Annual General Assembly - M.J. Maillis GroupAnnual General Assembly ... Core Product Range overview...

19

Annual General Assembly June 28, 2010

Transcript of Annual General Assembly - M.J. Maillis GroupAnnual General Assembly ... Core Product Range overview...

Annual General Assembly

June 28, 2010

22

Forward Looking Statement Disclaimer

This presentation, and comments made by management thereon, contains

forward-looking statements which are based on current expectations and

assumptions about future events. These forward-looking statements are

subject to risks and uncertainties - many of which are beyond M.J. Maillis

Group ability to control or estimate precisely - that could cause actual results to

differ materially from those expressed in the forward-looking statements.

You are cautioned not to place undue reliance on these forward-looking

statements, which speak only as of the date of this presentation. M.J. Maillis

Group does not undertake any obligation to publicly release any revisions to

these forward-looking statements to reflect events or circumstances after the

date of these materials.

33

Overview

• Issues of General Assembly

• Speech of Mr. Maillis

• Financial Results

• The Group’s Restructuring

• Approval of General Assembly’s issues

4

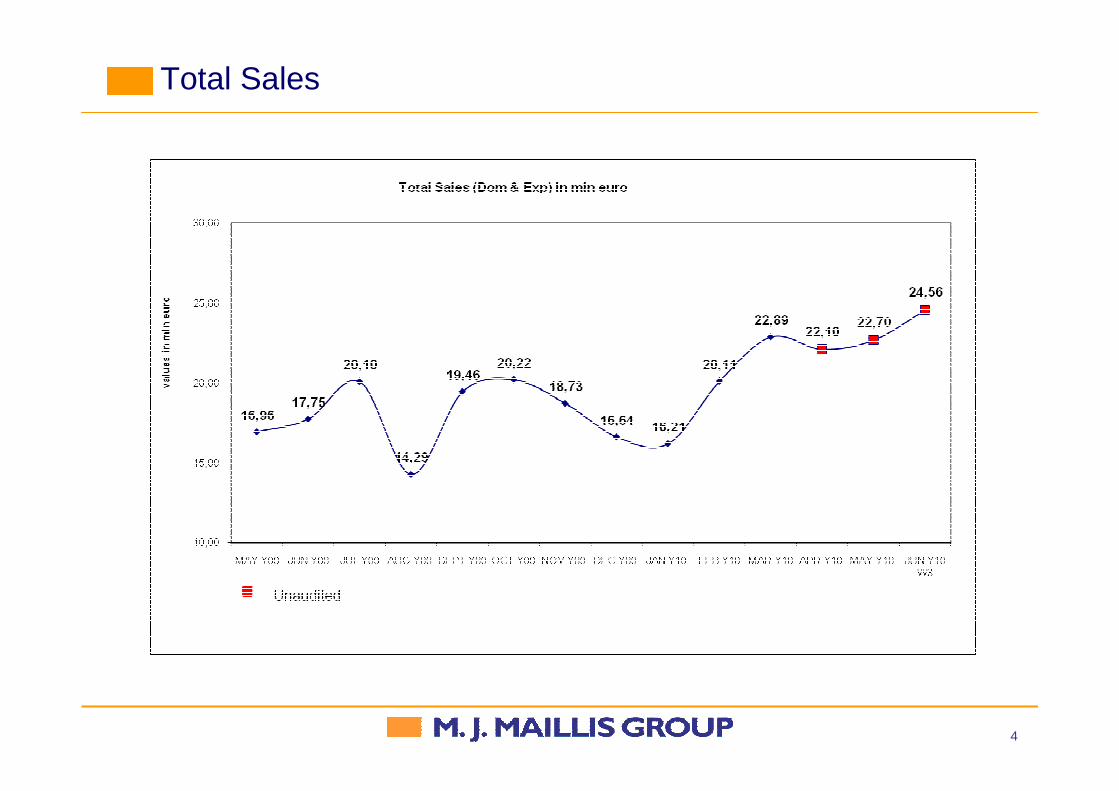

Total Sales

The Maillis Total Solution

5

Packaging Material

Packaging Equipment Service & Support

The Maillis Total Solution

The Business Model

We provide our clients around the world with comple te high technology and cost effective packaging solutions, that combine packaging equipme nt, packaging materials, service and support

