ANNUAL REPORT 2008 - Welcome to Lorex - Leader in security camera

44

2008 2008 ANNUAL REPORT ANNUAL REPORT

Transcript of ANNUAL REPORT 2008 - Welcome to Lorex - Leader in security camera

20082008ANNUAL REPORTANNUAL REPORT

forPDF_Lorex_AR.indd a1forPDF_Lorex_AR.indd a1 1/15/09 1:07:47 PM1/15/09 1:07:47 PM

TABLE OF CONTENTS

1 Financial Highlights 2 Chairman and CEO’s Message 8 Management’s Discussion and Analysis 22 Financial Statements Responsibility 23 Auditors’ Report to the Shareholders 25 Consolidated Balance Sheets 26 Consolidated Statements of Operations and Comprehensive Income 27 Consolidated Statements of Shareholders’ Equity 28 Consolidated Statements of Cash Flows 29 Notes to Consolidated Financial Statements

WHAT IF YOU COULD SEE BETTER? SOMEHOW REMAIN IN ROOMS THAT YOU HAVE LEFT? WHAT IF THE POWER OF YOUR VISION WAS EXPANDED BY MACHINES? WE HAVE THE INSIGHT TO HELP PEOPLE SEE BETTER. TO SEE MORE. WE’RE LOREX.

forPDF_Lorex_AR.indd a2forPDF_Lorex_AR.indd a2 1/15/09 1:07:49 PM1/15/09 1:07:49 PM

L O R E X T E C H N O L O G Y I N C . A N N U A L R E P O R T 2 0 0 8 1

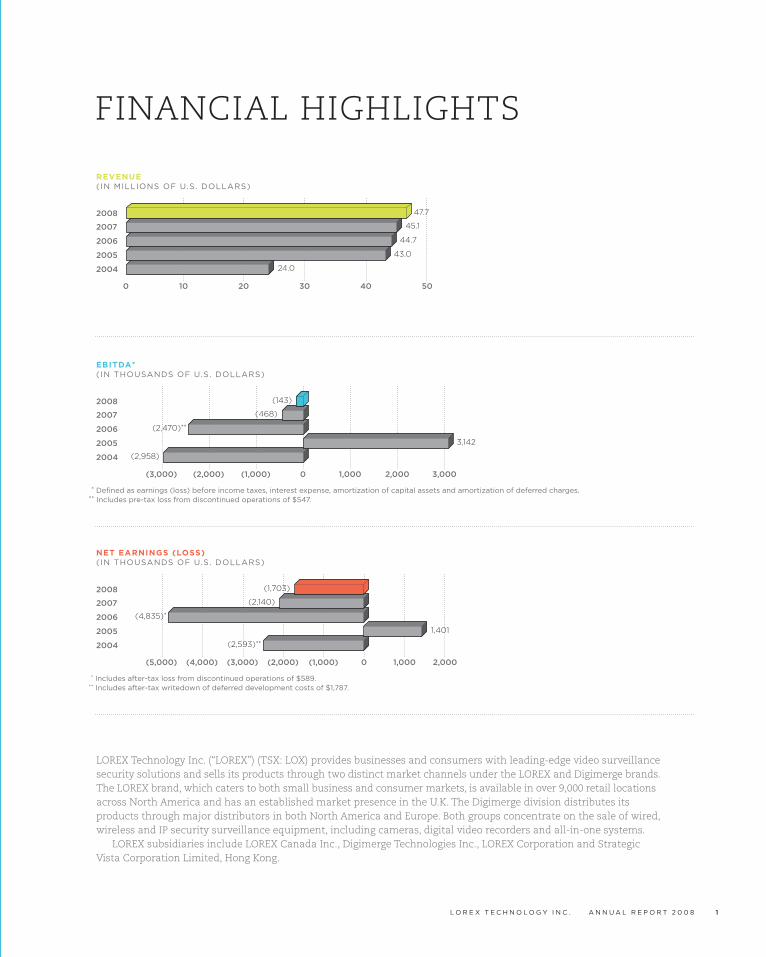

50403020100

2008

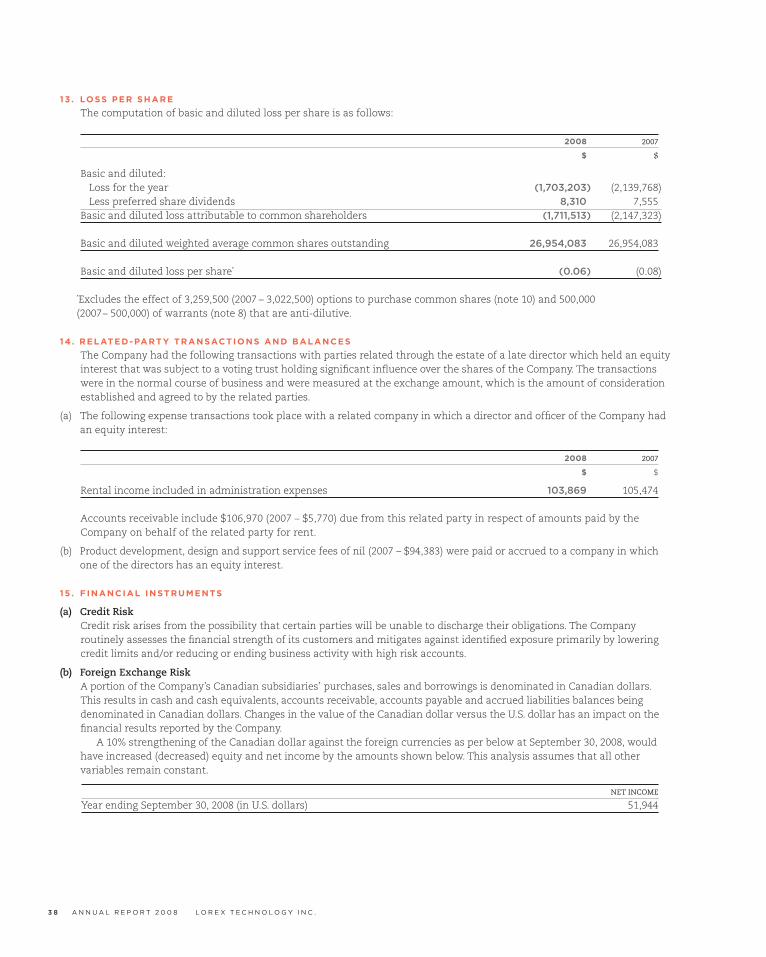

2007

2006

2005

2004

47.7

45.1

44.7

43.0

24.0

2,000 3,0001,000(1,000)(2,000)(3,000) 0

2008

2007

2006

2005

2004

(143)

(468)

(2,470)**

3,142

(2,958)

0 1,000 2,000(1,000)(3,000) (2,000)(4,000)(5,000)

2008

2007

2006

2005

2004

(1,703)

(2,140)

(4,835)*

1,401

(2,593)**

FINANCIAL HIGHLIGHTS

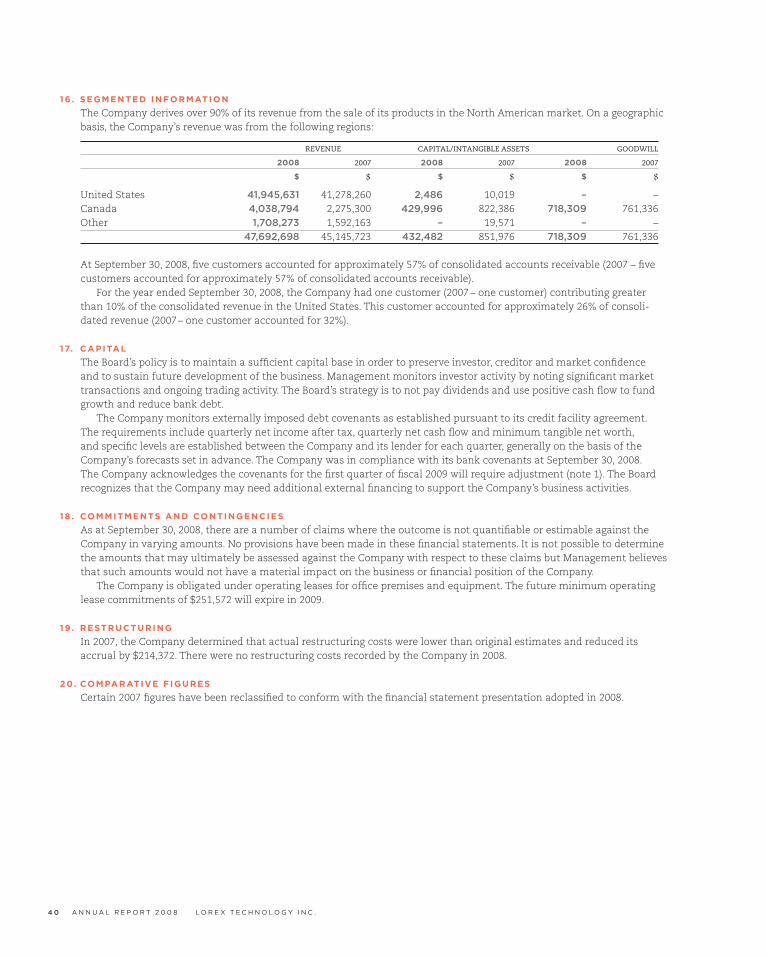

LOREX Technology Inc. (“LOREX”) (TSX: LOX) provides businesses and consumers with leading-edge video surveillance security solutions and sells its products through two distinct market channels under the LOREX and Digimerge brands. The LOREX brand, which caters to both small business and consumer markets, is available in over 9,000 retail locations across North America and has an established market presence in the U.K. The Digimerge division distributes its products through major distributors in both North America and Europe. Both groups concentrate on the sale of wired, wireless and IP security surveillance equipment, including cameras, digital video recorders and all-in-one systems.

LOREX subsidiaries include LOREX Canada Inc., Digimerge Technologies Inc., LOREX Corporation and Strategic Vista Corporation Limited, Hong Kong.

REVENUE(IN MILLIONS OF U.S. DOLLARS)

EBITDA*(IN THOUSANDS OF U.S. DOLLARS)

NET EARNINGS (LOSS)(IN THOUSANDS OF U.S. DOLLARS)

* Includes after-tax loss from discontinued operations of $589.** Includes after-tax writedown of deferred development costs of $1,787.

* Defi ned as earnings (loss) before income taxes, interest expense, amortization of capital assets and amortization of deferred charges.** Includes pre-tax loss from discontinued operations of $547.

forPDF_Lorex_AR.indd Sec1:1forPDF_Lorex_AR.indd Sec1:1 1/15/09 1:07:50 PM1/15/09 1:07:50 PM

A WORD FROM

THE MAN WITH THE

EYES

“ IN ANY BUSINESS, IN EVERY HOME, SECURITY COMES FROM KNOWING THAT THERE IS NOTHING THAT YOU CAN’T SEE. AND CONFIDENCE COMES FROM SEEING WELL.”

A N N U A L R E P O R T 2 0 0 8 L O R E X T E C H N O L O G Y I N C . 2

forPDF_Lorex_AR.indd Sec1:2forPDF_Lorex_AR.indd Sec1:2 1/15/09 1:07:51 PM1/15/09 1:07:51 PM

L O R E X T E C H N O L O G Y I N C . A N N U A L R E P O R T 2 0 0 8 3

Over all, LOREX succeeded in achieving growth in revenues in 2008; however, as the economy began to falter in the latter half of the year, the Company faced numerous challenges.

As a result of a shift in customer expectations, we took immediate action, implementing price reductions as we navigated through a new reality in business and consumer spending patterns. The effects of our implementing pricing strategies to refl ect the demand for lower-priced product negated profi tability from the fi rst half of the year and resulted in the loss that we incurred. We have strategies for 2009 that fi t the bill for today’s economic environment and are presently delivering security and surveillance solutions that answer today’s customer’s requirements.

