Profitability and Financial Performance Indicators in U.S ...

Upload

mark-slyterCategory

view

14download

0

How well do hospitals budget operating results? The relationship between budget variances and operating margin

A dissertation by Mark Slyter

HOW WELL DO HOSPITALS BUDGET OPERATING RESULTS? THE RELATIONSHIP BETWEEN BUDGET VARIANCES

AND OPERATING MARGIN

by

MARK F. SLYTER

S. ROBERT HERNANDEZ, COMMITTEE CHAIR NANCY M. BORKOWSKI

LARRY R. HEARLD DEAN G. SMITH

A DISSERTATION

Submitted to the graduate faculty of The University of Alabama at Birmingham, in partial fulfillment of the requirements for the degree of

Doctor of Science in Health Services Administration

BIRMINGHAM, ALABAMA

2016

ProQuest Number:

All rights reserved

INFORMATION TO ALL USERSThe quality of this reproduction is dependent upon the quality of the copy submitted.

In the unlikely event that the author did not send a complete manuscriptand there are missing pages, these will be noted. Also, if material had to be removed,

a note will indicate the deletion.

ProQuest

Published by ProQuest LLC ( ). Copyright of the Dissertation is held by the Author.

All rights reserved.This work is protected against unauthorized copying under Title 17, United States Code

Microform Edition © ProQuest LLC.

ProQuest LLC.789 East Eisenhower Parkway

P.O. Box 1346Ann Arbor, MI 48106 - 1346

10246287

10246287

2016

Copyright by Mark. F. Slyter

2016

iii

HOW WELL DO HOSPITALS BUDGET OPERATING RESULTS? THE RELATIONSHIP BETWEEN BUDGET VARIANCES

AND OPERATING MARGIN

MARK F. SLYTER

DOCTOR OF SCIENCE IN HEALTH SERVICES ADMINISTRATION

ABSTRACT

There is a near-universal assumption in both practice and literature that greater

accuracy and management to the budget improves profitability (Libby & Lindsay, 2010;

Umapathy, 1987). Prior to this study, this assumption has gone untested and we know

little about the wisdom of such an assumption.

The results of this study indicate greater accuracy in forecasting and/or tighter

management to the budget, or favorably exceeding it, leads to improved profitability.

More specifically, smaller unfavorable budget variances are associated with greater

operating margins while greater favorable budget variances are associated with greater

operating margins. A single standard deviation reduction in unfavorable revenue and

expense increases operating margin by 5.2% and 6.3%, respectively. An equivalent

favorable deviation in revenue and expense increases operating margin by 3.2% and

2.7%, respectively. Managers can improve hospitals’ operating margins by first

prioritizing the reduction and/or eliminating unfavorable variances, and second increasing

favorable variances.

Keywords: hospital, budget, variances, profitability, financial performance, multiple

linear regression

iv

DEDICATION

This dissertation is dedicated to my mother, Hazel Holt Slyter, who provided

consistent and positive reinforcement and encouragement as well as to my wife, Lisa

Slyter, and children, Catherine, Emma and Christian, for their patience and support in

attaining my life goal of a doctoral degree.

v

ACKNOWLEDGEMENTS

Sincere appreciation to the faculty and staff of the University of Alabama at

Birmingham School of Health Professions for their assistance and direction. Special

thanks to my dissertation committee Bob Hernandez, Nancy Borkowski, Larry Hearld,

and Dean Smith.

vi

TABLE OF CONTENTS

Page

ABSTRACT ................................................................................................................... iii

DEDICATION ............................................................................................................... iv

ACKNOWLEDGEMENTS ........................................................................................... v

LIST OF TABLES ......................................................................................................... viii

LIST OF FIGURES ....................................................................................................... ix

CHAPTER

1 INTRODUCTION ................................................................................................... 1

Significance of Study ................................................................................... 6 Research Question and Hypotheses ............................................................. 8 Plan of Work ................................................................................................ 8

2 LITERATURE REVIEW ........................................................................................ 10

The Purpose of Budgeting and Its Potential Influence on Performance ...... 10 Planning ................................................................................................. 12 Coordination .......................................................................................... 14 Oversight ................................................................................................ 15 Motivation .............................................................................................. 16 Motivation and the Expectancy Theory ................................................. 17

Criticisms of Budgeting ............................................................................... 19 The Relationship of Hospital Characteristics to Performance ..................... 21 Control Theory ............................................................................................. 25

3 RESEARCH METHODOLOGY............................................................................. 30

Data Sources and Collections ...................................................................... 30 Measures ...................................................................................................... 31 Research Question and Hypothesis .............................................................. 31 Data Preparation........................................................................................... 32 Data Analysis ............................................................................................... 37

vii

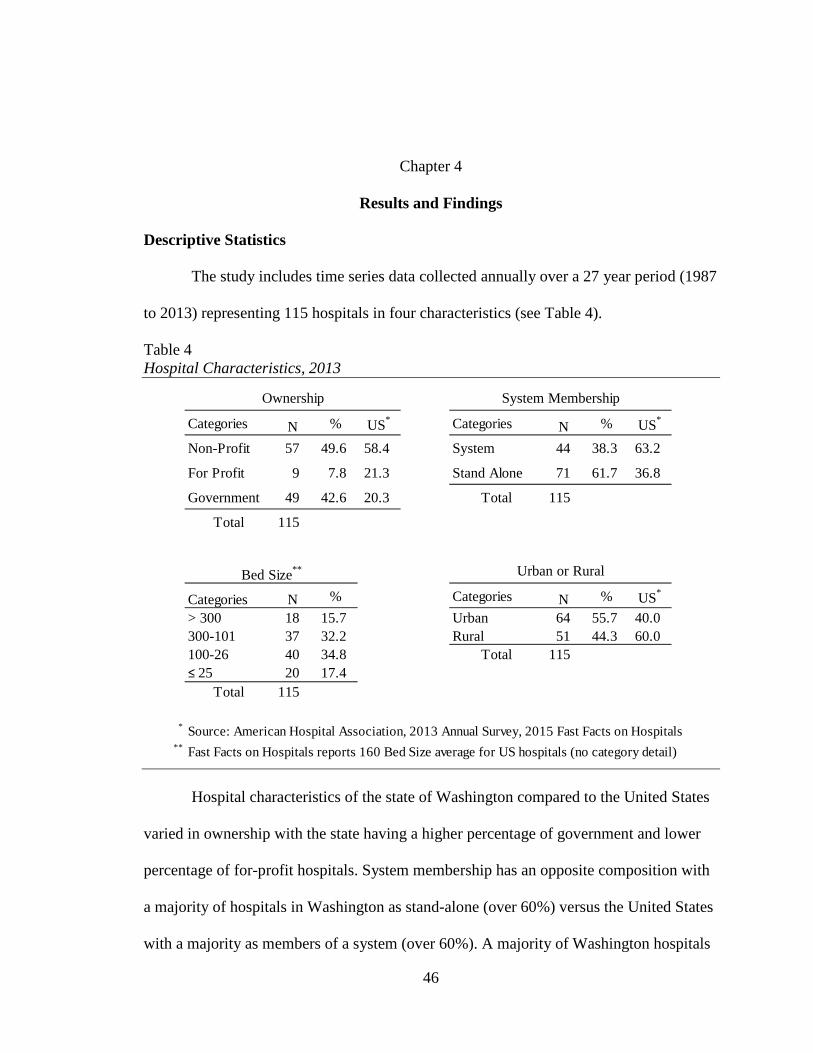

4 RESULTS AND FINDINGS ................................................................................... 46

Descriptive Statistics .................................................................................... 46 Research Question and Hypotheses ............................................................. 50

Page

5 SUMMARY AND CONCLUSIONS ...................................................................... 63

Purpose of Study: Research Question and Hypotheses ............................... 63 Discussion and Findings .............................................................................. 64 Limitations ................................................................................................... 66 Recommendation for Future Research ......................................................... 66 Final Conclusions......................................................................................... 68

6 LIST OF REFERENCES ......................................................................................... 69

7 APPENDIX .............................................................................................................. 89

