Basics of Valuation - C · PDF fileBasics of Valuation. Contents Articles Valuation (finance)...

25

PDF generated using the open source mwlib toolkit. See http://code.pediapress.com/ for more information. PDF generated at: Fri, 15 Aug 2014 12:58:42 UTC Basics of Valuation

Transcript of Basics of Valuation - C · PDF fileBasics of Valuation. Contents Articles Valuation (finance)...

PDF generated using the open source mwlib toolkit. See http://code.pediapress.com/ for more information.PDF generated at: Fri, 15 Aug 2014 12:58:42 UTC

Basics of Valuation

ContentsArticles

Valuation (finance) 1Book value 6Discounted cash flow 9Valuation using multiples 14

ReferencesArticle Sources and Contributors 21Image Sources, Licenses and Contributors 22

Article LicensesLicense 23

Valuation (finance) 1

Valuation (finance)

Accounting

•• Historical cost accounting•• Constant purchasing power

accounting•• Management accounting•• Tax accounting

Business portal

•• v•• t• e [1]

In finance, valuation is the process of estimating what something is worth.[2] Items that are usually valued are afinancial asset or liability. Valuations can be done on assets (for example, investments in marketable securities suchas stocks, options, business enterprises, or intangible assets such as patents and trademarks) or on liabilities (e.g.,bonds issued by a company). Valuations are needed for many reasons such as investment analysis, capital budgeting,merger and acquisition transactions, financial reporting, taxable events to determine the proper tax liability, and inlitigation.

Valuation overviewValuation of financial assets is done using one or more of these types of models:1. Absolute value models that determine the present value of an asset's expected future cash flows. These kinds of

models take two general forms: multi-period models such as discounted cash flow models or single-period modelssuch as the Gordon model. These models rely on mathematics rather than price observation.

2. Relative value models determine value based on the observation of market prices of similar assets.3. Option pricing models are used for certain types of financial assets (e.g., warrants, put options, call options,

employee stock options, investments with embedded options such as a callable bond) and are a complex presentvalue model. The most common option pricing models are the Black–Scholes-Merton models and lattice models.

Common terms for the value of an asset or liability are market value, fair value, and intrinsic value. The meanings ofthese terms differ. For instance, when an analyst believes a stock's intrinsic value is greater (less) than its marketprice, an analyst makes a "buy" ("sell") recommendation. Moreover, an asset's intrinsic value may be subject topersonal opinion and vary among analysts.The International Valuation Standards include definitions for common bases of value and generally accepted practiceprocedures for valuing assets of all types.

Valuation (finance) 2

Business valuationBusinesses or fractional interests in businesses may be valued for various purposes such as mergers and acquisitions,sale of securities, and taxable events. An accurate valuation of privately owned companies largely depends on thereliability of the firm's historic financial information. Public company financial statements are audited by CertifiedPublic Accountants (USA), Chartered Certified Accountants (ACCA) or Chartered Accountants (UK and Canada)and overseen by a government regulator. Alternatively, private firms do not have government oversight—unlessoperating in a regulated industry—and are usually not required to have their financial statements audited. Moreover,managers of private firms often prepare their financial statements to minimize profits and, therefore, taxes.Alternatively, managers of public firms tend to want higher profits to increase their stock price. Therefore, a firm'shistoric financial information may not be accurate and can lead to over- and undervaluation. In an acquisition, abuyer often performs due diligence to verify the seller's information.There are commonly three pillars to valuing business entities: comparable company analyses, discounted cash flowanalysis, and precedent transaction analysisFinancial statements prepared in accordance with generally accepted accounting principles (GAAP) show manyassets based on their historic costs rather than at their current market values. For instance, a firm's balance sheet willusually show the value of land it owns at what the firm paid for it rather than at its current market value. But underGAAP requirements, a firm must show the fair values (which usually approximates market value) of some types ofassets such as financial instruments that are held for sale rather than at their original cost. When a firm is required toshow some of its assets at fair value, some call this process "mark-to-market". But reporting asset values on financialstatements at fair values gives managers ample opportunity to slant asset values upward to artificially increase profitsand their stock prices. Managers may be motivated to alter earnings upward so they can earn bonuses. Despite therisk of manager bias, equity investors and creditors prefer to know the market values of a firm's assets—rather thantheir historical costs—because current values give them better information to make decisions.This method estimates the value of an asset based on its expected future cash flows, which are discounted to thepresent (i.e., the present value). This concept of discounting future money is commonly known as the time value ofmoney. For instance, an asset that matures and pays $1 in one year is worth less than $1 today. The size of thediscount is based on an opportunity cost of capital and it is expressed as a percentage or discount rate.In finance theory, the amount of the opportunity cost is based on a relation between the risk and return of some sortof investment. Classic economic theory maintains that people are rational and averse to risk. They, therefore, need anincentive to accept risk. The incentive in finance comes in the form of higher expected returns after buying a riskyasset. In other words, the more risky the investment, the more return investors want from that investment. Using thesame example as above, assume the first investment opportunity is a government bond that will pay interest of 5%per year and the principal and interest payments are guaranteed by the government. Alternatively, the secondinvestment opportunity is a bond issued by small company and that bond also pays annual interest of 5%. If given achoice between the two bonds, virtually all investors would buy the government bond rather than the small-firmbond because the first is less risky while paying the same interest rate as the riskier second bond. In this case, aninvestor has no incentive to buy the riskier second bond. Furthermore, in order to attract capital from investors, thesmall firm issuing the second bond must pay an interest rate higher than 5% that the government bond pays.Otherwise, no investor is likely to buy that bond and, therefore, the firm will be unable to raise capital. But byoffering to pay an interest rate more than 5% the firm gives investors an incentive to buy a riskier bond.For a valuation using the discounted cash flow method, one first estimates the future cash flows from the investmentand then estimates a reasonable discount rate after considering the riskiness of those cash flows and interest rates inthe capital markets. Next, one makes a calculation to compute the present value of the future cash flows.

Valuation (finance) 3

Guideline companies methodMain article: Comparable company analysisThis method determines the value of a firm by observing the prices of similar companies (called "guidelinecompanies") that sold in the market. Those sales could be shares of stock or sales of entire firms. The observedprices serve as valuation benchmarks. From the prices, one calculates price multiples such as the price-to-earnings orprice-to-book ratios—one or more of which used to value the firm. For example, the average price-to-earningsmultiple of the guideline companies is applied to the subject firm's earnings to estimate its value.Many price multiples can be calculated. Most are based on a financial statement element such as a firm's earnings(price-to-earnings) or book value (price-to-book value) but multiples can be based on other factors such asprice-per-subscriber.

Net asset value methodMain article: Cost methodThe third-most common method of estimating the value of a company looks to the assets and liabilities of thebusiness. At a minimum, a solvent company could shut down operations, sell off the assets, and pay the creditors.Any cash that would remain establishes a floor value for the company. This method is known as the net asset valueor cost method. In general the discounted cash flows of a well-performing company exceed this floor value. Somecompanies, however, are worth more "dead than alive", like weakly performing companies that own many tangibleassets. This method can also be used to value heterogeneous portfolios of investments, as well as nonprofits, forwhich discounted cash flow analysis is not relevant. The valuation premise normally used is that of an orderlyliquidation of the assets, although some valuation scenarios (e.g., purchase price allocation) imply an "in-use"valuation such as depreciated replacement cost new.An alternative approach to the net asset value method is the excess earnings method. This method was first describedin ARM34, and later refined by the U.S. Internal Revenue Service's Revenue Ruling 68-609. The excess earningsmethod has the appraiser identify the value of tangible assets, estimate an appropriate return on those tangible assets,and subtract that return from the total return for the business, leaving the "excess" return, which is presumed to comefrom the intangible assets. An appropriate capitalization rate is applied to the excess return, resulting in the value ofthose intangible assets. That value is added to the value of the tangible assets and any non-operating assets, and thetotal is the value estimate for the business as a whole.

