Risorse educative aperte e corsi open online: sfide e opportunità per l'educazione

Bologna, 17 ottobre, 2018

La filiera Automotive italiana si confronta con le sfide globali: la solidità finanziaria alla base della futura competitività

Andrea Marinoni Senior Partner

2 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

Agenda

This document shall be treated as confidential. It has been compiled for the exclusive, internal use by our client and is not complete without the underlying detail analyses and the oral presentation.

It may not be passed on and/or may not be made available to third parties without prior written consent from .

© Roland Berger

Q&A

C

5' Tempo

Conquistare la solidità finanziaria, prerequisito per la competitività

Sfide per i fornitori Auto

B

'10 Tempo

Perché si parla di disruption nel settore Auto

Scenario di riferimento

A

'10 Tempo

3 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

Agenda

This document shall be treated as confidential. It has been compiled for the exclusive, internal use by our client and is not complete without the underlying detail analyses and the oral presentation.

It may not be passed on and/or may not be made available to third parties without prior written consent from .

© Roland Berger

Q&A

C

Conquistare la solidità finanziaria, prerequisito per la competitività

Sfide per i fornitori Auto

B

Perché si parla di disruption nel settore Auto

Scenario di riferimento

A

5' Tempo

'10 Tempo

'10 Tempo

4 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

Tutti i business tendono ad uno stato "friction free" nella misura in cui tecnologia, normativa e comportamenti dei consumatori lo consentono

Convincimento chiave

Source: Roland Berger

5 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

Per oltre 100 anni il settore dell'Auto ha accettato alcune "friction" che non ne hanno impedito il successo, nonostante alti costi sociali

Existing "frictions" in the Automotive industry

Very low asset productivity: In average, a car is only used for 60 minutes per day, accounting for less than 5%

Casualties: Nearly 1.3 million people die in road crashes per year, accounting for 2.2% of all deaths globally and additional 20-50 million people are injured or disabled

Congestion: Commuters spend by far more than 10 bn hours per year in congestions, accounting for ~10% of their driving time

Emissions: Road transportation cause more than 5,500 Mt CO2, reflecting 17% of global CO2 emissions

> More than 100 USD bn cost through congestion

> More than 500 USD bn cost through road accidents

> Additional non-quantified cost for CO2 emissions

Frictions in Automotive industry Cost impact

6 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

Guardando avanti, quattro trend chiave concorrono alla disruption del settore Auto - MADE

Source: Roland Berger

Disruption

Alternative fuels

Autonomous Non-traditional entrants

ICE advancement

Electrified

New retail

Start-up OEMs

Low cost brands

Connected

Digitized

Mobility

Emissions regulations

Light-weighting

Fuel cells

Big data

Artificial Intelligence

7 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

MADE – ma non solo – nell'orizzonte di medio lungo termine dei player dell'Automotive

Car buyers

OEMs

Competition Supply base

Capital markets/ financing

Technology/ legislation

Long-term Short-term

Volatility of capital markets

"Zero casualties"

Rising energy costs

Availability of skilled workforce

Supplier insolvencies

Factor cost inflation

Selective consolidation

"Rising star OEMs"

Global localization

Price pressure

Volume bundling

Emerging market

investors

New growth regions

Continued outsourcing

ADAS/ automated

driving

Further reduced

emissions

Comfort features

New players

(hardware and

software)

Volatility of exchange

rates

Demotorization

Digital technologies

Triad stagnation

Investors' and banks' view

on auto suppliers

New mobility concepts

Terms & conditions

Further reduced CO2

targets

Potential downturn

Diesel

Industry 4.0 New customers (IT/tech space)

Brexit

Automotive industry trend radar

Note: Excluding product segment specific technology and operational issues

Source: Lazard, Roland Berger

8 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

Verso lo scenario 2030: diversi percorsi di avvicinamento avendo chiaro che tutto il settore sarà radicalmente trasformato

Source: Roland Berger

Esempio

Tempo Oggi

Grado di cambiamento

Scenario alta velocità Scenario media velocità Scenario bassa velocità Scenario area

Automotive "End game zone"

2020 2025 2030

Domanda chiave: quale scenario è più probabile?