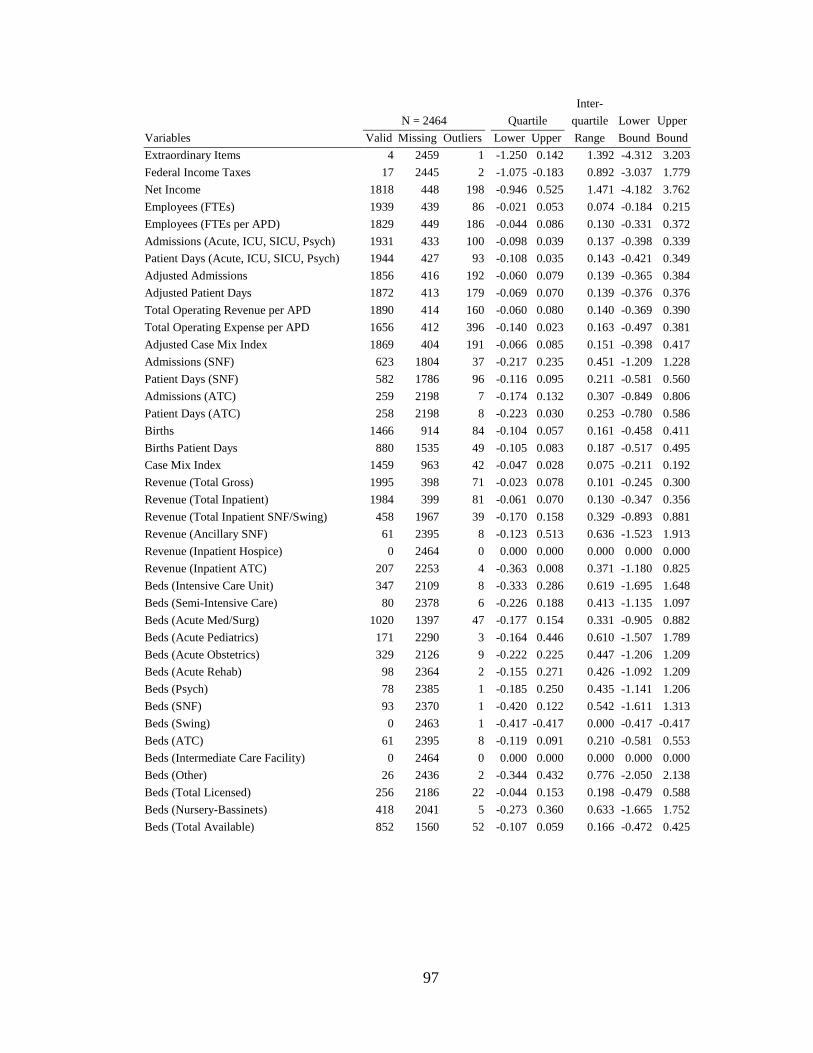

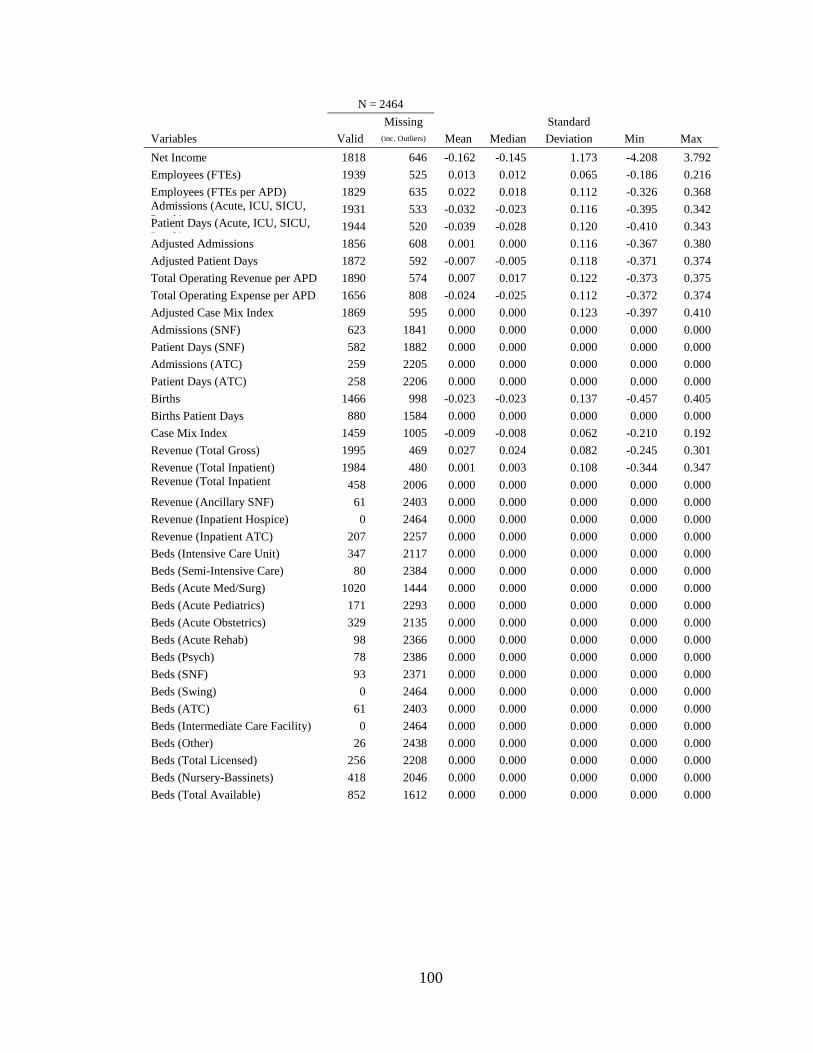

A Hospitals and Hospital Characteristics ........................................................ 89

B Quartile and Boundary Statistics (Dataset) .................................................. 95

C Descriptive Statistics (Dataset) .................................................................... 98

D University of Alabama at Birmingham Institutional Review Board

Letter of Approval........................................................................................ 101

viii

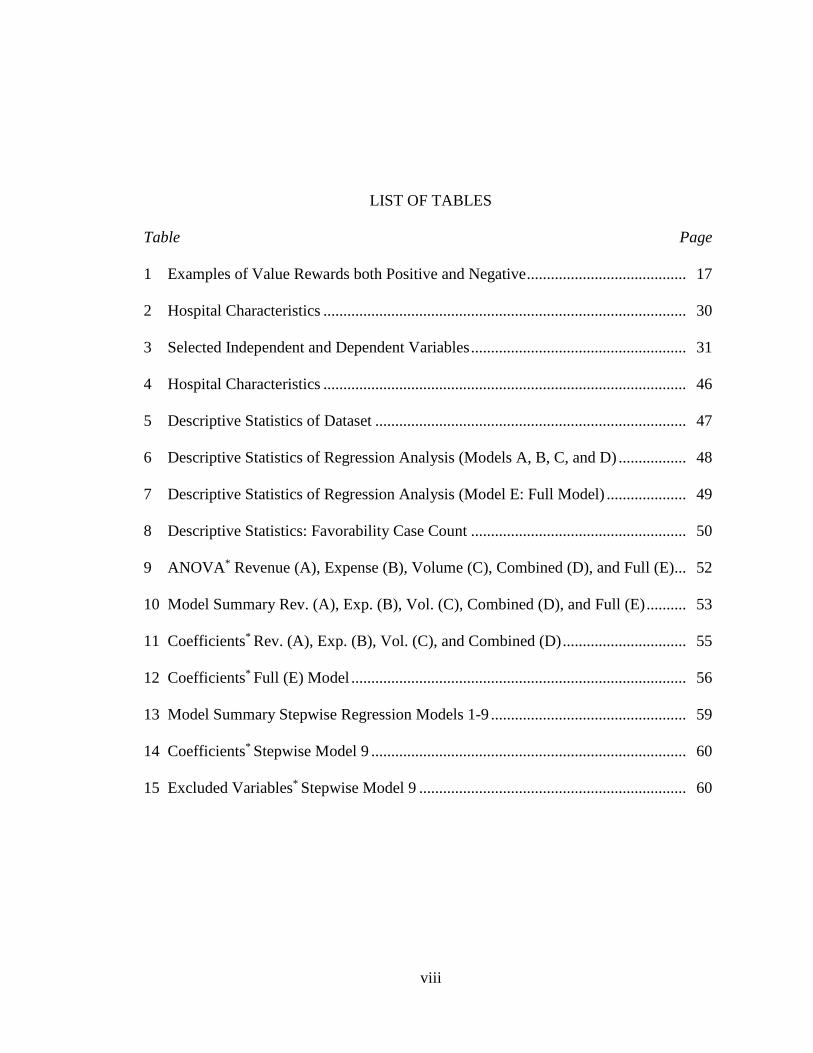

LIST OF TABLES

Table Page

1 Examples of Value Rewards both Positive and Negative ........................................ 17

2 Hospital Characteristics ........................................................................................... 30

3 Selected Independent and Dependent Variables ...................................................... 31

4 Hospital Characteristics ........................................................................................... 46

5 Descriptive Statistics of Dataset .............................................................................. 47

6 Descriptive Statistics of Regression Analysis (Models A, B, C, and D) ................. 48

7 Descriptive Statistics of Regression Analysis (Model E: Full Model) .................... 49

8 Descriptive Statistics: Favorability Case Count ...................................................... 50

9 ANOVA* Revenue (A), Expense (B), Volume (C), Combined (D), and Full (E) ... 52

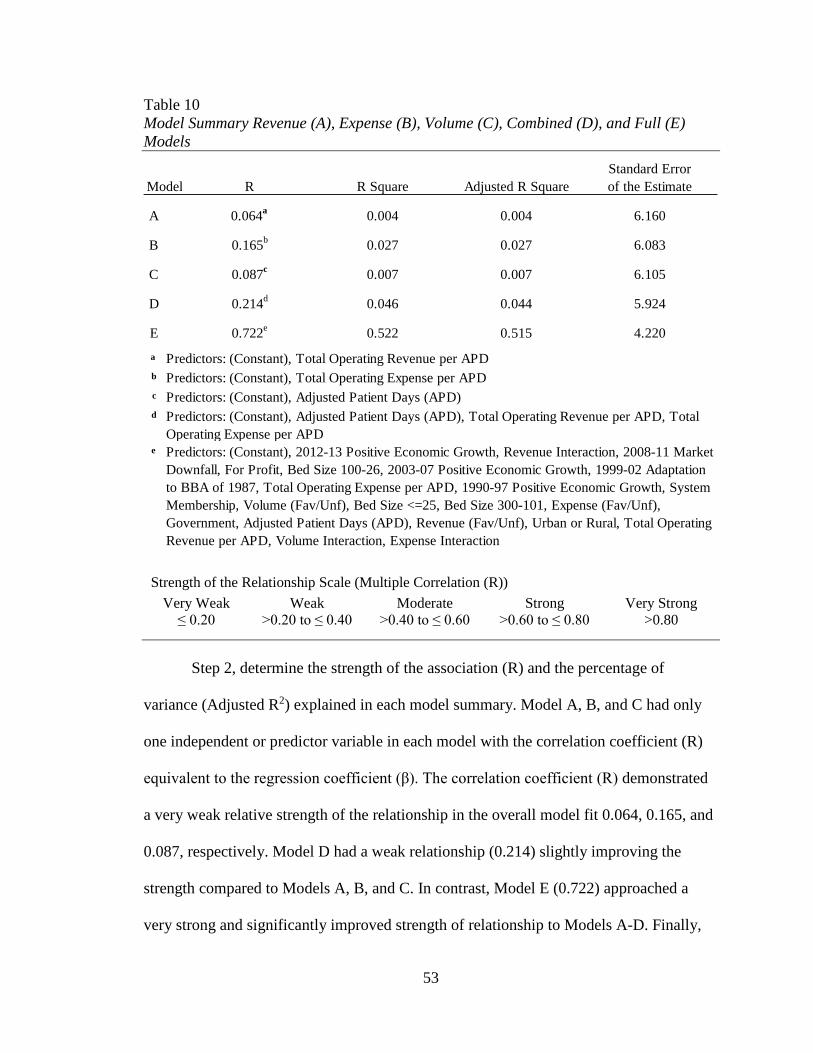

10 Model Summary Rev. (A), Exp. (B), Vol. (C), Combined (D), and Full (E) .......... 53

11 Coefficients* Rev. (A), Exp. (B), Vol. (C), and Combined (D) ............................... 55

12 Coefficients* Full (E) Model .................................................................................... 56

13 Model Summary Stepwise Regression Models 1-9 ................................................. 59

14 Coefficients* Stepwise Model 9 ............................................................................... 60

15 Excluded Variables* Stepwise Model 9 ................................................................... 60

ix

LIST OF FIGURES

Figure Page

1 Hospital closures in the United States, 1987-2012 .................................................. 4

2 Hospital mergers in the United States, 1998-2014 .................................................. 6

3 Components of the budgeting process ..................................................................... 11

4 Traditional annual budgeting process ...................................................................... 21

5 Control theory and budgets ...................................................................................... 27

6 Variance formulas for independent variables (X) .................................................... 32

7 Favorable/unfavorable variance formulas for independent variables (X) ............... 33

8 Favorable/unfavorable dummy variable formulas ................................................... 34

9 Favorable/unfavorable budget variance interaction formulas .................................. 34

10 Operating margin formula ........................................................................................ 35

11 Outlier formulas for lower and upper bounds .......................................................... 35

12 Hospital characteristics dummy variable formulas .................................................. 36

13 Time dummy variable formulas ............................................................................... 36

14 Multiple linear regression models for revenue (A), expense (B), volume (C),

combined (D), and full model (E) ............................................................................ 38

15 Multiple linear regression equations ........................................................................ 42

16 Favorable and unfavorable budget variance impact on operating margin ............... 58

1

Chapter 1

Introduction

Health care costs too much. This is an ever increasing sentiment in the United

States, and there is certainly evidence to support this opinion. Federal spending is

increasing faster than tax revenues and elevating the national debt issues. An

overwhelming majority of federal spending is comprised of entitlements, specifically–

Medicare, Medicaid, and Social Security. The largest entitlement, Medicare and

Medicaid, is a primary driver of federal debt because these health care costs are

disproportionately rising faster than other segments of government spending. Legislators

in the United States are responding with extensive reforms to lower payment rates for

providers.

