Brazil: Responses to the Financial Crisis Responses to the Financial Crisis Lima, Peru March 2009...

59

1 Brazil: Responses to the Financial Crisis Lima, Peru March 2009 Mario Torós

Transcript of Brazil: Responses to the Financial Crisis Responses to the Financial Crisis Lima, Peru March 2009...

1

Brazil: Responses to theFinancial Crisis

Lima, PeruMarch 2009

Mario Torós

2

I. Domestic Economic Conditions

3

Domestic Demand x Supply

Domestic Demand

GDP

% against same quarter the year before

Source: IBGE

3.2

1.3

-4.5

-3.0

-1.5

0.0

1.5

3.0

4.5

6.0

7.5

9.0

1Q 03

3Q 03

1Q 04

3Q 04

1Q 05

3Q 05

1Q 06

3Q 06

1Q 07

3Q 07

1Q 08

4Q 08

4

Investment Growth

Source: IBGE

1Q99

1Q00

1Q01

1Q02

1Q03

1Q04

1Q05

1Q06

1Q07

1Q08

-15

-10

-5

0

5

10

15

20

annual growth1999/2003: -2.6%2004/2008: 9.9%

19.7

4Q08

3.8

% against same quarter the year before

5

Payroll

Source: IBGE

%

-8.2

1.6

4.25.9 5.8

6.97.8

-9.5

-7.5

-5.5

-3.5

-1.5

0.5

2.5

4.5

6.5

8.5

10.5

2003 2004 2005 2006 2007 2008Jan 09Jan 08

6

average 00/03664

average 04/081,415

thou

sand

average 95/99-323

-1,100

0

1,100

2,20019

95

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Job Creation

Source: MTE

1,452

7

Unemployment%

Source: IBGE

2004

20052006

2007

20087

8

9

10

11

12

13

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec6

6.8%

8

Credit Growth

Source: Banco Central

Jan

2004

=100

Households

Companies

Jan09/Jan08+23.2%

Jan09/Jan08 +37.2%

100130160190220250280310340370400

Jan 04

Jul 04

Jan 05

Jul 05

Jan 06

Jul 06

Jan 07

Jul 07

Jan 08

Jul 08

Jan 09

New loans (Jan09/Jan08)Companies -11.4Households -1.8total -8.1

9

Formal Job Creation

Source: MTE

mill

ion

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

Jan 95

Jan 96

Jan 97

Jan 98

Jan 99

Jan 00

Jan 01

Jan 02

Jan 03

Jan 04

Jan 05

Jan 06

Jan 07

Jan 08

Jan 09

2003645 thousand

average 1995-200249 thousand

average 2004-20081,415 thousand

10

Retail Sales20

03=1

00

3 month moving averageseasonally adjusted

Sources: IBGE and Banco Central

90

100

110

120

130

140

150

Jan 00

Jan 01

Jan 02

Jan 03

Jan 04

Jan 05

Jan 06

Jan 07

Jan 08

Jan 09

11

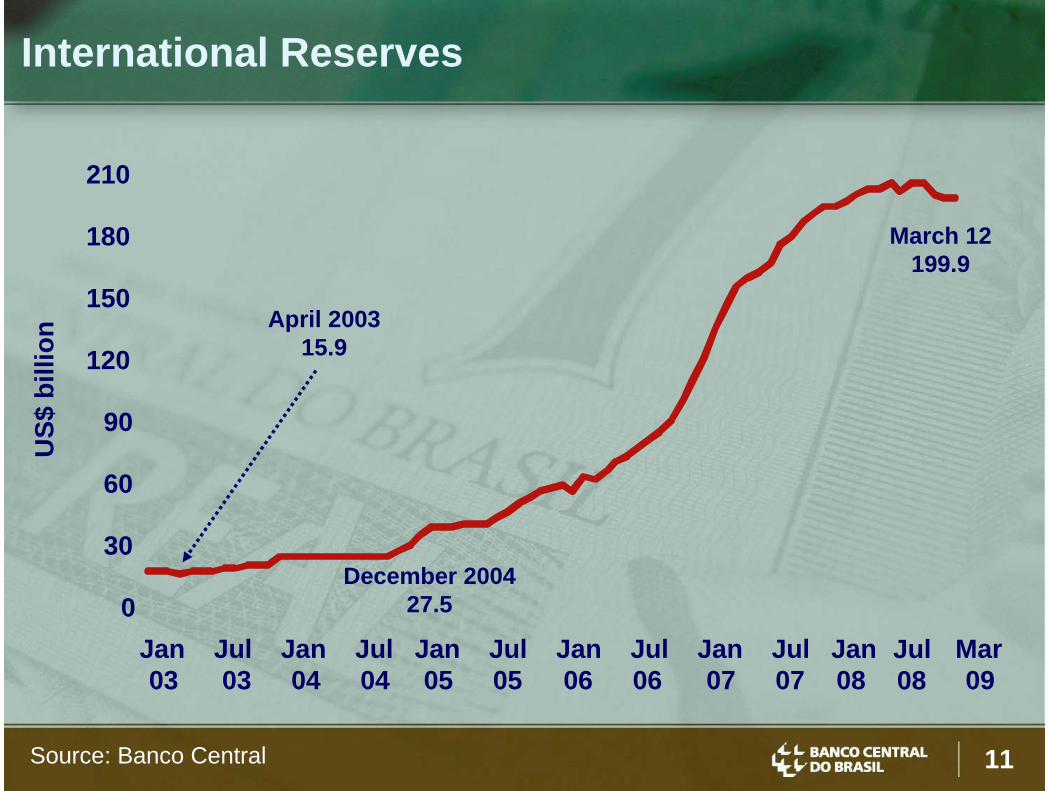

International ReservesU

S$ b

illio

n

Source: Banco Central

Jan 03

Jul 03

Jan 04

Jul04

Jan 05

Jul 05

Jan 06

Jul 06

Jan 07

Jul07

Jan 08

Mar 09

Jul08

December 200427.5

April 2003 15.9

March 12199.9

0

30

60

90

120

150

180

210

12

Public Sector External Debt/GDP%

Source: Banco Central

-5

0

5

10

15

20

25

30

35

40

45

90 92 94 96 98 00 02 04 06 08

Gross Debt/GDP Net Debt/GDP

13

Net External Debt x Sovereign Rating (S&P)