> Alta percentuale di veicoli elettrici

> Alta percentuale di guida automatizzata

> Basso tasso di proprietà di automobili

> Impatto significativo sulla distribuzione dei profitti e sulla struttura del settore

9 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

Con il nostro "Automotive Disruption Radar" monitoriamo su base globale 27 indicatori che guidano il cambiamento

Main indicators in the "Automotive Disruption Radar"

Source: Roland Berger

27 indicators

Type approval process

Autonomous vehicle – Computing power

Digital sales channel – OEM

EV portfolio

Automotive products (Level 4+)

R&D intensity – Autonomous driving

Test roads – Autonomous vehicle

Vehicle-2-vehicle communication

EV/PHEV charging infrastructure

Mobile network – 5G coverage

Venture Capital invest – Artificial intelligence

Venture Capital invest – Mobility

Battery cost – EVs

Patent activities

Automotive association activities

CO2 legislation

Restrictions for ICEs

Customer curiosity

Mobility behavior

EV preference

Digitized culture preference

Autonomous vehicle preference

Mobility concept preferences

EV/PHEV sales

Amount of shared vehicles

Mobility planning

Multi modal mobility

Industry activity

5

Customer interest

1

Regulation

2

Technology

3

Infrastructure

4

10 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

La guida autonoma è un percorso a più livelli (5 secondo SAE): diversi percorsi/approcci per costruttori tradizionali e new comer

Note: AD classification for SAE international (Society of Automotive Engineers) has one level more vs. NHTSA (National Highway Traffic Safety Administration), with high and full automation Source: SAE, Roland Berger

Google car (Waymo)

All modes door 2 door

Robocab (cities) Highway (high speed) Parking and other

closed environments (eg. theme park, plants)

Highway autopilot

In lane traffic jam assistance

On-going initiatives on full autonomous vehicles

Line keeping system

1 2 3 4 5 Automation Levels (SAE)

Navya shuttle

Uber robocab Driver

assistance

2016 Partial

automation

2016 Conditional automation

2018 High automation

2020-25 Full automation

2025-30 Expected first launch

OEMs way

Tech players way

Good weather conditions

Limited lateral or longitudinal

control

Limited AD in very specific conditions

Driver has to take control

back from car at any time

Full autonomous drive in specific

environment

No driver required

11 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

Gli annunci da parte degli OEM sulla guida autonoma stanno accelerando

Source: Evercore, OEM information, Press review

Lanci attesi dei veicoli autonomi

Automation level (SAE)

5 Full automation

4 High

automation

3 Conditional automation

• BMW / Ottomatika

• Fiat Chrysler / Google (tests)

• Uber / Daimler

• Uber / Volvo

• Lyft / Nutonomy

• Waymo (Google) / Avis

• Apple / Hertz

• Fiat / BMW / Intel / FCA

• Toyota / Nvidia

• Microsoft / Baidu

Full autonomous drive under specific

environment (ex : valet parking)

Driver could take control back at any moment (ex :

highway auto-pilot)

No more driver required (ex : robocab)

2018 2019 2020 2025 2021

Google Waymo

Nutonomy Self-driving taxis

Mercedes F015 (in 2030)

Audi A8 "Jack"

Nissan Propilot

Renault Zoe EV

Volvo XC90

Audi A8

BMW iNext

Driverless car

2024 Partnerships

Key acquisitions • Delphi / Ottomatika (2015)

• GM / Cruise

• Ford / Argo AI

• Uber / Otto

• GM / Lyft (investment)

• Intel / Mobileye

Other moves • Aurora creation by ex Tesla /

Google employees

• Launch of Lyft open data platform

• Mass-Manufacturing started by GM

?

