Boston LDC Gas Forum - National Fuel Gas Company Fuel Gas Supply Corporation Boston LDC Gas Forum pp...

27

National Fuel Gas Supply Corporation Boston LDC Gas Forum Empire Pipeline, Inc. une 2014 Gas Forum – Ju Jeffrey Schauger G l M Boston LDC 1 General Manager Interstate Marketing

Transcript of Boston LDC Gas Forum - National Fuel Gas Company Fuel Gas Supply Corporation Boston LDC Gas Forum pp...

NationalFuelGasSupplyCorporationBoston LDC Gas Forum

pp y pEmpirePipeline,Inc.

une 2014

Gas Forum –Ju

Jeffrey SchaugerG l M

Boston LDC

1

General ManagerInterstate Marketing

National Fuel Gas CompanySafeHarborForForwardLookingStatementsf gThis presentation may contain “forward‐looking statements” as defined by the Private Securities Litigation Reform Act of 1995, including statements regarding future prospects, plans, objectives, goals, projections, estimates of oil and gas quantities, strategies, future events or performance and underlying assumptions, capital structure, anticipated capital expenditures, completion of construction projects, projections for pension and other post‐retirement benefit obligations, impacts of the adoption of new accounting rules, and possible outcomes of litigation or regulatory proceedings, as well as statements that are identified by the use of the words “anticipates,” “estimates,” “expects,” “forecasts,” “intends,” “plans,” “predicts,” “projects,” “believes,” “seeks,” “will,” “may,” and similar expressions. Forward‐looking statements involve risks and uncertainties which could cause actual results or outcomes to differ materially from those expressed in the forward‐looking statements. The Company’s expectations, beliefs and projections are expressed in good faith and are believed by the Company to have a reasonable basis, but there can be no assurance that management’s expectations, beliefs or projections will result or bein good faith and are believed by the Company to have a reasonable basis, but there can be no assurance that management s expectations, beliefs or projections will result or be achieved or accomplished.

In addition to other factors, the following are important factors that, in the view of the Company, could cause actual results to differ materially from those discussed in the forward‐looking statements: factors affecting the Company’s ability to successfully identify, drill for and produce economically viable natural gas and oil reserves, including among others geology, lease availability, title disputes, weather conditions, shortages, delays or unavailability of equipment and services required in drilling operations, insufficient gathering, processing and transportation capacity, the need to obtain governmental approvals and permits, and compliance with environmental laws and regulations; changes in laws, regulations or judicial interpretations to which the Company is subject, including those involving derivatives, taxes, safety, employment, climate change, other environmental matters, real property, and exploration and production activities such as hydraulic fracturing; governmental/regulatory actions, initiatives and proceedings, including those involving rate cases (which address, among other things, target rates of return, rate design and retained natural gas), environmental/safety requirements, affiliate relationships, industry structure, and franchise renewal; changes in the price of natural gas or oil; changes in price differentials between similar quantities of natural gas or oil sold at different geographic locations, and the effect of such changes on commodity production, revenues and demand for pipeline transportation capacity to or from such locations; other changes in price differentials between similar quantities of natural gas or oil having different quality, heating value, hydrocarbon mix or delivery date; impairments under the SEC’s full cost ceiling test for natural gas and oil reserves; uncertainty of oil and gas reserve estimates; significant differences between the Company’s projected and actual production levels for natural gas or oil; changes in demographic patterns and weather conditions; changes in the availability, price or accounting treatment

une 2014

of derivative financial instruments; delays or changes in costs or plans with respect to Company projects or related projects of other companies, including difficulties or delays in obtaining necessary governmental approvals, permits or orders or in obtaining the cooperation of interconnecting facility operators; financial and economic conditions, including the availability of credit, and occurrences affecting the Company’s ability to obtain financing on acceptable terms for working capital, capital expenditures and other investments, including any downgrades in the Company’s credit ratings and changes in interest rates and other capital market conditions; changes in economic conditions, including global, national or regional recessions, and their effect on the demand for, and customers’ ability to pay for, the Company’s products and services; the creditworthiness or performance of the Company’s key suppliers, customers and counterparties; economic disruptions or uninsured losses resulting from major accidents, fires, severe weather, natural disasters, terrorist activities, acts of war, cyber attacks or pest infestation; significant differences between the Company’s projected and actual capital expenditures and operating expenses; h i l t i l ti th i t t t i t d th t l /t t t l t d t th C ’ i d th t ti t b fit

