AIC Reports 113

119

AIC Reports Research and Public Policy Series 113 Anti-money laundering and counter-terrorism financing across the globe: A comparative study of regulatory action Julie Walters, Carolyn Budd, Russell G Smith, Kim-Kwang Raymond Choo, Rob McCusker and David Rees

Transcript of AIC Reports 113

AIC Reports

Research and Public Policy Series 113

Anti-money laundering and counter-terrorism financing across the globe: A comparative study of regulatory action

Julie Walters, Carolyn Budd, Russell G Smith, Kim-Kwang Raymond Choo, Rob McCusker and David Rees

www.aic.gov.au

AIC Reports

Research andPublic Policy Series

113

Anti-money laundering and counter-terrorism financing across the globe: A comparative study of regulatory action

Julie Walters, Carolyn Budd, Russell G Smith, Kim-Kwang Raymond Choo, Rob McCusker and David Rees

© Australian Institute of Criminology 2011

ISSN 1836-2060 (Print) 1836-2079 (Online)

ISBN 978 1 921532 81 8 (Print) 978 1 921532 82 5 (Online)

Apart from any fair dealing for the purpose of private study, research, criticism or review, as permitted under the Copyright Act 1968 (Cth), no part of this publication may in any form or by any means (electronic, mechanical, microcopying, photocopying, recording or otherwise) be reproduced, stored in a retrieval system or transmitted without prior written permission. Inquiries should be addressed to the publisher.

Project no. 0140

Published by the Australian Institute of Criminology GPO Box 2944 Canberra ACT 2601 Tel: (02) 6260 9200 Fax: (02) 6260 9299 Email: [email protected] Website: http://www.aic.gov.au

Please note: minor revisions are occasionally made to publications after release. The online versions available on the AIC website will always include any revisions.

Disclaimer: This research report does not necessarily reflect the policy position of the Australian Government.

Edited and typeset by the Australian Institute of Criminology

A full list of publications in the AIC Reports series can be found on the Australian Institute of Criminology website at http://www.aic.gov.au

iiiForeword

Foreword

Most developed countries across the globe have enacted legislation to proscribe acts of money laundering and financing of terrorism, and to enable the proceeds of crime to be recovered from offenders. Such legislation reflects the principles developed by the Financial Action Task Force’s (FATF-GAFI) 40 plus Nine Recommendations to combat money laundering and the financing of terrorism (FATF-GAFI 2004) to varying degrees. FATF-GAFI was established in 1989 as an international body to examine techniques employed by criminals to launder the proceeds of crime and the approaches taken internationally to counteract such activities, as well as to identify policies to impede money laundering and the financing of terrorism. FATF-GAFI issued 40 Recommendations to combat money laundering in 1990 and expanded these to deal with the problem of financing of terrorism after the 11 September 2001 attacks by adding a further Nine Special Recommendations on terrorism financing.

Despite the normative approach taken in the FATF-GAFI Recommendations, the specific legislative and procedural responses taken by individual countries have differed in many respects. Documenting these differences and comparing key aspects of the regimes in different countries is of considerable value to regulators and analysts for several reasons.

Law enforcement and prosecutorial agencies need to understand the differences that exist in criminal laws relating to money laundering between different countries when investigating and prosecuting illegal conduct, as conduct of this nature often entails cross-border activity requiring mutual assistance between agencies and extradition of suspects across jurisdictional borders.

Understanding the approaches taken by different countries to enhancing compliance with legislation and with soft regulatory measures can help policymakers develop best-practice mechanisms for increasing compliance with regulatory controls. Improved compliance has the potential to increase the quality of the financial intelligence gathered and the potential utility of regulatory regimes internationally.

Comparative research on the implementation of AML/CTF systems may illustrate the potential advantages of, and problems with, proposed changes to the regimes, such as extending the requirements to designated non-financial businesses and professions. Some countries have far greater experience with these approaches than others and it is important to make use of constructive lessons that have been learned.

The present research sought to compare the legal framework and compliance, and enforcement outcomes of the AML/CTF regimes across countries with disparate legal traditions. The countries included in the scope of the project were from the European Union (the United Kingdom, France, Germany and Belgium), Asia (the Republic of China (Taiwan), Hong Kong and Singapore), the United States and Australia. Within each of the selected countries, the structure of the criminal provisions proscribing money laundering and the financing of terrorism were reviewed and the judicial interpretation of these laws compared. Information is also presented on the number of businesses regulated within each country’s AML/CTF system and the extent to which businesses outside the formal financial sector are regulated. The approach taken to financial intelligence reporting is also compared with the evidence presented on the nature and extent to which financial reports are required and undertaken in the selected countries as well as the circumstances

iv Anti-money laundering and counter-terrorism financing across the globe

triggering reports. The extent to which entities comply with each country’s AML/CTF regime is also considered and a number of quasi-indicators of compliance are presented, as well as the actions taken by regulators for non-compliance and the extent to which regulators and others have adopted non-punitive strategies to encourage or enhance compliance with the regimes.

One of the principal findings concerns the vast differences that exist between countries in the designation of crimes considered to be predicate offences for money laundering—that is, the types of serious crimes that can generate funds for laundering. These differences can have important implications where cross-border prosecutions are undertaken, as there may not be a corresponding degree to which conduct is proscribed in different countries, thus creating barriers to mutual legal assistance and extradition of suspects.

Another clear finding related to the extensive differences that exist between the countries examined is the extent to which specific regulated entities comply with their reporting obligations. Australia, for example, requires businesses to lodge a report in respect of all attempted transactions that raise suspicions of illegality, while Belgium requires businesses to undertake a degree of preliminary analysis of transactions prior to submitting a report to authorities. Belgium, France and Germany further limit the circumstances that trigger a reporting obligation to those associated with a list of specific crimes. The German system, for example, limits those crimes to either money laundering or the financing of terrorism. Other countries consider all serious crimes as potential predicate offences for money laundering reporting purposes.

As might be expected, the volume of reports of suspicious financial activity submitted by regulated entities each year has increased considerably, with entities both in Australia and the United States increasing the number of reports made to regulators by more than 300 percent between 2002–03 and 2008–09. Such increases are due to the increasing publicity of reporting obligations by regulators, increasing numbers of entities being subject to reporting obligations and potentially an increase in underlying criminality. Further research is required to understand the precise reasons behind the increase in reporting in the countries examined.

Interestingly, designated non-financial businesses and professions demonstrated similar levels of reporting to regulators across the countries examined. None of the countries that have included legal practitioners, accountants, real estate agents, dealers of precious metals and stones, and trust and company service providers, in their AML/CTF regimes reported receiving volumes of reports from these businesses by comparison with those from financial services businesses. Financial services businesses (particularly banks), continue to contribute the bulk of financial intelligence through reports of suspicious financial activities due to the large number of transactions dealt with on a daily basis.

Despite certain similarities, and the shared basis in FATF-GAFI’s Recommendations, the elements of international AML/CTF regimes differ sufficiently to make direct comparisons between countries difficult. Care is needed in making direct comparisons between countries owing to their different legislative requirements, different cultures of compliance and differing patterns of financial crime and terrorism. The Australian Institute of Criminology has published a separate report that examines these different factors in some depth and such differences need to be considered in making any direct comparisons between countries. Prosecution, enforcement and reporting data can reveal interesting trends regarding the development of the AML/CTF regime over time within a specific country, or the impact changes to the regime have had on these measures. Using such measures as evaluative criteria between different countries can, however, be misleading unless local circumstances are considered in detail.

Future comparative studies of this nature would benefit from multilingual research, access to data held by regulators and other government agencies rather than reliance on publicly available information alone and from qualitative information held by financial intelligence units, regulated businesses and AML/CTF regulators. The present study does, however, provide a preliminary indication of how a number of countries from different legal traditions and continents have approached the challenges raised by money laundering and financing of terrorism in the twenty-first century.

