Basic Financial Reporting. A-IFRS Workshop

38

Basic Financial Reporting. A-IFRS Workshop

-

date post

21-Oct-2014 -

Category

Documents

-

view

1.767 -

download

5

description

Transcript of Basic Financial Reporting. A-IFRS Workshop

Basic Financial Reporting.

A-IFRS Workshop

Objectives

• Gain an understanding of the requirements of– AASB 101 Presentation of Financial Statements

– AASB 107 Cash Flow Statements

– FRD 110 Cash Flow Statements

– AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors

• Understand the requirements on initial adoption of A-IFRS

• Understand the key disclosure requirements

2 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

1. OverviewObjectives• Overview of scope and application of

AASB 101, AASB 107 and AASB 108• Requirements on initial adoption

Overview• AASB 101 “Presentation of Financial Statements”

– Supersedes:– AASB 1001/AAS 6 “Accounting Policies”– AASB 1014/AAS 23 “Set-Off and Extinguishment of Debt”– AASB 1018 “Statement of Financial Performance”– AASB 1034/AAS 37 “Financial Report Presentation and Disclosures”– AASB 1040/AAS 36 “Statement of Financial Position”

• AASB 107 “Cash Flow Statements”

• FRD 110 “Cash Flow Statements”– Supersedes AASB 1026 “Statement of Cash Flows”

• AASB 108 “Accounting Policies, Changes in Accounting Estimates and Errors”

– Supersedes AASB 1001 “Accounting Policies”

4 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

Overview

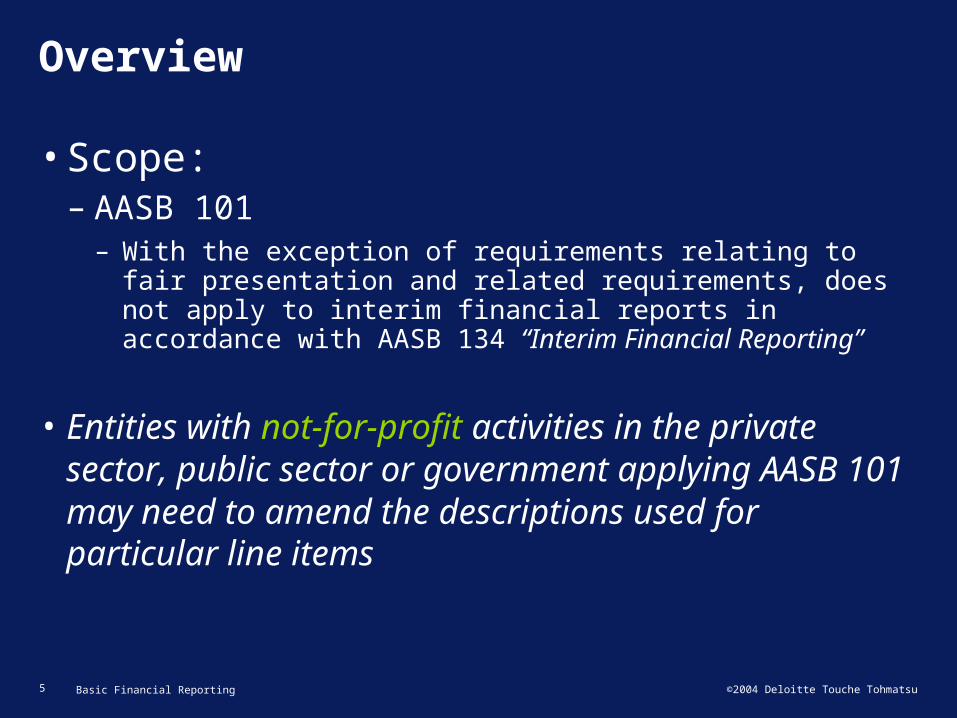

•Scope:– AASB 101

– With the exception of requirements relating to fair presentation and related requirements, does not apply to interim financial reports in accordance with AASB 134 “Interim Financial Reporting”

• Entities with not-for-profit activities in the private sector, public sector or government applying AASB 101 may need to amend the descriptions used for particular line items

5 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

Overview

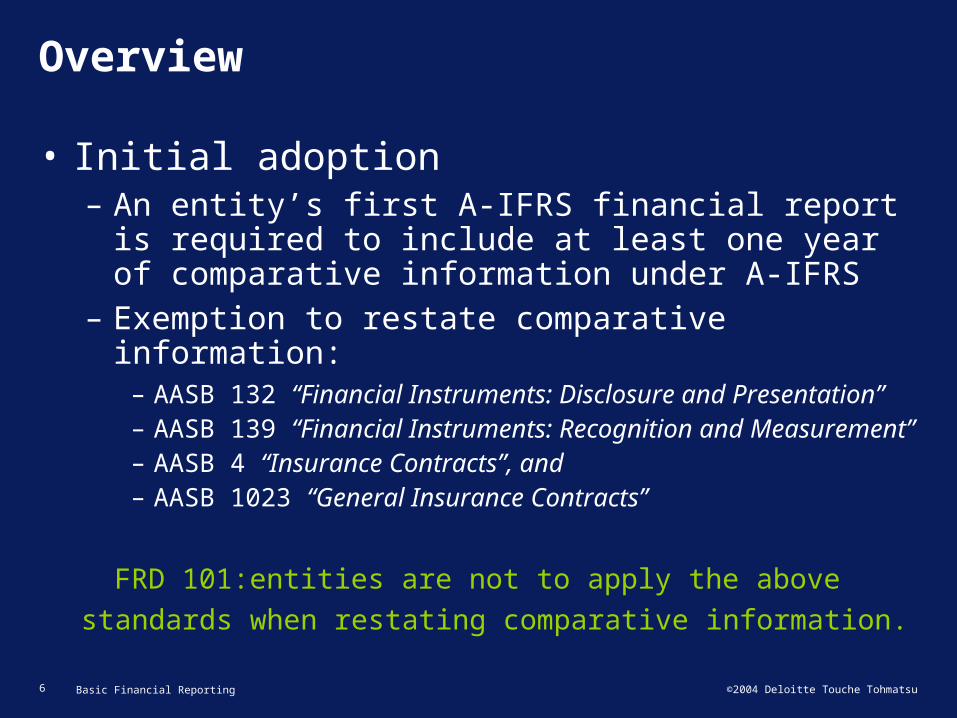

• Initial adoption– An entity’s first A-IFRS financial report is

required to include at least one year of comparative information under A-IFRS

– Exemption to restate comparative information:– AASB 132 “Financial Instruments: Disclosure and

Presentation”– AASB 139 “Financial Instruments: Recognition and

Measurement”– AASB 4 “Insurance Contracts”, and– AASB 1023 “General Insurance Contracts”

FRD 101:entities are not to apply the above standards when restating comparative information.

