(Apresentação Geral JSL Day ENG...

72

Transcript of (Apresentação Geral JSL Day ENG...

Institutional Presentation

Fernando Antonio SimõesFernando Antonio Simões

HistoryHistory2000 - 20102000 - 2010

Creation of Company

foundation

Service diversification

Consolidation of logistics integrated services

Beginning of cargo

transportation activities of Julio

Simões

Group’s 1st acquisition

Acquisition of Transcoffer

Operation in new

businessesCharter

services and Tourism,

Rental of light vehicles

Acquisition of Transcel

Acquisition ofTransportadora

Grande ABC(April/08)

Acquisition of

LubianiLogística

(June/07)

Beginning of dedicated, customized

servicesForestry, auto, rental of heavy

equipment

19501950 19701970 19801980 19901990

Beginning of integrated

services and new

industries Mining and

food products

Urban DistributionFood and

Civil Aviation

Passenger transportation

concessions

IPOPerpetuity and

support to growth

> 2011 - 2012> 2011 - 2012

Acquisition of Rodoviário Schio

Merger of Simpar Concessionárias

Creation of JSL Aluguel de Caminhões

Creation of CS Brasil

Outsourcing of light vehicles for the 2007 Pan American Games

2011 Proforma Net Revenue:

R$2.7 billionCAGR01-11: 28.3%

Organizational IdentityOrganizational Identity

Business

Mission

Vision

Values

Solutions and Services of industrial and social integration.

To provide services and logistics solutions, through a dedicated workforce, generating value for our clients and shareholders, and contributing to the development of the communities where we operate.

Maintain our position as the leading Logistics Operator in the market, offering the broadest range of services and innovative solutions, that are recognized for their excellence and are aligned with the clients’ needsTo be recognized for the professionalism of our managementTo become a benchmark in the utilization and commercialization of assets.

The client: Understand and serve, to ensure a long term relationship.People: They make all the difference in our business.Hard work: You don´t build anything without it.Simplicity: Objective in our actions, to ensure agility.Profit: Indispensable for growth and perpetuation.

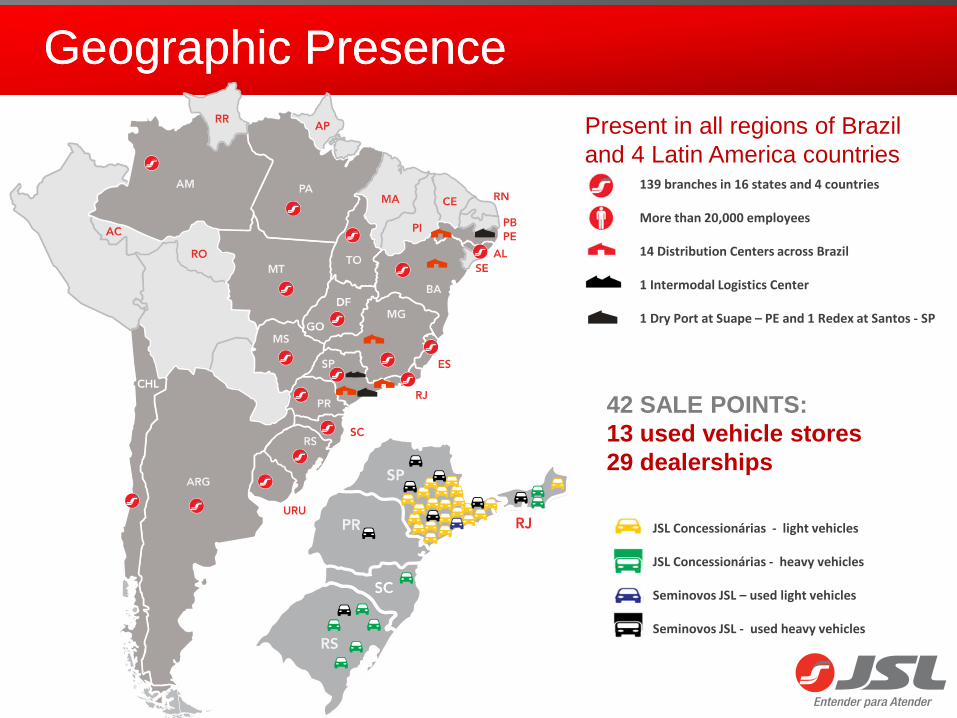

Geographic PresenceGeographic Presence

42 SALE POINTS:13 used vehicle stores29 dealerships

JSL Concessionárias - light vehicles

JSL Concessionárias - heavy vehicles

Seminovos JSL – used light vehicles

Seminovos JSL - used heavy vehicles

Present in all regions of Braziland 4 Latin America countries

139 branches in 16 states and 4 countries

More than 20,000 employees

14 Distribution Centers across Brazil

1 Intermodal Logistics Center

1 Dry Port at Suape – PE and 1 Redex at Santos - SP

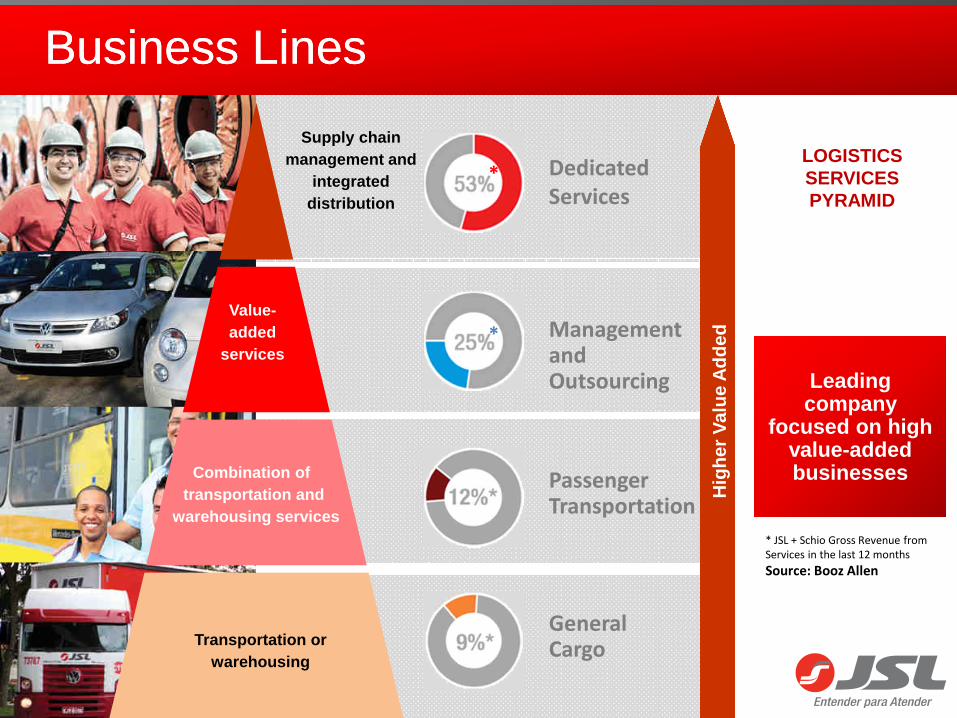

Business LinesBusiness Lines

Dedicated Logistics Services

Fleet Management

and Outsourcing

Passenger Transportation

General Cargo Transportation

% of Gross Revenue from Services of JSL + Schio – Base: last 12 months

Diversified RevenueDiversified Revenue

Solid relations with clients and diversified revenu e

Food and Beverage

15%

Pulp and Paper

12%

Public

13%

Steel and Mining

11%

Automotive

11%

Passenger Transportation

10%

Agriculture

6%

Petrochemical

5%

Others

6%

ConsumerGoods

5%

Capital Goods

4%

EletricEnergy

2%

¹ JSL + Schio Proforma last 12 months

50 largest clients represent around

58% of the gross revenue

Breakdown of Gross Revenue from Services by Sector¹

Presence in more than 16 sectors of the

economy

Presence in more than 16 sectors of the

economy

Historical relationships and activitiesHistorical relationships and activities

Rankings correspond to the classification of JSL in the respective segments in ILOS Logistics Award 2012, traditional award that recognizes the best companies in the industry

OTHERS

10 years3 services

18 years4 services

4 years1 service

2 years2 services

2 years3 services

ELETRIC & BIOENERGY

3 years1 service

2 years1 service

2 years1 service

3 years3 services

3 years2 services

56 years9 services

34 years12 services

22 years1 service

9 years7 services

5 years7 services

PULP AND PAPER

17 years5 services

16 years1 service

17 years2 services

16 years2 services

16 years6 services

AUTOMOTIVE

28 years3 services

10 years7 services

3 years1 service

6 years2 services

28 years1 service

METAL & MINING

9 years4 services

15 years5 services

20 years4 services

13 years7 services

39 years7 services

FOOD & BEVERAGE

1º 1º1º 2º

JSL has been building relationships with its clients for more than 50 years

Currently with more than 300 clients

They begin in great majority with 1 service

JSL in figuresJSL in figures

+22,000 employees

More than 34,000 operating assets

Over 300 active clients

LTM logistics revenue

3.2 billion3.2 billion16 industries

CAGR2001-2011

28.3%28.3%25%

organic

Logistics

Dealerships and Insurance Brokers¹

VehiclesSold

Number R$ million

Total New Used Revenue

Total 2,031 1,323 708 82.7

Light 1,907 1,213 694 60.1

Heavy 124 110 14 22.6

¹Monthly average in 2012

• 1.156 insured

assets

• 66% renewal rate

15.3 million km mileage¹

6.4 milion liters of fuel¹

7,100 tires

bought¹

9.3 million transported passengers¹

30.7 million in

charter service payments¹

Da prospecção à operaçãoDa prospecção à operação

Eduardo PereiraEduardo Pereira

From prospecting to operationFrom prospecting to operation

• Services• Monitoring

From Prospecting to OperationFrom Prospecting to Operation

• Prospecting• Pricing• Closing

• Check list• Dedicated structure

Financing and acquisition

Implementation

Operation

Asset resale

New business development

From business

prospecting to operation

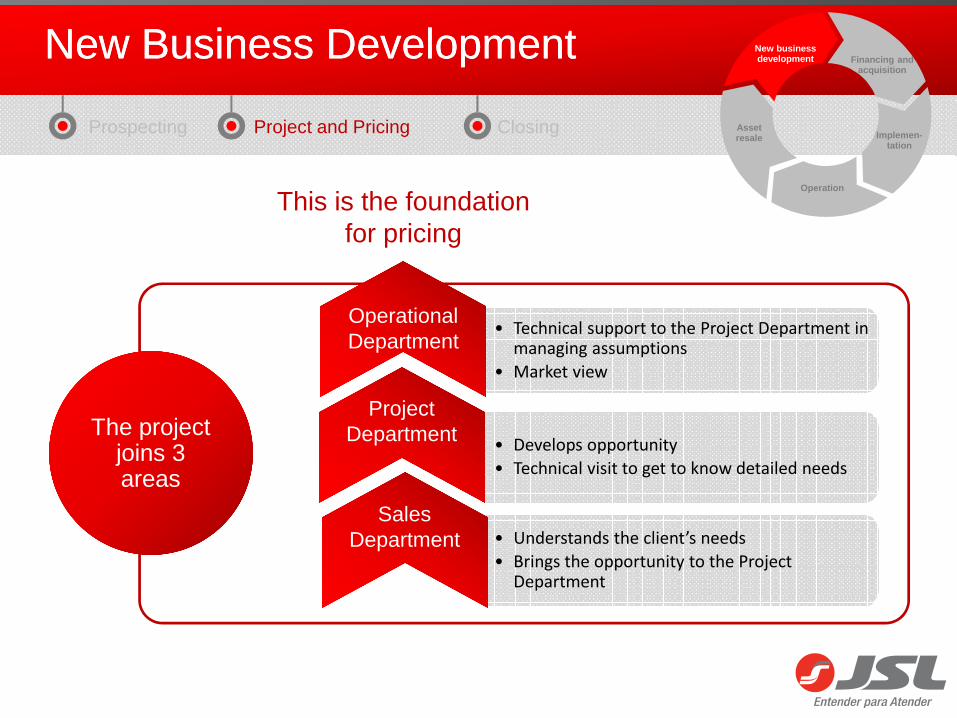

New Business DevelopmentNew Business Development

Active prospecting through clients

• The client contacts our sales department

• The Sales Department develops a new opportunity

• The Operational Department identifies a new potential service for a current client and submits it to the Sales Department

