Annual Country Classification Review - S&P Dow … CLASSIFICATION CONSULTATION Annual Country...

27

COUNTRY CLASSIFICATION CONSULTATION Annual Country Classification Review Summary S&P Dow Jones Indices is undergoing its annual country classification review and is consulting with the investment community on the current standing of several countries. The S&P Dow Jones Global Equity Index Series is divided into three major country classifications – developed, emerging, and frontier. There are also other countries globally that we do not include in those categories, and consider them as “stand-alone” for index construction purposes. For each country, a number of factors are used in determining this classification, both quantitative and qualitative in nature. Additionally, the opinions and experiences of institutional investors are critically important in determining whether a market should be classified as developed, emerging, or frontier. S&P Dow Jones Indices responds to the institutional consensus by ensuring that the indices and associated data support the investment approaches institutions want to employ. We are seeking your feedback on certain countries currently under review. To ensure that consensus is obtained, please complete the questions included in this document and return to S&P Dow Jones Indices Client Services. Your feedback is of utmost importance to us and it may impact the country classification for the S&P Dow Jones Global Equity Index Series in 2015. Please respond by Tuesday, September 30, 2014. Please be advised that all comments will be reviewed and considered before a final decision is made, however S&P Dow Jones Indices makes no guarantees or is under any obligation to comply with any of the responses. The survey may result in no changes or outcome of any kind. Process S&P Dow Jones Indices uses quantitative data to initially assess market eligibility for the developed, emerging and frontier country classifications. Countries must meet certain initial criteria to be considered for the S&P Developed, Emerging or Frontier indices; they must meet a certain number of additional criteria to be considered specifically for the developed and emerging classifications, and must withstand a final measure of country economic status to be classified as developed. The table below summarizes these requirements.

-

Upload

truongtuong -

Category

Documents

-

view

221 -

download

1

Transcript of Annual Country Classification Review - S&P Dow … CLASSIFICATION CONSULTATION Annual Country...

COUNTRY CLASSIFICATION

CONSULTATION

Annual Country Classification Review

Summary

S&P Dow Jones Indices is undergoing its annual country classification review and is consulting with the investment community on the current standing of several countries. The S&P Dow Jones Global Equity Index Series is divided into three major country classifications – developed, emerging, and frontier. There are also other countries globally that we do not include in those categories, and consider them as “stand-alone” for index construction purposes. For each country, a number of factors are used in determining this classification, both quantitative and qualitative in nature.

Additionally, the opinions and experiences of institutional investors are critically important in determining whether a market should be classified as developed, emerging, or frontier. S&P Dow Jones Indices responds to the institutional consensus by ensuring that the indices and associated data support the investment approaches institutions want to employ.

We are seeking your feedback on certain countries currently under review. To ensure that consensus is obtained, please complete the questions included in this document and return to S&P Dow Jones Indices Client Services. Your feedback is of utmost importance to us and it may impact the country classification for the S&P Dow Jones Global Equity Index Series in 2015. Please respond by Tuesday, September 30, 2014.

Please be advised that all comments will be reviewed and considered before a final decision is made, however S&P Dow Jones Indices makes no guarantees or is under any obligation to comply with any of the responses. The survey may result in no changes or outcome of any kind.

Process

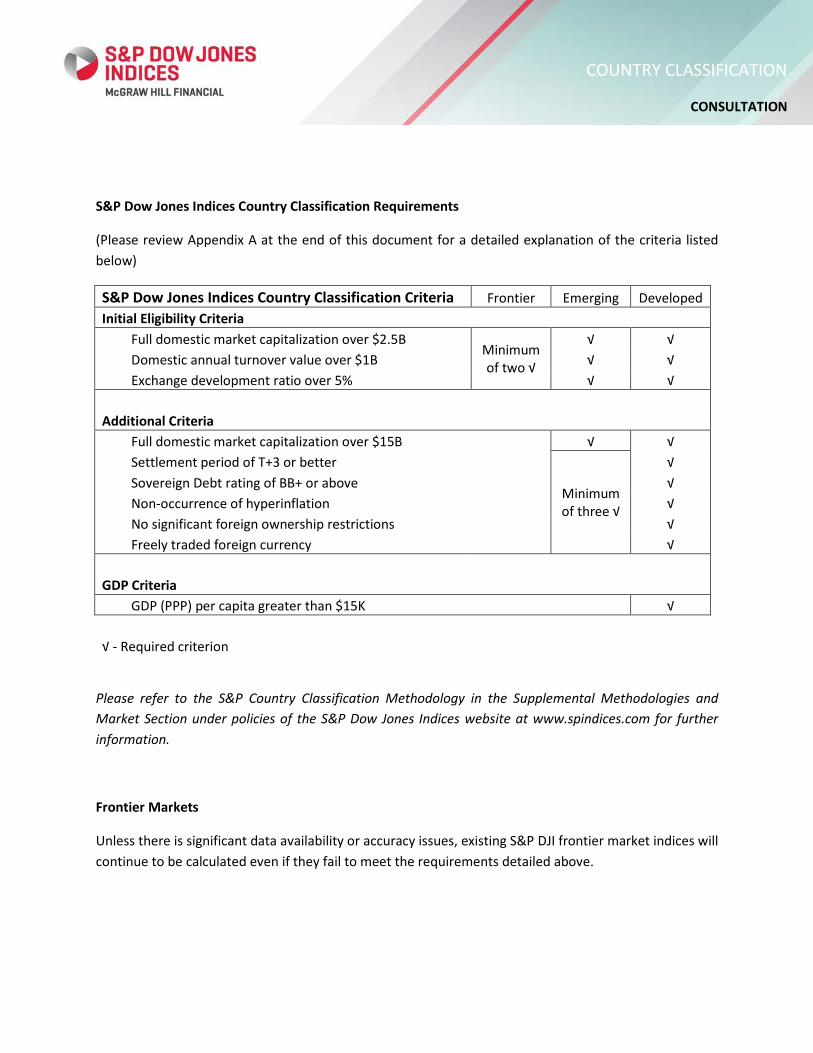

S&P Dow Jones Indices uses quantitative data to initially assess market eligibility for the developed, emerging and frontier country classifications. Countries must meet certain initial criteria to be considered for the S&P Developed, Emerging or Frontier indices; they must meet a certain number of additional criteria to be considered specifically for the developed and emerging classifications, and must withstand a final measure of country economic status to be classified as developed. The table below summarizes these requirements.

COUNTRY CLASSIFICATION

CONSULTATION

S&P Dow Jones Indices Country Classification Requirements

(Please review Appendix A at the end of this document for a detailed explanation of the criteria listed below)

S&P Dow Jones Indices Country Classification Criteria Frontier Emerging Developed Initial Eligibility Criteria

Full domestic market capitalization over $2.5B Minimum of two √

√ √ Domestic annual turnover value over $1B √ √ Exchange development ratio over 5% √ √

Additional Criteria

Full domestic market capitalization over $15B √ √ Settlement period of T+3 or better

Minimum of three √

√ Sovereign Debt rating of BB+ or above

√

Non-occurrence of hyperinflation

√ No significant foreign ownership restrictions

√

Freely traded foreign currency √

GDP Criteria

GDP (PPP) per capita greater than $15K √

√ - Required criterion

Please refer to the S&P Country Classification Methodology in the Supplemental Methodologies and Market Section under policies of the S&P Dow Jones Indices website at www.spindices.com for further information.