Our development team, with the support of our top-tier group of vendor partners, will strive to continue to provide next-generation surveillance solutions. We will build upon our recent successes and expand our existing core group of products, including IP cameras, LCD/DVR surveillance systems and wireless network cameras, all of which are projected to generate revenue growth.

Industry guidance for the security market projects continued growth for 2009 although more moderate than in prior years. Management has developed new product options at lower price points to address budget- conscious consumers and will continue its campaign to attract new business from the e-commerce market and the professional security integrator.

We are proud to report that the LOREX brand, which caters to both small business and consumer markets, is available in over 9,000 retail locations across North America and has an established market presence in the U.K. The Digimerge division continues to expand, and we are enjoying success at many levels throughout the North American distribution sales channel.

Our Board of Directors, the Executive Management Team and LOREX employees remain determined and dedicated to successful results.

On behalf of the Board, I would like to extend sincere thanks to all members of the LOREX Team and look forward to continued growth for LOREX and all stockholders.

Henry SchnurbachChairman & CEO

For Lorex, 2008 was a year for clarity. For foresight. For vision. That’s our approach for looking forward. And it’s working.

CHAIRMAN AND CEO’S MESSAGE

forPDF_Lorex_AR.indd Sec1:3forPDF_Lorex_AR.indd Sec1:3 1/15/09 1:07:52 PM1/15/09 1:07:52 PM

Lorex’s ultra Digital wireless MONITORING System with 7” digital lcd receiver and quad view mode shows up to four camera views on the same screen. mix and match indoor and outdoor night-vision cameras to see anywhere, anytime and, with the built-in camera microphone, hear anything for Listen-in Surveillance.

LW2602

HEY!I’M READY FOR

MY CLOSE-UP!

She needed the cameras but she hated the hookups. Then someone whispered “wireless” in her ear, and the answer was upon her! Thanks to Lorex, the solution to her problem was simple and clear. So was the resolution.

NO HANGING

WIRES!

SCALABLE WIRELESS SECURIT Y

A N N U A L R E P O R T 2 0 0 8 L O R E X T E C H N O L O G Y I N C . 4

forPDF_Lorex_AR.indd Sec1:4forPDF_Lorex_AR.indd Sec1:4 1/15/09 1:08:04 PM1/15/09 1:08:04 PM

This 20” LCD Monitor with built-in digital video recorder will provide superior image quality in live view and playback modes. Easy to install and operate, the L20WD800 is the first surveillance system actually designed to be seen by customers and guests — while providing the highest level of surveillance protection available in a packaged retail kit.

L20WD

WATCH OUT!AND AROUND…

AND OVER…

NOW SEE HERE

How could he possibly keep an eye on every aisle? And how long would it take for the wrong sort to see that he couldn’t? Well, fortunately he could – with a little help. The right camera and monitor set-up, with its integrated DVR, had extended his vision, and suddenly he had the whole picture. And the ability to play it back.

ALL-IN-ONE SECURIT Y

L O R E X T E C H N O L O G Y I N C . A N N U A L R E P O R T 2 0 0 8 5

forPDF_Lorex_AR.indd Sec1:5forPDF_Lorex_AR.indd Sec1:5 1/15/09 1:08:09 PM1/15/09 1:08:09 PM

LOREX’s new Wireless Easy-Connect Network Camera allows users to remotely monitor their home or business through a secure, password- protected connection that requires no networking knowledge. Simply connect the camera into a router and run the installation CD, and users are on their way to see, hear and protect what matters.

OH, BRAD,YOU’RE SO REMOTE! LNE3003

GONE FOR GOOD

Now he can care from a distance because he knows that being away no longer means being out of touch. With a hand-held device and Internet access, he keeps an eye on things at home and at the offi ce and at the factory and…

REMOTE MONITORING SECURITY

A N N U A L R E P O R T 2 0 0 8 L O R E X T E C H N O L O G Y I N C . 6

forPDF_Lorex_AR.indd Sec1:6forPDF_Lorex_AR.indd Sec1:6 1/15/09 1:08:24 PM1/15/09 1:08:24 PM

Because the DVR is so small, it can be installed horizontally or on its edge or even attached to the wall or an LCD monitor using a standard Vesa mount. Yet with 3D VGA output, H.264 video compression and pentaplex operation, this DVR solution is everything you need for home or business.

LH314

NOW I

HAVE THE

POWER!

Watching was one thing. Remembering was another. Now with one surprisingly small, yet amazingly powerful device it was easy for him to keep a record of everything the cameras saw. Everything. And that gave him confi dence.

LOOK BACK IN TIME

NETWORK-READY DIGITAL VIDEO SECURIT Y

L O R E X T E C H N O L O G Y I N C . A N N U A L R E P O R T 2 0 0 8 7

forPDF_Lorex_AR.indd Sec1:7forPDF_Lorex_AR.indd Sec1:7 1/15/09 1:08:30 PM1/15/09 1:08:30 PM

A N N U A L R E P O R T 2 0 0 8 L O R E X T E C H N O L O G Y I N C . 8

The following is Management’s Discussion and Analysis (MD&A) of the fi nancial position of LOREX Technology Inc. (“LOREX”or the “the Company”) and the fi nancial review for the years ended September 30, 2008 and 2007. This discussion should be read in conjunction with the Audited Consolidated Financial Statements and related notes. All amounts are in U.S. dollars unless otherwise stated. As a result of rounding differences, certain fi gures in this MD&A may not total.

CAUTIONARY STATEMENTS REGARDING FORWARD-LOOKING STATEMENTS

This MD&A for the year ended September 30, 2008, was completed on December 3, 2008, and contains notes and explanations of important events to this date.

Certain information contained in this report may contain statements that are forward-looking, such as statements relating to anticipated future revenues of the Company and the success of product offerings. Such forward-looking statements involve important risks and uncertainties that could signifi cantly affect anticipated results in the future and, accordingly, such results may differ materially from those expressed in any forward-looking statements made by or on behalf of the Company. These risks and uncertainties include, without limitation, changes in competition, changes in technologies that have an impact on products being developed and sold by the Company, changes in customer demand and the availability of raw materials required to manufacture the Company’s products. Any of these risks and uncertainties could cause actual results to vary materially from current results or the Company’s currently anticipated future results. The Company wishes to caution readers not to place undue reliance on such forward-looking statements that speak only as of the date made.

OVERVIEW OF THE COMPANY

LOREX Technology Inc. (“LOREX”) (TSX: LOX) provides businesses and consumers with leading-edge video surveillance security solutions and sells its products through two distinct market channels under the LOREX and Digimerge brands. The LOREX brand, which caters to both small business and consumer markets, is available in over 9,000 retail locations across North America and has an established market presence in the U.K. The Digimerge division distributes its products through major distributors in both North America and Europe. Both groups concentrate on the sale of wired, wireless and IP security surveillance equipment including cameras, digital video recorders and all-in-one systems.

LOREX subsidiaries include LOREX Canada Inc., Digimerge Technologies Inc., LOREX Corporation and Strategic Vista Corporation Limited, Hong Kong.

REPORTING CURRENCY

The Company uses the U.S. dollar as its reporting currency.The Company and its subsidiaries that use the Canadian dollar as the functional currency translate all assets and

liabilities to U.S. dollars at the period-end exchange rate, and all revenue and expense items are translated to U.S. dollars at an average rate of exchange for the period for reporting purposes. Exchange rate differences arising on translation are deferred as a separate component of shareholders’ equity. The U.S. dollar is the functional currency of certain of the Company’s subsidiaries – Digimerge Technologies Inc., LOREX Corporation and Strategic Vista Corporation Limited. For other U.S. subsidiaries that are considered fully integrated foreign operations, non-Canadian-dollar monetary assets and liabilities are translated into Canadian dollars at the rate of exchange prevailing as at the consolidated balance sheet dates, while non-monetary assets and liabilities are translated at historical rates of exchange. Revenues and expenses are translated into Canadian dollars at the rate in effect at the date of transaction. Realized and unrealized foreign exchange gains and losses are included in net earnings for the period in which they occur.

MD&A Management’s Discussion and Analysis

forPDF_Lorex_AR.indd Sec1:8forPDF_Lorex_AR.indd Sec1:8 1/15/09 1:08:35 PM1/15/09 1:08:35 PM

L O R E X T E C H N O L O G Y I N C . A N N U A L R E P O R T 2 0 0 8 9

BUSINESS AND F INANCIAL DEVELOPMENTS

During the past year, the following signifi cant developments had an impact on the Company’s operations and fi nancial results.

Sales and MarketingThe Company introduced the next generation of its integrated systems and digital video recorder/camera bundles to assure the Company’s continued competitiveness and to maintain or grow market share.

The Company introduced a line of wireless cameras featuring digital frequency-hopping and WIFI-friendly technologies, allowing the Company to accelerate its representation into the consumer security market.

The Company executed a product and brand public relations campaign, increasing market presence in trade and non-trade publications using video, Web and print media. Initiatives commenced in July 2008 and resulted in increased marketing costs for the year. The benefi ts of the marketing campaign should have an impact on future revenue.

The Company experienced falling demand in the third quarter as a result of overall declines in consumer spending, most noticeably with its largest account. The Company responded to the challenge by offering customers lower-priced options, the benefi ts of which began to be realized in the fourth quarter as revenue increased by $880,000 as compared to the third quarter. The Company believes that it should continue to realize additional revenue growth opportunities in 2009 with its expanded lineup of products at economic price levels.

OperationsDuring the year the Company reduced inventory by $3.2 million in fi scal 2008 as it reduced the number of products offered and improved purchasing effi ciency. Reductions in inventory lowered working capital requirements and resulted in a reduction in debt by $2.3 million from $9.2 million to $6.9 million. Accounts payable and accrued liabilities were also reduced by $1.3 million from $6.7 million to $5.4 million due to improvements in business operations. Management plans to continue its efforts in 2009 to improve operational effi ciency by further reducing inventory requirements.

The Company expanded its marketing activities to e-tailers and is initiating a sales campaign to make selected products available directly to price-conscious consumers.

The Company realized the positive effects of its quality assurance programs and experienced a signifi cant reduction in defective returns and related provision expense including the cost to service product returns.

FinancialDuring the year the Company complied with its quarterly bank covenants, certain of which were modifi ed at the Company’s request. Specifi c covenants, based on the Company’s projections, are agreed to by the Company and its lender for each quarter and are revisited regularly. Before adjusting for changes in working capital, the Company experienced a net loss and negative cash fl ows from operations for the year ended September 30, 2008. Based on its current projections, the Company believes specifi c covenants will not be met in the fi rst quarter of 2009 and will require amendment to its bank covenant or the receipt of an interim waiver of compliance. Failure to comply with debt covenants creates a loan default that could result in the Company having to immediately pay the loan outstanding unless a waiver is obtained. While the Company has requested modifi cations that have been historically approved, there is no certainty that the Company will be successful in obtaining modifi cations to covenants in the future. While the Company had excess availability under its covenant of $1.3 million at September 30, 2008, and forecasts excess availability through fi scal 2009, Management believes that it would be prudent to have availability of additional fi nancing to support the Company’s plans for continued sales growth and/or to ensure suffi cient working capital in the event of a reduction in customer demand.

SUMMARY OF KEY INDICATORS

The Company’s revenue for fi scal 2008 was $47.7 million as compared to $45.1 million in fi scal 2007. Growth was achieved primarily by increased sales to North American nationally branded online e-tailers, consumer electronics retailers and professional distributors and through the in-house webstore. While current market conditions may have affected consumer buying patterns, Management believes that the demand for surveillance products continues to grow and that the Company has positioned itself to increase shipments in higher-growth channels such as e-commerce.

Gross profi t for fi scal 2008 was $15.3 million (32.1%) as compared to $13.3 million (29.5%) in fi scal 2007. The $2.0 million increase was primarily the result of sales growth and the 2.6% increase in gross profi t margin, which was primarily the result of improved product assortment.

