Application of Activity Based Costing in a Textile Company ... · 2.1 Absorption Costing Absorption...

24

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 602 MARCH 2013 VOL 4, NO 11 Application of Activity Based Costing in a Textile Company of Pakistan-A Case study Danish Iqbal Godil Department of Management Sciences Bahria University – (Karachi Campus) Dr.Syed Shabib- ul- Hasan Department of Public Administration University of Karachi Yousuf Abid Head of Department - Management Sciences Bahria University – (Karachi Campus) Abstract Recent changes in technologies have resulted in development of manufacturing processes that have made traditional costing systems useless. This research examines the implementation of ABC in AVL Textile Company and evaluates the contribution of newly implemented system in problem solving, related to allocation of overhead cost. This was a case study based research and the authors have tried to find out the difference in product cost resulting from the change of method i.e. from conventional to ABC. The outcomes showed significant differences in cost of five products selected for this study. However in spite of the fact that ABC is a better approach than conventional costing, management had encountered numerous problems with its practical implementation. Keyterms: Activity Bases costing, Conventional Costing, Textile Company.

-

Upload

truongdung -

Category

Documents

-

view

227 -

download

1

Transcript of Application of Activity Based Costing in a Textile Company ... · 2.1 Absorption Costing Absorption...

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 602

MARCH 2013

VOL 4, NO 11

Application of Activity Based Costing in a Textile Company of

Pakistan-A Case study

Danish Iqbal Godil

Department of Management Sciences

Bahria University – (Karachi Campus)

Dr.Syed Shabib- ul- Hasan

Department of Public Administration

University of Karachi

Yousuf Abid

Head of Department - Management Sciences

Bahria University – (Karachi Campus)

Abstract

Recent changes in technologies have resulted in development of manufacturing processes that

have made traditional costing systems useless. This research examines the implementation of

ABC in AVL Textile Company and evaluates the contribution of newly implemented system in

problem solving, related to allocation of overhead cost. This was a case study based research

and the authors have tried to find out the difference in product cost resulting from the change of

method i.e. from conventional to ABC. The outcomes showed significant differences in cost of

five products selected for this study. However in spite of the fact that ABC is a better approach

than conventional costing, management had encountered numerous problems with its practical

implementation.

Keyterms: Activity Bases costing, Conventional Costing, Textile Company.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 603

MARCH 2013

VOL 4, NO 11

1. Introduction

Firms are not gaining what they could gain from cost system. They are still with the frame of

mind for local competition rather than the global competition. The reason behind is that they rely

on less technological and simpler designed cost systems. These systems cannot help managers to

move towards the betterment of their activities and they do not have actual data to implement

their planned decisions about customers, services, products and processes.

Technological innovation and global competition have changed the business environment a lot.

This change forces the organizations to use the innovative tools for the financial and non

financial information of the organizations. The new change in the business environment demands

the organizations to gather the relevant data and information about the customers, costs,

procedures, services, products and activities. ABC is perceived as the most accurate costing

system by some of practitioners and academics. Even in the text books of accounting it is

demonstrated as much more superior over traditional based costing.

Most of the firms in the textile sector of Pakistan are using conventional costing system.

According to their research only 12% of the companies were following ABC system where as

88% were using other costing methods. As a result, their product cost and behaviour was not

appropriately identified due to which most of the companies were costing their products on

comparative or market basis. (Danish Iqbal , Dr.Shabib)

1.1 Background of the Company.

AVL Textile Company (Original name omitted) is in operation for almost 60 years i.e. since

1952. The trend of the company showed moderate growth during this period. Textile suiting is

the main product of the company. Company is dealing in more than 25 types of worsted fabrics.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 604

MARCH 2013

VOL 4, NO 11

Company has more than 521 employees that include both hourly (21.11%) and permanent

(78.89%) employees. Employees are working in three shifts.

Primarily AVL Textile Company was not following any appropriate costing system and products

were not accordingly charged with overheads, due to which cost of products were distorted.

Management has realized the fact and has decided to switch to other superior costing method i.e.

ABC.

This paper shows the adoption of activity based costing in an AVL Textile Company. In this

research the authors have tried to find out the difference in product cost resulting from the

change of method i.e. from conventional to ABC. Evaluation of both the methods was carried out

by analyzing the management accounts of company and by personal interviews with costing and

finance employees.

