ANALYTICAL REPORT NOVEMBER 2015 - Financial ... AND OBJECTIVES In February 2015, the Financial...

72

PAYMENT PROTECTION INSURANCE RESEARCH ANALYTICAL REPORT NOVEMBER 2015

Transcript of ANALYTICAL REPORT NOVEMBER 2015 - Financial ... AND OBJECTIVES In February 2015, the Financial...

PAYMENT PROTECTION INSURANCE RESEARCH

ANALYTICAL REPORT

NOVEMBER 2015

ABOUT COMRESComRes provides specialist research and insight into reputation, public policy and communications. It is

a founding member of the British Polling Council, and its staff are members of the UK Market Research

Society, committing it to the highest standards of research practice.

ComRes won the 2014 Market Research Society Award for Public Policy / Social Research for its

innovative research into online communications.

The consultancy also conducts regular public research for organisations including The Independent, ITV

News, the BBC, and other media outlets, as well as a wide range of public sector and corporate clients.

ComRes is a member of the British Polling Council and abides by its rules.

For further information about ComRes, this research or any other research requirements please contact

BACKGROUND AND OBJECTIVESIn February 2015, the Financial Conduct Authority (FCA) commissioned ComRes to conduct a large-scale

quantitative study into Payment Protection Insurance (PPI) from a consumer perspective, and more

specifically the trends in PPI complaints. In July 2015, the FCA decided to expand the scope of the

project and commissioned ComRes to double the interview sample, and explore consumers’ attitudes

towards the PPI-related Plevin case.

The key objectives of the study were:

To understand the market in terms of PPI holders, PPI complainants and potentially eligible

future PPI complainants;

To explore understanding and perceptions of PPI and the complaints process;

To discover prompts, barriers and motivations to making a PPI complaint;

To assess intended future behaviour regarding complaining about PPI;

To analyse the potential impact of the Plevin vs. Paragon Personal Finance case on complaining

behaviour regarding PPI;

To understand the appetite for insurance to cover repayments on borrowings in the wake of PPI.

This quantitative survey forms part of a wider programme aimed at assessing whether the current FCA

approach to PPI redress is continuing to meet the objectives of securing appropriate protection for

consumers and enhancing the integrity of the UK’s financial system.

The views expressed in this report are those of the authors and not necessarily those of the FCA, nor do

they reflect FCA policy or constitute guidance to firms.

Page 4

TABLE OF CONTENTS

Contents

PAYMENT PROTECTION INSURANCE RESEARCH ........................................ 1

ABOUT COMRES ..................................................................................... 2

BACKGROUND AND OBJECTIVES.............................................................. 3

METHODOLOGY ..................................................................................... 8

REPORTING CONVENTIONS ................................................................... 10

EXECUTIVE SUMMARY........................................................................... 11

1. KNOWLEDGE OF PPI AND RELATED ISSUES ......................................... 14

1.1 KNOWLEDGE AND UNDERSTANDING OF PPI ..................................... 15

1.2 AWARENESS OF ISSUES WITH PPI...................................................... 17

2. PERSONAL EXPERIENCE OF PPI ........................................................... 19

2.1 PERSONAL EXPOSURE TO PPI ........................................................... 20

2.2 CHECKING ABOUT PPI ..................................................................... 22

2.3 CLAIMING ON A PPI POLICY............................................................. 26

2.4 CONCERNS WITH PPI....................................................................... 28

3. COMPLAINING ABOUT PPI ................................................................. 30

3.1 COMPLAINTS ALREADY MADE ......................................................... 31

3.2 TIMING OF COMPLAINTS................................................................. 32

3.3 TRIGGERS FOR COMPLAINTS ........................................................... 34

3.4 CHANNELS FOR COMPLAINTS.......................................................... 35

3.5 EXPERIENCE OF COMPLAINTS PROCESS ............................................ 37

3.6 COMPLAINT RESOLUTION ............................................................... 38

4. COMPENSATION............................................................................... 39

4.1 EXPERIENCE OF COMPENSATION ..................................................... 40

4.2 PAST USE OF COMPENSATION ......................................................... 41

4.3 LIKELY USE OF POTENTIAL FUTURE COMPENSATION......................... 42

5. POTENTIAL FUTURE COMPLAINTS – DEFINITE PPI HOLDERS................. 43

Page 5

5.1 INTENTION OF COMPLAINING ......................................................... 44

5.2 BARRIERS TO COMPLAINING – PEOPLE NOT INTENDING TO COMPLAIN

........................................................................................................... 45

5.3 BARRIERS TO COMPLAINING – PEOPLE WHO INTEND TO COMPLAIN... 47

5.4 PROMPTS FOR COMPLAINTS............................................................ 48

5.5 TIMEFRAME OF INTENDED COMPLAINTS .......................................... 50

5.6 LIKELY CHANNELS FOR COMPLAINTS ............................................... 51

6. POTENTIAL FUTURE COMPLAINTS – POSSIBLE PPI HOLDERS................. 52

6.1 TIMEFRAME OF POTENTIAL COMPLAINTS ......................................... 53

6.2 CHANNELS FOR POTENTIAL COMPLAINTS ........................................ 54

7. THE IMPACT OF PLEVIN VS. PARAGON PERSONAL FINANCE................. 55

7.1 INTRODUCING THE CASE ................................................................ 56

7.2 PEOPLE ALREADY INTENDING TO COMPLAIN.................................... 58

7.3 PEOPLE NOT INTENDING TO COMPLAIN OR NOT KNOWING IF THEY

INTEND TO COMPLAIN ......................................................................... 59

7.3 REASONS FOR NOT INTENDING TO COMPLAIN AFTER HEARING NEW

INFORMATION ..................................................................................... 63

8. APPETITE FOR REPAYMENT INSURANCE AFTER PPI .............................. 64

8.1 REPAYMENT INSURANCE NOW THAT PPI IS NO LONGER BEING SOLD . 65

8.2 CONSIDERATION OF REPAYMENT INSURANCE .................................. 67

8.3 BARRIERS TO PURCHASE OF INSURANCE COVER ............................... 69

FURTHER INFORMATION....................................................................... 71

Page 6

TABLE OF FIGURESFigure 1: Multi-phase project ..................................................................................... 8

Figure 2: Key subgroups............................................................................................. 8

Figure 3: Knowledge of PPI ....................................................................................... 15

Figure 4: Understanding of PPI.................................................................................. 16

Figure 5: Becoming aware of issues with PPI.............................................................. 17

Figure 6: Sources of knowledge of issues with PPI ..................................................... 18

Figure 7: Use of PPI and other products .................................................................... 20

Figure 8: Association of PPI with specific credit products........................................... 21

Figure 9: Sources of knowledge about PPI ................................................................. 22

Figure 10: Reasons for not checking to date ............................................................. 23

Figure 11: Reasons for checking about PPI ................................................................ 24

Figure 12: Timeframe for checking ........................................................................... 24

Figure 13: Claiming on PPI........................................................................................ 26

Figure 14: Views of PPI (1/2)..................................................................................... 28

Figure 15: Views of PPI (2/2)..................................................................................... 29

Figure 16: Complaining about PPI ............................................................................. 31

Figure 17: Acquiring PPI ........................................................................................... 32

Figure 18: Awareness vs. complaining ...................................................................... 33

Figure 19: Triggers for complaining.......................................................................... 34

Figure 20: Methods of raising complaints on PPI ....................................................... 35

Figure 21: Complaint resolution................................................................................ 38

Figure 22: Compensation received ............................................................................ 40

Figure 23: Past use of compensation......................................................................... 41

Figure 24: Likely use of potential future compensation ............................................. 42

Figure 25: Reasons for not complaining .................................................................... 45

Figure 26: Barriers to complaining ............................................................................ 47

Figure 27: Reported effectiveness of prompts to complain ........................................ 49

Figure 28: Timeframe of intended complaints ........................................................... 50

Figure 29: Expected channel of raising complaints .................................................... 51

Figure 30: Timeframe of hypothetical complaints...................................................... 53

Page 7

Figure 31: Expected channel of raising complaints on PPI.......................................... 54

Figure 32: Impact of Plevin – summary...................................................................... 57

Figure 33: Impact of Plevin - intention to complain (1/2) .......................................... 58

Figure 34: Impact of Plevin - intention to complain (2/2) .......................................... 60

Figure 35: Impact of Plevin - timeframe of hypothetical complaints........................... 61

Figure 36: Impact of Plevin - expected channels of raising complaints on PPI ............ 62

Figure 37: Impact of Plevin - barriers to complaining ................................................ 63

Figure 38: Repayment situations if unable to work .................................................... 65

Figure 39: Consideration of repayment insurance ..................................................... 67

Figure 40: Insurance products purchased.................................................................. 68

Figure 41: Reasons for not purchasing other insurance ............................................. 70

Page 8

METHODOLOGYComRes conducted this research through a multi-phase online study of 20,001 UK adults aged 18 and

over, as described in Figure 1.

Figure 1: Multi-phase project

PART I PART II

The fieldwork was conducted in six distinct phases, with breaks between each to analyse the data and

assess potential areas for further exploration. Key subgroups from the research are shown in Figure 2.

Figure 2: Key subgroups

Phase 1

pilot

Survey of

1,000

adults

6-9/3/15

Phase 1

Survey of

3,000

adults

12-22/3/15

Phase 2

Survey of

4,000

adults

15-24/4/15

Phase 3

Survey of

2,000

adults

1-12/5/15

Phase 4

pilot

Survey of

1,015

adults

13-17/8/15

Phase 4

Survey of

8,986

adults

24/8-

7/9/15

Page 9

A complete methodology can be found in the separate technical report on this study, which includes

detailed information regarding questionnaire design, weighting, and statistical reliability. The final

questionnaires used in each phase of the research are also included in the technical report.

Page 10

REPORTING CONVENTIONSWEIGHTING

Throughout this report, all of the figures that are reported are of weighted results. For this study,

sample data were weighted to the profile of all UK adults aged 18+. Data were weighted by gender, age,

socio-economic grade and region. Further information on the weighting applied during this study is

provided in the separate Technical Report.

SUBGROUP ANALYSIS

Differences between subgroups are only reported where they are statistically significant at the 95% level.

NETS

Throughout this report, we make use of nets to aggregate certain sets of figures – our conventions for

doing so are outlined below:

Where the report refers to “x% agree with”, this is a NET measure of those who ‘strongly agree’ or

‘tend to agree’ [the same logic applies to “disagree”].

Where it refers to “x% find y easy”, this is a NET measure of those who answer ‘very easy’ or

‘fairly easy’ [the same logic applies to “difficult”].

Where it refers to “x% are likely to”, this is a NET measure of those who answer ‘very likely or

‘fairly likely’ [the same logic applies to “unlikely”].

o Alternatively, “most likely” with reference to timeframes may refer to those who select 8-

10 on a scale of 0-10, where 0 = ‘not likely at all’ and 10 = ‘certain’.

Where it refers to “x% were satisfied”, this is a NET measure of those who answer ‘very satisfied

or ‘fairly satisfied [the same logic applies to “dissatisfied”].

BASES

A table of all bases is available in the separate Technical Report.

