Alcohol Excise Tax Report

23

Megan C. Diaz, MA Frank J. Chaloupka, PhD David H. Jernigan, PhD March 2, 2015 THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS Report prepared for

description

Alcohol Excise Tax Report

Transcript of Alcohol Excise Tax Report

Megan C. Diaz, MA

Frank J. Chaloupka, PhD

David H. Jernigan, PhD

March 2, 2015

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

Report prepared for

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

Table of Contents

Executive Summary .......................................................1

Introduction .................................................................. 2

Alcohol Consumption in Texas ....................................... 2

High School Alcohol Use ........................................................... 2

College Alcohol Use .................................................................. 3

Alcohol Use in the General Population ..................................... 3

Alcohol Use and Harm .............................................................. 4

Alcohol Taxes and Inflation in Texas ..............................4

The Costs of Alcohol Use................................................ 6

Modeling the Effects of a Tax Increase ........................... 9

Consumption and Increased Tax Revenue ............................... 9

Health Gains ............................................................................10

Underage Drinking Impact ....................................................... 11

Fetal Alcohol Syndrome Impact ..............................................12

Tax Increase Opposition ...............................................12

Impact on the Average Texan ..................................................13

Productivity and Jobs Impact ..................................................14

Tax Avoidance and Evasion .....................................................16

Conclusion ...................................................................16

About the Authors ........................................................17

About Texans Standing Tall ..........................................18

References ...................................................................19

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

1

Excessive alcohol use kills 6,514 Texans each year,9

including 1,296 in fatal traffic crashes.13

Alcohol taxes protect health and prevent underage

drinking. Extensive empirical research has confirmed

that increases in alcohol excise taxes reduce

underage drinking,38,39,40 binge drinking, driving under

the influence,27 crime, rape,30 homicides, suicides,33,34

fetal alcohol syndrome, sexually transmitted

diseases,32 violence against children,31 and other

consequences of excessive drinking.

Alcohol problems cost Texas an estimated

$19 billion per year.3

Government in Texas, and by extension Texas

taxpayers, directly pays $7.7 billion of these costs.3

Texas last raised its alcohol excise taxes when

Ronald Reagan was President.1,2 In the thirty years

since then, these taxes have lost 56 percent of their

value because they do not rise with inflation.

This erosion from inflation has caused alcohol

excise tax revenue to fall to $208 million, which is

two-tenths of one percent of total tax revenues,

and less than two percent of the direct costs of

alcohol problems to Texas taxpayers.

Excise taxes on spirits in Texas are currently the

45th lowest in the nation.17 Similarly, the excise tax

on wine is the 43rd lowest in the nation18 and the

beer excise tax is the 30th lowest.19

A 10 cent per drink increase in alcohol excise taxes

would raise $708 million in new revenue for the

State of Texas, and would result in an 8.6 percent

reduction in alcohol consumption.

If Texas raised its alcohol excise taxes by 10 cents per

drink, 46 percent of Texans would pay no additional

tax because they do not drink alcohol. An additional

32 percent—the moderate drinkers—would pay

an additional $4.53 per person per year in taxes.

Excessive and high-risk drinkers would pay 80

percent of the tax—an average of $26.64 per person—

because they do the bulk of the drinking.37

Among excessive and non-excessive drinkers, people

making more than $75,000 per year would pay more

per person than any other income group because

they tend to drink more alcohol.

That same 10 cent per drink increase in the alcohol

excise tax would create 15,189 new jobs in Texas,

as revenues shift from the alcohol industry to

government, health care and other relatively

labor-intensive sectors and services.55

A 10 cent per drink increase in alcohol excise taxes

would also save 402 lives in Texas. It would keep

66 babies from being born with fetal alcohol

syndrome, reduce teenage pregnancy by 359 cases,

and prevent 112 alcohol-impaired driving fatalities

in Texas, while preventing 113,205 cases of alcohol

abuse and dependence.

Executive Summary

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

2

IntroductionTexas has not increased its excise taxes on beer, wine and distilled spirits since 1984.1,2,i The current excise tax is less than two cents a drink on beer and wine and less than three cents a drink on distilled spirits. In 2013 the combined excise tax on beer, wine and spirits provided $208 million in revenue to the state, a number that stands in stark contrast to the $19 billionii it costs the citizens and the state of Texas in alcohol-related harm each year.3 Underage drinking alone cost Texas $2.1 billion, ten times the annual revenue collected in alcohol excise taxes.

This report assesses the potential effects of increases in the excise taxes on beer, wine and spirits in Texas. The report begins by describing alcohol consumption patterns in Texas for high school students, college students, and the general population, as well as the harms caused by their excessive consumption. This is followed by a discussion of alcohol taxes in Texas, including how inflation has eroded the value of the alcohol excise tax set in 1984 and contributed to the decreasing contribution of alcohol excise taxes in total tax revenue. The next section describes how much excessive alcohol use is costing the state of Texas, both overall and for the government specifically, and includes health care costs, productivity losses, and other alcohol-related costs. The costs are further broken down to those caused by underage and binge drinking. The penultimate section models the effects of an alcohol excise tax increase, highlighting the impact of the increase on consumption and revenue, health gains, alcohol attributable deaths, underage drinking, and fetal alcohol syndrome. The report concludes with a section providing evidence demonstrating that the arguments used in opposition to alcohol excise tax increases, including the impact on jobs and the costs to the average Texan, are false, misleading, or greatly overstated.

Alcohol Consumption in TexasHIGH SCHOOL ALCOHOL USE

Young people in Texas are drinking despite minimum age laws; for students in 7th-12th grade, alcohol use exceeds the use of tobacco and marijuana.4 In 2013, 67 percent of Texas high school students had consumed alcohol during their life, 36 percent had consumed at least one drink in the 30 days prior to the survey, and 21 percent had binge drunk in the 30 days prior to the survey.iii, 5 Drinking starts at an early age, with 18 percent of students in grades 9 through 12 reporting having had their first full drink of alcohol for the first time before the age of 13.6 In 2013, 10 percent of 12th graders reported extreme binge drinking.6,iv

i Texas has two kinds of alcohol-specific taxes: a mixed alcoholic beverage tax for consumption on-premises and an excise tax on beer, wine, and spirits. This report will focus specifically on Texas alcohol excise tax.

ii The number reported in the study is $16,524.8 million; the figure used has been updated to adjust for inflation and is reported in 2013 dollars. iii Binge drinking is defined as drinking five or more alcoholic drinks in one single occasion on at least 1 day for men, and 4 drinks for women. A single

occasion constitutes drinking all drinks at the same time or within a couple of hours of each other. The Youth Risk Behavior Surveillance System defines binge drinking as 5 or more drinks of alcohol in a row within a couple of hours for both men and women.

iv Extreme binge drinking is defined as drinking 10 or more drinks in one single occasion.

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

3

Young Texans are also engaging in risky behavior: 11 percent of students have driven a car one or more times when they have been drinking alcohol, and 29 percent have ridden one or more times in the last 30 days in a car driven by someone who had been drinking.6 In addition, Texas currently ranks 5th in the country in teen pregnancies,8 and has ranked as high as 3rd.7 Nearly one in four high school students report having drunk alcohol or used drugs before their last sexual encounter.6

COLLEGE ALCOHOL USE

Like Texas high school students, many more college students drink alcoholic beverages than use tobacco and marijuana. In Texas, approximately 81 percent of college students report having used alcohol in their lifetime, 75 percent report having had a drink in the last year, and 62 percent report having had a drink in the last month. Additionally, 43 percent of males and 38 percent of females report binge drinking in the last month.4 Drinking patterns vary by age: 75 percent of legal-aged students report drinking compared to 46 percent of underage students. That being said, obtaining alcohol is not difficult for underage college students, as 11 percent used fake IDs, 24 percent report being able to buy alcohol at bars and stores without being asked for an ID, and 78 percent report being able to obtain alcohol from someone over the age of 21.4