Adam Tomison Director

vContents

Contents

iii Foreword

vii Acknowledgements

viii Acronyms and abbreviations

xi Executive summary

1 Introduction

1 Background

2 Aims and definitions

5 Geographical scope

5 Methodology

6 Structure of this report

8 Regulatory regime

8 Financial intelligence units

9 Australia

12 United States

15 European Union

16 United Kingdom

19 Belgium

22 France

24 Regulated sector

25 Germany

27 Asia

28 Hong Kong

31 Singapore

33 Republic of China, Taiwan

36 Comparative analysis

40 Case law

50 Conclusion

51 The profile of designated entities

51 Australia

52 United States

54 The United Kingdom

57 Belgium

58 France

58 Germany

59 Hong Kong

59 Singapore

60 Republic of China, Taiwan

62 Comparative analysis and conclusions

64 Conclusion

66 Extent of compliance and enforcement activity

66 Australia

69 United States

73 United Kingdom

75 Belgium

76 France

77 Germany

78 Singapore

79 Hong Kong

81 Taiwan (Republic of China)

82 Comparative analysis

87 Best practice strategies to enhance compliance

87 Strategies to enhance compliance

90 Conclusion

92 References

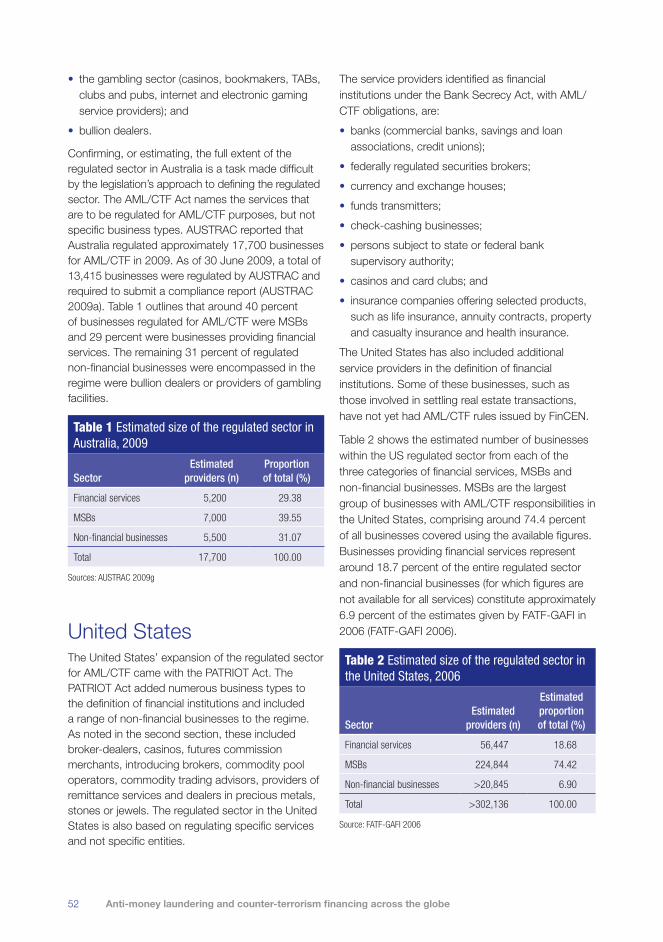

Tables52 Table 1: Estimated size of the regulated sector

in Australia, 2009

52 Table 2: Estimated size of the regulated sector in the United States, 2006

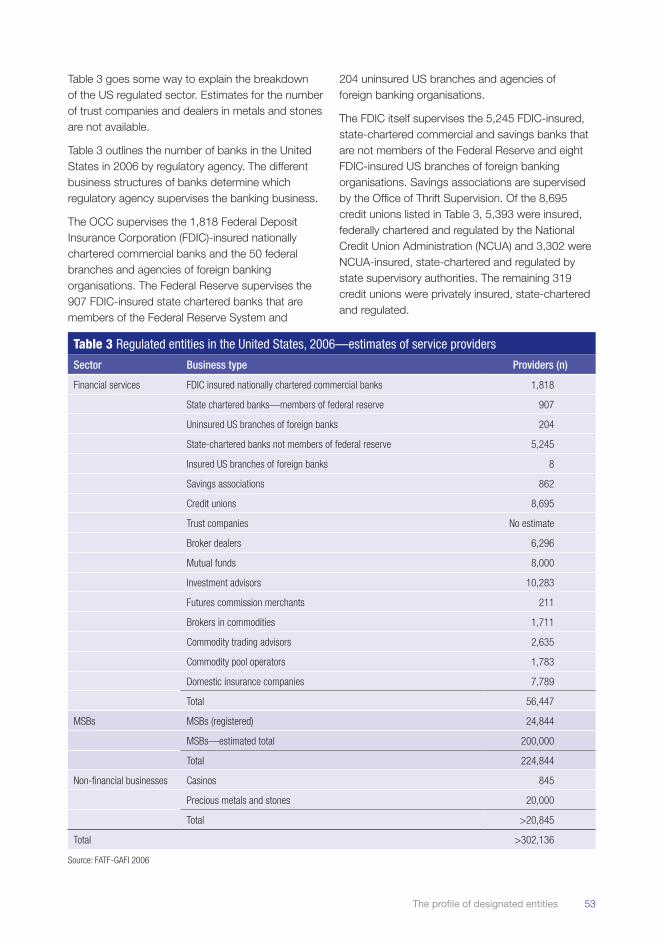

53 Table 3: Regulated entities in the United States, 2006—estimates of service providers

54 Table 4: Estimated size of the regulated sector in the United Kingdom, 2007

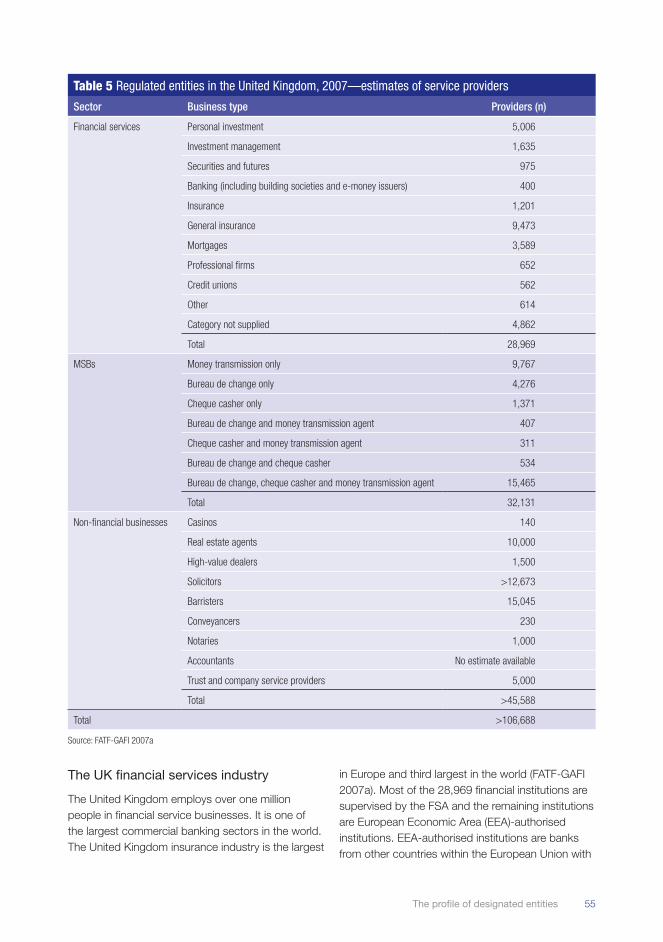

55 Table 5: Regulated entities in the United Kingdom, 2007—estimates of service providers

56 Table 6: Banks authorised by either Financial Services Authority or European Economic Area, 2007

vi Anti-money laundering and counter-terrorism financing across the globe

56 Table 7: Principals and agents of money service businesses in the United Kingdom, 2007

57 Table 8: Non-financial businesses in the United Kingdom, 2007—including calculations and estimates

57 Table 9: Selected reporting entities in Belgium, 2006

58 Table 10: Banks operating in Belgium, 2006

58 Table 11: Investment firms in Belgium by business type, 2006

58 Table 12: Credit institutions (finance companies) in France, 2008

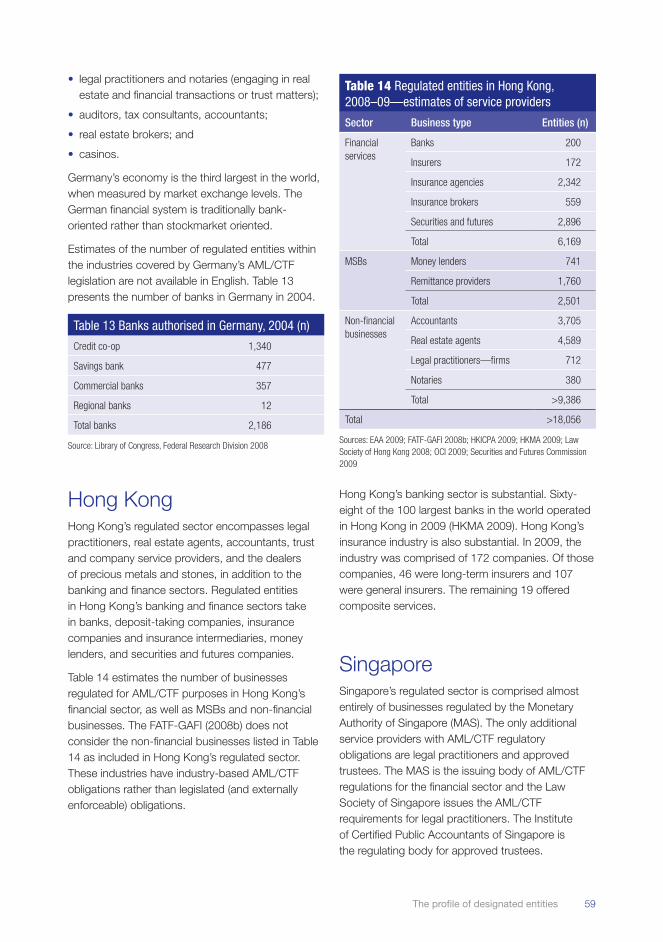

59 Table 13: Banks authorised in Germany, 2004

59 Table 14: Regulated entities in Hong Kong, 2008–09—estimates of service providers

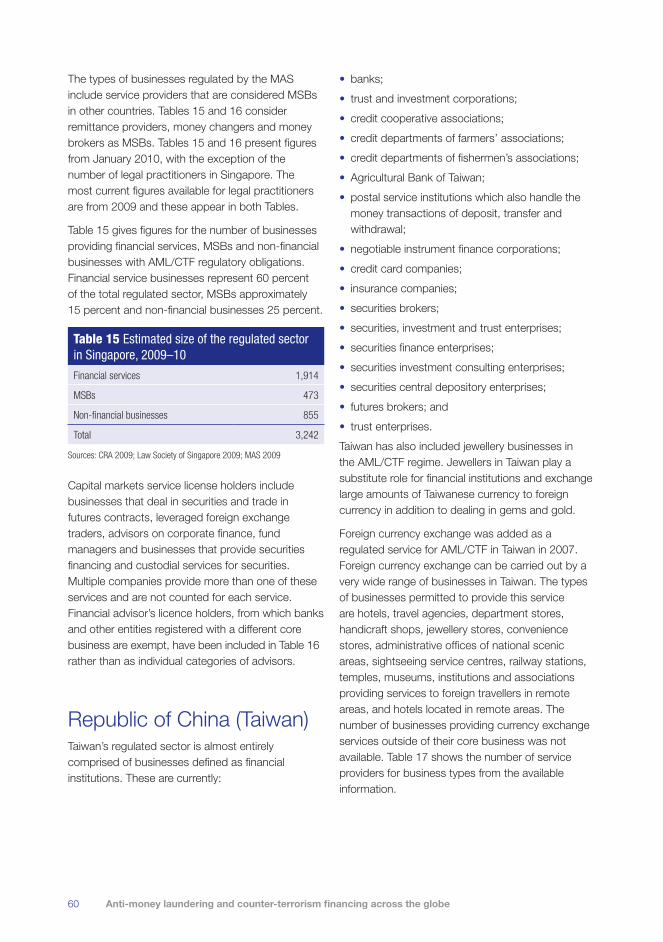

60 Table 15: Estimated size of the regulated sector in Singapore, 2009–10

61 Table 16: Regulated entities in Singapore, 2009–10—estimates of service providers

62 Table 17: Regulated entities in Taiwan, 2007—estimates of service providers

63 Table 18: Inclusion of non-financial businesses in AML/CTF regimes

63 Table 19: Non-financial businesses, money service businesses and the financial sector as a proportion of the regulated sector in Australia, the United Kingdom and Singapore

