APAR - Initial Coverage

17

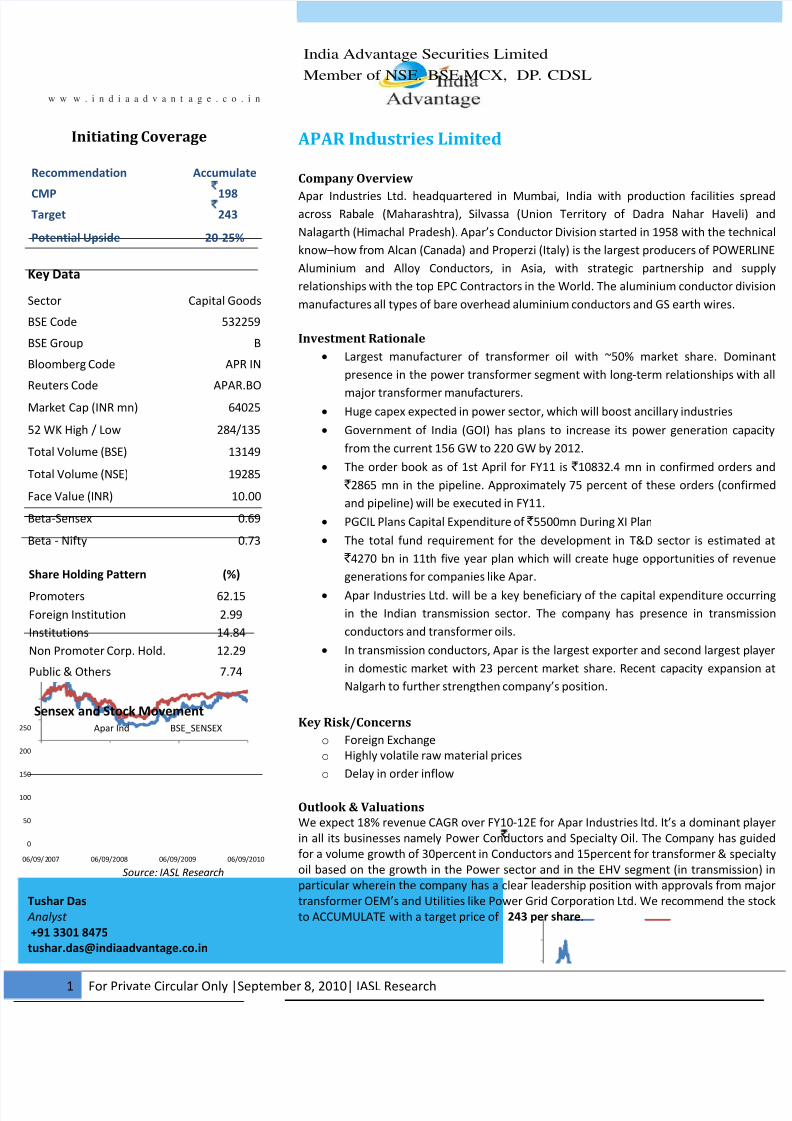

India Advantage Securities Limited Member of NSE. BSE.MCX, DP . CDSL 1 For Private Circular Only |September 8, 2010| IASL Research w w w . i n d i a a d v a n t a g e . c o . i n Company Overview Apar Industries Ltd. headquartered in Mumbai, India with production facilities spread across Rabale (Maharashtra), Silvassa (Union Territory of Dadra Nahar Haveli) and Nalagarth (Himachal Pradesh). Apar’s Conductor Division started in 1958 with the technical know–how from Alcan (Canada) and Properzi (Italy) is the largest producers of POWERLINE Aluminium and Alloy Conductors, in Asia, with strategic partnership and supply relationships with the top EPC Contractors in the World. The aluminium conductor division manufactures all types of bare overhead aluminium conductors and GS earth wires. Investment Rationale • Largest manufacturer of transformer oil with ~50% market share. Dominant presence in the power transformer segment with long‐term relationships with all major transformer manufacturers. • Huge capex expected in power sector, which will boost ancillary industries • Government of India (GOI) has plans to increase its power generation capacity from the current 156 GW to 220 GW by 2012. • The order book as of 1st April for FY11 is ` 10832.4 mn in confirmed orders and ` 2865 mn in the pipeline. Approximately 75 percent of these orders (confirmed and pipeline) will be executed in FY11. • PGCIL Plans Capital Expenditure of ` 5500mn During XI Plan • The total fund requirement for the development in T&D sector is estimated at ` 4270 bn in 11th five year plan which will create huge opportunities of revenue generations for companies like Apar. • Apar Industries Ltd. will be a key beneficiary of the capital expenditure occurring in the Indian transmission sector. The company has presence in transmission conductors and transformer oils. • In transmission conductors, Apar is the largest exporter and second largest player in domestic market with 23 percent market share. Recent capacity expansion at Nalgarh to further strengthen company’s position. Key Risk/Concerns o Foreign Exchange o Highly volatile raw material prices o Delay in order inflow Outlook & Valuations We expect 18% revenue CAGR over FY10‐12E for Apar Industries ltd. It’s a dominant player in all its businesses namely Power Conductors and Specialty Oil. The Company has guided for a volume growth of 30percent in Conductors and 15percent for transformer & specialty oil based on the growth in the Power sector and in the EHV segment (in transmission) in particular wherein the company has a clear leadership position with approvals from major transformer OEM’s and Utilities like Power Grid Corporation Ltd. We recommend the stock to ACCUMULATE with a target price of `243 per share. Initiating Coverage Key Data Sector Capital Goods BSE Code 532259 BSE Group B Bloomberg Code APR IN Reuters Code APAR.BO Market Cap (INR mn) 64025 52 WK High / Low 284/135 Total Volume (BSE) 13149 Total Volume (NSE) 19285 Face Value (INR) 10.00 Beta‐Sensex 0.69 Beta ‐ Nifty 0.73 Recommendation Accumulate CMP `198 Target `243 Potential Upside 20‐25% Share Holding Pattern (%) Promoters 62.15 Foreign Institution 2.99 Institutions 14.84 Non Promoter Corp. Hold. 12.29 Public & Others 7.74 Tushar Das Analyst +91 3301 8475 [email protected] Source: IASL Research 0 50 100 150 200 250 06/09/2 007 06/09/2008 06/09/2009 06/09/2010 Apar Ind BSE_SENSEX Sensex and Stock Movement APAR Industries Limited

Transcript of APAR - Initial Coverage

8/6/2019 APAR - Initial Coverage

http://slidepdf.com/reader/full/apar-initial-coverage 1/16

India Advantage Securities Limited

Member of NSE. BSE.MCX, DP. CDSL

1 For Private Circular Only |September 8, 2010| IASL Research

w w w . i n d i a a d v a n t a g e . c o . i n

Company Overview

Apar Industries Ltd. headquartered in Mumbai, India with production facilities

across Rabale (Maharashtra), Silvassa (Union Territory of Dadra Nahar Havel

Nalagarth (Himachal Pradesh). Apar’s Conductor Division started in 1958 with the tec

know–how from Alcan (Canada) and Properzi (Italy) is the largest producers of POWE

Aluminium and Alloy Conductors, in Asia, with strategic partnership and

relationships with the top EPC Contractors in the World. The aluminium conductor d

manufactures all types of bare overhead aluminium conductors and GS earth wires.

Investment Rationale

• Largest manufacturer of transformer oil with ~50% market share. Dom

presence in the power transformer segment with long‐term relationships w

major transformer manufacturers.

• Huge capex expected in power sector, which will boost ancillary industries

• Government of India (GOI) has plans to increase its power generation ca

from the current 156 GW to 220 GW by 2012.

• The order book as of 1st April for FY11 is ` 10832.4 mn in confirmed orde

` 2865 mn in the pipeline. Approximately 75 percent of these orders (con

and pipeline) will be executed in FY11.

• PGCIL Plans Capital Expenditure of ` 5500mn During XI Plan

• The total fund requirement for the development in T&D sector is estima

` 4270 bn in 11th five year plan which will create huge opportunities of re

generations for companies like Apar.

• Apar Industries Ltd. will be a key beneficiary of the capital expenditure occ

in the Indian transmission sector. The company has presence in transm

conductors and transformer oils.

• In transmission conductors, Apar is the largest exporter and second largest

in domestic market with 23 percent market share. Recent capacity expans

Nalgarh to further strengthen company’s position.

Key Risk/Concerns

o Foreign Exchange

o Highly volatile raw material prices

o Delay in order inflow

Outlook & Valuations

We expect 18% revenue CAGR over FY10‐12E for Apar Industries ltd. It’s a dominant

in all its businesses namely Power Conductors and Specialty Oil. The Company has g

for a volume growth of 30percent in Conductors and 15percent for transformer & sp

oil based on the growth in the Power sector and in the EHV segment (in transmiss

particular wherein the company has a clear leadership position with approvals from

transformer OEM’s and Utilities like Power Grid Corporation Ltd. We recommend the

to ACCUMULATE with a target price of `243 per share.

