Austria - Country Presentation (Full)

31

© www.igd.com/analysis Country Presentation Austria Updated March 2011

Transcript of Austria - Country Presentation (Full)

© www.igd.com/analysis

Contents

Map

Demographics

Political Outlook

Economic Overview

The Retail Market

Europanel Data

Top Retailers

Challenges and Opportunities

Retailers covered include:

© www.igd.com/analysis

Area: 83,879 sq. km

Capital City: Vienna

National Currency: Euro

Population (2010):8.37 million inhabitants

Population Density: 99 people/km

President: Heinz Fischer

Ruling Party:SPÖ-ÖVP coalition

Chancellor of Austria: Werner Faymann

Source: CIA, Statistik Austria

Country Facts

© www.igd.com/analysis

Demography: Populations of States

Region Population Area (sq km) Population Density

(people/km)

% Total Population

Vienna 1,698,822 415 4,097 20.3

Lower Austria 1,607,976 19,186 84 19.2

Upper Austria 1,411,238 11,980 118 16.8

Styria 1,208,372 16,401 74 14.4

Tyrol 706,873 12,640 56 8.4

Carinthia 559,315 9,538 59 6.7

Salzburg 529,861 7,156 74 6.3

Vorarlberg 368,868 2,601 142 4.4

Burgenland 283,965 3,962 72 3.4

Source: Statistik Austria 2010

© www.igd.com/analysis

Demographics

Source: Statistik Austria 2010www.igd.com/analysis/datacentre

Population Split by Age, 2009 (%)Population Growth Forecast (000’s)

15.0 17.5

67.5

© www.igd.com/analysis

Political & Economic Outlook

The good working relationship between the Social Democratic Party and the Austrian People’s Party will sustain their grand-coalition government

Austria should continue to build on its good relations with the newer EU member states and support the EU's expansion to the western Balkans, particularly Croatia but it remains strongly opposed to Turkish EU membership

Being small, Austria has traditionally been an open, export-oriented country. Its strength lies in its small and medium-sized companies, many of them family-owned, that make highly specialised, top-quality products and export them all over the world

World trade recovery to pre-crisis levels along with the strong economic growth of Germany - Austria’s main trade partner - driven the Austrian economy to grow over the course of 2010

The rapid economic recovery is likely to continue. For 2011 Austria expects economic growth of 1.6%, with a plus of up to 2% forecast for 2012

Unemployment has not risen as steeply as in other European countries, partly due to government intervention with subsidised programmes for employers

Due to continued positive development on the labour market, private consumption is expected to remain stable and move upward

© www.igd.com/analysis

Economic Overview

2007 2008 2009 2010 2011e

GDP (Nominal €bn) 272.0 283.1 274.3 283.5 292.6

GDP Growth (%) 3.55 2.05 -3.82 0.3 1.59

GDP per Capita (€) 32,851 34,148 33,051 34,077 35,126

Unemployment(%) 4.40 3.80 4.80 4.13 4.20

Consumer Price Inflation (%) 2.20 3.22 0.40 1.50 1.74

Food Price Inflation (%) 2.20 3.20 0.40 1.69 3.20

Source: IGD Datacentre, IMF Statistics 2011 www.igd.com/analysis/datacentre

© www.igd.com/analysis

Grocery Retail Market Sizes 2010

Top 10 Western European Markets Top 10 Global Markets

Source: Retail Analysis Datacentre

Country Grocery Retail Market(€bn)

1. France 208.17

2. Germany 162.46

3. United Kingdom 161.96

4. Italy 129.56

5. Spain 97.05

6. Switzerland 39.77

7. Belgium 34.92

8. Netherlands 34.46

9. Sweden 24.55

10. Greece 23.72

12. Austria 20.85

Country Grocery Retail Market

(US$bn)

1. USA 881.84

2. China 789.91

3. Japan 359.96

4. India 350.38

5. Brazil 289.92

6. France 276.04

7. Russia 256.38

8. Germany 215.43

9. United Kingdom 214.60

10. Italy 171.80

37. Austria 27.65

© www.igd.com/analysis

The Retail Market

Source: IGD Datacentre 2011 www.igd.com/analysis/datacentre

2007 2008 2009 2010 2011e

Consumer Spend (€bn) 146.61 153.43 152.25 156.50 161.22

Total Retail Market (€bn) 47.87 49.48 50.30 52.08 53.73

Grocery Retail Market (€bn) 18.81 19.60 20.13 20.85 21.54

Grocery Retail Spend / Capita (€)