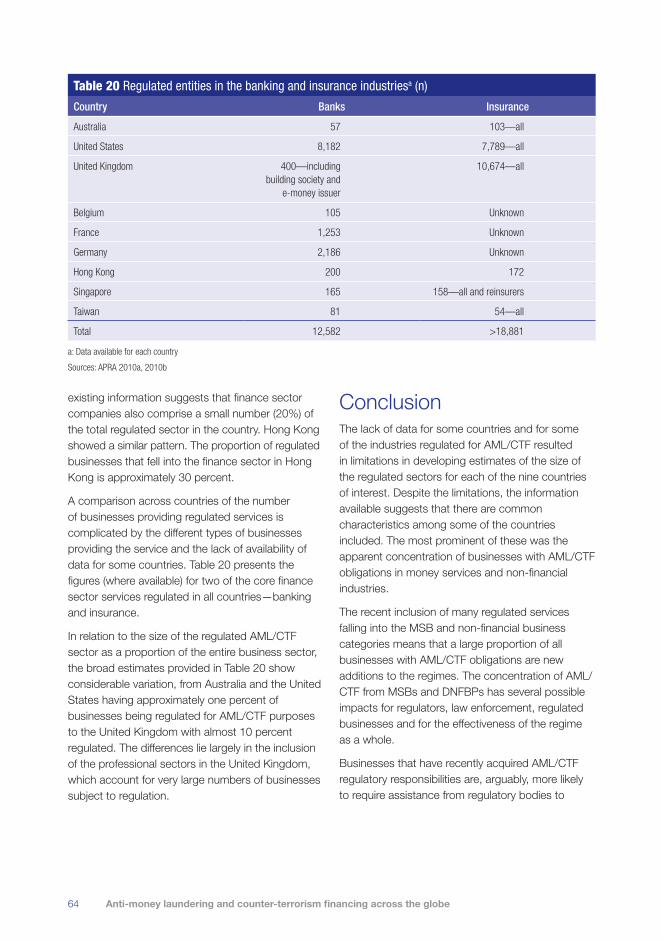

64 Table 20: Regulated entities in the banking and insurance industries

67 Table 21: Reports submitted to AUSTRAC, 2008–09

67 Table 22: Suspicious financial activity reports submitted to AUSTRAC

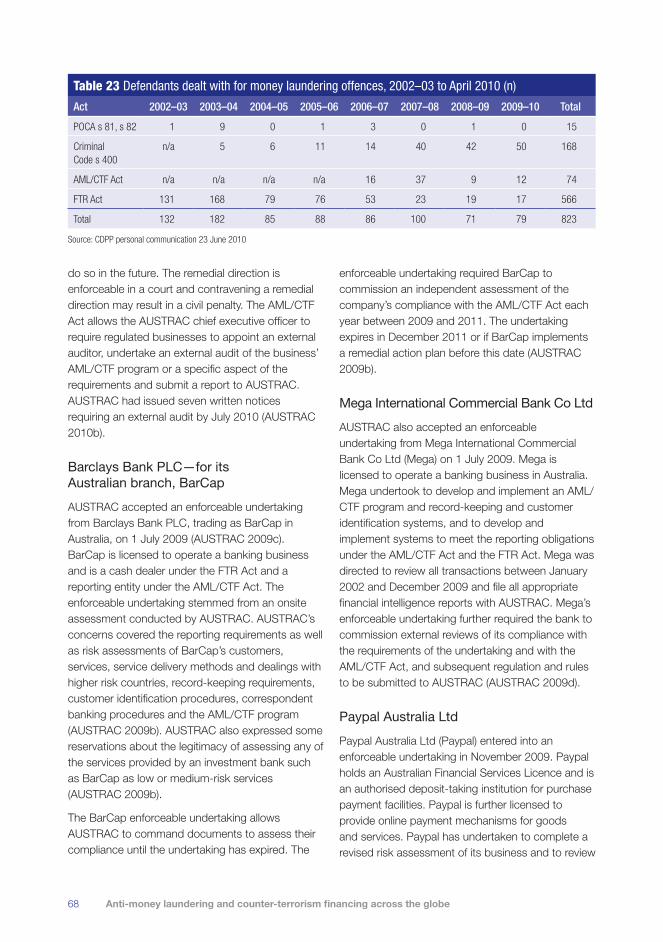

68 Table 23: Defendants dealt with for money laundering offences, 2002–03 to April 2010

69 Table 24: Suspicious financial activity reports filed with FinCEN (by fiscal year)

70 Table 25: Money laundering charges and prosecutions in the United States, 1994–2001

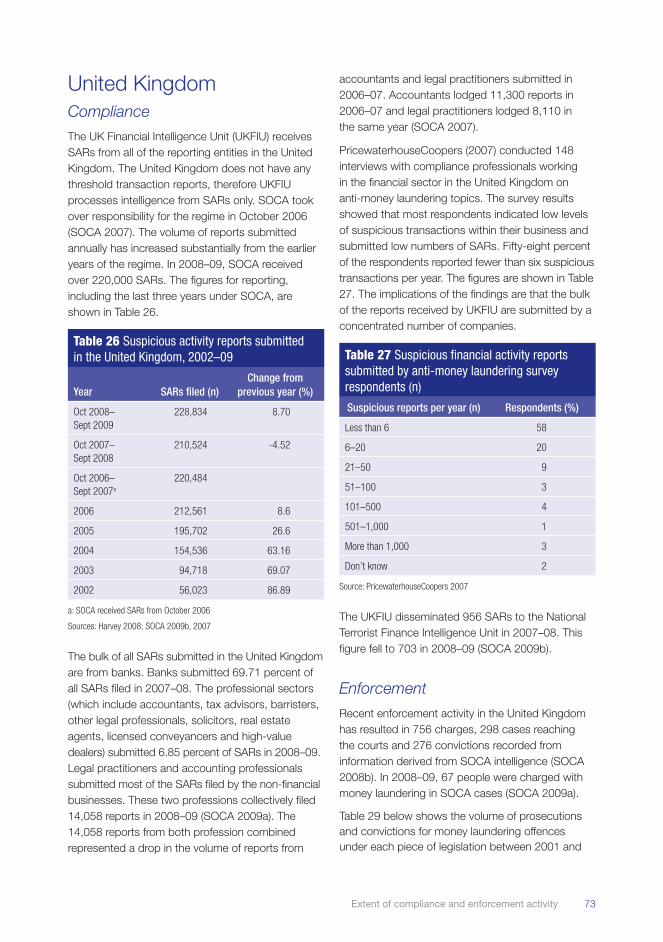

73 Table 26: Suspicious activity reports submitted in the United Kingdom, 2002–09

73 Table 27: Suspicious financial activity reports submitted by anti-money laundering survey respondents

74 Table 28: Institutions found to have failed to apply anti-money laundering regulations in the United Kingdom

74 Table 29: Money laundering prosecutions in the United Kingdom, 2001–04

75 Table 30: SOCA UK’s asset recovery, 2007–08 and 2008–09

75 Table 31: Disclosures of suspicious financial activity—by year

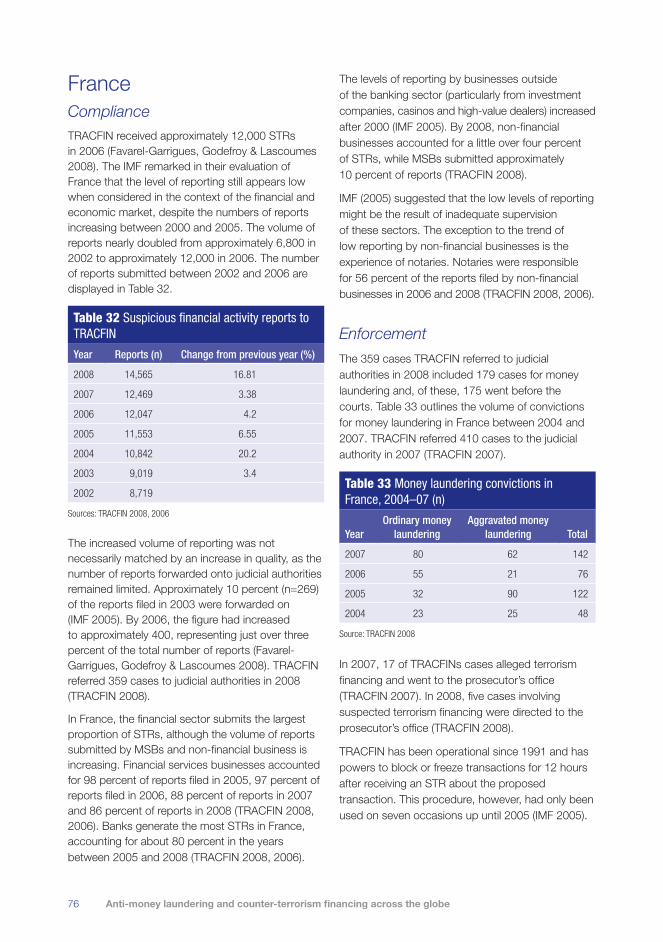

76 Table 32: Suspicious financial activity reports to TRACFIN

76 Table 33: Money laundering convictions in France, 2004–07

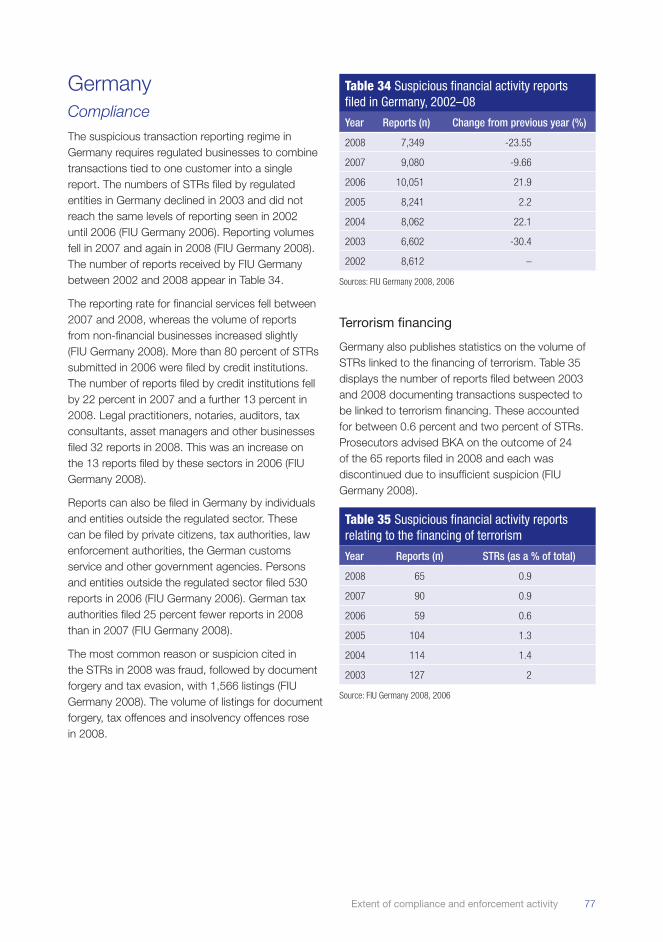

77 Table 34: Suspicious financial activity reports filed in Germany, 2002–08

77 Table 35: Suspicious financial activity reports relating to the financing of terrorism

78 Table 36: Reported outcomes to financial intelligence unit Germany, 2007–08 (n)

78 Table 37: Offences for money laundering, concealment of unlawfully acquired assets in Germany, 2002–08

78 Table 38: Suspicious financial activity reports in Singapore, 2004–08

79 Table 39: Money laundering convictions in Singapore, 2005–08

79 Table 40: Suspicious financial activity reports filed in Hong Kong, 2004–07

80 Table 41: Suspicious transaction reports submitted in Hong Kong by sector, 2004–07

80 Table 42: Suspicious financial activity reports related to terrorism financing, 2003–07

80 Table 43: Persons convicted of money laundering in Hong Kong, 2004–09

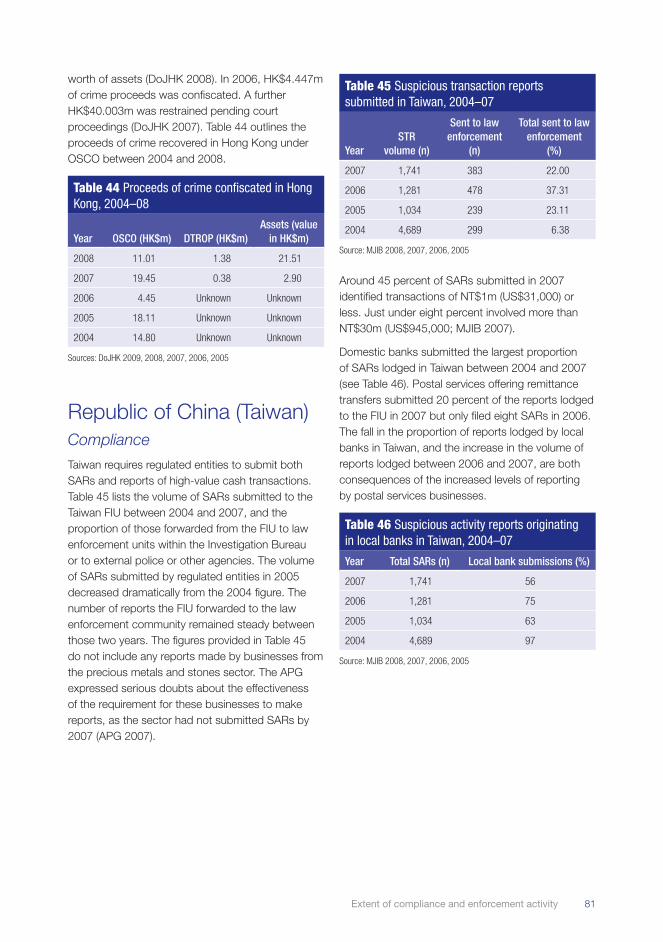

81 Table 44: Proceeds of crime confiscated in Hong Kong, 2004–08

81 Table 45: Suspicious transaction reports submitted in Taiwan, 2004–07

81 Table 46: Suspicious activity reports originating in local banks in Taiwan, 2004–07

82 Table 47: Money laundering prosecutions and proceeds in Taiwan, 2004–07

82 Table 48: Businesses allegedly used to launder money, 2005–07

83 Table 49: Suspicious financial activity reports submitted from the financial sector based on proportion of that sector

88 Table 50: UK financial intelligence unit contact with the reporting sector, 2006–07

89 Table 51: Money Laundering Prevention Centre contact with the reporting sector, 2003–07

viiAcknowledgements

Acknowledgements

This report is based on research undertaken by current and former staff within the Global, Economic and Electronic Crime Research Program at the Australian Institute of Criminology. The authors are grateful to the many individuals who agreed to participate in consultations with the authors both within Australia and overseas between 2008 and 2010, and to the agency staff and the external referee who provided helpful feedback on earlier drafts.

The information contained in this report was current at 1 April 2011.

viii Anti-money laundering and counter-terrorism financing across the globe

ADIs authorised deposit taking institutions

AIC Australian Institute of Criminology

AML/CTF anti-money laundering/counter-terrorism financing

AML/CTF Act Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (Cth)

Annunzio-Wylie Act Annunzio-Wylie Anti-Money Laundering Act 1992

APG Asia/Pacific Group on Money Laundering

ARS alternative remittance services

AUSTRAC Australian Transaction Reports and Analysis Centre

BaFIN German Financial Supervisory Authority

BKA Federal Office of Criminal Investigation (Bundeskriminalamt)

Bank Secrecy Act Bank Records and Foreign Transaction Reporting Act 1970

CAD Commercial Affairs Department

CBFA Banking, Finance and Insurance Commission

CCA Court of Criminal Appeal

CDPP Commonwealth Director of Public Prosecutions

CDSA Corruption, Drug Trafficking and Other Serious Crimes (Confiscation of Benefits) Act (Cap 65A)

Consent order Consent to the Assessment of Civil Money Penalty Order

COSC Central Office for Seizure and Confiscation

CoTUNA Charter of the United Nations Act 1945 (Cth)

Criminal Code Criminal Code Act 1995 (Cth)

CTIF-CFI Cellule de Traitement des Informations Financieres

