ANNUAL REPORT - ORLEN Lietuva · ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 5...

88

ANNUAL REPORT OF PUBLIC COMPANY ORLEN LIETUVA FOR THE YEAR 2011 1 ANNUAL REPORT of Public Company Orlen Lietuva for the year 2011

Transcript of ANNUAL REPORT - ORLEN Lietuva · ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 5...

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 1

ANNUAL REPORT of Public Company Orlen Lietuva for the year 2011

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 2

About Public Company ORLEN Lietuva

ORLEN Lietuva is a crude oil refining company, which owns and operates a fuels refinery, a network of crude oil and petroleum product pipelines, and a marine terminal.

The Company’s main areas of activities include production and wholesale of the petroleum products. The Refinery is capable of processing about 10 million tons of crude oil annually.

The Company owns, via its subsidiary AB Ventus – Nafta, a network of filling stations, operated under ORLEN brand.

ORLEN Lietuva is a wholy owned subsidiary of the Polish Oil Concern PKN ORLEN S.A., a leader of the refining sector of Central and Eastern Europe.

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 3

Board*of Directors

Ireneusz Fąfara

Chairman of the Board of Direc-tors and General Director, Public Company ORLEN Lietuva

Vita Petrošienė

Deputy General Director for Business Support, Public Company ORLEN Lietuva

Krystian Pater

Member of the Management Board, Refinery Operations, PKN ORLEN

* December 31, 2011

Sławomir Robert Jędrzejczyk

Chief Financial Officer, PKN ORLEN

Jarosław Szaliński

Chief Financial Officer, Public Company ORLEN Lietuva

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 4

ANNUAL REPORT of Public Company Orlen Lietuva for the year 2011Despite the market instability and challenges faced by the refining industry worldwide, the result of the year 2011 evidences the continuous pursuit of Public Company ORLEN Lietuva and its subsidiaries (hereinafter – the Group) to increase operational efficiency as well as maintain a positive cash flow and steady increase in sales.

Performance optimization and labor efficiency increase were one of the most serious challenges for Public Company ORLEN Lietuva (hereinafter – the Parent Company) during the last year. In 2011, reorganizational changes were continued. The Parent Company succeeded in reduction of its energy consumption, increasing yields of the light petroleum products, reduction of manpower and implementation of the projects related to improvement of the Parent Company’s management.

The supply chain management undertakings implemented in the Parent Company allowed smooth coordination of operations, logistics and sales activities, reducing the level of inventories and, at the same time, the working capital demand as well as mitigating the impact of inventory depreciation on financial results.

Organizational changes and restructuring were followed by the workforce reduction during the last year. In comparison with 2010, the number of active employees in the Group decreased by 132. The number of active employees in the Group at the end of 2011 was 2,508.

Last year the Parent Company implemented only the most essential projects required for upgrade of existing units to ensure safe and continuous production process and compliance of petroleum products with the new requirements of the European Union.

Operating Results

In 2011, the feedstock processing volume was 9.5 million tons, i.e. by 0.2 million tons (2 %) higher than during the last year (9.3 million tons).

Sales of petroleum products by the Group in 2011 amounted to 9 million tons, compared to 8.7 million tons of petroleum products in 2010. Petroleum product sales volume increased by 0.3 million tons or 4 % if compared to 2010. As a result of the increased world prices for crude and petroleum products and higher sales by the Parent Company, revenue of the Group increased by 41.2 % and reached USD 8.2 billion (LTL 20.3 billion) in 2011, while the revenue in the year 2010 amounted to USD 5.8 billion (LTL 15.1 billion).

Despite the serious competition on the Baltic markets, the Group managed to increase its gasoline and diesel fuel sales on the markets of Lithuania, Latvia and Estonia. Volume of the said products sold to the above markets increased by 22.8 % in comparison with 2010.

In 2011, the Group exceeded the level of 2010 sales to Ukrainian market and markets of other CIS, reaching almost 700 thousand tons of gasoline and diesel fuel, i.e. by 6.6 % higher than during the previous year. Such sales results were impacted by the quality of fuel and recognition of the refined petroleum products on the market.

Increase of the refining volumes was followed by growth of the seaborne sales in 2011, amounting to 4.9 million tons, in comparison with 4.8 million tons in the year 2010.

Commercial Sales and Logistics Divisions of the Parent Company were successful in increasing efficiency of their activities, Operations Division reduced fuel consumption and improved the light products yield (73.9 % compared to 73.5 % in 2010), while

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 5

due to the increased refining volumes the capacity utilization reached 88.6 % compared to 88 % in 2010. In 2011, the Parent Company implemented the whole range of the projects intended for improvement of products’ quality as well as operations efficiency. All the indicated achievements had a positive impact on the Parent Company’s performance.

In 2011, the fuel stations of the Group operating under ORLEN LIETUVA and VENTUS brands sold 71.66 million liters of fuel, i.e. decrease by 13.6 % versus 2010. The main reasons for such reduction were further increase of fuel prices (diesel fuel price increased by approx. 0.50 LTL/liter, while growth of gasoline prices was by approx. 0.15 LTL/liter in comparison with 2010) as well as increasing size of the shadow economy. Due to the increased competition on the fuel retail market the fuel sales supporting promotions were less successful than in the year 2010.

The volume of sales in the shops of the fuel stations increased by 3 % in comparison with the year 2010 due to the continued growth of fast food and coffee sales as well as recovery in tobacco sales.

Financial Results

The net loss of the Group for the year 2011 under the International Financial Reporting Standards (IFRS) amounted to USD 5.6 million (LTL 13.9 million), while the net loss for 2010 was USD 31.4 million (LTL 81.9 million). Operating profit for the year 2011 comprised USD 25.2 million (LTL 62.6 million) in comparison with USD 11.3 million (LTL 29.4 million) for 2010.

Changes in financial indicators of the Group for the year 2011 in comparison to the same period of the last year were as follows: the return on assets was -0.003 (-0.017 in 2010), and the return on equity was -0.007 (-0.042 in 2010). Changes of other indicators were as follows: the long term debt to equity ratio was 0.49 (0.23 in 2010), the current ratio was 1.08 (0.84 in 2010), the asset turnover ratio was 4.38 (3.13 in 2010), and the net debt to equity ratio was 0.45 (0.33 in 2010).

Information on financial risk management of the Group is available in Note 27 of Financial Statements. Information includes financial risk management objectives, used insurance instruments to which the accounting of insurance transactions is applicable as well as the information on the extent of pricing risk, credit risk and cash flow risk of the Group.

Modernization, Mandatory and Other Projects

In 2011 the Parent Company implemented only the most essential projects required for upgrade of existing units to ensure safe and continuous production process and increase profitability.

The total amount of investments made by the Group into the modernization, mandatory and other projects during the year 2011 comprised USD 39.7 million, i.e. were by 134 % higher than in the year 2010 (USD 17 million in 2010).

In 2011, the following modernization projects significant to the Parent Company were implemented: Sulphur Degassing and Granulation Project, replacement of FCC Unit Reactor R-201 internals as well as implementation of Emergency Shutdown/Distributed Control Systems (ESD/DCS) with replacement of pneumatic devices to electronic devices.

Taking into consideration the financial status, the main targets were increase of the Parent Company’s profitability and implementation of the projects with the short pay-back period requiring minimum investment. In 2011, the number of such projects completed by the Parent Company amounted to 14, with the total budget reaching USD 3.9 million and the positive impact on EBITDA (Earnings before Interest, Taxes, Depreciation and Amortization) comprising approx. USD 20 million per year. The main projects intended for EBITDA improvement were as follows: FCC Unit capacity increase in summer period, installation of soot blowers for boilers KU-401/1,2, and utilization of Reactor R-301 in LK-2 Complex for kerosene hydrotreatment.

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 6

Work Compensation Policy and Employees’ Development

The Parent Company has the effective Collective Agreement concluded in 2009, offering its employees an attractive package of social benefits and guarantees. Work compensation policy is labor market oriented. Increase of the salaries for employees is based on the principles of internal equity and external competitiveness. At the end of 2011, negotiations with the joint representative team of the trade unions were commenced for conclusion of a new collective agreement. Collective Agreement in subsidiary UAB Paslaugos Tau was already signed at the end of the year, and negotiations started in other subsidiary UAB EMAS. Such collective agreements concluded are considered as the guarantee for fulfillment by the employer of its obligations towards the employees.

Continuous improvement of the employees’ qualifications is the priority area of the human resources management. Rich library, computerized Training Center of the Parent Company as well as training policy of the Parent Company ensure good conditions for employee training and professional education.

