Baltic Household Outlook: Little change in household income 2011

Baltic

economic

outlook

Mārtiņš Āboliņš Economist

Global economy remains in a moderate cyclical slowdown in growth. OECD leading indicators show signs of stabilization.

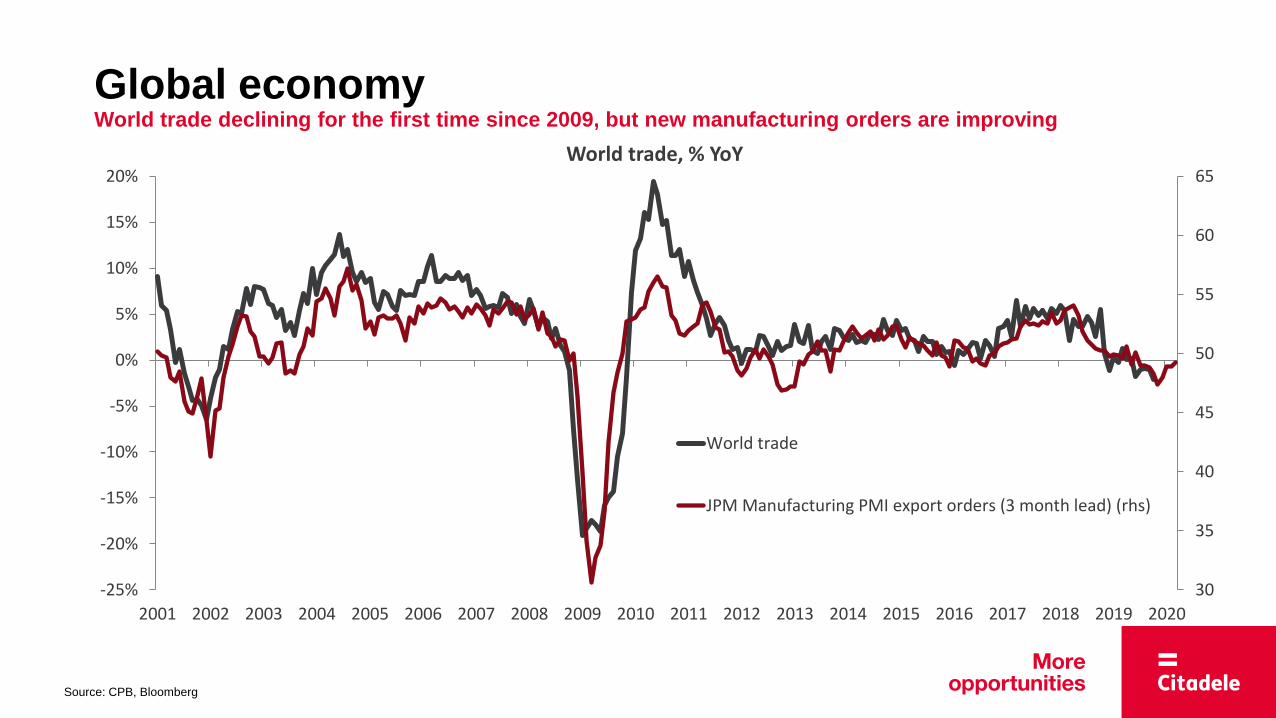

Manufacturing and world trade remain the weakest link in the global economy. The China-US agreement has reduced the risks associated with world trade.

