Akcomputerforensics 130222081008-phpapp02-140809110602-phpapp02

description

-A

PROJECT REPORT

ON

INSURANCE POLICY OF

Bharti AXA Life INSURANCE

GUIDED BY :

Ms. Dipalipatel.Faculty Member,

S.K. School of Business Management

Hemchandrachary North Gujarat University, Patan

On

September 10th, 2014

“In partial fulfillment of the requirement for the Production & Operation Management

Course in the Master of Business Administration Programme”

Submitted By:

ZALA RAKESH .D ( )

PATE KAMAL (33)

SOLANKY JORSANG (53)

index

S. no. Content Page no.

1. Executive Summary 04

2. About Insurance 04

3. About General Insurance 05

4. Life Insurance and India 06

6. Working of Life Insurance 12

7. About Bhari AXA Insurance 13

8. Features Bhari AXA Insurance 14

9. Bharti Group 15

11. Structure of Bhari AXA Insurance 18

13. Descriptions of few products 19

HISTORY & GROWTH OF ORGANISATION

Monopoly of LIC has been broken to make Indian Insurance to change its face and pace to tap the market and to make the new challenges in it.

Insurance in India is not about India only; it is an open sector for the private players.

The name which we would see in Indian insurance market is something like: - Bharti (Indian company) + AXA(foreign player), BAJAJ (Indian company) + Allianz (foreign player), TATA (Indian company) + AIG (foreign player) and so many like them.

Companies now are tapping a lot of ways to capture the market and hence adopting different ways to hold the large portion of the market.

Our project is to understand the different marketing strategies adopted by the companies to increase their market share and along with it meeting their own targets to achieve the position of no.1 in respective field or segment of the market.

About Bharti AXA Insurance Ltd.:-

Bharti AXA Life Insurance is a joint venture between Bharti, one of India’s leading

business groups with interests in telecom, agri business and retail, and AXA, world

leader in financial protection and wealth management. The joint venture company has a

74% stake from Bharti and 26% stake of AXA Asia Pacific Holdings Ltd (APH).

The company that launched its national operations in December 2006 has over 3000

employees across over 12 states in the country and their business philosophy is built

around the promise of making people "Life Confident".

The following quote from their website and other press media did make a connection to

what we got as an answer to one of the questions about their expansion strategies and

customer acceptance."As we expand our presence across the country to cater to your insurance and wealth management needs with our product and service offerings, we continue to bring 'life confidence' to customers spread across India. Whatever your plans in life, you can be confident that Bharti AXA Life will offer the right financial solutions to help you achieve them"

The Bharti group is very popular across the length and breadth of the country as

leading cell phone service provider - Airtel and if marketed as Airtel Insurance, people

easily recognize the brand name. Also marketing message and bundling could very

well be done with the backing of Airtel.

The market as of 2006, is dominated by LIC with 63 % share while ICICI Prudential

and Bajaj Allianz are leading private players with market shares of 10.6 % and 7.4 %

respectively. Bharti AXA has the challenges of second wave entrant while it has the

advantage to learn from the existing players and enjoy the already created insurance

awareness.

The insurance products by Bharti AXA Life Insurance Company Ltd include:o Wealth Confidento Future Confident

o Future Confident II

o Secure Confident

o Save Confident

o Invest Confident

Each life insurance or general insurance product of Bharti AXA Life is named confident as they believe in making each customer 'Life Confident' giving them the assurance that the future of their loved ones is financially secure even in their absence.

1. Individual Plans :

a. Bharti AXA Life Bright Stars :- A Unit Linked Child product. Bharti AXA Life Bright Stars provides a launch pad for your child’s bright future. What else, we also have Jumpstart benefit which is paid out at maturity along with Policy Fund Value, which enables your child to explore more career options.

b. Bharti AXA Life Spot Suraksha :- Spot Suraksha helps us to create a pool of wealth to meet your long-term needs, with an added advantage of simplified buying process.

c. Bharti AXA Dream Life Pension :- A Unit Linked Pension Product, Dream Life Pension, Bharti AXA Life Insurance’s unique pension product ensures that our retirement life is your Dream Life.

d. Bharti AXA Life AspireLife :- Unit Linked Endowment Product, Aspire Life helps us to create a pool of wealth to meet our long-term needs, while also providing us adequate protection in case the need arises.

e. Bharti AXA Life InvestConfident :- Unit Linked Single Premium Product, we have always strived hard to achieve the best for us and your loved ones, so when it

comes to making an investment decision, we would expect the best from it too.

f. Bharti AXA Life WealthConfident:- A unit-linked investment cum protection policy, our wealth, your status ensures that we get preferential status wherever we go.

g. Bharti AXA Life FutureConfident :- A unit-linked policy which offers comprehensive protection along with wealth creation in the long term.

h. Bharti AXA Life SaveConfident :- Traditional money back insurance product for long term savings,our changing lifestages decide our financial milestone planning. When we foresee intermittent financial requirements in the years to come, like regular expenses related to our child’s education, liquidity becomes a key aspect of your planning along with long term savings, and protection for your family.

i. Bharti AXA Life SecureConfident :- A Long Term Life Insurance, all of us desire to maximise the happiness for our family at all times, irrespective of the circumstances. The thought of unfortunate events befalling us may cause us anxiety about providing a secured happiness to our loved ones.

2. Group Plans :

a. Bharti AXA Life – Swasthya Sanjeevani :- Swasthya Sanjeevani is a single premium group critical illness product, providing comprehensive protection against 6 critical illnesses.

b. Bharti AXA Life – Sanjeevani :- Sanjeevani is a single premium group term life insurance product, offering protection to your family.

c. Bharti AXA Life Mortgage Credit Shield :- Mortgage Credit Shield is a Group Product that provides coverage to people who have availed of a Mortgage\ Home loan\ Home equity loan from an Institution/Bank.

d. Bharti AXA Life Credit Shield :- Credit Shield is a Group Product that provides coverage to people who have availed of a loan for 1 to 5 years from Group Policyholder.

e. Bharti AXA Life Life Shield :- Life Shield is a single premium group term life insurance product.

Bharti AXA Life eAajeevan Sampatti+ (Online Non Linked Participating Whole Life Limited Pay Life Insurance Product)

A plan that offers dual benefit of guaranteed payouts

and protection for your lifetime

At various stages in life, you assume roles that are in line with your

responsibilities. Be it that of a caring husband, a responsible father or a

loving grandfather. In this journey of life, you are key to ensuring that

your family is adequately protected.

At Bharti AXA Life, we have decided to act by partnering you

throughout your life. We bring to you, Bharti AXA Life eAajeevan

Sampatti+, a traditional non linked participating whole life limited pay

plan that ensures you a worry-free life with guaranteed payouts and

adequate protection.

What are my advantages with

Bharti AXA Life eAajeevan Sampatti+?

Limited Pay Period:

You may choose a Premium Payment Term of 10 years or 15

years at inception of your policy.

Guaranteed Annual Payouts:

This plan assures Guaranteed Annual Payouts until Maturity (except

in the

policy year coinciding with maturity). Once you complete the 10th

Policy year,

you will start receiving an annual payout until maturity or death of

Life

Insured, whichever is earlier, subject to policy being in-force. The

Guaranteed

Annual Payout percentage depends on the Policy term op

Cash Bonuses:

This Policy also offers non-guaranteed cash bonuses subject to the

policy

being in-force. The Policy participates in the performance of the

participating

insurance fund and surplus is distributed as bonus. This non-

guaranteed

benefit (as percentage of Sum Assured on Maturity) is paid out as cash

bonus

every year starting from the end of 6th Policy year, until maturity or

death,

whichever is earlier. No bonuses shall be payable in the first 5 policy

years.

Lifelong Protection: Your coverage under the Policy will continue until you reach the age of 100 or 85 years as per the Policy term selected.

In case of unfortunate event of death of Life insured (applicable even in case of minor lives), subject to the policy being in-force the Sum Assured payable on death will be higher of:

a) Sum Assured on Maturity OR b) 11 times Annualised Premium

The base Annualised Premium paid will exclude any modal factors and underwriting extra.

The death benefit payable shall be higher of Sum Assured payable on death or 105% of all premiums paid (excluding an underwriting extra premium).

In case of death during the Grace period, the Death Benefit after deducting the unpaid due premium shall be paid.

In case of death after the policy is converted into paid-up the Paid up value on death will be paid to the nominee.

In case the policy is Lapsed, no Death benefit is payable.

The life insurance coverage starts immediately from issuance of the policy and is applicable to minor lives as well.

The Annualised Base premium is the sum of premiums payable in a policy year and excludes modal factors and underwriting extra (if applicable).

Maturity Benefit:

Sum Assured on Maturity is paid if the Life Insured survives till the maturity of the Policy and the policy is in-force.

Discounts on opting for a Higher Sum Assured on Maturity:

You will be eligible to receive a discount on your premium rate if you opt for a Sum Assured n Maturity of Rs. 4,00,000 or more.

Tax Benefits: You may avail of tax benefits on the premiums paid as well as the benefits received as per the prevailing tax laws under Section 80C and Section 10 (10D) of the Income Tax Act, 1961. The tax benefits are subject to change as per change in tax laws from time to time.