6 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

2. Overall Considerations

Objectives• Understand requirements to be

in compliance with A-IFRS

Fair presentation

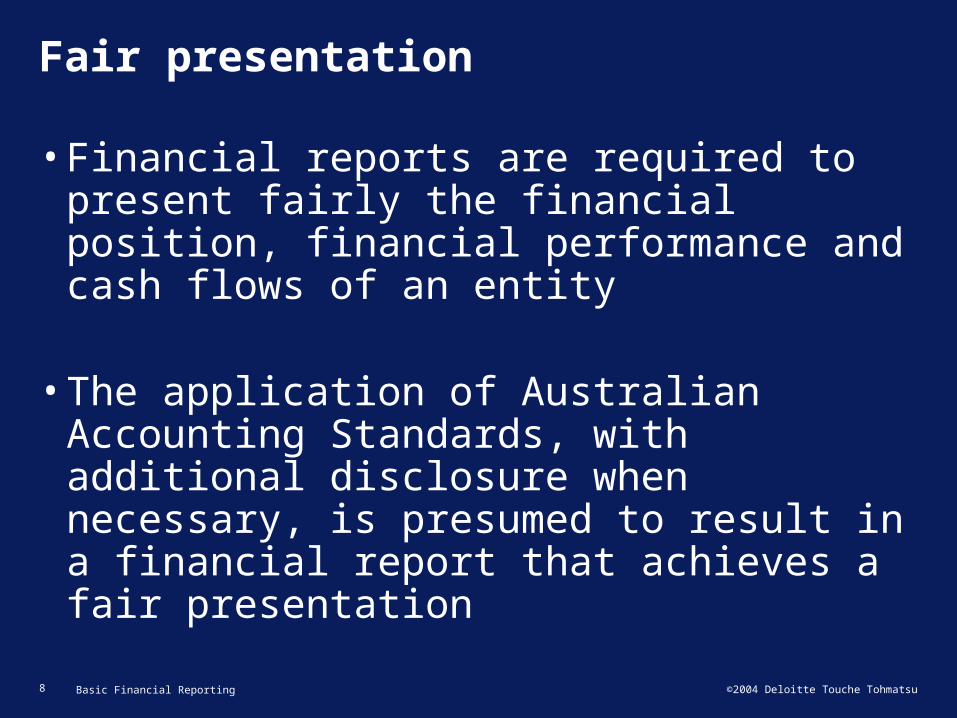

•Financial reports are required to present fairly the financial position, financial performance and cash flows of an entity

•The application of Australian Accounting

Standards, with additional disclosure when necessary, is presumed to result in a financial report that achieves a fair presentation

8 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

Compliance with Australian Accounting Standards

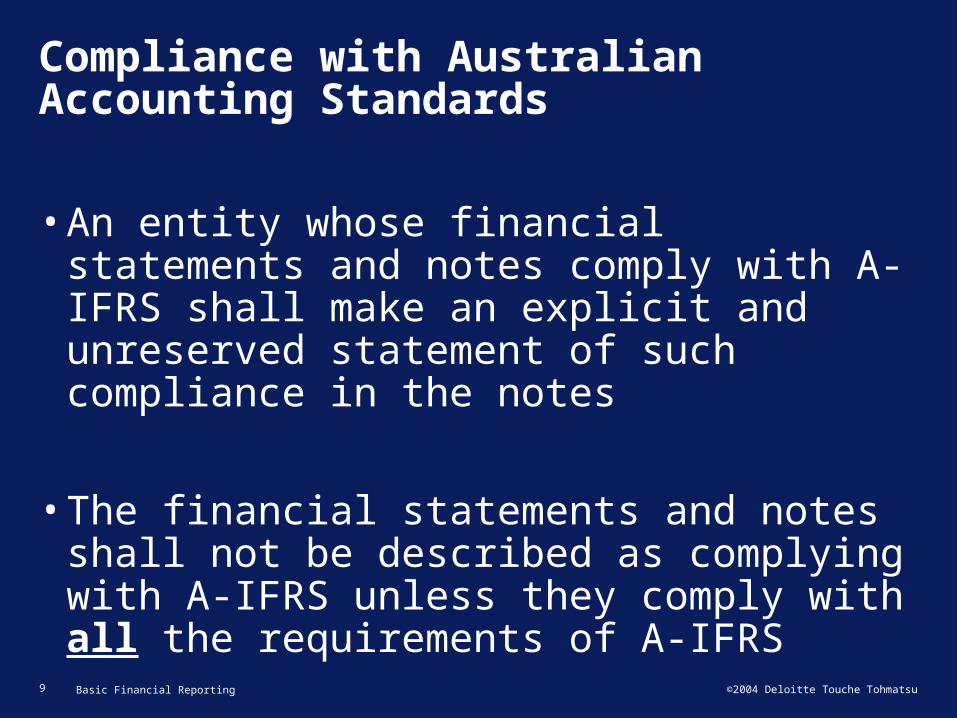

•An entity whose financial statements and notes comply with A-IFRS shall make an explicit and unreserved statement of such compliance in the notes

•The financial statements and notes shall not be described as complying with A-IFRS unless they comply with all the requirements of A-IFRS

9 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

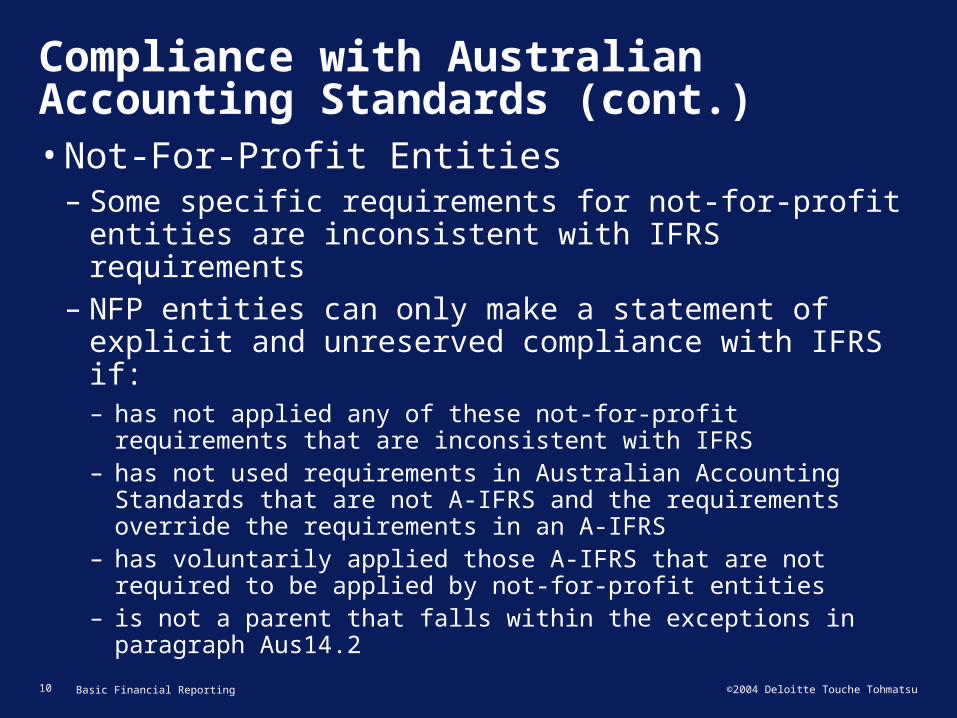

Compliance with Australian Accounting Standards (cont.)•Not-For-Profit Entities

– Some specific requirements for not-for-profit entities are inconsistent with IFRS requirements

– NFP entities can only make a statement of explicit and unreserved compliance with IFRS if:– has not applied any of these not‑for‑profit requirements

that are inconsistent with IFRS– has not used requirements in Australian Accounting

Standards that are not A-IFRS and the requirements override the requirements in an A-IFRS

– has voluntarily applied those A-IFRS that are not required to be applied by not‑for‑profit entities