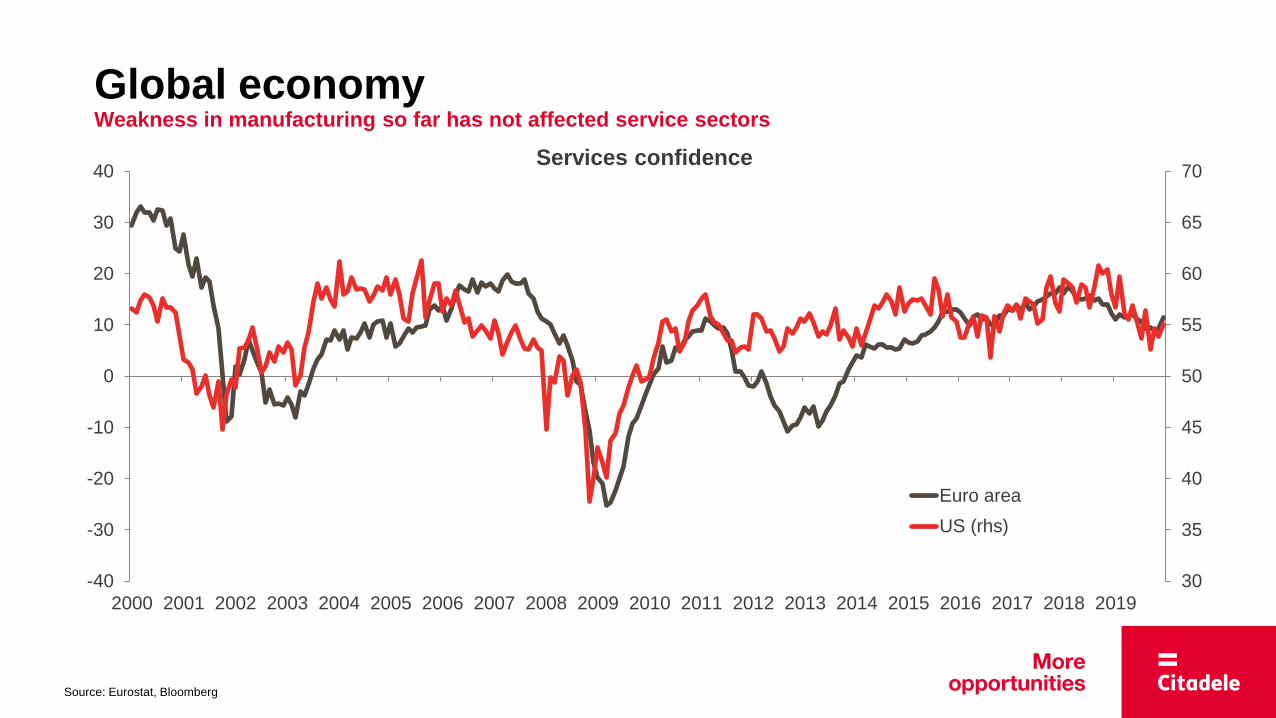

Service sectors and labour markets have not yet been affected by weakness in global manufacturing. However, these indicators respond to economic cycle fluctuations with a delay.

Concerns about the recession have not yet materialized, but risks remain and are still largely negative.

Most major central banks have cut interest rates and resumed stimulus measures in 2019, but fiscal policy will become less expansionary in 2020.

Financial markets are generally very positive. In the absence of negative surprises, global economic growth should pick up in the second half of the year.

Global economy The global economy is showing some signs of stabilization

95

96

97

98

99

100

101

102

103

1995199719992001200320052007200920112013201520172019

OECD composite leading indicator (100=long term average)

Source: OECD

Source: Bloomberg

Global economy Manufacturing remains the weakest link in the global economy

30

35

40

45

50

55

60

65

70

Ap

r-0

6

Au

g-0

6

De

c-0

6

Apr-

07

Au

g-0

7

De

c-0

7

Ap

r-0

8

Au

g-0

8

De

c-0

8

Ap

r-0

9

Au

g-0

9

De

c-0

9

Apr-

10

Au

g-1

0

De

c-1

0

Ap

r-1

1

Au

g-1

1

De

c-1

1

Ap

r-1

2

Au

g-1

2

De

c-1

2

Apr-

13

Au

g-1

3

De

c-1

3

Ap

r-1

4

Au

g-1

4

De

c-1

4

Ap

r-1

5

Au

g-1

5

De

c-1

5

Apr-

16

Au

g-1

6

De

c-1

6

Ap

r-1

7

Au

g-1

7

De

c-1

7

Ap

r-1

8

Au

g-1

8

De

c-1

8

Apr-

19

Au

g-1

9

De

c-1

9

Manufacturing PMI (values above 50 indicate expansion)