During 2011, the number of the Group employees who attended the training on formal safety programs amounted to 156; the Parent Company has the license for such trainings issued by the Ministry of Education and Science of the Republic of Lithuania. 400 employees attended trainings on fire safety, 180 employees completed the courses in first aid and hygiene for work under potential exposure to occupational risks.

The Parent Company turns special attention to the continuous improvement of workers’ qualifications to ensure proper servicing by its operational staff of additional process equipment and modernized units. During the year 2011, on-the-job trainings in this relation were attended by 374 employees, while 47 employees have improved their qualifications in execution of specialized works in other training institutions. More than 450 employees participated in trainings on improvement of negotiation skills, quality improvement, as well as in the areas of ecology, occupational health and safety, engineering, finance and accounting, law, computer literacy, internal audit of quality management system, assessment of organizational changes associated risks, identification of potentially explosive atmosphere, health care, etc.

In spring of 2011, the Parent Company completed the leadership training project for top and middle level managers aimed at improvement of the Parent Company’s internal communication and pursuit of the Company’s objectives. Special attention is also given to improvement of foreign language (English, Russian, Lithuania, and Polish) skills and knowledge, with more than 100 employees engaged in the said skills improvement courses. In 2011, the Languages Ambassador of the Year competition organized by the Ministry of Education and Science of the Republic of Lithuania awarded the Parent Company a nomination for strategic learning of languages for work.

Organizational Changes and Restructuring

Performance optimization and labor efficiency increase are considered as the most serious targets to achieve profitability; therefore in 2011 the Group was further executing the process of restructuring.

The Parent Company was further executing the process of restructuring by reducing its non-core activities and outsourcing the relevant services. This way, to facilitate saving of the costs the Parent Company in 2011 refused from further activities of its Non-Destructive Testing Laboratory, outsourced the services of maintenance and repairs of railcars, rolling stock and railways, commenced reorganization in Railway Transport and Infrastructure Section with further intended outsourcing of the rail maneuvering services. Upon implementation of the work organization associated changes, introduction of advanced technical measures and tools, modernization of processes and staff optimization in many organizational units of the Parent Company the labor efficiency increased.

Organizational changes and restructuring allowed for the staff reduction during the last year. The number of the Group active employees reduced by 132, with the total number of 2,508 at the end of 2011.

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 7

Changes in the Group Structure

By the 25 October 2011 Decision of the District Court of the City of Warsaw, Mazeikiu Nafta Trading House Sp. z o.o. in Liquidation was excluded from the National Court Register of Poland upon completion of the liquidation procedures.

Maintaining the Management Systems and their Recerti-fication

Activities of the Parent Company comply with the strict international integrated management system standards implemented by many European companies. In the European business practice, the companies which have introduced ISO 9001 standard are considered as the solid and reliable partners oriented towards the long-term plans and quality instead of pursue of the short-term profitability.

In 2011 the Parent Company further continued improvement of its internal order, implementation of more efficient management followed by better comprehension of the objectives and processes by the employees; but the most important here is the trust of the clients in our products and work quality.

The Parent Company performs continuous maintaining and improvement of its Integrated Management System. In June of 2011, LQRA Ltd successfully completed recertification of the Parent Company’s management system including environmental management, quality management as well as occupational health and safety management, issuing the certificate effective by the 11 July 2014.

Social Responsibility

Having secured one of the leading positions in Lithuanian economy, the Group seeks not only to improve its business results, but also to enhance quality of life of the Group employees and their families as well as communities of Mažeikiai, Biržai Districts, Palanga town as well as the community of Lithuania.

The Parent Company, taking care of the community in line with the provisions of its Social Policy, in cooperation with Mažeikiai District Municipality, granted support for installation of four children playgrounds and ten bus stop shelters in Mažeikiai. The Parent Company has also financed the disabled elderly people nursing services in Mažeikiai District provided by Mažeikiai Branch of the Lithuanian Red Cross Society.

Taking into consideration the needs of local community as well as national culture the Parent Company granted support to the XIII Festival of Wind Instruments in Mažeikiai, Biržai Town Festival, XVII Klaipėda Jazz Festival, as well as became the general sponsor of the 71st season of the Lithuanian National Philharmonic.

The General Assembly of the United Nations proclaimed the year 2011 as the International Year of Chemistry. The Parent Company has joined the initiative with a program propagating chemical science and increasing appreciation in chemistry, patronized by the Lithuanian National Commission for UNESCO. Within the framework of the said program the Parent Company granted support to the 49th Chemistry Olympiad of Lithuanian Secondary School Students as well as for the preparation of school students to the International Junior Science Olympiad in Durban (South Africa) where Lithuanian representatives received silver and bronze medals. In addition, the Parent Company organized ‘Live Chemistry’ days in Mažeikiai and Vilnius presenting the importance of chemistry in daily life and encouraging interest of young people in the sustainable future creating science,

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 8

as well as granted a one-time scholarship to Artūras Katelnikovas, chemistry PhD student of Vilnius University for the light synthesizing research. The Parent Company also granted support to Vilnius University, Kaunas University of Technology and Klaipėda University to facilitate environmental researches and improve the quality of chemistry studies.

Ownership Structure

Shares of the Parent Company are owned by the sole shareholder Polski Koncern Naftowy Orlen S.A. entitled to 100 % of the shares.

In 2011, the Group did not acquire or transfer any of its own shares either.

Branches

The Parent Company has no branches established. The Parent Company has Public Company ORLEN Lietuva Representative Office in Ukraine.

Year 2012 – year of continued labor efficiency improve-ment in all business segments

In the year 2012, the Group will further focus on improvement of labor efficiency in all business segments as well as manpower optimization through the processes of restructuring and elimination of non-core activities. Such arrangements are necessary seeking to ensure the long-term perspective not only for ORLEN Lietuva Group but for the whole PKN Orlen Group under the conditions of increasing competitiveness.

The forecasted throughput of the Parent Company’s Refinery in 2012 is about 9.6 million tons of feedstock.

The Group will further pursue its strategy and the goal of creating shareholder value by becoming the most efficient oil companies in Central and Eastern Europe.

Chairman of the Board of Directors

Ireneusz Fąfara

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 9

Independent auditor’s report to the shareholder of AB ORLEN Lietuva 12Consolidated statement of financial position 13Consolidated statement of comprehensive income 14Consolidated statement of cash flows 15Consolidated statement of changes in equity 16

1. Reporting entity 18

2. Accounting policies 19

2.1. Principles of presentation 19

2.2. Basis of measurement 19

2.3. Impact of amendments and interpretations of IFRSs on consolidated financial statements of the Group 192.3.1. Binding amendments and interpretations to IFRSs 192.3.2. IFRSs and interpretations to IFRSs not yet effective 192.3.3. Functional and presentation currency 23

2.4. Applied accounting policies 242.4.1. Changes in accounting policies and estimates 242.4.2. Transactions in foreign currencies 242.4.3. Principles of consolidation 242.4.4. Investments in subsidiaries 24

2.4.4.1. Investment in associates 242.4.4.2. Consolidation procedures 25

2.4.5. Business combinations 252.4.6. Operating Segments 252.4.7. Property, plant and equipment 262.4.8. Intangible assets 27

2.4.8.1. Goodwill 272.4.8.2. Rights 28

2.4.9. Perpetual usufruct of land 282.4.10. Borrowing cost 292.4.11. Impairment of assets 292.4.12. Inventories 302.4.13. Receivables 302.4.14. Cash and cash equivalents 312.4.15. Non-current assets held for sale 312.4.16. Equity 31

2.4.16.1. Share capital 312.4.16.2. Share premium 312.4.16.3. Revaluation surplus 322.4.16.4. Foreign exchange differences 322.4.16.5. Other reserve capitals 322.4.16.6. Retained earnings 32

2.4.17. Liabilities 322.4.17.1. Government grants 32

2.4.18. Employee benefits: Jubilee bonuses and post-employment benefits 322.4.19. Provisions 33

2.4.19.1. Environmental provision 332.4.19.2. Business risk 332.4.19.3. Restructuring 332.4.19.4. CO2 emissions 332.4.19.5. Accruals 33

2.4.20. Revenue from sale 342.4.20.1. Revenue from sales of finished goods, merchandise, materials and services 34

2.4.21. Costs 342.4.21.1. Cost of sales 342.4.21.2. Distribution expenses 34

Content

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 10

2.4.21.3. General and administrative expenses 342.4.22. Other operating revenue and expenses 34

2.4.22.1. Financial income and expense 352.4.22.2. Income tax expense 352.4.22.3. Earnings per share 36

2.4.23. Consolidated statement of cash flows 362.4.24. Financial instruments 36

2.4.24.1. Recognition and derecognition in the consolidated statement of financial position 362.4.24.2. Measurement of financial assets and liabilities 372.4.24.3. Transfers 382.4.24.4. Impairment of financial assets 38