Sources: Banco Central and Bloomberg

US$

bill

ion

1Q 02

3Q 02

1Q 03

3Q 03

1Q 04

3Q 04

1Q 05

3Q 05

1Q 06

3Q 06

1Q 07

3Q 07

1Q 08

4Q 08

BBB-

BB+

BB

BB-

B+

BB-

-28.9

-40

0

40

80

120

160

200

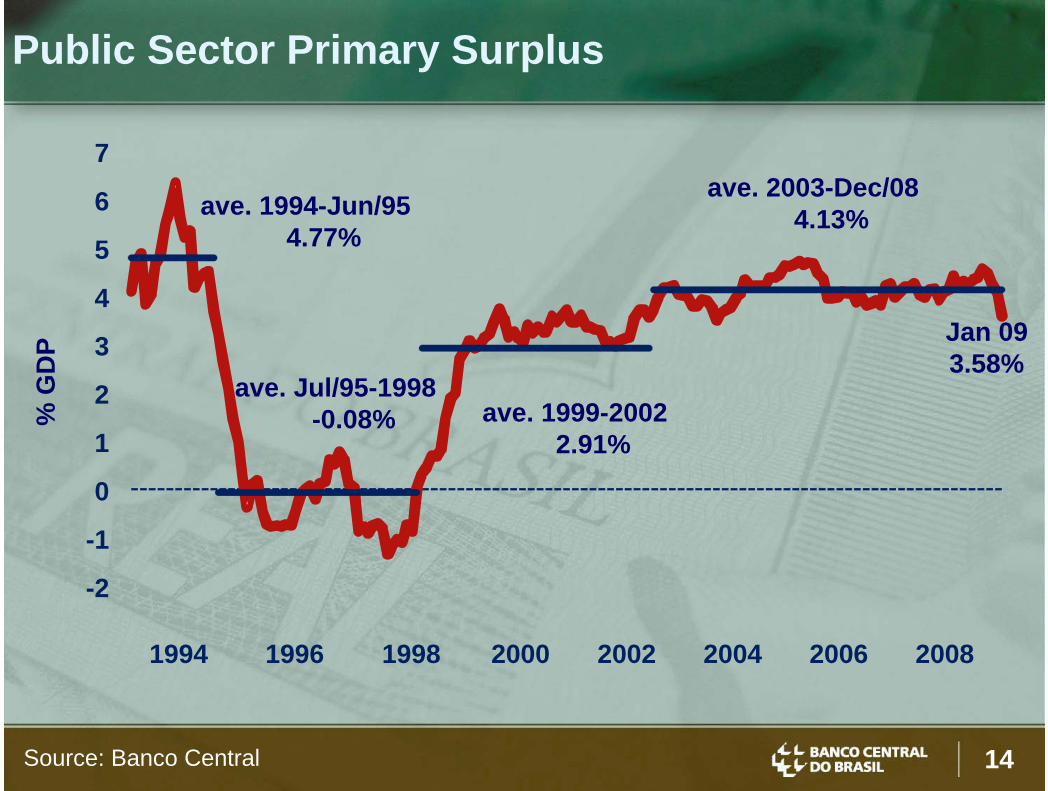

14

Public Sector Primary Surplus%

GD

P

Source: Banco Central

Jan 093.58%

ave. 1994-Jun/954.77%

ave. 1999-20022.91%

ave. 2003-Dec/084.13%

-2

-1

0

1

2

3

4

5

6

7

1994 1996 1998 2000 2002 2004 2006 2008

ave. Jul/95-1998-0.08%

15

% G

DP

Credit/GDP: Brazil x Central Economies - 2007

Sources: World Bank and Banco Central * January 2009

0

20

40

60

80

100

120

140

160

180

200

220

Brazil* Australia Sweden Canada Spain UK USA

41.2

16

Brazilian Banks: Capital Ratio

Source: Banco Central

%

Brazil 11%

Basel8%

6

8

10

12

14

16

18

20

2000 2001 2002 2003 2004 2005 2006 2007 2008

18.0%

Floor

17

Real Effective FX RateJu

n 94

=100

15 currency basket

Source: Banco Central

99.4

60

80

100

120

140

160

180

Jan 88

Jul 89

Jan 91

Jul 92

Jan 94

Jul 95

Jan 97

Jul 98

Jan 00

Jul 01

Jan 03

Jul 04

Jan 06

Jul 07

Jan 09

18

II. Crisis Impacts

19

“Commodities Boom and Bust”:CRB Index and Brazilian Terms of Trade

Sources: Funcex and Bloomberg

2006

=10

0

Terms of TradeCRB

Jan 03

Jul 03

Jan 04

Jul 04

Jan 05

Jul 05

Jan 06

Jul 06

Jan 07

Jul 07

Jan 08

Jan09

Jul 08

200

250

300

350

400

450

500

90