2,272 2,365 2,425 2,506 2,586

Grocery as a % of Retail 39.3% 39.6% 40.0% 40.0% 40.0%

IGD Grocery Retail Market corresponds to the total annual turnover (excluding VAT) of retail outlets predominantly selling food. It includes the sales of non-food articles (i.e. health & beauty, pet care, clothing, DIY etc) sold by hypermarkets, supermarkets, discounters, neighborhood stores, specialised food stores (bakeries, butchers, etc) and open markets. It excludes all cash & carry, delivered wholesale, foodservice and drugstores/chemists

© www.igd.com/analysis

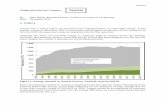

Retail Consumer Spend Per Capita Austria

Source: IGD Datacentre 2011www.igd.com/analysis/datacentre

© www.igd.com/analysis

The Grocery Retail Market – Structure By Format

The most significant change in the market over the past decade has been the decline of the superettes and traditional grocers, as the major retailers have become a more dominant force

The Austrian grocery industry is a highly concentrated market where the three largest retail players account for approximately 67% percent of the total sales volume

The Austrian market is dominated by German retailers, largely due to the linguistic, cultural and historical links between the two countries

Rewe International - the Austrian-based affiliated company of the German Rewe Group - is the number one on the domestic market ahead of Spar Austria and Hofer

The hard discounters Hofer and Lidl have an overall market share of around 18 per cent. Both retailers grew strongly between 2003 and 2007 before their performance stagnated

There is still a general ban on Sunday trading, although this is lifted in some major tourist areas

© www.igd.com/analysis

Top Grocery Retailers 2010

Source: IGD. Note: excludes Cash & Carry and members club operations

Retailer Grocery Sales(€m)

% Change Grocery Sales

09-10

IGD Grocery Retail Market

Share (%)

No. of Grocery Stores

Rewe Austria 5,744 +0.3% 27.5% 1,926

Spar Austria 5,129 +4.5% 24.6% 1,463

Hofer (ALDI) 3,204 +3.9% 15.4% 430

Markant Austria 1,005 +9.0% 4.8% 1,434

Tengelmann 648 +3.6% 3.1% 330

Lidl 606 +5.0% 2.9% 215

M-Preis 540 +7.3% 2.6% 187

www.igd.com/analysis/datacentre

© www.igd.com/analysis

Market Share - Austria

2009 2010 2011e

Rewe Austria 28.4% 27.5% 27.4%

Spar Austria 24.4% 24.6% 24.8%

Hofer (Aldi) 15.3% 15.4% 15.4%

Markant 4.6% 4.8% 5.0%

Tengelmann 3.1% 3.1% 3.1%

Lidl 2.9% 2.9% 3.0%

M-Preis 2.5% 2.6% 2.7%

Austria Market Share - 2010

Source: IGD Market Share. The methodology is detailed at the end of this presentation

www.igd.com/analysis/datacentre

© www.igd.com/analysis

Banner Total Sales(€m) Format No. of Stores Sales Area

(sqm)Av. Sales Area

(sqm)

Billa, Merkur 4,102 S/S 1,120 1,240,000 1,107

Adeg 760 C/F 482 n/a n/a

Penny 695 H/S D 302 166,100 550

Magnet 187 H 22 65,494 2.977

Bipa 602 H&B 571 142,750 250

Rewe entered the Austrian market in 1996

In Austria, Rewe operates several retail chains: supermarkets Billa and Merkur, discounter Penny, health & beauty chain Bipa and convenience stored Adeg

Rewe has a minority share in Sutterluetty, a small independent food retailer

www.igd.com/analysis/datacentre*Note= Rewe’s consolidated sales from these operations.