2.4.25. Lease 392.4.26. Contingent assets and contingent liabilities 402.4.27. Subsequent events after reporting date 40

3. The Management Board estimates and assumptions 40

4. Operating segments 41

4.1. Revenue and financial result by segment 42

4.2. Other segment data 444.2.1. Assets by operating segment 444.2.2. Recognition and reversal of impairment allowances 454.2.3. Geographical information 45

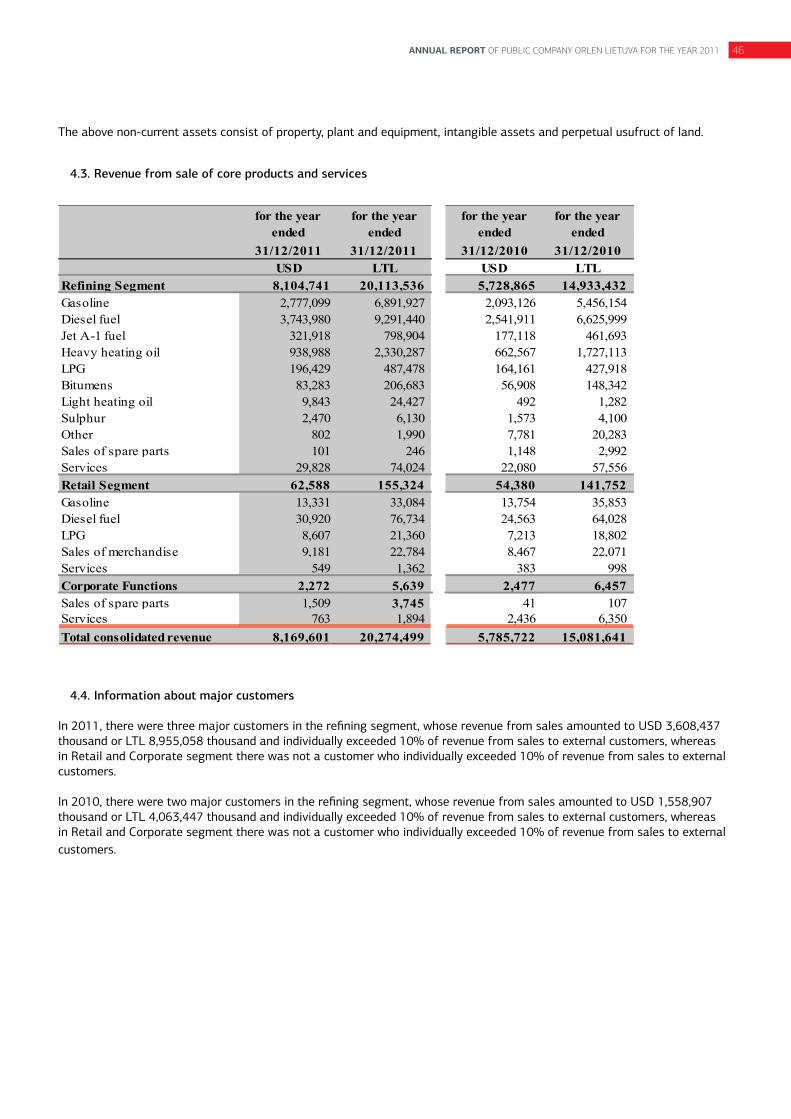

4.3. Revenue from sale of core products and services 46

4.4. Information about major customers 46

5. Property, plant and equipment 47

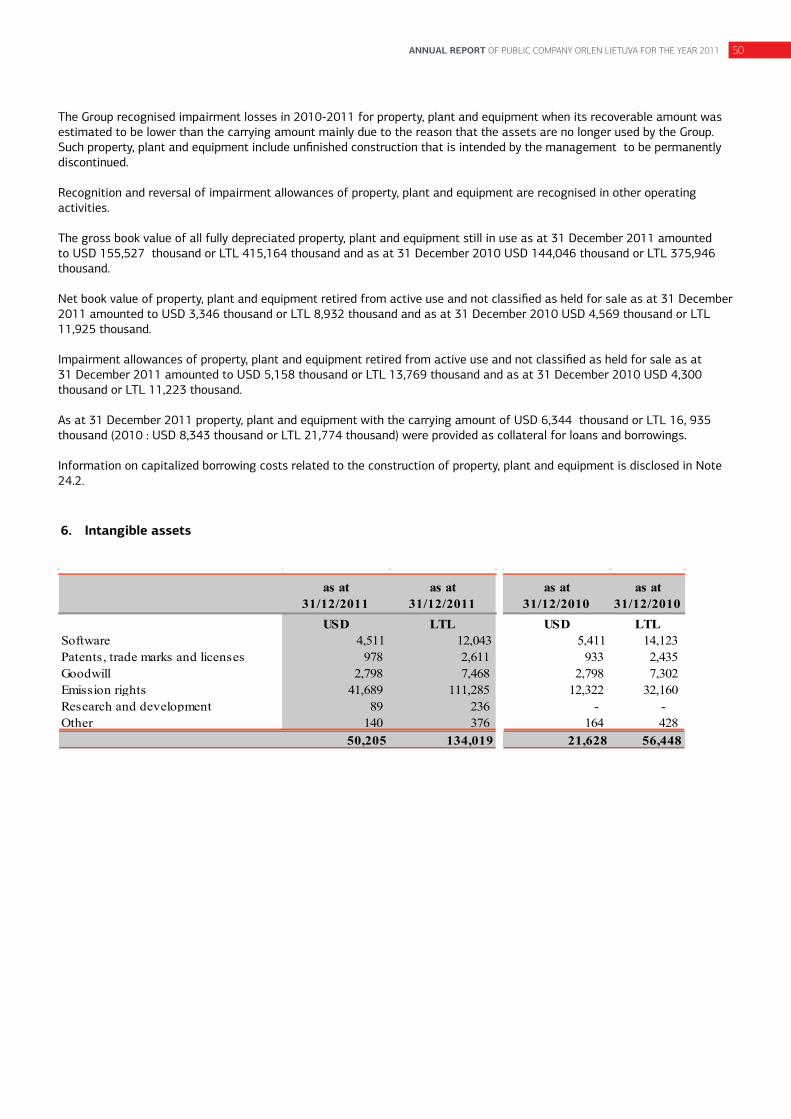

6. Intangible assets 50

7. Perpetual usufruct of land 54

8. Investments into equity-accounted investees 54

9. Inventories 54

10. Trade and other receivables 55

11. Other short-term financial assets 56

12. Cash and cash equivalents 56

13. Non-current assets classified as held for sale 57

14. Share capital 57

15. Earnings per share 58

16. Loans and borrowings 58

17. Long-term employee benefits 61

18. Provisions 62

18.1. Environmental provision 64

18.2. Business risk provision 64

18.3. Restructuring provision 65

18.4. CO2 emission provision 65

19. Trade and other liabilities 66

20. Other financial liabilities 66

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 11

21. Sales revenue 67

22. Operating expenses 67

23. Other operating revenue and expenses 69

23.1. Other operating revenue 69

23.2. Other operating expenses 70

24. Financial revenue and expenses 70

24.1. Financial revenue 70

24.2. Financial expenses 70

25. Income tax expense 71

25.1. The differences between income tax expense recognised in profit or loss and the amount calculated based on profit before tax 71

25.2. Deferred tax 72

25.3. Change in deferred tax assets and liability, net 72

26. Financial instruments 73

26.1. Financial instruments by category and class 73

26.2. Fair value of financial instruments 76

27. Financial risk management 77

28. Capital commitments 83

29. Contingencies 84

30. Guarantees and sureties 85

31. Related party transactions 85

31.1. Information on material related party transactions concluded by the Group on other than market terms 85

31.2. Transactions with members of the Management Board and Supervisory Board, their spouses, siblings, descendants and ascendants and their other relatives 85

31.3. Transactions concluded by the Group with related parties through the key executive personnel 85

31.4. Transactions and balance of settlements of the Group with related parties 85

32. Remuneration together with profit-sharing paid and due or potentially due to Management Board, Supervisory Board and other members of key executive personnel of Parent Company and the Capital Group companies in accordance with IAS 24 86