Gas Forum –Ju changes in laws, actuarial assumptions, the interest rate environment and the return on plan/trust assets related to the Company’s pension and other post‐retirement benefits,

which can affect future funding obligations and costs and plan liabilities; the cost and effects of legal and administrative claims against the Company or activist shareholder campaigns to effect changes at the Company; increasing health care costs and the resulting effect on health insurance premiums and on the obligation to provide other post‐retirement benefits; or increasing costs of insurance, changes in coverage and the ability to obtain insurance.

Forward‐looking statements include estimates of oil and gas quantities. Proved oil and gas reserves are those quantities of oil and gas which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible under existing economic conditions, operating methods and government regulations. Other estimates of oil and gas quantities, including estimates of probable reserves, possible reserves, and resource potential, are by their nature more speculative than estimates

Boston LDC

2

Other estimates of oil and gas quantities, including estimates of probable reserves, possible reserves, and resource potential, are by their nature more speculative than estimates of proved reserves. Accordingly, estimates other than proved reserves are subject to substantially greater risk of being actually realized. Investors are urged to consider closely the disclosure in our Form 10‐K available at www.nationalfuelgas.com. You can also obtain this form on the SEC’s website at www.sec.gov.

For a discussion of the risks set forth above and other factors that could cause actual results to differ materially from results referred to in the forward‐looking statements, see “Risk Factors” in the Company’s Form 10‐K for the fiscal year ended September 30, 2013 and the Forms 10‐Q for the quarters ended December 31, 2013 and March 31, 2014. The Company disclaims any obligation to update any forward‐looking statements to reflect events or circumstances after the date thereof or to reflect the occurrence of unanticipated events.

NFG PL&S/Midstream Focus

NiagaraNiagaraChippawa

Hopewell

Corning

JacksonEllisburg

une 2014

Leidy

Gas Forum –Ju

Holbrook

Boston LDC

3

Winter 2014 – Buffalo, NYune 2014

Gas Forum –Ju

Boston LDC

4

Winter 2014 – Erie, PAune 2014

Gas Forum –Ju

Boston LDC

5

Recent Extreme Winter Conditions Send Throughput SoaringWinter Throughput on NFGSC

80,000

90,000

g p

60,000

70,000

(MDth)