CTR Currency Transaction Reports

DNFBPs designated non-financial businesses and professions

DTROP Drug Trafficking (Recovery of Proceeds) Ordinance

EEA European Economic Area

FATF-GAFI Financial Action Task Force (Le Groupe d’action financière)

Acronyms and abbreviations

ixAcronyms and abbreviations

FDIC Federal Deposit Insurance Corporation

FinCEN Financial Crimes Enforcement Network

FIU financial intelligence unit

FTR Act Financial Transaction Reports Act 1988 (Cth)

FSA Financial Services Authority

Germany MoneyLaundering Act Act on the Detection of Proceeds from Serious Crimes

HKICPA Hong Kong Institute of Certified Public Accountants

HMRC Her Majesty’s Revenue and Customs

IFTIs international funds transfer instructions

IMF International Monetary Fund

INCSR International Narcotics Control Strategy Report

JFIUHK Joint Financial Intelligence Unit Hong Kong

MAS Monetary Authority of Singapore

MLCA Taiwan Money Laundering Control Act

MLPC Money Laundering Prevention Centre

LPP Legal Professional Privilege

LTTE Liberation Tigers of Tamil Eelam

MLRO money laundering reporting officer

Money Laundering

Control Act Money Laundering Control Act 1986

MSBs money service businesses

MJIB Investigation Bureau, Ministry of Justice, Republic of China

NatWest National Westminster Plc

NCIS National Criminal Intelligence Service

NCS National Crime Squad

NCUA National Credit Union Administration

OCC Office of the Comptroller of the Currency

OSCO Organised and Serious Crimes Ordinance

PATRIOT Act Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act 2001

POBO Prevention of Bribery Ordinance

POCA 2002 Proceeds of Crime Act 2002 (Cth)

POCA 1987 Proceeds of Crime Act 1987 (Cth)

x Anti-money laundering and counter-terrorism financing across the globe

POCA 2002 UK Proceeds of Crime Act 2002

SARs Suspicious Activity Reports

SEF Singapore Exchange and Finance Pty Limited

SMRs suspicious matter reports

SOCA Serious Organised Crime Agency

SOCPA Serious Organised Crime and Police Act 2005 (UK)

STRs Suspicious Transaction Reports

STRO Suspicious Transaction Reporting Office

Terrorism Act Terrorism Act 2000

Third MoneyLaundering Directive Directive 2005/60/EC of the European Parliament and the Council of 26 October

2005 on the prevention of the use of the financial system for the purpose of money laundering and terrorist financing

TRACFIN Traitement du renseignement et action contre les circuits financiers clandestins

TSOFA Terrorism (Suppression of Financing) Act

UKIS UK Immigration Service

UNATMO United Nations (Anti-Terrorism) Ordinance

UKFIU UK Financial Intelligence Unit

xiExecutive summary

Executive summary

This report presents a review of the different approaches taken by nine countries, including Australia, to the adoption of anti-money laundering and counter-terrorism financing (AML/CTF). In response to mounting international concern about money laundering in the late 1980s, countries around the world established the Financial Action Task Force (FATF-GAFI) to set international standards and develop policies to combat money laundering and terrorist financing. In 1990, the FATF-GAFI issued a set of 40 Recommendations to guide the fight against money laundering and these were expanded following 2001 to include nine additional Recommendations to respond to the financing of terrorism.

The FATF-GAFI’s 40 plus nine Recommendations to combat money laundering and the financing of terrorism (FATF-GAFI 2004) have three primary objectives—to support the criminalisation of money laundering and the financing of terrorism, to ensure that assets linked to money laundering or the financing of terrorism can be frozen and confiscated and to ensure that financial institutions and other regulated businesses comply with the recommendations.

This report reviews the state of international responses to the FATF-GAFI Recommendations in order to assess how countries have applied the requirements, which sectors have been subject to regulation and how compliance and enforcement are undertaken.

Nine countries were chosen for review—Australia, the United States, the United Kingdom, France, Germany, Belgium and in Asia, Singapore, Hong Kong and the Republic of China (Taiwan). These were chosen to provide an indication of how diverse nations in separate continents have approached

AML/CTF implementation. They were also chosen to be indicative of the measures taken in countries with different legal traditions and different types of risk in terms of money laundering and financing of terrorism.

