allcargo global - visit note-cy11e introduced -centrum-241109

9

INDIA Allcargo Global Logistics Visit Note/CY11E introduced 24 Nov 2009 Logistics Y/E Dec (Rsmn) Rev YoY (%) EBITDA EBITDA (%) Adj PAT YoY (%) DEPS (Rs) RoE (%) RoCE (%) P/E (x) EV/EBITDA (x) CY07 16,135 80.2 1,424 8.8 766 26.9 6.1 17.7 15.9 30.8 17.0 CY08 23,141 43.4 2,201 9.5 1,077 40.7 8.6 19.9 16.1 21.9 11.8 CY09E 21,137 (8.7) 2,488 11.8 1,446 34.3 11.6 18.6 15.4 16.3 9.5 CY10E 25,138 18.9 3,106 12.4 1,798 24.3 14.4 17.7 15.2 13.1 7.4 CY11E 28,736 14.3 3,810 13.3 2,305 28.2 18.5 19.5 17.3 10.2 5.8 Source: Company, Centrum Research Estimates Buy Target Price: Rs235 CMP: Rs189* Upside: 24% *as on 23 November 2009 Siddhartha Khemka [email protected] +91 22 4215 9857 Mahantesh Sabarad [email protected] +91 22 4215 9855 On firm ground We met the Group CFO, Mr. S Suryanarayanan of Allcargo Global Logistics to get an update on the company’s growth strategy. We remain positive on the company’s prospects on expected global trade recovery in 2010-11. We have introduced CY11E and estimate an EPS of Rs18.5. Reiterate Buy with a higher target price of Rs235 (earlier Rs190) valuing the stock at 13x (earlier 12x) one-year forward earnings, to factor in the improved financial health. Valuation upgrade on robust financial health: We reiterate Buy with a higher target price of Rs235 (earlier Rs190), upgrading the company’s valuations to 13x (earlier 12x) one-year forward earnings. Expected recovery in global trade and improved financials justify our upgrade. We expect RoCE to improve to 17.3% in CY11E from 15.5% in CY09E. The debt-equity ratio is estimated to reduce to 0.1x from 0.3x expected at the end of CY09E. Blackstone deal complete: Blackstone converted its warrants into 1.5mn equity shares (face value of Rs10), which matured in Sept-09 at Rs934 per share (Rs186.8 ex-split), infusing Rs1.4bn into the company. The FCCDs (fully and compulsorily convertible debentures) were also converted into 1.08mn equity shares at Rs934/share. Expansion of ICDs underway: The expansion of its CFS/ICD (container freight station/inland container depot) network is now underway with the Indore ICD already commencing operations. The Dadri ICD in JV with Concor is likely to be operational by Q2CY10. The ICDs at Nagpur, Hyderabad and Bangalore in JV with Hind Terminals will likely be ready by end CY10. Backward integration into 3PL warehousing: Allcargo has added another link in its value chain through third party logistics (3PL) services. This will enable it to offer services like freight forwarding, custom clearance, transportation, warehousing and distribution. The warehouses in Mumbai and Goa are already operational and it plans to add facilities in Indore, Hyderabad, Nagpur and Bangalore. Key Data Bloomberg Code AGLL IN Reuters Code ALGL.BO Current Shares O/S (mn) 117.2 Diluted Shares O/S(mn) 124.8 Mkt Cap (Rsbn/USDmn) 22.1/475.1 52 Wk H / L (Rs) 196/78 Daily Vol. (3M NSE Avg.) 10,853 Face Value (Rs) 2 1 USD = Rs46.6 Shareholding Pattern Foreign, 17.9 Institutions, 1.2 Non Promoter Corp. Hold., 1.0 Promoters, 77.7 Public & Others, 2.1 As on 30 September 2009 One Year Indexed Stock Performance 0 25 50 75 100 125 150 175 200 225 Nov-08 Jan-09 Mar-09 May-09 Jul-09 Sep-09 Nov-09 AL LCARGO GLOB AL NS E S&P CNX N IFTY IN DEX Price Performance (%) 1M 6M 1Yr Allcargo 12.0 16.8 101.3 NIFTY 2.1 20.4 88.4 Source: Bloomberg , Centrum Research *as on 23 November 2009 Please refer to important disclosures/disclaimers insi de

-

Upload

zeenat-kerawala -

Category

Documents

-

view

216 -

download

0

Transcript of allcargo global - visit note-cy11e introduced -centrum-241109

8/7/2019 allcargo global - visit note-cy11e introduced -centrum-241109

http://slidepdf.com/reader/full/allcargo-global-visit-note-cy11e-introduced-centrum-241109 1/8

INDIA

Allcargo Global Logistics

Visit Note/CY11E introduced 24 Nov 2009

Logistics

Y/E Dec (Rsmn) Rev YoY (%) EBITDA EBITDA (%) Adj PAT YoY (%) DEPS (Rs) RoE (%) RoCE (%) P/E (x) EV/EBITDA

CY07 16,135 80.2 1,424 8.8 766 26.9 6.1 17.7 15.9 30.8 1

CY08 23,141 43.4 2,201 9.5 1,077 40.7 8.6 19.9 16.1 21.9 1

CY09E 21,137 (8.7) 2,488 11.8 1,446 34.3 11.6 18.6 15.4 16.3

CY10E 25,138 18.9 3,106 12.4 1,798 24.3 14.4 17.7 15.2 13.1

CY11E 28,736 14.3 3,810 13.3 2,305 28.2 18.5 19.5 17.3 10.2

Source: Company, Centrum Research Estimates

Buy

Target Price: Rs235

CMP: Rs189*Upside: 24%

*as on 23 November 2009

Siddhartha [email protected]+91 22 4215 9857

Mahantesh Sabarad

[email protected]+91 22 4215 9855

On firm ground

We met the Group CFO, Mr. S Suryanarayanan of Allcargo Global Logistics to get an update on thecompany’s growth strategy. We remain positive on thecompany’s prospects on expected global traderecovery in 2010-11. We have introduced CY11E andestimate an EPS of Rs18.5. Reiterate Buy with a highertarget price of Rs235 (earlier Rs190) valuing the stock at 13x (earlier 12x) one-year forward earnings, tofactor in the improved financial health.

