An NSF I/UCRC Could there be a new era with much lower utility bills? Tim Mount Dyson School of...

26

An NSF I/UCRC Could there be a new era with much lower utility bills? Tim Mount Dyson School of Applied Economics and Management Cornell University esented at the NY Association of Energy Economics 4/26/12

-

Upload

agatha-copeland -

Category

Documents

-

view

214 -

download

0

Transcript of An NSF I/UCRC Could there be a new era with much lower utility bills? Tim Mount Dyson School of...

An NSF I/UCRC

Could there be a new era with much lower utility bills?

Tim MountDyson School of Applied Economics and Management

Cornell University

Presented at the NY Association of Energy Economics 4/26/12

An NSF I/UCRC

Research on the Smart Grid requires collaboration across disciplines

Power System Engineering Research Center (PSERC) Researchers at CornellEngineers Economists

Lindsay Anderson Wooyoung Jeon**Hsiao-Dong Chiang Alberto Lamadrid**Andrew Hunter Jung Youn Mo*Bob Thomas Surin Maneevitjit**Lang Tong Tim MountMax Zhang Dick SchulerRay Zimmerman Bill Schulze+ Hao Lu*Alejandro Dominguez-Garcia + University of Illinois Dan Shawhan, RPICarlos Murillo-Sanchez, * Graduate Student,

Universidad Nacional de Colombia ** Supported by PSERC

2

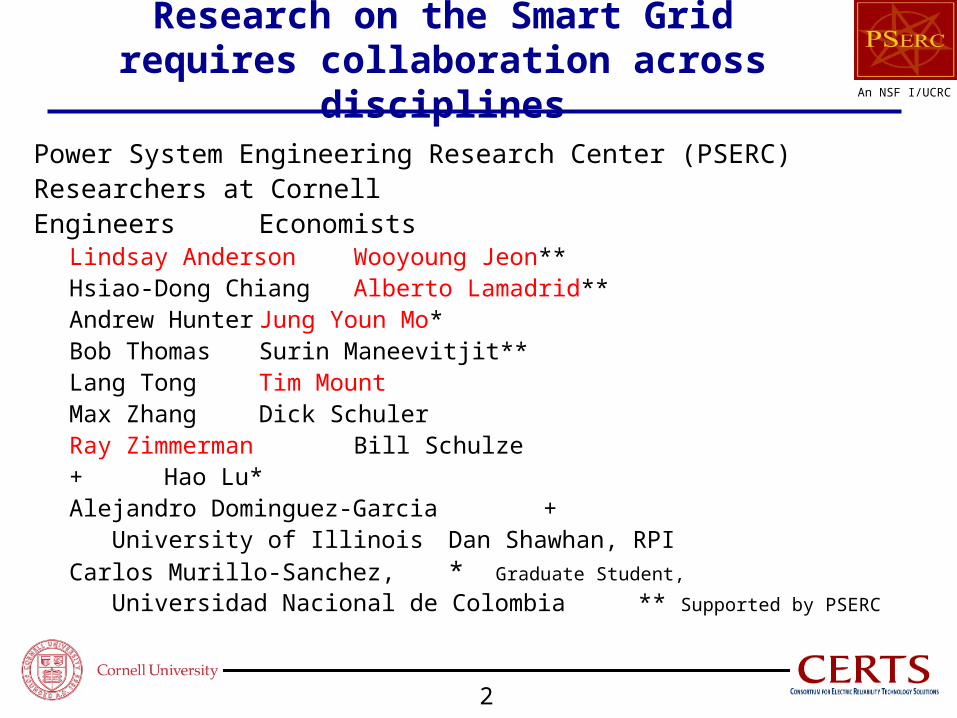

An NSF I/UCRCWhat research do we do at Cornell?

Reduced Network for New York State and New England

3

An NSF I/UCRC

How can high penetrations of wind generation be integrated into the grid?

