Báo cáo tổng hợp

18

1 General Information Contact name SAIGON THUONG TIN COMMERCIAL JOINT STOCK BANK Head office 266-268 Nam Ky Khoi Nghia Street, Ward 8, District 3, Hochiminh City (HCMC), Vietnam Tel: (84 8) 39 320 420 – Fax: (84 8) 39 320 424 Website: www.sacombank.com.vn Chartered Capital VND 10,740,230,130,000 (as at 31 December 2011) SWIFT code SGTTVNVX Number of Employees 9,607 employees (as of 31 December 2011) 1. Establishment and development SAIGON THUONG TIN COMMERCIAL JOINT STOCK BANK (Sacombank) was established under Decision No. 05/GP-UB dated on 03/01/1992 of People's Committee of Hochiminh city and operated by Decision No.0006/NH-GP dated 05/12/1991 of The State Bank of Vietnam. Sacombank officially went into operation on 21.12.1991, it was established through the merger of Go Vap Economic Development Bank and three community credit institutions: Tan Binh, Thanh Cong and Lu Gia. Sacombank was among the first joint stock banks incorporated in Ho Chi Minh City. Period 1991-1995, Sacombank is one of the first joint stock banks in Hochiminh city. It started with initial capital of only VND3 billion. The active network located mainly in the suburban districts and the business scope is very small. Sacombank has made a remarkable point in the first year through policy decisions, guidelines such as focus on handling bad debts; expand its network, the issuance of debentures, made quick money transfer service. In 1993, Sacombank opened its branch office in Hanoi. It was the first bank to provide

Transcript of Báo cáo tổng hợp

1

General Information

Contact name

SAIGON THUONG TIN COMMERCIAL JOINT STOCK BANK

Head office

266-268 Nam Ky Khoi Nghia Street, Ward 8, District 3,

Hochiminh City (HCMC), Vietnam

Tel: (84 8) 39 320 420 – Fax: (84 8) 39 320 424

Website: www.sacombank.com.vn

Chartered Capital

VND 10,740,230,130,000 (as at 31 December 2011)

SWIFT code

SGTTVNVX

Number of Employees

9,607 employees (as of 31 December 2011)

1. Establishment and development

SAIGON THUONG TIN COMMERCIAL JOINT STOCK BANK

(Sacombank) was established under Decision No. 05/GP-UB dated on

03/01/1992 of People's Committee of Hochiminh city and operated by Decision

No.0006/NH-GP dated 05/12/1991 of The State Bank of Vietnam. Sacombank

officially went into operation on 21.12.1991, it was established through the

merger of Go Vap Economic Development Bank and three community credit

institutions: Tan Binh, Thanh Cong and Lu Gia. Sacombank was among the

first joint stock banks incorporated in Ho Chi Minh City.

Period 1991-1995, Sacombank is one of the first joint stock banks in

Hochiminh city. It started with initial capital of only VND3 billion. The active

network located mainly in the suburban districts and the business scope is very

small. Sacombank has made a remarkable point in the first year through policy

decisions, guidelines such as focus on handling bad debts; expand its network,

the issuance of debentures, made quick money transfer service. In 1993,

Sacombank opened its branch office in Hanoi. It was the first bank to provide

2

express remittance service between Hanoi and HCMC. The service has greatly

reduced physical cash transactions between the two Vietnam’s largest cities.

Period 1995-1998, Sacombank focused on the task of planning and

developing. In parallel, the bank continued to strengthen and reorganize. With

innovative public issue of shares, Sacombank's capital has increased from

VND23 billion to VND71 billion, which was initially established financial

capacity for the development of the bank.

Period 1999 - 2001, capital increased from VND71 billion to VND190

billion. In 1999, Sacombank inaugurated its Head Office at 278 Nam Ky Khoi

Nghia, District 3, HCMC. While upgrading the branch office under the

expanding network more than 20 provinces and major economic areas, and

established relationships with more than 80 foreign bank branches around the

world. Meanwhile, Sacombank became a member of the Association of

Telecommunications Contact Global Bank (SWIFT), Visa and Master Card.

Period 2001 - 2005, accomplished the economic development goals set

for 5-year planning period. Especially with the capital contribution of 03

foreign shareholders are financial institutions - the world's strongest banks and

factoring sector has access to support advanced technology and management

experience operating modern prepared for the process of international

economic integration. At the same time, the Bank initially successful model

developed joint ventures through capital contribution to establish joint venture

fund management - securities companies - insurance companies.

Period 2006-2010, Sacombank channels its efforts on improving

operational efficiency, management capacity upgrading, resolving inadequacies

and improving the bank’s adaptability and competitiveness. In 2006,

Sacombank is the first Vietnamese bank to be listed on the HOSE with a

chartered capital of VND1,900 billion. Year 2009 is a memorable year to

Sacombank with many milestones. In May, Sacombank was rated a “gold”

stock by the financial market. It has been a blue-chip since listing on the HOSE

and has attracted many local and foreign investors. In June, a branch was

opened in Phnom Penh. The bank achieved its aim of expanding into Indochina

3

to support cross border enterprises of Vietnam, Laos, and Cambodia. After that,

in September, the bank upgraded the core banking system from Smartbank to

T24 R8 in all its transaction offices. In 2010, Sacombank has successfully

completed all 2001-2010 targets, with a growth rate of 64% per year. Building

a firm foundation while making necessary changes in the restructuring process,

The Bank is now taking actions to achieve the 2011 - 2020 targets.

After more than 20 years of operation, Sacombank becomes one of the

biggest joint-stock commercial bank in Vietnam with the Chartered Capital up

from VND190 billion in 2001 to VND10,740 billion in 12/2011. The network

with over 408 branches and transaction offices spread from north to south, the

staff of 9,607 people (12/2011), and relations with over 9700 agents of 250

banks in 91 countries around the world. Sacombank is also a joint stock bank

with the mass number of shareholders in Vietnam with over 74,130

shareholders, the shareholders of the factoring strategy is the financial group

and largest bank in the world such as:

Dragon Financial Holdings of Britain

International Financial Company (IFC) under the World Bank

Group Australia and New Zealand Bank (ANZ)

Along with these achievements, Sacombank aims to become a retail

bank versatile - modern - the best of Vietnam and large scale regional.