Initiating Coverage

Key Data

ector Capital Goods

BSE Code 532259

BSE Group B

Bloomberg Code APR IN

Reuters Code APAR.BO

Market Cap (INR mn) 64025

52 WK High / Low 284/135

Total Volume (BSE) 13149

Total Volume (NSE) 19285

ace Value (INR) 10.00

Beta‐Sensex 0.69

Beta ‐ Nifty 0.73

Recommendation Accumulate

CMP `198 Target `243

Potential Upside 20‐25%

Share Holding Pattern (%)

Promoters 62.15

Foreign Institution 2.99

nstitutions 14.84

Non Promoter Corp. Hold. 12.29

Public & Others 7.74

Tushar Das

Analyst

+91 3301 8475

Source: IASL Research

09/ 2007 06/09/2008 06/09/2009 06/09/2010

Apar Ind BSE_SENSEX

Sensex and Stock Movement

APAR Industries Limited

8/6/2019 APAR - Initial Coverage

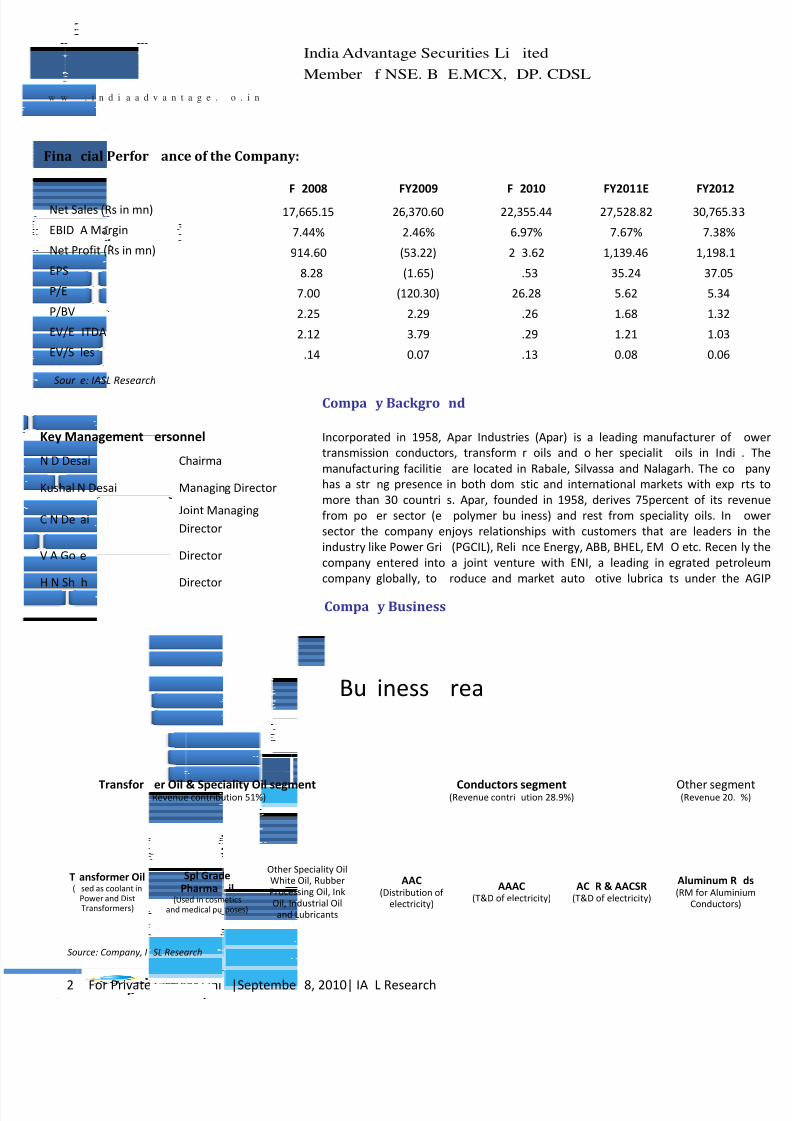

http://slidepdf.com/reader/full/apar-initial-coverage 2/162

w w

Fina

Key M

N D De

Kushal

C N De

V A Go

H N Sh

Sour

T(

Net S

EBID

Net P

EPS

P/E

P/BV

EV/E

EV/S

So

For Private

. i n d i a a d

cial Perfor

anagement

sai

N Desai

ai

e

h

e: IASL Researc

Transfor(

ansformer Oil sed as coolant in

Power and Dist

Transformers)

ales (Rs in mn

A Margin

rofit (Rs in mn

ITDA

les

urce: Company, I Circular Onl

v a n t a g e .

ance of th

ersonnel

Chairma

Managin

Joint Ma

Director

Director

Director

h

er Oil & SpecRevenue contribu

Spl GradPharma

(Used in cosmand medical pu

)

)

SL Research

|Septembe

o . i n

e Company:

g Director

naging

iality Oil segmtion 51%)

e

il etics

poses)

Other SWhite

ProcesOil, In

and L

F

17,

7

9

India Adv

Member

8, 2010| IA

Compa

Incorpora

transmiss

manufact

has a str

more tha

from po

sector th

industry l

company

company

Compa

Bu

ent

peciality Oil

Oil, Rubber

sing Oil, Ink

dustrial Oil

ubricants

2008

665.15

.44%

14.60

8.28

7.00

2.25

2.12

.14

antage Sec

f NSE. B

L Research

y Backgro

ted in 1958,

ion conducto

uring facilitie

ng presence

n 30 countri

er sector (e

e company e

ike Power Gri

entered into

globally, to

y Business

iness

AAC

(Distribution of electricity)

FY2009

26,370.60

2.46%

(53.22)

(1.65)

(120.30)

2.29

3.79

0.07

urities Li

E.MCX,

nd

Apar Industri

rs, transform

are located

in both dom

s. Apar, foun

polymer bu

njoys relation

(PGCIL), Reli

a joint vent

roduce and

rea

Conductors (Revenue contri

AAA(T&D of ele

F

22,

6.

2

2

ited

DP. CDSL

es (Apar) is a

r oils and o

in Rabale, Silv

stic and inter

ded in 1958,

iness) and re

ships with cu

nce Energy, A

ure with ENI,

market auto

segment ution 28.9%)

Cctricity)

AC(T&D

2010

355.44

.97%

3.62

.53

6.28

.26

.29

.13

leading man

her specialit

assa and Nala

national mark

derives 75per

st from speci

stomers that

BB, BHEL, EM

a leading in

otive lubrica

R & AACSR

of electricity)

FY2011E

27,528.82

7.67%

1,139.46

35.24

5.62

1.68

1.21

0.08

ufacturer of

oils in Indi

garh. The co

ets with exp

cent of its re

ality oils. In

are leaders i

O etc. Recen

egrated petr

ts under the

Other segm(Revenue 20.

Aluminum R(RM for Alumin

Conductors

FY2012

30,765.3

7.38%

1,198.1

37.05

5.34

1.32

1.03

0.06

v

i

o

e

)

3

8/6/2019 APAR - Initial Coverage

http://slidepdf.com/reader/full/apar-initial-coverage 3/16

India Advantage Securities Limited

Member of NSE. BSE.MCX, DP. CDSL

3 For Private Circular Only |September 8, 2010| IASL Research

w w w . i n d i a a d v a n t a g e . c o . i n

1. Conductors Segments:

• Apar’s conductor division was started in 1958 with technical know how from Alcan, Canada and Properzi, Italy. Today,

contributes half of India’s total export of aluminium power conductors and a significant portion of its domestic consumptio

• Types of Conductors: The division manufactures all types of bare overhead aluminium conductors such as All Alumin

Conductors (AAC), Aluminium Alloy Conductor (AAAC), Aluminium Conductors Steel Reinforced (ACSR), All Aluminium S

Reinforced Conductors (AASRC), Galvanized Steel Earth Wires and value added alloy based conductors.

• AAC are made up of one or more strands of aluminum wire depending on the required current carrying capacity. T

conductors are used for distribution of electricity specially at substations. AAC conductors have very high degree of corro

resistance.

• AAAC conductors are manufactured consisting of one or more of high strength aluminium ‐ magnesium – silicon alloy w

These conductors are widely used in overhead transmission lines for primary and secondary distribution of power. It prov

very high strength than AAC. Aluminium alloy conductors by Apar were first in India through its own R&D activitie

contributes more than 60‐65percent revenue to the conductor segment.

• AACSR conductors are of one or more aluminium strands as outer wire and wire stranded with zinc coated high steel

wire. These are also used for transmission and distribution of current. These conductors provide excellent mechanical

tensile strength, thus, are best suited for extra long spans, river crossing etc. It contributes more than 60‐65percent reve

to the conductor segment.

• Clients: PGCIL is the largest client of Apar for conductors. It also sells conductors to BOOT contractors such as Adani Po

Reliance Infrastructures, JP Power, Jindal Power etc.

• Approval from all Indian and global utilities: Apar enjoys approvals from all Indian and overseas utilities in strategic mar

like Iran, Iraq, the Middle East and Africa. The company enjoys preferred supplier status with them.