In fi scal 2008, the Company experienced a net loss from continuing operations of $(1.7) million as compared to a net loss from continuing operations of $(2.1) million in fi scal 2007. The reduction in net loss in 2008 was primarily the result of inventory management, which is refl ected in improved inventory turns and lower writedowns for impairment.

forPDF_Lorex_AR.indd Sec1:9forPDF_Lorex_AR.indd Sec1:9 1/15/09 1:08:35 PM1/15/09 1:08:35 PM

A N N U A L R E P O R T 2 0 0 8 L O R E X T E C H N O L O G Y I N C . 1 0

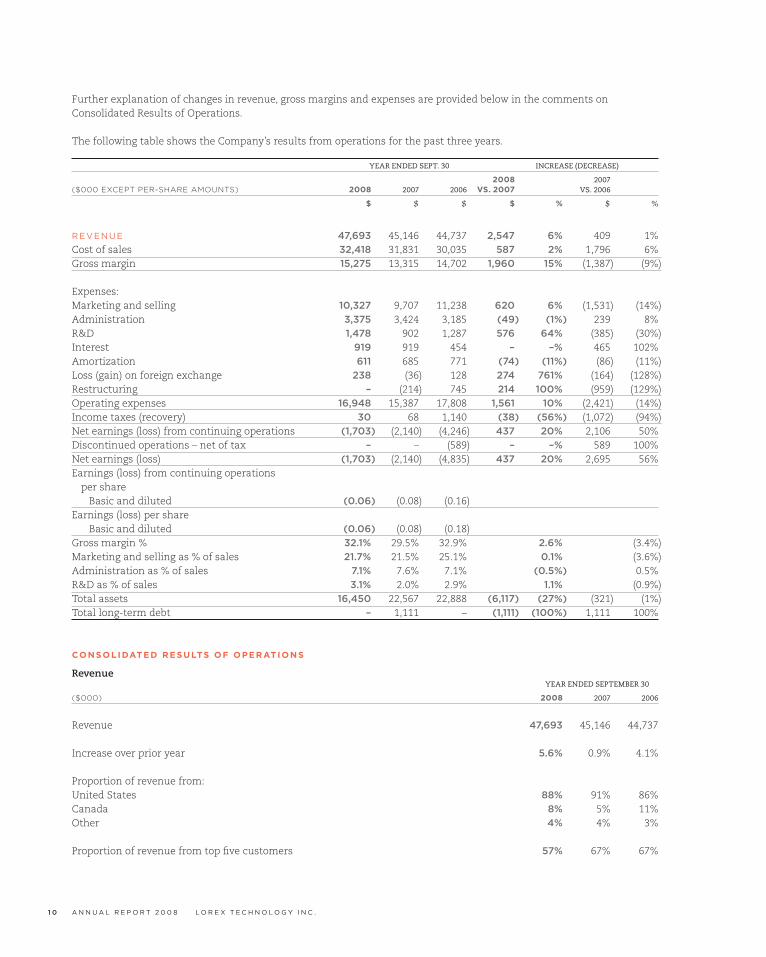

Further explanation of changes in revenue, gross margins and expenses are provided below in the comments on Consolidated Results of Operations.

The following table shows the Company’s results from operations for the past three years.

YEAR ENDED SEPT. 30 INCREASE (DECREASE)

2008 2007 ($000 EXCEPT PER-SHARE AMOUNTS) 2008 2007 2006 VS. 2007 VS. 2006

$ $ $ $ % $ %

REVENUE 47,693 45,146 44,737 2,547 6% 409 1%Cost of sales 32,418 31,831 30,035 587 2% 1,796 6%Gross margin 15,275 13,315 14,702 1,960 15% (1,387) (9%)

Expenses: Marketing and selling 10,327 9,707 11,238 620 6% (1,531) (14%)Administration 3,375 3,424 3,185 (49) (1%) 239 8% R&D 1,478 902 1,287 576 64% (385) (30%)Interest 919 919 454 – –% 465 102%Amortization 611 685 771 (74) (11%) (86) (11%)Loss (gain) on foreign exchange 238 (36) 128 274 761% (164) (128%)Restructuring – (214) 745 214 100% (959) (129%)Operating expenses 16,948 15,387 17,808 1,561 10% (2,421) (14%)Income taxes (recovery) 30 68 1,140 (38) (56%) (1,072) (94%)Net earnings (loss) from continuing operations (1,703) (2,140) (4,246) 437 20% 2,106 50%Discontinued operations – net of tax – – (589) – –% 589 100%Net earnings (loss) (1,703) (2,140) (4,835) 437 20% 2,695 56%Earnings (loss) from continuing operations per share Basic and diluted (0.06) (0.08) (0.16) Earnings (loss) per share Basic and diluted (0.06) (0.08) (0.18) Gross margin % 32.1% 29.5% 32.9% 2.6% (3.4%)Marketing and selling as % of sales 21.7% 21.5% 25.1% 0.1% (3.6%)Administration as % of sales 7.1% 7.6% 7.1% (0.5%) 0.5%R&D as % of sales 3.1% 2.0% 2.9% 1.1% (0.9%)Total assets 16,450 22,567 22,888 (6,117) (27%) (321) (1%)Total long-term debt – 1,111 – (1,111) (100%) 1,111 100%

CONSOLIDATED RESULTS OF OPERATIONS

Revenue YEAR ENDED SEPTEMBER 30

($000) 2008 2007 2006

Revenue 47,693 45,146 44,737

Increase over prior year 5.6% 0.9% 4.1%

Proportion of revenue from:United States 88% 91% 86%Canada 8% 5% 11%Other 4% 4% 3%

Proportion of revenue from top fi ve customers 57% 67% 67%

forPDF_Lorex_AR.indd Sec1:10forPDF_Lorex_AR.indd Sec1:10 1/15/09 1:08:36 PM1/15/09 1:08:36 PM

L O R E X T E C H N O L O G Y I N C . A N N U A L R E P O R T 2 0 0 8 1 1

2008 Compared to 2007Revenue in 2008 grew compared to the prior year by 5.6%, primarily as a result of increased sales of integrated systems and professional cameras. On a customer basis, LOREX brand sales increased primarily through national online e-tailers and through the in-house webstore. Sales growth came from a broader customer base as the Company continued to lower its concentration with its top one, fi ve and 10 customers compared to the prior year.

Under the Digimerge brand, sales grew to $6.9 million from $6.0 million in fi scal 2007 on the correction of a supply problem experienced in 2007 and due to increased camera shipments.

2007 Compared to 2006Revenue in 2007 was maintained as compared to the prior year, primarily as a result of increased sales of LCD observation systems, surveillance cameras and simplifi ed home surveillance systems, while sales of prior-generation CRT observation systems and digital video recorders decreased. On a customer basis, sales increased through consumer electronics, national retail, offi ce superstore and direct Web sale channels, while sales to club warehouse and home improvement channels decreased. The decrease in club warehouse channel sales resulted from the loss in fi scal 2006 of a signifi cant warehouse club account. The Company expects growth in fi scal 2008, which Management forecasts will be achieved by growth in every business sector as new product offerings become staple offerings by the Company’s customers to retail customers.

Sales of the Company’s professional products under the Digimerge brand to security distributors in the commercial market decreased to $6.0 million in fi scal 2007 from $6.8 million in fi scal 2006, a decrease of 12%, due to supply problems that have been corrected.

Gross Profi t YEAR ENDED SEPTEMBER 30

2008 2007 2006 Gross profi t 32.1% 29.5% 32.9%

Cost of sales includes the cost of manufactured products based on FOB factory prices, inbound freight, duty and provisions to record inventory to its net realizable value.

The Company outsources its manufacturing to third parties in South Korea, Taiwan and China. Gross margins in 2008 were higher than 2007 primarily as a result of a favourable product mix. Gross margins in 2007 were lower than 2006 primarily as a result of additional inventory writedowns recorded after

Management determined that shifting market dynamics increased opportunity for the sale of advanced product, narrowing the market for product featuring earlier technology.

Marketing and Selling Expense YEAR ENDED SEPTEMBER 30

($000) 2008 2007 2006

Marketing and selling expense 10,327 9,707 11,238As a percentage of sales 21.7% 21.5% 25.1%

The principal components of marketing and selling expense are outbound freight and distribution costs associated with product shipments, warranty/repair service costs, and salary and commission expenses for both internal and external sales and support personnel. Other costs include sales display and detailing costs to ensure the Company’s products are displayed to enhance revenues.

The increase in marketing and selling expense from 2007 to 2008 was primarily the result of increased spending on the initiation of public relations campaigns and related outside marketing support for its wireless digital and IP cameras. In 2009 Management plans to reduce spending on outside marketing support compared to 2008. In addition, the Company incurred higher costs to market its in-house webstore, which experienced parallel revenue growth.

The decrease in marketing and selling expense in 2007 compared to 2006 resulted primarily from a decrease in warranty/repair service costs as compared to prior periods. Management – anticipated reduced return rates for products manufactured through new supplier relationships decreased due to improvements in product engineering and quality assurance programs. In addition to the decrease in warranty service expense, there was a decrease in expenses attributable to the rationalization process started in 2006.

forPDF_Lorex_AR.indd Sec1:11forPDF_Lorex_AR.indd Sec1:11 1/15/09 1:08:36 PM1/15/09 1:08:36 PM

A N N U A L R E P O R T 2 0 0 8 L O R E X T E C H N O L O G Y I N C . 1 2

Administration Expense YEAR ENDED SEPTEMBER 30

($000) 2008 2007 2006

Administration expense 3,375 3,424 3,185As a percentage of sales 7.1% 7.6% 7.1%

The main components of administration expenses are wages and benefi ts, professional fees, general and offi ce expenses and costs associated with the public company reporting requirements.

The Company slightly reduced its administrative cost in 2008, which resulted in a return to 2006 expense levels as a percentage of sales.

The increase in 2007 was due to an increase in professional and related fees incurred in relation to exiting a debt facility and as a result of increased stock option expense resulting from the issuance of new options and modifi cation of existing options during the year. The increase was partially offset by general decreases in other administration expenses.

For fi scal 2009, the Company is not anticipating any material changes to its administration budget other than the impact of the Canadian exchange rate.

Restructuring Expense YEAR ENDED SEPTEMBER 30

($000) 2008 2007 2006

$ $ $

Restructuring expense – (214) 745

In fi scal 2007, the Company reversed part of a restructuring expense accrued in fi scal 2007 for severance expense, as actual requirements were lower than originally estimated. No restructuring activities were undertaken during fi scal 2008.

Research and Development YEAR ENDED SEPTEMBER 30

($000) 2008 2007 2006

Research and development 1,478 902 1,287As a percentage of sales 3.1 2.0% 2.9%

Research and development expenses include the wages and benefi ts paid to individuals in the Company’s product development group, subcontractors and the amortization costs associated with capitalized tooling and product design costs.