What premiums do I need to pay? Premium rates applicable to you will depend on your age, Premium Payment Term, policy term and the selected Sum Assured on Maturity.

High Discount for Sum Assured on Maturity:

You will receive a discount in premium rate if you choose a higher Sum Assured on Maturity.

Sum Assured on Maturity Premium Rate DiscountEqual to or greater than Premium rate discount is 2%.

` 4,00,000 Premium Payment Mode: You may choose monthly, quarterly, semi-annual or annual Premium Payment Mode.

Mode chosen Premium amountMonthly premium Equal to 0.09 of Annualised Premium

Quarterly premium Equal to 0.27 of Annualised Premium

Semi-annual premium Equal to 0.52 of Annualised Premium

For monthly premium mode policies up to 3 months premium will be collected in advance at the time of commencement of the policy. In case of advance premium;

i) The collection of advance premium shall be allowed only if the premium is collected within the same financial year. ii) The premium so collected in advance shall only be adjusted on the due date of the premium.

What happens if I am unable to pay premiums?

While we recommend that all your premiums be paid on the

respective due

dates, we also understand that sudden changes in lifestyle like an

increase in

responsibility or an unexpected increase in household expenses may

affect

your ability to pay future premiums. You have following flexibilities in

order to

ensure that your benefits under the Policy continue in full or part.

Grace Period: Grace period is the period after the premium due date, during which

you may pay your premiums without any impact on the Policy benefits.

The grace period for all Premium Payment Modes is 30 days.

Lapsation:

If the Premium is not paid on the due date the Policyholder gets a 30

days Grace Period to pay the due premiums, Benefits under the

policy remain unaltered during this period.

• If Policy has not acquired a Surrender Value:

If policyholder does not pay the due premiums within the Grace

Period, the policy shall lapse with effect from the date of such unpaid

premium (‘lapse date’). Policyholder will get two (2) years to Reinstate

the Policy from the date of the first unpaid premium.

If the policyholder does not reinstate the Policy within the period

allowed for reinstatement, the Policy shall be terminated on the

completion of the period allowed for reinstatement and no benefits

shall be payable.

• If Policy has acquired a Surrender Value:

The policy acquires a surrender value after the payment of one

Annualised

Premium. If policyholder does not pay the due premiums within the

Grace

Period, the Policy shall be converted into paid up, with effect from the

date of

such unpaid premium (‘lapse date’). Policyholder will get two (2)

years to

Reinstate the Policy from the date of the first unpaid premium.

If the policyholder does not reinstate the Policy or surrender the Policy

within the period allowed for reinstatement, the Policy shall

continue in paid up status and the paid up value as on the date the

policy becomes Paid Up, shall be payable either on death or on

maturity of the policy.

If the policyholder reinstates the policy during the reinstatement

period then all benefits will be reinstated.

Loans under Policy:

Financial burdens cannot be predicted and may arise at any time.

Hence this

Policy offers you the flexibility to take a loan from the Company. This

is only

possible if all your premiums due under the Policy are paid and the

Policy has

acquired Surrender Value. The maximum amount of loan will not

exceed 70%

of the acquired Surrender Value. The loans given under the Policy are

as per

the Policy provisions.

Reinstatement:

You have a flexibility to reinstate all the benefits under your policy

within two years if your policy has lapsed or is in paid up status after

the due date of the premium in default. However, the Company would

require:

a) A written application from you for reinstatement;

b) Satisfactory evidence of insurability;

c) Payment of all overdue premiums with interest as specified by

company

from time to time.

Reduced Paid up Value:

If the policy has acquired a Surrender Value and has thereafter lapsed

due to

any reasons then the policy will be converted into paid up. Once the

policy

becomes paid up, the base benefits shall be reduced to a paid up

value.

The Policy shall cease to participate in any future bonuses (if any)

that may

be declared by the Company. The Policyholder shall be entitled to

Paid Up

Value as on the date the policy becomes Paid Up and this will be paid

either

on death or on maturity of the policy as applicable. The Guaranteed

Annual

Payouts will be calculated on the Paid Up value on maturity. In

case of

surrender of a paid up policy, the surrender value will be as per

policy

provisions.

Paid up value on Maturity = Number of Premiums paid X Sum Assured on Maturity

Premium Payment Term

Paid up value on Death = Number of Premiums paid X Sum Assured on death

Premium Payment Term

In Case of Death or Maturity, Paid up value as shown above will be paid

to the nominee/policyholder

In case of a paid up policy, the benefits payable on Surrender

will be calculated

Can I surrender my policy? We would want you to pay premiums regularly till the end of Premium

Payment

Term and stay invested till maturity to get maximum benefits under the

policy.

However incase you are not able to pay all premiums and want to

exit the

policy earlier then only surrender value (if acquired) will be payable to

you.

Surrender Value:

The policy acquires a surrender value after the payment of one

Annualised Premium. Guaranteed Surrender Value is calculated as a

percentage of all premiums paid excluding any extra premium.

The Guaranteed Surrender Value factors at different policy years

are as mentioned in the table below:

Premium Payment

Term/Policy Year

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

10 15years years

10% 10%

10% 10%

30% 30%

50% 50%

50% 50%

50% 50%

50% 50%

50% 50%

50% 50%

50% 50%

55% 50%

55% 50%

55% 50%

55% 55%

60% 55%

Premium10

15

PaymentTerm/Policy Year

years

years

16

60%

55%

17

60%

55%

18

60%

60%

19

70%

60%

20

70%

60%

21

70%

60%

22

70%

70%

23

80% 70%

24 80% 70%

25 80% 70%

26 90% 80%

27 90% 80%

28 90% 80%

29 90% 80%

30 90% 90%

The sum of all survival benefits already paid will be deducted from this surrender value.

The Company shall declare special surrender values at such other rates not less than the Guaranteed Surrender Value specified above. These rates are not guaranteed and will be declared by the company from time to time, subject

Do I have the flexibility to enhance my Policy through additional features? Yes. You may enhance your protection under this Policy by opting

for the following riders:

Hospi Cash Rider (UIN 130B007V02):

This rider allows payment of a fixed benefit for each day of

hospitalization and also provides lump sum benefit in case of surgery.

Premium Waiver Rider (UIN 130B005V02):

This rider allows premium payments to be waived in case of an

unfortunate event of death of the policyholder during the Premium

Payment Term.

Please refer rider brochure for complete details on terms and

conditions and exclusions before opting for the rider*.

*Riders are optional and are available at an extra cost.

Product at a glance

Parameter

Minimum Age at Entry (age last birthday)

Maximum Age at Entry (age last birthday)

Maximum Age at Maturity (age last

birthday)

Premium Payment Term options available

Minimum Sum Assured on Maturity (`)

Maximum Sum Assured on Maturity (`)

Minimum Premium (`)

Premium Payment Modes

* Through autopay onlyEligibility Criteria

91 days

60 years for ‘To age 100’ policy term50 years for ‘To age 85’ policy term

100 or 85 years depending on the policy term chosen

10 years & 15 years

` 50,000

No Limit, subject to underwriting

Will depend on the minimum Sum Assured on Maturity

Annual,

Benefits at a Glance

Benefits Description

Life Insurance Benefit In case of unfortunate event of death of Lifeinsured, the Sum Assured payable on death

will be higher of:

a) Sum Assured on Maturity OR

b) 11 times Annualised Premium (excluding

any

modal factors and underwriting

extra

premium).

The death benefit payable shall be higher

of

Sum Assured payable on death or 105% of

all

premiums paid (excluding underwriting

extra).

Maturity Benefit Sum Assured on Maturity.

Survival Benefit 1. Guaranteed payout of 5.5% of the SumAssured on Maturity paid every year

starting from the end of 10th Policy year

for ‘To age 100’ policy term.

2. Guaranteed payout of 6% of the Sum

Assured on Maturity paid every year

starting from the end of 10th Policy year

for ‘To age 85’ policy term.

3. Non-guaranteed Cash bonuses paid

every

year starting from end of 6th Policy

year

onwards.

TERMS AND CONDITIONS: 1. Free-look option: If you disagree with any of the terms and conditions of

the Policy, you have the option to return the original Policy Bond along with

a letter stating reasons for the objection within 30 days of receipt of the

Policy Bond (“the free look period”). The Policy will accordingly be

cancelled and you will be refunded an amount equal to the Premium paid

subject to a deduction of a proportionate risk premium for the period on

cover, the expenses incurred by the Company on medical examination (if

any) and stamp duty charges. All rights under this Policy shall stand

extinguished immediately on the cancellation of the Policy under the free

look option.

2. If the Life Insured under the Policy, whether medically sane or insane,

commits suicide, within one year of the date of issuance of the Policy, the

Policy shall be void and the Company will only be liable to pay the

premiums paid until date.

3. If the Life Insured under the Policy, whether medically sane or insane,

commits suicide, within one year of the date of reinstatement of the

Policy, the Policy shall be void and the Company will only be liable to pay

the higher of 80% of premiums paid or the surrender value.