As the largest recipient of government provider payments, hospitals are the target

of significant payment reductions (Medicare Payment Advisory Commission, 2012).

Payment reductions are occurring at a time when hospitals are experiencing declining

operating margins with the current median margins at only 3% (American Hospital

Association, 2013). The decline in hospital margins is expected to continue with

reductions in Medicare, disproportionate share, and other payments scheduled in the

Patient Protection and Affordable Care Act (ACA) (Steingart & Smith, 2014). The

Congressional Budget Office and Joint Committee on Taxation (2012) report estimates

hospital reimbursements would be reduced by $260 billion from 2013-2022. In this

health reform environment, hospitals have only a few response options–lower the cost of

2

service, discontinue the service, close or sell the hospital, or change the service by

altering the care delivery model.

There is extensive evidence to support hospital capacity to lower costs for

services without compromising quality. Eliminating waste and inefficiency are some of

the most cited opportunities for hospitals in reducing the cost of care (Delaune & Everett,

2008; Institute of Medicine, 2001; Kelley, 2009; Smith, Saunders, Stuckhardt, &

McGinnis, 2013). Berwick, a leading champion of reducing inefficiencies, estimated that

waste exceeds 20% of total health care expenditures in just six areas: (a) overtreatment,

(b) failures of care coordination, (c) failures in execution of care processes, (d)

administrative complexity, (e) pricing failures, and (f) fraud and abuse (Berwick &

Hackbarth, 2012).

These findings are consistent with an earlier study by Zuckerman, Hadley, and

Iezzoni (1994) which identified inefficiency opportunities specific to hospitals. The

opportunity to lower costs is also supported by The Dartmouth Institute research related

to variations in care. Fisher et al. (2003a) found regional Medicare spending differences

were largely explained by the practice patterns of inpatient and specialist physicians.

These higher spending differences did not correlate to improved quality, access, health

outcomes, or satisfaction with care (Fisher et al., 2003a, 2003b).

To pursue lower cost strategies, many hospitals are adopting “break-even on

Medicare” budget plans that establish stepwise reductions in cost structure (Alkire, 2014;

Herman, 2012; Minich-Pourshadi, 2011). In general, these strategies are focused on

reducing the annual growth rate in expenses over the next five or more years from

roughly 5% down to 1-2% per year (Kerns, Koppenheffer, & Drayton, 2013). Over time,

3

these strategies are intended to achieve a cost structure that is at or below hospital

Medicare payments. These strategies emphasize the importance of setting and achieving

performance measures that build upon successive improvements targeted in a hospital’s

budget.

Eliminating services or closing a hospital as a response to health reform is an

option that several hospitals have selected during periods of transition. Hospitals

regularly limit or discontinue underperforming services to balance their budgets. For

example, Hsia, Kellermann, and Shen (2011) explored the decline of hospital emergency

departments from 1990 to 2009 due to low profit margins, competition, change in

ownership, and designation as the safety-net provider.

These closures can be disruptive, but they pale in comparison to the closure of a

hospital that impacts access to services and jobs as well as the overall economy of a

community. For most communities, hospitals provide an essential economic base

accounting for 15% to 20% of employment and income (Doeksen, Johnson, &

Willoughby, 1997). Furthermore, hospitals are frequently an economic asset in attracting

business and industry to a community.

Hospital closures accelerate following periods of rapid payment change (see

Figure 1). In the late 1980s hospital closures spiked after the introduction of the

Prospective Payment System in 1983 (Office of Inspector General, 2002). The trend

subsided until the late 1990s when hospital closures rose sharply in the three years

following the Budget Reconciliation Act of 1997 (Office of Inspector General, 2003a,

2003b). The ACA of 2010 (Office of the Legislative Counsel, 2010) is another significant

payment reform with the potential to escalate the number of hospital closures once again.

4

Figure 1. Hospital closures in the United States, 1987-2012.

Note: Adapted from “Hospital Closure, 2000” by Office of Inspector General, p. 5. Hospital Closure, 1987-1999.

Adapted from “A data book: Health care spending and the Medicare program” by Medicare Payment Advisory

Commission, p. 53. Annual changes in number of acute care hospitals participating in the Medicare program, 2000–

2012. Adapted U.S. Government works no permission required under U.S. Code Title 17 § 105.

A related exit strategy to closure is selling the hospital. The merger and

acquisition activity in the hospital sector mirrors closure trends with financial pressures

typically triggering the pursuit of this strategy (see Figure 2). Hospitals contend these

mergers add value through enhanced efficiency, leverage, and purchasing power as well

as reduction in duplication, excess capacity, transaction, and infrastructure costs.

Although this rationale continues to influence hospital consolidation decisions, the

current drive for size and scale is strategic, it positions the hospital for the shift from

volume to value payment arrangements (Molpus & Elek, 2010). Currently, merger and

acquisition decisions for hospitals center on transforming the care delivering model,

securing covered lives, managing population health, and mitigating risk.

An alternative to cost reduction, closing, or selling strategies in response to health

reform is for a hospital to transform its own health care delivery model. A generally

accepted description of the desired transformation is defined by the Institute for

69

8876

56 5750

42

16

37 37 38 43

64 6963

3446

63

32 28 28 2430

512 17

0102030405060708090

100

5

Healthcare Improvement’s Triple Aim dimensions–improving the patient experience,

improving the health of the population, and reducing per capita cost of health care

(Stiefel & Nolan, 2012). This model is driven by the Centers for Medicare & Medicaid

Services (CMS) through its numerous demonstration projects (Centers for Medicare &

Medicaid Services, 2015).

Additionally, private businesses are collaborating in this transformation effort to

make care more accessible. Two of the most notable examples of these private

consortium efforts are the Health Care Transformation Task Force (2015) and the Health

Transformation Alliance (2016). The Health Care Transformation Task Force (HCTTF)

is a group of businesses that bring together patients, payers, providers and purchasers to

achieve sweeping transformation. As proposed, between 2015 and 2020, each business in

the HCTTF consortium commits to attaining 75% of its care through a value-based

payment arrangement. In a similar emphasis on value, the Health Transformation

Alliance (HTA) has goals to improve health care benefits and outcomes for its

employees. Transformational examples of public and private sector organizations are

clear indications that health care delivery is changing, and hospitals will need to change

in similar ways to respond to the market.

The ability of hospitals to respond to payment reductions and delivery system

changes can be measured through budget performance. Hospitals plan responses and

program these into the capital and operational budgets. Although payers and trade

associations have annual financial performance data for hospitals these surveys do not

capture budget information. Due to this lack of information, there is a gap in studies that

describe the relationship between budget variances and profitability.

6

The use of budgets to improve profitability is a common practice and a direct

function of achievement would be smaller unfavorable and/or greater favorable budget

variances. Budget variances are a measure of forecasting accuracy and/or tighter

management. A budget variance is the difference between actual and budgeted

performance (Bragg, 2013). These variances are measured by the budget variances of

selected indicators in revenue, expense, and volume. Profitability is measured by the

operating margin. Operating margin is the net operating income divided by total

operating revenue and is a common measure of profitability (Cleverley, 2008; Cleverley,

Cleverley, LaFortune, & Handlon, 2015; Cleverley, Cleverley, & Song, 2010). The

operating margin is a direct function of budget variances, smaller unfavorable variances

and/or greater favorable variances should lead to a higher operating margin.

Figure 2. Hospital mergers in the United States, 1998-2014.

Note: Adapted from “Trend watch chart book 2015: Trends affecting hospitals and health systems” by Avalere Health

for the American Hospital Association, p. 25. Announced Hospital Mergers and Acquisitions, 1998-2014. Irving Levin

Associates, Inc. (2015). The Health Care Services Acquisition Report. Twenty-First Edition.

Significance of the Study

Organizations emphasize operating margin performance because it is a key

measure of their long-run viability (Cleverley, 2008; Cleverley et al., 2015; Fitch Ratings,

139

110

86 83

5838

59 50 54 60 6050

7693

10789

100

020406080

100120140160

7

2015; Healthcare Financial Management Association, 2014; Miyagi, 2008; Moody's

Investors Service, 2013; Standard & Poor's, 2013). Organizations place a similar

emphasis on budgeting because of its potential effect on operating margin. As discussed

in the review of the literature, budgeting has four main purposes: (1) planning

(forecasting), (2) coordination, (3) oversight, and (4) motivation (Merchant & Van der

Stede, 2012). The significance of this study is to provide evidence in understanding the

forecasting (budget variances) effect on operating margin.

The value of this study is reinforced by the prevalence of the budget process in

organizations and its relationship to improved performance. Budget processes are

adopted by most organizations as standard operating practices. In a survey of over 400

companies, 97% reported the use of a formal budgeting process in their organizations

(Umapathy, 1987). This near-universal adoption of the budget process demonstrates

value to organizations; it is viewed as an essential tool in influencing performance. In a

survey of over 550 managers, Libby and Lindsay (2010) reported 79% of respondents

used budgets to motivate and evaluate performance.

The relevance of this current study to hospitals is its potential to improve

operational effectiveness and strategic management. A more in-depth understanding of

budget variance influences on profitability could aid hospitals in setting and adjusting

day-to-day operational performance. This evidence-based corrective activity would

benefit hospital managers in prioritizing effort towards sources of greatest influence on

the operating margin.