– is not a parent that falls within the exceptions in paragraph Aus14.2

10 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

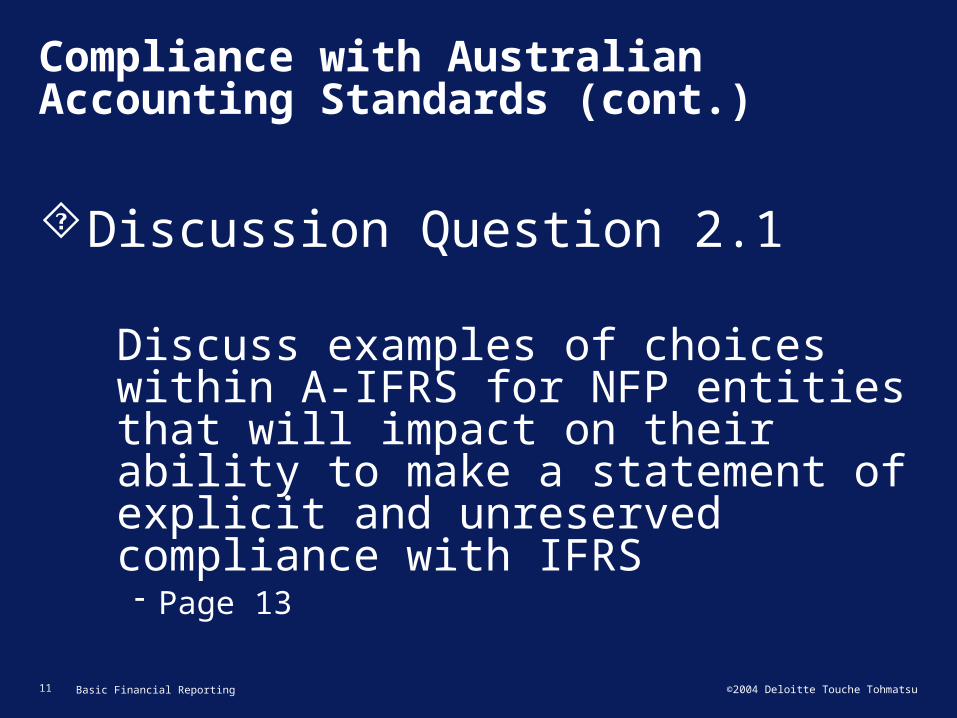

Compliance with Australian Accounting Standards (cont.)

Discussion Question 2.1

Discuss examples of choices within A-IFRS for NFP entities that will impact on their ability to make a statement of explicit and unreserved compliance with IFRS Page 13

11 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

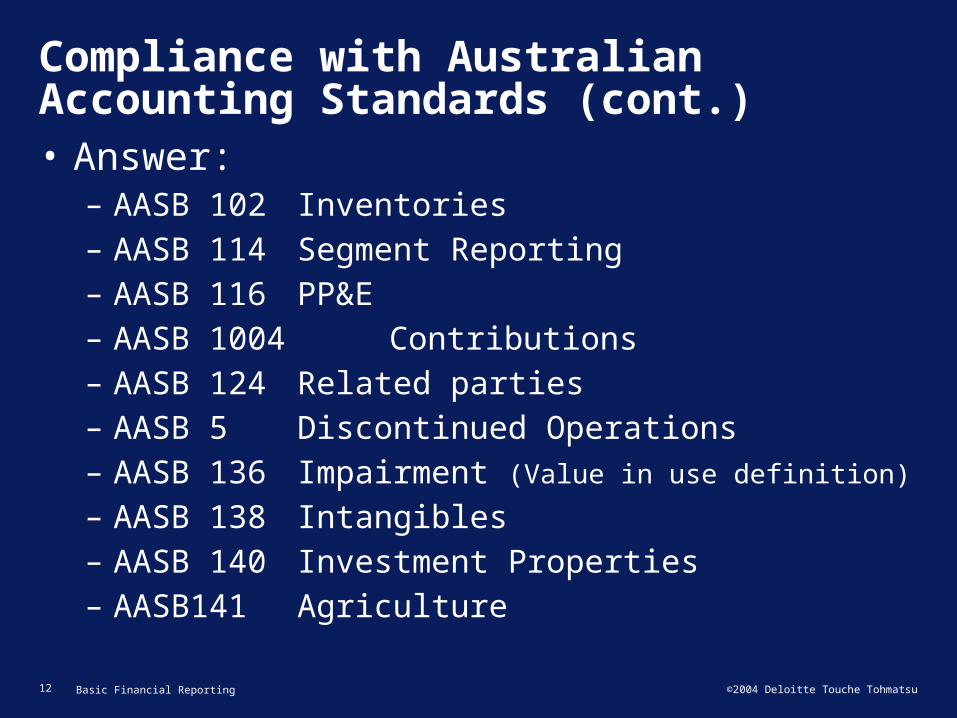

Compliance with Australian Accounting Standards (cont.)• Answer:

– AASB 102 Inventories– AASB 114 Segment Reporting– AASB 116 PP&E– AASB 1004 Contributions– AASB 124 Related parties– AASB 5 Discontinued Operations– AASB 136 Impairment (Value in use definition)

– AASB 138 Intangibles– AASB 140 Investment Properties– AASB141 Agriculture

12 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

Compliance with Australian Accounting Standards (cont.)

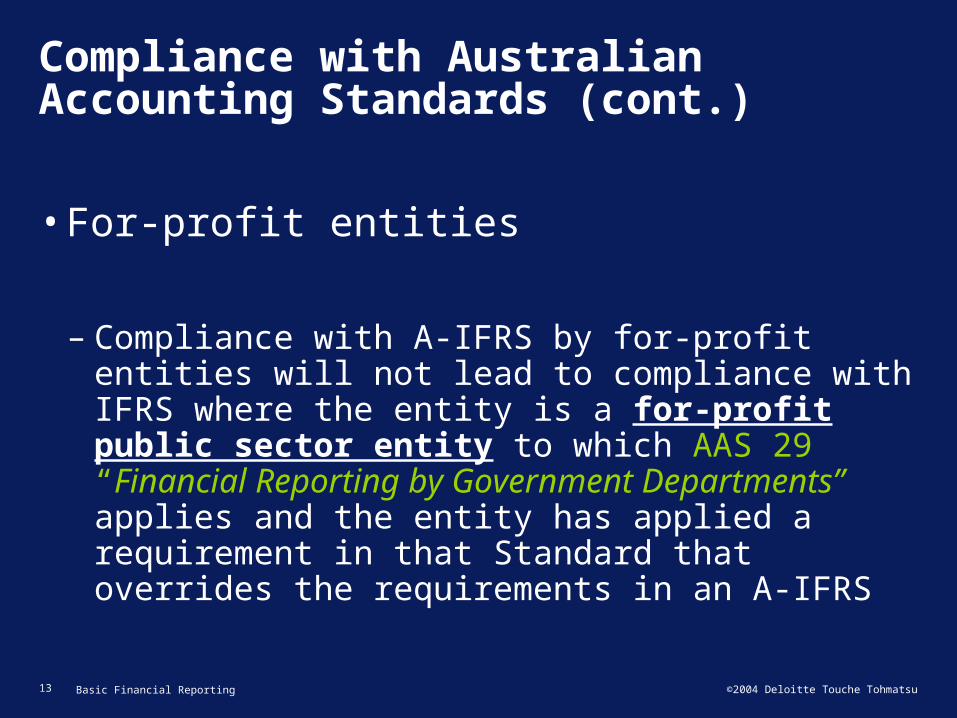

•For-profit entities

– Compliance with A-IFRS by for‑profit entities will not lead to compliance with IFRS where the entity is a for‑profit public sector entity to which AAS 29 “Financial Reporting by Government Departments” applies and the entity has applied a requirement in that Standard that overrides the requirements in an A-IFRS