33. Remuneration arising from the agreement with the entity authorized the conduct audit of the financial statements 87

34. Employment structure 87

35. Significant events after the end of the reporting period 88

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 12

Independent auditor’s report to the shareholder of AB ORLEN Lietuva

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 13

Consolidated statement of financial position

Note

USD LTL USD LTLASSETSNon-current assetsProperty,plant and equipment 5 927,699 2,476,399 988,054 2,578,720 Intangible assets 6 50,205 134,019 21,628 56,448 Perpetual usufruct of land 7 102 271 98 258 Investments into equity-accounted investees 8 1,756 4,689 1,646 4,295 Deferred tax assets 25 64,077 171,045 65,611 171,239 Other investments 1,612 4,302 - - Other non-current assets 2,854 7,617 2,536 6,620 Total non- current assets 1,048,305 2,798,342 1,079,573 2,817,580 Current assetsInventory 9 478,793 1,278,093 446,625 1,165,644 Trade and other receivables 10 265,963 709,962 271,075 707,479 Short term financial assets 11 6,539 17,456 13,002 33,934 Income tax receivable 2,835 7,568 3,453 9,013 Cash and cash equivalents 12 59,704 159,373 34,687 90,530 Non-current assets held for sale 13 5,129 13,690 480 1,254 Total current assets 818,963 2,186,142 769,322 2,007,854

Total assets 1,867,268 4,984,484 1,848,895 4,825,434 LIABILITIES AND SHAREHOLDERS' EQUITYEQUITYShare capital 14 181,886 708,821 181,886 708,821 Share premium 77,507 295,548 77,507 295,548 Other reserves 27,654 74,052 27,662 74,073 Currency translation reserve (607) (205,236) 2,338 (242,489)Retained earnings 462,107 1,124,984 466,334 1,136,421 Total equity 748,547 1,998,169 755,727 1,972,374 LIABILITIESLong-term liabilitiesInterest-bearing loans and borrowings 16 349,608 933,243 164,598 429,584 Employee benefits 17 7,597 20,280 7,359 19,207 Provisions 18 5,987 15,982 3,000 7,829 Deferred tax liabilities 25 1 3 3 9 Total long-term liabilities 363,193 969,508 174,960 456,629 Short-term liabilitiesTrade and other liabilities 19 653,901 1,745,523 724,684 1,891,354 Interest-bearing loans and borrowings 16 48,230 128,744 121,389 316,813 Income tax liability 190 507 - - Provisions 18 47,893 127,846 56,653 147,860 Deferred income 11 30 11 28 Other financial liabilities 20 5,303 14,157 15,471 40,376 Total short-term liabilities 755,528 2,016,807 918,208 2,396,431

Total liabilities 1,118,721 2,986,315 1,093,168 2,853,060

Total equity and liabilities 1,867,268 4,984,484 1,848,895 4,825,434

Ireneusz FąfaraGeneral Director Chief Financial Officer

Consolidated financial statements set out on pages 6 to 85 were approved by the General Director and the ChiefFinancial Officer on 28 March 2012.

as at 31/12/2011 as at 31/12/2010

Jaroslaw Szalinski

Consolidated financial statements set out on pages 13 to 88 were approved by the General Director and the ChiefFinancial Officer on 28 March 2012.

Ireneusz FąfaraGeneral Director

Jaroslaw SzalinskiChief Financial Officer

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 14

Consolidated statement of comprehensive income

Notefor the year

ended 31/12/2011

for the year ended

31/12/2011

for the year ended

31/12/2010

for the year ended

31/12/2010USD LTL USD LTL

Income statementSales revenue 21 8,169,601 20,274,499 5,785,722 15,081,641 Cost of sales 22 (7,927,040) (19,672,536) (5,531,717) (14,419,528)Gross profit on sale 242,561 601,963 254,005 662,113 Distribution expenses 22 (165,763) (411,373) (152,185) (396,701)General and administrative expenses 22 (70,251) (174,342) (73,397) (191,324)Other operating revenue 23 71,743 178,045 24,307 63,360 Other operating expenses 23 (53,076) (131,717) (41,465) (108,086)Profit from operation 25,214 62,576 11,265 29,362 Financial revenue 24 5,460 13,548 1,191 3,104 Financial expenses 24 (33,847) (83,999) (29,806) (77,697)Financial revenue and expenses (28,387) (70,451) (28,615) (74,593)Share of profit of equity-accounted investees

8 160 398 149 387

Profit/(loss) before tax (3,013) (7,477) (17,201) (44,844)Income tax expense 25 (2,571) (6,381) (14,218) (37,063)Net profit/(loss) (5,584) (13,858) (31,419) (81,907)

Items of other comprehensive income/(expenses):Foreign exchange differences on consolidation (1,596) 39,653 (3,265) 153,184

(1,596) 39,653 (3,265) 153,184

Total net comprehensive income/(expenses) (7,180) 25,795 (34,684) 71,277

Net profit/(loss) attributable to:equity holders of the parent (5,584) (13,858) (31,419) (81,907)

Total comprehensive income/(expenses) attributable to:

equity holders of the parent (7,180) 25,795 (34,684) 71,277

Net profit/(loss) per share attributable to equity holders of the parent

15 (0.01) (0.02) (0.04) (0.12)

Ireneusz Fąfara Jaroslaw SzalinskiGeneral Director Chief Financial Officer

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 15

Consolidated statement of cash flows

Notefor the year

ended 31/12/2011

for the year ended

31/12/2011

for the year ended

31/12/2010

for the year ended

31/12/2010USD LTL USD LTL

Cash flow - operating activitiesNet profit/(loss) (5,584) (13,858) (31,419) (81,907)Adjustments for:Share in profit/(loss) from investments accounted under equity method

8 (160) (398) (149) (387)

Depreciation and amortisation 5,6,7 79,510 197,319 92,538 241,218 Foreign exchange (gain)/loss (1,270) 27,541 2,101 52,328 Interest expenses 24 13,885 34,460 21,296 55,511 (Profit)/loss on investing activities 31,159 78,364 17,470 45,539 Change in receivables 4,668 (3,790) (83,574) (257,760)Change in inventories (28,570) (104,492) (59,210) (232,514)Change in liabilities (82,242) (178,886) 275,651 808,715 Change in provisions 41,133 105,973 47,057 132,743 Income tax expense 25 2,571 6,381 14,218 37,063 Income tax (paid)/received (1,515) (3,760) (1,139) (2,969)Emission rights recognised at fair value 6 (47,646) (118,243) (43,099) (112,347)Net cash provided by operating activities 5,939 26,611 251,741 685,233 Cash flows - investing activitiesAcquisition of property, plant and equipment and intangible assets (68,407) (169,766) (60,787) (158,454)Disposal of property, plant and equipment and intangible assets

5,6,7 319 791 40,965 106,784

Disposal of shares 229 568 - - Acquisition of sharesDerivatives (1,255) (3,350) - - Increase/(decrease) in deposits 5,604 13,907 (11,429) (29,792)Interest received 865 2,147 1,032 2,689 Net cash (used in) investing activities (62,645) (155,703) (30,219) (78,773)Cash flows - financing activitiesProceeds from loans and borrowings 1,220,487 3,028,883 1,976,721 5,152,719 Repayment of loans and borrowings (1,108,053) (2,749,855) (2,287,655) (5,963,232)Interest paid (14,983) (37,183) (22,916) (59,734)(Outflow)/inflow from cash pool (15,190) (39,635) 15,350 40,061 Net cash (used in) financing activities 82,261 202,210 (318,500) (830,186)

Net (decrease)/increase in cash and cash equivalents

25,555 73,118 (96,978) (223,726)

Effect of exchange rate changes (538) (4,275) (1,944) (7,101) Cash and cash equivalents, beginning of the period 12 34,687 90,530 133,609 321,357

Cash and cash equivalents, end of the period 12 59,704 159,373 34,687 90,530

Ireneusz Fąfara Jaroslaw SzalinskiGeneral Director Chief Financial Officer

791

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 16

Consolidated statement of changes in equity

USD

Share capital

Share premium

Revaluation reserve

Other reserve capitals

Foreign exchange

differences

Retained earnings

Total equity

1 January 2011 181,886 77,507 109 27,553 2,338 466,334 755,727 Loss for the year - - - - - (5,584) (5,584)Transfer of cumulative translation differences after liquidation of subsidiary

- - - - 278 (278) -

Transfer of cumulative result of the previous year by way of dividends

- - - - (1,627) 1,627 -

Foreign currency translation differences of foreign operations

- - - - (1,596) - (1,596)

Total comprehensive income/(expenses)

- - - - (2,945) (4,235) (7,180)

Transfer from legal reserve - - - (8) - 8 - Transactions with owners in their capacity as owners - - - (8) - 8 -

