Chapter 20 BOND PORTFOLIO MANAGEMENT. Chapter 20 Questions What are three major bond-portfolio...

25

Chapter 20 Chapter 20 BOND PORTFOLIO MANAGEMENT BOND PORTFOLIO MANAGEMENT

-

Upload

ashlynn-whitehead -

Category

Documents

-

view

232 -

download

6

Transcript of Chapter 20 BOND PORTFOLIO MANAGEMENT. Chapter 20 Questions What are three major bond-portfolio...

Chapter 20Chapter 20

BOND PORTFOLIO BOND PORTFOLIO MANAGEMENTMANAGEMENT

Chapter 20 QuestionsChapter 20 Questions

• What are three major bond-portfolio What are three major bond-portfolio management strategies?management strategies?

• What are the two specific strategies for What are the two specific strategies for passive portfolio management?passive portfolio management?

• What are the six strategies for active What are the six strategies for active portfolio management?portfolio management?

• What do we mean by matched-funding What do we mean by matched-funding techniques, and what are the four specific techniques, and what are the four specific strategies?strategies?

Chapter 20 QuestionsChapter 20 Questions

• How are futures contracts used to hedge How are futures contracts used to hedge against cash deposits or withdrawals from a against cash deposits or withdrawals from a bond portfolio?bond portfolio?

• How are futures used to change the How are futures used to change the systematic risk (i.e., duration) of an actively systematic risk (i.e., duration) of an actively managed portfolio?managed portfolio?

• What are some of the general advantages What are some of the general advantages of using derivatives in bond-portfolio of using derivatives in bond-portfolio management?management?

Alternative Bond Portfolio Alternative Bond Portfolio StrategiesStrategies

1. Passive portfolio strategies1. Passive portfolio strategies

2. Active management strategies2. Active management strategies

3. Matched-funding techniques3. Matched-funding techniques

Passive Portfolio Passive Portfolio StrategiesStrategies

• Passive strategies Passive strategies emphasize buy-and-emphasize buy-and-hold, low energy hold, low energy managementmanagement

• Try to earn the Try to earn the market return rather market return rather than beat the than beat the market returnmarket return

Passive Portfolio Passive Portfolio StrategiesStrategies

• Buy and holdBuy and hold– Buy a portfolio of bonds and hold them to maturityBuy a portfolio of bonds and hold them to maturity– Can by modified by trading into more desirable Can by modified by trading into more desirable

positionspositions

• IndexingIndexing– Match performance of a selected bond indexMatch performance of a selected bond index– Performance analysis involves examining tracking Performance analysis involves examining tracking

error for differences between portfolio error for differences between portfolio performance and index performanceperformance and index performance

Active Management Active Management StrategiesStrategies

• Active management Active management strategies attempt to strategies attempt to beat the marketbeat the market

• Mostly the success Mostly the success or failure is going to or failure is going to come from the come from the ability to accurately ability to accurately forecast future forecast future interest ratesinterest rates

Active Management Active Management StrategiesStrategies

• Interest-rate anticipationInterest-rate anticipation– Risky strategy relying on uncertain forecasts of Risky strategy relying on uncertain forecasts of

future interest rates, adjusting portfolio durationfuture interest rates, adjusting portfolio duration– Ladder strategy staggers maturitiesLadder strategy staggers maturities– Barbell strategy splits funds between short Barbell strategy splits funds between short

duration and long duration securitiesduration and long duration securities

• Valuation analysis Valuation analysis – A form of fundamental analysis, this strategy A form of fundamental analysis, this strategy

selects bonds that are thought to be priced below selects bonds that are thought to be priced below their estimated intrinsic valuetheir estimated intrinsic value

Active Management Active Management StrategiesStrategies

• Credit analysisCredit analysis– Detailed analysis of the bond issuerDetailed analysis of the bond issuer– Determines expected changes in default riskDetermines expected changes in default risk– Try to predict rating changes and trade Try to predict rating changes and trade

accordinglyaccordingly• Buy bonds with expected upgradesBuy bonds with expected upgrades• Sell bonds with expected downgradesSell bonds with expected downgrades