In addition to operational relevance for hospitals, a better understanding of

budgeting could improve an organization’s ability to select, measure, and achieve

8

strategies. Budgets are a quantitative reflection of the strategies or expectations hospitals

set in response to the market. The evolving health care environment is placing greater

emphasis on strategy for hospitals. Porter and Lee (2015) suggested that this stress is

relatively foreign to a sector that equates strategy to good operational performance. As

operational effectiveness and strategy assumes greater importance for hospitals so too

does an understanding of the measures of success recognized in the budget.

Research Question and Hypotheses

The purpose of this study was to examine the relationship between hospital

budget variances and profitability. Specifically, this study examined the following

research question and three hypotheses for hospitals:

Are smaller budget variances (more accurate forecasting and/or tighter management)

associated with greater operating margins?

1. H1: Smaller budget variances are associated with greater operating margins.

2. H2: Smaller unfavorable budget variances are associated with greater operating

margins.

3. H3: Greater favorable budget variances are associated with greater operating margins.

Plan of Work

Following the study introduction in Chapter 1, Chapter 2 provides a review of the

research literature on budgeting and its relationship to performance. Evidence is

examined regarding the organizational rationale for using budgets and the ways in which

the budgeting process is associated with performance. Chapter 2 concludes with a review

9

of Control Theory, which illustrates why budgets have an effect on financial

performance.

Chapter 3 describes the research design used in the study and discusses the study

hypotheses. The methodology includes a description of the sample, variables, and

analysis. Chapter 4 presents the results of the hypotheses tested. Chapter 5 provides a

discussion and interpretation of study findings and notes study limitations. This final

chapter also outlines practical recommendations for hospital managers and potential

opportunities for future research.

10

Chapter 2

Literature Review

A review of the literature associated with budgeting and its relationship to

performance provides context and insights. Therefore, this literature review considers the

following areas: (1) the purpose of budgeting and its potential influence on performance,

(2) the relationship of hospital characteristics to performance, and (3) a theory to explain

the association between budgeting and performance.

The Purpose of Budgeting and Its Potential Influence on Performance

Budgeting is a component of management control systems (MCS) research. First

defined by Anthony (1965), management control is “the process by which managers

ensure that resources are obtained and used effectively and efficiently in the

accomplishment of the organization’s objectives” (p. 17). This definition identifies a

fundamental reason that organizations budget–to provide managers a process of influence

on performance and a tool to achieve organizational plans. Organizations that maintain

appropriate controls are likely to favorably influence performance toward plan objectives,

“regardless of whether these objectives are to maximize shareholder returns, heal the

sick, or educate the young” (Merchant & Otley, 2006, p. 785)

The purpose of budgeting extends beyond management control as this activity

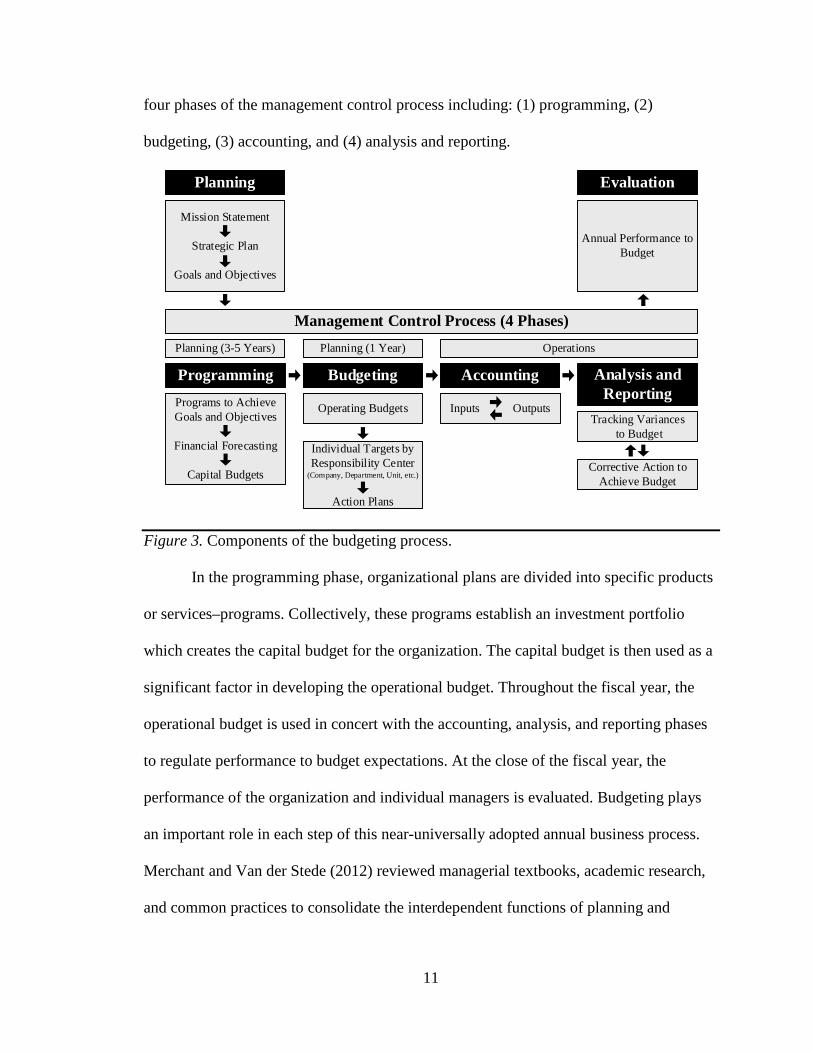

intertwines with every step in the traditional annual budgeting process (see Figure 3).

Ronen and Livingstone (1975) emphasized that the functions of budgeting span across

planning, control, and motivation. The budgeting process begins with planning, and these

decisions feed the management control process. Anthony and Young (2003) identified

11

four phases of the management control process including: (1) programming, (2)

budgeting, (3) accounting, and (4) analysis and reporting.

Mission Statement

Strategic Plan

Goals and Objectives

Budgeting

Operating BudgetsTracking Variances

to Budget

Annual Performance to Budget

Planning Evaluation

ProgrammingPrograms to Achieve Goals and Objectives

Financial Forecasting

Capital Budgets

Individual Targets by Responsibility Center

(Company, Department, Unit, etc.)

Action Plans

Analysis and Reporting

Accounting

Operations

Management Control Process (4 Phases)

Inputs Outputs

Planning (3-5 Years)

Corrective Action to Achieve Budget

Planning (1 Year)

Figure 3. Components of the budgeting process.

In the programming phase, organizational plans are divided into specific products

or services–programs. Collectively, these programs establish an investment portfolio

which creates the capital budget for the organization. The capital budget is then used as a

significant factor in developing the operational budget. Throughout the fiscal year, the

operational budget is used in concert with the accounting, analysis, and reporting phases

to regulate performance to budget expectations. At the close of the fiscal year, the

performance of the organization and individual managers is evaluated. Budgeting plays

an important role in each step of this near-universally adopted annual business process.

Merchant and Van der Stede (2012) reviewed managerial textbooks, academic research,

and common practices to consolidate the interdependent functions of planning and

12

budgeting into four main purposes: (1) planning, (2) coordination, (3) oversight, and (4)

motivation.

Planning. Budgeting has a complementary role in planning; planning positions

organizations for the future while budgeting measures the performance to the plan

(Gapenski, 2011). Budgets play an important role in translating planning strategies into

measurable expectations for managers (Merchant, 1981; Simons, 2013). While there is a

functional purpose of budgets in planning, there remains scarce research studies

concerning the relationship between these two activities.

Langfield-Smith (1997) reviewed management control systems (MCS) and

strategy and concluded that knowledge in this relationship was limited to nine empirical

studies (Daniel & Reitsperger, 1992; Daniel & Reitsperger, 1991; Govindarajan, 1988;

Govindarajan & Fisher, 1990; Govindarajan & Gupta, 1992; Khandwalla, 1972;

Merchant, 1985b; Miller & Friesen, 1982; Simons, 1987) and eight case studies (Archer

& Otley, 1991; Dent, 1991; Knights & Willmott, 1993; Roberts, 1990; Simons, 1987,

1990, 1991, 1994). Additionally, these studies had a narrow focus in examining

situational influences on the type of control systems (e.g., budgets, auditing, incentives)

best suited for particular strategies (prospector or defender).

A common conclusion in these studies was MCS does play a supportive role in

strategy implementation and influences strategic formulation, implementation, and

change (Langfield-Smith, 1997). The situational influences in this type of contingency

research are limited by the assumption in the existence of a single best way to manage or

organize.

13

Beyond the situational influences of strategy on MCS, there are a few examples of

the relationship of MCS on strategy, such as the effectiveness of MCS activities leading

up to selecting a strategy (Mintzberg, 1978; Mintzberg & Waters, 1985) or the absence of

controls in establishing their strategies in many organizations (Goold & Quinn, 1990). A

reason for the limitations in planning and MCS research is the differing view of the scope

of these controls.

The seminal work of Anthony (1965) in MCS established a practicing definition

which did not include strategic planning and therefore arbitrarily narrowed the early

research in this area. As previously mentioned, Anthony and Young (2003) described

strategy formulation as a separate planning function outside of MCS but included

programming that contains the planning components of forecasting and capital budgeting.

Goold and Quinn (1990) viewed planning strategy as another control activity in a

system that is focused on longer-term goals. Merchant and Van der Stede (2012),

however, viewed planning and MCS as separate but interconnected activities. Whether

MCS is perceived as a separate or inclusive part of planning, researchers have

consistently recognized that budgets serve a role in the preparation and measurement of

strategic goals.

Emmanuel, Otley, and Merchant (1990) regarded financial forecasting as an

element of budgeting and an essential component of the planning process. Many research

studies examine financial forecasting as it relates to the accuracy of analysts predicting

future earnings. Evidence is building to support the idea that select factors (e.g., past

performance, experience, resources, portfolio complexity, forecast period) are positively

associated with forecast accuracy (Brown, 2001; Clement, 1999; Sinha, Brown, & Das,

14

1997; Stickel, 1992); contradicting early findings that did not control for these

differences (Brown & Rozeff, 1980; Butler & Lang, 1991; O'Brien, 1990; Richards,

1976). These studies are limited to factors associated with forecast accuracy and do not

address the research question in this study: Are smaller budget variances (e.g., forecast

accuracy) associated with greater operating margins (e.g., higher earnings)?

Coordination. Budgets are used to coordinate and communicate activity in an

organization. The financial strategies and goals of the organization are communicated

down to management control units or responsibility centers in the budget (Cleverley et

al., 2010). Concurrently, frontline leaders are communicating up the chain of command

the constraints, resources, and risks as well as other information to validate and modify

the top-down budget expectations (Merchant & Van der Stede, 2012).