2. Speciality Oil: • The company ventured in to speciality oil business in 1969 with technical know‐how from US based Sun Oil Company.

division have four products viz transformer oil, white oils, rubber processing oils and Industrial oils. Brief description of

products are as follows:

Product % sub‐seg Application Purpose Prospects

Transformer

Oils

50% Power & Distribution Transformers

Used as coolant and

insulation medium

Industry is expected to grow wit

the CAGR of 15‐20% with the ris

demand for transformers

White Oils 12%

Pharmaceuticals products, cosmetics

and food related applications

Serves as base

material

Robust growth in health care

product, cosmetics and polymer

industries.

Rubber Process

Oil 13%

Rubber products such as automobile

tyres and tubes, bicycle tyres, tyre

retreading material, battery

containers etc

Helps in blending

rubber with other

chemicals

Growing demand from the tyres

and automobile industries

Ink Oil

25%

Used in manufacture of ink for

coloured news print

Serves as base

material

Evolution in print media with bla

ink getting replaced with coloure

ink in many printed materials

Industrial &

Automotive

Lubricants

Used in compressors, refrigerators

and automobile engines

Provides lubrication

between moving

machine parts

Increasing number of OEM

projects; rising demand from

automobile industry; increasing

industrialization.

Source: Company, IASL Research

8/6/2019 APAR - Initial Coverage

http://slidepdf.com/reader/full/apar-initial-coverage 4/164

w w

Co

A

SOL

Apa

cont

UNI

Apa

such

con

man

clien

Unif

mon

Unif

FY1

orga

So

For Private

. i n d i a a d

• Largest

50percen

• Second

conducto

• Clients: B

Areva T&

pany Stru

ar Industries L

D OFF POLY

sold its pol

ributed aroun

FLEX ACQUI

has acquired

as power di

uctor industr

y tenders alo

ts better. This

lex expects sa

ths, Uniflex pl

lex Cables pla

. The total d

nised sector v

urce: Company, I

Circular Onl

v a n t a g e .

anufacturer

t. Apar is the f

ajor

Contribur division. It c

HEL, Bharat B

D etc are som

ture

d.

ER BUSINE

ymers busine

d 10percent t

ITION SYN

65 percent i

stribution, ae

and conduct

g with Unifle

combination

les of ` 300 c

ans to launch

ns to increase

omestic cable

alued at arou

SL Research

|Septembe

o . i n

f transformer

ifth largest tra

tor

to

the

revntributed 28.

ijlee, ABB, Em

of the estee

Petroleum

(Tra

Poweroil

(Manu

Apa(50:50 JV wit

Agip br

SS

ss to Paris‐h

the company

RGY WITH

Uniflex Cabl

rospace, defe

or and cables

x after the ac

makes Apar th

ores with ex

a slew of prod

its capacity a

market com

d ` 5,000 cror

India Adv

Member

8, 2010| IA

oil: Apar is th

nsformer oil

nues:

This

di percent to th

co, Voltamp

ed clients of

Specialities Pteding in petroleu

Specialities Pr(General

Uniflex Cableacturing of PV

Chematek Lubh Chematek Spnd of automoti

adquartered

’s revenue in

ONDUCTOR

s through an

ce and telec

businesses ar

uisition. It wi

e only Indian

orts of ` 75 c

ucts in the do

its Umergao

rising both t

s.

antage Sec

f NSE. B

L Research

e biggest man

anufacturer,

ision

is

the

see revenues in

ransformers,

he company.

. Ltd, Singaporm based produ

duct FZE, UAE (rading)

Ltd (65% S) / Elastomeric C

ricants Ltd (50, Italy, for the

e Oil of ENI Sp

Eliokem India

Y2008.

BUSINESS

investment o

ommunicatio

complement

ll help both t

ompany that

rores in FY11

estic market

plant in Guj

e organised

urities Li

E.MCX,

ufacturer of t

lobally.

cond

major

cFY10.

Crompton Gre

(100% S) ts)

100% S)

ables)

A) arketing of . Italy)

Private Ltd

f ` 795 million

s. The powe

ary to each ot

e conductor

provides cond

and ` 1,000 c

, which it curr

rat. Uniflex e

nd unorganis

ited

DP. CDSL

ransformer oil

ntributor

to

t

aves, IMP Po

Qua

for ` 923 mill

in FY2008. U

cables indus

her. Apar’s co

division and U

uctors for tran

ores in the n

ently exports.

xpects a cash

ed sectors is

in India with

he

revenues

o

ers, Transfor

ntum Apar SpeAustralia

(Marketing of S

arine Cables

(65%

ion in Febru

iflex produce

try is around

nductor divisi

niflex to fetch

smission as w

ext five years.

To cater to th

breakeven le

around ` 20,0

the market sh

f

the

compan

mers and Rec

iality Oils Pty L(65% S) peciality Oils)

Wires Pvt Ltd

S)

ry 2008. Pol

s cables for s

3x as large

on is jointly q

orders and s

ell as distribut

Over the ne

domestic de

el of profitabi

00 crores, wit

a

t

e

e

i

i

8/6/2019 APAR - Initial Coverage

http://slidepdf.com/reader/full/apar-initial-coverage 5/165

w w

For Private

. i n d i a a d

Circular Onl

v a n t a g e .

|Septembe

o . i n

India Adv

Member

8, 2010| IA

evenue Co

par has two

onductor

segniflex Cables.

Apar derive

half of India

of its domes

Segment PrConductors

Transformer

Power/Tele

Total

reak – Up o

Source: Compa

Sourc

antage Sec

f NSE. B

L Research

mposition

main busin

ment.

Power

Cond

43

28 per cent

’s total export

tic consumpti

duct

s & Speciality

om Cables

Consolidat

y, IASL Research

e: Company, IASL

urities Li

E.MCX,

ss segments:

nd

telecom

c

ctors

%

f its total rev

of aluminium

n.

Oils

d Gross Rev

Research

ited

DP. CDSL

Transformer

bles

business

enue from th

power condu

Domesti

7

6

7

7

nue in FY10

and specialit

is

operated

th

Power

Teleco

Cable

8%

export mark

ctors and a si

c Market

%

%

%

%

y oils segme

rough

its

subs

&

m

s

Transformer

Oil &

peciality Oils

49%

t. Apar contri

nificant prop

Export Mark

25%

31%

22%

28%

i

8/6/2019 APAR - Initial Coverage

http://slidepdf.com/reader/full/apar-initial-coverage 6/16

India Advantage Securities Limited

Member of NSE. BSE.MCX, DP. CDSL

6 For Private Circular Only |September 8, 2010| IASL Research

w w w . i n d i a a d v a n t a g e . c o . i n

Key highlights of Q1 FY2011 Result

• Net Sales increased from Rs. 5032.50 Million to Rs 6172.91 Million; representing a growth of Rs 1140.41 Million up by 2

percent over corresponding period of previous year.

• EBIDTA increased from Rs.328.60 Million to Rs. 368.75 Million; representing a growth of Rs. 40.15 Million (12.2%) o

corresponding period of previous year.

• PBT increased from Rs. 266.17 Million to Rs. 339.77 Million; representing a growth of Rs. 73.60 Million (27.7%) o

corresponding period of previous year.

• PAT decreased from Rs. 244.79 Million to Rs. 240.15 Million; down marginally by 1.9 percent over corresponding period

previous year. This was due to increase in average tax incidence by 21.29 percent since tax exemption status for Silvassa pl

of Oil division got over in the last quarter (Q4FY10) and the division contributed more to company’s profit than Nalagarh pl

of Conductor, which continues to enjoy tax exemption, has earned lower profit in this quarter.

Segment Revenue

Conductor:

• Sales revenue in Q1 FY1 1 was up 3.6 percent over the corresponding period of previous year from Rs. 2841.19 Million to

2943.07 Million representing a growth of Rs 101.88 Million. The corresponding volume growth was 10.3 percent.

• Segment Level profit was down by 15.1 percent from Rs 169.81 Million to Rs 144.12 Million.

• The Q1FY11 had an improved level of operations with a good overall capacity utilization compared to the previous few quartThe business with domestic & export customers has picked up, and the execution of orders in this quarter was smooth. T

resulted in an improved quantum of production & sales.

• The orders on hand as of 31st July 2010 stood at Rs 12,258.9 Million.

Transformer and Specialty Oils:

• Sales revenue increased from Rs 2197.96 Million to Rs 3295.36 Million, representing a growth of Rs 1097.40 Million (49.9

over the corresponding period of previous year. The corresponding volume was up 12.3 percent as volume increased fr

59,232 KL to 66,511 KL.

• Segment Level profit increased from Rs 186.24 Million to Rs 244.58 Million; representing a growth of Rs 58.34 Million (31.3

over the corresponding period of previous year.

• Sales

volumes

across

all

the

5

sub

segments

of

the

oil

division

have

shown

growth

both

in

the

domestic

market

and

in

expoVolume growth has been the highest in Transformer oils.

• Further, in the case of transformer oils, the sales mix has further improved for high performance oils targeted at EHV custom

of 220 KV to 765 KV power transformers both in domestic and overseas markets. This has led to better profitability of

business.