31 December 2011 181,886 77,507 109 27,545 (607) 462,107 748,547

1 January 2010 181,886 77,507 109 27,526 4,788 498,595 790,411 Loss for the year - - - - - (31,419) (31,419)Transfer of cumulative translation differences after liquidation of subsidiary

- - - - 19 (19) -

Transfer of cumulative result of the previous year by way of dividends

- - - - 796 (796) -

Foreign currency translation differences of foreign operations

- - - - (3,265) - (3,265)

Total comprehensive income/(expenses) - - - - (2,450) (32,234) (34,684)

Transferred to legal reserve - - - 27 - (27) - Transactions with owners in their capacity as owners - - - 27 - (27) -

31 December 2010 181,886 77,507 109 27,553 2,338 466,334 755,727

Ireneusz Fąfara Jaroslaw SzalinskiGeneral Director Chief Financial Officer

Equity attributable to equity holders of the parent

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 17

LTL Equity attributable to equity holders of the parent

Share capital

Share premium

Revaluation reserve

Other reserve capitals

Foreign exchange

differences

Retained earnings

Total equity

1 January 2011 708,821 295,548 437 73,636 (242,489) 1,136,421 1,972,374 Loss for the year - - - - - (13,858) (13,858)Transfer of cumulative translation differences after liquidation of subsidiary

- - - - 595 (595) -

Transfer of cumulative result of the previous year by way of dividends

- - - - (2,995) 2,995 -

Foreign currency translation differences of foreign operations

- - - - 39,653 - 39,653

Total comprehensive income/(expenses) - - - - 37,253 (11,458) 25,795

Transferred from legal reserve

- - - (21) - 21 -

Transactions with owners in their capacity as owners - - - (21) - 21 -

31 December 2011 708,821 295,548 437 73,615 (205,236) 1,124,984 1,998,169

1 January 2010 708,821 295,548 437 73,565 (397,722) 1,220,448 1,901,097 Loss for the year - - - - - (81,907) (81,907)Transfer of cumulative translation differences after liquidation of subsidiary

- - - - 50 (50) -

Transfer of cumulative result of the previous year by way of dividends

- - - - 1,999 (1,999) -

Foreign currency translation differences of foreign operations

- - - - 153,184 - 153,184

Total comprehensive income/(expenses) - - - - 155,233 (83,956) 71,277

Transferred to legal reserve - - - 71 - (71) - Transactions with owners in their capacity as owners

- - - 71 - (71) -

31 December 2010 708,821 295,548 437 73,636 (242,489) 1,136,421 1,972,374

Ireneusz Fąfara Jaroslaw SzalinskiGeneral Director Chief Financial Officer

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 18

Accounting policies, notes and other supplementary information

1. Reporting entity

Public Company ORLEN Lietuva (hereinafter – the Parent company) is incorporated and domiciled in Lithuania. Its registered office is located at the address: Mažeikių St. 75, Juodeikiai village, Mazeikiai District, Republic of Lithuania. The Parent company comprises an oil refinery enterprise in Mažeikiai operating since 1980, the Būtingė terminal operating since 1999, and an oil products pumping station in Biržai operating since 1970. The sole shareholder of the Parent company is PKN ORLEN S.A.

The consolidated financial statements as at 31 December 2011 include the Parent company and subsidiary companies. The Parent company also prepares separate financial statements.

The Consolidated group (hereinafter “the Group”) consists of the Parent company and its seven subsidiaries (eight subsidiaries in 2010). The Group has one associate which is accounted for using the equity method. The subsidiaries and the associate included into the Group’s consolidated financial statements are listed below:

31/12/2011 31/12/2010

SubsidiariesAB Ventus nafta Lithuania 2002 100 100 Retail trade in petroleum products.

SIA ORLEN Latvija Latvia 2003 100 100

Wholesale trading in petroleum productsin Latvia. This company is a subsidiary ofUAB Mažeikių Naftos prekybos namaiwhich holds 100 percent of shares of thiscompany. SIA Mazeikiu NaftaTirdcniecibas Nams changed the name toSIA ORLEN Latvija in December 2011.

OU ORLEN Eesti Estonia 2003 100 100

Wholesale trading in petroleum productsin Latvia. This company is a subsidiary ofUAB Mažeikių Naftos prekybos namaiwhich holds 100 percent of shares of thiscompany. OU Mazeikiu Nfta TradingHouse changed the name to OU ORLENEesti in December 2011.

Sp.z.o.o. Mazeikiu Nafta Trading House

Poland 2003 0 100 The company was liquidated in November 2011.

UAB Mažeikių Naftos sveikatos priežiūros centras

Lithuania 2007 100 100Provides services in relation to healthcare, training, hygienic assessment ofwork places and other related services.

UAB Paslaugos tau Lithuania 2008 100 100 Cleaning of premises, maintenance ofterritory.

UAB EMAS Lithuania 2009 100 100 Installation, supervision, repair ofelectrical equipment and related services.

Associated company

UAB Naftelf Lithuania 1996 34 34Trading in aviation fuel and constructionof storage facilities thereof.

100

It has two subsidiaries SIA ORLENLatvija and OU ORLEN Eesti. Theiractivity is wholesale trading in petroleumproducts in Latvia and Estonia.

UAB Mažeikių Naftos prekybos namai

Lithuania 2003 100

Year of establishment/

acquisition Nature of activity

Share of the Group (% )Subsidiary/associated

companyEstablished

in

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 19

2. Accounting policies

2.1. Principles of presentation

The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) adopted by the European Union (EU). The consolidated financial statements cover the period from 1 January to 31 December 2011 and the comparative period from 1 January to 31 December 2010.

Presented consolidated financial statements are compliant with all requirements of IFRSs adopted by the EU and present a true and fair view of the Group’s financial position as at 31 December 2011 and comparative data as at 31 December 2010, results of its operations and cash flows for the year ended 31 December 2011 and comparative data as at 31 December 2010.

The consolidated financial statements have been prepared assuming that the Group will continue to operate as a going concern in the foreseeable future. As at the date of approval of these consolidated financial statements there is no evidence indicating that the Group will not be able to continue its operations as a going concern.

The foregoing financial statements, except for cash flow statement, have been prepared using the accrual basis of accounting.

The consolidated financial statements were authorized for issue by the General Director on 28 March 2012.

2.2. Basis of measurement

The consolidated financial statements have been prepared on the historical cost basis except for the following items in the statement of financial position:

• Derivative financial instruments are measured at fair value;• Non-derivative financial instruments at fair value through profit or loss are measured at fair value.

2.3. Impact of amendments and interpretations of IFRSs on consolidated financial statements of the Group

2.3.1. Binding amendments and interpretations to IFRSs

The amendments adopted from 1 January 2011 had no impact on the foregoing consolidated financial statements.

2.3.2. IFRSs and interpretations to IFRSs not yet effective

The Group intends to adopt amendments to IFRSs that are published but not effective as at 31 December 2011, in accordance with their effective date. In the current reporting period the Group did not make decision to voluntary early adopt amendments and interpretations to standards.

IFRSs and interpretations to IFRSs adopted by EU

Amendments to IFRS 7 Disclosures - Transfers of Financial Assets

The Amendments require disclosure of information that enables users of financial statements:• to understand the relationship between transferred financial assets that are not derecognised in their entirety and the

associated liabilities; and • to evaluate the nature of, and risks associated with, the Group’s continuing involvement in derecognised financial assets.

The Amendments define “continuing involvement” for the purposes of applying the disclosure requirements.

Effective date for periods beginning is the date of 1 July 2011 or after that date

The Group does not expect the amendment to IFRS 7 to have material impact on the consolidated financial statements, because of the nature of the Group’s operations and the types of financial assets that it holds.

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 20

Standards and interpretations waiting for approval of EU

Amendments to IFRS 7 Financial Instruments: Disclosures - Offsetting Financial Assets and Financial Liabilities

The Amendments contain new disclosure requirements for financial assets and liabilities that are:• offset in the statement of financial position; or• subject to master netting arrangements or similar agreements.

Effective date for periods beginning is the date of 1 July 2013 or after that date

The Group does not expect the Amendments to have any impact on the consolidated financial statements since it does not apply offsetting to any of its financial assets and financial liabilities and it has not entered into master netting arrangements.

New standard and additions – IFRS 9 Financial Instruments

The new Standard replaces the guidance in IAS 39, Financial Instruments: Recognition and Measurement, about classification and measurement of financial assets. The Standard eliminates the existing IAS 39 categories of held to maturity, available for sale and loans and receivable.