With BMW / Intel

Toyota

PSA Diverse prototypes tested

Hyundai Ioniq

12 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

Il dominio tecnologico con il più alto livello di disruption è il powertrain

Impact of technology shifts by domain

Source: Lazard, Roland Berger

Disruption impact on current business

Supplier domain Low High

Interior

Exterior

Chassis

Powertrain

Powertrain > E-motors and power electronics

> Battery systems

> Simple 1-2 step reduction gears

Interior > New HMI / display technologies

> Extended Infotainment solutions

> Increased interior insulation (NVH)

> Integration of electronics and surfaces

Next generation vehicle concept

Substantial new requirements for the supply base

Chassis > Advanced driver assistance systems and autonomous features

> Adaptive suspensions

> Active steering and braking systems

> Shifting material focus and growing importance of multi-material applications

> Growth of non-structural composites

Exterior

13 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

2025 2020 2010 2030/2035 2015

101.9 94.9

74.4

88.8

Nel breve medio termine i volumi sono previsti in leggera crescita, in rallentamento rispetto al passato - incertezza nel lungo periodo

> Growth has recently being slowing down in mature markets

> In the future, supplier revenue growth will be determined more by the product portfolio and content per vehicle than by underlying production volume growth

> After 2025, a decline of overall production volumes might occur in a disruptive scenario

Business as usual

Disruptive scenario (RoboCabs)

Recovery and sustained growth

Growth slow down

Growth stagnation

Emergence of shared and autonomous

mobility

Short term Mid term Long term

> Slowing growth in mature markets – US – Europe – Japan – Korea

> Shifting content per vehicle

> Suppliers growth perspective will depend on product portfolio

> Less ownership and higher utilization of mobility services

> Exponential adoption of RoboCabs possible

Today

CAGR 3.5%

CAGR 2.4%

CAGR ~1-2%

Shared mobility ?

Short to long term growth perspectives [LV production; m units]

Source: IHS, Global RB Mobility Revenue and Profit Pool Model, Lazard, Roland Berger

14 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

Agenda

This document shall be treated as confidential. It has been compiled for the exclusive, internal use by our client and is not complete without the underlying detail analyses and the oral presentation.

It may not be passed on and/or may not be made available to third parties without prior written consent from .

© Roland Berger

Q&A

C

Conquistare la solidità finanziaria, prerequisito per la competitività

Sfide per i fornitori Auto

B

Verso la disruption nel settore Auto

Scenario di riferimento

A

5' Tempo

'10 Tempo

'10 Tempo

15 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

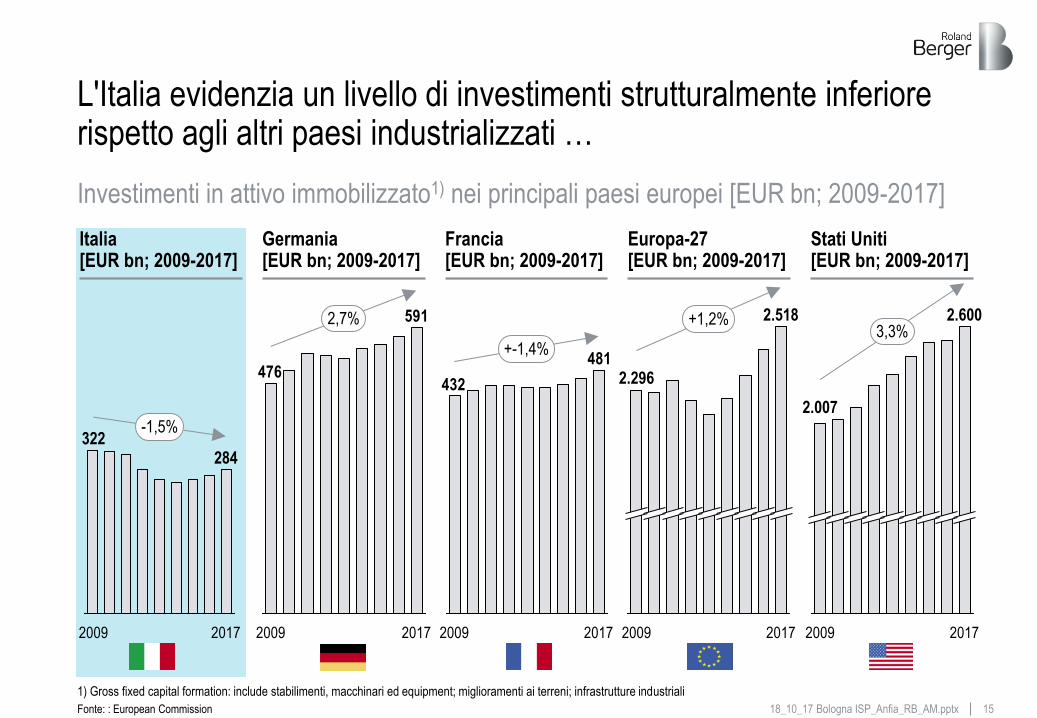

L'Italia evidenzia un livello di investimenti strutturalmente inferiore rispetto agli altri paesi industrializzati …