Frontier Markets

Unless there is significant data availability or accuracy issues, existing S&P DJI frontier market indices will continue to be calculated even if they fail to meet the requirements detailed above.

COUNTRY CLASSIFICATION

CONSULTATION

Consultation

We are seeking your feedback on several countries below which have been identified as either potential candidates to have their classification changed, or that warrant continued monitoring for future possible changes in classification. We have included some general information on the characteristics of the markets below that are likely relevant to the investment community. We greatly appreciate any feedback you may have, and please do not hesitate to include any additional information in your responses that we may not have considered.

List of countries under review:

• Egypt • Kuwait • Morocco • Nigeria • Oman • Pakistan • Palestine • Saudi Arabia • Zimbabwe

China A-Shares

China A-Shares are currently not eligible for S&P Dow Jones Indices branded indices due to their lack of practical investability. Based on the results from previous client consultations on this subject, China A-Shares will remain ineligible for the time being and the situation will continue to be monitored closely by S&P Dow Jones Indices. Please refer to the following link for the announcement of the results of our recent client consultation on this subject:

http://us.spindices.com/documents/index-news-and-announcements/20140714-spdji-china-a-shares.pdf?force_download=true

Russia/Ukraine

S&P DJI continues to closely monitor the situation in Russia and the ongoing conflict with Ukraine. If the situation were to escalate resulting in increased sanctions or other significant changes to the markets in either country, S&P DJI will likely consult with clients on the treatment of these countries in our global benchmark indices.

COUNTRY CLASSIFICATION

CONSULTATION

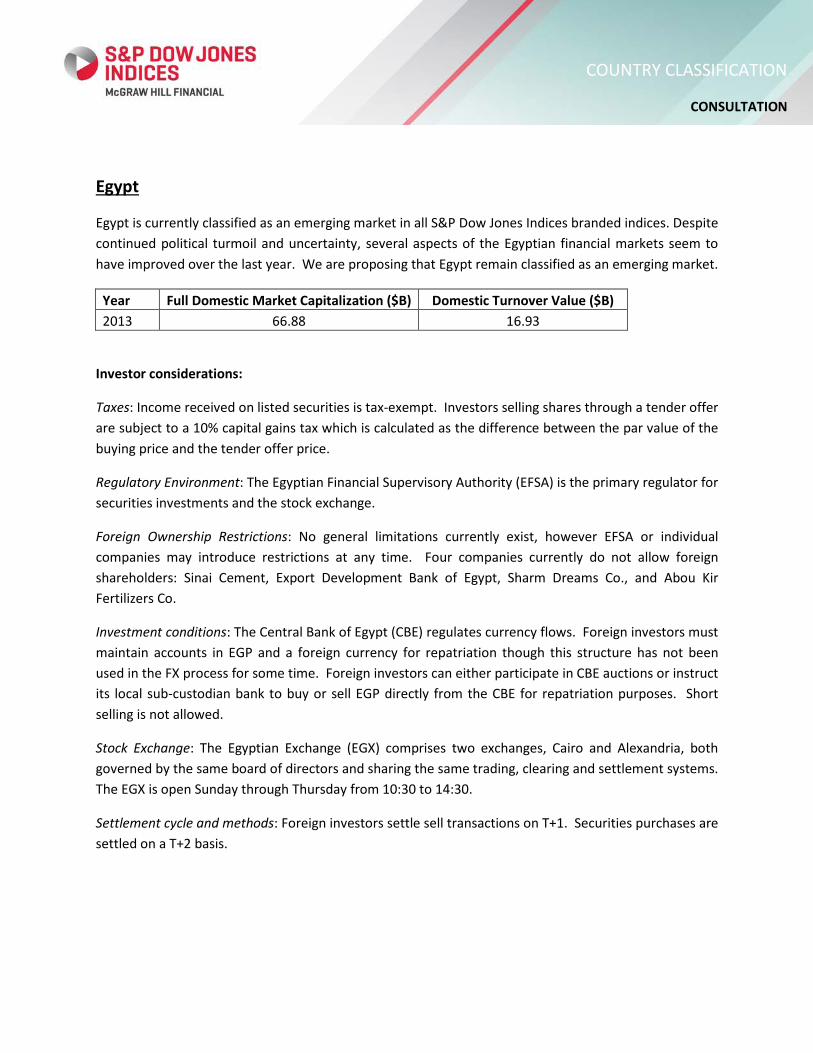

Egypt

Egypt is currently classified as an emerging market in all S&P Dow Jones Indices branded indices. Despite continued political turmoil and uncertainty, several aspects of the Egyptian financial markets seem to have improved over the last year. We are proposing that Egypt remain classified as an emerging market.

Year Full Domestic Market Capitalization ($B) Domestic Turnover Value ($B) 2013 66.88 16.93

Investor considerations:

Taxes: Income received on listed securities is tax-exempt. Investors selling shares through a tender offer are subject to a 10% capital gains tax which is calculated as the difference between the par value of the buying price and the tender offer price.

Regulatory Environment: The Egyptian Financial Supervisory Authority (EFSA) is the primary regulator for securities investments and the stock exchange.

Foreign Ownership Restrictions: No general limitations currently exist, however EFSA or individual companies may introduce restrictions at any time. Four companies currently do not allow foreign shareholders: Sinai Cement, Export Development Bank of Egypt, Sharm Dreams Co., and Abou Kir Fertilizers Co.

Investment conditions: The Central Bank of Egypt (CBE) regulates currency flows. Foreign investors must maintain accounts in EGP and a foreign currency for repatriation though this structure has not been used in the FX process for some time. Foreign investors can either participate in CBE auctions or instruct its local sub-custodian bank to buy or sell EGP directly from the CBE for repatriation purposes. Short selling is not allowed.

Stock Exchange: The Egyptian Exchange (EGX) comprises two exchanges, Cairo and Alexandria, both governed by the same board of directors and sharing the same trading, clearing and settlement systems. The EGX is open Sunday through Thursday from 10:30 to 14:30.

Settlement cycle and methods: Foreign investors settle sell transactions on T+1. Securities purchases are settled on a T+2 basis.

COUNTRY CLASSIFICATION

CONSULTATION

Weight in S&P Dow Jones Indices:

Benchmark Index Current Weight Projected Weight S&P Emerging BMI 0.348% S&P Frontier BMI 4.986%

• Should Egypt be classified as a Frontier or Emerging market?

COUNTRY CLASSIFICATION

CONSULTATION

Kuwait

Kuwait is currently classified as a frontier market in all S&P Dow Jones Indices branded indices. Despite meeting many of the criteria for emerging market status, there remains uncertainty on many issues regarding foreign investability. We are proposing that Kuwait remain classified as a frontier market.

Year Full Domestic Market Capitalization ($B) Domestic Turnover Value ($B) 2013 102.85 27.43

Investor considerations:

Taxes: A 15% withholding tax is applicable for dividends and interest income for non-resident investors. Residents of the Gulf Cooperation Council (GCC) may be eligible for tax exemption on dividend and interest income. Listed securities are exempt from capital gains tax. Unlisted securities are subject to a 15% capital gains tax.

Regulatory Environment: The Ministry of Commerce and Industry (MOCI) is the main regulator of the securities and financial market. The MOCI has delegated the regulation of capital markets to the Capital Markets Authority (CMA), who in turn supervises the Kuwait Stock Exchange (KSE)as they oversee all market participants doing business on the KSE. The KSE grants listing approvals.

