Economic outlook for ports · 2020. 2. 26. · Economic outlook for ports Theo Notteboom President...

20

Economic outlook for Economic outlook for ports ports Theo Notteboom President and professor, ITMMA - University of Antwerp, Belgium ESPO 2013- The European Sea Ports Conference Varna, Bulgaria – 30-31 May 2013

Transcript of Economic outlook for ports · 2020. 2. 26. · Economic outlook for ports Theo Notteboom President...

Economic outlook for Economic outlook for portsports Theo Notteboom President and professor, ITMMA - University of Antwerp, Belgium

ESPO 2013- The European Sea Ports Conference Varna, Bulgaria – 30-31 May 2013

EUROPEAN PORT TRAFFIC: SURPASSING PRE-CRISIS VOLUMES?

-20%

-15%

-10%

-5%

0%

5%

10%

15%

2006 2007 2008 2009 2010 2011 2012 Q1 2013

Pe

rcen

tage

gro

wth

co

mp

ared

to

th

e p

rrev

iou

s ye

ar

Total throughput

GDP growth EU27

Year-on-year growth in total EU port traffic (basis = ton) and EU GDP

Ports still ‘overreact’ to swings in economic growth

Traffic decline in 2012: -2% to 3.79 billion tons

Note: growth figures 2012 and Q1 2013 are estimates based on a sample of about 60 European ports

Traffic peaked in 2008: 4.18 billion tons

A weakening GDP multiplier?

Source: Alphaliner Weekly Newsletter, vol. 2013, issue 17, April 2013

The GDP multiplier in the EU container port system?

0.00

1.00

2.00

3.00

4.00

5.00

6.00

-10%

-05%

00%

05%

10%

15%

20%

2006 2007 2008 2009 2010 2011 2012 Q1 2013

TEU growth

GDP growth EU27

GDP Multiplier (right axis)New situation = negative GDP

growth combined with growth in

container volumes

Complexity behind TEU growth: Derived (economic activity) Substitution (containerisation) Incidental (traffic imbalances) Induced (transhipment)