6

Tools

Core Product Range overview - Strapping

SteelAluminium

ConstructionPaper & Corrugated

TimberCan & Bottles

Printing & Graphics

Products

Machines

Material

Systems

Migration to

KeyMarketsSectors

7

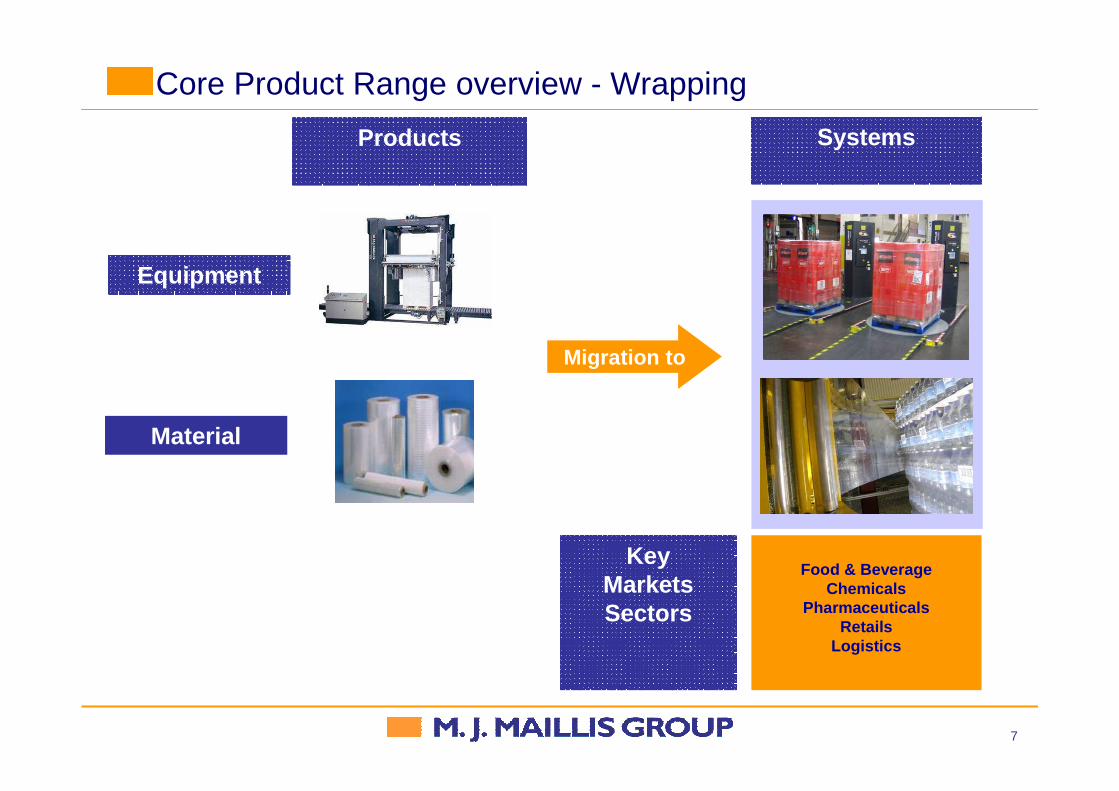

Core Product Range overview - Wrapping

Food & BeverageChemicals

PharmaceuticalsRetails

Logistics

Systems

KeyMarketsSectors

Equipment

Material

Migration to

Products

8

• Market Leader in product categories of Solutions

• Preferred Supplier by an increasing number of well recognized multinationals, through the Group’s Unique Value Proposition