4

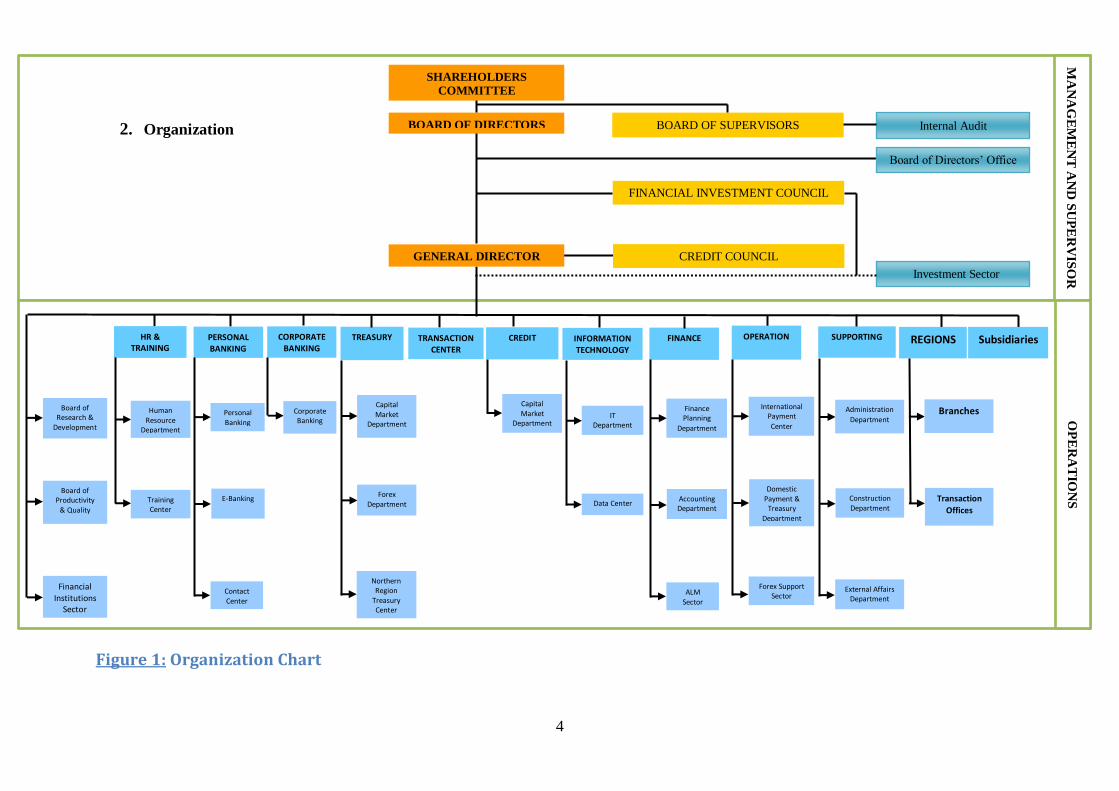

2. Organization

Figure 1: Organization Chart

HR & TRAINING

Human Resource

Department

Training Center

Board of Research &

Development

Board of Productivity

& Quality

Financial Institutions

Sector

PERSONAL BANKING

Personal Banking

E-Banking

Contact Center

CORPORATE BANKING

Corporate Banking

SHAREHOLDERS

COMMITTEE

BOARD OF DIRECTORS BOARD OF SUPERVISORS

FINANCIAL INVESTMENT COUNCIL

CREDIT COUNCIL GENERAL DIRECTOR

Board of Directors’ Office

Internal Audit

Investment Sector

TREASURY

Capital Market

Department

Forex Department

Northern Region

Treasury Center

TRANSACTION CENTER

CREDIT

Capital Market

Department

INFORMATION TECHNOLOGY

IT Department

Data Center

FINANCE

Finance Planning

Department

Accounting Department

ALM Sector

OPERATION

International Payment

Center

Domestic Payment &

Treasury Department

Forex Support Sector

REGIONS

Branches

Transaction

Offices

Subsidiaries SUPPORTING

Administration

Department

Construction Department

External Affairs Department

MA

NA

GE

ME

NT

AN

D S

UP

ER

VIS

OR

O

PE

RA

TIO

NS

5

3. Human Resources

By late 2011, Sacombank has a total of 9,607 employees. Despite a tight

labor market, the human resource capacity was enhanced with consistent staff

training and development, competitive remuneration, good management practices

and a professional working environment. Staff training was provided on an average

of two times per employee per year. The approaches of self-learning, on-the-job

training and distant learning were provided. The banks saw continual improve its

staff quality and have met human resource development requirements.

To be one of the best workplaces in Vietnam, Sacombank adopts the

workforce development objective of building a professional, modern and

stimulating work environment to attract, manage, retail and nurture talent”. To

improve its human resource management, Sacombank has developed a range of

initiatives based on:

1. Findings from an internal analysis of strengths and weaknesses of its

existing talents;

2. Opportunities and threats of the banking industry, arising from existing

and potential domestic and socio-economic conditions;

3. Bank’s strategic direction of its human resources; and

4. Organizational culture and staff welfare.

Besides maintaining a competitive compensation scheme and promoting

Sacombank’s brand in the labor market, the Human Resources Department (HRD)

has also established collaboration with universities and colleges in Ho Chi Minh

City for direct recruitment and internships for students. Sacombank is able to

formulate human resource policies, which not only increase the number of staff for

its growth but also create jobs for fresh graduates. From early 2011, Sacombank

strengthened its cooperation with universities by conducting recruitment exercises,

training programs, scientific research programs, site visits, provision of part-time

jobs for students, as well as providing banking services for students.