-20%

-15%

-10%

-5%

0%

5%

10%

15%

2006 2007 2008 2009 2010 2011 2012 Q12013

Pe

rcen

tage

gro

wth

co

mp

ared

to

th

e p

rrev

iou

s ye

ar

Containers

Liquid bulk

Dry bulk

Conventional general cargo

Roro traffic

Total throughput

GDP growth EU27

Year-on-year growth in total EU port traffic (basis = ton) for cargo groups

The shock effect of 2009 and 2010 Mixed growth pattern after 2010

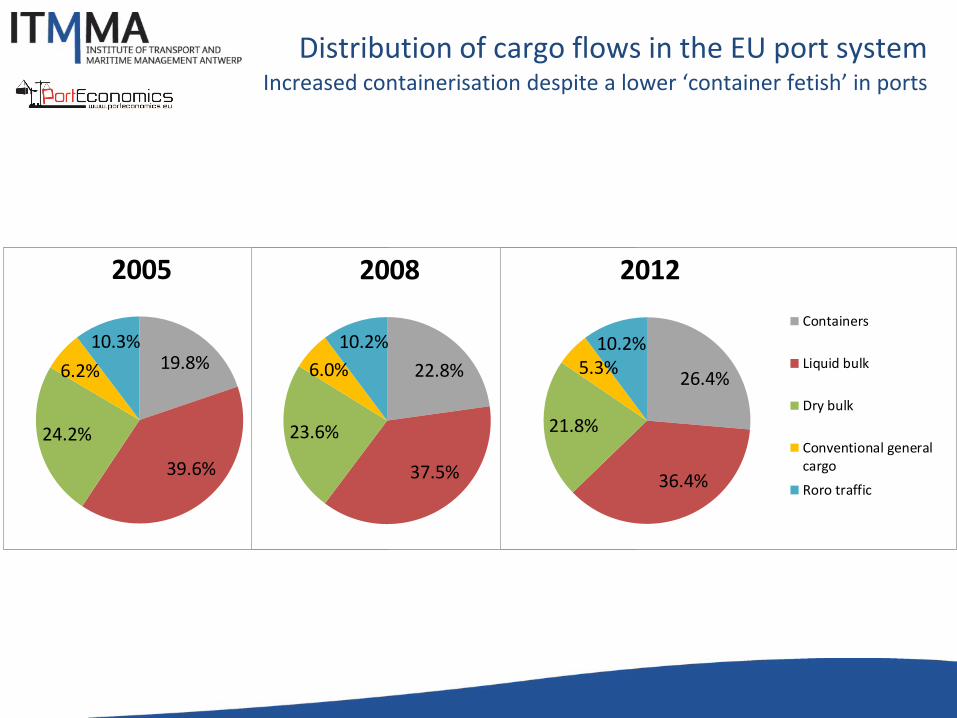

Distribution of cargo flows in the EU port system Increased containerisation despite a lower ‘container fetish’ in ports

19.8%

39.6%

24.2%

6.2%

10.3%

2005

Containers

Liquid bulk

Dry bulk

Conventional general cargo

Roro traffic

22.8%

37.5%

23.6%

6.0%

10.2%

2008

Containers

Liquid bulk

Dry bulk

Conventional general cargo

Roro traffic

26.4%

36.4%

21.8%

5.3%10.2%

2012

Containers

Liquid bulk

Dry bulk

Conventional generalcargo

Roro traffic

75

80

85

90

95

100

105

110

115

2005 2006 2007 2008 2009 2010 2011 2012 Q1 2013

Ind

ex e

volu

tio

n -

20

08

= 1

00

Containers

Liquid bulk

Dry bulk

Conventional general cargo

Roro traffic

Total

Are we back at pre-crisis traffic levels? Index evolution of throughput in the EU port system (2008=100)

Only container volumes managed to get above the 2008 level (+5% in 2012)

Liquid bulk saw a minor drop in 2009, but

records further traffic decline after 2009

Dry bulk and conventional general cargo

remain 15 to 20% below 2008 levels.

Total throughput is still about 10% below the 2008 level

Throughput in the European container port system (79 ports)

-

10

20

30

40

50

60

70

80

90

100

110

1201985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Co

nta

iner

thro

ug

hp

ut

in m

illi

on

TE

Us (

79 p

ort

s)