• The company expects continued growth of at least 15 percent in the transformer oil segment for the next 3‐4 years based

the ongoing expansions in the power sector in India. More specifically, the growth in the EHV segment as the transmiss

networks are built is expected to be strong, where the company has a clear leadership position with approvals from ma

transformer OEM’s and Utilities like Power Grid Corporation Ltd.

INVESTMENT RATIONALE

8/6/2019 APAR - Initial Coverage

http://slidepdf.com/reader/full/apar-initial-coverage 7/16

India Advantage Securities Limited

Member of NSE. BSE.MCX, DP. CDSL

7 For Private Circular Only |September 8, 2010| IASL Research

w w w . i n d i a a d v a n t a g e . c o . i n

Q1 FY2011 Result Q1FY2010 Q1FY2009 Var %

Net Sales 6,172.91 5,032.50 23%

Operating Income 76.08 12.79 495%

Total Income 6,248.99 5,045.29 24%(Increase)/Decrease in stock (49.89) (26.17) 91%

Consumption of Raw Materials 4,985.46 3,855.52 29%

Purchase of traded goods 56.86 118.83 ‐52%

Employee cost 61.70 56.57 9%

Other Expenditure 826.45 711.98 16%

Total Expenditure 5,880.58 4,716.73 25%

PBDIT (Ops) 368.41 328.56 12%

(% of Total Net Sales) 6% 6.5%

Interest & Fin. Charges (1.54) 30.80 ‐105%

PBDT (Ops) 369.95 297.76 24%

Depreciation 30.52 28.74 6%

PBT (Ops) 339.43 269.02 26%

Other Income 0.34 0.04 750%

PBT (Before Ext. Items) 339.77 269.06 26%

Exceptional items ‐ 2.89 ‐100%

PBT 339.77 266.17 28%

Tax Provisions 99.62 21.38 366%

Profit after Tax 240.15 244.79 ‐2%

1. Income Q1FY2010 Q1FY2009 Var. (%

Conductors 2,943.07 2,841.19 4%

Transformers & Speciality Oils 3,295.36 2,197.96 50%

Others/Unallocated 13.14 8.58 53%

TOTAL 6,251.57 5,047.73 24%

Less: Inter segment revenue 2.58 2.44 6%

Net Sales 6,248.99 5,045.29 24%

2. Profit / (Loss) before interest & tax Q1FY2010 Q1FY2009 Var. (%)

Conductors 144.12 169.81 ‐15%

Transformers & Speciality Oils 244.58 186.24 31%

Others 2.58 1.43 80%

TOTAL 391.28 357.48 9%

Less:

i) Interest (Net) (1.54) 30.80 ‐105%

ii) Other unallocable expenses (Net) 53.05 60.51 ‐12%

Total Profit Before Tax 339.77 266.17 28%

Source: Company, IASL Research

Source: Company, IASL Research

Source: Company, IASL Research

8/6/2019 APAR - Initial Coverage

http://slidepdf.com/reader/full/apar-initial-coverage 8/16

India Advantage Securities Limited

Member of NSE. BSE.MCX, DP. CDSL

8 For Private Circular Only |September 8, 2010| IASL Research

w w w . i n d i a a d v a n t a g e . c o . i n

1 Largest Manufacturer of transformer oil with around 50% market share

Apar is the market leader in transformer oils with over 50 percent market share in India under the brand POWEROIL. Transformer o

used in power generation and transmission transformers. Apar is the dominant supplier in power transformer sector (132 kV to 80

meeting the special requirements of OEMs, Utilities and Power Transmission & Distribution Companies.. It exports transformer oils to

35 countries including Middle East, Malaysia, Brazil, Kenya, South Africa, Australia and New Zealand. Apar is the fifth largest transf

oil producer worldwide.

Other specialty oils

Apart from manufacturing transformer oils, Apar also manufactures liquid paraffin’s, white oils, rubber processing oils, ink oils, ind

oils & lubricants.

STRONG DEMAND FOR COMPANY’S PRODUCTS

The government plans to spend Rs1.73tn on power transmission and distribution in the Eleventh Five‐Year Plan (FY08‐12). This tran

into ~8x growth in demand for the company’s products. Management expects demand for conductors to increase from 0.25mt

present to 2.1mtpa by FY12. The company is poised to take advantage of this multifold growth, having undertaken ~25 percent expa

in installed capacity. Management has increased capacity to 337351MT from 269881MT. As for transformer oils, the demand is exp

to reach 900mn litres pa as compared to 110mn litres pa currently.

Focus on the value added products

Apar

is

focusing

on

the

development

of

high

value

a

product

which

is

a

high

margin

business.

The

Transformer

oil

segment

has

recsignificant orders for its high oxidation stability grade products meeting special application requirements of Extra High V

transformers, with ratings of 400 KV to 800 KV from several global transformer majors. This segment is expected to have a much h

demand in the years to come as the BRIC countries, including India build high voltage transmission networks. Apar, is so far the only

company to have this approval from global transformer OEM’s.

Apar is focusing on developing high temperature conductors which can carry a higher amount of current. The capacity to carry

current is being increased by 25 per cent, 50 per cent and up to 100 per cent. At the moment, in India, there is no significant dema

the conductors. With the government's focus on high‐voltage transmission grid, the demand for high voltage conductors is expec

witness a major push in the coming years.

34

4339

60

40

0

20

40

60

80

100

120

0

10

20

30

40

50

60

70

FY2006 FY2007 FY2008 FY2009 FY2010

Transformer Oil Volume Realisations

Source: Company, IASL Research

8/6/2019 APAR - Initial Coverage

http://slidepdf.com/reader/full/apar-initial-coverage 9/169

w w

T

`91

`5

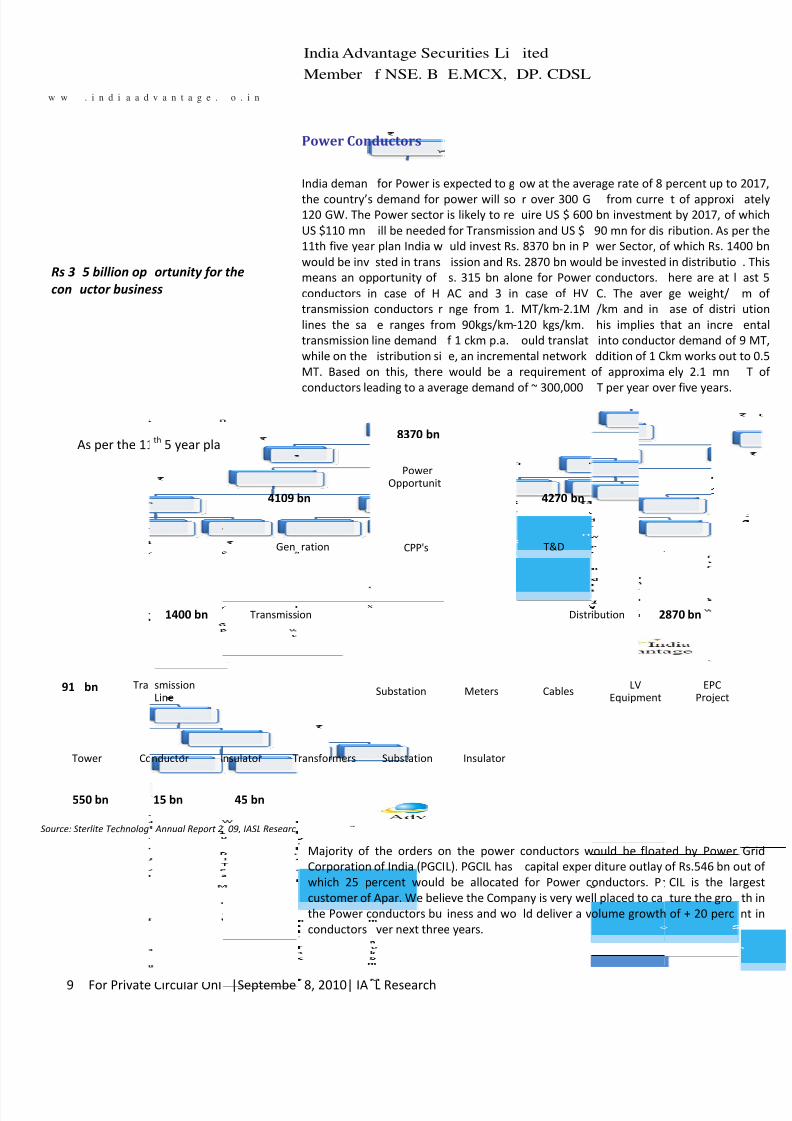

Rs 3con

Source: S

For Private

. i n d i a a d

Tra

ower Co

bn

`50 bn

5 billion opuctor busine

As per the 11

terlite Technolog

Circular Onl

v a n t a g e .