China Euro area US

30

35

40

45

50

55

60

65

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

World trade, % YoY

World trade

JPM Manufacturing PMI export orders (3 month lead) (rhs)

Source: CPB, Bloomberg

Global economy World trade declining for the first time since 2009, but new manufacturing orders are improving

Global economy Weakness in manufacturing so far has not affected service sectors

Source: Eurostat, Bloomberg

30

35

40

45

50

55

60

65

70

-40

-30

-20

-10

0

10

20

30

40

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Services confidence

Euro area

US (rhs)

7.6

3.6

0

2

4

6

8

10

12

14

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Unemployment rate, %

Euro area

United States

Source: Eurostat

Global economy Unemployment in the world has reached its lowest level in recent decades

Global economy Central banks have resumed monetary stimulus and the era of low interest rates is continuing

Source: Bloomberg

-5

0

5

10

15

20

25Benchmark policy rates

US UK Japan Euro area

Global economy GDP projections have been revised downwards, but a slight acceleration in growth is expected in 2020

Source: IMF, Bloomberg

3.4

3.8 3.6

3 3.1

1.6

2.4

2.9

2.3

1.9

6.7 6.8 6.6

6.1 5.9

1.9

2.5

1.9

1.2 1.0

2.2 2.5

1.5

0.5 0.6

2.4 2.4 2.3

1.2 1.2

2.8 3.0

1.7 1.45

1.2

2.4 2.3

1.5

2

1.5

0.3

1.6

2.3

1.2

1.7

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2016

2017

2018

2019

2020

2016

2017

2018

2019

2020

2016

2017

2018

2019

2020

2016

2017

2018

2019

2020

2016

2017

2018

2019

2020

2016

2017

2018

2019

2020

2016

2017

2018

2019

2020

2016

2017

2018

2019

2020

2016

2017

2018

2019

2020

GDP in constant prices, % YoY

World USA China Euro area Germany Sweden Finland Denmark Russia

Source: Eurostat

4.2%

2.9%

3.7%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

201120122013201420152016201720182019Q1

2019Q2

2019Q3

Real GDP, % annual change

Euro area Estonia

Latvia Lithuania

Baltic region Strong growth continues in the Baltic region, but the Latvian economy has become significantly cooler

7.6%

-6.3%

8.3%

4.8%

6.9%

8.0%

16.1%

23.3%

-14.3%

5.9%

-0.9%

4.1%

2.0%

6.1%

-0.3%

13.4%

1.0%

5.2%

3.7%

3.7%

4.4%

4.0%

4.2%

10.8%

-20% -10% 0% 10% 20% 30%

Finance and insurance

Construction

Taxes on production

Manufacturing

Trade and transport

Professional services

Information andcommunication

Agriculture

GDP growth in Q3 2019, % YoY

Lithuania

Latvia

Estonia

Economic sentiment Weaker external environment has adverse impact on economic sentiment

Source: DG ECFIN

60

70

80

90

100

110

120

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Economic sentiment index

Estonia Latvia

Lithuania Euro area

Lending Domestic lending in the Baltics is financed from domestic savings

0

5000

10000

15000

20000

25000

2008 2010 2012 2014 2016 2018

Loans to resident households and non-financial companies, MEUR

Estonia Latvia Lithuania

0%

50%

100%

150%

200%

250%

300%

350%

2008 2010 2012 2014 2016 2018

Resident loan-to-deposit ratio, %

Estonia Latvia Lithuania

Source: Bank of Latvia, Bank of Lithuania, Bank of Estonia

10.3

5.8

20.5

4.8

14.0

6.4

0

5

10

15

20

25

2004 2006 2008 2010 2012 2014 2016 2018

Price to income ratio in Baltic capitals, (Apartment prices relative to average annual gross salary)

