ATM working group - webarchive.nationalarchives.gov.uk/http:/... · 5 1 Introduction Background 1....

74

ATM working group Cash machines – meeting consumer needs

Transcript of ATM working group - webarchive.nationalarchives.gov.uk/http:/... · 5 1 Introduction Background 1....

ATM working group

Cash machines – meeting consumer needs

Published on 13 December 2006

ATM working group

Cash machines – meeting consumer needs

1

Contents

Report Page

Summary 3Letter from John McFall MP, Chairman of the ATM working group, to Ed Balls MP 3

1 Introduction 5Background 5The Treasury Committee’s inquiry into cash machine charges 5Remit of the ATM working group 7Membership of the working group 7

2 Financial inclusion 9Introduction 9Evidence and analysis 9

Total numbers of free cash machines 9Total numbers of charging cash machines 9Distribution of free cash machines 10The distribution of free cash machines and financial inclusion 11Evidence from the CAB Service 12Free of charge cash withdrawals and the Post Office 12Other sources of free-of-charge access to cash 13

IMPROVING ACCESS TO FREE-OF-CHARGE CASH MACHINES 15Private sector contribution 15Paying a premium to cash machine operators in lower-income areas without other free-of-charge machines 17

Public sector contribution 18Action by local communities and individual landlords 21PRACTICAL STEPS AND MONITORING PROGRESS 23

3 Transparency of charges 25Introduction 25Evidence 25Proposals for improved transparency 27

On-screen signage 28External signage 29An enduring solution 31

Signage at free machines 32

4 The future of the free cash machine network 33

5 Maps 34Clusters of low-income areas without convenient access to free cash machines 56Individual ‘super output areas’ without convenient access to free cash machines 60

6 Contact details of banks, building societies and independent operators 64

2

Appendix 1: Example on-screen charging notices 67

Appendix 2: Examples of the standardised external charging notice 68

Appendix 3: Example of signage at a free cash machine 69

3

Summary

Letter from John McFall MP, Chairman of the ATM working group, to Ed Balls MP

I attach a copy of the report from the ATM working group.

The working group has examined what we can do to give low-income communities the best possible chance of having access to cash without facing charges that they are least well placed to bear. And where charges are applied, how we can be sure consumers are provided with clear up-front information. The working group noted the importance of basing its proposals on credible evidence. In the working group, I have had a constructive dialogue with banks, building societies, consumer groups, independent cash machine operators and the Post Office.

Regarding financial inclusion, this report details the systematic analysis undertaken by LINK to identify low-income areas that currently lack access to free cash machines. This report lists all those low-income areas that do not currently have such access. The working group considered that the focus should be on the breadth of coverage of the free cash machine estate rather than simply the aggregate number of free or charging machines.

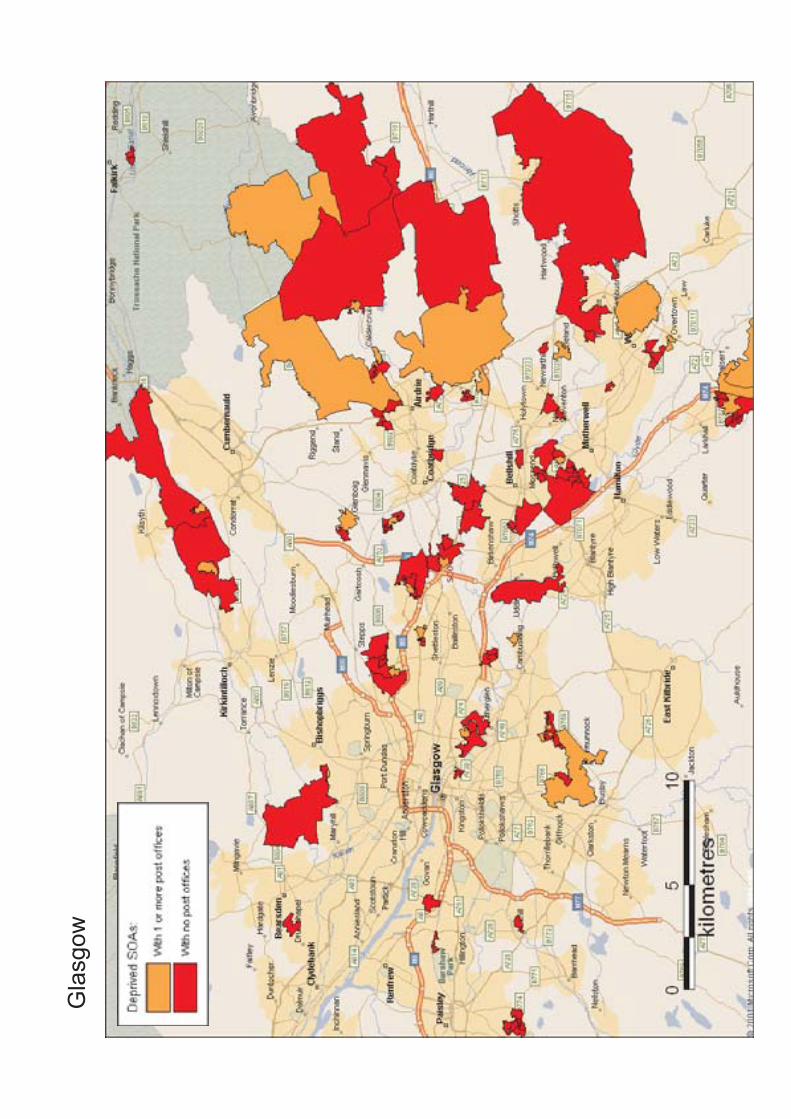

A number of banks, building societies and independent operators as well as the Post Office have committed to install free machines to expand provision into the areas identified in the research. I warmly welcome this positive response. Other banks continue to provide their customers with free-of-charge cash withdrawals using their bank cards over the counter in the post office branches which already exist in many of these target areas.

To underpin and support these individual commitments the working group recommended and LINK members have agreed to the introduction of a ‘financial inclusion premium’ that will provide a long-term and enduring incentive for ATM operators to expand the availability of free cash machines in low-income areas that currently lack them and also help protect free machines where they are the only such ATM in these areas. The introduction of the financial inclusion premium will use the market forces that already shape the deployment of free cash machines to achieve and sustain an important public and social policy objective. I believe that this is the first example of such an innovative approach anywhere in the world.

The Public sector can help achieve the goal of deploying free cash machines in areas that currently lack access. In particular, a joined-up policy for planning permissions between central Government, local authorities and the police is essential if ambitions to provide significantly more communities with access to free cash machines are to be achieved in a timely and cost-effective manner. The Government should also consider how the introduction of rate relief could help achieve the desired public policy objective. The working group hopes that the Treasury and the Government will encourage local authorities and other public sector landlords to consider whether they can assist their local community by offering to house a free cash machine.

Critical to achieving the objective of deploying additional free cash machines will be

4

identifying appropriate sites. Local knowledge can make an invaluable contribution. The report details many successful examples of partnerships between local community groups and banks to help find sites for free cash machines. The working group encourages community groups, local authorities, Citizens Advice Bureaux, credit unions, sub-postmasters, small businesses and others to help identify suitable sites.

By working together in this way, I am hopeful that we can accomplish a significant expansion of free cash machines in low-income areas, helping these communities to thrive by ensuring local availability of the cash that is so vital to local economic activity, and so helping to promote financial inclusion.

Concerning the transparency of cash machine charges the working group sought to agree a lasting solution that builds on the progress made and experience gained over the past few years. The objective has been to enable consumers to see at a glance whether a machine is free or charging. The working group’s new proposals incorporated into LINK rules earlier this month were based on consumer research and will extend the best practice established by some of the charging machine operators across all the UK’s charging machines.

The working group recommends the provision of clearer on-screen information, together with larger and standardised external signage. The working group has recommended a timescale for implementing this change that seeks to minimise unnecessary costs that would otherwise fall on the users of these machines and recognises the investment made by those charging operators that already exceed the new minimum standards. The new rules, properly implemented and enforced, should provide a robust and enduring standard which satisfies all stakeholders.