-1,5%

284

2009

322

2017

591

476

2009 2017

2,7%

481

432

2009 2017

+-1,4%

2.518

2017

2.296

2009

+1,2%

Investimenti in attivo immobilizzato1) nei principali paesi europei [EUR bn; 2009-2017]

Italia [EUR bn; 2009-2017]

Germania [EUR bn; 2009-2017]

Francia [EUR bn; 2009-2017]

Europa-27 [EUR bn; 2009-2017]

Stati Uniti [EUR bn; 2009-2017]

2.600

2.007

2009 2017

3,3%

Fonte: : European Commission

1) Gross fixed capital formation: include stabilimenti, macchinari ed equipment; miglioramenti ai terreni; infrastrutture industriali

16 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

… pur con una inversione di tendenza mostrata da una ripresa degli investimenti confermata nel medio termine

Investimenti in attivo immobilizzato1): focus Italia [2012-19; EUR bn; prezzi costanti]

305298284

274265260266285

2012 2019F 2017 2014 2018F 2013 2016 2015

-2,3% 3,5% 3,6%

Forecast > In Italia gli investimenti in asset sono stati

fortemente colpiti dalla recessione, registrando una ripresa più lenta rispetto ai paesi Europei comparabili (CAGR 12-15 -2,3% in Italia vs. +0,85% Euro Area)

> Nel 2015 gli investimenti hanno iniziato a dimostrare segni di ripresa, in linea con un aumento della produzione industriale e un miglioramento dell'outlook economico

> I feedback del mercato suggeriscono un aumento sino al 2019 (+3,6% CAGR 2017-19) spinto dalla ripresa, su scala globale, dei settori pivot dell'economia Italiana (e.g. settore dei macchinari prevista una crescita del 4% a livello globale)

Investimenti [EUR bn]

1) Gross fixed capital formation: include stabilimenti, macchinari ed equipment; miglioramenti ai terreni; infrastrutture industriali