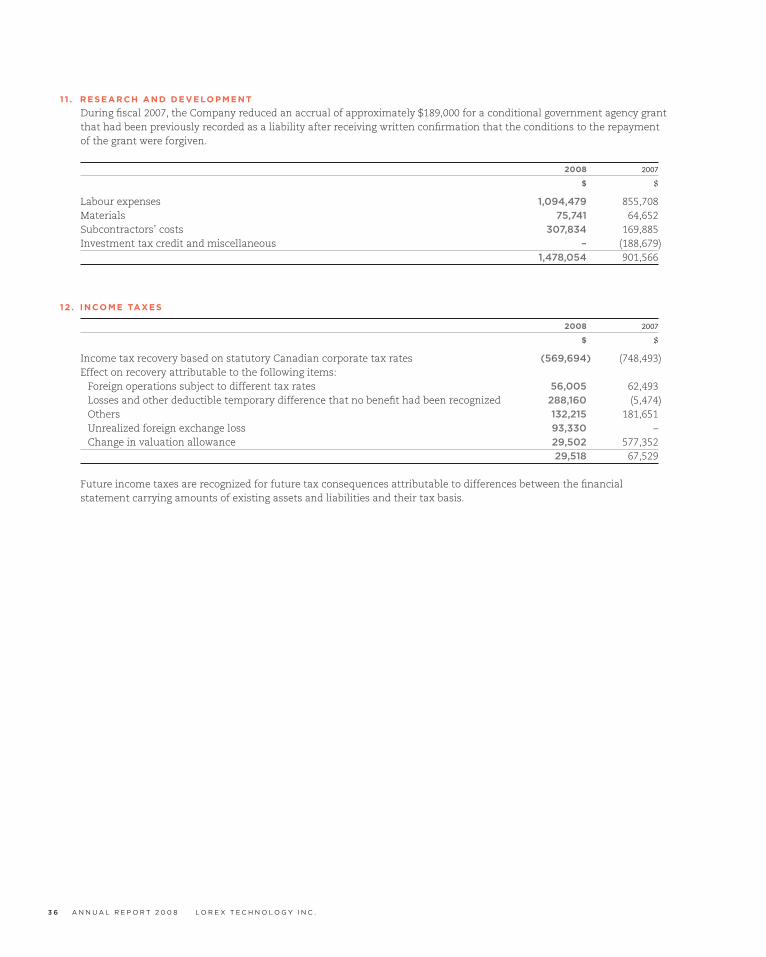

In fi scal 2007, the Company benefi ted from a reversal of an accrual that was forgiven for a conditional government grant. The reversal of the grant reduced research and development expense reported during that period by $189,000. The remaining increase in research and development costs incurred from 2007 to 2008 relates primarily to increased use of third-party development support of new product lines. Management believes that the Company is competitively positioned with its new lines of cameras, digital video recorders and integrated systems and utilizing new digital wireless and IP networking technologies.

The decrease in 2007 was primarily the result of reduced fees paid to third-party contractors and employees as a result of restructuring that occurred in fi scal 2006.

In 2009, Management expects a return to 2007 expense levels prior to the reversal of the grant above.

forPDF_Lorex_AR.indd Sec1:12forPDF_Lorex_AR.indd Sec1:12 1/15/09 1:08:36 PM1/15/09 1:08:36 PM

L O R E X T E C H N O L O G Y I N C . A N N U A L R E P O R T 2 0 0 8 1 3

Interest Expense YEAR ENDED SEPTEMBER 30

($000) 2008 2007 2006

Interest expense 920 919 454

The Company’s interest expense in 2008 remained the same as that in 2007 despite increased business activities. In 2007, the Company changed its debt facility from Canada to the U.S., where prime rates were higher. The increase in interest rate offset the lower average debt balance experienced during 2008.

The increased interest expense in fi scal 2007 compared to fi scal 2006 was primarily the result of higher average debt levels and increased cost of borrowings.

Amortization of Capital Assets YEAR ENDED SEPTEMBER 30

($000) 2008 2007 2006

Amortization of capital assets 611 686 771

The primary capital assets of the Company subject to amortization are tooling and equipment, product and packaging design costs, patents and trademarks, and computer hardware.

During 2008 the Company purchased $221,000 of capital assets (2007 – $98,000, 2006 – $691,000).

Loss (Gain) on Foreign Exchange YEAR ENDED SEPTEMBER 30

($000) 2008 2007 2006

Loss (gain) on foreign exchange 238 (36) 128

In 2008, the Company recognized a foreign exchange loss due to the impact of the strengthening of the U.S. dollar relative to the Canadian dollar on its U.S.-denominated liabilities recorded in its Canadian subsidiaries.

In 2007, the Company recognized a foreign exchange gain due to the impact of the weakening of the U.S. dollar relative to the Canadian dollar on its U.S.-denominated liabilities recorded in its Canadian subsidiaries.

Income Taxes YEAR ENDED SEPTEMBER 30

2008 2007 2006

Income tax rate (1.8%) (3.3%) (32.4%)

The Company recognizes future income taxes for future tax consequences attributable to differences between the fi nancial statement carrying amounts of existing assets and liabilities and their tax basis.

The actual effective tax rate for 2008 is (1.8%), which is due to a valuation allowance recorded against any future income tax assets, that are unlikely to be realized. Furthermore, there are permanent items that are not deductible such as stock option expenses.

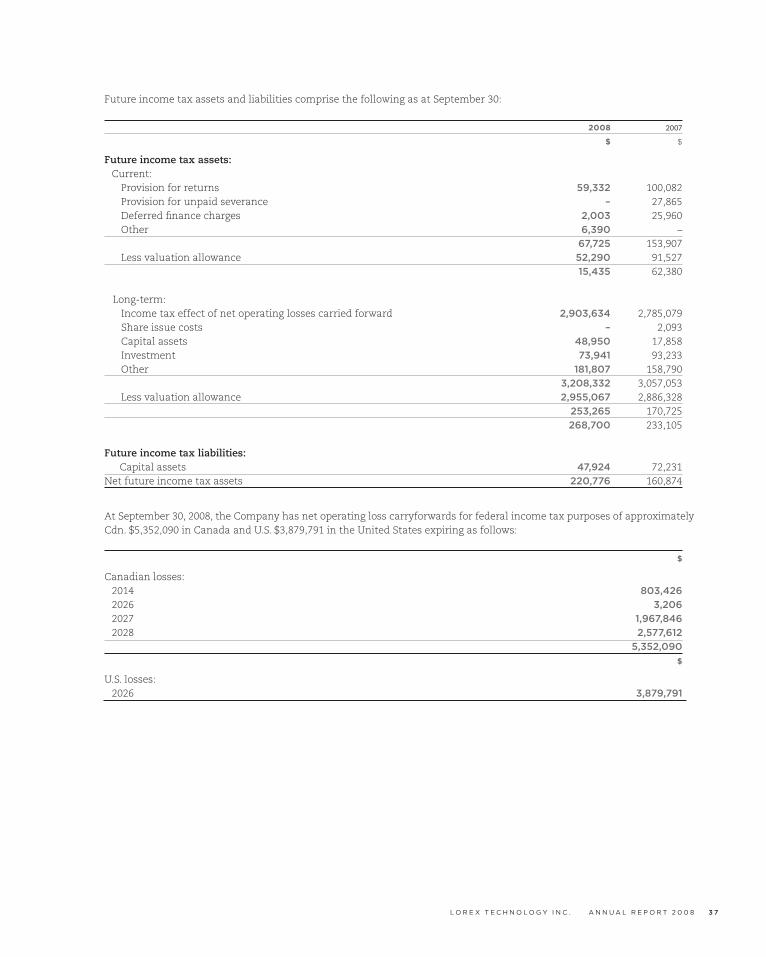

In fi scal 2006, a valuation allowance was provided against the benefi t of certain tax loss carryforward balances previously recorded that no longer met the accounting criteria for recognition. As at September 30, 2006, a valuation allowance of $2.6 million was provided against certain of the Company’s future income tax assets. As at September 30, 2008, the valuation allowance was $3.0 million.

forPDF_Lorex_AR.indd Sec1:13forPDF_Lorex_AR.indd Sec1:13 1/15/09 1:08:36 PM1/15/09 1:08:36 PM

A N N U A L R E P O R T 2 0 0 8 L O R E X T E C H N O L O G Y I N C . 1 4

QUARTERLY F INANCIAL RESULTS

($000 EXCEPT PER-SHARE AMOUNTS) 2008 2007

FOR THE QUARTERS ENDING SEPT. 30 JUNE 30 MAR. 31 DEC. 31 SEPT. 30 JUNE 30 MAR. 31 DEC. 31

Revenue 11,096 10,217 12,625 13,755 12,151 12,148 12,129 8,717Net income (loss) (431) (1,423) 19 132 (574) (123) (772) (671)Per share basis (0.02) (0.05) 0.00 0.00 (0.02) 0.00 (0.03) (0.02)

The Company experienced balanced growth in the fi rst two quarters of fi scal 2008 compared to the prior-year periods. In the third and fourth quarters of fi scal 2008, the Company recorded lower sales to a signifi cant warehouse club customer as a result of its incurring reduced demand, and the Company offered signifi cant price concessions. In the fourth quarter, the Company partially reversed this trend by increasing sales by $880,000 over the prior quarter and signifi cantly reduced losses. The Company anticipates growth to continue in 2009 as Management navigates through the current negative economic cycle. The loss in the fourth quarter was primarily a result of credit provisions taken when two customers reorganized their debt, and the Company incurred both bad debts and a foreign currency accounting loss.

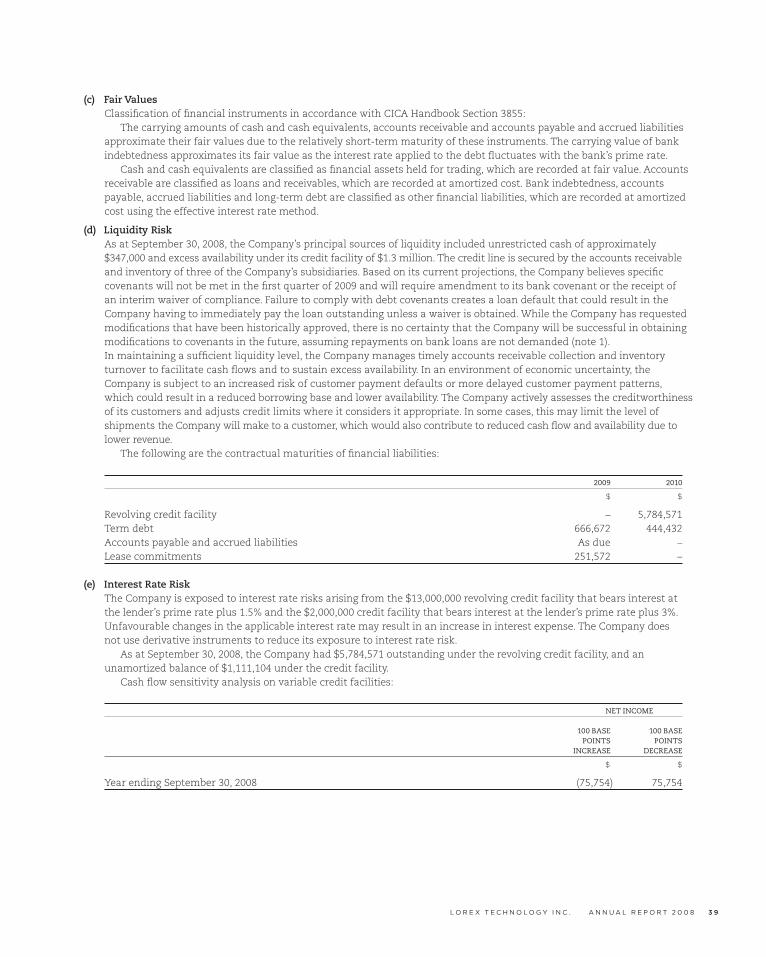

LIQUIDITY AND CAPITAL RESOURCES

In 2008, cash decreased by $73,000 as the Company as is policy transfers excess cash to reduce its loans outstanding. On May 31 2007, the Company entered into a U.S. $13,000,000 credit facility with a new lender for revolving credit loans

that bore interest at the lender’s prime rate plus 1.5%. The credit line is secured by the accounts receivable and inventory of three of the Company’s subsidiaries – LOREX Corporation, LOREX Canada Inc. and Digimerge Technology Inc. The amount available under the facility is subject to certain fi nancial ratios, as defi ned by the agreement.

In addition, a separate credit facility of U.S. $2,000,000 was established by the Company with the same lender that bears interest at the lender’s prime rate plus 3%. The U.S. $2,000,000 facility has a term of 36 months and is repayable in equal instalments over a 36-month term. As of September 30, 2008, the unamortized balance of this facility was $1,111,104. The credit facility is secured by the accounts receivable and inventory of three of the Company’s subsidiaries – LOREX Corporation, LOREX Canada Inc. and Digimerge Technology Inc.

In relation to the new credit facilities, the Company issued 500,000 warrants at a strike price of Cdn. $0.3025. Using the Black-Scholes model, the fair value of the warrants of U.S. $105,567 and the fi nance costs of U.S. $271,556 related to the loan were deferred and offset against the initial loan advance, and are accounted for using the effective interest method over 36 months. The offset to the fair value of the warrants was recorded to contributed surplus.