5

1 Introduction

Background

1. The UK’s first cash machine, also known as an Automated Teller Machine (ATM) was installed by Barclays bank in its Enfield branch in 1967. Withdrawal from a cash machine is now the most important method of cash acquisition by consumers. Nearly two thirds of adults are regular cash machine users and in 2005 cash machines dispensed over £172 billion. Usage of cash machines by benefit recipients has increased as the Government has moved towards the direct payment of benefits into bank accounts. Despite the increasing use of credit and debit cards as a method of paying for goods and services, the number of transactions at cash machines is expected to continue to grow.

2. In the UK there are currently two main methods of funding the provision of cash machines. The first type of machine is free at the point of use and funded through a system of interchange fees which are paid by the card issuer to the operator of the ATM. For example, if a customer of Barclays uses a cash machine owned by Lloyds TSB to make a free cash withdrawal then Barclays will pay Lloyds an ‘interchange fee’ for this service. Machines which are free at the point of use will typically be those machines in bank branches or in busier non-branch locations which attract a relatively high volume of transactions each month. The second type of machine is known as a convenience or charging machine. These machines are funded through direct charges to consumers. These machines will typically operate at a lower volume than machines which are free to use and are therefore able to be placed in locations that may not support the provision of a free-to-use machine. As acknowledged by the Government, the Treasury Committee and consumer groups, in a competitive market, it is appropriate that a variety of models exist to fund cash machine provision.

3. The LINK network enables cardholders to obtain cash and obtain balance information from all ATMs in the country. LINK has two constituent parts, the LINK company and the LINK scheme. The LINK company operates the technical infrastructure that allows the network of cash machines in the UK to operate. The LINK scheme is open to every ATM operator and card issuer in the UK and all major UK retail credit institutions, as well as a number of independent ATM operators are members. The LINK scheme sets the rules, practices and procedures for the operation of cash machines, and, in accordance with competition law, the level of the interchange fee. The scheme seeks to ensure universal, reliable and secure access to cash and maintains and enforces rules covering technical standards, interchange fees, signage and other issues. LINK does not itself deploy ATMs, choose where they are deployed or whether and how much they charge. These decisions are properly made by the individual banks, building societies and independent ATM operators that are members of the LINK Scheme.

The Treasury Committee’s inquiry into cash machine charges

4. In December 2004, following concern regarding the growth in the number of charging machines and some sales by banks of free machines to charging operators, the Treasury Committee announced an inquiry into cash machine charges. The Committee examined the principle of charging and the increasing prevalence of machines at which a charge is levied, the clarity of the presentation of these charges to the consumer and concerns over

6

the impact that the spread of charging might be having on financial exclusion and low-income households. The Committee took evidence from consumer groups, high-street banks and building societies, the Post Office, leading independent operators of charging cash machines, LINK and the then Financial Secretary to the Treasury, Stephen Timms MP.

5. The Committee’s Report1, which was published in March 2005, concluded that “cash machines which charge consumers are a legitimate business model” but that their spread could raise public policy concerns if they displaced existing free machines. The Committee expressed concern that “free access to cash withdrawals could decline as banks sell or close their existing network and the remaining machines become concentrated in fewer locations”.2 The Committee concluded that “This will lead to public policy concerns if areas of the country are left without access to free cash withdrawals—particularly if this exacerbates existing financial exclusion”.3 The Committee noted that whether this occurred would depend partly on the attitude of the banks, the Post Office and local site owners. The Committee called on the Government and the financial services industry to conduct research into the geographical location of free cash machines. Regarding the transparency of charges the Committee concluded that the industry had a duty to “provide consumers with sufficient information to allow an informed choice about whether to use a charging machine” and that “poor standards of transparency are detrimental to consumers and hinder competition”.4 The Committee welcomed improvements to transparency agreed by LINK in December 2004 but concluded that they did not go far enough.

6. At a debate on the Treasury Committee’s report held in Westminster Hall on 16 February 2006, the Chairman of the Treasury Committee, the Rt Hon John McFall MP called for a serious and systematic analysis of the geographical location of free cash machines to discover which low-income areas lacked access. He called for the banks to expand provision of free cash machines into any under-served low-income areas identified by the research. He noted that the LINK interchange fee arrangements could lead to the concentration of free cash machines in fewer locations and called on the banks to examine how they could alter the situation. On transparency of charges, he welcomed the improvements instituted by LINK but called for further improvements so that consumers could see “at a glance” whether a machine was free or charging.

7. In his response to the debate in Westminster Hall the then Economic Secretary to the Treasury, Ivan Lewis MP offered to organise a meeting between members of the Treasury Select Committee, key representatives of the banks, independent cash machine operators, consumer groups and members of the financial inclusion taskforce.

8. His intention was that:

Rather than holding parallel debates—perhaps firing shots across each other’s bows—we should get together in the interests of all consumers, particularly

1 Treasury Committee, Fifth Report of session 2004-05, Cash Machine Charges, March 2005, HC 191

2 Ibid, para 63

3 Ibid, para 64

4 Ibid, page 4

7

financially excluded communities and vulnerable consumers, and see whether we can reach a consensus.5

9. This meeting was held on 4 May 2006. At this meeting John McFall MP said that:

I see this as a good opportunity to take stock of the progress made in the year since the Treasury Committee’s report into cash machines and to identify areas in need of further improvement. I want to work with banks, consumer groups and charging cash machine operators to develop proposals and to resolve the issues of transparency of signage and financial inclusion. I propose a working group be established, which I will chair, to examine these issue and report back to the Economic Secretary.

10. The Economic Secretary agreed with major banks, consumer groups and charging cash machine operators that this working group should gather evidence and report back before Christmas. On 5 May 2006, Ed Balls MP was appointed Economic Secretary to the Treasury. He indicated that the working group process had his full support.6

Remit of the ATM working group

11. At its first meeting the working group agreed to focus and deliver recommendations on two key issues: financial inclusion and the availability of free cash machines in low-income areas and the transparency of signage on charging cash machines. The working group noted that much of the debate on the availability of free cash machines in low-income areas had been based on anecdotal evidence. An overarching objective of the group was therefore to improve the evidence base on the growth and location of cash machines at the local level. The working group agreed the following remit.

Transparency of cash machine charges: Report on progress made in introducing clear information regarding the charges levied and suggest areas in need of further improvement.

The location of free and charging ATMs: To establish the facts about areas that currently lack access to free cash machines.

Changes to the LINK interchange arrangements: How the LINK interchange fee arrangements can be used to support the provision of free cash machines in financially excluded and low-income areas.

Whether it is possible to secure a commitment from the banks to keep cash machines free and to expand into any under-served areas identified by the research.

Membership of the working group

12. The working group recognised the importance of seeking a range of views. Membership consisted of

5 Hc Deb, 16 Feb 2006, Col 549WH

6 Speech by Economic Secretary to the Treasury, Ed Balls MP, to the British Bankers Association, 11 October 2006

8

Consumer organisations: Which?, the National Consumer Council and Citizens Advice.

Banks and building societies: Alliance and Leicester, Barclays, The Co-operative Bank, HBOS, HSBC, Lloyds TSB, Nationwide, and RBS.

Charging cash machine operators7 including Cardpoint and Hanco.

The LINK Scheme Director, Edwin Latter, who was also asked to represent the 22 other card-issuing institutions and 10 other independent ATM operators participating in the LINK network.

Post Office Ltd.

13. HM Treasury were present as observers.

14. The working group would also like to thank the independent members of the LINK consumer standing committee, including its Chairman Ken Andrew, Baroness Gibson of Market Rasen and Margaret Bloom for their contribution.

7 The Co-operative Bank and Alliance and Leicester also operate a number of charging cash machines.

9

2 Financial inclusion

Introduction

15. The working group divided its efforts into three strands.

16. Firstly it sought to undertake a comprehensive and systematic analysis of the distribution of free cash machines in low-income areas. This analysis found a small but significant proportion of low-income areas without convenient access to free-of-charge cash machines.