95

100

105

110

115

20

Commodities and Real FX Rate:Partial Offsetting

Jan

2006

= 1

00

Source: Bloomberg * March 6

Jan 06

Apr06

Jun 06

Sep06

Dec06

Mar 07

May07

Aug07

Nov 07

Feb08

May08

Jul 08

Oct08

Mar* 09

CRB/USD CRB/BRL

60

70

80

90

100

110

120

130

140

21

Stocks x Brazilian Real

Sources: Banco Central and BMFBovespa

poin

ts x

100

0

R$/

US$

Bovespa IndexFX Rate

1.50

1.75

2.00

2.25

2.50

25

35

45

55

65

75

Jun 07

Aug07

Oct07

Dec07

Feb08

Apr08

Jun 08

Jul 08

Sep08

Nov 08

Feb09

22

Industrial Output and Inflation (CPI)

USA EU Japan China Russia India Turkey South

Africal

Chile Colombia Mexico Peru Brazil

Sep 08 -6.3 -2.5 0.2 11.4 6.4 5.5 -4.2 4.7 3.6 -3.5 -2.2 ... 9.7

Oct 08 -4.2 -5.6 -7.1 8.2 1.7 -0.3 -8.5 -1.8 -0.8 -7.4 -2.3 ... 1.1

Nov 08 -5.9 -8.1 -16.6 5.4 -8.7 2.4 -13.9 -4.8 -5.7 -13.3 -5.4 ... -6.2

Dec 08 -7.8 ...-20.6 5.7 -10.2 ... ... ... -3.7 ... ... ... -14.5

USA EU Japan China Russia India Turkey South

Africa

Chile Colombia Mexico Peru Brazil

Sep 08 4.9 3.6 2.1 4.6 15.0 11.0 11.1 13.1 9.2 7.6 5.5 6.2 6.3

Oct 08 3.7 3.2 1.7 4.0 14.2 11.1 12.0 12.1 9.9 7.9 5.8 6.5 6.4

Nov 08 1.1 2.1 1.0 2.4 13.8 11.1 10.8 11.8 8.9 7.7 6.2 6.8 6.4

Dec 08 0.1 1.6 0.4 1.2 13.3 11.1 10.1 9.5 7.1 7.7 6.5 6.7 5.9

Dec-Sep (p.p.) -4.8 -2.0 -1.7 -3.4 -1.7 0.2 -1.0 -3.6 -2.1 0.1 1.1 0.4 -0.4

Industrial Output (% p.y.)

Inflation – Consumer Price Index (% p.y.)