smission

Line

nductor I

`1400 bn

15 bn

ortunity for ss

th 5 year pla

Annual Report 2

|Septembe

o . i n

Gen

Transmiss

nsulator T

`4109

`45 bn

the

09, IASL Researc

India Adv

Member

8, 2010| IA

Power Con

India deman

the country’s120 GW. The

US $110 mn

11th five yea

would be inv

means an op

conductors i

transmission

lines the sa

transmission

while on the

MT. Based o

conductors

le

ration

ion

ransformers

Majority of

Corporation

which 25 p

customer of

the Power c

conductors

bn

antage Sec

f NSE. B

L Research

ductors

for Power is

demand for

Power sector

ill be needed

r plan India w

sted in trans

portunity of

n case of H

conductors r

e ranges fro

line demand

istribution si

n this, there

ading

to

a

ave

Power

Opportunit

CPP's

Substation

Substation

the orders o

of India (PGCI

ercent would

Apar. We beli

onductors bu

ver next thre

`8370 bn

urities Li

E.MCX,

expected to g

power will sois likely to re

for Transmiss

uld invest Rs.

ission and Rs

s. 315 bn alo

AC and 3 in

nge from 1.

m 90kgs/km‐

f 1 ckm p.a.

e, an increme

would be a

rage

demand

Insulator

Meters

n the power

L). PGCIL has

be allocated

eve the Comp

iness and wo

e years.

ited

DP. CDSL

ow at the ave

r over 300 Guire US $ 600

ion and US $

8370 bn in P

. 2870 bn wou

ne for Power

case of HV

MT/km‐2.1M

120 kgs/km.

ould translat

ntal network

requirement

of

~

300,000

T&D

Distr

Cables

conductors w

capital expen

for Power c

any is very we

ld deliver a v

`4270 bn

rage rate of 8

from curre bn investmen

90 mn for dis

wer Sector, o

ld be invested

conductors.

C. The aver

/km and in

his implies t

into conduct

ddition of 1 C

of approxima

T

per

year

ov

ibution

LV

Equipment

ould be float

diture outlay

onductors. P

ll placed to ca

olume growth

`2

percent up to

t of approxit by 2017, of

ribution. As p

f which Rs. 14

in distributio

here are at l

ge weight/

ase of distri

hat an incre

or demand of

km works out

ely 2.1 mn

er

five

years.

EPC

Project

ed by Power

of Rs.546 bn o

CIL is the la

ture the gro

of + 20 perc

870 bn

w

e

9

t

r

8/6/2019 APAR - Initial Coverage

http://slidepdf.com/reader/full/apar-initial-coverage 10/16

India Advantage Securities Limited

Member of NSE. BSE.MCX, DP. CDSL

10 For Private Circular Only |September 8, 2010| IASL Research

w w w . i n d i a a d v a n t a g e . c o . i n

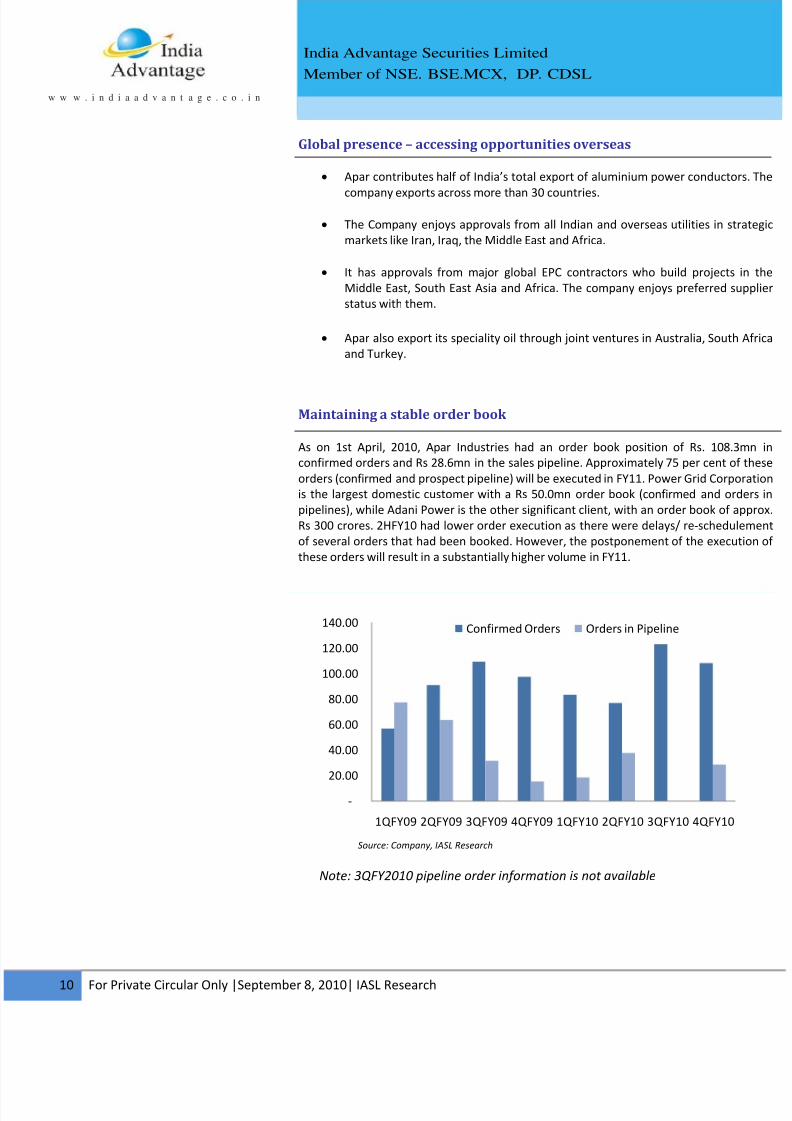

Global presence – accessing opportunities overseas

• Apar contributes half of India’s total export of aluminium power conductor

company exports across more than 30 countries.

• The Company enjoys approvals from all Indian and overseas utilities in str

markets like Iran, Iraq, the Middle East and Africa.

• It has approvals from major global EPC contractors who build projects

Middle East, South East Asia and Africa. The company enjoys preferred su

status with them.

• Apar also export its speciality oil through joint ventures in Australia, South

and Turkey.

Maintaining a stable order book

As on 1st April, 2010, Apar Industries had an order book position of Rs. 108.3

confirmed orders and Rs 28.6mn in the sales pipeline. Approximately 75 per cent of

orders (confirmed and prospect pipeline) will be executed in FY11. Power Grid Corpo

is the largest domestic customer with a Rs 50.0mn order book (confirmed and ord

pipelines), while Adani Power is the other significant client, with an order book of a

Rs 300 crores. 2HFY10 had lower order execution as there were delays/ re‐schedule

of several orders that had been booked. However, the postponement of the execut

these orders will result in a substantially higher volume in FY11.

‐

20.00

40.00

60.00

80.00

100.00

120.00

140.00

1QFY09 2QFY09 3QFY09 4QFY09 1QFY10 2QFY10 3QFY10 4QFY10

Confirmed Orders Orders in Pipeline

Note: 3QFY2010 pipeline order information is not available

Source: Company, IASL Research

8/6/2019 APAR - Initial Coverage

http://slidepdf.com/reader/full/apar-initial-coverage 11/16

India Advantage Securities Limited

Member of NSE. BSE.MCX, DP. CDSL

11 For Private Circular Only |September 8, 2010| IASL Research

w w w . i n d i a a d v a n t a g e . c o . i n

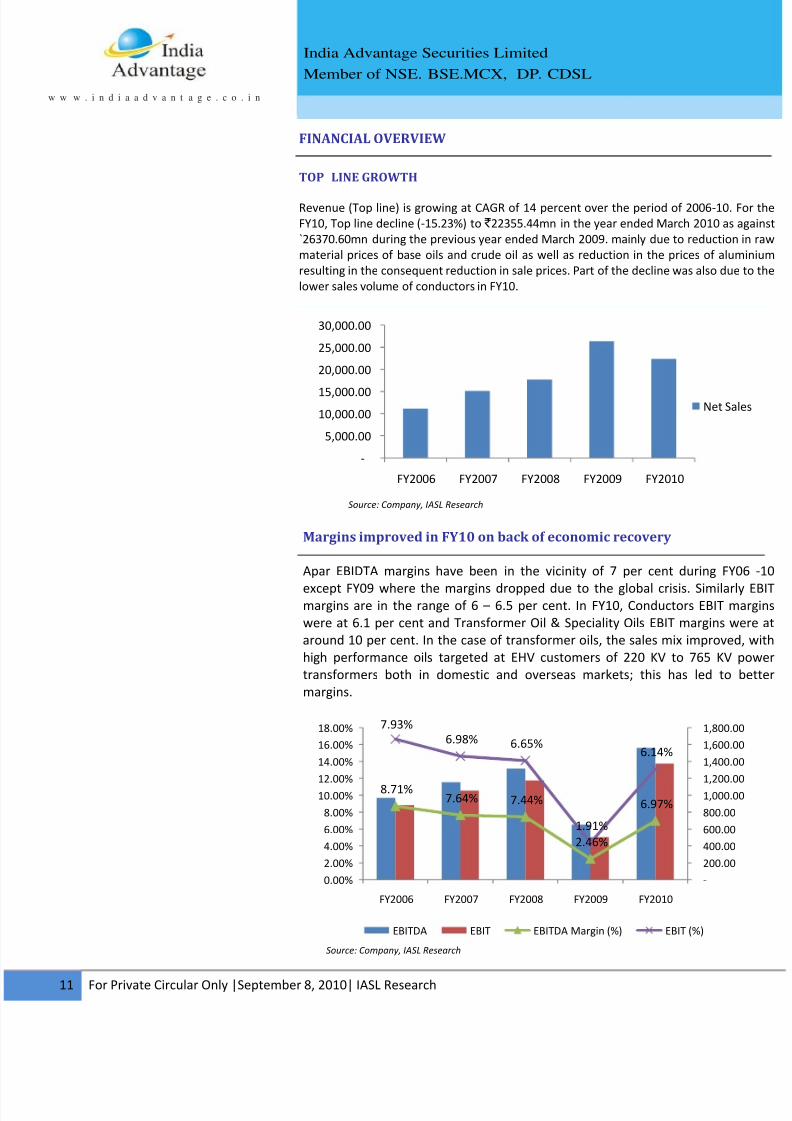

TOP LINE GROWTH

Revenue (Top line) is growing at CAGR of 14 percent over the period of 2006‐10. F

FY10, Top line decline (‐15.23%) to ` 22355.44mn in the year ended March 2010 as a

`26370.60mn during the previous year ended March 2009. mainly due to reduction

material prices of base oils and crude oil as well as reduction in the prices of alum

resulting in the consequent reduction in sale prices. Part of the decline was also due

lower sales volume of conductors in FY10.