Risky sexual behavior is prevalent, with 56 percent of heavy drinkers and 25 percent of moderate drinkersv engaging in unprotected sex, and 47 percent of heavy drinkers engaging in unplanned sex at least once during the school year because of alcohol consumption. In addition, 25 percent of students report driving after drinking at least once in an average month, and 21 percent of students reported riding in a car with a peer that was high or drunk.4

Every year, 372 young people under the age of 21 die in Texas because of excessive alcohol use. The majority of these deaths are from motor vehicle traffic crashes, homicides, or suicides.9 In 2013 underage drinking cost Texans $2.1 billion, with the largest share of cost to the state coming from alcohol-related traffic crashes.9

ALCOHOL USE IN THE GENERAL POPULATION

Adults in Texas also drink alcohol: On average, 53 percent of adults in Texas drank in the last month, while 26 percent reported binge drinking.10

From 2007 to 2008, 1.3 million people, or 6.9 percent of the population ages 12 and above, fit the criteria for alcohol abuse or dependence; of these, 1.29 million required alcohol treatment for alcohol use, but did not receive any.vi,10 From 2011-2012, 6.7 percent of the Texas population fit this criteria; this percentage is similar to the United States average (6.6 percent) and has not changed significantly from 2008-2012.11 Heavy alcohol usevii among persons aged 21 or older is 6.9 percent, or approximately 1.2 million people. Of this group, only 3.2 percent received treatment for alcohol use.11

v According to the Dietary Guidelines for Americans, moderate drinking is up to 1 drink per day for women and up to 2 drinks per day for men.5

vi “Needing but not receiving treatment in the survey” refers to respondents classified as needing treatment for alcohol, but not receiving treatment for an alcohol problem at a specialty facility (i.e., drug and alcohol rehabilitation facilities [inpatient or outpatient], hospitals [inpatient only], and mental health centers).vii Heavy alcohol use is defined as drinking 5 or more drinks on the same occasion on each of 5 or more days in the past 30 days.

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

4

ALCOHOL USE AND HARM

Excessive alcohol usevii kills 6,5149 Texans each year. Alcohol-related harm occurs to non-drinkers as well as drinkers. With respect to crime, 11 percent of sexual assault offenders in Texas in 2012 reported being under the influence of alcohol at the time of their offense.12 Impaired driving was responsible for the deaths of 1,296 people; put differently, 38 percent of all traffic deaths were caused by a driver with a blood alcohol concentration of .08 g/dL or higher. For Texas, this figure represents a 7 percent increase in deaths from 2011.13 The Texas Department of Transportation reports 6,573 serious injury crashes due to driving under the influence (DUI) in which 9,447 people were seriously injured in 2012;14 in addition, there were 89,256 DUI arrests, a 1.8 percent increase from 2011.12 Underage arrests for DUIs constituted 8.3 percent of all DUI arrests.15

Alcohol Taxes and Inflation in TexasTexas has two kinds of alcohol-specific taxes: mixed beverage taxes and an alcohol excise tax. The state collects a mixed beverage gross receipts tax, which is set at 6.7 percent, and a mixed beverage sales tax, which is set at 8.25 percent, of the retail price as of January 1, 2014. These taxes are paid when establishments with a mixed beverage or private club permit sell alcoholic beverages. The mixed beverage sales taxes raised $568 million in fiscal year 2014,16 and these revenues will rise with inflation. However, the tax applies to only sales by mixed beverage or private club permit holders.

Excise taxes, in general, are placed on selected goods in addition to other types of taxes, such as a general sales tax. Excise taxes are paid by producers when they put alcohol into distribution in Texas and are then passed on to the consumer as part of the cost of alcohol. These taxes are imposed at the gallon level and vary by the type of alcohol. Alcohol excise taxes in Texas are low in comparison to other states. The excise tax on spirits in Texas is currently the 45th lowest in the nation.17 The wine excise tax is 43rd in the nation,18 and the beer excise tax is 30th.19 Because the taxes are levied on alcohol producers, the consumer does not actually see the alcohol excise tax as a line item when purchasing beer, wine, or spirits. The increase in taxes will, however, be paid for by the consumer through an increase in the retail price of alcoholic beverages. For alcoholic beverages, empirical evidence suggests that this price increase is usually larger than the actual excise tax increase, a phenomenon referred to as overshifting.20 In economics, overshifting occurs when a producer is able to pass along to the consumer the full amount of the excise tax increase and an additional price increase.

Since the excise tax on alcohol is based on the volume of the beverage, its value erodes over time because of inflation. The alcohol excise tax in Texas has not been indexed to keep up with inflation and thus, its effectiveness to generate revenue and to decrease excessive drinking and its consequences has declined significantly. Declining inflation-adjusted alcohol excise taxes and tax revenues are not a problem particular to Texas—federal, state and local governments across the country have all seen declines in real

viii Excessive alcohol consumption is defined as binge drinking (defined above) plus heavy drinking (defined as consuming more than one drink a day for women and more than two drinks for men) plus any alcohol consumed by underage drinkers plus any alcohol consumed by pregnant women.

The excise tax on spirits in Texas is currently the 45th lowest in the nation. The wine excise tax is 43rd

in the nation and the beer excise tax is 30th.

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

5

tax rates and tax collections, since most have failed to either increase the alcohol excise tax or index it for inflation. The result is that alcohol—and, in Texas, especially beer and wine—gets cheaper every year in comparison with other goods and services.

Figure 1 illustrates the erosion that occurs over time because of the lack of indexing for inflation. In 1984, a six-pack of beer had an excise tax rate of 11 cents after that year’s increase in the excise tax. Had the tax kept up with inflation, the current excise tax on a six-pack of beer would be 25 cents. This is equivalent to a 56 percent drop in the real value of the beer excise tax.

$0.11

$0.25

56%

0%

10%

20%

30%

40%

50%

60%

$

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Beer Excise Tax Indexed for Inflation Beer Excise Tax Not Indexed for Inflation

Percent of Value Lost due to Inflation

Source: Consumer Price Index -‐ All Urban Consumers 1984-‐2014, and author's calculalons

FIGURE 1: Beer Excise Taxes for a 6 Pack in Texas, 1984-2014

If Beer Tax Kept Up With Inflation From 1984

Had Texas simply indexed its current alcohol excise tax to keep up with inflation, the revenue generated in 2013 would have been $472 million, instead of $208 million. From beer alcohol excise taxes alone the excise tax collected would have been $236 million, instead of $104 million.

Figure 2 further illustrates the consequences of failing to increase excise taxes to keep up with inflation by comparing the contribution of combined alcohol taxes to total tax collections in Texas. In 1984, alcohol taxes accounted for two percent of total tax collections. The contribution of alcohol taxes was halved by 1996 and this takes into account the 1993 increase in the mixed beverage tax.21 In 2013, the combined tax contribution of alcohol excise taxes and the additional mixed beverage sales tax imposed in 1993 was less than one percent of all taxes collected. Furthermore, if only the excise tax portion of total alcohol tax revenues is used in this analysis, the revenue from alcohol excise taxes accounted for only two-tenths of one percent of total tax revenue in 2013.

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

6

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

2.2%

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

FIGURE 2: Combined Alcohol Tax Revenue as a Percent of

Total State Revenue Collections, 1984-2013

Source: Texas Transparency - State Finance 1984 - 2013 and author's calculations

The Costs of Alcohol UseExcessive alcohol use is the third leading cause of preventable death in the United States. Approximately 60 percent of these deaths are caused by diseases such as cirrhosis and strokes, while the remaining 40 percent of deaths are from fatal injuries, violence and other causes.22

In Texas, excessive alcohol consumption has many adverse consequences beyond the mortality figures cited above. In terms of health consequences, excessive alcohol use increases healthcare costs because of increased injuries and costly chronic health conditions, such as liver cirrhosis and fetal alcohol syndrome (FAS).

Like other studies, 3, 23 the costs included in this report follow the guidelines proposed in Guidelines for Cost of Illness Studies in the Public Health Service. Costs include both direct and indirect costs and exclude intangible costs such as pain, suffering and lost quality of life. The cost estimates used are from 2006 and contained in a study by Sacks and colleagues. The 2006 costs have been adjusted for inflation, using the CPI for all goods and services, to reflect costs in 2013 dollars.