The majority of the information used in this report came from publicly available documents published by regulatory bodies, financial intelligence units, law enforcement and other government agencies, industry bodies and FATF-GAFI itself. The authors also undertook a number of consultations with stakeholders in the countries in question in order to supplement the publicly available written material.

Regulatory regimeThe regulatory regime in each country was examined by reviewing its criminal and regulatory legislation including assert recovery provisions, the nature of each country’s government regulator (or financial intelligence unit), the extent of the regulated sector and the nature of the obligations cast upon reporting entities including laws against disclosing the fact of reporting to the business in question (tipping-off) and the nature of compliance and enforcement activities.

Overall, AML/CTF regimes across the countries in question share a common basis in FATFs Recommendations and accordingly, they were remarkably similar in their responses to, and implementation of, the Recommendations. A key area of difference between the nine countries is the extent and size of the regulated sector in each country. This affects not only the scale of reporting undertaken, but also the capacity to regulate and enforce compliance for large numbers of regulated businesses in some countries.

xii Anti-money laundering and counter-terrorism financing across the globe

All of the countries considered have made money laundering a criminal offence and one distinct from the crime that generated the funds in question. One of the key components of criminal money laundering offences that differs between each country is the consideration given to predicate offences, that is, the type of criminal conduct that generates funds which can then be laundered. Australia, the United States, Belgium, Germany, Hong Kong, Singapore and Taiwan all restrict money laundering predicate crimes to serious offences. Germany has included specific less serious offences as predicate offences, whereas Taiwan places a further restriction by adding a lower limit of NT$20m for the amount of funds in question. The definition of a serious, indictable, or felony offence differs between countries and is tied to minimum imprisonment periods in each country, generally a minimum period of 12 months imprisonment.

The real difference in the potential application of money laundering offences in these nine countries lies in the maximum prison sentences tied to potential predicate crimes. An offence can only become a predicate crime for a money laundering charge where the maximum sentence available for the predicate crime satisfies the conditions for money laundering in a specific jurisdiction. Illegal logging crimes, for example, do not carry the required sentences to meet the definition of a predicate offence for money laundering in Australia. The same offence in Indonesia, however, carries a maximum sentence that satisfies the severity condition of a money laundering charge in that jurisdiction.

Taiwan is the only country considered in this report that has not criminalised the financing of terrorism. Australia has criminalised financing individual terrorists, terrorist organisations and terrorist acts through providing funds and other resources. The United States and the United Kingdom have made illegal the funding of terrorist groups or acts, while Singapore has specifically mentioned individual terrorists and acts. Hong Kong has focused entirely on terrorist acts and purposes.

Reporting requirementsThe reporting requirements within each country showed considerable variation. All of the countries required at least some sectors to submit reports of suspicious financial transactions, although the conditions of reporting were quite varied between countries.

In Australia, the systematic reporting requirements introduced under the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (Cth) (AML/CTF Act) exceed those enacted in most of the other countries examined. While there were requirements in every country to submit a suspicious financial activity report in some form or other, Australia was the only country that required reports for each of the following—systematic reports for suspicious financial activity, high-value cash transactions, international movements of cash, international movements of value and international funds transfers—indicating the scope of the formal regime in Australia exceeds the others in this regard.

Australia, the United Kingdom and Taiwan require all regulated entities to submit reports of suspicious transactions. The remaining six countries have caveats, or additional guidelines, for when a report of suspicious activity is warranted.

The United States limits the transactions considered for reporting of this kind with a monetary threshold. Belgium, France and Germany also limit the transactions that might warrant a report but do so by considering the crimes they might be connected to. France’s regulated entities must report transactions suspected to be connected to drug trafficking, organised crime, fraud against the European Communities, corruption, or terrorism financing. Belgium, like France, limits the reports received to those related to specific crimes which include terrorism or terrorist financing, organised crime, illicit trafficking, serious fraud and organised tax fraud, corruption, environment crime and counterfeiting. Belgium, however, only requires financial institutions to submit disclosures of suspicious transactions.

xiiiExecutive summary

Australia is one of two countries that have not mirrored the reporting requirements for cash for the movement of bearer negotiable instruments across international borders. The United States, United Kingdom, Belgium, France, Germany and Singapore subject movements of bearer negotiable instruments to the same reporting requirements, with the same thresholds, as cash movements.

Australia, instead, can require individuals moving bearer negotiable instruments across international borders to submit a report to a police or customs officer on request. There is no mandatory requirement to report all movements. Hong Kong similarly has no requirement for bearer negotiable instruments. Taiwan does not require reports for movements of instruments of value.

Australia is the only country under consideration that requires all regulated entities to report all electronic funds transfers (international funds transfer instructions—IFTIs) regardless of value.

Tipping-off clausesEach of the nine countries currently has ‘tipping-off’ provisions that criminalise the revealing of details of a report about a suspicious transaction to those involved. The variations in tipping-off clauses come from the extent of the information encompassed and the exemptions made.

The United States and France have the simplest models for tipping-off and prohibit disclosing information connected to a report after it has been filed to those involved in the transaction. Belgium and Germany extend this to prohibit a disclosure connected to a report to any third party as well as the subject of a report. Both Hong Kong and Singapore prohibit the disclosure of any information related to reports to any person where the disclosure might prejudice an investigation.

Tipping-off in the United Kingdom applies to details of investigations as well as reports and extends to all third parties. The United Kingdom also has additional tipping-off provisions for civil recoveries, asset confiscations and money laundering offences. Taiwan’s provisions are similar as they encompass both reports of suspect transactions and any suspected money laundering offence.

The approaches taken by Hong Kong and Singapore are somewhat different. Hong Kong and Singapore also limit the crimes that might trigger a transaction report to indictable offences in the case of Hong Kong and to drug trafficking or other criminal conduct in the case of Singapore. All individuals in Hong Kong, not just reporting entities, carry this obligation and an identical one to report suspicions of terrorist property. Singaporeans who come across transactions that might be connected to drug trafficking or criminal conduct in the course of business must submit a report. In addition, all persons in Singapore, and any Singaporean citizens overseas, must report any transactions suspected to be linked to the financing of terrorism.

Including a reporting requirement for cash transactions that exceed a threshold was less common among the nine countries considered. Australia and the United States require regulated entities to submit a report of transaction made using cash above a specific threshold set in legislation. The Australian threshold is AUD$10,000 and the United States threshold is US$10,000. Taiwan also requires regulated entities to submit a report of any cash transaction valued at NT$1m or over.

Singapore, rather than requiring a report for every cash transaction beyond a threshold, suggests to its regulated entities that large cash transactions are likely to be suspicious and warrant reporting. France and Germany have not required regulated entities to submit cash transaction reports. Germany, however, requires businesses to retain customer identification for cash transactions valued at €15,000 or more. French-regulated entities are similarly required to scrutinise cash transactions beyond a threshold limit and retain that information. Belgium prohibits cash payments of more than €15,000, rendering any reporting of this nature redundant. The United Kingdom and Hong Kong do not have any large cash transaction requirements.

Almost all of the nine countries have identical requirements to report the movements of cash across country borders, on entry and exit, but vary in the threshold amount required to trigger a report. Hong Kong is the only country considered that currently does not require reporting of international movements of cash.

xiv Anti-money laundering and counter-terrorism financing across the globe

In the United Kingdom, the definition of suspicion in relation to money laundering was examined in R v DaSilva, with the court requiring a suspicion that is more than fanciful in order for an offence of money laundering, or assisting, to be present. Cases have also questioned the extent to which proof of a predicate offence is necessary to establish money laundering.

The application of AML/CTF legislation to legal practitioners has also generated substantial debate. The decisions in the European Union and Bowman v Fels in the United Kingdom confirmed that legal practitioners are exempt from reporting requirements if they act in connection with giving legal advice to a client. Further issues debated in these cases were centred on the offence of making an ‘arrangement’ for money laundering.

The profile of the regulated sectorsDocumenting the composition and size of the regulated sectors in each of the countries in question proved difficult owing to the limited data available in some countries. Difficulties were particularly encountered in obtaining information concerning industries without prudential regulation or other long-standing registration processes. Additional problems arose in obtaining information from some non English-speaking countries. Accordingly, the data located were somewhat incomplete, making comparisons across countries problematic.

Generally, the core financial institutions (the banking industry, finance companies and insurance industry) are regulated for AML/CTF purposes in all nine countries, although variations exist between the regulated sectors in relation to money service businesses (MSBs) and non-financial businesses including the professions.

The way in which AML/CTF requirements are applied to legal practitioners across the different countries gives rise to the greatest variations. Hong Kong and Singapore include legal practitioners in the full scope of their requirements, while legal practitioners in Germany, Belgium, the United Kingdom and France

Australia specifically prohibits disclosing the details of reports of suspicious financial activity and any person or matter triggering a report to any third party. Australia also has one of the most extensive lists of persons exempt from tipping-off. Australia, like the United Kingdom, France and Singapore, exclude legal practitioners (in specific circumstances) from the requirements. Australia extends the exemptions beyond this to accountants, businesses with a joint anti-money laundering program and anyone trying to dissuade a customer from committing an offence under any law in Australia.

Judicial interpretationThe jurisprudence in the countries considered is continuing to evolve, with a number of cases having come before the courts in which questions of law have arisen. Courts have considered the meaning of ‘structuring’, ‘concealing’, ‘profits’ of crime and ‘suspicion’. The Australian case of R v Narayanan addressed the definition of structuring under the Financial Transaction Reports Act 1988 (Cth) (FTR Act) with the court defining structuring as two or more non-reportable transactions conducted to ensure, or to attempt to ensure, that the transaction was not a significant cash transaction. The court stated that multiple transactions that had been subjected to structuring could still, collectively, constitute a significant cash transaction.

In the United States, two cases have narrowed the scope of money laundering offences, one in terms of the process of laundering, the other in terms of what can be laundered. Regalado Cuellar v United States centred on the definition of concealment, finding that hiding currency for the purpose of transport was in itself not an act of laundering. The second case, United States v Santos et al, questioned what was meant by proceeds of crime and decided that it referred only to the profits generated.