6

In 2010, Sacombank launched the Potential Trainee Program targeted at

senior students at universities and colleges in Ho Chi Minh City. Interns were

selected and assigned specific job functions that were based on the interns’ specific

potential. The interns will complete their graduation thesis as stipulated during the

internship. All internship-related expenses were covered by the bank. Upon

completion of the internship, trainees who have exhibited good performance were

employed to work at the branches where they interned. The Potential Trainee

Program received very favorable response from the branch network and also

captured the attention of the students in Ho Chi Minh City. In 2011, despite the

implementation of a more stringent selection process (comprising of qualifying tests

and interview), the Potential Trainee Program attracted 10,500 applicants, of which

880 were short-listed and 400 students were selected.

The bank also developed the Golden Idea program that awards employees

who demonstrated creativity and innovation. Notably, Sacombank conducted an on-

line employee satisfaction survey for the first time. The survey gathered opinions

and feedback of almost 5,000 Sacombank employees on improving staff policies.

In parallel, Sacombank also gave outstanding performance and long-service

awards. Medals were awarded to staff who served more than 10 years. It also

honors Sacombank talents in the Golden Book.

4. Scope of Operations

Sacombank is allowed to conduct:

Deposit taking, receiving foreign capital, funding business capital

requirements;

Local and international payments, transactions, and funds transfers;

Trading and investing in gold, foreign currency, and securities;

Other services offered by foreign banks in line with those allowed by the

State Bank of Vietnam.

7

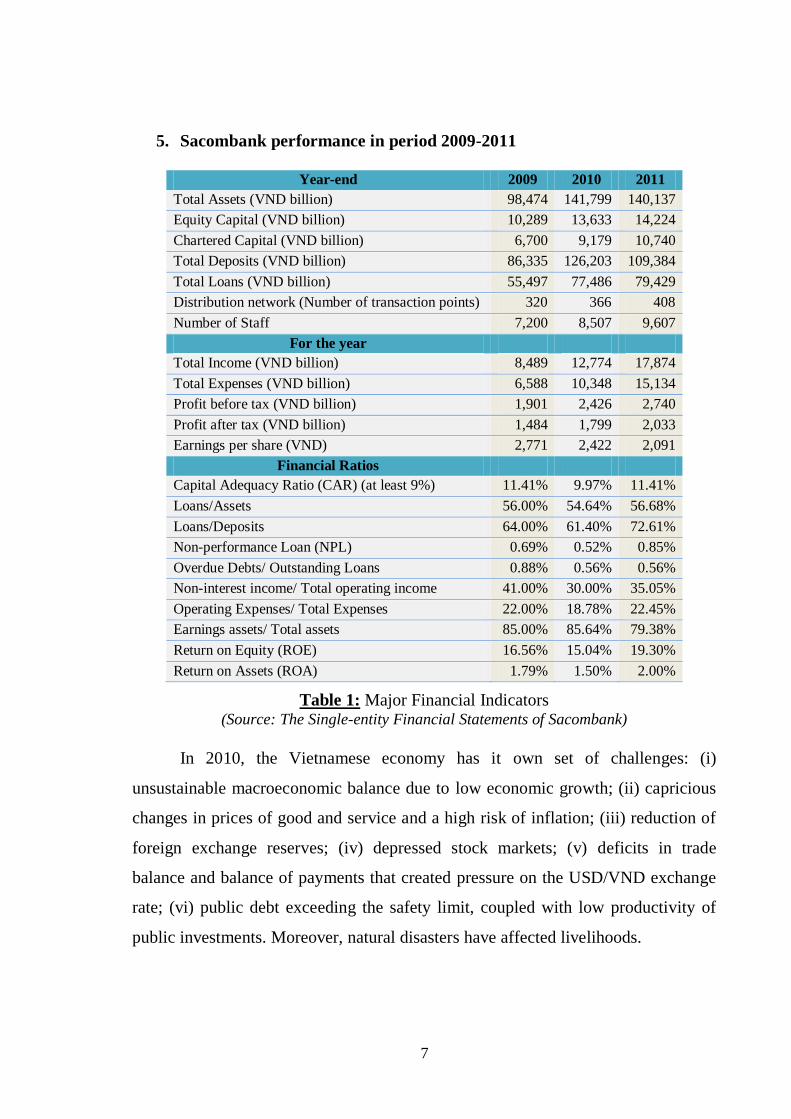

5. Sacombank performance in period 2009-2011

Year-end 2009 2010 2011

Total Assets (VND billion) 98,474 141,799 140,137

Equity Capital (VND billion) 10,289 13,633 14,224

Chartered Capital (VND billion) 6,700 9,179 10,740

Total Deposits (VND billion) 86,335 126,203 109,384

Total Loans (VND billion) 55,497 77,486 79,429

Distribution network (Number of transaction points) 320 366 408

Number of Staff 7,200 8,507 9,607

For the year

Total Income (VND billion) 8,489 12,774 17,874

Total Expenses (VND billion) 6,588 10,348 15,134

Profit before tax (VND billion) 1,901 2,426 2,740

Profit after tax (VND billion) 1,484 1,799 2,033

Earnings per share (VND) 2,771 2,422 2,091

Financial Ratios

Capital Adequacy Ratio (CAR) (at least 9%) 11.41% 9.97% 11.41%

Loans/Assets 56.00% 54.64% 56.68%

Loans/Deposits 64.00% 61.40% 72.61%

Non-performance Loan (NPL) 0.69% 0.52% 0.85%

Overdue Debts/ Outstanding Loans 0.88% 0.56% 0.56%

Non-interest income/ Total operating income 41.00% 30.00% 35.05%

Operating Expenses/ Total Expenses 22.00% 18.78% 22.45%

Earnings assets/ Total assets 85.00% 85.64% 79.38%

Return on Equity (ROE) 16.56% 15.04% 19.30%

Return on Assets (ROA) 1.79% 1.50% 2.00%

Table 1: Major Financial Indicators (Source: The Single-entity Financial Statements of Sacombank)

In 2010, the Vietnamese economy has it own set of challenges: (i)

unsustainable macroeconomic balance due to low economic growth; (ii) capricious

changes in prices of good and service and a high risk of inflation; (iii) reduction of

foreign exchange reserves; (iv) depressed stock markets; (v) deficits in trade

balance and balance of payments that created pressure on the USD/VND exchange

rate; (vi) public debt exceeding the safety limit, coupled with low productivity of

public investments. Moreover, natural disasters have affected livelihoods.