13 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

3. Structure and Content of Financial Statements

Objectives• Be aware of information required to be

presented on the face of the statements• Understand the option to present

information either on the face or in the notes

• Understand AASB 107 requirements

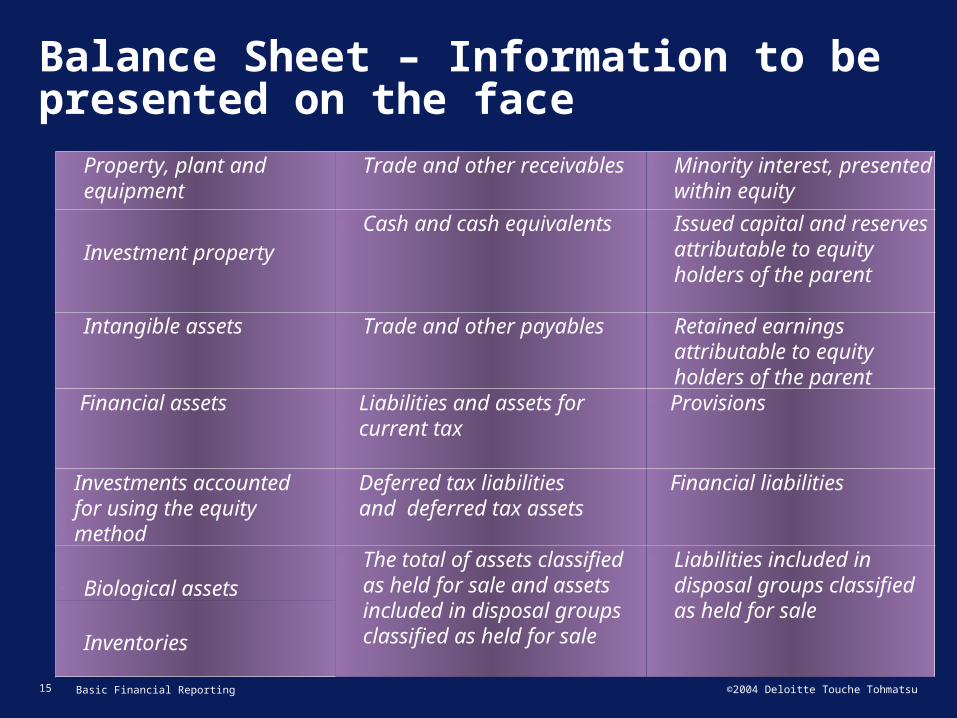

Balance Sheet – Information to be presented on the face

• Property, plant and equipment

• Trade and other receivables

• Minority interest, presented within equity

• Investment property• Cash and cash

equivalents• Issued capital and

reserves attributable to equity holders of the parent

• Intangible assets • Trade and other payables • Retained earnings attributable to equity holders of the parent

• Financial assets • Liabilities and assets for • current tax

• Provisions

• Investments accounted• for using the equity • method

• Deferred tax liabilities • and deferred tax assets

• Financial liabilities

• Biological assets• The total of assets

classified as held for sale and assets included in disposal groups classified as held for sale

• Liabilities included in disposal groups classified as held for sale• Inventories

15 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

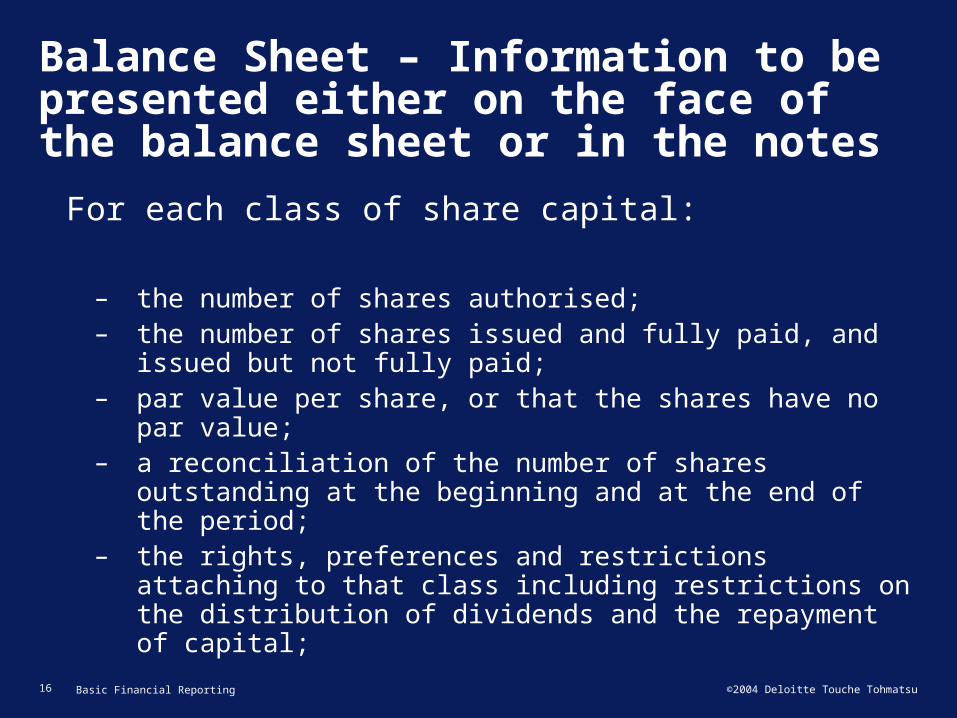

Balance Sheet – Information to be presented either on the face of the balance sheet or in the notes

For each class of share capital:

– the number of shares authorised;– the number of shares issued and fully paid, and issued

but not fully paid;– par value per share, or that the shares have no par value;– a reconciliation of the number of shares outstanding at

the beginning and at the end of the period;– the rights, preferences and restrictions attaching to that

class including restrictions on the distribution of dividends and the repayment of capital;

16 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

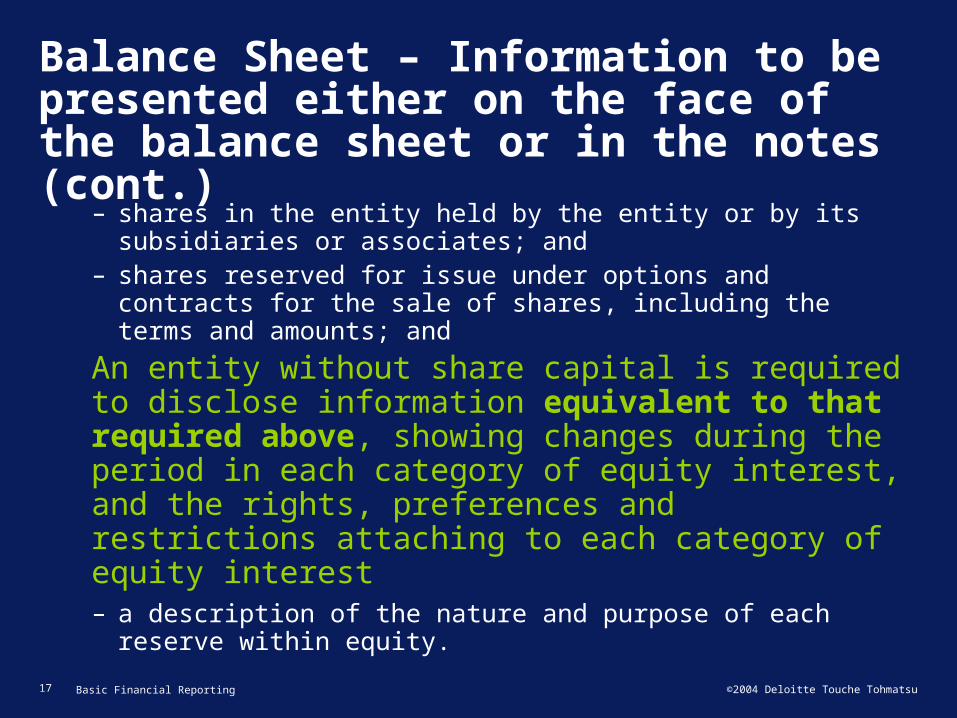

Balance Sheet – Information to be presented either on the face of the balance sheet or in the notes (cont.)

– shares in the entity held by the entity or by its subsidiaries or associates; and

– shares reserved for issue under options and contracts for the sale of shares, including the terms and amounts; and

An entity without share capital is required to disclose information equivalent to that required above, showing changes during the period in each category of equity interest, and the rights, preferences and restrictions attaching to each category of equity interest– a description of the nature and purpose of each reserve

within equity.