Fonte: European Commission (AMECO); IHS

17 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

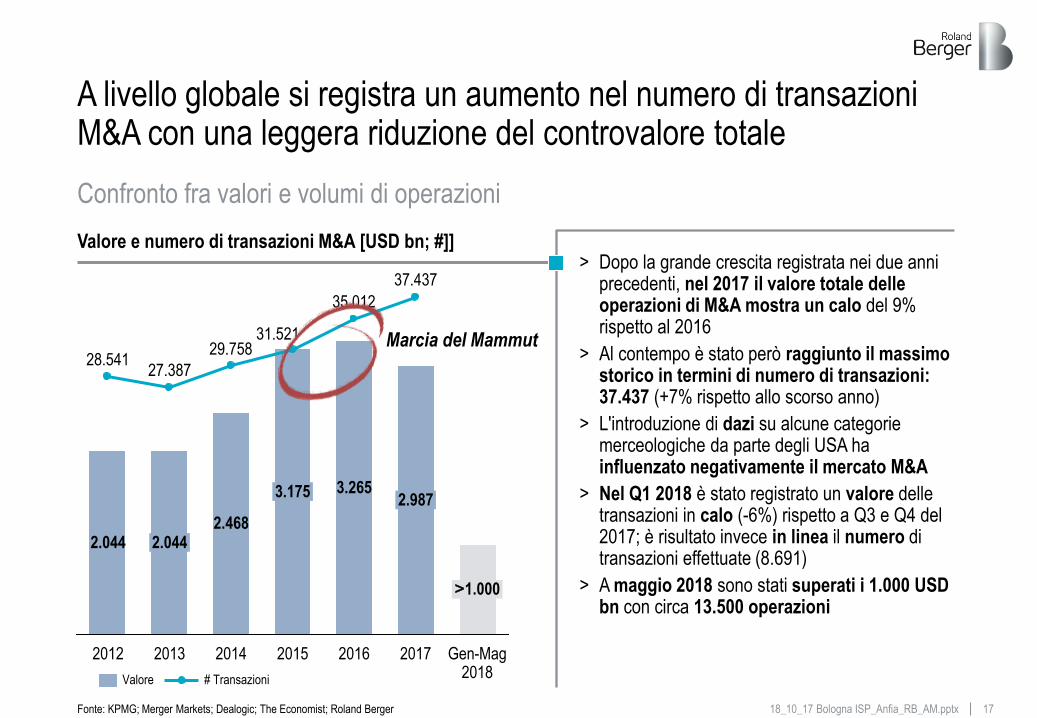

A livello globale si registra un aumento nel numero di transazioni M&A con una leggera riduzione del controvalore totale

> Dopo la grande crescita registrata nei due anni precedenti, nel 2017 il valore totale delle operazioni di M&A mostra un calo del 9% rispetto al 2016

> Al contempo è stato però raggiunto il massimo storico in termini di numero di transazioni: 37.437 (+7% rispetto allo scorso anno)

> L'introduzione di dazi su alcune categorie merceologiche da parte degli USA ha influenzato negativamente il mercato M&A

> Nel Q1 2018 è stato registrato un valore delle transazioni in calo (-6%) rispetto a Q3 e Q4 del 2017; è risultato invece in linea il numero di transazioni effettuate (8.691)

> A maggio 2018 sono stati superati i 1.000 USD bn con circa 13.500 operazioni

Confronto fra valori e volumi di operazioni

Valore e numero di transazioni M&A [USD bn; #]]

Fonte: KPMG; Merger Markets; Dealogic; The Economist; Roland Berger

Gen-Mag 2018

2016 2013 2014 2012 2017

29.758

2.044 2.044

2015

28.541 27.387

3.175

2.468

31.521

37.437

2.987

>1.000

35.012

3.265

Valore # Transazioni

Marcia del Mammut

18 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

Il mercato rimane solido in Italia, con un numero di operazioni in crescita e una flessione del controvalore del 20% nel 2017

2017: operazioni con società Acquirente Straniera e Target

Italiana

2017: operazioni con società Acquirente

Italiana e Target Estera

Mercato M&A Italia, valore cumulato delle operazioni per anno [EUR bn, 2011/2017]

Focus sul 2017: punti chiave

[# operazioni] Operazioni M&A di società estere su target Italiane nel 2017

266

[# operazioni] Operazioni M&A di società Italiane su target estere nel 2017

159

[EUR m] Valore medio di un'operazione M&A nel 2017 85

[EUR m] Valore medio di un'operazione M&A nel 2017 57

329 340 381 543 583 829

[USD bn, 2016] Mercato M&A Globale 2.987 [USD bn, 2016] Mercato M&A Europeo 656

7

17 1410

14

26

3

4 1310

12

187

13

2732

20

15

9

23

2016

2

28

2014 2013

50

26

31

58 56

2015 2017

47

2011 2012 2017: operazioni con società Acquirente

Italiana e Target Italiana

[# operazioni] Operazioni M&A di società Italiane su target Italiane nel 2017

392

[EUR m] Valore medio di un'operazione M&A nel 2017 38

# operazioni

Mercato M&A Italia e operazioni Cross-border

817

Fonte: MergerMarket; KPMG; Roland Berger

19 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

Nel 2018 si osserva una rilevante attività M&A nella componentistica Automotive con operazioni promosse da investitori USA e cinesi

2013

Amtek / Neumayer Tekfor

Wanxiang Group/ A123

Ningbo Huaxiang / HIB Trim Parts

Huayu Auto. Systems / Yanfeng Visteon JV

BorgWarner/ Wahler

Mahle/ Behr

Gentherm/ W.E.T. Automotive

Tokai Rubber/ Anvis

Grammer/ Nectec

Gentex/ JCI HomeLink

TMT / ZF Boge

Halla/ Visteon climate business

Wangfeng/ Meridian Lightweight

Nidec/ Honda Elesys

2014

Amtek/ Kuepper Group

AVIC/ Hilite

AVIC/ KOKI Technik

AUNDE/ Fehrer

Amtek/ Kaiser

Bosch / ZF Lenksysteme

Shanghai Prime Machinery/Nedschroef

MAHLE/ Letrika

ZF/ TRW

Lear/ Eagle Ottawa

Visteon/ JCI auto. electronics bus.