As at September 30, 2008, the Company’s principal sources of liquidity included unrestricted cash of $347,000 and excess availability under its credit facility of $1.3 million.

Based on its current projections, the Company believes specifi c covenants will not be met in the fi rst quarter of 2009, please see discussion in the Financial section on page 9.

forPDF_Lorex_AR.indd Sec1:14forPDF_Lorex_AR.indd Sec1:14 1/15/09 1:08:36 PM1/15/09 1:08:36 PM

L O R E X T E C H N O L O G Y I N C . A N N U A L R E P O R T 2 0 0 8 1 5

Working CapitalAccounts ReceivableThe Company’s accounts receivable balance decreased from $7.9 million at September 30, 2007, to $5.3 million at September 30, 2008, due primarily to lower revenues in the fourth quarter of 2008 as compared to the same period in 2007 and a decrease in days sales outstanding, which were 45 days at September 30, 2008, versus 53 days at September 30, 2007.

InventoryThe Company’s inventory balance decreased during the year from $11.7 million at September 30, 2007, to $8.5 million at September 30, 2008. The decrease was the result of product management improvements, including a reduction in the number of products.

Accounts Payable and Accrued LiabilitiesThe Company’s accounts payable and accrued liabilities decreased by $1.3 million from $6.7 million at September 30, 2007, to $5.4 million at September 30, 2008, refl ective of stricter purchasing controls and increased deposits to suppliers.

Capital and Intangible Assets and ExpendituresCapital and intangible assets, net of accumulated amortization, decreased by $419,000 to $432,000 at September 30, 2008. Additions to capital assets were $220,000. No additions to intangible assets were made.

For fi scal 2009, the Company anticipates maintaining expenditures for capital assets. This investment should be funded from cash fl ow from operations.

Capital Stock and DividendsAs at September 30, 2008, the Company had 26,954,083 common shares outstanding. During 2008, the Company issued no new shares. The Company has not declared any dividends on its common shares over the past three fi scal years and does not plan to declare or pay any dividends on its common shares in the next 12 months.

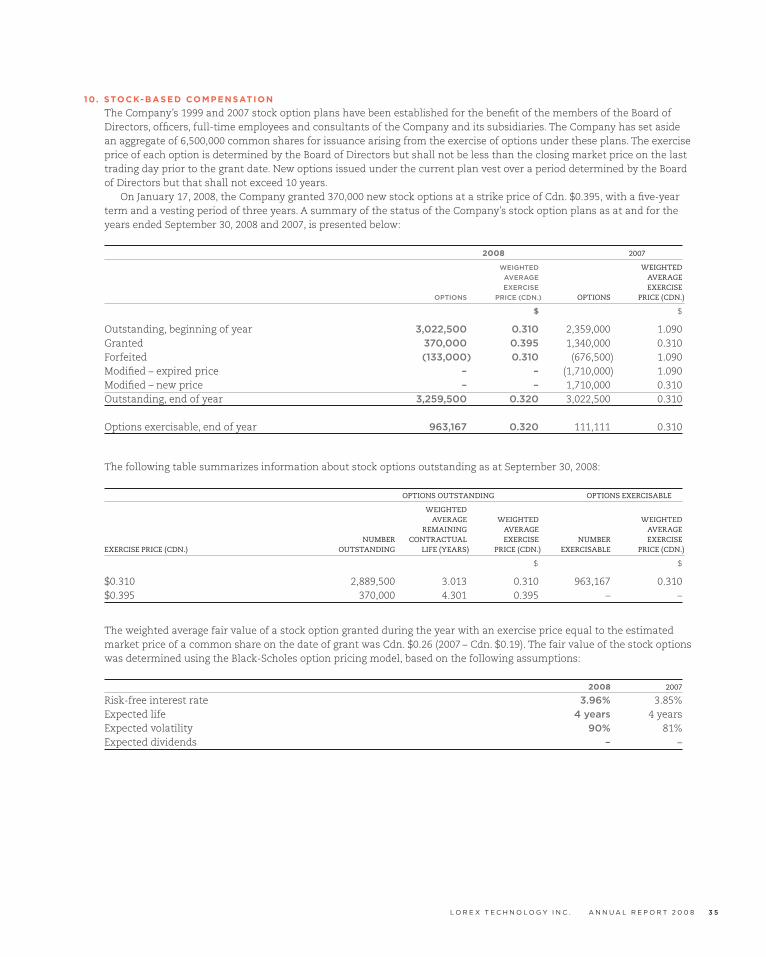

On January 17, 2008, the Company granted 370,000 new stock options at a strike price of Cdn. $0.395, with a fi ve-year term. Compensation cost of $306,000 was recognized in the current year related to these options.

RELATED-PARTY TRANSACTIONS

During the quarter, the Company had transactions with parties that were related through the estate of a late director, which held an equity interest that was subject to a voting trust holding a signifi cant infl uence over the shares of the Company. Amounts recorded for rent were $104,000.

Related-party transactions have been recorded at the exchange amount, which is the amount of consideration established and agreed by the related parties.

FOURTH-QUARTER RESULTS

Revenue for the fourth quarter decreased by $1.1 million as compared to the same period in the prior year. This decrease was primarily a result of a reduction in shipments to a warehouse club customer due to reduced demand by their primary customer, the small business owner.

Gross profi t was 33.9% compared to 23.4% in the prior-year fourth quarter. The increase was primarily a result of customer mix.

Operating expenses were $4.2 million or 37.6% of revenue compared to $3.4 million or 28% in the prior-year quarter. The increase in operating expenses resulted primarily from an increase in foreign exchange losses of $314,000, increased outside marketing support of $155,000 and increased provision for bad debts of $153,000.

forPDF_Lorex_AR.indd Sec1:15forPDF_Lorex_AR.indd Sec1:15 1/15/09 1:08:36 PM1/15/09 1:08:36 PM

A N N U A L R E P O R T 2 0 0 8 L O R E X T E C H N O L O G Y I N C . 1 6

CRIT ICAL ACCOUNTING POLICIES AND ESTIMATES

The Company prepares its fi nancial statements in accordance with Canadian generally accepted accounting principles (GAAP). Signifi cant accounting policies and methods used in the preparation of the fi nancial statements are described in note 1 to the Company’s 2008 Audited Consolidated Financial Statements. Certain of the policies are more signifi cant than others and are therefore considered critical accounting policies. Accounting policies are considered critical if they rely on a substantial amount of judgment in their application or if they result from a choice between accounting alternatives and that choice has a material impact on reported results or fi nancial position. The policies identifi ed as critical to the Company are discussed below.

Use of EstimatesThe preparation of fi nancial statements in conformity with GAAP requires Management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the fi nancial statements and the reported amounts of revenue and expenses during the reporting period. The Company evaluates its estimates and assumptions on a regular basis, based on historical experience and other relevant factors. Signifi cant estimates are used in, but not limited to, determining the allowance for doubtful accounts, the provision for returns, inventory valuation, the income tax valuation allowances, the useful lives of assets, valuation of intangible assets and product development and the fair values of reporting units for purposes of goodwill impairment tests. Actual results could differ materially from those estimates and assumptions.

Revenue RecognitionThe Company derives its revenue from direct sales to retail customers and end-users, as well as through distributors and system integrators. Customers typically issue standard purchase orders to the Company. The Company recognizes product revenue when goods are received by the customer as performance has occurred, all specifi ed acceptance criteria have been met and the earnings process is considered complete. Product returns from customers are deducted from revenue along with a provision for anticipated returns pertaining to prior product sales. The provision for returns is based on historical results.

Inventory ValuationThe Company values its inventory at the lower of cost or net realizable value. The Company performs a quarterly assessment of its inventory value taking into consideration factors such as inventory reliability, future demand for the inventory, expected new product introductions, competitive pressures and numerous other factors. A change to these assumptions could have an impact on the valuation of inventory and have a resulting impact on margins.

GoodwillGoodwill is the residual amount that results when the purchase price of an acquired business exceeds the sum of the amounts allocated to the assets acquired, less liabilities assumed, based on their fair values. The amount of goodwill disclosed on the consolidated balance sheets has changed during the year due to foreign exchange.

Goodwill is not amortized and is tested for impairment annually, or more frequently, if events or changes in circumstances indicate that the asset might be impaired. The impairment test is carried out in two steps. In the fi rst step, the carrying amount of the reporting unit is compared with its fair value. When the fair value of a reporting unit exceeds its carrying amount, goodwill of the reporting unit is considered not to be impaired and the second step of the impairment test is unnecessary. The second step is carried out when the carrying amount of a reporting unit exceeds its fair value, in which case, the implied fair value of a reporting unit’s goodwill is compared with its carrying amount to measure the amount of the impairment loss, if any. The implied fair value of goodwill is determined in the same manner as the value of goodwill is determined in a business combination, using the fair value of the reporting unit as if it were the purchase price. When the carrying amount of reporting unit goodwill exceeds the implied fair value of the goodwill, an impairment loss is recognized in an amount equal to the excess and is presented as a separate line in the statement of operations and comprehensive income. The Company conducted its annual goodwill assessment in the fourth quarter of fi scal 2008 and fi scal 2007 and concluded there was no impairment in the recorded value of the goodwill.

Income TaxesThe Company records a valuation allowance against future income tax assets when Management believes it more likely than not that some portion or all of the future income tax assets will not be realized. Management considers factors such as the projected future taxable income in each jurisdiction, the nature of income tax assets, the carryforward periods of use and tax planning strategies. Management discretion is utilized in this determination unless accounting or tax rules prevail. A change in these factors could have an impact on the estimated valuation allowance and income tax expense.

forPDF_Lorex_AR.indd Sec1:16forPDF_Lorex_AR.indd Sec1:16 1/15/09 1:08:37 PM1/15/09 1:08:37 PM

L O R E X T E C H N O L O G Y I N C . A N N U A L R E P O R T 2 0 0 8 1 7

CHANGES IN ACCOUNTING POLICIES

The Canadian Institute of Chartered Accountants (CICA) issued a new accounting standard, Section 1535, Capital Disclosures, which requires the disclosure of both qualitative and quantitative information that provides users of fi nancial statements with information to evaluate the entity’s objectives, policies and processes for managing capital. This new section became effective for the Company beginning October 1, 2007. Following is the disclosure in respect of the new section:

Capital Disclosures:The Company funds the day-to-day operating activities by its working capital through managing the fl ow of cash and receivable collections in meeting its short-term fi nancial obligations.

The Company’s current principal source of capital for fi nancing beyond working capital is from the two credit facilities established with the primarily lender. Management strives to maintain excess availability under its revolving credit facility to meet unforeseeable business events. This is achieved through effective management of receivables and inventory, which facilitates cash fl ows and maintains the good quality of collateral pledged against the credit loan to support for excess availability.

As at September 30, 2008, the Company’s principal sources of liquidity included unrestricted cash of approximately $347,000 and excess availability under its credit facility of approximately $1.3 million.

Based on its current projections, the Company believes specifi c covenants will not be met in the fi rst quarter of 2009. Please see discussion in the Financial section on page 9.

The Company’s policy is to maintain a suffi cient capital base in order to preserve investor, creditor and market confi dence and to sustain future development of the business. Management monitors investor activity by noting signifi cant market transactions and ongoing trading activity. The Board’s strategy is to not pay dividends and to use positive cash fl ow to fund growth and reduce bank debt.

The Company monitors imposed debt covenants as established pursuant to its credit facility agreement. The requirements include quarterly net income after tax, quarterly net cash fl ow and minimum tangible net worth, and specifi c levels are established between the Company and its lender for each quarter, generally on the basis of the Company’s forecasts set in advance. The Company was in compliance with its bank covenants at September 30, 2008. The Company acknowledges the covenants for the fi rst quarter of fi scal 2009 will require adjustment due to the Company’s expectation that current covenants will not be met. The Board recognizes that the Company may need additional external fi nancing to support the Company’s future business activities as the breach may result in immediate repayment if the covenant is not waived or amended.

