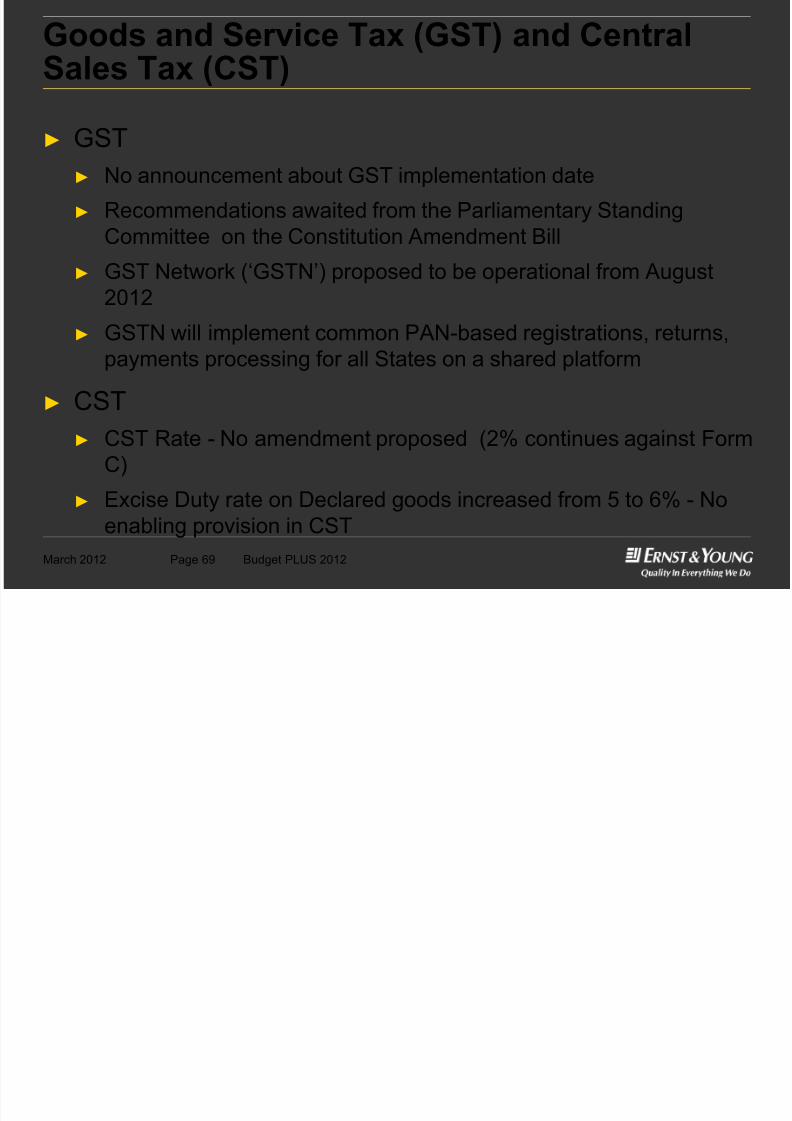

► GST► No announcement about GST implementation date

► Recommendations awaited from the Parliamentary Standing

Committee on the Constitution Amendment Bill

► GST Network (‘GSTN’) proposed to be operational from August

2012

► GSTN will implement common PAN-based registrations, returns,

payments processing for all States on a shared platform

► CST

► CST Rate - No amendment proposed (2% continues against Form

C)

► Excise Duty rate on Declared goods increased from 5 to 6% - No

enabling provision in CST

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 70/71

Questions?

This presentation contains information in summary form and is

therefore intended for general guidance only. It is not intended to

be a substitute for detailed research or the exercise of

professional judgment. Neither Ernst & Young Pvt. Ltd. nor any

other member of the global Ernst & Young organization can

accept any responsibility for loss occasioned to any person acting

or refraining from action as a result of any material in this

publication. On any specific matter, reference should be made to

the appropriate advisor.

Visit our India Budget 2012 webpage to read our

published thought leadership series on the Union

Budget 2012-13.

You may also visit our Tax & Regulatory Services

webpage to know more about our services.

7/31/2019 Budget PLUS 2012-Key Features of Indias Union Budget 2012-13-16March

http://slidepdf.com/reader/full/budget-plus-2012-key-features-of-indias-union-budget-2012-13-16march 71/71

Ernst & Young Pvt. Ltd.

© 2012 Ernst & Young. All Rights Reserved.

Ernst & Young is a registered trademark.

www.ey.com/india

![Indias Future[571]](https://static.fdocuments.us/doc/165x107/577d35651a28ab3a6b905299/indias-future571.jpg)