UsageIn finance, valuation analysis is required for many reasons including tax assessment, wills and estates, divorcesettlements, business analysis, and basic bookkeeping and accounting. Since the value of things fluctuates over time,valuations are as of a specific date like the end of the accounting quarter or year. They may alternatively bemark-to-market estimates of the current value of assets or liabilities as of this minute or this day for the purposes ofmanaging portfolios and associated financial risk (for example, within large financial firms including investmentbanks and stockbrokers).Some balance sheet items are much easier to value than others. Publicly traded stocks and bonds have prices that arequoted frequently and readily available. Other assets are harder to value. For instance, private firms that have nofrequently quoted price. Additionally, financial instruments that have prices that are partly dependent on theoreticalmodels of one kind or another are difficult to value. For example, options are generally valued using theBlack–Scholes model while the liabilities of life assurance firms are valued using the theory of present value.Intangible business assets, like goodwill and intellectual property, are open to a wide range of value interpretations.It is possible and conventional for financial professionals to make their own estimates of the valuations of assets or liabilities that they are interested in. Their calculations are of various kinds including analyses of companies that

Valuation (finance) 4

focus on price-to-book, price-to-earnings, price-to-cash-flow and present value calculations, and analyses of bondsthat focus on credit ratings, assessments of default risk, risk premia, and levels of real interest rates. All of theseapproaches may be thought of as creating estimates of value that compete for credibility with the prevailing share orbond prices, where applicable, and may or may not result in buying or selling by market participants. Where thevaluation is for the purpose of a merger or acquisition the respective businesses make available further detailedfinancial information, usually on the completion of a non-disclosure agreement.It is important to note that valuation requires judgment and assumptions:•• There are different circumstances and purposes to value an asset (e.g., distressed firm, tax purposes, mergers and

acquisitions, financial reporting). Such differences can lead to different valuation methods or differentinterpretations of the method results

•• All valuation models and methods have limitations (e.g., degree of complexity, relevance of observations,mathematical form)

•• Model inputs can vary significantly because of necessary judgment and differing assumptionsUsers of valuations benefit when key information, assumptions, and limitations are disclosed to them. Then they canweigh the degree of reliability of the result and make their decision.

Valuation of a suffering companyAdditional adjustments to a valuation approach, whether it is market-, income-, or asset-based, may be necessary insome instances like:•• Excess or restricted cash•• Other non-operating assets and liabilities•• Lack of marketability discount of shares•• Control premium or lack of control discount•• Above- or below-market leases•• Excess salaries in the case of private companiesThere are other adjustments to the financial statements that have to be made when valuing a distressed company.Andrew Miller identifies typical adjustments used to recast the financial statements that include:• Working capital adjustment•• Deferred capital expenditures• Cost of goods sold adjustment•• Non-recurring professional fees and costs• Certain non-operating income/expense items[3]

Valuation of intangible assetsValuation models can be used to value intangible assets such as for patent valuation, but also in copyrights, software,trade secrets, and customer relationships. Since few sales of benchmark intangible assets can ever be observed, oneoften values these sorts of assets using either a present value model or estimating the costs to recreate it. Regardlessof the method, the process is often time-consuming and costly.Valuations of intangible assets are often necessary for financial reporting and intellectual property transactions.Stock markets give indirectly an estimate of a corporation's intangible asset value. It can be reckoned as thedifference between its market capitalisation and its book value (by including only hard assets in it).

Valuation (finance) 5

Valuation of mining projectsIn mining, valuation is the process of determining the value or worth of a mining property. Mining valuations aresometimes required for IPOs, fairness opinions, litigation, mergers and acquisitions, and shareholder-related matters.In valuation of a mining project or mining property, fair market value is the standard of value to be used. TheCIMVal Standards ("Canadian Institute Of Mining, Metallurgy and Petroleum on Valuation of Mineral Properties")are a recognised standard for valuation of mining projects and is also recognised by the Toronto Stock Exchange(Venture). The standards, spearheaded by K. Spence & Dr. W. Roscoe,[4] stress the use of the cost approach, marketapproach, and the income approach, depending on the stage of development of the mining property or project.Depending on context, Real options valuation techniques are also sometimes employed; for further discussion heresee Business valuation: Option pricing approaches, Corporate finance: Valuing flexibility, as well as Mineraleconomics in general.

Asset pricing modelsSee also Modern portfolio theory

•• Capital asset pricing model•• Arbitrage pricing theory• Black–Scholes (for options)•• Fuzzy pay-off method for real option valuation•• Single-index model•• Markov switching multifractal

References[1] http:/ / en. wikipedia. org/ w/ index. php?title=Template:Accounting& action=edit[2] http:/ / financial-dictionary. thefreedictionary. com/ valuation[3] Joseph Swanson and Peter Marshall, Houlihan Lokey and Lyndon Norley, Kirkland & Ellis International LLP (2008). A Practitioner's Guide

to CorRestructuring, Andrew Miller’s Valuation of a Distressed Company p. 24. ISBN 978-1-905121-31-1[4] Standards and Guidelines for Valuation of Mineral Properties. Special committee of the Canadian Institute Of Mining, Metallurgy and

Petroleum on Valuation of Mineral Properties (CIMVAL), February 2003. (http:/ / web. cim. org/ standards/ documents/ Block487_Doc69.pdf)

External links• Valuation filter for public companies (http:/ / www. macroaxis. com/ invest/ ratio/ Current_Valuation) Allows

free look up of current enterprise values

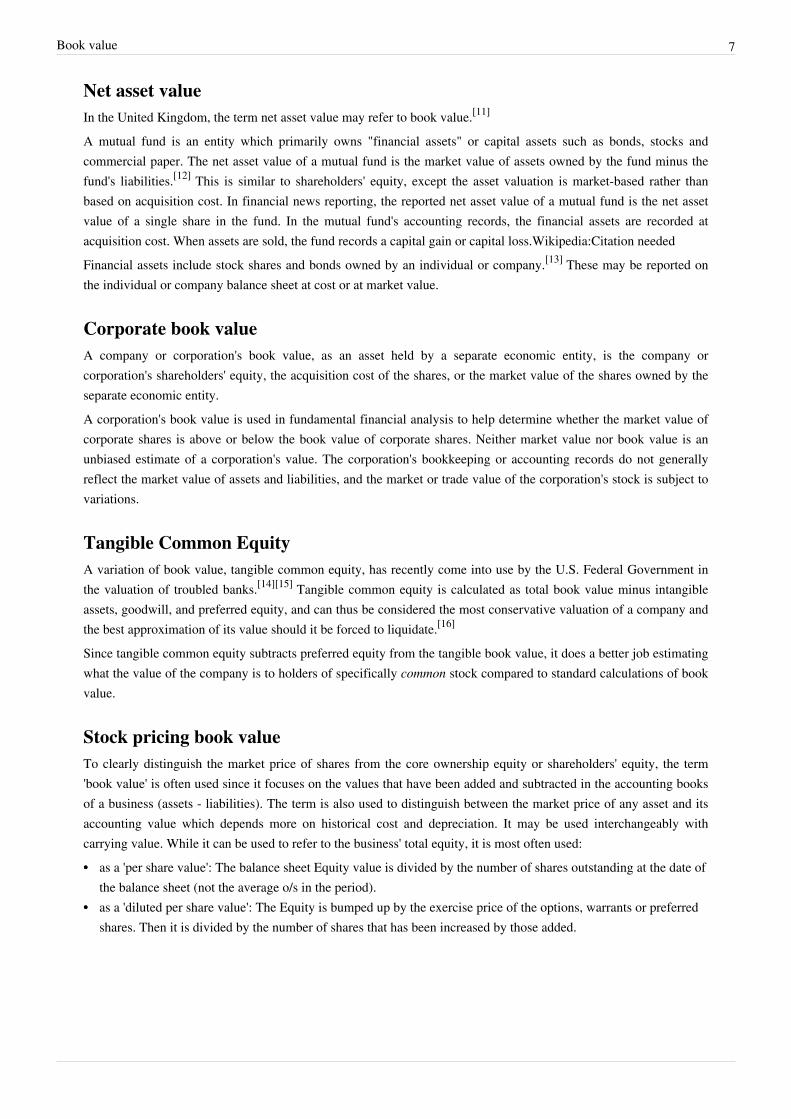

Book value 6

Book valueIn accounting, book value or carrying value is the value of an asset according to its balance sheet account balance.For assets, the value is based on the original cost of the asset less any depreciation, amortization or impairment costsmade against the asset. Traditionally, a company's book value is its total assets minus intangible assets andliabilities.[1] However, in practice, depending on the source of the calculation, book value may variably includegoodwill, intangible assets, or both.[2] When intangible assets and goodwill are explicitly excluded, the metric isoften specified to be "tangible book value".[3]

In the United Kingdom, the term net asset value may refer to the book value of a company.