Estonia Latvia Lithuania

-60%

-40%

-20%

0%

20%

40%

60%

2007 2009 2011 2013 2015 2017 2019

Real estate prices, % YoY

Estonia Latvia Lithuania

Real estate Real estate prices in the Baltics continue to grow, but mostly in line with wages

Source: Oberhaus, CSB, Statistics Estonia, Statistics Lithuania, Citadele calculations

External trade Trade balance in the Baltics has shifted from large deficits to surpluses

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

External trade blanace, % GDP

Latvija

Igaunija

Lietuva

Source: Bank of Latvia, Bank of Estonia, Bank of Lithuania, Eurostat

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

2013 2014 2015 2016 2017 2018 2019

Export of goods, current prices (3m MA), % y-o-y

Estonia Latvia Lithuania World trade

External trade Exports in Baltics moving in line with global trade

Source: Eurostat, CPB Netherlands

Manufacturing The resilience of the Baltic manufacturing to the weakening of external demand is not unlimited

Source: Eurostat

-10%

-5%

0%

5%

10%

15%

20%

2012 2013 2014 2015 2016 2017 2018 2019

Manufacturing, % YoY (3 month MA)

Estonia Latvia Lithuania Germany

-10% -5% 0% 5% 10% 15% 20% 25%

Food products

Furniture

Chemicals

Cars and car parts

Wood products

Machinery and equipment

Textiles and apparel

Rubber, plastics, non-metalic minerals

Manufacturing (total)

Fabricated metal products

Computers, electronics and optics

Manufacturing by sectors I-XI 2019, % YoY

Lithuania

Latvia

Estonia

Manufacturing Electronics and metal products remain the best performing sectors

Source: Eurostat

New orders New industrial orders in Baltics declining in line with Germany and Scandinavia

-60

-40

-20

0

20

40

60

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

New industrial orders

Estonia Latvia Lithuania Scandinavia Germany

Source: DG ECFIN

Manufacturing Engineering industries are among the fastest growing sectors in the Baltics

0.5% 2.6%

5.2% 5.3% 5.9% 6.5% 6.6%

12.1% 12.8% 13.0% 13.7%

17.3% 18.2%

20.6% 23.0%

30.9% 31.7%

32.9% 34.3%

46.3% 47.3%

60.9%

0.0% 30.0% 60.0% 90.0%

United KingdomNorwayGreeceFrance

GermanyEU-28

ItalySpain

NetherlandsSweden

DenmarkCzechiaPortugalFinlandEstoniaPoland

RomaniaHungaryBulgaria

LatviaIreland

Lithuania

Industrial production in metal products, electronics, car parts and machinery 2019 comapred to 2015, %

Source: Eurostat

Services Business and ICT services remain the strongest performing sectors in the Baltics

-5.0%

0.4%

5.3%

4.4%

-2.4%

11.8%

6.6%

-50.6%

1.2%

5.2%

7.2%

14.6%

17.1%

36.8%

6.8%

3.5%

23.4%

23.1%

42.1%

20.8%

42.5%

-60% -40% -20% 0% 20% 40%

Finance

Tourism

Transport

Services (total)

Construction

IT and Telecoms

Business services

Export of services in Q3 2019, % YoY

Lithuania

Latvia

Estonia

0

100

200

300

400

500

600

700

2005 2007 2009 2011 2013 2015 2017 2019

Export of ICT and business services, MEUR/Q

Estonia Latvia Lithuania

Source: Bank of Latvia, Bank of Lithuania, Bank of Estonia

Construction Construction sector in the Baltics is past cyclical peak and growth is slowing down