4. This is a participating traditional insurance Policy.

SECTION 41 OF INSURANCE ACT 1938 1. “No person shall allow or offer to allow, either directly or indirectly, as an

inducement to any person to take out or renew or continue an insurance

in respect of any kind of risk relating to lives in India, any rebate of the

whole or part of the commission payable or any rebate of the premium

shown on the Policy nor shall any person taking out or renewing or

continuing a Policy accept any rebate except such rebate as may be

allowed in accordance with the published prospectus or tables of the

Insurer.”

Provided that acceptance by an insurance agent of commission in connection with a Policy of life insurance taken out by himself on his own life shall not be deemed to be acceptance of a rebate of premium within the meaning of this sub section if at the time of such acceptance the insurance agent satisfies the prescribed conditions establishing that he is a bona fide insurance agent employed by the Insurer.

2. Any person making default in complying with the provisions of this section

shall be punishable with fine which may extend to five hundred rupees.

Bharti AXA Life Flexi Save - A Limited Pay traditional participating life insurance plan Life’s needs and desires grow at every stage. It can be the desire for a bigger house, holiday with your family, buying your dream car or better educational for your children. Thus it becomes important that your savings build up the same way your desires do. However, it is most important that your savings are available to you when you require them the most.

At Bharti AXA Life we have decided to act. We bring to you, Bharti AXA Life Flexi Save that offers you the choice to withdraw your savings when you want to and helps you achieve your goals at all life stages.

What are my advantages with Bharti AXA Life Flexi Save?

1. Option to choose Premium Payment term: There are three premium payment

terms / policy terms to choose from.

Premium Paying Term 5 pay 7 pay 12 pay

Policy Term 20 years 25 years 30 years

2. Potential upside through Bonus: Non Guaranteed Simple reversionary bonus

is declared at the end of each year, starting from the first policy year. This

bonus gets accrued to your policy and is paid out along with Maturity benefit

or Death benefit (whichever is earlier). Terminal bonus may also be declared,

which will be paid out in case of death or maturity, whichever is earlier.

3. Basic Life Insurance Cover: In case of death of the Life Insured, the nominee

will get Higher of Base Sum Assured or 105% of premiums paid or a multiple

of the Annual Base Premium as stated in ‘Death Benefit’ section below, plus

non guaranteed accrued bonus plus terminal bonus (if any), in case of an

unfortunate event of death of the life insured.

4. Maturity Benefit: On maturity of the policy, get 100% of your Sum Assured

along with non guaranteed accrued bonus and terminal bonus (if any).

5. Flexibility to modify your policy term: Anytime during the Flexi benefit period,

you can decide to pre-pone your maturity benefit of the policy and avail the full

benefits due in the policy (i.e.100% of Sum Assured plus accrued bonus till

date plus terminal bonus (if any)).

Premium Paying Term 5 pay 7 pay 12 pay

Flexi Benefit Period Any time between Any time between Any time betweenthe end of the end of the end of

10 to 20 years 15 to 25 years 20 to 30 years

Please also note that once the policy completes 10 policy years, 15 policy years

and 20 policy years for 5, 7 and 12 year premium payment term respectively, the policy would have acquired the full Maturity Benefit and therefore Surrender and Paid-up benefits will not be applicable

6. Tax Benefits: You can avail the tax benefits on the premiums paid (subject to

a maximum of Rs.1,00,000) and on the benefits received subject to the

prevailing provisions under Section 80C and Section 10 (10D) respectively of

the Income Tax Act, 1961. The tax benefits are subject to change as per

change in Tax laws from time to time.

Your key benefits with Bharti AXA Life Flexi Save

1. Maturity Benefit:

On Maturity of the policy you will get • 100% of Sum Assured; plus

• Accrued Reversionary and Terminal bonus ,(if any)

Please also note that once the policy completes 10 policy years, 15 policy years and 20 policy years for 5, 7 and 12 year premium payment term respectively, the policy would have acquired the full Maturity Benefit and therefore Surrender and Paid-up benefits will not be applicable.

2. Death Benefit:

In the unfortunate event of death of life insured, provided all due premiums till the date of death have been paid and the policy is in-force, the policyholder or nominee shall receive Higher of 1. Sum Assured or

2. 105% of premiums paid till date of death or 3. A multiple of Annual Base Premium as provided below

Multiple of Annual Premium

Premium payment term/Age Less than 45 years 45 years and above

5 years 11 7

7 years 11 11

12 years 11 11

Along with the above, the nominee receives the accrued reversionary bonus and terminal bonus, (if any)

In case of death during the Grace period, the Death Benefit after deducting the unpaid due premium shall be paid.

In case of death after the policy is converted into paid-up the Paid up value will be paid to the nominee.

In case the policy is Lapsed, no Death benefit is payable.

What is the frequency of premium payment?

• Premium payment mode: You can choose Monthly, Quarterly, Semi-annual or Annual Premium. Monthly Premium* = 0.09 of Annual Premium, Quarterly Premium* = 0.27 of Annual Premium, Semi-annual Premium = 0.52 of Annual Premium.

* Through Auto Pay only

Service Tax & cess will be levied as per prevailing rates

Other Features:

• Grace period: Grace period is the period given to you from your premium due

date, to pay the premium without any impact on the benefits in your policy.

Grace Period for all modes is 30 days.

• Lapsation: If the Premium is not paid on the due date Policyholder gets a 30

days Grace Period to pay due premiums, Benefits under the policy remain

unaltered during this period.

If Policy has not acquired a Surrender Value:

If policyholder does not pay the due premiums within the Grace Period, the policy shall lapse with effect from the date of such unpaid premium (‘lapse date’). Policyholder will get two (2) years to Reinstate the Policy from the date of the first unpaid premium.

If the policyholder does not reinstate the Policy within the period allowed for reinstatement, the Policy shall be terminated on the completion of the period allowed for reinstatement and no benefits shall be payable.

If Policy has acquired a Surrender Value:

If policyholder does not pay the due premiums within the Grace Period, the Policy shall be converted into paid up, with effect from the date of such unpaid premium (‘lapse date’).Policyholder will get two (2) years to Reinstate the Policy from the date of the first unpaid premium.

If the policyholder does not reinstate the Policy or surrender the Policy within the period allowed for reinstatement, the Policy shall continue in paid up status and the paid up value along with Vested Simple Reversionary Bonuses (if any) as on the date the policy becomes Paid Up, shall be payable either on death or on maturity of the policy.

If the policyholder reinstates the policy during the reinstatement period then all benefits will be reinstated.

• Loans under Policy:

Financial burdens cannot be predicted and may arise at any time. Hence this Policy offers you the flexibility to take a loan from the Company. This is only possible if all your premiums due under the Policy are paid and the Policy has acquired Surrender Value. The maximum amount of loan will not exceed 70% of the acquired Surrender Value. The loans given under the Policy are as per the Policy provisions.

• Reinstatement:

You have a flexibility to reinstate all the benefits under your policy within two years (subject to policy term) if your policy has lapsed or is in paid up status after the due date of the premium in default. However, the Company would require:

a) A written application from you for reinstatement;

b) Satisfactory evidence of insurability;

c) Payment of all overdue premiums with interest as specified by company from

time to time;

• Reduced Paid up Value:

If the policy has acquired a Surrender Value and has thereafter lapsed due to any reasons then the policy will be converted into paid up. Once the policy becomes paid up, the base benefits shall be reduced to a paid up value.

The Policy shall cease to participate in any future bonuses (if any) that may be declared by the Company. The Policyholder shall be entitled to Paid Up Value including the Vested Simple Reversionary Bonuses (if any) as on the date the policy becomes Paid Up and these will be paid either on death or on maturity of the policy. In case of surrender of a paid up policy, the surrender value will be as per policy provisions.

Paid Up Value = Number of Premiums paid X Sum Assured +Accrued Bonus (till date of policy becoming paid up) Premium Payment Term

In Case of Death or Maturity, Paid up value as shown above will be paid to the nominee/policyholder

In case of a paid up policy, the benefits payable on Surrender will be the Surrender Value plus the vested reversionary bonuses as on the date the policy become paid up. The Surrender Value will be calculated as follows

Surrender Value on Paid Up = Paid Up Value * Base Surrender Value

Factor Surrender Value of Bonus on Paid Up = Accrued Bonus till the

date of Paid Up * Surrender Value Factor for Bonuses / 1000

Can I surrender my policy?

We would want you to pay premiums regularly till the end of premium payment term and stay invested till maturity to get maximum benefits under the policy. However incase you are not able to pay all premiums and want to exit the policy earlier then only surrender value (if acquired) will be payable to you.