European port system

Hamburg-Le Havre range

Mediterranean range

UK range

Atlantic range

Baltic

Black Sea

Non-anticipated traffic gap of >20 million TEU

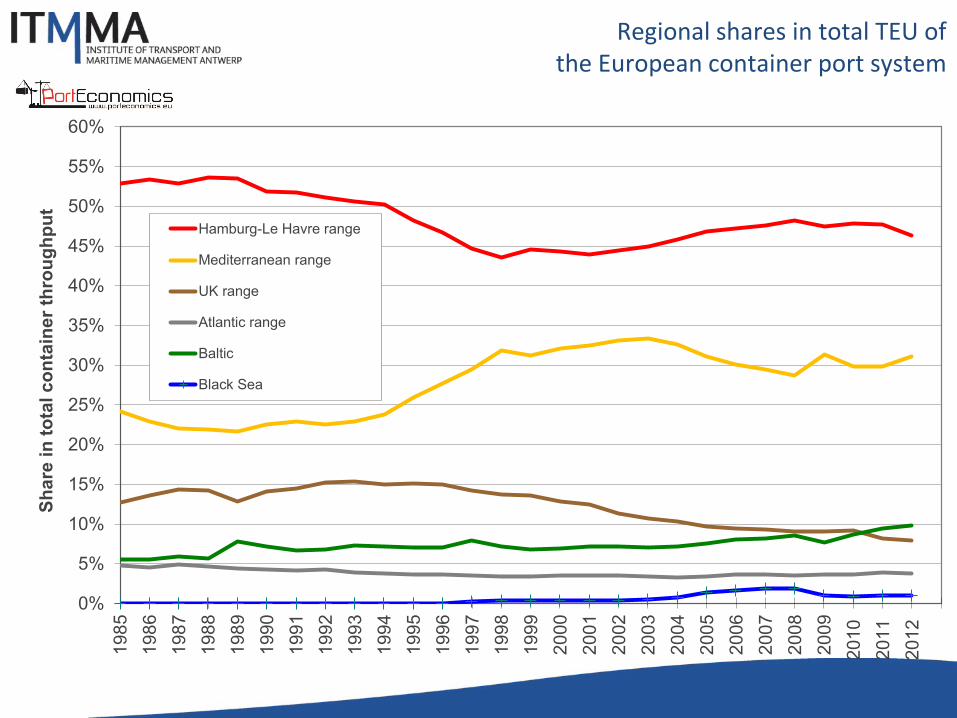

Regional shares in total TEU of the European container port system

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

60%1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Sh

are

in

to

tal co

nta

iner

thro

ug

hp

ut

Hamburg-Le Havre range

Mediterranean range

UK range

Atlantic range

Baltic

Black Sea

Middle East – Far East

Main shipping route

Americas

Americas

Transhipment/interlining port (transhipment incidence >75%)

Multi-port gateway region

Main shipping route

Gateway port

Gateway port also handling substantial transhipment flows

1

2

9

3

6

7

5

4

10

8

11

12

Main stand-alone gateways

2013 - T. Notteboom – ITMMA, University of Antwerp

UK

Germany

France

Belg.

NL

Ireland

Romania

Sweden

Spain

Croatia

Hungary

Czech Republic Slovakia

Serbia Bosnia&

Herz.

Alb.

Greece

Bulgaria

Turkey

Lithuania

Latvia

Estonia

Norway

Finland

Ukraine

Belarus

Russia

Portugal

Mace.

Den.

Austria

Switz.

Italy

Poland

Multi-port gateway regions (% in European TEU traffic)

Nantes-St-Nazaire

Bordeaux

Bilbao

Brest

Marseille-Fos

Sines

Lisbon

Leixoes

Valencia

Malaga Algeciras Cadiz

Barcelona

Tarragona

Cagliari

Gioia Tauro

Taranto Naples

Thessaloniki

Piraeus

Constantza

Le Havre

Rouen

Marsaxlokk

Genoa

Livorno

La Spezia Savona

Venice

Ravenna

Trieste Koper

Varna

Burga

s Vigo

Gijon Santander Ferrol (A) Antwerp

(B) Zeebrugge (C) Ghent (D) Rotterdam (E) Amsterdam (F) Dunkirk (G) Southampton (H) Felixstowe (I) Thamesport (J)Tilbury (K) Bremerhaven (L) Kotka (M) Hamina (N) Helsinki (O) Wilhelmshaven

(A) (B)

(C)

(D)

(E)

(F) (G)

(H)

(I) (J)

Lübeck Gdansk Gdynia

Hamburg (K)

Teesport

Hull

Grangemouth

Belfast

Dublin

Cork

Liverpool

Aarhus

Göteborg

Szczecin

Copenhagen

Malmö

Helsingborg

Oslo Bergen

Tallinn

Klaipeda

St-Petersburg

Ventspils Riga

Rauma

Turku

Stockholm

(L) (M)

(N)

Sevilla

Morocco Algeria Tunisia

Cyprus

Malta

(O)