Key: C/F = Convenience/Forecourt, H/S D= Hard/Soft Discount, S/S = Superstore/Supermarket, H = Hypermarket

H&B = Health & Beauty

© www.igd.com/analysis

In 2010, Rewe’s chains Billa, Merkur and Bipa grew strongly, while Penny and Adeg had weaker performance

Rewe Austria is progressively upgrading its Merkur stores, including improving the presentation islands for its fresh food, convenience and organic ranges

In April 2010, Rewe announced it was placing increased focus on traceability and local sourcing for many of product ranges in its Billa format in Austria

Rewe plans to develop its retail chain Adeg. It will introduce a modern shopping concept and comprehensive trainings for store managers in order to attract customers

© www.igd.com/analysis

The new Adeg private label range "Adeg mit Leib und Seele“ was launched in January 2011 and aimed to boost the regionality of Adeg

All products under the brand "Adeg mit Leib und Seele“ originate from Austria. The range was launched with 11 products and will be extended up to 100 SKUs in the near future

In February 2011, Rewe introduced its new standard umbrella PL range at Billa, which will replace the existing Quality First label and some branded products�

“Billa” PL products was started with dairy products. Rewe plans to launch 250 SKUs in food categories only by the end of 2011

“Billa” products are 10-20% cheaper than the equivalent brand products and claim to have the same quality as brands

Billa’s private label share is approx 20% from total sales

© www.igd.com/analysis

Banner Total Sales (€m) Format No. of Stores Sales Area

(sqm)Av. Sales Area

(sqm)

Interspar1,017 H 64 160,640 2,510

Eurospar / Spar 4,100 S/S 1,367 862,577 631

Spar Express 12 C/F 11 1,551 141

Source: IGD Datacentre 2011

Austria has been a member of International Spar since 1954

In 1970, Spar Österreichische Warenhandels-AG was established, through the merger of all 10 existing wholesale companies

Spar Austria is the largest privately owned company in Austria

The majority of the Spar Austria stores are owned by independent retailers

Key: S/S = Superstore/Supermarket, H= Hypermarket, C/F = Convenience/Forecourt

www.igd.com/analysis/datacentre

© www.igd.com/analysis

Spar, ViennaDuring the last few years, Spar Austria has modernised and increased the selling area of a significant number of both independent retailer and company-owned shops

There has been a particular emphasis on fresh foods and local sourcing in hypermarkets, offering customers a comprehensive range of fresh products, cheese, fish, meat and snacks

Spar offers multi-tier private label ranges, consisting of approx 3,000 products under various the PL brands in different categories and price segments (S-Budget, Spar, Spar Natur, Spar Vital, Spar Premium etc). PL share is 34% from total sales

Spar’s priorities in 2011:

Further expansion of convenience chain, with focus on high frequented city locations

Expansion of Interspar hypermarket format Source: Retail Analysis photo gallery

© www.igd.com/analysis

Interspar, SalzburgNew INTERSPAR hypermarket flagship store

In March 2010, a new INTERSPAR hypermarket flagship store was opened in Salzburg-Taxham. The store represents the new food marketplace concept in combination with non-food worlds, offering customers a modern shopping experience

Highlights of the store:

New floors and shelves, a clearly structured and optimised arrangement of the departments

Innovative lighting concepts for the improved presentation of products

Reduction of CO2 through innovations in energy saving freezing technologies

Improvement of fresh food departments, with strong focus on regional suppliers and regional food products offered at service counters

Source: SPAR

© www.igd.com/analysis

Banner Total Sales (€m)

Format No. of Stores

Sales Area (sqm)

Av. Sales Area (sqm)

Hofer 3,204 H/S D 430 301,000 700

ALDI Sud entered Austria in 1967 with the acquisition of the Hofer chain

Austria is ALDI's second most important market in Europe, after Germany

Aldi operates seven regional divisions. Each serve between 40 to 70 stores and are located at Hausmannstaetten, Rietz, Sattledt, Stockerau, Trumau, Weissenbach and Loosdorf

Key: H/S D = Hard/Soft Discount

www.igd.com/analysis/datacentreSource: IGD Datacentre 2011

© www.igd.com/analysis

Hofer offers 850 basis SKUs and 30-40 promotional SKUs, which rotate twice a week