Margins improved in FY10 on back of economic recovery

Apar EBIDTA margins have been in the vicinity of 7 per cent during FY0

except FY09 where the margins dropped due to the global crisis. Similarlymargins are in the range of 6 – 6.5 per cent. In FY10, Conductors EBIT m

were at 6.1 per cent and Transformer Oil & Speciality Oils EBIT margins we

around 10 per cent. In the case of transformer oils, the sales mix improved

high performance oils targeted at EHV customers of 220 KV to 765 KV p

transformers both in domestic and overseas markets; this has led to b

margins.

FINANCIAL OVERVIEW

‐

5,000.00

10,000.00

15,000.00

20,000.00

25,000.00

30,000.00

FY2006 FY2007 FY2008 FY2009 FY2010

Net Sal

8.71%7.64% 7.44%

2.46%

6.97%

7.93%

6.98% 6.65%

1.91%

6.14%

‐

200.00

400.00

600.00

800.00

1,000.00

1,200.00

1,400.00

1,600.00

1,800.00

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

FY2006 FY2007 FY2008 FY2009 FY2010

EBITDA EBIT EBITDA Margin (%) EBIT (%)

Source: Company, IASL Research

Source: Company, IASL Research

8/6/2019 APAR - Initial Coverage

http://slidepdf.com/reader/full/apar-initial-coverage 12/16

India Advantage Securities Limited

Member of NSE. BSE.MCX, DP. CDSL

12 For Private Circular Only |September 8, 2010| IASL Research

w w w . i n d i a a d v a n t a g e . c o . i n

0.57

0.61

0.35

0.58 0.57

0.52

0.46

‐

0.10

0.20

0.30

0.40

0.50

0.60

0.70

FY2006 FY2007 FY2008 FY2009 FY2010 FY2011EFY201

12.95

14.90

28.28

(1.65)

7.53

35.24

37.05

(5.00)

‐

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

FY2006 FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E

0%

10%

20%

30%

40%

50%

60%

70%

FY2006 FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E

RoCE (%) RoE(%)

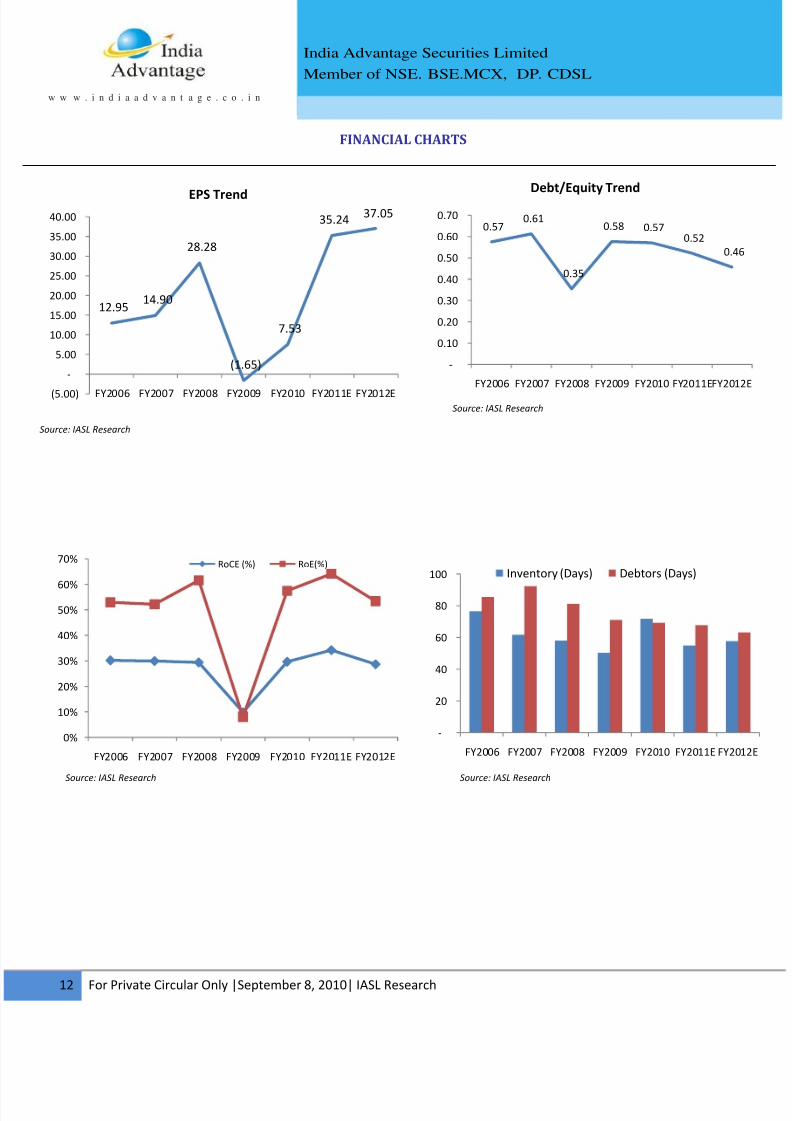

FINANCIAL CHARTS

EPS Trend

Debt/Equity Trend

‐

20

40

60

80

100

FY2006 FY2007 FY2008 FY2009 FY2010 FY2011E FY20

Inventory (Days) Debtors (Days)

Source: IASL Research

Source: IASL Research

Source: IASL Research

Source: IASL Research

8/6/2019 APAR - Initial Coverage

http://slidepdf.com/reader/full/apar-initial-coverage 13/16

India Advantage Securities Limited

Member of NSE. BSE.MCX, DP. CDSL

13 For Private Circular Only |September 8, 2010| IASL Research

w w w . i n d i a a d v a n t a g e . c o . i n

VALUATIONS

We expect 18% revenue CAGR over FY10‐12E for Apar Industries ltd. Apar Industri

the dominant player in all its businesses namely Power Conductors and Specialty Oil.

Company has guided for a volume growth of 30 percent in Conductors and 15 per

for transformer & specialty oil based on the growth in the Power sector and in the

segment (in transmission) in particular wherein the company has a clear leader

position with approvals from major transformer OEM’s and Utilities like Power

Corporation Ltd. We recommend the stock to ACCUMULATE with a target price of `per share.

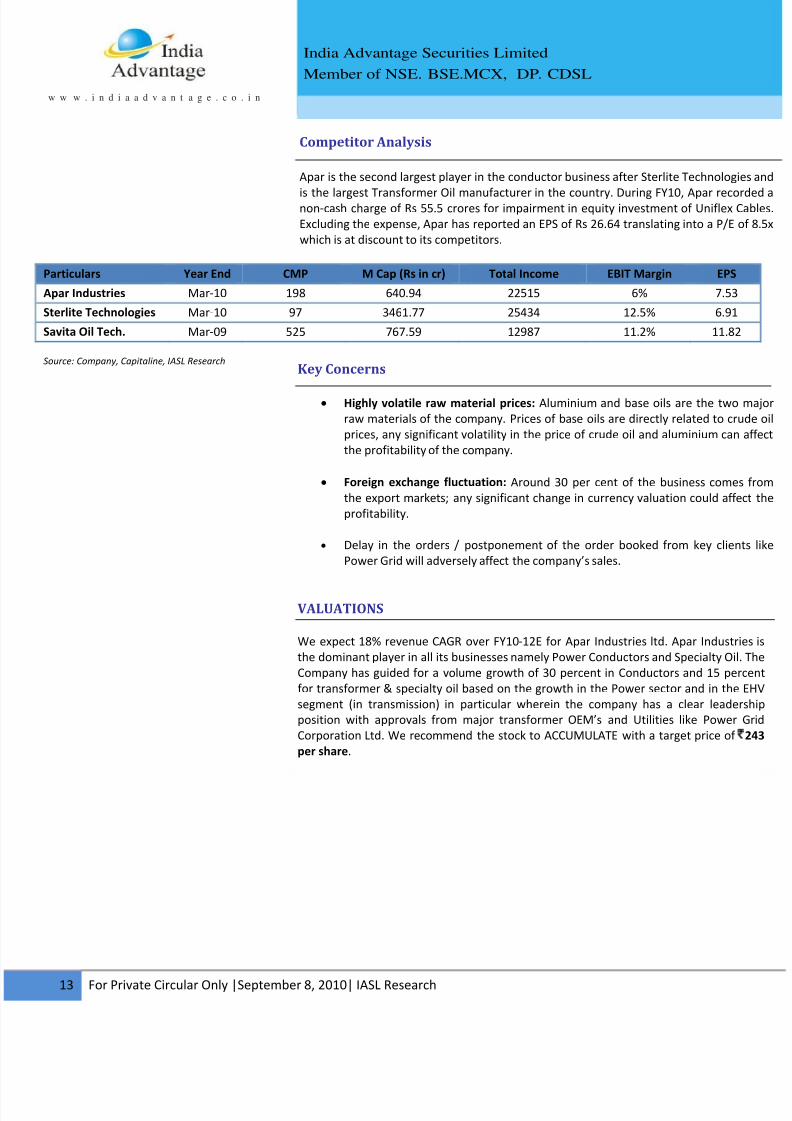

Competitor Analysis

Apar is the second largest player in the conductor business after Sterlite Technologi

