Alexander Wang Beauty - Extension Line Development

129

-

Upload

picha-choo -

Category

Art & Photos

-

view

83 -

download

6

Transcript of Alexander Wang Beauty - Extension Line Development

1

Table of Contents

Executive Summary ------------------------------------------------------------------------------------- 2 Company Summary ------------------------------------------------------------------------------------ 3-9

Brand Profile -------------------------------------------------------------------------------------3-4

Brand Identity ----------------------------------------------------------------------------------- 5-7

Positioning in the Market ---------------------------------------------------------------------- 8-9

Market Analysis ---------------------------------------------------------------------------------------10-47

Size of retail market ---------------------------------------------------------------------------10-14

Key players -------------------------------------------------------------------------------------15-26

SWOT ------------------------------------------------------------------------------------------ 27-30

PESTEL --------------------------------------------------------------------------------------- 31-40

Porter’s 5 Forces ----------------------------------------------------------------------------- 41-43

Positioning for Extension ------------------------------------------------------------------- 44-47

Target Consumer ------------------------------------------------------------------------------------ 48-51

Demographic -------------------------------------------------------------------------------------48

Psychographic ------------------------------------------------------------------------------------49

Behavioral Information ----------------------------------------------------------------------49-50

4Ps Strategy -------------------------------------------------------------------------------------------- 52-68

Product --------------------------------------------------------------------------------------------52

Pricing ------------------------------------------------------------------------------------------ 53-54

Placement ---------------------------------------------------------------------------------------- 55

Promotion-------------------------------------------------------------------------------------- 56-68

Conclusion ------------------------------------------------------------------------------------------------ 69

Bibliography-------------------------------------------------------------------------------------------- 70-71

Appendix----------------------------------------------------------------------------------------------- A1-A2

2

Executive Summary

Alexander Wang has become one of the most popular and talented contemporary

designers in today’s fashion industry. The brand extensions include an accessories line, a t-shirt

line, and an objects line that all follow his modern grunge aesthetic. However, we found a gap in

the cosmetics department. With the amount of younger women dressing in his clothing, there is

no doubt that they will want makeup to match. We aim to create a cosmetics line for the

Alexander Wang brand that will combine quality and the Wang aesthetic to create products that

his customers can’t help but buy.

We aim to use the same simple color schemes and clean cut lines that are commonly used

in his garments to bring the customer beauty, confidence, and practicality. The mixture of natural

and bold colors will become essentials for the Wang customers and more. We expect the

products to be successful even in strong competition with a wider variety of modern yet bold

color choices, variety of products, and package appeal. In order to gain attention in stores, the

individual makeup cases will include gold and marble details, which will follow the brand’s

aesthetic and style. Our key success factors will be to keep consistent with the brand’s aesthetic,

selling at Alexander Wang’s online and in-store, selling in Sephora stores and online, and

providing products/packaging that will help attract the customer and create a broader customer

base.

3

Company Summary

History

Alexander Wang was very young when started his own line of clothing. According to his

online biography from the official website, he attended Parsons School of Design in 2002, but

dropped out after two years of education and interned with various notable fashion companies

such as Marc Jacobs, Derek Lam, and Teen Vogue. This helped to further himself and his name

in the fashion industry. Soon after, in 2005, he launched his own cashmere knitwear collection

and two years later, in 2007, he launched his first women’s ready-to-wear line (official website).

In 2009, Women’s T by Alexander Wang and the accessories line was launched, followed by the

Men’s T line in 2011. All of his success in the industry has taken less then 10 years to evolve,

which shows his talent in fashion and knowing what his customer wants.

Ownership

Santlofer stated in her book, Contemporary Fashion Designers That You Should Know,

that the organization was established by Alexander Wang in 2005 as a family-owned company

with his brother Dennis Wang as chief principal officer, his sister-in-law Aimie Wang as the

CEO, and himself as the creative director. The majority of the funding came from his family and

in 2007, Alexander Wang was awarded $200,00 from the CFDA/Vogue fashion award, which

helped to expand the company (53-54).

Distribution

According to the official Alexander Wang website, “the company opened its first flagship

store in SOHO, New York in 2011, following in 2012 with the second flagship store in Beijing,

and the recent one in Tokyo in 2013.” The expansion of the company into other geographic

regions reflects its effective distribution strategies. Today the company operates in over 15 stores

4

worldwide. It also has many distribution channels, such as e-commerce retailing directly on its

own website as well as selling merchandise to wholesalers like Net-A-Porter. According to

Fashionbi, there are more then 30 department stores and premier retailers, like Neiman Marcus,

Nordstrom, and Barney’s New York, that sell his lines both in store and online. There are also

concessions in department stores and a pop-up shop in collaboration with Joyce at Gateway

Arcade in Hong Kong.

Growth Projections

The beauty industry continues to grow each year according to Franchise Help’s analysis

of the Beauty Industry. They state “for the interested entrepreneur this continuing growth and

evolution offers a diverse menu of opportunity”. They also state that, “The beauty industry

continues to expand globally, with some projections claiming 8.5% growth by 2014”. With the

gradual growth of both the Alexander Wang brand and the beauty industry, this extension should

also grow in popularity after its launch. With the help of e-commerce and wholesale, we hope to

expand the cosmetics extension to all Alexander Wang stores and wholesalers around the world.

5

Brand Identity

As a person

Alexander Wang Inc. as a person is portrayed through the soul of Alexander Wang, the

29-year-old New Yorker, who is young and full of passion. With his passion and ambition, he

created a very successful brand that represents his downtown city style perfectly. In Vogue’s

British edition, Wang states, “I wanted to see people on the street that I don’t know wearing my

clothes. That excites me”, which could be the mission of his “M.O.D” (Model Off Duty) style.

His brand is made for a young, casual woman whom like to look good without putting in a lot of

effort.

As a product

Alexander Wang Inc. includes products in accessories, the ready-to-wear line, the T-shirt

line for men and women, footwear, and the objects line. Despite the launch of these products in a

short span of time (5 years) the brand identity has not been lost.

As a symbol

There is no graphic label for the Alexander Wang brand other then the actual typed name.

The T by Alexander Wang symbol is a simple “T” in bold font, which depicts the simplicity and

structure of the product. The company is successful in the branding of specific features in their

products. They use the color black commonly throughout every collection including clothing,

accessories, the website and in their flagship stores. They also place an emphasis on symmetry

throughout their handbags and some garment silhouettes. Metal is largely used in the accessories

to show off their rigid, modern aesthetic. The repetition of these branding features makes their

products easily recognized as Alexander Wang without needing a label.

6

As an organization

Alexander Wang Inc. is privately owned with no public stock. It’s still a family owned

and lead company and as stated in Santlofer’s book about Alexander Wang: “The company has

already spread its business globally with a very clear customer segmentation for the target

market” (Santlofer). This could be one of the leading reasons why the company has grown so

rapidly in such a short period of time. With the opening of their new flagship store in Beijing,

China in 2012, the Wang’s Asian family background and professional analysis/predictions of the

market made this a great business opportunity to help the expansion of their business globally.

7

Brand Identity Matrix

8

Current Positioning the Market Price/Quality Matrix

Price Research of the Market

Price

Qua

lity

Low

High

Low High

9

Alexander Wang’s close competitors in the market include Marc Jacobs, Michael Kors,

Chloe, and Chanel. They all distribute in most high-end department stores and have many retail

stores. They all use e-commerce sites and have their own websites to promote and sell their

products. These brands, however, have been in the market much longer then Alexander Wang,

and therefore have had more experience and a broader customer base. Alexander Wang has

managed to keep up with them in a shorter amount of time, which shows the potential the brand

has in the future.

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

Fore

ver

21

Uni

qlo

Zara

RVC

A Ar

man

i Exc

hang

e To

psho

p G

ap

Juic

y Co

utur

e BC

BGM

axaz

ria

Amer

ican

App

arel

J.Cre

w

Alic

e an

d O

livia

Mic

hael

Kor

s Ra

lph

Laur

en

Mar

c Ja

cobs

Alex

ande

r W

ang

Chlo

e Ch

anel

Average Price of Clothing Average Price of Footwear Average Price of Accessories Average Price of Cosmetics

10

Market Analysis

Size of the market

Overview of the make-up industry

Based on the data from DATAMONITOR (see appendix1) there are three major cosmetic

markets throughput the world: Europe, Asia-Pacific, and the United States. The United States

accounts for 20.6% of the global make-up market Value, Europe accounts for 44%, Asia-Pacific

areas accounts for 23.2% and the rest of the world accounts for 12.3%. The U.S market, in

comparison to other areas, has the advantage of geographic unity; in addition, it accounts the

biggest market segmentation among the world as an individual country. Besides, our company

Alexander Wang Inc. was founded in the U.S. Because of these factors, we decided to choose the

U.S to be our first target geographic area to launch our cosmetic line.

United Make-up Market Segmentation 2005-2009

11

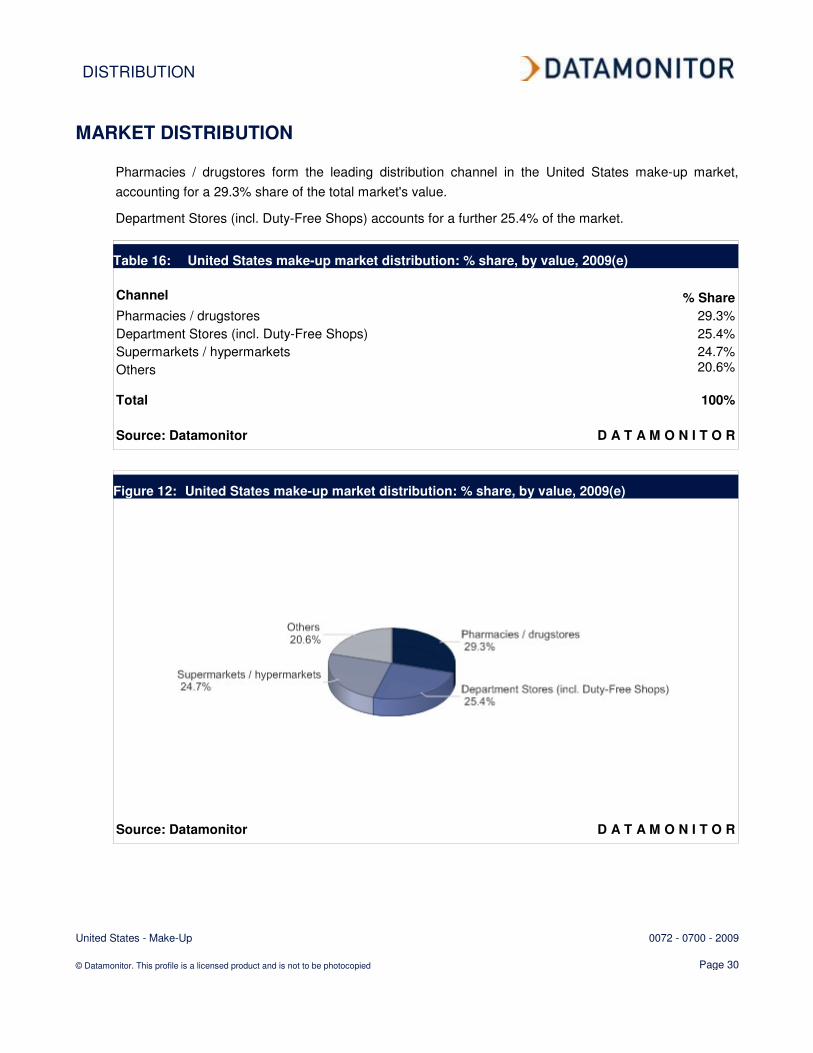

The make-up industry is divided into four major categories: the eye make-up, face make-

up, lip make-up, and nail make-up. In 2009, U.S area, the face make-up is the biggest, by

accounting for 36.1% of the total market value. The eye make-up has a share of 31.0% of the

market and then lip make-up has 22.3%, the rest, 10.7%, is nail make-up.

According to Gale American Industry Overview in 2011, the structure of retail products in the

make-up market could be divided into three classes, upscale, mid-level, and low-scale by

classifying their distribution channel and price matrix. The mid-level and low-scale products

sometimes are categorized as mass products and the upscale products are categorized as prestige

products.

Industry value and forecast

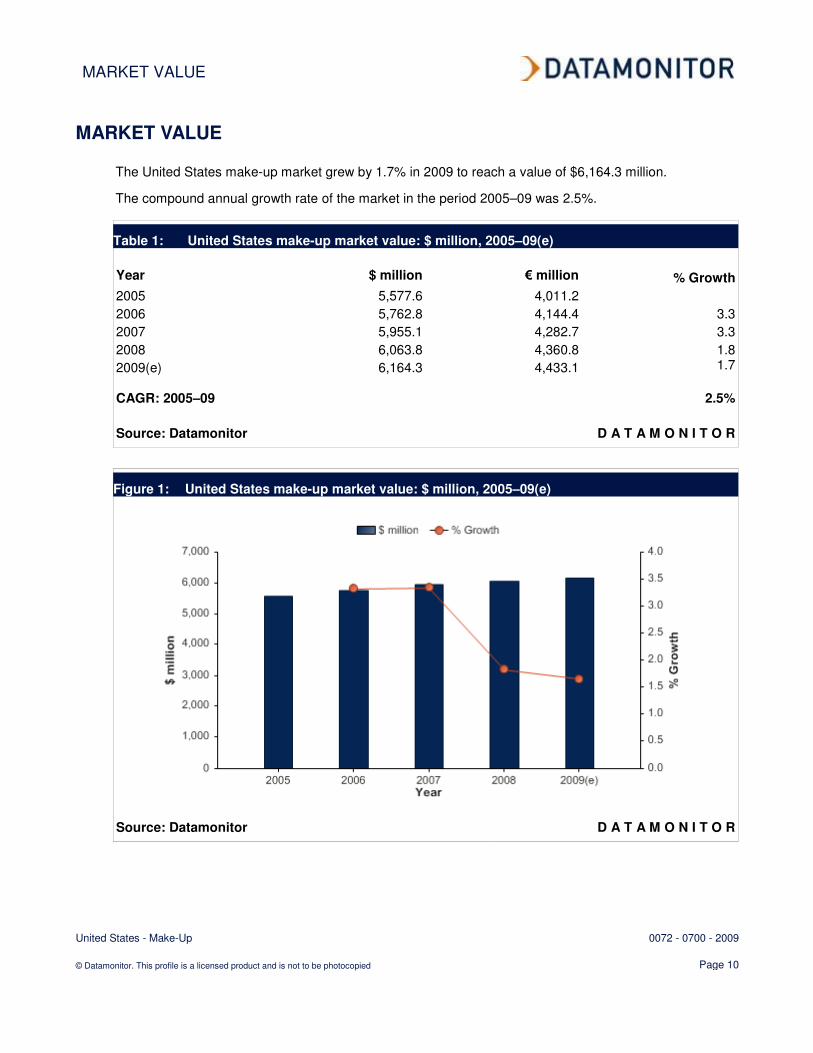

In 2005, make-up industry in the United States had a market value of $5577.6 million and

it had a trend of continuous growing pace. From 2005 to 2007 the growth rate was 3.3% and then

it had a decreasing rate from 2007 to 2009, 1.8% and 1.7%. The compound annual growth rate of

the market in this period was 2.5%. From DATAMONITOR's data, the forecast of the market

value in 2014 will be $6,592.8 million, the growth of 2009-2014 will be about 1.4%, and the

market has a trend of being stable.

United States Market Value 2005-2009

12

United States Market Value Forecast 2009-2014

Industry volume and forecast

In 2005, the volume of make-up market in the U.S had $722.3 million units. Then the growth

rate from 2005 to 2007 was 1.8% and it decreased in 2008, the rate was 0.9% and from 2008 to

2009 the growth rate was 0.8%. The growth rate from 2005 to 2009 was 1.3%. From the

forecast, the market volume will reach 784.7 million units in 2014 and the growth rate of 2009 to

2014 will be 0.6%

United States Market Volume 2005-2009

13

United States Market Volume Forecast 2009-1014

Market Share

There are four leading players accounting the majority of the market share, and the entire

industry has a trend of being concentrated. L'Oreal S.A. is the biggest company, generating a

26.7% share of the market's value. Estee Lauder Companies Inc., has 19.0% of the market share

and Revlon, Inc. accounts the 18.1%. Then the rest 36.1% separates to other companies.

Market

Analysis

14

Based on the factors of market segmentation, market volume and value in cosmetic

industry in the U.S, we could see that the U.S is a big market compared to other geographic

areas. Even though the overall growth rate is small our target geographic area still has greater

capacity to allow more companies to involve into the cosmetic industry.

Moreover, the majority of cosmetic industry was occupied by three companies, so that

our new line might have less chance to gain big market share but there are opportunities for us to

develop our products to be at the up-scale level and gain higher profits.

15

Key Players

The four leading and largest cosmetic companies in the U.S. Market are L’Oreal, Estee

Lauder, Revlon, and P&G; all which hold about three-fourths of the total market value in 2009

(75.7%).

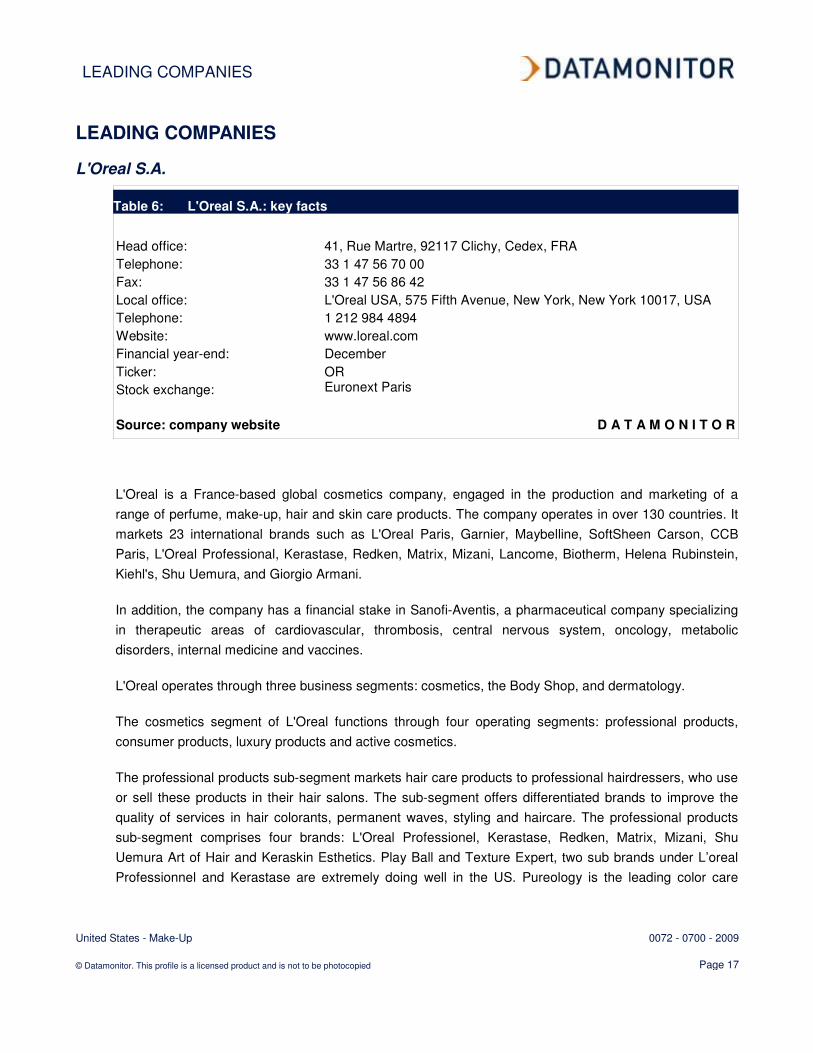

L’Oreal S.A

The L'Oréal Group is the largest cosmetics company. It is based in France and operates

over 130 countries worldwide. Its cosmetic production comprises of 4 categories: fragrance,

make-up, hair, and skin care products. It has more than 23 well-known international brands in the

cosmetic segment as well as The Body Shop and dermatology (Datamonitor).

L’Oreal Cosmetics Segments (Excluding any Fragrances, Hair Care, and Dermatology)

Sales, L'Oréal S.A., 26.7, 27%

Sales, Estée Lauder

Companies Inc., 19, 19% Sales, Revlon

Inc., 18.1, 18%

Sales, P&G, 11.7, 12%

Sales, Others, 24.3, 24%

U.S. Makeup Market Value in 2009 $6,164.3 million.

16

* Brands that offer makeup and color cosmetics

Based on the company’ s brands offered and financial report from Datamonitor, leading

and well-known makeup brands like Lancome, YSL Beaute, Giorgio Armani Beauty, and Urban

Decay are potential competitors to Alexander Wang beauty extension line. YSL Beaute and

Armani Beauty are designer’ s extension line (beauty) and focus on makeup and color cosmetics,

while Lancome focuses more on its fragrance and skin care lines. Compared to Alexander Wang

Inc, which has a fresher and modern aesthetic, both YSL Beaute and Armani Beauty are rather

Types of Merchandise

Brand Names

Distribution Channels

Consumer Products

L’Oreal Paris*

Garnier

Maybeline New York*

Softsheen Carson

Essie*

Le Club des Creatures de Beaute*

- Mass Merchandiser - Beauty Superstores - Drug Stores - Supermarket -E-commerce

Luxury Products

Lancome*

YSL Beaute*

Armani Beauty*

Helena Rubinstein*

Biotherm

Shu Uemura

Kiehl’ s

Urban Decay*

- Premium Department Stores (Nordstorm, Belk, Macy’s, Barney’ s New York) - High-end Outlets (Saks Fifth) - Brands’ Own Boutiques - Travel Retails - Brands’ Websites - E-commerce

17

considered classic cosmetics and also have higher price points. Today L’Oreal is still the largest

company that dominates and specializes in the cosmetic industry. It has a large amount of

financial resource to spend on media especially in advertising (television commercials,

magazines, and Internet) which is the most important promotional tool in the beauty market.

However, L’ Oreal is still subjected to lose market share in prestige and designers’ name

cosmetics segment. Makeups in consumer products segment such as L’ Oreal Paris and

Maybeline New York are negligible since they have different price lines, distribution channels,

and target markets.

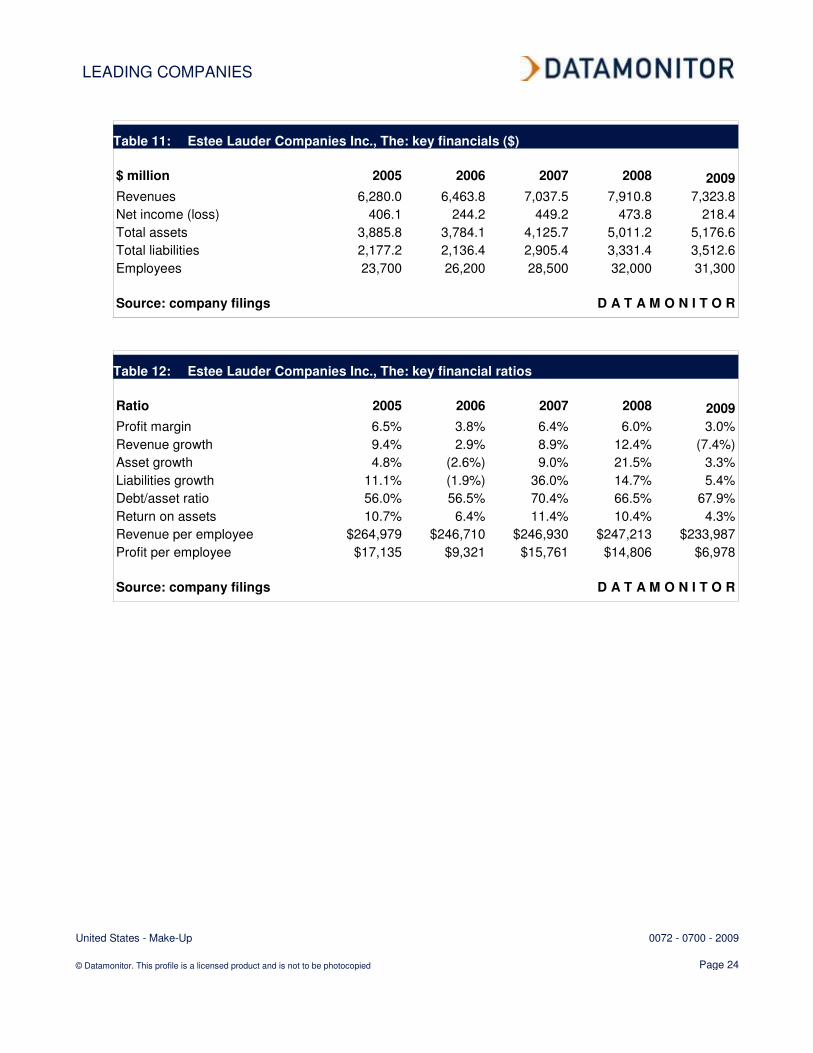

Estée Lauder Companies, Inc.

Estée Lauder is the second largest cosmetics and beauty company based in New York

City. It markets as well as manufactures makeup, skin care, hair care, and fragrance products

over 140 countries. It also has wholly-owned offices in 43 countries worldwide.

Estée Lauder Cosmetics Segments (Excluding any Fragrances, Hair Care, and Dermatology)

* Brands that offer makeup and color cosmetic

Types of Merchandise

Brand Names

Distribution Channels

Mid-Premium Luxury

Products

Bobbi Brown*

Estee Lauder*

M.A.C.*

Clinique

Aramis

Jo Malone

La Mer

La Series

- Premium Department Stores (Nordstorm, Belk, Macy’s, Barney’s New York) - High-end Outlets (Saks Fifth) - Brands’ Own Boutiques - Travel Retails - Brands’ Websites - E-commerce

18

While the company emphasizes skin care and fragrances more, Estée Lauder, M.A.C.,

and Bobbi Brown are still leading brands that dominate makeup and color cosmetics segment.

M.A.C. and Bobbi Brown would be considered major competitors but may have slightly lower

price to Alexander Wang’s beauty line since they both are considered artistry cosmetics rather

than designers’ lines. Both brands, however, share similar aesthetics in terms of product,

packaging, and store design (minimal, sleek, edgy, and dark)

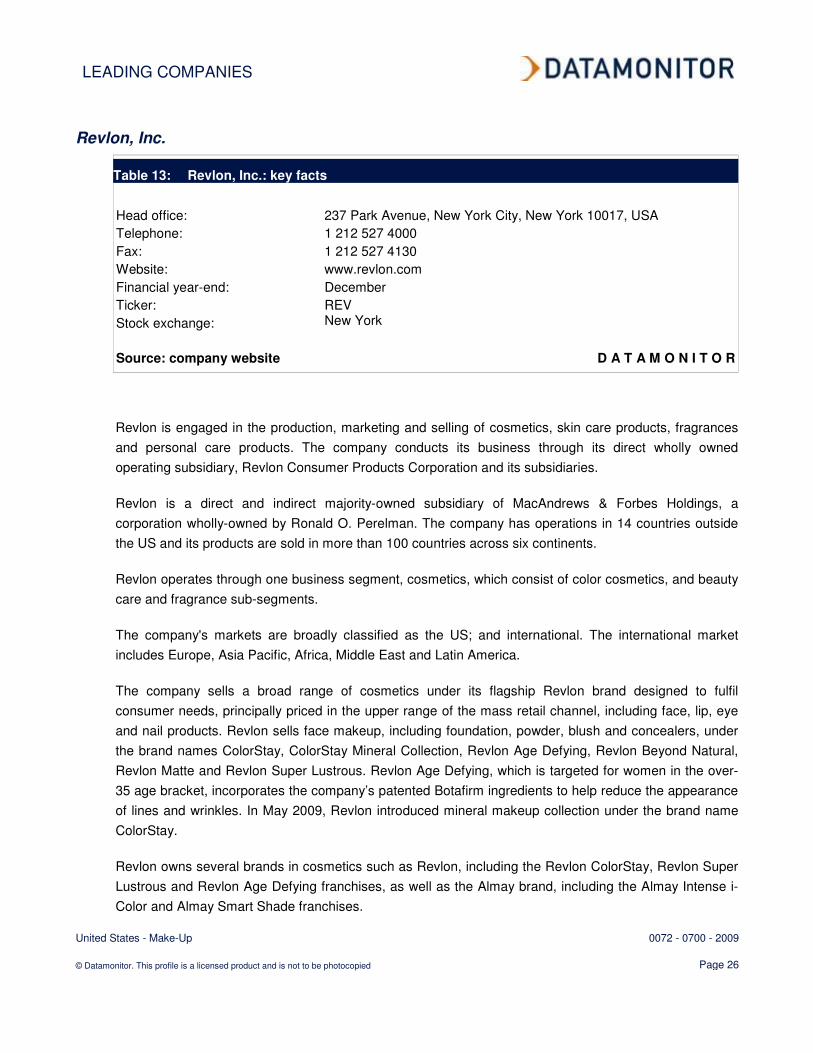

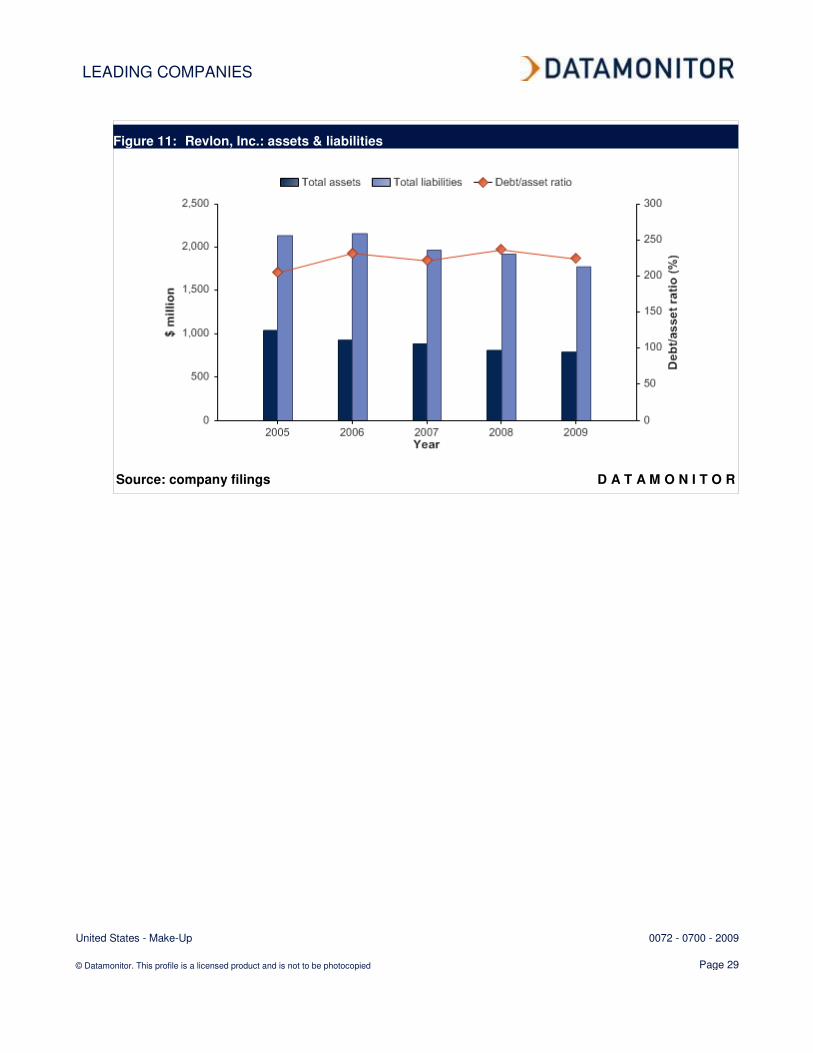

Revlon, Inc.

According to Datamonitor, Revlon, Inc. is the third largest cosmetics and beauty

company. Unlike the other top players, Revlon offer very few skin care products but highly

emphasizes on their makeup and color cosmetics segment. The company operates in 14 countries

outside the U.S. with products distributed and sold over 100 countries worldwide. The company

sells their cosmetics under its Revlon brand. Leading product brands are makeup such as

ColorStay, Revlon Age Defying, Revlon Beyond Natural, Revlon Matte, and Revlon Super

Lustrous. Recently in 2009, the company launched its mineral makeup collection under the brand

name ColorStay. Unlike L’Oreal and Estee Lauder, the majority of Revlon’s target consumers

are considered mass market and thus the company distributes its products through mass retailers,

chain drug store, as well as certain department stores (Datamonitor).

P&G Co.

From P&G’s 2009 official financial report, the company generated total revenue at $114

billion. The revenue from the beauty segment (including skin care, makeup, and hair care)

accounted for 23% of the total revenue or $26.3 billion. The company had 14.3% on profit

margin or $3.76 billions. The cosmetic brand that generated the most profit in makeup lines was

CoverGirl. It was the largest color cosmetic brand in the U.S. The cosmetic products are sold

primary in drugstores, convenience stores, and supermarkets targeting the mass market. In 2008,

CoverGirl LashBlast mascara was the company’s strongest eye makeup product and took much

19

share from L’Oreal’s Maybeline. P&G spends around 10% of its budget on digital marketing.

Celebrity endorsement and advertising is the company’s main promotional tool. CoverGirl’s

main competitor is L’Oreal’s brand Maybeline New York. Another P&G’s makeup brand is Max

Factor which sells products primary in Europe. Both CoverGirl and Max Factor represented

around 6% of the company’s total revenue.

Other competitors that sell their cosmetic products in drugstores and supermarkets are

Revlon, Almay, L’oreal, NYC Cosmetics, and Wet ‘n’ Wild Cosmetics.

Other private brands

Other private brands that had 24% of total market share in 2009 included Avon,

Neutrogena (Johnson & Johnson), Benefit Cosmetics, Illamasqua, Eye Lips Face (ELF), Stila,

Clarins, and Nars.

Marc Jacobs Beauty

Marc Jacobs just recently launched his new beauty line in September 2013. The first

beauty store was launched in Manhattan as well as the color collections and custom-designer

fixtures in 11 existing Marc Jacobs locations. There are currently about 300 Marc Jacobs store

globally and Robert Duffy, CEO of Marc Jacobs International, L.L.C., stated that more beauty

sections will be added to the stores soon. Marc Jacobs Beauty also distributed its product at 330

Sephora freestanding stores in North America. The beauty line generated around $1 million sale

in just two weeks with mascara and liquid eyeliner being the best sellers. It is projected that the

color collection will generate $ 15 million at retail from August through December and $20

million at retail at the end of 2014. The makeup line is expected to be launched in Europe in

2014 as well with the Middle East and Asia to follow. The product mix consists of four

categories: eye, lip, face, and nail (Irdale and Naughton).

20

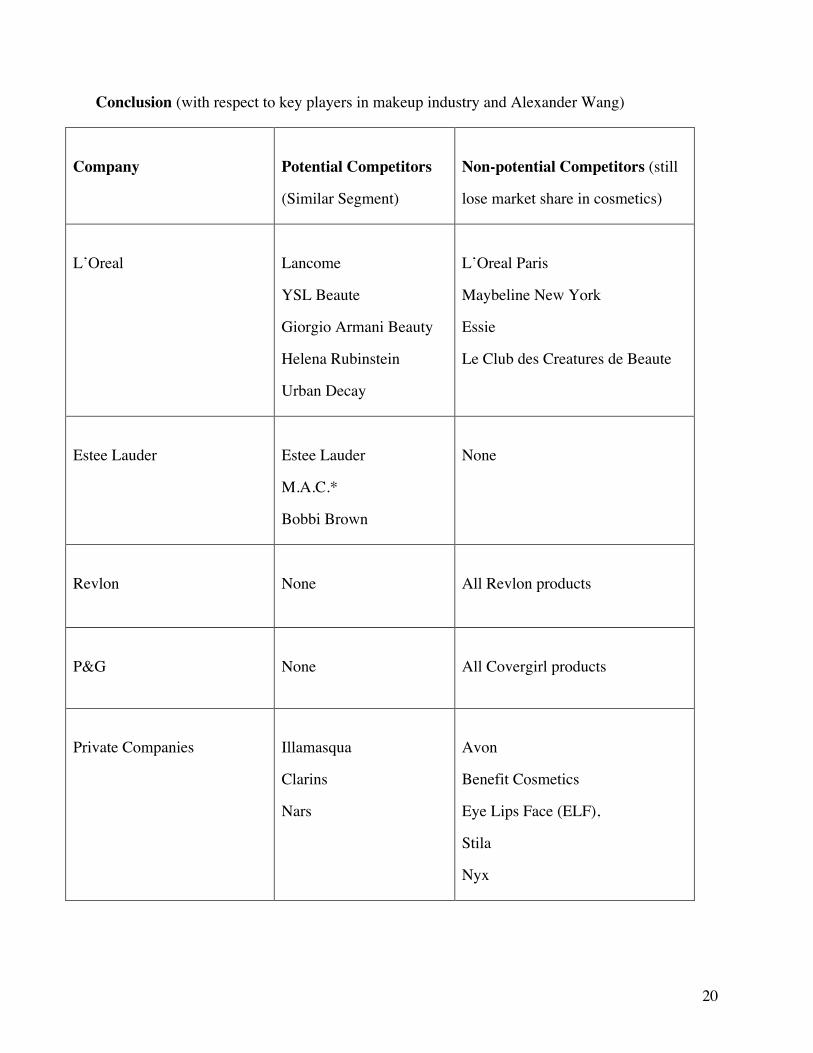

Conclusion (with respect to key players in makeup industry and Alexander Wang)

Company

Potential Competitors

(Similar Segment)

Non-potential Competitors (still

lose market share in cosmetics)

L’Oreal

Lancome

YSL Beaute

Giorgio Armani Beauty

Helena Rubinstein

Urban Decay

L’Oreal Paris

Maybeline New York

Essie

Le Club des Creatures de Beaute

Estee Lauder

Estee Lauder

M.A.C.*

Bobbi Brown

None

Revlon

None

All Revlon products

P&G

None

All Covergirl products

Private Companies

Illamasqua

Clarins

Nars

Avon

Benefit Cosmetics

Eye Lips Face (ELF),

Stila

Nyx

21

Designers’ lines

Chanel

Dior

Dolce&Gabbana Beauty

Marc Jacobs Beauty

None

Alexander Wang will rarely compete with make-up brands at mass-market level, such as

Covergirl and Revlon, since its products target at different consumers, have higher price range,

and are distributed at different segment retailers. Most of the competitive brands are prestige

products with unique designs and premium quality. Designers’ names and aesthetics are

commonly used as selling point. Classic designer brands like Chanel, Dior, YSL, Armani have

higher price range, while artistry brands like MAC, Illamasqua, Nars, and Urban Decay are

lower. Lancome, Estee Lauder, and Clarins are operated under the companies that primarily

specialize in cosmetics. Even though these competitive brands have different price points, they

are still distributed at the same or similar retailers such as premium department stores

(Nordstorm, Belk, Macy’ s, Barney’ s New York), high-end outlets (Saks Fifth), travel retails

(Airports, Duty Free shops). For example at a premium department store, MAC and Chanel

cosmetics may have their concessions next to each other; either brand can attract the customers

at the moment regardless of different price lines and thus they are subjected to compete each

other for market share in makeup.

Marc Jacobs Beauty may be the most relevant competitor to Alexander Wang’s beauty

line since their brands target toward the similar age group of young consumers or the millennial.

Marc Jacobs and Alexander Wang may share very similar price ranges, products design and

aesthetics because their characteristics are considered modern and young. Since both brands

possess very talented designers and earn their recognition and popularity in the recent years, they

are still subjected to compete each other at the cosmetics level. However, Marc Jacobs has higher

22

competitive advantage in terms of the company’s size and popularity. While Marc Jacobs gears

toward the younger millennial group, Alexander Wang may gain advantage from the older

millennial; however, they can still share the overlapped age group of consumers.

Potential Competitors (with respect to Alexander Wang beauty line)

Types of Makeup

Brands

Classic Designers

Chanel

Dior

YSL

Armani Beauty

Helena Rubinstein

Modern Designers

Dolce&Gabbana

Marc Jacobs Beauty

Premium Artistry

MAC

Illamasqua

Lower-Premium Artistry

Urban Decay

Nars

Cosmetic Specialists

Estee Lauder

Clarins

23

Financial and investment analysis

L’Oreal generated total revenues of $ 24.3 billion (2009) with $22.6 billion in cosmetics

segment (93% of total revenues) The company’s net income was around $2.5 billion. The U.S.

market accounted for 24.4% of the total revenue or around $5.9 billion. The company had 10.3%

profit margin (Datamonitors).

Estée Lauder generated total revenue around $7.3 billion at the end of June 2009 with net

income at $ 218.4 million. The revenue from makeup segment accounted for $2.8 billion (38%

of the total revenue). The lower net sales from the company’s heritage brands and the makeup

artist brands were the causes of revenue decline in the recent years. The U.S. market accounted

for 41.2% of the total revenue (around $3 billion) The company also had 3% on profit margin in

2009 (Datamonitor).

24

Revlon, Inc. generated $1.3 billion at the end of December 2009. The company earned

total net income at $48.4 million. The revenue from beauty care and fragrance accounted for

$510,4 million (39.4% of total revenue). The decline in revenue came from lower net sales of

certain makeup products. The U.S. market accounts for 57.7% of the total revenue or around

$747.9 million. The company had 3.8% on profit margin. The revenue growth has decreased

since 2006 (Datamonitor).

25

2009 Financial Report L’Oreal Estee Lauder Revlon

Revenue (Billions $) 24.3 7.3 1.3

US Revenue (Billions $) 5.93 3 0.75

Revenue Growth Flat/Slight Decrease

Profit Margin Slight Decrease Dramatic Decrease Slight Decrease

Impact on profit margin (from both L’Oreal and Estee Lauder’s 2009 annual report)

- Increase in operation expense

- Decrease in net sales

- Recession / uncertain economic environment

- Exchange rate / depreciation and losses from foreign exchange transaction

- Higher cost of global IT system

26

Forecast

According to Datamonitor:

Compound annual growth rate from 2009-2014: flat/ slight decrease

Slight increase in market value or 7% in 2014

As a new entrant in makeup market, Alexander Wang will launch its makeup line only in

the U.S. during the first 6 months. Like Marc Jacob Beauty, if Alexander Wang could get shelf

space at Sephora, there is a chance the company will get market share up to $1-1.5 million in

sales for the first month after launch, and around $7 million at the end of six-month period

(assuming that Marc Jacobs and Alexander Wang will share equal shelf space) However, if the

company decides to expand and sell its products oversea, it will be subjected to impacts like

exchange rate and global costs which might lead to decrease in net sales as well as high costs and

expenses.

27

SWOT Analysis

Strengths!- Brand Loyalty!- Emerging and talented designer!- Unique and modern design!- The designer’s name is brand identity!- Very fast growing company!- Strong product differentiation!- No need to compete with mass market segment!- Financial resource!- Private and Family Owned Company!-High potential in creating extension or diffusion lines.!- Perceived high quality products!

Weaknesses!- Very small market share at the early stage!- Low economies of scale!- Fewer relationship with manufacturers and retailers compared to other brands!- No experience in cosmetics production!- Not owning or manufacturing the products and depending on cosmetic manufacturers!- Low ability to bargain with suppliers!- High advertising and media cost!- Need to negotiate with retailers for self space!

Opportunities!- Fashion is a major influence on the cosmetic industry!- Consumers differentiate themselves through styles and brands of makeup products offered!- Consumers prefer designer brands over retailer or generic brands!- Stable and slightly growing market growth!- High growth of beauty superstores such as Sephora!- Being less subjected to price war.!- Recession-proof products !- Huge market size!- Cosmetics are main financial resources for major fashion companies.!

Threats!- Very high competition and pressure from the larger and well-established key players in cosmetic industry.!- Competition with other designer beauty lines (Marc Jacobs, YSL Beaute, Chanel)!- Being subjected to acquisition from larger companies. (Armani Beauty YSL to L’Oreal)!- Customers’ demand in safety and organic certification. (Higher cost)!- Green movement causing limited use in certain raw materials (microbead)!

28

Strengths

The company has to rely on its brand identity or the designer’s name “Alexander Wang”

in order to enter the makeup industry and earn the market share. The design of color cosmetics

and makeup must be unique and reflects the designer’s aesthetics. The essence of the designer’s

youngness and modernity may create attention and interest to many people easily. Alexander

Wang will get its existing customers to buy its beauty products instead of competitors. Those

who wear Alexander Wang collections can also have their Alexander Wang makeup to fully

express their identities and love marks. The company also has huge family, corporate, and

external financial resources to support this new extension line. Since the company is a fast

growing business and successful at launching new lines, it should be able to manage this new

beauty line efficiently as well.

Weaknesses

Alexander Wang is relatively new in the fashion industry and still focusing on its ready-

to-wear lines. Unlike other key players, the company has no experience and no facility

specialized in cosmetic segment. Thus at the beginning, the company will not take risk in

operating its own cosmetic manufacturing. The company will need to rely on cosmetic suppliers

and manufacturers; it will have low ability to bargain with them compared to more popular

brands. High fixed costs are unavoidable if it decides to open its own beauty stores. New

cosmetic brands will require very high spending for advertising and sales promotion to acquire a

minimum level of exposure and to be able to attract the target customers. This is especially true

in the cosmetic industry where the market is huge and the overall advertising spending reaches

29

up to $3 billion (KSM). High cost of promotional tools and other expenses may lead to lower

profit margin at the early stage.

Opportunities

Though the cosmetic industry is very large and competitive, even acquiring small market

shares still provide large scale of profit. Alexander Wang will not compete with the key

competitors’ mass-market brands (which occupy majority of market shares) and thus the

company will not be subjected to retaliation like price war since its own beauty line will utilize

brand identity (designer’s name) and its aesthetics and designs are as the unique selling

proposition. Fashion is also a major influence in cosmetic brands. Target customers whose styles

fit with Alexander Wang or the existing brand loyalists will seek out and buy the products no

matter what. Fashion and luxury brands create brand loyalty by providing affordable products

like cosmetics and accessories to give the customers experience in which they are able to engage

and connect with the brand; the companies then hope for those customers to return and buy other

product lines like clothing or accessories in the future. Large fashion companies like Chanel and

Giorgio Armani gain their financial resources from cosmetic products since they generate the

most revenues and profits compared to clothing and unattainable luxury product lines. Another

opportunity today is the rapid growth of beauty superstores like Sephora which will be one of the

main distribution channels for theAlexander Wang beauty line (Loeb).

Threats

New entrants in cosmetics industry may find difficulty in competing for market share

under the high pressure. They are also subjected to acquisition from the large cosmetic

30

companies. (Even fashion brands like YSL and Giorgio Armani operate their beauty lines under

L’Oreal) Customers’ demand in safety and organic products are also rising. The company must

ensure those qualities with the suppliers and manufacturers. Corporate social responsibility is

also a major issue in many businesses today, especially large and international corporations.

Alexander Wang must be very careful with issues like product testing and labor conditions that

might be able to create a negative image since the company used to get involved with such

lawsuits.

31

PESTEL

Political Factors

Democratic and Stable

The U.S government is known for being democratic, fair and transparent policies. U.S is a

developed country with a stable society, and the government is open and welcome to the

development of new businesses. This government attitude could reduce the barriers for us to

launch the new product line.

Well-Organized Government Structure

In the United States, even the federal laws are mostly enacted by Congress, they still

authorize certain government agencies to create regulations. There are two major organizations

that are involved in the cosmetic, toiletry and fragrance industry: the CTFA and FDA. Each

agency has its clear responsibility and authority

Cosmetic, Toiletry and Fragrance Association

The CTFA stands for Cosmetic, Toiletry and Fragrance Association, was founded in

1894 and majorly provides the services of scientific, legal, regulatory, and legislative and also

represents manufactures, distributors and industry suppliers. The Cosmetic Ingredient Review

(CIR), conducted by a panel of scientific and medical experts, was developed under the CTFA’s

sponsorship in the mid-1970s and it gathers information about ingredient safety and makes the

information available to manufacturers.

FDA and Its Regulation

The FDA stands for Food and Drug Administration. This organization involves in the

industry of food, drugs, medical devices, radiation-emitting products, vaccines, blood and

32

biologics, animal veterinary, tobacco products and Cosmetics. For the cosmetics industry, they

are in charge of regulating safety and labeling. There are three major regulations created by the

FDA for the cosmetic industry. All the color additives have to be tested and approved before use,

ingredients like mercury compounds, chloroform, and methylene chloride have been banned

from use. Poisonous or harmful substances, filthy, putrid or decomposed substances should not

be contained in cosmetics, and they have to be made and held under sanitary conditions. The

ingredients and quantity used in the cosmetics have to be listed and labeled correctly. In addition,

the FDA has the authority to check the products that are already available on the market and has

the right of take legal action to against companies if some safety issues are found.

Economical Factors

Strong Economy

The US is one of the most well developed countries with the highest economy status

among the world. According to the trading economics data “ The Gross Domestic Product in the

United States was worth 1584.80 million US dollars in 2012. The GDP value of the United

States represents 25.0 percent of the world economy.” The wealth country has stronger

consumption power and higher consumption level, which means the consumers in the U.S, has

less price-conscious of purchasing the up-scale cosmetics compared to countries with a weaker

economic status.

Unemployment Rate

At the end of 2008, the U.S started the experiencing the economy recession and then the

unemployment rate increased to 9.3% in 2009 and to 9.6% 2010; this was the highest rate of

unemployment rate since 1983. However, the rate started to decrease in 2011 and the

unemployment rate went back to be 9.0%, meaning that there are 14.2 million unemployed

people in the U.S.

33

Recession and Its Recovery

U.S has its strength as a well-developed economy but the economy was involved in some

big recessions in the past. The latest one is the recession in 2008 and it lasted for two consecutive

years. Then the U.S government took the action of bring the massive fiscal stimulus to recover

the economic status from the recession and in 2011. Currently the economy status has been

recovered from the recession and is back on track, with a stable growth rate.

The cosmetic industry is not influenced by the economic situations easily. During the past

recession in 1930, it established the “recession proof” image and it didn’t fluctuate much in the

1960s and 1980s recession either. Moreover, during the recent recession in the early 2000s, the

market started to be resuscitating and the cosmetic industry was one of the industries in the

fastest pace, it grew from $11.8 billion in 2003 to $13 billion in 2005 and the growth is

continuing with the recovery of the economy.

No matter how much the economy fluctuates, women still wear the make-up. Make-up

products are usually considered as inexpensive and small objects which lead the price conscious

to be weak for the cosmetic products.

34

Social Factors

Income distribution

Income distribution in different age groups

The age group from 45-54 has the highest median income and age group of 15-24 has the

lowest median income from the record in 2011 and 2012 in the U.S. Overall the median income

has a trend of growing up from 2011 to 2012 in every age group.

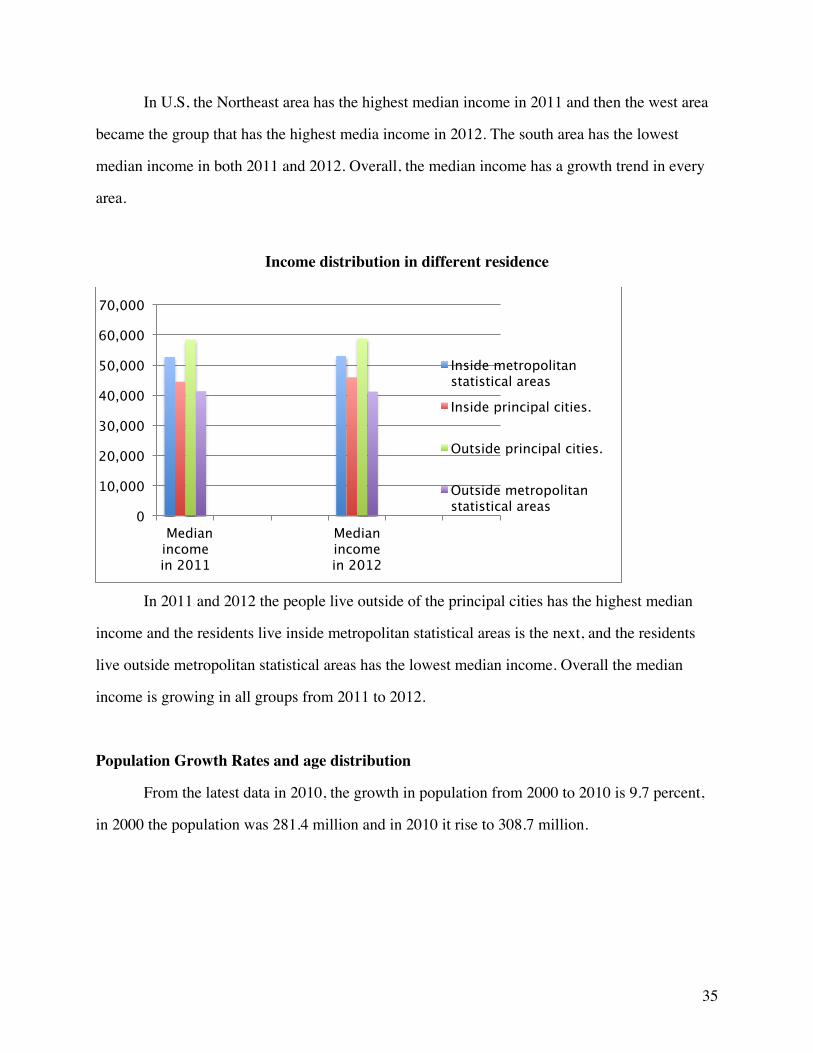

Income distribution in different region

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Median income in 2011

Median income in 2012

15-24 years 25-34 years 35-44years 45-54 years 55-64 years 65 years and older

44,000 46,000 48,000 50,000 52,000 54,000 56,000

Median income in

2011

Median income in

2012

Northeast Midwest South West

35

In U.S, the Northeast area has the highest median income in 2011 and then the west area

became the group that has the highest media income in 2012. The south area has the lowest

median income in both 2011 and 2012. Overall, the median income has a growth trend in every

area.

Income distribution in different residence

In 2011 and 2012 the people live outside of the principal cities has the highest median

income and the residents live inside metropolitan statistical areas is the next, and the residents

live outside metropolitan statistical areas has the lowest median income. Overall the median

income is growing in all groups from 2011 to 2012.

Population Growth Rates and age distribution

From the latest data in 2010, the growth in population from 2000 to 2010 is 9.7 percent,

in 2000 the population was 281.4 million and in 2010 it rise to 308.7 million.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Median income in 2011

Median income in 2012

Inside metropolitan statistical areas Inside principal cities.

Outside principal cities.

Outside metropolitan statistical areas

36

From the data of age distribution from 1960 to 2010, the median age changed from 29.5

to 37.2, the U.S has a trend of ageing.

37

Social Mobility and Education

The mobility of people in the U.S is not high, the age group from 18 to 24 has the biggest

mobility and other than that, other groups are more stable.

People age over 18, 30% of them have graduated in for high school and 18% of them

have graduated college and obtained bachelor degree, and 9.8% percent of people obtained

higher degree. The overall education level in the U.S is considered as high.

Attitude towards cosmetic and fashion

From the previous economic recession, and also the period of abundance, people started

to pursuit low cost products like fast fashion or counterfeit cosmetics instead of high quality

products. This trend could be a one of the threats to gain the market share.

(United States Census Bureau)

Technological Factors

Focus on reformulating products to rely on natural products

Because of the macro development of technology the consumers are becoming more educated

on choosing their products that’s good for them. The overall trends of going green also

influenced the cosmetic industry, and consumers are pursuing the green products. The research

and technological improvements should focus on vegetable and plant materials instead of

synthetic chemicals to satisfy consumer’s demands for mildness and reduced toxicity.

Short life cycle and fast path of technological obsolescence

In the time of abundance period, there are more products available on the market than the actual

demand from consumers and also the high technology were developed to provide more channels

for people to receive information and compare the products. These factors could influence the

life cycle and obsolescence for the products and this also apply to the cosmetic industry.

38

U.S is in the leader place of innovation

In our target country, the United States has strength of being as one of the leaders in the

technology innovation since the World War II. The technical strength could benefit the cosmetic

industry as well. It might be more opportunities to involve high technology into the cosmetic or

make-up and skin care tools. Besides, popularize of using high technology could provide better

e-commerce and advertising channels.

The growth of pharmaceutical markets

From the country analysis the pharmaceutical markets have a growing trend in the U.S.

Mean while, the cosmeceutical (cosmetics and pharmaceutical) had big market share and

consumer popularity in Europe and Asia but not yet U.S. These types of products might have a

chance to be developed and spread with the trend of “going-green”.

Color IQ by Sephora

Sephora developed the best beauty invention of the year in 2013, the Pantone color IQ,

the device they developed could scan your face and found out what the color of customer’s skin

and then help the customer to find out the right products in right color to match their skin.

Environmental Factors

“going green” trend

Many surveys demonstrated the increase of consumer awareness for the environmental

issues, and there are three major concerns from the consumers, animal right, availability of clean

air and water, and waste management.

Well-establish environmental policies

The United States has a well-established environmental policy framework both federal

and state. The Environmental Protection Agency (EPA) is the agency under the federal

government that protect human health and environment and the smaller agencies exist under

them take control of manage the water, air and waste. The Clean Air act was one of the major

39

regulations established to improve the air quality.

Poor performance

Even the U.S is in a leading place among many areas in the world, but the environmental

performance is not satisfactory. The U.S government is trying to find the solution or develop

new technologies to improve current status.

Animal Testing

The animal right is one of the major concern from environmental aspect. In cosmetic

industry, the animal testing is the major issue that receiving against voice and complains from

consumer. However according to CTFA, the cosmetic, toiletries and Fragrance Association, this

issue cannot be avoided and they believe that human health and safety is more important.

Recyclable products and energy

Under the trend of going green the recyclable products and energy is favored. Even the

ingredients of cosmetic are either nature or synthesized, the package of the products could use

more recyclable material and provide consumer a more green and environmental concerned

impression.

Legal factors

Well-established legal framework for business in the U.S

The legal framework in the U.S has been well-established, and each state has its

individual state laws function with the federal law system. This complete system gives the clear

guide of what is allowed and what is not for the business which could protect the overall

environment and avoid vicious competition.

Multiplicity of state laws

Besides the federal law system, the state laws in the United States varies in region, and

this gives difficulty for business to expand and follow the laws in different state at the same time.

40

FDA labeling regulations

FDA, the food and drug administration, have a specific labeling regulation for cosmetic

industry and FDA states “The FD&C Act prohibits the marketing of adulterated or misbranded

cosmetics in interstate commerce”. All the ingredients and quantity has to be clearly labeled.

Foreign investment is favored in the U.S

The U.S is the largest direct foreign investment receipt among the world, and the U.S

government has an open attitude to the investment. This policy could bring more chances for

business to obtain financial support from other countries and also might attract investor from

foreign country to start the business in the U.S.

41

Porter’s 5 Forces

The following information refers primarily from Datamonitor See Appendix

Competitive Rivalry: Moderate!- Top companies at luxury level focus their production more on skin care and fragrances.!- In U.S., major companies diversify their products geographically.!- Top players hold 75% of the total market share.!- Other 25% contains global and recognizable brands including designers’ beauty lines.!- Large cosmetic companies have their own facilities specialize in product development and SCM.!- High fixed cost for new companies.!

Bargaining Power of Suppliers: Moderate!- Raw materials like chemical and mineral products for cosmetics are commonly available.!- Cosmetic products can be produced with many alternative raw materials.!- Switching suppliers (manufacturers) have very little negative consequence to the production.!- Suppliers (manufacturers) are large in scales!- Raw material suppliers are not dependent solely to the cosmetic manufacturers. The same goes with cosmetic manufacturers where they are not dependent to the retailers.!

Bargaining Power of Customers: Moderate to High!- Retailers have strong position as distributors!- Consumers differentiate themselves through different styles and brands.!- Company is obliged to offer products that are in trend and needed by the customers.!- Customers have multiple brands to choose from.!- The larger the retailers, the greater the power customers have.!

Threat of New Entrant: Moderate to High!- The strength of brand identity, brand loyalty, and differentiations are the keys to prevent threats from the larger companies.!- Designer and fashion names for cosmetics can negate the competition at mass-market level.!- New Entrants may be able to target niche markets.!- Low economies of scale.!- Products are subjected to price war from the similar brands.!- Less power in fighting for shelf space.!- New Entrants have difficulty in international expansion.!

Threat of Substitution: Low!- Very few substitutions for makeup.!- Designer names make it impossible for substitution.!- People who disinterest in brand name may choose other brands that offer the same types of products. (Old people)!- People may use natural and traditional cosmetics instead of manufactured products!

42

Bargaining Power of Suppliers - Moderate

From the Datamonitor, it rather explains the relationship between raw material suppliers

and the company that will manufacture its own products. For this case, Alexander Wang is not a

manufacture and the company will not operate its own cosmetic manufacturing facility since it

would cost too much. Based on this case, we can assume that the company has to rely on

cosmetic manufacturers for the production. The manufacturers will have bargaining power with

Alexander Wang. Since manufacturers are commonly available, switching manufacturers may

not affect the company’s production. Manufacturers are not dependent solely on Alexander

Wang since there are more private cosmetic brands that are willing to do business with them.

Bargaining Power of Customers – Moderate to High

Alexander Wang is likely to distribute its beauty products through its own stores and

Sephora. At Sephora, customers would have many brands to choose from. The larger the store,

the more cosmetics brand Sephora will offer. Besides the shelf space and display, Alexander

Wang needs to offer unique colors and designs in order to attract potential customers from other

brands, especially Marc Jacobs Beauty. At Alexander Wang Store, customers are obliged to buy

its product, while at Sephora, the customers who are more price-conscious may choose other

brands that have similar qualities or colors.

Threat of New Entrant – Moderate to High

Distribution channels for Alexander Wang’s beauty line in the U.S. are limited when

compared to other brands like Marc Jacobs Beauty. Other than Sephora, Alexander Wang has

only few stores in the U.S. that can install the makeup section. However, Alexander Wang does

not have to compete on price with mass-market brands. The company will target to niche market

at the early stage since the company has very low economies of scale. The only concern is that

the company will subjected to compete and spend on promotional tools to attract potential

43

consumers. As soon as the beauty line grows more, the company hopes to be able to open more

beauty stores as well as gain more shelf space at other high-end retailers.

Threat of Substitution - Low

There is rarely any alternative product to makeup, unless people decided to use natural

and traditional cosmetics from plants such as raw flower dye for blush or tree bark powder.

Companies or designers offer unique packaging designs in which it’s impossible for brand

loyalists to change. However, those who do not have brand loyalty may buy other designer’s

brand based on the similar value of makeup, for example a girl may buy either Chanel or YSL

lipsticks but not L’ Oreal Paris lipstick since it’s considered as a mass-market product;

Alexander Wang beauty line may also face this kind of situation. People who are disinterested in

brand names like senior citizens may choose other brands that offer the same types of products

regardless of the brand names.

Competitive Rivalry - Moderate

Alexander Wang may not be able to compete the top players since the company is small

and not specialized in cosmetics. The company can disregard high fixed cost since it won’t likely

to own its cosmetic manufactures. However, top companies like L’Oreal and Estee Lauder are

now focusing more on skin care and fragrance segments; with the rapid growth of the company,

it is an opportunity for Alexander Wang to focus on makeup and gain some share from the 25%

of the market. The company will have to compete with other designers’ cosmetic lines that are

more popular, such as Marc Jacobs Beauty and YSL Beaute. Again, Alexander Wang needs to

rely on its unique designs, name, and brand loyalty.

44

Positioning for Extension

Price Matrix

45

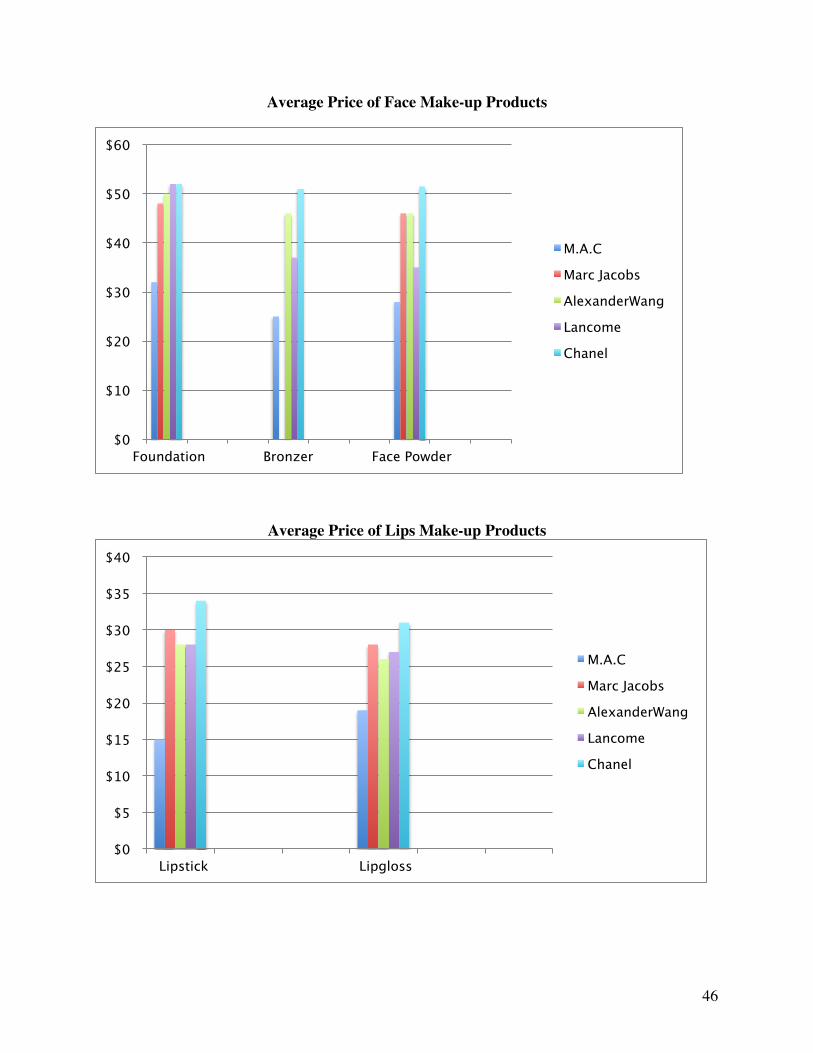

By analyzing the market and the market, and from the price and quality matrix we

selected the major competitors that really close to our market position and target customers, to be

M.A.C, Marc Jacobs, Lancome and Chanel. We chose M.A.C because of their similar aesthetic

to our company in the packaging design and we have the target customer in the younger age.

Marc Jacobs is the most direct brand we are competing to, they started from fashion then extend

the beauty line just several months ago. Lancome is one of the biggest cosmetic brands and has

similar price level to us, and the Chanel gained its fame in fashion industry too and it’s one of the

most high-end cosmetic brands. From these reasons, we chose these four companies to compare

the price.

Average Price Of Eye Makeup Products

$0

$10

$20

$30

$40

$50

$60

$70

Mascara Liquid Eyeliner Pencil Eyeliner Single Eyeshadow Basic Eyeshadow Set

M.A.C

Marc Jacobs

AlexanderWang

Lancome

Chanel

46

Average Price of Face Make-up Products

Average Price of Lips Make-up Products

$0

$10

$20

$30

$40

$50

$60

Foundation Bronzer Face Powder

M.A.C Marc Jacobs AlexanderWang Lancome Chanel

$0

$5

$10

$15

$20

$25

$30

$35

$40

Lipstick Lipgloss

M.A.C Marc Jacobs AlexanderWang Lancome Chanel

47

Average Price of Brushes

The price of Lancome and Marc Jacobs is very close and this is also where our price ranges is,

but lower than Chanel but higher than M.A.C to keep our brand image of being high-end.

All of our direct competitors have their own retail store in the shopping department, and

wholesale it to Sephora. They also use e-commerce to wholesale and retail as well. Since we

share the target customer and in the same market position, we are intending to sale our products

in the same distribution channels as our competitors did.

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

$90.00

Powder Brush Bronzer Brush Eyeshadow Brush Eyebow Brush

M.A.C Marc Jacobs AlexanderWang Lancome Chanel

48

Target Consumer

Demographic

Ever since women’s equal rights have evolved throughout the 20th century, there has been

a large change on consumer behavior. Women consider wearing cosmetics as a way to gain self-

confidence and express social politeness. We are going to try and focus on the greatest range of

age among United States cosmetic consumers, which is between 18 to 34 years old according to

KSM. The prestige beauty consumer has an income of $66,738 and they like to keep up with the

latest fashion trends. They are more likely to purchase cosmetics at a department store such as

Nordstrom, Neiman Marcus, etc. Cosmetic consumers are mostly female and about 74% of US

women wear makeup according to KSM. Although they live in the United States, they are a very

diverse group of women with families that come from all over the world, meaning they all have

very different with distinct features including skin, eyes, hair, and lips.

In order to keep up with the trends, and healthy skin, premium cosmetics ensures great

quality and a brand name product. Premium cosmetics occupy about 23% of the market (Sena).

That is almost a quarter of the market and a very important aspect to the industry. According to

KSM better educated, and higher income women are the ones who use premium cosmetics. Over

the two past decades, 64% of workingwomen earn over half of the family’s income. They have

the highest buying power in the family, therefore they purchase over 80% of the consumer

goods, which include cosmetics and anything else her family needs. As a result of this rise in

education and income, these women have become more demanding consumers, meaning that we

need to give them what they want; a quality product that they will bring with them everywhere.

A product that they will want to use everyday because it makes them feel better and more

confident. They want a product that they wont have to worry about throughout the day. We will

give them the quality product that they want, with the brand name that they love.

49

Psychographics

This customer is more likely to live in urban areas in the Northeast and West regions.

They spend about $34 a month on beauty products. They like their cosmetics to be easy to use,

and fun yet sophisticated. They keep themselves clean and live a healthy lifestyle. These females

care about their appearance and how they look, while still keeping there skin, face, eyes, hair,

etc. up to par. It is part of a daily routine for these women. Waking up, working out, taking a

shower, getting dressed and putting on their makeup. It is a routine that about 74% of U.S.

women do every morning (KSM) and it is only getting more popular with time. These women

like to read magazines and are influenced by what they see in their advertisements. They are

concerned about social and environmental issues and are more likely to buy a product for a cause

(KSM). They want a product that is hypoallergenic and natural not something that will clog

pores and cause breakouts. She is always searching for a product that works and makes her feel

confident about herself. When she puts her makeup on in the morning she wants that feeling of

fulfillment so that she can go out into her hectic life without having to worry about how her

makeup looks. She wants it to be long lasting so she wont have to re-apply halfway through the

day because she wont have time with her busy schedule. She wants to know that is she is

spending money on value and brand, and that she is gaining their aesthetic and value that she

wants with her purchase.

Behavioral Information

The average US woman spends $144 annually on cosmetics (Women Wear Daily, 2011).

More and more cosmetic consumers are shopping online with websites like Amazon, EBay, and

Sephora. 28% of online beauty shoppers buy off of Amazon, 18% off of Sephora, 13% off of

EBay, and the rest include online drugstores, department stores, and mass retailors (referring to

figure 5 graph). According to the figure 1 graph, 28% of beauty shoppers research products

online before they purchase them in the store. 16% shop online to replenish and try new

products. 56% mostly buy online because they know what they want and can order it quickly and

50

from their homes. 42% of women are most likely to purchase a product after hearing good

reviews from their family and friends (KSM). Mass merchandisers and drug stores are the most

popular channels for cosmetics consumer to purchase from because of their price and selection.

This consumer loves to engage in conversation about their beauty products, and therefore use

social media. Websites/apps like Facebook, Twitter, Google, and many different blogs help this

consumer to communicate with other consumers about what products they did and didn’t like. A

large part of the cosmetic industry is the advertisements on television and in magazines. There is

no doubt that consumers are influenced by magazines and television to buy beauty products. In

fact, 58% of cosmetic advertisement spending goes into magazines, 31% goes into network and

cable TV, and the remaining 11% goes into syndication and web display. This shows the

importance of advertisements in the cosmetic industry, especially in women’s fashion

magazines.

KSM

51

With our demographic, psychographic, and behavioral research, we have found an

industry that is important to the US woman and is growing in popularity each year. We have

found a large market for cosmetics among working/active women in the US. By targeting a

younger customer, we will follow the brands aesthetic and gain the widest range of customers.

Using social media sites like Instagram, Facebook, and Twitter, will help promote our new

extension and communicate with our customers. With a wide range of consumers purchasing and

researching products online, we will make sure to use e-commerce sites like Sephora. With

cosmetics as a necessity in a women’s everyday life, our products will be very accessible and

easily a favorite among the premium cosmetics.

52

The 4Ps

Product

Our premium cosmetics line for Alexander Wang will include eyeliner, mascara, eye

shadow, lipstick, lip-gloss, foundation, powder, bronzer, and cosmetic brushes. We want to cover

all the essentials that women want and need when putting on their makeup everyday. We also

want to provide quality natural makeup that is not harmful to the skin. We will use a mineral

base for all face powders and eye shadows in order to ensure safety and quality. By including the

dark marble texture on our round products and the gold accented corners on our square products,

we maintain the Wang aesthetic throughout the collection. With a range of different colors, we

aim to target most, if not all, ethnicities and eye colors. We chose to create liquid and pencil

eyeliner for our customers so they can choose as they please. For the pencil eyeliner and mascara

colors, a simple black and brown will match any eye color and skin tone. For the liquid, a simple

navy and black for customers bold side. For eye shadows, the colors are drawn from Alexander

Wang’s last three collections. With a mix of natural browns, shades of grey, and subtle pops of

color, there is a shade for everyone. For our face products including liquid foundation, powder,

and bronzer, a range of bronze and yellow skin tones can match with most skin tones. For our

lipsticks and gloss, we chose natural pinks, pale browns, and a mix of bold colors. Our brushes

include an eyeliner brush, an eye shadow brush, a powder brush, and a bronzer brush. They are

the essential brushes needed to complete any beauty look. We decided to provide eye shadow

and brush values packs so you can get a variety of products in one. Our eye shadow groupings

will include three colors that go with different eye colors. Our brush value pack will include mini

brushes with a case for any traveling our customer may do.

Face & Lips

53

Price

The pricing strategy for our new extend line Alexander Wang Beauty is based on three major

factors, the price of our fashion products positioned in the market and our competitors’ retail

price, and our cost or expense of our products.

First, by looking and analyzing our company Alexander Wang Inc.’s position in the market,

our price of fashion products, including the clothing, footwear, accessories, is really close to

Ralph Lauren, Marc Jacobs. Brands like Chanel and Cloe has higher average price than us,

especially in clothing and accessories. Since we are developing a horizontal brand extension,

then our pricing strategies will be kept as same as our fashion products. Our new cosmetic line

will be in the same price zone in the market position.

Second, by researching our competitors in the cosmetic industry and we found four major

competitors that are really close to our price range. The M.A.C, Marc Jacobs, Lancome and

Chanel. Since Alexander Wang has its fame for fashion already and it is growing a really fast

pace, it is one of the stimulus for consumers to take the purchasing action for our new cosmetic

products, consider this factor we decided to set up our price to be higher than the M.A.C even

our target customer is the same. Chanel has much higher market position than Alexander Wang

and they have a long history for the brand and stronger customer loyalty than Alexander Wang,

so our price range will be lower than Chanel. Then we decided to set our price to be really close

to Marc Jacobs and Lancome.

Moreover, Our products will all be produced in nature materials so the cost of technologies

and ingredients will increase, in order to keep our mark up and margin our retail price has to be

set up high enough to maintain the goal. Our package design for our products is new and fresh,

some interesting elements have been added into these could increase the cost of packaging which

could increase the expense too. So our overall price is considered to be high. Specifically,we

decided to set up some of our unique designed products to be higher than our most director

competitor to gain the customer who purchasing for our aesthetics. Then we set up the lipstick

54

and lip-gloss to be lower than our competitors, since these is the most often purchased due to its

color verities so that customer might try our products because of the lower price.

Product Price Sheet

55

Placement

We will sell our products in all Alexander Wang stores including the new flagship store

in Beijing. In store, we want to place the products near the check out counter so when entering

the store, leaving the store, and purchasing, the products will be easily seen. We will also sell at

beauty counters in department stores that sell the Alexander Wang ready-to-wear lines. These

include Neiman Marcus, Bloomingdales, Saks Fifth Avenue, Barney’s, and many more. Sephora

is one of our most important places to sell our products. We want to keep up with our

competitors and many are selling in Sephora stores. Sephora is one of the most popular online

and in store beauty distributers in the world.

A huge aspect of our placement will be on the Internet and phone apps. Our products will

also be sold in these department stores online website as well as our own. Our presence in e-

commerce is very important in order to follow what our customer wants. Most importantly we

want to sell our product on the Sephora online store as well. Our placement online and in store

will make it easy for our customer to shop for our products and know where to find them. We

want to make their experience stress free and easy.

56

Promotion

As a new entrant to cosmetic industry, Alexander Wang beauty line needs to use many

promotional tools to gain minimum level of exposure to the potential consumers.

At the early stage, the company will focus primarily on reach strategy with heavy advertising and

public relations in order to build brand awareness and brand loyalty. Sales promotion will keep at

minimum since it is not effective for high-end cosmetic brands. Personal selling will put

emphasis on in-store customer services.

Product Lifecycle (with respect to Alexander Wang Beauty)

Introduction – Heavy advertising campaign and public relations to build brand awareness.

Growth – Heavy advertising campaign and public relations to build brand loyalty.

Maturity - Advertising and personal selling to maintain distribution.

Decline –Introducing new cosmetic collections.

Advertising Campaign

Advertising campaign is necessary to let the customers be aware of Alexander Wang’s

new beauty line. With continuity in advertising, customers will be able to recognize this new

brand and finally take action in buying the products. The ad content will primarily shows

Alexander Wang’s models along with the products in which the aesthetics and styles are similar

to Alexander Wang’s ads for clothing line.

57

58

Advertising

Three main media types will be used to reach customers: fashion magazine, outdoor

advertising, and internet advertising.

Fashion Magazine + Digital Magazine

According to KSM, high-end beauty consumers are best reached through magazine and

digital media. Alexander Wang’s consumers fall into this category in which they reflect the

young, urban, prestige costumers where they can be influenced by surround media. High-end

consumers can be easily influenced by fashion magazines. They are also the highest magazine

readers among the groups. Magazines also have high-pass-along rate and reproduction.

In 2010, the beauty industry spent approximately $3 billion in advertising with 58%

represented fashion magazine ad ($1.6 billion) (KSM). Alexander Wang beauty line needs to

plan carefully on its advertising budget and publication. Alexander Wang will contract

publishers in advanced to ask for a single or double spread in the fashion magazines (as well as

digital magazine) Potential publishers are Vogue, Elle, Harper Bazaar, Marie Claire, and Allure.

59

Vogue has the most readers among all fashion magazines; it is a great advantage to gain high

exposure from Vogue. The publisher also has an established relationship with Alexander Wang.

Elle and Harper Bazaar are considered high-end fashion magazines which target Alexander

Wang’s customers. Marie Claire and Allure though focus more on mass-market level, they

dedicate majority of their contents on cosmetics which will somehow generate attention among

consumers who are interested in cosmetic products. Digital, mobile, and social media usages

have been gaining popularity in the past few years and are projected to increase even higher.

Fashion Magazines are trying to provide online and mobile applications on various devices such

as smartphone and digital tablets. (KSM)

60

Outdoor Advertising

Billboard

61

Billboard will be highly effective in urban areas and large cities where most target

consumers live, such as New York City, Los Angeles, and Miami. However, the advertisings are

subjected to high noise level which can distract the consumers. Billboard is also appropriate for

the start-up brand with limited budget since the cost of media is moderate and the message of the

ad can reach numerous target audiences.

Mall Advertising

Alexander Wang will distribute cosmetic products through premium department stores as

well as beauty stores like Sephora. Mall banner has a very high advantage in which it attracts

many potential customers and there’s also higher chance the customers will go to the store and

buy the products after they see that ad.

62

Taxi

Taxi tops advertising and Taxi TV Advertising

Moving ad is a great way to reach customers at different places. According to Medialife

Magazine, more than 40% of New Yorkers who have upper-income ride taxi regularly with 56%

of them are being female whom ages between 18-34. Majority of Alexander Wang’s target

customers fall into this category in which they tend to live in the cities and prefer traveling by

taxis to subway. TV advertising inside the taxi is common today. Customers can interact with the

touch screen to view ads, times, and map while riding the taxi to their destinations.

63

Internet and Social Media

Alexander Wang Beauty will also advertise the products through fashion and beauty

websites such as style.com, WWD, and BoF (web banner ads and video ads). Online advertising

has grown rapidly and will become the largest and leading media in the future. It has a huge

advantage than other types of media in which it can target specific groups of customer. Social

media, such as Facebook, Twitter, Instagram, Pinterest, and Youtube, is very important since

more than 55% of customers follow and update about the brands through social media.

Advertising through mobile devices is vital for Alexander Wang’s customers since majority of

them are considered millennial who expose themselves through social media and online channels

(Fromm and Garton).

64

Public Relations

Press Release and Blogger Reviews

In order to capture media attention, publicity is used to introduce new cosmetic products.

Alexander Wang Beauty will send public release to fashion presses, publishers and bloggers. In

addition to press release, the company will give away test-products to the selected bloggers in

advanced, so they can review them and publish online articles during the launch period. Fashion

and beauty bloggers are influential to customers who spend time online finding information

about the products.

Fashion Show

Alexander Wang can also promote its beauty line during Ready-to-Wear fashion show in

which each season the company can introduce a new set of make up along with the collections.

65

The event will create attention to the new beauty collection in advanced before the it hit the store

in next season.

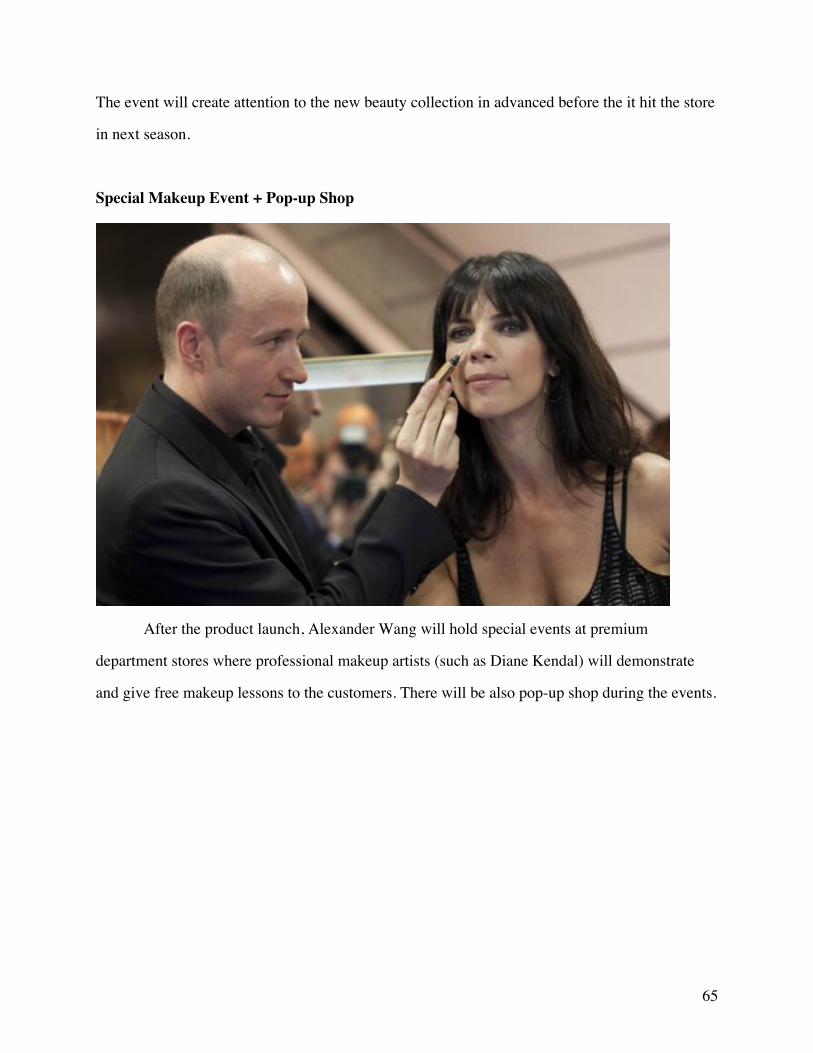

Special Makeup Event + Pop-up Shop

After the product launch, Alexander Wang will hold special events at premium

department stores where professional makeup artists (such as Diane Kendal) will demonstrate

and give free makeup lessons to the customers. There will be also pop-up shop during the events.

66

Promotion Calendar

Fashion Magazines

Vogue, Elle, and Harpers Bazaar will do the pre-launch advertising in their September

Issues (August) to create attention. Elle and Harpers Bazaar will continue to advertise during

launch period. Since Vogue’s September Issue has the highest sales and exposure level, it

doesn’t need to advertise more because it already got attention from majority of the audiences;

and also that the magazine will probably focus more on high-end ready-to-wear lines for

Spring/Summer season. Allure and Marie Claire will start advertising right after the launching.

People who read both magazine and have interests in cosmetic products will seek out and buy the

makeup right away. They will also advertise again during November before Christmas season.

Another same paradigm of advertising will occur after January or the period before Fall/Winter

fashion week, where additional collections and new colors will be introduced in February.

67

Outdoor Advertising

Billboards and taxis will start advertising at most 3 days prior launching date since both

requires time to setup completely. They will continue to advertise for another month before the

ads get obsolete (especially for people who see the ads everyday). Another advertising will occur

after February, or during Fall/Winter fashion week.

Indoor Advertising

Advertisings will start after the product hit the department stores. When potential or

target customers see the ads, there’s a higher chance that they will go directly to the stores and

buy the products. The department stores will advertise again during holiday seasons.

Online Advertising

Web banner ads will appear regularly on various fashion and beauty sites after launch

period and will continue after the post launch until the end of December (one month before a

new collection comes out) Video advertising will stay on sites only launch period to create

attention and interest to the target customers.

Social Media Advertising

Facebook and Twitter are great tools to provide teasers during pre-launching to create