Financial assets will be classified into one of two categories on initial recognition: financial assets measured at amortized cost; or financial assets measured at fair value.

The 2010 additions to IFRS 9 replace the guidance in IAS 39 Financial Instruments: Recognition and Measurement, about classification and measurement of financial liabilities and the derecognition of financial assets and financial liabilities.

The Standard retains almost all of the existing requirements from IAS 39 on the classification and measurement of financial liabilities and for derecognition of financial assets and financial liabilities.

The Standard requires that the amount of change in fair value attributable to changes in the credit risk of a financial liability designated at initial recognition as fair value through profit or loss, be presented in other comprehensive income (OCI), with only the remaining amount of the total gain or loss included in profit or loss. However, if this requirement creates or enlarges an accounting mismatch in profit or loss, then the whole fair value change is presented in profit or loss.

Amounts presented in OCI are not subsequently reclassified to profit or loss but may be transferred within equity.

Derivative financial liabilities that are linked to and must be settled by delivery of an unquoted equity instrument whose fair value cannot be reliably measured, are required to be measured at fair value under IFRS 9.

Moreover, amendments change the disclosure and restatement requirements relating to the initial application of IFRS 9 Financial Instruments (2009) and IFRS 9 (2010).

The amended IFRS 7 requires to disclose more details about the effect of the initial application of IFRS 9 when the Group does not restate comparative information in accordance with the amended requirements of IFRS 9.

Effective date of IFRS 9 and its additions for periods beginning is the date of 1 January 2015 or after that date

The Group does not expect IFRS 9 to have material impact on the consolidated financial statements. The classification and measurement of the Group’s financial liabilities are not expected to change under IFRS 9 because of the nature of the Group’s operations and the types of financial assets that it holds.

New Standard – IFRS 10 Consolidated Financial Statements

IFRS 10 provides a new single model to be applied in the control analysis for all investees, including entities that currently are SPEs in the scope of SIC-12. IFRS 10 introduces new requirements to assess control that are different from the existing requirements in IAS 27 (2008). Under the new single control model, an investor controls an investee when: • it is exposed or has rights to variable returns from its involvements with the investee, • has the ability to affect those returns through its power over that investee and • there is a link between power and returns.

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 21

The new standard also includes the disclosure requirements and the requirements relating to preparation of consolidated financial statements. These requirements are carried forward from IAS 27 (2008).

Effective date for periods beginning is the date of 1 January 2013 or after that date.

The Group does not expect the new standard to have any impact on the consolidated financial statements, since the assessment of control over its current investees under the new standard is not expected to change the conclusion regarding the Group’s control over its investees.

New Standard – IFRS 11 Joint arrangements

IFRS 11, Joint Arrangements, supersedes and replaces IAS 31, Interest in Joint Ventures. IFRS 11 does not introduce substantive changes to the overall definition of an arrangement subject to joint control, although the definition of control, and therefore indirectly of joint control, has changed due to IFRS 10.

Under the new Standard, joint arrangements are divided into two types, each having its own accounting model defined as follows:• A joint operation is one whereby the jointly controlling parties, known as the joint operators, have rights to the assets, and

obligations for the liabilities, relating to the arrangement.• A joint venture is one whereby the jointly controlling parties, known as joint venturers, have rights to the net assets of the

arrangement.

IFRS 11 effectively carves out, from IAS 31 jointly controlled entities, those cases in which although there is a separate vehicle, that separation is ineffective in certain ways. These arrangements are treated similarly to jointly controlled assets/operations (line by line accounting of underlying assets and liabilities), and are now called joint operations. The remainder of IAS 31 jointly controlled entities, now called joint ventures, are stripped of the free choice of equity accounting or proportionate consolidation; they must now always use the equity method.

Effective date for periods beginning is the date of 1 January 2013 or after that date.

The Group does not expect IFRS 11 to have material impact on the consolidated financial statements since it is not a party to any joint arrangements.

New Standard – IFRS 12 Disclosure of interests in other entities

IFRS 12 requires additional disclosures relating to significant judgments and assumptions made in determining the nature of interests in an entity or arrangement, interests in subsidiaries, joint arrangements and associates and unconsolidated structured entities.

Effective date for periods beginning is the date of 1 January 2013 or after that date.The Group does not expect IFRS 12 to have material impact on the consolidated financial statements.

New Standard – IFRS 13 Fair value measurement

IFRS 13 replaces the fair value measurement guidance contained in individual IFRSs with a single source of fair value measurement guidance. It defines fair value, establishes a framework for measuring fair value and sets out disclosure requirements for fair value measurements. IFRS 13 explains ‘how’ to measure fair value when it is required or permitted by other IFRSs. IFRS 13 does not introduce new requirements to measure assets or liabilities at fair value, nor does it eliminate the practicability exceptions to fair value measurements that currently exist in certain standards.

The standard contains an extensive disclosure framework that provides additional disclosures to existing requirements to provide information that enables financial statement users to assess the methods and inputs used to develop fair value measurements and, for recurring fair value measurements that use significant unobservable inputs, the effect of the measurements on profit or loss or other comprehensive income.

Effective date for periods beginning is the date of 1 January 2013 or after that date.

The Group does not expect IFRS 13 to have material impact on the consolidated financial statements since management

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 22

considers the methods and assumptions currently used to measure the fair value of assets to be consistent with IFRS 13.

Amendments to IAS 1 Presentation of Items of Other Comprehensive Income

The amendments require that an entity present separately the items of OCI that may be reclassified to profit or loss in the future from those that would never be reclassified to profit or loss. Consequently an entity that presents items of OCI before related tax effects will also have to allocate the aggregated tax amount between these sections.

Effective date for periods beginning is the date of 1 July 2012 or after that date.

The change is not expected to have significant impact on the consolidated financial statements of the Group.

Amendments to IAS 12 Income taxes - Deferred Tax: Recovery of Underlying Assets

The 2010 amendment introduces an exception to the current measurement principles based on the manner of recovery in paragraph 52 of IAS 12 for investment property measured using the fair value model in accordance with IAS 40 by introducing a rebuttable presumption that in these for the assets the manner of recovery will be entirely by sale. Management’s intention would not be relevant unless the investment property is depreciable and held within a business model whose objective is to consume substantially all of the asset’s economic benefits over the life of the asset. This is the only instance in which the rebuttable presumption can be rebutted.

Effective date for periods beginning is the date of 1 January 2012 or after that date.

The amendments are not relevant to the Group’s consolidated financial statements, since the Group does not have any investment properties measured using the fair value model in IAS 40.

Amended to IAS 19 Employee Benefits

Actuarial gains and losses will be recognised immediately in other comprehensive income. This change will:• remove the corridor method and hence is expected to have a significant effect on entities that currently apply this method

to recognise actuarial gains and losses; and • eliminate the ability for entities to recognise all changes in the defined benefit obligation and in plan assets in profit or loss,

which currently is allowed under IAS 19.

Effective date for periods beginning is the date of 1 January 2013 or after that date.

The Group does not expect that the amendments have material impact on the consolidated financial statements.

Amended IAS 28 Investments in associates and joint ventures

There are limited amendments made to IAS 28 (2008): • Associates and joint ventures held for sale. IFRS 5 Non-current Assets Held for Sale and Discontinued Operations applies

to an investment, or a portion of an investment, in an associate or a joint venture that meets the criteria to be classified as held for sale. For any retained portion of the investment that has not been classified as held for sale, the equity method is applied until disposal of the portion held for sale. After disposal, any retained interest is accounted for using the equity method if the retained interest continues to be an associate or a joint venture.

• Changes in interests held in associates and joint ventures. Previously, IAS 28 (2008) and IAS 31 specified that the cessation of significant influence or joint control triggered remeasurement of any retained stake in all cases, even if significant influence was succeeded by joint control. IAS 28 (2011) now requires that in such scenarios the retained interest in the investment is not remeasured.

• Effective date for periods beginning is the date of 1 January 2013 or after that date.

It is expected that the standard, when initially applied, will have a significant impact on the consolidated financial statements. However, the Group is not able to prepare an analysis of the impact this will have on the consolidated financial statements until the date of initial application.

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 23

Amendments to IAS 32 Financial Instruments: Presentation - Offsetting Financial Assets and Financial Liabilities

The Amendments do not introduce new rules for offsetting financial assets and liabilities; rather they clarify the offsetting criteria to address inconsistencies in their application.

The Amendments clarify that an entity currently has a legally enforceable right to set-off if that right is:• not contingent on a future event; and • enforceable both in the normal course of business and in the event of default, insolvency or bankruptcy of the entity and

all counterparties.