Asset book valueAn asset's initial book value is its actual cash value or its acquisition cost. Cash assets are recorded or "booked" atactual cash value. Assets such as buildings, land and equipment are valued based on their acquisition cost, whichincludes the actual cash cost of the asset plus certain costs tied to the purchase of the asset, such as broker fees. Notall purchased items are recorded as assets; incidental supplies are recorded as expenses. Some assets might berecorded as current expenses for tax purposes. An example of this is assets purchased and expensed under Section179 of the US tax code.Wikipedia:Citation needed

Depreciable, amortizable and depletable assetsMonthly or annual depreciation, amortization and depletion are used to reduce the book value of assets over time asthey are "consumed" or used up in the process of obtaining revenue.[4] These non-cash expenses are recorded in theaccounting books after a trial balance is calculated to ensure that cash transactions have been recorded accurately.Depreciation is used to record the declining value of buildings and equipment over time. Land is not depreciated.Amortization is used to record the declining value of intangible assets such as patents. Depletion is used to record theconsumption of natural resources.[5]

Depreciation, amortization and depletion are recorded as expenses against a contra account. Contra accounts are usedin bookkeeping to record asset and liability valuation changes. "Accumulated depreciation" is a contra-asset accountused to record asset depreciation.[6]

Sample general journal entry for depreciation[7]

•• Depreciation expenses: building... debit = $150, under expenses in retained earnings•• Accumulated depreciation: building... credit = $150, under assetsThe balance sheet valuation for an asset is the asset's cost basis minus accumulated depreciation.[8] Similarbookkeeping transactions are used to record amortization and depletion."Discount on notes payable" is a contra-liability account which decreases the balance sheet valuation of theliability.[9]

When a company sells (issues) bonds, this debt is a long-term liability on the company's balance sheet, recorded inthe account Bonds Payable based on the contract amount. After the bonds are sold, the book value of Bonds Payableis increased or decreased to reflect the actual amount received in payment for the bonds. If the bonds sell for lessthan face value, the contra account Discount on Bonds Payable is debited for the difference between the amount ofcash received and the face value of the bonds.[10]

Book value 7

Net asset valueIn the United Kingdom, the term net asset value may refer to book value.[11]

A mutual fund is an entity which primarily owns "financial assets" or capital assets such as bonds, stocks andcommercial paper. The net asset value of a mutual fund is the market value of assets owned by the fund minus thefund's liabilities.[12] This is similar to shareholders' equity, except the asset valuation is market-based rather thanbased on acquisition cost. In financial news reporting, the reported net asset value of a mutual fund is the net assetvalue of a single share in the fund. In the mutual fund's accounting records, the financial assets are recorded atacquisition cost. When assets are sold, the fund records a capital gain or capital loss.Wikipedia:Citation neededFinancial assets include stock shares and bonds owned by an individual or company.[13] These may be reported onthe individual or company balance sheet at cost or at market value.

Corporate book valueA company or corporation's book value, as an asset held by a separate economic entity, is the company orcorporation's shareholders' equity, the acquisition cost of the shares, or the market value of the shares owned by theseparate economic entity.A corporation's book value is used in fundamental financial analysis to help determine whether the market value ofcorporate shares is above or below the book value of corporate shares. Neither market value nor book value is anunbiased estimate of a corporation's value. The corporation's bookkeeping or accounting records do not generallyreflect the market value of assets and liabilities, and the market or trade value of the corporation's stock is subject tovariations.

Tangible Common EquityA variation of book value, tangible common equity, has recently come into use by the U.S. Federal Government inthe valuation of troubled banks.[14][15] Tangible common equity is calculated as total book value minus intangibleassets, goodwill, and preferred equity, and can thus be considered the most conservative valuation of a company andthe best approximation of its value should it be forced to liquidate.[16]

Since tangible common equity subtracts preferred equity from the tangible book value, it does a better job estimatingwhat the value of the company is to holders of specifically common stock compared to standard calculations of bookvalue.

Stock pricing book valueTo clearly distinguish the market price of shares from the core ownership equity or shareholders' equity, the term'book value' is often used since it focuses on the values that have been added and subtracted in the accounting booksof a business (assets - liabilities). The term is also used to distinguish between the market price of any asset and itsaccounting value which depends more on historical cost and depreciation. It may be used interchangeably withcarrying value. While it can be used to refer to the business' total equity, it is most often used:•• as a 'per share value': The balance sheet Equity value is divided by the number of shares outstanding at the date of

the balance sheet (not the average o/s in the period).•• as a 'diluted per share value': The Equity is bumped up by the exercise price of the options, warrants or preferred

shares. Then it is divided by the number of shares that has been increased by those added.

Book value 8

Uses1. Book value is used in the financial ratio price/book. It is a valuation metric that sets the floor for stock prices

under a worst-case scenario. When a business is liquidated, the book value is what may be left over for the ownersafter all the debts are paid. Paying only a price/book = 1 means the investor will get all his investment back,assuming assets can be resold at their book value. Shares of capital intensive industries trade at lower price/bookratios because they generate lower earnings per dollar of assets. Business depending on human capital willgenerate higher earnings per dollar of assets, so will trade at higher price/book ratios.

2. Book value per share can be used to generate a measure of comprehensive earnings, when the opening andclosing values are reconciled. BookValuePerShare, beginning of year - Dividends + ShareIssuePremium +Comprehensive EPS = BookValuePerShare, end of year.[17]

Changes are caused by1.1. The sale of shares/units by the business increases the total book value. Book/sh will increase if the additional

shares are issued at a price higher than the pre-existing book/sh.2.2. The purchase of its own shares by the business will decrease total book value. Book/shares will decrease if more

is paid for them than was received when originally issued (pre-existing book/sh).3.3. Dividends paid out will decrease book value and book/sh.4. Comprehensive earnings/losses will increase/decrease book value and book/sh. Comprehensive earnings, in this

case, includes net income from the Income Statement, foreign exchange translation changes to Balance Sheetitems, accounting changes applied retroactively, and the opportunity cost of options exercised.

New share issues and dilutionThe issue of more shares does not necessarily decrease the value of the current owner. While it is correct that whenthe number of shares is doubled the EPS will be cut in half, it is too simple to be the full story. It all depends on howmuch was paid for the new shares and what return the new capital earns once invested. See the discussion at stockdilution.

Net book value of long term assetsBook value is often used interchangeably with "net book value" or "carrying value," which is the original acquisitioncost less accumulated depreciation, depletion or amortization. Book value is the term which means the value of thefirm as per the books of the company. It is the value at which the assets are valued in the balance sheet of thecompany as on the given date.

References[1] Hermanson, Roger H., James Don Edwards, R. F. Salmonson, (1987) Accounting Principles Volume II, Dow Jones-Irwin, p. 694. ISBN

1-55623-035-4[2] Graham and Dodd's Security Analysis, Fifth Edition, pp 318 - 319[3] Investopedia.com Tangible Book Value Per Share - TBVPS (http:/ / www. investopedia. com/ terms/ t/ TBVPS. asp#axzz1hBac0bcg)

retrieved 21 Dec 2011[4] Meigs and Meigs, Financial Accounting 4th ed. p. 90.[5] Wolk, Harry I., James L. Dodd and Michael G. Tearney (2004). Accounting Theory: Conceptual Issues in a Political and Economic

Environment, 6th ed. South-Western. pp. 330-331. ISBN 0-324-18623-1.[6][6] Meigs, p.91[7][7] Meigs, p.90[8][8] Meigs, p.105[9][9] Meigs, p. 313[10] Hermanson, Roger H., James Don Edwards, R. F. Salmonson, (1987) Accounting Principles Volume II, Dow Jones-Irwin, p. 657. ISBN

1-55623-035-4[11] Book Value (http:/ / www. investopedia. com/ terms/ b/ bookvalue. asp)

Book value 9

[12] Net Asset Value (http:/ / www. sec. gov/ answers/ nav. htm)[13] Groppelli, Angelico A. (2000) Finance, 4th ed., p.25.[14] Wall Street Journal 2/23/09, US Eyes Large Stake in Citi (http:/ / online. wsj. com/ article/ SB123535148618845005. html)[15] New York Times 2/24/09, Stress Test for Banks Exposes Rift on Wall St. (http:/ / www. nytimes. com/ 2009/ 02/ 25/ business/ economy/

25bank. html?_r=2)[16][16] Tangible Common Equity via Wikinvest[17] http:/ / www. retailinvestor. org/ earnings. html Use Book Value To Calculate Comprehensive EPS