Page 11

EXECUTIVE SUMMARY

Understanding and perceptions of PPI

Three quarters of the adult population aged 18 and over (74%) have heard of PPI. Of those who have

heard of PPI, most (77%) are aware of issues and or problems with the product.

Understanding is not as widespread, however – only two in five of those who have heard of PPI (42%) say

that they have a good understanding of the product. A similar proportion of those who have heard of PPI

(46%) say that they have some understanding of it, with just one in eight (12%) saying that they have no

understanding of what PPI is.

PPI holders

More than a fifth of adults (22%) have or have had PPI, although only one third of those who know that

they have or have had PPI (36%) say that they have known this all along.

One in nine adults (11%) are unsure if they have had PPI – broken down into 8% of the population who

are not 100% sure if they have had PPI and 3% who really don’t know.

Among those who are unsure if they have had PPI, around half (49%) say that they are unlikely to check

whether they have had it. Fewer than two in five (37%) say that they are likely to check, with the prospect

of compensation being the main driver for checking – mentioned by one in two of those who intend to

check say that compensation is the key motivating factor in doing so.

PPI complainants and perceptions of the complaints process

Approximately half of those who have or have had PPI (47%) have made a complaint about their policy,

or in the case of those with multiple policies, about at least one of their PPI policies. In contrast, 50%

have not made a complaint about any of their policies. A further 4% say that they do not know whether

they have complained.

Two thirds of complainants (64%) have made a complaint directly via the provider of the PPI product,

while three in ten (31%) have made a complaint via a Claims Management Company (CMC). The process

of making a complaint is generally considered easy by those who have been through it – three in five of

these complainants (59%) say that the process was easy. Nine in ten complainants whose complaint was

resolved (91%) have received compensation, and the vast majority of those who have received

compensation (85%) report being satisfied with the amount of compensation received.

Prompts, barriers and motivations to making a complaint

Nearly half of those who have, have had or may have had PPI (46%) express concerns about the way that

PPI was sold to them. Similarly, 44% refer to concerns about the cost of PPI.

Among those people who have complained about at least one PPI policy, the triggers for complaining

were media news stories explaining how to complain (cited as the trigger for 27% of complaints), letters

from the provider explaining how to complain (20%), media advertisements explaining how to complain

(19%) and cold calls from CMCs explaining how to complain (18%).

Among those who do not intend to complain or complain again, the main reason for not complaining is

being happy and having no concerns about the policy that was sold to them (cited by 35% of those who

do not intend to complain in the future and still have at least one policy left to complain about). The

other commonly given reasons include thinking that the amount of compensation received would not be

worth the time and effort it would take to achieve it (cited by 15%) and not being sure whether they

should be concerned (11%).

Page 12

Among those who intend to complain in the future about at least one policy, the main reasons given for

not having complained already are not having the time or energy (cited by 40%), having needed to check

whether they have or have had PPI (30%) and not being sure how to complain (21%).

When asked about the prompts that could make them complain for the first time, again or sooner than

originally envisaged, two thirds of those people who have, have had or may have had PPI (64%) say that a

letter from their provider explaining how to complain would make them more likely to complain.

Similarly, more than half (54%) say that communications from the government explaining how to

complain would make them more likely to complain. Only one in five (20%) say that a cold call from a

CMC would make them more likely to complain.

Future complaints

Among those who have or have had PPI, only one in eight (12%) intend to complain in the future,

whether for the first time or having already complained about a different policy. Around three quarters

(72%) do not intend to complain in the future, while 16% do not know if they will complain. More than

two in five of those intending to complain (44%) are most likely to do so in the next six months.

For those who are not 100% sure whether they have PPI or “really don’t know”, we introduceda

hypothetical scenario where we suggested that these people discovered that they definitely have or have

had a PPI policy. In this scenario, one quarter of people uncertain whether they have PPI (26%) are most

likely to complain within the next six months.

The impact of Plevin vs. Paragon Personal Finance

We gave those people who have or have had a PPI policy information about the recent Plevin vs. Paragon

Personal Finance case and its potential implications for them. The effect of this information is outlined

below:

For those who were already intending to complain about a PPI policy, two in five (41%) say that

they now intend to complain sooner than they did before, citing increased awareness (28%of

those now intending to complain sooner) and expectation of compensation (11%) as the key

reasons for their changed position. Around half (47%) say that they still intend to complain at the

same time as they did previously, and 13% say that they now intend to complain later than

before.

For those who were not intending to complain, only 13% say that they now intend to complain

about one of their PPI policies. The majority – three in five (59%) – say that they still do not intend

to complain.

For those who previously did not know whether they intended to complain, three in ten (31%)

change their mind and say that they now intend to complain. Three in five (57%) say that they

still do not know whether they intend to complain.

Information about Plevin therefore does have a noticeable impact on likelihood to complain – around

one in five of those previously either not intending to complain or not knowing whether they intended to

complain (17%) now intend to complain after hearing information about Plevin.

Appetite for repayment insurance after PPI

To explore the consumer appetite for repayment insurance after PPI, we introduced a hypothetical

scenario where those in work with at least one of three credit products were asked to think about what

Page 13

would happen if they became unable to work for longer than a month due to accident, sickness or

unemployment. One in five (19%) say that, in this scenario, they would probably not be able to pay some

or all of their repayments. Only one in ten (10%) say that they have insurance to cover all of their

repayments.

Among those working people with credit products who do not have insurance to cover all of their

repayments, a quarter (26%) say that they have considered taking out insurance that protects their

repayments or short-term income but have decided against it. The main reasons for this are cost and a

lack of trust - a quarter of people who have not purchased insurance cover for any of their borrowings

(23%) say that they decided not to buy these products because they were too expensive, with a further

one in five (21%) saying that they do not trust the providers.

Key demographic subgroups

Less financially sophisticated individuals are a key audience in the context of PPI: they are much less

likely than the more financially sophisticated to report having a good understanding of PPI (22% vs. 52%)

and to have known all along that they have held PPI (32% vs. 39%), while being much more likely to be

unaware of what their PPI policy entitles them to (60% vs. 43%).

Lower social grades are important in terms of the prompt for and channel of their complaints – those in

social grades DE and C2 are more likely than those in social grades AB and C1 to say that they were

prompted to complain by a cold call from a Claims Management Company (23% of DE and 20% of C2 vs.

15% of AB and C1) and to have complained through a CMC (37% of DE and 35% of C2 vs. 26% of AB and

28% of C1).

1. KNOWLEDGE OF PPI ANDRELATED ISSUES

Page 15

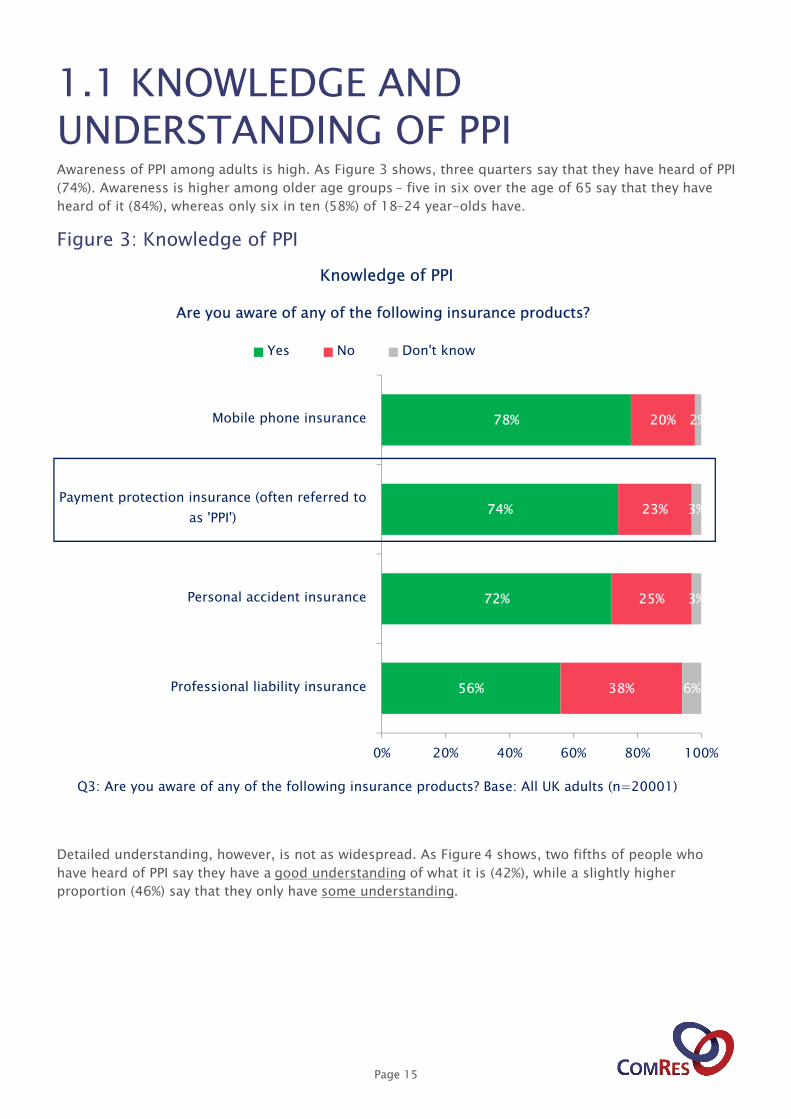

1.1 KNOWLEDGE AND UNDERSTANDING OF PPIAwareness of PPI among adults is high. As Figure 3 shows, three quarters say that they have heard of PPI

(74%). Awareness is higher among older age groups – five in six over the age of 65 say that they have

heard of it (84%), whereas only six in ten (58%) of 18-24 year-olds have.

Figure 3: Knowledge of PPI

Detailed understanding, however, is not as widespread. As Figure 4 shows, two fifths of people who

have heard of PPI say they have a good understanding of what it is (42%), while a slightly higher

proportion (46%) say that they only have some understanding.

56%

72%

74%

78%

38%

25%

23%

20%

6%

3%

3%

2%

0% 20% 40% 60% 80% 100%

Professional liability insurance

Personal accident insurance

Payment protection insurance (often referred to

as 'PPI')

Mobile phone insurance

Knowledge of PPI

Yes No Don't know

Are you aware of any of the following insurance products?

Q3: Are you aware of any of the following insurance products? Base: All UK adults (n=20001)

Page 16

Figure 4: Understanding of PPI

Consistent with the findings relating to awareness of PPI, of those aware of PPI, understanding is higher

among older age groups. Almost half of those aged 65+ (47%) and half of those aged 55-64 (50%) say

that they have a good understanding of PPI, compared to one in five 18–24 year olds (21%).

Reported understanding is particularly high among those with a high combined annual household

income. More than half of those in households earning more than £60,000 per year (55%) have a good

understanding of PPI, compared to just over a third of those in households earning less than £20,000

(36%).

The more financially sophisticated also tend to say that they have a good understanding of PPI, with half

(52%) of them saying so, compared to only one in five of those who are less financially sophisticated

(22%).1

1 More financially sophisticated and less financially sophisticated individuals were categorised using a financial

sophistication indication question. Further information on how this was derived can be found in the separate technical

report on this study, in Appendix C.

42% 46% 12%

0% 20% 40% 60% 80% 100%

Understanding of PPI

I have a good understanding of what PPI is

I have some understanding of what PPI is

I have heard of PPI but do not know what it really is

Q4: Which of the statements below best describes your understanding of payment protection

insurance (PPI)? Base: All who are aware of PPI (n=14932)

Page 17

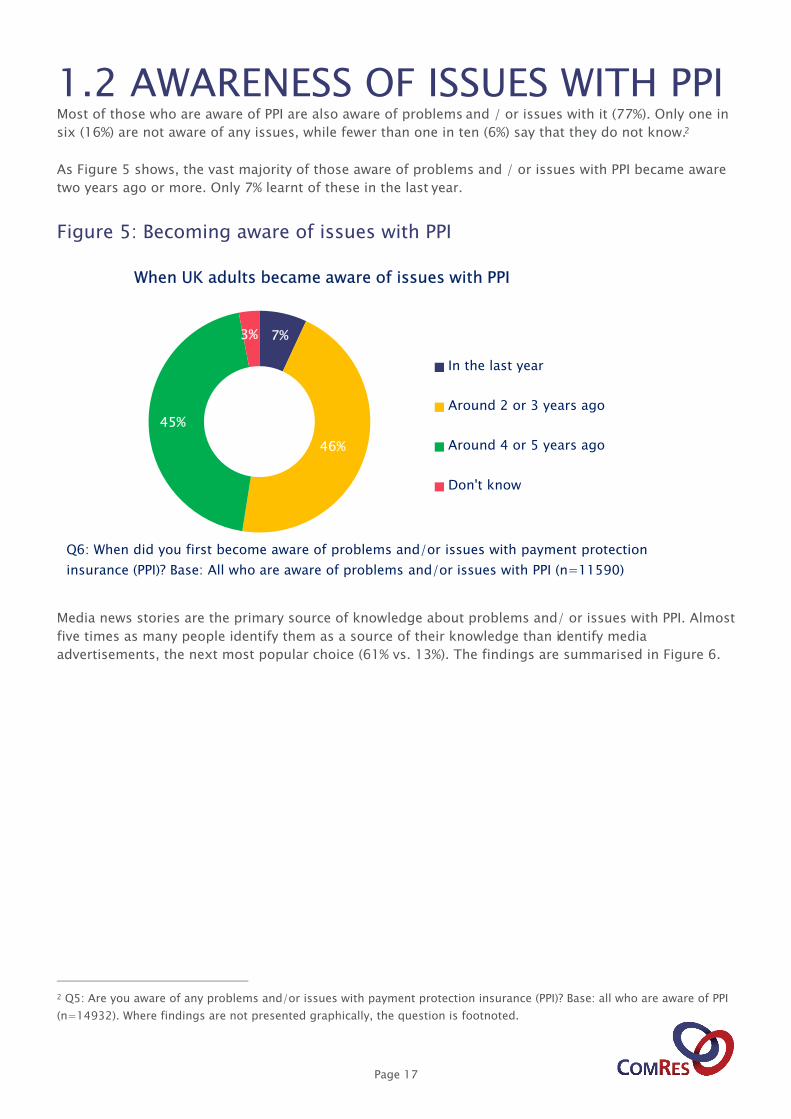

1.2 AWARENESS OF ISSUES WITH PPIMost of those who are aware of PPI are also aware of problems and / or issues with it (77%). Only one in

six (16%) are not aware of any issues, while fewer than one in ten (6%) say that they do not know.2

As Figure 5 shows, the vast majority of those aware of problems and / or issues with PPI became aware

two years ago or more. Only 7% learnt of these in the last year.

Figure 5: Becoming aware of issues with PPI

Media news stories are the primary source of knowledge about problems and/ or issues with PPI. Almost

five times as many people identify them as a source of their knowledge than identify media

advertisements, the next most popular choice (61% vs. 13%). The findings are summarised in Figure 6.

2 Q5: Are you aware of any problems and/or issues with payment protection insurance (PPI)? Base: all who are aware of PPI

(n=14932). Where findings are not presented graphically, the question is footnoted.

7%

46%

45%

3%

When UK adults became aware of issues with PPI

In the last year

Around 2 or 3 years ago

Around 4 or 5 years ago

Don't know

Q6: When did you first become aware of problems and/or issues with payment protection

insurance (PPI)? Base: All who are aware of problems and/or issues with PPI (n=11590)

Page 18

Figure 6: Sources of knowledge of issues with PPI

Q7: How did you first become aware of problems and/or issues with payment protection insurance (PPI)? Base: All who are aware of problems and/or issues with PPI (n=11590)

2. PERSONAL EXPERIENCE OF PPI

Page 20

2.1 PERSONAL EXPOSURE TO PPIAs Figure 7 shows, more than one in five UK adults say that they have had payment protection insurance

(22%).3 This is more than the proportion with personal accident (20%) or professional liability insurance

(14%), but less than the proportion who have had mobile phone insurance (32%).

Figure 7: Use of PPI and other products

The mean number of PPI policies that people with PPI had or have is 2, and almost half of people with

PPI (47%) have or have had more than one policy.4

Exposure to PPI is higher among middle-aged groups. Two thirds (28%) of 35-54 year olds say they had

or have had PPI, compared to 20% of 65+ year olds, for example.

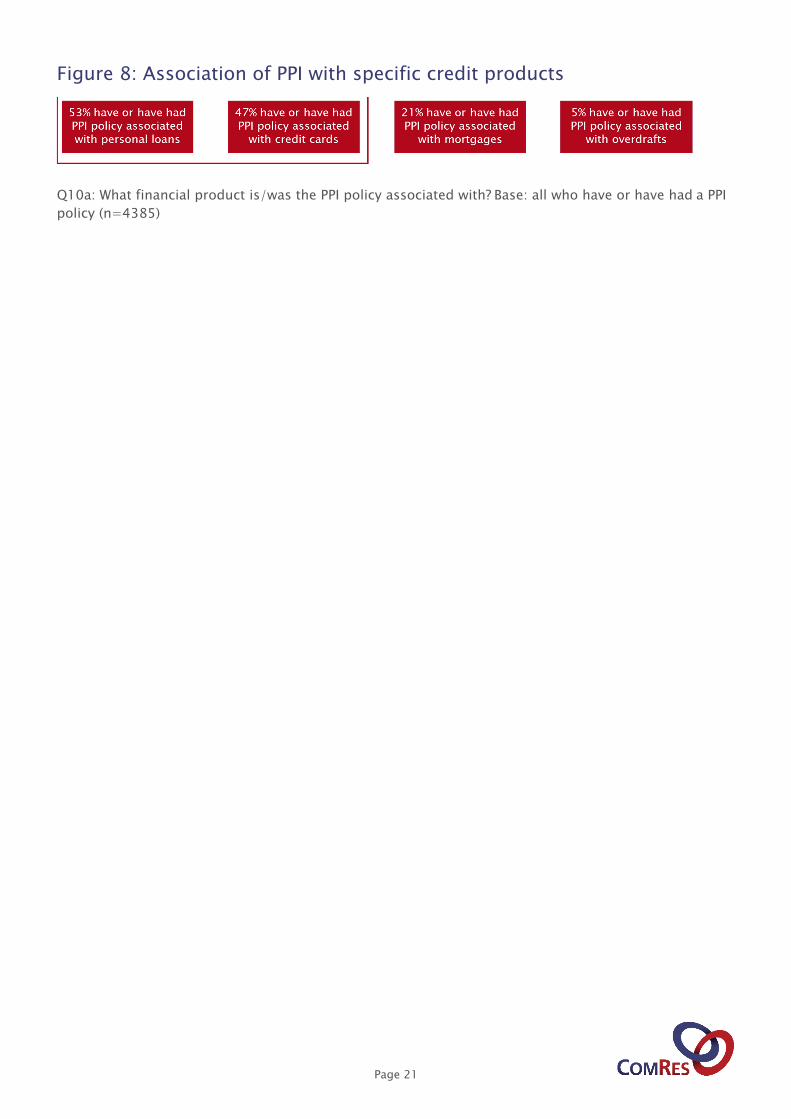

As shown in Figure 8, around half of all people who have or have had PPI (53%) held a policy associated

with a personal loan. A similar proportion (47%) hold or have held a policy associated with a credit card.

One in five PPI holders (21%) have or have had PPI for a mortgage and 5% for an overdraft.

One in seven people who have or have had PPI have held a policy where they do not know what credit

product this is associated with (15%).

3 In this section we are reporting policies that respondents are aware of having now or in the past based on recall. It is

possible that respondents have or have had additional policies they do not remember or were never aware of.

4 Q10: How many Payment Protection Insurance (PPI) policies have you had? Base: all who have or have had PPI (n=4385)

Q9: Have you ever had any of the following financial products? Base: All UK adults (n=20001)

Page 21

Figure 8: Association of PPI with specific credit products

Q10a: What financial product is/was the PPI policy associated with? Base: all who have or have had a PPI

policy (n=4385)

Page 22

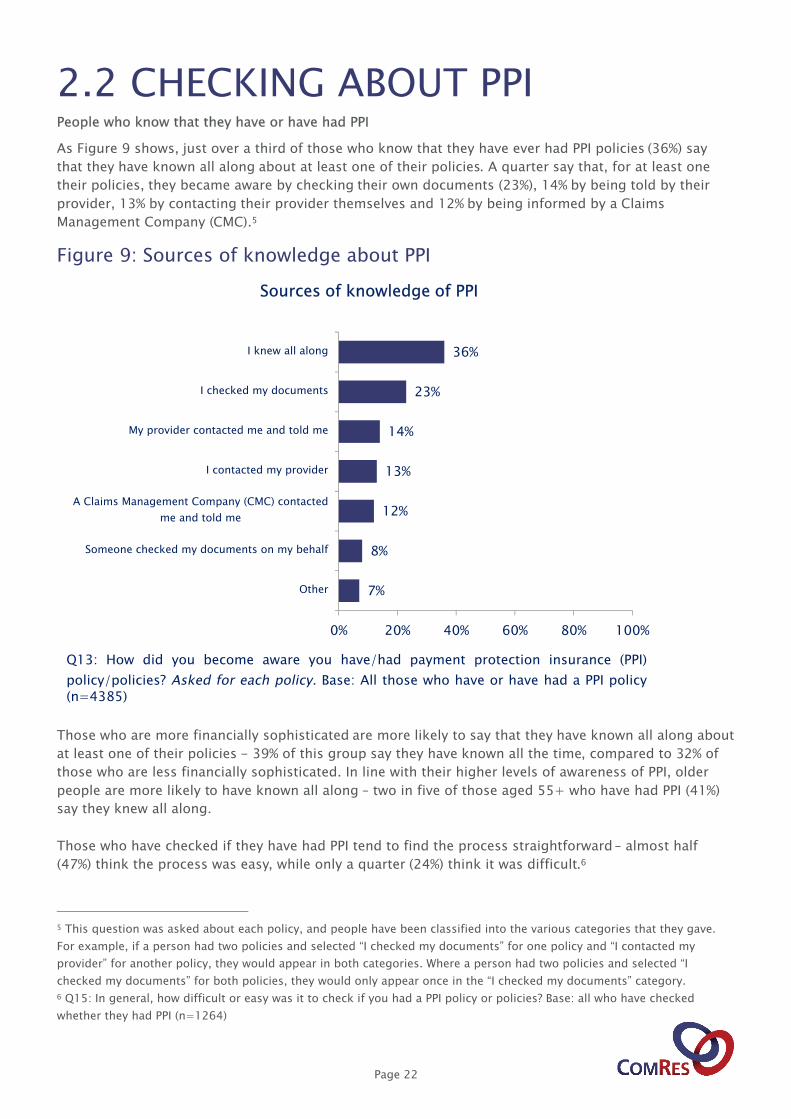

2.2 CHECKING ABOUT PPIPeople who know that they have or have had PPI

As Figure 9 shows, just over a third of those who know that they have ever had PPI policies (36%) say

that they have known all along about at least one of their policies. A quarter say that, for at least one

their policies, they became aware by checking their own documents (23%), 14% by being told by their

provider, 13% by contacting their provider themselves and 12% by being informed by a Claims

Management Company (CMC).5

Figure 9: Sources of knowledge about PPI

Those who are more financially sophisticated are more likely to say that they have known all along about

at least one of their policies - 39% of this group say they have known all the time, compared to 32% of

those who are less financially sophisticated. In line with their higher levels of awareness of PPI, older

people are more likely to have known all along – two in five of those aged 55+ who have had PPI (41%)

say they knew all along.

Those who have checked if they have had PPI tend to find the process straightforward – almost half

(47%) think the process was easy, while only a quarter (24%) think it was difficult.6

5 This question was asked about each policy, and people have been classified into the various categories that they gave.

For example, if a person had two policies and selected “I checked my documents” for one policy and “I contacted my

provider” for another policy, they would appear in both categories. Where a person had two policies and selected “I

checked my documents” for both policies, they would only appear once in the “I checked my documents” category.

6 Q15: In general, how difficult or easy was it to check if you had a PPI policy or policies? Base: all who have checked

whether they had PPI (n=1264)

7%

8%

12%

13%

14%

23%

36%

0% 20% 40% 60% 80% 100%

Other

Someone checked my documents on my behalf

A Claims Management Company (CMC) contacted

me and told me

I contacted my provider

My provider contacted me and told me

I checked my documents

I knew all along

Sources of knowledge of PPI

Q13: How did you become aware you have/had payment protection insurance (PPI)

policy/policies? Asked for each policy. Base: All those who have or have had a PPI policy (n=4385)

Page 23

People who are unsure whether they have or have had PPI

One in ten adults (11%) are unsure if they have ever had PPI – this is broken down into 8% who say that

they are not 100% sure and 3% who say that they really don’t know (see Figure 7).

As Figure 10 shows, a third (35%) of those who are unsure whether they have ever had PPI say the reason

that they have not checked so far is that they are not sure whether it would be worth it, and three in ten

say that they do not know how to check (29%) or that they can’t locate their documents (28%).

Figure 10: Reasons for not checking to date

Among those who are unsure whether they have ever had PPI, almost two in five (37%) say they are likely

to check whether they have ever had PPI. However, half of this audience (49%) say they are unlikely to

check.7 Among those likely to check, the prospect of compensation is indicated as the primary driver for

checking, as Figure 11 shows; concerns about the (possible) policy also play a major role.

7 Q16: How likely, if at all, would you say that you are to check whether you have ever had a payment protection insurance

(PPI) policy? Base: all who are not 100% sure or really don’t know whether they have had PPI (n=2117)

12%

15%

15%

28%

29%

35%

0% 20% 40% 60% 80% 100%

Other

Haven't had time

I can't be bothered to check

Can't locate documents

I don't know how to check

I am not sure that it would be worth it

Reasons for not checking to date

Q20: What would you say is the reason that you have not checked so far whether or not you

have ever had a payment protection insurance (PPI) policy? Multiple answers possible Base: All

who are not 100% sure or really don’t know whether they have or have had a PPI policy

(n=2117)

Page 24

Figure 11: Reasons for checking about PPI

As Figure 12 shows, those who say they are likely to check whether they have ever had PPI are more

likely to check either in the very near future or in the very distant future. More than a third (38%) are

most likely to check in the next six months, whereas a similar proportion (36%) are most likely to check

in more than three years. Given the time gap involved, this set of figures may give a better indication of

overall propensity to check than the timing of checking - it appears relatively unlikely that those who

say that they are most likely to check in more than three years’ time will ever check whether they have

indeed held a PPI policy.

Figure 12: Timeframe for checking

We asked people to rate how likely they would be to check in each of a series of timeframes, on a 0-10 scale. We

then calculated the timeframe in which these people are most likely to check – allocating them to one of the time

slots based on the slot for which they select the highest score. Where people select the same score for two or more

time slots, we allocated people to the latest time slot (i.e. if a person selected 2 for “in 0-6 months”, 3 for “in 7-12

months”, 6 for “in 1-3 years” and 6 for “in more than three years”, they would be allocated to “in more than three

years”).

3%

12%

24%

26%

29%

50%

0% 20% 40% 60% 80% 100%

Other

CMC advised me to

For own records

Better understand if I should be concerned

Concerned about whether my PPI was mis-sold to me

Might be eligible for compensation

Why check whether you have PPI?

Q17: Why do you plan to check whether you have ever had a PPI policy? Multiple answers

possible. Base: All who are unsure if they have or have had PPI and are likely to check if

they have had it (n=780)

Page 25

11%

36%

5%

10%

38%

0% 20% 40% 60% 80% 100%

Don't know

In more than…

In 1-3 years

In 7-12 months

In 0-6 months

Timeframe for checking

Showing time period in which people are most likely to check

Q19a: How likely, if at all, would you say that you are to check, within the following time

periods, whether you have ever had a payment protection insurance (PPI) policy? Please

indicate how likely on a scale of 0 to 10 where 0 = not likely at all and 10 = certain. Base: All

who are unsure if they have or have had PPI and are likely to check if they have had it (n=735)

Page 26

2.3 CLAIMING ON A PPI POLICYIn the context of this report, “claiming” refers to the act of claiming on a policy in the same way that a

policyholder might claim on any insurance policy – for example, a PPI holder might have claimed against

their policy if they were made redundant, to cover the repayments on their loan until they could find a

new job. In contrast, “complaining” will be used to refer to people complaining about their policy being

mis-sold to them.

Most people who have or have had a PPI policy have not made a claim on it/ them. As Figure 13 shows,

two in five (39%) say they have claimed on a policy, while three in five (58%) say they have not. People

who first became aware of issues with PPI in the last year are more likely than those who became aware

two years ago or more to have made a claim on their policy (65% of those who became aware within the

last year vs. 37% around 2 or 3 years ago and 39% around 4 or 5 years ago or more).

Those with a PPI attached to an overdraft are most likely to have made a claim on at least one of their

policies (although the policy that they complained about may not have been related to their overdraft),

with more than half (55%) saying so. This compares to slightly more than two in five of those with at

least one PPI attached to a mortgage (42%), a credit card (42%) or a personal loan (45%).

Those who became aware that they had a PPI policy after contacting their provider are most likely to

have made a claim, with three in five (60%) saying they did so – compared to only a third of those who

say they knew all along that they had a PPI policy (32%).

Figure 13: Claiming on PPI

Of those who have made a claim, a quarter (23%) say that their insurer has not paid out on their policy /

at least one of their policies. In contrast, three quarters (76%) say their insurer has paid out on their

39%

58%

3%

Have made a claim on their PPI(NB: This question is about a claim on the policy as opposed to complaining about how the

policy was mis-sold)

Yes

No

Don't know

Q11: Have you ever made a claim on any of your PPI policy/policies, because you became ill, had an accident or became unemployed and needed the policy to cover your loan or other debt repayments? Base: All who have or have had PPI (n=4385)

Page 27

policy / at least one of their policies. 7% indicate that at least one claim is ongoing. 3% say that they do

not know.8

As highlighted in Figure 14, one in six of those who have, have had or may have had PPI (16%) say that

they thought the PPI covered them, but when they claimed their claim was rejected.

8 Q12: As a result of your claim on any of your payment protection insurance (PPI) policy/policies, did the insurer pay out

on your claim and cover your repayments while you were ill or unemployed etc.? Base: All UK adults who have claimed on a

PPI policy (n=1679)

Page 28

2.4 CONCERNS WITH PPIConcerns about PPI are widespread among adults, as indicated by levels of agreement with a series of

statements that we tested relating to PPI.

As Figure 14 shows, nearly half of people who have, have had or may have had a PPI policy (46%) are

concerned about the way it was sold to them. Those who are more financially sophisticated (50%) are

more likely than those who are less financially sophisticated (45%) to agree that they are concerned

about the way the PPI was sold to them. Moreover, concerns are most prevalent for those who have or

have had a PPI policy associated with an overdraft (69%), although it is important to stress that these

concerns are not necessarily about any PPI policy/ies associated with an overdraft. Two thirds of people

who have or have had a PPI policy associated with a personal loan or a credit card (64% ) have these

concerns, as do half of those who have or have had a PPI associated with a mortgage (54%).

Similarly, more than two in five people who have, have had or may have had a PPI policy (44%) have

concerns about its cost. Those from a higher social grade are more likely than those from a lower social

grade to say that have concerns about the cost of PPI. For instance, half of those from social grade AB

(48%) are concerned, compared to two in five from social grade DE (41%). This difference is also found

with regard to levels of combined annual household income – for example, 55% of those with an annual

household income of £80,001 - £100,000 have concerns about the cost of PPI, compared to 42% of

those with an annual household income of less than £20,000.

Central to many concerns about PPI is a lack of understanding. As Figure 14 shows, one quarter (25%)

say that they were not aware until recently that they in fact have or have had PPI – this proportion rises

to half (50%) among those whose PPI is/was associated with an overdraft.

Figure 14: Views of PPI (1/2)

7%

9%

16%

21%

9%

16%

28%

25%

48%

34%

39%

37%

12%

17%

9%

9%

24%

24%

8%

9%

0% 20% 40% 60% 80% 100%

I thought the PPI covered me but when I

claimed it was rejected

I was not aware, until recently, that I had

a PPI policy

I have/had concerns about the cost of PPI

I have/had concerns about the way the

PPI policy was sold to me

Views of PPI

Strongly agree Tend to agree

Neither agree nor disagree Tend to disagree

Strongly disagree

Q22a: To what extent do you agree or disagree with the following statements? Base: All who have, have had or may have had a PPI policy (n=6502)

Page 29

As Figure 15 shows, more than two in five (44%) of those who have, have had or may have had PPI report

being unaware of what their policy entitles them to – a figure that rises to 60% among those less

financially sophisticated. Again, the proportion of those unaware of what their policy entitles them to is

particularly high among those whose PPI is/was associated with an overdraft (64%) but is lower among

those whose PPI is/was associated with a mortgage (40%).

Similarly, two in five (43%) say that they do not understand the terms and conditions of their policy. This

figure rises to three in five (60%) among those less financially sophisticated, and a similar proportion of

those whose PPI is/was associated with an overdraft (61%) but is lower among those whose PPI is/was

associated with a mortgage (42%).

As already highlighted in Section 2.3, one in six (16%) of those who have, have had or may have had PPI

say that they thought the PPI covered them, but their claim was rejected.

Among those who have, have had or may have had a policy, only a quarter (25%) have no concerns about

their PPI policy (see Figure 15). Those who are more financially sophisticated are also more likely not to

have concerns about their PPI policy, with a third (31%) saying so, compared to a quarter (24%) of those

less financially sophisticated. Two in five of those who have, have had or may have had a PPI policy (39%)

are neither concerned nor unconcerned – potentially suggesting a lack of knowledge.

Figure 15: Views of PPI (2/2)

9%

14%

14%

16%

30%

29%

39%

35%

36%

21%

13%

12%

14%

8%

8%

0% 20% 40% 60% 80% 100%

I have no concerns about the PPI policy

I do/did not know what the PPI policy

entitles me to

I do/did not understand the terms and

conditions associated with the PPI policy

Views of PPI

Strongly agree Tend to agree

Neither agree nor disagree Tend to disagree

Strongly disagree

Q22b: To what extent do you agree or disagree with the following statements? Base: All who have, have had or may have had a PPI policy (n=6502)

3. COMPLAINING ABOUT PPI

Page 31

3.1 COMPLAINTS ALREADY MADEApproximately half of PPI holders (47%) say that they have made a complaint about at least one of their

PPI policies, as Figure 16 shows. A similar proportion (50%) say that they have not made a complaint

about any of their PPI policies. 39% of PPI holders have complained about all of the policies that they can

recall.

Figure 16: Complaining about PPI

Complaints have been least common among those who knew all along that they held a PPI policy – just

one third of these people have complained about one or more policies (33%), compared to:

Almost three quarters of PPI holders who became aware that they had PPI through directly

contacting their provider (72%);

Almost two thirds of those who found out that they held PPI by checking their documents (63%);

Three in five of those who were informed that they had PPI by a CMC (59%).

47%

50%

4%

Have made a complaint about at least one PPI

Yes

No

Don't know

Q23a: Have you complained about the payment protection insurance (PPI) policy which you had? Base: All who have or have had a PPI policy (n=4385)

Page 32

3.2 TIMING OF COMPLAINTSFor many people there is a considerable time lag between when they acquired PPI and when they actually

became aware that they held a PPI policy.

We asked about each PPI policy that people held – as shown in Figure 17, two in five people who have or

have had PPI (39%) say that they acquired a PPI policy before 2000.

Figure 17: Acquiring PPI

We then asked PPI holders who had complained about at least one of their PPI policies about when they

became aware that they held each PPI policy and about the timing of each of their individual complaints

– as outlined in Figure 18.

One in six became aware that they held a PPI policy in 2014 (17%), one in five became aware in 2013

(19%), and one in seven (15%) in 2012.

Half of all complaints about PPI were made in 2013 or 2014 (50%). This is consistent with initial findings

that 46% of people aware of problems and/ or issues with PPI found out about them two or three years

ago (see Figure 5).

Indeed, the figures on the timing of complaints align relatively closely with when PPI holders first

became aware that they held a PPI policy (which was asked to a smaller subsection of PPI holders).9 Two

thirds of complaints (66%) were made in the same year as the holder became aware that they held a PPI

policy, and the average length of time between becoming aware of holding a PPI policy and complaining

about it is 1.13 years, across all complaints.

9 For phases 2, 3 and 4 of the research, we included an additional question (Q23b) for those who have complained about a

PPI policy, asking them about when they became aware that they held each policy. Further detail about this can be found in

the Questionnaire Design section in the technical report.

22%

39%

28%

28%

12%

0% 20% 40% 60% 80% 100%

Can't remember

Before 2000

2000-2004

2005-2010

Since 2010

Period when acquired PPI

Q10b: When did you get this financial product? Base: All UK adults who have or have had a PPI policy (n=4385)

Page 33

Figure 18: Awareness vs. complaining

30%

3%

5%

10%

9%

15%

19%

17%

6%

0% 20% 40% 60% 80% 100%

2007 or earlier

2008

2009

2010

2011

2012

2013

2014

2015

Year when became aware of

having PPI

Q23b: When did you become aware that

you held this policy? Base: All who have

complained about at least one PPI policy [Phases 2/3/4] (n=1651)

9%

8%

2%

4%

9%

10%

18%

25%

25%

9%

0% 20% 40% 60% 80% 100%

Don't know

2007 or earlier

2008

2009

2010

2011

2012

2013

2014

2015

Year when complaint made

Q24a: When did you complain about the

payment protection insurance (PPI) policy

which you had? Base: All who have

complained about at least one PPI policy[All phases] (n=2068)

Page 34

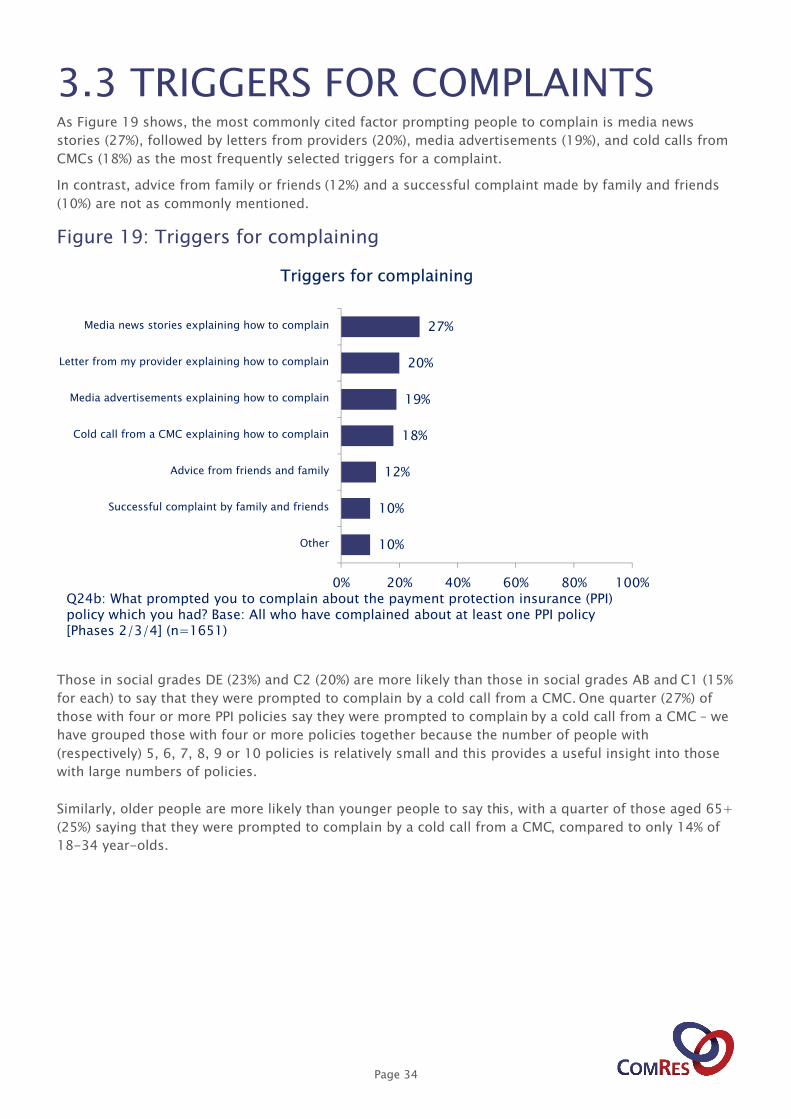

3.3 TRIGGERS FOR COMPLAINTSAs Figure 19 shows, the most commonly cited factor prompting people to complain is media news

stories (27%), followed by letters from providers (20%), media advertisements (19%), and cold calls from

CMCs (18%) as the most frequently selected triggers for a complaint.

In contrast, advice from family or friends (12%) and a successful complaint made by family and friends

(10%) are not as commonly mentioned.

Figure 19: Triggers for complaining

Those in social grades DE (23%) and C2 (20%) are more likely than those in social grades AB and C1 (15%

for each) to say that they were prompted to complain by a cold call from a CMC. One quarter (27%) of

those with four or more PPI policies say they were prompted to complain by a cold call from a CMC – we

have grouped those with four or more policies together because the number of people with

(respectively) 5, 6, 7, 8, 9 or 10 policies is relatively small and this provides a useful insight into those

with large numbers of policies.

Similarly, older people are more likely than younger people to say this, with a quarter of those aged 65+

(25%) saying that they were prompted to complain by a cold call from a CMC, compared to only 14% of

18-34 year-olds.

10%

10%

12%

18%

19%

20%

27%

0% 20% 40% 60% 80% 100%

Other

Successful complaint by family and friends

Advice from friends and family

Cold call from a CMC explaining how to complain

Media advertisements explaining how to complain

Letter from my provider explaining how to complain

Media news stories explaining how to complain

Triggers for complaining

Q24b: What prompted you to complain about the payment protection insurance (PPI) policy which you had? Base: All who have complained about at least one PPI policy [Phases 2/3/4] (n=1651)

Page 35

3.4 CHANNELS FOR COMPLAINTSAs Figure 20 illustrates, two thirds of individual complaints are made directly via the provider of the PPI

(64%) and one third are made via CMCs (31%).

PPI holders from lower social grades are more likely than all PPI holders to complain through a CMC -

37% of those in social grades DE say that they complained through a CMC, compared to 28% of those in

social grade C1 and 26% of those in social grade AB.

Only small minorities of complaints were made through a financial advisor (7%) or a lawyer (4%).

Figure 20: Methods of raising complaints on PPI

Perhaps linked to the perceived complexity of their financial circumstances, those with 4 or more

policies are more likely than average to have complained about at least one of their policies via a CMC –

44% of these people complained through this route, vs. 31% for all PPI complainants.

There is a high degree of ‘continuity’ between the trigger for complaining and the subsequent method

of complaining. Of those people who have been triggered into complaining by a cold call from a CMC,

84% went on to raise a complaint via a CMC. Of those who have been triggered into complaining by a

letter from their provider, 80% went on to raise a complaint via their provider.

4%

4%

7%

31%

64%

0% 20% 40% 60% 80% 100%

via a lawyer

Other

via a financial advisor

via a Claims Management Company

(CMC)

directly to the provider of the PPI

Methods of raising complaints on PPI

I complained…

Q25: How did you go about complaining about the payment protection insurance

(PPI) policy which you had Base: All who have complained about at least one PPIpolicy (n=2068)

Page 36

One quarter of those who complained referred their complaint to the Financial Ombudsman (25%).10

Younger people are significantly more likely than older people to have referred their most recent

complaint to the Financial Ombudsman, with almost half of 18-34 year-olds (45%) saying this,

compared to only one in seven of those aged 65+ (15%).

10 Q27: With regard to your most recent payment protection insurance (PPI) policy complaint, did you refer your complaint

to the Financial Ombudsman? Base: All who have complained about at least one PPI policy (n=2068)

Page 37

3.5 EXPERIENCE OF COMPLAINTS PROCESSThree in five PPI holders who have made a complaint (59%) say that they found the process of

complaining about their most recent PPI policy easy.11

A quarter (24%) report finding it very easy – while one in five (22%) report the process to be either

very or fairly difficult. The process of complaining seems to elicit fairly consistent responses

across multiple complaints, as three quarters of PPI holders who made more than one complaint

(73%) reportedly find previous experience(s) not to be different from their most recent

experience.12

Indeed, we asked PPI complainants about improvements to the complaints process – inquiring in the

form of an open-ended question about the one change that these people would make to the process if

given the opportunity. 13

Three in ten of those who had complained about PPI (28%) expressed their satisfaction with the

complaints process and said that no improvements could be made:

“It was very straightforward.”

Where those who had complained did suggest improvements, these were relatively diverse. The most

commonly given improvements tend to relate to making the complaints process faster (mentioned by

12% of PPI complainants):

“The process should be quicker and easier to claim for.”

A further 8% suggested that the process could be made easier, and 8% suggested that there should be

an automatic refund (rather than needing to go through the process of making a complaint):

“Providers should have a template for sending the complaint.”

7% suggested that there could be more information explaining how to complain, and 7% said that the

process could be improved by the removal of third party intermediaries such as CMCs:

“I would claim directly rather than through a CMC and save myself 25%.”

11 Q33a: With regard to your most recent payment protection insurance (PPI) policy, how difficult or easy did you find the

process of complaining about PPI? Base: All who have complained about at least one PPI policy (n=2068)

12 Q33b: Thinking about your other PPI complaints, did these experiences differ from your most recent PPI complaint? If

yes, please specify how the experience of your other complaints was different. Base: All who have complained about more

than one PPI policy [phase 4] (n=427)

13 Q34: If you could make one change to the process of complaining about your payment protection insurance (PPI) policy

what would it be? Base: All who have complained about at least one PPI policy (n=2068)

Page 38

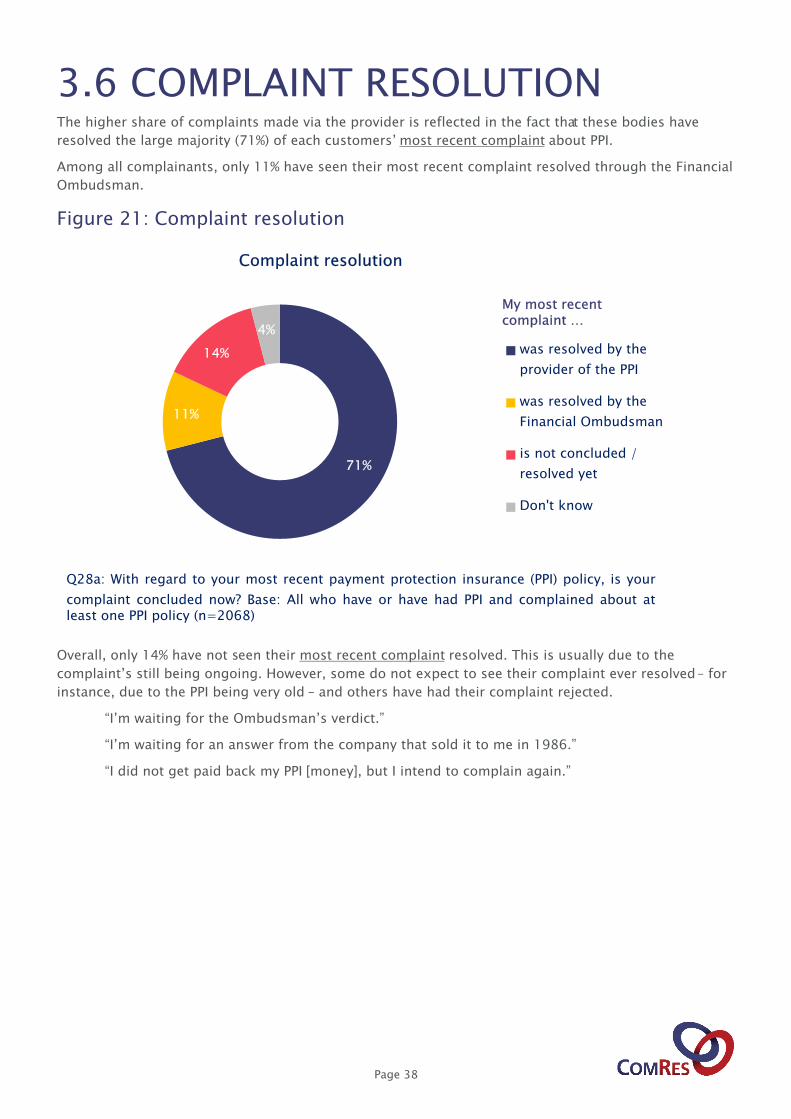

3.6 COMPLAINT RESOLUTIONThe higher share of complaints made via the provider is reflected in the fact that these bodies have

resolved the large majority (71%) of each customers’ most recent complaint about PPI.

Among all complainants, only 11% have seen their most recent complaint resolved through the Financial

Ombudsman.

Figure 21: Complaint resolution

Overall, only 14% have not seen their most recent complaint resolved. This is usually due to the

complaint’s still being ongoing. However, some do not expect to see their complaint ever resolved – for

instance, due to the PPI being very old – and others have had their complaint rejected.

“I’m waiting for the Ombudsman’s verdict.”

“I’m waiting for an answer from the company that sold it to me in 1986.”

“I did not get paid back my PPI [money], but I intend to complain again.”

71%

11%

14%

4%

Complaint resolution

was resolved by the

provider of the PPI

was resolved by the

Financial Ombudsman

is not concluded /

resolved yet

Don't know

My most recent complaint …

Q28a: With regard to your most recent payment protection insurance (PPI) policy, is your

complaint concluded now? Base: All who have or have had PPI and complained about at least one PPI policy (n=2068)

4. COMPENSATION

Page 40

4.1 EXPERIENCE OF COMPENSATIONAmong those PPI complainants whose claim was resolved, nine in ten (91%) did receive compensation –

almost two thirds (63%) £2,000 or less.

Of those who complained but did not receive compensation, 70% complained directly to their provider

and 26% complained via a CMC.

Figure 22: Compensation received

Among those who have received compensation, the majority (85%) are satisfied, with two in five (41%)

very satisfied.14 Just 14% say that they are dissatisfied with the compensation received, including only 5%

who say that they are very dissatisfied. Those who complained via their provider (87%) are more likely to

be satisfied than those who complained via a CMC (81%).

14 Q30: Taking everything into consideration, to what extent would you say that you are satisfied or dissatisfied with this

sum of compensation? Base: All who have complained about at least one PPI policy and received PPI compensation

(n=1554)

9%

4%

7%

17%

21%

19%

24%

0% 20% 40% 60% 80% 100%

I did not receive compensation

£10001 or more

£5001 - £10000

£2001 - £5000

£1001 - £2000

£501 - £1000

£500 or less

Compensation received

Q29: With regard to your most recent payment protection insurance (PPI) policy, how much

compensation, if any, did you receive as a result of your complaint? Base: All who have had their most recent PPI complaint resolved (n=1708)

Page 41

4.2 PAST USE OF COMPENSATIONAs Figure 23 illustrates, almost half of people who received compensation from their most recent

complaint used this sum for saving and/ or investing (43%) and more than a third used it for paying

down one or more kinds of debt (37%), while a third (32%) spent it. It is worth stressing that the total

categories given in the figure below have been added as an analytical tool after fieldwork – this

categorisation was not presented to respondents completing the survey, and individuals may also fall

into multiple categories. Similarly, the total figures are not reflective of monetary values – we do not

have information on the amount of money that each respondent saved or the amount that they spent,

for example. A person may have saved £5 in a bank account and spent £300 on a large purchase, and

would be classified in both categories.15

Figure 23: Past use of compensation

15 The questions on compensation were only asked in phases 1-3 of the research, being removed for phase 4 to ensure

that there was sufficient space to ask questions about Plevin vs. Paragon Personal Finance without encountering

respondent fatigue. Further information on this is available in the separate technical report on this study.

Q31: Thinking of the compensation you got as one-off unexpected additional income, can you

recall how you used it? Multiple answers possible Base: All those who have complained about at least one PPI policy and received compensation (n=791)

35%

10%

0%

20%

40%

60%

80%

100%

TOTAL: Saved/Invested

(43%)

Saved it in my bank

account

Saved/invested in

dedicated

account/investment

plan

18% 16%

TOTAL: Spent (32%)

Spent it on

everyday

expenses

Spent it on a

large purchase

16%

8%4% 3%

14%

TOTAL: Paid Down Debt (37%)

Used it to pay down credit card

debt

Used it to pay down/clear

overdraft

Used it to pay down mortgage

Used it to pay down student

loan debt

Used it to pay down other debts

Past use of compensation

Page 42

4.3 LIKELY USE OF POTENTIAL FUTURE COMPENSATIONWhen asking all those who have, have had or may have had PPI how they would use future compensation

money responses are broadly similar to the ways in which complainants who received compensation

reported using it:

PPI holders are more likely to say that they would save the money (46%, compared to 43% who

did save and / or invest the money that they received from compensation [see Figure 23]) than

spend it or use it to pay down debt;

More than two in five of those aged 25-34 (43%) and those aged 35-44 (42%) would use

compensation to pay down various debts.

Figure 24: Likely use of potential future compensation

Q46: If you do complain and receive compensation as one-off additional income, how do you

think you would use it? Multiple answers possible Base: All who have, have had or may have had a PPI policy (n=3137)

38%

12%

0%

20%

40%

60%

80%

100%

TOTAL: Save/Invest

(46%)

Save it in my bank

account

Save/invest in

dedicated

account/investme

nt plan

14% 14%

TOTAL: Spend (26%)

Spend it on

everyday expenses

Spend it on a large

purchase

15%

7% 8%2%

14%

TOTAL: Pay Down Debt (34%)

Use it to pay down credit

card debtUse it to pay down/clear

overdraftUse it to pay down

mortgageUse it to pay down student

loan debtUse it to pay down other

debts

Likely use of potential future compensation

5. POTENTIAL FUTURE COMPLAINTS – DEFINITE PPI HOLDERS

Page 44

5.1 INTENTION OF COMPLAININGAmong all who have or have had PPI, only one in eight (12%) intend to complain or complain again,

compared to three quarters (72%) who do not intend to do so and 16% who do not know if they will

complain.16

Approximately two thirds of those intending to complain (63%) have already complained about their

policy / at least one of their policies. Around one third (35%) have never complained before and intend

to complain for the first time. 2% do not know if they have complained before.

Those who have become aware of issues with PPI within the last year seem more intent on making a

complaint or complaining again than those who learned about problems 2-3 years ago and 4-5 years

ago (34% vs. 13% and 7% respectively).

16 Q35: Do you intend to complain (or make another complaint) about any of the payment protection insurance (PPI)

policies you have? Base: All who have or have had a PPI policy (n=4385)

Page 45

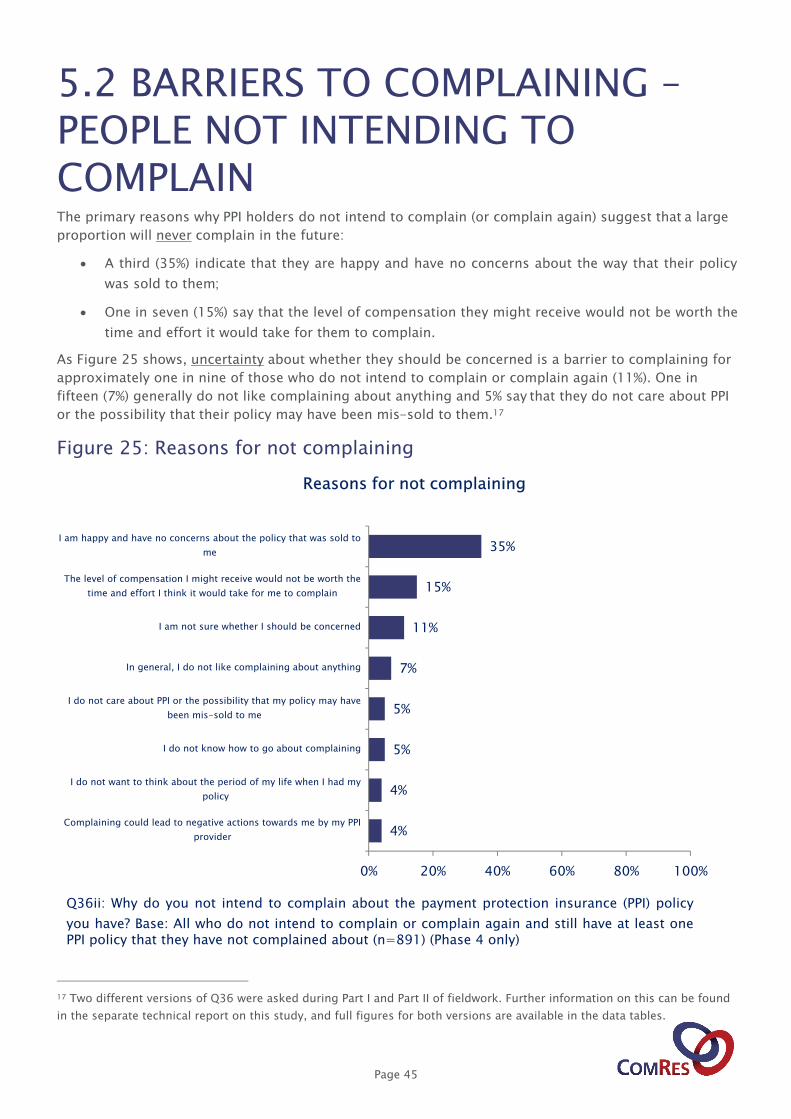

5.2 BARRIERS TO COMPLAINING –PEOPLE NOT INTENDING TO COMPLAINThe primary reasons why PPI holders do not intend to complain (or complain again) suggest that a large

proportion will never complain in the future:

A third (35%) indicate that they are happy and have no concerns about the way that their policy

was sold to them;

One in seven (15%) say that the level of compensation they might receive would not be worth the

time and effort it would take for them to complain.

As Figure 25 shows, uncertainty about whether they should be concerned is a barrier to complaining for

approximately one in nine of those who do not intend to complain or complain again (11%). One in

fifteen (7%) generally do not like complaining about anything and 5% say that they do not care about PPI

or the possibility that their policy may have been mis-sold to them.17

Figure 25: Reasons for not complaining

17 Two different versions of Q36 were asked during Part I and Part II of fieldwork. Further information on this can be found

in the separate technical report on this study, and full figures for both versions are available in the data tables.

4%

4%

5%

5%

7%

11%

15%

35%

0% 20% 40% 60% 80% 100%

Complaining could lead to negative actions towards me by my PPI

provider

I do not want to think about the period of my life when I had my

policy

I do not know how to go about complaining

I do not care about PPI or the possibility that my policy may have

been mis-sold to me

In general, I do not like complaining about anything

I am not sure whether I should be concerned

The level of compensation I might receive would not be worth the

time and effort I think it would take for me to complain

I am happy and have no concerns about the policy that was sold to

me

Reasons for not complaining

Q36ii: Why do you not intend to complain about the payment protection insurance (PPI) policy

you have? Base: All who do not intend to complain or complain again and still have at least one PPI policy that they have not complained about (n=891) (Phase 4 only)

Page 46

Moreover, perceived difficulty of the complaining process does not seem to be a major concern to PPI

holders in terms of intentions to complain, for both those who have or have had a PPI policy and those

who are unsure whether they have or have had PPI. More than a third of those who have, have had or

may have had a PPI policy (35%) believe that it would be easy to complain, and fewer than one in ten (9%)

believe it would be very difficult.

However, those who have not yet complained about any of their policies are more likely than those who

have done so to anticipate that the complaining process would be difficult – one in three of those who

have, have had or may have had PPI policy but have not yet complained (33%) think that the process

would be difficult, compared to one quarter of those who have already complained (25%) about at least

one of their policies.18

18 Q43: How difficult or easy do you think the process of complaining about a PPI policy might be? Base: All who have, have

had or may have had a PPI policy (n=6502)

Page 47

5.3 BARRIERS TO COMPLAINING –PEOPLE WHO INTEND TO COMPLAINAmong PPI holders who intend to complain or complain again, the main reason why they have not

complained already is a lack of time and energy, selected by two in five (40%) – this highlights the

challenge of inertia in relation to personal financial issues and triggering action. One in five (21%) cite a

lack of knowledge about how to make a complaint.

Figure 26: Barriers to complaining

This is very different from the responses of those PPI holders who do not intend to complain (see Figure

25), where a perception that the level of possible compensation they might receive would not be worth

the time and effort required to complain was cited by just 15% and a lack of knowledge about

complaining by just 5%.

1%

1%

1%

21%

30%

40%

0% 20% 40% 60% 80% 100%

Long time ago

Told I don't qualify

Already checked

I am not sure how to

I had to check if I ever had PPI

I have not had the time/energy

Barriers to complaining

- showing top six

Q41: What has prevented you from complaining already? Base: All who intend to complain or complain again about at least one PPI policy (n=508)

Page 48

5.4 PROMPTS FOR COMPLAINTSWhen prompted on which methods would make them more likely to complain again, for the first time or

to complain sooner than originally planned, people who have, have had or may have had PPI appear

three times more responsive to letters from providers explaining how to complain (64% reportedly would

be more likely to complain following receipt of this letter) than to cold calls from CMCs (20% reportedly

would be more likely to complain after being prompted in this manner). This again highlights the

propensity of people to make complaints through providers rather than CMCs, already observed in those

people who did make a complaint (see Figure 20).

As Figure 27 shows, more than half of those who have, have had or may have had PPI (54%) say that

communications from the government explaining how to complain would make them more likely to

complain.

Although there is no clear pattern for those 11% who say it is likely that something ‘other’ would have

prompted them to complain, many of these people say that more information would have prompted

them to do so, for instance, from an online consumer advice website.19

19 Different options were used for Q44 in different phases of the fieldwork, which explains the variable base sizes in Figure

27. Further information is included in the technical report, in section 2 on Questionnaire Design.

Page 49

Figure 27: Reported effectiveness of prompts to complain

3%

6%

7%

13%

14%

15%

16%

18%

19%

30%

8%

14%

23%

33%

34%

36%

27%

36%

36%

34%

28%

24%

31%

24%

26%

24%

27%

23%

21%

16%

14%

44%

26%

17%

14%

13%

16%

11%

11%

10%

47%

12%

13%

12%

12%

12%

15%

12%

13%

10%

0% 20% 40% 60% 80% 100%

Other

Cold call from a Claims Management Company…

Media advertisments from CMCs

Media advertisements explaining how to complain

Media news stories explaining how to complain

Advice from friends and family

A deadline on complaining

Communications from the government…

Successful complaint by family and friends

Letter from my provider explaining how to…

Reported effectiveness of prompts to complain

Very likely Fairly likely Not very likely

Not at all likely Don't know

Q44: How likely, if at all, would you say the following scenarios would be to prompt you to

complain, or, if you are already intending to complain, to do so sooner? Base: All those who have, have had or may have had a PPI policy (n=3137-6502)

Page 50

5.5 TIMEFRAME OF INTENDED COMPLAINTSThose who intend to complain reportedly plan to do so in the near future: on a scale from zero (not

likely at all) to ten (certain), more than two in five (44%) are most likely to complain in the next six

months.

A third (34%) of those intending to complain are most likely to complain in more than three years. As

with the perceived likelihood of checking whether they have had PPI at all (see Checking about PPI20),

this time gap suggests that it is relatively unlikely that these people will complain at all.

Figure 28: Timeframe of intended complaints

Using responses on a 0-10 scale for each option, we identified the time period in which people say they are most

likely to complain. Where people select the same score out of 10 for two or more time slots, we allocated people to

the latest time slot (i.e. if a person selected 2 for “in 0-6 months”, 3 for “in 7-12 months”, 6 for “in 1-3 years” and 6

for “in more than three years”, they would be allocated to “in more than three years”.

20 Section 2.2.

7%

34%

5%

10%

44%

0% 20% 40% 60% 80% 100%

Don't know

In more than 3 years

In 1-3 years

In 7-12 months

In 0-6 months

Timeframe of intended complaints

Showing time period in which people are most likely to complain

Q38: How likely, if at all, would you say that you are to complain within the following

time periods? Base: All who intend to complain or complain again about at least one PPI

policy [Excluding pilot for phase 4] (n=474)

Page 51

5.6 LIKELY CHANNELS FOR COMPLAINTSThose who intend to complain state that they expect to do so through methods broadly similar to those

who have already complained. As Figure 29 shows, approximately half (49%) intend to complain directly

to the provider. A quarter (26%) expects to complain through a CMC, followed at a distance by financial

advisors (12%) and lawyers (8%).

Figure 29: Expected channel of raising complaints

49%

26%

12%

8% 2%

Expected channels of raising complaints on PPI

directly to the provider of the

PPI

via a Claims Management

Company (CMC)

via a financial advisor

via a lawyer

Other

I intend to complain…

Q39: How are you intending to complain? Base: All who intend to complain/ complain again about at least one PPI policy (n=508)

6. POTENTIAL FUTURE COMPLAINTS – POSSIBLE PPI HOLDERS

Page 53

6.1 TIMEFRAME OF POTENTIAL COMPLAINTSFor those who are not 100% sure whether they have had PPI or “really don’t know”, we introduced a

hypothetical scenario in phases two, three and four of the research where we suggested that they had

discovered that they definitely held a PPI policy.21

Firstly, we then asked them to rate how likely they would be to complain in this situation, on a scale

from 0-10. We then calculated the timeframe in which these people are most likely to complain –

allocating them to one of the time slots based on the slot for which they select the highest score. Where

people select the same score out of 10 for two or more time slots, we allocated people to the latest time

slot (i.e. if a person selected 2 for “in 0-6 months”, 3 for “in 7-12 months”, 6 for “in 1-3 years” and 6 for

“in more than three years”, they would be allocated to “in more than three years”.

Using this analysis, a quarter (26%) are most likely to complain in the next six months, whereas a third

(35%) are most likely to complain in more than 3 years. Another quarter (26%) say they do not know

when they would complain.22 As with Figure 28, it seems unlikely that the two latter groups would

indeed complain at all.

Figure 30: Timeframe of hypothetical complaints

For Figure 30, we identified the time period in which people say they are most likely to complain using responses on

a 0-10 scale for each option. In cases where equal scores were provided for each period we assigned the value to

the option that is more distant in time to provide a more conservative evaluation.

21 For phases two and three of the research, we introduced an additional set of questions for those who were not sure

whether they had held a PPI policy – either saying that they “really don’t know” or are “not 100% sure”. Further detail on this

can be found in the Questionnaire Design section in the technical report.

22 The high proportion of “don’t know” responses reflects a common trend when asking hypothetical questions, as

respondents can find it difficult to place themselves in the situation posed.

26%

35%

5%

8%

26%

0% 20% 40% 60% 80% 100%

Don't know

In more than 3 years

In 1-3 years

In 7-12 months

In 0-6 months

Timeframe of hypothetical complaints

Showing time period in which people are most likely to complain

Q23c: Imagine that you checked whether you had payment protection insurance (PPI) and

discovered that you had one or more PPI policies. How likely, if at all, would you say that

you would be to complain within the following time periods? Base: All who are not 100%

sure or really don't know if they have had a PPI policy [Phases 2/3] (n=594)

Page 54

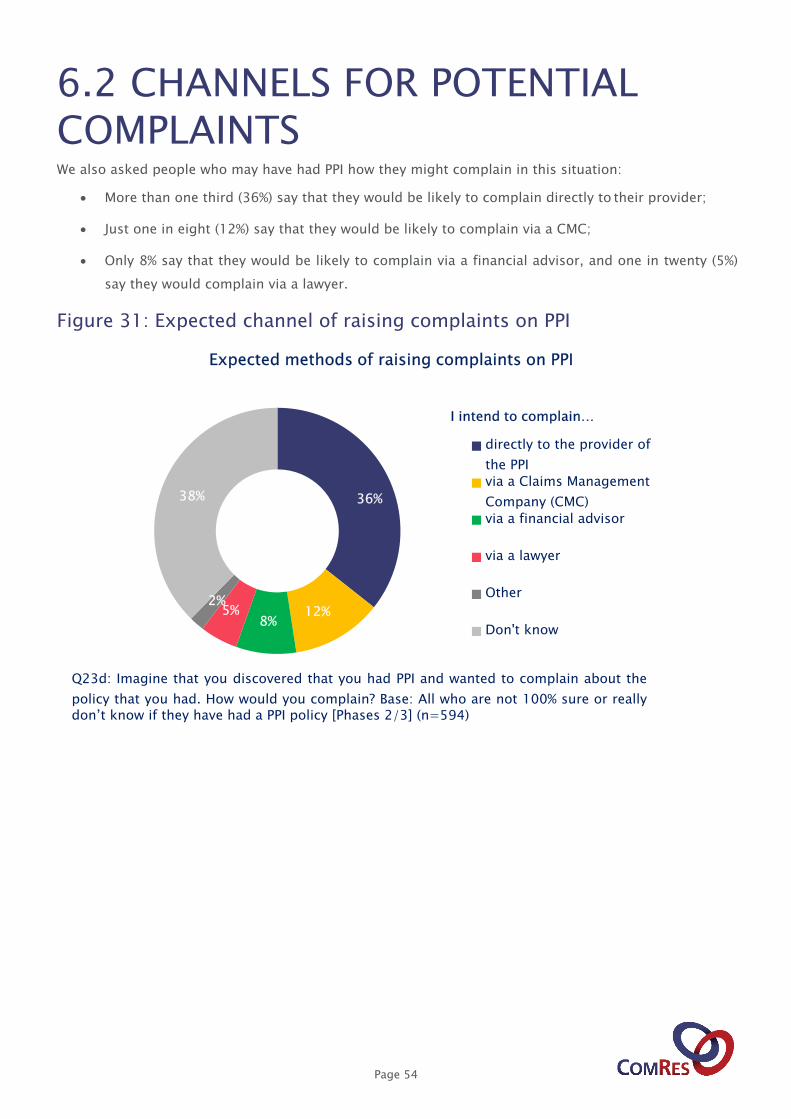

6.2 CHANNELS FOR POTENTIAL COMPLAINTSWe also asked people who may have had PPI how they might complain in this situation:

More than one third (36%) say that they would be likely to complain directly to their provider;

Just one in eight (12%) say that they would be likely to complain via a CMC;

Only 8% say that they would be likely to complain via a financial advisor, and one in twenty (5%)

say they would complain via a lawyer.

Figure 31: Expected channel of raising complaints on PPI

36%

12%8%

5%2%

38%

Expected methods of raising complaints on PPI

directly to the provider of

the PPI

via a Claims Management

Company (CMC)

via a financial advisor

via a lawyer

Other

Don't know

I intend to complain…

Q23d: Imagine that you discovered that you had PPI and wanted to complain about the

policy that you had. How would you complain? Base: All who are not 100% sure or really don’t know if they have had a PPI policy [Phases 2/3] (n=594)

7. THE IMPACT OF PLEVIN VS. PARAGON PERSONAL FINANCE

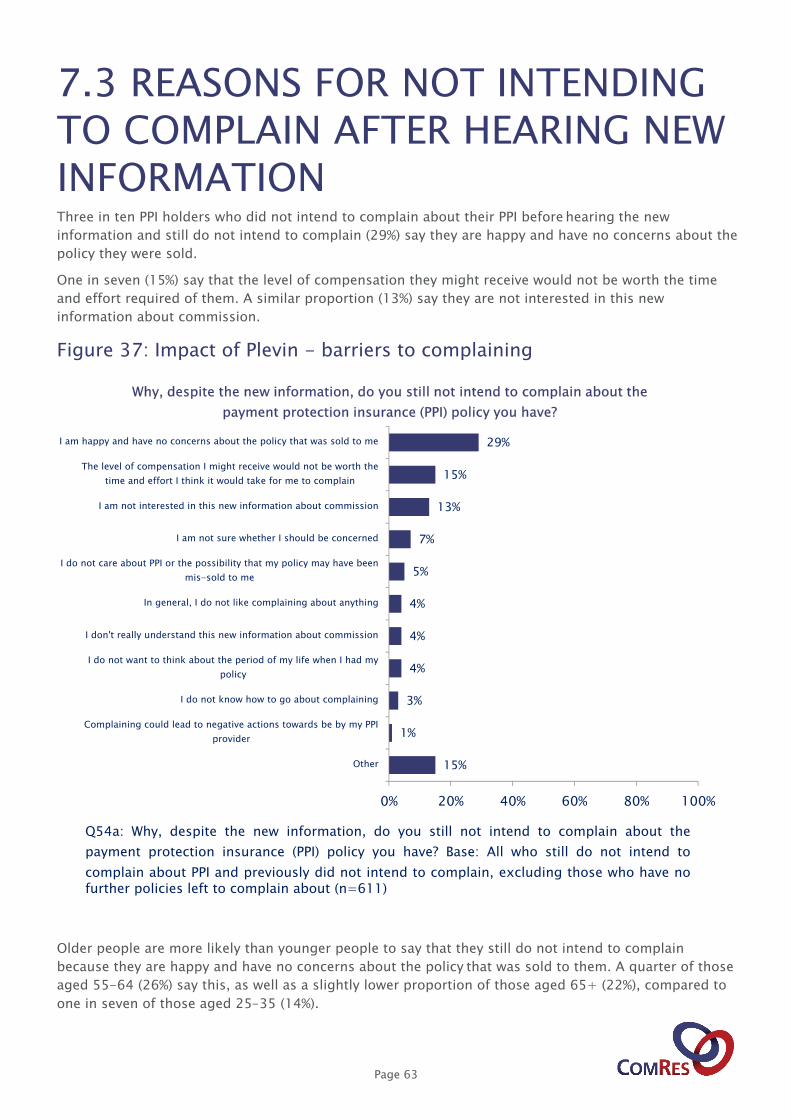

Page 56

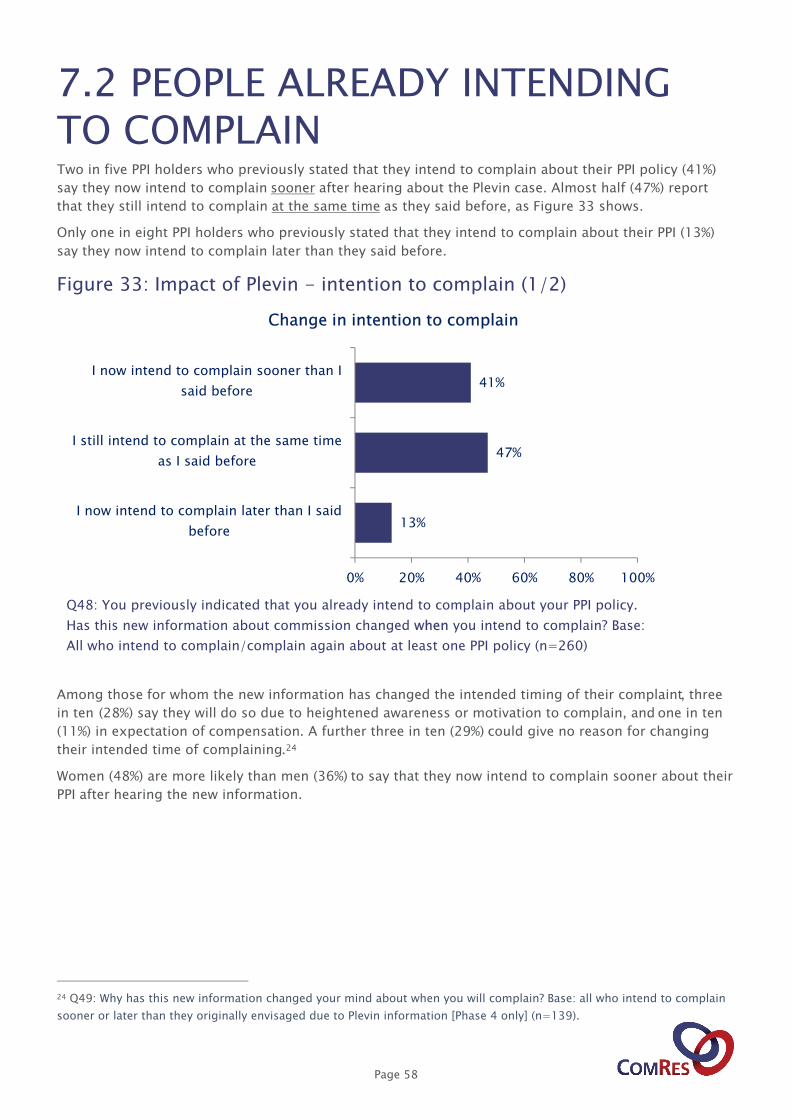

7.1 INTRODUCING THE CASEIn wave 4 of the research, we wanted to understand whether information regarding the outcome of the

Plevin vs. Paragon Personal Finance case had an impact on complaining behaviour around PPI. To do