Bond Portfolio Management

26

1 Bond Portfolio Management Term Structure Yield Curve Expected return versus forward rate Term structure theories Managing bond portfolios Duration Convexity Immunization and trading strategy

-

Upload

bevis-browning -

Category

Documents

-

view

41 -

download

0

description

Bond Portfolio Management. Term Structure Yield Curve Expected return versus forward rate Term structure theories Managing bond portfolios Duration Convexity Immunization and trading strategy. Overview of Term Structure. The relationship between yield to maturity and maturity. - PowerPoint PPT Presentation

Transcript of Bond Portfolio Management

1

Bond Portfolio Management

Term Structure Yield Curve Expected return versus forward rate Term structure theories

Managing bond portfolios Duration Convexity Immunization and trading strategy

2

The relationship between yield to maturity and maturity.

Information on expected future short term rates can be implied from yield curve.

The yield curve is a graph that displays the relationship between yield and maturity.

Three major theories are proposed to explain the observed yield curve.

Overview of Term Structure

3

Figure 15.1 Treasury Yield Curves

1). Pure yield curve; 2). on-the-run yield curve (page 485)

4

Table 15.1

1-year rate is 5%, 2-year rate is 6%, 3-year rate is 7%, 4-year rate is 8%. Compute the yield to maturity of a 3-year coupon bond with a coupon rate of 10%.

5

11)1(

)1()1(

n

n

nn

n y

yf

fn = one-year forward rate for period n

yn = yield for a security with a maturity of n

)1()1()1( 11 n

nn

nn fyy

Forward Rates from Observed Rates

6

Example: page 487

4 yr = 8.00% 3yr = 7.00% f4 = ?

7

Downward Sloping Spot Yield Curve

Zero-Coupon Rates Bond Maturity12% 111.75% 211.25% 310.00% 49.25% 5

8

Forward Rates Downward Sloping Y C

1yr Forward Rates

1yr= = 0.115006

2yrs= = 0.102567

3yrs= = 0.063336

4yrs= = 0.063008

9

Expectation Theory Forward rate = expected rate (page 494)

Liquidity Premium Theory Upward bias over expectations Equation 15.8 on page 499

Theories of Term Structure

10

Figure 15.4 Yield Curves

11

Figure 15.4 Yield Curves (Concluded)

12

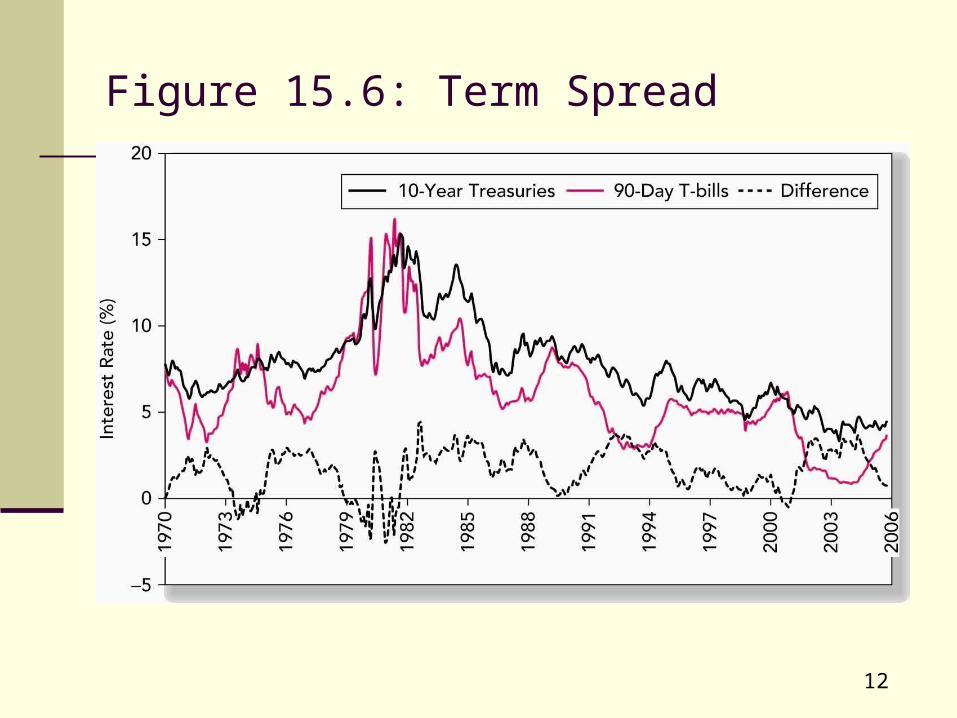

Figure 15.6: Term Spread

13

A measure of the effective maturity of a bond. The weighted average of the times until each payment is received,

with the weights proportional to the present value of the payment. Duration is shorter than maturity for all bonds except zero coupon

bonds. Duration is equal to maturity for zero coupon bonds.