8

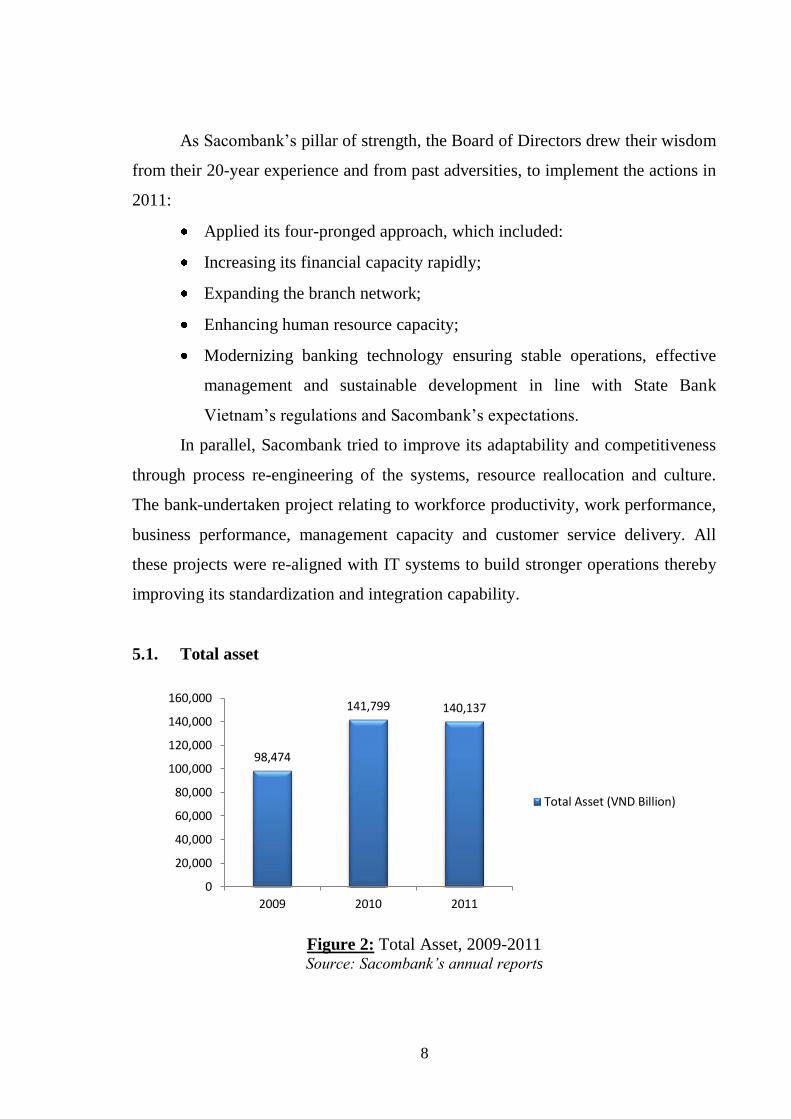

As Sacombank’s pillar of strength, the Board of Directors drew their wisdom

from their 20-year experience and from past adversities, to implement the actions in

2011:

Applied its four-pronged approach, which included:

Increasing its financial capacity rapidly;

Expanding the branch network;

Enhancing human resource capacity;

Modernizing banking technology ensuring stable operations, effective

management and sustainable development in line with State Bank

Vietnam’s regulations and Sacombank’s expectations.

In parallel, Sacombank tried to improve its adaptability and competitiveness

through process re-engineering of the systems, resource reallocation and culture.

The bank-undertaken project relating to workforce productivity, work performance,

business performance, management capacity and customer service delivery. All

these projects were re-aligned with IT systems to build stronger operations thereby

improving its standardization and integration capability.

5.1. Total asset

Figure 2: Total Asset, 2009-2011 Source: Sacombank’s annual reports

98,474

141,799 140,137

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2009 2010 2011

Total Asset (VND Billion)

9

The graph presents data on the total asset of Sacombank over an 6 years

period, from 2006 till 2011. It will be noticed that the total asset of the bank

increased, but not stable. In 2009, total asset of Sacombank is VND98,474 billion.

The following year, it rose sharply to VND141,799 billion, with an overall increase

of VND43,325 billion. In 2011, total asset fell slightly VND140,137 billion,

showing a 1.17% decrease when compare with 2010. With that sum of asset,

Sacombank is still one of the biggest banks in Vietnam.

As mentioned above, the decline is not great if you know last year was a

difficult year for Vietnam's economy. This demonstrates that the bank had the right

policy to cope with these difficulties.