17. Secondly, on the basis of that evidence and analysis on the scale of the issue, the group considered potential solutions. It concluded that a combination of action by individual banks, building societies and other ATM operators, adjustments to the LINK Scheme’s rules on interchange fees to include a ‘financial inclusion premium’ increasing the viability of machines in low-income areas, support from the public sector, and engagement by local communities offered the best hope of addressing the issue in an effective manner.

18. Finally, the group considered how this plan could be implemented and progress monitored.

Evidence and analysis

Total numbers of free cash machines

19. There were 33,250 free cash machines in the United Kingdom at end-June 2006. While this represents an increase of around four thousand over the past five years, the rate of growth has slowed considerably. There was almost no change in the total number of free cash machines in 2005. There was a net increase of around 300 free machines in the first six months of 2006, with the effect of removals and occasional conversions of free sites to charging outweighed by the installation of new free machines and also by a small number of conversions from charging to free.

20. There had been no major sales of free cash machines by banks to charging operators since those reported in the Treasury Select Committee’s 2005 report. Where machines had converted from free to charging, this had often been due to the expiry of individual site-owners’ contracts with free cash machine operators, and the site owner’s preference for an alternative contract with a charging operator, principally because a higher rent was offered by the charging operator.

21. Overall, the group could not find any firm evidence that the aggregate number of free cash machines was likely to decrease.

Total numbers of charging cash machines

22. The number of charging cash machines had continued to grow since the Treasury Committee’s report, reaching 25,500 in June 2006. While the growth in the number of charging machines may tail off as this market also becomes increasingly saturated, further growth is expected in the near term.

10

23. Growth in the proportion of transactions that are charged has, however, been generally slower than the growth in the number of charging machines. The average number of transactions per charging machine has fallen from more than 17 per day in 2002 to around 13 per day in June 2006.8 Around 4% of cash withdrawal transactions were at charging machines in the first six months of 2006, a modest increase from the 3.6% figure reported to the Treasury Committee in respect of October 2004. The total number of free cash withdrawals had increased by around 16 million per month in the first six months of 2006 compared with the same period in 2004 (from 214 million to 230 million), and the total number of charged transactions had by around 2 million per month from 8 million to 10 million.

24. The growing number and proportion of cash machines that are charging does not of itself equate to deterioration in access to free-of-charge cash withdrawals. The installation of a charging cash machine only negatively affects free-of-charge access to cash if it replaces a free machine where there are no alternative free machines in the vicinity.9 The Treasury Committee recognised that charging machines are a legitimate business model, and that their introduction has increased the overall availability of cash and helped sustain small businesses. The installation of a charging machine where there has previously been no cash machine at all benefits those consumers who are prepared to pay the charge for the extra convenience of a withdrawal, without harming other consumers who prefer not to. The working group therefore focused not on the number of charging machines, but on the number of free cash machines and, most critically, the distribution and location of these machines.

Distribution of free cash machines

Changes in the distribution of free cash machines

25. The Treasury Committee expressed concern in its 2005 report that a substantial reduction in the availability of free machines could exacerbate financial exclusion. It observed that even if the overall number of free cash machines increased slightly, there might be greater concentration of those free machines in certain locations so that rises in overall numbers did not translate into an increase in generally available and genuinely different sites. The Committee was concerned that free machines would become clustered in fewer locations, while cardholders in low-footfall locations including poorer areas might be left without free machines, thereby aggravating relative disadvantage in these communities. The Committee recommended that research be conducted into the geographical distribution of free cash machines.

26. The working group sought to determine how the distribution of free cash machines might be changing over time given current market conditions, and also how the current distribution of free cash machines compared with indicators of deprivation.10

8 Free-of-charge cash machines attracted an average of 230 cash withdrawal transactions per day in June 2006.

9 Most charging machines had been deployed in locations where there was not previously a cash machine at all, though there were also some cases of sites losing free machines to be replaced by charging machines.

10 Data on changes in the free cash machine estate is published quarterly on LINK’s website (www.link.co.uk), together with the distances to the next nearest free machine and deprivation index details.

11

27. Published LINK figures show that in the first quarter of 2006, 51 machines were converted from free to charging. In the same period, 26 were converted from charging to free. 325 other free machines were removed, and 467 installed, leading to a net increase of 117 free machines.

28. Looking in more detail at the location of the free machines affected, 25 (49%) of the 51 converted to charging were more than 1 kilometre from the next nearest free machine, compared with 7 (27%) of those converted from charging to free. Of the 422 free machines removed 19 (7%) were more than 1 kilometre from the next nearest, as were 32 (8%) of the 521 new installations. Therefore, although the total number of free-of-charge cash machines did increase in the first quarter of 2006, the number of solo machines more than 1 kilometre distant from the next nearest actually decreased slightly.

29. In the second quarter of 2006, 23 sites converted from charging to free, and 44 from free to charging. 327 other free machines were removed, and 542 installed, leading to a net increase of 194 free machines.

30. The working group was reluctant to draw firm conclusions on the basis of the first two quarters of 2006. It was difficult to distinguish a decisive trend, and changes were relatively small compared with the total size of the free ATM estate – over 33,000 machines. This analysis showed, however, that tracking overall numbers of free machines did not necessarily indicate whether access to free-of-charge cash machine withdrawals was expanding. Continued production and publication of data on changes in the distribution of the free cash machine estate would enable more accurate analysis over the coming years.

The distribution of free cash machines and financial inclusion

31. The working group sought to establish the extent of any material gaps in access to free-of-charge cash machines in low-income areas. Comparing LINK data on the distribution of cash machines with the Index of Multiple Deprivation (published by the Department for Communities and Local Government) enables an assessment of how many low-income areas do not have convenient access to free-of-charge cash machine withdrawals.

32. This Index splits the country into approximately 40,000 “super output areas” with a population of around 1,400 in each area, and ranks these areas in terms of criteria such as income, employment, health, disability, education, skills and training, barriers to housing and services, crime and living environment. Where the population is highly concentrated, these areas can be small in geographical terms. Where the population is sparse, they can cover many square miles.

33. The working group focused on areas in the bottom quartile of the Index for England, Northern Ireland, Scotland and Wales respectively. Most low-income areas were relatively well-served by free cash machines, tending to have more free cash machines than more prosperous areas. One explanation for this could be the relative proximity of many relatively deprived areas to town centres. But 1,701 areas within the most deprived quartile (around 16%) had neither a free cash machine within the area, nor a free cash machine within 1 kilometre of the centre of the area. About 4% of the UK population live in such areas.

34. The full list of these areas and a variety of maps showing clusters of areas without convenient access to free cash machines (nationally and by region), as well as more detailed

12

maps of some regions where such areas are concentrated, are available in the Annex to this report.

35. Although the Index of Multiple Deprivation enables analysis at a very granular level, and the list of areas without free-of-charge access to cash is a long one on account of the inclusion of some very small areas, there are also inevitably some limitations to this statistical analysis. For example, although the ‘super output areas’ are often drawn to take account of natural boundaries such as rivers or motorways, it is not easy to take these into account when calculating average distances to the next nearest free cash machine outside the area. The distance to the nearest cash machine was calculated in a straight line—‘as the crow flies’. The distance to the nearest cash machine when travelling on foot by the most direct route is likely to be greater. The working group considered that the analysis could be complemented by those with local knowledge such as Citizens Advice Bureaux, community groups and local authorities.

36. The data also showed that slightly less than half of these areas without free-of-charge machines (47%) had charging cash machines. 31% had a Post Office branch within the area.