Effective date for periods beginning is the date of 1 January 2014 or after that date.

The Group does not expect the Amendments to have any impact on the consolidated financial statements since it does not apply offsetting to any of its financial assets and financial liabilities and it has not entered into master netting arrangements.

IFRIC Interpretation 20: Stripping Costs in the Production Phase of a Surface Mine

The Interpretation addresses the following issues:• recognition of production stripping costs as an asset;• initial measurement of the stripping activity asset; and• subsequent measurement of the stripping activity asset.

Surface mining companies will capitalize production stripping costs that benefit future periods, if certain criteria are met. Capitalization, and the deprecation period, will depend on the identified component of the ore body to which the stripping activity relates.

Effective date for periods beginning is the date of 1 January 2013 or after that date.

The IFRIC is not relevant to the Group’s financial statements, since the Group does not incur any stripping costs in the production phase of a surface mine.

2.3.3. Functional and presentation currency

Items included in the financial statements of each of the Group’s entities are measured using the currency of the primary economic environment in which the entity operates (the ‘functional currency’). The functional currency of the Parent Company is the US dollar (USD) as it mainly influences sales prices for goods and services and material costs, the funds from financing activities are mainly generated in the USD and the Group retains the major part of receipts from its operating activities in the USD. A significant portion of the Group’s business is conducted in US dollars and management uses the USD to manage business risks and exposures and to measure performance of the business.

The consolidated financial statements are presented in US dollars, which is the Parent Company’s functional currency, and, due to the requirements of the laws of the Republic of Lithuania, also in Lithuanian Litas (LTL) being an additional presentation currency. Since 2 February 2002 the exchange rate of the Litas has been pegged to the euro at a rate of LTL 3.4528 = EUR 1.

CURRENCIES31/12/2011 31/12/2010 31/12/2011 31/12/2010

LTL/USD 2.48170 2.60670 2.6694 2.6099EUR/USD 0.71875 0.75495 0.7731 0.7559LVL/USD 0.50765 0.53505 0.5401 0.5365PLN/USD 2.95005 3.01210 3.4002 2.9944

average exchange ratefor the reporting period

exchange rateat the end of the reporting period

The consolidated financial statements of the Group, prepared in US dollars, the functional currency of the Parent Company, are translated to the presentation currency, Lithuanian Litas by using period end exchange rate for translation of assets and liabilities and average exchange rate for the year for translation of income and expenses (unless this average is not a reasonable approximation of the cumulative effect of the rates prevailing on the transaction dates, in which case income and expenses are translated at rates prevailing at the dates of the transactions). All resulting exchange differences are recognized as cumulative translation adjustments in other comprehensive income.

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 24

Accounting policies for foreign currency transactions are disclosed in Note 2.4.2.

2.4. Applied accounting policies

2.4.1. Changes in accounting policies and estimates

The Group will change an accounting policy only if the change:is required by an IFRS; orresults in the consolidated financial statements providing reliable and more relevant information about the effects of transactions, other events or conditions on the Group’s financial position, financial performance or cash flows.

In case of change in accounting policy it is assumed that the new policy had always been applied. The amount of the resulting adjustment is made to the equity. For comparability, the Group adjust the comparative information for the earliest prior period presented as if the new accounting policy had always been applied, unless it is impracticable to determine either the period-specific effects or the cumulative effect of the change.

An estimate may need revision if changes occur in the circumstances on which the estimate was based or as a result of new information or more experience.

2.4.2. Transactions in foreign currencies

A foreign currency transaction is recorded, on initial recognition in the functional currency, by applying to the foreign currency amount the spot exchange rate between the functional currency and the foreign currency at the date of the transaction.

At the end of each reporting period:1. foreign currency monetary items, including units of currency held by the Group and receivables and liabilities due in a defined or definable units of currency are translated using the closing rate, i.e. the spot rate at the end of the reporting period;non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rate at the date of the transaction; andnon-monetary items that are measured at fair value in a foreign currency are translated using the exchange rates at the date when the fair value was determined.

Exchange differences arising on the settlement of monetary items or on translating monetary items at rates different from those at which they were translated on initial recognition during the period or in previous consolidated financial statements are recognised by the Group in profit or loss in the period in which they arise.

2.4.3. Principles of consolidation

The consolidated financial statements of the Group comprise the financial statements of Public Company ORLEN Lietuva and its subsidiaries prepared as at the end of the same reporting period using uniform accounting principles in relation to similar transactions and other events in similar circumstances.

2.4.4. Investments in subsidiaries

Subsidiaries are entities under the Parent’s control. Control is the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities. It is assumed that the Parent Company controls another entity if it holds directly or indirectly – through its subsidiaries – more than 50% of the voting rights in an entity, unless in exceptional circumstances, it can be clearly demonstrated that such ownership does not constitute control. Control also exists when the Parent Company owns half or less of the voting power of an entity when there is:• power over more than half of the voting rights by virtue of an agreement with other investors,• power to govern the financial and operating policies of the entity under a statute or an agreement,• power to appoint or remove the majority of the members of the board of directors or equivalent governing body and control

of the entity is by that board or body, or• power to cast the majority of votes at meetings of the board of directors or equivalent governing body and control of the

entity is by that board or body.• Subsidiaries are consolidated from the date control commences to the date control ceases.

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 25

2.4.4.1. Investment in associates

Investments in associates (entities over which the investor has significant influence and that are neither controlled nor jointly controlled) are accounted for using the equity method, based on financial statements of associates prepared as at the end of same reporting period as separate financial statements of the Parent Company and using uniform accounting principles in relation to similar transactions and other events in similar circumstances.

It is assumed that the Investor has significant influence over another entity, if it has ability to participate in financial and operating decisions of the entity. Particularly, the significant influence is evidenced when the Group holds directly or indirectly more than 20%, and no more than 50% of the voting rights of an entity and participation in financial and operating decisions is not contractually or actually restrained and is actually executed.

2.4.4.2. Consolidation procedures

The consolidated financial statements are prepared using the line by line method and the proportionate method. When investor has significant influence over another entity, equity method is used to evaluate shares in entity.

Consolidated financial statements are the financial statements of a Group presented as those of a single economic entity.

In preparing consolidated financial statements using line by line method, an entity combines the financial statements of the Parent Company and its subsidiaries line by line by adding together like items of assets, liabilities, equity, income and expenses and then performs adequate consolidation procedures, including eliminations. Intra-group balances, revenue and expenses, as well as unrealized profits and losses and cash flows from intra-group transactions are eliminated. Unrealized losses are eliminated after assets, to which they relate are tested for impairment. Unrealized profits and losses are settled proportionately with non-controlling interest.

In line by line method the following steps are then taken: the carrying amount of the Parent’s investment in each subsidiary and the Parent’s portion of equity of each subsidiary are eliminated,intra group balances are eliminated,unrealized profits or losses from intra group transactions are eliminated,intra group revenue and expenses are eliminated.

Under the equity method, the investment in an associate is initially recognised at cost and the carrying amount is increased or decreased to recognise the investor’s share of the profit or loss of the investee after the date of acquisition. The investor’s share of the profit or loss of the investee is recognised in the investor’s profit or loss. Distributions received from an investee reduce the carrying amount of the investment. Adjustments to the carrying amount may also be necessary for a change in the investor’s proportionate interest in the investee arising from changes in the investee’s other comprehensive income. Such changes include those arising from the revaluation of property, plant and equipment and from foreign exchange translation differences. The investor’s share of those changes is recognised in other comprehensive income of the investor.

2.4.5. Business combinations

The Group accounts for each business combination by applying the acquisition method. Applying the acquisition method requires:identifying the acquirer,determining the acquisition date,recognising and measuring the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquire, andrecognising and measuring goodwill or a gain from a bargain purchase.

The fair value of assets, liabilities and contingent liabilities for the purpose of allocating the acquisition cost is determined in accordance with principles set in attachment B to IFRS 3.

2.4.6. Operating Segments

An operating segment is a component of the Group: that engages in business activities from which it may earn revenue and incur expenses (including revenue and expenses relating to transactions with other components of the same group),whose operating results are regularly reviewed by the Group’s chief operating decision maker to make decisions about resources to be allocated to the segment and assess its performance, andfor which discrete financial information is available.

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 26

The operations of the Group were divided into following segments:the refining segment, which includes refinery products processing and wholesale, oil production and sale as well as supporting production, corporate functions which are reconciling item and include activities related to management and administration and other support functions as well as remaining activities not allocated to separate segments.