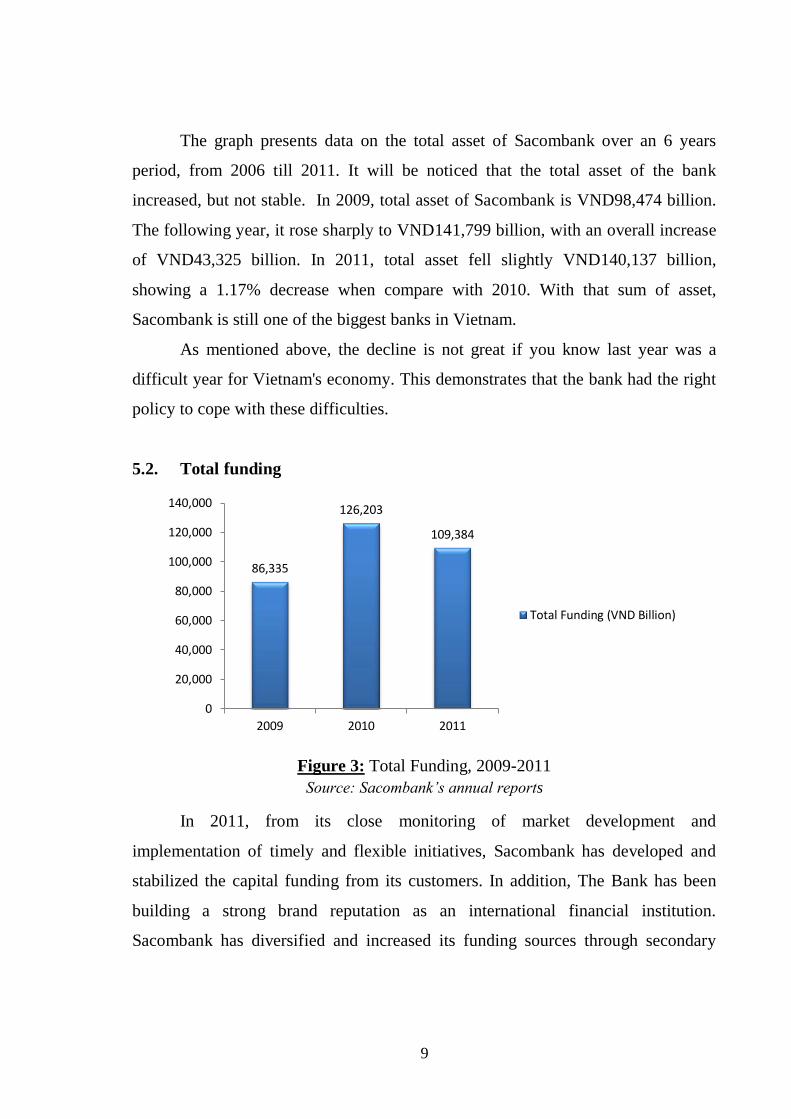

5.2. Total funding

Figure 3: Total Funding, 2009-2011

Source: Sacombank’s annual reports

In 2011, from its close monitoring of market development and

implementation of timely and flexible initiatives, Sacombank has developed and

stabilized the capital funding from its customers. In addition, The Bank has been

building a strong brand reputation as an international financial institution.

Sacombank has diversified and increased its funding sources through secondary

86,335

126,203

109,384

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2009 2010 2011

Total Funding (VND Billion)

10

markets. The dependence on local transactions was gradually reduced through

Letters of Credit (L/C) with long-term refinancing at reasonable interest rates.

On 31 December 2011, its total funding decreased by 13.32% from late 2010

and achieved VND109,384 billion. Of this amount, funds raised from enterprises

and retail customers residents was VND103,285 billion, decreased by 0.5%,

constituting 94.42% of the total funding. However, the market share of Sacombank

deposit base has still grown steadily annually and reached 4.8% at end of 2011

(Total funding of Vietnam’s banking industry in 2011 is estimated at

VND2,278,833 billion - Source: The State Bank of Vietnam).

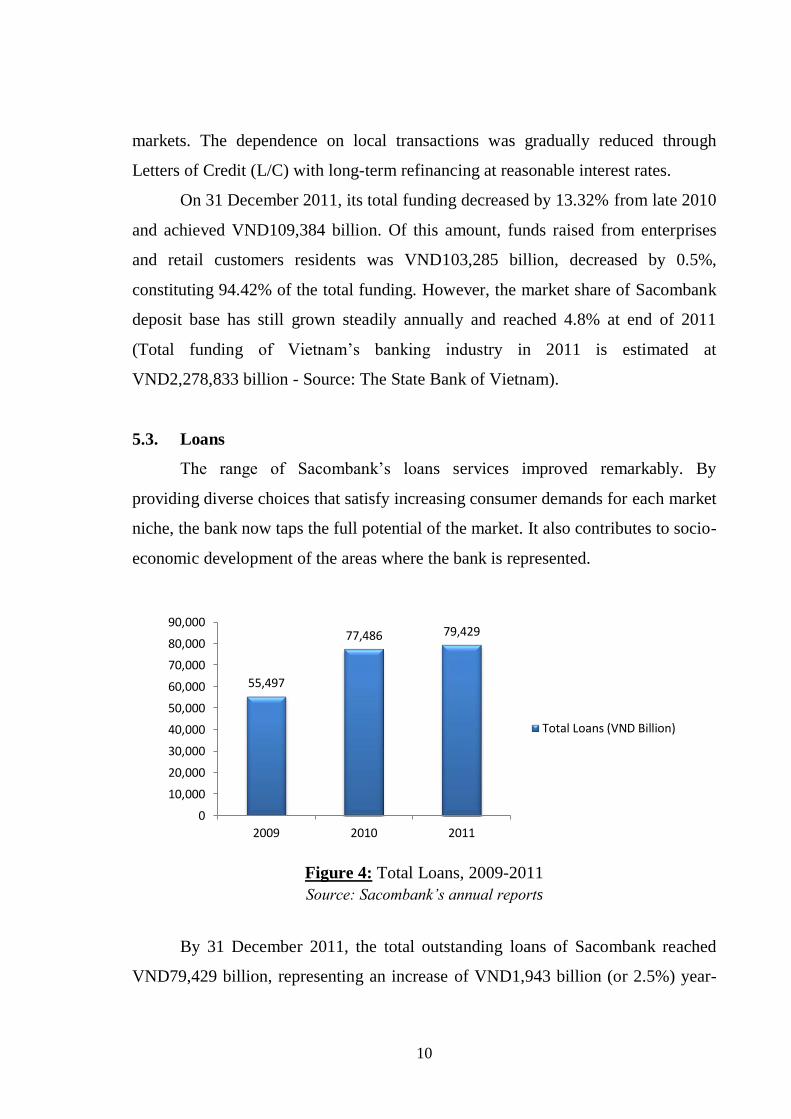

5.3. Loans

The range of Sacombank’s loans services improved remarkably. By

providing diverse choices that satisfy increasing consumer demands for each market

niche, the bank now taps the full potential of the market. It also contributes to socio-

economic development of the areas where the bank is represented.