Financial InstrumentsTwo new accounting standards were issued by the CICA: Section 3862, Financial Instruments – Disclosures, and Section 3863, Financial Instruments – Presentation. These sections replace Section 3861, Financial Instruments – Disclosure and Presentation, once adopted. The objective of Section 3862 is to provide users with information to evaluate the signifi cance of the fi nancial instruments on the entity’s fi nancial position and performance, the nature and extent of risks arising from fi nancial instruments and how the entity manages those risks. The provisions of Section 3863 deal with the classifi cation of fi nancial instruments, related interest, dividends, losses and gains, and the circumstances in which fi nancial assets and fi nancial liabilities are offset. These new sections became effective for the Company beginning October 1, 2007. Following are disclosures in respect of these sections:

Credit RiskCredit risk arises from the possibility that certain parties will be unable to discharge their obligations. The Company routinely assesses the fi nancial strength of its customers and mitigates against identifi ed exposure primarily by lowering credit limits and/or reducing or ending business activity with high-risk accounts.

Foreign Exchange RiskA portion of the Company’s Canadian subsidiaries’ purchases, sales and borrowings is denominated in Canadian dollars. This results in cash and cash equivalents, accounts receivable, accounts payable and accrued liabilities balances being denominated in Canadian dollars. Changes in the value of the Canadian dollar versus the U.S. dollar has an impact on the fi nancial results reported by the Company.

A 10% strengthening of the Canadian dollar against the foreign currencies as per below at September 30, 2008, would have increased (decreased) equity and net income by the amounts shown below. This analysis assumes that all other variables remain constant.

NET INCOME

12 months ending September 30, 2008 (in U.S. dollars) 51,944

forPDF_Lorex_AR.indd Sec1:17forPDF_Lorex_AR.indd Sec1:17 1/15/09 1:08:37 PM1/15/09 1:08:37 PM

A N N U A L R E P O R T 2 0 0 8 L O R E X T E C H N O L O G Y I N C . 1 8

Liquidity RiskAs at September 30, 2008, the Company’s principal sources of liquidity included unrestricted cash of approximately $347,000 and excess availability under its credit facility of $1.3 million. The credit line is secured by the accounts receivable and inventory of three of the Company’s subsidiaries. Based on its current projections, the Company believes specifi c covenants will not be met in the fi rst quarter of 2009. Please see discussion in the Financial section on page 9.

In maintaining a suffi cient liquidity level, the Company manages timely accounts receivable collection and inventory turnover to facilitate cash fl ows and to sustain excess availability. In an environment of economic uncertainty, the Company is subject to an increased risk of customer payment defaults or more delayed customer payment patterns, which could result in a reduced borrowing base and lower availability. The Company actively assesses the creditworthiness of its customers and adjusts credit limits where it considers appropriate. In some cases, this may limit the level of shipments the Company will make to a customer, which would also contribute to reduced cash fl ow and availability due to lower revenue.

The future minimum operating lease commitments and contractual repayments on bank loans for the next fi ve years are as follows:

2009 2010

$ $

Revolving credit facility 5,784,571Term debt 666,672 444,432Accounts payable As due Operating lease commitment 251,572

Interest Rate RiskThe Company is exposed to interest rate risks arising from the $13,000,000 revolving credit facility that bears interest at the lender’s prime rate plus 1.5% and the $2,000,000 credit loan that bears interest at the lender’s prime rate plus 3%. Unfavourable changes in the applicable interest rate may result in an increase in interest expense. The Company does not use derivative instruments to reduce its exposure to interest rate risk.

As at September 30, 2008, the Company had $5,784,571 outstanding under the revolving credit facility and an unamortized balance of $1,111,104 under the credit loan.

Cash fl ow sensitivity analysis on variable credit facilities:

NET INCOME

100 BP 100 BP

INCREASE DECREASE

$ $

12 months ending September 30, 2008 (75,754) 75,754

InventoryIn March 2007, the CICA issued Handbook Section 3031, Inventories, which replaces Section 3030, Inventories. Under this new section, inventories are required to be measured at the lower of cost or net realizable value, which is different from the existing guidance of the lower of cost or market. The new section contains guidance on the determination of cost and also requires the reversal of any writedowns previously recognized. Certain minimum disclosures are required, including the accounting policies used, carrying amounts, amounts recognized as an expense and writedowns. The Company has adopted this policy and the impact on the fi nancial statements was not signifi cant.

forPDF_Lorex_AR.indd Sec1:18forPDF_Lorex_AR.indd Sec1:18 1/15/09 1:08:37 PM1/15/09 1:08:37 PM

L O R E X T E C H N O L O G Y I N C . A N N U A L R E P O R T 2 0 0 8 1 9

RECENT ACCOUNTING PRONOUNCEMENTS

Convergence to International Financial Reporting Standards (IFRS)In January 2006, the CICA Accounting Standards Board (AcSB) adopted a strategic plan for the direction of accounting standards in Canada. The AcSB has recently confi rmed that accounting standards in Canada for public companies are to converge with IFRS effective for fi scal periods beginning on or after January 1, 2011. The Company has assembled an IFRS transition team, which has started to assess the impact of the convergence of Canadian GAAP and IFRS, and will implement the new IFRS standards.

Goodwill and Intangible AssetsIn February 2008, the CICA issued Handbook Section 3064, Goodwill and Intangible Assets. Section 3064 states that upon their initial identifi cation, intangible assets are to be recognized as assets only if they meet the defi nition of an intangible asset and the recognition criteria. This section also provides further information on the recognition of internally generated intangible assets (including research and development costs). As for subsequent measurement of intangible assets, goodwill and disclosure, Section 3064 carries forward the requirements of the old Section 3062, Goodwill and Other Intangible Assets. The new section will become effective on October 1, 2008, for the Company. The Company expects that the impact on the fi nancial statements will not be signifi cant.

RISK FACTORS

The risks and uncertainties described below are not the only risk factors affecting the Company. Additional risks and uncertainties not presently known to the Company or that are currently deemed immaterial also may impair the Company’s business operations. If any of the following risks actually occur, the business, results of operations and fi nancial condition of the Company could be materially and adversely affected.

Financing RisksThe Company is fi nanced primarily by two credit facilities with a lender that are subject to quarterly income, cash fl ow and tangible net worth covenants. Should the Company fail to meet any of its covenants or obtain waivers or amendments for breaches of covenants, its lender may request immediate repayment of amounts outstanding on the two credit facilities or impose more restrictive measures against the Company, which may limit operational effectiveness. In addition, the Company borrows on a base that is calculated using the accounts receivable of its North American operating companies and the inventory of LOREX Corporation and is subject to certain reserves and limitations. The Company could be required to obtain additional borrowings from its existing lender or through other fi nancing should the borrowing formula be insuffi cient to support normal business activities.

Business RisksAlthough the market for the Company’s products is expanding, its ability to remain competitive is dependent upon assessing changing markets and providing new products and functionality. The Company believes that its future success depends upon its ability to enhance current products and develop and introduce new product offerings with enhanced performance and functionality at competitive prices. While there can be no assurances that the Company will be able to develop new products to meet changes in the marketplace or that the sale of such new products will be profi table, the Company pays close attention to and anticipates changes in the market. Sales management meets regularly with its customers to identify current and anticipated end-user requirements.

Supplier and Customer RisksThe Company purchases its products from a number of select manufacturers in the Far East. The Company relies on these sources for product development, product reliability, timely delivery and future product warranty support. If a supplier were to discontinue, restrict the supply or interrupt servicing repairs, the Company would attempt to replace the supplier in a timely manner. If it could not do so, the Company’s business may be harmed by the resulting product manufacturing and delivery delays. In addition, the failure of the Company’s products to perform to customer/consumer expectations could give rise to product warranty claims and/or returns. To minimize this production risk, the Company contracts with a number of sources to perform its manufacturing requirements and performs quality assurance testing in the Far East and in North America. In addition to these risks, the Company relies on its customers honouring their purchase orders. Should a customer fail to honour its order, the Company would be required to sell its overstock to different customers. To mitigate this risk, the Company sources product that can be sold to different customers in a variety of channels.

forPDF_Lorex_AR.indd Sec1:19forPDF_Lorex_AR.indd Sec1:19 1/15/09 1:08:37 PM1/15/09 1:08:37 PM

A N N U A L R E P O R T 2 0 0 8 L O R E X T E C H N O L O G Y I N C . 2 0

Competitive and Industry RisksThe Company expects that additional competition may develop from existing surveillance/security companies and from new entrants as demand for product expands and the market for these products becomes more established. Certain of the Company’s competitors have greater fi nancial resources than the Company and may be able to sustain recurring losses to establish market share at the Company’s expense. Competition may force price reductions affecting gross margins. The Company must continue to innovate with newer technology to maintain and expand its customer base. The demand for security solutions by small business in a challenging economic environment may affect the revenues of the Company.

Customer Concentration RisksThe Company is dependent on a few customers for the majority of its products. In fi scal 2008, 10 customers accounted for approximately 67% of total sales. One of these customers accounted for approximately 26% of total sales. In the prior-year quarter, this customer represented approximately 32% of total sales. A reduction in shipments to this customer had a signifi cant effect on the Company’s overall revenue and profi tability for the reporting period. Management has taken steps to increase shipments with this customer and continues to add to its customer base in order to reduce its customer concentration risk. If any signifi cant customer discontinues its relationship with the Company for any reason or signifi cantly reduces expected purchase commitments for the Company’s products, the business prospects and corresponding fi nancial condition could be materially adversely affected.

Foreign Exchange RisksThe Company generates approximately 88% of its revenues in U.S. dollars, and product purchases are transacted in U.S. dollars. As a result, the Company reports its fi nancial results in U.S. dollars. However, certain expenses incurred by the Company, primarily salaries to Canadian employees, are paid in Canadian dollars. Changes in the value of the Canadian dollar versus the U.S. dollar has an impact on the fi nancial results reported by the Company. The Company does not currently enter into any foreign exchange contracts to hedge against currency risk, but may do so in the future.

Reliance on Key Employees and Third-Party RelationshipsThe Company’s ability to develop and sell its products will depend, to a great extent, on its ability to attract and retain highly qualifi ed personnel and to develop and maintain third-party relationships for assistance in the conduct of research efforts, product development and manufacturing and sales support. Competition for such personnel and relationships is intense. The Company is highly dependent on the principal members of its management staff, as well as its third-party relationships, the loss of whose services might impede the achievement of development objectives. The persons working with the Company are affected by a number of infl uences outside of the control of the Company. The loss of key employees and/or key collaborators may affect the speed and success of product development. Although the Company believes that its collaborative partners will have an economic motivation to commercialize the Company’s product included in any collab-orative agreement, the amount and timing of resources diverted to these activities generally is expected to be controlled by the third party.

Patents and Proprietary TechnologyThe Company has risk related to its ability to obtain patents, maintain trade secret protection and operate without infringing the rights of third parties. The Company has fi led applications for patents in certain jurisdictions. There can be no assurance that the Company’s existing patent applications will be allowed, that the Company will develop future proprietary products that are patentable, that any issued patents will provide the Company with any competitive advantages or will not be successfully challenged by any third parties, or that the patents of others will not have an adverse effect on the ability of the Company to do business. In addition, there can be no assurance that others will not independently develop similar products or duplicate some or all of the patent protection held by the Company. Furthermore, there can be no assurance that the confi dentiality of the Company’s trade secrets can be maintained or that such trade secrets will not be or have not already been independently discovered by others.

In addition, the Company may be required to obtain licences under patents or other proprietary rights of third parties. No assurance can be given that any licences required under such patents or proprietary rights will be available on terms acceptable to the Company. If the Company does not obtain such licences, it could encounter delays in introducing one or more of its products to the market while it attempts to design around such patents or could fi nd that the development, manufacture or sale of products requiring such licences could be foreclosed. In addition, the Company could incur substan-tial costs in defending itself in claims brought against the Company on such patents or in claims in which the Company attempts to enforce its own patents against other parties.

forPDF_Lorex_AR.indd Sec1:20forPDF_Lorex_AR.indd Sec1:20 1/15/09 1:08:37 PM1/15/09 1:08:37 PM

L O R E X T E C H N O L O G Y I N C . A N N U A L R E P O R T 2 0 0 8 2 1

DERIVATIVE INSTRUMENTS AND OFF-BALANCE-SHEET ARRANGEMENTS

As at September 30, 2008, the Company was not party to any derivative instruments or off-balance-sheet arrangements.