17 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

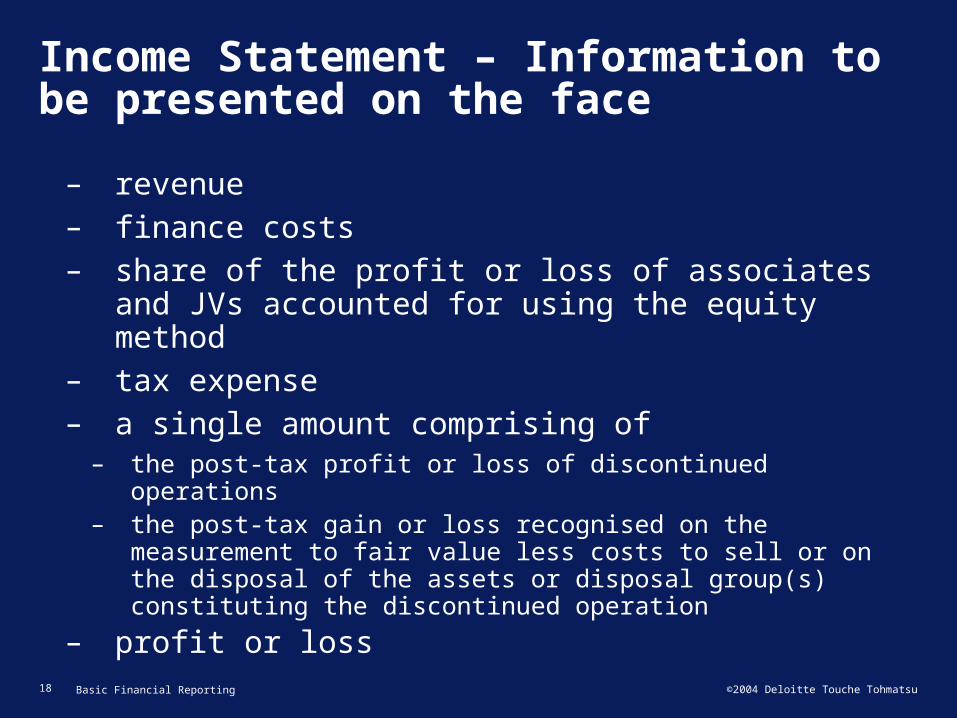

Income Statement – Information to be presented on the face

– revenue– finance costs– share of the profit or loss of associates and JVs

accounted for using the equity method– tax expense– a single amount comprising of

– the post‑tax profit or loss of discontinued operations– the post‑tax gain or loss recognised on the measurement

to fair value less costs to sell or on the disposal of the assets or disposal group(s) constituting the discontinued operation

– profit or loss

18 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

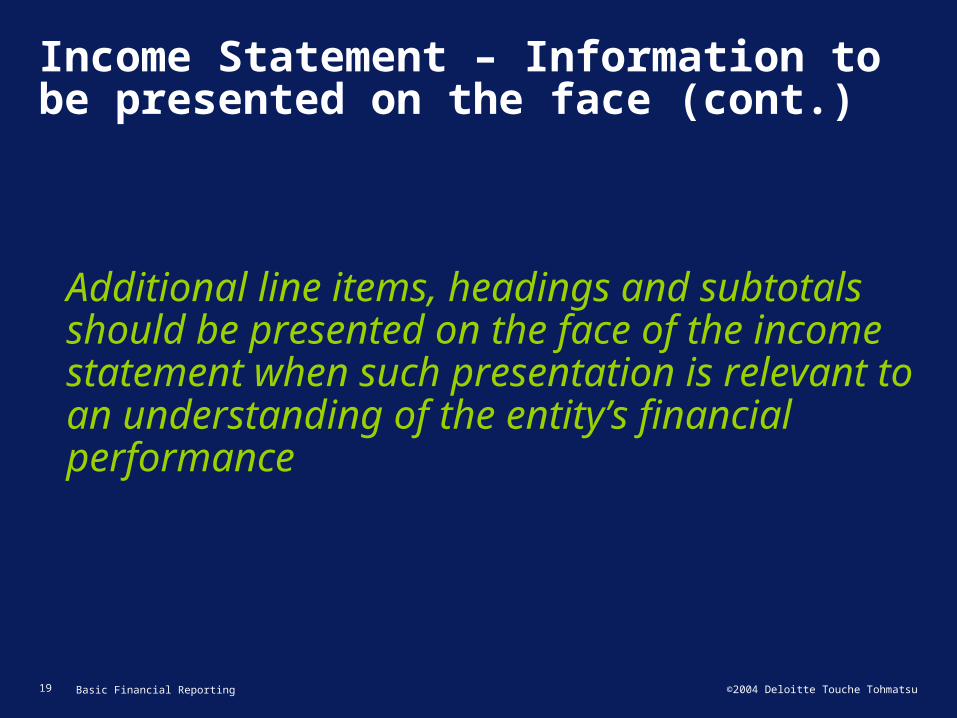

Income Statement – Information to be presented on the face (cont.)

Additional line items, headings and subtotals should be presented on the face of the income statement when such presentation is relevant to an understanding of the entity’s financial performance

19 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

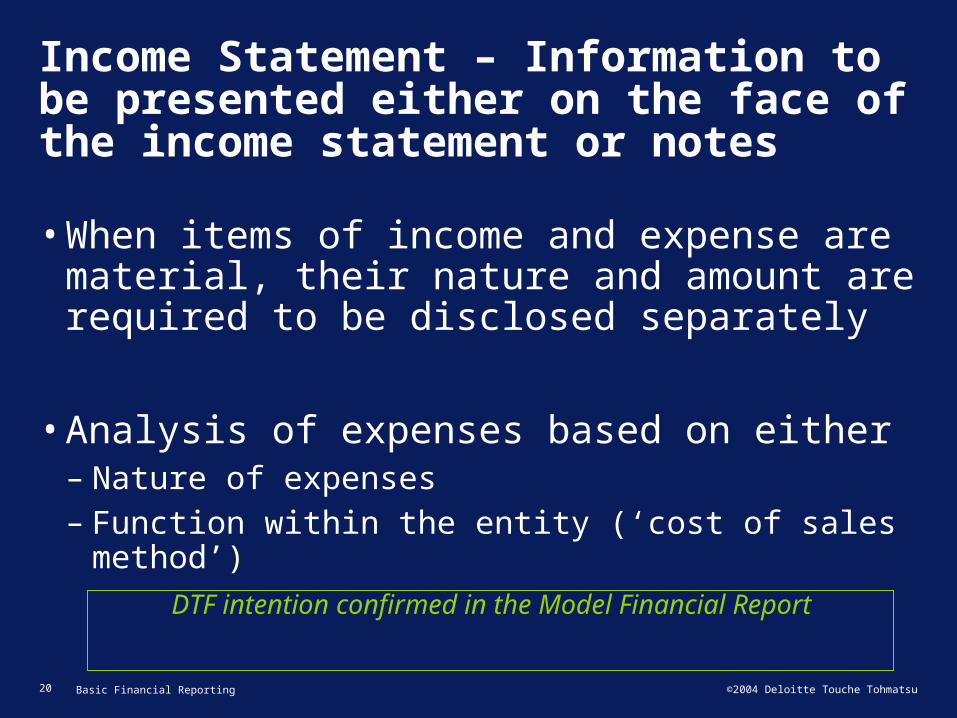

Income Statement – Information to be presented either on the face of the income statement or notes

•When items of income and expense are material, their nature and amount are required to be disclosed separately