Evidence from the CAB Service

37. In March 2006, Citizens Advice conducted a month-long campaign with bureaux in England, Wales and Scotland to survey the prevalence and impact of charging cash machines. Bureaux were asked to identify both free and charging cash machines in their local area in an attempt to map areas that lacked access to free machines. The research identified over 75 areas which lacked access to free of charge cash machines.11 These included Chapeltown in Leeds; Muirhouse and Drylaw in Edinburgh; East Malling in Kent; and Lozells in Birmingham. Members of the working group welcomed this research, noting that it was based on the detailed local knowledge of individual Citizens Advice Bureaux.

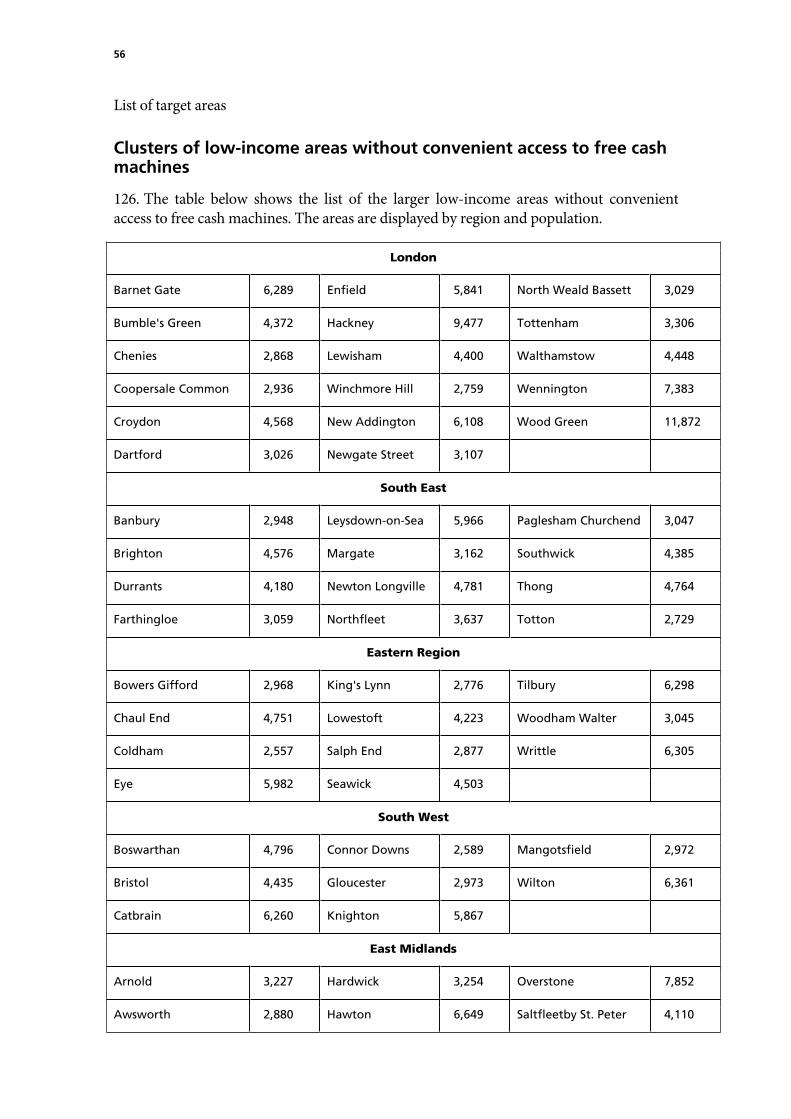

Free of charge cash withdrawals and the Post Office

38. 526 of the 1,701 areas without a free-of-charge cash machine currently have one or more Post Office branches. Post Office branches play an important role in free-of-charge access to cash.

39. A number of banks and building societies – including Alliance & Leicester, Bank of Ireland, Barclays, Clydesdale, The Co-operative Bank, Lloyds TSB, Nationwide Building Society, as well as cahoot, Smile, First Direct and National Savings and Investments – pay the Post Office to allow their cardholders to make free-of-charge cash withdrawals over Post Office counters. In addition all banks and building societies offering basic bank accounts allow some or all of their basic bank account holders free-of-charge cash withdrawals over Post Office counters. All new basic bank accounts include the service, though some older basic bank accounts, as well as other accounts offered by banks and building societies not listed above do not offer the service. In total around 40% of bank and building society customers with LINK-enabled cards are able to withdraw cash over Post Office counters, as are around 37% of basic bank account holders (including 100% of basic

11 Citizens Advice, Out of pocket, July 2006

13

bank accounts opened since April 2003). This means that of the 6.6 million basic bank accounts currently open, 2.6 million are accessible at the Post Office and 4 million are only accessible through ATMs and bank branches. In total, there are around 3 million free-of-charge cash withdrawals over Post Office counters using LINK cards every month.

40. Although working group members recognised that the Government review of the future of the Post Office network could lead to some branch closures, members of the group considered that the Post Office would continue to play a significant role in providing free-of-charge access to cash over the counter in rural and urban-deprived areas where there was currently no free-of-charge cash machine. The working group considered it important to draw attention to this option for many - though not all - account holders to make free-of-charge cash withdrawals over Post Office counters. This was a significant investment for the banks and building societies paying for the service, as well as for the Post Office. The more detailed maps, included as an annex to this report, identify which of those areas that have no free-of-charge cash machine are, however, currently served by a Post Office branch.

41. The Department for Work and Pensions (DWP) has confirmed that it will not renew its contract with Post Office Limited to provide the Post Office Card Account (POCA) when it runs out in 2010. While the precise details of replacement services for those customers currently receiving their benefits through the POCA are yet to be confirmed by government, the DWP has stated an intention to migrate people who currently use the POCA to receive their benefit payments to other bank accounts. As the DWP contacts the 4.5 million holders of Post Office Card Accounts about opening a bank account for receipt of benefits, it is important for the DWP to include information about which bank accounts provide the option of free-of-charge cash withdrawals over Post Office counters.

Other sources of free-of-charge access to cash

42. While cash machines are the most common method of accessing cash free of charge, and over-the-counter transactions at Post Office branches or bank and building society branches offer another alternative for eligible account holders, cashback at retail outlets such as supermarkets is a further option. There were 287 million cashback transactions in 2005.12

43. There are, however, certain limitations to the role cashback can play in providing free-of-charge access to cash in lower-income communities. Cashback is only available when a purchase is made, whereas the cardholder may not wish to make any purchase in the outlet at which cashback is available. Furthermore, retailers often do not accept use of cards for transactions under a certain minimum value. Cashback also requires both a debit card (with only four of the 17 basic bank accounts listed in the Financial Services Authority’s leaflet on basic banking providing a debit card) and a retailer that accepts the card (with consumers in some of the areas without access to free-of-charge cash machines tending to use local shops such as convenience stores which are less likely to offer cashback and may not accept any form of electronic payment). Furthermore, not all retailers accept the

12 In 2005, 8.2 million people used cashback, 2.4 million cashed a cheque to withdraw cash from a bank or building

society counter, 2.3 million made cash withdrawals using a passbook and 2 million workers were paid in cash. This compares with 33.8 million people using cash machines. £172 billion was withdrawn from cash machines compared with £7.2 billion through cashback and £20 billion using cards over the counter. For more information see UK Cash and Cash machine highlights, APACS 2006.

14

Electron and Solo cards that are offered with basic bank accounts even if they accept Maestro (formerly Switch) transactions.

15

IMPROVING ACCESS TO FREE-OF-CHARGE CASH MACHINES

44. The Treasury Committee, the Government and members of the working group attached importance to promoting financial inclusion. A cash machine can make an important contribution to economic activity in an area. Much of the cash withdrawn is likely to be spent in the vicinity. This is true of both charging and free cash machines, although free machines attract a significantly greater number of transactions than charging machines.

45. On the other hand it is neither economic nor feasible to have a free cash machine at every street corner or in every village. In some areas there will be a lack of suitable sites which allow sufficient public access and have acceptable levels of security for the machine and its users. In other places, for example a long stretch of relatively remote coastline, scattered population and consequent lack of demand may mean that is not economic to run any type of cash machine at any location within the area.