Discounted cash flow

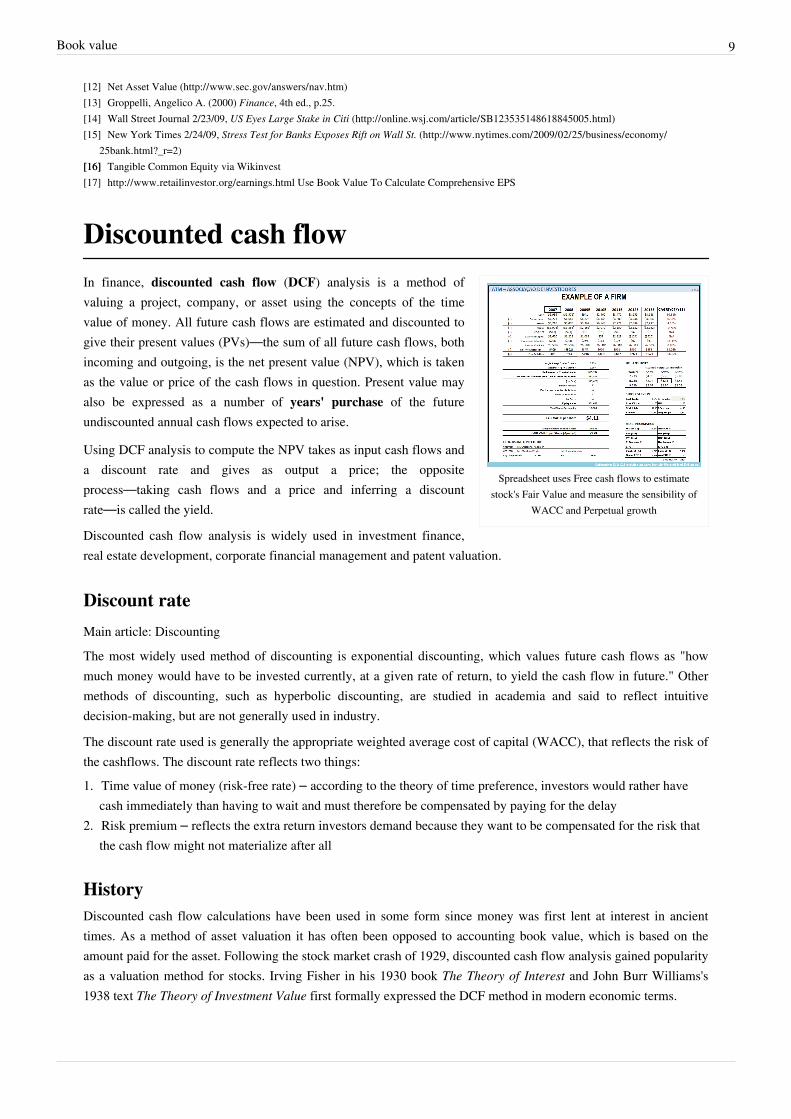

Spreadsheet uses Free cash flows to estimatestock's Fair Value and measure the sensibility of

WACC and Perpetual growth

In finance, discounted cash flow (DCF) analysis is a method ofvaluing a project, company, or asset using the concepts of the timevalue of money. All future cash flows are estimated and discounted togive their present values (PVs)—the sum of all future cash flows, bothincoming and outgoing, is the net present value (NPV), which is takenas the value or price of the cash flows in question. Present value mayalso be expressed as a number of years' purchase of the futureundiscounted annual cash flows expected to arise.

Using DCF analysis to compute the NPV takes as input cash flows anda discount rate and gives as output a price; the oppositeprocess—taking cash flows and a price and inferring a discountrate—is called the yield.

Discounted cash flow analysis is widely used in investment finance,real estate development, corporate financial management and patent valuation.

Discount rate

Main article: DiscountingThe most widely used method of discounting is exponential discounting, which values future cash flows as "howmuch money would have to be invested currently, at a given rate of return, to yield the cash flow in future." Othermethods of discounting, such as hyperbolic discounting, are studied in academia and said to reflect intuitivedecision-making, but are not generally used in industry.

The discount rate used is generally the appropriate weighted average cost of capital (WACC), that reflects the risk ofthe cashflows. The discount rate reflects two things:1. Time value of money (risk-free rate) – according to the theory of time preference, investors would rather have

cash immediately than having to wait and must therefore be compensated by paying for the delay2. Risk premium – reflects the extra return investors demand because they want to be compensated for the risk that

the cash flow might not materialize after all

HistoryDiscounted cash flow calculations have been used in some form since money was first lent at interest in ancienttimes. As a method of asset valuation it has often been opposed to accounting book value, which is based on theamount paid for the asset. Following the stock market crash of 1929, discounted cash flow analysis gained popularityas a valuation method for stocks. Irving Fisher in his 1930 book The Theory of Interest and John Burr Williams's1938 text The Theory of Investment Value first formally expressed the DCF method in modern economic terms.

Discounted cash flow 10

Mathematics

Discounted cash flowsThe discounted cash flow formula is derived from the future value formula for calculating the time value of moneyand compounding returns.

Thus the discounted present value (for one cash flow in one future period) is expressed as:

where• DPV is the discounted present value of the future cash flow (FV), or FV adjusted for the delay in receipt;• FV is the nominal value of a cash flow amount in a future period;• i is the interest rate or discount rate, which reflects the cost of tying up capital and may also allow for the risk that

the payment may not be received in full;• n is the time in years before the future cash flow occurs.Where multiple cash flows in multiple time periods are discounted, it is necessary to sum them as follows:

for each future cash flow (FV) at any time period (t) in years from the present time, summed over all time periods.The sum can then be used as a net present value figure. If the amount to be paid at time 0 (now) for all the futurecash flows is known, then that amount can be substituted for DPV and the equation can be solved for i, that is theinternal rate of return.All the above assumes that the interest rate remains constant throughout the whole period.

Continuous cash flowsFor continuous cash flows, the summation in the above formula is replaced by an integration:

where is now the rate of cash flow, and .

Example DCFTo show how discounted cash flow analysis is performed, consider the following simplified example.•• John Doe buys a house for $100,000. Three years later, he expects to be able to sell this house for $150,000.Simple subtraction suggests that the value of his profit on such a transaction would be $150,000 − $100,000 =$50,000, or 50%. If that $50,000 is amortized over the three years, his implied annual return (known as the internalrate of return) would be about 14.5%. Looking at those figures, he might be justified in thinking that the purchaselooked like a good idea.1.1453 x 100000 = 150000 approximately.However, since three years have passed between the purchase and the sale, any cash flow from the sale must be discounted accordingly. At the time John Doe buys the house, the 3-year US Treasury Note rate is 5% per annum. Treasury Notes are generally considered to be inherently less risky than real estate, since the value of the Note is

Discounted cash flow 11

guaranteed by the US Government and there is a liquid market for the purchase and sale of T-Notes. If he hadn't puthis money into buying the house, he could have invested it in the relatively safe T-Notes instead. This 5% per annumcan therefore be regarded as the risk-free interest rate for the relevant period (3 years).Using the DPV formula above (FV=$150,000, i=0.05, n=3), that means that the value of $150,000 received in threeyears actually has a present value of $129,576 (rounded off). In other words we would need to invest $129,576 in aT-Bond now to get $150,000 in 3 years almost risk free. This is a quantitative way of showing that money in thefuture is not as valuable as money in the present ($150,000 in 3 years isn't worth the same as $150,000 now; it isworth $129,576 now).Subtracting the purchase price of the house ($100,000) from the present value results in the net present value of thewhole transaction, which would be $29,576 or a little more than 29% of the purchase price.Another way of looking at the deal as the excess return achieved (over the risk-free rate) is (114.5 - 105)/(100 + 5) orapproximately 9.0% (still very respectable).But what about risk?We assume that the $150,000 is John's best estimate of the sale price that he will be able to achieve in 3 years time(after deducting all expenses, of course). There is of course a lot of uncertainty about house prices, and the outcomemay end up higher or lower than this estimate.(The house John is buying is in a "good neighborhood," but market values have been rising quite a lot lately and thereal estate market analysts in the media are talking about a slow-down and higher interest rates. There is aprobability that John might not be able to get the full $150,000 he is expecting in three years due to a slowing ofprice appreciation, or that loss of liquidity in the real estate market might make it very hard for him to sell at all.)Under normal circumstances, people entering into such transactions are risk-averse, that is to say that they areprepared to accept a lower expected return for the sake of avoiding risk. See Capital asset pricing model for a furtherdiscussion of this. For the sake of the example (and this is a gross simplification), let's assume that he values thisparticular risk at 5% per annum (we could perform a more precise probabilistic analysis of the risk, but that isbeyond the scope of this article). Therefore, allowing for this risk, his expected return is now 9.0% per annum (thearithmetic is the same as above).And the excess return over the risk-free rate is now (109 - 105)/(100 + 5) which comes to approximately 3.8% perannum.That return rate may seem low, but it is still positive after all of our discounting, suggesting that the investmentdecision is probably a good one: it produces enough profit to compensate for tying up capital and incurring risk witha little extra left over. When investors and managers perform DCF analysis, the important thing is that the net presentvalue of the decision after discounting all future cash flows at least be positive (more than zero). If it is negative, thatmeans that the investment decision would actually lose money even if it appears to generate a nominal profit. Forinstance, if the expected sale price of John Doe's house in the example above was not $150,000 in three years, but$130,000 in three years or $150,000 in five years, then on the above assumptions buying the house would actuallycause John to lose money in present-value terms (about $3,000 in the first case, and about $8,000 in the second).Similarly, if the house was located in an undesirable neighborhood and the Federal Reserve Bank was about to raiseinterest rates by five percentage points, then the risk factor would be a lot higher than 5%: it might not be possiblefor him to predict a profit in discounted terms even if he thinks he could sell the house for $200,000 in three years.In this example, only one future cash flow was considered. For a decision which generates multiple cash flows inmultiple time periods, all the cash flows must be discounted and then summed into a single net present value.