Hofer continuously extends its service offers from mobile phones, videos and photo development. It views financial services as an opportunity, and is also looking to extend the range of holiday and travel services it offers

In 2010, Hofer opened 30 Diskont petrol stations in its store car parks in all regions of Austria. There are plans to open another 70 petrol stations until the end of 2012

Hofer’s assortment consists mostly of private labels. Company’s strategy is to avoid listing brands where possible

Hofer seeks to differentiate its offer by introducing its own organic private label range ‘Zurueck zum Ursprung’

Source: Retail Analysis photo gallery

© www.igd.com/analysis

Banner Total Sales(€m)

Format No. of Stores Sales Area (sqm)

Av. Sales Area (sqm)

Markant 1,005 S/S 1,434 616,620 430

Nah & Frisch 431 C/C 39 132,600 3,400

Source: IGD Datacentre 2011

Key: S/S = Superstore/Supermarket, C/C= Cash & Carry

Markant Austria is a member of EMD. Set up in 1969 as a buying cooperative for family-owned businesses, it aims to guard the independence of small and medium-sized traders in Austria

There are 36 member retailers, which include:

www.igd.com/analysis/datacentre

© www.igd.com/analysis

There are 12 operational shareholders, including grocery retailers and drugstores. The key grocery players are:

ZEV-Markant independent retailers operate individual fascias and the ‘Nah & Frish’ banner

Pfeiffer/Unimarkt is the largest group within the cooperative, following the acquisition of Hornig in 2005 and the subsequent expansion of the Unimarktfranchise chain

Group’s priorities 2011:

Main focus is to continue to grow the size of its network across Austria

Concentration of the resources on the local customer approach

Pfeiffer Handel GmbHBrückler Grosshandelsges mbHWien Kastner Großhandels Ges. mbH, ZwettlJulius KiennastWedl & Dick Ges mbH

© www.igd.com/analysis

Banner Total Sales(€m)

Format No. of Stores

Sales Area (sqm)

Av. Sales Area (sqm)

Zielpunkt (Plus) 648 H/S D 330 161,370 489

Kik, OBI 455 O 325 315,106 970

Key: H/S D = Hard/Soft Discount, O = Other non-grocery

Tengelmann entered the Austrian market in 1976

In Austria, Tengelmann used to operate discount stores under the fascia of Zielpunkt

In May 2010, Tengelmann decided to sell Zielpunkt to the Luxembourg-based investment funds bluO. Zielpunkt was Tengelmann’s last foreign discount subsidiary

bluO plans to further operate the company under the name Zielpunkt

Tengelmann continues to operate its Kik textile discount chain and OBI DIY stores in Austria

www.igd.com/analysis/datacentreSource: IGD Datacentre 2011

© www.igd.com/analysis

Banner Total Sales (€m)

Format No. of Stores Sales Area (sqm) Av. Sales Area (sqm)

Lidl 606 H/S D 215 139,750 650

Lidl established its Austrian office in 1994 and opened its first stores in November 1998, over 30 years after Aldi’s market entry

This late entry means that Lidl still has a relatively small share of the Austrian market

Key: H/S D = Hard/Soft Discount

www.igd.com/analysis/datacentreSource: IGD Datacentre 2011

© www.igd.com/analysis

Lidl currently operates approximately 200 stores in Austria, which are served from distribution centres near Salzburg, northern Austria, and Müllendorf, south of Vienna

Lidl offers an average of 1,300 SKUs in its Austrian outlets. Its assortment comprises private labels, brands and local/regional products

The Austrian operations are being used as the base from which to expand into the Balkan States, including Slovenia and Croatia

The new distribution structure may well be used to support European distribution into Eastern Europe, rather than simply to support activity in Austria

In December 2010, Lidl started to offer low-cost ticket cards worth EUR 73 in cooperation with the German railway operator Deutsche Bahn

Source: Retail Analysis photo gallery

© www.igd.com/analysis

Banner Total Sales (€m)

Format No. of Stores

Sales Area (sqm)

Av. Sales Area (sqm)