Hopwood (1976) described this vertical, bidirectional communication as one of

the most important benefits of the budgeting process. The vertical sharing of information

suggests a relationship to budget participation, organizational commitment, and job

performance (Parker & Kyj, 2006). Communication also occurs laterally to various

divisions, businesses, and functional areas to align budget expectations across the

organization.

For example, the finance and operational departments cross reference and align

their budgeted volume targets with the marketing department. Emmanuel et al. (1990)

identified the importance of budgets in coordinating the interrelated and aggregate

activities of the various responsibility centers as well as heightening the visibility of top

priorities within the organization.

15

Oversight. The most fundamental purpose of budgeting is its oversight controls.

These controls focus on the basic accounting function of budgets that set estimates and

establish financial expectations over a specified period of time. Budgeted financial

expectations serve as an essential management control process (Hansen, Otley, & Van

der Stede, 2003) and remain a universally adopted business practice (Ekholm & Wallin,

2000; Hansen & Van der Stede, 2004; Libby & Lindsay, 2010; Otley, 1999; Umapathy,

1987).

All four phases of management control have an oversight role in budgeting

(Anthony & Young, 2003). In the programming phase, capital investment and other

resource allocation techniques are designated and layered into respective department

budgets (Merchant & Van der Stede, 2012). The adjustment of this planned capital spend

based on deviations to the operational budget is the primary oversight function in the

programming phase. Beyond capital spending adjustments, the oversight activity in

budgeting is concentrated with the phases of budgeting, accounting, analysis, and

reporting.

In the budgeting phase, organizations typically set the budget to cover the

forthcoming year. Cleverley et al. (2010) succinctly defined a budget as “a quantitative

expression of a plan of action” (p. 356). Anthony and Young (2003) added to this

definition: “formulated within a ceiling of estimated available resources” (p. 487). As

outlined in the coordination role, the budget is then translated to the various responsibility

centers and respective managers.

The dissemination of accountability serves as a formal authorization to define a

manager’s discretion in controlling production and spending as well as his or her overall

16

scope of responsibility (Emmanuel et al., 1990). With regard to budgetary motivation, the

tiered goal application from the organizational level down to the individual level has an

effect on performance (Baum, Locke, & Smith, 2001; Latham & Locke, 1975; Locke &

Latham, 2002; Martocchio & Frink, 1994; Rodgers & Hunter, 1991).

The accounting, analysis, and reporting phases of budgetary oversight serve as the

attention-directing function to alert managers of a deviation and the specific areas to

focus on to better understand the variation (Simon, 1954). The accounting function

supplies the actual performance by recording inputs and outputs. Actual performance is

then compared to the budget and prior year in the analysis and reporting phases. During

this phase, variances are reviewed and managers begin to problem solve in earnest by

identifying issues and courses of action and weighing the economic consequences of

these actions (Simon, 1954).

Motivation. As a MCS, budgets are a tool in the process of influencing behavior

(Flamholtz, Das, & Tsui, 1985). Budgets were naturally adopted for evaluation because

they provided a commonly available standard of measurement against actual performance

(Hansen et al., 2003). Adoption of budgets as the predominant standard for evaluation

was reinforced by shareholders’ desire to connect performance measures to return on

investment (Otley, 1999). Budgets easily link individual and firm performances and

provide management teams compensation to track more consistently with organizational

profitability (Merchant & Van der Stede, 2012).

Based on this connection, budgets quantify desired returns while measuring both

unit and manager performance against these expected targets (Brownell & Dunk, 1991).

If targets are attached to a valued reward (see Table 1) then a manager’s motivation is

17

enhanced and he or she is more likely to achieve the budget (Argyris, 1952). The budget-

incentive combination serves to attract attention in an effort-directing role as well as to

motivate with an effort-inducing purpose (Merchant & Van der Stede, 2012).

Table 1 Examples of Value Rewards both Positive and Negative

(Merchant, 1998)

Due to this accessible and measurable connection to desired outcomes, the use of

budgets in performance evaluations is a common practice (Merchant, 1981). Numerous

studies and accounting texts also support the connection between achievement of budget

targets and a monetary reward in performance evaluation (Atkinson, Banker, Kaplan, &

Young, 1995; Govindarajan, 1988; Gupta, 1987; Horngren, Bhimani, Datar, & Foster,

2002; Porter, 1980; Simons, 1987; Zimmerman & Yahya-Zadeh, 2011). However, the

effect of monetary incentives on budget performance is dependent on skill, complexity,

goals, and rewards (Bonner & Sprinkle, 2002).

Motivation and the Expectancy Theory. Vroom’s (1964) expectancy theory of

motivation is often used to describe budgetary motivation. The theory suggests that goals

are effective in motivating individuals if they have (1) a positive correlation between

Positive Rewards Negative Rewards

Monetary Nonmonetary Salary Increases Bonuses Stock Options Restricted stock Paid time off Prizes (e.g., Trips) Perquisites

(e.g., Country Club membership)

Promotion Titles Elevated decision-making Job assignments Office assignments Reserved parking Autonomy Power Recognition Praise Job Security

Absence of positive reward No increase in salary Loss of bonus Loss of job Loss of autonomy No promotion Demotion Chastisement Public humiliation

18

effort and performance–that is reasonably attainable; (2) a positive relationship between

performance and a valued reward; (3) a valued reward that satisfies a need; and (4) a

desire that exceeds the required effort. All of these elements are dependent on how

deeply the employee values the reward (valence), how competent and capable the

employee feels about achieving the goal (expectancy), and the level of trust the employee

has in receiving the reward if the goal is achieved (instrumentality).

Ronen and Livingstone (1975) examined the expectancy theory more specifically

related to budgets and identified five assumptions in the research literature: (1) budgets

should be reasonably attainable (Bayton, 1943; Becker & Green, 1962; Cherrington &

Cherrington, 1973; Child & Whiting, 1949; Hofstede, 1968; Lewin, Dembo, Festinger, &

Sears, 1944; Stedry, 1959); (2) budgets should include participation between manager

and superior (Becker & Green, 1962; Caplan, 1966; Cherrington & Cherrington, 1973;

Coch & French, 1948; Kay, French, & Meyer, 1962; Leavitt, Pondy, & Boje, 1964;

Lewin, 1936; Lewin et al., 1944; Vroom, 1964; Welsch, 1976); (3) budgets emphasize

management by exception with attention drawn to unfavorable deviations as opposed to

favorable variations (Birnberg & Nath, 1967; Cherrington & Cherrington, 1973; Sayles &

Chandler, 1971; Vroom, 1964); (4) budgets require an appropriate level of controllability

where the manager has the competency, capability and authority to make decisions and

execute them (Feather, 1967; Vroom & Maier, 1961) dependent on variables in their

personality (Lefcourt, 1965; Rotter, Liverant, & Crowne, 1961; Sutcliffe, 1956); and (5)

budgets are well-suited for evaluating performance because they are limited to

quantitative, monetary measures.

19

Rockness (1977) reinforced these five assumptions and added that budgets need

to be reasonably difficult, predictably tied to the reward, and used in conjunction with

regular feedback of the results. Additional studies have supported the value of difficult

but achievable budget targets in achieving favorable performance (Hirst & Lowy, 1990;

Merchant & Manzoni, 1989; Wentzel, 2002). In the absence of achievable targets, setting

high budget goals has had an adverse effect on performance (Kenis, 1979).

In the research literature, the evaluation of a manager’s performance in achieving

an assigned budget is often based on the following three key constructs: budget use,

budget emphasis, and budget participation (Sivabalan, Booth, Malmi, & Brown, 2009).

Budget use focuses on evaluations as the primary purpose for budgeting (Abernethy &

Stoelwinder, 1991; Swieringa & Moncur, 1975). Budget emphasis research has resolved

initial conflicting results to demonstrate the manager’s attention and collaboration on the

budget improves achievement of these targets (Brownell & Dunk, 1991; Brownell &

Hirst, 1986; Hopwood, 1972; Otley, 1978; Van der Stede, 2001). Finally, budget

participation between the manager and supervisor is evident when setting expectations

supports the positive effect on job performance (Argyris, 1952; Becker & Green, 1962;

Brownell, 1982; Merchant, 1981; Nouri & Parker, 1998; Shields & Shields, 1998).

Researchers have noted that intervening variables, such as motivation and role ambiguity,

need further study to explain conflicting results (Bryan & Locke, 1967; Stedry, 1959).

Criticisms of Budgeting

Budget slack, commonly referred to as sandbagging or padding the budget, is one

of several issues that challenges the effectiveness of a traditional annual budgeting

process. Budget slack introduces contradictory evidence to refute the use of difficult

20

targets, supervisor attention, and budget participation (Dunk, 1993; Fisher, Maines,

Peffer, & Sprinkle, 2002; Merchant, 1985a; Schiff & Lewin, 1970). Budget slack is an

inherent enticement for managers at all levels to understate budgets in order to maximize

their individual reward (Horngren et al., 2002; Jensen, 2001, 2003). Although moderating

strategies demonstrate an ability to lessen the effect of budget slack (Waller, 1988;

Weitzman, 1976; Young & Lewis, 1995), few organizations employ these strategies in

practice (Atkinson et al., 1995; Waller, 1994).

In addition to the issue of budget slack, Hope and Fraser (2013) cited three main

dysfunctions to the annual budgeting process: (1) budgeting is cumbersome and

expensive; (2) budgeting is antiquated and does not take advantage of real-time

capabilities of today’s technology; and (3) fixed targets in budgeting only lead to

incremental improvements and incentives to ‘game the numbers’ for personal gain.

Additional criticisms reference annual budgets as time-consuming, rigid, and strategically

stifling which frequently lead to an appropriations mentality–spend the annual budget

allocations in full otherwise next year’s budget could be reduced (Gurton, 1999; Hope &

Fraser, 1999, 2003; Schmidt, 1992).

Activities in the planning, programming, budgeting, accounting, analysis,

reporting, and evaluation phases often overlap (see Figure 4) as the organization prepares

future expectations for the coming year (planning, programming, and budgeting);

manages the current year (accounting, analysis, and reporting); and evaluates the

performance of the prior year (evaluation). This future, current, and prior fiscal year

overlap of activities places organizations in a perpetual budgeting process. Each phase

contributes to the prolonged process. The planning and programming phase involves

21

analysis, pro forma development, investment priorities, and other activities often

involving shareholder or organizational governance boards. Typically, several months are

needed to translate the plan and program into a capital and operating budget. The

operations phase is typically managed over a 12 month period known as the fiscal year.