Discounted cash flow 12

Methods of appraisal of a company or projectThis is necessarily a simple treatment of a complex subject: more detail is beyond the scope of this article.For these valuation purposes, a number of different DCF methods are distinguished today, some of which areoutlined below. The details are likely to vary depending on the capital structure of the company. However theassumptions used in the appraisal (especially the equity discount rate and the projection of the cash flows to beachieved) are likely to be at least as important as the precise model used.Both the income stream selected and the associated cost of capital model determine the valuation result obtainedwith each method. This is one reason these valuation methods are formally referred to as the Discounted FutureEconomic Income methods.•• Equity-Approach

• Flows to equity approach (FTE)Discount the cash flows available to the holders of equity capital, after allowing for cost of servicing debt capitalAdvantages: Makes explicit allowance for the cost of debt capitalDisadvantages: Requires judgement on choice of discount rate•• Entity-Approach:

• Adjusted present value approach (APV)Discount the cash flows before allowing for the debt capital (but allowing for the tax relief obtained on the debtcapital)Advantages: Simpler to apply if a specific project is being valued which does not have earmarked debt capitalfinanceDisadvantages: Requires judgement on choice of discount rate; no explicit allowance for cost of debt capital, whichmay be much higher than a "risk-free" rate

• Weighted average cost of capital approach (WACC)Derive a weighted cost of the capital obtained from the various sources and use that discount rate to discount thecash flows from the projectAdvantages: Overcomes the requirement for debt capital finance to be earmarked to particular projectsDisadvantages: Care must be exercised in the selection of the appropriate income stream. The net cash flow to totalinvested capital is the generally accepted choice.

• Total cash flow approach (TCF)Wikipedia:Please clarifyThis distinction illustrates that the Discounted Cash Flow method can be used to determine the value of variousbusiness ownership interests. These can include equity or debt holders.Alternatively, the method can be used to value the company based on the value of total invested capital. In each case,the differences lie in the choice of the income stream and discount rate. For example, the net cash flow to totalinvested capital and WACC are appropriate when valuing a company based on the market value of all investedcapital.

ShortcomingsCommercial banks have widely used discounted cash flow as a method of valuing commercial real estate construction projects. This practice has two substantial shortcomings. 1) The discount rate assumption relies on the market for competing investments at the time of the analysis, which would likely change, perhaps dramatically, over time, and 2) straight line assumptions about income increasing over ten years are generally based upon historic increases in market rent but never factors in the cyclical nature of many real estate markets. Most loans are made

Discounted cash flow 13

during boom real estate markets and these markets usually last fewer than ten years. Using DCF to analyzecommercial real estate during any but the early years of a boom market will lead to overvaluation of theassetWikipedia:Citation needed.Discounted cash flow models are powerful, but they do have shortcomings. DCF is merely a mechanical valuationtool, which makes it subject to the principle "garbage in, garbage out". Small changes in inputs can result in largechanges in the value of a company. Instead of trying to project the cash flows to infinity, terminal value techniquesare often used. A simple annuity is used to estimate the terminal value past 10 years, for example. This is donebecause it is harder to come to a realistic estimate of the cash flows as time goes on involves calculating the periodof time likely to recoup the initial outlay.

References

External links• Continuous compounding/cash flows (http:/ / ocw. mit. edu/ courses/ nuclear-engineering/

22-812j-managing-nuclear-technology-spring-2004/ lecture-notes/ lec03slides. pdf)• The Theory of Interest (http:/ / www. econlib. org/ library/ YPDBooks/ Fisher/ fshToI. html) at the Library of

Economics and Liberty.• Monography about DCF (including some lectures on DCF) (http:/ / www. wacc. biz).• Foolish Use of DCF (http:/ / www. fool. com/ news/ commentary/ 2005/ commentary05032803. htm). Motley

Fool.• Getting Started With Discounted Cash Flows (http:/ / www. thestreet. com/ university/ personalfinance/

10385275. html). The Street.• International Good Practice: Guidance on Project Appraisal Using Discounted Cash Flow (http:/ / www. ifac.

org/ Members/ DownLoads/ Project_Appraisal_Using_DCF_formatted. pdf), International Federation ofAccountants, June 2008, ISBN 978-1-934779-39-2

• Equivalence between Discounted Cash Flow (DCF) and Residual Income (RI) (http:/ / papers. ssrn. com/ sol3/papers. cfm?abstract_id=381880) Working paper; Duke University - Center for Health Policy, Law andManagement

• Download of business case spreadsheets for discounted cash flow calculation http:/ / www. thebusinesscase. info(Downloads/For Professionals and Students)

Further reading• International Association of CPAs, Attorneys, and Management (IACAM) (http:/ / www. iacam. org/ ) (Free DCF

Valuation E-Book Guidebook)• International Federation of Accountants (2007). Project Appraisal Using Discounted Cash Flow.• Copeland, Thomas E.; Tim Koller; Jack Murrin (2000). Valuation: Measuring and Managing the Value of

Companies. New York: John Wiley & Sons. ISBN 0-471-36190-9.• Damodaran, Aswath (1996). Investment Valuation: Tools and Techniques for Determining the Value of Any Asset.

New York: John Wiley & Sons. ISBN 0-471-13393-0.• Rosenbaum, Joshua; Joshua Pearl (2009). Investment Banking: Valuation, Leveraged Buyouts, and Mergers &

Acquisitions. Hoboken, NJ: John Wiley & Sons. ISBN 0-470-44220-4.• James R. Hitchnera (2006). Financial Valuation: Applications and Models. USA: Wiley Finance.

ISBN 0-471-76117-6.• Chander Sawhney (2012). Discounted Cash Flow –The Prominent Income Approach to Valuation. INDIA: (http:/

/ corporatevaluations. in/ static-1047-22-oth -Articles and Research Hub).

Valuation using multiples 14

Valuation using multiplesValuation using multiples or relative valuation is a method of estimating the value of an asset by comparing it tothe values assessed by the market for similar or comparable assets.The process consists of:• identifying comparable assets (the peer group) and obtaining market values for these assets.• converting these market values into standardized values relative to a key statistic, since the absolute prices cannot

be compared. This process of standardizing creates valuation multiples.•• applying the valuation multiple to the key statistic of the asset being valued, controlling for any differences

between asset and the peer group that might affect the multiple.

Valuation multiplesA valuation multiple is simply an expression of market value of an asset relative to a key statistic that is assumed torelate to that value. To be useful, that statistic – whether earnings, cash flow or some other measure – must bear alogical relationship to the market value observed; to be seen, in fact, as the driver of that market value.In stock trading, one of the most widely used multiples is the price-earnings ratio (P/E ratio or PER) which is popularin part due to its wide availability and to the importance ascribed to earnings per share as a value driver. However,the usefulness of P/E ratios is lessened by the fact that earnings per share is subject to distortions from differences inaccounting rules and capital structures between companies.Other commonly used multiples are based on the enterprise value of a company, such as (EV/EBITDA, EV/EBIT,EV/NOPAT). These multiples reveal the rating of a business independently of its capital structure, and are ofparticular interest in mergers, acquisitions and transactions on private companies.Not all multiples are based on earnings or cash flow drivers. The price-to-book ratio (P/B) is a commonly usedbenchmark comparing market value to the accounting book value of the firm's assets. The price/sales ratio andEV/sales ratios measure value relative to sales. These multiples must be used with caution as both sales and bookvalues are less likely to be value drivers than earnings.Less commonly, valuation multiples may be based on non-financial industry-specific value drivers, such asenterprise value / number of subscribers for cable or telecoms businesses or enterprise value / audience numbers for abroadcasting company. In real estate valuations, the sales comparison approach often makes use of valuationmultiples based on the surface areas of the properties being valued.

Peer groupA peer group is a set of companies or assets which are selected as being sufficiently comparable to the company orassets being valued (usually by virtue of being in the same industry or by having similar characteristics in terms ofearnings growth and/or return on investment).In practice, no two businesses are alike, and analysts will often make adjustment to the observed multiples in order toattempt to harmonize the data into more comparable format. These adjustments may be based on a number offactors, including:•• Industrial / business environment factors: Business model, industry, geography, seasonality, inflation•• Accounting factors: Accounting policies, financial year end•• Financial: Capital structure•• Empirical factors: SizeThese adjustments can involve the use of regression analysis against different potential value drivers and are used totest correlations between the different value drivers.

Valuation using multiples 15

When the peer group consists of public quoted companies, this type of valuation is also often described ascomparable company analysis (or "comps", "peer group analysis", "equity comps", " trading comps", or "publicmarket multiples"). When the peer group consists of companies or assets that have been acquired in mergers oracquisitions, this type of valuation is described as precedent transaction analysis (or "transaction comps", "dealcomps", or "private market multiples")

Advantages/Disadvantages of Multiples

DisadvantagesThere are a number of criticisms levied against multiples, but in the main these can be summarised as:• Simplistic: A multiple is a distillation of a great deal of information into a single number or series of numbers. By

combining many value drivers into a point estimate, multiples may make it difficult to disaggregate the effect ofdifferent drivers, such as growth, on value. The danger is that this encourages simplistic – and possibly erroneous– interpretation.

•• Static: A multiple represents a snapshot of where a firm is at a point in time, but fails to capture the dynamic andever-evolving nature of business and competition.