Costs are categorized into healthcare costs, productivity loss-related costs, and other costs. Healthcare costs include the treatment costs for 54 fatal and nonfatal alcohol-related conditions (both alcohol dependence and FAS are included), research and prevention costs, insurance administration costs, and the cost of training substance abuse and mental health professionals. Productivity losses include: premature mortality; impaired productivity at work, home and while institutionalized; work-related absenteeism; crime related productivity losses, such as lost work days, to victims, and from incarcerations; and FAS-related productivity losses. Other costs include: property damage because of crimes and fire; criminal justice system costs, which include police protection, court system costs, correctional institutions, private legal costs and alcohol-related crimes such as driving under the influence; motor vehicle crashes; and FAS-related special education.3

... by 2013 the revenue from alcohol excise taxes accounted for two-tenths of one percent of total tax revenue.

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

7

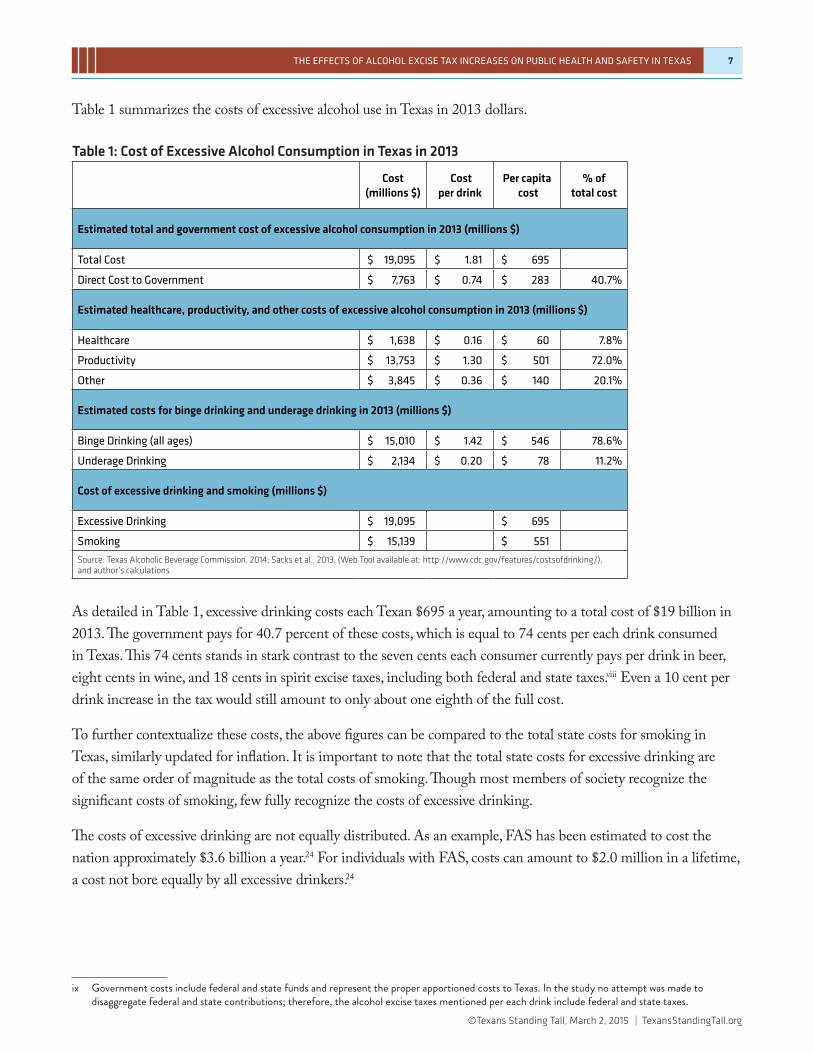

Table 1 summarizes the costs of excessive alcohol use in Texas in 2013 dollars.

Table 1: Cost of Excessive Alcohol Consumption in Texas in 2013

Cost (millions $)

Cost per drink

Per capita cost

% of total cost

Estimated total and government cost of excessive alcohol consumption in 2013 (millions $)

Total Cost $ 19,095 $ 1.81 $ 695

Direct Cost to Government $ 7,763 $ 0.74 $ 283 40.7%

Estimated healthcare, productivity, and other costs of excessive alcohol consumption in 2013 (millions $)

Healthcare $ 1,638 $ 0.16 $ 60 7.8%

Productivity $ 13,753 $ 1.30 $ 501 72.0%

Other $ 3,845 $ 0.36 $ 140 20.1%

Estimated costs for binge drinking and underage drinking in 2013 (millions $)

Binge Drinking (all ages) $ 15,010 $ 1.42 $ 546 78.6%

Underage Drinking $ 2,134 $ 0.20 $ 78 11.2%

Cost of excessive drinking and smoking (millions $)

Excessive Drinking $ 19,095 $ 695

Smoking $ 15,139 $ 551

Source: Texas Alcoholic Beverage Commission, 2014; Sacks et al., 2013, (Web Tool available at: http://www.cdc.gov/features/costsofdrinking/), and author’s calculations

As detailed in Table 1, excessive drinking costs each Texan $695 a year, amounting to a total cost of $19 billion in 2013. The government pays for 40.7 percent of these costs, which is equal to 74 cents per each drink consumed in Texas. This 74 cents stands in stark contrast to the seven cents each consumer currently pays per drink in beer, eight cents in wine, and 18 cents in spirit excise taxes, including both federal and state taxes.viii Even a 10 cent per drink increase in the tax would still amount to only about one eighth of the full cost.

To further contextualize these costs, the above figures can be compared to the total state costs for smoking in Texas, similarly updated for inflation. It is important to note that the total state costs for excessive drinking are of the same order of magnitude as the total costs of smoking. Though most members of society recognize the significant costs of smoking, few fully recognize the costs of excessive drinking.

The costs of excessive drinking are not equally distributed. As an example, FAS has been estimated to cost the nation approximately $3.6 billion a year.24 For individuals with FAS, costs can amount to $2.0 million in a lifetime, a cost not bore equally by all excessive drinkers.24

ix Government costs include federal and state funds and represent the proper apportioned costs to Texas. In the study no attempt was made to disaggregate federal and state contributions; therefore, the alcohol excise taxes mentioned per each drink include federal and state taxes.

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

8

To further illustrate this statement, consider the cost of underage drinking, $2.1 billion a year, a cost that is paid by all Texans but is caused by underage adults who choose to break the law and drink.

Figure 3 further compares the total cost of excessive alcohol use, $19 billion, and the share of the cost that the government pays, $7.7 billion, to the total alcohol revenue collected for all alcohol imposed taxes, $977 million, and the total alcohol excise tax revenue, $208 million. There is no doubt that production and consumption of alcohol generates tax revenue, but at the current rates, this benefit is dwarfed by the costs caused by excessive alcohol use.

FIGURE 3: The Cost of Excessive Alcohol Consumption and

Total Alcohol Tax Collections in 2013

$19, 095

$7,763

$2,134$977

$208$

$5,000

$10,000

$15,000

$20,000

2013

Dol

lars

(in

Mill

ions

of D

olla

rs)

Total Cost

Governmental Cost

Underage Drinking Cost

Total Alcohol Tax Collections*

Total Alcohol Excise Tax Collections

Source: Texas Alcoholic Beverage Commission, 2013; Texas Transparency - State Finance 2013; Sacks et al., 2013, and author's calculations

* Total Alcohol Tax Collections include: mixed beverage tax, beer, wine , liquor and malt excise tax, and airline/passenger train beverage tax.