Surrender Value: The policy acquires a surrender value after the payment of two annualized regular premiums for premium payment term of 5 and 7 years and for premium payment term of 12 years the policy acquires a surrender value after the payment of three annualized premiums. Guaranteed Surrender value is calculated as a percentage of all premiums paid excluding any extra premium

The minimum guaranteed Surrender Values rates at different policy years are as defined in the table below:

Premium Payment 5 years 7 years 12 yearsTerm/Policy Year

1 0 0 0

2 30% 30% 0

3 30% 30% 30%

4 50% 50% 50%

5 55% 50% 50%

6 65% 50% 55%

7 65% 50% 55%

8 75% 55% 60%

9 85% 55% 60%

10 90% 60% 60%

11 90% 65% 60%

12 90% 70% 60%

13 90% 75% 60%

14 90% 80% 60%

15 90% 90% 65%

Premium Payment 5 years 7 years 12 yearsTerm/ Policy Year

16 90% 90% 65%

17 90% 90% 70%

18 90% 90% 75%

19 90% 90% 85%

20 90% 90% 90%

21 90% 90%

22 90% 90%

23 90% 90%

24 90% 90%

25 90% 90%

26 90%

27 90%

28 90%

29 90%

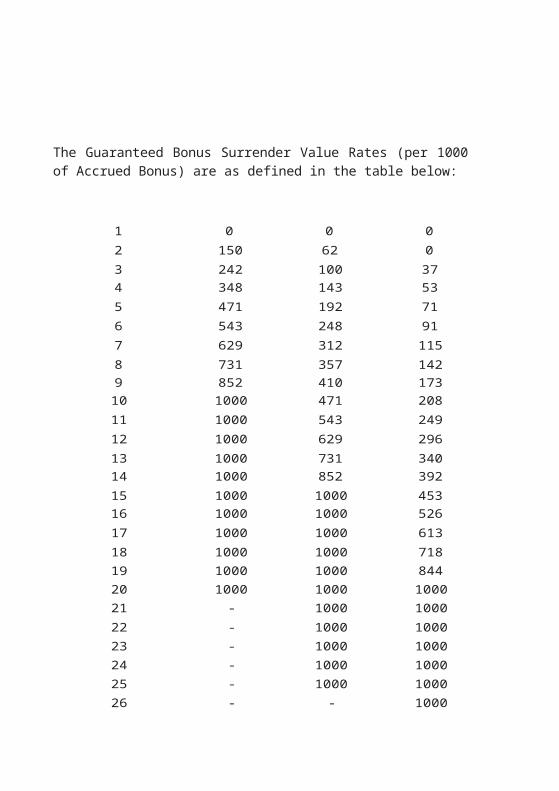

The Guaranteed Bonus Surrender Value Rates (per 1000 of Accrued

Bonus) are as defined in the table below:

Policy Term/ 20 years 25 years 30 yearsPolicy Year

1 0 0 0

2 150 62 0

3 242 100 37

4 348 143 53

5 471 192 71

6 543 248 91

7 629 312 115

8 731 357 142

9 852 410 173

10 1000 471 208

11 1000 543 249

12 1000 629 296

13 1000 731 340

14 1000 852 392

15 1000 1000 453

16 1000 1000 526

17 1000 1000 613

18 1000 1000 718

19 1000 1000 844

20 1000 1000 1000

21 - 1000 1000

22 - 1000 1000

23 - 1000 1000

24 - 1000 1000

25 - 1000 1000

26 - - 1000

27 - - 1000

28 - - 1000

29 - - 1000

The Company may allow surrender values at such other rates not less

than the Guaranteed Surrender Value specified above. These rates will be

declared by the company from time to time, subject to prior approval from

IRDA. There will be an additional non guaranteed surrender value

payable, calculated as per 1000 of the vested reversionary bonuses.

Do I get the flexibility to enhance my protection through additional

features?

Yes. To enhance your protection, you may customize your policy by opting

for the following rider.

Hospi Cash Rider (UIN 130B007V02): This rider allows payment of a

fixed benefit for each day of hospitalization and also provides lump

sum benefit in case of surgery.

Please refer rider brochure for complete details on terms and

conditions and exclusions before opting for the rider.

Riders are optional and are available at an extra cost.

Boundary Conditions

Parameter Eligibility Criteria

Minimum age at entr y 8 years for 20 years policy term3 years for 25 years policy term0 years for 30 years policy term

Maximum age at entr y 65 years for 20 years policy term60 years for 25 years policy term55 years for 30 years policy term

Maximum Maturity Age 85 years

Minimum Sum Assured Depends on the minimum premium

Minimum Annual Base Premium Rs 30,000 for 20 year termRs 24,000 for 25 year termRs 15,000 for 30 year term

Policy Term

Premium Payment Term

Premium Payment Modes

* Through Auto Pay only

20, 25 and 30 years

5 years for 20 years policy term7 years for 25 years policy term

12 years for 30 years policy term

Annual, Semi annual, Quarterly*,

Monthly*

Disclaimers • Bharti AXA Life Insurance is the name of the Company and Bharti AXA Life Flexi Save

is only the name the traditional participating insurance policy and does not in any way

represent or indicate the quality of the policy or its future prospects. • This product brochure is indicative of the terms, conditions, warranties and exceptions

contained in the insurance policy bond

• Life Insurance Coverage is available under this policy • Insurance is the subject matter of the solicitation. • Bharti AXA Life Insurance Company Limited, Registration No.: 130

Registered Office: Unit 601 & 602, 6th floor Raheja Titanium,

Off Western Express Highway, Goregaon (E), Mumbai-400 063.

UIN: 130N055V02

Bharti AXA Life Future Invest -Linked Limited Pay Life Insurance Product

This product does not offer any liquidity during the first five years of the contract. The policyholders will not be able to surrender/ withdraw the money invested in Linked Insurance Products completely or partially till the end of fifth year

You put effort to make sure your family is well protected and always gets the best. Why should your insurance plan not invest majority of the money that you put in towards securing your family’s future?

At Bharti AXA Life, we have decided to act. Bharti AXA Life Future Invest, a Unit Linked Plan ensures that you get the most out of your insurance policy. The plan is a market-linked policy that invests the premium amount paid by you towards building your fund without charging any allocation fee. This plan also provides you with benefits for 10 years while you pay premiums only for the first five, thus extending the protection and investment benefits into the future.

What are the advantages of Bharti AXA Life Future Invest?

■

■

■

■

■

■

■

Limited Premium Payment:

The benefits of this policy accrue to you for 10 years with an

option to choose from two premium payment terms -Single pay

and 5 years.

Zero Allocation Charge:

With this plan, you are not charged any premium allocation charge.

Life Insurance Benefit :

Higher of the Fund Value or Sum Assured.

Fund Options:

You may choose from an array of 6 funds.

Extendable Investment Period (Settlement Period):

Take advantage of staying invested in the funds for an extended period of

5 years after maturity.

Liquidity Benefit with Partial Withdrawal:

You have the option to avail the Partial withdrawal facility from your

policy fund value, after your policy has completed 5 years.

Tax benefits for premiums paid as well as benefits received, as

per the prevailing Tax laws.

What are the benefits of Bharti AXA Life Future Invest?

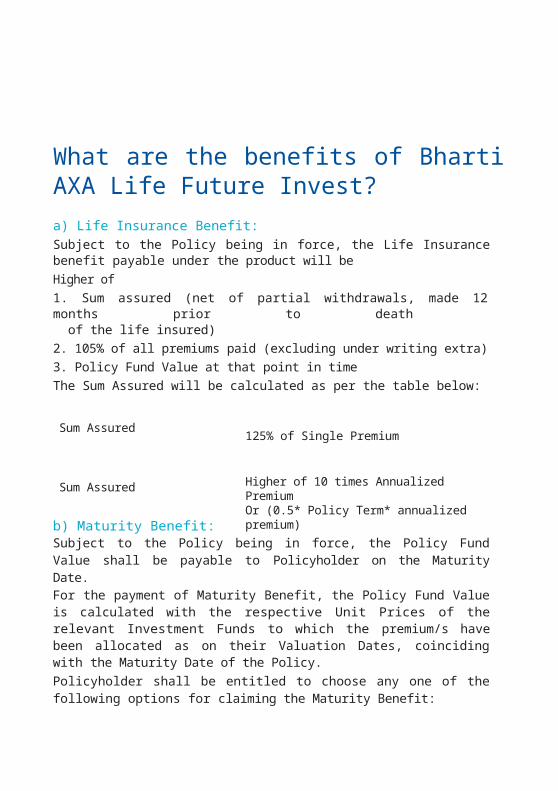

a) Life Insurance Benefit:

Subject to the Policy being in force, the Life Insurance benefit payable under the product will be

Higher of

1. Sum assured (net of partial withdrawals, made 12 months prior to death

of the life insured)

2. 105% of all premiums paid (excluding under writing extra)

3. Policy Fund Value at that point in time

The Sum Assured will be calculated as per the table below:

Premium Payment Term: Single Pay

Sum Assured

Premium Payment Term: 5 Years

Sum Assured

b) Maturity Benefit:

125% of Single Premium

Higher of 10 times Annualized Premium Or (0.5* Policy Term* annualized premium)

Subject to the Policy being in force, the Policy Fund Value shall be payable to Policyholder on the Maturity Date. For the payment of Maturity Benefit, the Policy Fund Value is calculated with the respective Unit Prices of the relevant Investment Funds to which the premium/s have been allocated as on their Valuation Dates, coinciding with the Maturity Date of the Policy.

Policyholder shall be entitled to choose any one of the following options for claiming the Maturity Benefit:

1. Lump sum payment of the Policy Fund Value; or

2. Withdrawal of Maturity Benefit at regular inter vals chosen by

Policyholder during the Settlement Period. (as mentioned in section F below)

3. A combination of the above mentioned two options.

Policyholder is required to apply to the Company, in the specified form, intimating of the choice of the Maturity Benefit option, at least 90 days prior to the Maturity Date. The default option in case of non-receipt of such an application would be Option 1 as mentioned above.