•• Difficulties in comparisons: Multiples are primarily used to make comparisons of relative value. But comparingmultiples is an exacting art form, because there are so many reasons that multiples can differ, not all of whichrelate to true differences in value. For example, different accounting policies can result in diverging multiples forotherwise identical operating businesses.

• Dependence on correctly valued peers: The use of multiples only reveals patterns in relative values, not absolutevalues such as those obtained from discounted cash flow valuations. If the peer group as a whole is incorrectlyvalued (such as may happen during a stock market "bubble") then the resulting multiples will also be misvalued.

•• Short-term: Multiples are based on historic data or near-term forecasts. Valuations based on multiples willtherefore fail to capture differences in projected performance over the longer term, and will have difficultycorrectly valuing cyclical industries unless somewhat subjective normalization adjustements are made.

AdvantagesDespite these disadvantages, multiples have several advantages.•• Usefulness: Valuation is about judgement, and multiples provide a framework for making value judgements.

When used properly, multiples are robust tools that can provide useful information about relative value.• Simplicity: Their very simplicity and ease of calculation makes multiples an appealing and user-friendly method

of assessing value. Multiples can help the user avoid the potentially misleading precision of other, more ‘precise’approaches such as discounted cash flow valuation or EVA, which can create a false sense of comfort.

•• Relevance: Multiples focus on the key statistics that other investors use. Since investors in aggregate movemarkets, the most commonly used statistics and multiples will have the most impact.

These factors, and the existence of wide-ranging comparables, help explain the enduring use of multiples byinvestors despite the rise of other methods.

Valuation using multiples 16

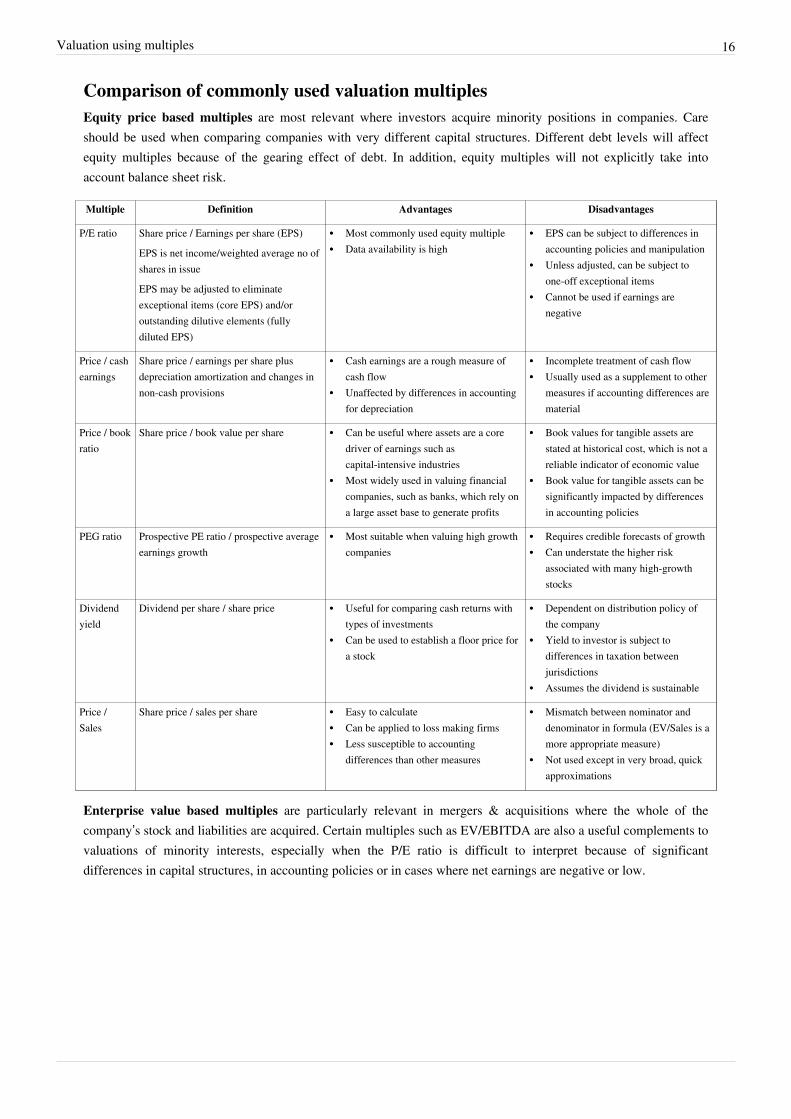

Comparison of commonly used valuation multiplesEquity price based multiples are most relevant where investors acquire minority positions in companies. Careshould be used when comparing companies with very different capital structures. Different debt levels will affectequity multiples because of the gearing effect of debt. In addition, equity multiples will not explicitly take intoaccount balance sheet risk.

Multiple Definition Advantages Disadvantages

P/E ratio Share price / Earnings per share (EPS)

EPS is net income/weighted average no ofshares in issue

EPS may be adjusted to eliminateexceptional items (core EPS) and/oroutstanding dilutive elements (fullydiluted EPS)

•• Most commonly used equity multiple•• Data availability is high

•• EPS can be subject to differences inaccounting policies and manipulation

•• Unless adjusted, can be subject toone-off exceptional items

•• Cannot be used if earnings arenegative

Price / cashearnings

Share price / earnings per share plusdepreciation amortization and changes innon-cash provisions

•• Cash earnings are a rough measure ofcash flow

•• Unaffected by differences in accountingfor depreciation

•• Incomplete treatment of cash flow•• Usually used as a supplement to other

measures if accounting differences arematerial

Price / bookratio

Share price / book value per share •• Can be useful where assets are a coredriver of earnings such ascapital-intensive industries

•• Most widely used in valuing financialcompanies, such as banks, which rely ona large asset base to generate profits

•• Book values for tangible assets arestated at historical cost, which is not areliable indicator of economic value

•• Book value for tangible assets can besignificantly impacted by differencesin accounting policies

PEG ratio Prospective PE ratio / prospective averageearnings growth

•• Most suitable when valuing high growthcompanies

•• Requires credible forecasts of growth•• Can understate the higher risk

associated with many high-growthstocks

Dividendyield

Dividend per share / share price •• Useful for comparing cash returns withtypes of investments

•• Can be used to establish a floor price fora stock

•• Dependent on distribution policy ofthe company

•• Yield to investor is subject todifferences in taxation betweenjurisdictions

•• Assumes the dividend is sustainable

Price /Sales

Share price / sales per share •• Easy to calculate•• Can be applied to loss making firms•• Less susceptible to accounting

differences than other measures

•• Mismatch between nominator anddenominator in formula (EV/Sales is amore appropriate measure)

•• Not used except in very broad, quickapproximations

Enterprise value based multiples are particularly relevant in mergers & acquisitions where the whole of thecompany’s stock and liabilities are acquired. Certain multiples such as EV/EBITDA are also a useful complements tovaluations of minority interests, especially when the P/E ratio is difficult to interpret because of significantdifferences in capital structures, in accounting policies or in cases where net earnings are negative or low.

Valuation using multiples 17

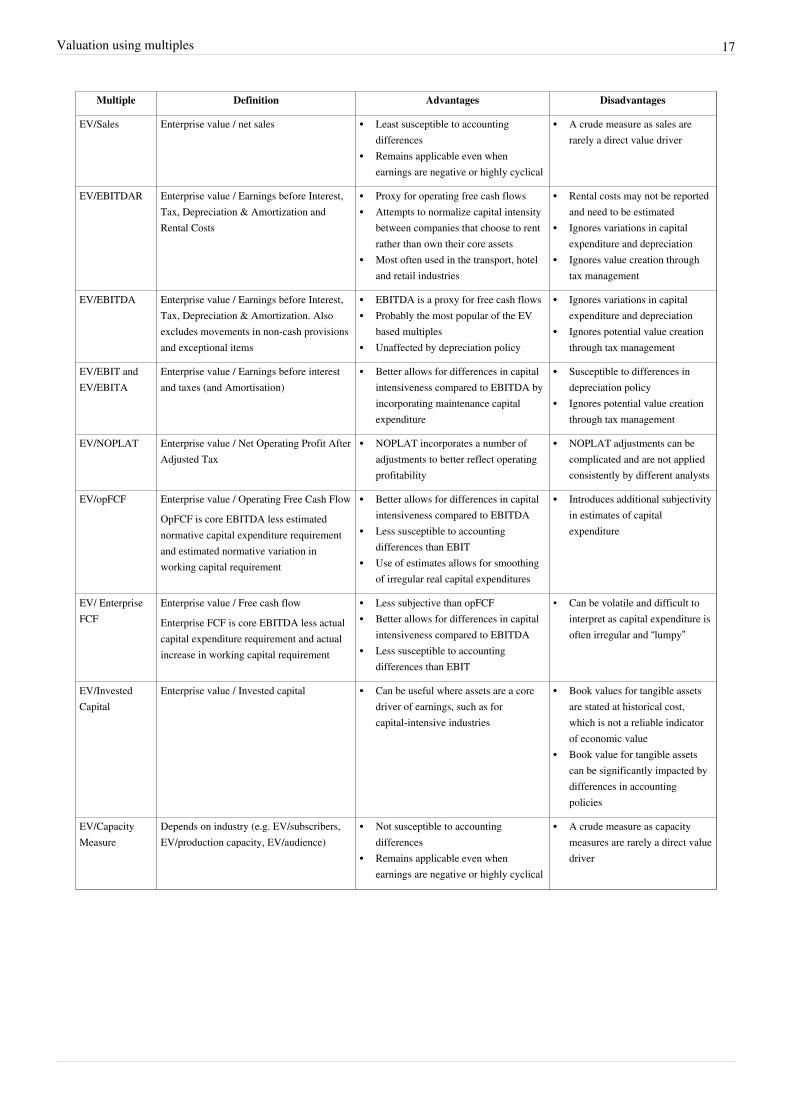

Multiple Definition Advantages Disadvantages

EV/Sales Enterprise value / net sales •• Least susceptible to accountingdifferences