Lastly, it is important to note that these estimates are substantially underestimated. Limitations include: the inability to estimate household productivity for stay-at-home parents and to calculate the lack of productivity because of “hangovers”; inaccurate mortality and morbidity totals that were estimated based on alcohol being the primary cause of death or illness and do not include contributing causes that were alcohol-related; and the omission of intangible costs—one study that analyzed the cost of underage drinking estimated that intangible costs were twice as large as tangible costs.25

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

9

Modeling the Effects of a Tax IncreaseCONSUMPTION AND INCREASED TAX REVENUE

Empirical evidence suggests that alcohol tax-induced price increases are fully passed on to consumers by producers in a one to two ratio.20 In other words, a 10 cent increase in alcohol excise taxes will actually lead to a 10 to 20 cent price increase. This is an important point because even though the tax is levied on suppliers, the actual cost of the tax is fully passed on to consumers in the form of price increases. Like other goods, the demand for alcohol conforms to the fundamental principles of economics, with the quantity demanded of alcohol increasing as prices fall and decreasing as prices rise. The Community Guide recently analyzed 73 studies regarding the relationship between alcohol consumption and prices and confirmed that this basic principle of economics applies to alcohol demand.26 Their comprehensive review also concluded that higher prices on beer, wine and spirits not only decrease consumption by the general population, but they also decrease the consumption by heavy drinkers. A section below focuses on the effect that higher prices have on consumption by young adults and underage drinkers.

Modeling the change in consumption that will occur because of an excise tax increase involves applying the price elasticity of demand. The price elasticity of demand is a measure used by economists to estimate the price sensitivity of consumers. It predicts how much consumption will change as a result of a change in price. For instance, an elasticity of -0.70 implies that a 10 percent increase in price would lead to a 7 percent drop in consumption. The estimates below use the elasticity estimates provided in the Community Guide Review. These elasticities are -0.50 for beer, -0.64 for wine, and -0.79 for spirits, and represent the median value of elasticities found in the Community Guide’s systematic review of studies.

Table 2: Changes in Consumption Given Various Excise Tax Increases Proposed Tax Increase per Drink

$ 0.05 $ 0.10 $ 0.25 $ 0.30

Reduction in Spirit Consumption -5.8% -11.5% -28.9% -34.6%

Reduction in Wine Consumption -3.5% -7.0% -17.5% -21.1%

Reduction in Beer Consumption -4.2% -8.4% -21.0% -25.2%

Increase in Alcohol Excise Tax Revenue (in millions) $ 383.00 $ 707.99 $ 1,419.35 $ 1,568.59

Source: Texas Alcoholic Beverage Commission, 2014 and author’s calculations

Table 2 shows the percentage decrease in the consumption of beer, wine, and spirits given various hypothetical tax increases per drink. In addition, the table shows how much excise tax collections would increase. From this simulation, it is important to note the “win-win” nature of alcohol excise tax increases: even relatively small price changes result in modest decreases in consumption (especially for the five cent and ten cent scenario) but are accompanied by considerably larger revenue gains to the state, $383 and $708 million respectively. Under the ten cent scenario, the additional revenue generated effectively quadruples the alcohol excise tax collections from 2013. Because demand for alcohol is somewhat inelastic, even when consumption decreases as the result of an excise tax increase, revenue to the state of Texas will increase considerably, not decrease.

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

10

HEALTH GAINS

As estimated above, a 10 cent tax increase per drink would reduce the consumption of beer (8.4 percent), wine (7 percent), and spirits (11.5 percent), but these are not the only effects that an increase in excise taxes would have. These reductions in consumption will be accompanied by large health gains. Based on the existing research literature, a 10 percent increase in the price of alcohol can be expected to reduce instances of drinking and driving by men by 7.4 percent and by women by 8.1 percent.27 Higher alcohol prices also lead to reductions in cirrhosis,28, 29 rape and robbery,30 violent behavior towards children,31 sexually transmitted diseases32 and suicide rates.33, 34 One recent study on alcohol tax increases and their benefits estimates that a doubling of the federal alcohol tax would reduce alcohol-related mortality by 35 percent, traffic fatalities by 11 percent, sexually transmitted disease by six percent, violence by two percent and crime by 1.4 percent.35

Table 3: Reductions in Mortality, Illness, Teenage Pregnancy, and Underage Drinking in Texas as a Result of Alcohol Excise Tax Increases

Expected Reduction with Tax Increase

Total Number

Percent Attributable to Alcohol Consumption

Total Attributable to Alcohol Consumption

5 Cent Tax Increase per Drink

10 Cent Tax Increase per Drink

25 Cent Tax Increase per Drink

30 Cent Tax Increase per Drink

Mortality

Traffic Deaths 3,3982 38%2 1,2962 59 112 244 266

Homicides 1,3636 47% 6411 29 55 121 132

Alcoholic Liver Disease 10836 100%1 1,083 49 93 204 223

Liver Cirrhosis 22746 40%1 910 41 78 171 187

Alcohol Abuse 826 100%1 82 4 7 15 17

Suicide 2,8896 23%1 664 30 57 125 137

TOTAL 212 402 880 962

Illness and Teenage Pregnancy

Fetal Alcohol Syndrome 771*, 5 100%1 771 35 66 145 158

Teenage Pregnancy 48,4243 9% 4,1654 189 359 785 856

Alcohol Dependence or Abuse

1,313,0005 100% 1,313,000 59,693 113,205 247,462 269,758

Heavy Alcohol Use 1,200,0005 100% 1,200,000 54,555 103,462 226,165 246,542

Prevalence of Underage Drinking

Underage Drinking in the past 30 days (15-18 year olds)

1,512,9327 36%**, 8 544,656 24,762 46,959 102,651 111,901

Underage Binge Drinking (15-18 year olds)

1,512,9327 21%***, 8 317,716 14,444 27,393 59,880 65,275

Source: 1) Alcohol Related Disease Impact (ARDI) application, 2013; 2) U.S. Department of Transportation National Highway Traffic Safety Administration. 2012 Motor Vehicle Crashes: Overview; 3) Texas Department of State Health Services; 4) Underage Drinking Enforcement Training Center. Underage Drinking in Texas: The Facts; 5) SAMHSA; 6) Compressed Mortality 2010, Underlying Causes of Death from CDC WONDER; 7) American Fact Finder; 8) YRBSS; and author’s calculations.

* Calculated using 2010 live births in Texas (385,746) and approximated that there are 2 cases of FAS per 1,000 live births per CDC studies.

** Refers to the percentage of 15 to 18 year olds that drank alcohol in the past 30 days.

*** Refers to the percentage of 15 to 18 year olds that binge drank in the past 30 days.

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

11

Table 3 models the reductions that would occur in mortality, illness, teenage pregnancy and underage drinking rates given various excise tax increase scenarios. These estimates assume that increases in the alcohol excise tax would affect all alcohol consumers equally, and therefore are likely to underestimate the true impact. A 10 cent increase per drink would prevent 112 alcohol-related traffic fatalities, 55 homicides, 93 deaths from alcoholic liver disease, 78 deaths from liver cirrhosis, seven deaths from alcohol abuse, and 57 suicides each year, for a total of 402 deaths prevented per year. In addition, 66 babies would not be born with FAS, and there would be 359 fewer teenage pregnancies annually. Finally, the tax increase would prevent 113,205 cases of alcohol dependence and abuse, 103,462 cases of heavy alcohol use, 46,959 cases of underage drinking among high school students, and 27,393 instances of binge drinking by underage drinkers ages 15-18.