Finally, the evaluation phase takes a few months to audit fiscal year ending performance,

evaluate individual leader performance, and award incentives.

Plan & Program(3 months)

Operations (Accounting, Analysis and Reporting)(12 months)

Evaluation(2 months)

Budgeting(3 months)

1 2 3 4 5 6 7 8 9 10 11 12Traditional Annual Budget Cycle (12 month recurring cycle)

Figure 4. Traditional annual budgeting cycle.

To varying degrees, practitioners and academics recognize the limitations of

annual budgets, but few businesses have abandoned this practice. However, many

companies are supplementing their annual budgeting process with rolling forecasts,

benchmark modeling, balanced scorecards, and other more dynamic methods and tools

(Arterian, 1998; Ekholm & Wallin, 2000).

The Relationship of Hospital Characteristics to Performance

Hospital characteristics have the potential to influence budget variances, but there

is no evidence to support or refute an association. In the absence of this information,

hospital characteristics and performance studies are reviewed because of the

interconnectivity of budgets to performance (Otley, 1999). The relationship of hospital

22

characteristics to performance in the literature focuses on ownership, system

membership, size (number of beds), and location (urban or rural).

Hospital ownership and performance is often examined in relation to the property

rights theory, which suggests a connection between the owner or decision maker and the

economic behavior and outcome (Kim & Mahoney, 2005). Conversely, Becker and Sloan

(1985) found negligible differences in efficiency between for-profit, not-for-profit, and

government hospitals once factors other than ownership were held constant. Additionally,

for-profit and not-for-profit hospitals have similar after-tax profit margins and

proportions of care for Medicare, Medicaid, and charity care (Becker & Sloan, 1985;

Gapenski, Vogel, & Langland-Orban, 1993; Sloan & Vraciu, 1983; Younis, Younies, &

Okojie, 2006).

Other researchers, however, reported that for-profit hospitals were more profitable

than not-for-profit hospitals (Herzlinger & Krasker, 1986; Sear, 1991) particularly in

rural settings (Ferrier & Valdmanis, 1996; Younis, 2012; Younis, Rice, & Barkoulas,

2001). This detected difference could be a result of lower levels of community benefit

provided by for-profit hospitals (Arrington & Haddock, 1990; Fitzgerald & Jacobsen,

1987).

Evidence is mounting to suggest that for-profit hospitals operate at a lower cost

than other types of hospitals with the same or better quality performance (Jiang,

Friedman, & Begun, 2006; McKay & Deily, 2005). For-profit hospitals frequently elect

to provide a higher mix of profitable medical services and are more responsive to changes

in profitability (Horwitz, 2005). Additionally, financial performance has been found to

23

improve in hospital conversions to for-profit status with no differences in quality and

charity care (Joynt, Orav, & Jha, 2014).

In a comparison study of hospital ownership to cost and quality in a select group

of common conditions for Medicare patients, Sloan, Picone, Taylor, and Chou (2001)

discovered that for-profit hospitals received higher payments with no appreciable

difference in outcomes. Similarly, Renn, Schramm, Watt, and Derzon (1985) indicated

that for-profit hospitals used significantly higher charges to achieve more favorable profit

margins with no discernable difference in efficiency compared to other types of hospitals.

Financial pressures in the hospital industry can drive membership into a larger

health care system. This follows the economic theory that states that as an organization

increases in size, the potential increases for efficiencies are sought through economies of

scale, market leverage, and spreading of risk. Testing this theory to enhance hospital

financial performance is a central theme of studies related to system membership.

Contrary to the perceived benefit of an affiliation strategy, the evidence does not

support a favorable relationship between system membership and improved profitability

(Becker & Sloan, 1985; Carey, 2003; Clement et al., 1997; Gapenski et al., 1993;

Tennyson & Fottler, 2000). The exception to this finding can be seen when system

membership includes higher pricing which result in greater profits (Cleverley, 1992;

Joynt et al., 2014; Levitz & Brooke, 1985; Manheim, Shortell, & McFall, 1989; Renn et

al., 1985; Sloan et al., 2001).

Another area of research in system membership suggests no cost efficiency

benefits associated with membership (Becker & Sloan, 1985; Cleverley, 1992; Coyne,

1982; Levitz & Brooke, 1985; Renn et al., 1985). There is evidence, however, that when

24

combining measures of cost and quality, system membership does improve performance

(Jiang et al., 2006; McKay & Deily, 2005) particularly for rural hospitals (Broyles,

Brandt, & Biard‐Holmes, 1998).

In most studies, the size of a hospital is measured simplistically as the number of

staffed or licensed beds. Although less prevalent, these studies mirror the economic

theory research previously assessed in system membership. The size of a hospital has a

weak negative influence on profitability (Gapenski et al., 1993), which is consistent with

conclusions by Younis et al. (2006) that hospitals greater than 100 beds were less

profitable than smaller hospitals based on less managed care and competition in rural

settings. Younis (2012) further identified the size and profitability relationship as

nonlinear with higher profits in hospitals with 50 to 400 beds and lower margins in

hospitals with less than 50 and greater than 400 beds.

Posnett (1999) found a similar nonlinear relationship between size and economies

of scale where increases in the number of beds and economies of scale were realized for

small hospitals (less than 200 beds), flattened for mid-sized hospitals (200 to 400 beds),

and declined for large hospitals (over 400 beds). Other size to economies of scale studies

demonstrated a limited relationship ranging from weak (Berry, 1967, 1974; Carr &

Feldstein, 1967; Evans, 1971; Lave & Lave, 1970) to no association (Francisco, 1970;

Gapenski et al., 1993).

Studies assessing location relationships to performance typically focus on urban

versus rural settings. A majority of this research relates to the previously discussed

relationship to the size of the hospital and the economic viability of rural hospitals

(Moscovice, 1989). As compared to urban hospitals, rural hospitals experienced lower

25

profits, lower occupancy rates, higher labor ratios, and slower growth rates (Younis,

2012). These results suggest two distinctly different populations and explains why studies

in this area often focus on the implications of policy concessions for rural hospitals

(Moscovice & Stensland, 2002).

One policy that is often studied is the 1997 Balanced Budget Act’s creation of the

critical access hospitals designation and its implications to rural communities. Li,

Schneider, and Ward (2009) found conversion to a critical access status significantly

increased a hospital’s operating revenues, expenses, and margins. These favorable policy

interventions helped curb the increasing trend of rural hospital closures (Office of

Inspector General, 2003a; Poley & Ricketts, 2001), but the current needs are once again

escalating as costs outpace the implementation of reimbursement reforms (Ellison, 2015;

NRHA, 2013).

The two previous sections of this literature review focused on the budgeting

relationship to performance and the influence of hospital characteristics. In this next

section, the attention shifts from identifying how previous research studies fit into the

existing body of knowledge to a theoretical framework that could explain the association

between budgeting and performance. This framework is grounded in Control Theory

which is generally attributed to the work of Wiener (1948).

Control Theory

This review of literature highlights the difficulty faced by hospitals in improving

financial performance. However, the hospital industry has historically adapted to

payment challenges such as the introduction of Medicare and Medicaid in 1967,

diagnosis-related groups (DRGs) prospective payment system in 1983, managed care

26

proliferation in the 1980s, and the Balanced Budget Act of 1997 (Whetsell, 1999). A key

response by hospitals to each of these payment disruptions was to reset their targets and

implement strategies measured against new norms. Budgets quantify these adjusted

expectations and serve as a reference within a management control system. Control

theory examines these self-regulating systems and provides an appropriate theoretical

framework for the relationship between budget variances and operating margin.

Control theory incorporates a feedback loop as an essential component to drive

action (Carver & Scheier, 1982; Wiener, 1948). The purpose of this feedback loop is to

minimize deviations from the target or referent standard. To minimize deviations, Klein

(1989) identified four critical elements in the feedback loop: (1) a referent standard, (2) a

sensor, (3) a comparator, and (4) an effector. These elements are often compared to a

thermostat regulating temperature to achieve a desired climate.

In a similar manner, the feedback loop of a budget control system functions to

achieve the desired organizational results (see Figure 5). The budget target is set as a

referent standard or desired state. The individual’s sense of his or her actual performance

or present state is measured by a sensor such as an interpretation of a financial report.

The perception of the present state (e.g., financial report) is compared to the desired state

(e.g., budget). If there is a perceived discrepancy between the present and desired states

an action is performed with the intent of reducing the discrepancy. The budget control

loop is closed with regular monitoring by the sensor and ongoing discrepancy

adjustments by the effector.

Carver and Scheier (1981) identified two primary elements of human behavior

within control theory, cognitive and affective elements. The cognitive element describes

27

individuals’ evaluation of their perceived performance against the referent or goal

standard. To assess performance, humans need to know the performance discrepancy and

its impact to the individual, the organization, and other stakeholders (Fellenz, 1997). The

affective element relates to an individual’s actions or behavioral modifications in

resolving any perceived discrepancy between his or her actual and desired performance.

Both of these elements play important roles in the budget control process.

Figure 5. Control theory and budgets.

Note: Adapted from “An integrated control theory model of work motivation” by Klein (1989, p. 151). The simple

feedback loop. Academy of Management does not require permission for dissertation not sold for commercial

distribution and/or monetary gain.

One of the most cited criticisms of control theory is its mechanistic application to

human behavior. Humans are conceptual not mechanical decision makers who take a host

of tangible and intangible factors into consideration before acting on an identified

discrepancy (Locke, 1991). Combining factors guides decision making in terms of how

an individual will or will not act to a given variance. A potential bridge to this criticism

could include a more micro-level theory of goal setting.

Sensor

INPUT ActualPerformance

Comparator

Actual Budget

Effector

OUTPUT Action forRemediation

Variance to Budget

Referent Standard

Budget Target (goal)

Perceptual Signal Error Signal

Reference Signal

SystemEnvironment

28

As a complement for human behavior deficiencies in control theory, a goal setting

theory by Locke and Latham (1990, 2002) asserts that performance improves when

setting specific, difficult goals such as a budget (Chow, 1983; Hirst & Lowy, 1990;

Rockness, 1977; Stedry & Kay, 1966). Evidence supports the favorable relationship

between setting goals and improving performance (Locke & Latham, 1990, 2002; Locke,

Shaw, Saari, & Latham, 1981).

The goal setting theory is consistent with the fundamental incentive of business,

to remain viable, and in most cases, maximize profit (Alchian, 1950; Demsetz, 1983).