Figure 4: Total Loans, 2009-2011

Source: Sacombank’s annual reports

By 31 December 2011, the total outstanding loans of Sacombank reached

VND79,429 billion, representing an increase of VND1,943 billion (or 2.5%) year-

55,497

77,486 79,429

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2009 2010 2011

Total Loans (VND Billion)

11

on-year. Sacombank’s market share in 2011 continued to grow compared to the

previous year, accounting for 3.29% of the total outstanding loans of the banking

industry (Total outstanding loans of Vietnam’s banking industry in 2011 is

estimated at VND2,410,676 billion - source: The State Bank of Vietnam).

In addition, Sacombank enhances its credit risk management through the

Overdue Debt Prevention and Settlement Committee and sub-committees. Credit

quality has increased as evident in the continual drop in overdue and bad debts. As

at 31 December 2011, the overdue and bad debts ratios were only 0.85% (VND677

billion) and 0.65% (VND445 billion) respectively. This is much lower than the

industry average and the bank’s 2011 ceiling threshold (that is less than 2%).

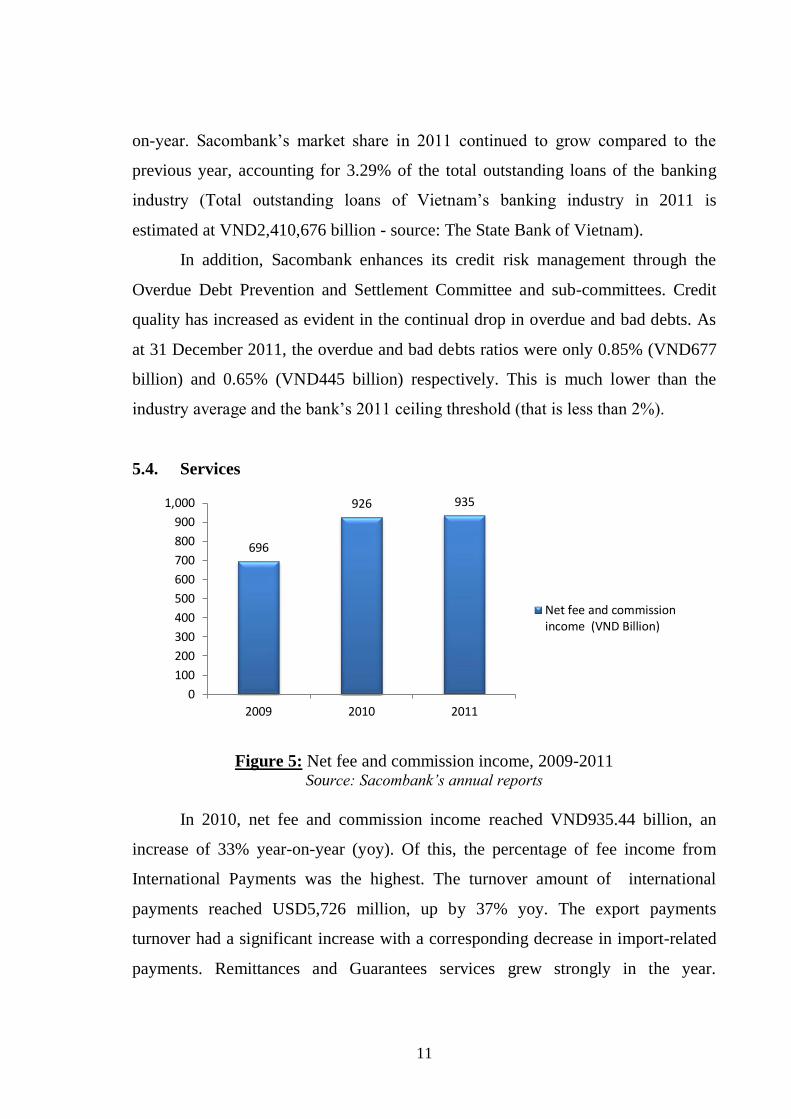

5.4. Services

Figure 5: Net fee and commission income, 2009-2011 Source: Sacombank’s annual reports

In 2010, net fee and commission income reached VND935.44 billion, an

increase of 33% year-on-year (yoy). Of this, the percentage of fee income from

International Payments was the highest. The turnover amount of international

payments reached USD5,726 million, up by 37% yoy. The export payments

turnover had a significant increase with a corresponding decrease in import-related

payments. Remittances and Guarantees services grew strongly in the year.

696

926 935

0

100

200

300

400

500

600

700

800

900

1,000

2009 2010 2011

Net fee and commissionincome (VND Billion)

12

Remittance turnover recorded VND2,834,292 billion, up 76% yoy. The value of

Guarantees reached VND8,504 billion, up 73% yoy. These achievements were

made possible by Sacombank’s commitment to reduce dependence on interest

incomes through various means.

The bank formulated a stable income structure by improving import and

export financing, accelerating guarantee services, revising current remittance

products using advanced core banking technology and leveraging on its domestic

and overseas network. Concurrently, e-banking products with new features were

launched and the Customer Service Center was upgraded. The International

Payment Center has also revised its business model to streamline administrative

procedures and strengthened its advisory payment services.