40,000

50,000

onthly Throu

ghpu

t (

une 2014

20,000

30,000Mo

Gas Forum –Ju

0

10,000

Nov Dec Jan Feb Mar Nov Dec Jan Feb Mar Nov Dec Jan Feb Mar

Boston LDC

6

Winter 2011‐2012 Winter 2012‐2013 Winter 2013‐2014

Winter 13‐14: Top Gas Inventory Ends at 11.6 BcfNFGSC Storage Inventory

70

80

NFGSC Storage Inventory

50

60

22.1 Bcf

35.1 BcfMarch 15, 2012

40

50

Bcf April 8, 2013

Low of 11.6 Bcf on April 2, 2014

une 2014

20

30

April 2, 2014

Gas Forum –Ju

0

10

Boston LDC

7

Nov‐11 Feb‐12 May‐12 Aug‐12 Nov‐12 Feb‐13 May‐13 Aug‐13 Nov‐13 Feb‐14

Winter 2011‐2012

Winter 2012‐2013

Winter 2013‐2014

NFG PL&S/Midstream Focus

NiagaraNiagaraChippawa

Hopewell

Corning

JacksonEllisburg

une 2014

Leidy DRY GAS

Gas Forum –Ju

Holbrook

WET GASWET GASWET GAS

Boston LDC

8

Recent Expansions Have Transformed the System

ProjectProject

Northern Access 320,000 Dth/d

Tioga County Extension 350,000 Dth/d

( ) h/d

Northern Access

Tioga County Extension

Line N (2011, 2012 & 2013) 353,000 Dth/d

Total New Capacity 1,023,000 Dth/d

une 2014

Northern Access $72 million

Tioga County Extension $58 million

Line N (2011, 2012 & 2013) $58 millionLine N Projects

Gas Forum –Ju

Total Capital Expenditures * $188 million

Boston LDC

9* Capital Cost is for Expansion Only – Excludes Modernization Cost

Supply Corporation

Buffalo Station

201120112 New 2,370 HP Units

20 22012 2 New 10,310 HP Units

Recent Expansions Have Transformed the System

ProjectProject

Northern Access 320,000 Dth/d

Tioga County Extension 350,000 Dth/d

( ) h/d

Northern Access

Tioga County Extension

Line N (2011, 2012 & 2013) 353,000 Dth/d

Total New Capacity 1,023,000 Dth/d

une 2014

Northern Access $72 million

Tioga County Extension $58 million

Line N (2011, 2012 & 2013) $58 millionLine N Projects

Gas Forum –Ju

Total Capital Expenditures * $188 million

Boston LDC

11* Capital Cost is for Expansion Only – Excludes Modernization Cost

Supply Corporation

East AuroraEast AuroraStation

2 New 2,370 HP Units

Supply CorporationEllisburg Station

2 New 4,740 HP Units

Predominant Flows ‐ 2008une 2014

Gas Forum –Ju

Boston LDC

14

Predominant Flows ‐ 2008

Predominant Flows ‐ Currentune 2014

Gas Forum –Ju

Boston LDC

15

Predominant Flows ‐ Current

Directly Connected Production Continues to Increase1 00030 00

800

900

1,000

25.00

30.00

23.69 MMDth(846 MDth/d)

nth)

Day)

600

700 20.00

MDth

per M

on

(MDth per D

400

500 15.00

une 2014

(MM

2.74 MMDth(88 MDth/d)

200

300

5.00

10.00

Gas Forum –Ju ( / )

‐

100

0.00

n‐09

ar‐09

y‐09

ul‐09

p‐09

v‐09

n‐10

ar‐10

y‐10

ul‐10

p‐10

v‐10

n‐11

ar‐11

y‐11

ul‐11

p‐11

v‐11

n‐12

ar‐12

y‐12

ul‐12

p‐12

v‐12

n‐13

ar‐13

y‐13

ul‐13

p‐13

v‐13

n‐14

Boston LDC

16

Jan

Ma

May Ju Sep

No Jan

Ma

May Ju Sep

No Jan

Ma

May Ju Sep

No Jan

Ma

May Ju Sep

No Jan

Ma

May Ju Sep

No Jan

Upper Devonian ‐ NFGSC Marcellus ‐ NFGSC Marcellus ‐ NFG Midstream Marcellus ‐ Empire

NationalFuelisaMajorSWPATransporter

800

900

600

700

per D

ay)

400

500

hput (M

Dth

p

une 2014

200

300

Daily Throu

g

Gas Forum –Ju

0

100

2009 2010 2011 2012 2013 2014

Boston LDC

17

2009 2010 2011 2012 2013 2014

TCP DTI Equitrans Other TGP NFGSC

Source: Production Data – Bentek Northeast Natural Gas Production Monitor (November 2013)

h h

Niagara is Now a Net Export Point to Canada

500

600

NFGSC Throughput at Niagara

300

400

100

200

Dth/day

une 2014

(100)

0

MD

Gas Forum –Ju

(300)