46. The working group’s analysis identified a total of 309 clusters of low-income areas where there was no free cash machine within a kilometre (these 309 clusters contained a total of nearly 1,300 ‘super output areas’). Outside of these clusters, there were a further 427 individual and smaller low-income areas—with an average population of 1440—which also had no free cash machine within a kilometre, although immediately adjacent areas did have access to free machines.

47. The working group estimated that around 400 cash machines would be enough to serve all the major population clusters if suitable sites could be found. But some of these clusters, or some parts of these clusters, were likely to prove unsuitable for cash machines because of a lack of suitable premises or scattered population. This was perhaps even more likely to be true of the 427 other smaller areas where there was currently no free cash machine provision. The working group estimated that perhaps around half of these 427 isolated areas might contain practicable sites for the installation of ATMs – so that a further 200 machines could potentially be deployed to meet the need for free-of-charge access to cash in these areas.

48. Although the working group was not in a position to make precise estimates until more of these areas had been visited, it therefore calculated that a total of around 600 cash machines would effectively cover all eligible areas where it might be feasible to have a machine. Given the desire of a number of cash machine operators to deploy free cash machines in these areas, the key determinant of whether anything approaching 600 could be deployed would be the availability of suitable sites. The working group sought to identify how the prospects of bringing free machines into as many as possible of these areas could be maximised.

Private sector contribution

Action by individual cash-machine operators

49. During the working Group sessions, a number of banks and also an independent ATM deployer made clear that they would seek to increase their deployment of free cash machines in low-income areas.

16

Royal Bank of Scotland announced in July its intention to invest in an initial 300 free-of-charge cash machines in the target communities. RBS had issued an invitation to MPs, local authorities, credit unions and the communities they represented to identify potential sites. As part of this programme, 159 firm sites had been identified by end-November 2006 and installation was well underway across a number of them.

HBOS announced in July plans to install 100 new free cash machines in lower income and rural areas of Scotland and Northern England, the HBOS Group's two heartlands. HBOS had identified 201 low-income areas in Scotland that were serviced solely by charging ATMs and a further 199 in the North of England. Subject to planning permissions and site availability, HBOS planned to install machines in areas such as Bardowie, Rutherglen and Carmunock in Scotland, Newburn in Newcastle upon Tyne, Birkby in Huddersfield and Appleton in Widnes. HBOS had identified 46 firm sites by end-November and was set to install the first machines before Christmas.

HSBC announced earlier in 2006 a decision to roll out 500 new free cash machines, and aimed to place around 100 of these in lower-income areas. HSBC had been working with Citizens Advice in support of their initiative to reduce the number of 'free cash machine deserts', and had agreed to deploy free ATMs in at least 10% of the low-income areas identified by Citizens Advice. The initial locations selected by HSBC were Warkworth in Northumberland, Chapeltown in Leeds, Redbourn in Hertfordshire, Seven Sisters in Gwent, St Austell in Cornwall, Bowburn in Durham, Tottenham in London and Muirhouse in Edinburgh. Using their local knowledge, the regional Citizens Advice teams had been seeking suitable sites for the ATMs. Agreement had already been reached for deployments in Warkworth, Seven Sisters and St Austell. Other sites were currently under negotiation. The first machine was due to open in early December and would be located in Warkworth.

Barclays had plans to install 95 new free cash machines in branches that did not currently have them by the end of March 2007, of which around 10% would be in lower income areas and around 20% in branches that were the last remaining branch in the community.

Under an agreement with the Bank of Ireland, the Post Office announced plans to install an extra 500 free-of-charge cash machines in its branches, on top of the 1,000 it had already committed to roll out within the next five years. Though not focused solely on low-income areas, the Bank of Ireland and Post Office were looking for sites where it was economically feasible to replace charging cash machines with new free-to-use services. The Post Office anticipated that installations would soon hit an average of ten per week, and Bank of Ireland had identified around 200 sites within the target lower-income areas.

Independent ATM operator Bank Machine undertook to install 100 free machines in target areas, and had identified 22 firm sites by end-November 2006.

The Co-operative Bank had so far identified 20 sites in target lower-income areas where it would work towards replacing a charging cash machine with a free machine, a move enabled by changes in LINK’s interchange arrangements.

17

50. In addition to supporting their customers’ use of these additional free cash machines through the payment of interchange, Barclays, Lloyds TSB and a number of the other largest card issuers continued to offer all their cardholders the ability to make cash withdrawals over Post Office counters in a commercial arrangement with the Post Office, thereby providing their customers with free-to-the-customer cash withdrawals in a large number of the target areas.

51. Though too early to make firm commitments, a number of other LINK Members also made clear their willingness to consider how they could contribute. This included charging machine operators who were prepared to look at their cash machines on a case-by-case basis to establish if it would be economic to convert any critical machines from charging to free given potential changes to the interchange payment arrangements.13 However, any conversion of machines from charging to free would also depend on the attitude of the individual site-owner.

52. The working group noted that if LINK members succeeded in deploying close to the number of additional free machines which they planned, then there would be enough new free machines to reach the total of 600 that the working group estimated might be required. However, the working group again stressed that the key to installing cash machines in the target areas would be the existence of suitable sites. In some cases these would not exist. While the working group expected a significant expansion in the number of free cash machines in low-income areas on the basis of the work underway, it would not therefore be realistic to expect every cardholder to have a free machine at their doorstep.

Paying a premium to cash machine operators in lower-income areas without other free-of-charge machines

53. Operators of free cash machines currently receive a fee payment from the cardholder’s bank or building society each time that their machines are used by the cardholder. For example, if a Barclays customer uses a Lloyds TSB cash machine to make a free cash withdrawal, Barclays pays Lloyds a fee. The amount paid by the card issuing bank or building society is determined through the LINK interchange rules. These rules set “multilateral interchange fees” at different levels depending on whether the cash machine is in a bank branch, in a non-branch site owned by the cash machine operator or a related company, or in other non-branch sites unconnected with the cash machine operator. In accordance with competition law, these multilateral interchange fees are set so that revenue per transaction is equal to the average cost of transactions at the three categories of site.

54. The multilateral interchange arrangement offers a number of benefits to consumers. In particular it enables all cardholders to use all machines without the need for every cash machine operator to agree rates with every card issuer. The multilateral interchange arrangement is therefore fundamental to allowing universal access to the cash machine network. One downside, however, is that with fees set to cover average costs, a cash machine which is installed and run at average cost, but attracts a lower than average number of transactions is likely to be loss-making. In some low-income areas, the likely maximum volume of transactions is lower than average, making it consequently more difficult to maintain free machines in these areas. In its 2005 report, the Treasury

13 Independent ATM deployers currently operate over 2,000 free cash machines in addition to charging machines.

18

Committee expressed concern that this mechanism by which the interchange fee is calculated may give banks an incentive to pursue efficiency savings by reducing the availability of free cash machines in low-footfall areas. This could be a factor leading toward the concentration of free cash machines in fewer but busier locations.

55. The working group looked at proposals to add a premium to the interchange paid at free machines that are in low-income areas, are more than one kilometre distant from the next nearest free cash machine, and attract a number of transactions that is below the average level expected to make them profitable. This ‘financial inclusion premium’ would be paid by all card issuing members of LINK. It would recognise the additional social value of machines in these locations compared with sites where there are multiple alternative free machines, and potentially bring expected revenue for a lower-volume machine in one of these locations up to the average revenue for a free machine.

56. The combination of action by individual members, together with adjustments to the interchange regime to introduce a ‘financial inclusion premium’, could meet the objectives set by the working group of steps that would take effect immediately, and provide a solution that would be lasting and sustainable.