Super M 34 H 9 22,500 2,500

MPREIS 506 S/S 178 267,000 1,500

MPREIS is a regional, family-owned operator with a strongly differentiated concept. Created by Therese Mölk in the 1920s, the company prides itself in its human values and aspiration for quality

Based in Tyrol, MPREIS works closely with local suppliers to create a unique and differentiated offer for its customers

MPREIS offers an average of 10,000 SKUs, which includes 500 organic SKUs and 2,000 regional products from Tyrol

The retailer is also well-known for its architectural stance and has been dubbed the ‘Sexy Supermarket’

Each store is designed by a different architect and includes the use of environmentally friendly materials

Source: IGD Datacentre 2011 Key: S/S = Superstore/Supermarket, H= Hypermarket www.igd.com/analysis/datacentre

© www.igd.com/analysis

Banner Total Sales (€m)

Format No. of Stores

Sales Area (sqm)

Av. Sales Area (sqm)

METRO C&C 793 C&C 12 95,604 7,967

Media Markt, Saturn 1,078 O 42 131,628 3,134

Key: C&C = Cash & Carry, O = Other non-grocery

METRO C&C entered the Austrian market in 1971

METRO C&C stores are in average 8,000sqm and offer an assortment of more than 48,000 SKUs

Metro also operates its Media Markt consumer electronics chain in Austria

In 2010, Media Saturn announced the acquisition of 7 new locations of which 4 are former branches of the Austrian bankrupted Cosmos chain

METRO priority for 2011 is to expand by developing delivery services and strengthening own brands

www.igd.com/analysis/datacentreSource: IGD Datacentre 2011

© www.igd.com/analysis

Challenges and Opportunities

The fight for market leadership is between Rewe and Spar Austria

Discount supermarkets in Austria are struggling to increase their market share

In Austrian grocery retailing the price has been the main point of distinction between the players in the market for some years

In light of increasing price competition, retailers will need to differentiate their trading strategies to move the focus away from pure price

There is currently a push amongst all retailers for organic / regional / local food products in a bid to build customer loyalty. All the major players now carry their own organic private label ranges, as consumers expect to find organic products in store

Sustainability will continue to be an important part of the retail sector in Austria

© www.igd.com/analysis

IGD Market Share Methodology

IGD has a single, universal methodology to enable comparisons of market shares and consolidation levels between countries. It is calculated by comparing retailers’ sales from grocery formats with IGD’s grocery retail market size.

IGD defines the grocery retail market as all food, drink and non-food products (e.g. health & beauty, pet care, clothing, DIY) sold through all retail outlets selling predominantly food in a given country.

This definition includes both modern retail formats such supermarkets and hypermarkets, and traditional retail formats such as open air markets and traditional food stores such as bakers. However, it excludes Cash & Carry operations and drugstores/pharmacies and sales tax.

IGD market sizes are ‘top down’, derived from national statistical bodies wherever possible. In all other cases, the figures published in this report represent IGD estimates and are based on a consistent methodology and knowledge of local markets.

For each retailer, the turnover used is total sales from grocery format, and therefore excludes non-food formats (such as DIY, electrical stores, department stores etc). IGD also exclude Cash & Carry formats and drugstores/pharmacies from this measure, to ensure the data sources are comparable; 1.Retail turnover is excluding VAT 2.Retail turnover is excluding non-food formats (e.g. furniture, electrical stores etc) 3.Cash & Carry operations are excluded 4.Where known, we have subtracted the Cash & Carry operations of players such as Carrefour

and Rewe to use a pure grocery retail estimate of turnover.

IGD’s market shares differ from panel-based or till-roll markets shares (e.g. from ACNielsen, TNS or IRI) due to the different methodologies; the latter are based on limited categories/retailers.

© www.igd.com/analysis

For More Information

Visit the Austria hubpage on Retail Analysis

Use the IGD Datacentre for key macroeconomic data on Serbia, plus statistics on retailers’ operations by banner and format

Visit the photo archive for images of retailers operating in Czech Republic

Got a MyReports subscription? Try checking our International Research reports

To find out how an IGD Customised Briefing can bring you up to speed on the market and the key players, email [email protected]

Still can’t find what you’re looking for? Contact us [email protected] or 01923 857141