Further cases have defined the actions that can constitute a conspiracy to commit money laundering. In Australia, A Ansari v R, H Ansari v R allowed a broad interpretation of conspiracy to launder money where the fault element for the laundering offence is recklessness. In the United States, the courts have ruled that the offence of conspiracy was to be treated the same as an actual act of money laundering.

xvExecutive summary

The volume of reports submitted to authorities in Hong Kong, Singapore, France, the United Kingdom, the United States and Australia steadily increased over the period for which reporting data was available. Reporting entities in each country generally submitted a vastly increased volume of reports in 2008 or 2008–09 compared with the base year. Between 2004 and 2008, Singapore experienced an increase in reports of more than 580 percent. Reporting numbers in the United Kingdom and United States grew by 308 percent and 359 percent respectively. Singapore, unlike the United Kingdom and European Union countries, did not vastly expand the number of industries encompassed in the AML/CTF regime in that time.

Germany and Taiwan recorded a fall in the volume of reports over the period of available data. In 2007, Taiwan’s Finance Intelligence Unit (FIU) received less than 40 percent of the reports filed in 2004; and Germany’s FIU received 14 percent fewer reports in 2008 than in 2002.

The fluctuations in report volumes, particularly suspect transaction reports, are likely to have been influenced by factors outside of the level of suspicious activities. Any amendments made to the AML regimes, particularly any expansion in the reporting requirements or thresholds, were likely to have had an impact on the volume of reports. Also, as KPMG (2007) noted, the vast increases in reporting volumes in some countries may reflect an increased capacity to capture suspect transactions, rather than an increase in suspicious activities, in order to meet AML/CTF compliance requirements.

Including non-financial businesses in the AML/CTF regimes of these countries probably has not had a large impact on the volume of reports each FIU received within the timeframes considered in this report. Businesses in the financial services sector overwhelmingly submitted the largest proportion of reports in each of the countries considered, even in countries where non-financial businesses constituted a large percentage of the regulated sector. The non-financial businesses in the countries considered were still filing relatively low numbers of reports in the last year for which data was available. At best, the reports were low in volume and, at worst, were non-existent.

have obligations only when dealing with customers in financial transactions or the settlement of real estate transactions. Legal practitioners in the United States and Taiwan are excluded from AML/CTF obligations. Australian legal practitioners, with the exception of those holding an Australian Financial Services Licence, are also excluded from AML/CTF responsibilities.

The requirements for legal practitioners in the United Kingdom, France, Belgium, Germany and Singapore are further complicated by legal professional privilege. Legal professionals in these countries, which would otherwise have AML/CTF obligations for at least some transactions, are exempt from the obligation to report suspicious transactions under some circumstances. Where the information was gained in circumstances protected by legal privilege, the lawyer involved is not required to submit a report.

Non-financial businesses in Australia, the United Kingdom and Singapore (3 countries with the most data available to estimate the size of the regulated sector) contributed the largest proportion of the regulated sectors in those countries. Undertaking a comparison between the numbers of businesses providing regulated services in all of the countries considered is a task complicated by the variations in the types of business providing services and the lack of available data for some countries. It can be concluded, however, in relation to the size of the regulated AML/CTF sector as a proportion of the entire business sector, that Australia and the United States have approximately one percent of businesses regulated for AML/CTF purposes, while the United Kingdom has almost 10 percent regulated. Complete comparative data is not available for other countries. The differences lie largely in the inclusion of the professional sectors in the United Kingdom, which account for very large numbers of businesses subject to regulation.

ComplianceMost of the countries considered in this report, with the exception of Germany and Taiwan, showed an increase in the volume of reports between the base year and the last year for which data were available.

xvi Anti-money laundering and counter-terrorism financing across the globe

Prosecution and enforcementAs with the levels of reporting suspicious financial activity, the number of people charged or prosecuted for money laundering has also generally increased within the nine countries analysed in this report. The approach to reporting enforcement figures also varied between countries.

Prosecution data in the Australian statistics show the number of charges dealt with by the public prosecutor, Germany reports the number of convictions, Taiwan measures prosecutions, the United Kingdom provides convictions and formal cautions and Hong Kong records convictions only. Statistics were not able to be gathered from France, Belgium and Singapore. Nevertheless, some general trend data can be extracted for the countries that published information in this area.

Most countries reported annual increases in the levels of enforcement activity in each country. By contrast, Germany reported a 40 percent decrease in the number of offences between 2002 and 2003. However, the number of recorded offences then increased between 2003 and 2007, with a 160 percent increase in the number of convictions in 2005 and 2006.

The United Kingdom demonstrated a dramatic increase from 16 offenders found guilty or cautioned in 2003 to 1,328 offenders in 2006. Convictions in Hong Kong increased from 49 convictions in 2004 to 179 in 2007. The volume of Australian offenders dealt with for criminal money laundering offences increased from five in the 2003–04 financial year, to 50 in 2009–10. Despite the increased volume of offenders dealt with during this period, Australia’s volume of prosecutions is still low compared with other countries considered within this report. Statistics from the United States were obtained for the period 1994 to 2001 and it was found that the volume of money laundering charges remained constant during this period.

Professions with reporting requirements in the United Kingdom were responsible for only eight percent of suspicious reports in 2007, with the majority of these submitted by solicitors and accountants. In 2007, in Belgium, less than two percent of reports originated from non-financial businesses (excluding notaries), with legal practitioners and real estate agents submitting only three and two disclosures respectively. In Taiwan, only high-value dealers are required to submit reports; no businesses in this industry had submitted a report prior by 2007. The United States was the only country in this report to show comparable levels of reporting between the different sectors, with 48 percent of suspicious financial transaction reports in 2007 submitted by businesses outside of the financial sector.

The low levels of reporting from businesses outside of the financial sector cast doubt on the effectiveness of the regime in reaching these industries. Low levels of supervision have been suggested by the International Monetary Fund (IMF) as an explanation of the low numbers of reports by these industries in France. Recent changes to regulatory regimes in several countries, including Australia and those in the European Union, means that it is too early to adequately evaluate the level of compliance in this area.

Belgium had one of the highest percentages of reports leading to cases being forwarded to prosecution officials in 2007. Belgium’s FIU received just over 12,000 reports and submitted 1,666 cases to the public prosecutor in that year. This represented 13 percent of all reports submitted and 23 percent of the total number of files opened. Taiwan’s FIU also passed on a large proportion of cases to law enforcement in 2007. The Taiwanese FIU received fewer than 2,000 reports in that year and sent more than 20 percent of these onto law enforcement agencies. France, by contrast, passed on approximately 400 reports to law enforcement (3%) of the 12,000 reports received in 2007. The United Kingdom filed charges in 766 cases, resulting in 276 convictions, from more than 220,000 reports filed with the FIU.

xviiExecutive summary

Future initiativesFuture comparative studies of this nature should aim to provide more complete information on the variables under consideration. This would entail undertaking qualitative research targeted at the regulators and industry associations in each country and, in the case of non-English-speaking locations, would require multilingual research and access to business and government statistical collections. Additional qualitative research would be likely to provide a more complete picture of the AML/CTF enforcement outcomes and the utility of the financial intelligence gathered by AML regimes. Additional qualitative information could inform regulators and others of the potential value of providing feedback to regulated businesses and highlight the effectiveness of other compliance-enhancing initiatives. This research may also inform regulators and policymakers of the practical implications for regulated businesses of the changes made to AML/CTF preventative systems in place.

As is apparent from this review, the challenges of conducting such research from open source documents are considerable, as public source material provides only a limited perspective. Problems also exist within individual nations where data are not being collected, or are collected in variable formats using different data fields, categories and definitions. The FATF-GAFI Mutual Evaluations provide a good deal of uniformly collected and comparable information, but often these reports are incomplete. Regulators and FIUs also collect considerable amounts of data from the regulated sectors in annual compliance reports, but these are not readily available or are collected using non-uniform categories across countries.

Ideally, a single repository of AML/CTF compliance and regulatory data should be established, although in practice, the resources required for this would be prohibitive. At present, the most that can be asked is that FIUs, law enforcement agencies and regulators maintain a dialogue to develop the use of harmonised data recording practices for the key variables of policy importance such as measures of enforcement outcomes and compliance statistics. The present report aimed to provide a basis for comparing the AML regimes by mapping the key components of the AML systems and identifying variables for tracking the use of those systems and has suggested areas for improving data collection in these areas. It is hoped that it provides an indication of the areas requiring most attention for dialogue and discussion in the years ahead.

Best-practice strategies to enhance complianceThe strategies employed by the FIUs and AML/CTF regulators to enhance compliance fall into two principal categories—dialogue between the FIU and reporting entities, and increasing the ease of submission. The countries considered in this report have all adopted some aspects of both of these broad strategies for heightening compliance through non-punitive means.

Electronic report filing systems are common throughout all nine countries examined. Information available suggests that electronic filing has all but replaced paper disclosures in most cases.

In terms of feedback from FIUs to industry, it appears that the UK’s FIU publishes more information on the volume and type of feedback provided to reporting entities than the Financial Crimes Enforcement Network (FinCEN) in the United States. A key feature of the feedback given to reporting entities in the United Kingdom is the systematic visits and seminars conducted within each sector. The Serious Organised Crime Agency (SOCA) also provides more general feedback to reporting businesses with website-based guidance on producing useful suspicious activity reports (SARs). Reporting entities also receive alerts to industry which detail information about the SARs regime. France has released less information on the feedback systems between Traitement du renseignement et action contre les circuits financiers clandestins (TRACFIN) and reporting entities in English than other countries, making gauging the level of interaction less accurate. TRACFIN’s annual report, however, contains some information intended for a reporting audience in the form of sanitised cases.

A number of FIUs reported providing or assisting in training key officers in reporting entities. The sector-specific seminars run by SOCA in the United Kingdom are conducted as an education tool for money laundering reporting officers. The United States, United Kingdom and Hong Kong all report formal processes for seeking feedback from reporting entities and others.

1Introduction

Introduction

BackgroundThe primary aims of those who commit economic crimes are to secure a financial advantage and to be able to make use of stolen funds without being detected by police and regulatory agencies. Many criminals, but by no means all, seek to disguise the origins of their criminally derived funds by engaging in a process of money laundering. Others, however, simply spend the money obtained with little attempt at concealment—which often leads to detection by police then prosecution and punishment. Organised criminals, in particular, see many benefits in money laundering, which include the ability to enhance their lifestyle and to enable the profits of their crimes to be re-invested in future criminal activities or in legitimate business operations.