12

34

5

67

New England

New York State

4

An NSF I/UCRC

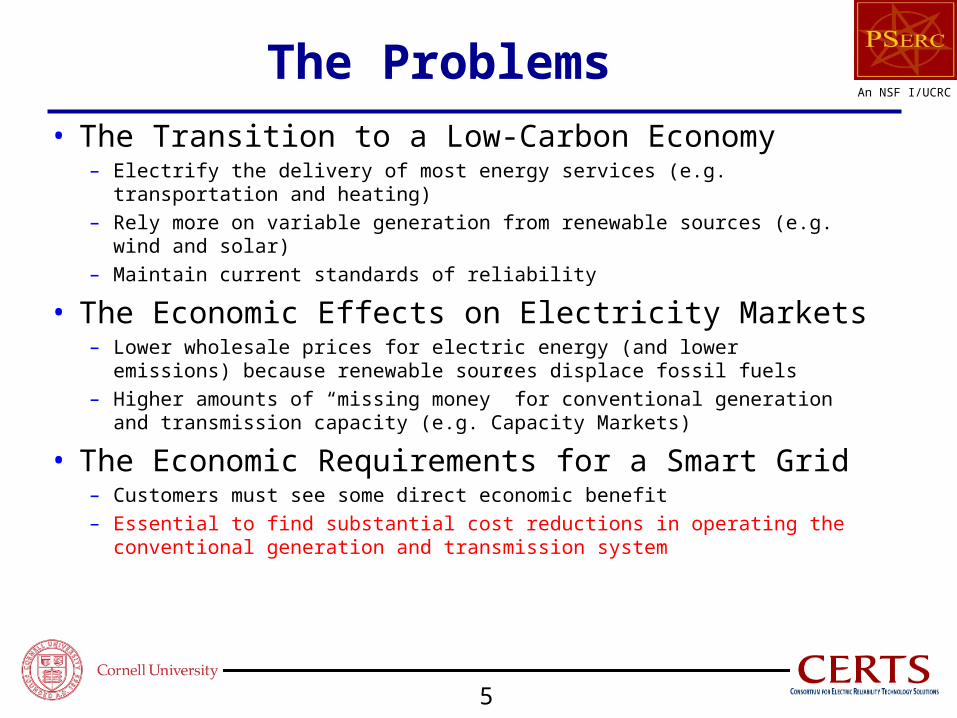

The Problems

• The Transition to a Low-Carbon Economy– Electrify the delivery of most energy services (e.g. transportation and

heating)– Rely more on variable generation from renewable sources (e.g. wind and

solar)– Maintain current standards of reliability

• The Economic Effects on Electricity Markets– Lower wholesale prices for electric energy (and lower emissions) because

renewable sources displace fossil fuels– Higher amounts of “missing money” for conventional generation and

transmission capacity (e.g. Capacity Markets)

• The Economic Requirements for a Smart Grid– Customers must see some direct economic benefit– Essential to find substantial cost reductions in operating the conventional