23

Wholesale Prices

Source: FGV

% %

2

4

6

8

10

12

14

16

0

10

20

30

40

Jan 07

Mar 07

May07

Jul 07

Sep07

Nov 07

Jan 08

Mar 08

May08

Jul 08

Sep08

Nov 08

Jan 09

agricultureindustrial

in 12 months

24

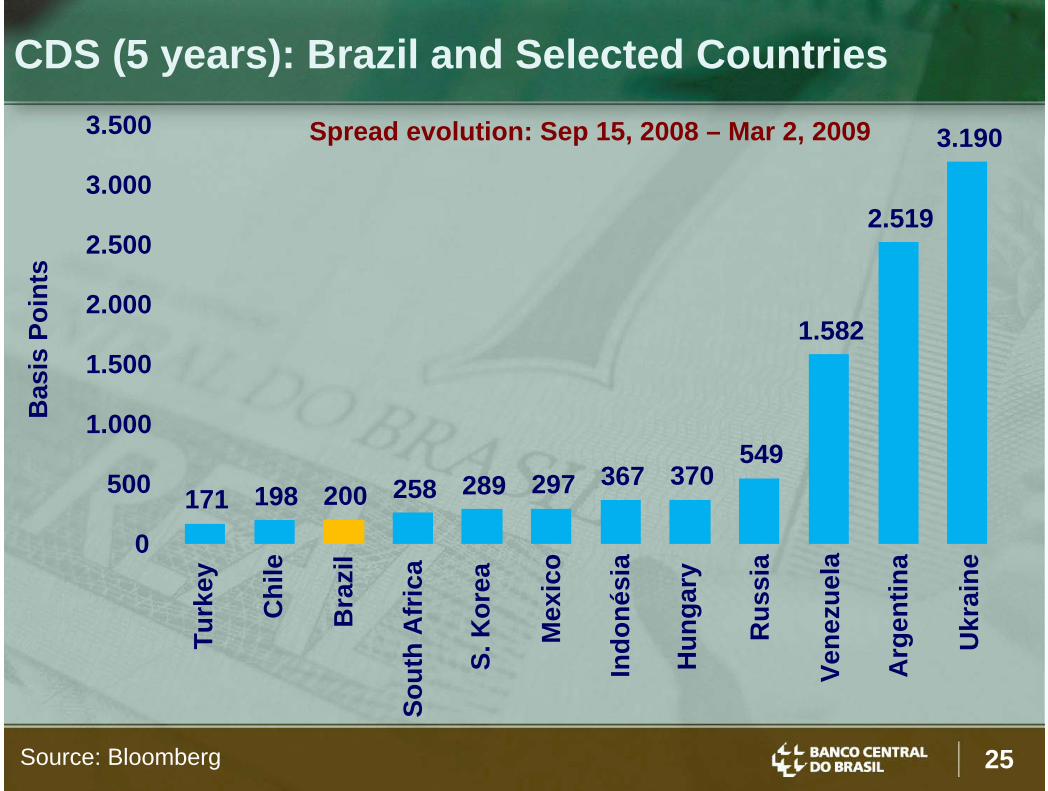

CDS (5 years): Brazil and Selected Countries

Source: Bloomberg

Spread evolution: Jun 14, 2007 – Mar 2, 2009

Chi

le

Turk

ey

Bra

zil

S. K

orea

Mex

ico

Sout

hA

fric

a

Indo

nesi

a

Hun

gary

Rus

sia

Vene

zuel

a

Arg

entin

a

Ukr

aine

Bas

ispo

ints

254 333 338 417 431 433 546 552 720

2.241

3.2483.608

0

500

1.000

1.000

2.000

2.500

3.000

3.500

4.000

25Source: Bloomberg

CDS (5 years): Brazil and Selected CountriesB

asis

Poin

ts

Spread evolution: Sep 15, 2008 – Mar 2, 2009

Turk

ey

Bra

zil

Chi

le

S. K

orea

Mex

ico

Sout

hA

fric

a

Indo

nési

a

Hun

gary

Rus

sia

Vene

zuel

a

Arg

entin

a

Ukr

aine

171 198 200 258 289 297 367 370549

1.582

2.519

3.190

0

500

1.000

1.500

2.000

2.500

3.000

3.500

26

%Stock Exchanges: Brazil and Selected Countries

Jun 14, 2007 – Mar 2, 2009

Source: BloombergIn

dia

Chi

na

Fran

ce

Japa

n

UK

Spai

n

Ger

man

y

USA

Hon

gK

ong

Bra

zil-60

-50

-40

-30

-20

-10

0NIKKEI CAC 40 S&P DAX Xangai FTSE IBEX 35 Mumbai H. Seng Ibovespa

27

Sep 15, 2008 – Mar 2, 2009

%

Source: Bloomberg

Stock Exchanges: Brazil and Selected Countries

Indi

a

Chi

na

Fran

ce

Japa

n

UK

Spai

n

Ger

man

y

USA

Hon

gK

ong

Bra

zil-45

-40-35-30-25-20-15-10-505

S&P NIKKEI Mumbai DAX CAC 40 H. Seng FTSE IBEX 35 Ibovespa Shanghai

28

Currencies: Brazil and Emerging Economies

Source: Bloomberg

Jun 14, 2007 – Mar 2, 2009

Arg

entin

a

Chi

le

Bra

zil

Hun

gary

Turk

ey

Indo

nési

a

Mex

ico

Sout

hA

fric

a

Rus

sia

S. K

orea

Ukr

aine

