Benefits of global diversification on a real estate portfolio - Journal of

10

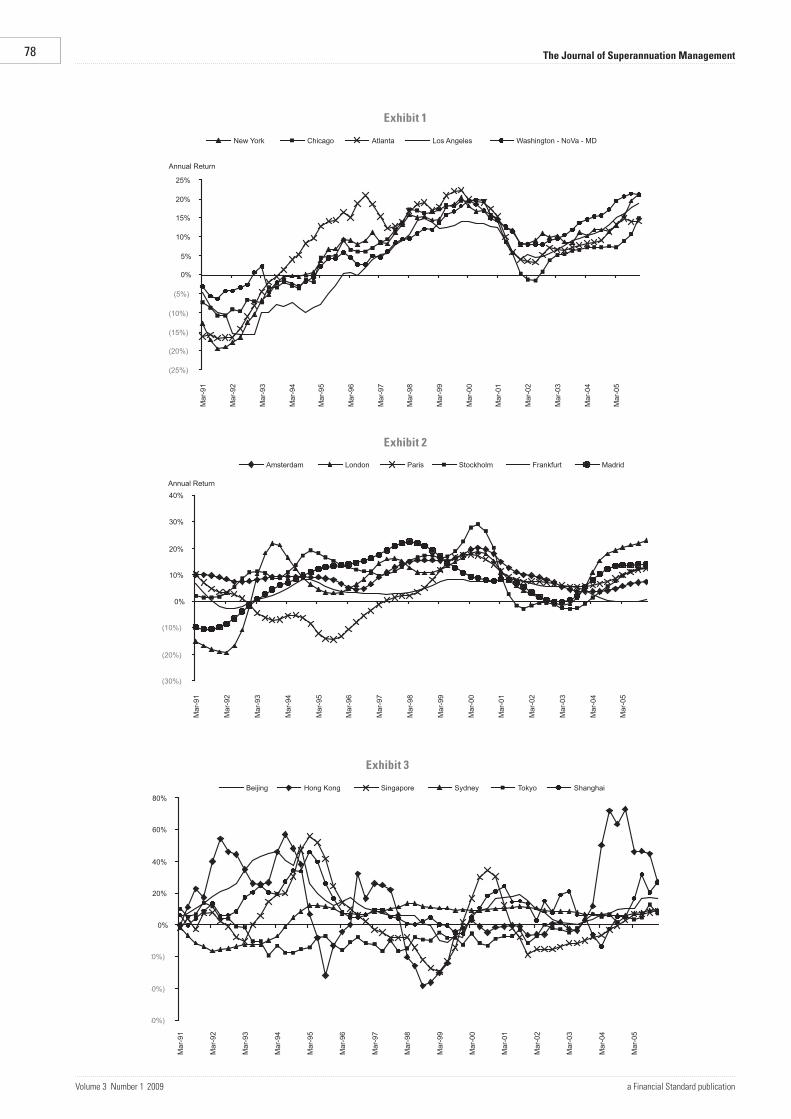

73 The Journal of Superannuation Management a Financial Standard publication Volume 3 Number 1 2009 Property & Portfolio Research, Inc. (PPR) is an independent real estate research and portfolio strategy firm that provides leading institutional real estate market participants with objective research on real estate cycles and their implications for investment strategy. We help clients apply our market research, analytics, and strategic thinking to stay ahead of market trends and maximise risk-adjusted returns. Founded by Susan Hudson-Wilson, PPR employs over 50 economists on its staff of over 90 employees worldwide. PPR’s industry experts cover each of the real estate quadrants: public and private, debt and equity. PPR is wholly owned by DMG Information, a subsidiary of the Daily Mail and General Trust, a leading diversified British media company. C apital flows are increasingly global across all asset classes, including the real estate world. Even the least sophisticated investor generally understands the benefit of a global investment strategy when considering a stock or bond portfolio. Consequently, institutional investors should also apply a global view on asset allocation to real estate investment. Because global real estate portfolios contain assets influenced by different national economies, with very different drivers, growth rates, and risk, the correlation of total returns between assets in these markets can be very low. Low or negative correlations provide the ultimate recipe for the “free lunch” of modern portfolio theory; returns that are the weighted average of assets within the portfolio, but volatility less than the weighted volatility of the individual assets. Unlike the case in domestic investments, however, the movement of foreign exchange rates must be considered, as unfavorable currency movements can severely hinder performance. Real estate is generally a long-hold investment strategy, but property income and ultimately the final selling price will be received in the local currency and must, at some point, be repatriated to US dollars. In this paper we focus on the benefits of global diversification on a real estate portfolio and the effect of currency movements on those returns, using historical return data for 18 international office markets. In the United States, pension funds represent a sizeable portion of the private equity universe. Of those pension funds that held greater than 2 per cent of total assets in real estate in 2005, approximately 7.6 per cent of total assets in 2006 were allocated to real estate. Broadening our perspective to a larger sample of pension funds, including those who have more recently begun to make real estate investments, approximately 6.5 per cent of assets were allocated to real estate in 2006, about 130 basis points lower than their target. 1 Within those real estate assets, a small but growing portion has been allocated to international real estate. With current international allocations at only about 3.3 per cent, it is expected that the percentage of international real estate in all real estate held by pension funds should continue to rise. Indeed, of the capital flows projected for 2007, 11 per cent has been slated for international investment. 2 Broadening our perspective to the entire private Benefits of global diversification on a real estate portfolio By Adam Hastings, Quantitative Analyst Property & Portfolio Research and Hans Nordby , Director of US Market Research and Forecasting, Property & Portfolio Research

Transcript of Benefits of global diversification on a real estate portfolio - Journal of