In case of option 2 or 3, the inherent risk of fluctuating markets during the Settlement Period, in respect of Policy Fund Value, shall be borne by Policyholder and applicable Fund Management Charge will be levied.

c) Investment Fund Options:

Depending on your financial objectives, you have the choice of

investing your

premiums in any or all of the following six investment funds mentioned

below:

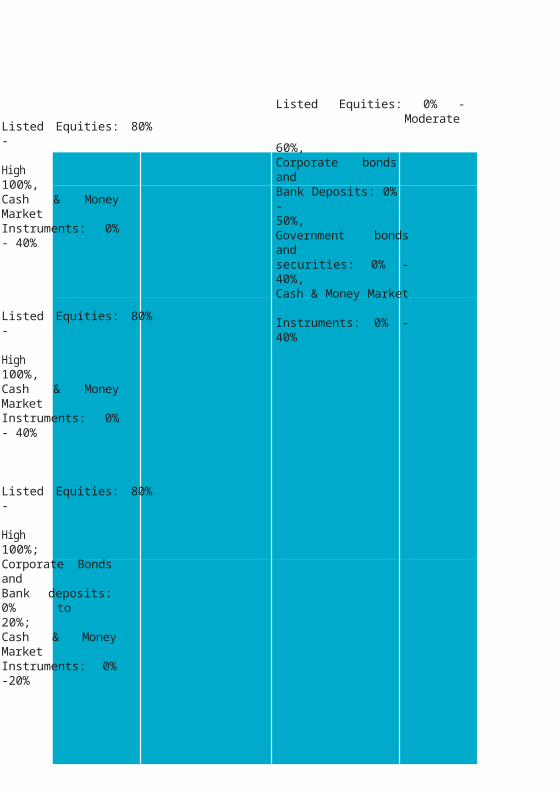

Investment Objective Fund

Growth To provide long termOpportunities capital appreciation byPlus Fund investing in stocksSFIN: across all market ULIF01614/12 capitalization ranges/2009EGRWT (Large, Mid or small) HOPPL130

Grow Money To provide long termPlus Fund capital appreciation bySFIN: investing across a ULIF01214/12 diversified high quality/2009EGROM equity portfolio ONYPL130

Build India To provide long termFund capital appreciation,SFIN through exposure to ULIF01909/02 equity investments in /2010EBUILDI Infrastructure and alliedNDA130 sectors, and by

diversifying investments across varioussub-sectors of the

infrastructure sector

Save’n’Grow To provide steadyMoney Fund accumulation ofSFIN: income in medium to ULIF00121/08 long term by investing /2006BSAVEN in high quality debtGROW130 papers and government

securities and a limited opportunity of capital appreciation. Thiswould be more of a defensively managed fund

Asset Allocation Risk-ReturnPotential

Listed Equities: 80% -

High 100%,Cash & Money Market Instruments: 0% - 40%

Listed Equities: 80% -

High 100%,Cash & Money Market Instruments: 0% - 40%

Listed Equities: 80% -

High 100%;Corporate Bonds and Bank deposits: 0% to 20%;Cash & Money Market Instruments: 0% -20%

Listed Equities: 0% -

Moderate 60%,Corporate bonds and Bank Deposits: 0% -50%,Government bonds and securities: 0% - 40%, Cash & Money Market Instruments: 0% - 40%

Investment Objective Asset Allocation Risk-ReturnFund Potential

Steady Money To provide steady Corporate bonds and LowFund accumulation of Bank Deposits: 20% -SFIN: income in medium to 80%,ULIF00321/08 long term by investingGovernment bonds/2006DSTDY in corporate bonds and and securities: 40% -MOENY130 government securities 60%,

Cash & Money MarketInstruments -0% - 40%

Safe Money To provide capital Corporate bonds and LowFund protection through Bank Deposits: 0% -SFIN: investment in low-risk 60%,ULIF01007/07 money-market & Government bonds/2009LSAFEM short-term debt and securities: 40% -ONEY130 instruments with 60%,

maturity of 1 year or Cash & Money Marketlesser. Instruments -0% - 40%

The company shall also maintain a Discontinued Policy Fund that comprises of the fund values of all the policies that have been discontinued and will earn a minimum interest computed at a rate specified by IRDA from time to time which is currently 4% pa. The discontinued policy fund shall be a unit fund with the following asset categories:

Assets

Money Market

securities

Government securities

Discontinued Policy FundSFIN: ULIF02219/01/2011DDISCONTLF130

0% - 40%

60% - 100%

d) Liquidity Benefit with Partial Withdrawals: We understand that you may have an urgent requirement for money

from time to time. The partial withdrawal facility gives you the flexibility to withdraw money from your Policy Fund Value anytime after the completion of five policy years, subject to the Policy being in force. Each partial withdrawal should be a minimum of ` 1,000 and after withdrawal the Policy Fund Value should not be less than 120% of annualized premium. In a Policy Year You can request for maximum of 2 partial withdrawals that are free of charge, subject to the limit of minimum Partial Withdrawal and the minimum Policy Fund Value. Withdrawals more than 2 times in a Policy Year are not allowed.

e) Manage your funds with Switch and Premium Redirection facilities ■ Through the features of Switch & Premium Redirection, you may manage

your asset allocation between equity and debt depending on your need.

e.g. You can move your money to a low-risk investment fund before the

policy matures to protect yourself against any adverse movements in the

equity markets

■ You can switch up to 12 times in a policy year free of charge, subject to the

Policy being in force. Switches more than twelve times in a policy year will

be charged at Rs 100 per switch. The minimum value of a switch should

be Rs.1,000. Unutilized Switches of any Policy Year cannot be carried

for ward to the succeeding Policy Years.

■ The minimum investment in any allocated fund should not be less than 5%.

f) Settlement Period

The Settlement Period is the period not exceeding five years commencing from the Maturity Date and is an option available to the Policyholder.

■

■

■

■

■

■

The Policyholder is required to apply to The Company, in the specified form, intimating of the choice of the Maturity Benefit option, at least 90 days prior to the Maturity Date.

The Policyholder is entitled to choose a frequency to make periodical withdrawals from the Fund.

Depending on the frequency of withdrawals chosen, the number of units as on the Maturity Date will be divided equally as per the frequency. The withdrawal amount will be calculated with the respective Unit Prices of the relevant Investment Funds to which the Annual Regular Premiums have been allocated as on their Valuation Dates, multiplied by the number of units.

The Company shall levy fund management charge during the settlement period and no other charges shall be levied.

At any time during the Settlement Period the policy holder can withdraw the balance available Policy Fund value as on that date.

However the Policyholder is not entitled to avail of any life insurance benefit or opt for partial withdrawals or Switches between Investment Funds during this period.

If the Life Insured dies during the Settlement Period, then the existing Policy Fund Value shall be paid to the Nominee and the Policy will stand terminated.

What happens if I am unable to pay premiums?

a) Grace Period: (applicable only for the premium payment term of 5 years) Grace period available to you will be

■ Fifteen days for Monthly Premium Payment mode; ■ Thirty days for Annual/Semi-annual/Quarterly Premium Payment mode

b) Discontinuance of Premium: (applicable only for the premiumpayment term of 5 years)

While we recommend that all your premiums are paid on the respective due dates, we also understand that due to sudden changes in lifestyle like an increase in responsibility or an unexpected increase in household expenses may affect your ability to pay future premiums.

If any premium due, remains unpaid even after the grace period, the Company will send a written notification within 15 days of the expir y of the grace period, stating that, the policyholder can exercise any of the options mentioned below, within 30 days of the date of receipt of the notification. The Policy will remain in force during this period and all charges will be deducted.

You are entitled to exercise one of the following options :

(i) Revival of the policy within Revival Period

(ii) Intimate the company of the intention to revive the policy within Revival

period of two years starting from the date of discontinuance of the

policy; or

(iii) Complete withdrawal from the policy without any risk cover

The conditions for revival of the policy are as follows:

1. Revival of the policy within the Revival Period

A request to revive the policy will be accepted subject to the following:

• Satisfactor y evidence of insurability of the Life Insured

• Payment in full of an amount equal to all the premiums due but unpaid from the date of discontinuance of policy till the Revival of Policy.

Revivals will be as per the Board Approved Under writing Policy. The effective date of revival is the date on which the above requirements are met and approved by the Company. On this date, all outstanding charges shall be deducted from the above payment for the period between the premium due date and the Effective date of revival.

2. Intimate the company of the intention to revive the policy within revival period of two years starting from the date of discontinuance of the policy

In case You intimate your intention to revive the policy, and if the revival period expires before the end of the lock in period, then proceeds of the discontinued policy fund shall be refunded to you at the end of the lock-in period.