2. Literature Review

Companies usually focus their attention towards their revenue growth without understanding that

the business is generating profitable growth or not. Many companies have fallen victim by

adopting this practice. Companies give exclusive incentives to their sales force on revenue

generating goals without recognizing that whether those deals are profitable or not. Now the

companies, which can think forward, started realizing that not every customer is a profitable for

them. Customers, who frequently buy products and return them back, give companies a burden

of high cost to serve.

Still, the firms are not gaining what they could gain from cost system. They are still with the

frame of mind for local competition rather than the global competition. The reason behind is that

they rely on less technological and simpler designed cost systems. These systems cannot help

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 605

MARCH 2013

VOL 4, NO 11

managers to move towards the betterment of their activities, and they do not have actual data to

implement their planned decisions about customers, services, products and processes.

Technological innovation and global competition have changed the business environment a lot.

This change forces the organizations to use the innovative tools for the financial and non

financial information of the organizations. The new change in the business environment demands

the organizations to gather the relevant data and information about the customers, costs,

procedures, services, products and activities. Firms typically use their cost system to (Kaplan &

Cooper).

Design product mix and investment decision;

Help employees to learn and improve their activities;

Create such goods and services both of which meet the hope of the customers and the

end result would be profit;

Negotiate about quality, product, features, price, service and delivery with customer;

Proficient and useful processes (distribution and service) to customer segment and target

markets (Cardos, I.R, Pete, S).

2.1 Absorption Costing

Absorption costing can also be called full costing. This method involves expensing out of all cost

related to the manufacturing of specific product. This method uses overhead costs and total direct

costs involved in the product manufacturing, as the cost base. The traditional cost allocation

system is based on 3 steps.

Accumulating costs of both manufacturing and service departments

Cost of service departments is allocated to manufacturing departments.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 606

MARCH 2013

VOL 4, NO 11

Allocating the revised manufacturing cost to different customers, products and services.

This costing system is considered as good tactical choice by some firms. It can be beneficial for

the firms if the main cost of the services and products is direct cost and activities that support the

production of the goods or service at lower cost, are at standardized product lines. For any

professional service firm (accounting or law) labour cost is the largest cost, so they do not need

ABC. ABC approach is more often preferred by the firms other than these because if they go for

volume based costing there might be chances of inaccuracies. Some of the products are over cost

while some are under cost, because activity usage is not proportionate to the output volume.

Before adopting any cost system, the firm needs to understand the relationship among activities,

resources and services or products. Some of the resources used in the operations can me marked

out to individual services or products and classified as direct labour costs or direct material.

Merits of Absorption Costing

Absorption costing recognizes the role of fixed cost in the manufacturing process and this

system is always used to prepare financial reports. In case of constant production, this system

shows less variation in profits.

Limitations of Absorption Costing

We can see the limitations of absorption costing with the help of an example shown in

table I. It reveals that how much cost is being spent on what department but it does not give any

idea that why these expenses are being incurred and how to control these expenses? This method

is used to present financial reports and in those reports we can only compare the increase or

decrease in cost of each department but cannot understand the reason behind the change in value.

The departments that exist in a firm perform their specific functions to serve the internal and

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 607

MARCH 2013

VOL 4, NO 11

external customers. Understanding the activities and the task is the key step for any firm to know

the real serving cost of its customers.

Under this method the derived cost is much distorted, and it negatively affects the decision

making. Some of the products and services are charged for the cost which never incurred on

them.

2.2 Activity Based Costing

ABC system was first originated in USA after taking years of researches. In managerial

accounting, it is regarded as the most innovative cost calculation system. Earlier traditional cost

system was used in the organizations which provide quite distorted cost calculations. This

drawback of traditional cost system was first discussed by Peter Drucker in 1963.

ABC and (ABM) Activity Based Management systems are designed for managers to gather the

actual and correct information of the price of each source that is required by the each customer,

service and product. It may lead to better cost control. With a number of activities identified,

instead of a single overhead cost pool, it is easier to see where cost improvements are needed.

With these sorts of utilities, these systems are very helpful for managers to understand the clear

view of operations before making any decision.

ABC system first collects overhead costs of all the activities of the entire organization and then

allocates the cost of those activities to the services, products and customers that are involved in

that activity. The process that identifies the appropriate cost drivers and their effect on the cost of

giving service or making product is known as activity analysis. Many people consider this

activity analysis as the most critical aspect of ABC system. This system assigns the cost of

overhead s to cost objects recognizing the activities and resources along with their amounts and

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 608

MARCH 2013

VOL 4, NO 11

costs required for the output. After that the firm allocates the cost of activity to services or

products by multiplying each activity’s cost by the amount consumed by that activity. ABC

system does not have many limitations while traditional cost systems have many limitations that

can disfigure the cost of product. Distortion occurs when there is a high degree of product

diversity or high overhead ratio.