Foreign Ownership Restrictions: Kuwait is open to some types of foreign investment, but with varied restrictions. The individual and aggregate foreign ownership limits for listed banks are 5% and 49% respectively. Government bureaucracy is prevalent. Regulations are not transparent and can be biased in favor of domestic interests. Non-GCC citizens may not own land. However, residents and non-residents may hold foreign exchange accounts, and there are no restrictions or controls on payments, transactions, transfers, or repatriation of profits.

As per Kuwait's Direct Foreign Capital Investment Law of 2001, foreign firms are permitted 100% foreign ownership in certain industries including infrastructure, insurance, IT and software development, hospitals and pharmaceuticals, air, land & sea freight, tourism, hotels, & entertainment, and housing projects & urban development. Projects involving oil and gas exploration and production are not authorized for foreign investment and must be approved by a separate law.

Investment Conditions: Securities lending and short selling are not allowed. Currency controls do not apply in the Kuwaiti market.

COUNTRY CLASSIFICATION

CONSULTATION

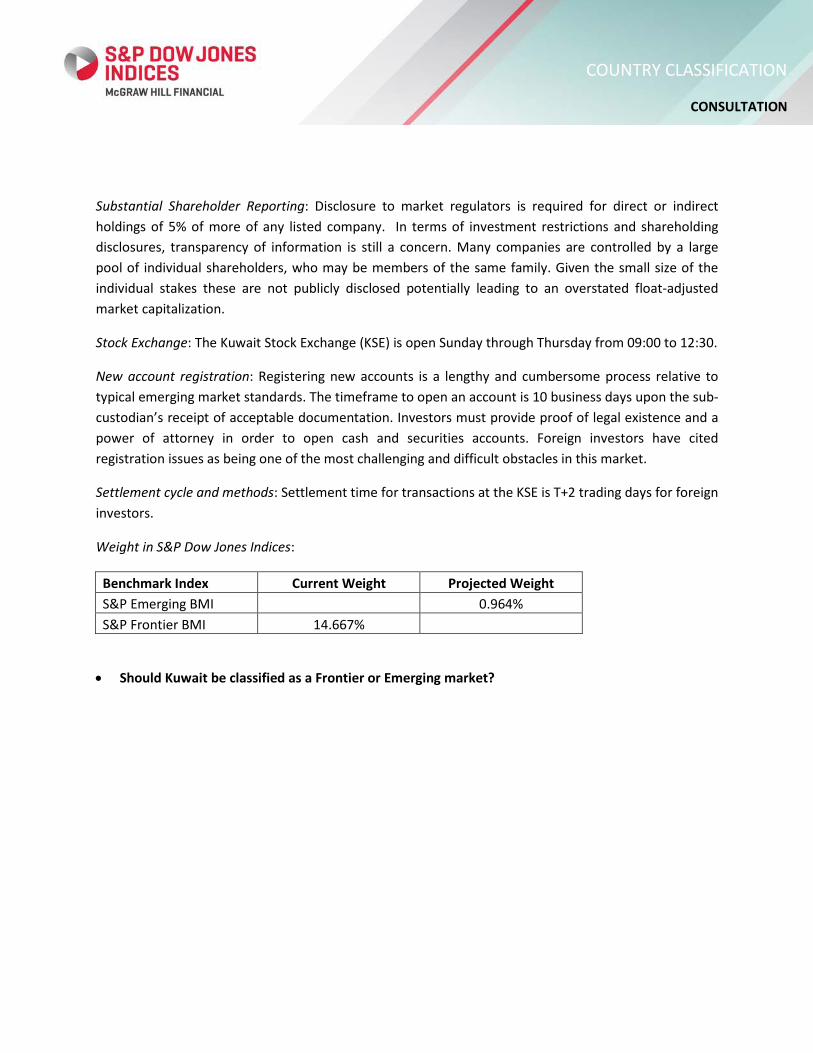

Substantial Shareholder Reporting: Disclosure to market regulators is required for direct or indirect holdings of 5% of more of any listed company. In terms of investment restrictions and shareholding disclosures, transparency of information is still a concern. Many companies are controlled by a large pool of individual shareholders, who may be members of the same family. Given the small size of the individual stakes these are not publicly disclosed potentially leading to an overstated float-adjusted market capitalization.

Stock Exchange: The Kuwait Stock Exchange (KSE) is open Sunday through Thursday from 09:00 to 12:30.

New account registration: Registering new accounts is a lengthy and cumbersome process relative to typical emerging market standards. The timeframe to open an account is 10 business days upon the sub-custodian’s receipt of acceptable documentation. Investors must provide proof of legal existence and a power of attorney in order to open cash and securities accounts. Foreign investors have cited registration issues as being one of the most challenging and difficult obstacles in this market.

Settlement cycle and methods: Settlement time for transactions at the KSE is T+2 trading days for foreign investors.

Weight in S&P Dow Jones Indices:

Benchmark Index Current Weight Projected Weight S&P Emerging BMI 0.964% S&P Frontier BMI 14.667%

• Should Kuwait be classified as a Frontier or Emerging market?

COUNTRY CLASSIFICATION

CONSULTATION

Morocco

Morocco is currently classified as an emerging market in all S&P Dow Jones Indices branded indices. Liquidity in this market has declined to very low levels over the last several years as seen in the table below; however it still meets the criteria for an Emerging Market. We are proposing that Morocco remain classified as an emerging market.

Year 2008 2009 2010 2011 2012 2013 2014

Domestic Turnover Value ($B)

12.923

5.810

4.245

4.059

3.949

3.046 3.200 *Liquidity data based on 12 months prior to the end of June in each respective year

Year Full Domestic Market Capitalization ($B) 2013 55.03

Investor considerations:

Taxes: Dividends paid to a non-resident are subject to a 15% withholding tax unless the rate is reduced under an applicable tax treaty. Capital gains tax rates are 15% on listed equities, 15% on mutual funds that invest at least 60% of their assets in listed equities, 20% on other mutual funds, and 20% on non-listed equities. There is also a .1% tax on all FX transactions that is incorporated into the FX rate and applies to all investor transactions of MAD.

Regulatory Environment: The Moroccan Securities Ethics Council (CDVM) is the primary market regulator. The Exchange Control Office ensures bank compliance with exchange control regulations.

Foreign Ownership Restrictions: Generally no restrictions on foreign ownership of Moroccan companies but Investors must get approval from regulators before investing in certain sectors such as mining, banking, and pharmaceuticals.

Investment Conditions: The financial instruments available are still basic. Short selling is not allowed. Stock lending is allowed but not market practice due to lack of regulation. Offshore foreign exchange transactions are not allowed. Onshore transactions must be related to a securities transaction. Transactions in foreign currency are monitored by the administration but generally not restricted.

Substantial Shareholder Reporting: Shareholders acquiring 5% of a bank security must notify the market regulator within 30 days of acquisition. There are also multiple ownership thresholds which require notification to regulators and the stock exchange if ownership either exceeds or has decreased and no longer exceeds. Fines may be levied for non-compliance.

COUNTRY CLASSIFICATION

CONSULTATION

Stock Exchange: The Casablanca Stock Exchange is open Monday to Friday from 09:00 to 15:30, with an OTC market also operating.

Settlement cycle and method: Settlement time for transactions at the Casablanca Stock Exchange is T+3. The basic principle governing the trade settlement system is simultaneous delivery of securities against cash payment (DVP settlement). The settlement of trades between market participants organized by the Casablanca Stock Exchange is carried out by delivery of securities against cash payment on a reciprocal and simultaneous basis. In addition, this must occur within a standard period of time which is the period which runs from the trade date to that of theoretical settlement.