57. The arrangements for the ‘financial inclusion premium’ would also be flexible enough to be dynamic over time as the distribution of free cash machines changed, or, in the longer-term, as the distribution of low-income areas changed. The new arrangements would help to achieve an important public policy objective by harnessing and working with the market forces that already shaped decisions on deployment of free cash machines through the interchange mechanism. The same set of criteria could cover not only new free machines, but could also be applied to free cash machines that were the “last ATM in town”, more than one kilometre from the next nearest free cash machine, in low-income areas, and running at below average transaction volumes.14 For example, Barclays had deployed a cash machine at its branch in Treherbert, Rhondda Valley, in response to requests from the local community and MP when the only other bank present had closed its branch and cash machine, the Barclays machine therefore becoming the last ATM in town. The proposed financial inclusion premium in the interchange arrangements would make similar decisions in the future more commercially viable.

Public sector contribution

58. There are a number of ways in which the public sector can assist banks, building societies and independent cash machine operators to deploy free cash machines where this is considered desirable for public policy reasons.

Planning Permission

59. Seeking and obtaining planning permissions is often the most significant obstacle to deployment of a free cash machine. If the effort by working Group members to deploy new free machines in low-income areas is to achieve rapid results, active assistance from local

14 A number of Independent ATM Operators made an alternative proposal that card-issuing banks and building

societies pay their charges at existing charging cash machines. LINK Scheme members preferred the interchange premium because it would have a wider coverage (embracing not just those areas where there were only charging cash machines, but also areas where there was no ATM at all, and “last free ATM in town” sites), would be more dynamic over time and would carry a significantly lower cost per target area.

19

authorities with regard to meeting planning permission requirements and obtaining planning consents will be another key factor. In other areas, security will be a critical factor in whether or not it is possible to deploy a cash machine. Advice, guidance and constructive assistance from local authorities and police forces will be important. The working group noted a number of cases brought to its attention where the deployment of free machines was being held back or prevented by delays in obtaining planning consents.

In Tottenham, planning for a free cash machine near to Tottenham football club had been submitted and declined because of concerns around security and health and safety, despite there being a charging machine directly opposite the proposed site.

In Handsworth, a low-income area that currently lacked access to a free ATM, planning permission for a new free cash machine had been refused on the grounds that installation was likely to encourage criminal activity and was contrary to the Unitary Development Plan for Birmingham and Government Guidance on “planning out crime.”15 At the same time, there were over ten charging cash machines within 1 kilometre of the proposed site.

60. Working group members produced dozens of other examples where planning permission to install a free machine had been refused on the grounds of crime prevention, traffic congestion (e.g. parking concerns or even pavement crowding), objections from neighbours, the residential nature of the area and in a number of cases "undue noise".

61. The Government has indicated that guidance issued to local authorities regarding the location of cash machines and crime prevention places strong emphasis on the role of planning in helping to reduce crime.16 Planning authorities are asked to have robust policies which address crime prevention issues in their development plans. Crime prevention can legitimately be a material consideration in relation to planning applications.17

62. Working group members considered that it would be useful for planning guidance to be amended to reflect the importance of installing free cash machines in low-income communities that currently lack access to free-of-charge cash withdrawals. Local authorities could also consider the provision of suitable and secure sites for free cash machines as part of their development and regeneration planning. In some cases it might be appropriate to make provision of a suitable site for a free cash machine a condition of providing planning consent. Noting the importance of security for cash machines, working group members believed it was necessary for police forces to work constructively to deal with security issues. LINK members attached obvious importance to the security of individual cash machine users—their cardholders—and to the security of their cash machines themselves. Consumer groups, including the National Consumer Council and Citizens Advice, offered to support planning applications for free machines in the target areas. Any effort to reduce crime by preventing the installation of free cash machines needed to be carefully weighed against the positive economic and social benefits that could flow from the provision of a new cash machine. A free cash machine could help to sustain local business, economic activity and therefore local communities. Vibrant communities

15 West Midland Police, Press release, Designing out cash machine crime in Handsworth, 1 February 2006

16 'Planning Policy Statement 1: Delivering Sustainable Development' (PPS1), 2005.

17 HC Deb, Mon 23 Oct 2006, col 1658W

20

helped to combat crime. Leaving large areas without any access to cash machines as part of ‘planning out crime’ could have material negative consequences for local communities.

63. Policy on planning permissions for cash machines needed to take a rounded view of the overall public benefits of a new machine. There needed to be a joined-up approach by DCLG, local authorities and police forces.

Business Rates

64. Installing and maintaining additional free machines in low-income areas will result in additional cost for cash machine operators and card issuing banks and building societies. In many low-income areas currently without free-of-charge cash machines, machines may be uneconomic even with the proposed ‘financial inclusion premium’ interchange rates paid for free transactions. One of the most significant costs for such machines is often taxation in the form of business rates. Where there is a desire to install a cash machine to support public policy objectives to promote financial inclusion, and the installation cannot be commercially justified by the machine operator, waiving of business rates may be the critical factor in determining whether or not a machine is deployed. Rate relief in such instances will make it possible to deploy more free-of-charge machines. This will benefit local communities without loss of tax revenue given the current absence of free machines in these areas. Rate relief could therefore significantly increase the prospects of achieving the desired public policy objectives.

65. There is precedent for using rate relief to encourage ATMs in particular areas.

In Scotland, since 1st April 2003, the sites of ATMs in settlements of less than 3,000 in areas designated as rural by Scottish Ministers have been exempt from rating.18 This exemption is only available to ATMs that are not located in bank and building society branches.

In Northern Ireland, there is an intention to introduce rate relief for ATMs in rural areas. This will only apply to ATMs that are not in a bank or building society branch and have a separate entry on the valuation list. The Policy is intended to “encourage the spread of ATMs throughout rural areas of Northern Ireland”.19

66. The working group encouraged authorities in England and Wales—including the Department for Communities and Local Government, HM Treasury and Valuation Office—to consider the introduction of policies providing rate relief. Together with authorities in Northern Ireland and Scotland they should consider whether new cash machine deployments in target urban areas currently without access to free cash machines could be extended the same rate relief as rural areas.

Public-sector landlords

67. In some low-income areas there may be public sector landlords who can offer sites at which a cash machine can be deployed. The working group noted a number of examples of innovative partnerships between public sector landlords and cash machine operators.

18 Section 30 of the Local Government in Scotland Act

19 Northern Ireland, Department of Finance and Personnel, Rate reliefs for business in Northern Ireland, Consultation Document, March 2005, para 105, page 46

21

RBS had installed a machine in the London Borough of Harrow's council offices, alongside the social housing payments office.

RBS had also reached agreement to install a new free machine in a council-owned building in Denaby Main Forum in Doncaster, an area in the lowest 5% of the deprivation index and over 1 kilometre from the next nearest free-of-charge machine. The site, run by a trust, already housed retail outlets, a community shop, a training centre, an advice and information centre, a credit union collection point, and a satellite job centre. The new free-of-charge machine would support the local community, and generate extra takings for the other retail outlets in the precinct.

68. The working group considered that a co-ordinated effort by government to identify and support provision of other such public sector sites could materially improve the chances of bringing free cash machines to many low-income areas. HM Treasury could encourage public sector landlords to consider whether they could assist their local community by housing a free cash machine.

69. The Group noted that in the Beacon Scheme, administered by the Department for Communities and Local Government, local authorities were encouraged to apply for an award for best practice on promoting financial inclusion. The Scottish Executive also set local authority objectives to reduce the vulnerability of low-income families to financial exclusion and debt. The working group thought that local authorities working to meet these objectives in relation to financial inclusion should be encouraged to consider how a free cash machine could assist that, and how they might attract a free cash machine to their area, for example by locating machines on council property which was accessible to the public.

Action by local communities and individual landlords

70. The success of efforts to bring new free-of-charge cash machines to low-income communities will depend critically on the availability of sites. A number of banks and other LINK members that have already begun efforts to roll out new free cash machines have found identifying suitable sites to be perhaps the greatest challenge to this objective. In the search for such sites, local knowledge is likely to prove invaluable. The working Group wanted to encourage local community leaders, councils, MPs, credit unions, Citizens Advice Bureaux, community groups and others to help to identify where there is demand and need for a free ATM, and where there are sites that might be suitable.