In case You intimate your intention to revive the Policy and do not revive the policy till sixty days before the end of lock in period, provided that the revival period has not expired at the end of lock-in period, the Company shall send a notice to you forty five days before the end of the lock-in period to exercise one of the below options within a period of thirty days of receipt of such

notice:

a. Revive the policy immediately; or

b. Intimation to Revive the policy within Revival Period starting from the date

of discontinuance of the policy; or

c. Payout the proceeds at the end of the lock-in-period or the revival period,

whichever is later

In case You do not exercise any of the options within the notice period of thirty days, the treatment of such policy shall be in accordance with (c). In case You opt for option (b) then the fund value shall continue to remain in the discontinued policy fund till the policy is revived or up to the end of the revival period whichever is earlier. If the policy is not revived within the Revival Period, the proceeds of the discontinued policy fund shall be paid out to You at the expir y of Revival Period.

3. Complete withdrawal from the policy without any risk cover

The policy will be treated as surrendered and the surrender

provisions as mentioned in Section (C) given below will be applicable.

c) Option to surrender the policy:

If you opt to Surrender the Policy within the lock-in period, then the

Policy Fund Value less the applicable Discontinuance Charges as

mentioned in the section D of “Charges Applicable” below,

calculated as at the date the request of such surrender, shall be

credited to the Discontinued Policy Fund, that earns a minimum

interest computed at a rate as specified by IRDA and shall become

payable on completion of five policy years.

On seeking surrender of the Policy after completion of 5 policy

years, the

Surrender Value which at all times is equal to the Policy Fund Value

shall be

payable.

Surrender of the Policy shall terminate the Policy and extinguish all

rights, benefits and interests of the policyholder in the Policy.

Charges Applicable

a) Premium Allocation Charge:

There is no premium allocation charge. 100% of premiums paid will be allocated in the funds chosen by you.

b) Mortality Charge:

This charge is levied to provide you with life insurance benefit. This charge is applied on the Sum at Risk (as defined below) and is deducted proportionately by cancellation of units on a monthly basis.

■ Sum At Risk is defined as the excess of Sum Assured over Policy Fund

Value as on the corresponding Policy Date in the relevant Policy Month.

Mortality charges per thousand Sum At Risk (per annum) for sample ages of healthy lives are as follows:

Gender / Age last birthday (in years)

Male

Femal

e

30 40 50

` 0.89 ` 1.56 ` 4.33

` 0.84 ` 1.24 ` 3.13

These rates are guaranteed to remain the same during the policy benefit period.

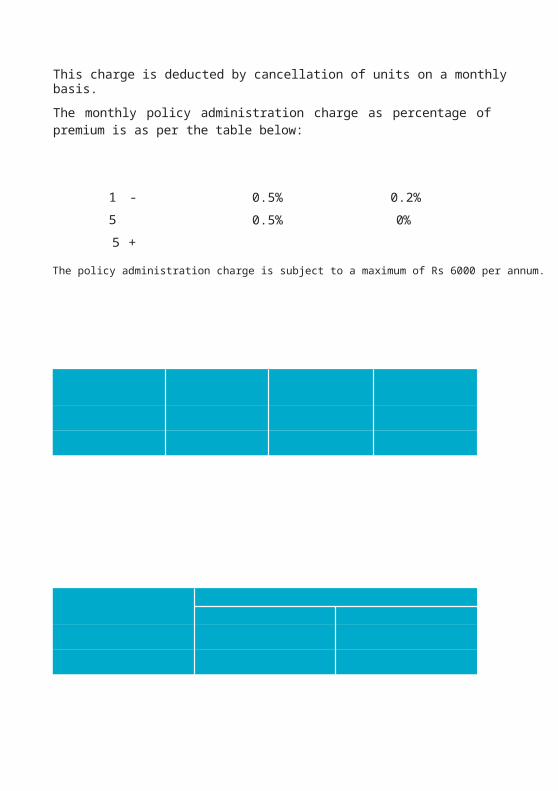

c) Policy administration charge:

This charge is deducted by cancellation of units on a monthly basis.

The monthly policy administration charge as percentage of premium is

as per the table below:

Policy Year

1 -

5

5 +

Premium Payment Term

5 years Single premium

0.5% 0.2%

0.5% 0%

The policy administration charge is subject to a maximum of Rs 6000 per annum.

d) Discontinuance Charge:

The Discontinuance Charge shall be levied at the time of surrender

or on discontinuance of premium. The Surrender Value that you will

receive will be the policy fund value less this charge. The

discontinuance charges are applicable on the policy fund value and

are as follows:

For premium payment term of 5 years

Year of discontinuance Discontinuance charge forof premium/ surrender policies with annualized

premium less than or equal to ` 25,000 p.a.

Lower ofa) 20% of Annual Premium

1 b) 20% of Fund Value

c) `

3,000

Lower ofa) 15% of Annual Premium

2 b) 15% of Fund Value

c) `

2,000

Lower ofa) 10% of Annual Premium

3 b) 10% of Fund Value

c) `

1,500

Lower ofa) 5% of Annual Premium

4 b) 5% of Fund Value

c) ` 1,000

5 and onwards NIL

Discontinuance charge for policies withannualized premium above ` 25,000 p.a.

Lower ofa) 6% of Annual Premiumb) 6% of Fund Valuec) ` 6,000

Lower ofa) 4% of Annual Premiumb) 4% of Fund Valuec) ` 5,000

Lower ofa) 3% of Annual Premiumb) 3% of Fund Valuec) ` 4,000

Lower ofa) 2% of Annual Premiumb) 2% of Fund Valuec) ` 2,000

NIL

For Single Pay

Year of discontinuance Discontinuance charge for policies with annualizedof premium/ surrender premium less than or equal to ` 25,000 p.a.

Lower of a) 1% of Annual Premium

1 b) 1% of Fund Valuec) ` 6,000

Lower of a) 0.5% of Annual Premium

2 b) 0.5% of Fund Valuec) ` 5,000

Lower of a) 0.25% of Annual Premium

3 b) 0.25% of Fund Valuec) ` 4,000

Lower of a) 0.1% of Annual Premium

4 b) 0.1% of Fund Valuec) ` 2,000

5 and onwards NIL

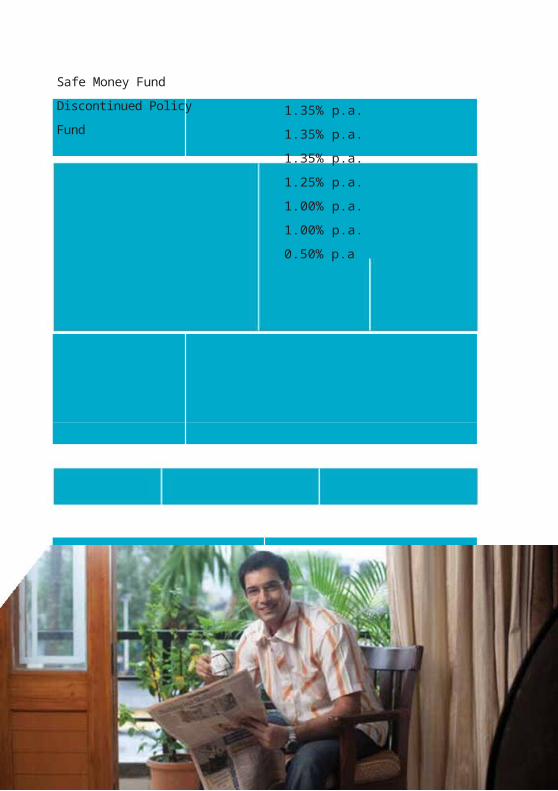

e) Fund Management Charge:

This is a charge that is levied on each of the Investment Funds and is

adjusted in the unit price calculation on a daily basis.

Fund Name

Growth Opportunities Plus

Fund Grow Money Plus Fund

Build India Fund

Save’n’grow Money

Fund Steady Money

Fund

Safe Money Fund

Discontinued Policy

Fund Fund Management Charge

1.35% p.a.

1.35% p.a.

1.35% p.a.

1.25% p.a.

1.00% p.a.

1.00% p.a.

0.50% p.a

Product at a glance

Parameters

Minimum age at entr

y

Maximum age at

entr y

Maximum age at

maturity Premium

modes

Minimum premium

Policy benefit period

Premium payment

term

*Payment only through ECS

Eligibility

18 years (age last birthday)

59 years (age last birthday)

69 years (age last birthday)

Yearly, Half-yearly, Quarterly* and

Monthly*. Premium Payment Term: 5

years

Annual - ` 18,000

Semi Annual - `

9,000

Quarterly - ` 4,500

Monthly - ` 1,500

Premium payment term: Single Pay ` 50,000

10 years

Single Pay and 5 years

What are the Tax Benefits under this product? You can avail the tax benefits on the premiums paid and the benefits

received as per the prevailing tax laws under Section 80C and

Section 10(10D) of the Income Tax Act, 1961. The tax benefits are

subject to change as per change in Tax laws from time to time.

Terms and conditions 1. Free-look option:

If You disagree with any of the terms and conditions of the Policy,

You have

the option to return the original Policy Bond along with a letter

stating

reasons for the objection within 15 days of receipt of the Policy

Bond (“the

free look period”). The Policy will accordingly be cancelled and

the

policyholder will be refunded an amount equal to the sum of the

Policy

Administration Charge and Mortality Charge, deducted from the

Policy

Fund Value and the Policy Fund Value less proportionate risk

premium for

the period on cover, the medical expenses incurred by the insurer

(if any)

and stamp duty charges. All rights under this policy shall

stand

extinguished immediately on the cancellation of the Policy under

the free

look period.