There are three stages to laundering the proceeds of crime. In the initial or placement stage, the money launderer introduces illegal profits into the financial system. In some cases, illegally obtained funds may already lie within the financial system, such as where funds have been misappropriated electronically from the accounts of businesses. Placement can also entail splitting large amounts of cash into less conspicuous smaller sums that are then deposited directly into a bank account, or by purchasing a series of financial instruments, such as cheques or money orders, that are then collected and deposited into accounts at other locations.

After the funds have entered the financial system, the launderer may engage in a series of transactions to distance the funds from their source. In this layering stage, the funds might be channelled through the purchase of investment instruments, or by transferring money electronically through a series of accounts at various banks. The launderer might also seek to disguise the transfers as payments for goods or services, thus giving them a legitimate appearance. Another device used at the layering stage is to use corporate and trust vehicles to disguise the true beneficial ownership of the tainted property.

Having successfully processed criminal proceeds through the first two phases, the money launderer then moves to the third or integration stage in which the funds re-enter the legitimate economy. The launderer might choose to invest the funds in real estate, luxury assets, or business ventures. It is at this stage that criminals seek to enjoy the benefits of their crimes, without risk of detection.

In response to mounting international concern about money laundering, FATF-GAFI was established in 1989. FATF-GAFI is an inter-governmental body which sets international standards and develops and promotes policies to combat money laundering and terrorist financing. In 1990, FATF-GAFI issued a set of 40 Recommendations to guide the fight against money laundering (FATF-GAFI 2004). The 40 Recommendations set out the framework for anti-money laundering efforts and provide a set

2 Anti-money laundering and counter-terrorism financing across the globe

The strong emphasis that FATF-GAFI places on regulating financial institutions and other businesses aims to prevent money laundering and the financing of terrorism by making these activities more difficult for offenders to commit and facilitating the detection of offences by contributing information to law enforcement agencies. The removal of Burma (Myanmar) from FATF-GAFI’s Non-Cooperative Countries and Territories list in October 2006 (FATF-GAFI 2007b) signified basic levels of compliance with the 40 plus nine Recommendations by the vast majority of countries globally.

There is, however, considerable disparity in the manner in which different countries across the globe have implemented the Recommendations and the scope and application of the Recommendations continues to evolve as local legislation and case law appears. Some countries have, for example, placed stringent limitations on the scope of the Recommendations through the enactment of local legislation, as interpreted by the courts. On occasions, this has limited greatly the application of the Recommendations to specific business sectors or types of transactions. By contrast, many countries, such as Australia, have recently introduced further legislation or amended existing legislation to implement FATF-GAFI’s Recommendations more fully. The new legislation in these countries has yet to be tested, either before the courts in connection with prosecutions for non-compliance, by law enforcement organisations using the information gathered, or by the FATF-GAFI mutual evaluation process. It is timely, therefore, to review the state of international responses to the FATF-GAFI Recommendations to assess how countries have applied the requirements, what sectors have been subject to regulation and how compliance and enforcement are undertaken.

Aims and definitionsThis report presents an environmental scan of the differing approaches taken by nine countries, including Australia, to adopting an AML/CTF regulatory regime and aims to make a meaningful comparison between those regimes in a number of key areas. It also seeks to document potential measures of the extent of the application of

of counter-measures covering the criminal justice system and law enforcement, the financial system and its regulation, and measures to enhance international cooperation.

Following the attacks on the United States on 11 September 2001, FATF-GAFI expanded its mandate to deal with the financing of terrorism and created an additional nine Recommendations aimed at combating the funding of terrorist acts and terrorist organisations (FATF-GAFI 2008c). Financial transaction monitoring expanded considerably with the inclusion of counter-terrorism financing into the regime. The financing of terrorism often involves the use of legitimately derived funds, unlike money laundering which invariably involves the proceeds of criminal activities. As such, regulators have been required to examine a wide and ever-increasing number of transactions in an attempt to locate those which could show evidence of money laundering or financing of terrorism.

In June 2003, FATF-GAFI completed a major review of its Recommendations. The revised Recommendations were designed to combat increasingly sophisticated money laundering techniques, such as the use of corporate and trust entities to disguise the true ownership and control of illegal proceeds, and the increased use of professionals to advise and assist in money laundering. The Recommendations indicate the measures FATF considers necessary within criminal justice and regulatory systems, the preventive measures FATF-GAFI suggests are to be taken by financial institutions and certain other businesses and professions, and measures to facilitate international cooperation (FATF-GAFI 2004).

The FATF-GAFI 40 plus nine Recommendations to combat money laundering and the financing of terrorism have three primary objectives (FATF-GAFI 2004):

• to support the criminalisation of money laundering and the financing of terrorism;

• to ensure that assets linked to money laundering or the financing of terrorism can be frozen and confiscated; and

• to ensure that financial institutions and other regulated businesses comply with the Recommendations.

3Introduction

that took place or were attempted in a single country in a single year. The volume could also simply reflect the results of action by regulators in educating regulated businesses concerning their reporting obligations. The extent to which suspect and other transactions are reported is also dependent on the view taken by those in the regulated sectors concerning the necessity for, and effectiveness of, reporting. Some may take the view that reporting is unnecessary in most situations, while others may report even low-risk matters in order to avoid risk of enforcement action for regulatory non-compliance. The number of reports made also reflects the number of transactions that take place within a country each year. Many reports may reflect the presence of a large economy with an active financial services sector—the business sector likely to be responsible for the highest proportion of suspect matter reports.

Similar considerations apply to the use of money laundering convictions as a measure of money laundering that occurs in a given country (Reuter & Truman 2005). Few convictions may mean that there is little detected money laundering occurring, or that money laundering simply is not being detected, reported or dealt with by police and prosecutors. Further, it may also mean that prosecutors favour charging predicate offences or alternative changes rather than using offences of money laundering where these exist. Put simply, official crime statistics in this area often provide a poor measure of underlying money laundering activity. These and other problems of evaluation will be canvassed more fully in another AIC report.

As the countries discussed in this report share a common basis in having agreed to be bound by FATF-GAFI’s Recommendations and other international AML/CTF standards, the central aspects of their AML/CTF regimes are similar. The legal definitions, however, of these common aspects are not uniform across all of the countries considered.

The following are definitions of key aspects of AML/CTF regimes discussed in this report that will be used throughout the report:

• alternative remittance services (ARS)—transmission of money or value, including informal systems or networks, outside of the formal banking sector;

regulatory requirements within each selected country and to assess and compare the extent of compliance and enforcement activities under each regime.

The aim of this report is to provide an intensive comparative review and analysis of some of the primary AML/CTF regulatory issues across the globe, not to reproduce the information contained in FATF-GAFI Mutual Evaluation Reports. Some commentators, such as Harvey (2005) and Sproat (2007), have sought to evaluate the performance of the AML/CTF regime using data on money laundering prosecutions, suspect transaction reporting, asset recoveries and other activity measures. Both Harvey (2008) and Sproat (2007) note the difficulty of evaluating the impact of AML/CTF regimes in the absence of clear evidence on the volume of money laundering prior to implementing enhanced AML/CTF systems. Accordingly, there is little base-line data upon which to undertake a rigorous evaluative assessment. The impact on less tangible goals such as maintaining or improving the integrity of financial systems is more difficult to gauge.

The present report does not seek to evaluate the effectiveness of the AML/CTF regimes of the countries examined as this research activity will be undertaken in another Australian Institute of Criminology (AIC) study. It is apparent, however, that the measures of AML/CTF activity provided in this report are insufficient to draw conclusions on the value of the AML/CTF system in any of the countries examined or to compare performance between them. Many of the core aspects of implementation of the regime globally, such as financial intelligence reporting volumes and conviction rates, cannot be considered proxy measures of the success of the AML/CTF system in the absence of a direct link between these indicia and a working definition of success for the regime. Arguably, the volume of items such as reports of suspicious financial activity could be evidence of either a large-scale money laundering problem or a small one. Simply relying on reporting activity levels is an inadequate measure of the success or otherwise of the regime, as reporting is influenced by a range of considerations in addition to levels of underlying laundering activity and predicate crime. The volume of reports of suspicious financial activities in any given year, for example, could reflect close to the total number of suspect transactions

4 Anti-money laundering and counter-terrorism financing across the globe

• reports of suspicious financial activity—reports lodged by financial institutions and other regulated entities to the financial intelligence unit of any transaction suspected of being the proceeds of criminal activity or involved in the financing of terrorism.

• reports of high-value cash transactions—reports lodged by financial institutions and other regulated entities to the financial intelligence unit of any transaction in cash greater than a nominated value threshold.

• reports of international movements of cash—reports lodged to the financial intelligence unit of the movement of physical currency across national borders, usually above a nominated threshold.

• reports of international electronic transactions—reports lodged by financial institutions and other regulated entities to the financial intelligence unit of the electronic transfer of funds overseas, usually above a nominated threshold;

• FIU—a central agency responsible for receiving (and as permitted, requesting), analysing and disseminating disclosures of financial information:

– concerning suspected proceeds of crime and potential financing of terrorism; or

– required by national legislation or regulation in order to combat money laundering and terrorist financing;

• tipping-off provisions—requirements for entities filing reports of suspicious financial activity to avoid disclosing information about the details or the report, or the existence of a report, to the subject of the report or another prohibited party;

• criminal penalties—penalties imposed following a criminal conviction for an offence;

• civil penalties—penalties imposed following civil proceedings rather than proving an offence to a criminal standard or with criminal court procedures;

• predicate offences—financially motivated offences generating funds to be laundered;

• criminal asset recovery—freezing or confiscating the assets generated by a crime after a conviction for that offence; the required standard of proof is usually beyond a reasonable doubt;

• regulated entities—businesses, including financial institutions, MSBs and designated non-financial businesses and professions with AML/CTF obligations under respective regulatory regimes;

• regulated sector—all businesses providing a financial, money service, or non-financial designated service currently regulated for AML/CTF purposes in each country;

• financial institution—a person or entity conducting, as a business, one or more of the following activities or operations on behalf of a customer:

– accepting deposits and other repayable funds from the public;

– lending and financing commercial transactions;

– financial leasing;

– transferring money or value;

– issuing and managing means of payment such as stored value cards;

– providing financial guarantees and commitments;

– trading in money market instruments, foreign exchange, exchange, interest rate and index instruments, transferable securities or commodities;

– participating in securities issues;

– portfolio management;

– otherwise investing, administering, or managing funds on behalf of another person;

– underwriting and placing life insurance and other investment-related insurance products; and

– money and currency exchanging;

• designated non-financial businesses and professions (DNFBPs)—businesses, outside of financial institutions, identified by AML/CTF legislation as exposed to risks of money laundering and the financing of terrorism. The DNFBPs identified by FATF-GAFI are:

– casinos;

– real estate agents;

– dealers in precious metals;

– dealers in precious stones;

– legal practitioners, notaries, other legal professionals and accountants providing services to external clients; and

– trust and company service providers.