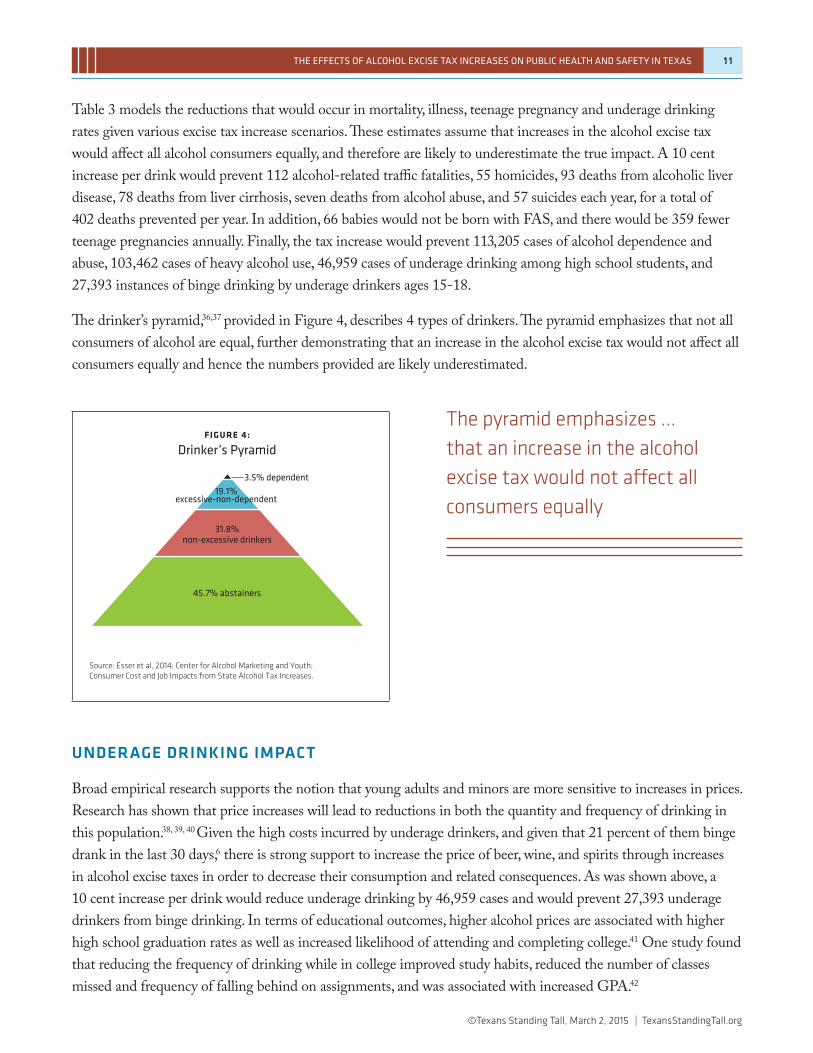

The drinker’s pyramid,36,37 provided in Figure 4, describes 4 types of drinkers. The pyramid emphasizes that not all consumers of alcohol are equal, further demonstrating that an increase in the alcohol excise tax would not affect all consumers equally and hence the numbers provided are likely underestimated.

FIGURE 4: Drinker’s Pyramid

Source: Esser et al, 2014; Center for Alcohol Marketing and Youth: Consumer Cost and Job Impacts from State Alcohol Tax Increases.

3.5% dependent

19.1%excessive-non-dependent

45.7% abstainers

31.8%non-excessive drinkers

UNDERAGE DRINKING IMPACT

Broad empirical research supports the notion that young adults and minors are more sensitive to increases in prices. Research has shown that price increases will lead to reductions in both the quantity and frequency of drinking in this population.38, 39, 40 Given the high costs incurred by underage drinkers, and given that 21 percent of them binge drank in the last 30 days,6 there is strong support to increase the price of beer, wine, and spirits through increases in alcohol excise taxes in order to decrease their consumption and related consequences. As was shown above, a 10 cent increase per drink would reduce underage drinking by 46,959 cases and would prevent 27,393 underage drinkers from binge drinking. In terms of educational outcomes, higher alcohol prices are associated with higher high school graduation rates as well as increased likelihood of attending and completing college.41 One study found that reducing the frequency of drinking while in college improved study habits, reduced the number of classes missed and frequency of falling behind on assignments, and was associated with increased GPA.42

The pyramid emphasizes ... that an increase in the alcohol excise tax would not affect all consumers equally

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

12

FETAL ALCOHOL SYNDROME IMPACT

Fetal Alcohol Effects, Fetal Alcohol Syndrome or Fetal Alcohol Spectrum Disorder are the various terms used to describe the range of effects that can occur to an individual if exposed to alcohol in utero. Some of these effects may include physical, mental, behavioral, and/or learning disabilities and can have both short- and long-term implications.43 While studies take the cost of Fetal Alcohol Syndrome (FAS) into account when estimating the economic cost of excessive alcohol consumption,23,44,45 no study to date has estimated the direct impact of alcohol excise taxes on FAS. However, as described above, empirical studies have shown that increasing alcohol excise taxes reduces all aspects of drinking in all populations,46 which includes women of childbearing age and pregnant women. Given this evidence, it is almost certain that higher alcohol taxes would reduce FAS rates.

Experience in tobacco is relevant to this issue. Empirical research on the effects of increases in cigarette excise taxes has shown that an increase in cigarette taxes leads to decreases in the smoking rates of pregnant women and to higher average birth weights.47 More specifically, a 10 percent increase in the price of cigarettes leads to reduced smoking rates of seven percent for pregnant women. Estimates that include the effect of higher prices on the decision of a pregnant woman to smoke conclude that pregnant women are responsive to price increases, including those with the highest smoking rates.48

Tax Increase OppositionIncreases in alcohol excise taxes will decrease alcohol consumption and therefore negatively impact the income of beer, wine and spirit producers. The most common arguments used by the alcohol (and tobacco) industry to oppose an increase in excise taxes are as follows: 1) the tax increase won’t have the intended impact in terms of reducing consumption and its consequences; 2) the tax increase will not generate a significant increase in tax revenues; 3) the tax increase could disproportionately affect poor individuals and working class consumers; 4) the tax increase will lead to massive job losses; and 5) the tax increase will lead to tax avoidance and evasion. The empirical evidence refuting the first two of these counterarguments has been described above: there is abundant empirical evidence that alcohol tax increases lead to significant reductions in excessive drinking and its consequences, while generating higher tax revenues. The remaining arguments are discussed in this section.

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

13

IMPACT ON THE AVERAGE TEXAN

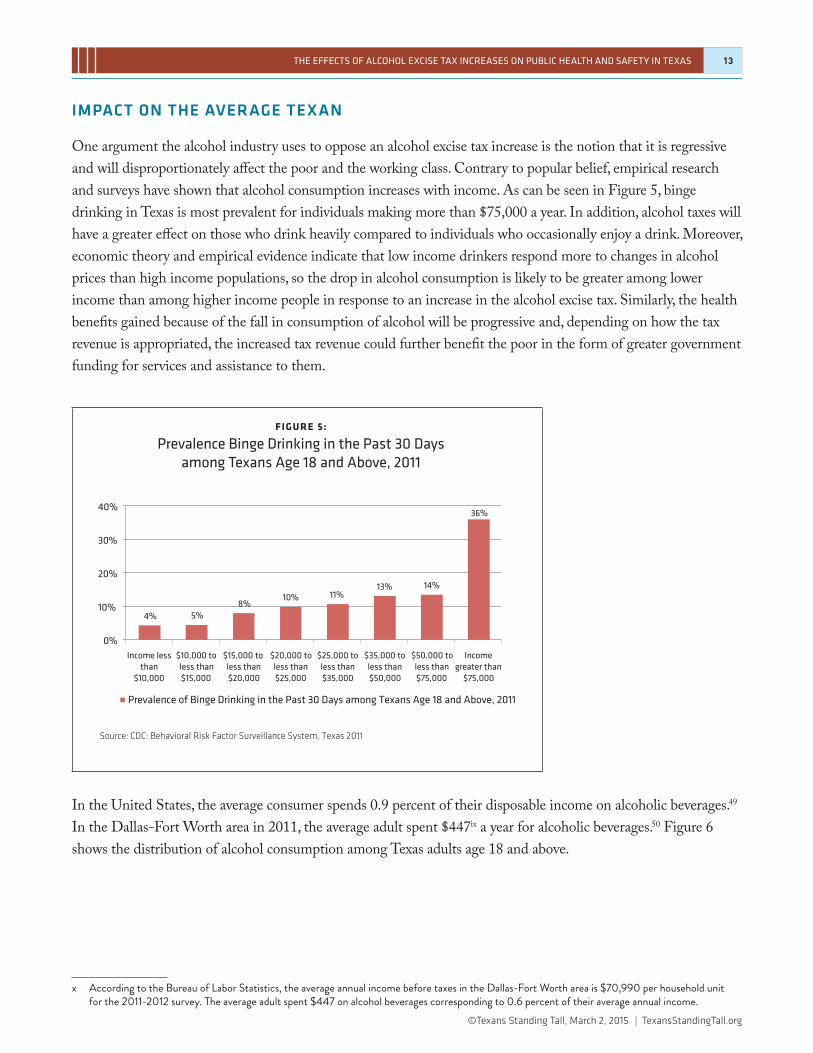

One argument the alcohol industry uses to oppose an alcohol excise tax increase is the notion that it is regressive and will disproportionately affect the poor and the working class. Contrary to popular belief, empirical research and surveys have shown that alcohol consumption increases with income. As can be seen in Figure 5, binge drinking in Texas is most prevalent for individuals making more than $75,000 a year. In addition, alcohol taxes will have a greater effect on those who drink heavily compared to individuals who occasionally enjoy a drink. Moreover, economic theory and empirical evidence indicate that low income drinkers respond more to changes in alcohol prices than high income populations, so the drop in alcohol consumption is likely to be greater among lower income than among higher income people in response to an increase in the alcohol excise tax. Similarly, the health benefits gained because of the fall in consumption of alcohol will be progressive and, depending on how the tax revenue is appropriated, the increased tax revenue could further benefit the poor in the form of greater government funding for services and assistance to them.