Weight in S&P Dow Jones Indices:

Benchmark Index Current Weight Projected Weight S&P Emerging BMI 0.245% S&P Frontier BMI 3.560%

Should Morocco be classified as a Frontier or Emerging market?

COUNTRY CLASSIFICATION

CONSULTATION

Nigeria

Nigeria is currently classified as a frontier market in all S&P Dow Jones Indices branded indices. Despite many of the quantitative criteria being met for emerging market status, market accessibility issues remain which do not exist in other emerging markets. We are proposing that Nigeria remain classified as a frontier market.

Year Full Domestic Market Capitalization ($B) Domestic Turnover Value ($B) 2013 82 6.25

Investor considerations:

Taxes: Non-residents are subject to a withholding tax rate of 10% on dividends and corporate bond interest income but are exempt from withholding tax on government bond interest income. Investors that are residents of a country with a double taxation agreement in place with Nigeria can apply for a 2.5% tax rebate. Capital gains are tax-exempt for all investors.

Regulatory Environment: The securities market is regulated by the Nigerian Securities and Exchange Commission, while operations on the Nigerian Stock Exchange (NSE) are overseen jointly by the SEC and NSE. The Central Bank of Nigeria oversees the banking sector.

Foreign Ownership Restrictions: Foreign investors cannot purchase instruments on the Nigerian Stock Exchange’s negative list, which includes companies prospecting in crude oil and companies of a military and defensive nature.

Investment conditions: Short selling is not permitted on the NSE and free of payment trades are allowed only with prior approval from the NSE. Securities lending is allowed, however no providers currently offer this. Foreign currency can be repatriated without restriction; however capital flows must be reported to the central bank. Third-party FX transactions are permitted but with several documentation requirements. Offshore FX transactions are not allowed.

Substantial Shareholder Reporting: Brokers and issuers must report any transaction involving 5% or more of an issue to the SEC. Companies must also disclose shareholders who own 10% or more of its outstanding shares annually.

Stock Exchange: The Nigerian Stock Exchange is open for trading Monday through Friday from 09:30 to 14:30 via the computer terminals of the Automated Trading System, which offers automatic execution of trade orders.

Settlement cycle and methods: Securities transaction settlement occurs on T+3.

COUNTRY CLASSIFICATION

CONSULTATION

Weight in S&P Dow Jones Indices:

Benchmark Index Current Weight Projected Weight S&P Emerging BMI 0.828% S&P Frontier BMI 12.577%

Should Nigeria be classified as a Frontier or Emerging market?

COUNTRY CLASSIFICATION

CONSULTATION

Oman

Oman is currently classified as a frontier market in all S&P Dow Jones Indices branded indices. Despite many of the quantitative criteria being met for emerging market status, market accessibility issues remain which do not exist in other emerging markets. We are proposing that Oman remain classified as a frontier market.

Year Full Domestic Market Capitalization ($B) Domestic Turnover Value ($B) 2013 24.5 4.34

Investor considerations:

Taxes: Dividends and interest income are tax-exempt and capital gains tax is not applicable to foreign investors.

Regulatory Environment: The Capital Market Authority regulates the market policies and strategies, the listing and trading of shares, and licensing to brokers and market-makers.

Foreign Ownership Restrictions: Foreign ownership may be restricted by company bylaws which limit the aggregate ownership to between 49% and 70%. These limits are monitored by the Capital Market Authority.

Investment conditions: Short selling is prohibited. Currency controls do not apply in Oman, and both third-party and offshore FX transactions are permissible. Foreign investors must provide proof of legal existence if they wish to obtain an account for trading.

Substantial Shareholder Reporting: Investors must disclose ownership of 10% or more of a company’s issued capital to the CMA. Additional approvals are required from the CMA and/or the central bank if ownership exceeds certain thresholds or if the company owned is a bank.

Stock Exchange: The Muscat Securities Market trading system accepts electronic orders from brokers and is open from 10:00 to 13:00 Sunday through Thursday.

Settlement cycle and methods: Transaction settlement occurs on a T+3 basis.

COUNTRY CLASSIFICATION

CONSULTATION

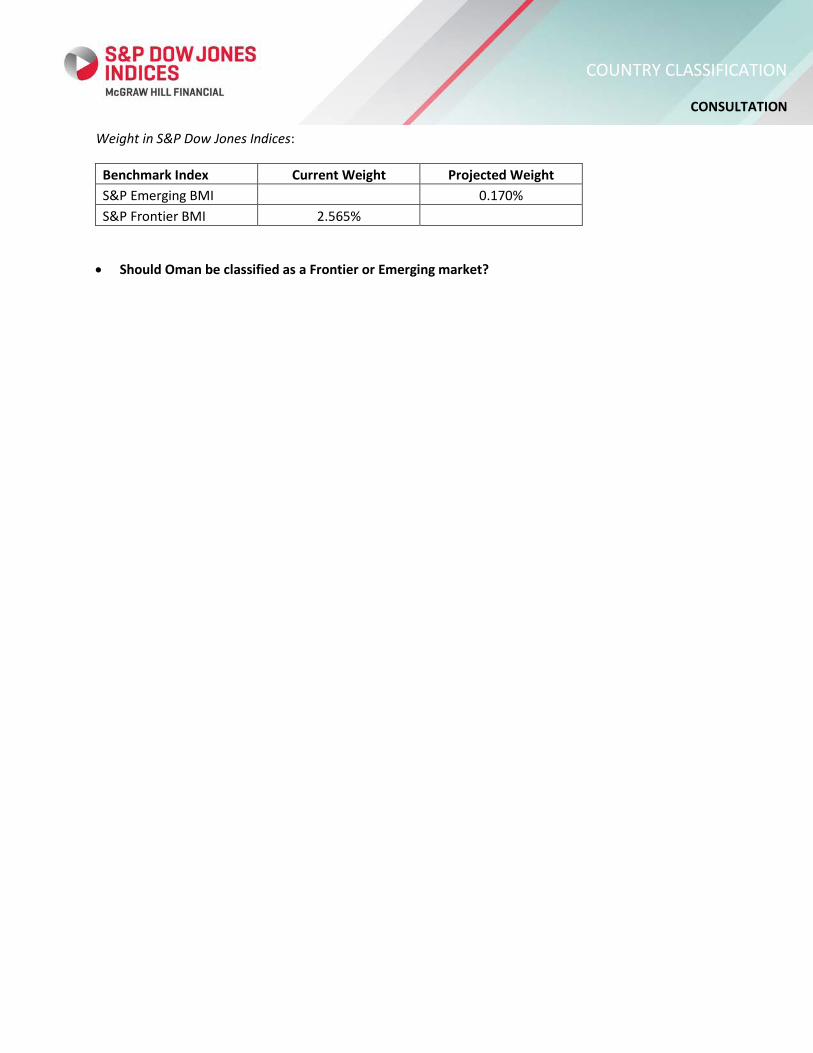

Weight in S&P Dow Jones Indices:

Benchmark Index Current Weight Projected Weight S&P Emerging BMI 0.170% S&P Frontier BMI 2.565%

• Should Oman be classified as a Frontier or Emerging market?

COUNTRY CLASSIFICATION

CONSULTATION

Pakistan

Pakistan is currently classified as a frontier market in all S&P Dow Jones Indices branded indices. Despite many of the quantitative criteria being met for emerging market status, market accessibility issues remain which do not exist in other emerging markets. We are proposing that Pakistan remain classified as a frontier market.