•• Remains applicable even whenearnings are negative or highly cyclical

•• A crude measure as sales arerarely a direct value driver

EV/EBITDAR Enterprise value / Earnings before Interest,Tax, Depreciation & Amortization andRental Costs

•• Proxy for operating free cash flows•• Attempts to normalize capital intensity

between companies that choose to rentrather than own their core assets

•• Most often used in the transport, hoteland retail industries

•• Rental costs may not be reportedand need to be estimated

•• Ignores variations in capitalexpenditure and depreciation

•• Ignores value creation throughtax management

EV/EBITDA Enterprise value / Earnings before Interest,Tax, Depreciation & Amortization. Alsoexcludes movements in non-cash provisionsand exceptional items

•• EBITDA is a proxy for free cash flows•• Probably the most popular of the EV

based multiples•• Unaffected by depreciation policy

•• Ignores variations in capitalexpenditure and depreciation

•• Ignores potential value creationthrough tax management

EV/EBIT andEV/EBITA

Enterprise value / Earnings before interestand taxes (and Amortisation)

•• Better allows for differences in capitalintensiveness compared to EBITDA byincorporating maintenance capitalexpenditure

•• Susceptible to differences indepreciation policy

•• Ignores potential value creationthrough tax management

EV/NOPLAT Enterprise value / Net Operating Profit AfterAdjusted Tax

•• NOPLAT incorporates a number ofadjustments to better reflect operatingprofitability

•• NOPLAT adjustments can becomplicated and are not appliedconsistently by different analysts

EV/opFCF Enterprise value / Operating Free Cash Flow

OpFCF is core EBITDA less estimatednormative capital expenditure requirementand estimated normative variation inworking capital requirement

•• Better allows for differences in capitalintensiveness compared to EBITDA

•• Less susceptible to accountingdifferences than EBIT

•• Use of estimates allows for smoothingof irregular real capital expenditures

•• Introduces additional subjectivityin estimates of capitalexpenditure

EV/ EnterpriseFCF

Enterprise value / Free cash flow

Enterprise FCF is core EBITDA less actualcapital expenditure requirement and actualincrease in working capital requirement

•• Less subjective than opFCF•• Better allows for differences in capital

intensiveness compared to EBITDA•• Less susceptible to accounting

differences than EBIT

• Can be volatile and difficult tointerpret as capital expenditure isoften irregular and “lumpy”

EV/InvestedCapital

Enterprise value / Invested capital •• Can be useful where assets are a coredriver of earnings, such as forcapital-intensive industries

•• Book values for tangible assetsare stated at historical cost,which is not a reliable indicatorof economic value

•• Book value for tangible assetscan be significantly impacted bydifferences in accountingpolicies

EV/CapacityMeasure

Depends on industry (e.g. EV/subscribers,EV/production capacity, EV/audience)

•• Not susceptible to accountingdifferences

•• Remains applicable even whenearnings are negative or highly cyclical

•• A crude measure as capacitymeasures are rarely a direct valuedriver

Valuation using multiples 18

Example (discounted forward PE ratio method)

Mathematics

Condition: Peer company is profitable.Rf = discount rate during the last forecast year tf = last year of the forecast period. C = correction factor P = currentstock Price NPP = net profit peer company S = number of shares NPO = net profit of target company after forecastperiod

Process Data DiagramThe following diagram shows an overview of the process of company valuation using multiples. All activities in thismodel are explained in more detail in section 3: Using the Multiples method.

Using the Multiples Method

Determine Forecast Period

Determine the year after which the company value is to be known.Example:‘VirusControl’ is an ICT startup that has just finished their business plan. Their goal is to provide professionals withsoftware for simulating virus outbreaks. Their only investor is required to wait for 5 years before making an exit.Therefore VirusControl is using a forecast period of 5 years.

Valuation using multiples 19

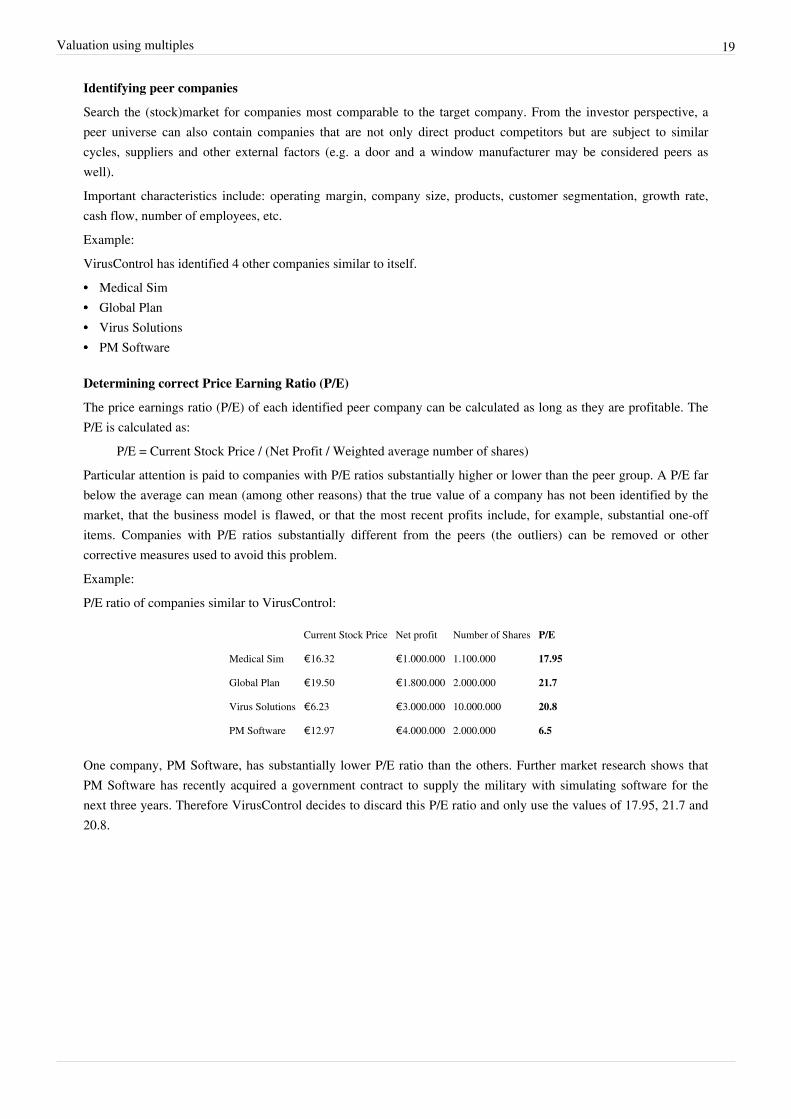

Identifying peer companies

Search the (stock)market for companies most comparable to the target company. From the investor perspective, apeer universe can also contain companies that are not only direct product competitors but are subject to similarcycles, suppliers and other external factors (e.g. a door and a window manufacturer may be considered peers aswell).Important characteristics include: operating margin, company size, products, customer segmentation, growth rate,cash flow, number of employees, etc.Example:VirusControl has identified 4 other companies similar to itself.•• Medical Sim•• Global Plan•• Virus Solutions•• PM Software

Determining correct Price Earning Ratio (P/E)

The price earnings ratio (P/E) of each identified peer company can be calculated as long as they are profitable. TheP/E is calculated as:

P/E = Current Stock Price / (Net Profit / Weighted average number of shares)Particular attention is paid to companies with P/E ratios substantially higher or lower than the peer group. A P/E farbelow the average can mean (among other reasons) that the true value of a company has not been identified by themarket, that the business model is flawed, or that the most recent profits include, for example, substantial one-offitems. Companies with P/E ratios substantially different from the peers (the outliers) can be removed or othercorrective measures used to avoid this problem.Example:P/E ratio of companies similar to VirusControl:

Current Stock Price Net profit Number of Shares P/E

Medical Sim €16.32 €1.000.000 1.100.000 17.95

Global Plan €19.50 €1.800.000 2.000.000 21.7

Virus Solutions €6.23 €3.000.000 10.000.000 20.8

PM Software €12.97 €4.000.000 2.000.000 6.5

One company, PM Software, has substantially lower P/E ratio than the others. Further market research shows thatPM Software has recently acquired a government contract to supply the military with simulating software for thenext three years. Therefore VirusControl decides to discard this P/E ratio and only use the values of 17.95, 21.7 and20.8.