Sensata/ Schrader

Delphi/ Unwired Technology

Federal-Mogul/ TRW valves business

2015

AVIC Automotive/ Henniges

China National Tire/ Pirelli

Delphi/ HellermannTyton

Continental/ Elektrobit

BorgWarner/ Remy International

Grupo Antolin/ Magna interior business

Mann+Hummel / Affinia

Magna/ Getrag

Linamar/ Montupet

Johnson Electric / Stackpole

MAHLE/ Delphi thermal business

NGK Spark Plug/ Wells Vehicle Electronics

Valeo/ Peiker Acustic

Harman/ Symphony Teleca/Redbend

2016

Illinois Tool Works/ TRW Auto. Elec. & Comp.

Musashi Seimitsu/ Hay

Freudenberg/ TBVC

Yinyi Group/ Punch Powertrain

Plastic Omnium/ Faurecia exterior bus.

Ningbo Joyson/ KSS

Megatech/ Boshoku Europe

Valeo/ FTE Automotive

Samsung/ Harman

Valeo/ Ichikoh

VBP Group/ Mobile Climate Ctrl. Group

American Axle/ Metaldyne

Mecaplast/ Key Plastics

CIE Automotive / Grupo Amaya Telleria

Intel/ Mobileye

Superior Industries/ Uniwheels

Lear/Grupo Antolin (Seating & Metal B.ness)

BorgWarner/ Sevcon

ZMJ/CRCI / Bosch SMG

Luxshare / ZF Body Controls

Fountain West/Bosch Mahle Turbo Chargers

2017

KSS/ Takata

TE Connectivity/ Hirschmann Car Comm.

Fuxin Dare Automotive/ Carcoustics

Motherson Sumi Systems /PKC Group

Genuine Parts/ Alliance Automotive

CIE Automotive/ Newcor

WABCO/ RH Sheppard

Selected automotive supplier acquisitions, 2012-2017 (YTD)

Key: Acquirer/Target Note: Excluding financial sponsor led transactions. Some 2017 transactions are signed, but not yet closed

Source: Zephyr, Capital IQ, Thomson, Dealogic, Merger Market, press research, Lazard, Roland Berger

2018

Tenneco Inc./Federal-mogul Corporation

Autoliv Inc../ Veoneer Inc

Jiye Auto Parts Gmbh/Grammer Ag

Aptiv Plc/Kum Inc.

Schaeffler India Ltd/LUK India Pvt Ltd

Superior Industries Intern. Germany Ag/Uniwheels Ag

Accuride Corporation/Mefro Wheels Gmbh

Magna International Inc./Olsa Spa

Shanghai Daimay Automotive Interior/Motus Integrated Tech.

Samvardhana Motherson Group Bv/Reydel Automotive

Z. Wanfeng Auto Wheel /Wuxi Xiongwei Jinggong

Pacific Industrial Co/Schrader-Bridgeport & August France

Pierer Industrie Ag/ Pankl Racing Systems

Zhejiang Geely Royal Engine/Ningbo Umd

20 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

20

L'Automotive segue l'organizzazione di filiera, in cui la testa è tipicamente il costruttore e grandi OES rappresentano snodi chiave

> Passengers per uso urbano / periurbano / commuting

• Transportation - W. Europe

Domanda finale

> Passengers per media-lunga distanza

> PaC

> Powertrain

> Chassis

> Exteriors

> Interiors

> Infotainment

> Coach / bus

> Metro

> …

Building block industriali – Filiera e catena di fornitura rilevante - Illustrativo