Year Full Domestic Market Capitalization ($B) Domestic Turnover Value ($B) 2013 58.64 17.26

Investor considerations:

Taxes: Withholding tax of 10% is applied to dividends; however certain scenarios may lower that rate to 7.5%. Capital gains generated from securities held for less than six months are subject to a 10% tax rate, those that are generated from securities held for 6 to 12 months are subject to an 8% tax rate, and securities held for longer than 12 months are exempt from tax. Those percentages are due to increase to 17.5%, 9.5%, and remain at 0, respectively, in July 2015. Additionally, the exchange deducts a transaction tax of .01% of the trade value on all sales.

Regulatory Environment: The State Bank of Pakistan regulates dealings in FX, securities, currency, and all other exchange control regulations. The Securities and Exchange Commission of Pakistan is also involved in various aspects of securities regulation.

Foreign Ownership Restrictions: No limitations are in place for foreign investors with the exception of insurance companies, in which 100% ownership is permitted with the condition that the investor remit at least 4 million US dollars from outside of Pakistan. Approval is also required for foreign investment in the following industries: arms and ammunition, security printing, currency, and radioactive substances.

Investment conditions: Foreign investors are not permitted to short sell in the ready market but are permitted to do so in the futures market. Foreign investors must obtain a unique identification number to trade on the exchanges which are used to track transactions by brokers. Special Convertible Rupee Accounts must be established for currency repatriations. Third-party FX transactions are currently permitted however offshore transactions are not possible.

Substantial Shareholder Reporting: The Companies Ordinance of 1984 and the Listed Companies Ordinance of 2002 requires investors to report the company and regulatory body ownership of more than 10% of outstanding shares. Investors who intend to acquire more than 5% of a bank or financial institution are required to obtain written approval beforehand from the regulatory bodies.

COUNTRY CLASSIFICATION

CONSULTATION

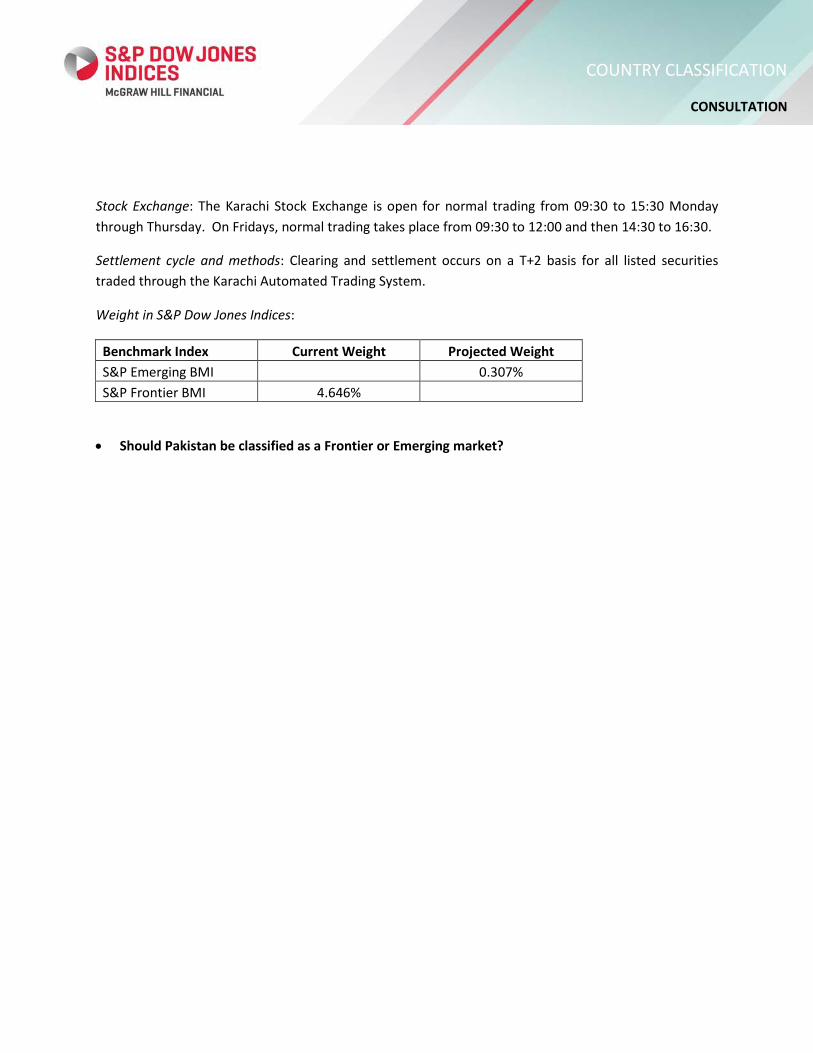

Stock Exchange: The Karachi Stock Exchange is open for normal trading from 09:30 to 15:30 Monday through Thursday. On Fridays, normal trading takes place from 09:30 to 12:00 and then 14:30 to 16:30.

Settlement cycle and methods: Clearing and settlement occurs on a T+2 basis for all listed securities traded through the Karachi Automated Trading System.

Weight in S&P Dow Jones Indices:

Benchmark Index Current Weight Projected Weight S&P Emerging BMI 0.307% S&P Frontier BMI 4.646%

• Should Pakistan be classified as a Frontier or Emerging market?

COUNTRY CLASSIFICATION

CONSULTATION

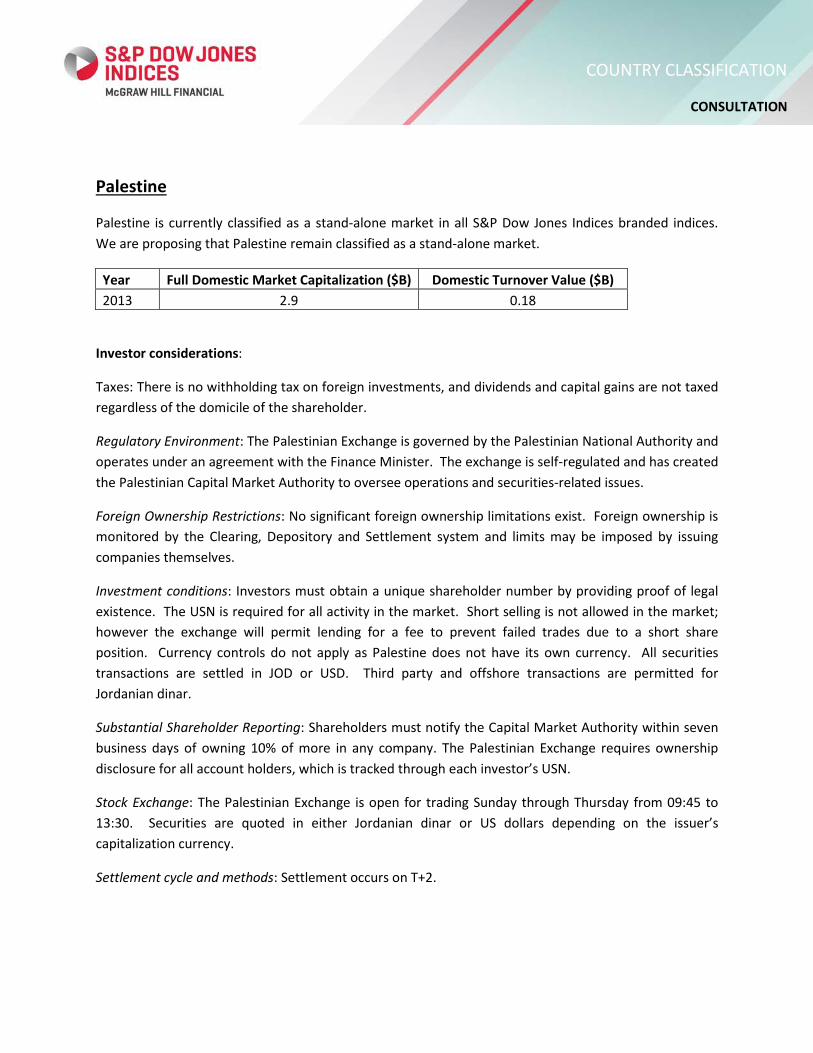

Palestine

Palestine is currently classified as a stand-alone market in all S&P Dow Jones Indices branded indices. We are proposing that Palestine remain classified as a stand-alone market.