5Introduction

Australia. A Roundtable discussion was also held in Canberra in 2007 with 25 law enforcement and industry stakeholders.

Additional consultations held in the eight countries of interest expanded on the available information on the regulatory environment in those countries and on law enforcement responses to money laundering and the financing of terrorism offences.

• In London, the British Bankers’ Association, the Law Society of England and Wales, the Solicitors Regulation Authority, selected legal practices, the Institute of Chartered Accountants in England and Wales, the Fraud Advisory Panel, the Financial Services Authority, the Organised and Financial Crime Unit, UK Home Office, the Serious and Organised Crime Agency, HM Treasury, the Foreign and Commonwealth Office, Counter Terrorism Policy Department, the International Association of Money Transfer Networks Ltd and the Economic and Specialist Crime Operational Command Unit, Specialist Crime Directorate of the Metropolitan Police Service all provided information on the United Kingdom.

• Consultations with the Ministry of Justice, FIU Germany and Dr Thomas Spies contributed additional statistics and regulatory information for Germany.

• The Banking Commission, situated within the International Chamber of Commerce, and the FATF-GAFI Secretariat in Paris also participated in consultations as part of this project.

• In Belgium, information was provided by the Belgian Financial Intelligence Processing Unit in Brussels.

• In the United States, consultations were held with the Peterson Institute for International Economics, Professor Peter Reuter, Maryland School of Public Policy, the Terrorist Financing Operations Section of the Federal Bureau of Investigation, US Treasury Executive Office for Asset Forfeiture, FinCEN, IMF and Mr Bruce Zagaris, Partner, Berliner, Corcoran and Rowe LLP.

• In Singapore, consultations were held with representatives of the International Centre for Political Violence and Terrorism Research/Nanyang Technological University, Deutsche Bank AG, DBS Bank Ltd, Commercial Affairs Department, OCBC Bank, United Overseas Bank Limited, Citibank Singapore Ltd, BNP Paribas Singapore Branch and the Association of Banks in Singapore.

• civil asset recovery—freezing or confiscating assets that are believed to be generated by a crime in a process held independently from criminal proceedings or not reliant on a conviction for an offence; the required standard of proof is usually on the balance of probabilities and not beyond a reasonable doubt; and

• unexplained wealth—requiring persons possessing suspect assets to demonstrate their lawful acquisition to a court; this process reverses the onus of proof.

The scope and application of each of these terms and concepts is governed by the precise terms of local legislation, as interpreted by the courts. The above definitions are used, in a general sense, for discussion purposes across all jurisdictions.

Geographical scopeThis report compares data from eight countries that demonstrate diverse experiences of implementing AML/CTF measures from the position adopted in Australia. The jurisdictions were selected from North America (United States), Europe (United Kingdom, France, Germany, Belgium) and Asia (Singapore, Hong Kong, Republic of China (Taiwan)) in order to provide an indication of how diverse nations in separate continents have approached AML/CTF implementation. They were also chosen to be indicative of the measures taken in countries with different legal traditions; and of those that experience different types of risk in terms of money laundering and financing of terrorism.

MethodologyThe majority of the information used in this report has been sourced from publicly available documents produced by regulatory bodies, financial intelligence units, law enforcement and other government agencies, industry bodies and FATF-GAFI itself.

The authors undertook a number of consultations with stakeholders in order to supplement the publicly available information. Consultations with the Australian Transaction Reports and Analysis Centre (AUSTRAC)—the Australian financial intelligence unit—provided additional estimates of the number of businesses currently regulated for AML/CTF in

6 Anti-money laundering and counter-terrorism financing across the globe

from regulatory agencies were not available. Mutual Evaluation reports published by FATF-GAFI, IMF, or APG were also employed to estimate the number of businesses in industries with AML/CTF requirements for some countries.

Compliance and enforcement

Compliance and enforcement data were derived from several years of financial intelligence unit and government agency annual reports, activity reviews and the Mutual Evaluation reports. English language translations were not available from some agencies; data were also gathered from agency websites in these instances.

Structure of this reportThis report provides a summary of the regulatory regime and key cases in each country, the estimated size of the regulated sector and the extent of compliance and enforcement activity in each jurisdiction.

The second section describes the AML/CTF legislative regime in each of the nine countries. It includes the criminal provisions for money laundering and the financing of terrorism, as well as the basis of the preventative regulatory measures in place for each country. The structure of the financial intelligence unit, the scope of the regulated sector, the obligations to submit financial intelligence reports, the inclusion of tipping-off provisions and the basis of the required compliance programs are discussed. Less focus is placed on specific customer identification requirements, record keeping provisions and ongoing customer due diligence. A detailed discussion of emerging areas of concern, such as the use of informal banking systems and charities for money laundering and terrorism financing activities, is also beyond the scope of this report. These areas, however, are noted where countries regulate them for AML/CTF purposes.

The second section also provides some consideration of case law arising from money laundering convictions and sanctions applied for non-compliance with AML/CTF regulations. The focus is on prosecutions and other events specifically

• In Hong Kong, consultations were conducted with HK Customs & Excise, Joint Financial Intelligence Unit, Department of Justice, Independent Commission Against Corruption, Hong Kong Monetary Authority, Commercial Crime Bureau, Hong Kong Police Service, Hong Kong Association of Banks and University of Hong Kong.

• In Taiwan, the Money Laundering Prevention Centre (MLPC), Central Bank of the Republic of China, Banking Bureau, Financial Supervisory Commission, Financial Examination Bureau, Criminal Investigation Bureau, National Police Administration, Ministry of the Interior, Interpol Taipei, Office of Homeland Security (Counter Terrorism Office), Crime Research Centre/National Chung-Cheng University, and SinoPac Bank in Taipei also contributed information during consultations.

Regulatory regime and case law

The details on the regulatory regime for each country were sourced from the following publicly available documents:

• legislation;

• guidance notes released by regulatory and industry bodies for specific sectors;

• annual reports from financial intelligence units and government agencies and departments; and

• Mutual Evaluation Reports conducted by FATF-GAFI, IMF and the Asia/Pacific Group on Money Laundering (APG).

The cases discussed for each country have been sourced from published case transcripts and other court documents, legal industry body websites, regulatory compliance agency publications and some media reports.

Evaluating the size of the regulated sector

The estimates of the size of the regulated sectors in each of the countries were drawn extensively from publicly available information from regulatory and supervisory agencies. Information from industry bodies without compliance or enforcement powers was used to estimate the number of businesses with AML/CTF obligations where official figures

7Introduction

A range of measures have been used in an attempt to gauge the degree of compliance and enforcement in each jurisdiction. The countries considered within the scope of this report have not adopted and reported uniform measurements of compliance of enforcement activity and as a result, the information presented for each country is a combination of financial intelligence report statistics, prosecutions statistics and asset freezing and recovery figures.

The final section documents some of the strategies adopted by financial intelligence units and regulators to promote compliance in the selected jurisdictions. The use of electronic report filing, the provision of timely feedback to industry, the extent of training provided to the regulated sectors and the degree to which financial intelligence units have sought feedback from the regulated sectors are methods for boosting compliance are discussed in this section.

involving regulated businesses in the jurisdictions where this information is available. Discussion of criminal prosecutions of individuals for money laundering in some countries has also been included where this has challenged the perception of the money laundering offence in some way.

The third section attempts to describe and compare the size of the regulated sector in each country considered in the scope of the report. The contribution of businesses from the financial, money service and DNFB industries are compared for each country where the information is available. This section also documents the extent of regulation of key non-financial businesses such as legal practitioners, accountants, the gambling industry and dealers in precious metals and stones.

The fourth section surveys the extent of compliance and enforcement activity in the nine countries.

8 Anti-money laundering and counter-terrorism financing across the globe

Regulatory regime

This section presents information on a sample of international AML/CTF regulatory regimes and aims to compare the scope of the regime in Australia with that in the United States and selected countries in the European Union and Asia. The comparison of the AML/CTF regulatory regimes in this section is centred on the key legislation, extent of the regulated sector, the key obligations under the AML/CTF legislation and the financial intelligence unit. This section also addresses case law as it relates to AML/CTF and its implementations in the selected countries.

Financial intelligence unitsFIUs were first established in the late 1980s and early 1990s in response to a need to centralise money laundering information. The scope of FIU responsibilities was subsequently widened to include the financing of terrorism following the increased risks of the twenty-first century. This represented new challenges as the methods of the financing of terrorism are different from those normally associated with money laundering (Schott 2004).

All FIUs share three core functions, which are to receive, analyse and disseminate information in order to combat money laundering and terrorist

financing domestically and as Schott (2004) argues, internationally. Aside from these common core functions, however, the design of FIUs can differ dramatically. Schott (2004) identifies four types of FIU. These are based on an administrative model, a law enforcement model, a judicial (prosecutorial) model and a hybrid model.

The administrative model FIU may be either independent or attached to a regulatory or supervisory authority. The role of the administrative FIU as an intermediary between law enforcement and reporting entities allows this type of FIU to remain neutral. The information channelled through administrative model FIUs is also more easily exchanged between the FIUs of other countries. The drawback of the administrative model is that the separation of the FIU from law enforcement organisations limits its powers to obtain evidence and assert measures based on suspicious transactions. This style of FIU may also be subject to more stringent supervision by political authorities (Schott 2004).