14.7 17.2

27.2 29.2 30.8 32.739.0

42.246.3

67.9 68.9

0

10

20

30

40

50

60

70

%

29

Sep 15, 2008 – Mar 2, 2009

Currencies: Brazil and Emerging Economies

Source: Bloomberg

%

Arg

entin

a

Chi

le

Sout

hA

fric

a

Bra

zil

S. K

orea

Indo

nési

a

Turk

ey

Hun

gary

Mex

ico

Rus

sia

Ukr

aine

13.8 16.7

26.9 30.235.0 36.9

41.0 41.9 43.6 44.0

76.8

0

10

20

30

40

50

60

70

80

30

Currencies: Brazil and Central Economies

Source: Bloomberg

-20.7

-5.6

5.8 5.9

17.8 21.127.1 29.8 32.7

40.1

52.3

-30-20-10

0102030405060

Japa

n

Switz

erla

nd

Euro

Den

mar

k

Nor

way

Can

ada

Bra

zil

Swed

en

Aus

tral

ia UK

New

Zeal

and

%

Jun 14, 2007 – Mar 2, 2009

31

Currencies: Brazil and Central Economies

Source: Bloomberg

%

-6.9

5.7

13.2 13.3

20.824.5

28.0 28.133.8 34.8 36.3

-10-505

10152025303540

Japa

n

Switz

erla

nd

Euro

Den

mar

k

Can

ada

Nor

way

Aus

tral

ia UK

N. Z

eala

nd

Bra

zil

Swed

en

Sep 15, 2008 – Mar 2, 2009

32

Currencies: Increased Volatility

0

10

20

30

40

50

60

70

80

May08

Jun08

Jul08

Aug08

Sep08

Oct08

Nov08

Dec08

Jan09

Brazil Mexico India S. Korea South AfricaEuro

33

Export Finance FX Flow (ACC)

Source: Banco Central

5 Day Moving Average

US$

mill

ion Lehman

Brothers

1st USD Repo

Auction

1st TradeFinanceAuction

50

100

150

200

250

300

350

400

9/5 9/19 10/3 10/17 10/31 11/14 11/28 12/12 12/26 1/9 1/23 2/6 2/20 2/27

34

CCI (Consumer Confidence Index)

90

95

100

105

110

115

120

125

Jan06

Jul06

Jan07

Jul07

Jan08

Jul08

Jan09

Consumer Confidence IndexCurrent SituationExpectations

Sep

2005

=100

Source: FGV

35

Business Expectations Index

Source: Fecap

110

115

120

125

130

135

Feb04

Oct04

Jun05

Feb06

Oct06

Jun07

Feb08

Jan09

36

Industrial Output20

02 =

100

s.a

.