Major Clients

9

Global Agreements with Multinational

�ArcelorMittal 2year global agreement

�US Steel 3year European agreement

�Corus Tata 3year global agreement

�Nestle Preferred supplier agreement for 460 factorie s

�Procter & Gamble Preferred European supplier agreem ent

�Unilever 2year global agreement, for 271 factories

�CRH 2year European agreement

�Alcoa 3year European agreement

�CCHBC 2year European agreement, for 28 countries

�Henkel 2year agreement, for 97 factories

�Reckitt Benckiser Exclusive film supplier in Europe

�Pepsico Annual European agreement

10

Financial Results

11

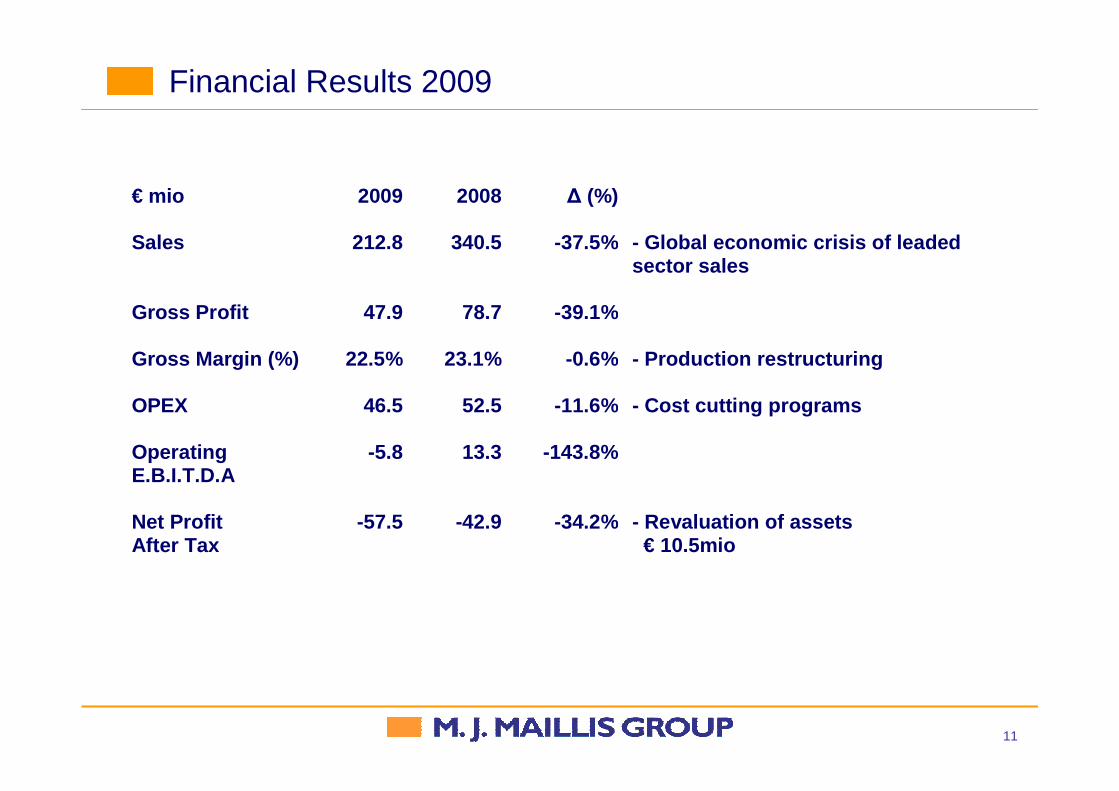

Financial Results 2009

€ mio 2009 2008 ∆ (%)

Sales

212.8 340.5 -37.5% - Global economic crisis of leaded sector sales

Gross Profit 47.9 78.7 -39.1%

Gross Margin ( %) 22.5% 23.1% -0.6% - Production restructuring

OPEX 46.5 52.5 -11.6% - Cost cutting programs

Operating E.B.I.T.D.A

-5.8 13.3 -143.8%

Net Profit After Tax

-57.5 -42.9 -34.2% - Revaluation of assets € 10.5mio

12

• Provisions

Substantial, non recurring, provisions booked in 2009 total amount of Euro 9.1mio for:

mio €- Stock near obsolescence 2.1- Restructuring cost 2.7- Bad debts 1.6

• Revaluation of assets

Write-off of goodwill amortization amounted to 11.5 mio € so as to adjust goodwill at the fair value as evaluated in the Group’s 5year business plan

mio €Austria 1.2France 3.0Germany 7.3

Financial Results 2009 - Notes

13

Upward trend in sales for the Q1 2010/ +5pp in Gross Margin / EBITDA Positive

€ mio Q1 2010 Q1 2009 ∆ (%)

Sales 59.2 51.5 +15%

Gross Profit 14.3 9.8 +45%

Gross Margin (%) 24.1% 19.1% +5 pp

OPEX11.1 11.5 -4%

Operating E.B.I.T.D.A 0.9 -3.3 +127%

E.B.I.T.D.A 0.5 -4,9 +109%

Financial Results Q1 2010

1414

Improved Sales & Margins

Improved margins as the result of production effici encies and higher volumes

mio€

51.5 51.9 53.9 55.6 59.2

9.8 11.513.7 12.9 14.3

-3.3 -2.5

0.4

-0.4

0.9

19.1%

22.2%

25.4%

23.3% 24.1%

Q1 09 Q2 09 Q3 09 Q4 09 Q1 10

mln €

Turnover Gross Margin

Operating E.B.I.T.D.A Gross Margin (%)

15

The Group’s Restructuring

16

The Group’s Restructuring

16/4/2010BoD approves Principal Debt Restructuring Proposal/ Main Shareholder

Proposal of the Group’s creditors, for the restructuring of debt liabilities of the MAILLIS Group, totaling approximately Euro 230 million. Basic points of the proposal:

• Capitalization of outstanding loans: For an amount of Euro 70 million with issuance of new common shares of the listed parent company to the Group’s creditors

• For the re-financing of the remaining outstanding loans:

- A syndicated loan of Euro 110 million- A bond loan, of Euro 50 million, with capitalizable (PIK) rate, convertible to new common shares of the listed parent company- New working capital line: For an amount of Euro 16 million for the financing of the Group’s growth