The methodology of ABC has the following assumptions:

organization resources are consumed by the activities included in business processes,

rather than products, or organizational units;

activities included in business processes are performed in order to produce goods or

provide services;

Substantial proportion of indirect costs does not depend on the volume of products, but

varies with the intensity of their activities.

Following steps shall be followed in the development of activity based costing:

Identification of relevant activities within the company

According to the philosophy of the ABC method it is not a product that is responsible for the

formation of the costs, but certain actions are. Therefore, one should specify a list of actions that

will make up the appropriate processes.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 609

MARCH 2013

VOL 4, NO 11

Determining the cost of operations (so-called cost pool)

Each activity extracted in the previous step must be measured and shall be attributed to the right

direction as close as possible to actual value. Cost pool can be defined as a grouping of

individual costs, the sum of which is allocated by means of one allocation base.

Identifying cost carriers (so-called cost drivers)

Cost drivers are cost carriers i.e. reasons behind cost. Cost of resources consumed and cost

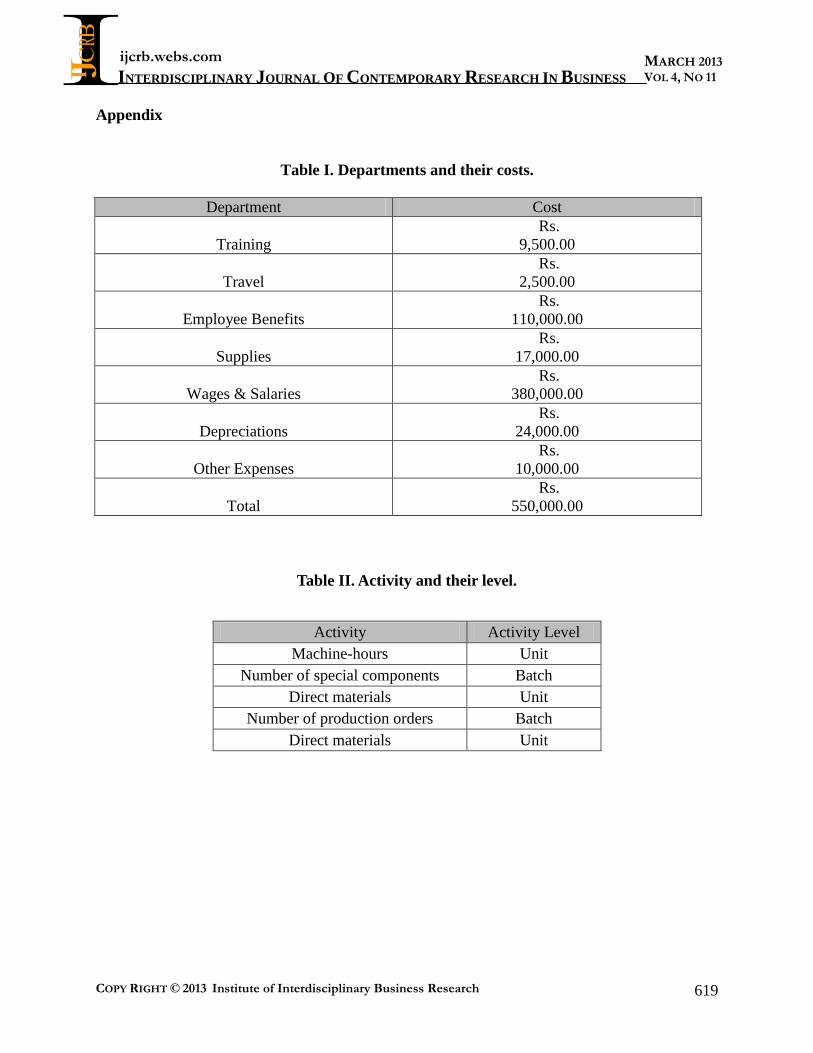

drivers have direct causality. Cost drivers can be of unit, product, batch and facility level.

Direct tracing and estimation are the ways that can assign the cost of resources to activities. If

direct tracing is not available then the managers and the supervisors of the department estimate

the effort or amount of time spent by the employees on their respective activities. Table II shows

the activity and their level whereas Table III shows resources along with their cost drivers.