FIGURE 5: Prevalence Binge Drinking in the Past 30 Days

among Texans Age 18 and Above, 2011

4% 5%8%

10% 11%13% 14%

36%

0%

10%

20%

30%

40%

Income lessthan

$10,000

$10,000 toless than$15,000

$15,000 toless than$20,000

$20,000 toless than$25,000

$25,000 toless than$35,000

$35,000 toless than$50,000

$50,000 toless than$75,000

Incomegreater than

$75,000

Prevalence of Binge Drinking in the Past 30 Days among Texans Age 18 and Above, 2011

Source: CDC: Behavioral Risk Factor Surveillance System, Texas 2011

In the United States, the average consumer spends 0.9 percent of their disposable income on alcoholic beverages.49 In the Dallas-Fort Worth area in 2011, the average adult spent $447ix a year for alcoholic beverages.50 Figure 6 shows the distribution of alcohol consumption among Texas adults age 18 and above.

x According to the Bureau of Labor Statistics, the average annual income before taxes in the Dallas-Fort Worth area is $70,990 per household unit for the 2011-2012 survey. The average adult spent $447 on alcohol beverages corresponding to 0.6 percent of their average annual income.

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

14

FIGURE 6: Distribution of Alcohol Consumption Among

Adults (age 18+) in Texas’s Population

22%

32%

46%Excessive Drinkers

Non-Excessive Drinkers

Abstainers

Source: Center for Alcohol Marketing and Youth:Consumer Costs and Job Impacts from State Alcohol Tax Increases

Table 4 models what an excessive and non-excessive drinker in Texas would pay in taxes after an alcohol excise tax increase. As the table shows, taxes are a much more targeted intervention than is often assumed. A ten cent increase per drink would cost the average Texan who does not drink excessively only $4.53 a year; in contrast, excessive drinkers would pay an additional $26.64 a year.37 The majority of the tax increase will be paid by excessive drinkers, who make up 22 percent of Texas residents. The fact that 22 percent of the population will pay six times as much as a non-excessive drinker (46 percent of the population) demonstrates the effectiveness of alcohol taxation. Lastly, 32 percent of Texans would pay no additional tax because they do not drink.

Table 4: Cost of Tax Increase to Excessive and Non-Excessive Drinker Proposed Tax Increase per Drink

$ 0.05 $ 0.10 $ 0.25 $ 0.30

Cost to Excessive Drinker $ 13.97 $ 26.64 $ 56.86 $ 61.98

Cost to Non-Excessive Drinker $ 2.38 $ 4.53 $ 9.67 $ 10.54

Source: Center for Alcohol Marketing and Youth: Consumer Costs and Job Impacts from State Alcohol Tax Increases and author’s calculations.

PRODUCTIVITY AND JOBS IMPACT

For the alcohol industry the fall in income is a huge motivator to use its influence in politics. From 2008 to 2014, the alcohol industry donated more than $51 million to federal political campaigns.51 In Texas the alcohol industry is one of the top 15 contributors to state campaigns: in 2012, contributions were close to $3 million.52 The Beer Institute, the leading national lobbying body for beer producers, claims that the beer industry in Texas is responsible for 160,390 jobs, and that these jobs generate $3,135 million in business and personal taxes and $915 million in consumption taxes.53 Institutions such as the Beer Institute argue that excise tax increases will lead to declines in employment and tax collections.

The majority of the tax increase will be paid by excessive drinkers, who make up 22 percent of Texas residents.

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

15

This argument has two central flaws. First, according to the federal Bureau of Labor Statistics, Texas has 1.2 million jobs in the “leisure and hospitality” sector.54 Thus the Beer Institute is claiming that 13 percent, or one in eight jobs in the leisure and hospitality sector is in place entirely because of beer sales. It is doubtful that beer’s economic impact is that widespread.

The second flaw is that it assumes that individuals and their families will not spend the money they save on alcohol purchases on other goods and services in the economy, and the government revenues raised by a tax (and shifted from alcohol producers) will somehow disappear from the economy. The alcoholic beverage industry’s job estimates look at the impact in only their own industry. They do not account for the jobs created by increased consumer spending on other goods and services when spending on alcohol is reduced in response to tax increases as well as the jobs created by government spending of new alcohol tax revenues.55

One recent study estimated the net impact of state alcohol tax increases on jobs, accounting for changes in consumer spending resulting from the tax increase as well as government spending of new tax revenues. Placing the funds generated by a 5 cent, 10 cent, 25 cent and 30 cent excise tax increase per drink into the Texas General Fund would generate estimated net increases of 7,852; 15,189; 34,774; and 38,947 jobs respectively. If the new tax revenues were instead earmarked for health care, an estimated 1,206; 2,332; 5,348; and 5,990 net jobs would be created, respectively, for each excise tax increase scenario. As an example, funds earmarked for healthcare could be used to increase support for addiction treatment and prevention programs (such as those to increase awareness and provide treatment for FAS).

It is important to note that the simulated net increase in generated jobs was calculated by accounting for changes in individual purchases of alcoholic beverages, changes in purchases of other goods and services, and government spending of new alcohol excise tax revenues. In other words, the loss of jobs resulting from the decrease in beer, wine and spirit consumption is fully taken into account and is more than made up for with the creation of jobs in other sectors, resulting in a net increase in jobs.

Table 5: Net Increase in Jobs in Year Following, Given Various Excise Tax Increases Proposed Tax Increase per Drink

$ 0.05 $ 0.10 $ 0.25 $ 0.30

Net Increase in Jobs 7,852 15,189 34,774 38,947

Net Increase in Health Care Jobs (if tax earmarked) 1,206 2,332 5,348 5,990

Source: Wada et al., 2014 (Web Tool available at: http://www.camy.org/action/taxes/taxtool/index.html) and author’s calculations

In addition, the net gain in jobs described does not take into account the productivity improvements and decrease in “hangovers” that will occur because of the decrease in consumption of beer, wine, and spirits. Ensuring Solutions to Alcohol Problems, a group funded by The Pew Charitable Trusts, estimates that a hypothetical 100 employee firm in Texas has nine problem drinkers. This hypothetical firm loses two working days a month due to sickness, injury and absence because of alcohol use. In addition, this hypothetical firm has alcohol-related health care costs of $60,573 a year.56

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

16

TAX AVOIDANCE AND EVASION

While tax avoidance and evasion might seem like a legitimate concern, it is important to keep in mind that alcohol excise tax increases represent only a small percentage of the final price paid for alcoholic beverages. For the average consumer it would be costly to avoid and evade paying the increase in alcohol excise taxes. Experience in the few states that have increased alcoholic beverage excise taxes in recent years suggests that there is little to no cross-border shopping following the tax increase. Illinois, for example, raised its alcohol taxes in September 2009. After the increase, the beer tax in Illinois (23.1 cents per gallon) was higher than those in the neighboring states of Indiana (11.5 cents per gallon), Iowa (19 cents per gallon) and Wisconsin (6.45 cents per gallon). Following the tax increase, Illinois beer tax revenues went up by 22.7 percent, while tax revenues went down by 3.6, 1.0 and 4.2 percent in Indiana, Iowa, and Wisconsin, respectively, suggesting that Illinois beer drinkers living near state borders did not leave the state to buy beer in an effort to avoid the tax increase.57