These goals are quantified in the budget and become the measurement standard for the

organization; budget goals are then translated to the business units and managers. A

manager’s ability to achieve the budget becomes the primary incentive for performance

(Merchant & Manzoni, 1989).

Managers who achieve the budget enhance their opportunities for advancement,

bonuses, and higher salaries. In contrast, managers who fail to achieve the budget face

negative repercussions which could ultimately lead to job loss. As a standard for

incentives, the budget is a powerful motivator on performance. The relationship between

motivation and performance has strong support in the research literature with roots that

stem from the work of Porter and Lawler (1968).

The goal setting theory incorporates measures of expectancy. As reviewed in the

motivational studies related to budgeting, Vroom (1964) introduced the expectancy

theory which states, “people choose the option (course of action) they believe will result

in the greatest benefit to them, provided there is a good chance they actually can attain

the benefit” (Smith & Hitt, 2005, p. 36). In weighing expected value, people are

29

motivated by difficult goals if they are achievable (Merchant & Manzoni, 1989).

Cherrington and Cherrington (1973) supported the expectancy theory related to budgeting

and suggested that an appropriate reward for high budget participation improved

performance and job satisfaction.

The manager-subordinate relationship is also a significant factor in budget

performance. The balance theory by Heider (1946) suggests “people strive to achieve

balanced sentiments in their interactions with others” (Miles, 2012, p. 66). That is to say,

there is a desire to align one’s self with others who share similar attitudes. When this is

not possible it creates dissonance, tension, and an elevated potential for conflict in a

relationship.

If an unbalanced relationship exists for either the manager or subordinate then

there is a natural desire to remedy the situation. Heider (1958) offered two simple

remedies for unbalance: (1) change your perception and valuation, or (2) leave the

relationship. This is challenging in practice for the manager-subordinate relationship

which, if not remedied, will negatively affect budget performance and job satisfaction

(Brownell, 1982).

For this current investigation, control theory was tested by measuring hospital

budget variances (referent standard) association with operating margins (sensor–actual

performance). The assumption was that smaller budget variances would be associated

with improved operating margins.

30

Chapter 3

Research Methodology

This study focused on acute care hospitals submitting budget and year end audited

financial reports to the Washington State Department of Health (DOH) Hospital and

Patient Data Section (HPDS) of the Center for Health Statistics (CHS). Hospitals in the

state of Washington have a unique requirement to submit both budget and year end

reports for the purpose of understanding trends and guiding leaders in making more

informed public health and policy decisions. From 1987 to 2013, the HPDS was

comprised of 115 acute care hospitals represented in one or more years as well as hospital

characteristics of ownership, system membership, bed size, and urban or rural locations

(see Table 2).

Table 2 Hospital Characteristics

Data Sources and Collection

This study utilized a longitudinal dataset for the years 1987-2013 (27 years). The

dataset was constructed from the Washington State Department of Health’s Hospital and

Patient Data Section (DOH/HPDS) of the Center for Health Statistics (Huyck, 2013).

DOH/HPDS applied a standard data collection process using generally accepted

accounting principles. The Washington State Department of Health (1990) Accounting

Categories N % Categories N % Categories N % Categories N %Non-Profit 57 49.6 System 44 38.3 > 300 18 15.7 Urban 64 55.7For Profit 9 7.8 Stand Alone 71 61.7 300-101 37 32.2 Rural 51 44.3Government 49 42.6 Total 115 100.0 100-26 40 34.8 Total 115 100.0

Total 115 100.0 ≤ 25 20 17.4Total 115 100.0

System Membership Urban or RuralOwnership Bed Size

31

and Reporting Manual for Hospitals provides uniform accounting and reporting standards

based on the Audits of Providers of Health Care Services, July 1990, of the American

Institute of Certified Public Accountants. In accordance to these standards, Washington

hospitals summit required data to DOH/HPDS using department-supplied electronic

forms for both budget and year end reporting.

Measures

In addition to the four hospital characteristics, the database consists of over 60

financial (income statement) and utilization input measures such as number of

employees, admissions, patient days, and births (see Appendix B for a full list of data

elements). These metrics were narrowed in the study to common industry measures for

revenue, expense, and volume (see Table 3).

Table 3 Selected Independent and Dependent Variables

Research Question and Hypotheses

The measures of the study were prepared to examine the relationship between

hospital budget variances (revenue, expense, and volume) and profitability (operating

margin). Specifically, this study examined the following research question and three

hypotheses for hospitals:

Are smaller budget variances (more accurate forecasting and/or tighter management)

associated with greater operating margins?

Independent Variables Dependent Variable Variance actual to budget in: 1. Total Operating Revenue per Adjusted Patient Days (Revenue) 2. Total Operating Expense per Adjusted Patient Days (Expense) 3. Adjusted Patient Days (Volume)

Operating Margin

32

1. H1: Smaller budget variances are associated with greater operating margins.

2. H2: Smaller unfavorable budget variances are associated with greater operating

margins.

3. H3: Greater favorable budget variances are associated with greater operating margins.

Data were prepared to address the three hypotheses. For Hypothesis 1, data were

prepared to provide absolute value of budget variances and the actual (positive, negative,

or zero) operating margin. Data preparation for Hypotheses 2 and 3 isolated the

unfavorable and favorable variances.

Data Preparation

Variances reflect the percent variance for independent (budget variances)

variables in the analysis. The percent variance is the difference between actual and

budget for each variable (3), hospital (115), and year (27) in the dataset. The variables

were constructed to reflect the absolute value of each variance to budget measures for

revenue, expense, and volume (see Figure 6). Hypothesis 1 addressed smaller budget

variances (regardless of whether the variance is favorable or unfavorable).

𝑋𝑋ℎ𝑦𝑦 = ��𝐴𝐴ℎ𝑦𝑦 − 𝐵𝐵ℎ𝑦𝑦�

�𝐵𝐵ℎ𝑦𝑦��

𝑋𝑋ℎ𝑦𝑦 = actual to budget percent variance with each hospital (h) and respective year (y) 𝐴𝐴ℎ𝑦𝑦 = actual variable with each hospital (h) and respective year (y) 𝐵𝐵ℎ𝑦𝑦 = budget variable with each hospital (h) and respective year (y)

Figure 6. Variance formula for independent variables (X).

Hypotheses 2 and 3 addressed a more specific component of the budget variance–

the impact of unfavorable and favorable variances. To address the unfavorable and

33

favorable hypotheses, a full model was developed to isolate favorable and unfavorable

measures of revenue, expense, and volume budget variances. The use of dummy and

interaction variables were incorporated in the full model to achieve distinct favorable and

unfavorable measures.

Revenue and Volume Unfavorable Variance Actual less than Budget

Favorable or No Variance: Actual greater than or equal to Budget

𝑋𝑋ℎ𝑦𝑦 = 𝐼𝐼𝐼𝐼 𝐴𝐴 < 𝐵𝐵 𝑡𝑡ℎ𝑒𝑒𝑒𝑒 �−1×�𝐴𝐴ℎ𝑦𝑦 − 𝐵𝐵ℎ𝑦𝑦�

�𝐵𝐵ℎ𝑦𝑦��

𝑋𝑋ℎ𝑦𝑦 = 𝐼𝐼𝐼𝐼 𝐴𝐴 ≥ 𝐵𝐵 𝑡𝑡ℎ𝑒𝑒𝑒𝑒 ��𝐴𝐴ℎ𝑦𝑦 − 𝐵𝐵ℎ𝑦𝑦�

�𝐵𝐵ℎ𝑦𝑦��

Expense

Unfavorable Variance: Actual greater than Budget

Favorable or No Variance: Actual less than or equal to Budget

𝑋𝑋ℎ𝑦𝑦 = 𝐼𝐼𝐼𝐼 𝐴𝐴 > 𝐵𝐵 𝑡𝑡ℎ𝑒𝑒𝑒𝑒 �−1×�𝐴𝐴ℎ𝑦𝑦 − 𝐵𝐵ℎ𝑦𝑦�

�𝐵𝐵ℎ𝑦𝑦��

𝑋𝑋ℎ𝑦𝑦 = 𝐼𝐼𝐼𝐼 𝐴𝐴 ≤ 𝐵𝐵 𝑡𝑡ℎ𝑒𝑒𝑒𝑒 ��𝐴𝐴ℎ𝑦𝑦 − 𝐵𝐵ℎ𝑦𝑦�

�𝐵𝐵ℎ𝑦𝑦��

𝑋𝑋ℎ𝑦𝑦 = actual to budget percent variance with each hospital (h) and respective year (y) 𝐴𝐴ℎ𝑦𝑦 = actual variable with each hospital (h) and respective year (y) 𝐵𝐵ℎ𝑦𝑦 = budget variable with each hospital (h) and respective year (y)

Figure 7. Favorable/unfavorable variance formulas for independent variables (X).

Data were prepared to convey consistent favorable (positive) and unfavorable

(negative) variance to budget measures for revenue, expense, and volume (see Figure 7).

Revenue and volume has an unfavorable (negative) variance when actual is less than

budget and favorable or no effect when actual is greater than or equal to budget. Expense

has an opposite variance calculation. Expense has an unfavorable (negative) variance

when actual is greater than budget and favorable or no effect when actual is less than or

equal to budget. The formulas used in the model determined the absolute value of the

34

difference between actual and budget then applied the appropriate negative or positive

variance for the respective revenue, expense, and volume.

Before including in the model, the favorable and unfavorable variables were

converted to binary dummy variables (favorable = 0, unfavorable = 1) for revenue,

expense, and volume (see Figure 8). In the full regression model, these dummy variables

identified the significance and association of a favorable or unfavorable relationship to

operating margin.

Revenue (Fav/Unf) = 0 (Favorable), 1 (Unfavorable) Expense (Fav/Unf) = 0 (Favorable), 1 (Unfavorable) Volume (Fav/Unf) = 0 (Favorable), 1 (Unfavorable)

Figure 8. Favorable/unfavorable dummy variable formulas.

In addition to understanding the favorable and unfavorable relationship,

interaction variables were added to the model for revenue, expense, and volume. The

interaction variables accounted for favorable/unfavorable as well as the magnitude of the

variance. To calculate the budget interaction variables the favorable/unfavorable dummy

variables were multiplied by the original budget variances for revenue, expense, and

volume (see Figure 9).

Revenue Interaction = Total Operating Revenue per APD × Revenue (Fav/Unf) Expense Interaction = Total Operating Expense per APD × Expense (Fav/Unf) Volume Interaction = Adjusted Patient Days (APD) × Volume (Fav/Unf)

Figure 9. Favorable/unfavorable budget variance interaction formulas.