Accounting for the costs of product.

In the last step the extents to which the product or service to be charged according to specific

activities should be to determined and charged accordingly.

Activity Based Costing- A critical review

ABC is perceived as the most accurate costing system by some of the practitioners and

academics. Even in the text books of accounting it is demonstrated as much more superior over

traditional based costing. However, ABC is the refined version of traditional based costing

system, so it also suffers some of the weaknesses of absorption based system. ABC is based on

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 610

MARCH 2013

VOL 4, NO 11

subjective uninformed cost allocations. The major difference between ABC and traditional based

system is the number of allocation bases.

Absorption costing requires allocation criteria, volume assumptions and subjective selection of

absorption criteria. ABC costing system is more complicated and essentially not an accurate or

useful one. ABC cannot predict profits, if the production volume changes. In practice it is used to

develop the “full cost” of a product which includes fixed cost. So, it is not conducive to good

decision-making.

ABC overlooks controls and does not distinguish a blockage from resources with surplus

capacity. If there is an internal capacity constraint in a firm means the production capacity is

lower than the demand for its products, the company should establish the best product mix as per

each product’s per unit contribution of limited resource.

ABC views the link between resource consumption and activities as absolute, linear and definite.

Any addition in activities increases the cost and any reduction in activities decreases the cost.

However, in actual there are discontinuities of costs. Developing 10 cost pools and assigning

costs from them is costly than a single pool.

Allocation of all kind is random and the use of both traditional cost accounting and ABC may

lead towards a false decision making process. The initial enthusiasm gained by the ABC is due to

the disappointing feeling with the traditional cost accounting and the lack of better alternatives.

The interest in the method declined when the weaknesses of ABC system are experienced by the

firms. Most of firms that initially adopted ABC ultimately abandoned it; they did it by judging

with many case studies and the published literature. It seems that the advantage to the firms is

not from the cost allocation system but from the fact that the ABC system involved in depth

analysis of costs and processes and noticed to ignore features of organizational activities. ABC

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 611

MARCH 2013

VOL 4, NO 11

actually emphasized the requirement to focus and to cut down the cost of complexity of

operations (Ronen, B and Geri, N, 2005)

3. Research Methodology

The author has selected 5 products for initial analysis i.e. Product A ,B ,C,D and E. Currently

AVL Textile Company is following ABC system, so first product cost under conventional

costing was calculated for comparing it with product cost under ABC.

3.1 Traditional Costing System of AVL Textile Company Ltd.

Step 1. Identification of direct expenses.

Direct expenses are those expenses which are charged directly to the manufactured goods

according to their actual utilization .Wool, polyester, dyes and chemical are main sources of

direct material in AVL textile where as direct expenses also include direct labour.

For the sake of understanding cost of direct material of product A is shown in Table IV whereas

summary of cost of material of all products is shown in Table V.

Step 2. Identification of manufacturing overheads and their bases of allocation on cost

objects.

Object that requires distinct cost measurement are called cost objects (Raffish and Turney,

1991). Here we have 5 cost objects i.e. 5 products.

Total production overhead of the AVL Textile Company per quarter was Rs.36, 896,077. A total

meter produced was used as an allocation base as it links all production overheads to products.

Step 3. Computation of rate per meter

Rate per meter is computed as follows.

Total production overhead costs / Total meters

Rs.36, 896,077 / 664,540 meters = Rs.55.521 per meter

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 612

MARCH 2013

VOL 4, NO 11

Step 4. Charging rate per meter to products.

Last step was to charge this rate per meter to cost objects i.e. products.

Table VI shows the total cost of selected products at AVL Company under Traditional Costing

System.

3.2 Activity Bases costing system.

Evaluation of ABC was carried out as under.

3.2.1 Allocating Service Department Costs

First of all service department cost has been allocated to production department. According to

direct method, cost of each service department is directly allocated to the production departments

and not to any other service providing departments. This method ignores any reciprocity of

services between service departments. AVL textile has adopted the same approach and has

allocated the cost of service department to production departments as per Table VII.

Step 1. Identifying products of evaluation

First step is to identify the product for evaluation. The author has identified 5 products for

evaluation of ABC i.e. Product A, B, C, D and E.

Step 2. Evaluating the key activities of the Company

Company’s activities are divided into direct and indirect. Here direct activities means direct

material i.e. cost of polyester, wool, chemical and dyes used) where direct labour means cost of

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 613

MARCH 2013

VOL 4, NO 11

labour hours utilized. Indirect activities are electricity, depreciation, gas and stores & spares.