(200)Northern Access project was placed in‐service

November 2012

Boston LDC

18

(400)Nov‐05 Nov‐06 Nov‐07 Nov‐08 Nov‐09 Nov‐10 Nov‐11 Nov‐12 Nov‐13

Midstream BusinessesDeliveringIntothePremiumEasternCanadianMarketg

$3 50

$4.00Dawn to Dominion South Point

Dawn to TGP 300 Zone 4

Differential

Differential

Winter 13/14 Premiums in Excess of $25

$3.00

$3.50

u

Dawn to TGP 300 ‐ Zone 4Differential

$2.00

$2.50

$ pe

r MMBtu

une 2014

$1.00

$1.50

Gas Forum –Ju

$0.00

$0.50

Boston LDC

19

$0.00

Source: ICE Daily Cash Prices

Line N Expansion to TGP 219 Pool

I S i N b 2014

Mercer Expansion

In‐Service: November 2014

System: NFGSC

Capacity: 105,000 Dth/day

Market: Range Resources

Executed PA; 10 Yrs

Interconnect( )

Mercer Expansion

une 2014

Mercer (TGP Station 219)

Capital Cost: $33.6 Million Expansion: $29.6 million System Modernization: $4 million

Mercer(TGP Station

219)

Gas Forum –Ju

Facilities 3,550 HP Compressor 2.08 miles – 24” Replacement Pipeline

Boston LDC

20

Continued Expansion to TGP 219 Pool & TETCO M2

In‐Service: November 2015

Westside Expansion & Modernization

In Service: November 2015

System: NFGSC

Capacity: 175,000 Dth/day Market:

Executed PA with Range Resources; 145,000 Dth per day; 10 Yrs

Executed PA with Seneca Resources; 30,000 Dth per day; 10/15 Yrs

Interconnect

une 2014

Mercer(TGP Station

219)

Interconnect Mercer (TGP Station 219) Holbrook (TETCO)

Capital Cost: $76.2 million Expansion: $39 6 million

Westside Expansion & Modernization

Gas Forum –Ju Expansion: $39.6 million

System Modernization: $36.6 million

Facilities 3,550 HP Compressor 23 3 miles – 24” Replacement Pipeline

Holbrook (TETCO)

Boston LDC

21

23.3 miles 24 Replacement Pipeline

Deliveries into Eastern Canada

In‐Service: November 2015

Northern Access 2015

Canada & In Service: November 2015

System: NFGSC

Capacity: 140,000 Dth/dayN th

Canada & Eastern U.S.

Niagara (TCPL) Market: Executed PA – Lease

arrangement with TGP

Overall Path

Northern Access 2015

Niagara (TCPL)