is the largest Transformer Oil manufacturer in the country. During FY10, Apar reconon‐cash charge of Rs 55.5 crores for impairment in equity investment of Uniflex C

Excluding the expense, Apar has reported an EPS of Rs 26.64 translating into a P/E o

which is at discount to its competitors.

Particulars Year End CMP M Cap (Rs in cr) Total Income EBIT Margin EPS

Apar Industries Mar‐10 198 640.94 22515 6% 7.53

Sterlite Technologies Mar‐10 97 3461.77 25434 12.5% 6.91

Savita Oil Tech. Mar‐09 525 767.59 12987 11.2% 11.82

Key Concerns

• Highly volatile raw material prices: Aluminium and base oils are the two

raw materials of the company. Prices of base oils are directly related to cru

prices, any significant volatility in the price of crude oil and aluminium can

the profitability of the company.

• Foreign exchange fluctuation: Around 30 per cent of the business comes

the export markets; any significant change in currency valuation could affe

profitability.

• Delay in the orders / postponement of the order booked from key clien

Power Grid will adversely affect the company’s sales.

Source: Company, Capitaline, IASL Research

8/6/2019 APAR - Initial Coverage

http://slidepdf.com/reader/full/apar-initial-coverage 14/16

India Advantage Securities Limited

Member of NSE. BSE.MCX, DP. CDSL

14 For Private Circular Only |September 8, 2010| IASL Research

w w w . i n d i a a d v a n t a g e . c o . i n

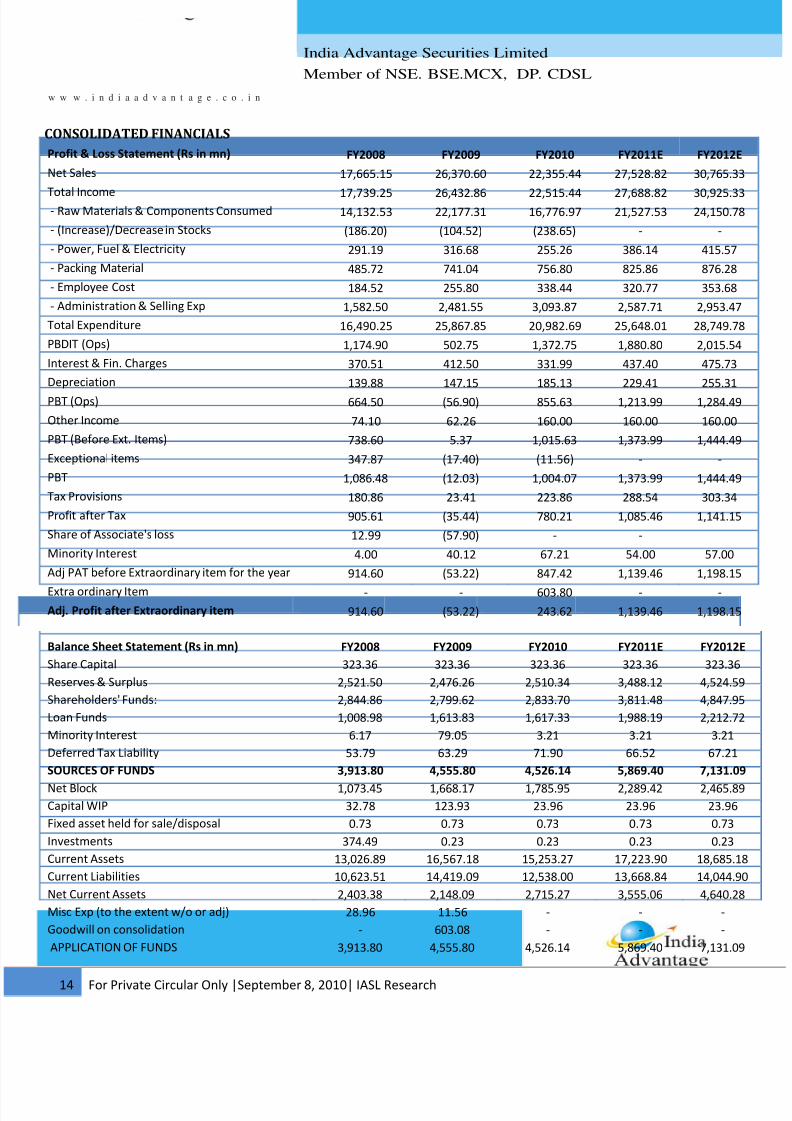

Profit & Loss Statement (Rs in mn) FY2008 FY2009 FY2010 FY2011E FY2012E

Net Sales 17,665.15 26,370.60 22,355.44 27,528.82 30,765.33

Total

Income

17,739.25 26,432.86 22,515.44 27,688.82 30,925.33‐ Raw Materials & Components Consumed 14,132.53 22,177.31 16,776.97 21,527.53 24,150.78

‐ (Increase)/Decrease in Stocks (186.20) (104.52) (238.65) ‐ ‐

‐ Power, Fuel & Electricity 291.19 316.68 255.26 386.14 415.57

‐ Packing Material 485.72 741.04 756.80 825.86 876.28

‐ Employee Cost 184.52 255.80 338.44 320.77 353.68

‐ Administration & Selling Exp 1,582.50 2,481.55 3,093.87 2,587.71 2,953.47

Total Expenditure 16,490.25 25,867.85 20,982.69 25,648.01 28,749.78

PBDIT (Ops) 1,174.90 502.75 1,372.75 1,880.80 2,015.54

Interest & Fin. Charges 370.51 412.50 331.99 437.40 475.73

Depreciation 139.88 147.15 185.13 229.41 255.31

PBT (Ops) 664.50 (56.90) 855.63 1,213.99 1,284.49

Other Income 74.10 62.26 160.00 160.00 160.00

PBT (Before Ext. Items) 738.60 5.37 1,015.63 1,373.99 1,444.49

Exceptional items 347.87 (17.40) (11.56) ‐ ‐

PBT 1,086.48 (12.03) 1,004.07 1,373.99 1,444.49

Tax Provisions 180.86 23.41 223.86 288.54 303.34

Profit after Tax 905.61 (35.44) 780.21 1,085.46 1,141.15

Share of Associate's loss 12.99 (57.90) ‐ ‐

Minority Interest 4.00 40.12 67.21 54.00 57.00

Adj PAT before Extraordinary item for the year 914.60 (53.22) 847.42 1,139.46 1,198.15