Product cost includes 80% of direct cost. Product recipe is shown in Table VIII where as

following formulae were used to calculate the cost of material.

Wool Tops = RWo x Wo% x To

Whereas:-

RWo = Rate of Wool

Wo% = Percentage of Wool

To = Tops per meter

Polyester Tops = RPo x Po% x To

Whereas:-

RPo. = Rate of Polyester

Po% = % of Polyester.

To = Tops per meter

Step 3. Evaluation of major overheads within the company.

After evaluating the key activities the next step is to evaluate the major overheads taking place

within an organization. According to the philosophy of the ABC method it is not a product that is

responsible for the formation of the costs, but certain actions are Table IX shows major

overheads taking place in AVL Textile.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 614

MARCH 2013

VOL 4, NO 11

Step 4.Evaluating cost carriers (so-called cost drivers)

Cost drivers are cost carriers i.e. reasons behind cost. Cost of resources consumed and cost

drivers have direct causality. Table X shows the cost drivers of AVL Textile.

Step 5. Evaluating the calculation of cost/meter

Cost/meter of each manufacturing department was computed as per following formulae and was

allocated to products accordingly.

Dyeing = CDY X To

Spinning = CSP X ACnm X ACy

STnm

STTPI

Weaving = CWE X LPI

STPI

Mending =

CME

Finishing =

CFI + CFCI

CDY

Cost per meter of Dyeing Department.

To

Tops per meter

CSP

Cost per meter of Spinning Dept

STnm

Standard Count N.M

ATnm

Actual Count N.M

STTPI

Standard Twist per inch.

ACy

Actual Yarn per meter

CWE

Cost per meter in Weaving Department

LPI

Pics (Local)

STPI

Pics (Standard)

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 615

MARCH 2013

VOL 4, NO 11

CFI

Cost per meter in Finishing Dept

CFCI

Cost per meter in Finished Cloth Inspection Department

CME

Cost meter in Mending Dept.

Step 6. Accounting for the costs of product.

Cost of product (Material and Manufacturing Overhead) as mentioned in Table XI was computed

and evaluated. Summary of Product cost (ABC System) is shown in Table XII.

4. Findings

Costing system of AVL Textile was evaluated which shows significant difference in product cost

under ABC and Traditional costing system. It is clear from the figures of cost results shown in

Table XIII that the cost under Traditional costing is lower than ABC, and the difference is quite

significant. Cost of Product A is lower by Rs.30.29/- per meter, Product B by Rs.18.87/- per

meter, Product C by Rs.26.77/-per meter, Product D by Rs. 40.49/- per meter and Product E by

Rs. 21.76/- per meter.

5. Summary and Conclusions

ABC system was successfully implemented in AVL Textile Company and the authors have

thoroughly evaluated the system which showed that the goods of AVL Textile do not consume

manufacturing overhead on unit basis as represented by traditional costing. This was done

through the assessment of both costing systems i.e. ABC and Traditional system.

ABC system contains two valuable insights. First, all those activities which are performed by

many resources are not demanded in percentage to the total number of units sold or produced.

Diversity and complexity of the customer and product mix creates the demand. Second, ABC

cannot be presented as models of how spending and expenses fluctuate in the short run. These

systems assess the resource costs used to perform activities for different outputs. The production

of products, services, sales, marketing and delivery to customers create demand for the firm’s

activities. The magnitude of each supplied activity to yield is calculated by the cost drivers of

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 616

MARCH 2013

VOL 4, NO 11

activity such as, no. of purchase orders processed, no. of the machine and direct labour hours, no.

of receipts, number of setup hours and number of parts maintained. The ABC model estimates

the resource costs by summing across the costs of all resources provided to execute activities for

individual outputs (Kaplan, R.S and Cooper, R).

If the quantity on hand from existing resource supply is lesser than the activity usage, then there

are more chances of higher spending to increase the supply of resources. If the available supply

is higher than the activity usage, expenses or the spending of resources will not decrease

automatically. If the management wants to achieve higher profits, it must take serious actions

either to reduce spending on resources by reducing the unused capacity or to use the available

capacity to provide assistance for achieving higher business volume by increasing revenues.

Profits and costs are fixed if management does not take any action and leaves the unused

capacity uninterrupted.

6. Problems encountered

It was identified that full-time availability of main employees (which was almost

impossible) was a pre-requisite to successful implementation.

Resistance from some employees was also seen during the implementation.