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

2011 2012 2013 2014 2015 2016 2017 2018 2019

Construction, % YoY

Estonia Latvia Lithuania

Source: Eurostat

Construction The sentiment of construction companies indicates weak growth or a slight decline in construction in 2020

-100

-80

-60

-40

-20

0

20

40

60

80

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Construction sentiment – activity in the last 3 months

Estonia Latvia Lithuania

Source: DG ECFIN

Trade Retail sales growth in the Baltics has slowed, but overall domestic consumption remains strong

-5%

0%

5%

10%

15%

20%

2011 2012 2013 2014 2015 2016 2017 2018 2019

Retail trade turnover in euros, % YoY (3 month average)

Estonia Latvia Lithuania

Source: Eurostat

Consumer confidence Slower economic growth has not yet affected consumer sentiment

-60

-50

-40

-30

-20

-10

0

10

20ja

nv.-

07

ma

ijs-0

7

se

pt.-0

7

janv.-

08

ma

ijs-0

8

sept.-0

8

jan

v.-

09

maijs

-09

se

pt.-0

9

jan

v.-

10

ma

ijs-1

0

se

pt.-1

0

jan

v.-

11

ma

ijs-1

1

se

pt.-1

1

jan

v.-

12

ma

ijs-1

2

se

pt.-1

2

jan

v.-

13

ma

ijs-1

3

se

pt.-1

3

jan

v.-

14

ma

ijs-1

4

se

pt.-1

4

jan

v.-

15

ma

ijs-1

5

se

pt.-1

5

jan

v.-

16

ma

ijs-1

6

se

pt.-1

6

jan

v.-

17

ma

ijs-1

7

se

pt.-1

7

jan

v.-

18

ma

ijs-1

8

se

pt.-1

8

jan

v.-

19

ma

ijs-1

9

se

pt.-1

9

Consumer confidence

Estonia Latvia Lithuania

Source: DG ECFIN

Inflation Consumer price inflation remains moderate

-6%

-4%

-2%

0%

2%

4%

6%

8%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Inflation (HICP), % y-o-y

Estonia Latvia Lithuania Euro area

Source: Eurostat

Labour market Unemployment in the Baltics is close to pre-crisis lows

0

5

10

15

20

25

2008 2010 2012 2014 2016 2018

Unemployment rate, %

-15%

-10%

-5%

0%

5%

10%

15%

2009 2011 2013 2015 2017 2019

Average gross monthly wage, % YoY

Estonia Latvia Lithuania

Source: Eurostat

Darba tirgus Household unemployment expectations have risen slightly but remain at a low level

-40

-20

0

20

40

60

80

100

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Household unemployment expectations

Estonia Latvia Lithuania

Source: DG ECFIN

Global economy remains in a moderate cyclical slowdown in growth, but concerns about the

recession have not materialized. Short-term indicators point to a stabilization of the situation.

Business sentiment in the Baltics has deteriorated, the export sector is adversely affected by

weaker external demand and economic growth is likely to slow down. Short-term macroeconomic

indicators remain better than in 2016.

There is currently no significant macroeconomic imbalance in the Baltic States and concerns

about significant crisis are unfounded. Foreign trade is balanced, lending is financed by local

deposits and real estate prices relative to wages are significantly lower than in the pre-crisis period.

In 2019 Latvian economy was affected by several one-off factors. For example, the decrease in

transit freight, the negative impact of weather conditions on the energy sector, the sharp fall in wood

prices, changes in Estonian excise duties and tighter fiscal policy.

Economic growth in the Baltics in 2020 will continue to be supported by IT and business

services as well as domestic consumption sectors. Meanwhile, manufacturing will be negatively

affected by external factors, while slower activity in construction will be due to fluctuations in the EU

funds financing cycle.

In the medium term, the demographic situation and rapid wage growth remain the greatest

risks to the economic development of the Baltic region.

Conclusions Lead indicators signal further slowdown in growth

Thank you for attention!

AS “Citadele banka”

Republikas laukums 2A

Rīga, Latvija