•Analysis of expenses based on either– Nature of expenses– Function within the entity (‘cost of sales

method’)DTF intention confirmed in the Model Financial Report

20 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

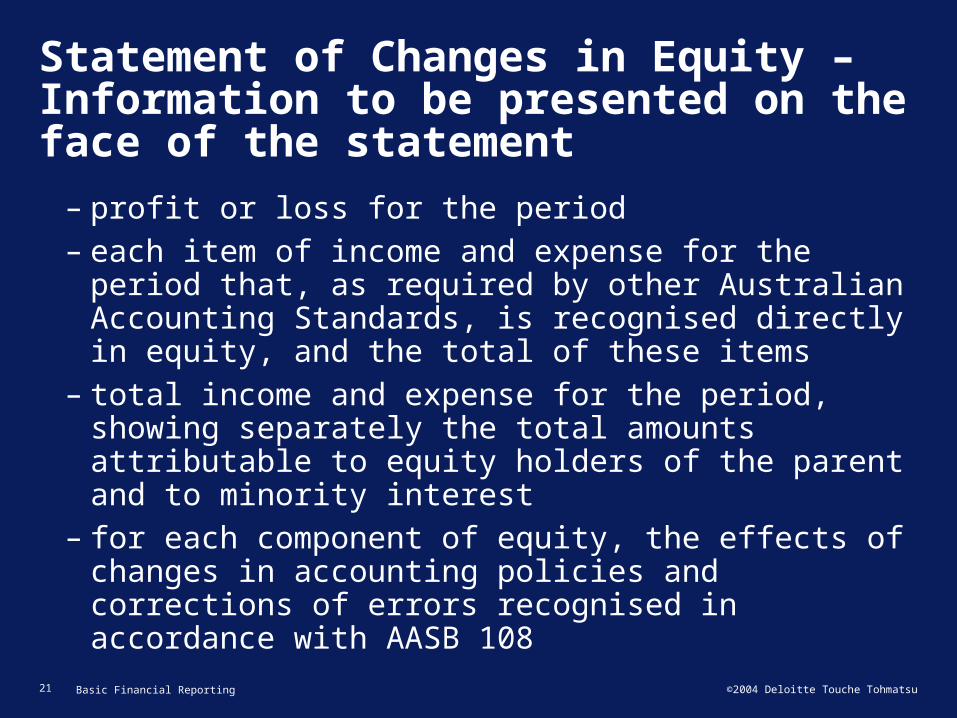

Statement of Changes in Equity – Information to be presented on the face of the statement

– profit or loss for the period– each item of income and expense for the period

that, as required by other Australian Accounting Standards, is recognised directly in equity, and the total of these items

– total income and expense for the period, showing separately the total amounts attributable to equity holders of the parent and to minority interest

– for each component of equity, the effects of changes in accounting policies and corrections of errors recognised in accordance with AASB 108

21 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

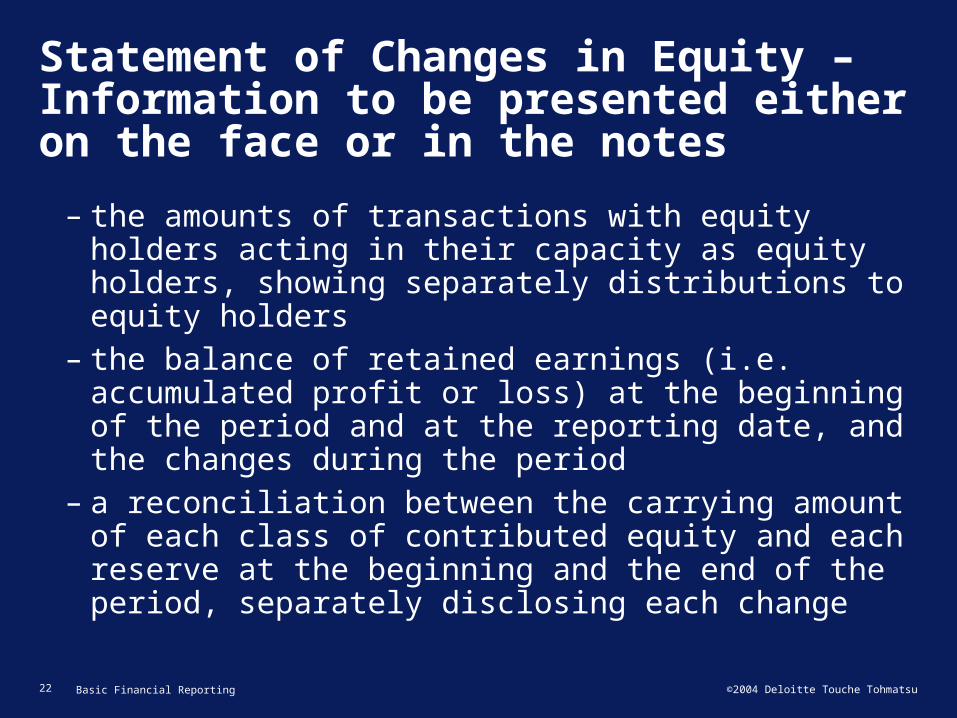

Statement of Changes in Equity – Information to be presented either on the face or in the notes

– the amounts of transactions with equity holders acting in their capacity as equity holders, showing separately distributions to equity holders

– the balance of retained earnings (i.e. accumulated profit or loss) at the beginning of the period and at the reporting date, and the changes during the period

– a reconciliation between the carrying amount of each class of contributed equity and each reserve at the beginning and the end of the period, separately disclosing each change

22 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

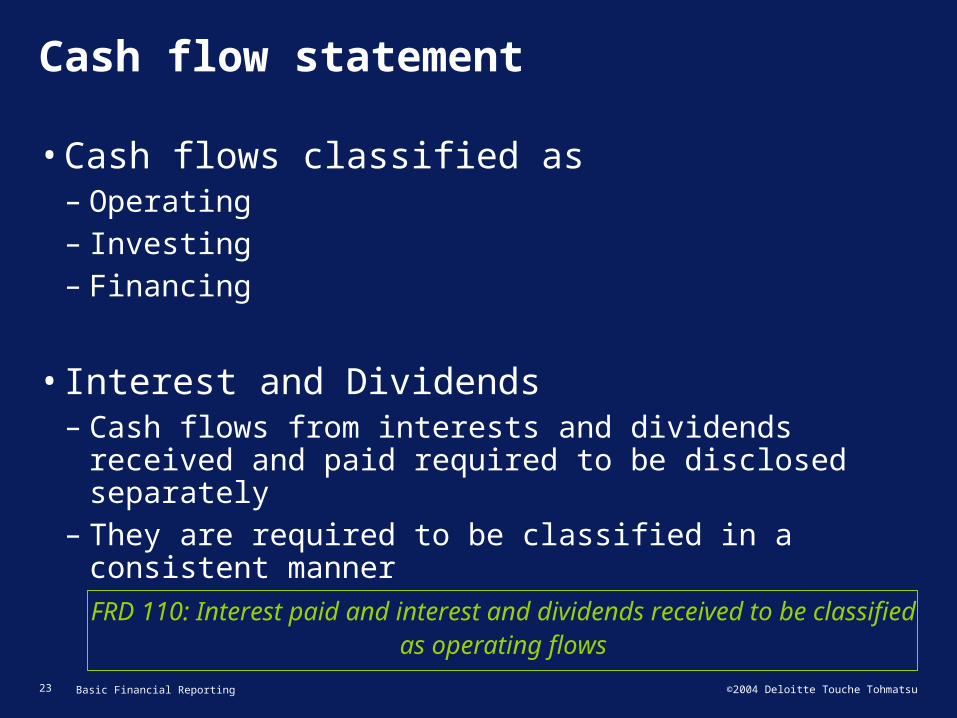

Cash flow statement

•Cash flows classified as– Operating– Investing– Financing

•Interest and Dividends– Cash flows from interests and dividends received

and paid required to be disclosed separately– They are required to be classified in a consistent

mannerFRD 110: Interest paid and interest and dividends

received to be classified as operating flows23 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