Valuation upgrade on robust financial health: Wereiterate Buy with a higher target price of Rs235(earlier Rs190), upgrading the company’s valuationsto 13x (earlier 12x) one-year forward earnings.

Expected recovery in global trade and improvedfinancials justify our upgrade. We expect RoCE toimprove to 17.3% in CY11E from 15.5% in CY09E. Thedebt-equity ratio is estimated to reduce to 0.1x from0.3x expected at the end of CY09E.

Blackstone deal complete: Blackstone converted itswarrants into 1.5mn equity shares (face value of Rs10), which matured in Sept-09 at Rs934 per share(Rs186.8 ex-split), infusing Rs1.4bn into the company.

The FCCDs (fully and compulsorily convertibledebentures) were also converted into 1.08mn equityshares at Rs934/share.

Expansion of ICDs underway: The expansion of its

CFS/ICD (container freight station/inland containerdepot) network is now underway with the Indore ICDalready commencing operations. The Dadri ICD in JVwith Concor is likely to be operational by Q2CY10.

The ICDs at Nagpur, Hyderabad and Bangalore in JVwith Hind Terminals will likely be ready by end CY10.

Backward integration into 3PL warehousing: Allcargo has added another link in its value chainthrough third party logistics (3PL) services. This willenable it to offer services like freight forwarding,custom clearance, transportation, warehousing anddistribution. The warehouses in Mumbai and Goa arealready operational and it plans to add facilities in

Indore, Hyderabad, Nagpur and Bangalore.

Key Data

Bloomberg Code AGLL

Reuters Code ALGL.Current Shares O/S (mn) 11

Diluted Shares O/S(mn) 12

Mkt Cap (Rsbn/USDmn) 22.1/47

52 Wk H / L (Rs) 196

Daily Vol. (3M NSE Avg.) 10,8

Face Value (Rs)

1 USD = Rs46.6

Shareholding Pattern

Foreign, 17.9

Institutions, 1.2

Non PromoterCorp. Hold., 1.0

Promoters, 77.7

Public &

Others, 2.1

As on 30 September 2009

One Year Indexed Stock Performance

0

25

5075

100

125

150

175

200

225

Nov-08 Jan-09 Mar-09 May-09 Jul-09 Sep-09 Nov-09

A LLC ARGO GLOB AL N SE S& P C NX N IFTY IN DEX

Price Performance (%)

1M 6M 1Y

Allcargo 12.0 16.8 101

NIFTY 2.1 20.4 88

Source: Bloomberg , Centrum Research *as on 23 November 2009

Please refer to important disclosures/disclaimers inside

8/7/2019 allcargo global - visit note-cy11e introduced -centrum-241109

http://slidepdf.com/reader/full/allcargo-global-visit-note-cy11e-introduced-centrum-241109 2/8

2 Allcargo Global Logisti

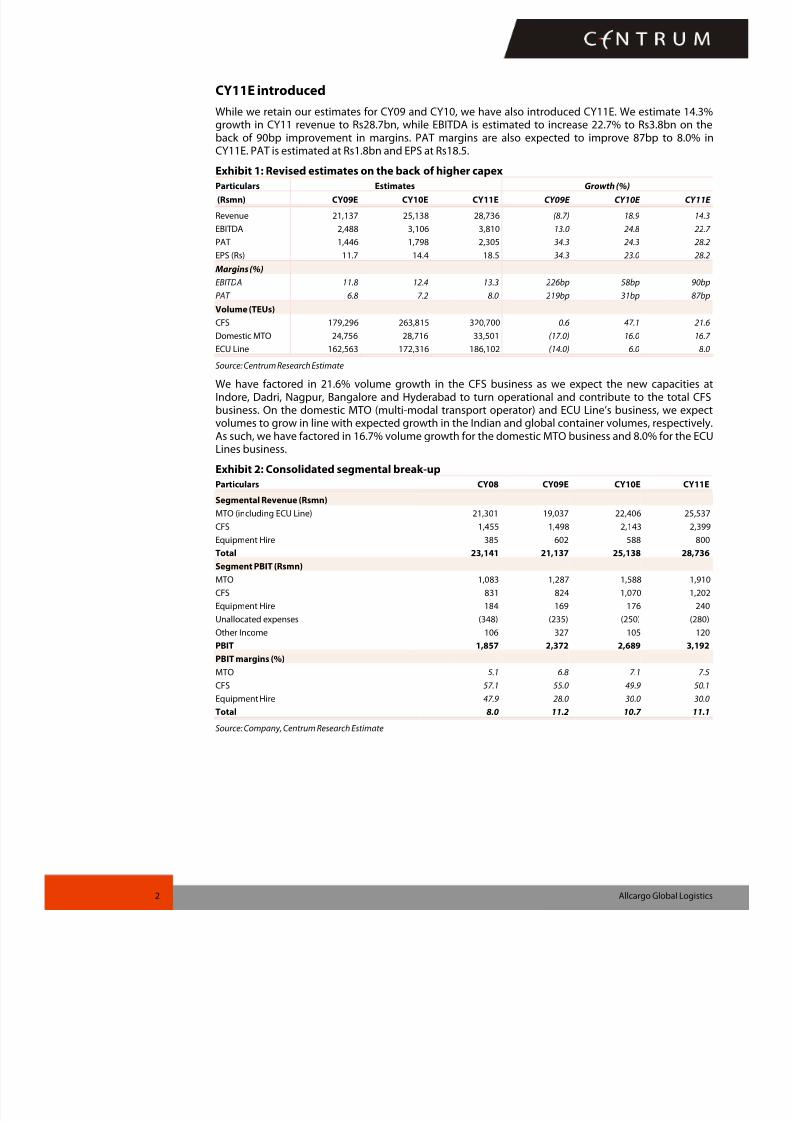

CY11E introduced

While we retain our estimates for CY09 and CY10, we have also introduced CY11E. We estimate 14.3growth in CY11 revenue to Rs28.7bn, while EBITDA is estimated to increase 22.7% to Rs3.8bn on thback of 90bp improvement in margins. PAT margins are also expected to improve 87bp to 8.0% CY11E. PAT is estimated at Rs1.8bn and EPS at Rs18.5.

Exhibit 1: Revised estimates on the back of higher capexParticulars Estimates Growth (%)

(Rsmn) CY09E CY10E CY11E CY09E CY10E CY11

Revenue 21,137 25,138 28,736 (8.7) 18.9 14.

EBITDA 2,488 3,106 3,810 13.0 24.8 22.

PAT 1,446 1,798 2,305 34.3 24.3 28.

EPS (Rs) 11.7 14.4 18.5 34.3 23.0 28.

Margins (%)

EBITDA 11.8 12.4 13.3 226bp 58bp 90b

PAT 6.8 7.2 8.0 219bp 31bp 87b

Volume (TEUs)

CFS 179,296 263,815 320,700 0.6 47.1 21.

Domestic MTO 24,756 28,716 33,501 (17.0) 16.0 16.

ECU Line 162,563 172,316 186,102 (14.0) 6.0 8Source: Centrum Research Estimate

We have factored in 21.6% volume growth in the CFS business as we expect the new capacities Indore, Dadri, Nagpur, Bangalore and Hyderabad to turn operational and contribute to the total CFbusiness. On the domestic MTO (multi-modal transport operator) and ECU Line’s business, we expecvolumes to grow in line with expected growth in the Indian and global container volumes, respectivelAs such, we have factored in 16.7% volume growth for the domestic MTO business and 8.0% for the ECLines business.

Exhibit 2: Consolidated segmental break-up

Particulars CY08 CY09E CY10E CY11

Segmental Revenue (Rsmn)

MTO (including ECU Line) 21,301 19,037 22,406 25,53

CFS 1,455 1,498 2,143 2,39Equipment Hire 385 602 588 80

Total 23,141 21,137 25,138 28,73

Segment PBIT (Rsmn)

MTO 1,083 1,287 1,588 1,91

CFS 831 824 1,070 1,20

Equipment Hire 184 169 176 24

Unallocated expenses (348) (235) (250) (280

Other Income 106 327 105 12

PBIT 1,857 2,372 2,689 3,19

PBIT margins (%)

MTO 5.1 6.8 7.1 7.

CFS 57.1 55.0 49.9 50.

Equipment Hire 47.9 28.0 30.0 30.Total 8.0 11.2 10.7 11.

Source: Company, Centrum Research Estimate

8/7/2019 allcargo global - visit note-cy11e introduced -centrum-241109

http://slidepdf.com/reader/full/allcargo-global-visit-note-cy11e-introduced-centrum-241109 3/8

3 Allcargo Global Logisti

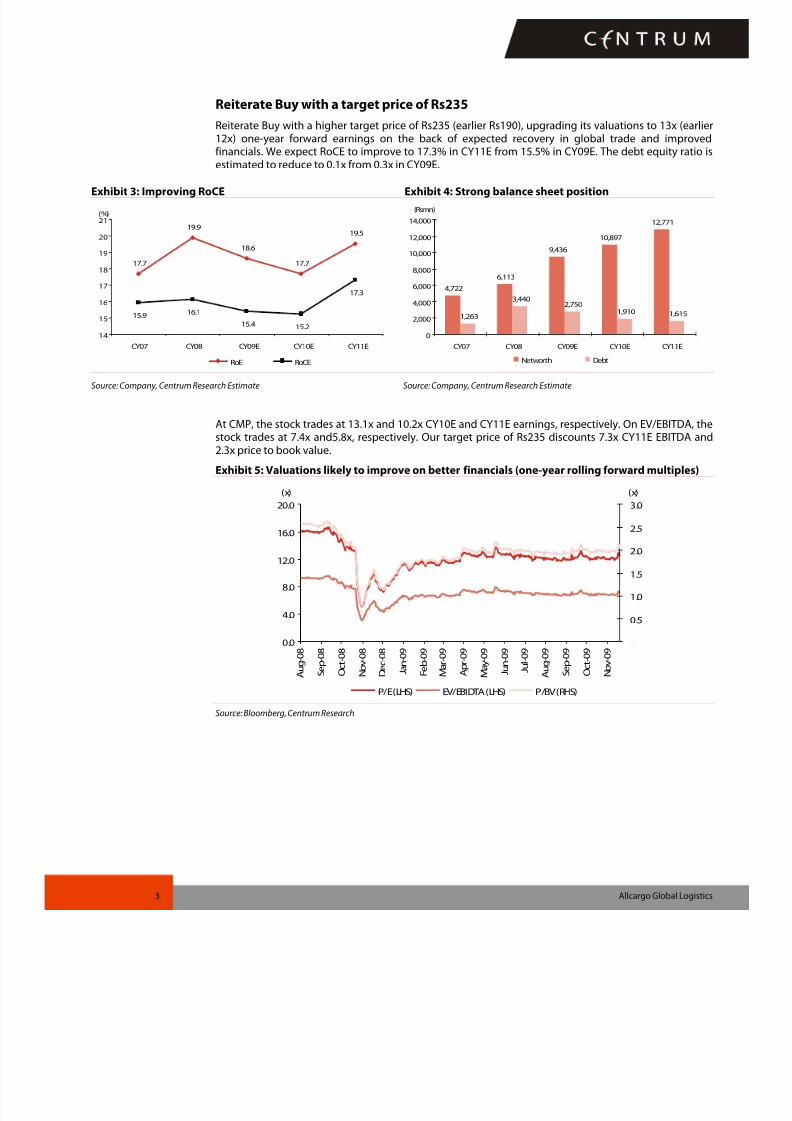

Reiterate Buy with a target price of Rs235

Reiterate Buy with a higher target price of Rs235 (earlier Rs190), upgrading its valuations to 13x (earli12x) one-year forward earnings on the back of expected recovery in global trade and improvefinancials. We expect RoCE to improve to 17.3% in CY11E from 15.5% in CY09E. The debt equity ratio estimated to reduce to 0.1x from 0.3x in CY09E.

Exhibit 3: Improving RoCE Exhibit 4: Strong balance sheet position

17.7

19.9

18.6

17.7

19.5

15.916.1

15.4 15.2

17.3

14

15

16

17

18

19

20

21

CY07 CY08 CY09E CY10E CY11E

(%)

RoE RoCE

4,722

6,113

9,436

10,897

12,771

1,263

3,4402,750

1,910 1,615

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

CY07 CY08 CY09E CY10E CY11E

(Rsmn)

Networth Debt

Source: Company, Centrum Research Estimate Source: Company, Centrum Research Estimate

At CMP, the stock trades at 13.1x and 10.2x CY10E and CY11E earnings, respectively. On EV/EBITDA, thstock trades at 7.4x and5.8x, respectively. Our target price of Rs235 discounts 7.3x CY11E EBITDA an2.3x price to book value.

Exhibit 5: Valuations likely to improve on better financials (one-year rolling forward multiples)

(x)

0.0

4.0

8.0

12.0

16.0

20.0

A u g - 0 8

S e p - 0 8

O c t - 0 8

N o v - 0 8

D e c - 0 8

J a n - 0 9

F e b - 0 9

M a r - 0 9

A p r - 0 9

M a y - 0 9

J u n - 0 9

J u l - 0 9

A u g - 0 9

S e p - 0 9

O c t - 0 9

N o v - 0 9

(x)

-

0.5

1.0

1.5

2.0

2.5

3.0

P/E (LHS) EV/EBIDTA (LHS) P/BV (RHS)

Source: Bloomberg, Centrum Research

8/7/2019 allcargo global - visit note-cy11e introduced -centrum-241109

http://slidepdf.com/reader/full/allcargo-global-visit-note-cy11e-introduced-centrum-241109 4/8

4 Allcargo Global Logisti

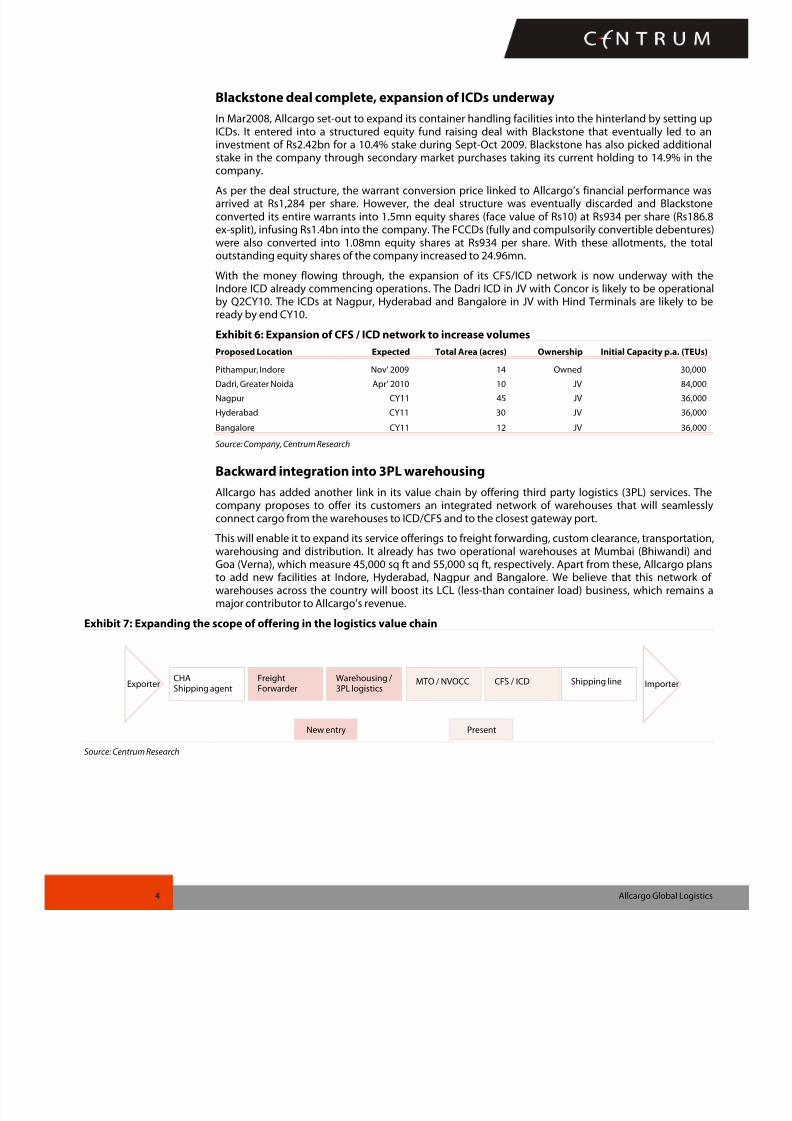

Blackstone deal complete, expansion of ICDs underway

In Mar2008, Allcargo set-out to expand its container handling facilities into the hinterland by setting uICDs. It entered into a structured equity fund raising deal with Blackstone that eventually led to ainvestment of Rs2.42bn for a 10.4% stake during Sept-Oct 2009. Blackstone has also picked additionstake in the company through secondary market purchases taking its current holding to 14.9% in th

company.As per the deal structure, the warrant conversion price linked to Allcargo’s financial performance waarrived at Rs1,284 per share. However, the deal structure was eventually discarded and Blackstonconverted its entire warrants into 1.5mn equity shares (face value of Rs10) at Rs934 per share (Rs186ex-split), infusing Rs1.4bn into the company. The FCCDs (fully and compulsorily convertible debenturewere also converted into 1.08mn equity shares at Rs934 per share. With these allotments, the totoutstanding equity shares of the company increased to 24.96mn.

With the money flowing through, the expansion of its CFS/ICD network is now underway with thIndore ICD already commencing operations. The Dadri ICD in JV with Concor is likely to be operationby Q2CY10. The ICDs at Nagpur, Hyderabad and Bangalore in JV with Hind Terminals are likely to bready by end CY10.

Exhibit 6: Expansion of CFS / ICD network to increase volumes

Proposed Location Expected Total Area (acres) Ownership Initial Capacity p.a. (TEUs

Pithampur, Indore Nov' 2009 14 Owned 30,000

Dadri, Greater Noida Apr' 2010 10 JV 84,000

Nagpur CY11 45 JV 36,000

Hyderabad CY11 30 JV 36,000

Bangalore CY11 12 JV 36,000

Source: Company, Centrum Research

Backward integration into 3PL warehousing

Allcargo has added another link in its value chain by offering third party logistics (3PL) services. Thcompany proposes to offer its customers an integrated network of warehouses that will seamlessconnect cargo from the warehouses to ICD/CFS and to the closest gateway port.

This will enable it to expand its service offerings to freight forwarding, custom clearance, transportatiowarehousing and distribution. It already has two operational warehouses at Mumbai (Bhiwandi) anGoa (Verna), which measure 45,000 sq ft and 55,000 sq ft, respectively. Apart from these, Allcargo planto add new facilities at Indore, Hyderabad, Nagpur and Bangalore. We believe that this network owarehouses across the country will boost its LCL (less-than container load) business, which remains major contributor to Allcargo’s revenue.

Exhibit 7: Expanding the scope of offering in the logistics value chain

Source: Centrum Research

ExporterCHAShipping agent

FreightForwarder

Warehousing /3PL logistics

CFS / ICD Shipping line ImporterMTO / NVOCC

New entry Present

8/7/2019 allcargo global - visit note-cy11e introduced -centrum-241109

http://slidepdf.com/reader/full/allcargo-global-visit-note-cy11e-introduced-centrum-241109 5/8

5 Allcargo Global Logisti

Volume recovery on the cards

We estimate Allcargo’s revenues to grow 14.3% in CY11E on the back of sustained volume growth in aits key businesses. The CFS business is estimated to register 21.6% growth in volumes on the back onew capacities. The domestic MTO and ECU Line’s businesses will likely witness 16.7% and 8.0% growtin volumes, respectively.

Global container shipping volumes are expected to see a recovery during 2010 and 2011, as the tradbetween countries improves. The International Monetary Fund (IMF) has upgraded global GDP growtforecast by 60bp to 2.5% for 2010, prompted by improved economic conditions. We expect India's EXItrade to benefit from the gradual recovery in industrial activity of its key trading partners, China, UGermany and Singapore.

We estimate India’s EXIM container volumes to grow 4.0% in FY10E to 7.1mn TEUs and 8.4% in FY11E t7.7mn TEUs.

Exhibit 8: ECU Line emerging stronger Exhibit 9: Buoyancy in CFS throughput

ECU Line

189,000

162,563

172,316

186,102

150,000

160,000

170,000

180,000

190,000

200,000

CY08 CY09E CY10E CY11E

(TEUs)

CFS Business

127,434

178,188 179,296

263,815

320,700

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

CY07 CY08 CY09E CY10E CY11E

(TEUs)

Source: Company, Centrum Research Estimate Source: Company, Centrum Research Estimate

8/7/2019 allcargo global - visit note-cy11e introduced -centrum-241109

http://slidepdf.com/reader/full/allcargo-global-visit-note-cy11e-introduced-centrum-241109 6/8

6 Allcargo Global Logisti

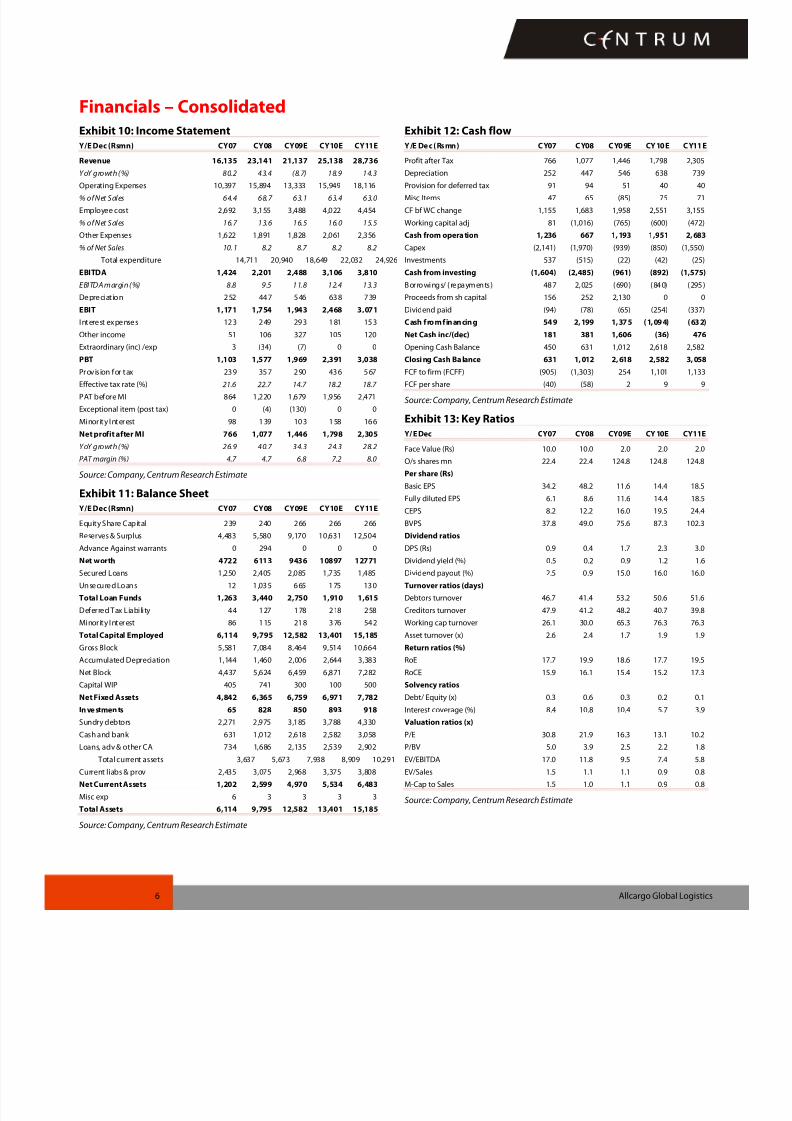

Financials – Consolidated

Exhibit 10: Income Statement

Y/E Dec (Rsmn) CY07 CY08 CY09E CY10E CY11E

Revenue 16,135 23,141 21,137 25,138 28,736

YoY growth (%) 80.2 43.4 (8.7) 18.9 14.3Operating Expenses 10,397 15,894 13,333 15,949 18,116

% of Net Sales 64.4 68.7 63.1 63.4 63.0

Employee cost 2,692 3,155 3,488 4,022 4,454

% of Net Sales 16.7 13.6 16.5 16.0 15.5

Other Expenses 1,622 1,891 1,828 2,061 2,356

% of Net Sales 10. 1 8.2 8.7 8.2 8.2

Total expenditure 14,711 20,940 18,649 22,032 24,926

EBITDA 1,424 2,201 2,488 3,106 3,810

EBITDA margin (%) 8.8 9.5 11.8 12.4 13.3

Depreciat ion 252 447 546 638 739

EBIT 1,171 1,754 1,943 2,468 3,071

Interest expenses 123 249 293 181 153

Other income 51 106 327 105 120

Extraordinary (inc) /exp 3 (34) (7) 0 0

PBT 1,103 1,577 1,969 2,391 3,038

Provis ion for tax 239 357 290 436 567

Effective tax rate (%) 21.6 22.7 14.7 18.2 18.7

PAT before MI 864 1,220 1,679 1,956 2,471

Exceptional item (post tax) 0 (4) (130) 0 0

Minority Interest 98 139 103 158 166

Net profit after MI 766 1,077 1,446 1,798 2,305

YoY growth (%) 26.9 40.7 34.3 24.3 28.2

PAT margin (%) 4.7 4.7 6.8 7.2 8.0

Source: Company, Centrum Research Estimate

Exhibit 11: Balance Sheet

Y/E Dec (Rsmn) CY07 CY08 CY09E CY10E CY11E

Equity Share Capital 239 240 266 266 266Reserves & Surplus 4,483 5,580 9,170 10,631 12,504

Advance Against warrants 0 294 0 0 0

Net worth 4722 6113 9436 10897 12771

Secured Loans 1,250 2,405 2,085 1,735 1,485

Unsecured Loans 12 1 ,035 665 175 130

Total Loan Funds 1,263 3,440 2,750 1,910 1,615

Deferred Tax Liability 44 127 178 218 258

Minority Interest 86 115 218 376 542

Total Capital Employed 6,114 9,795 12,582 13,401 15,185

Gross Block 5,581 7,084 8,464 9,514 10,664

Accumulated Depreciation 1,144 1,460 2,006 2,644 3,383

Net Block 4,437 5,624 6,459 6,871 7,282

Capital WIP 405 741 300 100 500

Net Fixed Assets 4,842 6,365 6,759 6,971 7,782

In ve stmen ts 65 828 850 893 918

Sundry debtors 2,271 2,975 3,185 3,788 4,330

Cash and bank 631 1,012 2,618 2,582 3,058

Loans, adv & other CA 734 1,686 2,135 2,539 2,902

Total current assets 3,637 5,673 7,938 8,909 10,291

Current liabs & prov 2,435 3,075 2,968 3,375 3,808

Net Current Assets 1,202 2,599 4,970 5,534 6,483

Misc exp 6 3 3 3 3

Total Assets 6,114 9,795 12,582 13,401 15,185

Source: Company, Centrum Research Estimate

Exhibit 12: Cash flow

Y/E Dec (Rs mn) CY07 CY08 CY09E CY10E CY11E

Profit after Tax 766 1,077 1,446 1,798 2,305

Depreciation 252 447 546 638 739Provision for deferred tax 91 94 51 40 40

Misc Items 47 65 (85) 75 71

CF bf WC change 1,155 1,683 1,958 2,551 3,155

Working capital adj 81 (1,016) (765) (600) (472)

Cash from opera tion 1, 236 667 1, 193 1,951 2, 683

Capex (2,141) (1,970) (939) (850) (1,550)

Investments 537 (515) (22) (42) (25)

Cash from investing (1,604) (2,485) (961) (892) (1,575)

Borrowings/ ( repayments) 487 2,025 (690) (840) (295

Proceeds from sh capital 156 252 2,130 0 0

Dividend paid (94) (78) (65) (254) (337)

Cash f rom f inancing 549 2, 199 1, 375 (1, 094) (632

Net Cash inc/(dec) 181 381 1,606 (36) 476

Opening Cash Balance 450 631 1,012 2,618 2,582Closi ng Cash Ba lance 631 1, 012 2, 618 2,582 3, 058

FCF to firm (FCFF) (905) (1,303) 254 1,101 1,133

FCF per share (40) (58) 2 9 9

Source: Company, Centrum Research Estimate

Exhibit 13: Key Ratios

Y/ E Dec CY07 CY08 CY09E CY 10E CY11E

Face Value (Rs) 10.0 10.0 2.0 2.0 2.0

O/s shares mn 22.4 22.4 124.8 124.8 124.8

Per share (Rs)

Basic EPS 34.2 48.2 11.6 14.4 18.5

Fully diluted EPS 6.1 8.6 11.6 14.4 18.5

CEPS 8.2 12.2 16.0 19.5 24.4

BVPS 37.8 49.0 75.6 87.3 102.3Dividend ratios

DPS (Rs) 0.9 0.4 1.7 2.3 3.0

Dividend yield (%) 0.5 0.2 0.9 1.2 1.6

Dividend payout (%) 2.5 0.9 15.0 16.0 16.0

Turnover ratios (days)

Debtors turnover 46.7 41.4 53.2 50.6 51.6

Creditors turnover 47.9 41.2 48.2 40.7 39.8

Working cap turnover 26.1 30.0 65.3 76.3 76.3

Asset turnover (x) 2.6 2.4 1.7 1.9 1.9

Return ratios (%)

RoE 17.7 19.9 18.6 17.7 19.5

RoCE 15.9 16.1 15.4 15.2 17.3

Solvency ratios

Debt/ Equity (x) 0.3 0.6 0.3 0.2 0.1

Interest coverage (%) 8.4 10.8 10.4 5.7 3.9

Valuation ratios (x)

P/E 30.8 21.9 16.3 13.1 10.2

P/BV 5.0 3.9 2.5 2.2 1.8

EV/EBITDA 17.0 11.8 9.5 7.4 5.8

EV/Sales 1.5 1.1 1.1 0.9 0.8

M-Cap to Sales 1.5 1.0 1.1 0.9 0.8

Source: Company, Centrum Research Estimate

8/7/2019 allcargo global - visit note-cy11e introduced -centrum-241109

http://slidepdf.com/reader/full/allcargo-global-visit-note-cy11e-introduced-centrum-241109 7/8

7 Allcargo Global Logisti

Disclaimer

Centrum Broking Pvt. Ltd.(“Centrum”) is a full-service, Stock Broking Company and a member of The Stock Exchange, Mumbai (BSE) and National Stock Exchange of India Ltd. (NSE). Oholding company, Centrum Capital Ltd, is an investment banker and an underwriter of securities. As a group Centrum has Investment Banking, Advisory and other business relationships witsignificant percentage of the companies covered by our Research Group. Our research professionals provide important inputs into the Group's Investment Banking and other busineselection processes.

Recipients of this report should assume that our Group is seeking or may seek or will seek Investment Banking, advisory, project finance or other businesses and may receive commissiobrokerage, fees or other compensation from the company or companies that are the subject of this material/report. Our Company and Group companies and their officers, directors aemployees, including the analysts and others involved in the preparation or issuance of this material and their dependants, may on the date of this report or from, time to time have "long"

"short" positions in, act as principal in, and buy or sell the securities or derivatives thereof of companies mentioned herein. Centrum or its affiliates may be owning 1% or more in the equity this company Our sales people, dealers, traders and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions that acontrary to the opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that are inconsistent with the recommendations expresseherein. We may have earlier issued or may issue in future reports on the companies covered herein with recommendations/ information inconsistent or different those made in this report. reviewing this document, you should be aware that any or all of the foregoing, among other things, may give rise to or potential conflicts of interest. We and our Group may rely information barriers, such as "Chinese Walls" to control the flow of information contained in one or more areas within us, or other areas, units, groups or affiliates of Centrum.

This report is for information purposes only and this document/material should not be construed as an offer to sell or the solicitation of an offer to buy, purchase or subscribe to any securitiand neither this document nor anything contained herein shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. This document does not solany action based on the material contained herein. It is for the general information of the clients of Centrum. Though disseminated to clients simultaneously, not all clients may receive threport at the same time. Centrum will not treat recipients as clients by virtue of their receiving this report. It does not constitute a personal recommendation or take into account the particuinvestment objectives, financial situations, or needs of individual clients. Similarly, this document does not have regard to the specific investment objectives, financial situation/circumstancand the particular needs of any specific person who may receive this document. The securities discussed in this report may not be suitable for all investors. The securities described herein mnot be eligible for sale in all jurisdictions or to all categories of investors. The countries in which the companies mentioned in this report are organized may have restrictions on investmentvoting rights or dealings in securities by nationals of other countries. The appropriateness of a particular investment or strategy will depend on an investor's individual circumstances aobjectives. Persons who may receive this document should consider and independently evaluate whether it is suitable for his/ her/their particular circumstances and, if necessary, seeprofessional/financial advice. Any such person shall be responsible for conducting his/her/their own investigation and analysis of the information contained or referred to in this document aof evaluating the merits and risks involved in the securities forming the subject matter of this document.

The projections and forecasts described in this report were based upon a number of estimates and assumptions and are inherently subject to significant uncertainties and contingenci

Projections and forecasts are necessarily speculative in nature, and it can be expected that one or more of the estimates on which the projections and forecasts were based will not materialior will vary significantly from actual results, and such variances will likely increase over time. All projections and forecasts described in this report have been prepared solely by the authors othis report independently of the Company. These projections and forecasts were not prepared with a view toward compliance with published guidelines or generally accented accountiprinciples. No independent accountants have expressed an opinion or any other form of assurance on these projections or forecasts. You should not regard the inclusion of the projections aforecasts described herein as a representation or warranty by or on behalf of the Company, Centrum, the authors of this report or any other person that these projections or forecasts or theunderlying assumptions will be achieved. For these reasons, you should only consider the projections and forecasts described in this report after carefully evaluating all of the informationthis report, including the assumptions underlying such projections and forecasts.

The price and value of the investments referred to in this document/material and the income from them may go down as well as up, and investors may realize losses on any investments. Paperformance is not a guide for future performance. Future returns are not guaranteed and a loss of original capital may occur. Actual results may differ materially from those set forth iprojections. Forward-looking statements are not predictions and may be subject to change without notice. Centrum does not provide tax advice to its clients, and all investors are strongadvised to consult regarding any potential investment. Centrum and its affiliates accept no liabilities for any loss or damage of any kind arising out of the use of this report. Foreign currencdenominated securities are subject to fluctuations in exchange rates that could have an adverse effect on the value or price of or income derived from the investment. In addition, investorssecurities such as ADRs, the value of which are influenced by foreign currencies effectively assume currency risk. Certain transactions including those involving futures, options, and othederivatives as well as non-investment-grade securities give rise to substantial risk and are not suitable for all investors. Please ensure that you have read and understood the current rdisclosure documents before entering into any derivative transactions.

This report/document has been prepared by Centrum, based upon information available to the public and sources, believed to be reliable. No representation or warranty, express or impliedmade that it is accurate or complete. Centrum has reviewed the report and, in so far as it includes current or historical information, it is believed to be reliable, although its accuracy acompleteness cannot be guaranteed. The opinions expressed in this document/material are subject to change without notice and have no obligation to tell you when opinions or informati

in this report change.This report or recommendations or information contained herein do/does not constitute or purport to constitute investment advice in publicly accessible media and should not breproduced, transmitted or published by the recipient. The report is for the use and consumption of the recipient only. This publication may not be distributed to the public used by the pubmedia without the express written consent of Centrum. This report or any portion hereof may not be printed, sold or distributed without the written consent of Centrum.

This report has not been prepared by Centrum Securities LLC. However, Centrum Securities LLC has reviewed the report and, in so far as it includes current or historical information, it believed to be reliable, although its accuracy and completeness cannot be guaranteed.

The distribution of this document in other jurisdictions may be restricted by law, and persons into whose possession this document comes should inform themselves about, and observe, asuch restrictions. Neither Centrum nor its directors, employees, agents or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequentincluding lost revenue or lost profits that may arise from or in connection with the use of the information.

This document does not constitute an offer or invitation to subscribe for or purchase or deal in any securities and neither this document nor anything contained herein shall form the basis any contract or commitment whatsoever. This document is strictly confidential and is being furnished to you solely for your information, may not be distributed to the press or other mediand may not be reproduced or redistributed to any other person. The distribution of this report in other jurisdictions may be restricted by law and persons into whose possession this repocomes should inform themselves about, and observe any such restrictions. By accepting this report, you agree to be bound by the fore going limitations. No representation is made that threport is accurate or complete.

The opinions and projections expressed herein are entirely those of the author and are given as part of the normal research activity of Centrum Broking and are given as of this date and asubject to change without notice. Any opinion estimate or projection herein constitutes a view as of the date of this report and there can be no assurance that future results or events will bconsistent with any such opinions, estimate or projection.

This document has not been prepared by or in conjunction with or on behalf of or at the instigation of, or by arrangement with the company or any of its directors or any other persoInformation in this document must not be relied upon as having been authorized or approved by the company or its directors or any other person. Any opinions and projections containeherein are entirely those of the authors. None of the company or its directors or any other person accepts any liability whatsoever for any loss arising from any use of this document or contents or otherwise arising in connection therewith.

Centrum and its affiliates might have managed or co-managed a public offering for the subject company in the preceding twelve months. Centrum and affiliates might have receivcompensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for service in respect of public offerings, corporate finandebt restructuring, investment banking or other advisory services in a merger/acquisition or some other sort of specific transaction. Centrum and affiliates may expect to rececompensation from the companies mentioned in the report.

As per the declarations given by them, Mr Siddhartha Khemka and Mr Mahantesh Sabarad , research analysts and the authors of this report and/or any of their family members do not servean officer, director or any way connected to the company/companies mentioned in this report. Further, as declared by them, they have not received any compensation from the abocompanies in the preceding twelve months. Our entire research professionals are our employees and are paid a salary.

While we would endeavor to update the information herein on a reasonable basis, Centrum, it's associated companies, their directors and employees are under no obligation to update or kethe information current. Also, there may be regulatory, compliance or other reasons that may prevent Centrum from doing so.

Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or Centrum policies,circumstances where Centrum is acting in an advisory capacity to this company, or any certain other circumstances.

8/7/2019 allcargo global - visit note-cy11e introduced -centrum-241109

http://slidepdf.com/reader/full/allcargo-global-visit-note-cy11e-introduced-centrum-241109 8/8

Sanjeev Patni Head - Institutional Equities [email protected] 91-22-4215 9699T. S. Baskaran Joint Head – Institutional Equities [email protected] 91-22-4215 9620/87

Research Dhananjay Sinha Economist Economy & Strategy [email protected] 91-22-4215 9619

Niraj Shah Sr Analyst Metals & Mining, Pipes [email protected] 91-22-4215 9685

Mahantesh Sabarad Sr Analyst Automobiles/Auto Ancillaries [email protected] 91-22-4215 9855

Madanagopal R Sr Analyst Power, Capital Goods [email protected] 91-22-4215 9684

Abhishek Anand Analyst Media, Education [email protected] 91-22-4215 9853

Adhidev Chattopadhyay Analyst Real Estate [email protected] 91-22-4215 9632

Ankit Kedia Analyst Media [email protected] 91-22-4215 9634

Manish Kayal Analyst Infrastructure [email protected] 91-22-4215 9313

Nitin Padmanabhan Analyst Technology [email protected] 91-22-4215 9690

Piyush Choudhary Analyst Telecom [email protected] 91-22-4215 9862

Pranshu Mittal Analyst Sugar, Retail [email protected] 91-22-4215 9854

Rajan Kumar Analyst Cement [email protected] 91-22-4215 9640

Rajagopal Ramanathan Analyst Banking & Financial Services [email protected] 91-22-4215 9644

Rohit Ahuja Analyst Oil & Gas [email protected] 91-22-4215 9636

Saikiran Pulavarthi Analyst Banking & Financial Services [email protected] 91-22-4215 9637

Siddhartha Khemka Analyst Logistics [email protected] 91-22-4215 9857

Sriram Rathi Analyst Pharmaceuticals [email protected] 91-22-4215 9643

Amit Sinha Associate Power, Capital Goods [email protected] 91-22-4215 9927

Janhavi Prabhu Associate Sugar, Retail [email protected] 91-22-4215 9864Jatin Damania Associate Metals & Mining, Pipes [email protected] 91-22-4215 9647

Komal Taparia Associate Economy & Strategy [email protected] 91-22-4215 9195

Rahul Gaggar Associate Hotels & Healthcare [email protected] 91-22-4215 9683

Sarika Dumbre Associate Telecom [email protected] 91-22-4215 9194

Shweta Mane Associate Banking & Financial Services [email protected] 91-22-4215 9928

Vijay Nara Associate Automobiles/Auto Ancillaries [email protected] 91-22-4215 9641

SalesV. Krishnan +91-22-4215 9658 [email protected] +91 98216 23870

Ashish Tapuriah +91-22-4215 9675 [email protected] +91 99675 44060

Ashvin Patil +91-22-4215 9866 [email protected] +91 98338 92012

Siddharth Batra +91-22-4215 9863 [email protected] +91 99202 63525

Centrum Securities (Europe) Ltd., UK Dan Harwood CEO +44-7830-134859 [email protected]

Michael Orme Global Strategist +44 (0) 775 145 2198 [email protected]

Centrum Securities LLC, USA

Melrick D’Souza +1-646-701-4465 [email protected]

Key to Centrum Investment Rankings

Buy: Expected outperform Nifty by>15%, Accumulate: Expected to outperform Nifty by +5 to 15%, Hold: Expected to outperformNifty by -5% to +5%, Reduce: Expected to underperform Nifty by 5 to 15%, Sell: Expected to underperform Nifty by>15%

Centrum Broking Private Limited

Member (NSE, BSE), Depository Participant (CDSL) and SEBI registered Portfolio Manager

Regn NosCAPITAL MARKET SEBI REGN. NO.: BSE: INB 011251130, NSE: INB231251134

DERIVATIVES SEBI REGN. NO.: NSE: INF 231251134 (TRADING & SELF CLEARING MEMBER) CDSL DP ID: 12200. SEBI REGISTRATION NO.: IN-DP-CDSL-20-99

PMS REGISTRATION NO.: INP000000456 Website: www.centrum.co.in

Investor Grievance Email ID: [email protected]

REGD. OFFICE AddressBombay Mutual Bldg.,2nd Floor, Dr. D. N. Road, Fort,

Mumbai - 400 001

Correspondence AddressCentrum House, 6th Floor, CST Road, Near Vidya Nagari Marg,

Kalina, Santacruz (E), Mumbai 400 098. Tel: (022) 4215 9000