Rijeka

2008 2012

1. Rhine-Scheldt Delta 24.7% 24.1%

2. Helgoland Bay 16.8% 15.8%

3. Seine Estuary 2.9% 2.6%

4. Portugese Range 1.4% 1.8%

5. Spanish Med range 6.9% 6.7%

6. Ligurian Range 4.5% 4.1%

7. North Adriatic 1.6% 1.9%

8. UK Southeast Coast 7.4% 6.3%

9. Gdansk Bay 0.9% 1.7%

10. Black Sea West 1.7% 0.9%

11. South Finland 1.6% 1.3%

12. Kattegat/The Sound 1.9% 1.8%

All 12 multi-port gateway regions 72.1% 69.0%

Stand-alone gatew ays 8.6% 11.8%

West Med hubs 11.3% 10.7%

Profile map of European seaport system

CONTAINERS

-80.00%-60.00%

-40.00%-20.00%

0.00%20.00%40.00%60.00%80.00%

100.00%120.00%140.00%160.00%

Pir

aeu

s

Gd

ansk

Sin

es

Cag

liari

Rig

a

Ko

pe

r

Leix

os

Rau

ma

The

ssal

on

iki

Talli

n

Mar

seill

e

Val

en

cia

Alg

ecir

as

Trie

ste

Du

nki

rk

Gen

oa

Nap

els

Ve

nic

e

Bre

me

n

Gd

ynia

Ro

tte

rdam

Mar

saxl

okk

Rije

ka

Go

the

nb

urg

Kla

ipe

da

Ko

tka

La s

pe

zia

An

twer

p

Rav

enn

a

Le H

avre

Ham

bu

rg

Zeeb

rugg

e

Lisb

on

Gio

ia T

auro

Legh

orn

Bar

celo

na

Co

nst

antz

a

Tara

nto

Savo

na

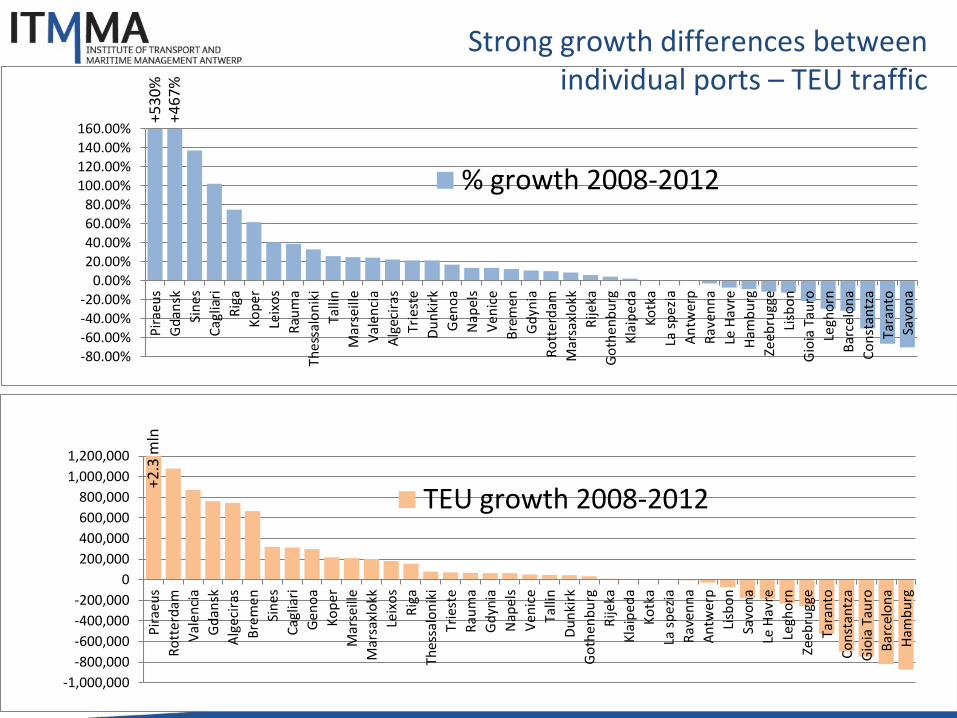

% growth 2008-2012+5

30

%+4

67

%

-1,000,000

-800,000

-600,000

-400,000

-200,000

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Pir

aeu

s

Ro

tte

rdam

Val

en

cia

Gd

ansk

Alg

ecir

as

Bre

me

n

Sin

es

Cag

liari

Gen

oa

Ko

pe

r

Mar

seill

e

Mar

saxl

okk

Leix

os

Rig

a

The

ssal

on

iki

Trie

ste

Rau

ma

Gd

ynia

Nap

els

Ve

nic

e

Talli

n

Du

nki

rk

Go

the

nb

urg

Rije

ka

Kla

ipe

da

Ko

tka

La s

pe

zia

Rav

enn

a

An

twer

p

Lisb

on

Savo

na

Le H

avre

Legh

orn

Zeeb

rugg

e

Tara

nto

Co

nst

antz

a

Gio

ia T

auro

Bar

celo

na

Ham

bu

rg

TEU growth 2008-2012

+2.3

mln

Strong growth differences between individual ports – TEU traffic

MARKET CONDITIONS AND COMPETITION

Market volatility and uncertainty

• Uncertainty is not a new phenomenon but the related intensity seems to be changing;

• Non-linear developments, market volatility, trend breaks, ‘wild cards’, ‘Black Swans’

• Market volatility has exogenous (e.g. economic cycles) and endogenous causes (actions of market players)

IMPLICATIONSIMPLICATIONS Ports as buffers – “uncertainty is the mother of inventory” (M. Christopher) Traditional forecasting techniques and port planning/investment tools? Need for flexibility (via adaptive planning tools), resilience and agility

A snapshot of the current and short-term future market conditions and competitive pressures