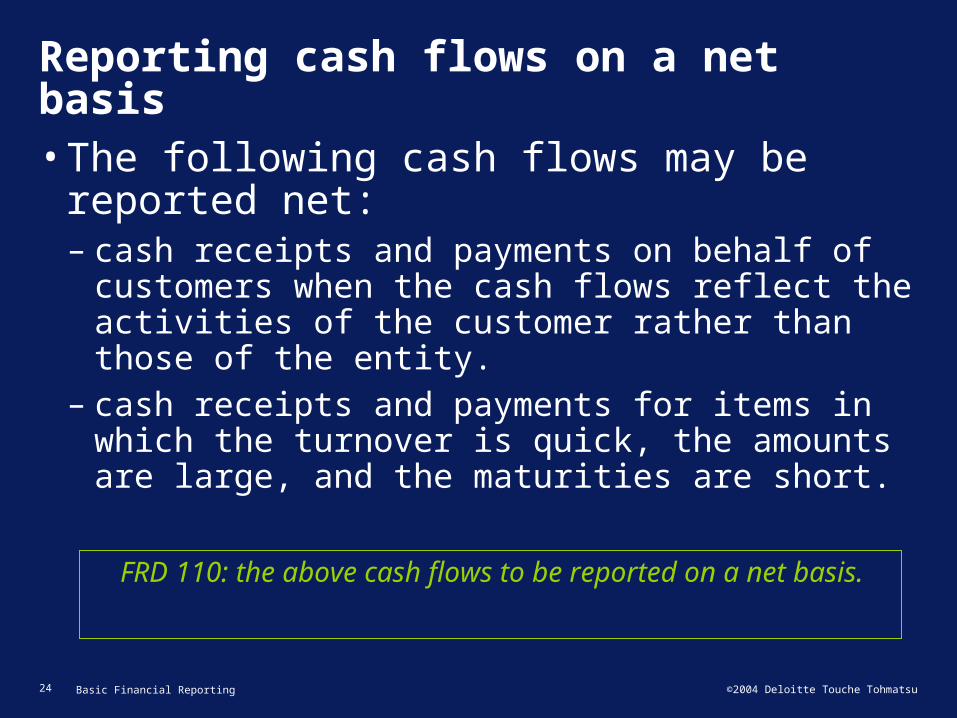

Reporting cash flows on a net basis

•The following cash flows may be reported net:– cash receipts and payments on behalf of

customers when the cash flows reflect the activities of the customer rather than those of the entity.

– cash receipts and payments for items in which the turnover is quick, the amounts are large, and the maturities are short.

FRD 110: the above cash flows to be reported on a net basis.

24 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

4. Accounting Policies, Changes in Accounting Estimates and Errors

Objectives• Understand criteria for selecting

and changing accounting policies• Understand accounting treatment

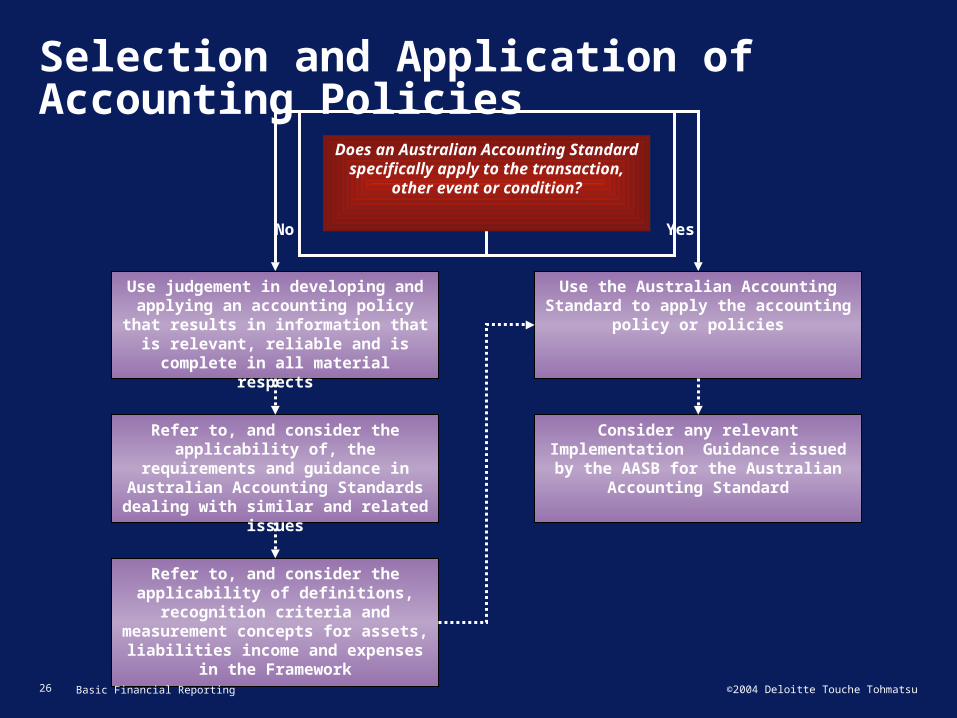

Selection and Application of Accounting Policies

Use judgement in developing and applying an accounting policy

that results in information that is relevant, reliable and is complete

in all material respects

YesNo

Does an Australian Accounting Standard specifically apply to the

transaction, other event or condition?

Refer to, and consider the applicability of, the requirements

and guidance in Australian Accounting Standards dealing with similar and related issues

Refer to, and consider the applicability of definitions,

recognition criteria and measurement concepts for

assets, liabilities income and expenses in the Framework

Use the Australian Accounting Standard to apply the accounting

policy or policies

Consider any relevant Implementation Guidance issued

by the AASB for the Australian Accounting Standard

26 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

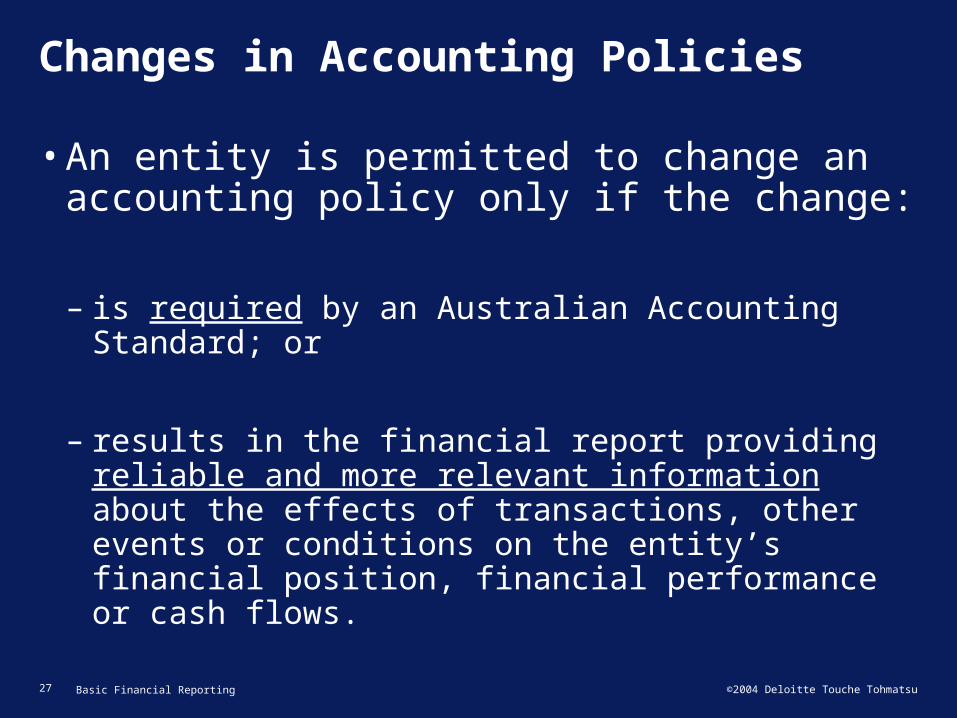

Changes in Accounting Policies

•An entity is permitted to change an accounting policy only if the change:

– is required by an Australian Accounting Standard; or

– results in the financial report providing reliable and more relevant information about the effects of transactions, other events or conditions on the entity’s financial position, financial performance or cash flows.