DISCLOSURE CONTROLS AND INTERNAL CONTROLS

The Company’s Chief Executive Offi cer and Chief Financial Offi cer are responsible for establishing and maintaining the Company’s disclosure controls and procedures and internal control over fi nancial reporting for the issuer. They are assisted in this responsibility by the senior management team.

The Chief Executive Offi cer and Chief Financial Offi cer, after evaluating the effectiveness of the Company’s disclosure controls and procedures and the design of internal controls at September 30, 2008, have concluded that the Company’s disclosure controls and the design of internal control procedures were adequate and effective to ensure that material information relating to the Company and its subsidiaries would have been known to them.

OUTLOOK

Our current projections indicate continuing increases in demand through next year for surveillance and security solutions despite forecast declines in consumer spending. Management has developed new product options at lower price points to address budget-conscious consumers and will continue its campaigns to attract new business from the e-commerce market and the professional security integrator. Management recognizes the importance of maintaining adequate capital to support the Company’s growth plans and/or the possibility of reduced demand. Management plans to address a possible shortfall of working capital by securing additional funding, increasing operating revenue and reducing operating expenses.

ADDITIONAL INFORMATION

Further information on the Company, including its Annual Information Form, is available on SEDAR at www.sedar.com.

Henry Schnurbach Jordan SchwartzChief Executive Offi cer Chief Financial Offi cer

December 3, 2008

forPDF_Lorex_AR.indd Sec1:21forPDF_Lorex_AR.indd Sec1:21 1/15/09 1:08:37 PM1/15/09 1:08:37 PM

A N N U A L R E P O R T 2 0 0 8 L O R E X T E C H N O L O G Y I N C . 2 2

Management is responsible for the preparation of the accompanying consolidated fi nancial statements and all other information contained in the Annual Report. The fi nancial statements have been prepared in conformity with Canadian generally accepted accounting principles, which involve Management’s best estimates and judgments based on available information.

Management maintains a system of internal accounting controls designed to provide reasonable assurance that transactions are authorized, assets are safeguarded and fi nancial records are reliable for preparing fi nancial statements.

The Board of Directors is responsible for ensuring that Management fulfi lls its responsibilities for fi nancial reporting and internal controls. The Board is assisted in exercising its responsibilities through the Audit Committee of the Board. The Committee meets periodically with Management and the independent auditors to satisfy itself that Management’s responsibilities are properly discharged and to recommend approval of the consolidated fi nancial statements to the Board.

KPMG, LLP were appointed as the Company’s auditors in 2003. Their report on the accompanying consolidated fi nancial statements follows. Their report outlines the extent of their examination, as well as an opinion on the fi nancial statements.

Henry Schnurbach Jordan SchwartzChief Executive Officer Chief Financial Officer

FINANCIALSTATEMENTSRESPONSIBILITY

forPDF_Lorex_AR.indd Sec1:22forPDF_Lorex_AR.indd Sec1:22 1/15/09 1:08:38 PM1/15/09 1:08:38 PM

L O R E X T E C H N O L O G Y I N C . A N N U A L R E P O R T 2 0 0 8 2 3

We have audited the consolidated balance sheets of Lorex Technology Inc. as at September 30, 2008 and 2007, and the consolidated statements of operations and comprehensive income, shareholders’ equity and cash fl ows for the years then ended. These fi nancial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these fi nancial statements based on our audits.

We conducted our audits in accordance with Canadian generally accepted auditing standards. Those standards require that we plan and perform an audit to obtain reasonable assurance whether the fi nancial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the fi nancial statements. An audit also includes assessing the accounting principles used and signifi cant estimates made by management, as well as evaluating the overall fi nancial statement presentation.

In our opinion, these consolidated fi nancial statements present fairly, in all material respects, the fi nancial position of the Company as at September 30, 2008 and 2007, and the results of its operations and its cash fl ows for the years then ended in accordance with Canadian generally accepted accounting principles.

Chartered Accountants, Licensed Public Accountants

Toronto, CanadaDecember 3, 2008

AUDITORS’ REPORT TO THESHAREHOLDERS

forPDF_Lorex_AR.indd Sec1:23forPDF_Lorex_AR.indd Sec1:23 1/15/09 1:08:38 PM1/15/09 1:08:38 PM

A N N U A L R E P O R T 2 0 0 8 L O R E X T E C H N O L O G Y I N C . 2 4

FINANCIALSTATEMENTS Consolidated Financial Statements

forPDF_Lorex_AR.indd Sec1:24forPDF_Lorex_AR.indd Sec1:24 1/15/09 1:08:38 PM1/15/09 1:08:38 PM

L O R E X T E C H N O L O G Y I N C . A N N U A L R E P O R T 2 0 0 8 2 5

CONSOLIDATED BALANCE SHEETS(Expressed in U.S. dollars)

SEPTEMBER 30, 2008 AND 2007

2008 2007

$ $

ASSETS

Current assets: Cash and cash equivalents 347,467 420,212 Accounts receivable 5,349,192 7,851,180 Inventory (NOTE 4) 8,468,575 11,689,525 Prepaid expenses and deposits 865,259 759,990 Future income taxes (NOTE 12) 15,435 62,380 15,045,928 20,783,287

Capital assets (NOTE 5) 398,463 704,656Intangible assets (NOTE 6) 34,019 147,320Future income taxes (NOTE 12) 253,265 170,725Goodwill (NOTE 7) 718,309 761,336 16,449,984 22,567,324

LIABIL IT IES AND SHAREHOLDERS’ EQUITY

Current liabilities: Bank indebtedness (NOTE 8) 6,895,675 9,200,267 Accounts payable and accrued liabilities 5,375,340 6,657,755 12,271,015 15,858,022

Future income taxes (NOTE 12) 47,924 72,231

Long-term debt (NOTE 8) – 1,111,100

Shareholders’ equity: Capital stock (NOTE 9) 9,746,310 9,746,310 Contributed surplus 1,223,227 912,165 Accumulated other comprehensive income 1,495,486 1,498,271 Defi cit (8,333,978) (6,630,775) 4,131,045 5,525,971Going concern (NOTE 1)

Commitments and contingencies (NOTE 18)

16,449,984 22,567,324

See accompanying notes to consolidated fi nancial statements.

On behalf of the Board:

Henry Schnurbach Gerald SlanDirector Director

forPDF_Lorex_AR.indd Sec1:25forPDF_Lorex_AR.indd Sec1:25 1/15/09 1:08:39 PM1/15/09 1:08:39 PM

A N N U A L R E P O R T 2 0 0 8 L O R E X T E C H N O L O G Y I N C . 2 6

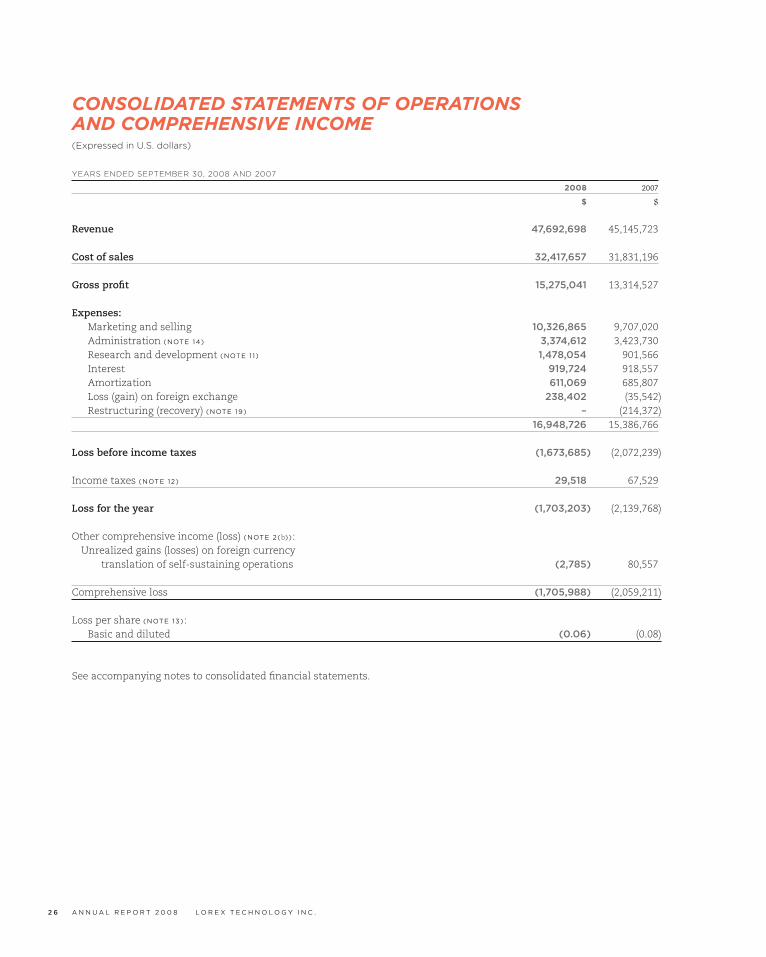

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME(Expressed in U.S. dollars)

YEARS ENDED SEPTEMBER 30, 2008 AND 2007

2008 2007

$ $

Revenue 47,692,698 45,145,723

Cost of sales 32,417,657 31,831,196

Gross profi t 15,275,041 13,314,527

Expenses: Marketing and selling 10,326,865 9,707,020 Administration (NOTE 14) 3,374,612 3,423,730 Research and development (NOTE 1 1) 1,478,054 901,566 Interest 919,724 918,557 Amortization 611,069 685,807 Loss (gain) on foreign exchange 238,402 (35,542) Restructuring (recovery) (NOTE 19) – (214,372) 16,948,726 15,386,766

Loss before income taxes (1,673,685) (2,072,239)

Income taxes (NOTE 12) 29,518 67,529

Loss for the year (1,703,203) (2,139,768)

Other comprehensive income (loss) (NOTE 2(b)): Unrealized gains (losses) on foreign currency translation of self-sustaining operations (2,785) 80,557

Comprehensive loss (1,705,988) (2,059,211)

Loss per share (NOTE 13): Basic and diluted (0.06) (0.08)

See accompanying notes to consolidated fi nancial statements.

forPDF_Lorex_AR.indd Sec1:26forPDF_Lorex_AR.indd Sec1:26 1/15/09 1:08:39 PM1/15/09 1:08:39 PM

L O R E X T E C H N O L O G Y I N C . A N N U A L R E P O R T 2 0 0 8 2 7

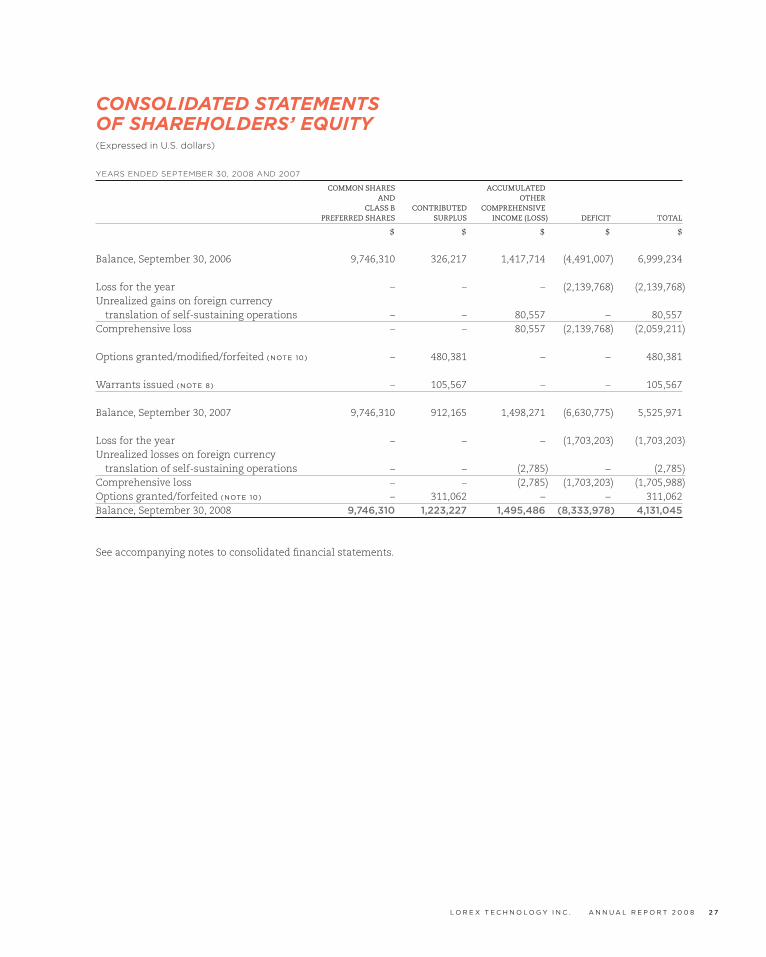

CONSOLIDATED STATEMENTS OF SHAREHOLDERS’ EQUITY(Expressed in U.S. dollars)