ConclusionAlcohol excise tax increases are effective in reducing consumption, improving health outcomes, enhancing productivity, creating jobs, and reducing the high costs associated with excessive drinking, while providing much needed revenue to the state of Texas. Heavy drinkers will pay the vast majority of the excise tax increases, but they and their families and communities will also benefit the most. A ten cent increase in the tax on a drink will generate $708 million in new tax revenues, despite the reductions in alcohol consumption that would result. The evidence presented in this report demonstrates that an increase in alcohol excise taxes will be beneficial to the state of Texas without having a negative economic impact on the state. These conclusions are not unique: in their landmark 2004 report Reducing Underage Drinking: A Collective Responsibility,58 the National Research Council and the Institute of Medicine, the leading scientific advisory bodies to the U.S. Congress, called for Congress to increase alcohol excise taxes as a central part of a comprehensive plan to reduce underage drinking and related consequences.

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

17

About the AuthorsMegan C. Diaz is a PhD Candidate in the Department of Economics at the University of Illinois at Chicago. Her fields of focus are Health Economics and Public Finance. She is a Research Assistant at the Institute for Health and Research Policy’s Health Policy Center, where her research and work focuses on tobacco markets, tobacco use, tobacco marketing, new and emerging tobacco products, and tobacco prices and taxes. She has collaborated with leading researchers in the field of tobacco economics, including Dr. Frank Chaloupka, Dr. John Tauras, and others; pending publications include “Economic Impact of Arkansas’ Tobacco Tax Increase on Low-Income Households in Arkansas” with the Centers for Disease Control and “Are Vaping Products Displacing Cigarettes? Evidence from Nielsen Retail Data, 2007-2013.”

Frank J. Chaloupka, Ph.D. is a Distinguished Professor at the University of Illinois at Chicago (UIC), where he has been on the faculty since 1988. He is Director of the UIC Health Policy Center and Director of the World Health Organization Collaborating Centre on the Economics of Tobacco and Tobacco Control. Dr. Chaloupka holds appointments in the College of Liberal Arts and Sciences’ Department of Economics and the School of Public Health’s Division of Health Policy and Administration. He is a Fellow at the University of Illinois’ Institute for Government and Public Affairs, and is a Research Associate in the National Bureau of Economic Research’s Health Economics Program and Children’s Program. Dr. Chaloupka is Co-Director of Bridging the Gap: Research Informing Policy and Practice for Healthy Youth Behavior and Director of BTG’s ImpacTeen Project. He is also Co-Director of the International Tobacco Evidence Network. Hundreds of publications and presentations have resulted from Dr. Chaloupka’s research on the effects of economic, policy, and environmental factors on health behavior, including tobacco use, drinking, drug use, diet, physical activity, and related outcomes.

David H. Jernigan, Ph.D. is an Associate Professor in the Department of Health, Behavior and Society and the Director of the Center on Alcohol Marketing and Youth at the Johns Hopkins Bloomberg School of Public Health, where he teaches courses on media advocacy and alcohol policy. He also leads two other research projects: a collaboration with Boston University School of Public Health looking at youth alcohol brand preference and brand-level exposure to alcohol marketing, and a four-university collaborative examining the social and health effects of changes in alcohol pricing. He has worked as an adviser to the World Health Organization (WHO) and the World Bank, was principal author of WHO’s first Global Status Report on Alcohol and Global Status Report on Alcohol and Youth, and co-authored Media Advocacy and Public Health: Power for Prevention and Alcohol in the Developing World: A Public Health Perspective.

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

18

About Texans Standing TallTexans Standing Tall (TST) is the statewide coalition working to make alcohol, tobacco, and other drugs irrelevant in the lives of youth by creating healthier and safer communities. Research indicates that the most effective ways to reduce youth substance use at statewide and community levels are policy and environmental changes. As such, TST strives to implement and train others to use evidence-based community prevention strategies to reduce alcohol, tobacco, and other drug use among Texas youth.

Raising alcohol excise taxes is proven to reduce underage and risky alcohol use and associated negative consequences. In 2002, TST commissioned Texas Perspectives, Inc. to prepare the report “The Fiscal Impact of Raising Texas Alcohol Taxes.” Because alcohol use among youth in Texas remains high, and the impact of excessive alcohol use on all Texans is unparalleled, Texans Standing Tall commissioned the authors to prepare an updated report on the impact of increasing alcohol excise taxes in Texas.

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

19

1. Alcoholic Beverage Code - Title 5. Taxation. (1984). at http:// www.statutes.legis.state.tx.us/Docs/AL/htm/AL.201.htm

2. Texas Alcoholic Beverage Commission. The History of the Texas Alcoholic Beverage Commission. (2005). at http://www.tabc.state.tx.us/about_us/history/70HistoryBook.pdf

3. Sacks, J. J. et al. State Costs of Excessive Alcohol Consumption, 2006. Am. J. Prev. Med. 45, 474–485 (2013).

4. Department of State Health Services. Texas School Survey of Substance Use Among College Students. (2013). at http://www.utexas.edu/research/cswr/gcattc/docu-ments/2013CollegeSurvey.pdf

5. Drinking Levels Defined | National Institute on Alcohol Abuse and Alcoholism (NIAAA). at http://www.niaaa.nih.gov/alcohol-health/overview-alcohol-consumption/moderate- binge-drinking

6. Centers for Disease Control and Prevention. Youth Risk Behavior Surveillance System Texas 2013 Results. at http://nccd.cdc.gov/youthonline/App/Results.aspx?LID=TX

7. Guttmacher Institute. U.S. Teenage Pregnancies, Births and Abortions, 2008: State Trends by Age, Race and Ethnicity. (2013). at http://www.guttmacher.org/pubs/USTPtrendsState08.pdf

8. The Office of Adolescent Health, U.S. Department of Health and Human Services. Texas Adolescent Reproductive Health Facts. at http://www.hhs.gov/ash/oah/

9. Centers for Disease Control and Prevention. Alcohol-Related Disease Impact (ARDI) application. (2013). at http://apps.nccd.cdc.gov/DACH_ARDI/Default.aspx.

10. Substance Abuse and Mental Health Services Administration (SAMHSA). State Estimates of Substance Use from the National Survey on Drug Use and Health, 2008-2009 and 2009-2010. at http://www.samhsa.gov/data/sites/default/files/NSDUHStateEst2009-2010/AdultTabs/NSDUHsaeAdultTabs2010.htm

11. Substance Abuse and Mental Health Services Administration (SAMHSA). Behavioral Health Barometer: Texas, 2013. (2013). at http://www.samhsa.gov/data/StatesInBrief/2k14/Texas_BHBarometer.pdf

12. Department of Public Safety. Annual Report of 2012 UCR Data Collection: Crime in Texas Overview. (2012). at http://www.txdps.state.tx.us/director_staff/public_information/2012CIT.pdf

13. U.S. Department of Transportation National Highway Traffic Safety Administration. Traffic Safety Facts Research Note. (2013). at http://www-nrd.nhtsa.dot.gov/Pubs/811856.pdf

14. Texas Department of Transportation. Total and DUI (Alcohol) Fatal and Injury Crashes Comparison. (2012). at http://ftp.dot.state.tx.us/pub/txdot-info/trf/crash_statistics/2012/35_2012.pdf

15. Texas Department of Public Safety. Selected Non-Index Crimes: DUI Arrests from The Texas Crime Report for 2012. (2012). at http://www.txdps.state.tx.us/crimereports/12/citCh4.pdf

16. Texas Transparency. Revenue by Category. (2014). at http://www.texastransparency.org/State_Finance/Revenue/Revenue_by_Category.php

17. Tax Foundation. Map: Spirits Excise Tax Rates by State, 2014. at http://taxfoundation.org/blog/map-spirits-excise-tax-rates-state-2014

18. Tax Foundation. Map: Wine Excise Tax Rates by State, 2014. at http://taxfoundation.org/blog/map-wine-excise-tax-rates-state-2014

19. Tax Foundation. Map: Beer Excise Tax Rates by State, 2014. at http://taxfoundation.org/blog/map-beer-excise-tax-rates-state-2014

20. Kenkel, D. S. Are Alcohol Tax Hikes Fully Passed through to Prices? Evidence from Alaska. Am. Econ. Rev. 95, 273–277 (2005).