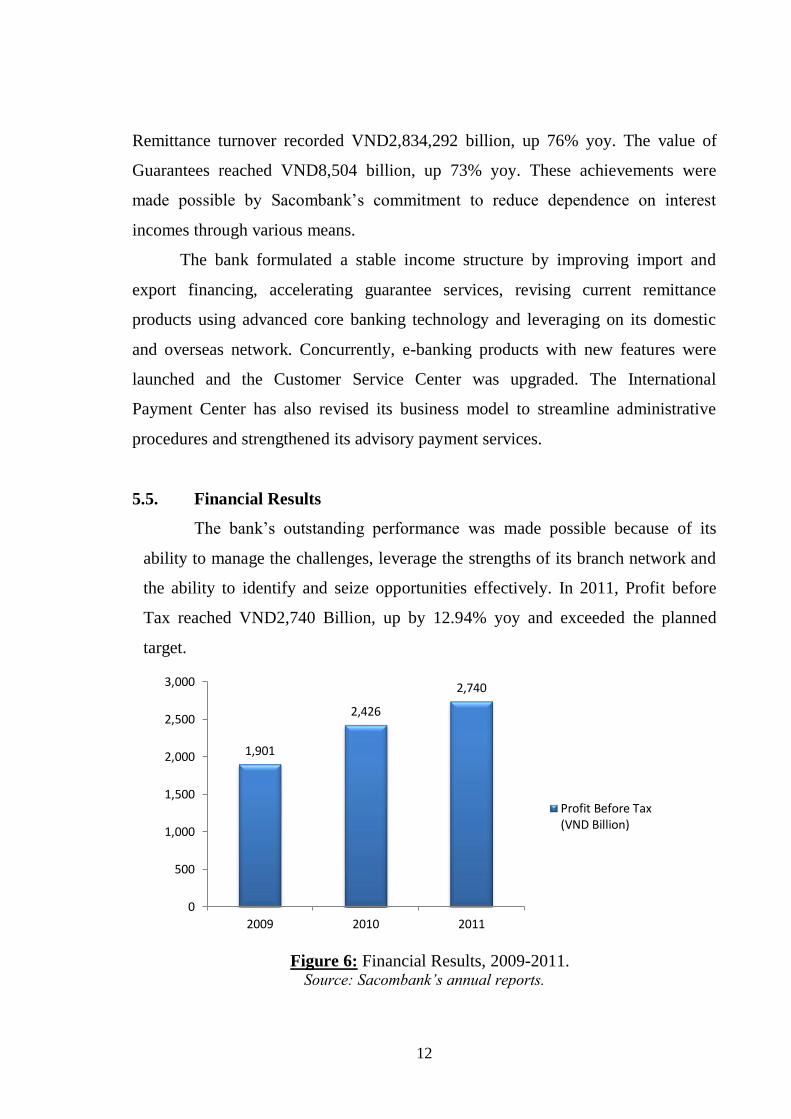

5.5. Financial Results

The bank’s outstanding performance was made possible because of its

ability to manage the challenges, leverage the strengths of its branch network and

the ability to identify and seize opportunities effectively. In 2011, Profit before

Tax reached VND2,740 Billion, up by 12.94% yoy and exceeded the planned

target.

Figure 6: Financial Results, 2009-2011. Source: Sacombank’s annual reports.

1,901

2,426

2,740

0

500

1,000

1,500

2,000

2,500

3,000

2009 2010 2011

Profit Before Tax(VND Billion)

13

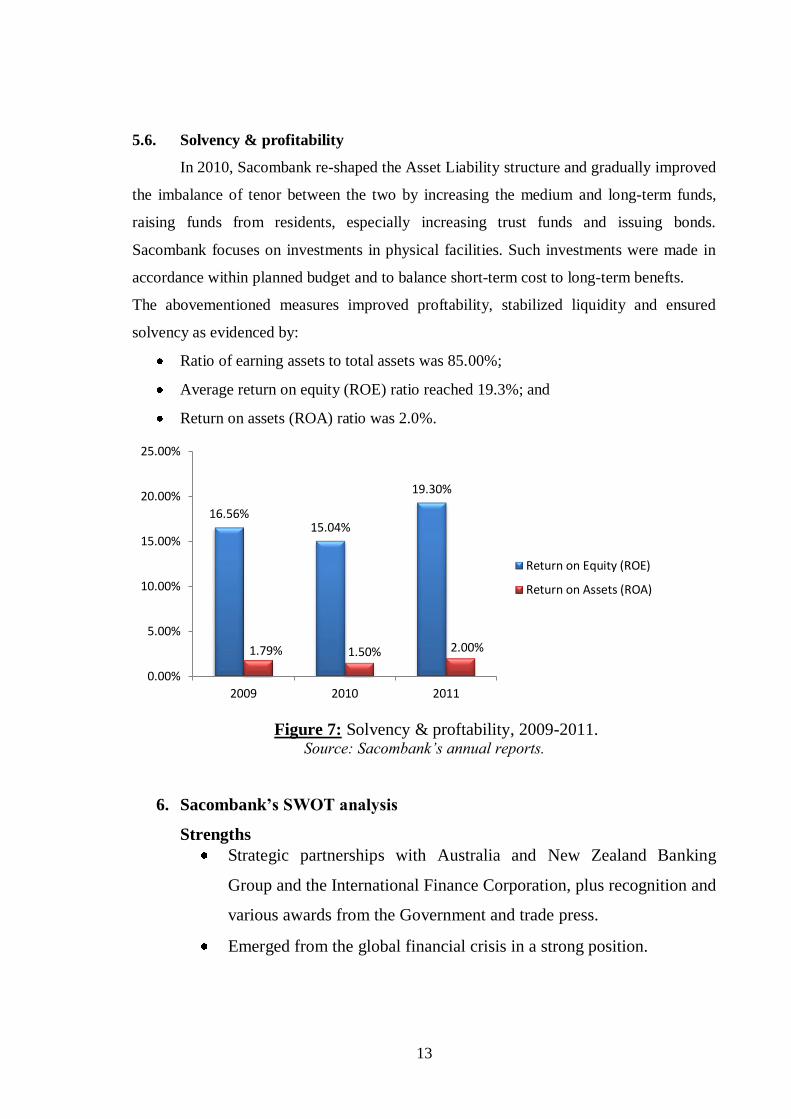

5.6. Solvency & profitability

In 2010, Sacombank re-shaped the Asset Liability structure and gradually improved

the imbalance of tenor between the two by increasing the medium and long-term funds,

raising funds from residents, especially increasing trust funds and issuing bonds.

Sacombank focuses on investments in physical facilities. Such investments were made in

accordance within planned budget and to balance short-term cost to long-term benefts.

The abovementioned measures improved proftability, stabilized liquidity and ensured

solvency as evidenced by:

Ratio of earning assets to total assets was 85.00%;

Average return on equity (ROE) ratio reached 19.3%; and

Return on assets (ROA) ratio was 2.0%.

Figure 7: Solvency & proftability, 2009-2011. Source: Sacombank’s annual reports.

6. Sacombank’s SWOT analysis

Strengths

Strategic partnerships with Australia and New Zealand Banking

Group and the International Finance Corporation, plus recognition and

various awards from the Government and trade press.