Active Management Active Management StrategiesStrategies

• Yield-spread analysisYield-spread analysis– Monitor spreads within and across sectors, bond Monitor spreads within and across sectors, bond

ratings, or industriesratings, or industries– Trade in anticipation of changing spreadsTrade in anticipation of changing spreads

• Bond swapsBond swaps– Selling one bond (S) and purchasing another (P) Selling one bond (S) and purchasing another (P)

simultaneouslysimultaneously– Swaps to increase current yield or YTM, take Swaps to increase current yield or YTM, take

advantage of shifts in interest rates or realignment advantage of shifts in interest rates or realignment of yield spreads, improve quality of portfolio, or for of yield spreads, improve quality of portfolio, or for tax purposestax purposes

Active Management Active Management StrategiesStrategies

• Bond SwapsBond Swaps– Pure yield pickup swapPure yield pickup swap

• Swapping low-coupon bonds into higher coupon bondsSwapping low-coupon bonds into higher coupon bonds

– Substitution swapSubstitution swap• Swapping a seemingly identical bond for one that is Swapping a seemingly identical bond for one that is

currently thought to be undervaluedcurrently thought to be undervalued

– Tax swapTax swap• Swap in order to manage tax liability (taxable & munis)Swap in order to manage tax liability (taxable & munis)

– Swap strategies and market-efficiencySwap strategies and market-efficiency• Bond swaps by their nature suggest market inefficiencyBond swaps by their nature suggest market inefficiency

Active Management Active Management StrategiesStrategies

• Core-PlusCore-Plus– A combination approach of passive and active bond A combination approach of passive and active bond

management stylesmanagement styles– A large, significant part of the portfolio is passively A large, significant part of the portfolio is passively

managed in one of two sectors:managed in one of two sectors:• The U.S. aggregate sector, which includes mortgage-The U.S. aggregate sector, which includes mortgage-

backed and asset-backed securitiesbacked and asset-backed securities• The U.S. Government/Corporate sector aloneThe U.S. Government/Corporate sector alone

– The rest of the portfolio is actively managedThe rest of the portfolio is actively managed• Often focused on high yield bonds, foreign bonds, Often focused on high yield bonds, foreign bonds,

emerging market debtemerging market debt• Diversification effects help to manage risksDiversification effects help to manage risks

Matched-Funding Matched-Funding TechniquesTechniques

• Classical (“pure”) immunization strategies Classical (“pure”) immunization strategies attempt to earn a specified rate of return attempt to earn a specified rate of return regardless of changes in interest ratesregardless of changes in interest rates– Must balance the components of interest rate riskMust balance the components of interest rate risk

• Price risk: problem with rising interest ratesPrice risk: problem with rising interest rates• Reinvestment risk: problem with falling interest ratesReinvestment risk: problem with falling interest rates

– Immunize a portfolio from interest rate risk by Immunize a portfolio from interest rate risk by keeping the portfolio duration equal to the keeping the portfolio duration equal to the investment horizoninvestment horizon

• Duration strategy superior to a strategy based only a Duration strategy superior to a strategy based only a maturity since duration considers both sources of maturity since duration considers both sources of interest rate riskinterest rate risk

Matched-Funding Matched-Funding StrategiesStrategies

Many immunization Many immunization strategies are strategies are designed to take the designed to take the sting out of rising sting out of rising interest rates for a interest rates for a bond portfolio!bond portfolio!

Matched-Funding Matched-Funding TechniquesTechniques

• Immunization StrategiesImmunization Strategies– Difficulties in Maintaining Immunization Difficulties in Maintaining Immunization

StrategyStrategy• Rebalancing required as duration declines Rebalancing required as duration declines

more slowly than term to maturitymore slowly than term to maturity• Modified duration changes with a change in Modified duration changes with a change in

market interest ratesmarket interest rates• Yield curves shiftYield curves shift

Matched-Funding Matched-Funding TechniquesTechniques

Dedicated portfoliosDedicated portfolios• Designing portfolios that will service liabilitiesDesigning portfolios that will service liabilities• Different types:Different types:

– Exact cash matchExact cash match• Conservative strategy, matching portfolio cash flows to Conservative strategy, matching portfolio cash flows to

needs for cashneeds for cash• Useful for sinking funds and maturing principal paymentsUseful for sinking funds and maturing principal payments

– Dedication with reinvestmentDedication with reinvestment• Does not require exact cash flow match with liability Does not require exact cash flow match with liability

streamstream• Great choices, flexibility can aid in generating higher Great choices, flexibility can aid in generating higher

returns with lower costsreturns with lower costs

Matched-Funding Matched-Funding TechniquesTechniques

• Horizon matchingHorizon matching– Combination of cash-matching and Combination of cash-matching and

immunizationimmunization– With multiple cash needs over specified With multiple cash needs over specified

time periods, can duration-match for the time periods, can duration-match for the time periods, while cash-matching within time periods, while cash-matching within each time periodeach time period

Derivatives in Fixed-Derivatives in Fixed-Income ManagementIncome Management

• Derivatives can be used to modify Derivatives can be used to modify portfolio risk and returnportfolio risk and return

• Using derivatives for asset allocationUsing derivatives for asset allocation– Adjusting allocations in the underlying Adjusting allocations in the underlying

assets can be very expensiveassets can be very expensive– Less costly to achieve a similar asset Less costly to achieve a similar asset

allocation exposure using derivatives, allocation exposure using derivatives, especially for temporary adjustmentsespecially for temporary adjustments

Derivatives in Fixed-Derivatives in Fixed-Income ManagementIncome Management

• To control portfolio cash flowsTo control portfolio cash flows– Hedging portfolio cash inflows and Hedging portfolio cash inflows and

outflowsoutflows

• Treasury bond futures contractTreasury bond futures contract– Typically used contract for risk Typically used contract for risk

management of fixed-income portfoliosmanagement of fixed-income portfolios– Delivery in T-bondsDelivery in T-bonds

• Those that are delivered are the cheapest-to-Those that are delivered are the cheapest-to-deliver (CTD) that satisfies the contractdeliver (CTD) that satisfies the contract

Derivatives in Fixed-Derivatives in Fixed-Income Management Income Management

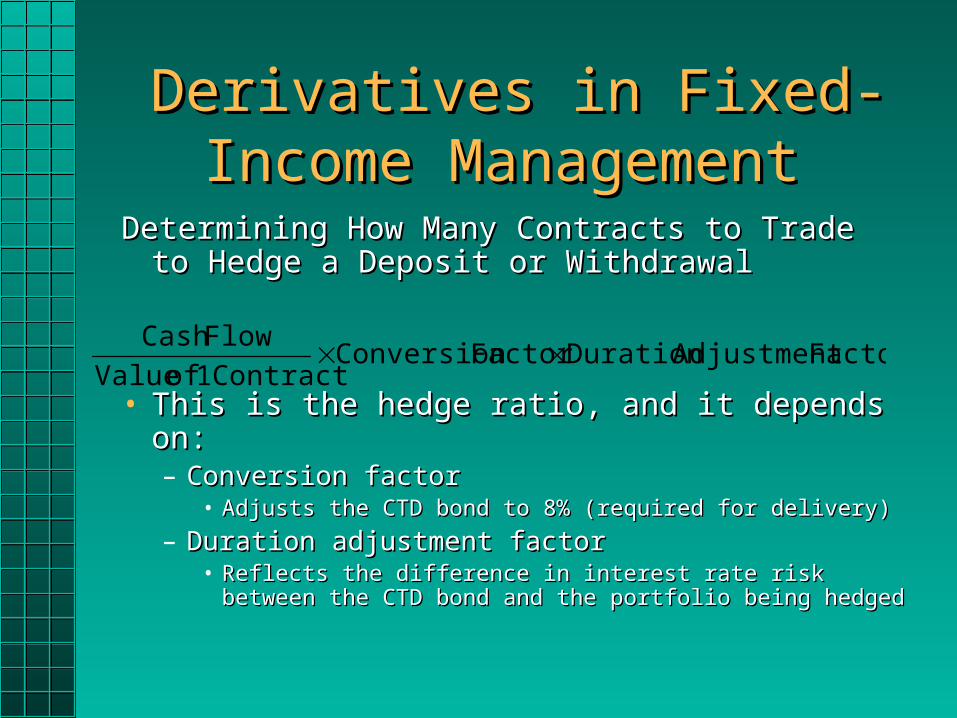

Determining How Many Contracts to Trade to Determining How Many Contracts to Trade to Hedge a Deposit or WithdrawalHedge a Deposit or Withdrawal