Valuation using multiples 20

Determining future company value

The value of the target company after the forecast period can be calculated by:Average corrected P/E ratio * net profit at the end of the forecast period.Example:VirusControl is expecting a net profit at the end of the fifth year of about €2.2 million. They use the followingcalculation to determine their future value:((17.95 + 21.7 + 20.8) / 3) * 2.200.000 = €44.3 million

Determining discount rate / factor

Determine the appropriate discount rate and factor for the last year of the forecast period based on the risk levelassociated with the target companyExample:VirusControl has chosen their discount rate very high as their company is potentially very profitable but also veryrisky. They calculate their discount factor based on five years.

Risk Rate 50%

Discount Rate 50%

Discount Factor 0.1316

Determining current company value

Calculate the current value of the future company value by multiplying the future business value with the discountfactor. This is known as the time value of money.Example:VirusControl multiplies their future company value with the discount factor:44,300,000 * 0.1316 = 5,829,880 The company or equity value of VirusControl : €5.83 million

References

External links• Comparable Companies Analysis (http:/ / macabacus. com/ valuation/ comparable-companies)• Valuation Multiples: A Primer UBS Warburg (http:/ / www. scribd. com/ doc/ 79983013/

UBS-Valuation-Multiples-Primer).

Article Sources and Contributors 21

Article Sources and ContributorsValuation (finance) Source: http://en.wikipedia.org/w/index.php?oldid=620443111 Contributors: Accounting instructor, Aqeelzam, BD2412, BeL1EveR, Bgwhite, Boemmels, Bonadea, BusyStubber, Chakreshsinghai, Chhajjusandeep, Chimpex, DMCer, DWaterson, Dap242, Dbrandon30, Dbroadwell, DepartedUser4, DocendoDiscimus, Doprendek, Eastlaw, Edcolins, Edward,Enchanter, Erud, FactsAndFigures, Feco, Fenice, Flowanda, Fredouil, Funandtrvl, Good Olfactory, Gregalton, Haeinous, Hannibal19, HiMyNameIsFrancesca, HoulihanLokey, Hubbardaie,Investor123, J heisenberg, JamesAM, Jeremy112233, Jiminycricket55, John Quiggin, Jonathan de Boyne Pollard, JusticeIvory, Kaihsu, King brosby, Ladislav Mecir, LaidOff, Lamro, Levineps,LilHelpa, Listmeister, Lmatt, Master Scott Hall, Materialscientist, Mcrain, Mellery, Mergersguy, Michael Hardy, Mion, Mnmngb, MrOllie, Mulder416, Nhsmith, Niceguyedc, Nneonneo, Pearle,Pfortuny, Pgreenfinch, Physitsky, Poweroid, RCSB, RJN, Rinconsoleao, RkuipersNL, Ronz, SDC, Sam Hocevar, SchreiberBike, Simon123, Spizzwink, Squids and Chips, Stefanomione, StevenZhang, T4, TastyPoutine, Tearlach, TheAMmollusc, Urbanrenewal, Utc-100, Vukovic2, Waggers, Wikiwizard57685, Xezbeth, Zzuuzz, 154 anonymous edits

Book value Source: http://en.wikipedia.org/w/index.php?oldid=595865029 Contributors: Andersean, Barney Gumble, Billatq, Biscuittin, BlankVerse, Calltech, Carstensen, Chrisvls, Diupwijk,Dr.Soft, Drz, Earth, EdgeName, Edward, Eran117, Fayenatic london, Feco, Foggy Morning, Gabbe, GraemeL, Grafen, GreenZeb, Gregalton, Hu12, Iner22, Jerryseinfeld, JimVC3, Jni,Kingpin13, Kuru, Leonxlin, Levineps, Maarschalk, Macrakis, Michael Hardy, Mohamed-Ahmed-FG, Msablic, Ohnoitsjamie, PennySeven, Quinsareth, Retail Investor, Roadrunner, Ronnotel,Rsrikanth05, Shyam, SirIsaacBrock, SoPhIe WhO, Stephenb, T-dot, The Thing That Should Not Be, Titocosta, Trusilver, Ujax, Ultra megatron, Vlad2000Plus, WikipedianYknOK, ZainEbrahim111, Zencv, 80 anonymous edits

Discounted cash flow Source: http://en.wikipedia.org/w/index.php?oldid=610023338 Contributors: 1-is-blue, 10.219, 1exec1, Accountingstandards, Al64, Alansohn, Allentownrocks,Allstarecho, Americangao, Ancheta Wis, Angel ivanov angelov, AnnaFrance, BD2412, Bejnar, BenFrantzDale, Blueboatantilinks, Bob1960evens, Bonadea, Br809, Brownhonorman, Btyner,Buchoman, Caltas, Cashflowtrader, Chander sawhney, Cheese Sandwich, ChrisGualtieri, Cibergili, Clear memory, Coasterlover1994, Conversion script, Courcelles is travelling, DanielVonEhren,David Jaša, Dbrandon30, Denisarona, Doradus, Duoduoduo, EdJohnston, Edward, Ehrenkater, Electricmuffin11, Ertyqway, Everyking, Feco, Finnancier, Fintor, Flowanda, Freedom24,Funandtrvl, Gandigoo, Gary, GioCM, Gowish, GregRM, Gregalton, Haeinous, HenHei, Hoo man, Hu12, Investor123, Jc3, Jerryseinfeld, Jester7777, Jim whitson, Jtbandes, Kennethande, KurtShaped Box, Kuru, Kurykh, Lambiam, Lamro, Lartoven, Leastedrew, LilHelpa, Lobsterthermidor, Longhair, Lotje, Magioladitis, Mic, Mikeshultz, Mindmatrix, Mkeels, MountainSplash,MrOllie, Mrtrey99, Mschmidt224, Mydogategodshat, Nbarth, NeilN, Notinasnaid, OS2Warp, Officiallyover, Ohnoitsjamie, Patrick, Patstuart, Pdpinch, PhnomPencil, Physitsky, PoliticalJunkie,R'n'B, RJFJR, Radagast83, Rajesh acharya, Reach Out to the Truth, RichardVeryard, Robbiemorrison, Rossami, Roxyb, RoySiu06, Rrburke, Rtc, Ruhrfisch, Ryan0000, Sgeiger, Smallbones,Squids and Chips, Stand360, Stathisgould, SteinbDJ, SueHay, Sun Creator, The Anome, The Rambling Man, Thomas, Timesmagazine, Trappist the monk, Urbanrenewal, Vision3001, Vlad,Waggers, Westland, Wmessner, WojPob, Yeokaiwei, 197 ,زكريا anonymous edits

Valuation using multiples Source: http://en.wikipedia.org/w/index.php?oldid=619439520 Contributors: Black Swan01, Creet, Edward, EncMstr, Funandtrvl, Gregalton, Hmbr, Jeremy112233,Johnpseudo, Keepcool28, Klubell, Laterzii, Magioladitis, RkuipersNL, Saxbryn, SummerPhD, Tonywalton, Urbanrenewal, Zzuuzz, 47 anonymous edits

Image Sources, Licenses and Contributors 22

Image Sources, Licenses and ContributorsFile:Hauptbuch Hochstetter vor 1828.jpg Source: http://en.wikipedia.org/w/index.php?title=File:Hauptbuch_Hochstetter_vor_1828.jpg License: Public Domain Contributors: Photo: AndreasPraefckeFile:Portal-puzzle.svg Source: http://en.wikipedia.org/w/index.php?title=File:Portal-puzzle.svg License: Public Domain Contributors: AnomieFile:DCFM Calculator.JPG Source: http://en.wikipedia.org/w/index.php?title=File:DCFM_Calculator.JPG License: Attribution Contributors: Design and developed by Octávio Viana to ATMInvestor AssociationFile:ForMultiples.gif Source: http://en.wikipedia.org/w/index.php?title=File:ForMultiples.gif License: GNU Free Documentation License Contributors: RkuipersNLFile:MultiplesPDD.gif Source: http://en.wikipedia.org/w/index.php?title=File:MultiplesPDD.gif License: GNU Free Documentation License Contributors: RkuipersNL

License 23

LicenseCreative Commons Attribution-Share Alike 3.0//creativecommons.org/licenses/by-sa/3.0/