2. If the Life Insured under the Policy, whether medically sane or

insane,

commits suicide, within one year of the date of issue of the Policy or

within

one year from the latest date of revival of the Policy, the Policy shall

be void

and The Company will only be liable to pay the Policy Fund Value as

on the

date of death. Any charges recovered subsequent to the date of

death

shall be paid back to the nominee or beneficiar y along with death

benefit.

3. The Company also has the right to revise the asset allocation

of any

investment fund (s) with prior approval from IRDA

4. This is a non participating Unit Linked Insurance policy and

does not

provide for participation in the distribution of surplus or profits that

may be

declared by the Company

Revision of charges The Company reser ves the right to revise the following charges from

time to time, subject to the following maximum limits, with prior

approval from the Insurance Regulator y and Development Authority

(‘IRDA’):

Fund Management Charge:

This charge shall not exceed the maximum cap as prescribed by IRDA.

Policy Administration Charge:

This charge shall not exceed ` 6000 per annum or the maximum

limit as prescribed by IRDA.

Investment Fund Addition:

The Company may from time to time create and add new Investment

Funds with different fees/ charges with the approval of Insurance

Regulator y and Development Authority and consequently, new

Investment Funds will be made available to the policyholder. All

provisions of the product will apply to the additional Investment

Funds unless stated other wise.

Investment Fund Closure:

The Company reser ves the right to close any investment fund by

giving 3 months notice in writing. In such case, option will be given to

the policy holder to change the fund. And if no reply is received, the

company may shift the fund to a fund having the same fund

objective and same or lower fund management charge. This

switch will be free of charge.

Computation of Unit Price: The computation of unit price shall be done as stipulated by the Insurance and Regulator y Development Authority (IRDA), which is as follows

■ Market value of the investment held by the fund plus value of current

assets less value of current liabilities and provisions, if any and divided

by the number of units existing on the valuation date (before

creation/redemption of units).

Risks of investment in unit-linked policies ‘Bharti AXA Life Future Invest is the name of the unit linked insurance product. Unit linked insurance products are different from traditional Insurance products and investments in ULIP are subject to Market risk. The premium in unit linked insurance policy are subject to investment risk associated with capital market and the NAV of the units may go up or down based on the per formance of the investment funds and the factors influencing the capital markets and the policyholder is responsible for his/her decisions.

Bharti AXA Life Insurance Company Ltd. is only the name of the insurance

company and Bharti AXA Life Future Invest is only the name of the unit

linked insurance policy and does not in any way represent or indicate the

quality of the policy, its future prospects and per formance or the returns.

Bharti AXA Life Future Invest does not provide for participation in the

distribution of surplus or profits that may be declared by the Company.

Growth Opportunities Plus Fund, Grow Money Plus Fund, Build India Fund,

Steady Money Fund, Save’n’grow Money Fund and Safe Money Fund are

the names of the Investment Funds and do not in any manner indicate the

quality of the Investment Funds, their future prospects or returns. There

can be no assurance that the objective of any of the investment funds will

be achieved.

Please know the associated risks and the applicable charges, from your Insurance advisor or the Intermediar y or the policy bond.

All the tax benefits under the Policy are subject to the tax laws and other financial enactments as they exist from time to time. The tax benefits are subject to change with change in tax laws.

Why Bharti AXA Life Secure Income Plan?

Every month comes with a new wish. Be it a laptop for your child’s birthday, a trip abroad with your family, new ornaments for your wife or long due renovation for your home. You often postpone these desires in the pursuit of fulfilling immediate needs. The requirements are limitless while the means to accomplish these desires are limited.

At Bharti AXA Life, we have decided to act. With Bharti AXA Life Secure Income Plan - a traditional non-participating limited pay life insurance plan, you can fulfill your loved ones’ desires by providing them with guaranteed monthly income along with protection in case of an unfortunate event. This plan provides

you a second source of monthly income that enables you to fulfill those long pending wishes. Even in an adverse situation, if something unfortunate were to happen to you, you can ensure that your family maintains their lifestyle.

What are my advantages with Bharti AXA Life Secure Income Plan? 1. Guaranteed Income which is Tax Free#:

You star t receiving Guaranteed Income after the completion of the Premium Payment Term, until Maturity, provided the policy is in force and all due premiums have been paid. This income will be tax free#. #Subject to the prevailing provisions of section 10(10D) of the Income Tax Act,

1961. Tax benefits are liable to change as per changes in tax laws.

2. Guaranteed Addition: A fixed guaranteed addition, declared as a percentage of Sum Assured gets added to your policy each year after the completion of premium payment term, until maturity of the policy. These guaranteed additions get paid out either on death or at maturity, provided the policy is in force and all due premiums have been paid. This Guaranteed Addition percentage, as shown in the table below varies as per the policy term chosen.

Policy Term Premium Payment Term Annual Guaranteed Addition(applicable after premium

payment term)

15 years 5 years 7% of Sum Assured

17 years 7 years 8.5% of Sum Assured

20 years 10 years 10% of Sum Assured

3. Maturity Benefit: Sum Assured plus Guaranteed Additions get paid out

on Maturity.

4. Life Insurance Cover

In case of the unfor tunate death of the Life Insured, the nominee gets the Death Benefit which is as defined below for different Policy terms provided the policy is in force.

5. Tax benefits for premiums paid and benefits received are as per the prevailing tax laws which are subject to changes with change in tax laws.

What will be my Guaranteed Income?

Your Guaranteed Income is calculated based on your chosen Sum

Assured. You have the flexibility to choose your Policy term from 3

options. The

corresponding Premium Payment Term, Guaranteed Income and

Guaranteed Income Benefit Period for each policy term are as below:

Policy Premium Guaranteed Income* Guaranteed IncomeTerm Payment Term Benefit Period*(in months)

15 Years 5 Years 8% of Sum Assured p.a.10 years (120 months)

17 Years 7 Years 8% of Sum Assured p.a.10 years (120 months)

20 Years 10 Years 8% of Sum Assured p.a.10 years (120 months)

*The Guaranteed Income commences after the end of Premium Payment Term and will be paid out on a monthly basis, provided all due payments have been paid.

What premiums do I need to pay?

■ Premium amount applicable to you will be dependant on your age,

policy

term, premium payment mode and chosen Sum Assured.

■ Premium payment mode:

You can choose Monthly, Quar terly, Semi-annual or Annual Premium.

Monthly Premium = 0.09 of Annual Premium, Quar terly Premium

= 0.27

of Annual Premium, Semi-annual Premium = 0.52 of Annual

Premium.

Service Tax & cess will be levied as per prevailing rates

Provides a guaranteed monthly income after the completion of

the Premium Payment Term, provided the policy is in force.

What happens, if I am unable to pay premiums?

While we recommend that all your premiums be paid on the

respective due

dates, we also understand that sudden changes in lifestyle like

increased

responsibilities or unexpected increase in household expenses may

affect

your future ability to pay premiums. You have following flexibilities in

order to

ensure that your benefits under the policy continue in full or par t form.

■ Grace period:Grace period is the period given to you from your premium due

date, to pay the premium without any impact on the benefits in

your policy. Grace Period for all modes is 30 days.

■ LapsationIf policy has not acquired a Surrender Value

In case you do not pay the premiums within your grace period, your

policy

will lapse and your insurance cover will cease to exist. You have

the

option to reinstate the policy within the period given for

reinstatement of

the policy. At the end of the reinstatement period if the policy is

not

reinstated then the policy will be terminated and no benefits will be

payable.

If policy has acquired a Surrender Value

In case you do not pay the premiums within your grace period, your

policy

will be conver ted into paid up. You have the option to reinstate the

policy or surrender the policy within the period given for

reinstatement of

the policy. At the end of the reinstatement period if the policy is

not

reinstated or surrendered then the policy will continue in paid up

status

and the paid up value will be payable either on death or on maturity

of

the policy.

In case of the unfortunate death of the Life Insured,

the nominee is eligible to receive the Death Benefit

■ Reduced Paid up Value:If your policy has acquired a surrender value and your policy has

lapsed due to any reason, then your policy will be conver ted into

„paid up‟. Once your policy is conver ted into paid up, all benefits

will be reduced. The

Guaranteed Income Benefit will be reduced as per the policy

provision. The reduced Guaranteed Income Benefit will be paid on

an annual basis only. On Maturity or in case of death of the Life

Insured, reduced paid up value will be payable. In case of surrender

of a paid up policy, the

surrender value will be as per policy provisions.

■ ReinstatementYou have a flexibility to reinstate all the benefits under your policy within two years (subject to policy term) after the due date of the premium in default. However, the Company would require:

a) A written application from you for reinstatement;

b) Satisfactor y evidence of insurability;

c) Payment of all overdue premiums with interest as specified

by the

company from time to time;

In case of reinstatement of a paid up policy, the differential

amount of

guaranteed income due (i.e. guaranteed income calculated on

the full

Sum Assured less the reduced guaranteed income already paid),

if

applicable, shall be paid to the policyholder as a lump sum.