• This is the hedge ratio, and it depends on:This is the hedge ratio, and it depends on:– Conversion factorConversion factor

• Adjusts the CTD bond to 8% (required for delivery)Adjusts the CTD bond to 8% (required for delivery)

– Duration adjustment factorDuration adjustment factor• Reflects the difference in interest rate risk between the Reflects the difference in interest rate risk between the

CTD bond and the portfolio being hedgedCTD bond and the portfolio being hedged

Factor AdjustmentDuration Factor ConversionContract 1 of Value

FlowCash

Derivatives in Fixed-Derivatives in Fixed-Income Management Income Management

Using Futures in Passive Fixed-Income Using Futures in Passive Fixed-Income Portfolio ManagementPortfolio Management– Will use futures primarily to manage Will use futures primarily to manage

deposits and withdrawalsdeposits and withdrawals– Will not use futures to actively adjust Will not use futures to actively adjust

duration due to interest forecastsduration due to interest forecasts

Derivatives in Fixed-Derivatives in Fixed-Income Management Income Management

Using Futures in Active Fixed-Income Using Futures in Active Fixed-Income Portfolio ManagementPortfolio Management– Modifying systematic riskModifying systematic risk

• Changing the portfolio duration in light of interest Changing the portfolio duration in light of interest rate forecastsrate forecasts

• Lengthen duration if rates are expected to fallLengthen duration if rates are expected to fall

– Modifying unsystematic riskModifying unsystematic risk• Opportunities are more limited here, but can adjust Opportunities are more limited here, but can adjust

exposure to various sectors to take advantage of exposure to various sectors to take advantage of expected yield changesexpected yield changes

Derivatives in Fixed-Derivatives in Fixed-Income Management Income Management

Determining How Many Contracts to Determining How Many Contracts to Trade to Adjust Portfolio DurationTrade to Adjust Portfolio Duration– Here futures contracts are used to adjust Here futures contracts are used to adjust

the duration of a portfolio, thereby the duration of a portfolio, thereby managing interest rate riskmanaging interest rate risk• Weighted average approachWeighted average approach• Target duration = Contribution of current bond Target duration = Contribution of current bond

portfolio + contribution of the futures portfolio + contribution of the futures componentcomponent

Derivatives in Fixed-Derivatives in Fixed-Income ManagementIncome Management

Changing the Duration of a Corporate Bond Changing the Duration of a Corporate Bond PortfolioPortfolio– There are no corporate bond futures contracts, so There are no corporate bond futures contracts, so

strategies are based on using T-bond futuresstrategies are based on using T-bond futures• Corporate bond yields also impacted by changes in Corporate bond yields also impacted by changes in

default risk, unlike T-bond yieldsdefault risk, unlike T-bond yields• T-bonds are a “cross hedge” instrumentT-bonds are a “cross hedge” instrument• Differences could impact the number of contracts Differences could impact the number of contracts

required to hedge a corporate bond portfoliorequired to hedge a corporate bond portfolio

Derivatives in Fixed-Derivatives in Fixed-Income Management Income Management

Modifying the Characteristics of a Global Bond Modifying the Characteristics of a Global Bond PortfolioPortfolio– Positions in foreign bonds are positions in both Positions in foreign bonds are positions in both

securities and currenciessecurities and currencies– Futures and option contracts allow the portfolio Futures and option contracts allow the portfolio

manager to manage the risks of the currency and manager to manage the risks of the currency and the security separatelythe security separately

• In a passive strategy, the manager can hedge the risk In a passive strategy, the manager can hedge the risk exposureexposure

• In an active strategy, the manager can adjust the In an active strategy, the manager can adjust the exposure to try to benefit from expected changes in exposure to try to benefit from expected changes in exchange ratesexchange rates