• Public bidding

Operations Executive Board

Mining Forestry Sugar and ethanolManagement

and Outsourcing CS Brasil

Development Management

Sales Executive

Board

General and dedicated cargo

Rental light equipment

Rental heavy equipment

Car manufacturing Machines/ Equipment

Chilled and International

Prospecting

Financing and acquisition

Implemen-tation

Operation

Asset resale

New business development

Negotiation: Only Sales Area takes

part

Negotiation: Only Sales Area takes

part

Project and Pricing Closing

New Business DevelopmentNew Business Development

Prospecting Project and Pricing Closing

• Understands the client’s needs

• Brings the opportunity to the Project Department

• Technical support to the Project Department in managing assumptions

• Market view

The project joins 3 areas

The project joins 3 areas

This is the foundation for pricing

Financing and acquisition

Implemen-tation

Operation

Asset resale

New business development

Project Department

Sales Department

• Develops opportunity

• Technical visit to get to know detailed needs

Operational Department

The pricing assumptions are ratified by the operational manager and the price is ratified by the Sales Executive Officer, for final

approval by the CEO or another Executive Officer

The pricing assumptions are ratified by the operational manager and the price is ratified by the Sales Executive Officer, for final

approval by the CEO or another Executive Officer

• Period: 2 to 10 years

• Adjustments

• Minimum volume

• Cancellation penalties

• Obligation to purchase in case of early termination

• Period: 2 to 10 years

• Adjustments

• Minimum volume

• Cancellation penalties

• Obligation to purchase in case of early termination

• Asset acquisition price

• Fixed asset depreciation

• Return on fixed asset

• Residual amount

• Operating costs

• Administrative expenses

• Taxes

• Margin

• Asset acquisition price

• Fixed asset depreciation

• Return on fixed asset

• Residual amount

• Operating costs

• Administrative expenses

• Taxes

• Margin

Sales ConditionsSales Conditions

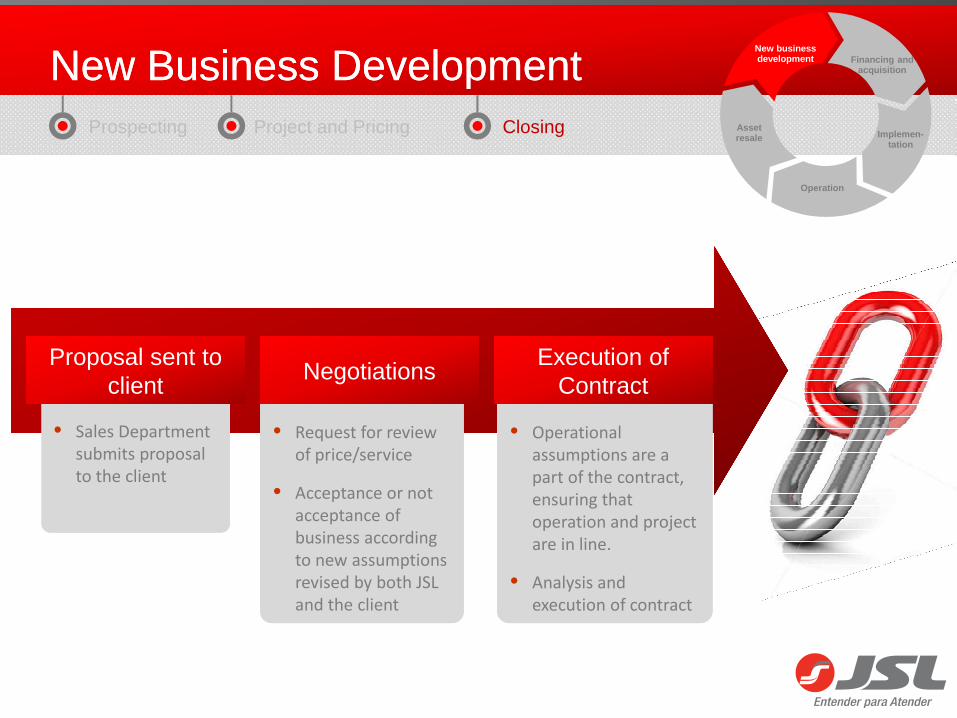

New Business DevelopmentNew Business Development

Prospecting Project and Pricing Closing

PricingPricing• Assumptions

• Management software

• Pricing spreadsheet

• Pricing and Sales Conditions

++

Financing and acquisition

Implemen-tation

Operation

Asset resale

New business development

Financing and acquisition

Implemen-tation

Operation

Asset resale

New business developmentNew Business DevelopmentNew Business Development

Prospecting Project and Pricing Closing

• Operational assumptions are a part of the contract, ensuring that operation and project are in line.

• Analysis and execution of contract

• Operational assumptions are a part of the contract, ensuring that operation and project are in line.

• Analysis and execution of contract

• Request for review of price/service

• Acceptance or not acceptance of business according to new assumptions revised by both JSL and the client

• Request for review of price/service

• Acceptance or not acceptance of business according to new assumptions revised by both JSL and the client

• Sales Department submits proposal to the client

• Sales Department submits proposal to the client

Proposal sent to client

Proposal sent to client

NegotiationsNegotiationsExecution of

ContractExecution of

Contract

Checklist of deployment for involved areas

E-mailInformar o layout do EDI (comunicação Cliente/JSL)

20-30 dias de antecedência

Verificar a possibilidade com o cliente de fornecer internet Solicitar link de internet

Informar necessidade de internet 3G

Informar os usuários para email2 dias de

antecedênciaFiscal - Abertura de filial Contato da área Prazo Via Aplicável

Entrar em contato com a matriz (Controladoria) para verificar a necessidade de abertura de filial ou ponto de apoio

Antônio Carlos Ajudarte

30 dias para Estado de SP,

60 dias outros

Estados

Enviar para o setor Fiscal o endereço da nova filial (ATENÇÃO: CEP Verificar se o CEP é o mesmo nos Correios/Prefeitura e outros órgãos)

Vânia de Siqueira

Enviar a documentação que comprove a regularidade do local (Laudo do bombeiro, certidão de débitos na prefeitura, pauta aprovada, habite-se)Enviar a documentação para a locação do local ao JurídicoVerificar na prefeitura se podemos exercer a atividade e enviar o comprovante (Depende de cada região: Uso do solo, diretrizes, viabilidade)

Providenciar licenças para o exercício da atividadeVerificar na prefeitura se não existe outra empresa cadastrada no local e enviar o comprovante (Prefeitura e Secretaria da Fazenda)

Fiscal - Documentação Contato da área Prazo Via AplicávelInformar ao setor Fiscal a operação juntamente com o número de inscrição e CNPJ

Fábio Barbosa7 dias de

antecedênciaE-mail

Solicitar a área Fiscal os formuláriosDefinir junto ao Fiscal a forma de preenchimento e emissão de conhecimentosLigar para a matriz em caso de dúvida quanto à tributação

Cadastro Contato da área Prazo Via AplicávelSolicitar cadastro dos veículos

Diorwilton Heusser

Após chegada dos

ativos

Sistema

Solicitar cadastro dos equipamentos

Solicitar cadastro de motoristasApós

admissão dos motoristas

Solicitar cadastro de usuários no sistemaApós

admissão dos usuários

Solicitar cadastro de rotas 1ª semana de

implantaçãoSolicitar cadastro de pontos de entrega (CNPJ origem/destino)

Solicitar cadastro de tabela comercial no sistemaApós

definido o modelo fiscal

Sistema de Gestão Contato da área Prazo Via AplicávelDefinir procedimentos padrões

Simone GonzalezAté 30 dias após início

da operaçãoE-mail

Definir meios de controle da operação

Definir os indicadores operacionaisValidar com SGI (Sistema de Gestão Integrada)Treinamento da equipe envolvida

Definir modelos de relatórios a serem usados na operação

ChecklistChecklist Financing and acquisition

Implemen-tation

Operation

Asset resale

New business development

Raio X das OperaçõesRaio X das Operações

Adriano ThieleAdriano Thiele

X-Ray of OperationsX-Ray of Operations

Business LinesBusiness Lines

Dedicated Services

Management and Outsourcing

Passenger Transportation

General Cargo

Leading company

focused on high value-added businesses

Leading company

focused on high value-added businesses

* JSL + Schio Gross Revenue from Services in the last 12 months

Source: Booz Allen

LOGISTICS SERVICES PYRAMID

Supply chain management and

integrated distribution

Value-added

services

Combination of transportation and

warehousing services

Transportation orwarehousing

Hig

her

Val

ue A

dded

*

*

R$1.5 billionLTM revenue

R$1.5 billionLTM revenue

Complete logistics solutionsComplete logistics solutions

Supply Chain Dedicated ServicesSupply Chain Dedicated Services

• High value added with integrated, flexible and customized solutions• Physical and human resources exclusively allocated to the operation• Specific IT and processes• Demands high technical specifications

* Proforma Schio + JSL Gross Revenue from Services in the last 12 months¹ Proforma Schio + JSL Gross Revenue from Dedicated Services n the last 12 months² 2Q12 base date

Main Sectors(% of Revenue¹):

• Food (26.6%)

• Pulp and Paper (19.5%)

• Automotive (18.5%)

• Steel and Mining (10.5%)

• Sugar and Ethanol (6.7%)

Main Sectors(% of Revenue¹):

• Food (26.6%)

• Pulp and Paper (19.5%)

• Automotive (18.5%)

• Steel and Mining (10.5%)

• Sugar and Ethanol (6.7%)

• Dedicated operations, customized client service

• Complete portfolio of services

• High client loyalty levels

• High cross-selling rates

• Dedicated operations, customized client service

• Complete portfolio of services

• High client loyalty levels

• High cross-selling rates

What we doWhat we doExpertise in several

sectors of the economyExpertise in several

sectors of the economy

Gross Revenue from Services

Gross Revenue from Services

INBOUND WAREHOUSING AND INTERNAL LOGISTICS

OUTBOUND

CAGR 08-11: +17.8%

*

• Input handling and warehousing• Production line supply• Stockroom management• Handling and warehousing of finished products• Shipment of finished products

* 10,412 Employees²7,819 Operational Assets²10,412 Employees²7,819 Operational Assets²

Supply Chain Dedicated ServicesSupply Chain Dedicated Services

• Revenue of R$157.6 million

• Services:- Loading and transportation of ore- Waste management- Highway maintenance- Industrial cleaning- Road watering

• 993 Employees¹ and 603 Operational Assets¹

• Revenue of R$157.6 million

• Services:- Loading and transportation of ore- Waste management- Highway maintenance- Industrial cleaning- Road watering

• 993 Employees¹ and 603 Operational Assets¹

Steel and MiningSteel and Mining

• Revenue of R$291.5 million• Services:

- Loading and transportation of wood - Handling and transportation of pulp

- Industrial cleaning- Waste removal

• 2,203 Employees¹ and 2,346 Operational Assets¹

• Revenue of R$291.5 million• Services:

- Loading and transportation of wood - Handling and transportation of pulp

- Industrial cleaning- Waste removal

• 2,203 Employees¹ and 2,346 Operational Assets¹

Pulp and PaperPulp and Paper

• Revenue of R$277.2 million

• Services:- Milk run- Just in time- Cross docking- Information management- Production line supply- Stockroom management