27 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

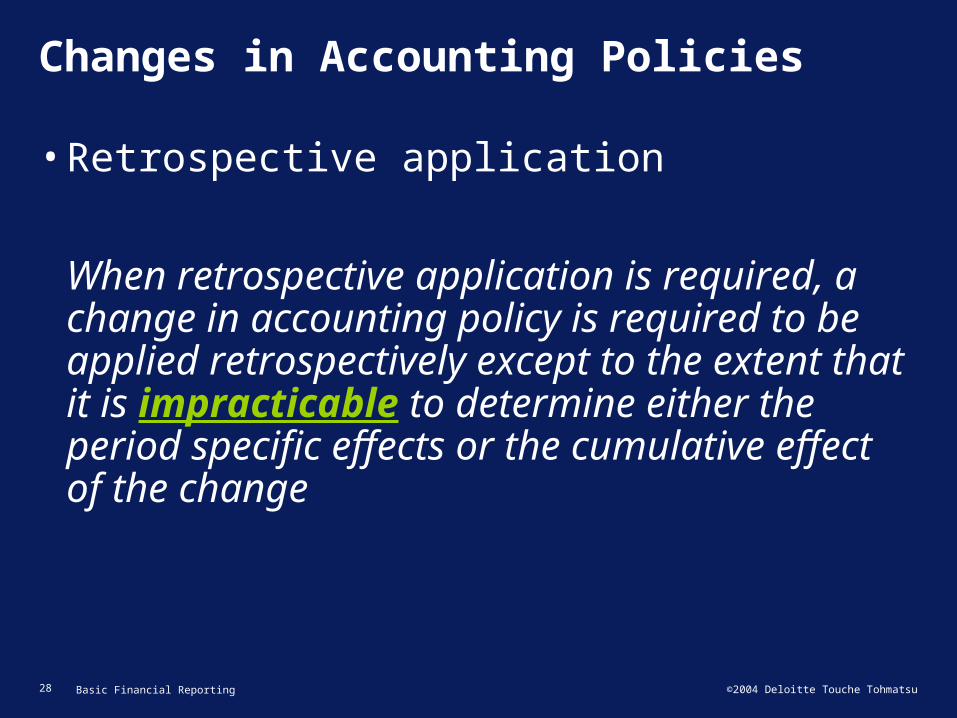

Changes in Accounting Policies

•Retrospective application

When retrospective application is required, a change in accounting policy is required to be applied retrospectively except to the extent that it is impracticable to determine either the period specific effects or the cumulative effect of the change

28 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

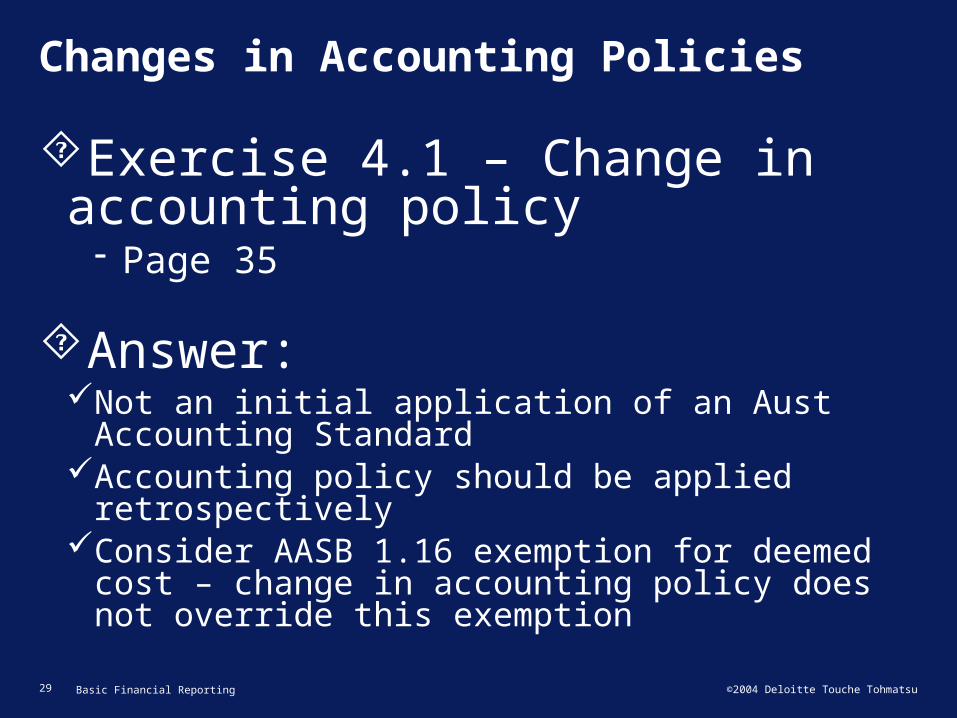

Changes in Accounting Policies

Exercise 4.1 – Change in accounting policy

Page 35

Answer:Not an initial application of an Aust Accounting

StandardAccounting policy should be applied

retrospectivelyConsider AASB 1.16 exemption for deemed cost

– change in accounting policy does not override this exemption

29 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

Changes in Accounting Estimates

•The effect of a change in an accounting estimate is required to be recognised prospectively by including it in profit or loss in:– the period of the change, if the change affects

that period only; or– the period of the change and future periods, if

the change affects both

30 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

Changes in Accounting Estimates

Discussion Question 4.1 – Change in accounting estimate

Page 36

Answer:Yes – even though the original estimate of the

outcome was made several years ago, and the case may continue for an additional year, or more, the change in the estimate of the outcome should be charged to the income statement in the year of the change.

31 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

Errors

•Material prior period errors to be corrected retrospectively in the first financial report authorised for issue after their discovery by:– restating the comparative amounts for the prior

period(s) presented in which the error occurred; or

– if the error occurred before the earliest prior period presented, restating the opening balances of assets, liabilities and equity for the earliest prior period presented

32 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

Errors (cont.)

•Limitations on retrospective restatement– Not required to be corrected when it is

impracticable to determine either the period-specific effects or the cumulative effect of the error

33 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

Errors (Cont.)

– When it is impracticable to determine the period-specific effects of an error on comparative information for one or more prior periods presented, the entity is required to restate the opening balances of assets, liabilities and equity for the earliest period for which retrospective restatement is practicable (which may be the current period)

34 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

Errors (Cont.)

– When it is impracticable to determine the cumulative effect, at the beginning of the current period, of an error on all prior periods, the entity is required to restate the comparative information to correct the error prospectively from the earliest date practicable

35 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

Workshop summary

Summary

Points to note – basic financial reporting:

- Financial statements change- Extraordinary items prohibited- Classification of current-non-current liabilities - No distinction between errors and fundamental

errors

37 Basic Financial Reporting ©2004 Deloitte Touche Tohmatsu

Deloitte Touche Tohmatsu is an organization of member firms devoted to excellence in providing professional services and advice. We are focused on client service through a global strategy executed

locally in nearly 150 countries. With access to the deep intellectual capital of 120,000 people worldwide, our member firms, including their affiliates, deliver services in four professional areas: audit, tax,

consulting, and financial advisory. Our member firms serve more than one-half of the world’s largest companies, as well as large national enterprises, public institutions, locally important clients, and

successful, fast-growing global companies. For regulatory and other reasons, certain member firms do not provide services in all four professional areas.

This document has been prepared as a general guide to the matters covered. It is not possible to cover all the situations that may be encountered in practice and, in addition, readers may have alternative

solutions to some of the questions raised and answers offered. Accordingly, this document should not be viewed as a substitute for detailed reading of the associated accounting pronouncements or professional advice on specific matters of concern. Whilst every effort has been made to ensure that the information

contained in this document is accurate, neither Deloitte Touche Tohmatsu nor any of its partners, directors, principles, consultants or employees shall be liable to any party in respect of decisions or

actions taken as a result of using the information in this document.

Copyright © Deloitte Touche Tohmatsu 2004. No part of this document may be reproduced, stored, transmitted in any form or by any means without the prior written permission of Deloitte Touche Tohmatsu.

The liability of Deloitte Touche Tohmatsu is limited by, and to the extent of, the Accountant’s Scheme under the Professional Standards Act 1994 (NSW).

Deloitte Touche Tohmatsu