Segment revenue are revenue reported in the statement of comprehensive income that are directly attributable to a segment and the relevant portion of revenue that can be allocated on a reasonable basis to a segment, including revenue from sales to external customers and revenue from transactions with other segments.

Segment expenses are expenses resulting from the operating activities of a segment that are directly attributable to the segment and the relevant portion of the Group’s expenses that can be allocated on a reasonable basis to a segment, including expenses relating to sales to external customers and expenses relating to transactions with other segments.

Segment expenses do not include:income tax expense,interest, including interest incurred on advances or loans from other segments, unless the segment’s operations are primarily of a financial nature,losses on sales of investments or losses on extinguishment of debt unless the segment’s operations are primarily of a financial nature,

Segment result is calculated on the level of operating result.

Segment assets are those operating assets that are employed by that segment in operating activity and that are either directly attributable to the segment or can be allocated to the segment on a reasonable basis. Particularly segment assets do not include assets connected with income tax.

The revenue, result, assets of a given segment are defined before inter-segment adjustments are made, after adjustments within a given segment.

2.4.7. Property, plant and equipment

Property, plant and equipment are assets that:are held for use in the production or supply of goods or services, for rental to others, or for administrative purposes, andare expected to be used during more than one period (one year or the operating cycle, if longer than one year).

Property, plant and equipment include both fixed assets (assets that are in the condition necessary for them to be capable of operating in the manner intended by management) and construction in progress (assets that are in the course of construction or development necessary for them to be capable of operating in the manner intended by management).

Property, plant and equipment are initially stated at cost. The cost of an item of property, plant and equipment comprises its purchase price, including any costs directly attributable to bringing the asset into use. The cost of an item of property, plant and equipment includes also the initial estimate of the costs of dismantling and removing the item and restoring the site on which it is located, the obligation for which is connected with acquisition or construction of an item of property, plant and equipment.

Property, plant and equipment are stated in the statement of financial position prepared at the end of the reporting period at the carrying amount. The carrying amount is the amount at which an asset is initially recognised (cost) after deducting any accumulated depreciation and accumulated impairment losses.

Depreciation of an item of property, plant and equipment begins when it is available for use, i.e. when it is in the location and condition necessary for it to be capable of operating in the manner intended by management, over the period reflecting its estimated economic useful life, considering the residual value. Fixed assets are depreciated with straight-line method and in justified cases units of production method of depreciation. Each part of an item of property, plant and equipment with a cost that is significant in relation to the total cost of the item is depreciated separately over the period reflecting its economic useful life.

The depreciable amount of an asset is determined after deducting its residual value from the initial value.

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 27

The following standard economic useful lives are used for property, plant and equipment:

• buildings and constructions 10-80 years• machinery and equipment 4-60 years• Vehicles and other 2-20 years

Appropriateness of the applied depreciation rates is reviewed periodically (at least once a year). The adjustments are accounted for prospectively.

The cost of significant repairs and regular maintenance programs is recognised as property, plant and equipment and depreciated in accordance with their economic useful lives. The cost of current maintenance of property, plant and equipment is recognised as an expense when it is incurred.

The Group reviews (once a year) the residual value of property, plant and equipment. Property, plant and equipment are tested for impairment, when there are indicators or events that may imply that the carrying amount of those assets may not be recoverable.

2.4.8. Intangible assets

An intangible asset is an identifiable non-monetary asset without physical substance.

An asset is identifiable if it either:is separable, i.e. is capable of being separated or divided from the Group and sold, transferred, licensed, rented or exchanged, either individually or together with a related contract, identifiable asset or liability, arises from contractual or other legal rights, regardless of whether those rights are transferable or separable from the Group.

An intangible asset is recognised if, and only if: it is probable that the expected future economic benefits that are attributable to the asset will flow to the Group; andthe cost of the asset can be measured reliably.

If the definition criteria of an intangible asset are not met, the cost incurred to acquire or self-develop an asset are recognised in profit or loss when incurred.

An intangible asset is measured initially at cost. An intangible asset that is acquired in a business combination is recognised initially at fair value.

After initial recognition, an intangible asset is presented in the statement of financial position at its net carrying amount.

Intangible assets with finite useful life are amortised using straight-line method. Amortisation begins when the asset is available for use, i.e. when it is in the location and condition necessary for it to be capable of operating in the manner intended by management. The asset is amortised over the period reflecting its estimated useful life. The amortisation period and the amortisation method are reviewed periodically (at least at each financial year-end). The changes are reflected in the future accounting periods (prospectively).

The depreciable amount of an asset with a finite useful life is determined after deducting its residual value. Excluding particular cases, the residual value of an intangible asset with a finite useful life is assumed to be zero.

The following standard economic useful lives are used for intangible assets:

• Licenses, patents and similar 2–15 years• Software 2–10 years

Intangible assets with an indefinite useful life are not amortised. Their value is decreased by the impairment allowances, if any. Additionally, the useful life of an intangible asset that is not being amortised is reviewed each period to determine whether events and circumstances continue to support an indefinite useful life assessment for that asset.

2.4.8.1. Goodwill

Goodwill acquired in a business combination , from the acquisition date, is allocated to each of the acquirer’s cash-generating units, (or groups of cash-generating units), that is expected to benefit from the synergies of the combination, irrespective of

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 28

whether other assets or liabilities of the acquiree are assigned to those units or groups of units.

The acquirer recognises goodwill as of the acquisition date measured as the excess of a) over b) below:a) the aggregate of: the consideration transferred, which generally requires acquisition-date fair value; the amount of any non-controlling interest in the acquiree; and in a business combination achieved in stages, the acquisition-date fair value of the acquirer’s previously held equity interest in the acquiree.b) the net of the acquisition-date amounts of the identifiable assets acquired and the liabilities assumed.

Occasionally, an acquirer will make a bargain purchase, which is a business combination in which the amount in point (b) exceeds the aggregate of the amounts specified in point (a). If that excess remains, after reassessment of correct identification of all acquired assets and liabilities, the acquirer recognises the resulting gain in profit or loss on the acquisition date as other operating profit for the period.

The acquirer measures goodwill at the amount recognised at the acquisition date less any accumulated impairment allowances.A cash-generating unit to which goodwill has been allocated is tested for impairment annually, and whenever there is an indication that the unit may be impaired. The annual impairment test may be performed at any time during an annual period, provided the test is performed at the same time every year.

A cash-generating unit to which no goodwill has been allocated is tested for impairment only when there are indicators that the cash-generating unit might be impaired.

An impairment loss recognised for goodwill is not reversed in a subsequent period.

If the initial accounting for a business combination is incomplete by the end of the reporting period in which the combination occurs, the acquirer reports in its consolidated financial statements provisional amounts for the items for which the accounting is incomplete. During the measurement period, the acquirer retrospectively adjusts the provisional amounts recognised at the acquisition date to reflect new information obtained about facts and circumstances that existed as of the acquisition date and, if known, would have affected the measurement of the amounts recognised as of that date. During the measurement period, the acquirer also recognises additional assets or liabilities if new information is obtained about facts and circumstances that existed as of the acquisition date and, if known, would have resulted in the recognition of those assets and liabilities as of that date. The measurement period ends as soon as the acquirer receives the information it was seeking about facts and circumstances that existed as of the acquisition date or learns that more information is not obtainable. However, the measurement period does not exceed one year from the acquisition date.

2.4.8.2. Rights

Carbon dioxide emission rights (CO2)

CO2 emission rights are initially recognised as intangible assets, which are not amortised (assuming the high residual value), but tested for impairment.

Granted emission allowances are presented as separate items as intangible assets in correspondence with deferred income at fair value as at the date of registration. Purchased allowances are presented as intangible assets at purchase price.

For the estimated CO2 emissions during the reporting period, a provision is created in operating activity costs (taxes and charges).

Grants are recognised proportionally with the related costs for which the grants were intended to compensate. Consequently, the cost of recognition of the provision in the statement of comprehensive income is compensated by a decrease of deferred income (grants) with taking into consideration the proportion of the estimated quantity of emission (accumulated) to the quantity of evaluated annual emission. The surplus of grant over the estimated emission in the reporting period is recognised as other operating income.

Granted/purchased CO2 emission allowances are amortised against the book value of provision, as its settlement. Outgoing of allowances is recognised using FIFO method (first in, first out).

ANNUAL REPORT of Public comPany orlen lietuva for the year 2011 29

2.4.9. Perpetual usufruct of land

Perpetual usufruct of land is recognised at acquisition cost and presented in a separate line of the consolidated statement of financial position.

As at the end of the reporting period perpetual usufruct of land is valued at the net carrying amount, i.e. at acquisition cost less any accumulated depreciation and impairment losses.