Can I surrender my policy? We would want you to pay premiums regularly and stay invested till Maturity to get maximum benefits under the policy. However in case you are not able to pay all premiums and want to exit the policy earlier then only surrender value will be payable to you.

Surrender Value For policy term of 15 and 17 years, your policy will acquire surrender value only if two annual premiums are paid. While for the 20 years policy term, your policy will acquire surrender value only if three annual premiums are paid.

The guaranteed Surrender Value is defined as a percentage of all premiums paid excluding any extra premium. The minimum guaranteed surrender value will be as per the table below

Policy Year Surrender value as a % of sum of premiumspaid less all extra premium

15 years 17 years 20 years2 30% 30% -

3 30% 30% 30%4 50% 50% 50%5 50% 50% 50%6 55% 50% 50%7 60% 55% 55%8 65% 55% 55%9 70% 60% 60%10 75% 65% 60%11 80% 70% 65%12 85% 75% 65%13 90% 80% 70%14 95% 85% 70%15 100% 90% 75%16 - 95% 80%17 - 100% 85%18 - 90%

19 - 95%20 - 100%

*The sum of all Guaranteed income paid till the year of surrender will be deducted from this Guaranteed Surrender Value. The company may declare surrender value that is higher than the guaranteed Surrender Values. In case of paid up policy, the surrender value will be different.

Paid Up Value Surrender Value1000 X Factor

How does the policy help me in case of a financial crunch?

Loans under policy:

Financial burdens cannot be predicted and may arise at any time.

Thus this policy gives flexibility to take loan from the company. This is

only possible if your policy is in force and has acquired surrender

value. The loans given under the policy are as per provisions under

the policy. Maximum loan

amount will not exceed 70% of Surrender Value.

Do I get the flexibility to enhance my protection through additional features?

Yes. To enhance your protection, you may customize your policy by opting for the following rider by paying extra premiums:

Hospital Cash Rider

This rider allows payment of a fixed benefit for each day of

hospitalization

and also provides lump sum benefit in case of surger y. UIN:

130B007V01

Please refer rider brochure for more details.

What are the tax benefits under this product? You can avail the tax benefits on the premiums paid (subject to a

maximum of Rs. 1,00,000) and the benefits received subject to the

prevailing

provisions under Section 80C and Section 10 (10D) respectively of

the

Income Tax Act, 1961.

The tax benefits are subject to change as per change in Tax laws from time

to time.

Product at a glanceParameters

Minimum age at entr y

Maximum age at entr y

Maximum age at

maturity Minimum

PremiumExcluding ser vice tax and cess

Policy Term

Premium Payment Term

Premium Payment Modes

* Payment only through ECS

Eligibility Criteria

3 years for 15 years policy term1 year for 17 years policy term0 year for 20 years policy term

65 years for 15 years policy term63 years for 17 years policy term60 years for 20 years policy term

80 years

For 15 years policy term • Rs. 30,000 for Annual Mode

• Rs. 15,600 for Semi-Annual Mode

•

Rs. 8,100 for Quarterly Mode

•

Rs. 2,700 for Monthl

y Mode For 17 years policy term

• Rs. 24,000 for Annual Mode • Rs. 12,480 for Semi-Annual

Mode • Rs. 6,480 for Quarterly Mode • Rs. 2,160 for Monthly Mode

For 20 years policy term• Rs. 18,000 for Annual Mode • Rs. 9,360 for Semi-Annual

Mode • Rs. 4,860 for Quarterly Mode • Rs. 1,620 for Monthly Mode

15, 17 and 20 years

5, 7 and 10 years for 15, 17 and 20 years policy term respectively

Annual, Semi-annual, Quar terly* & Monthly*

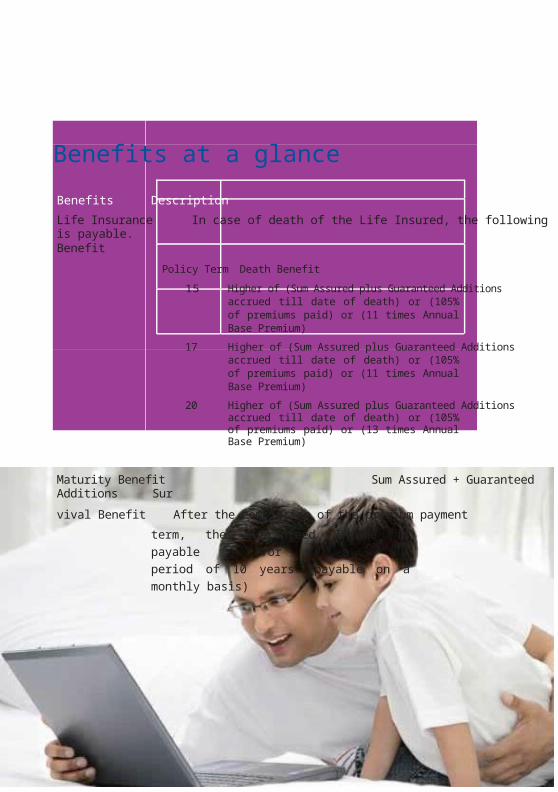

Benefits at a glance

Benefits Description

Life Insurance In case of death of the Life Insured, the following is payable.Benefit

Policy Term Death Benefit

15 Higher of (Sum Assured plus Guaranteed Additionsaccrued till date of death) or (105% of premiums paid) or (11 times Annual Base Premium)

17 Higher of (Sum Assured plus Guaranteed Additionsaccrued till date of death) or (105% of premiums paid) or (11 times Annual Base Premium)

20 Higher of (Sum Assured plus Guaranteed Additionsaccrued till date of death) or (105% of premiums paid) or (13 times Annual Base Premium)

Maturity Benefit Sum Assured + Guaranteed Additions Sur

vival Benefit After the completion of the premium payment

term, the Guaranteed Income is payable for a period of 10 years (payable on a monthly basis)

Terms and conditions

1. Free-look option:- If you disagree with any of the terms and

conditions of

the Policy, you have the option to return the original Policy Bond

along

with a letter stating reasons for the objection within 15 days of

receipt of

the Policy Bond (“the free look period”). The Policy will accordingly

be

cancelled and an amount equal to premiums paid less stamp duty

and

medical costs, if any, incurred by the Company will be refunded to

the

Policyholder.

2. If the Life Insured under the Policy, whether medically sane or

insane,

commits suicide, within one year of the date of issuance of the

Policy,

the Policy shall be void and the Company will only be liable to

pay the

premiums paid till date.

3. If the Life Insured under the Policy, whether medically sane or

insane,

commits suicide, within one year of the date of reinstatement of

the

Policy, the Policy shall be void and the Company will only be liable to

pay

the higher of the applicable Surrender Value or 80% of premiums

paid till

the date of death.

4. This is a non-par ticipating traditional Insurance policy

health insurance

Can my critical illness planprotect me for not onebut three different claims?Bharti AXA LifeTriple HealthInsurance PlanA plan that covers you for up to threedifferent critical illnesses and alsowaives off future premiums after thefirst claimYour health is paramount to you and your family. The growingconcern, however, is the increasing cost of health care. Which iswhy you need your health plan to cover you for not one or twobut three critical illnesses.At Bharti AXA Life, we have decided to act. Our latest healthproduct Bharti AXA Life Triple Health Insurance Plan offers youmultiple critical illnesses claim up to a maximum of 3 claims,provided each of them are from a separate group – Group A,Group B and Group C as classified on the following page andsubject to a no benefit period of 365 days between each claim.This plan pays you the Sum Assured to help you meetunexpected medical expenses.

About us:Bharti AXA Life Insurance is a joint venture between Bharti, one of India’sleading business groups with interests in telecom, agri business andretail, and AXA, one of the world’s leading company in financial protectionand wealth management. The joint venture company has a 74% stakefrom Bharti and 26% stake of AXA.As we further expand our presence across the country with a largenetwork of distributors, we continue to provide innovative products andservice offerings to cater to specific insurance and wealth managementneeds of customers. Whatever your plans in life, you can be confidentthat Bharti AXA Life will offer the right financial solutions to help youachieve them.

Why Bharti AXA Life Triple HealthInsurance Plan?The Policy includes 13 critical illnesses that are split into 3 groups. Shouldone have the misfortune of being diagnosed with any critical illness fromthese groups, the first claim could be made and the policyholder will still beeligible for a second and third claim from the other two groups in the futureyears. Subject to a 'no benefit period' of 365 days between each claim.For each claim, you are eligible to receive the full Sum Assured opted for byyou irrespective of whether it is the first, second or third claim.Critical Illness Cover from the other two groupscontinues even after a claim from one group is paidGroup A Group B Group C100% Sum AssuredpayableFirst Heart Attack ofSpecified Severity.Open Chest CABGMajor Organ Transplant

(Kidney or Heart)Kidney Failure RequiringRegular Dialysis.Heart Valve SurgeryStroke Resulting inPermanent SymptomsPermanent Paralysis ofLimbs.100% Sum AssuredpayableComa of SpecifiedSeverity.Multiple Sclerosis withPersisting Symptoms.Major Organ Transplant(Liver or Lung)100% Sum AssuredpayableCancer of SpecifiedSeverityBenign Brain TumourBone Marrow Transplant