generation and transmission system

5

An NSF I/UCRC

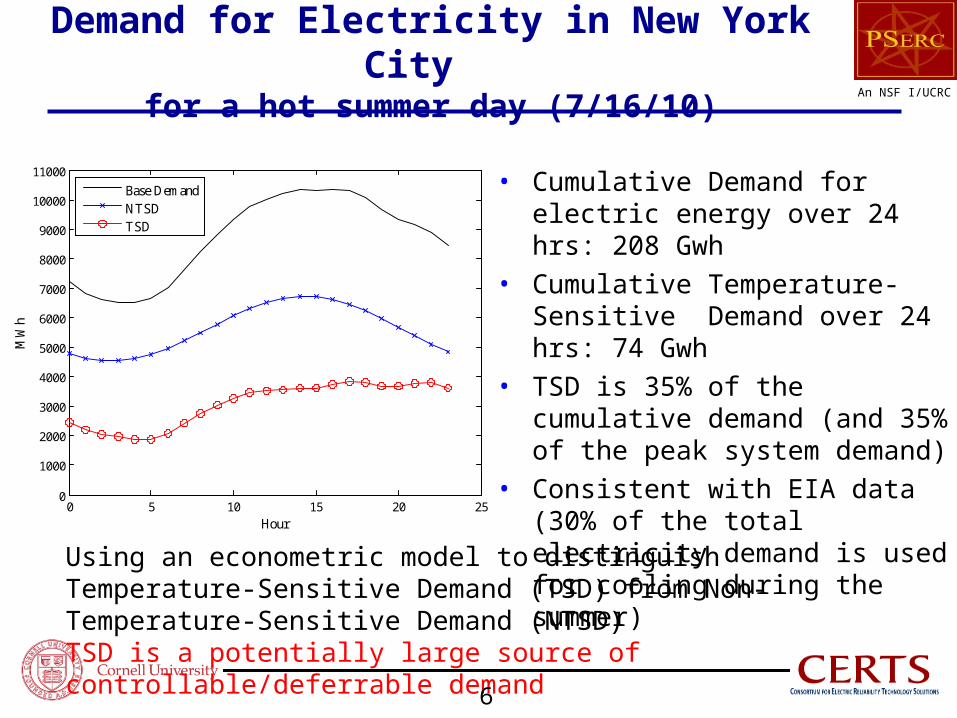

Demand for Electricity in New York City for a hot summer day (7/16/10)

• Cumulative Demand for electric energy over 24 hrs: 208 Gwh

• Cumulative Temperature-Sensitive Demand over 24 hrs: 74 Gwh

• TSD is 35% of the cumulative demand (and 35% of the peak system demand)

• Consistent with EIA data (30% of the total electricity demand is used for cooling during the summer)

Using an econometric model to distinguish Temperature-Sensitive Demand (TSD) from Non-Temperature-Sensitive Demand (NTSD)TSD is a potentially large source of controllable/deferrable demand

0 5 10 15 20 250

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

11000

Hour

MW

h

Base DemandNTSDTSD

6

An NSF I/UCRC

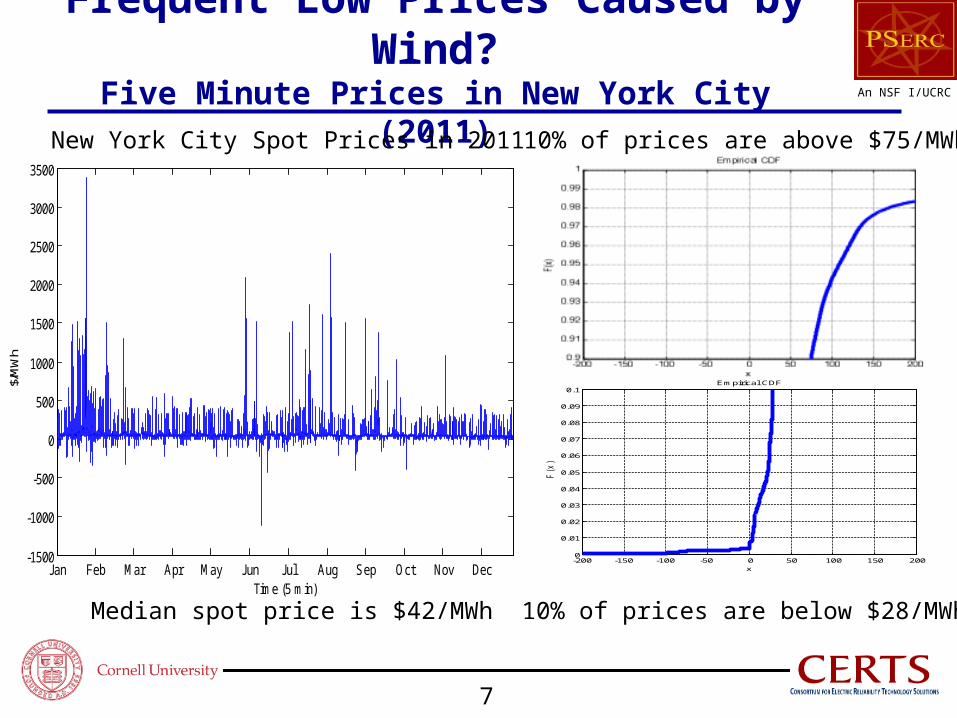

Frequent Low Prices Caused by Wind?Five Minute Prices in New York City (2011)

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec-1500

-1000

-500

0

500

1000

1500

2000

2500

3000

3500

$/M

Wh

Time (5 min)

7

10% of prices are below $28/MWhMedian spot price is $42/MWh

10% of prices are above $75/MWh

-200 -150 -100 -50 0 50 100 150 2000

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.09

0.1

x

F(x

)

Empirical CDF

New York City Spot Prices in 2011

An NSF I/UCRC

Model I: To illustrate the potential system benefits of

controllable/deferrable demand (with no networks constraints)

8

Specifications for the Analysis

• 10 GWh of customer storage is added to the system• 5 GWh from electric vehicles (PHEV Volt: 44% penetration)• 5 GWh from thermal storage (Ice batteries: 6% penetration)

• A System Operator controls all storage to minimize the total system costs of energy and ramping• The ramping costs are caused by moving the dispatch points of

conventional generators (in response to the daily demand profile and the inherent variability of wind generation)

• The System Operator determines the market prices for both Energy and Ramping

• All customers are assumed to have identical patterns of demand for electrical energy services

9

An NSF I/UCRC

System Level Results

10

Total Conventional Generation

- Net Load is defined as Base Load – Wind- Wind data are from NREL and wind capacity is assumed to be 2GW- Wind generation accounts for 12% of total daily demand

0 5 10 15 20 255000

6000

7000

8000

9000

10000

11000Total Conventional Generation

MW

h

Hour

Base LoadNet LoadOptimum

11

System Price for Energy

0 5 10 15 20 250

20

40

60

80

100

120

140

160System Price for Energy

$/M

Wh

Hour

Base LoadNet LoadOptimum

12

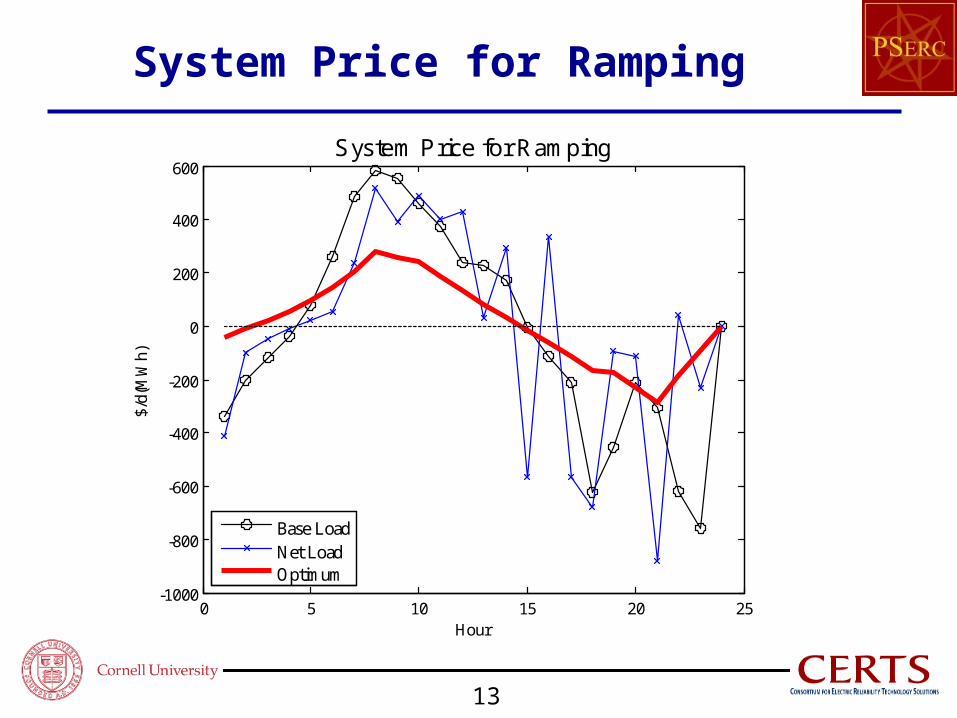

System Price for Ramping

0 5 10 15 20 25-1000

-800

-600

-400

-200

0

200

400

600System Price for Ramping

$/d(

MW

h)

Hour

Base LoadNet LoadOptimum

13

Optimum Energy Purchased and Energy Consumed

0 5 10 15 20 257000

7500

8000

8500

9000

9500

10000

10500

11000Actual Energy Purchase

Ene

rgy

Pur

chas

e ($

/MW

h)

Hour

Energy ConsumedEnergy Purchased

14

The energy services delivered to customers do not change

Composition of the Cooling DemandDirect (AC) v Stored (THERMAL)

0 5 10 15 20 25-200

0

200

400

600

800

1000

Hour

Coo

ling

Dem

and

(MW

h)

Load CoolingTHERMALAC

- Controllable Cooling Demand is proportional to TSD (6.2%)- AC provides ramping services during the system peak hours

15

Total System Costs and Total Payments by All Customers

Base Load(no Wind)

Net Load(with Wind)

Optimum Load

Payment by Customer

Energy Cost ($1000) 24,477 16,236 16,915 19,069 Ramping Cost($1000) 3,204 3,855 688 420 Total Operating Cost($1000) 27,681 20,091 17,603 19,489 FEIS(MWh)* 0 0 807 - Value of FEIS($1000)* 0 0 97 97 Total Cost of Serving Load($1000) 27,681 20,091 17,506 19,392 Max System Load(MW) 10,529 9,879 9,059 - Capacity Cost($1000)** 18,530 17,386 15,944 17,088 TOTAL SYSTEM COST($1000) 46,211 37,477 33,451 36,481 Total Saving in Gasoline($1000)*** 0 0 -2,720 -2,720 TOTAL COST TO CUSTOMERS 46,211 37,477 30,731 33,761 % Cost Reduction from Base Load - 18.9% 33.5% 26.9%

* Final Energy In Storage (FEIS), Valued at $120/MWh (Average Peak Price).** Annual Capital Cost for Peaker $88k/MW/year allocated to 100 peak hours. Specify 2 peak hours for this hot day.*** Each vehicle drives 27.2 Miles at 20 Miles/Gal at $4/Gal.

16

Composition of the Payments Made to the Regional Transmission Operator

- Positive (Negative) payments indicate Paying (Being Paid) for a service.- CD, Conventional Demand and DD, Deferrable Demand- WG, Wind Generation and CG, Conventional Generation- The SYSTEM COST of ramping is caused by ramping CG- WG accounts for 11% of Energy Supply and 45% of Ramping Demand- CD accounts for 2% of Energy Demand and 71% of Ramping Supply

Ramping Payment ($1000)

Energy Payment ($1000)

Total Payment ($1000)

Total Energy(MWh)

AveragePayment($/MWh)

1) CD 2120 18920 21,041 214911 982) WG 1735 -2154 -419 27070 -153) CG -1125 -17236 -18,361 196822 -934) DD -2730 470 -2,261 12296 -184Buyers (1)+(2) = 3,855 (1)+(4) = 19,390

Suppliers (3)+(4) = -3,855 (2)+(3) = -19,390

17

An NSF I/UCRC

Results for Different Types of Customer

18

Consider Four Types of Customer

• Assume that there are one million customers with identical initial daily patterns of demand– Type 1 No storage capabilities

– Type 2 Add THERMAL storage

– Type 3 Buy a PHEV Volt

– Type 4 Both THERMAL and PHEV

• All customers pay for:– ENERGY using real-time prices (PHEV can be paid)

– CAPACITY at the peak system load

– RAMPING using real-time prices (can be paid for reducing the system ramp)

19

Energy Purchased by Different Types of Customer

THERMAL customers do the heavy lifting0 5 10 15 20 25

5

6

7

8

9

10

11

12

13

14

15Energy Demand by Different Types of Customers

KW

h

Hour

No StorageTHERMAL OnlyPHEV OnlyTHERMAL and PHEVAverage

20

Total Payments Per Customer ($/day)

Base Load w no Wind

Base + Wind w no

Storage

Average Optimum w Storage

With no storage

With PHEV & Thermal

Storage

Energy 25 18 19 20 18

Ramping 3 2 1 1 -1

Capacity 18 18 17 19 14

Gasoline 0 0 -3 0 -5

TOTAL 46 38 34 40 26

Changefrom Base

- -17% -26% -13% -43%

The main source of savings for customers with storage (deferrable demand) is from lower payments for capacity (incentive compatible demand charges) and lower gasoline purchases

Total Payments Per Customer

Base Load Net Load TYPE 1No Storage

TYPE 2THERMAL

only

TYPE 3PHEV only

TYPE 4THERMAL

& PHEVAverage

Energy Payment ($) 24.48 18.03 18.92 18.60 19.38 19.13 19.07

Ramping Payment ($) 3.20 2.12 1.15 -0.40 0.46 -1.05 0.42

Total Payment ($) 27.68 20.15 20.07 18.20 19.84 18.08 19.49

Value of FEIS ($) 0 0 0 0.25 0.07 0.32 0.10

Total Payment of Serving Load ($) 27.68 20.15 20.07 17.96 19.77 17.76 19.39

KW at System Peak (KW) 10.53 10.53 10.53 8.56 9.88 8.00 9.71

Capacity Payment ($) 18.53 18.53 18.53 15.06 17.38 14.09 17.09

Total SYSTEM Payment ($) 46.21 38.68 38.60 33.02 37.15 31.85 36.48

Saving in Gasoline ($) 0 0 0 0 5.44 5.44 2.72

AVERAGE PAYMENT ($) 46.21 38.68 38.60 33.02 31.71 26.41 33.76

% Payment Reduction from Base Load 16.3% 16.5% 28.5% 31.4% 42.9% 26.9%

Optimum ENERGY payments are similar for all types of customer.Optimum CAPACITY and RAMPING payments are lower with storage.Customers with both THERMAL and PHEV are the big winners.

22

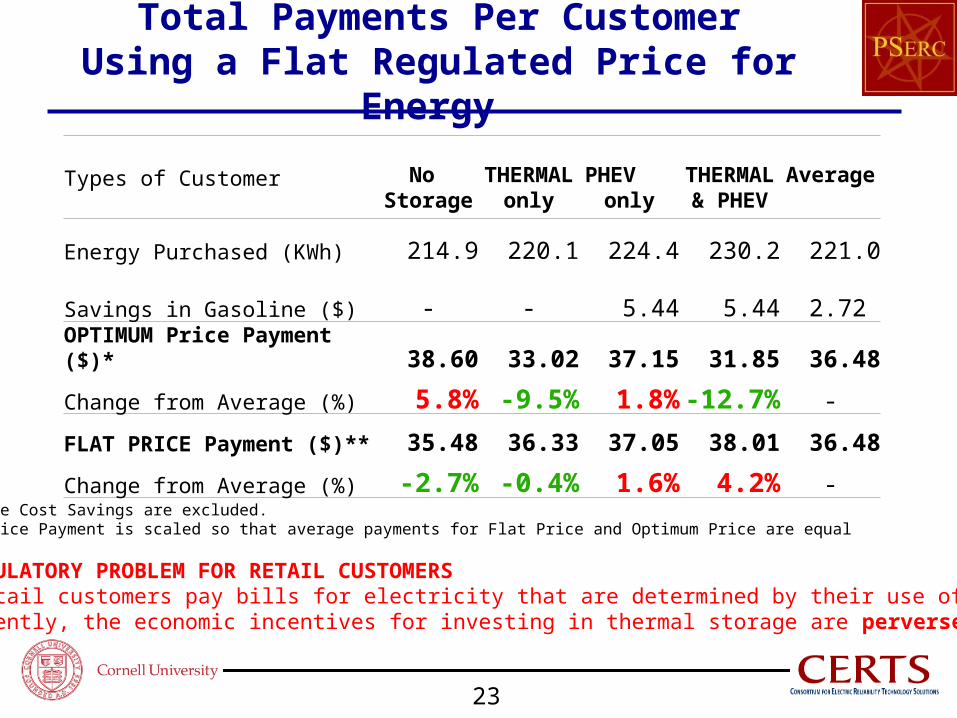

Total Payments Per CustomerUsing a Flat Regulated Price for Energy

Types of Customer No Storage

THERMAL only

PHEV only

THERMAL & PHEV

Average

Energy Purchased (KWh) 214.9 220.1 224.4 230.2 221.0

Savings in Gasoline ($) - - 5.44 5.44 2.72

OPTIMUM Price Payment ($)* 38.60 33.02 37.15 31.85 36.48

Change from Average (%) 5.8% -9.5% 1.8% -12.7% -

FLAT PRICE Payment ($)** 35.48 36.33 37.05 38.01 36.48

Change from Average (%) -2.7% -0.4% 1.6% 4.2% -

* Gasoline Cost Savings are excluded.** Flat Price Payment is scaled so that average payments for Flat Price and Optimum Price are equal

THE REGULATORY PROBLEM FOR RETAIL CUSTOMERSMost retail customers pay bills for electricity that are determined by their use of energy.Consequently, the economic incentives for investing in thermal storage are perverse.

23

An NSF I/UCRC

Conclusions

24

CONCLUSIONS

• High penetrations of renewable generation lower the wholesale price of energy BUT increase the ramping and capacity costs (“missing money”) for the conventional generators

• Wholesale customers and aggregators who have deferrable demand should get substantial economic benefits by:– Purchasing more energy at less expensive off-peak prices

– Reducing their demand (capacity) during expensive peak-load periods

– Selling ancillary services (ramping) to mitigate wind variability

• All market participants should pay for the services they use and get paid for the services they provide

• Most existing retail rate structures do not provide the correct economic incentives for deferrable demand

25

Issues for Future Research(Issues for regulators are RED)

• The economic benefits of deferrable demand for the grid are not adequately represented by the current rates charged to customers

– Customers (aggregators) should pay real-time prices for energy– Correct measurement and payments needed for each customer’s peak demand– Customers should pay/get paid for using/supplying ramping services

• The inherent variability of generation from renewable sources and the difficulty of forecasting these sources accurately are incompatible with the current structure of day-ahead markets and unit commitment

– Need a rolling horizon for optimizing real-time dispatch that uses updated forecasts of potential renewable generation and system conditions (e.g. like Australia)

– Customers (aggregators) should get updated (non-binding) projections of future prices at least 24 hours ahead to manage storage efficiently (e.g. like Australia)

• The structures/capabilities of existing distribution networks are major weak links in the electric delivery system for a future smart grid

– Need new scheduling algorithms for coordinating multiple stochastic sinks of deferrable demand to improve grid efficiency and for accommodating multiple sources of variable generation from renewable sources of energy

26