Case studies suggested that this approach could be successful, with two machines having been installed in Scotland by RBS working closely with the local MP (John Robertson) to identify suitable sites in his constituency. One machine had been installed in the local Woolworth's store, while a second machine had been installed in the Yoker Credit Union.

Nationwide’s work with the Abbeyview Regeneration Forum in Dunfermline provided another encouraging example. The only free cash machine in Abbeyview had recently been sold and converted to charging. Nationwide and members of the Regeneration Forum had jointly assessed the area for suitable sites, and the Regeneration Forum had approached a local site owner to gain his support for the initiative. Nationwide had subsequently installed a cash machine at the site owner’s convenience store.

22

HBOS had worked with a Community Housing Association providing both traditional housing and sheltered accommodation in two target areas. At present the nearest access to free cash for residents of these areas was two kilometres away. New free cash machines in these areas stood to benefit tenants, the Association itself and the wider local community. HBOS hoped to deploy free-of-charge ATMs to both areas over the next six months, once site survey work was completed and planning consent obtained. Through the support of MPs, HBOS was also planning to install free machines in Broughton/Salford (Hazel Blears MP) and Ardler, Dundee (Jim McGovern MP).

As already noted, HSBC had achieved success by working with individual Citizens Advice Bureaux, using their knowledge of local areas to help identify suitable sites for free cash machines.

71. Individual landlords and site operators also have a critical role to play in making sites available for cash machines. Landlords will often have a choice over whether a machine is free or charging. This will usually be a commercial decision, but one factor some landlords might underestimate in their decision-making is the extra revenue that a free machine may attract through an increased number of visitors and increased spending.

72. Research by LINK showed that convenience store retailers have seen customers increase their average spend by 65% after they have used an in-store cash machine. Cash machines also have a positive impact on footfall numbers. The LINK survey found that cash machines attracted more customer visits than, for example, the sale of magazines or sandwiches. Free machines attract more visitors than charging equivalents, and this is likely to translate into higher takings over the till. Thus even if a cash machine operator is prepared to offer a higher rent to install a machine on a charging rather than free basis, both landlord and cash machine operator could in some cases find a free machine to be more profitable. When the Bank of Ireland had recently installed a free cash machine in the Post Office branch in Speke, use of the cash machine had increased seven-fold. The Post Office had also collected other evidence of increased visits to Post Office branches after free machines had been installed.

23

PRACTICAL STEPS AND MONITORING PROGRESS

73. On the basis of the criteria agreed in the working group, LINK circulated the full list of target low-income areas to LINK Members early in the working group process. A number of LINK Members have begun to look for sites in those areas, with firm sites already identified for around 250 new free machines.

74. However, the working group believed further progress was achievable in the coming months. The key factor was harnessing the local knowledge of people based in relevant communities. The full list of target areas, alongside regional and local maps, are shown in sections 5 and 6 of this report. The working group invites landlords in both the private and the public sector, local community leaders, local government, regeneration offices, MPs and others to assist in the effort to identify sites. While recognising that the decision on whether or not to provide space for a free cash machine will be a decision for individual landlords, the working group hopes, in particular, that the government will encourage public sector landlords in target areas to offer sites where this may be feasible.

75. The full list of target areas is displayed on the LINK website, at http://www.link.co.uk/atm/access_to_cash.

76. The ATM locator on the LINK website (http://www.link.co.uk/atm_locator/index.php) also allows people to find the nearest ATM to them – and whether it is free or charging.

77. Through the web-site, landlords and others in the target areas are able to contact LINK if they consider that they can help provide or identify a site for deployment of a free cash machine. LINK will pass on these suggestions to banks, building societies and independent ATM operators willing to deploy free cash machines in these areas.

78. LINK will provide regular updates of the list of target areas, and to facilitate ongoing monitoring, will keep and publish records of:

how many of these can be removed from the target list on account of installation of new free machines (significantly more than 200 of the initial 1,701 areas already stand to be removed from the list on the basis of sites identified);

any new areas that should be added to the target list on account of removal of free machines.

79. LINK will also continue to publish quarterly data on changes in the number of free cash machines, including specific detail on conversions of free machines to charging and vice versa. At the same time, it will publish data showing the relative deprivation of areas in which new free cash machines have been installed or existing ones removed. A core aim will be to establish a clearly positive trend towards additional provision of free cash machines in low-income areas. Making the figures publicly available will allow progress to be tracked, including for example, through reports to and by LINK’s Consumer Standing Committee or the newly established Payments Industry Association. It will also enable the Government to monitor the situation, as recommended in the Treasury Committee’s report.

80. Published details of progress made will enable public recognition of successes achieved by individual banks, independent operators and the industry as a whole. It will also enable

24

evidence on the reasons for the inability to install a free-of-charge cash machine—for example security issues, landlords’ preference for charging machines, or absence of planning permission—to be collected and assessed.

81. The working group recognised, however, that it would not be possible to bring a free-of-charge cash machine to every area in the list, and that it was not yet possible to determine with confidence the precise total of new machines that could be deployed. Many areas would be unsuitable because of lack of sites with adequate public access, or because of security concerns. In some rural locations, the local population would be too scattered for a machine to be viable. But as LINK Members made progress in visiting and assessing each of the target areas over coming months, and as responses from communities in these target areas were received, more evidence would become available both on the degree of success of the actions suggested above, and on how many of the areas were genuinely unsuitable for free cash machines.

25

3 Transparency of charges

Introduction

82. In its 2005 report on cash machine charges, the Treasury Committee recommended that LINK and the consumer groups explore the feasibility and examine the costs and benefits of standardised labelling for charging and free cash machines. The Committee also called on LINK more generally to improve consumer representation within its organisation, suggesting that consumer groups could be invited to attend relevant meetings of LINK or to sit on working groups, so that their views—for example on the issue of transparency of signage on machines at which a charge is made—could be taken into account.

83. Given the differences in views submitted to the Treasury Committee regarding the degree of consumer awareness of charges, the Committee recommended independent research into awareness of charges, and suggested that this be undertaken by LINK in conjunction with the consumer groups and published in full.

84. These calls were reiterated in February 2006, during a debate in Westminster Hall in which John McFall MP called for improvements to transparency so that consumers could see “at a glance” whether a cash machine was charging and the amount of any charge levied, and Former Economic Secretary to the Treasury Ivan Lewis called for the gathering of credible evidence so that arguments and decisions could be based on properly considered analysis.20

85. In early 2006, LINK and its members established a Consumer Committee involving a combination of LINK Members, and independent representatives including delegates from the Citizens Advice Bureau and National Consumer Council. LINK also commissioned independent research into the effectiveness of the signage rule enhancements that had been agreed by LINK in late 2004 and came into force in July 2005, shortly after publication of the Treasury Committee’s report. LINK published the results from that survey in May 2006.

86. LINK Members and the Consumer Committee were able to review the findings of this research alongside other surveys conducted by consumer groups and individual LINK Members, and to take this into account in the preparation of evidence-based proposals for the enhancement of rules on cash machine signage. The ATM working group asked the Consumer Committee to bring proposals to the working group for discussion and, hopefully, agreement on an appropriate and enduring solution to the transparency issue.

Evidence

87. The rules on transparency of charging agreed by LINK Members in December 2004 require all charging cash machines to carry a message on all screens before a card is inserted stating that “This machine will charge [£xx.xx] for LINK cash withdrawals”.

20 See HC Deb, col 526WH & 548WH

26

88. All charging cash machines must also carry external signage saying that 'This machine will charge for LINK cash withdrawals'. The sign must be within the normal eye-line close to the cash machine, must be in font of at least size 14 and of consistent size with that used for similar information (e.g. that promoting balance enquiries for which there is no charge).

89. Where there is signage away from a charging cash machine that directs cardholders towards the machine and/or any signage of A3 size or greater, this signage must also include the words 'This machine will charge for LINK cash withdrawals'. The font size used, and the colour and background must be such that the message is clearly visible to anyone reading the sign.