Source: IBGE

90

95

100

105

110

115

120

125

130

135

Jan 01

Jul 01

Jan 02

Jul 02

Jan 03

Jul 03

Jan 04

Jul 04

Jan 05

Jul 05

Jan 06

Jul 06

Jan 07

Jul 07

Jan 08

Jul 08

Jan 09

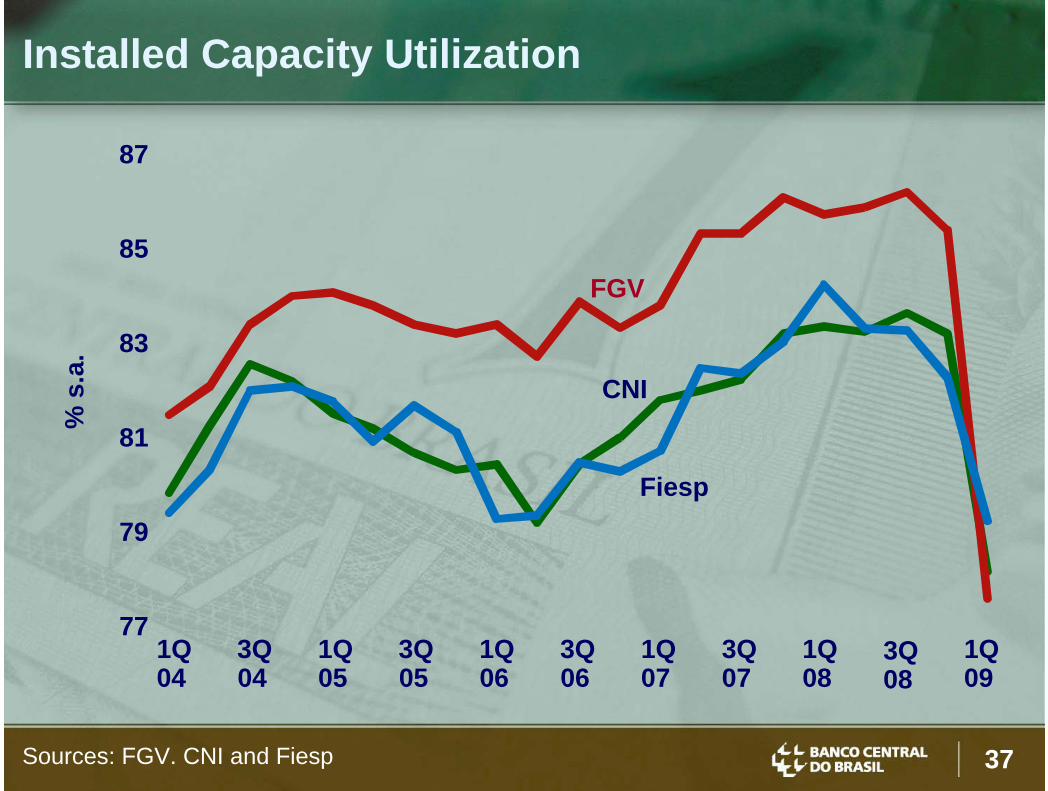

37

Installed Capacity Utilization

Sources: FGV. CNI and Fiesp

% s

.a.

1Q 04

3Q 04

1Q 05

3Q 05

1Q 06

3Q 06

1Q 07

3Q 07

1Q 08

1Q 09

77

79

81

83

85

87

CNI

FGV

Fiesp

3Q 08

38

ICI (Industrial Confidence Index)

Source: FGV

707580859095

100105110115120125

Jan06

Jul06

Jan07

Jul07

Jan08

Jul08

Jan09

Jul 2

005=

100

39

Inflation Target IPCA (12 months)

Sources: IBGE and Banco Central * March 6

MarketExpectations*

Feb 09 5.90%

20094.57%*

%

0

2

4

6

8

10

12

14

16

18

Jan 03

Jul 03

Jan 04

Jul 04

Jan 05

Jul 05

Jan 06

Jul 06

Jan 07

Jul 07

Jan 08

Jul 08

Jan 09

Jul 09

Jan 10

40

III. Central Bank Actions (so far…)

41

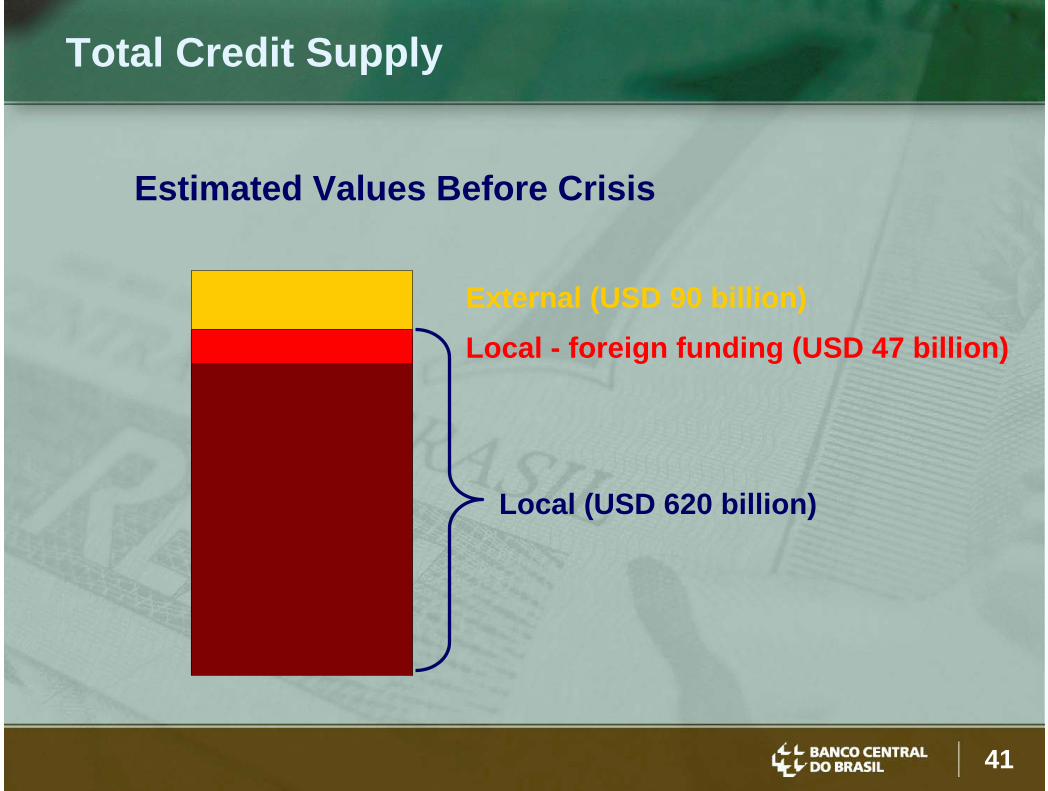

Total Credit Supply

External (USD 90 billion)