1. Driver assistance systems

2. Braking systems

3. Axles

4. Suspension systems

5. Wheels

6. Electronic braking assistant components

7. Tires

8. Steering systems

9. Parking brake

10. Active Front Steering

11. Pedals

12. 4-wheel steering

OEM

OES

Esempio: fornitore fastening systems

Fonte: Roland Berger

Esempio di filiera

Estratto dominii applicativi

21 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

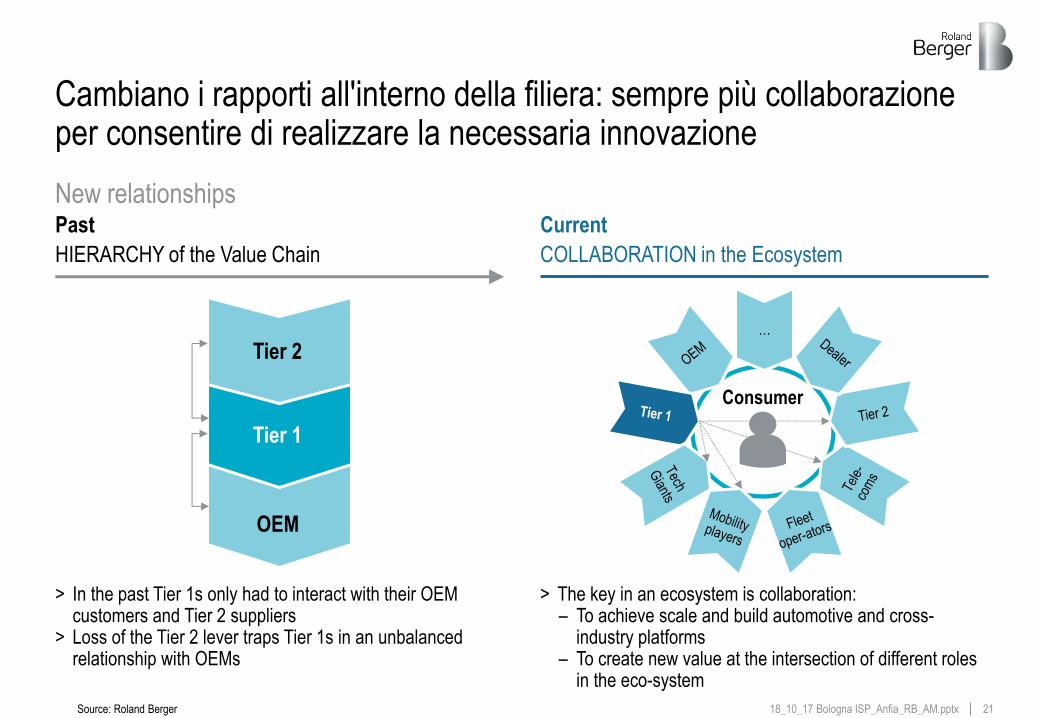

Cambiano i rapporti all'interno della filiera: sempre più collaborazione per consentire di realizzare la necessaria innovazione

New relationships Past

HIERARCHY of the Value Chain

> In the past Tier 1s only had to interact with their OEM customers and Tier 2 suppliers

> Loss of the Tier 2 lever traps Tier 1s in an unbalanced relationship with OEMs

Current

COLLABORATION in the Ecosystem

> The key in an ecosystem is collaboration: – To achieve scale and build automotive and cross-

industry platforms – To create new value at the intersection of different roles

in the eco-system

Tier 2

Tier 1

OEM

Consumer

…

Source: Roland Berger

22 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

La generazione di cassa e la sua allocazione condizionano la futura competitività dei fornitori: finanza di filiera come strumento abilitante

Capacity rightsizing

Target cost budget

Purchasing excellence

Lean overhead

Operational efficiency

Current cost

runrate

R&D efficiency

Maximize resource generation (efficiency) Strategically allocate resources (effectiveness)

Reduce cost and improve output adapting to lower volumes and higher competitive pressure

Generate additional cash by strategically focusing spending on the right products, investments and R&D activities

Target cash flow

Focus R&D on key segments

Rethink investments

Active portfolio management

Cash flow budget 2018

Reduce operational cost base Strategically rethink cash allocation

Supplier performance improvement – Main levers and budget impact

Source: Lazard, Roland Berger

23 18_10_17 Bologna ISP_Anfia_RB_AM.pptx

Agenda

This document shall be treated as confidential. It has been compiled for the exclusive, internal use by our client and is not complete without the underlying detail analyses and the oral presentation.

It may not be passed on and/or may not be made available to third parties without prior written consent from .

© Roland Berger

Q&A

C

Conquistare la solidità finanziaria, prerequisito per la competitività

Sfide per i fornitori Auto

B

Verso la disruption nel settore Auto

Scenario di riferimento

A

5' Tempo

'10 Tempo

'10 Tempo