• 1,322 Employees¹ and 1,164 Operational Assets¹

• Revenue of R$277.2 million

• Services:- Milk run- Just in time- Cross docking- Information management- Production line supply- Stockroom management

• 1,322 Employees¹ and 1,164 Operational Assets¹

AutomotiveAutomotive

*Percentage of proforma Schio + JSL Gross Revenue from Services in the last 12 months¹ 2Q12 base date

*

Supply Chain Dedicated ServicesSupply Chain Dedicated Services

• Revenue of R$398.1 million

• Services:- Inbound/outbound- Warehousing/handling of frozen and chilled products- Labor outsourcing

• 4,290 Employees¹ and1,944 Operational Assets

• Revenue of R$398.1 million

• Services:- Inbound/outbound- Warehousing/handling of frozen and chilled products- Labor outsourcing

• 4,290 Employees¹ and1,944 Operational Assets

Food and BeveragesFood and

Beverages

• Revenue of R$100.9 million

• Services:- Transportation of chopped sugarcane- Transportation of sugarcane from the field to the industrial unit941 Employees¹ and849 Operational Assets¹

• Revenue of R$100.9 million

• Services:- Transportation of chopped sugarcane- Transportation of sugarcane from the field to the industrial unit941 Employees¹ and849 Operational Assets¹

Sugar and Ethanol

Sugar and Ethanol

* Proforma Schio + JSL Gross Revenue from Services in the last 12 months¹ 2Q12 base date

*

Automotive (example)

Dedicated Services, Fleet Management and Outsourcing and Passengers Transportation

Fleet management and outsourcing

Transportation of employees

Internal handling and assembly of kits

Shipping.Outbound

Delivery of raw materials.Inbound

Inventory maintenance and management

Electronic registration of

inventory

Invoicing

Auto parts.Milk run.

Rental of vehicle withdriver at the client’s

disposal

Mining (example)Mining (example)

Dedicated Services, Fleet Management and Outsourcing and Passengers Transportation

Loading of ore

Highwaymaintenance

Transport of ore

Wastemanagement

Unloadingof ore

24-hour monitoring via satellite and telemetry

Transportationcenter

R$637 millionLTM revenue

R$637 millionLTM revenue

Equipment and Fleet Management and OutsourcingEquipment and Fleet Management and Outsourcing

Solution ranging from fleet size management to the complete management of the service

Gross Revenue from Fleet Magament and

Outsourcing

Gross Revenue from Fleet Magament and

Outsourcing

CAGR 08-11: +27%

• More than 19,000 leased vehicles in operation

• Lease with and without services

• More than 19,000 leased vehicles in operation

• Lease with and without services

Light Fleet Management and Outsourcing

Light Fleet Management and Outsourcing

• More than 1,000 leased heavy vehicles in operation

• More than 2,000 leased pieces of machinery and equipment in operation

• More than 1,000 leased heavy vehicles in operation

• More than 2,000 leased pieces of machinery and equipment in operation

Equipment and Heavy Fleet Management and OutsourcingEquipment and Heavy Fleet

Management and Outsourcing

• Proforma Schio + JSL Gross Revenue from Services in the last 12 months ¹ 2Q12 base date

*

*2,577 Employees¹

22,374 Operational Assets¹2,577 Employees¹

22,374 Operational Assets¹

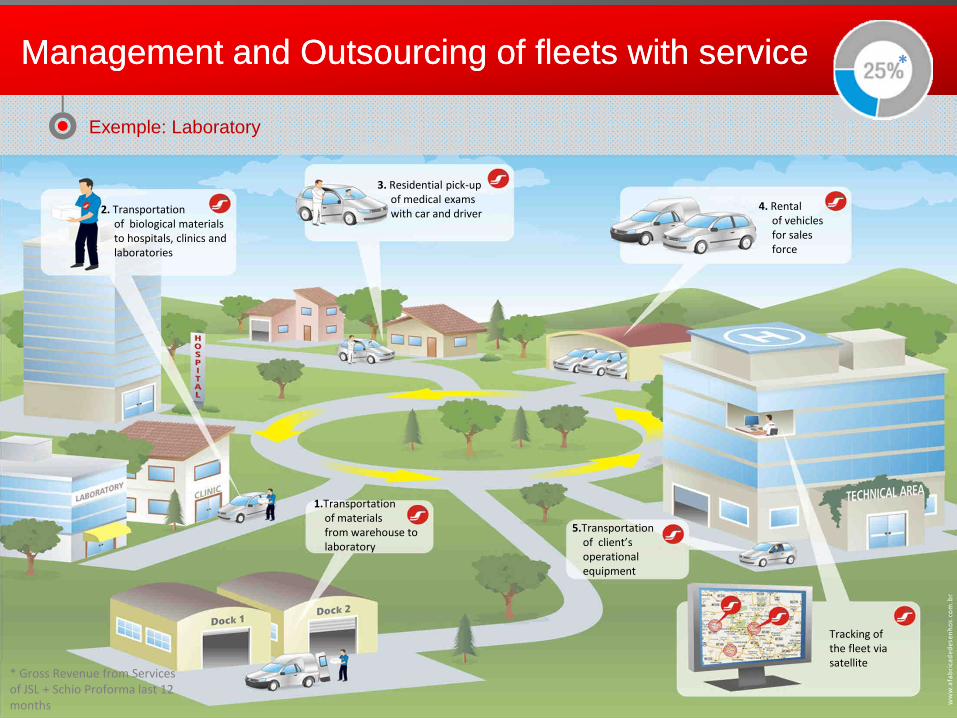

1.Transportation of materials from warehouse to laboratory

2. Transportation of biological materialsto hospitals, clinics and laboratories

4. Rentalof vehicles for sales force

3. Residential pick-up of medical exams with car and driver

5.Transportation of client’s operational equipment

Tracking of the fleet via satellite

Exemple: Laboratory

Management and Outsourcing of fleets with serviceManagement and Outsourcing of fleets with service *

* Gross Revenue from Services of JSL + Schio Proforma last 12 months

Passenger TransportationPassenger Transportation

R$ 351 millionGross revenue in the last 12 months

R$ 351 millionGross revenue in the last 12 months

CAGR 11-08: +14.9%Gross Revenue from Passenger

Transportation

Gross Revenue from Passenger

Transportation

Correlation diversification strategy

• Corporate (Permanent Charter) and Tourism Passenger Chartering

• Corporate (Permanent Charter) and Tourism Passenger Chartering

Charter ServicesCharter Services

• Municipal and intercity urban lines

• Municipal and intercity urban lines

Urban Transportation

Urban Transportation

*

* Pro-forma Gross Revenue from Services of JSL + Schio in the last 12 months¹ Reference date 2Q12

*

3,165 Employees¹1,072 Operating Assets¹3,165 Employees¹1,072 Operating Assets¹

Services for clients who present high variation in volumeInformation specification and management

General CargoGeneral Cargo

R$ 247 millionGross revenue in the last 12 months

R$ 247 millionGross revenue in the last 12 months

CAGR 08-11: +7,2%Gross Revenue from General

Cargo

Gross Revenue from General

Cargo

• Closed cargo transportation operations from point A to point B• More than 95% transported by independent contractors and third

parties • High seasonality within the month/year• Physical and human resources non-exclusive to a client/operation• Average cycles without guaranteed counter-flow• Expertise in the hiring of third parties/independent contractors• Contracts with reduced terms

• Closed cargo transportation operations from point A to point B• More than 95% transported by independent contractors and third

parties • High seasonality within the month/year• Physical and human resources non-exclusive to a client/operation• Average cycles without guaranteed counter-flow• Expertise in the hiring of third parties/independent contractors• Contracts with reduced terms

General Cargo TransportationGeneral Cargo Transportation

*

* Pro-forma Gross Revenue from Services of JSL + Schio in the last 12 months¹ Reference date 2Q12

*

292 Employees¹728 Operating Assets¹292 Employees¹728 Operating Assets¹

Management Structure

Dedicated structure to each operationDedicated structure to each operation

Chief Operations Officer

Adriano Thiele

Mining Forestry Sugar and EthanolManagement

and OutsourcingPassanger

Transportation

Business Development Management

Manager by Client

Waste ManagerFleet Outsourcing

ManagerCharting Manager

Mine handling Manager

Support areas: Maintenance, HSE and

Personnel

*

MAIN LINK WITH CLIENTS (SINGLE CHANNEL)• Ensures culture• Captures synergies• Identification and implementation of the best internal

and market practices

Quest for continuous improvement, generating new business and perpetuating

customer relationship

Quest for continuous improvement, generating new business and perpetuating

customer relationshipAdriano ThieleAdriano Thiele

Case: ValeCase: Vale

Optimization of passenger transportation routes

Improvement Project• Optimization/Redefining of routes

• Reduced mileage

• Increased occupancy rate of vehicles

• Reduced number of vehicles

• Use of Simulation Software

• Improvements shared with clients on a 50%/50% basis

• 168 Administrative Buses and Shifts

• Daily transportation of 6,300 employees

• 168 Administrative Buses and Shifts

• Daily transportation of 6,300 employees

Current OperationCurrent Operation

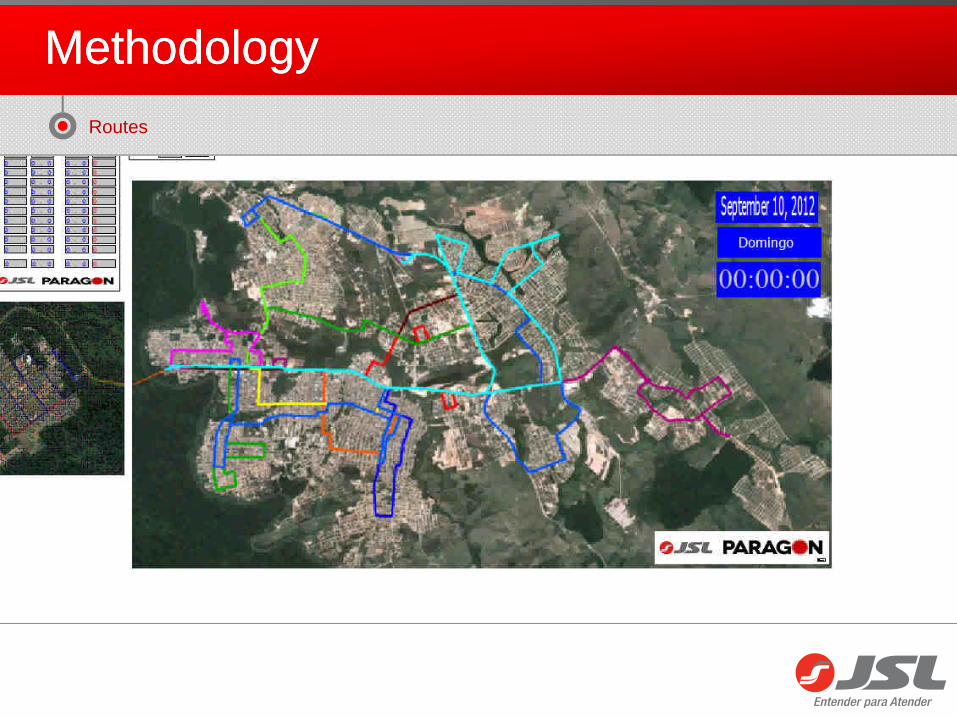

MethodologyMethodology

Chart Occupancy Rate – Monthly Analysis

Occ

upan

cy R

ate

MethodologyMethodology

Chart Occupancy Rate – Daily Analysis

Historical 28 daysOP34 route

Number of passengers

Num

ber

of o

ccur

renc

es%

Cum

ulative

MethodologyMethodology

Routes

Preliminary ResultsPreliminary Results

ADMINISTRATIVE CONTRACT - IRON/MANGANESE:

• 38 buses – daily transportation of 1,521 people

• Reduction of 2 buses (5.2% of total) due to the lower number of vehicles after passing the gateway

• Higher vehicle occupancy rate

ADMINISTRATIVE CONTRACT - IRON/MANGANESE:

• 38 buses – daily transportation of 1,521 people

• Reduction of 2 buses (5.2% of total) due to the lower number of vehicles after passing the gateway

• Higher vehicle occupancy rate

Preliminary simulation results

Preliminary simulation results

• Redefining of routes due to the occupancy rate - 6,300 pickup points

• Impact from adoption of equipment with higher number of seats

• Replicating the model developed for other mines

• Reduced number of pickup points

• Redefining of routes due to the occupancy rate - 6,300 pickup points

• Impact from adoption of equipment with higher number of seats

• Replicating the model developed for other mines

• Reduced number of pickup points

Current scenariosCurrent scenarios

Operations in numbersOperations in numbers

Total Gross Revenue from Services*R$ 2.8 billion

18.2 thousand Employees¹

31.3 thousand operating Assets¹

139 branches

Total Gross Revenue from Services*R$ 2.8 billion

18.2 thousand Employees¹

31.3 thousand operating Assets¹

139 branches

* Gross Revenue from Services JSL + Schio Proforma last 12 months¹ Base date 2T12

Pricing, Monitoringand Capital StructurePricing, Monitoring

and Capital Structure

Denys Marc FerrezDenys Marc Ferrez

Administrative StructureAdministrative Structure

• Executive Officers• Procurement• Asset Management• Legal Department• New Businesses• Customer Services

• Investor Relations• Financial Services• Controllership• Projects• Communication and Marketing• Cargo/Dedicated Services Operations• Electronic means of payment

• Fleet Outsourcing and Management• Information Technology• Schio• Dealerships

• HSE• Medical Department• Personnel Department• Recruiting and Selection• Cafeteria

YOU ARE

HERE!

Contract PricingContract Pricing

Pricing tables

Contract PricingContract Pricing

Sizing

Ano 2011 2012 2013 2014 2015 TOTALVolume (ton/ano) 333.333 2.000.000 2.000.000 2.000.000 2.000.000 8.333.333Período contrato (meses) 1 12 12 12 6 43Período safra (meses) 1 6 6 6 6 25Período safra (dias) 30 180 180 180 180 174Período de paralisações (%) 20% 20% 20% 20% 20% 20%Período de paralisações (dias/ano) 6 36 36 36 36 35Período produtivo (dias/ano) 24 144 144 144 144 139Período produtivo (dias/mês) 24 24 24 24 24 24Volume (ton/mês) 333.333 333.333 333.333 333.333 333.333 333.333Volume (ton/dia) 13.889 13.889 13.889 13.889 13.889 13.889Operação Colheita Colheita Colheita Colheita Colheita ColheitaEquipamento 1 colhedora colhedora colhedora colhedora colhedora colhedoraProdução (ton/hr/equipamento) 40 40 40 40 40 40DF - Disponibilidade física 90% 90% 90% 90% 90% 90%DO - Disponibilidade operacional 85% 85% 85% 85% 85% 85%DO + DF 77% 77% 77% 77% 77% 77%Produtividade (hr/mês) 441 441 441 441 441 441Produtividade (hr/dia) 18,36 18,36 18,36 18,36 18,36 18,36Produção (ton/dia/equipamento) 734,4 734,4 734,4 734,4 734,4 734,4Total de equipamento 1 (qtd) 19 19 19 19 19 19Operação Transbordo Transbordo Transbordo Transbordo Transbordo TransbordoEquipamento 1 trator trator trator trator trator tratorEquipamento 2 transbordo transbordo transbordo transbordo transbordo transbordoProdução (ton/hr/equipamento) 20 20 20 20 20 20DF - Disponibilidade física 90% 90% 90% 90% 90% 90%DO - Disponibilidade operacional 85% 85% 85% 85% 85% 85%DO + DF 77% 77% 77% 77% 77% 77%Produtividade (hr/mês) 441 441 441 441 441 441Produtividade (hr/dia) 18,36 18,36 18,36 18,36 18,36 18,36Produção (ton/dia/equipamento) 367,2 367,2 367,2 367,2 367,2 367,2Total de equipamento 1 (qtd) 38 38 38 38 38 38Total de equipamento 2 (qtd) 76 76 76 76 76 76Operação Transporte Transporte Transporte Transporte Transporte TransporteEquipamento 1 cavalo cavalo cavalo cavalo cavalo cavaloEquipamento 2 rodotrem rodotrem rodotrem rodotrem rodotrem rodotremProdução (ton/viagem) 60 60 60 60 60 60DF - Disponibilidade física 90% 90% 90% 90% 90% 90%DO - Disponibilidade operacional 85% 85% 85% 85% 85% 85%DO + DF 77% 77% 77% 77% 77% 77%Produtividade (hr/mês) 441 441 441 441 441 441Produtividade (hr/dia) 18,36 18,36 18,36 18,36 18,36 18,36Distancia média (km ida e volta) 62,5 62,5 62,5 62,5 62,5 62,5Tempo carga (hr) 0,5 0,5 0,5 0,5 0,5 0,5Tempo descarga (hr) 0,5 0,5 0,5 0,5 0,5 0,5Velocidade (km/hr) 35 35 35 35 35 35Produção (viagem/dia/equipamento) 7 7 7 7 7 7Produção (ton/dia/equipamento) 395 395 395 395 395 395Produção (km/mês/equipamento 1) 9886 9886 9886 9886 9886 9886Produção (km/mês/equipamento 2) 4943 4943 4943 4943 4943 4943Total de equipamento 1 (qtd) 36 36 36 36 36 36Total de equipamento 2 (qtd) 72 72 72 72 72 72

DIMENSIONAMENTO

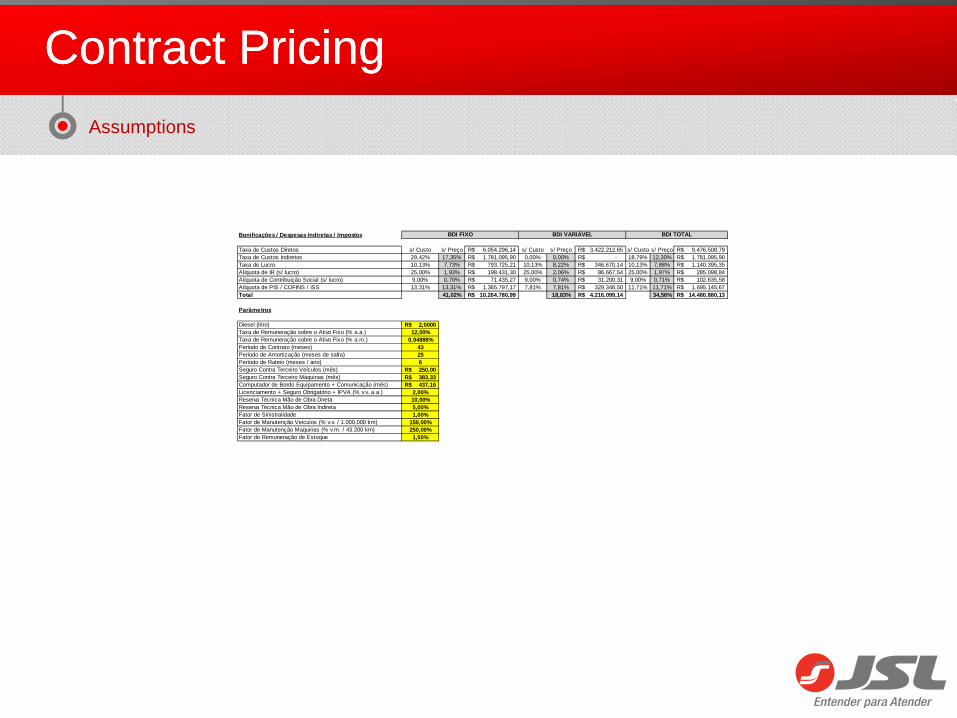

Contract PricingContract Pricing

Assumptions

Bonificações / Despesas Indiretas / Impostos

Taxa de Custos Diretos s/ Custo s/ Preço 6.054.296,14R$ s/ Custo s/ Preço 3.422.212,65R$ s/ Custo s/ Preço 9.476.508,79R$ Taxa de Custos Indiretos 29,42% 17,35% 1.781.095,90R$ 0,00% 0,00% -R$ 18,79% 12,30% 1.781.095,90R$ Taxa de Lucro 10,13% 7,73% 793.725,21R$ 10,13% 8,22% 346.670,14R$ 10,13% 7,88% 1.140.395,35R$ Alíquota de IR (s/ lucro) 25,00% 1,93% 198.431,30R$ 25,00% 2,06% 86.667,54R$ 25,00% 1,97% 285.098,84R$ Alíquota de Contribuição Social (s/ lucro) 9,00% 0,70% 71.435,27R$ 9,00% 0,74% 31.200,31R$ 9,00% 0,71% 102.635,58R$ Alíquota de PIS / COFINS / ISS 13,31% 13,31% 1.365.797,17R$ 7,81% 7,81% 329.348,50R$ 11,71% 11,71% 1.695.145,67R$ Total 41,02% 10.264.780,99R$ 18,83% 4.216.099,14R$ 34,56% 14.480.880,13R$

Parâmetros

Diesel (litro) 2,0000R$ Taxa de Remuneração sobre o Ativo Fixo (% a.a.) 12,00%Taxa de Remuneração sobre o Ativo Fixo (% a.m.) 0,94888%Período de Contrato (meses) 43Período de Amortização (meses de safra) 25Período de Rateio (meses / ano) 6Seguro Contra Terceiro Veículos (mês) 250,00R$ Seguro Contra Terceiro Máquinas (mês) 383,33R$ Computador de Bordo Equipamento + Comunicação (mês) 437,16R$ Licenciamento + Seguro Obrigatório + IPVA (% v.v. a.a.) 2,00%Reserva Técnica Mão de Obra Direta 10,00%Reserva Técnica Mão de Obra Indireta 5,00%Fator de Sinistralidade 1,00%Fator de Manutenção Veiculos (% v.v. / 1.000.000 km) 150,00%Fator de Manutenção Maquinas (% v.m. / 43.200 km) 250,00%Fator de Remuneração de Estoque 1,50%

BDI VARIÁVEL BDI TOTALBDI FIXO

Operação

Equipamento

Qtd.FIX Fator RT Fator

DF/DO

Hr - Km Prod. /

Mês

Investimento Residual

Custo Fixo Custo Variável

Lucro Impostos (IR/CS)

Impostos (PIS/COFINS/ISS)

PreçoUnitárioMensal

Custo de Propriedade

(RC + DP)

Seguro Contra Terceiro

Computador de Bordo

Fator de Sinistralidade

Documentação (IPVA + DPVAT + Licenc.)

Mão de Obra

Indiretos Total Lubrificante / Lavagem

Peças de Reposição Pneus / Esteiras Combustível

Total

Tipo Marca Equip. Acess. Total Equip. Acess. Total Qtd./Eqpto. Custo Custo /

Hr - Km Custo /

Mês Custo /

Mês Consumo (lt/hr - km/lt) Custo / Mês

COLHEITA Colhedora de esteira John Deere 3520 19 11% 76,50% 441 hr R$ 800.000,00 R$ - R$ 800.000,00 30% 0% 30% R$ 30.900,84 R$ 423,68 R$ 483,18 R$ 736,84 R$ - 4 R$ 59.788,74 R$ 27.163,26 R$ 119.496,55 R$ 5.600,42 R$ 46,30 R$ 20.400,00 R$ 6.381,68 40 lt/hr R$ 35.251,20 R$ 67.633,30 R$ 18.956,25 R$ 6.445,13 R$ 28.177,61 R$ 240.708,83

TRANSBORDO

Trator 185 cv John Deere 7185 38 21% 76,50% 441 hr R$ 200.000,00 R$ - R$ 200.000,00 30% 0% 30% R$ 8.460,94 R$ 464,04 R$ 529,20 R$ 201,75 R$ - 4 R$ 27.035,26 R$ 10.794,08 R$ 47.485,27 R$ 2.572,21 R$ 11,57 R$ 5.100,00 R$ 581,64 12 lt/hr R$ 10.575,36 R$ 18.829,21 R$ 6.717,66 R$ 2.284,00 R$ 9.985,49 R$ 85.301,63

Transbordo 10,5 ton Saltal VT10 76 11% 76,50% 441 hr R$ 80.000,00 R$ - R$ 80.000,00 30% 0% 30% R$ 3.090,08 R$ 423,68 R$ 483,18 R$ 73,68 R$ - 0 R$ - R$ 1.197,53 R$ 5.268,16 R$ - R$ 4,63 R$ 2.040,00 R$ 387,76 0 lt/hr R$ - R$ 2.427,76 R$ 779,60 R$ 265,06 R$ 1.158,84 R$ 9.899,42

TRANSPORTE

Cavalo 6x4 420 cv com ar condicionado Scania G420 36 19% 76,50% 9.886 km R$ 300.000,00 R$ - R$ 300.000,00 40% 0% 40% R$ 11.226,86 R$ 298,61 R$ 522,17 R$ 298,61 R$ 1.194,44 4 R$ 27.035,26 R$ 11.936,92 R$ 52.512,87 R$ 736,14 R$ 0,45 R$ 4.448,90 R$ 2.416,68 1,2 km/lt R$ 16.477,40 R$ 24.079,12 R$ 7.758,77 R$ 2.637,98 R$ 11.533,06 R$ 98.521,80

Rodotrem Canavieiro de 12,5m Rodolinea 72 8% 76,50% 4.943 km R$ 220.000,00 R$ - R$ 220.000,00 40% 0% 40% R$ 7.467,17 R$ 270,83 R$ 473,59 R$ 198,61 R$ 794,44 0 R$ - R$ 2.707,89 R$ 11.912,54 R$ - R$ 0,33 R$ 1.631,26 R$ 2.900,02 0,0 km/lt R$ - R$ 4.531,28 R$ 1.665,76 R$ 566,36 R$ 2.476,08 R$ 21.152,02

APOIO

Caminhão Comboio Abastecimento 9.000l VW 26260 / Gascom 4 25% 76,50% 2.400 km R$ 185.000,00 R$ 80.000,00 R$ 265.000,00 50% 10% 38% R$ 10.626,96 R$ 312,50 R$ 546,46 R$ 276,04 R$ 1.104,17 4 R$ 29.572,87 R$ 12.485,00 R$ 54.924,00 R$ 281,60 R$ 0,40 R$ 954,00 R$ 528,00 2,5 km/lt R$ 1.920,00 R$ 3.683,60 R$ 5.936,95 R$ 2.018,56 R$ 8.825,00 R$ 75.388,11

Caminhão Bombeiro 15.000l VW 26260 / Gascom 4 25% 76,50% 2.400 km R$ 185.000,00 R$ 90.000,00 R$ 275.000,00 50% 10% 37% R$ 11.154,22 R$ 312,50 R$ 546,46 R$ 286,46 R$ 1.145,83 4 R$ 25.311,69 R$ 11.401,86 R$ 50.159,02 R$ 281,60 R$ 0,41 R$ 990,00 R$ 528,00 2,5 km/lt R$ 1.920,00 R$ 3.719,60 R$ 5.457,90 R$ 1.855,69 R$ 8.112,92 R$ 69.305,13

Caminhão Oficina VW 26260 / Gascom 4 25% 76,50% 2.400 km R$ 185.000,00 R$ 60.000,00 R$ 245.000,00 50% 10% 40% R$ 9.572,44 R$ 312,50 R$ 546,46 R$ 255,21 R$ 1.020,83 4 R$ 25.311,69 R$ 10.890,55 R$ 47.909,69 R$ 281,60 R$ 0,37 R$ 882,00 R$ 528,00 2,5 km/lt R$ 1.920,00 R$ 3.611,60 R$ 5.219,11 R$ 1.774,50 R$ 7.757,96 R$ 66.272,86

Total 253 13% R$ 57.740.000,00 R$ 920.000,00 R$ 58.660.000,00 35% 10% 35% R$ 2.210.695,59 R$ 91.883,33 R$ 125.466,21 R$ 55.587,50 R$ 113.283,33 420 R$ 3.457.380,17 R$ 1.781.095,90 R$ 7.835.392,04 R$ 234.032,04 R$ 1.025.355,17 R$ 474.962,70 R$ 1.687.862,74 R$ 3.422.212,65 R$ 1.140.395,35 R$ 387.734,42 R$ 1.695.145,67 R$ 14.480.880,13

Total Máquinas 133 441 hr R$ 28.880.000,00 R$ - R$ 28.880.000,00 R$ 1.143.478,18 R$ 57.883,33 R$ 66.011,84 R$ 27.266,67 R$ - R$ 2.163.325,85 R$ 1.017.288,99 R$ 4.475.254,86 R$ 204.151,84 R$ 1.671,30 R$ 736.440,00 R$ 172.824,48 R$ 1.071.636,48 R$ 2.185.052,80 R$ 674.689,17 R$ 229.394,32 R$ 1.002.894,66 R$ 8.567.285,80

Total Veículos 120 3.206 km R$ 28.860.000,00 R$ 920.000,00 R$ 29.780.000,00 R$ 1.067.217,41 R$ 34.000,00 R$ 59.454,37 R$ 28.320,83 R$ 113.283,33 R$ 1.294.054,32 R$ 763.806,91 R$ 3.360.137,18 R$ 29.880,20 R$ 44,67 R$ 288.915,17 R$ 302.138,22 R$ 616.226,26 R$ 1.237.159,85 R$ 465.706,19 R$ 158.340,10 R$ 692.251,00 R$ 5.913.594,33

Operação Tipo Marca FIX RT TT

COLHEITA Colhedora de esteira John Deere 3520 19 2 21

TRANSBORDOTrator 185 cv John Deere 7185 38 8 46

Transbordo 10,5 ton Saltal VT10 76 8 84

TRANSPORTECavalo 6x4 420 cv com ar condicionado Scania G420 36 7 43

Rodotrem Canavieiro de 12,5m Rodolinea 72 6 78

APOIO

Caminhão Comboio Abastecimento 9.000l VW 26260 / Gascom 4 1 5

Caminhão Bombeiro 15.000l VW 26260 / Gascom 4 1 5

Caminhão Oficina VW 26260 / Gascom 4 1 5

Total 253 34 287

Contract PricingContract Pricing

Calculation spreadsheet

Contract PricingContract Pricing

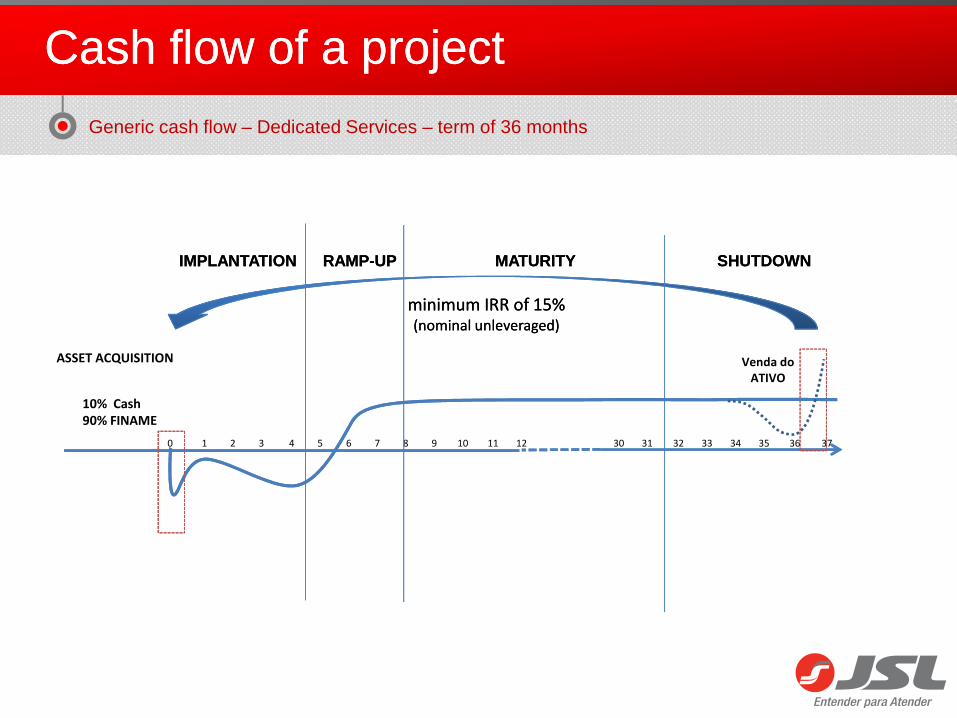

Mobilization period

Ramp-up of revenueand maturity

Sale of assetsexcluding renewal

Cash Flow

Premises• Amortization term: 36 months• Residual value from asset sales:

35.0%• Investment: R$66.5 million• Technical reserve: 10.00%

Nominal Delev. IRR

(p.a.)

• 18.8%

EBITDA margin

• 26.2%

Return

Cash flow of a projectCash flow of a project

IMPLANTATIONIMPLANTATION RAMP-UPRAMP-UP MATURITYMATURITY SHUTDOWNSHUTDOWN

ASSET ACQUISITION Venda doATIVO

minimum IRR of 15%(nominal unleveraged)

minimum IRR of 15%(nominal unleveraged)

10% Cash90% FINAME

0 1 2 3 4 5 6 7 8 9 10 11 12 30 31 32 33 34 35 36 37

Generic cash flow – Dedicated Services – term of 36 months

Meeting Results – Managerial IndicatorsMeeting Results – Managerial Indicators

Assessment for each operation

More than 500cost centers

em 000 Mês Meses

Anteriores

com

entá

rios

Mês Meses

Anteriores

Veiculo Modelo Qt. Fatur. Fat./Carro Julho Junho Km K m/Veic. Julho Junho

14856 19.745.255 1.329 1.342 1.272 160.374.846 10.795 74 64 Faturamento/ Investido 4,77%

Início do Contrato Mês/Ano Mês/Ano Mês/Ano Proximo Reajuste

Manutenção por

veículo

Ultimos Reajustes Mês Julho R$ 177,23

Indice Indice Agosto R$ 171,69

Acumulado Média 2012 Média 2011

Agosto Julho Junho Maio Abril 2012

F. Pagto 959,98 987,62 906,72 826,68 876,04 6.776,50 847,06 659,77

Salários 489,62 525,44 462,25 420,45 435,40 3.536,19 442,02 341,15

Encargos Sociais 324,78 331,40 329,37 287,61 263,18 2.219,01 277,38 214,21

Benefícios 145,57 130,77 115,09 118,63 177,46 1.021,30 127,66 104,41

Numero de Funcionários 312,00 313,00 284,00 273,00 2 72,00

Desp. Gerais 754,84 953,52 731,09 739,20 947,05 6.403,58 800,45 350,02

Total Desp. Filial 1.714,81 1.941,15 1.637,81 1.565, 88 1.823,09 13.180,08 1.647,51 1.009,80

Despesas Operacionais 14.072,53 13.741,72 13.325,31 13.092,32 12.084,76 100.194,02 12.524,25 8.550,57

Despesas Administrativas Local 344,28 679,34 510,1 4 515,01 682,46 4.652,87 581,61 459,49

Total Despesas 16.131,62 16.362,21 15.473,26 15.173, 22 14.590,31 118.026,98 14.753,37 10.019,85

Gestão 19.745,25 19.917,41 18.697,01 19.772,09 17.932,32 147.108,77 18.388,60 11.110,22

Reembolso Avarias 1.138,56 1.102,92 491,13 753,22 61 7,94 5.802,89 725,36 545,33

Reembolso Multas 65,48 62,43 58,16 136,68 520,25 1.2 24,93 153,12 112,47

Reembolso Sublocação 59,45 78,45 73,33 50,66 29,77 3 73,33 46,67 50,32

Faturamento Bruto 21.008,75 21.161,22 19.319,64 20. 712,65 19.100,28 154.509,92 19.313,74 11.818,34

Descontos e Abatimentos 217,73 224,15 (516,83) 251,16 391,33 1.128,07 141,01 108,50

Impostos (PIS / COFINS / ISS) 434,83 432,19 397,76 4 21,06 379,86 3.134,72 391,84 241,97

Faturamento Líquido 20.356,19 20.504,88 19.438,71 2 0.040,42 18.329,09 150.247,12 18.780,89 11.467,86

Resultado Oper. 4.224,57 4.142,67 3.965,45 4.867,21 3.738,78 32.220,14 4.027,52 1.448,01

% 20,11% 19,58% 20,53% 23,50% 19,57% 20,85% 20,85% 12,25%

Despesas Administrativas Matriz 2.026,44 1.794,71 1 .558,74 1.570,52 2.276,03 13.481,62 1.685,20 945,48

Resultado Liquido 2.198,14 2.347,95 2.406,71 3.296,6 9 1.462,75 18.738,52 2.342,32 502,53

% 10,46% 11,10% 12,46% 15,92% 7,66% 12,13% 12,13% 4,25%

Ebitda 10.410,55 10.689,33 10.611,77 11.541,02 9.467,15 82.534,79 10.316,85 5.406,64

Ebitda % 50,60% 51,57% 56,08% 56,88% 50,57% 54,52% 54,52% 46,70%

Meeting Results – Financial IndicatorsMeeting Results – Financial Indicators

Monthly financial assessment for each operation

Meeting Results – Operational IndicatorsMeeting Results – Operational Indicators

RESUMO GESTÃO E TERCEIRIZAÇÃO DE CAMINHÕES PRIVADOS acumulado

INDICADORES OPERACIONAIS

Previsto Por Veíc. Previsto Por Veíc. Previsto Por Veíc.

Total 0 4.172.424 0 4.940.266 0 4.281

Gestão 3.278

Reembolso Avarias 135

Reembolso Multas 232

Reembolso Sublocação 0

Previsto Diferença Previsto Diferença Média Previsto Diferença

R$ 0 3.788.989 0 3.993.781 0 3.800.338

Por Veículo 0 3.460 0 3.303 0 3.501

Total Mês Total Mês Total Mês

Alocadas Matriz R$ 463.690 537.956 535.981

Total Mês % Repres. /C.D.O. Total Mês % Repres. /C.D.O. Total Mês % Repres. /C.D.O.

Alocadas Local R$ 168.763 4,45% 197.095 4,94% 208.430 5,48%

Total Mês % Repres. /C.D.O. Total Mês % Repres. /C.D.O. Total Mês % Repres. /C.D.O.

Impostos R$ 79.726 2,10% 96.229 2,41% 86.394 2,27%

Total Mês % Repres. / Fat. % Repres. /C.D.O. Total Mês % Repres. / Fat. % Repres. /C.D.O. Total Mês % Repres. / Fat. % Repres. /C.D.O.

Depreciação e Remuneração De Capital R$ 2.299.016 55,10% 60,68% 2.436.229 49,31% 61,00% 2.179.136 46,90% 57,34%

Implantação Quant. Média Dias Ag. Fat. Média Dias Pós Fat. Total Dias Quant. Média Dias Ag. Fat. Média Dias Pós Fat. Total Dias Quant. Média Dias Ag. Fat. Média Dias Pós Fat. Total Dias

Implantação Total 113 22,0 100,0 122,0 39 17,0 102,0 119,0 58 46,3 140,1 186,4

Desmobilização

Desmobilização Cliente até o Pátio Total

Veículos Total

Total Mês Km / Veic. Total Mês Km / Veic. Total Mês Km / Veic.

Km Rodado Total 6.316.857 5.769 5.403.227 4.469 3.821.426 3.521

Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O. Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O. Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O.

Combustível - R$ R$ -277 -0,25 -0,00 -0,01% 905 0,75 0,00 0,02% 524 0,48 0,00 0,01%

Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O. Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O. Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O.

Pneus (novos, recapados, consertos e nitrogênio) R$ 119.437 109,07 0,02 3,15% 78.549 64,97 0,01 1,97% 86.355 79,56 0,02 2,27%

Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O. Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O. Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O.

Peças R$ 199.928 182,58 0,03 5,28% 212.659 175,90 0,04 5,32% 217.467 200,36 0,06 5,72%

Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O. Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O. Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O.

Manutenção (máquinas, equip., veículos, lubrificantes e serviços)R$ 174.681 159,53 0,03 4,61% 129.576 107,18 0,02 3,24% 162.785 149,98 0,04 4,28%

Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O. Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O. Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O.

Lubrificantes R$ 21.469 19,61 0,00 0,57% 25.126 20,78 0,00 0,63% 25.789 23,76 0,01 0,68%

Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O. Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O. Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O.

Manuseio de Cargas R$ 5.952 5,44 0,00 0,16% 26.677 22,07 0,00 0,67% 10.993 10,13 0,00 0,29%

Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O. Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O. Total Mês R$ / Veíc. Equip. R$ / Km % Repres. /C.D.O.

Total de Manutenção R$ 521.468 476,23 0,08 13,76% 472.588 390,89 0,09 11,83% 503.389 463,79 0,13 13,25%

Manutenção Total Mês Idade Média Quant. Veíc. Ticket Médio Total Mês Idade Média Quant. Veíc. Ticket Médio Total Mês Idade Média Quant. Veíc. Ticket Médio

Total de Manutenção R$ 520.625 17 1.083 480,72 470.586 18 1.209 389,24 458.707 1.057 433,97

Sublocação Diárias R$ / Diária Diárias R$ / Diária Diárias R$ / Diária

Locação (sub-locação) R$ #DIV/0! #DIV/0! #DIV/0!

Ticket Médio Diárias Por Evento

AVARIAS / MULTAS Pagto / Veículo% de Reembolso /

PagamentoPagto / Veículo

% de Reembolso /

PagamentoPagto / Veículo

% de Reembolso /

Pagamento

Pagamento 0,36 1,15% 0,52 1,01% 0,54

Reembolso 0,71 2,23% 1,49 2,93% 2,59

Saldo 0,34 194,19% 0,97 288,79% 2,05 481,63%

Reemb / Veículo % Repres. / Fat. Reemb / Veículo % Repres. / Fat. Reemb / Veículo % Repres. / Fat.

Pagamento 1,71 4,91% 5,21 8,28% 3,05

Reembolso 1,14 3,27% 0,85 1,35% 3,43

Saldo -0,57 66,62% -4,36 16,34% 0,39 112,67%

% de Saldo / Pagamento % de Saldo / Pagamento Saldo / Veículo% de Reembolso /

Pagamento

Pagamento -370,25% -909,35% 3,58

Reembolso -61,34% 42,88% 6,02

Saldo -519,55% -416,07% 2,44 167,96%

Nº Colaboradores H.E. (R$) R$ / Total Colab. % Repres. / F.P. Nº Colaboradores H.E. (R$) R$ / Total Colab. % Repres. / F.P. Nº Colaboradores H.E. (R$) R$ / Total Colab. % Repres. / F.P.

Admisnistrativos da filial 11 0 0 0,00% 10 0 0 0,00% 11 64 6 0,16%

Tráfego 1 0 0 0,00% 1 0 0 0,00% 1 0 0 0,00%

Total 12 0 0 0,00% 11 0 0 0,00% 12 64 6 0,16%

Folha / Colab. Indenizações Folha / Colab. Indenizações Folha / Colab. Indenizações

Folha De Pagamento R$ 3.608 0 3.658 0 3.545 215

3.936.316

84.521

Quant. Média Dias Quant. Média Dias

15 0,5

Quant. Média Dias

151.586

4.398.043

491.125

51.098

0

210.394

33.349

-212.995 -318.403

Avarias + Multas

-68.313 -342.276

177.045

Multas

40.996 76.526

Avarias

3.557.390

146.125

251.659

519.965

223.437

50.200-51.843

309.571-161.152 -368.603

Total MêsTotal Mês Total Mês

66.862 296.528136.365

263.180204.677 409.138

Total MêsTotal Mês Total Mês

117.061

46.392

84.521

40.53543.526

Total MêsTotal Mês Total Mês

2 5,0

11 12

Mai 2012 Jun 2012 Média 2012

Realizado Realizado Realizado

Faturamento Bruto

4.172.424 4.940.266 4.646.686

Realizado Realizado Média Real

Custos e Despesas Operacionais3.788.989 3.993.781 3.800.338

3.460 3.303 3.501

% Repres. / Fat. % Repres. / Fat. % Repres. / Fat.

11,11% 10,89% 11,53%

% Repres. / Fat. % Repres. / Fat. % Repres. / Fat.

4,04% 3,99% 4,49%

% Repres. / Fat. % Repres. / Fat. % Repres. / Fat.

1,91% 1,95% 1,86%

Total MêsTotal Mês Total Mês

0 0 0

Ticket Médio Diárias Por Evento Ticket Médio Diárias Por EventoTotal Evento Total Evento Ticket Médio Diárias Por Evento Total Evento

Total Mês Total Mês Total Mês

1.095 1.209 1.085

Horas Extras e Número De Colaboradores

Total Folha de Pagamento

40.239

Total Folha de Pagamento Total Folha de Pagamento

43.296

#DIV/0!#DIV/0!#DIV/0!

41.209

Monthly operational assessment for each operation

Operations with12 or more months ofRevenue

Other Operations(with less than 12

months ofRevenue)

2,271.0 451.7

333.5 (32.0)

14.7% -7.1%

233.5 (22.4)

1,655.1 838.5

14.1% -2.7%

510.5 43.1

22.5% 9.5%

175.0 (82.0)

7.7% -18.2%

981.1 1,115.4

1.4 9.0

0.81 n.a.

10.70 10.70

13.3 n.a.

6.5 n.a.

20.8% n.a.

Total

3,421.5

502.5

14.7%

351.8

2,493.6

14.1%

769.2

22.5%

233.6

6.8%

2,096.5

2.0

1.08

10.70

9.9

5.7

27.6%

ROIC LTM 06/30/2012(R$ million)

Total

Net Revenue 2,722.7

EBIT 301.6

EBIT Margin 11.1%

(=) Net Operating Profit less Taxes (NOPLAT) - 1

211.1

(=) Invested Capital - 2 2,493.6

ROIC - 1/2 8.5%

Recurring EBITDA 553.6

Recurring EBITDA Margin 20.3%

Recurring Net Profit 95.3

Recurring Net Profit Margin 3.5%

Net Debt 2,096.5

Net Debt/EBITDA-A 2.5

Earnings per Share 0.44

Share Price (09/14/2012) 10.70

P/E 24.3

EV/EBITDA LTM 8.0

ROE 11.3%

Return of operationsReturn of operations

Other Operations(with less than 12

months ofRevenue)

1,150.5

169.0

14.7%

118.3

838.5

14.1%

258.7

22.5%

58.6

5.1%

1,115.4

3.3

0.27

10.70

39.6

13.3

n.a.

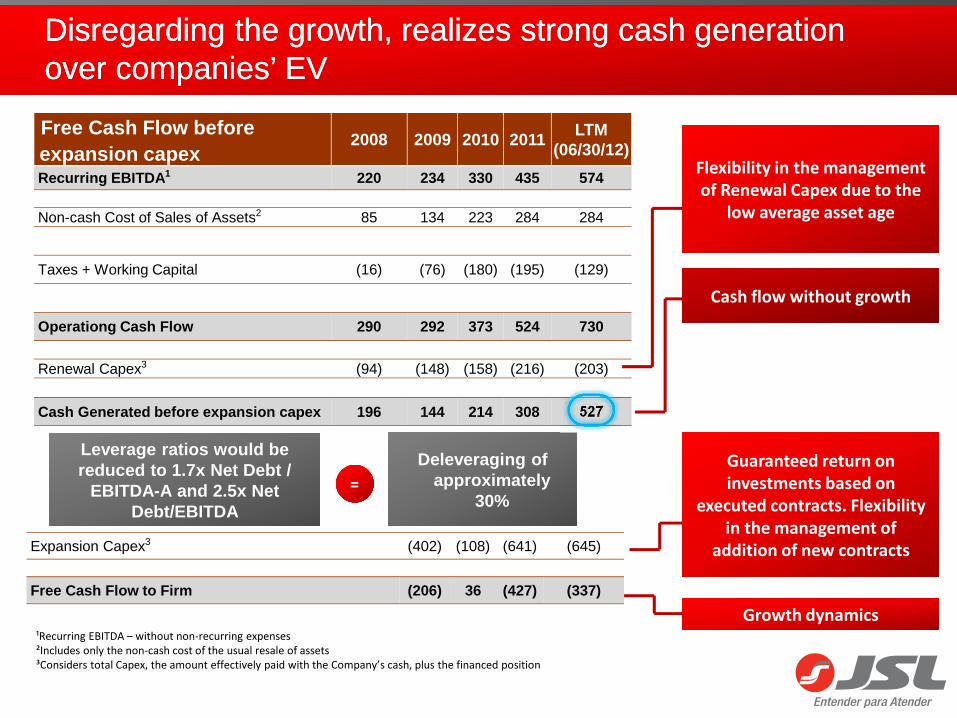

Disregarding the growth, realizes strong cash generationover companies’ EVDisregarding the growth, realizes strong cash generationover companies’ EV

Free Cash Flow beforeexpansion capex

2008 2009 2010 2011LTM

(06/30/12)

Recurring EBITDA 1 220 234 330 435 574

Non-cash Cost of Sales of Assets2 85 134 223 284 284

Taxes + Working Capital (16) (76) (180) (195) (129)

Operationg Cash Flow 290 292 373 524 730

Renewal Capex3 (94) (148) (158) (216) (203)

Cash Generated before expansion capex 196 144 214 308 527

¹Recurring EBITDA – without non-recurring expenses²Includes only the non-cash cost of the usual resale of assets³Considers total Capex, the amount effectively paid with the Company’s cash, plus the financed position

Deleveraging ofapproximately

30%

Cash flow without growthCash flow without growth

Guaranteed return on investments based on

executed contracts. Flexibility in the management of

addition of new contracts

Guaranteed return on investments based on

executed contracts. Flexibility in the management of

addition of new contracts

Flexibility in the management of Renewal Capex due to the

low average asset age

Flexibility in the management of Renewal Capex due to the

low average asset age

Growth dynamicsGrowth dynamics

Leverage ratios would bereduced to 1.7x Net Debt /

EBITDA-A and 2.5x Net Debt/EBITDA

Expansion Capex3 (402) (108) (641) (645)

Free Cash Flow to Firm (206) 36 (427) (337)

==

GROSS DEBT CASH AND INVESTMENTS NET DEBT

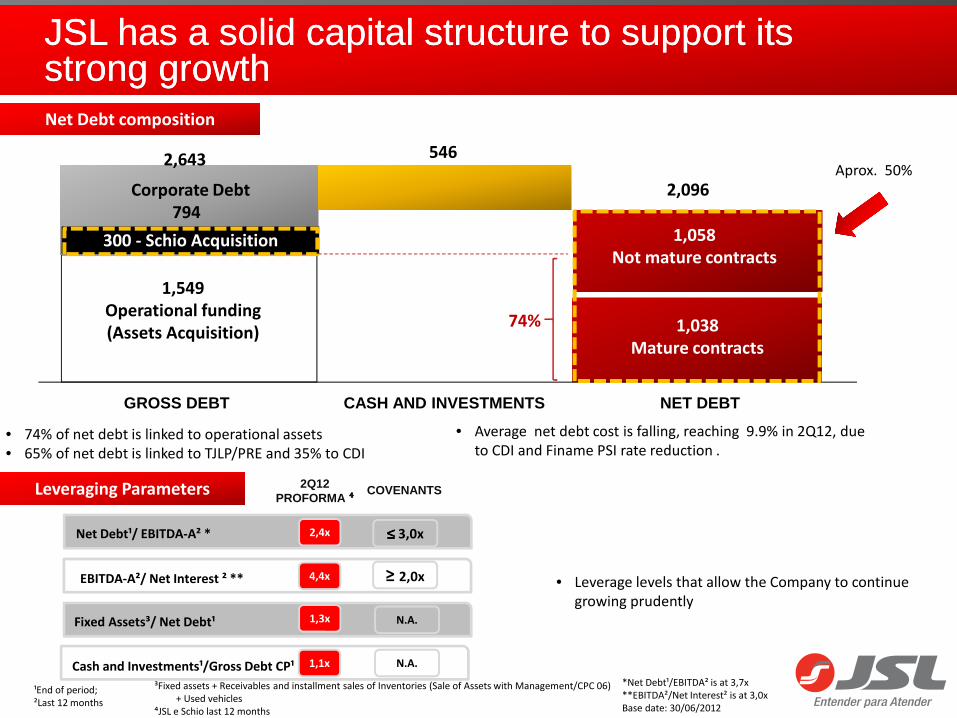

JSL has a solid capital structure to support its strong growthJSL has a solid capital structure to support its strong growth

• 74% of net debt is linked to operational assets• 65% of net debt is linked to TJLP/PRE and 35% to CDI

Net Debt compositionNet Debt composition

• Average net debt cost is falling, reaching 9.9% in 2Q12, due to CDI and Finame PSI rate reduction .

2,096

1,038Mature contracts

1,058Not mature contracts

1,549Operational funding(Assets Acquisition)

Corporate Debt794

5462,643

74%

300 - Schio Acquisition

• Leverage levels that allow the Company to continue growing prudently

¹End of period; ²Last 12 months

³Fixed assets + Receivables and installment sales of Inventories (Sale of Assets with Management/CPC 06) + Used vehicles

⁴JSL e Schio last 12 months

*Net Debt¹/EBITDA² is at 3,7x**EBITDA²/Net Interest² is at 3,0xBase date: 30/06/2012

1,3xFixed Assets³/ Net Debt¹

1,1xCash and Investments¹/Gross Debt CP¹

2,4xNet Debt¹/ EBITDA-A² *

Leveraging ParametersLeveraging Parameters

4,4xEBITDA-A²/ Net Interest ² **

N.A.

N.A.

2Q12PROFORMA ⁴⁴⁴⁴

COVENANTS

≥ 2,0x

≤≤≤≤ 3,0x

Aprox. 50%

Moreover, JSL has flexibility in managing CAPEX dueto low average age of fleet

• Linked to new contracts

• Low average age of fleet• Flexibility to manage the time of renewal

without harming maintenance

• 2.1 years is the current average age of the total fleet

Fleet Evolution (thousands)Fleet Evolution (thousands)

CAPEX Forecast 2012 (R$ million) 1S12R 2012E

Net Renewal CAPEX (23) 60

Gross renewal CAPEX 116 420

Revenue with resale of assets (139) (360)

Expansion CAPEX 289 590

Commited - 2011 new contracts 102 130

New contracts signed in 2012 and to be

captured 187 460

Others (IT, improvements, etc) 29 60

Net CAPEX 295 710

JSL's initiatives in sustainability projects in the logistics chain

JSL's initiatives in sustainability projects in the logistics chain

Irecê A. RodriguesIrecê A. Rodrigues

InstituteInstitute

Julio Simões Institute

Mission

Vision

The Julio Simões Institute was created in 2006 to organize and plan the execution of JSL’s social initiatives, allocating resources proportionally to its operational locations.

To promote initiatives and share expertise that IMPROVES ROAD TRANSPORTATION SAFETY and that QUALIFIES HUMAN CAPITAL in the logistics sector.

To become a BENCHMARK for good of professional ROAD TRANSPORTATION SAFETY and SUSTAINABLE DEVELOPMENT practices .

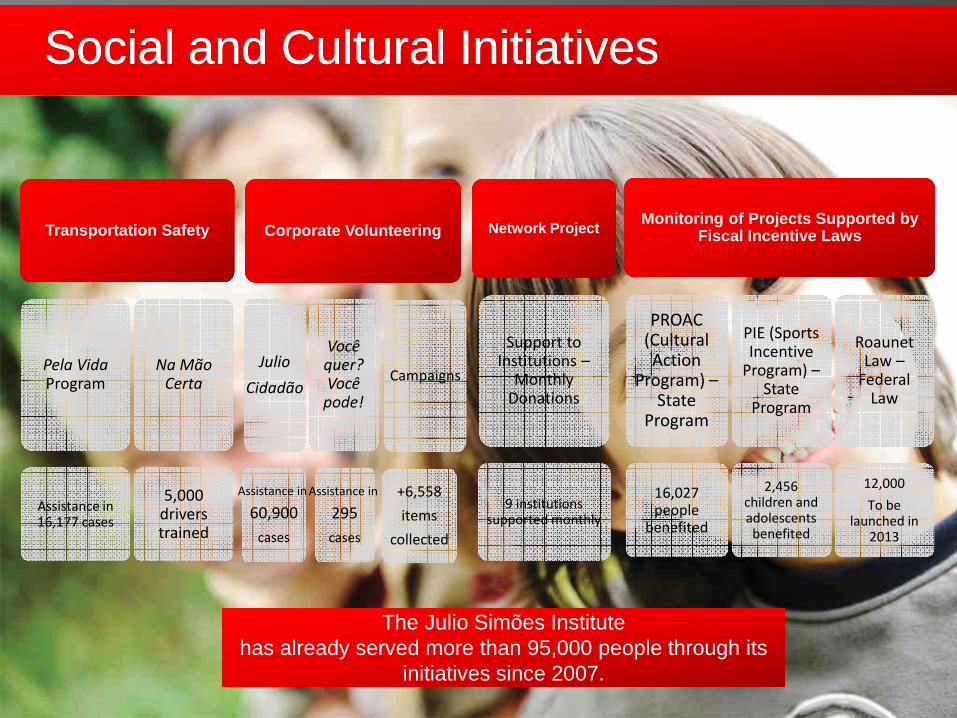

Social and Cultural InitiativesSocial and Cultural Initiatives

Transportation Safety

Pela Vida Program

Assistance in 16,177 cases

Na MãoCerta

5,000 drivers trained

Network Project

Support to Institutions –

Monthly Donations

9 institutions supported monthly

Monitoring of Projects Supported by Fiscal Incentive Laws

PROAC (Cultural Action

Program) –State

Program

16,027 people

benefited

PIE (Sports Incentive

Program) –State

Program

2,456 children and adolescents benefited

Roaunet Law –

Federal Law

12,000

To be launched in

2013

The Julio Simões Institutehas already served more than 95,000 people through its

initiatives since 2007.

The Julio Simões Institutehas already served more than 95,000 people through its

initiatives since 2007.

Corporate Volunteering

Julio

Cidadão

Assistance in

60,900

cases

Campaigns

+6,558

items

collected

Vocêquer?Vocêpode!

Assistance in

295

cases

CoverageCoverage

PA

MS

PR

SC

RS

AP

MA

PI

CE

PE

ALSEBA

TO

GO

DF

MG

RJ

ES

SP

RR

MT

AM

AC

RO

Pela Vida (For Life)

Monthly Donations -Social

Monthly Donations –Environmental

Campaigns

Projects Supported by Tax Incentive Laws

ActionsActions

Desenvolvimento de Novos Projetos / NegóciosDesenvolvimento de Novos Projetos / Negócios

Fábio VellosoFábio Velloso

Development of New Projects / BusinessesDevelopment of New Projects / Businesses

Development of New Projects / BusinessesDevelopment of New Projects / Businesses

To develop new projects and businesses in areas / scopes still unexplored by JSL

• Recycling of materials

• Industrial center

• Logistics center

• 4PL projects

• Highway projects

• Port and retroport projects

• Railway projects

• Projects in the pharmaceutical segment

• Projects in the gas distribution segment

• Projects in the energy segment

• Recycling of materials

• Industrial center

• Logistics center

• 4PL projects

• Highway projects

• Port and retroport projects

• Railway projects

• Projects in the pharmaceutical segment

• Projects in the gas distribution segment

• Projects in the energy segment

Projects under development

Projects under development

Example: Energy Segment (Current Scenario)Example: Energy Segment (Current Scenario)

58

FINAL DESTINATION

Work

Work

Work

Small Distribution Centers

SUPPLIERS

Work

Garage

DISTRIBUTION CENTERS

Example: Energy Segment (Proposed Scenario)Example: Energy Segment (Proposed Scenario)

SUPPLIERS

LOGISTICS CENTER

CONSOLIDATION CENTERS

FINAL DESTINATION

Work

Work

Work

Small Distribution Centers

Work

CONSOLIDATION CENTERS

Example: Pharmaceutical SegmentExample: Pharmaceutical Segment

PHARMACEUTICAL INDUSTRY

HOSPITALS

DISTRIBUTORS

LARGE PHARMACEUTICAL

CHAINS

PHARMACIES

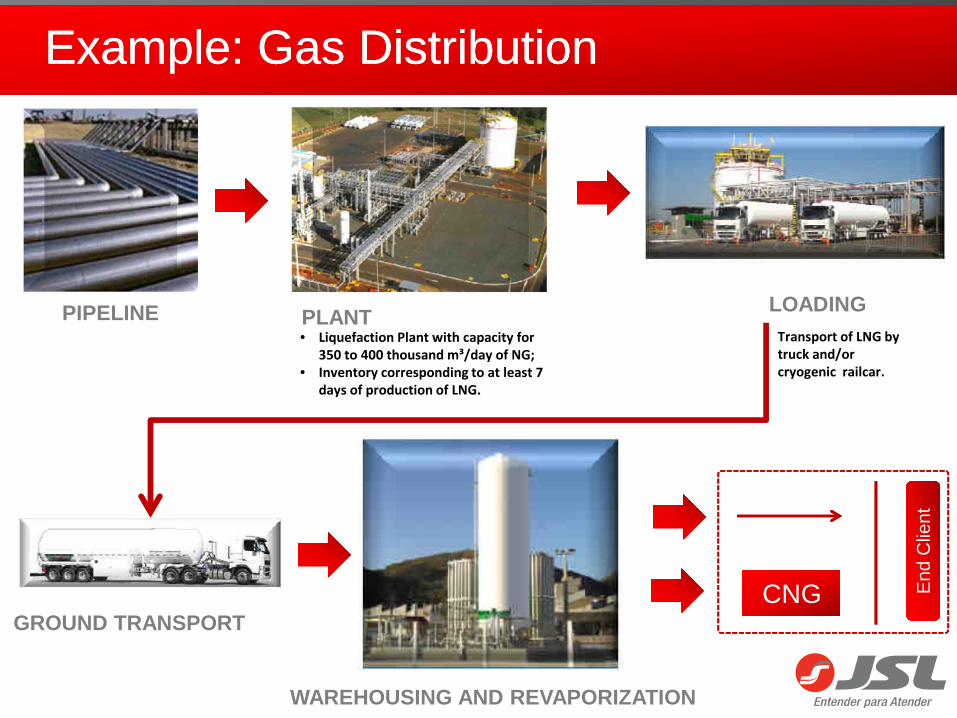

Example: Gas DistributionExample: Gas Distribution

PLANTLOADING

GROUND TRANSPORT

WAREHOUSING AND REVAPORIZATION

End

Clie

ntE

nd C

lient

PIPELINE• Liquefaction Plant with capacity for

350 to 400 thousand m³/day of NG;• Inventory corresponding to at least 7

days of production of LNG.

Transport of LNG by truck and/or cryogenic railcar.

CNGCNG

Example: Logistics CenterExample: Logistics Center

Dry warehouse/with temperature

control

Outdoor warehousing

Located at the exit to key highways

Close to ports

Truck center

Close to the railway

Strategies and ActionsStrategies and Actions

Fernando Antonio SimõesFernando Antonio Simões

Corporate GovernanceCorporate Governance

5 members,2 of which are independent member

3 members, 1 of which is independent member

Board of DirectorsBoard of Directors

Financial and Procurement

Committe

Financial and Procurement

Committe

Fiscal CouncilFiscal

Council

External Audit

External Audit

216,799,134 common sharesShareholders

• Novo Mercado

• Financial and Procurement Committee

• PricewaterhouseCoopers

• Code of Ethics

• Incorporation of dealerships

• 40% of board of directors is independent

• Guidance delivery

• Novo Mercado

• Financial and Procurement Committee

• PricewaterhouseCoopers

• Code of Ethics

• Incorporation of dealerships

• 40% of board of directors is independent

• Guidance delivery

Corporate Governance

Best Practices

Corporate Governance

Best Practices

Management Structure

ManagementManagementTreasury Shares

Treasury Shares

Fernando Antônio Simões

Fernando Antônio Simões

Other members of Simões

family

Other members of Simões

family

7% 13% 53% 25% 1% 1%

CEOCEO

Bloco de controle

Guidance Realized %

2010 300 330 110.0%

2011 400 435 108.8%

Guidance Realized %

2010 300 330 110.0%

2011 400 435 108.8%

226.0 333.0 427.0 499.0 593.0 727.0 1,027.7

1,478.0 1,477.8

2,028.5

2,739.7

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Organic Acquisitions

Growth JSL x PIBGrowth JSL x PIB

Proven historical growth

Elasticity x GDP

Source: Company

Net Revenues(R$ million)

*Proforma

05% 05%00%

08%03% 03%

36% 36%

08%

25%

19%

41%

2007 2008 2009 2010 2011 Reported FY11 JSL + Schio

GDP Gross Revenue from Services

6.2 x

6.6x 7.1x

3,900.0x

6.9 x

CAGR PIB 07-11: +4.8%

CAGR JSL 07-11: +29.7%

15.3 x

3.3x

History of the SectorHistory of the Sector

Many companies have gone out of business or shrunk, due to lack of strategic planning and management, succession plan and resilience in the business.

Many companies have gone out of business or shrunk, due to lack of strategic planning and management, succession plan and resilience in the business.

1.TNT

2.Dom Vital

3.Transbraçal

4.Itapemirim

5.Tresmaiense

6. Liderbrás

7. SEG

8. Tropical

9. Itaipava

10. Atlas

29th

1990

1.TNT

2.Tresmaiense

3.ITD

4.Dom Vital

5.Atlas

6. Transwilson

7. Cometa

8. Liderabras

9. Mercurio

10. Tora

25th

1.Prossegur

2.Cometa

3.Translor

4.Dom Vital

5.Itapemirim

6. ITD

7. Mercurio

8. Tora

10. Liderbras

9o

1996

1.Mercurio

3. Kwikasair

4. Itapemirim

5. Atlas

6. Tora

7. Cesa

8. Binotto

9. Atlas

10. Araçatuba

9th

2. Mercurio

3. Binotto

4. Cometa

5. Atlas

6. Kwikasair

7. Ramos

8. Ouro Verde

9. Cesa

10. Bertolini

2nd

2000 2011

1st JSL

1994 2002

JSL

JSL

JSL

Source: The Largest and Best Cargo Transportation Companies - Transporte Moderno Magazine

JSL

2. Mercurio

3. Prossegur

4. Cometa

5. Protege

6. Binotto

7. Atlas

8. Ramos

9. Itapemirim

10. Ouro

Verde

2. Mercurio

3. Tegma

4. Cometa

5. Sada

6. Cooper.SC

7. Ramos

8. Binotto

9. Atlas

10. Expresso

Araçatuba

2. Tegma

3. Sada

4. Cometa

5. Braspress

6. Ramos

7. Ouro Verde

8. Atlas

9. Schio

10. Cooper-

Carga

1st

2005 2008Ranking by net revenue in the road cargo transporta tion sector

New ContractsNew Contracts

Note: Although each contract is adjusted according to the inflation of its specific cost structure, to estimate the base of 2012and 2013 we used the IGP-M index (Source: Bacen).

2,267

696

2011R 2012E

115

2013E

1883,406

2,246

3,206

+34.9%

+11.4%

3,057

2,267

Contracts negotiated in 2012

ConsolidatedDedicated Services +

Passengers

HEAVYManagement

and outsourcing

LIGHTManagement

and outsourcing

Global Revenue (R$ thousand)

1,263.2 997.1 229.3 36.8

Term (months) 60 61 60 24

EBTIDA Margin 33.0% 23.1% 76.7% 51.2%

IRR 16.8% 17.7% 15.3% 18.3%

Residual Value 48.0% 47.0% 46.0% 80.0%

Gross Revenue from Services

Criteria for AcquisitionCriteria for Acquisition

Some points analyzed

• Entry in segments in which JSL does not have a strong presence

• Penetration in unique markets with an accelerated growth curve

• To penetrate into profitable and protected segments with entry barriers

• To operate in the sector through a more efficient business model

• Generate value via economy of scale

• Operational synergies

• To enable growth in a structured and systematic manner, with value generation that is sustainable in the long term

Current MarketCurrent Market

Brazil´s GDP100% = R$ 2.9 tri

Logistical Expenses100% = R$ 576 bi

Others94%

LSP6%

Source: World Bank - 2008

5.4%

16.5%24.5%

37.4%46.9%

58.3%

Brasil Alemanha França Espanha ReinoUnido

Holanda

% of total fleet

Source: DataMonitor, Unidas

Low penetration level

1 vehicle48%

2 to 5 vehicles

36%

6 to 15 vehicles

11%

More than16 vehicles

5%

Fleet Management and Outsourcing

Size of the companies’ fleet

Average age of Brazil’s truck fleet: 17.6 years

Average age of Brazil’s truck fleet: 17.6 years

Total of 206 thousand highway transportation companies

Germany France Spain England NetherlandsBrazil

Brazil’s Logistics MarketBrazil’s Logistics Market

• Companies with revenue of up to R$500.0 million

• Family management

• Some have made mistakes

• Disproportional liabilities

• Clients responsible for civil, labor and tax liabilities

• Competitive market (need for innovation)

• Solutions without integration

JSL’s PositionJSL’s Position

• Corporate Governance

• Credibility

• Committed and integrated staff

• Succession

• Differentiated board of directors

• Corporate Governance

• Credibility

• Committed and integrated staff

• Succession

• Differentiated board of directors

• Brazil’s largest service portfolio

• Cross-selling ability

• Resilience in business

• Flexibility in CAPEX management

• Diversified operations

• Penetration in sale of assets

• Geographic presence

• Scale

• Entry barriers

• Administrative/operational structure

• Brazil’s largest service portfolio

• Cross-selling ability

• Resilience in business

• Flexibility in CAPEX management

• Diversified operations

• Penetration in sale of assets

• Geographic presence

• Scale

• Entry barriers

• Administrative/operational structure

Solid Competitive Advantages

Solid Competitive Advantages

Sustainable GrowthSustainable Growth

THANK YOU