Year Full Domestic Market Capitalization ($B) Domestic Turnover Value ($B) 2013 2.9 0.18

Investor considerations:

Taxes: There is no withholding tax on foreign investments, and dividends and capital gains are not taxed regardless of the domicile of the shareholder.

Regulatory Environment: The Palestinian Exchange is governed by the Palestinian National Authority and operates under an agreement with the Finance Minister. The exchange is self-regulated and has created the Palestinian Capital Market Authority to oversee operations and securities-related issues.

Foreign Ownership Restrictions: No significant foreign ownership limitations exist. Foreign ownership is monitored by the Clearing, Depository and Settlement system and limits may be imposed by issuing companies themselves.

Investment conditions: Investors must obtain a unique shareholder number by providing proof of legal existence. The USN is required for all activity in the market. Short selling is not allowed in the market; however the exchange will permit lending for a fee to prevent failed trades due to a short share position. Currency controls do not apply as Palestine does not have its own currency. All securities transactions are settled in JOD or USD. Third party and offshore transactions are permitted for Jordanian dinar.

Substantial Shareholder Reporting: Shareholders must notify the Capital Market Authority within seven business days of owning 10% of more in any company. The Palestinian Exchange requires ownership disclosure for all account holders, which is tracked through each investor’s USN.

Stock Exchange: The Palestinian Exchange is open for trading Sunday through Thursday from 09:45 to 13:30. Securities are quoted in either Jordanian dinar or US dollars depending on the issuer’s capitalization currency.

Settlement cycle and methods: Settlement occurs on T+2.

COUNTRY CLASSIFICATION

CONSULTATION

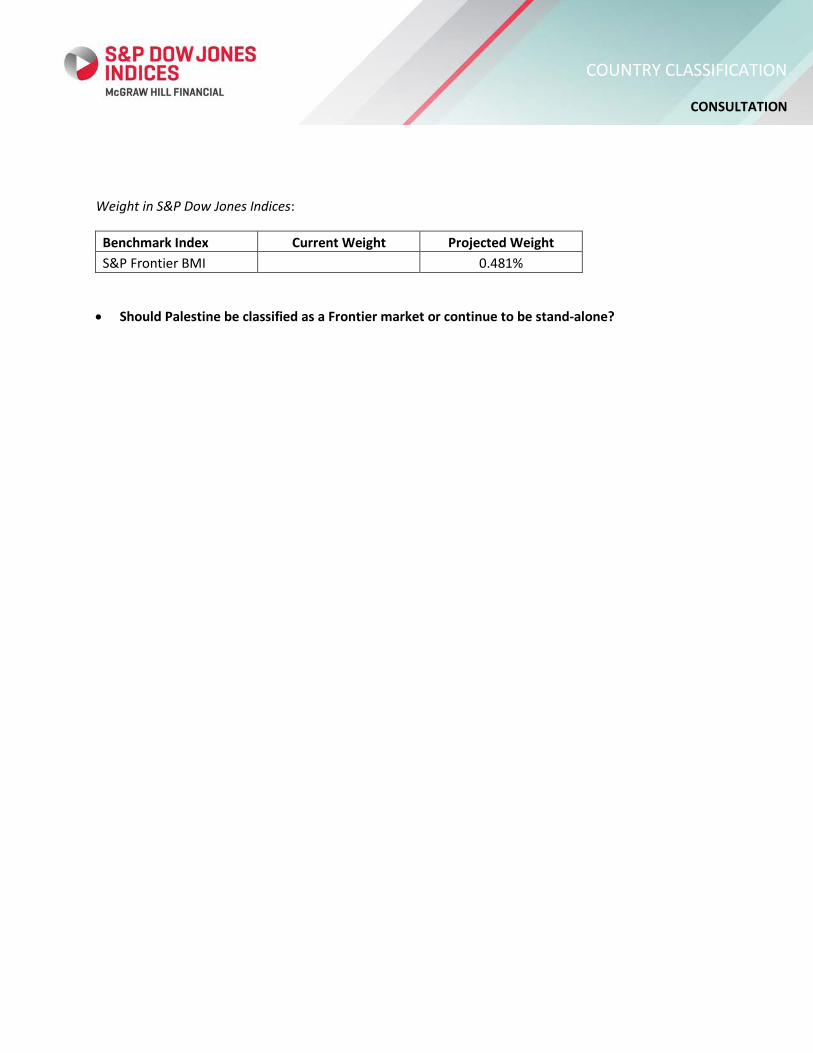

Weight in S&P Dow Jones Indices:

Benchmark Index Current Weight Projected Weight S&P Frontier BMI 0.481%

• Should Palestine be classified as a Frontier market or continue to be stand-alone?

COUNTRY CLASSIFICATION

CONSULTATION

Saudi Arabia

Saudi Arabia is currently classified as a stand-alone market in all S&P Dow Jones Indices branded indices. The very strict restrictions placed on non-GCC investors preclude it from being broadly included in benchmark indices. In recent communications from the Capital Market Authority there have been indications that restrictions will be loosened in the near future. Until then we are proposing that Saudi Arabia remain classified as a stand-alone market.

Year Full Domestic Market Capitalization ($B) Domestic Turnover Value ($B) 2013 466.14 365.2

Investor considerations:

Taxes: Non-resident investors are subject to a 5% withholding tax on dividends and income. Capital gains are tax-exempt.

Regulatory Environment: The Capital Market Authority (CMA) regulates the market and reports directly to the Prime Minister. Board members are appointed by a royal order and are authorized to regulate and develop the capital market and to protect participants.

Foreign Ownership Restrictions: Financial instruments listed on the stock exchange may be traded only by Saudi citizens, non-Saudi citizen residents, Saudi corporations and institutions, and citizens of the Gulf Cooperation Council (GCC). The maximum allowed direct ownership by GCC nationals is 25%. Each trade is monitored by the exchange trading system.

Currently foreign investors have limited opportunities to invest through equity-based mutual funds managed by local banks and a small number of exchange-traded funds. A single investor is not allowed to own more than 10% of the total value of a mutual fund. Currently, government entities of Saudi Arabia are working on a regulatory framework to allow direct foreign ownership of stocks.

Just recently the CMA announced that the government plans to open its stock market to foreign investors for the first time in early 2015. The CMA will now begin to develop rules that will govern foreign investment in the equity market and will assess the market’s readiness by year end. At this time it is unknown to what degree the markets will be opened however this appears to be significant progress towards foreign investors having the ability to gain direct exposure to Saudi Arabian equity markets.

COUNTRY CLASSIFICATION

CONSULTATION

Investment Conditions: Each investor must obtain approval from the CMA prior to investing in Saudi Arabia. The approval process takes 20 to 30 business days after all required documentation is received. Stock lending and short selling are not permitted in the market. Currency controls do not apply in Saudi Arabia.