Using Porter’s five forces model on competition

Pressure on margins Higher service levels for same or lower price Pressure towards differentiation and integration Hedging and spreading of risks

Challenge: how to increase a company’s share in the

cake?

Logistics sector has hardly any

influence on the size of the

cake

Consolidation results in less players trying to get a piece of the cake

A snapshot of the current and short-term future market conditions and competitive pressures

Using Porter’s five forces model on competition

‘Buyers’ of port services look for supply chain solutions and develop a strong network focus Ports operate in buyers’ markets: Shippers > logistics service providers > shipping lines > terminal operators and ports

However, margins are lowest for shipping lines: Refusal rate problem and GRIs + (forced) divestment in terminals and other activities

A snapshot of the current and short-term future market conditions and competitive pressures

Using Porter’s five forces model on competition

Incumbents defense of market share Market-based barriers to entry Capital requirements and access to capital Economies of scale (cf. container shipping) Less barriers in times of abundance, more barriers when players are facing hard times Threat of government (shelter) policies

Leader/follower Slow steaming Daily service? Impact on no. of ports of call

20

New kids on the block? Container market in Hamburg-Le Havre range

BELGIUMGERMANY

NETHERLANDS

Amsterdam

Rotterdam

AntwerpGhent

OstendZeebrugge

Flushing

Wilhelmshaven

Emden Bremerhaven

Hamburg

Dunkirk

Rouen

Le Havre

Entrants in other regions: - Rise of Gdansk (impact on

H-LH range) - Revival of Piraeus - London Gateway ? - Etc..

Wilhelmshaven JadeWeserPort (opened in Summer 2012)

25,000 TEU in 2012 Prospects for 2013 ?

Amsterdam Ceres Paragon Terminal – later renamed to ACT

(open in 2001 – closed in 2012)

Flushing WCT Window of opportunity ?

Conclusions

• EU port traffic volumes are still below 2008 levels (except for containers), although big differences exist between ports

• Ports are facing a multi-layered buyers’ market situation

• No signs that we will move to a sellers’ market in the short or medium term (cf. economic activity, capacity in the market)

• Ports that do not respond adequately to the buyers’ market imperatives will lose ground.

• Guarantee ports’ autonomy and adaptive capabilities to develop appropriate responses to volatility in the market and requirements of ‘buyers’.