Emerged from the global financial crisis in a strong position.

16.56% 15.04%

19.30%

1.79% 1.50% 2.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

2009 2010 2011

Return on Equity (ROE)

Return on Assets (ROA)

14

By not recycling the rapid growth of deposits into new loans, the bank

has reduced its loan-to-deposit ratio to less than 100%.

The bank also appears to be reducing its vulnerability to a lack of

liquidity within the banking system.

One of the largest and longest established commercial banks in

Vietnam.

Sacombank has one of the largest branch networks among commercial

banks.

Weaknesses

Lack of scale. Sacombank is a fairly large bank in Vietnam but a

small institution by international standards.

Potential direct and indirect problems from the bursting of the asset

price bubble.

Opportunities

Potential for continuing growth from a low base.

Leverage of strong position in the Small and medium enterprises

(SME) lending sector.

Expansion into southern China and countries in the Association of

Southeast Asian Nations.

Threats

Vulnerability to direct or indirect impact from the downturn in global

trade.

Vulnerable to government credit caps.

The increasing competition from other banks, including private

banking, particularly the 100% owned foreign banks such as HSCB,

ANZ.

Competition from other non-banking financial institutions and

investment funds operating in Vietnam as other financing channels for

enterprises.

15

7. Development Strategy

Based on its vision of “becoming the leading Retail Bank in the Region”,

Sacombank has developed several objectives, each with specific solutions and

roadmaps:

7.1. Human resources strategy

The Bank plans to have 13,000 employees in 2015. Therefore, it will:

Increase the employment of staff with appropriate capacity;

Identify and groom current staff in preparation for promotion and

succession;

Prepare recruitment and training policies to stabilize the number of staff

employees and maintain the attrition rate below 10% per year.

7.2. Banking technology strategy

IT plays a significant role in expanding operations. Based on the

development pathway of a modern bank, Sacombank shall implement a strong

IT strategy over the next 10 years, in order to:

Improve workforce productivity and provide a range of product and

services of international standards, through the use of advanced

technology (that is, continuous improvement and upgrading of the

T24 core banking system);

Improve the bank’s competitiveness and management capacity by

implementing the remaining features of the core banking system and

data warehouse, and continuous development of other technology

projects (excluding the T24 System). The MIS shall be improved to

support decision-making and implementation of the growth strategy

as well as to scale up organizational performance.

7.3. Financial strategy

In the next decade, Sacombank shall:

16

Enlarge the capital base. Accordingly, the Basel T1 shall be increased

by 15%-20% per annum and T2 capital shall be applied to seek

growth;

Increase total assets by an average of 15%-20% per annum;

Grow Profit before tax by an average of 17%-20%;

Increase ROE (Profit after tax/Average Shareholders Equity) to 15%-

17%;

Increase ROA (Profit after tax/Average total assets) to 1.5% - 1.7%.

7.4. Channel strategy

Sacombank aims to extend its branch network to 600 transaction points

nationwide by 2020. Apart from Laos and Cambodia, the bank will also consider

expanding to Malaysia, Singapore, the United States of America, Australia,

Europe and other Southeast Asian countries.

7.5. Business strategy (funding and lending)

Business approach in the next 10 years:

Total funding shall grow by an average of 15%-18% per annum in

2011-2020. Domestic funding shall represent 65%-85% of the total

fund raised;

Total loans shall grow by an average of 18%-20% per annum during

2011–2020.

7.6. Product and service strategy

Focusing on retail banking product and services, with a gradual

increase in fee based income. The ratio of total fee and commission

income to total income shall reach an average of 12%-18% per annum

within 2011-2020;

Satisfying customers’ needs in retail banking and provide the market

with reasonably priced financial product packages by cross-selling

with partners and member companies of the Sacombank Group;

17

Maximizing customers’ satisfaction by assuring product and service

quality at home and abroad;

Developing unique products and services to bring in operational

effectiveness and improved competitiveness;

Developing new services such as derivative products, structured

products, debt instrument products among others.

7.7. Management strategy

Improving Corporate Governance by using an advanced management

model;

Steadily developing the organization, human resources structure and

operational model;

Integrating Headquarters and transaction points for an effective

forecasting system;

Developing an advanced and professional risk management system in

accordance with international standards;

Improving internal audit process in accordance.

18

Contents General Information ....................................................................................................... 1

1. Establishment and development ............................................................................. 1

2. Organization ............................................................................................................ 4

Figure 1: Organization Chart ......................................................................................... 4

3. Human Resources .................................................................................................... 5

4. Scope of Operations ................................................................................................. 6

5. Sacombank performance in period 2009-2011 ....................................................... 7

5.1. Total asset .......................................................................................................... 8

Figure 2: Total Asset, 2009-2011 ............................................................................... 8

5.2. Total funding ..................................................................................................... 9

Figure 3: Total Funding, 2009-2011........................................................................... 9

5.3. Loans................................................................................................................ 10

Figure 4: Total Loans, 2009-2011 ............................................................................ 10

5.4. Services ............................................................................................................ 11

Figure 5: Net fee and commission income, 2009-2011 ............................................. 11

5.5. Financial Results ............................................................................................. 12

Figure 6: Financial Results, 2009-2011. .................................................................. 12

5.6. Solvency & profitability .................................................................................. 13

Figure 7: Solvency & proftability, 2009-2011. ............................................................ 13

6. Sacombank’s SWOT analysis ............................................................................... 13

7. Development Strategy ............................................................................................ 15

7.1. Human resources strategy .............................................................................. 15

7.2. Banking technology strategy ........................................................................... 15

7.3. Financial strategy ............................................................................................ 15

7.4. Channel strategy.............................................................................................. 16

7.5. Business strategy (funding and lending) ......................................................... 16

7.6. Product and service strategy ........................................................................... 16

7.7. Management strategy ...................................................................................... 17

![[HTN] Ôn thi tổng hợp](https://static.fdocuments.us/doc/165x107/577c78411a28abe0548f4b39/htn-on-thi-tong-hop.jpg)