Substantial Shareholder Reporting: No significant requirements exist.

Stock Exchange: The Saudi Stock Exchange (Tadawul) is open Sunday through Thursday from 11:00 to 15:30.

Settlement cycle and methods: Settlement time for transactions at Tadawul is T+0. Trades are settled instantaneously using electronic systems.

Weight in S&P Dow Jones Indices: Saudi Arabia currently resides outside of both the S&P Frontier BMI and S&P Emerging BMI indices due to foreign ownership restrictions. If the availability of Saudi stocks from a GCC perspective is used to judge the size of Saudi Arabia, it would rank 8th out of 21 markets based on size in the S&P Emerging BMI and would represent approximately 4.44% of the index.

Benchmark Index Current Weight Projected Weight S&P Emerging BMI 4.439%

• Should Saudi Arabia be classified as an Emerging market or continue to be stand-alone? If the latter, what changes need to take place in order to warrant the inclusion of Saudi Arabia in our emerging market indices?

COUNTRY CLASSIFICATION

CONSULTATION

Zimbabwe

Zimbabwe is currently classified as a stand-alone market in all S&P Dow Jones Indices branded indices. We are proposing that Zimbabwe remain classified as a stand-alone market.

Year Full Domestic Market Capitalization ($B) Domestic Turnover Value ($B) 2013 4.89 0.37

Investor considerations:

Taxes: Withholding tax on dividends is 10% on listed shares and 15% on unlisted securities. Foreign investors are also subject to a 1% capital gains tax for listed securities and 5% for unlisted securities.

Regulatory Environment: The Zimbabwe Stock Exchange is regulated by the Ministry of Finance as well as the Securities Commission.

Foreign Ownership Restrictions: Aggregate foreign ownership in any one company is limited to 40%, with a 10% limit per shareholder. These limits are monitored are monitored by companies in coordination with the stock exchange.

Investment conditions: Securities lending and short selling are not permitted. The Zimbabwean dollar has been withdrawn from circulation due to hyperinflation. All transactions are conducted in USD. Capital can be freely repatriated without approval, and foreign investors can transfer foreign currency through normal banking channels for securities transactions.

Substantial Shareholder Reporting: No significant requirements exist.

Stock Exchange: The Zimbabwe Stock Exchange is open for trading from 10:00 to 11:30 from Monday through Friday using a call-over system, and transactions are executed in US dollars.

Foreign Investor requirements: No significant requirements for foreign investors exist.

Settlement cycle and methods: Securities transactions settle on a T+5 basis.

Weight in S&P Dow Jones Indices:

Benchmark Index Current Weight Projected Weight S&P Frontier BMI 0.784%

• Should Zimbabwe be classified as a Frontier market or continue to be stand-alone?

COUNTRY CLASSIFICATION

CONSULTATION

Appendix A

Initial Criteria for S&P Dow Jones Global Equity Index Series Eligibility

Countries must meet a minimum of two of the following three criteria to be considered for inclusion in the S&P Dow Jones Country Indices:

• Full domestic market capitalization over US$ 2.5bn.

Market size is important. S&P Dow Jones Indices uses the full market capitalization of an exchange’s primary market as its measure. Float-adjusted capitalization is not used, as the availability of float information for smaller markets is not of the required standard. Thus, we do not have consistency of float information across all markets.

• Annual turnover value over US$ 1B.

An exchange must have significant turnover so that trading is unlikely to be characterized by a particular difficulty in trading. S&P Dow Jones Indices ascertains the total value of trading in a market’s domestic companies over the calendar year prior to the review.

• A market development ratio over 5%.

Many countries have very small markets that do not provide a sufficiently robust representation of the domestic market economy. To ensure only markets that have developed sufficiently are used, S&P Dow Jones Indices calculates a “market development ratio” by dividing the full domestic market capitalization of the exchange by the country’s GDP at purchasing power parity, sourced from the IMF. To be considered for the S&P Country Indices, this figure must be over 5%.

Additional Requirements for S&P Emerging Market Status

Countries must meet all three of the baseline criteria as well as have a full market capitalization over US$ 15bn, and must meet a minimum of three of the following five criteria to be considered for emerging market status:

• Settlement period of T+3 or better

Efficient, rapid settlement of trades is necessary for investors to be able to trade with confidence. S&P Dow Jones Indices requires markets to settle trades on a T+3 timescale or sooner.

COUNTRY CLASSIFICATION

CONSULTATION

• Major Ratings Agencies rate the sovereign debt at investment grade

A company’s ability to operate is directly affected by its home country’s financial situation. Standard & Poor’s Ratings Services has a team devoted to the analysis of country risk, and its rating of each country’s sovereign debt is used to ensure an appropriate level of risk.

• Non-occurrence of hyperinflation

Hyperinflation is defined here as an annual average consumer price index rate of over 15% at the time of the review.

• No significant foreign ownership restrictions

Foreign ownership restrictions cause issues achieving the required exposure to stocks in a given market. While S&P Dow Jones Indices recognizes that stocks in industries such as defense are commonly restricted, it uses the State Street Global Market Information Database to assess whether additional restrictions might cause investing issues.

• The country’s currency should be freely traded

Difficulties buying or selling a domestic currency, or repatriating capital from a market, hugely complicates the process of investing in a given market. S&P Dow Jones Indices uses the State Street Global Market Information Database to assess whether there any currency restrictions in place in each market.

Further Requirements for S&P Developed Market Status

To be considered for developed market status, countries must meet all eight of the initial and additional criteria and have a Gross Domestic Product per capita, at Purchasing Power Parity, greater than US$ 15,000.

Deviations from Baseline

Where this assessment indicates a possible change of classification, a more in-depth study is undertaken which covers both the primary and additional criteria, as well as the following quantitative and qualitative areas:

COUNTRY CLASSIFICATION

CONSULTATION

Economic & Political

• Further macroeconomic measures, such as the rate and variability of real GDP growth and the overall size of the economy

• Political factors including war, civil disruption, and disturbance, as well as the risk of war or civil unrest

• Restrictions on investments imposed by other governments

Related Investment Conditions

• Settlement procedures • Foreign exchange (FX) access and procedures • Rules on short sales, availability of futures contracts, etc. • Availability of alternative means of investment in the country’s stocks, such as DRs or a large

number of listings on other markets in other countries • The number of domestic listings

Market Consensus

• Desire for change o There must be a market consensus desiring the change of the country’s classification.

• The actions of other market participants o S&P Dow Jones Indices’ staff is in constant contact with the investor community, and

regularly canvases opinions concerning new countries of interest and issues of concern regarding existing S&P Dow Jones Global Equity Index countries.

o The actions of other index providers are relevant. All index providers attempt to incorporate the views of the investor community when assessing markets for country classification purposes. Changes to country classifications reflect changes in the sentiment of both that provider’s customers and the broader market.