17

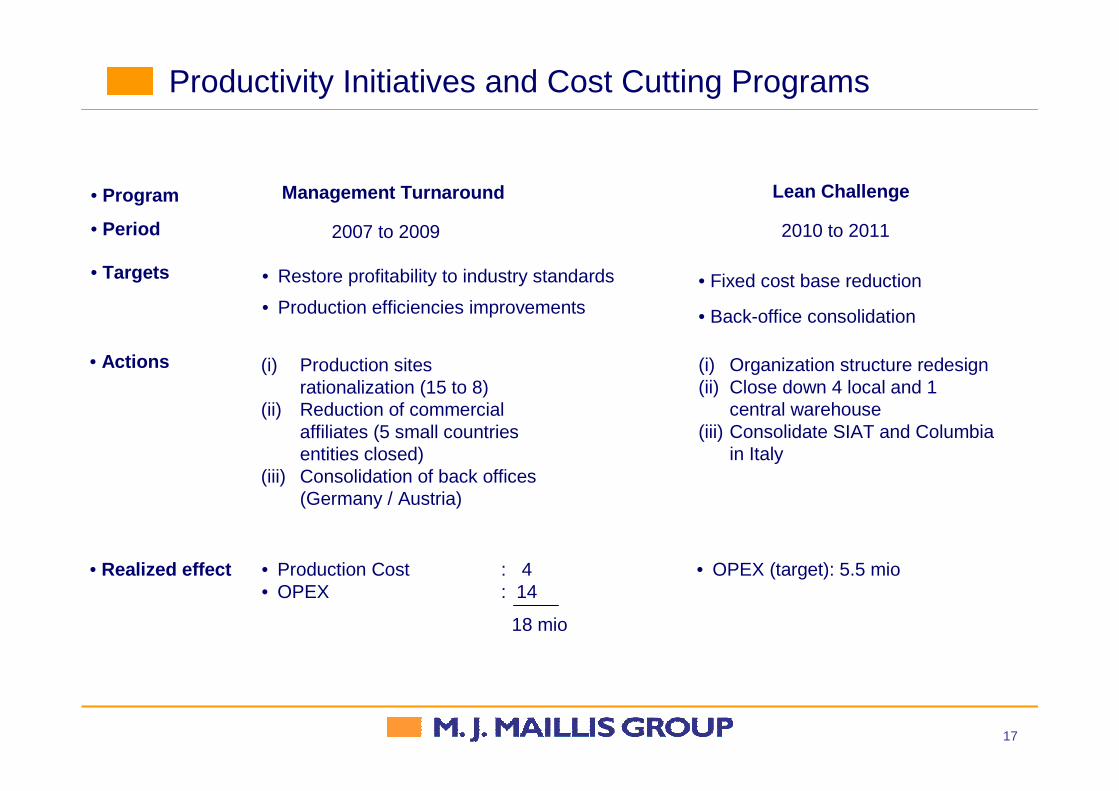

Productivity Initiatives and Cost Cutting Programs

Management Turnaround Lean Challenge

2007 to 2009

• Targets • Restore profitability to industry standards

• Production efficiencies improvements

2010 to 2011• Period

• Fixed cost base reduction

• Back-office consolidation

• Program

• Actions (i) Production sites rationalization (15 to 8)

(ii) Reduction of commercial affiliates (5 small countries entities closed)

(iii) Consolidation of back offices (Germany / Austria)

(i) Organization structure redesign(ii) Close down 4 local and 1

central warehouse(iii) Consolidate SIAT and Columbia

in Italy

• Realized effect • Production Cost : 4• OPEX : 14

18 mio

• OPEX (target): 5.5 mio

18

The New Group Structure

During the last four years, the Group having absorbed the impact of globalization, the changing conditions in the secondary packaging market, the global financial crisis and the breach of financial covenants, has undergone a major re-configuration:

• Products

• Customers

• Leveraged operating expenses(€ mio)

The Group is in a position to return to its previous profit levels, having adjusted to the new market conditions through a drastic turnaround, on the basis of its intact production capacity, brand name recognition and technological advantage, with further opportunity to expand to developing markets

• One-stop-shopping

• Multinational companies of global magnitude (complete solutions, cost effective)

““ OldOld ”” ““ NewNew””

• Providing the market with several stand-alone products

• Small/medium size customers / distributors (price per product)

• Structure

• Production units• Commercial companies• Personnel

15

2250

8 (6)

1650

24 19

• Corporate governance • Semi-independent affiliates

• Small customers with high margins through(Telesales)

61 47

• Centralized strategy / targets at a Group level

18

1919

Thank you