Arabia Monitor- Research Overview Q2 2015

23

Research Overview

-

Upload

bruce-yifu-jia- -

Category

Documents

-

view

17 -

download

0

Transcript of Arabia Monitor- Research Overview Q2 2015

Research Overview

1. About Arabia Monitor

2. Arabia Monitor Views

3. Arabia Monitor News

4. Arabia Monitor Membership

Outline

Putting regional developments within a global context

Forward-looking analysis that is ahead of the curve

Ahead of the Curve Our forward-looking perspective places regional developments in a broader context and delivers strategic investment and decision making insights.

Concise and clear bullet points that cut through the noise

Cutting through the Noise Arabia Monitor distils its research into executive-friendly bullet point format, ensuring our views are clear and our analysis concise.

Extensive high-level network for privileged access to insights

Privileged Access Arabia Monitor’s competitive edge is our collaboration with senior decision makers who add valuable insights from a position of authority.

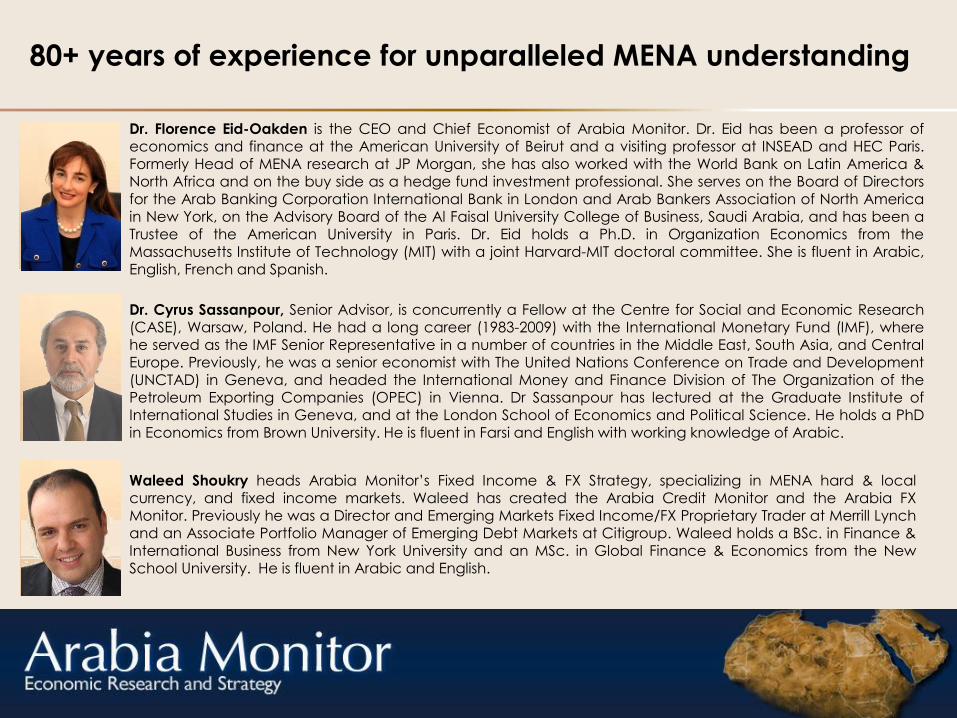

Dr. Florence Eid-Oakden is the CEO and Chief Economist of Arabia Monitor. Dr. Eid has been a professor of economics and finance at the American University of Beirut and a visiting professor at INSEAD and HEC Paris. Formerly Head of MENA research at JP Morgan, she has also worked with the World Bank on Latin America & North Africa and on the buy side as a hedge fund investment professional. She serves on the Board of Directors

for the Arab Banking Corporation International Bank in London and Arab Bankers Association of North America in New York, on the Advisory Board of the Al Faisal University College of Business, Saudi Arabia, and has been a Trustee of the American University in Paris. Dr. Eid holds a Ph.D. in Organization Economics from the Massachusetts Institute of Technology (MIT) with a joint Harvard-MIT doctoral committee. She is fluent in Arabic, English, French and Spanish.

Waleed Shoukry heads Arabia Monitor’s Fixed Income & FX Strategy, specializing in MENA hard & local currency, and fixed income markets. Waleed has created the Arabia Credit Monitor and the Arabia FX Monitor. Previously he was a Director and Emerging Markets Fixed Income/FX Proprietary Trader at Merrill Lynch and an Associate Portfolio Manager of Emerging Debt Markets at Citigroup. Waleed holds a BSc. in Finance & International Business from New York University and an MSc. in Global Finance & Economics from the New

School University. He is fluent in Arabic and English.

80+ years of experience for unparalleled MENA understanding

Dr. Cyrus Sassanpour, Senior Advisor, is concurrently a Fellow at the Centre for Social and Economic Research (CASE), Warsaw, Poland. He had a long career (1983-2009) with the International Monetary Fund (IMF), where he served as the IMF Senior Representative in a number of countries in the Middle East, South Asia, and Central Europe. Previously, he was a senior economist with The United Nations Conference on Trade and Development (UNCTAD) in Geneva, and headed the International Money and Finance Division of The Organization of the Petroleum Exporting Companies (OPEC) in Vienna. Dr Sassanpour has lectured at the Graduate Institute of International Studies in Geneva, and at the London School of Economics and Political Science. He holds a PhD in Economics from Brown University. He is fluent in Farsi and English with working knowledge of Arabic.

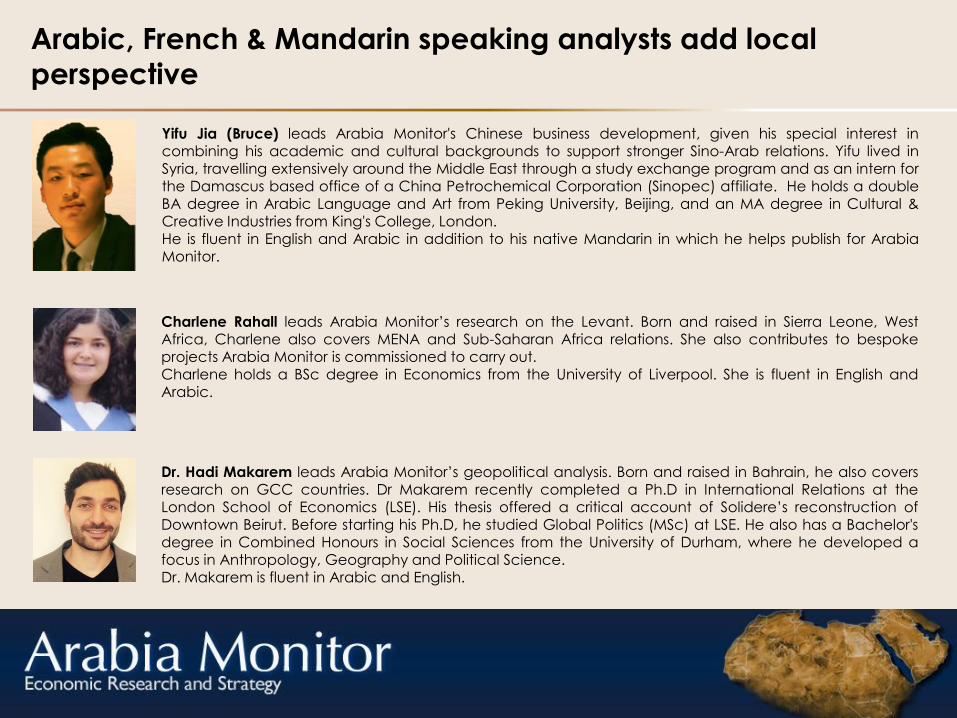

Arabic, French & Mandarin speaking analysts add local

perspective

Yifu Jia (Bruce) leads Arabia Monitor's Chinese business development, given his special interest in combining his academic and cultural backgrounds to support stronger Sino-Arab relations. Yifu lived in Syria, travelling extensively around the Middle East through a study exchange program and as an intern for the Damascus based office of a China Petrochemical Corporation (Sinopec) affiliate. He holds a double BA degree in Arabic Language and Art from Peking University, Beijing, and an MA degree in Cultural & Creative Industries from King's College, London. He is fluent in English and Arabic in addition to his native Mandarin in which he helps publish for Arabia Monitor.

Charlene Rahall leads Arabia Monitor’s research on the Levant. Born and raised in Sierra Leone, West Africa, Charlene also covers MENA and Sub-Saharan Africa relations. She also contributes to bespoke projects Arabia Monitor is commissioned to carry out. Charlene holds a BSc degree in Economics from the University of Liverpool. She is fluent in English and Arabic.

Dr. Hadi Makarem leads Arabia Monitor’s geopolitical analysis. Born and raised in Bahrain, he also covers

research on GCC countries. Dr Makarem recently completed a Ph.D in International Relations at the London School of Economics (LSE). His thesis offered a critical account of Solidere’s reconstruction of Downtown Beirut. Before starting his Ph.D, he studied Global Politics (MSc) at LSE. He also has a Bachelor's degree in Combined Honours in Social Sciences from the University of Durham, where he developed a focus in Anthropology, Geography and Political Science. Dr. Makarem is fluent in Arabic and English.

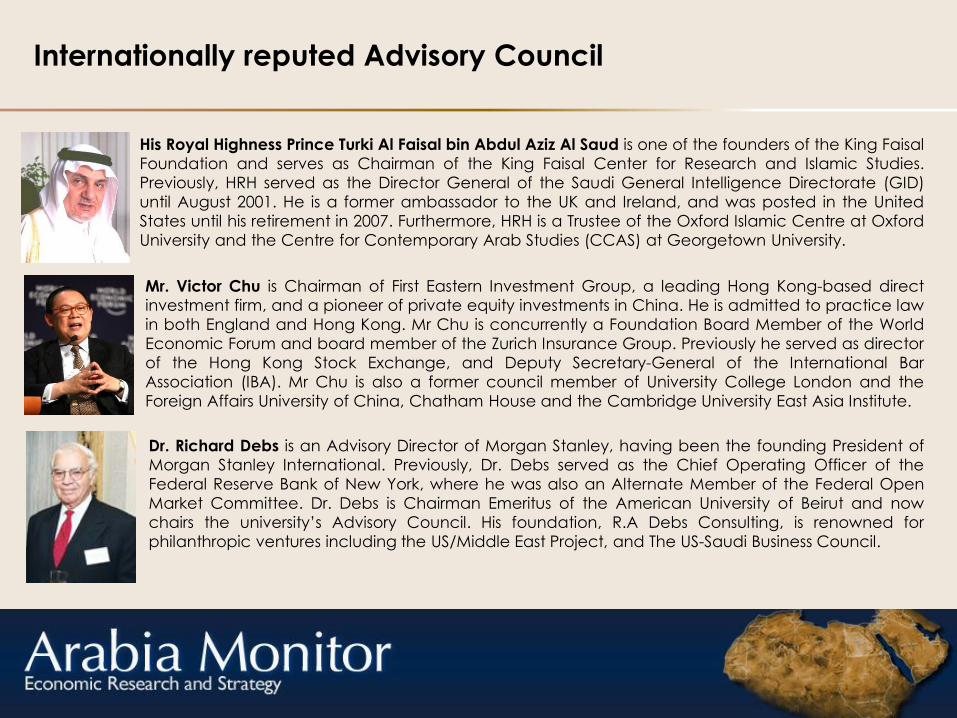

His Royal Highness Prince Turki Al Faisal bin Abdul Aziz Al Saud is one of the founders of the King Faisal

Foundation and serves as Chairman of the King Faisal Center for Research and Islamic Studies.

Previously, HRH served as the Director General of the Saudi General Intelligence Directorate (GID)

until August 2001. He is a former ambassador to the UK and Ireland, and was posted in the United

States until his retirement in 2007. Furthermore, HRH is a Trustee of the Oxford Islamic Centre at Oxford

University and the Centre for Contemporary Arab Studies (CCAS) at Georgetown University.

Mr. Victor Chu is Chairman of First Eastern Investment Group, a leading Hong Kong-based direct

investment firm, and a pioneer of private equity investments in China. He is admitted to practice law

in both England and Hong Kong. Mr Chu is concurrently a Foundation Board Member of the World

Economic Forum and board member of the Zurich Insurance Group. Previously he served as director

of the Hong Kong Stock Exchange, and Deputy Secretary-General of the International Bar

Association (IBA). Mr Chu is also a former council member of University College London and the

Foreign Affairs University of China, Chatham House and the Cambridge University East Asia Institute.

Dr. Richard Debs is an Advisory Director of Morgan Stanley, having been the founding President of

Morgan Stanley International. Previously, Dr. Debs served as the Chief Operating Officer of the

Federal Reserve Bank of New York, where he was also an Alternate Member of the Federal Open

Market Committee. Dr. Debs is Chairman Emeritus of the American University of Beirut and now

chairs the university’s Advisory Council. His foundation, R.A Debs Consulting, is renowned for

philanthropic ventures including the US/Middle East Project, and The US-Saudi Business Council.

Internationally reputed Advisory Council

1. About Arabia Monitor

2. Arabia Monitor Views

3. Arabia Monitor News

4. Arabia Monitor Membership

Outline

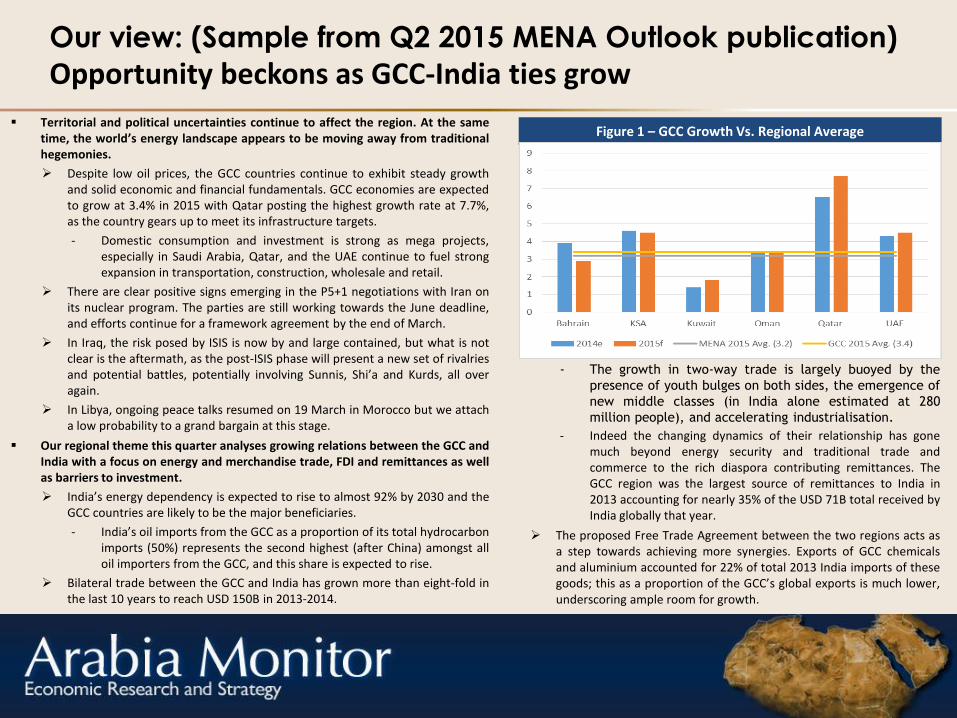

Our view: (Sample from Q2 2015 MENA Outlook publication)

Opportunity beckons as GCC-India ties grow

1 Arabia Monitor; IMF. 2 Arabia Monitor; Central Bank of Egypt.

Territorial and political uncertainties continue to affect the region. At the same time, the world’s energy landscape appears to be moving away from traditional hegemonies.

Despite low oil prices, the GCC countries continue to exhibit steady growth and solid economic and financial fundamentals. GCC economies are expected to grow at 3.4% in 2015 with Qatar posting the highest growth rate at 7.7%, as the country gears up to meet its infrastructure targets.

- Domestic consumption and investment is strong as mega projects, especially in Saudi Arabia, Qatar, and the UAE continue to fuel strong expansion in transportation, construction, wholesale and retail.

There are clear positive signs emerging in the P5+1 negotiations with Iran on its nuclear program. The parties are still working towards the June deadline, and efforts continue for a framework agreement by the end of March.

In Iraq, the risk posed by ISIS is now by and large contained, but what is not clear is the aftermath, as the post-ISIS phase will present a new set of rivalries and potential battles, potentially involving Sunnis, Shi’a and Kurds, all over again.

In Libya, ongoing peace talks resumed on 19 March in Morocco but we attach a low probability to a grand bargain at this stage.

Our regional theme this quarter analyses growing relations between the GCC and India with a focus on energy and merchandise trade, FDI and remittances as well as barriers to investment.

India’s energy dependency is expected to rise to almost 92% by 2030 and the GCC countries are likely to be the major beneficiaries.

- India’s oil imports from the GCC as a proportion of its total hydrocarbon imports (50%) represents the second highest (after China) amongst all oil importers from the GCC, and this share is expected to rise.

Bilateral trade between the GCC and India has grown more than eight-fold in the last 10 years to reach USD 150B in 2013-2014.

- The growth in two-way trade is largely buoyed by the

presence of youth bulges on both sides, the emergence of

new middle classes (in India alone estimated at 280

million people), and accelerating industrialisation.

- Indeed the changing dynamics of their relationship has gone much beyond energy security and traditional trade and commerce to the rich diaspora contributing remittances. The GCC region was the largest source of remittances to India in 2013 accounting for nearly 35% of the USD 71B total received by India globally that year.

The proposed Free Trade Agreement between the two regions acts as a step towards achieving more synergies. Exports of GCC chemicals and aluminium accounted for 22% of total 2013 India imports of these goods; this as a proportion of the GCC’s global exports is much lower, underscoring ample room for growth.

Figure 1 – GCC Growth Vs. Regional Average

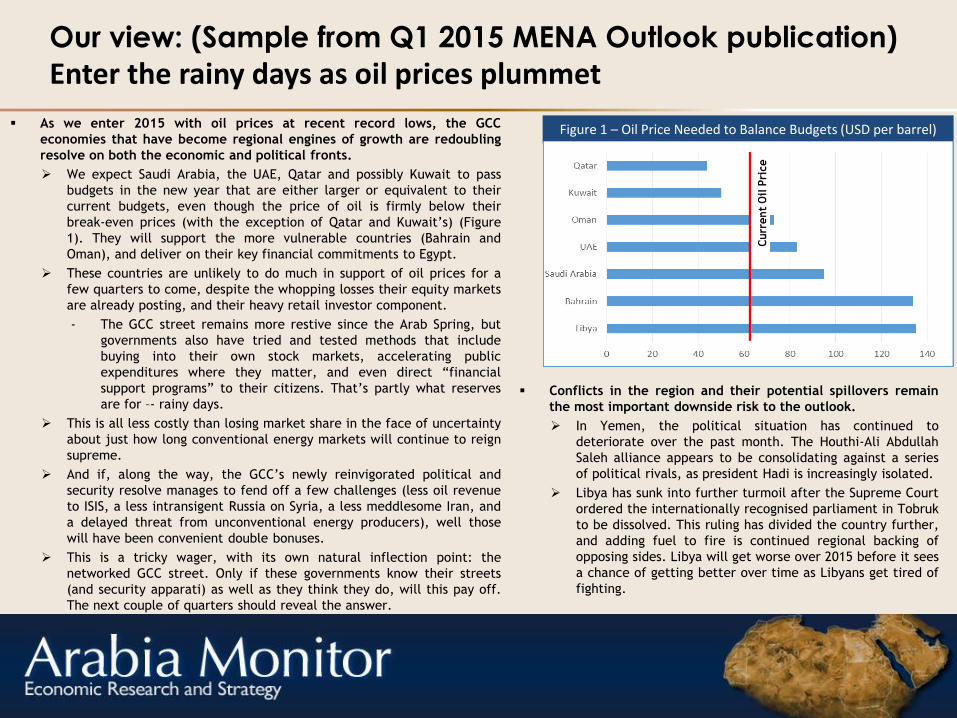

Our view: (Sample from Q1 2015 MENA Outlook publication)

Enter the rainy days as oil prices plummet

1 Arabia Monitor; IMF. 2 Arabia Monitor; Central Bank of Egypt.

As we enter 2015 with oil prices at recent record lows, the GCC

economies that have become regional engines of growth are redoubling

resolve on both the economic and political fronts.

We expect Saudi Arabia, the UAE, Qatar and possibly Kuwait to pass

budgets in the new year that are either larger or equivalent to their

current budgets, even though the price of oil is firmly below their

break-even prices (with the exception of Qatar and Kuwait’s) (Figure

1). They will support the more vulnerable countries (Bahrain and

Oman), and deliver on their key financial commitments to Egypt.

These countries are unlikely to do much in support of oil prices for a

few quarters to come, despite the whopping losses their equity markets

are already posting, and their heavy retail investor component.

- The GCC street remains more restive since the Arab Spring, but

governments also have tried and tested methods that include

buying into their own stock markets, accelerating public

expenditures where they matter, and even direct “financial

support programs” to their citizens. That’s partly what reserves

are for –- rainy days.

This is all less costly than losing market share in the face of uncertainty

about just how long conventional energy markets will continue to reign

supreme.

And if, along the way, the GCC’s newly reinvigorated political and

security resolve manages to fend off a few challenges (less oil revenue

to ISIS, a less intransigent Russia on Syria, a less meddlesome Iran, and

a delayed threat from unconventional energy producers), well those

will have been convenient double bonuses.

This is a tricky wager, with its own natural inflection point: the

networked GCC street. Only if these governments know their streets

(and security apparati) as well as they think they do, will this pay off.

The next couple of quarters should reveal the answer.

Figure 1 – Oil Price Needed to Balance Budgets (USD per barrel)

Conflicts in the region and their potential spillovers remain

the most important downside risk to the outlook.

In Yemen, the political situation has continued to

deteriorate over the past month. The Houthi-Ali Abdullah

Saleh alliance appears to be consolidating against a series

of political rivals, as president Hadi is increasingly isolated.

Libya has sunk into further turmoil after the Supreme Court

ordered the internationally recognised parliament in Tobruk

to be dissolved. This ruling has divided the country further,

and adding fuel to fire is continued regional backing of

opposing sides. Libya will get worse over 2015 before it sees

a chance of getting better over time as Libyans get tired of

fighting.

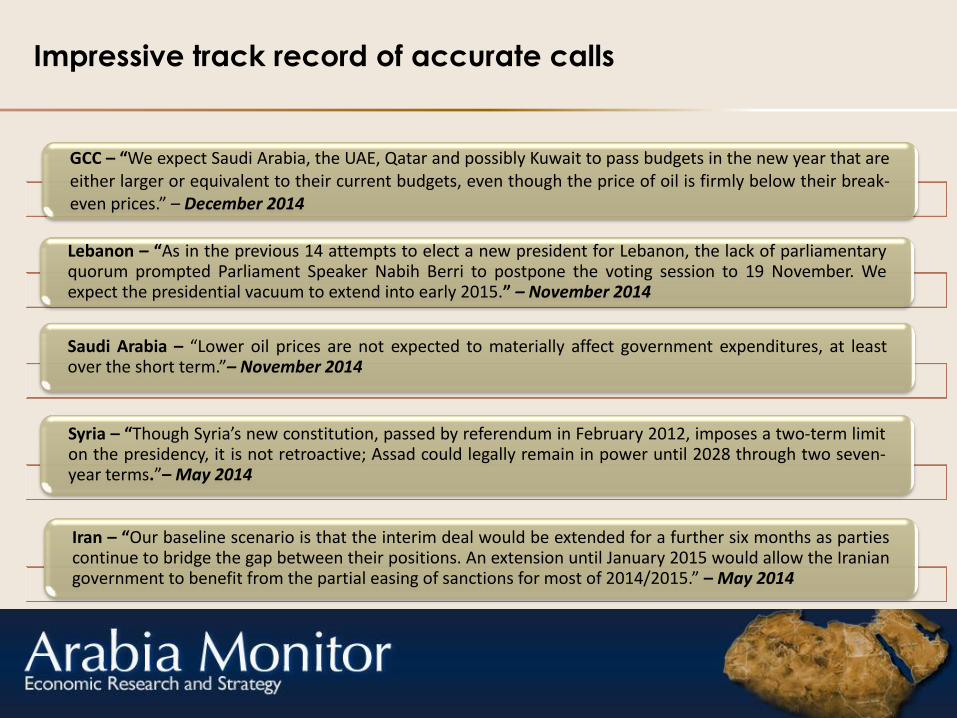

Impressive track record of accurate calls

GCC – “We expect Saudi Arabia, the UAE, Qatar and possibly Kuwait to pass budgets in the new year that are either larger or equivalent to their current budgets, even though the price of oil is firmly below their break-even prices.” – December 2014

Lebanon – “As in the previous 14 attempts to elect a new president for Lebanon, the lack of parliamentary quorum prompted Parliament Speaker Nabih Berri to postpone the voting session to 19 November. We expect the presidential vacuum to extend into early 2015.” – November 2014

Saudi Arabia – “Lower oil prices are not expected to materially affect government expenditures, at least over the short term.”– November 2014

Syria – “Though Syria’s new constitution, passed by referendum in February 2012, imposes a two-term limit on the presidency, it is not retroactive; Assad could legally remain in power until 2028 through two seven-year terms.”– May 2014

Iran – “Our baseline scenario is that the interim deal would be extended for a further six months as parties continue to bridge the gap between their positions. An extension until January 2015 would allow the Iranian government to benefit from the partial easing of sanctions for most of 2014/2015.” – May 2014

* Arabia Monitor’s Credit and FX Monitor views do not constitute trade recommendations

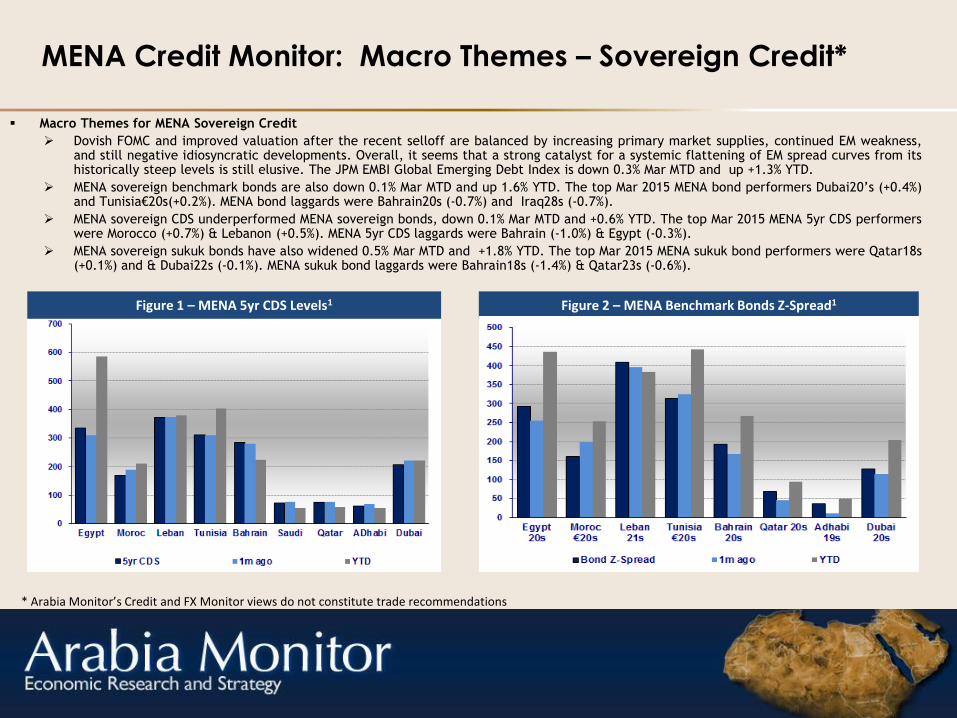

MENA Credit Monitor: Macro Themes – Sovereign Credit*

Macro Themes for MENA Sovereign Credit

Dovish FOMC and improved valuation after the recent selloff are balanced by increasing primary market supplies, continued EM weakness, and still negative idiosyncratic developments. Overall, it seems that a strong catalyst for a systemic flattening of EM spread curves from its historically steep levels is still elusive. The JPM EMBI Global Emerging Debt Index is down 0.3% Mar MTD and up +1.3% YTD.

MENA sovereign benchmark bonds are also down 0.1% Mar MTD and up 1.6% YTD. The top Mar 2015 MENA bond performers Dubai20’s (+0.4%) and Tunisia€20s(+0.2%). MENA bond laggards were Bahrain20s (-0.7%) and Iraq28s (-0.7%).

MENA sovereign CDS underperformed MENA sovereign bonds, down 0.1% Mar MTD and +0.6% YTD. The top Mar 2015 MENA 5yr CDS performers were Morocco (+0.7%) & Lebanon (+0.5%). MENA 5yr CDS laggards were Bahrain (-1.0%) & Egypt (-0.3%).

MENA sovereign sukuk bonds have also widened 0.5% Mar MTD and +1.8% YTD. The top Mar 2015 MENA sukuk bond performers were Qatar18s (+0.1%) and & Dubai22s (-0.1%). MENA sukuk bond laggards were Bahrain18s (-1.4%) & Qatar23s (-0.6%).

Figure 1 – MENA 5yr CDS Levels1 Figure 2 – MENA Benchmark Bonds Z-Spread1

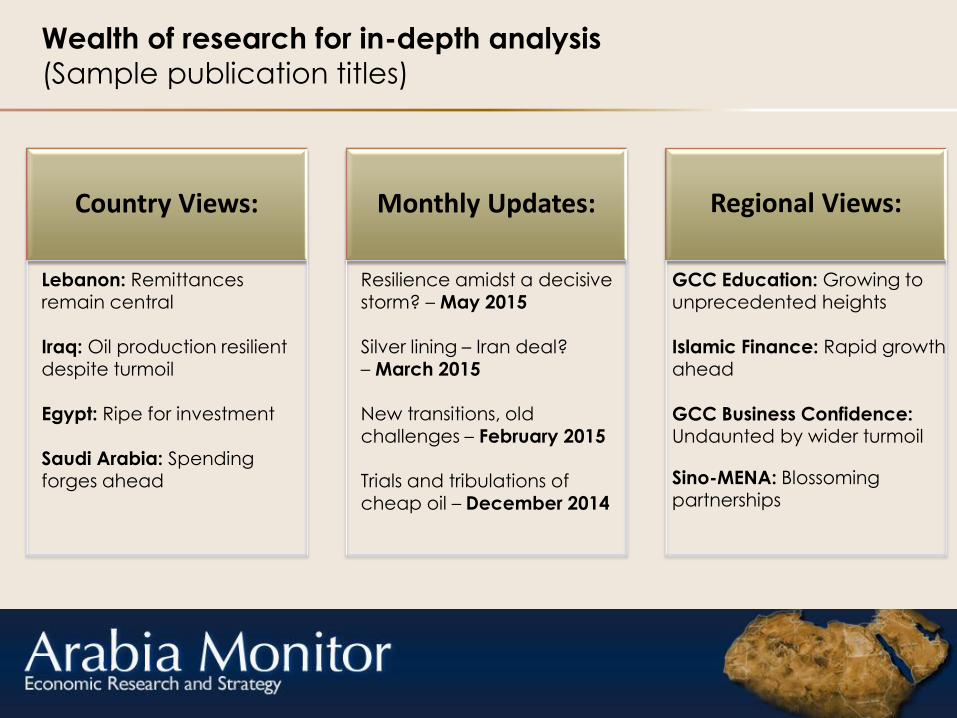

Wealth of research for in-depth analysis (Sample publication titles)

Country Views: Monthly Updates:

Regional Views:

Lebanon: Remittances remain central Iraq: Oil production resilient despite turmoil

Egypt: Ripe for investment Saudi Arabia: Spending forges ahead

Resilience amidst a decisive storm? – May 2015 Silver lining – Iran deal? – March 2015

New transitions, old challenges – February 2015

Trials and tribulations of cheap oil – December 2014

GCC Education: Growing to unprecedented heights Islamic Finance: Rapid growth ahead

GCC Business Confidence: Undaunted by wider turmoil

Sino-MENA: Blossoming partnerships

1. About Arabia Monitor

2. Arabia Monitor Views

3. Arabia Monitor News

4. Arabia Monitor Membership

Outline

A prominent opinion former throughout international media

Dr. Florence Eid

delivers a

keynote

speech at the

ONS

conference,

Norway –

August 2014

Sino-Saudi links boost

global economy – Dr.

Florence Eid Article in

China Daily

Saudi Reshuffle a Sign of

`Dynamic Change' - Dr. Florence

Eid shares insights with Bloomberg

TV - April 29, 2015

MENA and China: Joined at

the hip - Caijing Magazine,

China - October 13, 2014

New Opportunities in

the Arab World – Dr.

Florence Eid on

Caixin Weekly

Economic Review

View more…

1. About Arabia Monitor

2. Arabia Monitor Views

3. Arabia Monitor News

4. Arabia Monitor Membership

Outline

Cross-sector clientele realising the potential of our insights

21

Leverage our worldwide thought-leadership exposure

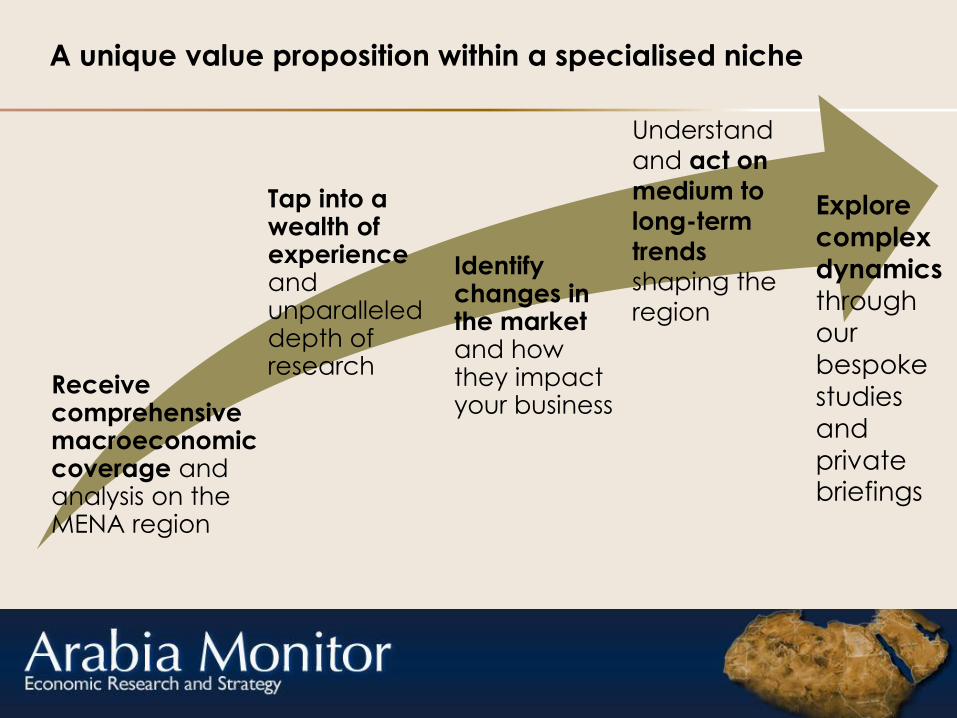

A unique value proposition within a specialised niche

Receive comprehensive macroeconomic coverage and analysis on the MENA region

Tap into a wealth of experience and unparalleled depth of research

Identify changes in the market and how they impact your business

Understand

and act on

medium to

long-term

trends shaping the

region

Explore

complex dynamics through

our

bespoke

studies and

private briefings

Arabia Monitor is an independent research firm specializing in macroeconomic and geopolitical studies on the

Middle East & North African region, which we view as the new emerging market. Our forward looking perspective

allows us to place recent developments in the region within a broader context and a long-term view. Our analysis is

based on the macroeconomic and financial balance sheet of Arab countries to deliver unique strategy insights and

forecasts to businesses across a wide range of sectors.

Arabia Advisors specialises in portfolio strategy and private placements. It works with firms, family offices and

government related organisations that are looking to streamline, re-balance or diversify their asset portfolios. Based

in the UAE as an off-shore company, Arabia Advisors services a regional and international client base with interest in

the Arab countries.

Arabia Monitor

18b Charles Street | London W1J 5DU

Tel +44 203 170 5533 | Fax +44 203 170 5532

email: [email protected]

www.arabiamonitor.com

© Arabia Monitor 2015

This is a publication of Arabia Monitor Limited (AM Ltd), and is protected by international copyright laws and is for

the subscriber's use only. This publication may not be distributed or reproduced in any form without written

permission.

The information contained herein does not constitute an offer or solicitation to sell any security or fund to or by

anyone in any jurisdictions, nor should it be regarded as a contractual document. Under no circumstances should

the information provided on this publication be considered as investment advice, or as a sufficient basis on which

to make investment decisions. The information contained herein has been gathered by AM Ltd from sources

deemed reliable as of the date of publication, but no warranty of accuracy or completeness is given. AM Ltd is not

responsible for and provides no guarantee with respect to any of the information provided herein or through the

use of any hypertext link.

Disclaimer