une 2014

Producing area to Niagara

Capital Cost: $66 million

Facilities

Clermont

Gas Forum –Ju Facilities

15,400 HP Hinsdale CS 7,700 HP Concord CS East Eden M&R Upgrades

Delivery Point

Boston LDC

22

y

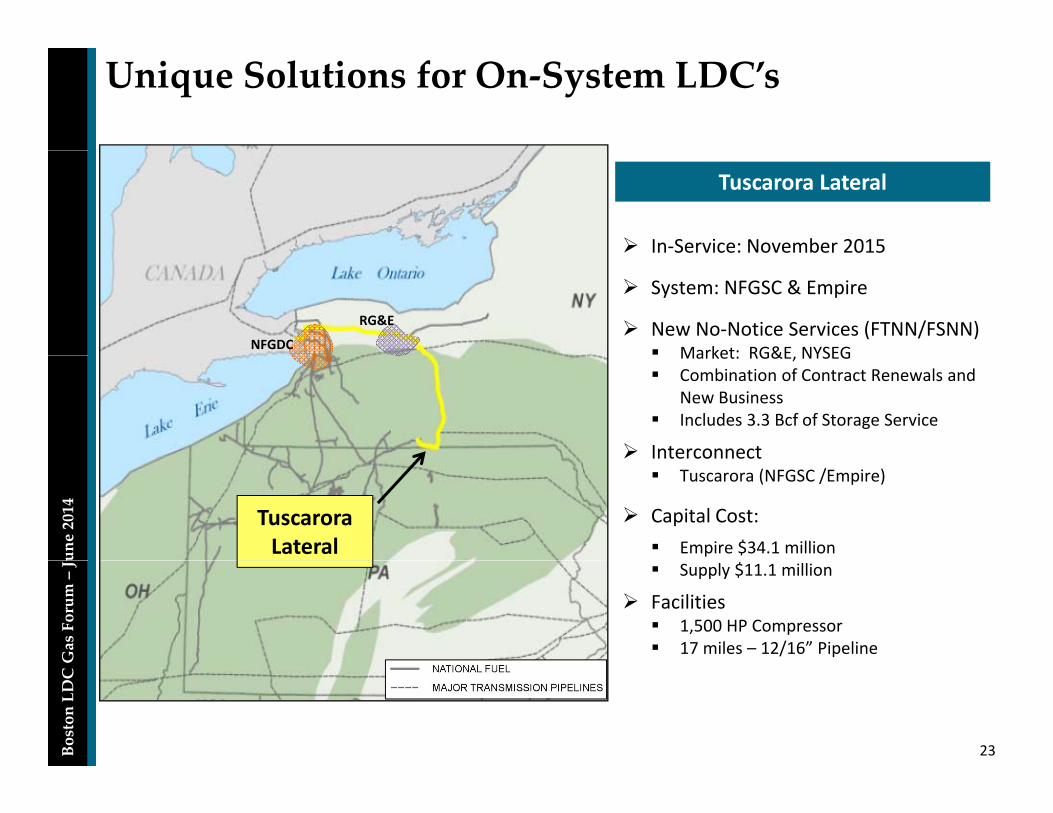

Unique Solutions for On‐System LDC’s

In‐Service: November 2015

Tuscarora Lateral

System: NFGSC & Empire

New No‐Notice Services (FTNN/FSNN) Market: RG&E NYSEGNFGDC

RG&E

Market: RG&E, NYSEG Combination of Contract Renewals and

New Business Includes 3.3 Bcf of Storage Service

Interconnect

une 2014

Interconnect Tuscarora (NFGSC /Empire)

Capital Cost: Empire $34.1 million

Tuscarora Lateral

Gas Forum –Ju Supply $11.1 million

Facilities 1,500 HP Compressor 17 miles – 12/16” Pipeline

Boston LDC

23

Additional Projects into Eastern CanadaNorthern Access 2016

Open Seasons in Progress: OS#195 ‐ NFGSC OS#12 ‐ Empire

Capacity: ~350,000 Dth/day Proposed Facilities Include: 100+ miles of 24”/30” Pipeline

Proposed In‐Service: Nov 2016

Transport Path: NFGSC to Empire @ Pendleton, with Deliveries to Chippawa

100+ miles of 24 /30 Pipeline Empire Compressor Station for

Pendleton deliveries Empire Dehydration M&R Facilities M&R Facilities

Chippawa(TCPL)

une 2014 Northern

Access 2016

Gas Forum –Ju

Boston LDC

24

Delivery Point

Empire South‐to‐North Expandability

Status: Open Season pending –J /J l 2014

2017 Empire Expansion

June/July 2014

Proposed In‐Service: Nov 2017

Capacity: ~325,000 Dth/day

26 Mile, 24”

p y , / y Gas Supply: Marcellus, Utica, NFG

Storage Delivery Points: Chippawa, TGP

une 2014

,ExtensionJackson200, other On‐System Points

Receipts: TGP 300, PVR, Jackson, Corning, Tuscarora

i ili i l d

TGP 300

Gas Forum –Ju Prospective Facilities May Include:

26 miles of 24” Pipeline from Jackson, PA to vicinity of TGP 300 Line

Boston LDC

25

3 Compressor Stations

Continued Line N Expansion

Line N 2017

Status: Finalizing Design, Open Season: Summer 2014

Proposed In‐Service: 2017p

Capacity: TBD

Gas Supply: Marcellus, Utica

une 2014

Delivery Points: Holbrook, Mercer, REX

Receipts: Producers in

Mercer

Gas Forum –Ju Receipts: Producers in

Marcellus/Utica Fairway

lb k

Line N 2017

REX

Boston LDC

26

HolbrookREX

ThankYou

une 2014

Gas Forum –Ju

Boston LDC

27