YEARS ENDED SEPTEMBER 30, 2008 AND 2007

COMMON SHARES ACCUMULATED AND OTHER CLASS B CONTRIBUTED COMPREHENSIVE PREFERRED SHARES SURPLUS INCOME (LOSS) DEFICIT TOTAL

$ $ $ $ $

Balance, September 30, 2006 9,746,310 326,217 1,417,714 (4,491,007) 6,999,234

Loss for the year – – – (2,139,768) (2,139,768)Unrealized gains on foreign currency translation of self-sustaining operations – – 80,557 – 80,557Comprehensive loss – – 80,557 (2,139,768) (2,059,211)

Options granted/modifi ed/forfeited (NOTE 10) – 480,381 – – 480,381

Warrants issued (NOTE 8) – 105,567 – – 105,567

Balance, September 30, 2007 9,746,310 912,165 1,498,271 (6,630,775) 5,525,971

Loss for the year – – – (1,703,203) (1,703,203)Unrealized losses on foreign currency translation of self-sustaining operations – – (2,785) – (2,785)Comprehensive loss – – (2,785) (1,703,203) (1,705,988)Options granted/forfeited (NOTE 10) – 311,062 – – 311,062Balance, September 30, 2008 9,746,310 1,223,227 1,495,486 (8,333,978) 4,131,045

See accompanying notes to consolidated fi nancial statements.

forPDF_Lorex_AR.indd Sec1:27forPDF_Lorex_AR.indd Sec1:27 1/15/09 1:08:40 PM1/15/09 1:08:40 PM

A N N U A L R E P O R T 2 0 0 8 L O R E X T E C H N O L O G Y I N C . 2 8

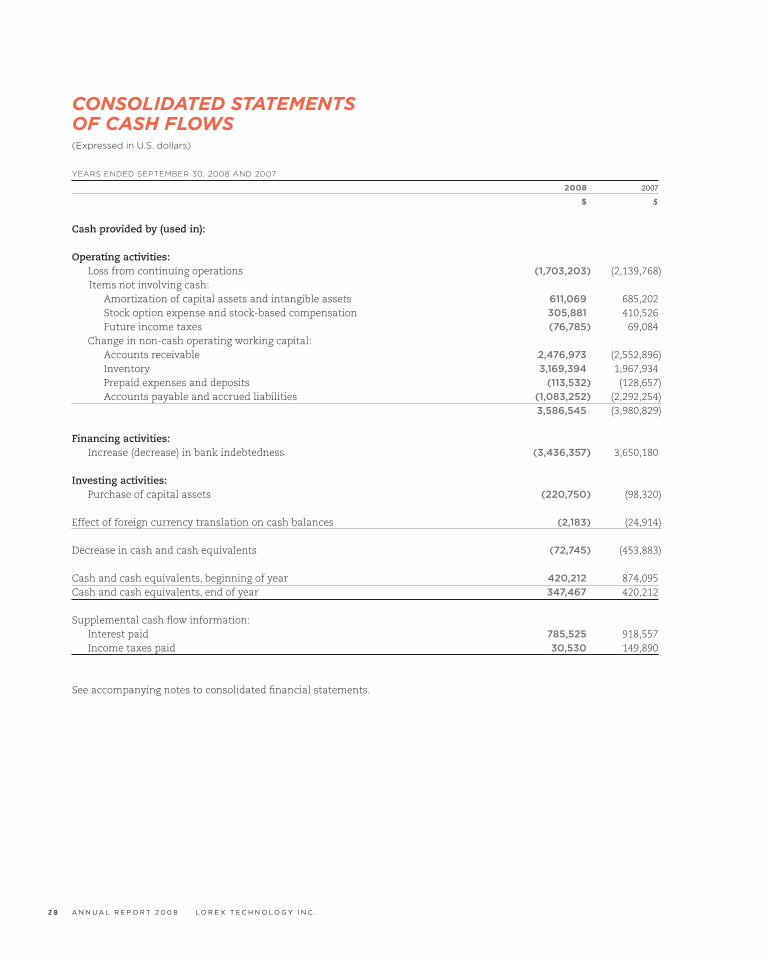

CONSOLIDATED STATEMENTSOF CASH FLOWS(Expressed in U.S. dollars)

YEARS ENDED SEPTEMBER 30, 2008 AND 2007

2008 2007

$ $

Cash provided by (used in):

Operating activities: Loss from continuing operations (1,703,203) (2,139,768) Items not involving cash: Amortization of capital assets and intangible assets 611,069 685,202 Stock option expense and stock-based compensation 305,881 410,526 Future income taxes (76,785) 69,084 Change in non-cash operating working capital: Accounts receivable 2,476,973 (2,552,896) Inventory 3,169,394 1,967,934 Prepaid expenses and deposits (113,532) (128,657) Accounts payable and accrued liabilities (1,083,252) (2,292,254) 3,586,545 (3,980,829)

Financing activities: Increase (decrease) in bank indebtedness (3,436,357) 3,650,180

Investing activities: Purchase of capital assets (220,750) (98,320)

Effect of foreign currency translation on cash balances (2,183) (24,914)

Decrease in cash and cash equivalents (72,745) (453,883)

Cash and cash equivalents, beginning of year 420,212 874,095Cash and cash equivalents, end of year 347,467 420,212

Supplemental cash fl ow information: Interest paid 785,525 918,557 Income taxes paid 30,530 149,890

See accompanying notes to consolidated fi nancial statements.

forPDF_Lorex_AR.indd Sec1:28forPDF_Lorex_AR.indd Sec1:28 1/15/09 1:08:40 PM1/15/09 1:08:40 PM

L O R E X T E C H N O L O G Y I N C . A N N U A L R E P O R T 2 0 0 8 2 9

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS(Expressed in U.S. dollars, unless otherwise noted)

YEARS ENDED SEPTEMBER 30, 2008 AND 2007

LOREX Technology Inc. (“LOREX” or the “the Company”) (TSX: LOX) provides businesses and consumers with leading-edge video surveillance security solutions and sells its products through two distinct market channels under the LOREX and Digimerge brands. The LOREX brand, which caters to both small business and consumer markets, is available in over 9,000 retail locations across North America and is gaining market presence in the U.K. The Digimerge division distributes its products through major distributors in both North America and Europe. Both groups concentrate on the sale of wired, wireless and IP security surveillance equipment, including cameras, digital video recorders and all-in-one systems.

1 . GOING CONCERN

These consolidated fi nancial statements have been prepared on a going-concern basis in accordance with Canadian generally accepted accounting principles (GAAP). The going-concern basis of presentation assumes that the Company will continue in operation for the foreseeable future and be able to realize its assets and discharge its liabilities and commitments in the normal course of business. There is substantial uncertainty about the appropriateness of the use of the going-concern assumption. Before adjusting for changes in working capital, the Company experienced a net loss and negative cash fl ows from operations for the year ended September 30, 2008. Based on the Company’s current projections, the Company believes it is unlikely that it will be in compliance with the existing quarterly fi nancial covenants beginning in the fi rst quarter of 2009. Failure to comply with these debt covenants could result in a requirement to immediately repay the bank loans. The Company has requested modifi cations to bank covenants, and the bank has accepted those amendments in the past. There is no certainty that the Company will be successful in obtaining modifi cations to these covenants in the event of a future covenant violation.

The ability of the Company to continue as a going concern and to realize the carrying value of its assets and discharge its liabilities when due is dependent on the successful completion of the actions taken or planned by Management that Management believes will mitigate the adverse conditions and events that raise doubt about the validity of the going-concern assumption used in preparing these consolidated fi nancial statements. There is no certainty that current strategies will be suffi cient to permit the Company to continue business operations beyond the foreseeable future since such strategies are contingent upon lender’s continuing support and the Company achieving profi tability.

The consolidated fi nancial statements do not refl ect adjustments that would be necessary if going-concern assumption were not appropriate. If the going-concern basis was not appropriate for these consolidated fi nancial statements, then adjustments would be necessary in the carrying value of assets and liabilities, the reported revenue and expenses and the balance sheet classifi cations used.

2 . S IGNIF ICANT ACCOUNTING POLICIES

(a) Basis of ConsolidationThe consolidated fi nancial statements include the accounts of the Company and its wholly owned subsidiaries: Lorex Canada Inc. (an Ontario corporation), LOREX Corporation (a Delaware corporation), Strategic Vista Corporation Limited (a Hong Kong corporation), Digimerge Technologies Inc. (an Ontario corporation), XBL Solutions Inc. (an Ontario corporation), and Strategic Vista Direct, Inc. (a Delaware corporation). Intercompany transactions and balances are eliminated on consolidation.

In fi scal 2004, Strategic Vista Corporation Limited entered into a joint venture to construct and operate a manufacturing facility in China. In fi scal 2006 the operations of the joint venture ceased, and the Company accounted for the joint venture as a discontinued operation. In fi scal 2007 the Company disposed of its interest in the joint venture.

(b) Foreign Currency TranslationThe U.S. dollar is the functional currency of certain of the Company’s subsidiaries, Digimerge Technologies Inc., LOREX Corporation and Strategic Vista Corporation Limited. For other U.S. subsidiaries that are considered fully integrated foreign operations with foreign currency transactions, non-Canadian-dollar monetary assets and liabilities are translated into Canadian dollars at the rate of exchange prevailing as at the consolidated balance sheet dates, while non-monetary assets and liabilities are translated at historical rates of exchange. Revenue and expenses are translated into Canadian dollars at the rate in effect at the date of transaction. Realized and unrealized foreign exchange gains and losses are included in loss for the year in which they occur.

forPDF_Lorex_AR.indd Sec1:29forPDF_Lorex_AR.indd Sec1:29 1/15/09 1:08:40 PM1/15/09 1:08:40 PM

A N N U A L R E P O R T 2 0 0 8 L O R E X T E C H N O L O G Y I N C . 3 0

The Company uses the U.S. dollar as its reporting currency for preparation of its consolidated fi nancial statements. Under this method, the Company and its subsidiaries that use the Canadian dollar as the functional currency translate all assets and liabilities at the year-end exchange rate, and all revenue and expense items are translated at an average rate of exchange for the year for U.S. dollar reporting. Exchange rate differences arising on translation are deferred as a separate component (accumulated other comprehensive income) of shareholders’ equity.

(c) Cash and Cash EquivalentsCash and cash equivalents include bank balances.

(d) InventoryInventory is stated at the lower of cost or net realizable value. Cost is determined on a weighted average basis. The Company has adopted the Canadian Institute of Chartered Accountants’ (CICA) Handbook Section 3031, Inventories, effective October 1, 2007.

(e) Capital and Intangible AssetsCapital and intangible assets are stated at cost. Amortization is calculated on a straight-line basis over the following terms: