An Overview of Developments in Connected TV Final

36

Mike Grant Founder & CEO 12 th May 2011 Connected TV: the storm approaches

-

Upload

mikedotgrant -

Category

Documents

-

view

218 -

download

0

Transcript of An Overview of Developments in Connected TV Final

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 1/36

Mike Grant

Founder & CEO12th May 2011

Connected TV: the storm approaches

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 2/36

Introduction to Caru Ventures Caru Ventures helps telecoms and media companies prepare for and then delive

successful innovation to the benefit of the company and its shareholders The company provides consulting and interim management services to organisat

of all sizes within the telecoms and media space

Founder and CEO, Dr Mike Grant, has spent twenty years working at the leadingedge of technology and service developments within the sector: Four patents in new optical transmission technologies Led the development and deployment of 3D graphics technology within the mobile

phone industry Built one of the worlds largest mobile games publishers

Supported the creation and deployment of IPTV services by broadcasters and telecoperators

Advised media regulators on PayTV and TV Advertising policy

Provided business planning and finance support to mobile operators acquiring 3Gmobile network licences

Supported governments seeking to licence spectrum to the mobile phone industry

Mike is currently working with three start-ups developing image recognitiontechnology, innovative solutions for connected TV, and new content business mo

He is also raising a Venture Capital Fund to support innovative organisations in tIT, Telecoms and Media space.

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 3/36

Agenda What is “Connected TV”?

1. Basic two way connectivity2. Home network connectivity3. New types of TV experiences

Market dynamics and changes in the value chain

Issues arising:1. Who owns the screen … and, hence, the consumer? 2. Can TV revenue levels be maintained?3. The impact on production and distribution costs4. Liability, privacy and consumer protection

5. What future linear TV?

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 4/36

Agenda

What is “Connected TV”? Market dynamics and changes in the value chain

Issues arising:

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 5/36

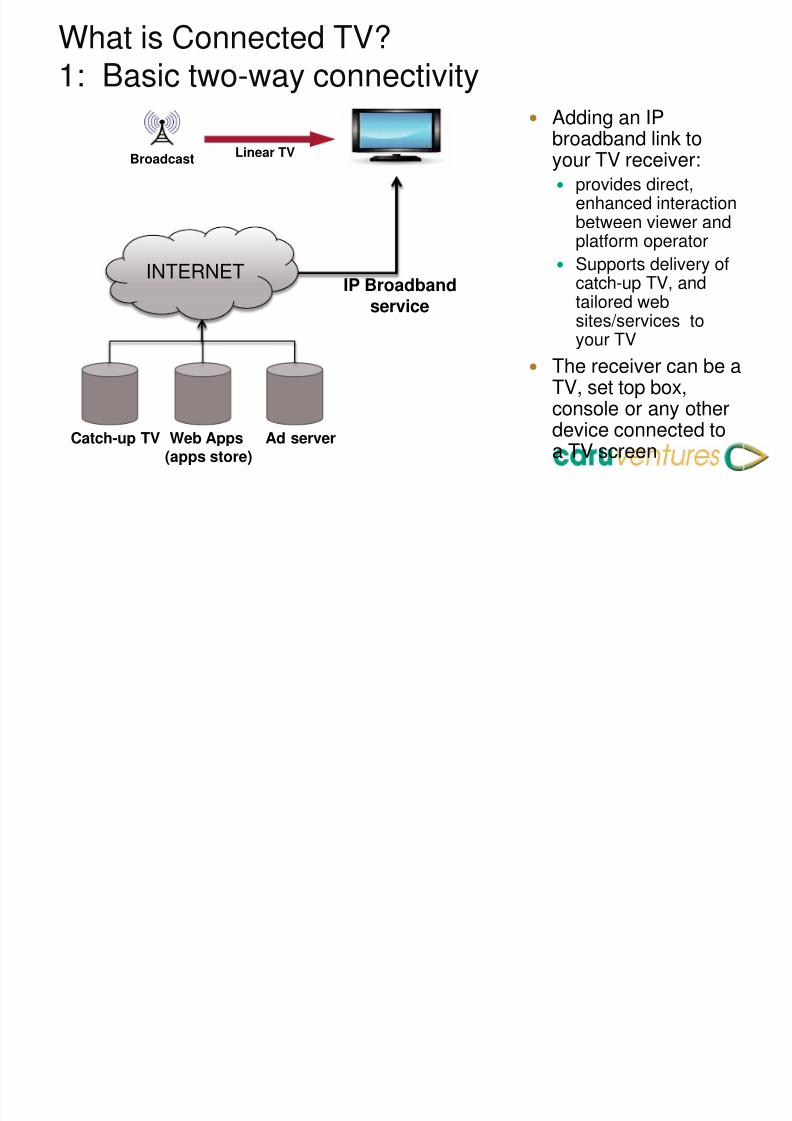

What is Connected TV?1: Basic two-way connectivity

Adding an IP

broadband link toyour TV receiver: provides direct,

enhanced interabetween viewer platform operato

Supports delivercatch-up TV, andtailored websites/services toyour TV

The receiver can TV, set top box,

console or any otdevice connecteda TV screen

INTERNET

BroadcastLinear TV

Catch-up TV Web Apps(apps store)

IP Broadbandservice

Ad server

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 6/36

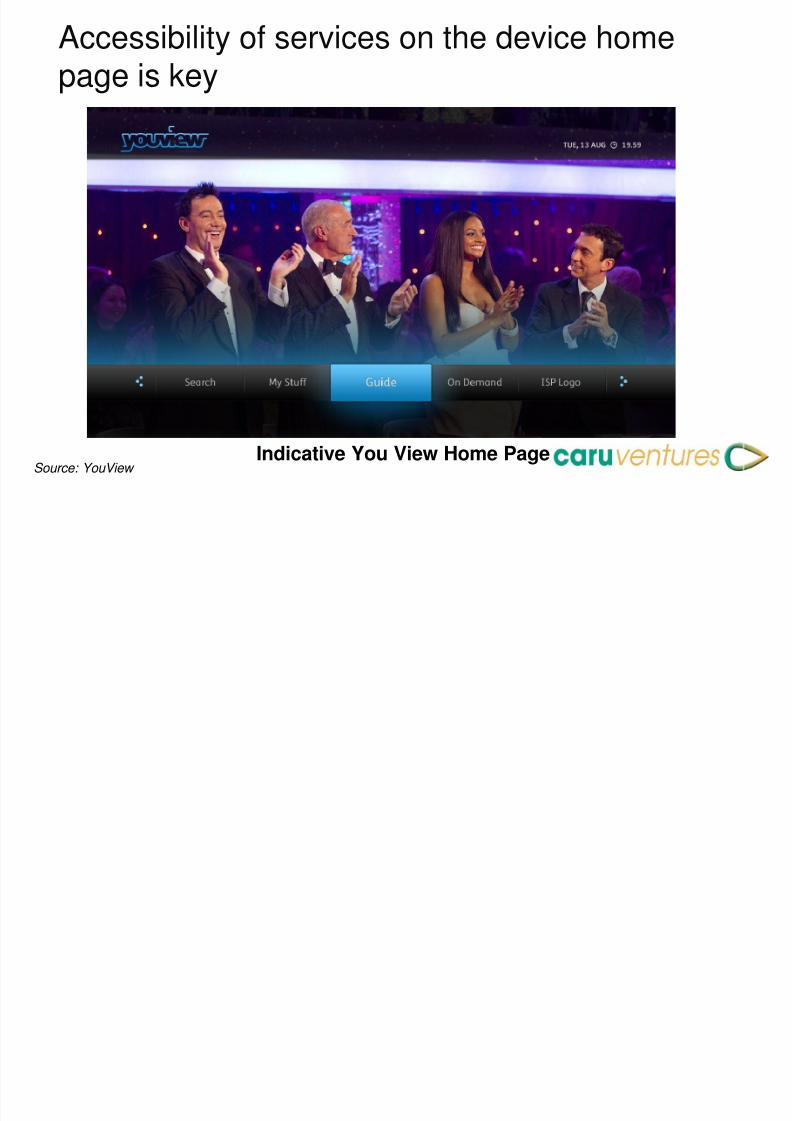

Accessibility of services on the device homepage is key

Indicative You View Home PageSource: YouView

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 7/36

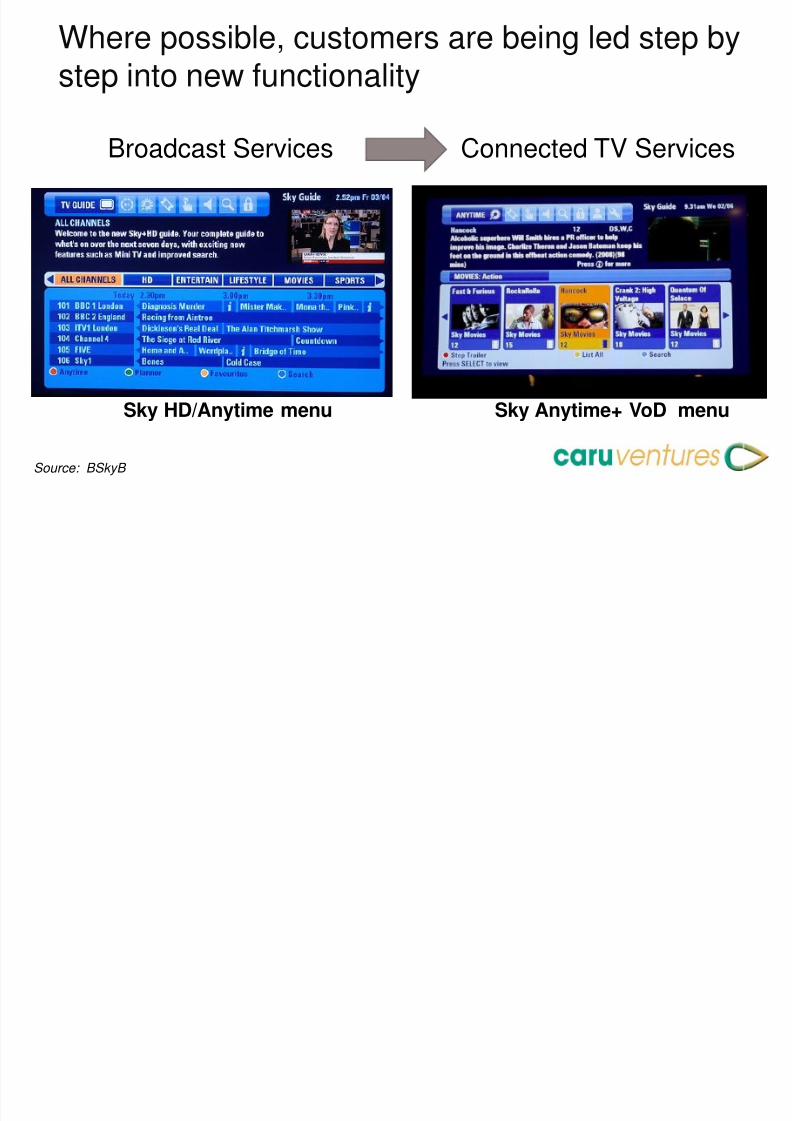

Where possible, customers are being led step step into new functionality

Sky HD/Anytime menu Sky Anytime+ VoD me

Broadcast Services Connected TV Servic

Source: BSkyB

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 8/36

However, adding web apps makes the interfacissue much more complicated

How many apps can a customermanage on his TV?

How many different ways of accecontent can a customer cope w

Source: Samsung

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 9/36

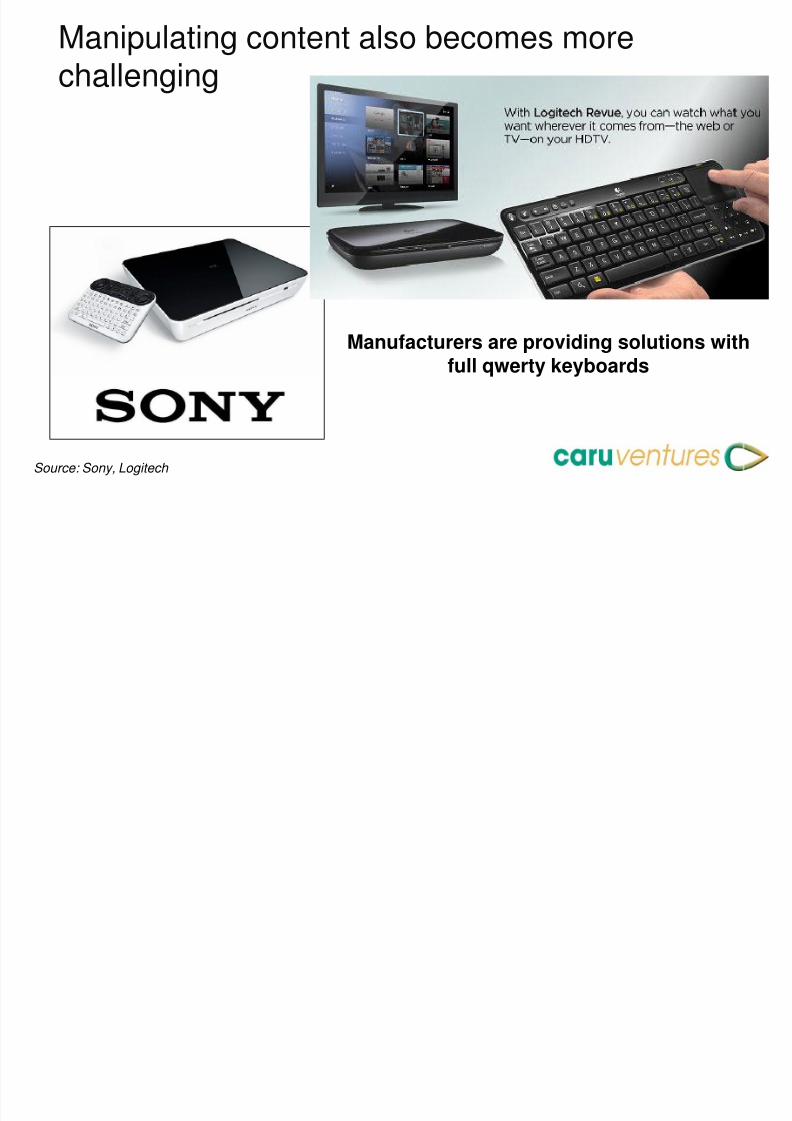

Manipulating content also becomes morechallenging

Manufacturers are providing solutionsfull qwerty keyboards

Source: Sony, Logitech

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 10/36

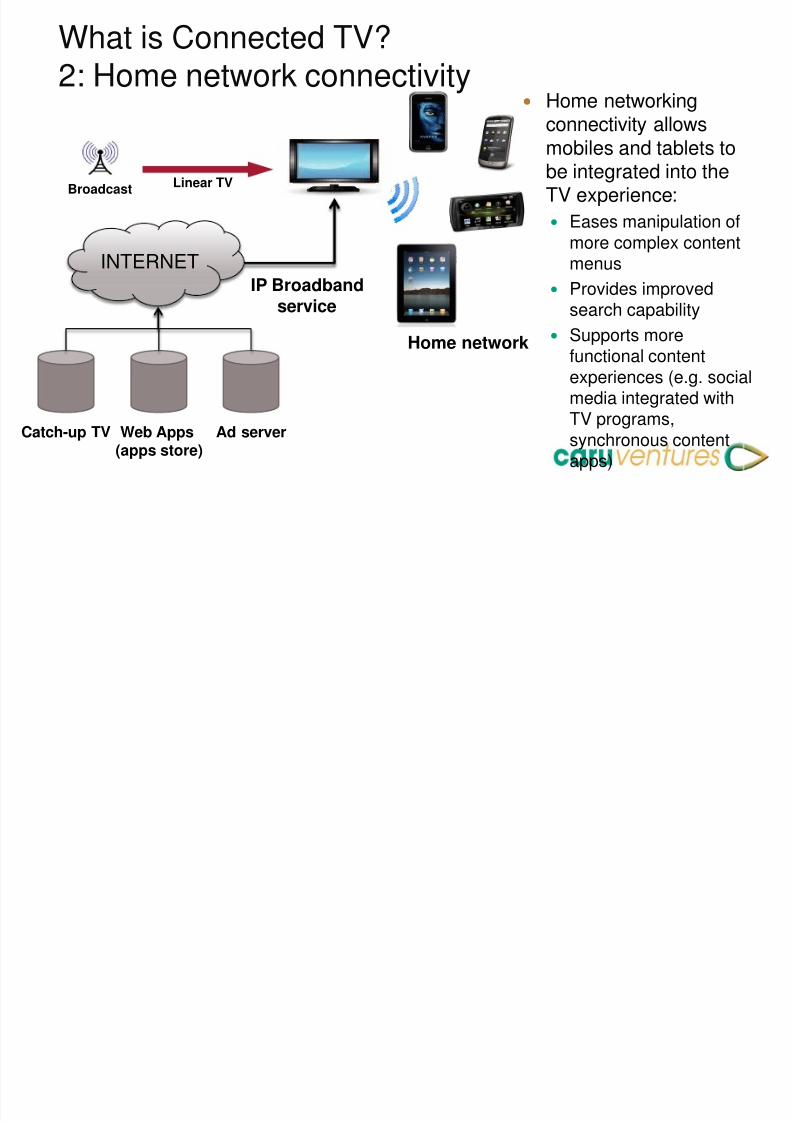

What is Connected TV?2: Home network connectivity

Home networkingconnectivity allows

mobiles and tabletbe integrated into TV experience:

Eases manipulatimore complex comenus

Provides improvesearch capability

Supports morefunctional contenexperiences (e.g.media integrated

TV programs,synchronous conapps)

BroadcastLinear TV

INTERNETIP Broadband

service

Home network

Catch-up TV Web Apps(apps store)

Ad server

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 11/36

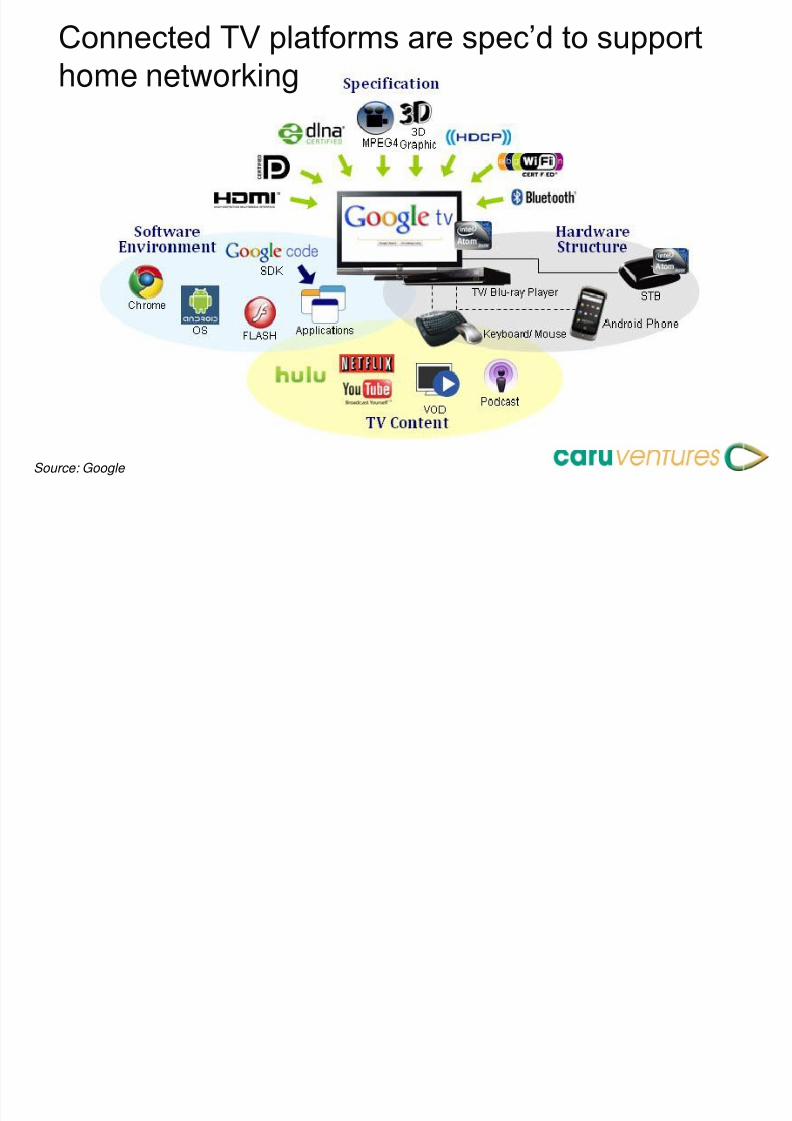

Connected TV platforms are spec‟d to support

home networking

Source: Google

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 12/36

What is Connected TV?3: New types of “TV” experiences

The introduction of IP changes the nature of TV content. Contenwill become time insensitive, interactive, and richer companion sites, made more relevant by dual/multi screen use social media components. multilayer program elements overlays leading to other content elements,

Content will become context sensitive Programs that present different content elements depending on

when or where you are watching, Program and application elements that change to match user valu

and preferences Program that are aware of more than one device in the hands of t

viewer Programs that are aware of the location of the consumer

Content will also be device sensitive

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 13/36

New experiences will be based on a newrelationship between producer and consumer

Content producer/program maker and consumer wfor the first time be able to engage in a directconversation

That conversation will enrich still further the newexperiences connected TV will support

These new TV experiences can be classified intothree distinct categories : Standalone experiences

Asynchronous applications

Synchronous experiences

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 14/36

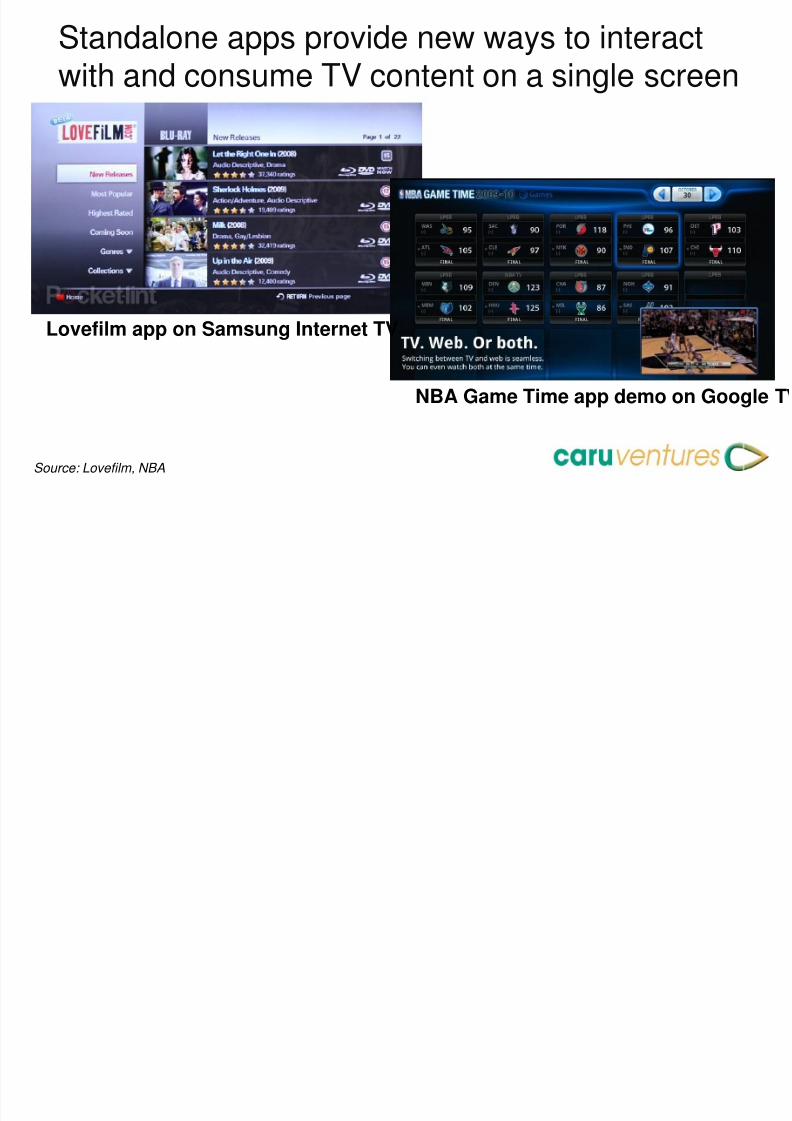

Standalone apps provide new ways to interactwith and consume TV content on a single scre

Lovefilm app on Samsung Internet TV

NBA Game Time app demo on

Source: Lovefilm, NBA

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 15/36

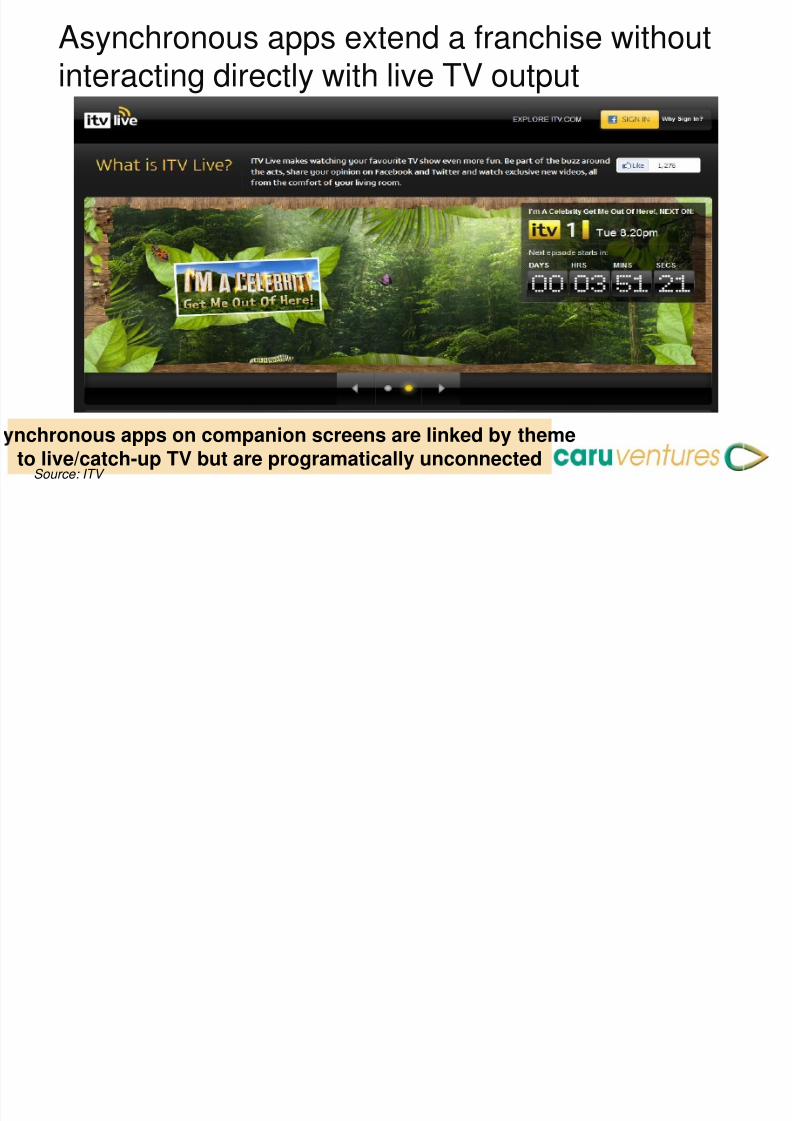

Asynchronous apps extend a franchise withouinteracting directly with live TV output

nchronous apps on companion screens are linked by themeto live/catch-up TV but are programatically unconnected

Source: ITV

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 16/36

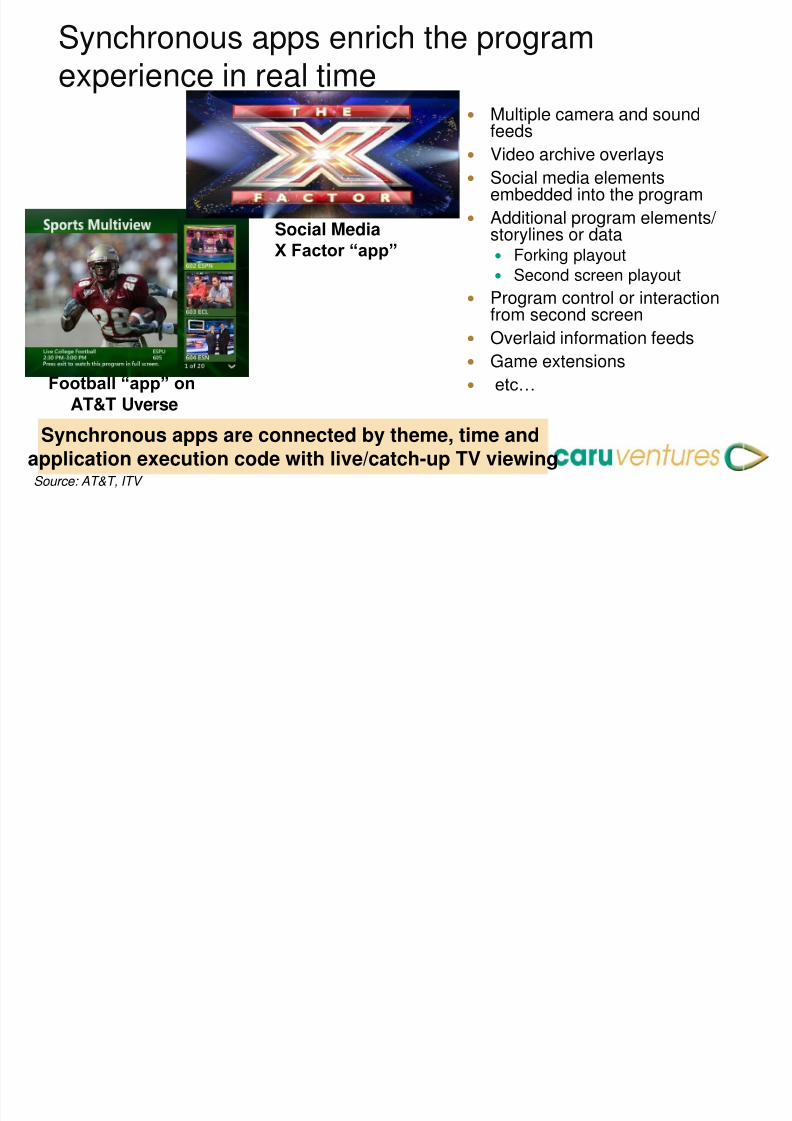

Synchronous apps enrich the programexperience in real time

Multiple camera and soundfeeds

Video archive overlays

Social media elementsembedded into the program

Additional program elementstorylines or data Forking playout

Second screen playout Program control or interacti

from second screen

Overlaid information feeds

Game extensions

etc…

Synchronous apps are connected by theme, time andapplication execution code with live/catch-up TV viewing

Football “app” on

AT&T Uverse

Social MediaX Factor “app”

Source: AT&T, ITV

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 17/36

Content organisations of all types are developapps for connected TV

Broadcasters

TV producers

Film studios

Newspaper companies

Social mediacompanies

Government agencies

Games companies

Retailers

Telecoms operators

Web retailers

Music distributors

Premier sports rights

holders Weather agencies

Travel companies

Online auction

companies Etc…

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 18/36

Agenda

What is “Connected TV”?

Market dynamics and changes in the value chain

Issues arising:

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 19/36

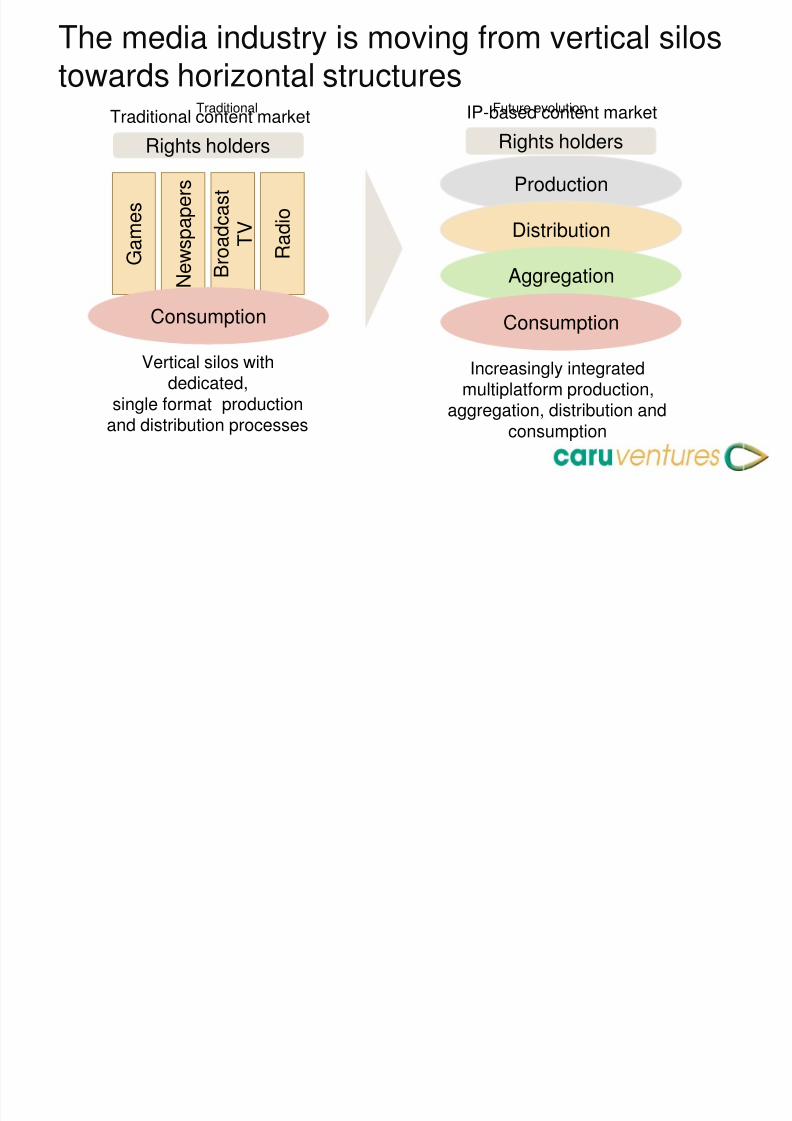

The media industry is moving from vertical silotowards horizontal structures

Traditional

Production

Distribution

Future evolution

G a m e s

Vertical silos withdedicated,

single format production

and distribution processes

N

e w s p a p e r s

B r o a d c a s t

T V

R a d i o

Increasingly integratedmultiplatform production,

aggregation, distribution andconsumption

Traditional content market IP-based content market

Rights holders Rights holders

Aggregation

ConsumptionConsumption

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 20/36

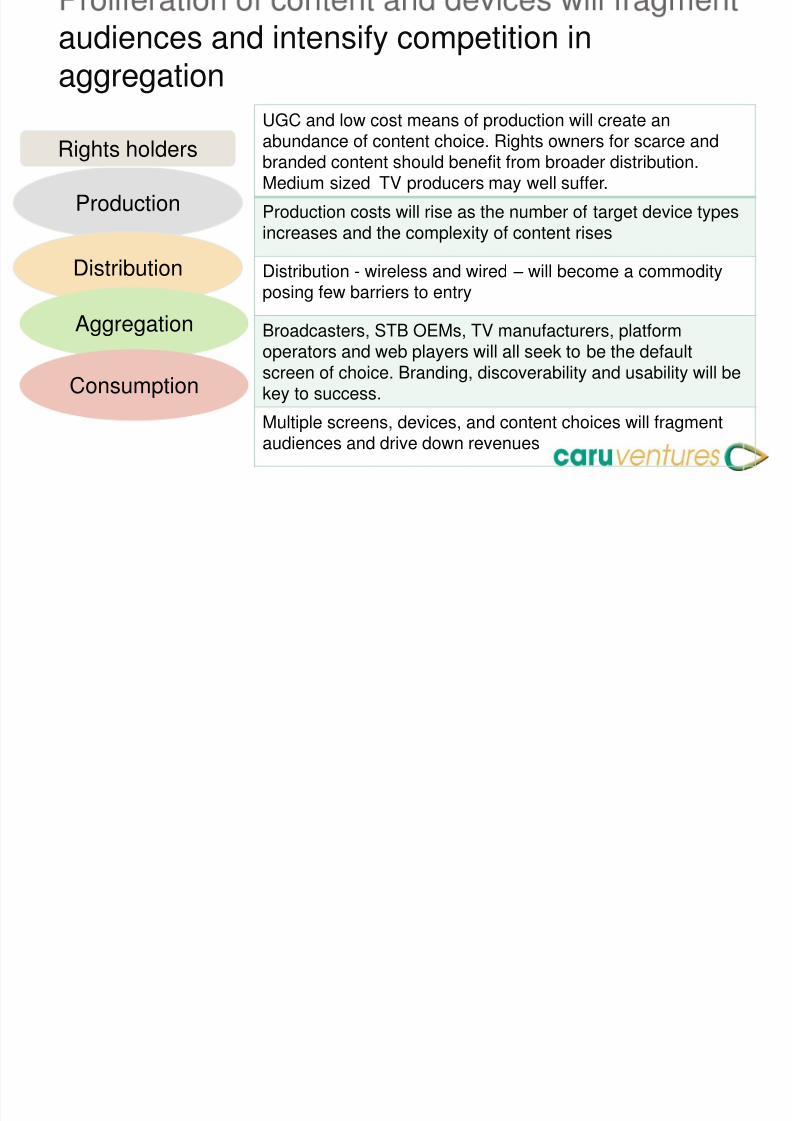

audiences and intensify competition inaggregation

Production

Distribution

Rights holders

Aggregation

Consumption

UGC and low cost means of production will create an

abundance of content choice. Rights owners for scarce abranded content should benefit from broader distribution.Medium sized TV producers may well suffer.

Production costs will rise as the number of target device tincreases and the complexity of content rises

Distribution - wireless and wired – will become a commodposing few barriers to entry

Broadcasters, STB OEMs, TV manufacturers, platformoperators and web players will all seek to be the defaultscreen of choice. Branding, discoverability and usability wkey to success.

Multiple screens, devices, and content choices will fragmaudiences and drive down revenues

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 21/36

Agenda

What is “Connected TV”?

Market dynamics and changes in the value chain

Issues arising

1. Who owns the screen … and, hence, the consum

2. Can TV revenue levels be maintained?3. The impact on production and distribution costs

4. Liability, privacy and consumer protection

5. What future linear TV?

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 22/36

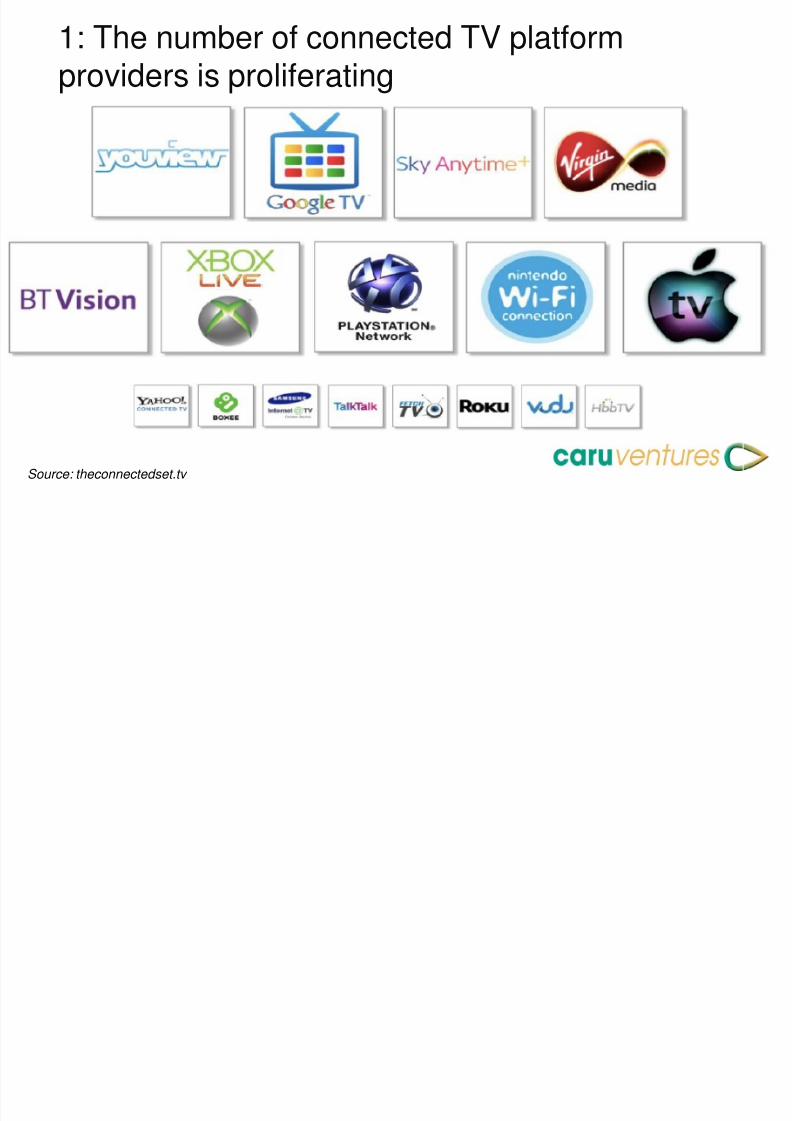

1: The number of connected TV platformproviders is proliferating

Independent VendorsFetch TV Source: IP Vision OEM TVs

Source: Sony

Source: theconnectedset.tv

A l h b l h h

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 23/36

As a result, the battle to own the home screenwill intensify …

Retailers, TV and STB OEMs, and Broadcasters may

seek to become service providers alongside the existiplatform operators Who will control the default set up of the screen and, with

default choices for consumers? Will YouView, Google, Apple, Sky and Virgin be the key

power brokers? How will content owners ensure they have primary

placement on all platforms of interest? Will the BBC need to lobby every Google TV STB and

games console manufacturer to ensure iPlayer is one of nine apps on the front page?

Will EPG regulations on placement of PSB “apps” apply? How will smaller content aggregators afford the costs of

bein on all ma or latforms?

d th h ll f t t t d

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 24/36

… and the challenge for content creators and

aggregators to capture audience share will rise

Presented with this level of choice, will audiences

coalesce around existing channel brands or fragmentacross multiple channels and device types? Who will be seen as the “TV providers” of the future?

The BBC, ITV, UK TV? Sky, Virgin, BT?

Apple, Samsung, Sony? Hulu, HBO, Disney, Endemol? Roku, Vudo, Fetch TV? Google/YouTube, Amazon/Lovefilm, Netflix? … other, yet to be invented, content aggregators?

2 C t d TV ill i

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 25/36

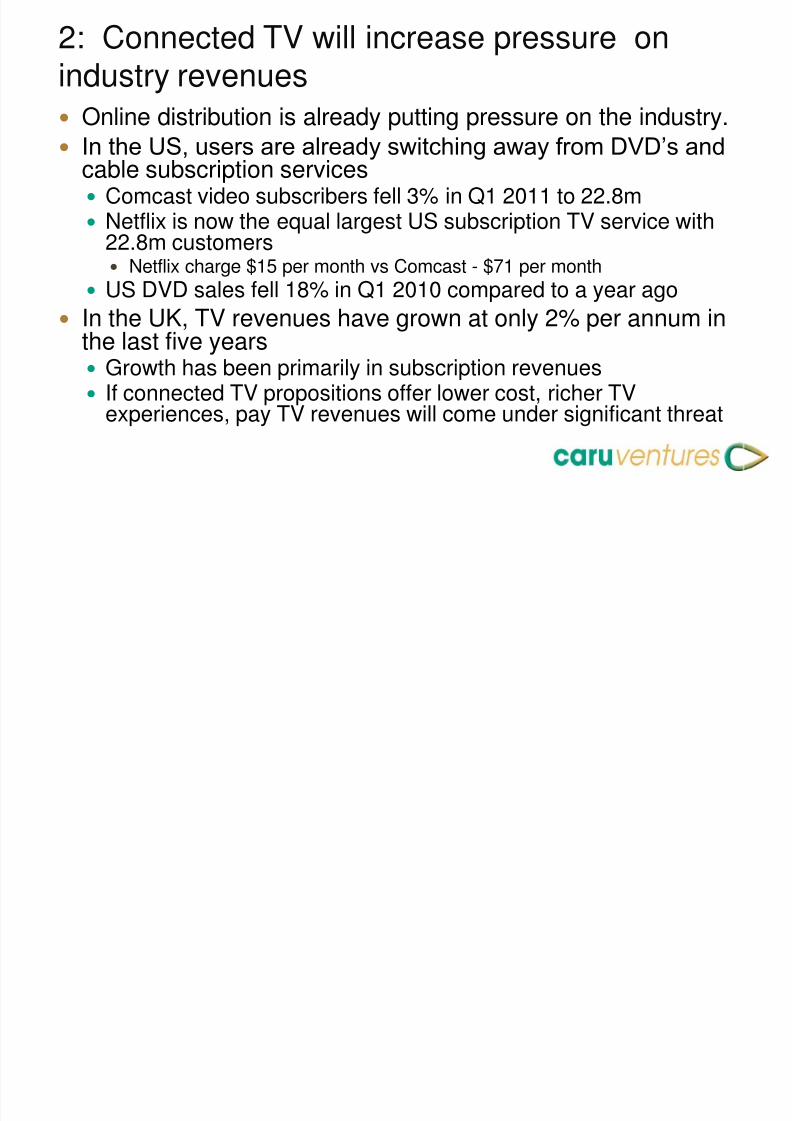

2: Connected TV will increase pressure onindustry revenues Online distribution is already putting pressure on the indust

In the US, users are already switching away from DVD‟s ancable subscription services Comcast video subscribers fell 3% in Q1 2011 to 22.8m Netflix is now the equal largest US subscription TV service wit

22.8m customers Netflix charge $15 per month vs Comcast - $71 per month

US DVD sales fell 18% in Q1 2010 compared to a year ago In the UK, TV revenues have grown at only 2% per annum

the last five years Growth has been primarily in subscription revenues If connected TV propositions offer lower cost, richer TV

experiences, pay TV revenues will come under significant thre

“N d l ” lik l t l

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 26/36

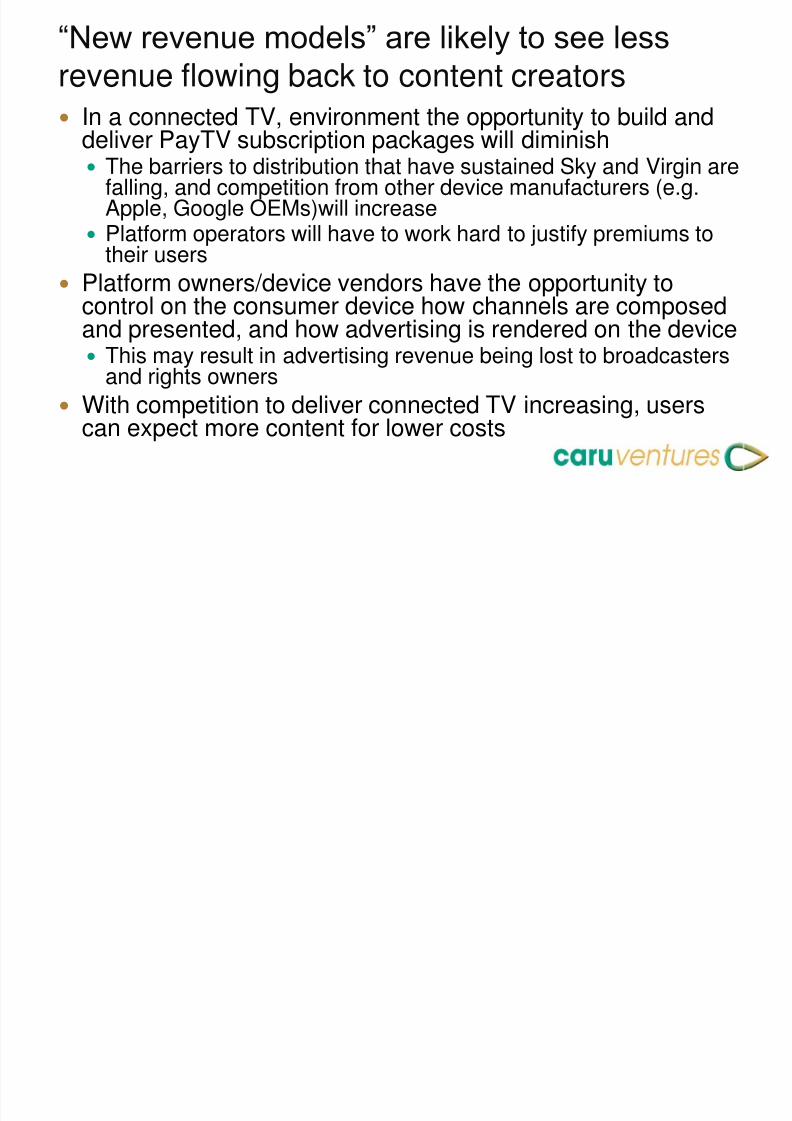

“New revenue models” are likely to see less

revenue flowing back to content creators In a connected TV, environment the opportunity to build an

deliver PayTV subscription packages will diminish The barriers to distribution that have sustained Sky and Virgin

falling, and competition from other device manufacturers (e.g.Apple, Google OEMs)will increase

Platform operators will have to work hard to justify premiums ttheir users

Platform owners/device vendors have the opportunity tocontrol on the consumer device how channels are composand presented, and how advertising is rendered on the dev This may result in advertising revenue being lost to broadcaste

and rights owners

With competition to deliver connected TV increasing, userscan expect more content for lower costs

i i l d i ifi t d it‟

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 27/36

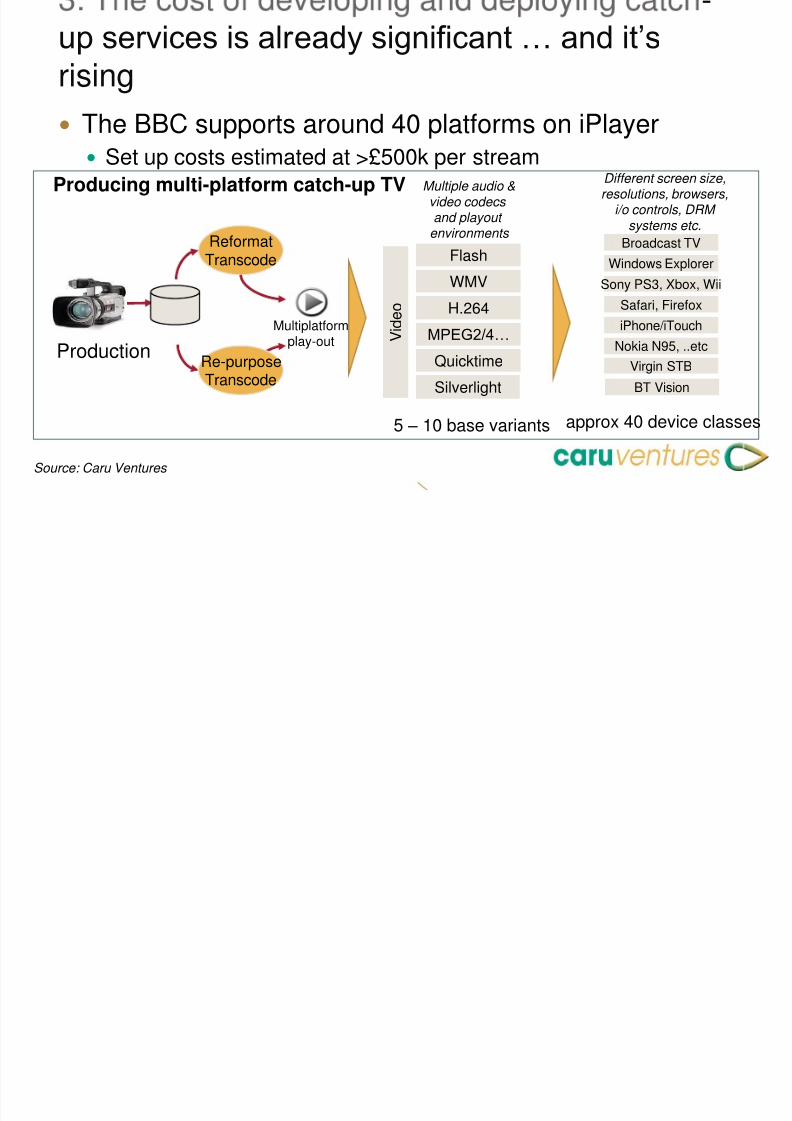

up services is already significant … and it‟s

rising

The BBC supports around 40 platforms on iPlayer Set up costs estimated at >£500k per stream

ReformatTranscode

Broadcast TV

Windows Explor

Sony PS3, Xbox, Safari, Firefox

iPhone/iTouch

Nokia N95, ..et

Multiple audio &video codecs and playout

environments

Multiplatform play-out

Re-purposeTranscode

Different screen sresolutions, brow

i/o controls, DRsystems etc.

Production

Producing multi-platform catch-up TV

Virgin STB

BT Vision

5 – 10 base variants approx 40 device

Flash

WMVH.264

MPEG2/4… V i d e o

Quicktime

Silverlight

Source: Caru Ventures

Introducing web technology into programs

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 28/36

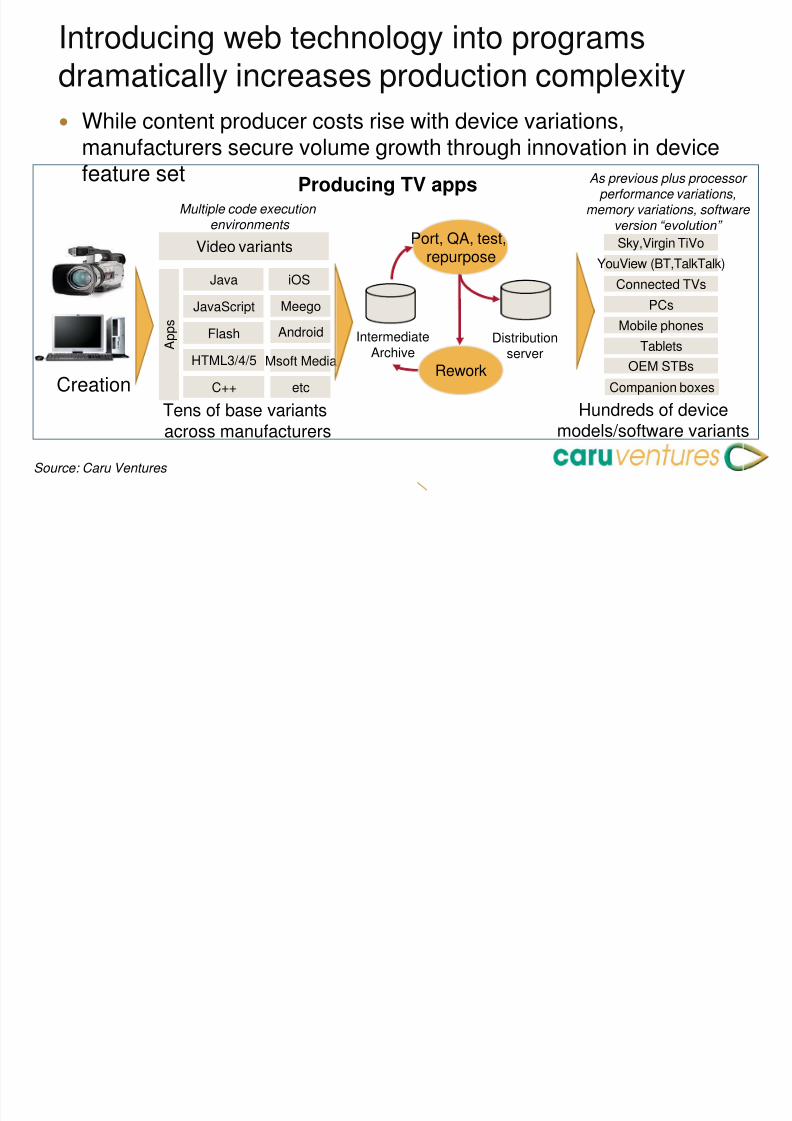

Introducing web technology into programsdramatically increases production complexity

While content producer costs rise with device variations,

manufacturers secure volume growth through innovation in devicfeature set

Port, QA, test,repurpose

Sky,Virgin TiVo

YouView (BT,TalkT

Connected TVsPCs

Mobile phones

TabletsIntermediate

Archive

Rework

As previous plus prperformance varia

memory variations, version “evoluti

Creation

Producing TV apps

OEM STBs

Companion box

Tens of base variantsacross manufacturers

Hundreds of devmodels/software va

Multiple code execution environments

Video variants

JavaJavaScript

Flash A p p s

HTML3/4/5

C++

iOSMeego

Android

Msoft Media

etc

Distributionserver

Source: Caru Ventures

challenge for program makers and TV app

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 29/36

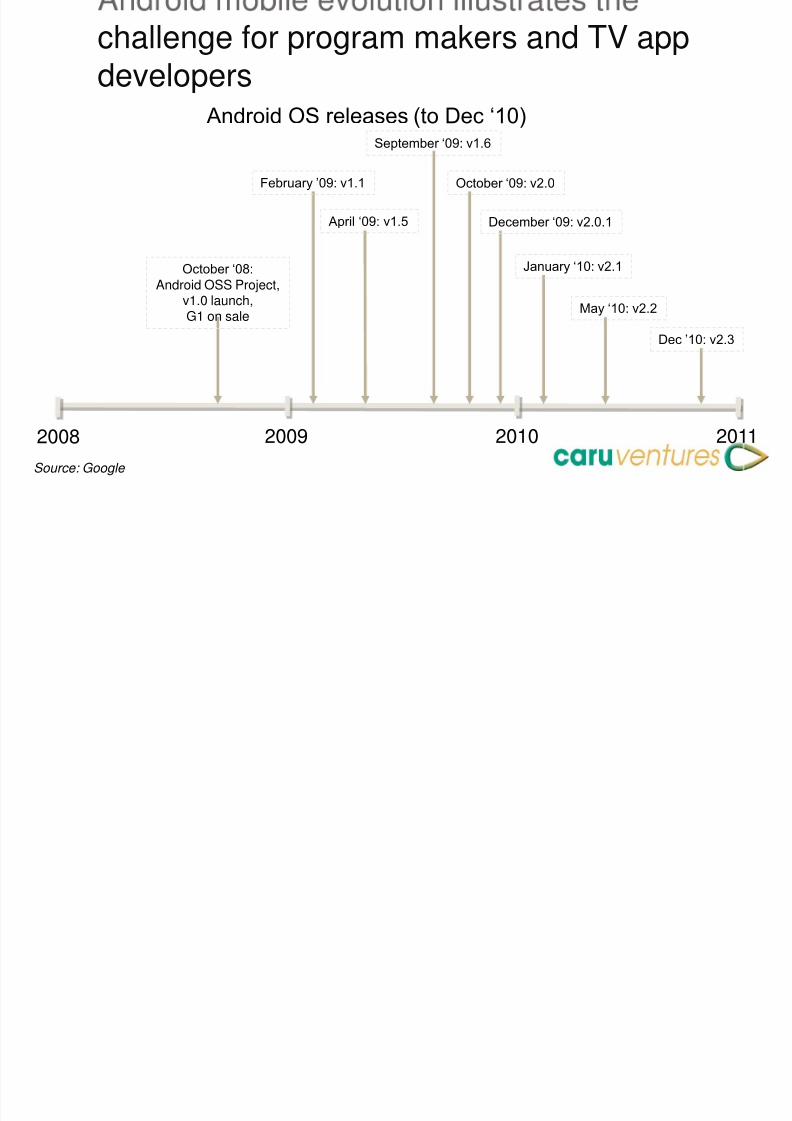

challenge for program makers and TV appdevelopers

2008 2009 2010

October „08:

Android OSS Project,v1.0 launch,G1 on sale

February ‟09: v1.1

April „09: v1.5

September „09: v1.6

October „09: v2.0

December „09: v2.0.1

January „10: v2.1

May „10: v2.2

Android OS releases (to Dec „10)

Dec ‟10

Source: Google

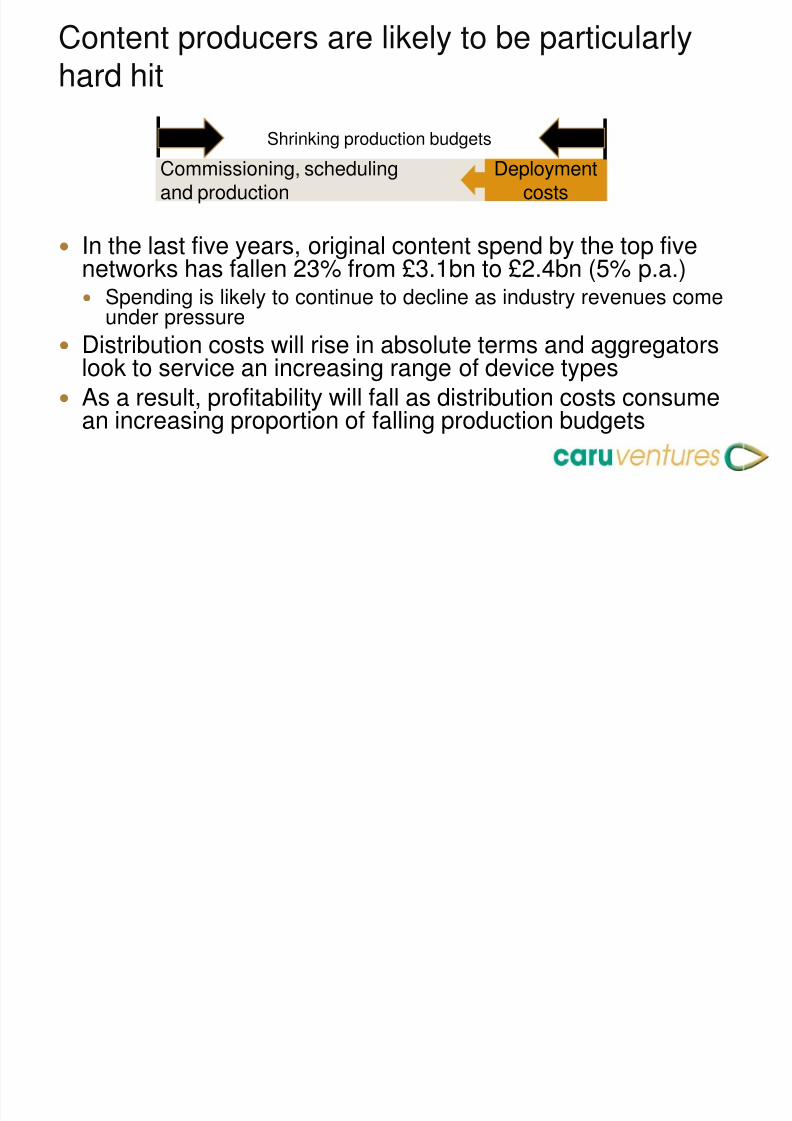

Content producers are likely to be particularly

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 30/36

Content producers are likely to be particularlyhard hit

In the last five years, original content spend by the top fivenetworks has fallen 23% from £3.1bn to £2.4bn (5% p.a.) Spending is likely to continue to decline as industry revenues com

under pressure

Distribution costs will rise in absolute terms and aggregatolook to service an increasing range of device types

As a result, profitability will fall as distribution costs consum

an increasing proportion of falling production budgets

Commissioning, schedulingand production

Deploymentcosts

Shrinking production budgets

4: A range of liability privacy and consumer

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 31/36

4: A range of liability, privacy and consumerprotection issues will arise How will rights owners ensure the integrity of their content when

played out over connected TV? Overlay of third-party content or commercial communications is possible the same time as the television broadcast without the broadcaster's cons

The broadcast playout signal (video and sound) could be altered intransmission or on the device itself without an active decision by the viewor rights owners.

How will platform owners/device manufacturers: Protect against viruses, malware or copyright infringement? Prevent access to applications or sites that link viewers to pirate websites Prevent exploitation of the broadcasters„ programmes and audiences by

parties? Protect children from exposure to inappropriate content?

What procedures will be put in place for removal of those widget

applications that appear to facilitate access to pirated content? Who will gather customer data and how will that data be protecte

It is not clear how existing legal and regulatory

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 32/36

It is not clear how existing legal and regulatoryframeworks apply to connected TV

Rights owners and platform operators are seeking to

ensure protection for their content in this ecosystem Compliance with the EU Audio Visual Media Services

directive and enforcement of contractual obligations byrights-holders

Protection against illegal distribution of content

Protection of the integrity of the “broadcast signal”,including the right to commercialise the screen

Clarity over data ownership and liability should a third papartner or independent vendor breach data protectionregulation.

The ability or otherwise to secure those legalprotections/clarifications will in large part dictate the

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 33/36

5: What future linear TV? Broadcasters have confidently predicted that linear TV as w

know it will be with us for some time The key issue, however, is that control over content

presentation is moving from the broadcaster to the user‟sdevice Platform owners have the power to control how broadcasters' line

and non-linear programmes and services are presented on EPG‟

and in search results The implications of this are:

EPGs will go backwards as well as forwards in time “+1” channels will disappear Channels presented on EPGs will be “virtual” channels where

programs are streamed on demand when selected by the user eit

from the cloud or a local cache Within ten years, we expect that only the PSBs and major (top 3)

commercial channels will still be broadcast real time in the mann

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 34/36

Conclusions [1/2] Connected TV represents a major revolution in the TV

experience for users Integrated TV + catch-up + web Mobile devices working in concert with your TV New content experiences and a new relationship betwee

viewers and producers

Power in the value chain is migrating to devicemanufacturers and platform owners Increasing competition at the device/platform level is

likely to drive costs up and depress revenues forplatform owners and content producers

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 35/36

Conclusions [2/2]

Securing content rights and protecting consumers

this new environment appears challenging Significant uncertainty exists as to how existing lega

and regulatory frameworks can be both applied andenforced in a trans-national connected TV

environment The underlying economics of IP and local storage

suggests linear broadcast TV as we know it willhave a limited role in the future

The storm is coming – be prepared

8/4/2019 An Overview of Developments in Connected TV Final

http://slidepdf.com/reader/full/an-overview-of-developments-in-connected-tv-final 36/36

For advice on Connected TV issues impactingyour business, contact

[email protected] +44 7785 227475

Sign up for my blog atwww.caruventures.com/Caru/Blog/Blog.html

Follow me on Twitter @caruventures

Join my panel discussions on Connected TV themes at:The Open Mobile Summit, London, 8th-9th June 2011

www.openmobilesummit.com International Broadcasting Conference, Amsterdam, 8th – 13th Septembe

www.ibc.org