90. The LINK ATM Scheme commissioned two independent surveys into compliance with these rules. Although a survey21 conducted during October and November 2005 found around 9% of machines did not have external notices and 1.6% still did not have information about the charges levied on the idle screen,22 a second survey in February and March 2006 found that almost all operators of charging cash machines had addressed these non-compliance issues.23 In both surveys, companies operating machines confirmed not to be compliant with LINK rules were fined; with an ultimate sanction of disconnection from the LINK network unless breaches were rectified. LINK considers that there is now a very high level of compliance with its rules, although there will be occasional instances of missing signs, for example because of vandalism or removal of signs. The working group welcomed the additional monitoring and enforcement action taken by LINK, and believed that it was important for this work to continue.

91. LINK commissioned a further independent survey in April 2006 to collect evidence on the effectiveness of signage at charging cash machines which were known to be compliant with the rules.24 This survey found that although most users of charging cash machines were repeat visitors and were fully aware of the charges, there were some users that failed to notice the three or more separate notifications required under the LINK rules and did not realise they had been charged. Overall, 19% of users of cardholders who had just used a charging machine said that they were not aware the machine charged, despite the notice on the exterior of the machine, the on-screen notice at the beginning of the transaction and even the question at the end of the transaction where they were asked to confirm acceptance of the charge.

92. This result could reflect both the insufficient prominence of charging information and the tendency of some users to pay no heed even to appropriately clear notices. In quick-stop locations such as petrol stations, the proportion of charging machine users not noticing the charging notifications was, for example, significantly higher than in convenience stores where time pressure may be somewhat less. For some cardholders, convenience and speed will sometimes be more important than price, and all members of the working group accepted that it would be difficult to achieve 100% recognition of charging notices unless these were made unreasonably intrusive.

21 LINK, news release, 13 December 2005

22 100% of machines met requirements to ask the cardholder to confirm acceptance of the specific charge or cancel the withdrawal before completion of the transaction.

23 LINK, news release, 10 April 2006

24 LINK, news release, 03 May 2006

27

93. A survey conducted by Citizens Advice found that 46 per cent of people said that they did not receive sufficient information in advance that they would be charged for a cash withdrawal. 73 per cent of people said that additional signage would enable them to make a more informed decision.25

94. LINK informed the working group that it had received around 70 direct complaints about lack of signs on specific charging cash machines since 1 July 2005. These had come from complainants who had been concerned about the charge, who had often taken time to study the cash machine before raising with LINK and who had made the effort to contact LINK despite cash machines carrying no invitation to complain directly to LINK.26 In almost all of the more recent cases, machines had subsequently been found to be technically compliant with LINK rules, but the notices had been missed by the cardholder. While there had been no such complaints in respect of most of LINK’s charging ATM operators—indicating variation between LINK Members in the quality of charging notices they had applied—this suggested that the minimum standards in LINK’s rules did not go far enough to pass an “at a glance” test. This variation in the proportion of customers identifying charging notices was also reflected in LINK’s April 2006 survey, and provided some useful indicators as to which of the styles and designs of notices introduced by charging operators had been most effective.

95. The LINK survey also found that cash machine users were more likely to notice on-screen notices than external notices, with four times as many users noticing the screen notice compared with the external notice. Many LINK members considered this unsurprising given the array of signs that can be present in a retail environment and the tendency of cash machine users to ignore these while looking for instructions on the screen. It could also be argued, however, that the small size and insufficient prominence of external notices was one factor why they were not identified.

96. One further important finding from the survey was that almost all charging and free cash machine users (over 95%) knew that cash machines at bank and building society branches were free.

97. The Consumer Committee agreed that the Treasury Committee recommendations, including those suggesting larger minimum font sizes and more standardised labelling needed to be considered and addressed in the light of this survey evidence.

Proposals for improved transparency

98. The consumer groups and other independent representatives on LINK’s Consumer Committee, as well as all the Members of the LINK Scheme, agreed that the objective of LINK’s signage rules should be to ensure charging machines could be identified “at a glance”.

99. As the Treasury Committee acknowledged in its report, LINK rules needed to strike an appropriate balance between cost and benefit. The costs of changes to notices about

25 Citizens Advice, Out of Pocket, July 2006

26 All cash machines must carry details and contact information for the LINK member responsible for maintaining charging notices and other aspects of the cash machine’s operation. LINK does not have responsibility for individual machines and LINK contact details are not present on cash machines. These 70 complaints are therefore assumed to represent only a very small proportion of those cardholders who had failed to identify advance notices of charges.

28

charges would be passed on to the users of charging machines in the form of higher charges. Changes that were costly but low impact would not benefit consumers. In the case of free machines, changes that were costly but low impact would increase the cost of running free machines and decrease the willingness to deploy them.

On-screen signage

100. The independent survey evidence indicated that screen notices were more effective than external signage. At least where messages can be downloaded remotely to cash machines, they could be deployed at relatively low cost and in a relatively short time scale. In the longer term, screen notices could be more reliably deployed across all cash machines and would be less vulnerable to vandalism and removal than external signs. The Consumer Committee therefore proposed that improved minimum standards for on-screen information needed to be at the core of the LINK signage rules for these rules to be effective in alerting as many customers as possible to the presence of charges.

101. Following work by LINK Members and the LINK Scheme Executive, the Consumer Committee suggested a number of measures to enhance the visibility of existing screen notices.

Screen notices should be of minimum size. Font size 18 for small screens (width less than 170mm), font size 26 for medium screens (width between 170mm and 200mm) and font size 32 for large screens (width greater than 200mm) should be the default standard. There would, however, be a significant minority of ATMs with screen functionality so limited that a particular font size could not be applied. For these machines, alternatives which went as far as practicable and reasonable to achieve the “at a glance” objective would need to be agreed between the relevant ATM operator and the LINK Scheme Executive.

Screen notices should normally be centre-justified horizontally and vertically. It should, however, be possible to put the message at the top of the screen where there was a desire or need to have another message underneath it, for example a message relating to security or how to insert the card.

The rules should include a requirement for contrasting text colour in accordance with Disability Discrimination Act guidelines. Text should, for example, be black / dark blue on a pale background, or yellow / white on a dark coloured background.

Text should, wherever possible, be sentence case to optimise readability.

The proportion of the screen above and below the charge message allowed for other information should not exceed 15% above and / or 15% below for small screens, 20% above and / or below for medium-sized screens, and 25% above and / or below for large screens except where screen functionality or size was limited and it could be shown that messages were closer to the “at a glance” test if at the top of the screen with other messages beneath them.

Any additional messages should not dominate or unreasonably distract from the charging message, e.g. should not be of larger font size or take up more of the screen than the charging notice so that the notice could no longer be considered to be visible “at a glance”.

29

Any ATM operator that had a case for some variation from the letter of the rules would need to agree the relevant design with the LINK Scheme Executive, which would have the option of consulting the Consumer Committee for approval if it considered there was reasonable doubt regarding whether the design would achieve the objective of being visible “at a glance”.

102. The working group agreed with the Consumer Committee that the wording of the screen warning should move to a standard phrase of “This machine will charge you [£xx.xx] for cash withdrawals”. The word ‘LINK’ (present in the current wording) would be dropped on account of evidence from the survey, Citizens Advice and charging operators that it confused cardholders. The word ‘you’ would be added for additional clarity. In cases where there the machine attracted a high proportion of credit cardholders then a variation on this wording would be allowed to provide extra information to these cardholders.

103. Examples of how the information might appear on-screen at a charging machine are shown in Appendix 1.

104. The working group agreed that the change should be implemented within a timescale that avoided unnecessary delay while also avoiding unnecessary cost. For some charging machines the required changes could be made by remotely downloading the upgraded messages. For other machines, the changes would require an engineer to visit the site. The working group agreed that:

Where changes to on-screen information can be implemented by remote download, they should be implemented by the end of June 2007.

Where changes to on-screen information require an engineer visit, they should be implemented by the end of December 2007.