Extra ordinary Item ‐ ‐ 603.80 ‐ ‐

Adj. Profit after Extraordinary item 914.60 (53.22) 243.62 1,139.46 1,198.15

CONSOLIDATED FINANCIALS

Source: IASL Research

Balance Sheet Statement (Rs in mn) FY2008 FY2009 FY2010 FY2011E FY2012E

Share Capital 323.36 323.36 323.36 323.36 323.36

Reserves & Surplus 2,521.50 2,476.26 2,510.34 3,488.12 4,524.59

Shareholders' Funds: 2,844.86 2,799.62 2,833.70 3,811.48 4,847.95

Loan Funds 1,008.98 1,613.83 1,617.33 1,988.19 2,212.72

Minority Interest 6.17 79.05 3.21 3.21 3.21

Deferred Tax Liability 53.79 63.29 71.90 66.52 67.21

SOURCES OF FUNDS 3,913.80 4,555.80 4,526.14 5,869.40 7,131.09

Net Block 1,073.45 1,668.17 1,785.95 2,289.42 2,465.89

Capital WIP 32.78 123.93 23.96 23.96 23.96

Fixed asset held for sale/disposal 0.73 0.73 0.73 0.73 0.73

Investments 374.49 0.23 0.23 0.23 0.23

Current Assets 13,026.89 16,567.18 15,253.27 17,223.90 18,685.1

Current Liabilities 10,623.51 14,419.09 12,538.00 13,668.84 14,044.9

Net Current Assets 2,403.38 2,148.09 2,715.27 3,555.06 4,640.28

Misc Exp (to the extent w/o or adj) 28.96 11.56 ‐ ‐ ‐

Goodwill on consolidation ‐ 603.08 ‐ ‐ ‐

APPLICATION OF FUNDS 3,913.80 4,555.80 4,526.14 5,869.40 7,131.09

8/6/2019 APAR - Initial Coverage

http://slidepdf.com/reader/full/apar-initial-coverage 15/16

India Advantage Securities Limited

Member of NSE. BSE.MCX, DP. CDSL

15 For Private Circular Only |September 8, 2010| IASL Research

w w w . i n d i a a d v a n t a g e . c o . i n

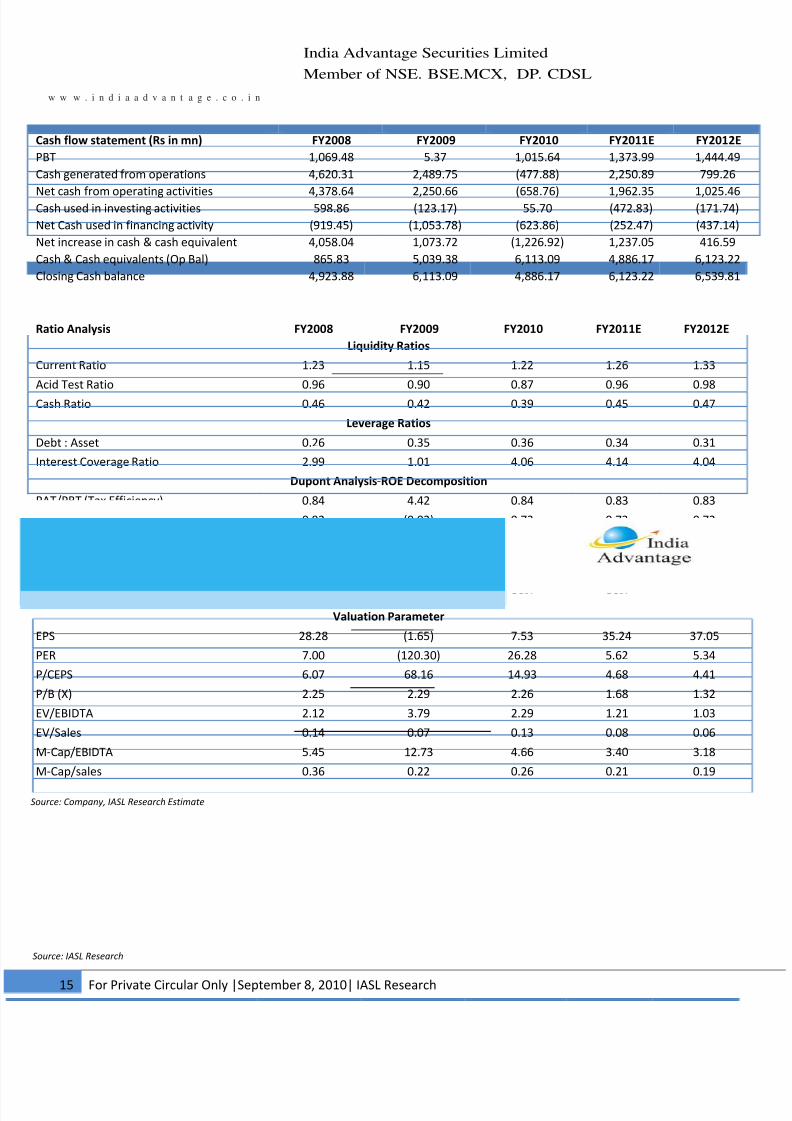

Cash flow statement (Rs in mn) FY2008 FY2009 FY2010 FY2011E FY2012E

PBT 1,069.48 5.37 1,015.64 1,373.99 1,444.49

Cash generated from operations 4,620.31 2,489.75 (477.88) 2,250.89 799.26

Net

cash

from

operating

activities

4,378.64 2,250.66 (658.76)

1,962.35 1,025.46Cash used in investing activities 598.86 (123.17) 55.70 (472.83) (171.74)

Net Cash used in financing activity (919.45) (1,053.78) (623.86) (252.47) (437.14)

Net increase in cash & cash equivalent 4,058.04 1,073.72 (1,226.92) 1,237.05 416.59

Cash & Cash equivalents (Op Bal) 865.83 5,039.38 6,113.09 4,886.17 6,123.22

Closing Cash balance 4,923.88 6,113.09 4,886.17 6,123.22 6,539.81

Ratio Analysis FY2008 FY2009 FY2010 FY2011E FY2012E

Liquidity Ratios

Current Ratio 1.23 1.15 1.22 1.26 1.33

Acid Test Ratio 0.96 0.90 0.87 0.96 0.98

Cash Ratio 0.46 0.42 0.39 0.45 0.47

Leverage Ratios

Debt : Asset 0.26 0.35 0.36 0.34 0.31

Interest Coverage Ratio 2.99 1.01 4.06 4.14 4.04

Dupont Analysis‐ROE Decomposition

PAT/PBT (Tax Efficiency) 0.84 4.42 0.84 0.83 0.83

PBT/EBIT (Interest Burden) 0.92 (0.02) 0.73 0.73 0.72

EBIT/Sales (OPM) 0.07 0.02 0.06 0.07 0.07

Sales/Total Assets (Asset Turnover) 4.51 5.79 4.94 4.69 4.31

TA/NW (Financial Leverage) 1.38 1.63 1.60 1.54 1.47

ROE 32% ‐2% 30% 30% 25%

Valuation Parameter

EPS 28.28 (1.65) 7.53 35.24 37.05

PER 7.00 (120.30) 26.28 5.62 5.34

P/CEPS 6.07 68.16 14.93 4.68 4.41

P/B (X) 2.25 2.29 2.26 1.68 1.32

EV/EBIDTA 2.12 3.79 2.29 1.21 1.03

EV/Sales 0.14 0.07 0.13 0.08 0.06

M‐Cap/EBIDTA 5.45 12.73 4.66 3.40 3.18

M‐Cap/sales 0.36 0.22 0.26 0.21 0.19

Source: IASL Research

Source: Company, IASL Research Estimate

8/6/2019 APAR - Initial Coverage

http://slidepdf.com/reader/full/apar-initial-coverage 16/16

India Advantage Securities Limited

Member of NSE. BSE.MCX, DP. CDSL

w w w . i n d i a a d v a n t a g e . c o . i n

IASL Research: E‐mail: [email protected]

Disclaimer: This document has been prepared by India Advantage Security Ltd. IASL is a full service, integrated portfolio management and brokerage group. Our rese

analysts and sales persons provide important input into our investment banking activities. This document does not constitute an offer or solicitation for the purchase or

of any financial instrument or as an official confirmation of any transaction. The information contained herein is from publicly available data or other sources believed t

reliable, but we do not represent that it is accurate or complete and it should not be relied on as such. IASL or any of its affiliates shall not be in any way responsible for

loss or damage that may arise to any person from any inadvertent error in the information contained in this report. This document is provided for assistance only and is

intended to be and must not alone be taken as the basis for an investment decision. The user assumes the entire risk of any use made of this information. Each recipie

this document should make such investigation as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred t

this document (including the merits and risks involved), and should consult his own advisors to determine the merits and risks of such investment. The investment discu

or views expressed may not be suitable for all investors. We and our affiliates, officers, directors, and employees may: (a) from time to time, have long or short position

and buy or sell the securities thereof, of company (ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or o

compensation or act as advisor or lender / borrower to such company (ies) or have other potential conflict of interest with respect to any recommendation and rel

information and opinions. This information is strictly confidential and is being furnished to you solely for your information.

This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part

any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, cou

or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject IASL and affiliates to

registration or licensing requirements within such jurisdiction. The distribution of this document in certain jurisdictions may be restricted by law, and persons in w

possession this document comes, should inform themselves about and observe, any such restrictions. The information given in this document is as of the date of this re

and there can be no assurance that future results or events will be consistent with this information. This information is subject to change without any prior notice.

reserves the right to make modifications and alterations to this statement as may be required from time to time. However, IASL is under no obligation to update or keep

information current. Nevertheless, IASL is committed to providing independent and transparent recommendation to its client and would be happy to provide

information in response to specific client queries. Neither IASL nor any of its affiliates, directors, employees, agents or representatives shall be liable for any dam

whether direct, indirect, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The analys

this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or t

securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report.

Analyst holding in stock: No.

Key to IASL Investment Rankings

Buy: Upside by>15%, Accumulate: Upside by +5% to 15%, Hold: Upside/Downside by ‐5% to +5%

Reduce: Downside by 5% to 15%, Sell: Downside by>15%

INDIA ADVANTAGE SECURITIES Ltd. (www.indiaadvantage.co.in)

Corporate Office: ‐ Om Plaza, Vasanji Lalji Road, Opp. Railway Station, Kandivali (W), Mumbai – 400 067.

Tel Phone nos.: 022 ‐ 3301 8475 Fax nos.: 022 – 2809 2800.