Sources: State Street – Guide to Custody in World Markets S&P Sovereign Debt Ratings IMF website World Bank website Stock Exchange websites

COUNTRY CLASSIFICATION

CONSULTATION

Appendix B

Country weights in SPDJI benchmark indices as of July 1, 2014:

Dow Jones Global Emerging Markets Total Stock Market Index

Dow Jones Global Frontier Total Stock Market Index

Dow Jones Global Developed Total Stock Market Index

Country Weight

Country Weight

Country Weight Brazil 13.15%

United Arab Emirates 12.42%

Austria 0.14%

Chile 2.19%

Argentina 8.41%

Australia 2.92% China 26.37%

Bangladesh 3.46%

Belgium 0.49%

Colombia 1.73%

Bulgaria 0.19%

Canada 4.21% Czech Republic 0.29%

Bahrain 2.17%

Switzerland 3.20%

Egypt 0.52%

Cyprus 0.24%

Germany 3.31% Hungary 0.28%

Estonia 0.31%

Denmark 0.61%

Indonesia 3.46%

Croatia 1.22%

Spain 1.35% India 12.10%

Jordan 3.15%

Finland 0.41%

Morocco 0.29%

Kenya 3.21%

France 3.63% Mexico 6.44%

Kuwait 15.07%

United Kingdom 8.07%

Malaysia 4.91%

Kazakhstan 2.60%

Greece 0.10% Peru 0.76%

Lebanon 1.62%

Hong Kong 1.27%

Philippines 2.16%

Sri Lanka 2.03%

Ireland 0.21% Poland 2.37%

Lithuania 0.24%

Israel 0.30%

Russia 7.21%

Latvia 0.04%

Iceland 0.01% Thailand 3.90%

Macedonia 0.08%

Italy 1.12%

Turkey 2.37%

Malta 0.33%

Japan 8.97% South Africa 9.51%

Mauritius 1.38%

South Korea 2.03%

Nigeria 12.93%

Luxembourg 0.10%

Oman 3.09%

Netherlands 1.05%

Pakistan 6.08%

Norway 0.41%

Qatar 10.18%

New Zealand 0.11%

Romania 1.49%

Portugal 0.10%

Serbia 0.19%

Sweden 1.26%

Slovenia 1.52%

Singapore 0.65%

Slovakia 0.12%

Taiwan 1.62%

Tunisia 0.65%

United States 52.36%

Ukraine 0.68%

Vietnam 4.92%

Source: S&P Dow Jones Indices

COUNTRY CLASSIFICATION

CONSULTATION

S&P Developed BMI S&P Emerging BMI S&P Frontier BMI Country Weight

Country Weight

Country Weight

Austria 0.14%

Brazil 11.61%

United Arab Emirates 12.99% Australia 2.98%

Chile 1.90%

Argentina 8.49%

Belgium 0.50%

China 22.72%

Bangladesh 2.40% Canada 4.32%

Colombia 1.56%

Bulgaria 0.25%

Switzerland 3.32%

Czech Republic 0.25%

Bahrain 2.14% Germany 3.39%

Egypt 0.35%

Botswana 0.60%

Denmark 0.62%

Hungary 0.23%

Cote d'Ivoire 0.59% Spain 1.40%

Indonesia 2.87%

Cyprus 0.22%

Finland 0.41%

India 9.93%

Ecuador 0.48% France 3.71%

Morocco 0.25%

Estonia 0.28%

United Kingdom 8.27%

Mexico 5.65%

Ghana 0.40% Greece 0.09%

Malaysia 3.95%

Croatia 1.31%

Hong Kong 1.25%

Peru 0.66%

Jamaica 0.31% Ireland 0.21%

Philippines 1.81%

Jordan 2.78%

Israel 0.28%

Poland 1.85%

Kenya 2.99% Italy 1.14%

Russia 6.15%

Kuwait 14.67%

Japan 9.10%

Thailand 3.17%

Kazakhstan 2.57% South Korea 2.00%

Turkey 1.93%

Lebanon 1.82%

Luxembourg 0.11%

Taiwan 14.90%

Sri Lanka 1.65% Netherlands 1.08%

South Africa 8.25%

Lithuania 0.19%

Norway 0.41%

Latvia 0.04% New Zealand 0.11%

Mauritius 1.45%

Portugal 0.10%

Namibia 0.24% Sweden 1.28%

Nigeria 12.58%

Singapore 0.65%

Oman 2.56% United States 53.13%

Panama 3.07%

Pakistan 4.65%

Qatar 9.76%

Romania 1.44%

Slovenia 1.59%

Slovakia 0.14%

Tunisia 0.58%

Trinidad and Tobago 1.35%

Ukraine 0.68%

Vietnam 2.49%

Zambia 0.26%

Source: S&P Dow Jones Indices

COUNTRY CLASSIFICATION

CONSULTATION

S&P/IFCI Composite Price Index

Dow Jones Developed Markets Index

Dow Jones Emerging Markets Index

Country Weight

Country Weight

Country Weight Brazil 9.98%

Austria 0.13%

Brazil 9.40%

Chile 1.61%

Australia 3.07%

Chile 1.57% China 19.33%

Belgium 0.49%

China 18.78%

Colombia 1.36%

Canada 4.39%

Colombia 1.24% Czech Republic 0.20%

Switzerland 3.45%

Czech Republic 0.21%

Egypt 0.25%

Germany 3.49%

Egypt 0.37% Hungary 0.20%

Denmark 0.63%

Hungary 0.20%

Indonesia 2.43%

Spain 1.45%

Indonesia 2.47% India 8.15%

Finland 0.39%

India 8.67%

South Korea 15.84%

France 3.87%

South Korea 15.99% Morocco 0.18%

United Kingdom 8.58%

Morocco 0.21%

Mexico 4.92%

Greece 0.05%

Mexico 4.58% Malaysia 3.19%

Hong Kong 1.33%

Malaysia 3.50%

Peru 0.53%

Ireland 0.20%

Peru 0.54% Philippines 1.52%

Israel 0.31%

Philippines 1.54%

Poland 1.53%

Italy 1.13%

Poland 1.70% Russia 5.29%

Japan 9.46%

Russia 5.17%

Thailand 2.62%

Luxembourg 0.11%

Thailand 2.78% Turkey 1.59%

Netherlands 1.12%

Turkey 1.69%

Taiwan 12.18%

Norway 0.37%

Taiwan 12.62% South Africa 7.10%

New Zealand 0.12%

South Africa 6.79%

Portugal 0.10%

Sweden 1.27%

Singapore 0.68%

United States 53.83%

Source: S&P Dow Jones Indices

COUNTRY CLASSIFICATION

CONSULTATION About S&P Dow Jones Indices S&P Dow Jones Indices LLC, a part of McGraw Hill Financial, is the world’s largest, global resource for index-based concepts, data and research. Home to iconic financial market indicators, such as the S&P 500® and the Dow Jones Industrial Average™, S&P Dow Jones Indices LLC has over 115 years of experience constructing innovative and transparent solutions that fulfill the needs of investors. More assets are invested in products based upon our indices than any other provider in the world. With over 830,000 indices covering a wide range of asset classes across the globe, S&P Dow Jones Indices LLC defines the way investors measure and trade the markets. To learn more about our company, please visit www.spdji.com. Standard & Poor’s and S&P are registered trademarks of Standard & Poor’s Financial Services LLC, a part of McGraw Hill Financial. Dow Jones is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). These trademarks have been licensed to S&P Dow Jones Indices LLC. It is not possible to invest directly in an index. S&P Dow Jones Indices LLC, Dow Jones, S&P and their respective affiliates (collectively “S&P Dow Jones Indices”) do not sponsor, endorse, sell, or promote any investment fund or other investment vehicle that is offered by third parties and that seeks to provide an investment return based on the performance of any index. This document does not constitute an offer of services in jurisdictions where S&P Dow Jones Indices does not have the necessary licenses. S&P Dow Jones Indices receives compensation in connection with licensing its indices to third parties.