After identifying the correct cost sales person were not ready to sell the products at given

prices.

Difficulties in the use of the ABC method were found to be associated with a proper

selection of key accounting personals and continuous updating of the model (large time-

consuming process).

7. Recommendation

Employing professionals in the field of accounting will be helpful for those organizations that are

trying to implement activity based costing system in future. AVL Textile Company can further

improve the costing system by

Installing separate utility meters (gas and electricity) in each department.

Repairs expenses shall not be taken as fixed expense.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 617

MARCH 2013

VOL 4, NO 11

Repairs expenses shall be charged on actual basis.

Labour time shall be recorded more appropriately i.e. with the introduction of labour time

ticket system.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 618

MARCH 2013

VOL 4, NO 11

References

Cardos, I.R and Pete.S (N.D), Activity-based Costing (ABC) and Activity based Management

(ABM) Implementation – Is This the Solution for Organizations to Gain Profitability? pp

154-166, viewed on March 01, 2013, retrieved from http://www.revecon.ro/articles/2011-

1/2011-1-9.pdf

Danish Iqbal Godil, Dr.Syed Shabib- ul- Hassan (2013), “Assessment of Current and Future

prospects of Activity Based Costing in the Textile Sector of Pakistan.” Interdisciplinary

Journal of Contemporary Research In Business, ISSN 2073-7122, IJCRB February

Edition 2013–IJCRB Vol .4, No. 10.

Kaplan,R.S and Cooper, R (1992) Activity-Based Systems: Measuring the Costs of Resource

Usage pp 8-14 retrieved from http://host.uniroma3.it/BB26B506-C866-4766-BAA9-

3D326E522C48/FinalDownload/DownloadId

9DE1F899AE8D5FB30EA012CC6C1D64EA/BB26B506-C866-4766-BAA9-

3D326E522C48/facolta/economia/db/materiali/insegnamenti/588_3929.pdf

Raffish, N and Turney, P (1991). “Glossary of Activity-Based Management”, Cost

Management Journal, Fall, 53-63.

Ronen, B and Geri, N (2005) Relevance lost: the rise and fall of activity-based costing pp 133-

136, viewed on March 01 2013, retrieved form

http://www.boazronen.org/PDF/Relevance%20Lost%20-

%20The%20Rise%20and%20Fall%20of%20Activity%20Based%20Costing.pdf

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 619

MARCH 2013

VOL 4, NO 11

Appendix

Table I. Departments and their costs.

Department Cost

Training

Rs.

9,500.00

Travel

Rs.

2,500.00

Employee Benefits

Rs.

110,000.00

Supplies

Rs.

17,000.00

Wages & Salaries

Rs.

380,000.00

Depreciations

Rs.

24,000.00

Other Expenses

Rs.

10,000.00

Total

Rs.

550,000.00

Table II. Activity and their level.

Activity Activity Level

Machine-hours Unit

Number of special components Batch

Direct materials Unit

Number of production orders Batch

Direct materials Unit

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 620

MARCH 2013

VOL 4, NO 11

Table III. Resources and Cost drivers.

Resource Resource Consumption Cost Driver

Materials management Time worked

Utilities Square-footage

Personnel Number of workers

Engineers Time worked

Quality Time worked

Storeroom Number of items picked for an order

Research and development Number of new codes developed

Accounting Time worked

Table IV. Cost of Direct Material (Product A)

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 621

MARCH 2013

VOL 4, NO 11

Table V. Summary of Direct Material Cost of 5 Products.

Table VI. Product Cost (Traditional Costing)

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 622

MARCH 2013

VOL 4, NO 11

Table VII. Allocation Sheet.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 623

MARCH 2013

VOL 4, NO 11

Table VIII. Recipe of 5Products.

Table IX. Major Overheads of AVL Textile.

Table X. Cost Drivers of AVL Textile.

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 624

MARCH 2013

VOL 4, NO 11

Table XI. Computation of Cost of Product (Material and Manufacturing Overhead)

ijcrb.webs.com

INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS

COPY RIGHT © 2013 Institute of Interdisciplinary Business Research 625

MARCH 2013

VOL 4, NO 11

Table XII. Cost of all Products (ABC System)

Table XIII. Cost Comparison- Traditional vs. ABC

Product

Traditional Costing System

ABC System

Difference

A

375.17

405.46

30.29

B

384.02

402.89

18.87

C

458.76

485.53

26.77

D

524.71

565.20

40.49

E

356.88

378.64

21.76