Duration

14

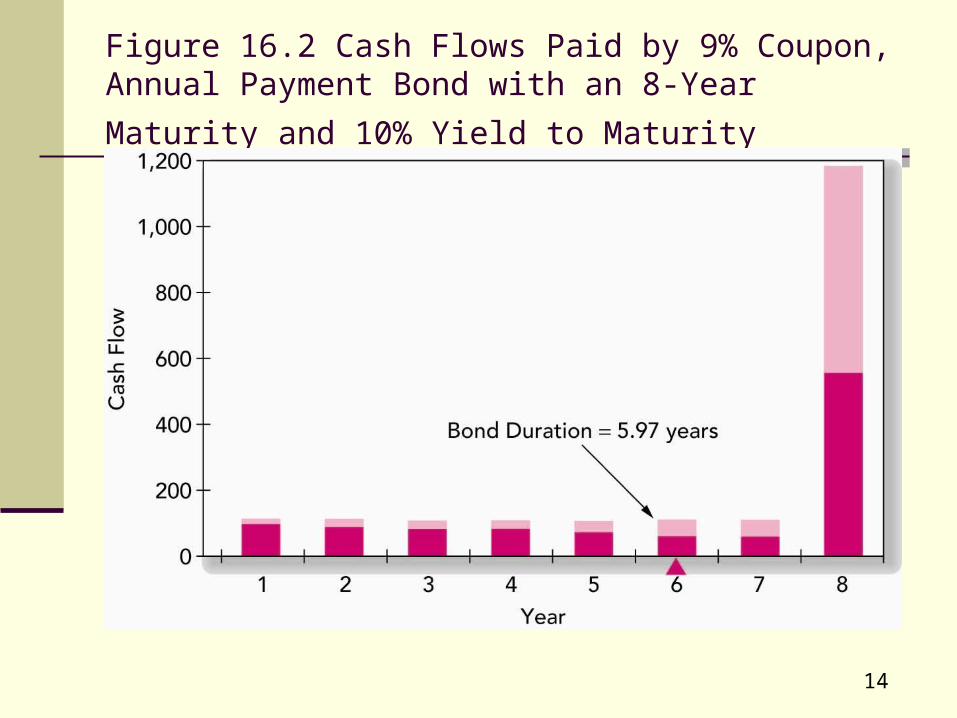

Figure 16.2 Cash Flows Paid by 9% Coupon, Annual Payment Bond with an 8-Year Maturity and 10% Yield to

Maturity

15

t tt

w CF y ice ( )1 Pr

twtDT

t

1

CF Cash Flow for period tt

Duration: Calculation

16

Example: Duration

See page 516-517.

17

Price change is proportional to duration and not to maturity.

P/P = -D x [(1+y) / (1+y)

D* = modified duration

D* = D / (1+y)

P/P = - D* x y

Duration/Price Relationship

18

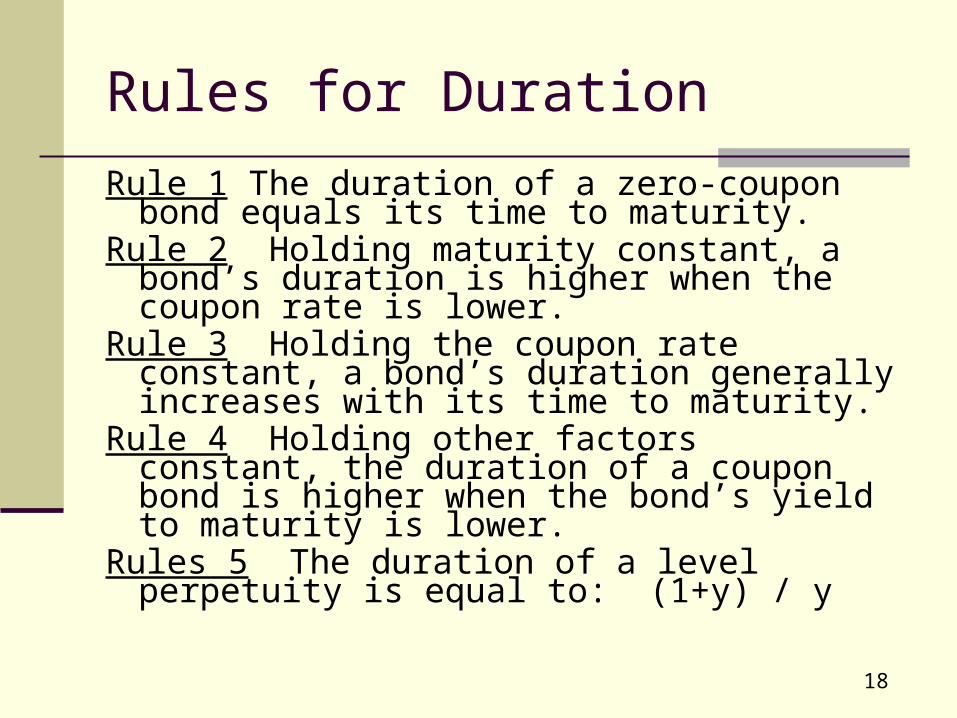

Rules for Duration

Rule 1 The duration of a zero-coupon bond equals its time to maturity.

Rule 2 Holding maturity constant, a bond’s duration is higher when the coupon rate is lower.

Rule 3 Holding the coupon rate constant, a bond’s duration generally increases with its time to maturity.

Rule 4 Holding other factors constant, the duration of a coupon bond is higher when the bond’s yield to maturity is lower.

Rules 5 The duration of a level perpetuity is equal to: (1+y) / y

19

Figure 16.3 Bond Duration versus Bond Maturity

20

Correction for Convexity

n

tt

t tty

CF

yPConvexity

1

22

)()1()1(

1

Correction for Convexity:

])([21 2yConveixityyD

P

P

21

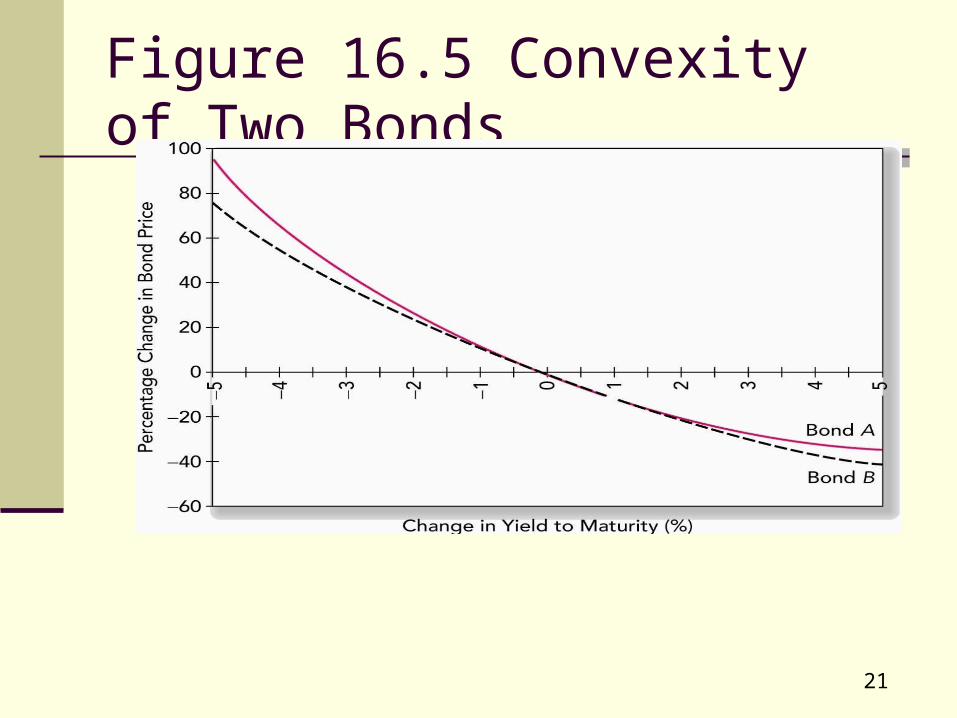

Figure 16.5 Convexity of Two Bonds

Which bond does you prefer?

22

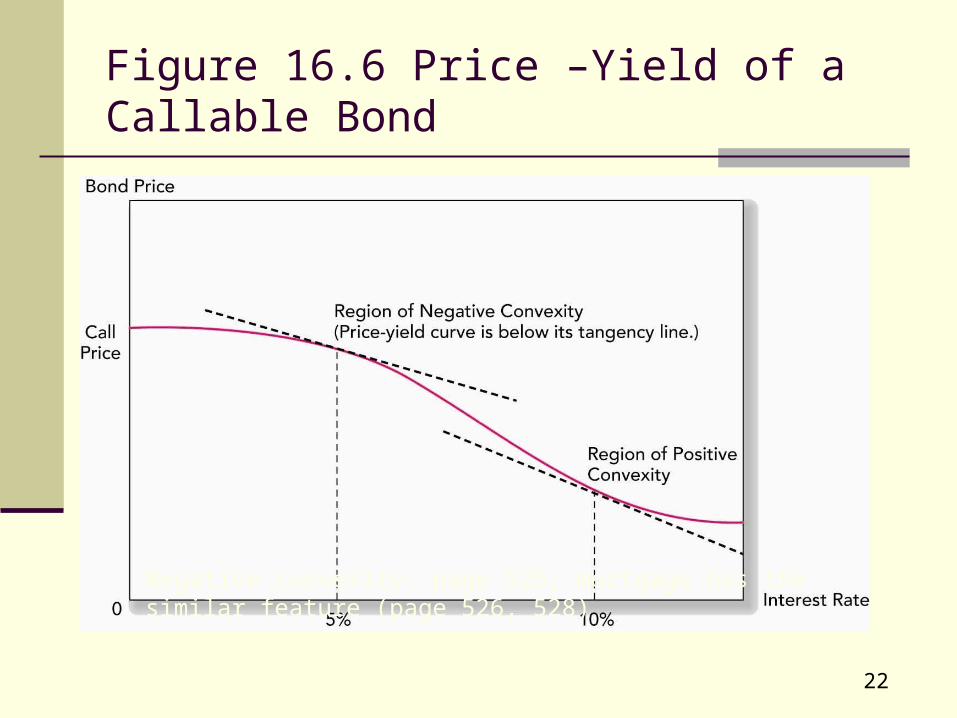

Figure 16.6 Price –Yield of a Callable Bond

Negative convexity: page 526; mortgage has the similar feature (page 526, 528)

23

Bond-Index Funds Lehman Aggregate Bond index Salomon Smith Barney Broad Investment Grade (BIG) Index Merrill Lynch U.S. Broad Market Index

Immunization of interest rate risk: Net worth immunization

Duration of assets = Duration of liabilities Target date immunization

Holding Period matches Duration

Cash flow matching and dedication Covered in fixed income class

Passive Management

24

Immunization

Price risk Reinvestment Immunization is the point that two effects are

cancelled out.

25

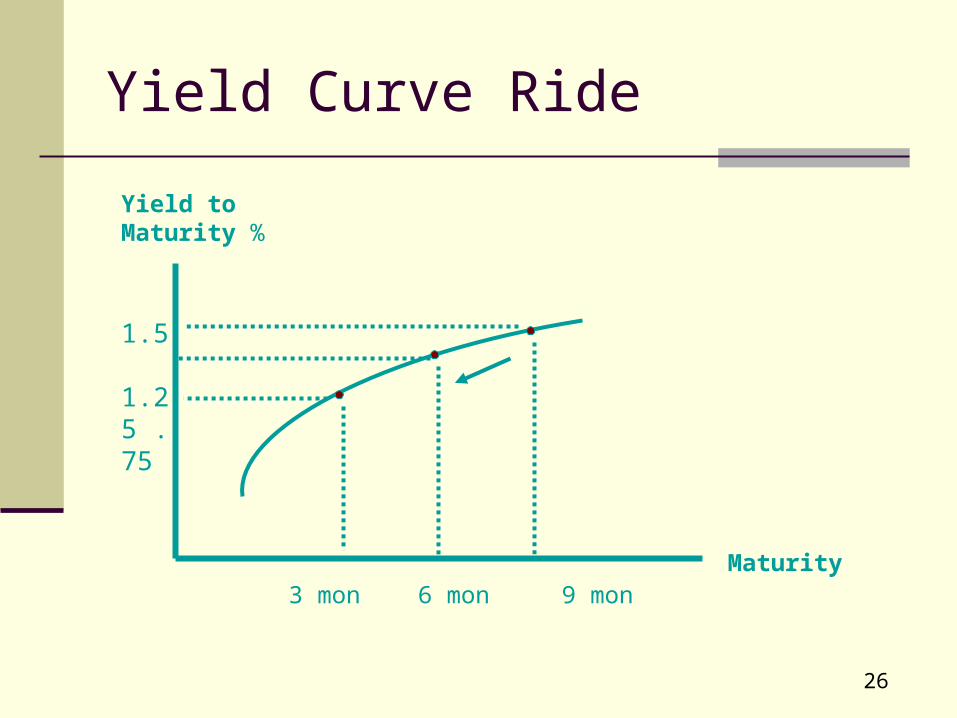

The key idea is to predict the interest rate movement

Or simply riding on the yield curve

Active Management: Swapping Strategies

26

Maturity

Yield to Maturity %

3 mon 6 mon 9 mon

1.5 1.25 .75

Yield Curve Ride

![PP20-Bond Portfolio Management[V1]](https://static.fdocuments.us/doc/165x107/577cd5891a28ab9e789b0bf6/pp20-bond-portfolio-managementv1.jpg)