AN INTEGRATED ENERGY EQUIPMENT & SERVICES HUB · KS ENERGY SERVICES LIMITED Annual Report 2009 AN...

141

AN INTEGRATED ENERGY EQUIPMENT & SERVICES HUB annual report 2009

Transcript of AN INTEGRATED ENERGY EQUIPMENT & SERVICES HUB · KS ENERGY SERVICES LIMITED Annual Report 2009 AN...

KS

EN

ER

GY

SE

RV

ICE

S L

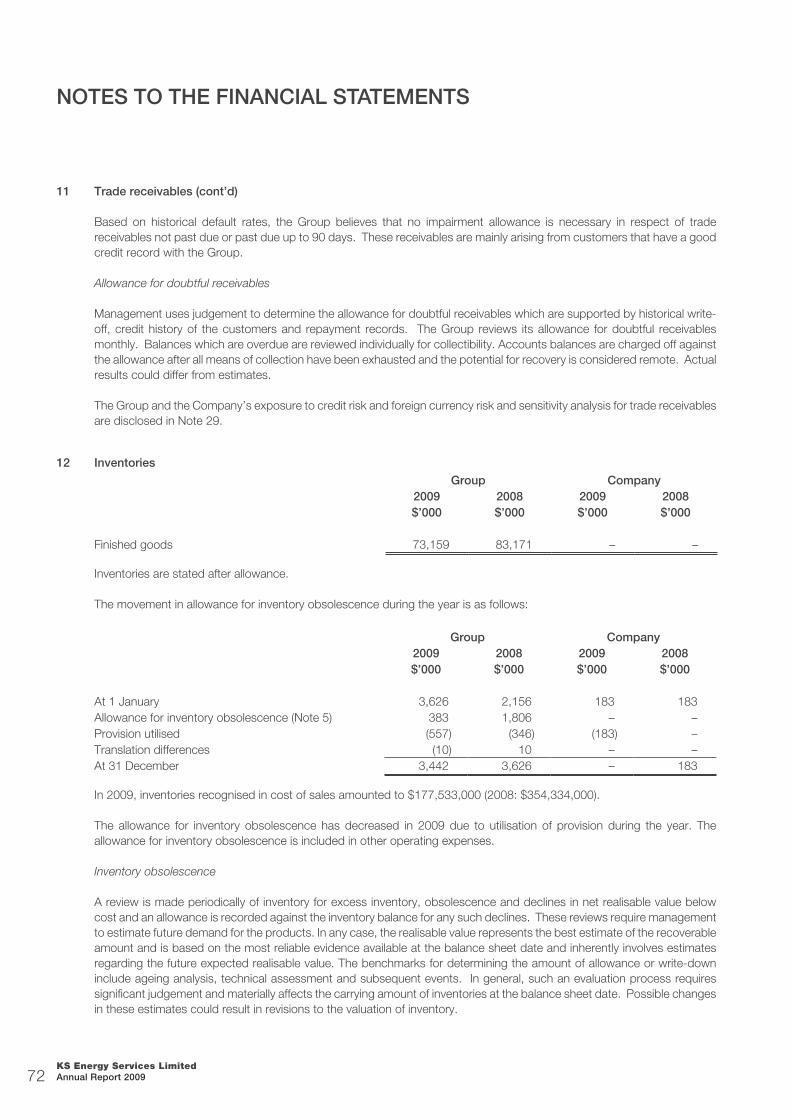

IMIT

ED

Annual R

epo

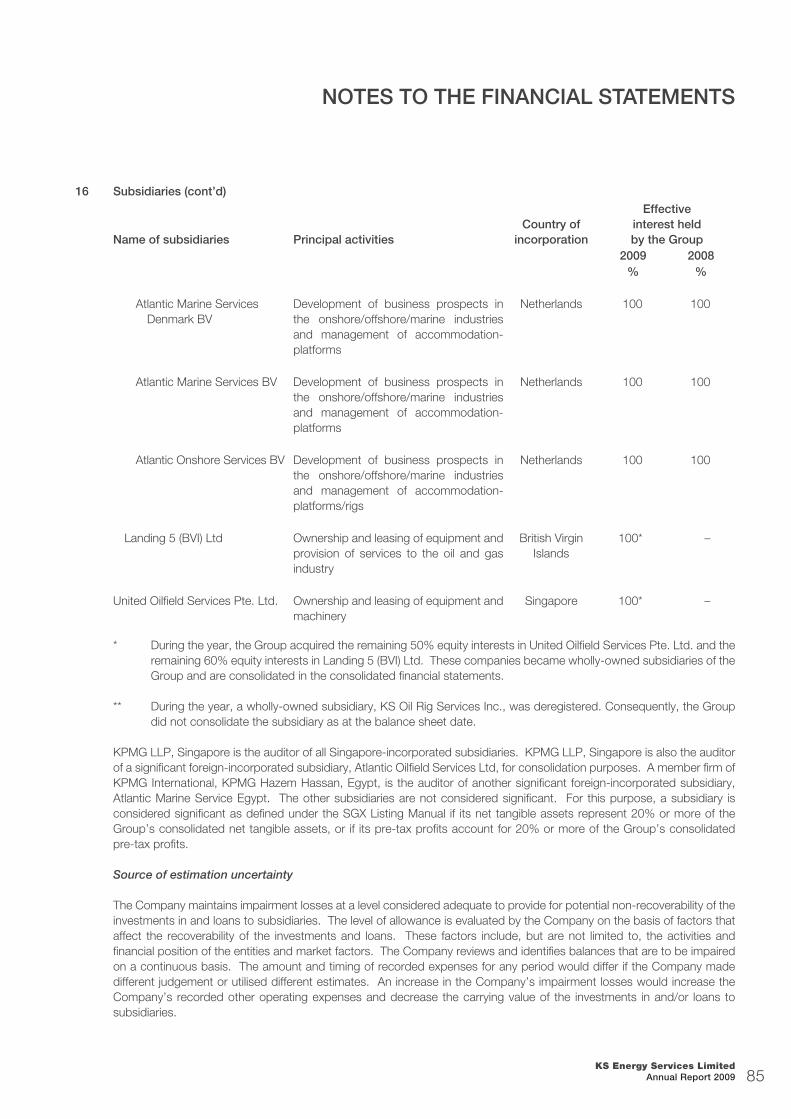

rt 2009

AN INTEGRATED ENERGY EQUIPMENT & SERVICES HUB

Design 5

AN INTEGRATED ENERGY EQUIPMENT & SERVICES HUBAN INTEGRATED ENERGY EQUIPMENT & SERVICES HUB

annual report

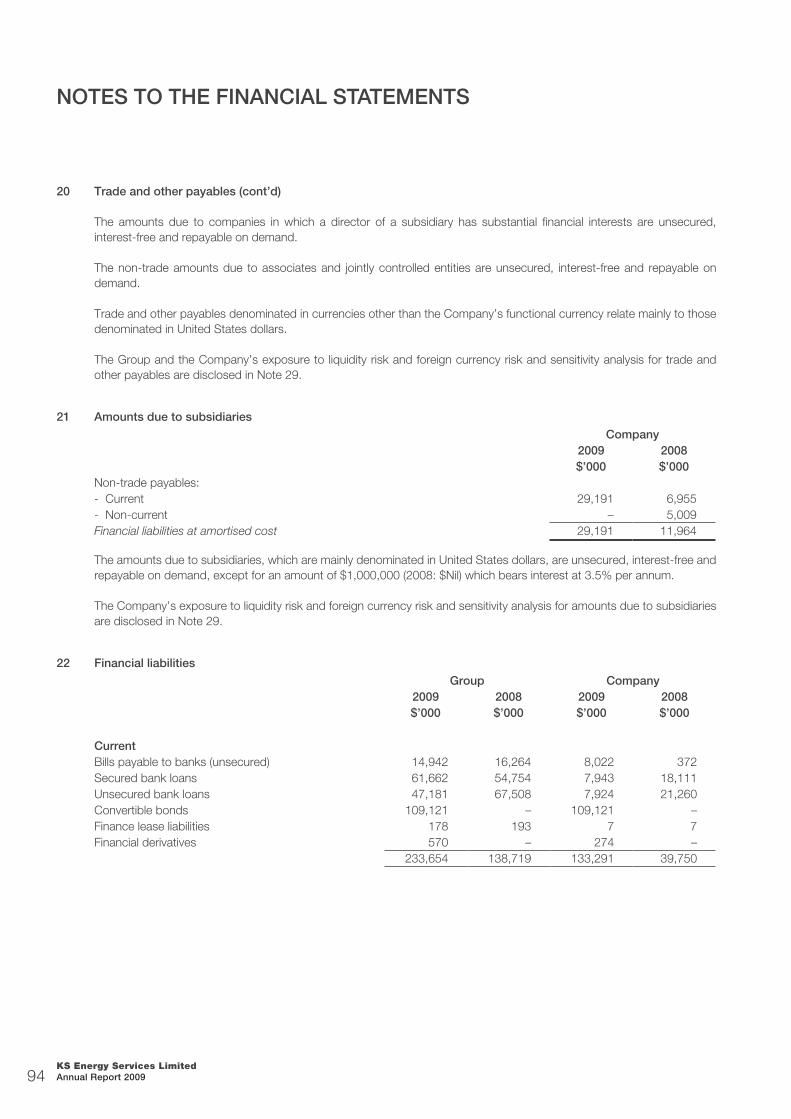

2009

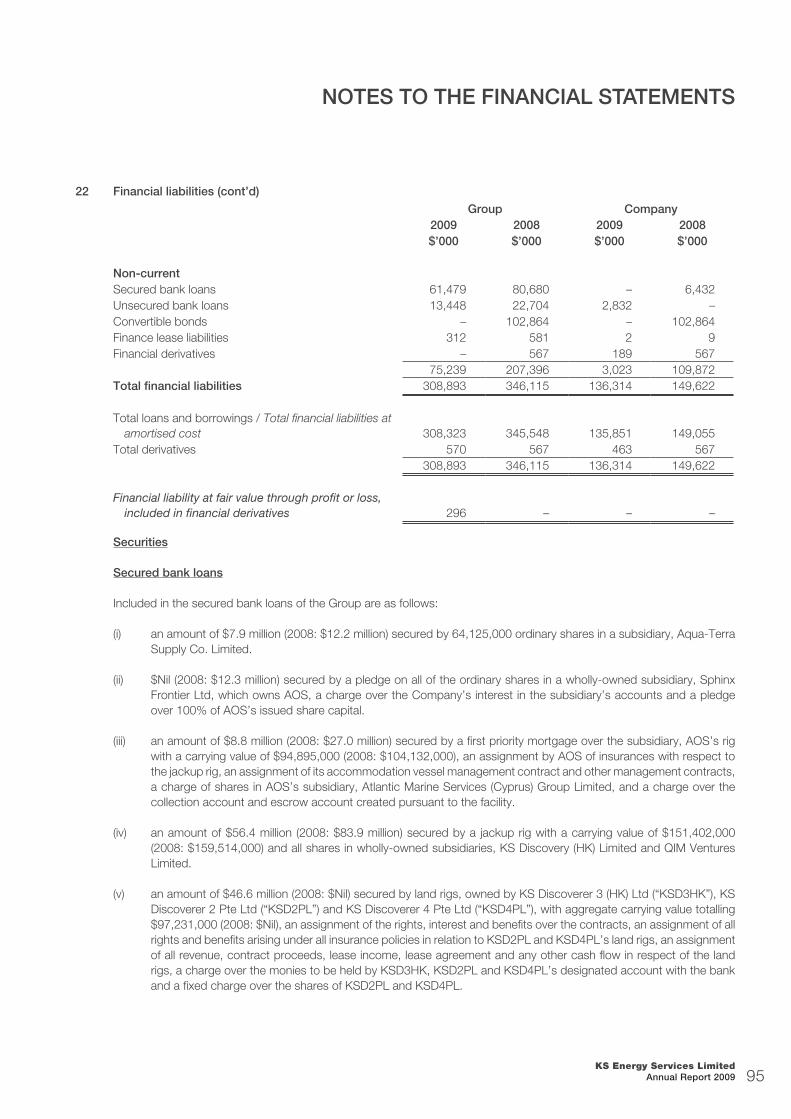

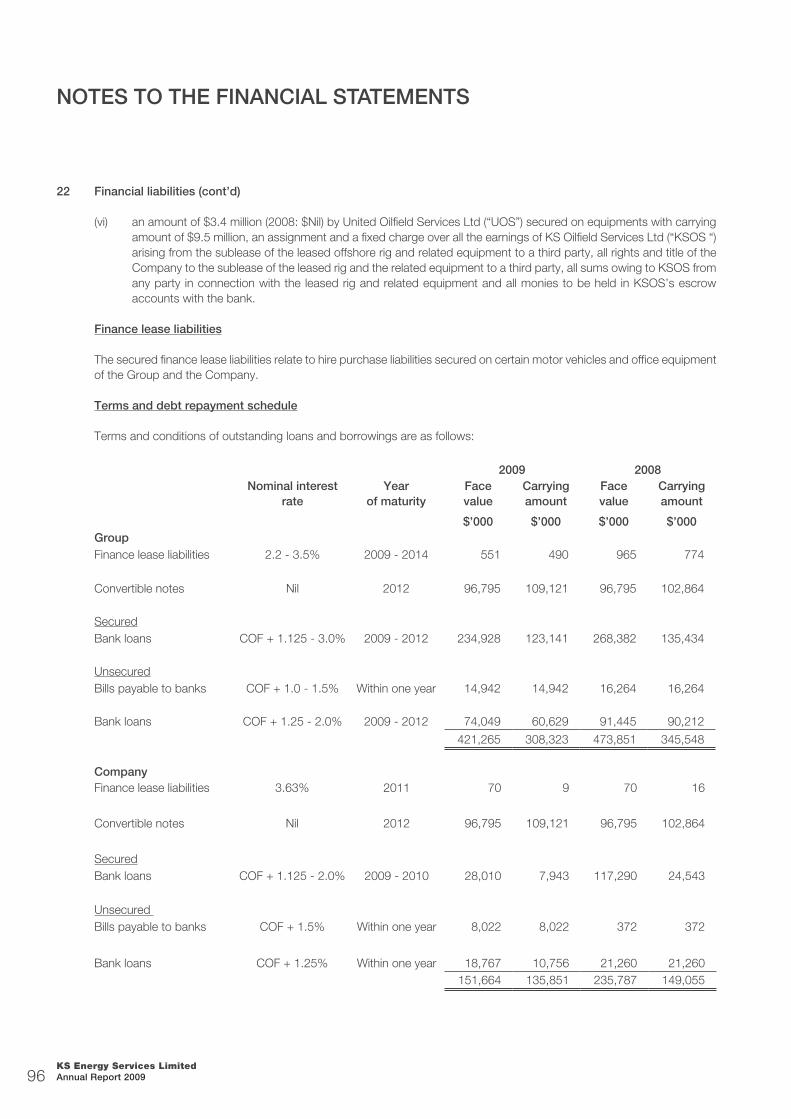

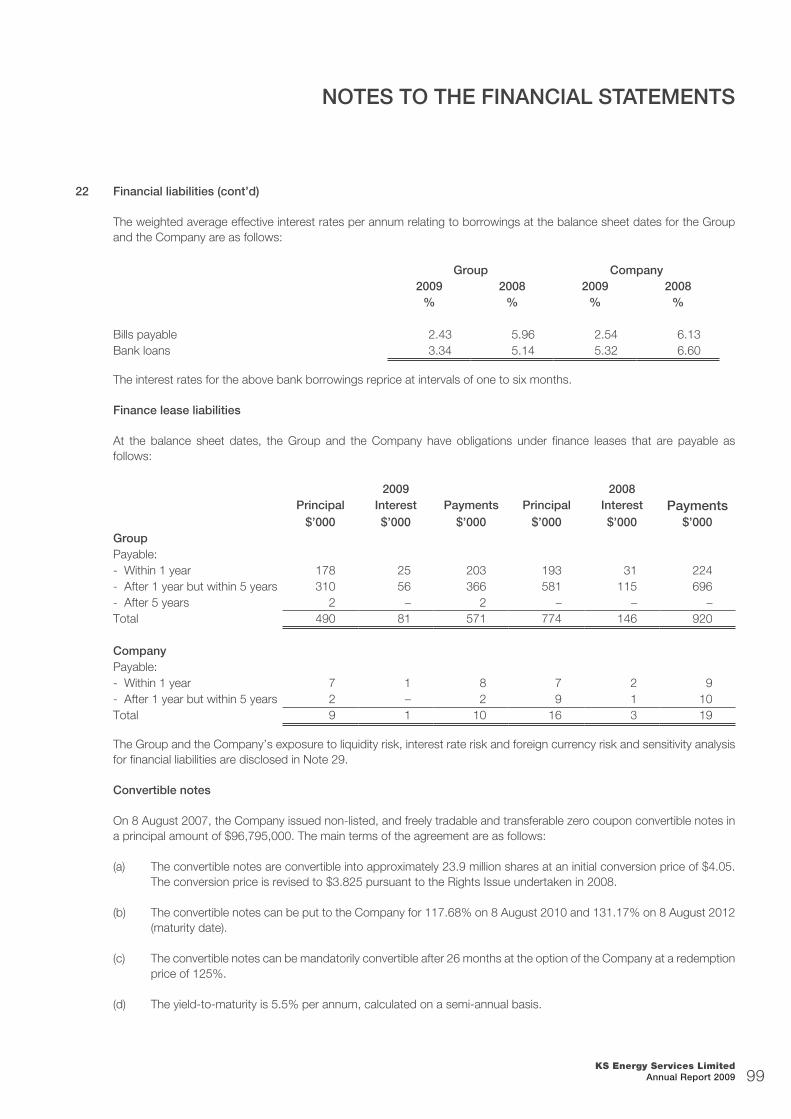

Contents

About KS Energy Services Limited 1

Chairman’s Message to Shareholders 2

Operation & Financial Review 6

Financial Highlights 12

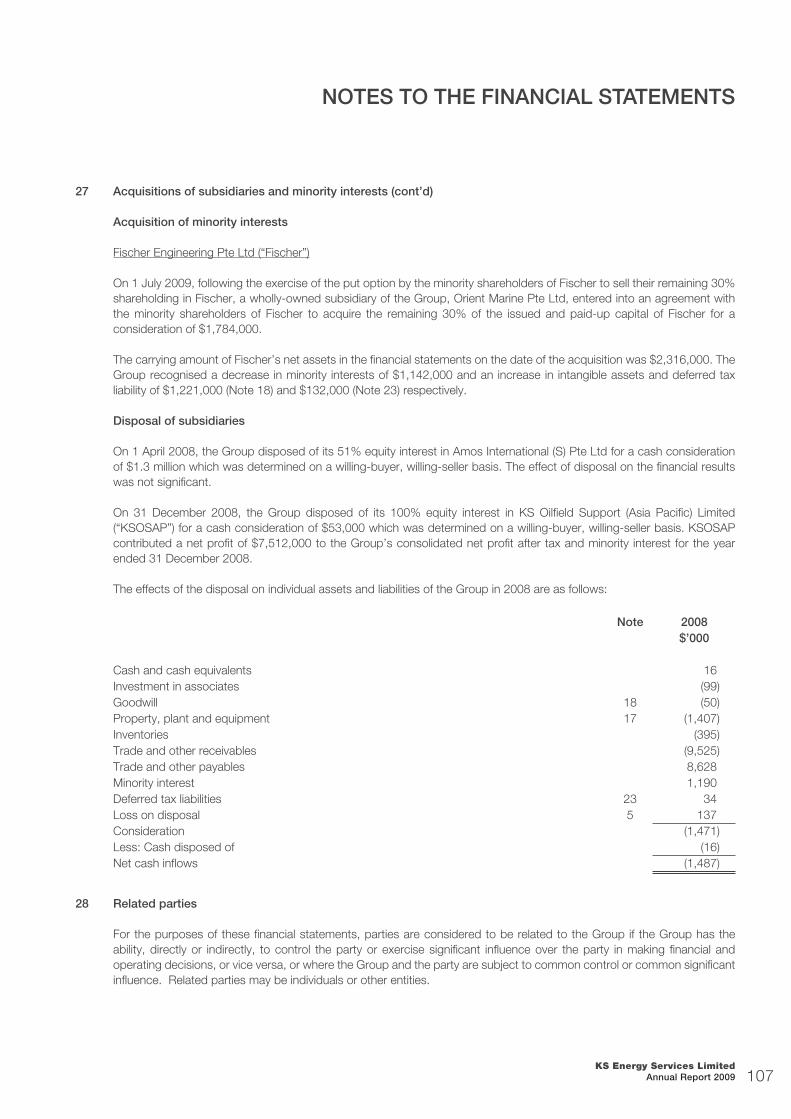

Corporate Data 14

Board of Directors 16

Board of Advisors 18

Management Board 19

Regional Directors 21

Group Structure 22

ABout Ks eneRgY seRVices liMiteD

A Globally Accredited and Integrated Oil & Gas Services Provider

KS Energy Services Limited (“KS Energy”) is a leading one-stop energy services provider to the global oil and gas (“O&G”), marine and petrochemical industries. The shares of KS Energy are traded on the main board of the Singapore Exchange.

The core activities of KS Energy are in distribution and capital equipment charter and services. For its distribution business, KS Energy ranks as one of the leading distributors of oil and gas equipment, spare parts, consumables and industrial products in the region. Together with Aqua-Terra Supply Co., Limited (“Aqua-Terra” or “ATS”) and SSH Corporation Ltd (“SSH”), the KS Energy Group distributes more than 60,000 oil and gas related products comprising more than 300 international brands of products.

Following the acquisition of Atlantic Oilfi eld Services Ltd (“AOS”) in May 2007, KS Energy now has the capability to supply, as well as operate capital equipment, including onshore and offshore rigs. Integrating the twin capabilities of AOS and KS Energy, the Group now has the ability to provide a full suite of services directly to the oil and gas companies, tendering for high value and high margin projects. Headquartered in Singapore, it has a geographical reach spanning South East Asia, China, the Middle East, the North Sea, Europe and the USA.

For more information, please visit our website: www.ksenergy.com.sg

KS Energy Services Limited Annual Report 2009 1

cHAiRMAn’s MessAge to sHAReHolDeRs

“We will be looking to expand our operations in Indonesia, Australia, India and Africa. In China, where we currently have more than 16 offi ces, we will be looking to consolidate and strengthen our operations and participate in more infrastructure and energy projects.”

KS Energy Services Limited Annual Report 20092

“Our total borrowings were lower this year and our gearing improved from 0.76 times to 0.58 times at the close of FY2009.”

Dear Shareholders,

The global uncertainties in 2009 continue to challenge the oil and gas industry. Lower energy demand coupled with reduced manufacturing activities led to lower oil prices. This in turn affected the businesses in the entire oil and gas supply chain.

However, this gave rise to many opportunities as businesses look for partnerships, strategic alliances and capital assets divestments. At KS Energy, our team put in extra efforts on both the operational and fi nancing fronts. The year saw our entry into clean energy with the deployment of our Titan 2 lift boat for the installation of windmills in Europe. While the tenure of the project was shortened by the inclement weather, it gave us invaluable experience and insight into the rapidly growing clean energy industry.

The performance of our drilling and distribution businesses was affected by the economic uncertainties over the last two years. Nonetheless, the situation has allowed us to improve our operations although compared to the previous fi nancial year, FY2009 ended with lower revenue and net profi t after tax.

The top view of one of KS Energy’s rig

Anchor chains one of the products distributed by the Group

KS Energy Services Limited Annual Report 2009 3

In anticipation of the financial challenges, we have successfully completed our first warrants issue which brought net proceeds of $16.4 million into the Group. The money had been used to fund our working capital needs. Our total borrowings were lower this year and our gearing improved from 0.76 times to 0.58 times at the close of FY2009.

Another highlight of the year was our proposal to consolidate our distribution business with that of our subsidiary – Aqua-Terra Supply Co Limited (“ATS”) and our associate company – SSH Corporation Ltd (“SSH”), subject to approvals from our shareholders and the relevant authorities. Once completed, our distribution businesses will be consolidated under our new subsidiary KS Distribution Pte Ltd (“KS Distribution”). This is a joint-venture company with Actis, a leading private equity investor in emerging markets. This new entity will start off with more than 60,000 line items representing 300 globally accredited brands and a reach across nine countries, a base from which it will continue to grow and expand.

For the year 2010, we expect the world economy to stabilise and demand for energy to increase. We will continue to consolidate our oil and gas operations and look for strategic alliances and acquisitions that can complement and add value to our businesses. Concurrently, we will invest in our people and strengthen our competitive capabilities to further grow our distribution business. We will be looking to expand our operations in Indonesia, Australia, India and Africa. In China, where we currently have more than 16 offices, we will be looking to consolidate and strengthen our operations and participate in more infrastructure and energy projects.

On behalf of all my fellow directors and colleagues, I thank you for the trust and confidence that you had given to us as we face the challenges of 2009. We appreciate your continuing support for the year 2010 and will do our best to grow KS Energy.

Yours sincerely, Kris Taenar Wiluan Executive Chairman and Chief Executive Officer

KS Energy Services Limited Annual Report 20094

“Another highlight of the year was our proposal to consolidate our distribution business with that of our subsidiary – Aqua-Terra Supply Co Limited (“ATS”) and our associate company – SSH Corporation Ltd (“SSH”). Our distribution businesses will be consolidated under our new subsidiary- KS Distribution Pte Ltd. (“KS Distribution”) ”

A Shackle - Product distributed by Aqua-Terra

Pipes - Product distributed by SSH

KS Energy Services Limited Annual Report 2009 5

OVERVIEW

FY2009 witnessed a year of volatile oil prices and sluggish global economy. Feeling the impact of the weak market demand, both our “Distribution” and “Drilling and Capital Equipment Charter” businesses reported weaker performance. As a result, KS Energy closed the year on lower revenue and profi tability.

Another challenge this year was the credit crunch as fi nancial institutions globally contracted their loan portfolios. To counter these effects, the Group successfully completed its fi rst warrant issue in August 2009, raising approximately $16.4 million. The money had been used to fund our working capital needs. Our total borrowings were lower this year and our gearing improved from 0.76 times to 0.58 times at the close of FY 2009.

Our integration efforts took another step forward as we continue with our efforts to streamline our “Distribution” business and re-organise our Drilling and Capital Equipment Charter business. The current slow-down in the global economic landscape has given us the opportunity to speed up our business consolidation and in the process, bring us closer to our vision to transform KS Energy into an integrated energy services hub.

“The current slow-down in the global economic landscape has given us the opportunity to speed up our business consolidation and in the process, bring us closer to our vision to transform KS Energy into an integrated energy services hub.”

opeRAtion & FinAnciAl ReVieW

KS Energy Services Limited Annual Report 20096

Subsequently, on 8 December 2009, we announced our proposal to consolidate our distribution businesses with that of our subsidiary – Aqua-Terra Supply Co Limited and our associate company - SSH Corporation Ltd. When approved, all our distribution businesses will be contained under our newly incorporated subsidiary – KS Distribution Pte Ltd, a joint-venture company owned by KS Energy and Actis – a leading private equity investor in emerging markets.

For our drilling and capital equipment charter business, the contracts previously secured commenced operation this year. The challenge in this business segment was the declining day rates. Contracts that are due for renewal were re-contracted at lower rates. We foresee that this situation will persist so long as uncertainty overhangs the recovery of the global economy.

FINANCIAL REVIEWRevenue

The Group’s revenue for the fi nancial year 2009 (“FY09”) amounted to $489.8 million compared to $611.0 million reported for the previous year (“FY08”), representing a decrease of 19.8%. By business segment, revenue from the Distribution business was lower by 33.3%, declining from $361.8 million in FY08 to $241.5 million in FY09. The revenue for the Drilling and Capital Equipment business remained relatively stable compared to the previous fi nancial year.

Other operating income was lower in FY09 due to the reduction in the sale of investments during the year compared to FY08. As a result, other operating income was lower by 38.5%, decreasing from $16.1 million to $9.9 million in FY09. Included in this fi gure are the gain of $2.0 million from the divestment of an associate and $4.5 million from the sale of available-for-sale equity securities.

KS Energy Services Limited Annual Report 2009 7

Expenses Distribution costs totalled $21.1 million in FY09, representing a decrease of 15.3%, compared to $24.9 million incurred in FY08. This is in line with the lower level of activities in the Group’s Distribution business.

Administrative expenses reported a drop of 24.5%, decreasing from $37.1 million to $28.0 million due to lower manpower costs and jobs credit grant received.

Other operating expenses contracted by 26.1%, decreasing from $31.4 million to $23.2 million mainly due to foreign exchange differences, lower allowance for doubtful debts and operating expenses from non-core assets that were divested last year.

With the repayment of borrowings, fi nance costs were also lower during the year. Finance costs decreased from $25.8 million to $17.0 million, representing a reduction of 34.1%.

Profi tabilityGross profi t margin narrowed from 27.0% to 23.0% refl ecting the diffi cult market conditions. In FY09, gross profi t totalled $112.9 million compared to $165.1 million in FY08, representing a decrease of 31.6%.

The share of results from associates declined from a profi t of $8.2 million in FY08 to a loss of $0.1 million in FY09 due to lower contribution from an associate.

The Group’s share of results of jointly controlled entities rose from a loss of $4.6 million in FY08 to a profi t of $19.4 million in FY09. This is mainly from the insurance claim for the KS Titan 1 lift boat as well as the gain from the divestment of a jointly controlled entity.

At the close of the fi nancial year 2009, the Group reported a net profi t after tax and minority interest of $40.0 million, representing a decrease of 22.9% from the net profi t after tax and minority interest of $51.9 million reported in FY08.

KS Energy Services Limited Annual Report 20098

BALANCE SHEET REVIEW

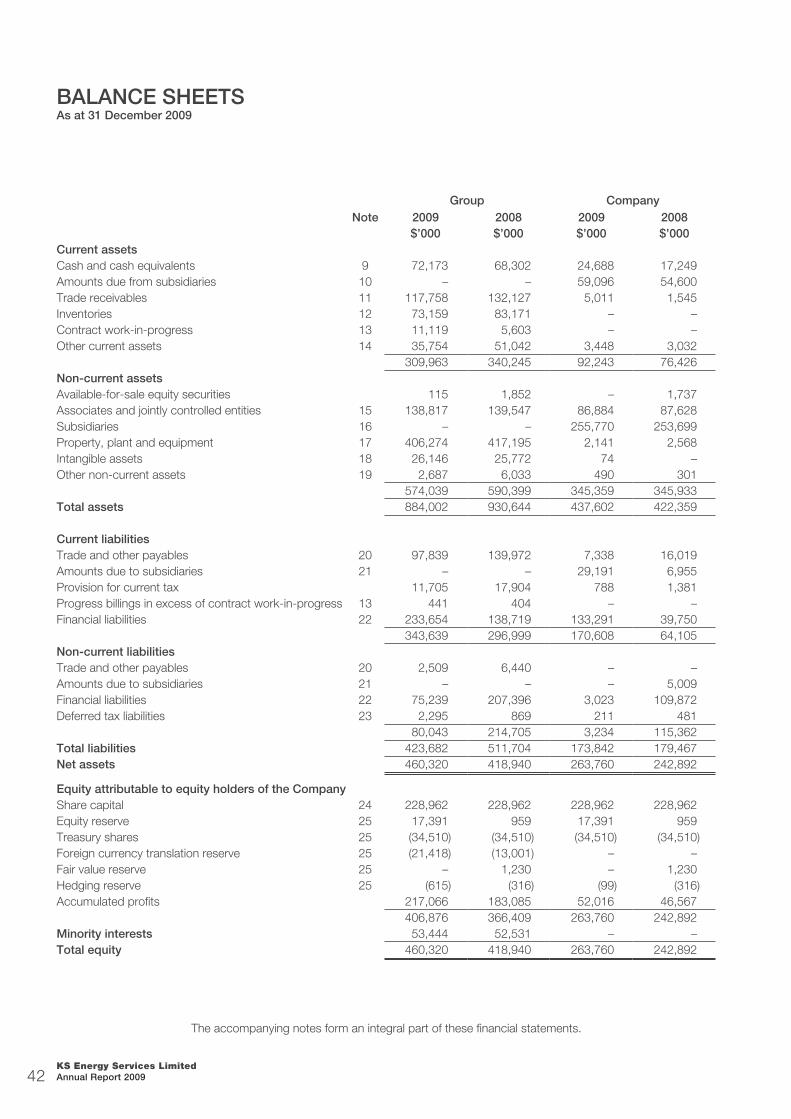

Current AssetsCompared to 31 December 2008, the Group’s current assets as at 31 December 2009 decreased by $30.2 million from $340.2 million to $310.0 million due mainly to decrease in trade receivables.

Non-current AssetsTotal non-current assets were lower this year mainly due to disposal of investment in available-for-sale equity securities and depreciation of plant and equipment during the year. Compared to the previous fi nancial year, total non-current assets was lower by $16.4 million, decreasing from $590.4 million to $574.0 million.

Current and Non-current LiabilitiesTotal current liabilities rose from $297.0 million last year to $343.6 million this year due to the reclassifi cation of convertible bond to current liabilities, ameliorated by net repayment of bank loans during the period. Total bank borrowings decreased from $345.5 million in FY08 to $308.3 million.

As a result of the reclassifi cation, the balance sheet showed a net current liabilities position and a reduction in non-current liabilities from $214.7 million to $80.0 million.

As announced on 26 January 2010, the Company has entered into a purchase agreement for the proposed issue of new convertible bonds of up to an aggregate of $107 million.

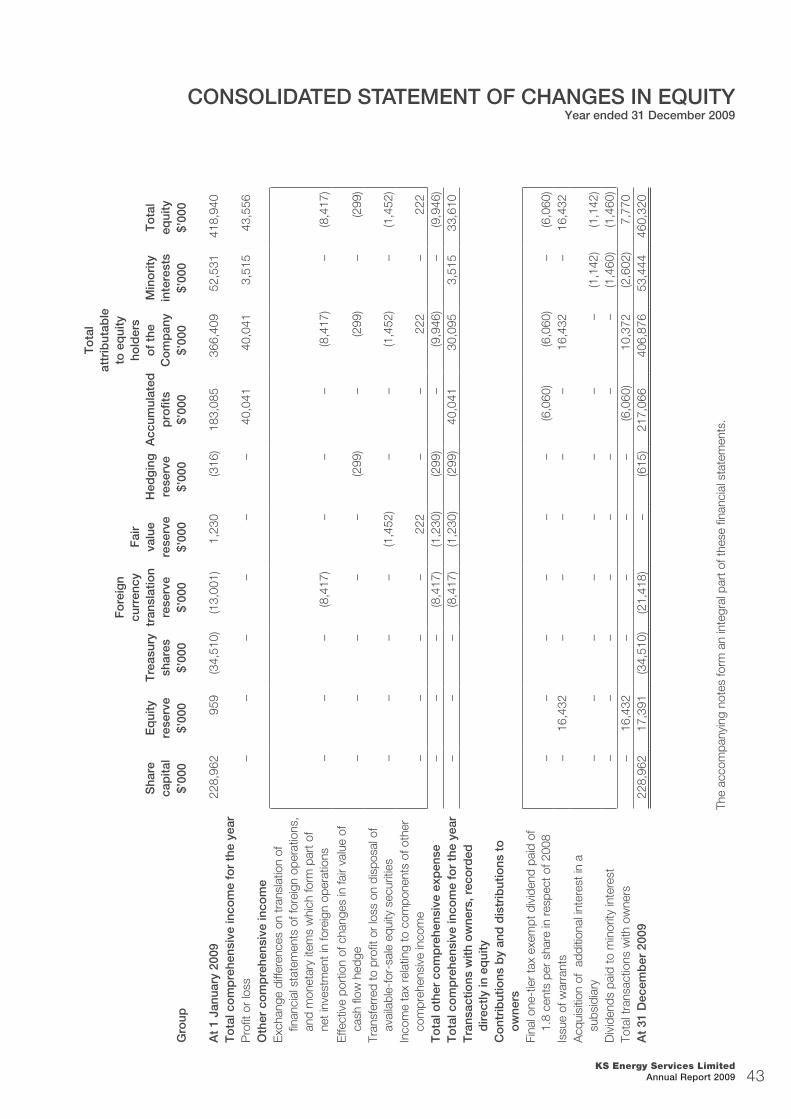

Equity attributable to equity holders of the parentEquity attributable to equity holders of the parent increased by $40.5 million from $366.4 million as at 31 December 2008 to $406.9 million as at 31 December 2009, and included in this amount are the proceeds from the issue of warrants.

KS Energy Services Limited Annual Report 2009 9

CASH FLOW STATEMENT REVIEW

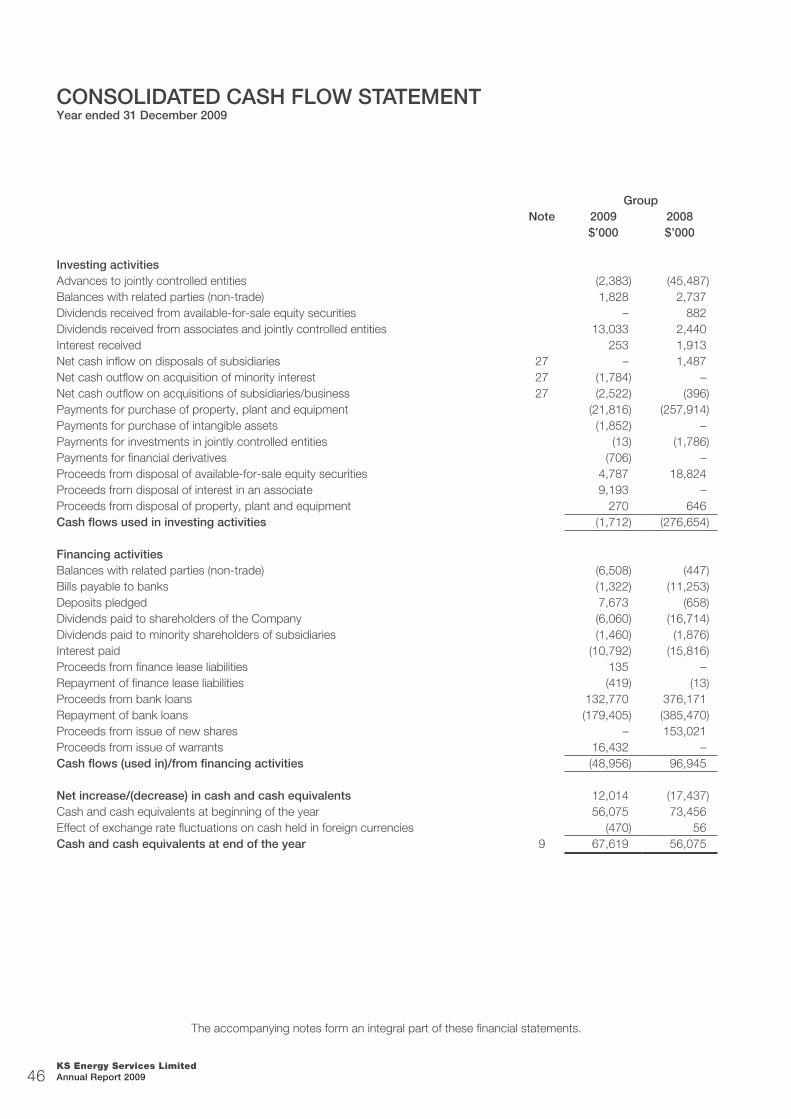

Cash Flow from Operating ActivitiesOperating activities generated cash infl ow of $62.7 million as at 31 December 2009.

Cash Flow from Investing ActivitiesNet cash outfl ow amounted to $1.7 million. This is attributable mainly to the costs incurred for capital equipment upgrading.

Cash Flow from Financing ActivitiesThere was a net cash outfl ow of $48.9 million due to the repayment of bank borrowings and payment of dividends to shareholders. Included in this amount is a cash infl ow of $16.4 million being proceeds from the issuance of warrants during the year.

At the close of the fi nancial year ended 31 December 2009, cash and cash equivalents totalled $72.2 million (FY08: $68.3 million).

“With the repayment of borrowings, fi nance costs were also lower during the year. Finance costs decreased from $25.8 million to $17.0 million, representing a reduction of 34.1%.”

Installation of windmill tower

KS Energy Services Limited Annual Report 200910

“At the close of the fi nancial year ended 31 December 2009, cash and cash equivalents totalled $72.2 million (FY08: $68.3 million).”

Valves distributed by KS Flow Control

Propeller used in vessels

KS Energy Services Limited Annual Report 2009 11

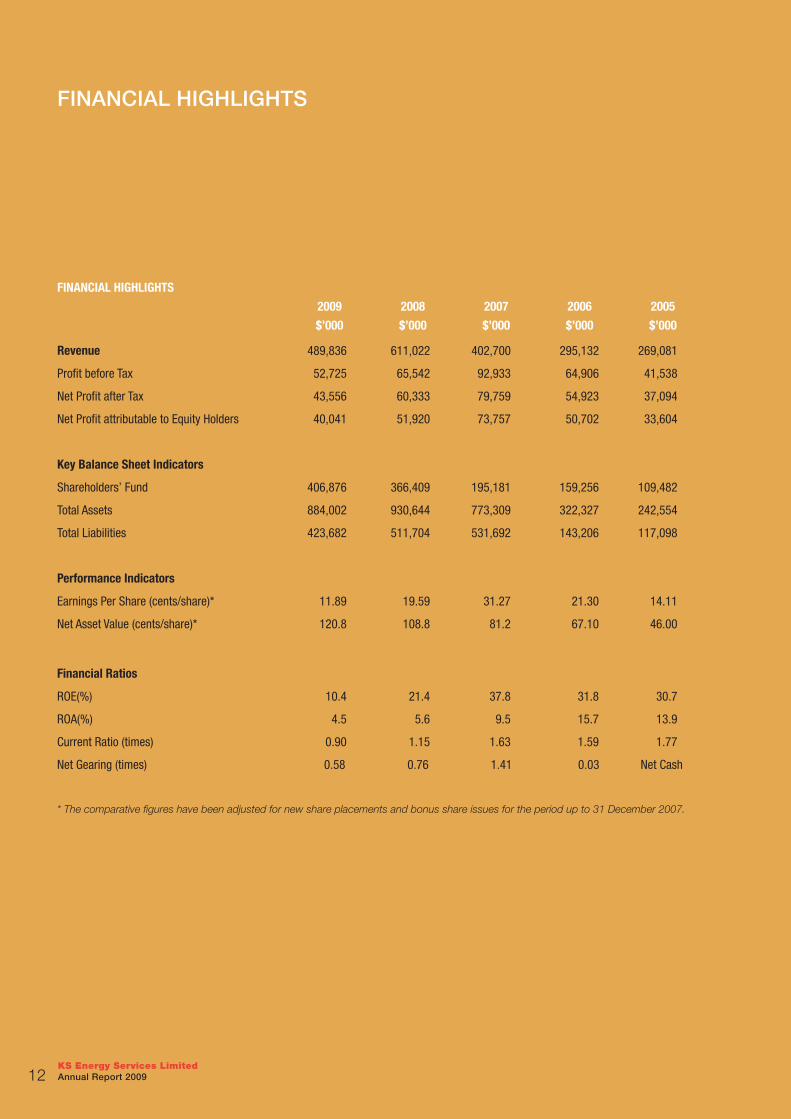

* The comparative figures have been adjusted for new share placements and bonus share issues for the period up to 31 December 2007.

FINANCIAL HIGHLIGHTS

2009 2008 2007 2006 2005

$’000 $’000 $’000 $’000 $’000

Revenue 489,836 611,022 402,700 295,132 269,081

Profit before Tax 52,725 65,542 92,933 64,906 41,538

Net Profit after Tax 43,556 60,333 79,759 54,923 37,094

Net Profit attributable to Equity Holders 40,041 51,920 73,757 50,702 33,604

Key Balance Sheet Indicators

Shareholders’ Fund 406,876 366,409 195,181 159,256 109,482

Total Assets 884,002 930,644 773,309 322,327 242,554

Total Liabilities 423,682 511,704 531,692 143,206 117,098

Performance Indicators

Earnings Per Share (cents/share)* 11.89 19.59 31.27 21.30 14.11

Net Asset Value (cents/share)* 120.8 108.8 81.2 67.10 46.00

Financial Ratios

ROE(%) 10.4 21.4 37.8 31.8 30.7

ROA(%) 4.5 5.6 9.5 15.7 13.9

Current Ratio (times) 0.90 1.15 1.63 1.59 1.77

Net Gearing (times) 0.58 0.76 1.41 0.03 Net Cash

FinAnciAl HigHligHts

KS Energy Services Limited Annual Report 200912

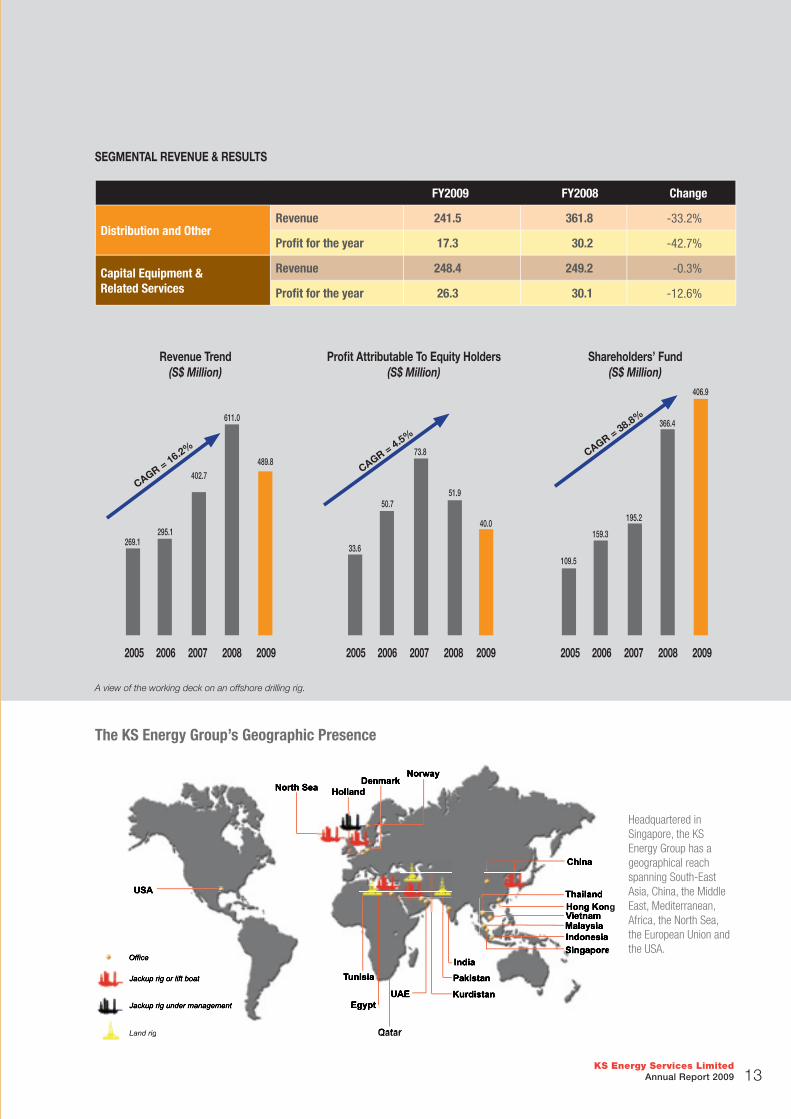

SEGMENTAL REVENUE & RESULTS

FY2009 FY2008 Change

Distribution and OtherRevenue 241.5 361.8 -33.2%

Profi t for the year 17.3 30.2 -42.7%

Capital Equipment & Related Services

Revenue 248.4 249.2 -0.3%

Profi t for the year 26.3 30.1 -12.6%

A view of the working deck on an offshore drilling rig.

Revenue Trend (S$ Million)

Profi t Attributable To Equity Holders (S$ Million)

Shareholders’ Fund (S$ Million)

33.6

50.7

40.0

51.9

73.8

2005 2006 2007 2008 2009

CAGR = 4.5%

2005 2006 2007 2008 2009

109.5

159.3

195.2

366.4

406.9

C

AGR = 38.8%

The KS Energy Group’s Geographic Presence

Egypt

North Sea Denmark

Pakistan

UAE

Qatar Qatar

USA

Kurdistan

Singapore Singapore

Malaysia

Thailand

Indonesia Indonesia

Vietnam

India

China

Hong Kong Hong Kong

Tunisia

Holland

Norway

Headquartered in Singapore, the KS Energy Group has a geographical reach spanning South-East Asia, China, the Middle East, Mediterranean, Africa, the North Sea, the European Union and the USA.

Jackup rig or lift boat

Land rig

Office

Jackup rig under management

2005 2006 2007 2008 2009

269.1295.1

402.7

611.0

489.8

CAGR = 16.2%

KS Energy Services Limited Annual Report 2009 13

BOARD OF DIRECTORS

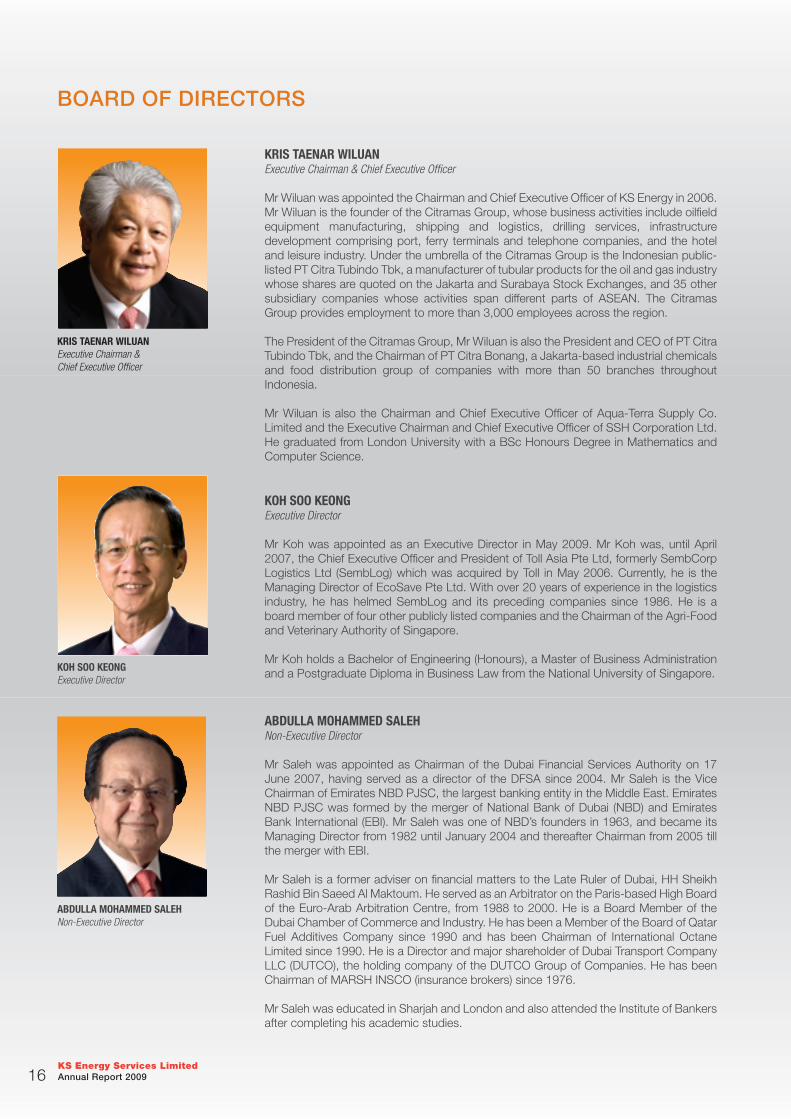

KRIS TAENAR WILUAN Executive Chairman & Chief Executive Offi cer

KOH SOO KEONG Executive Director

ABDULLAH MOHAMMED SALEH Non-Executive Director

LIM HO SENG Lead Independent Director

LEE BENG CHENG Independent Director

WONG MENG YENG Independent Director

NELSON McCALLUM GIBB Alternate Director to Mr Abdulla Mohammed Saleh and

Director of Group Business Development

AUDIT COMMITTEE

LIM HO SENG Chairman

WONG MENG YENG

LEE BENG CHENG

NOMINATING COMMITTEE

WONG MENG YENG Chairman

LEE BENG CHENG

KRIS TAENAR WILUAN

REMUNERATION COMMITTEE

LEE BENG CHENG Chairman

WONG MENG YENG

LIM HO SENG

COMPANY SECRETARIES

SHIRLEY LIM

BUSARAKHAM KOHSIKAPORN

REGISTERED OFFICE

No 19 Jurong Port Road Singapore 619093

Tel: (65) 6577 4600

Fax: (65) 6577 4618

Website: www.ksenergy.com.sg

Company Registration No: 198300104G

REGISTRAR & SHARE TRANSFER OFFICE

Tricor Barbinder Share Registration Services

(a division of Tricor Singapore Pte Ltd)

8 Cross Street #11-00 PWC Building Singapore 048424

AUDITORS

KPMG LLP

Certifi ed Public Accountants

16 Raffl es Quay #22-00 Hong Leong Building Singapore 048581

Partner-in-charge: TAN HUAY LIM

Year of appointment: 2005

BANKERS

Deutsche Bank

The Development Bank of Singapore Limited

The Hong Kong & Shanghai Banking Corporation Limited

ING Bank N.V.

Maybank Group

Oversea-Chinese Banking Corporation Limited

Standard Chartered Bank

United Overseas Bank Limited

coRpoRAte DAtA

KS Energy Services Limited Annual Report 200914

“Another challenge this year was the credit crunch as fi nancial institutions globally contracted their loan portfolios. To counter these effects, the Group successfully completed its fi rst warrant issue in August 2009, raising approximately $16.4 million. The money had been used to fund our working capital needs. Our total borrowings were lower this year and our gearing improved from 0.76 times to 0.58 times at the close of FY 2009.”

Loading steel pipes

Cutting wire ropes

KS Energy Services Limited Annual Report 2009 15

BoARD oF DiRectoRs

KOH SOO KEONGExecutive Director

KRIS TAENAR WILUANExecutive Chairman & Chief Executive Offi cer

Mr Wiluan was appointed the Chairman and Chief Executive Offi cer of KS Energy in 2006. Mr Wiluan is the founder of the Citramas Group, whose business activities include oilfi eld equipment manufacturing, shipping and logistics, drilling services, infrastructure development comprising port, ferry terminals and telephone companies, and the hotel and leisure industry. Under the umbrella of the Citramas Group is the Indonesian public-listed PT Citra Tubindo Tbk, a manufacturer of tubular products for the oil and gas industry whose shares are quoted on the Jakarta and Surabaya Stock Exchanges, and 35 other subsidiary companies whose activities span different parts of ASEAN. The Citramas Group provides employment to more than 3,000 employees across the region.

The President of the Citramas Group, Mr Wiluan is also the President and CEO of PT Citra Tubindo Tbk, and the Chairman of PT Citra Bonang, a Jakarta-based industrial chemicals and food distribution group of companies with more than 50 branches throughout Indonesia.

Mr Wiluan is also the Chairman and Chief Executive Offi cer of Aqua-Terra Supply Co. Limited and the Executive Chairman and Chief Executive Offi cer of SSH Corporation Ltd. He graduated from London University with a BSc Honours Degree in Mathematics and Computer Science.

KOH SOO KEONGExecutive Director

Mr Koh was appointed as an Executive Director in May 2009. Mr Koh was, until April 2007, the Chief Executive Offi cer and President of Toll Asia Pte Ltd, formerly SembCorp Logistics Ltd (SembLog) which was acquired by Toll in May 2006. Currently, he is the Managing Director of EcoSave Pte Ltd. With over 20 years of experience in the logistics industry, he has helmed SembLog and its preceding companies since 1986. He is a board member of four other publicly listed companies and the Chairman of the Agri-Food and Veterinary Authority of Singapore.

Mr Koh holds a Bachelor of Engineering (Honours), a Master of Business Administration and a Postgraduate Diploma in Business Law from the National University of Singapore.

ABDULLA MOHAMMED SALEH Non-Executive Director

Mr Saleh was appointed as Chairman of the Dubai Financial Services Authority on 17 June 2007, having served as a director of the DFSA since 2004. Mr Saleh is the Vice Chairman of Emirates NBD PJSC, the largest banking entity in the Middle East. Emirates NBD PJSC was formed by the merger of National Bank of Dubai (NBD) and Emirates Bank International (EBI). Mr Saleh was one of NBD’s founders in 1963, and became its Managing Director from 1982 until January 2004 and thereafter Chairman from 2005 till the merger with EBI.

Mr Saleh is a former adviser on fi nancial matters to the Late Ruler of Dubai, HH Sheikh Rashid Bin Saeed Al Maktoum. He served as an Arbitrator on the Paris-based High Board of the Euro-Arab Arbitration Centre, from 1988 to 2000. He is a Board Member of the Dubai Chamber of Commerce and Industry. He has been a Member of the Board of Qatar Fuel Additives Company since 1990 and has been Chairman of International Octane Limited since 1990. He is a Director and major shareholder of Dubai Transport Company LLC (DUTCO), the holding company of the DUTCO Group of Companies. He has been Chairman of MARSH INSCO (insurance brokers) since 1976.

Mr Saleh was educated in Sharjah and London and also attended the Institute of Bankers after completing his academic studies.

ABDULLA MOHAMMED SALEH Non-Executive Director

KRIS TAENAR WILUANExecutive Chairman & Chief Executive Offi cer

KS Energy Services Limited Annual Report 200916

LIM HO SENGLead Independent Director

Mr Lim is Lead Independent Director and Chairman of the Audit Committee and a member of the Remuneration Committee of the Group. He was appointed our Independent Non-Executive Director on 1 September 2005. He is the Chairman of Baker Technology Ltd and sits on the Board of several other public companies listed on the Stock Exchange of Singapore. He was the former Chief Executive Offi cer of NTUC Fairprice Cooperative Ltd. Mr Lim is a Fellow of the Institute of Certifi ed Public Accountants Singapore, the Institute of Certifi ed Public Accountants Australia and the Association of Chartered Certifi ed Accountants of United Kingdom. He is also a Fellow of the Institute of Chartered Secretaries & Administrators and the Singapore Institute of Directors.

LEE BENG CHENGIndependent Director

Mr Lee has extensive experience in the oil and gas and marine industries, having worked in the oil refi ning and petrochemical sectors, offshore drilling rig and platform construction including drilling several oil and gas wells both onshore and offshore in Asia. He held senior positions in several public-listed and private entities in the hydrocarbon industry in Singapore, Malaysia and China including Vice Chairman of the listed Shenzhen-Chiwan Petroleum Supply Base, Chairman of Singapore Offshore Petroleum Supply Base, President of Sembawang Marine & Logistics Ltd (formerly known as Sembawang Maritime Ltd), Managing Director of Hong Kong listed Promet Petroleum Ltd. Mr Lee holds a First Class Honours Degree in Mechanical Engineering and a Master of Science (with distinction) from Leeds University, UK. He is also a member of the Singapore Institute of Management, the Institute of Engineers Singapore and the Singapore Institute of Directors.

WONG MENG YENGIndependent Director

Mr Wong has been an advocate and solicitor in Singapore since 1984 and practises corporate law. He is currently a director of Alliance LLC, a law corporation he co-founded in 2001. Over the last 10 years he has been an Independent Director of several companies listed on the Singapore Exchange. Mr Wong graduated from the National University of Singapore in 1983 with a Bachelor of Laws (Honours) Degree.

NELSON McCALLUM GIBBAlternate Director to Mr Abdulla Mohammed Saleh and Director of Group Business Development

Mr Gibb was appointed as an alternate director to Mr Abdulla Mohammed Saleh on 22 December 2009. He has been with Dutco since 1996 and is currently the Group’s Chief Operating Offi cer. The Dutco Group is a leading Dubai based conglomerate comprising 20 Companies and over 25,000 employees.

The Company has signifi cant interests in all sectors of construction, hospitality & leisure, oil and gas, manufacturing, development and investments and trading. Dutco are partners in the Middle East with many international companies such as the Balfour Beatty plc from the UK and Mc Connell Dowell Ltd. from Australia. Prior to joining Dutco in 1996, Mr Gibb was the Director for the International Business of the leading Mechanical and Electrical Engineering Company, Balfour Kilpatrick Ltd (a member of the Balfour Beatty Group of Companies, a major UK listed Construction Group), whose Projects and Companies were based across Asia, Africa, and the Middle East.

Mr Gibb was educated in West Africa, Indonesia and Scotland, completing his BA (Hons) at Stratchclyde University in Glasgow. Mr Gibb sits on many of the Boards of the Group of Companies of the Dutco Group.

LIM HO SENGLead Independent Director

LEE BENG CHENG, BILLYIndependent Director

WONG MENG YENGIndependent Director

NELSON McCALLUM GIBBAlternate Director to Mr Abdulla Mohammed Saleh

KS Energy Services Limited Annual Report 2009 17

LEE SENG QUEE

Mr Lee joined the Company on 1 March 2007 as Strategic Advisor to Chairman.

Mr Lee has been with the Citramas Group since 1978, where he is responsible for corporate matters. He is also an Advisor to the Board of Directors of PT Citra Tubindo Tbk.

Mr Lee practises as a Public Accountant and holds professional qualifi cations including Fellow Member of the Institute of Certifi ed Public Accountants of Singapore; Fellow Member of CPA Australia; Fellow Member of the Association of Chartered Certifi ed Accountants; Fellow Member of the Institute of Chartered Secretaries and Administrators, UK and Member of the Singapore Institute of Directors. Mr Lee also holds a Master of Business Administration majoring in Business Laws from the Nanyang Business School, Nanyang Technological University.

Mr Lee is author of and updates the publication, CCH Hands On Guide for Corporate Secretarial Essentials.

SHEIKH FAISAL F.J. AL–THANI

Sheikh Al-Thani was appointed an Independent Director of the Group on 20 January 2006. He has over 23 years of working experience in the oil and gas industry in Qatar. He started his career in 1987 with state-owned Qatar Petroleum and spent more than a decade working there before being seconded to Arco Qatar, British Petroleum and Anadarko Qatar Energy Co., LLC as Deputy General Manager and Qatar Petroleum representative in the said companies. In March of 2008, he assumed the position of Sr. Director and Head of Business Development in the Middle East for Maersk Oil Qatar as seconded by Qatar Petroleum. Sheikh Al-Thani is the Chairman of both Naama Real Estate Company and Qatar National Export Import Company. He is a prolifi c author and has published numerous books on risk management and trends in the oil and gas industry in the Middle East. He is also the current Chairman of the Society of Petroleum Engineers International - Qatar Section and the Chairman and founding member of the local Qatar Society of Petroleum Engineers (QSPE), a Fulbright scholar, completed his fi rst degree in Petroleum Engineering at the University of Tulsa, Oklahoma followed by a Masters in Project Management at the University of Bath as well as a PhD in Project Finance at Leeds University, UK.

NG SHIN EIN

Ms Ng Shin Ein was appointed to the Board in 1 May 2009. She is the Regional Managing Director of Blue Ocean Associates Pte Ltd, a pan-asian investment and strategic advisory fi rm. Blue Ocean Associates takes proprietary stakes in companies and also advises corporates and other investment funds.

Prior to this, Ms Ng was with the Singapore Exchange, where she was responsible for developing Singapore’s capital market by bringing foreign companies to list in Singapore. Additionally, she was part of the Singapore Exchange’s IPO Approval Committee.

Ms Ng started her career as a corporate lawyer in Messrs Lee & Lee. Whilst in legal practice, she advised on joint ventures, mergers and acquisitions and fund-raising exercises.

Ms Ng also serves on the board of Yanlord Land Group Ltd and First Resources Ltd, both listed on SGX, and is also a director of NTUC Fairprice.

BoARD oF ADVisoRs

KS Energy Services Limited Annual Report 200918

MAnAgeMent BoARD

KRIS TAENAR WILUANExecutive Chairman & Chief Executive Offi cer

Mr Wiluan was appointed the Chairman and Chief Executive Offi cer of KS Energy in 2006. Mr Wiluan is the founder of the Citramas Group, whose business activities include oilfi eld equipment manufacturing, shipping and logistics, drilling services, infrastructure development comprising port, ferry terminals and telephone companies, and the hotel and leisure industry. Under the umbrella of the Citramas Group is the Indonesian public-listed PT Citra Tubindo Tbk, a manufacturer of tubular products for the oil and gas industry whose shares are quoted on the Jakarta and Surabaya Stock Exchanges, and 35 other subsidiary companies whose activities span different parts of ASEAN. The Citramas Group provides employment to more than 3000 employees across the region.

The President of the Citramas Group, Mr Wiluan is also the President and CEO of PT Citra Tubindo Tbk, and the Chairman of PT Citra Bonang, a Jakarta-based industrial chemicals and food distribution group of companies with more than 50 branches throughout Indonesia.

Mr Wiluan is also the Chairman and Chief Executive Offi cer of Aqua-Terra Supply Co. Limited and the Executive Chairman and Chief Executive Offi cer of SSH Corporation Ltd. He graduated from London University with a BSc Honours Degree in Mathematics and Computer Science.

KOH SOO KEONGExecutive Director

Mr Koh was appointed as an Executive Director in May 2009. Mr Koh was, until April 2007, the Chief Executive Offi cer and President of Toll Asia Pte Ltd, formerly SembCorp Logistics Ltd (SembLog) which was acquired by Toll in May 2006. Currently, he is the Managing Director of EcoSave Pte Ltd. With over 20 years of experience in the logistics industry, he has helmed SembLog and its preceding companies since 1986. He is a board member of four other publicly listed companies and the Chairman of the Agri-Food and Veterinary Authority of Singapore.

Mr Koh holds a Bachelor of Engineering (Honours), a Master of Business Administration and a Postgraduate Diploma in Business Law from the National University of Singapore.

DR ADAM PAUL BRUNET Managing Director of Oil, Gas and Energy ServicesCEO of Atlantic Oilfi eld Services Ltd

Dr Brunet has worked in the oil industry since he left college in 1977 and started work as a Field Engineer for Schlumberger S.A. in West Africa. Since 1983, Dr Brunet has been involved in establishing and managing PT Citra Tubindo Tbk (“Tubindo”) and is presently the Technical Director. He oversees the manufacturing processes, engineering and business development as well as procurement and marketing functions of Tubindo and its group of companies. Dr Brunet, a postgraduate from Oxford University, is also an established academic who specialises in operations management. Through strategic alliances and joint ventures, Dr Brunet has capitalised on Tubindo’s engineering capabilities to develop new technologies, products and services, transforming the company into an export driven entity supplying global oil and gas companies. In 2003, he established an intellectual properties subsidiary to develop the market for Tubindo’s technologies.

From 2006 to 2010, Dr Brunet has acted as an Executive Director in KS Energy focusing on the Capital Equipment Division and later Managing Director of Oil, Gas and Energy Services. In January 2009, Dr Brunet was appointed Executive Director of KS Energy subsidiary Atlantic Oilfi eld Services Ltd and became its CEO on 1 May 2009.

WOO PENG KONGManaging Director of Group Capital Equipment and Projects

Mr Woo joined the Group in 2004 when the GlobalTech group of companies, which he co-founded in 2002, became its subsidiaries. He was appointed subsequently as the Chief Operating Offi cer and Executive Director of the Group. In May 2009, he was appointed as Managing Director of Group Capital Equipment and Projects. In 2009, he took charge of the management and supervision of asset owning companies and capital equipment projects of the Group; oversaw the marketing and sale of oil & gas equipment; and managed the review and implementation of projects and investments. An engineer by training, Mr Woo has more than 25 years of experience in the oil and gas and marine industry, assuming diversifi ed senior management roles in engineering, sales & marketing, new business start-up and joint-ventures with particular expertise in business operations and fi nancial management. Mr Woo holds a First Class Honours Bachelor Degree in Mechanical Engineering from the then University of Singapore and a Certifi ed Diploma in Accounting & Finance from the Chartered Association of Certifi ed Accountants.

*Mr Woo resigned from the Management Board in January 2010.

KS Energy Services Limited Annual Report 2009 19

GOH BOON CHYEManaging Director of Group Distribution Business

Mr Goh joined the Group in 1999. He is responsible to grow the Group’s distribution businesses in new markets around the world. Mr Goh was the Chief Financial Offi cer in 1999. On 29 November 2002, Mr Goh held the post of Chief Operating Offi cer. Mr Goh was appointed the Chief Business Development Offi cer on 16 February 2006. Prior to 1998, Mr Goh held the post of Financial Controller in Parker Hannifi n Pte Ltd and Motorola Electronics Pte Ltd.

Mr Goh graduated from the then University of Singapore in 1976 with a Bachelor of Accountancy Degree and is a Certifi ed Accountant by profession. He also holds a MBA from Oklahoma City University. Mr Goh is a fellow of the Singapore Institute of Certifi ed Public Accountants and the Association of Chartered Certifi ed Accountants of United Kingdom.

WONG SOON YINChief Financial Offi cer

Ms Wong was appointed as Chief Financial Offi cer in December 2008. Ms Wong is responsible for the accounting and fi nance matters of the Company. She sits on the Board of various subsidiaries within the KS Group. She has almost 30 years of experience as an accounting professional. Prior to joining KS Energy, Ms Wong was the Chief Financial Offi cer of Green Dot Capital Pte Ltd. She has extensive accounting and fi nancial experience from her previous employment with the Singapore Technologies Group and Ernst & Young.

Ms Wong is a fellow with the Institute of Certifi ed Public Accountants of Singapore. She holds a Bachelor of Accountancy Degree from the then University of Singapore.

MAnAgeMent BoARD

DIANA LENGDirector of Group Treasury

Ms Leng joined the Group in 2007 and was appointed a member of the Management Board a year later. Ms Leng is responsible for Group Treasury, Corporate Finance, Mergers & Acquisitions, and all funding-related activities. She also sits on the Board of Atlantic Oilfi eld Services (AOS), the Group’s operating arm of its Capital Equipment Division as well as several other subsidiaries within the KS Group. Ms Leng brings with her considerable experience in banking and fi nance, having held several positions in banking, insurance and asset management. She started her banking career in the Netherlands, and held various positions internationally. In her last position as Director of Business Management of a global bank, she was responsible for the development and implementation of business strategies for its Corporate Lending Group in Asia. Prior to that, she was a Vice President in its Structured Finance department, handling origination, structuring and execution of transactions, as well as the provision of fi nancing solutions for clients trading in oil and other commodities. Ms Leng holds a Bachelor of Business Administration from Maastricht University, the Netherlands with a minor degree in Finance from the Leonard Stern School of Business at New York University, USA, and a Master of Business Administration (with Distinction) from Maastricht University.

NELSON McCALLUM GIBBAlternate Director to Mr Abdulla Mohammed Saleh and Director of Group Business Development

Mr Gibb was appointed as an alternate director to Mr Abdulla Mohammed Saleh on 22 December 2009. He has been with Dutco since 1996 and is currently the Group’s Chief Operating Offi cer. The Dutco Group is a leading Dubai based conglomerate comprising 20 Companies and over 25,000 employees.

The Company has signifi cant interests in all sectors of construction, hospitality & leisure, oil and gas, manufacturing, development and investments and trading. Dutco are partners in the Middle East with many international companies such as the Balfour Beatty plc from the UK and Mc Connell Dowell Ltd. from Australia. Prior to joining Dutco in 1996, Mr Gibb was the Director for the International Business of the leading Mechanical and Electrical Engineering Company, Balfour Kilpatrick Ltd (a member of the Balfour Beatty Group of Companies, a major UK listed Construction Group), whose Projects and Companies were based across Asia, Africa, and the Middle East.

Mr Gibb was educated in West Africa, Indonesia and Scotland completing his BA (Hons) at Stratchclyde University in Glasgow. Mr Gibb sits on many of the Boards of the Group of Companies of the Dutco Group.

KS Energy Services Limited Annual Report 200920

RegionAl DiRectoRs

ADI HARSONOChina & Pacifi c

Mr Harsono joined the company on 1 February 2008 and is responsible for managing the Company’s activities in China. Prior to joining KS Energy, Mr Harsono was the Director of Schlumberger in Jakarta, Houston and Shanghai. He spent 25 years with Schlumberger starting from a fi eld engineer in West Africa, Europe, Middle East, Australia, Asia and USA. He was also the General Manager of Schlumberger’s Smart Card Business in Shanghai. He is active in Business Association and government related activities that allow him access to high level business and government networks. Mr Harsono holds a Master Degree in Physics from Gadjahmada University, Yogyakarta, Indonesia.

SYED ABDEL NASSER BIN SYED HASSAN ALJUNIEDMiddle East & India

Mr Aljunied joined the Company on 1 January 2007 as the Strategic Investment Advisor for the Middle East in 2008. He currently sits on the board of Atlantic Oilfi eld Services, a Dubai based subsidiary of KS Energy. Mr Aljunied is a Director and shareholder of the Greenworld Group, an integrated timber producer in the Forestry and Wood production business. In 2000, Mr Aljunied co-founded Asiawerks Global Investment Group (AGI), a boutique private equity investment advisory fi rm. He has been an Independent and Non-Executive Director and Chairman of Audit Committee for Singapore listed Maveric Ltd since 2006. Additionally, he is also a board member and shareholder of CMS Trust Berhad, an asset management Company with more than RM2 billion under management. Prior to starting his businesses in 2000, he headed the Asian FX & Fixed Income derivatives team for the Emerging Markets Group at Credit Suisse First Boston (“CSFB”). During the 90s, he was Vice President & Money Manager at both Chase Private Bank and later Smith Barnet Asset Management where he managed Middle East private wealth and institutional money. Mr Aljunied graduated from the National University of Singapore with a Degree in double Physics.

MICHAEL D. REIZERAmericas

Mr Reizer joined the Company in 2007 and is responsible for managing the Company’s activities in North and South America. Prior to joining KS Energy, Mr Reizer was President and CEO of Bredero Shaw Ltd., a London/Houston based applicator of engineered coating systems to onshore and offshore pipelines. Mr Reizer joined Bredero in 1978 as Vice President, Asia and Middle East Operations, based in Singapore where he was located until 1991, and relocating to London, England as President of the Group. Mr Reizer also served as a Director of the International Pipeline Contractors Association. Prior to joining Bredero Shaw, he held Senior International Marketing positions with major suppliers to the International Oil and Gas Industry. Mr Reizer holds a Bachelor Degree in Biology from Regis University, Denver Colorado, USA.

ALFRED SCHWEGLER Europe & Africa

Mr Schwegler was appointed as the Regional Director for Europe and Africa of the Group on 1 May 2009, responsible for business activities in Europe and Africa. He sits on the board of Atlantic Oilfi eld Services Ltd since 30 May 2007. Mr Schwegler has more than 30 years of experience in the oil and gas business and has proven international experience especially in the North Sea.

Mr Schwegler holds a Bachelor degree in mechanical engineering Degree with major in energy.

KS Energy Services Limited Annual Report 2009 21

gRoup stRuctuRe

AS AT 31ST DECEMBER 2009

28.2% SSH Corporation Ltd*

54.8% Aqua-Terra Supply Co. Limited*

70% GlobalTech System Engineering Pte Ltd

99.9% PT KS Flow Control

80% GlobalTech Offshore & Marine Pte Ltd

100% KS Equipment (Shanghai) Ltd

100% GlobalTech Group Pte Ltd

100% KS Flow Control Pte Ltd

100% KS Distribution Pte Ltd

DiStribution anD othErS

* Listed on SGX Main Board

100% Sphinx Frontier Ltd

100% QIM Ventures Limited

100% Atlantic Marine Service Egypt

100% KS Discovery (HK) Limited

100% Specialist Resources International Pte Ltd

100% KS Technical Resources Pte Ltd

100% KS Discoverer 3 (HK) Limited

100% KS Discoverer 4 Pte Ltd

100% KS North Sea Rig Pte Ltd

100% KS Oilfield Services Ltd

100% United Oilfield Services Pte Ltd

100% KS Discoverer 2 Pte Ltd

50% Global Oilfield Services Pte Ltd

70% KT Lion Oilfield Services Limited

50% KSAM2 Petrodrill Offshore Inc

50% Casadilla Group Pte Ltd

50% Girdnal Oilfield Services Inc

50% Yakki International Pte Ltd

CapitaL EquipmEnt anD rELatED SErViCES

Note 1

Note 1

Note 1

Note 1 and 2

Note 3

Note 1

Note 1: Please note that pursuant to the Business Consolidation, this structure will change upon completion of Business Consolidation

Note 2: GlobalTech Offshore & Marine Pte Ltd became a wholly-owned subsidiary of KS Flow Control Pte Ltd on 7 January 2010

Note 3: As at 7 January 2010, GlobalTech Group Pte Ltd held 82% shareholding in GlobalTech System Engineering Pte Ltd

100% Atlantic Oilfield Services Ltd

100% Atlantic Marine Services (Cyprus) Group Limited

100% Atlantic Marine Services BV

100% Atlantic Onshore Services BV

100% Atlantic Marine Services Denmark BV

KS Energy Services Limited Annual Report 200922

“Other operating income was lower in FY09 due to the reduction in the sale of investments during the year compared to FY08. As a result, other operating income was lower by 38.5%, decreasing from $16.1 million to $9.9 million in FY09.”

KS Energy Services Limited Annual Report 2009 23

Financial Contents

Corporate Governance Statement 25

Directors’ Report 34

Statement by Directors 38

Independent Auditors’ Report 39

Consolidated Income Statement 40

Balance Sheets 42

Consolidated Statement of 43

Changes in Equity

Consolidated Cash Flow Statement 45

Notes to the Financial Statements 47

Statistics of Shareholders 130

Notice of Annual General Meeting 134

Proxy Form

KS Energy Services Limited Annual Report 2009 25

CORPORATE GOVERNANCE STATEMENT

KS Energy Services Limited (the “Company”) is committed to maintaining good standards of corporate governance in conducting the Group’s business and the Board of Directors of the Company (the “Board”) ensures that an effective self-regulatory and monitoring mechanism exists and is maintained.

The Company confirms that it has adhered to the principles and guidelines as set out in the 2005 Code of Corporate Governance (“Code”), where applicable, and explanations are provided for areas of non-compliance.

BOARD OF DIRECTORS

Principle 1: Board’s Conduct of its Affairs

The Board’s primary role is to protect and enhance long-term shareholders’ value. It sets the overall strategic direction of the Company and supervises the management of the Company (the “Management”). It is also responsible for the overall corporate governance of the Company including setting its strategic direction, establishing goals for the Management and monitoring the achievement of these goals.

The principal functions of the Board apart from its statutory responsibilities are to:

a) set values and standards of the Company and ensure that obligations to shareholders and others are understood and met;

b) provide entrepreneurial leadership, approve the strategic and financial objectives, corporate policies and authorisation matrix of the Company;

c) oversee the processes for risk management, financial reporting and compliance and evaluate the adequacy of internal controls; approve annual budget, key operational matters, major acquisition and divestment proposals, major funding proposals of the Company;

d) review management performance;

e) approve the nominations to the Board of Directors and appointment of key management, as may be recommended by the Nominating Committee; and

f) assume responsibility for corporate governance framework of the Company.

To facilitate effective management, certain functions of the Board have been delegated to various Board Committees, namely Audit, Nominating and Remuneration Committees. Each Board Committee has the authority to examine particular issue and report back to the Board with their recommendations. The ultimate responsibility for the final decision on all matters, however, lies with the Board. Further information regarding the functions of the respective Board Committees is set out in the later part of this Report.

The Board conducts regular scheduled meetings on a quarterly basis. Ad-hoc meetings are convened when circumstances require. The Company’s Articles of Association (the “Articles”) provide for Board meetings to be conducted by way of telephone and video conferencing.

KS Energy Services Limited Annual Report 200926

CORPORATE GOVERNANCE STATEMENT

The attendance of the Directors at meetings of the Board and Board committees as well as number of such meetings during the financial year is set out in the table below:

Board Audit CommitteeNominating Committee

Remuneration Committee

Name of DirectorNo. of

Meetings Held

AttendanceNo. of

Meetings Held

AttendanceNo. of

Meetings Held

AttendanceNo. of

Meetings Held

Attendance

Mr. Kris Taenar Wiluan 8 8 - - 2 2 - -

Mr. Koh Soo Keong* 8 8 - - - - - -

Mr. Abdulla Mohammed Saleh* (Alternate: Nelson McCallum Gibb)

6 1 - - - - - -

Mr. Lim Ho Seng 8 8 5 5 - - 5 4

Mr. Lee Beng Cheng 8 8 5 5 2 2 5 5

Mr. Wong Meng Yeng 8 8 5 5 2 2 5 5

Mr. Goh Boon Chye * 2 2 - - - - - -

Dr. Adam Paul Brunet* 1 1 - - - - - -

Sheikh Faisal F.J. Al-Thani* 1 0 - - - - - -

Mr. Woo Peng Kong* 2 2 - - - - - -

* Dr Adam Paul Brunet retired on 28 April 2009* Sheikh Faisal F. J. Althani retired on 28 April 2009* Mr Koh Soo Keong was re-designated as an executive director on 1 May 2009 * Mr. Goh Boon Chye resigned on 1 May 2009* Mr. Woo Peng Kong resigned on 1 May 2009* Mr. Abdulla Mohammed Saleh was appointed on 1 May 2009 (Alternate: Nelson McCallum Gibb was appointed on 22 December 2009)

Principle 2: Board Composition and Balance

The Board of Directors comprises the following:

Executive Directors Mr. Kris Taenar Wiluan Mr. Koh Soo Keong

Non-Executive and Non-Independent DirectorMr. Abdulla Mohammed Saleh (Alternate: Nelson McCallum Gibb)

Non-Executive and Independent DirectorsMr. Lim Ho SengMr. Lee Beng ChengMr. Wong Meng Yeng

There is an independent element on the Board with three independent directors out of six directors of the Company.

The size of the Board is reviewed on an ongoing basis and its current size is considered appropriate for the facilitation of effective decision making. As a team, the Board collectively provides core competencies in the areas of oil and gas industry knowledge, legal, accounting, finance, business and management experience. Key information of the Board members is set out on pages 16 and 17 of the Annual Report.

KS Energy Services Limited Annual Report 2009 27

CORPORATE GOVERNANCE STATEMENT

The duties and responsibilities of the executive directors are clearly set out in their service agreements and the duties and responsibilities of the non-executive directors are clearly set out in their Engagement Letters.

Each Director is responsible for his own training needs and utilizes a budget provided by the Company for his training requirements to keep abreast developments in law, regulation, accounting and industrial practices and changes in technology.

The Company has orientation programmes for newly appointed directors to familiarise themselves with the Company’s senior management, culture, business, governance and best practices. An orientation programme was conducted for a newly appointed director, Mr Abdulla Mohammed Saleh, in FY2009.

Principle 3: Chairman and CEO

The Board is of the opinion that there is an independent element on the Board to enable independent exercise of objective judgment on corporate affairs of the Group and that there is a good balance of power and authority. As such, there is no need for the role of the Chairman and the CEO to be separated.

The Group’s Executive Chairman and Chief Executive Officer (“CEO”), Mr. Kris Taenar Wiluan plays an instrumental role in developing the business of the Group and provides the Group with strong leadership and vision. He is responsible for the operational and strategic policies of the Group. The Group’s Executive Chairman also has the responsibilities of setting the meeting agenda of the board meetings, leading the other Board members, promoting high standards of corporate governance and maintaining effective communication with shareholders of the Company.

He ensures that board meetings are held when necessary. He reviews most board papers before they are presented to the Board and ensures that board members are provided with complete, adequate and timely information. As a general rule, board papers are sent to directors in advance in order for directors to be adequately prepared for the meeting. Management staff who can provide additional insight into matters under review to be discussed, are invited to attend board meetings, as and when necessary.

The two Executive Directors and the Management Board are responsible for the day-to-day operations of the Company. There is clear division of responsibilities between the Executive Chairman and the Executive Directors.

The Executive Chairman and CEO’s performance and appointment to the Board is reviewed periodically by the Nominating Committee (“NC”) and his remuneration package is reviewed by the Remuneration Committee (“RC”).

Lead Independent Director (“LID”)

Mr Lim Ho Seng was appointed LID on 1 May 2008. As LID, Mr Lim is the principal liaison to address shareholders’ concerns, in which direct contact through normal channels of the Chairman/CEO or CFO has failed to resolve or for which such contact is inappropriate. His other specific roles as LID are as follows:

a) act as liaison between the independent directors of the Board and the Chairman of the Board;

b) advise the Chairman of the Board as to the quality, quantity and timeliness of the information submitted by the Company’s management that is necessary or appropriate for the independent directors to effectively and responsibly perform their duties;

c) assist the Board and Company officers in better ensuring compliance with and implementation of the Governance Guidelines; and

d) serve as a liaison for consultation and communication with shareholders.

KS Energy Services Limited Annual Report 200928

CORPORATE GOVERNANCE STATEMENT

Principle 6: Access to InformationPrincipal 10: Accountability

Board members are provided with management information, background and explanatory notes pertaining to such areas e.g. budget, forecast, the funding positions and quarterly financial statements of the Group, to help them carry out their responsibilities effectively. In addition, all relevant information on material events and transactions are circulated to directors as and when they arise.

All Board members have direct access to senior management and to the Company Secretary. The appointment and the removal of the Company Secretary is a matter reserved for the Board.

The Board is updated on amendments/requirements of the Singapore Exchange Securities Trading Limited (“SGX-ST”), and other statutory and regulatory requirements from time to time.

Under the direction of the Executive Chairman, the Company Secretary’s responsibilities include ensuring that:

a) board procedures are followed;

b) applicable requirements of the Companies Act and listing rules of the SGX are complied with; and

c) good information flows within the Board and its committees and between senior management and Non-Executive directors.

All Board members also have separate and independent access to the senior management of the Company and the Group. All Board members are aware that they, whether as a group or individually, in the furtherance of their duties, can take independent professional advice, if necessary, at the Company’s expense.

BOARD COMMITTEES

Nominating Committee

Principle 4: Board Membership

The Nominating Committee comprises the following:

Mr. Wong Meng Yeng (Chairman and Independent Director)Mr. Lee Beng Cheng (Independent Director)Mr. Kris Taenar Wiluan (Executive Director)

The functions of the NC include the following:

a) identify, review and recommend candidates for appointment as Directors of the Company and appointment to the Board committee as well as to senior management positions in the Company;

b) evaluate the effectiveness of the Board as a whole and assess the contribution by each Director, to the effectiveness of the Board;

c) determine annually whether or not a Director is independent; and

d) make recommendations to the Board on the re-appointment or re-election of the Directors to the Board.

During the year, the NC met, reviewed and determined the independence of the Directors.

In accordance with the provisions of the Articles, one-third of the Directors retire by rotation and subject themselves to re-election at every Annual General Meeting (“AGM”). New Directors who are appointed by the Board will submit themselves for re-election at the following AGM.

KS Energy Services Limited Annual Report 2009 29

The NC has recommended the nomination of Mr. Kris Taenar Wiluan, Mr. Lee Beng Cheng and Mr. Abdulla Mohammed Saleh, for re-election at the forthcoming AGM. Their profiles are set out in pages 16 and 17 of the Annual Report.

Principle 5: Board Performance

An evaluation of the Board performance for FY2009 was conducted by the NC. The aim of this evaluation was to review the effectiveness of the Board as a whole and to provide an opportunity to obtain constructive feedback from each Director on whether the Board’s procedures and processes had allowed him to discharge his duties effectively. Board members are encouraged to propose changes which may be made to enhance Board effectiveness as a whole.

The NC, in considering the contribution of each Director to the effectiveness of the Board, had reviewed:

a) the attendance and participation of the Directors at Board and Board Committee meetings;

b) the competing time commitments of Directors with multiple board seats; and

c) the independence of independent Directors, where applicable.

Audit Committee

Principle 11: Audit Committee

The Audit Committee comprises the following:

Mr. Lim Ho Seng (Chairman and Lead Independent Director)Mr. Lee Beng Cheng (Independent Director)Mr. Wong Meng Yeng (Independent Director)

The AC performs the following functions:

a) reviews with the external auditors, their audit plan, evaluation of the accounting controls, audit reports and any matters which the external auditors wish to discuss;

b) reviews with the internal auditors, their audit plan, the adequacy of the internal audit procedures and their evaluation of the effectiveness of the overall internal control systems, including financial, operational and compliance controls and risk management;

c) reviews the quarterly and annual financial statements, including announcements to shareholders and the SGX-ST prior to submission to the Board so as to ensure the integrity of the Company’s financial statements;

d) reviews any significant findings and recommendations of the external and internal auditors and related management response and assistance given by the management to auditors;

e) reviews interested person transactions to ensure that internal control procedures approved by the shareholders are adhered to; and

f) conducts annual review of the independence and objectivity of the external auditors, including the volume of non-audit services provided by the external auditors, to satisfy itself that the nature and extent of such services will not prejudice the independence and objectivity of the external auditors before confirming their re-nomination.

During the year, the AC had reviewed the quarterly and full-year financial statements and, considered both the external and internal audit plans. It also reviewed adequacy of internal control procedures and transactions with Interested Persons. The AC met with both the external and internal auditors, without the presence of management, to obtain feedback on Management’s co-operation during the audit and on other matters or, concerns that warrants the AC’s attention.

CORPORATE GOVERNANCE STATEMENT

KS Energy Services Limited Annual Report 200930

The Company has put in place a Whistle-Blowing Policy for the Group to encourage and to provide a channel for employees of the Group to report and to raise in good faith and in confidence, any concerns about possible improprieties in matters of financial reporting or other matters. The objective of the Whistle-Blowing Policy is to facilitate independent investigation of such matters, and for appropriate follow-up action.

The AC has full authority to commission investigations and review findings into matters when alerted of any suspected fraud, irregularity, failure of internal controls or infringement of any law that may likely to have a material impact on the Group’s operating results.

The AC had reviewed the level of non-audit services performed by the external auditors to ensure that the independence and objectivity of the external auditors are not compromised.

The AC has recommended to the Board the re-appointment of KPMG LLP as auditors for FY2010.

Principle 12: Internal ControlsPrinciple 13: Internal Audit

The Group recognises the importance of the internal audit which, being independent of Management is one of the principal means through which the AC effectively discharges its responsibilities. The internal audit function is outsourced to Messrs BDO Raffles Consultants Pte Ltd (the “IA”), which reports directly to the AC.

The Group maintains a system of internal controls for all companies within the Group, but recognises that no internal control system will preclude all errors and irregularities. The system is designed to manage rather than to eliminate the risk of failure to achieve business objectives. The controls are to provide reasonable, but not absolute, assurance to safeguard shareholders’ investments and the Group’s assets.

The AC and the Board of Directors, with the assistance of internal audit, review the effectiveness of the key internal controls, including financial, operational and compliance controls, and risk management on an on-going basis.

Based on its review, the AC believes that the internal auditor is independent and has the appropriate standing to perform its function effectively. The internal auditor plans its internal audit schedules in consultation with Management and submits its plan to the AC for approval.

As part of the effort to further enhanced the Company’s risk management process, an Enterprise Risk Management (“ERM”) Committee was formed to assist the board in identifying potential events that may affect the entity, and manage risk within its risk appetite and to provide reasonable assurance regarding the achievement of entity objectives.

Remuneration Committee

Principle 7: Procedures for Developing Remuneration PoliciesPrinciple 8: Level and Mix of RemunerationPrinciple 9: Disclosure on Remuneration

The Remuneration Committee comprises the following:

Mr. Lee Beng Cheng (Chairman and Independent Director)Mr. Lim Ho Seng (Lead Independent Director)Mr. Wong Meng Yeng (Independent Director)

The functions of the RC include the following:

a) recommending to the Board base salary level, benefits and incentive programs, and identify components of salary which can best be used to focus management staff on achieving corporate objectives;

CORPORATE GOVERNANCE STATEMENT

KS Energy Services Limited Annual Report 2009 31

b) approving the structure of compensation programme (including but not limited to Directors’ fees, salaries, allowances, bonuses, options and benefits in kind) for the Directors and senior management to ensure that the programme is competitive and sufficient to attract, retain and motivate senior management of the required quality to run the Company successfully; and

c) reviewing, on annual basis, the compensation packages of the Company’s Directors and senior management personnel and determining appropriate adjustments.

The Company’s remuneration package comprises a base/fixed salary component and a variable bonus component that is linked to the Company/Group and individual performances.

Disclosure on Directors’ Remuneration

In setting the remuneration packages of the Executive Directors, the RC takes into account the respective performances of the Group and of the individual. In its deliberation, the RC takes into consideration, remuneration packages and employment conditions within the industry and benchmarked against comparable companies.

Non-Executive Directors are paid a basic fee and an additional fee for serving on any of the committees. The Chairman of each of these committees is compensated for his additional responsibilities that may be assigned to him. Such fees are approved by the shareholders of the Company as a lump sum payment at the AGM of the Company.

The Directors did not participate in any decision concerning their own remuneration.

The breakdown of Directors’ remuneration for FY 2009 is set out below:

Breakdown of the directors’ remuneration

Salary & CPF(%)

Fee(%)

Bonus & CPF(%)

Other Benefits(%)

Total(%)

$500,000 to below $1,000,000

Mr. Kris Tanear Wiluan 73 - 27 - 100

$250,000 to below $500,000

Mr. Woo Peng Kong Note 1 86 - 7 7 100

Mr. Goh Boon Chye Note 2 74 - 16 10 100

Below $250,000

Mr. Koh Soo Keong Note 3 100 - - - 100

Dr. Adam Paul Brunet Note 4 78 - 22 - 100

Mr. Lim Ho Seng - 100 - - 100

Mr. Lee Beng Cheng - 100 - - 100

Mr. Wong Meng Yeng - 100 - - 100

Sheikh Faisal F.J. Al-Thani Note 5 - 100 - - 100

Mr. Abdulla Mohammed Saleh Note 6

(Alternate: Nelson McCallum Gibb)- 100 - - 100

Note 1: Mr. Woo Peng Kong resigned as an Executive Director on 1 May 2009Note 2: Mr. Goh Boon Chye resigned as an Executive Director on 1 May 2009Note 3: Mr. Koh Soo Keong was re-designated as an Executive Director on 1 May 2009Note 4: Dr Adam Paul Brunet retired as Executive Director on 28 April 2009 Note 5: Sheikh Faisal F.J. Al-Thani retired as Independent Director on 28 April 2009Note 6: Mr. Abdulla Mohammed Saleh was appointed on 1 May 2009 (Alternate: Nelson McCallum Gibb was appointed on 22 December 2009)

CORPORATE GOVERNANCE STATEMENT

KS Energy Services Limited Annual Report 200932

The remuneration of the top 5 executives who are not Directors of the Company, falls within the remuneration band of $200,000 to below $500,000

COMMUNICATION WITH SHAREHOLDERS

Principle 14: Communication with ShareholdersPrinciple 15: Greater Shareholder Participation

The Company strives for timeliness and transparency in its disclosures to the shareholders and the public. All information on the Company’s developments and initiatives are first disseminated via SGXNET followed by a news release, where appropriate. The Company currently holds analyst briefing upon the release of its quarterly financial results.

The Company does not practise selective disclosure. Price-sensitive information is first publicly released via SGXNET, either before the Company meets with any group of investors or analysts or simultaneously with such meetings. Results and annual reports are announced or issued within the period prescribed by the SGX-ST.

The Company regularly updates its corporate website at www.ksenergy.com.sg through which shareholders will be able to access information on the Group. The website provides a business profile, corporate announcements, press releases and other information of the Group.

At general meetings of the Company, shareholders are given the opportunity to express their views and ask questions regarding the Company and the Group. The Chairpersons of the Board Committees, external auditors and key management staff are invited to attend the AGMs of the Company.

The Board may from time to time review the provisions of the existing Articles of the Company to ensure they are in line with the good corporate governance practices as recommended by the Code. If the Board thinks fit, it may propose any necessary amendments for shareholders’ approval.

DEALINGS IN SECURITIES

The Company has adopted a policy governing dealings in the securities of the Company for Directors and employees. Directors and employees are prohibited from dealing in the securities of the Company during the period commencing two weeks before the announcement of the Company’s financial statements for the first and third quarter of its financial year, and one month before the announcement of the Company’s half year and full year financial statements, as the case may be, and ending on the date of the announcement of the relevant results.

Directors and employees of the Company are also prohibited from dealing in the securities of the Company whilst in possession of price-sensitive information. The Company issues regular circulars to its Directors, principal officers and relevant officers who have access to unpublished material price-sensitive information to remind them of the aforementioned prohibition and of the requirement to report their dealings in shares of the Company.

MATERIAL CONTRACTS

Other than as disclosed below, there were no other material contracts entered into by the Company and its subsidiaries involving the interest of the CEO, Director or controlling shareholder, which were either subsisting at the end of the financial year or, if not then subsisting, entered into since the end of the previous financial year.

CORPORATE GOVERNANCE STATEMENT

KS Energy Services Limited Annual Report 2009 33

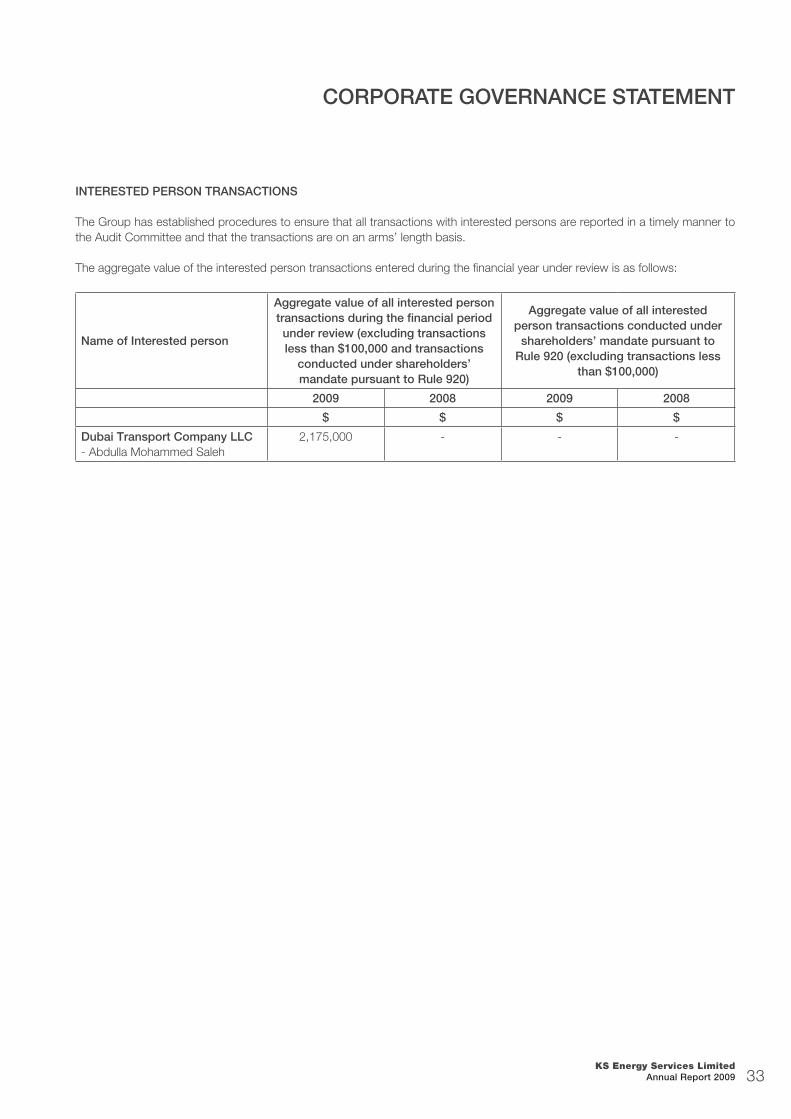

INTERESTED PERSON TRANSACTIONS

The Group has established procedures to ensure that all transactions with interested persons are reported in a timely manner to the Audit Committee and that the transactions are on an arms’ length basis.

The aggregate value of the interested person transactions entered during the financial year under review is as follows:

Name of Interested person

Aggregate value of all interested person transactions during the financial period under review (excluding transactions less than $100,000 and transactions

conducted under shareholders’ mandate pursuant to Rule 920)

Aggregate value of all interested person transactions conducted under

shareholders’ mandate pursuant to Rule 920 (excluding transactions less

than $100,000)

2009 2008 2009 2008

$ $ $ $

Dubai Transport Company LLC- Abdulla Mohammed Saleh

2,175,000 - - -

CORPORATE GOVERNANCE STATEMENT

KS Energy Services Limited Annual Report 200934

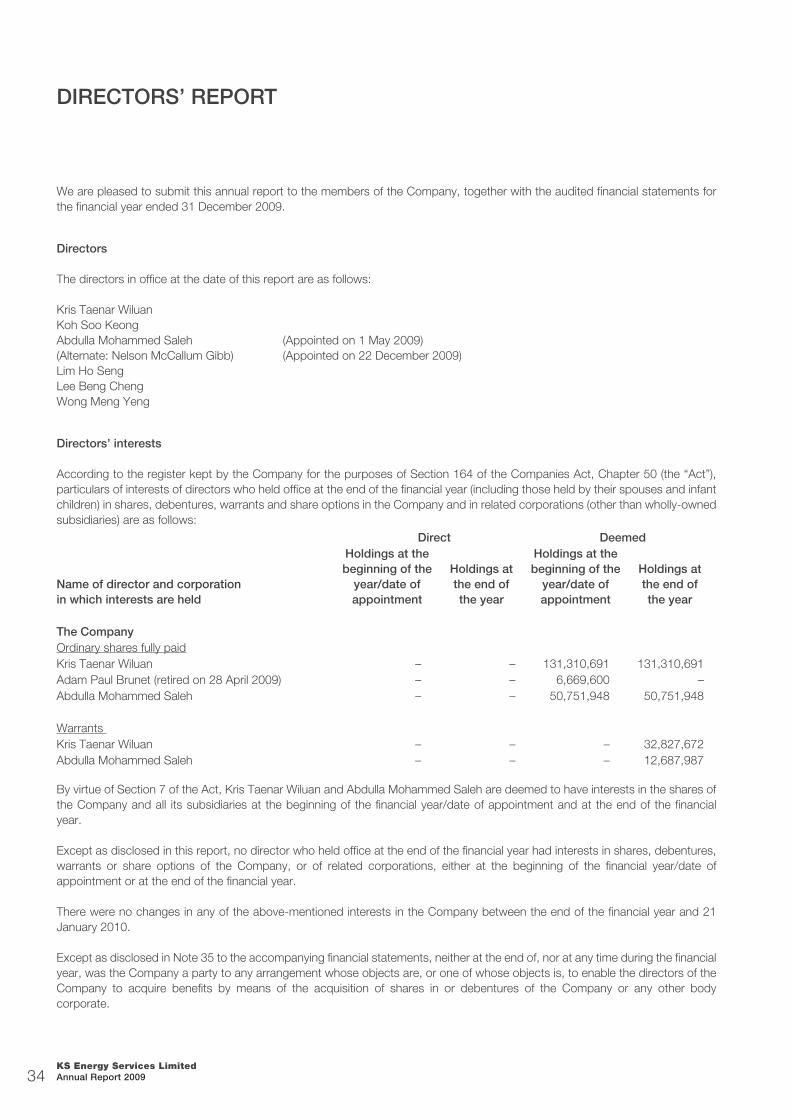

We are pleased to submit this annual report to the members of the Company, together with the audited financial statements for the financial year ended 31 December 2009.

Directors

The directors in office at the date of this report are as follows:

Kris Taenar Wiluan Koh Soo Keong Abdulla Mohammed Saleh (Appointed on 1 May 2009)(Alternate: Nelson McCallum Gibb) (Appointed on 22 December 2009)Lim Ho Seng Lee Beng Cheng Wong Meng Yeng

Directors’ interests

According to the register kept by the Company for the purposes of Section 164 of the Companies Act, Chapter 50 (the “Act”), particulars of interests of directors who held office at the end of the financial year (including those held by their spouses and infant children) in shares, debentures, warrants and share options in the Company and in related corporations (other than wholly-owned subsidiaries) are as follows:

Direct Deemed

Name of director and corporation in which interests are held

Holdings at the beginning of the

year/date of appointment

Holdings at the end ofthe year

Holdings at the beginning of the

year/date of appointment

Holdings at the end ofthe year

The CompanyOrdinary shares fully paidKris Taenar Wiluan – – 131,310,691 131,310,691Adam Paul Brunet (retired on 28 April 2009) – – 6,669,600 –Abdulla Mohammed Saleh – – 50,751,948 50,751,948

Warrants Kris Taenar Wiluan – – – 32,827,672Abdulla Mohammed Saleh – – – 12,687,987

By virtue of Section 7 of the Act, Kris Taenar Wiluan and Abdulla Mohammed Saleh are deemed to have interests in the shares of the Company and all its subsidiaries at the beginning of the financial year/date of appointment and at the end of the financial year.

Except as disclosed in this report, no director who held office at the end of the financial year had interests in shares, debentures, warrants or share options of the Company, or of related corporations, either at the beginning of the financial year/date of appointment or at the end of the financial year.

There were no changes in any of the above-mentioned interests in the Company between the end of the financial year and 21 January 2010.

Except as disclosed in Note 35 to the accompanying financial statements, neither at the end of, nor at any time during the financial year, was the Company a party to any arrangement whose objects are, or one of whose objects is, to enable the directors of the Company to acquire benefits by means of the acquisition of shares in or debentures of the Company or any other body corporate.

DIRECTORS’ REPORT

KS Energy Services Limited Annual Report 2009 35

Directors’ interests (cont’d)

During the financial year, the Company and/or its related corporations have in the normal course of business entered into transactions with parties which are affiliated to the directors, being related parties and parties in which some of the directors are deemed to have an interest, with the directors having disclosed their interests in such transactions pursuant to Section 156 of the Companies Act, Chapter 50. Such transactions may comprise sale and purchase of goods, operating lease arrangements, consultancy services and/or other transactions carried out on normal commercial terms and in the normal course of business of the Company and/or its related corporations. However, the directors have neither received nor become entitled to receive any benefit arising out of these transactions other than those to which they may be entitled as directors and members of these corporations.

Except as disclosed above and in Note 28 to the accompanying financial statements, since the end of the last financial year, no director has received or become entitled to receive a benefit by reason of a contract made by the Company or a related corporation with the director, or with a firm of which he is a member, or with a company in which he has a substantial financial interest.

Share options

The KS Energy Employee Share Option Scheme (the “Scheme”) and KS Energy Performance Share Plan (the “Plan”) was approved at the Company’s Extraordinary General Meeting held on 2 July 2009. The Scheme is administered by the Remuneration Committee (the “Committee”), comprising:

Lee Beng Cheng (Chairman)Wong Meng YengLim Ho Seng

Other information regarding the Scheme is set out below:

(a) Subject to the absolute discretion of the Committee, options may be granted, under the Scheme, to the Group’s employees, executive directors and non-executive directors provided that certain criteria are met. Subject to the absolute discretion of the Committee, Controlling Shareholders and their Associates who meet certain criteria are eligible to participate in the Scheme, provided that the participation of each Controlling Shareholder or his Associate and each grant of an option to any of them may only be effected with the specific prior approval of Shareholders in general meeting by a separate resolution.

(b) The aggregate number of ordinary shares over which options may be granted on any date under the Scheme, when added

to the number of ordinary shares issued and/or issuable in respect of:

all options granted under the Scheme;

all contingent award of ordinary shares granted pursuant to the rules of the Plan; and

all ordinary shares in the capital of the Company, options or awards granted under any other share option or share scheme of the Company then in force;

shall not exceed 15% of the total number of issued ordinary shares, excluding treasury shares, in the capital of the Company on the day preceding the relevant date of grant. Furthermore, the aggregate number of ordinary shares over which options may be granted under the Scheme to Controlling Shareholders and their Associates shall not exceed 25% of the ordinary shares available under the Scheme, and the number of ordinary shares over which options may be granted under the Scheme to each Controlling Shareholder or his Associate shall not exceed 10% of the ordinary shares available under the Scheme.

(c) The Scheme shall continue to be in force at the discretion of the Committee, subject to a maximum period of ten years commencing on the date on which the Scheme is adopted by shareholders of the Company in general meeting, provided that the Scheme may continue beyond the aforesaid period of time with the approval of shareholders of the Company in general meeting and of any relevant authority which may then be required.

DIRECTORS’ REPORT

KS Energy Services Limited Annual Report 200936

Share options (cont’d)

(d) The subscription price of the options shall be fixed by the Committee at its absolute discretion at:

the Market Price, determined by reference to the price equal to the average of the last dealt prices for a Share, as determined by reference to the daily official list or other publication published by the SGX-ST for five consecutive market days immediately preceding the offer date of that option, rounded up to the nearest whole cent in the event of fractional prices;

or at a discount to the Market Price, the quantum of such discount to be determined by the Committee at its absolute discretion, provided that the maximum discount shall not exceed 20% of the Market Price and is approved by shareholders of the Company in general meeting in a separate resolution.

(e) Options granted with the Exercise Price set at the Market Price may be exercised at any time after the first anniversary of the date of grant, provided that the option shall be exercised before the tenth anniversary of the date of grant or such earlier date as may be determined by the Committee, failing which the unexercised option shall immediately be null and void.