Local (USD 620 billion)

Estimated Values Before Crisis

Local - foreign funding (USD 47 billion)

42

September 24• Rise on reserve requirements over leasing

companies deposits postponed• “Additional Requirements” deduction value

rises from R$ 100 million to R$ 300 million• Measures freed up R$ 5.3 billion

Local Currency Liquidity

43

October 2• Up to 40% of Time Deposits Reserve

Requirements freed for acquisition of small banks (capital up to R$ 2.5 billion) assets

• Potential impact: R$ 25.3 billion

Local Currency Liquidity

44

October 8• Time Deposit Reserve Requirements

deduction value raised from R$ 300 million to R$ 700 million

• “Additional Requirements” ratio on cash and time deposits lowered from 8% to 5%

• Potential impact: R$ 21.8 billion

Local Currency Liquidity

45

October 13• “Additional Requirements” deduction raised

from R$ 300 million to R$ 1 billion• Time Deposit requirements deduction raised

from R$ 700 million to R$ 2 billion. Ratio for asset acquisition raised from 40% to 70%

• Capital ceiling of banks eligible to sell assets increased from R$ 2 billion to R$ 7 billion

• Potential impact: R$ 27.0 billion

Local Currency Liquidity

46

October 14• Facility for banks to use requirements for

buying other banks assets expanded• Demand Deposits reserve requirements

ratio lowered from 45% to 42%, freeing up R$ 4.0 billion

Local Currency Liquidity

47

October 14• National Monetary Council increases ratio

on demand deposits that banks must lend to agricultural sector from 25% to 30%

• Potential impact: R$ 4.5 billion for loans

Local Currency Liquidity

48

October 30• Changes on requirements framework to

foster use of liquidity freed up by previous measures

• 70% of time deposits requirements to be made in cash

• Target: to encourage large banks to acquire small banks assets

Local Currency Liquidity

49

November 13• Banks can use government bonds, instead

of cash, to meet part of the “Additional Reserve Requirements”

• Potential impact: R$ 42.1 billion

Local Currency Liquidity

50

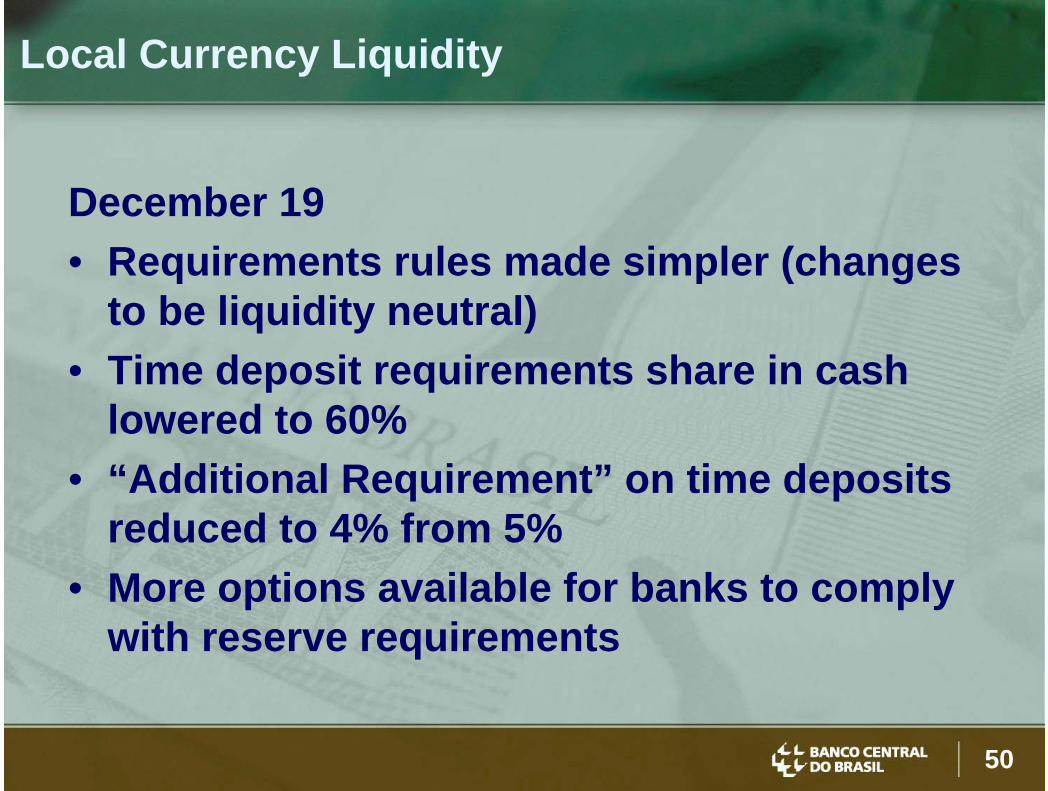

December 19• Requirements rules made simpler (changes

to be liquidity neutral)• Time deposit requirements share in cash

lowered to 60%• “Additional Requirement” on time deposits

reduced to 4% from 5%• More options available for banks to comply

with reserve requirements

Local Currency Liquidity

51

Local Currency Liquidity

Source: Banco Central

Reserve requirementseasying:

R$ 99.8 billionUS$ 43.3 billion

52

• Foreign currency swap contracts• Sales of USD in spot market• USD repurchase agreement auctions• Collateralized loans aimed at financing

exports• Currency swaps transactions with other

central banks (Fed)• Loans to companies and banks to roll over

external debts

Foreign Currency Liquidity

53

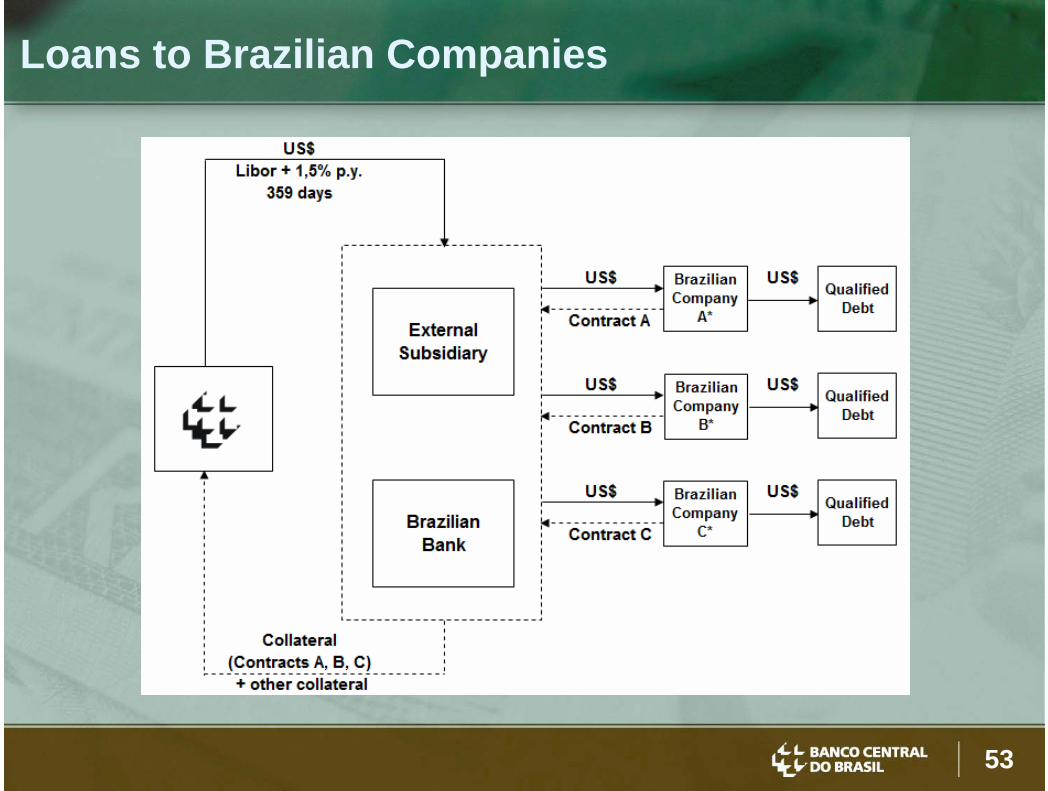

Loans to Brazilian Companies

54

Loans to Brazilian Banks

55

-20

-10

0

US$ billion

Mar 9th: US$ 11.0 billion

Currency Swaps Contracts

10

20

30

40

Mar/09Jun/07Sep/05Apr/02 Jan/04

Short in USD

Long in USD

Oct 1st: - US$ 21.4 billion

56

Foreign Currency Liquidity

57

Interest Rates

Source: Banco Central * 12/3

%

Selic (Overnight)6 Month Swap12 Month Swap

8

12

16

20

24

28

32

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Mar*09

58

Real Interest Rate (12 Month Swap)

Source: Banco Central * March 12

% ave. 96/9918.4%

ave. 00/0315.0%

ave. 04/0511.5%

ave. 06/088.2%

5

10

15

20

25

30

35

40

Jan96

Jan97

Jan98

Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Mar*09

5.4

59

Brazil: Responses to theFinancial Crisis

Lima, PeruMarch 2009

Mario Torós