By isolating the unfavorable budget variance relationships in the interaction

variables, the remaining or excluded variables were the favorable budget variances

captured in the full model by the original budget variances (Total Operating Revenue per

APD, Total Operating Expense per APD, and Adjusted Patient Days (APD).

35

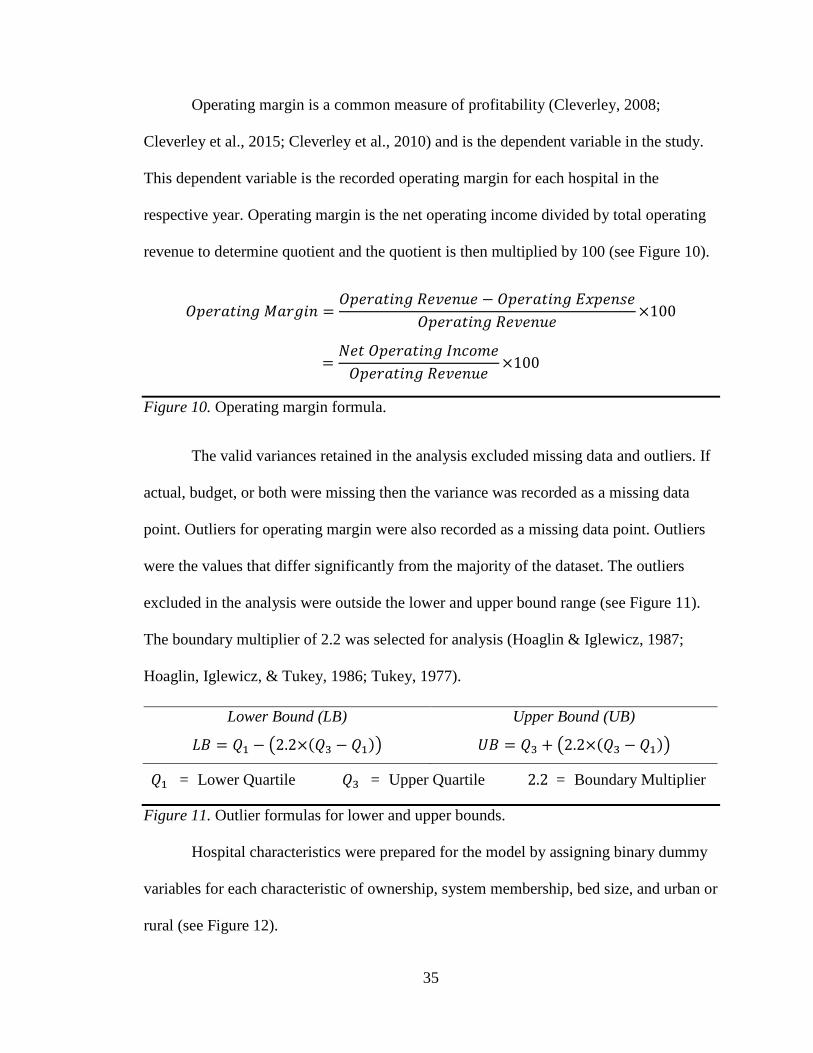

Operating margin is a common measure of profitability (Cleverley, 2008;

Cleverley et al., 2015; Cleverley et al., 2010) and is the dependent variable in the study.

This dependent variable is the recorded operating margin for each hospital in the

respective year. Operating margin is the net operating income divided by total operating

revenue to determine quotient and the quotient is then multiplied by 100 (see Figure 10).

𝑂𝑂𝑂𝑂𝑒𝑒𝑂𝑂𝑂𝑂𝑡𝑡𝑂𝑂𝑒𝑒𝑂𝑂 𝑀𝑀𝑂𝑂𝑂𝑂𝑂𝑂𝑂𝑂𝑒𝑒 =𝑂𝑂𝑂𝑂𝑒𝑒𝑂𝑂𝑂𝑂𝑡𝑡𝑂𝑂𝑒𝑒𝑂𝑂 𝑅𝑅𝑒𝑒𝑅𝑅𝑒𝑒𝑒𝑒𝑅𝑅𝑒𝑒 − 𝑂𝑂𝑂𝑂𝑒𝑒𝑂𝑂𝑂𝑂𝑡𝑡𝑂𝑂𝑒𝑒𝑂𝑂 𝐸𝐸𝐸𝐸𝑂𝑂𝑒𝑒𝑒𝑒𝐸𝐸𝑒𝑒

𝑂𝑂𝑂𝑂𝑒𝑒𝑂𝑂𝑂𝑂𝑡𝑡𝑂𝑂𝑒𝑒𝑂𝑂 𝑅𝑅𝑒𝑒𝑅𝑅𝑒𝑒𝑒𝑒𝑅𝑅𝑒𝑒×100

=𝑁𝑁𝑒𝑒𝑡𝑡 𝑂𝑂𝑂𝑂𝑒𝑒𝑂𝑂𝑂𝑂𝑡𝑡𝑂𝑂𝑒𝑒𝑂𝑂 𝐼𝐼𝑒𝑒𝐼𝐼𝐼𝐼𝐼𝐼𝑒𝑒

𝑂𝑂𝑂𝑂𝑒𝑒𝑂𝑂𝑂𝑂𝑡𝑡𝑂𝑂𝑒𝑒𝑂𝑂 𝑅𝑅𝑒𝑒𝑅𝑅𝑒𝑒𝑒𝑒𝑅𝑅𝑒𝑒×100

Figure 10. Operating margin formula.

The valid variances retained in the analysis excluded missing data and outliers. If

actual, budget, or both were missing then the variance was recorded as a missing data

point. Outliers for operating margin were also recorded as a missing data point. Outliers

were the values that differ significantly from the majority of the dataset. The outliers

excluded in the analysis were outside the lower and upper bound range (see Figure 11).

The boundary multiplier of 2.2 was selected for analysis (Hoaglin & Iglewicz, 1987;

Hoaglin, Iglewicz, & Tukey, 1986; Tukey, 1977).

𝑄𝑄1 = Lower Quartile 𝑄𝑄3 = Upper Quartile 2.2 = Boundary Multiplier

Figure 11. Outlier formulas for lower and upper bounds.

Hospital characteristics were prepared for the model by assigning binary dummy

variables for each characteristic of ownership, system membership, bed size, and urban or

rural (see Figure 12).

Lower Bound (LB)

𝐿𝐿𝐵𝐵 = 𝑄𝑄1 − �2.2×(𝑄𝑄3 − 𝑄𝑄1)�

Upper Bound (UB)

𝑈𝑈𝐵𝐵 = 𝑄𝑄3 + �2.2×(𝑄𝑄3 − 𝑄𝑄1)�

36

Not‐for‐Profit = excluded (1) For‐Profit = 0 (Other), 1 (For Profit) (2) Government = 0 (Other), 1 (Government) (3) System Membership = 0 (Stand Alone), 1 (System) Bed Size >300 = excluded (4) Bed Size 300‐101 = 0 (Other), 1 (300‐101) (5) Bed Size 100‐26 = 0 (Other), 1 (100‐26) (6) Bed Size ≤ 25 = 0 (Other), 1 (≤ 25) (7) Urban or Rural = 0 (Rural), 1 (Urban)

Figure 12. Hospital characteristics dummy variable formulas (1-7 included).

Five periods coinciding with significant macroeconomic change (economic

growth, adaptation to new regulation, and market downfalls) were added to the full model

to account for time and its potential effect. Time periods were prepared for the model by

assigning binary dummy variables for each period (see Figure 12). During positive

economic periods, higher operating margins (greater than 4%) were assigned a 1 and

lower operating margins a 0. During negative economic periods, lower operating margins

(less than 4%) were assigned a 1; higher operating margins were assigned a 0.

1987‐89 = excluded (1) 1990‐97 positive economic growth = 0 (Other), 1 (Operating Margin >4) (2) 1999‐02 adaptation to BBA of 1997 = 0 (Other), 1 (Operating Margin <4) (3) 2003‐07 positive economic growth = 0 (Other), 1 (Operating Margin >4) (4) 2008‐11 market downfall = 0 (Other), 1 (Operating Margin <4) (5) 2012‐13 positive economic growth = 0 (Other), 1 (Operating Margin >4)

Figure 13. Time dummy variable formulas (1-5 included).

The use of a 4% operating margin was selected based on a review of the average

and median operating margin trends for hospitals. The 2013 hospital medians by region

ranged from 2.3% to 4.5% with the Northwest median at 4.5% (Cleverley et al., 2015).

The 1994 to 2013 American Hospital Association (2014) reported the average hospital

operating margin as 4.0% , and the median as 3.8%.

37

Data Analysis

This study explored the relationships between variables using a non-experimental

research approach. This approach is defined by predictor variables that cannot be

controlled or altered. Relationships in non-experimental research describe a correlation

that could be valid in a larger population.

The first hypothesis addresses the budget variance relationship to operating

margin regardless of whether the variance is favorable or unfavorable. Hypothesis 1 tests

the assumption that more accurate forecasting and/or tighter management to the budget

matters in achieving higher operating margins. Hypotheses 2 and 3 test an additional

assumption that smaller unfavorable or greater favorable budget variances improves

operating margin performance.

Hypotheses 2 and 3 help clarify the impact of unfavorable and/or favorable

variances that could be masked in the results of Hypothesis 1. For example, the positive

and negative interaction and effect of non-isolated absolute value measures in Hypothesis

1 could lead to statistically significant budget variance relationships with the operating

margin but conflicting associations in comparing revenue, expense, and volume. To

address this potential conflict, the full model isolates unfavorable and favorable budget

variance measures.

To test the research question, the HPDS sample of the broader hospital population

was used to make generalizations or inferences about the hypothesized association in the

population. These sample tests and techniques are defined as inferential statistics. An

associational inferential statistic model was applied to determine both the correlation and

significance (regression). Multiple linear regression models were used to measure the

38

significance and association between the budget variance measures and operating margin

(see Figure 14).

Model A

Operating Margin (dependent variable) = β0 (intercept) +β1 (variance in Total Operating Revenue per Adjusted Patient Days)

Model B

Operating Margin (dependent variable) = β0 (intercept) +β2 (variance in Total Operating Expense per Adjusted Patient Days)

Model C

Operating Margin (dependent variable) = β0 (intercept) +β3 (variance Adjusted Patient Days)

Model D

Operating Margin (dependent variable) = β0 (intercept) +β1 (variance in Total Operating Revenue per Adjusted Patient Days) +β2 (variance in Total Operating Expense per Adjusted Patient Days) +β3 (variance Adjusted Patient Days)

Model E