21. Tax Code Chapter 183. Mixed Beverage Taxes. 934 (1994). at http://www.statutes.legis.state.tx.us/Docs/TX/htm/TX.183.htm

22. Centers for Disease Control and Prevention. Alcohol-Attribut-able Deaths and Years of Potential Life Lost — United States, 2001. at http://www.cdc.gov/mmwr/preview/mmwrhtml/mm5337a2.htm

23. Bouchery, E. E., Harwood, H. J., Sacks, J. J., Simon, C. J. & Brewer, R. D. Economic Costs of Excessive Alcohol Consumption in the U.S., 2006. Am. J. Prev. Med. 41, 516–524 (2011).

24. Texas Office for the Prevention of Developmental Disabilities. Fetal Alcohol Spectrum Disorder (FASD). at http://www.topdd.state.tx.us/fasd/

References

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

20

25. Miller, T. R., Levy, D. T., Spicer, R. S. & Taylor, D. M. Societal Costs of Underage Drinking. J. Stud. Alcohol Drugs 67, 519 (2006).

26. Community Preventive Services Task Force. The Community Guide-Summary-Excessive Alcohol Consumption: Increasing Alcohol Taxes. at http://www.thecommunityguide.org/alcohol/increasingtaxes.html

27. Kenkel, D. S. Drinking, Driving, and Deterrence: The Effectiveness and Social Costs of Alternative Policies. J. Law Econ. 36, 877–913 (1993).

28. Cook, P. J. & Tauchen, G. The Effect of Liquor Taxes on Heavy Drinking. Bell J. Econ. 13, 379–390 (1982).

29. Cook, Philip J. The Effect of Liquor Taxes on Drinking, Cirrhosis, and Auto Fatalities. (1981). at http://www.nap.edu/openbook.php?record_id=114&page=271

30. Cook, P. J. & Moore, M. J. Violence Reduction Through Restrictions on Alcohol Availability. (Cover story). Alcohol Health Res. World 17, 151 (1993).

31. Markowitz, S. & Grossman, M. The Effects of Beer Taxes on Physical Child Abuse. J. Health Econ. 19, 271–282 (2000).

32. Chesson, H., Harrison, P. & Kassler, W. J. Sex under the Influence: The Effect of Alcohol Policy on Sexually Transmitted Disease Rates in the United States. J. Law Econ. 43, 215–238 (2000).

33. Sloan, F. A., Reilly, B. A. & Schenzler, C. Effects of Prices, Civil and Criminal Sanctions, and Law Enforcement on Alcohol-Related Mortality: J. Stud. Alcohol Drugs 55, 454 (1994).

34. Markowitz, S., Chatterji, P. & Kaestner, R. Estimating the Impact of Alcohol Policies on Youth Suicides. J. Ment. Health Policy Econ. 6, 37–46 (2003).

35. Wagenaar, A. C., Tobler, A. L. & Komro, K. A. Effects of Alcohol Tax and Price Policies on Morbidity and Mortality: A Systematic Review. Am. J. Public Health 100, 2270–2278 (2010).

36. Esser, M. B. et al. Prevalence of Alcohol Dependence Among US Adult Drinkers, 2009–2011. Prev. Chronic. Dis. 11, (2014).

37. Center for Alcohol Marketing and Youth. Consumer Costs and Job Impacts from State Alcohol Tax Increases. Johns Hopkins Bloom. Sch. Public Health at http://www.camy.org/action/taxes/taxtool/index.html

38. Chaloupka, F. J., Grossman, M. & Saffer, H. The Effects of Price on Alcohol Consumption and Alcohol-Related Problems. Alcohol Res. Health 26, 22 (2002).

39. Grossman, M., Chaloupka, F. J., Saffer, H. & Laixuthai, A. Effects of Alcohol Price Policy on Youth: A Summary of Economic Research. J. Res. Adolesc. Lawrence Erlbaum 4, 347–364 (1994).

40. Cook, P. J. Paying the Tab: the Economics of Alcohol Policy. (Princeton University Press, 2007.).

41. Cook, P. J. & Moore, M. J. Drinking and schooling. J. Health Econ. 12, 411–429 (1993).

42. Powell, L. M., Williams, J. & Wechsler, H. Study Habits and the Level of Alcohol Use Among College Students. Educ. Econ. 12, 135–149 (2004).

43. The National Council on Alcoholism and Drug Dependence, Inc. (NCADD). Alcohol and Pregnancy - Fetal Alcohol Effects (FAE). NCADD at http://www.ncadd.org/index.php/learn-about-alcohol/fetal-alcohol-effects

44. Parker, D. L., Shultz, J. M., Gertz, L., Berkelman, R. & Remington, P. L. The Social and Economic Costs of Alcohol Abuse in Minnesota, 1983. Am. J. Public Health 77, 982–986 (1987).

45. Rice, D. P. Economic Costs of Substance Abuse, 1995. Proc. Assoc. Am. Physicians 111, 119–125 (1999).

46. Wagenaar, A. C., Salois, M. J. & Komro, K. A. Effects of Beverage Alcohol Price and Tax Levels on Drinking: A Meta-Analysis of 1003 Estimates From 112 Studies. Addiction 104, 179–190 (2009).

47. Evans, W. N. & Ringel, J. S. Can Higher Cigarette Taxes Improve Birth Outcomes? J. Public Econ. 72, 135–154 (1999).

48. Ringel, J. S. & Evans, W. N. Cigarette Taxes and Smoking During Pregnancy. Am. J. Public Health 91, 1851–1856 (2001).

49. U.S. Bureau of Labor Statistics. Consumer Expenditures in 2011. (2013). at http://www.bls.gov/cex/csxann11.pdf

50. U.S. Bureau of Labor Statistics. Consumer Expenditures for the Dallas-Fort Worth Area: 2011-2012. at http://www.bls.gov/ro6/fax/cex_dfw.htm

51. Center for Responsive Politics. Beer, Wine & Liquor: Long-Term Contribution Trends. at http://www.opensecrets.org/industries/indus.php?ind=N02

52. National Institute on Money in State Politics. National Institute on Money in State Politics: Texas 2012. Texas 2012. Follow the Money at http://followthemoney.org/database/state_overview.phtml?s=TX&y=2012

53. Beer Institute. Beer Serves America. The Economic Impact of the Beer Industry: 2012 Data Texas. at http://beer.guerrillaeconomics.net/view/e7683026-0f9d-4ad2-b945-70cd65729970/download

THE EFFECTS OF ALCOHOL EXCISE TAX INCREASES ON PUBLIC HEALTH AND SAFETY IN TEXAS

©Texans Standing Tall, March 2, 2015 | TexansStandingTall.org

21

54. Bureau of Labor Statistics. Economy at a Glance: Texas. at http://www.bls.gov/eag/eag.tx.htm#eag_tx.f.3

55. Wada, R., Chaloupka, F. J., Powell, L. M. & Jerrigan, D.

Employment Impacts of Alcohol Taxes. UIC Work. Pap. (2014).

56. Ensuring Solutions to Alcohol Problems. The Alcohol Cost Calculator for Business. at http://alcoholcostcalculator.org/business/

57. Frank J. Chaloupka. The Health & Economic Impact of Alcohol Tax Increases. (2014). Presentation at Texans Standing Tall Statewide Summit, Feb. 25, 2014.

58. Institute of Medicine and National Reasearch Council. Reducing Underage Drinking: A Collective Responsibility. (The National Academies Press, 2004). at /catalog/10729/reducing-under-age-drinking-a-collective-responsibility