Aerospace & Defence Investment Opportunites by Frost & Sullivan

21

GIL EUROPE GIL EUROPE Aerospace & Aerospace & Defence Defence May May 2012 2012 Dio Papiomytis Principal Consultant

-

Upload

frost-sullivan -

Category

Business

-

view

1.950 -

download

1

Transcript of Aerospace & Defence Investment Opportunites by Frost & Sullivan

GIL EUROPEGIL EUROPE

Aerospace & Aerospace & DefenceDefence

May May 20122012

Dio PapiomytisPrincipal Consultant

Commercial Aviation

� Rising Middle Class in EMs

� Shift in buying habits (mobile)

� Shift in consumptionhabits (e.g. IFE)

� Rising Middle Class in EMs

� Shift in buying habits (mobile)

� Shift in consumptionhabits (e.g. IFE)

• Shift in passenger behaviour-> focus on travel experience

• Rising fuel costs and green tax-> Green practices / tech

• Poor financial results -> Efficiency seeking (hybrids,

asset management, etc.)

• Shift in passenger behaviour-> focus on travel experience

• Rising fuel costs and green tax-> Green practices / tech

• Poor financial results -> Efficiency seeking (hybrids,

asset management, etc.)

Major Trends in CA Segments

• Requirements forlow emissions / fuelconsumption-> New aircraft programmes/ technologies (composites,MEA-AEA, engines)

• Rising backlog / pressure on supply chains-> restructuring

• Low unit margins-> Aftermarket focus

• Requirements forlow emissions / fuelconsumption-> New aircraft programmes/ technologies (composites,MEA-AEA, engines)

• Rising backlog / pressure on supply chains-> restructuring

• Low unit margins-> Aftermarket focus

• Commercialisation of operations

-> restructuring-> requirement for ROI

• Caps on aeronautical charges-> focus on non-aero revenues

-> Peer benchmarking-> Situational awareness (BI)

• Passenger at the core of operations-> Geolocation / LBS

• Commercialisation of operations

-> restructuring-> requirement for ROI

• Caps on aeronautical charges-> focus on non-aero revenues

-> Peer benchmarking-> Situational awareness (BI)

• Passenger at the core of operations-> Geolocation / LBS

Acknowledged Inefficiencies

Aircraft / GSE damage - $4.3B

Lost Baggage - $3B

Airline Earnings (or lack of) – 2003-12

FOD Damage- $1B

+ Lost assets, low productivity, dispersed

data, surplus inventories,

high capex, high fuel consumption…

+ Lost assets, low productivity, dispersed

data, surplus inventories,

high capex, high fuel consumption…

Source: IATA

Investment Attractiveness

HIGH

GROUND HANDLINGAttributesMarket Size: $35B

AVIONICSAttributesMarket Size: $5B

CABIN INTERIORS

AttributesMarket Size: $5BGrowth 2012-16: 8.5%Op. Margins: 14%Concentration: Mid-High

Major Trend: Consolidation

AIRPORTSAttributesMarket Size: $74BGrowth 2012-16: 6%Op. Margins: 17%Concentration: Very Low

Major Trend: Commercialisation

IT

AttributesMarket Size: $10BGrowth 2012-16: 10%Op. Margins: 5.5%Concentration: Low

Major Trend: Integration

MRO

AttributesMarket Size: $48B

MID

LOW

AIRLINES

AttributesMarket Size: $550BGrowth 2012-16: 8.2%Op. Margins: 1.3%Concentration: Very Low

Major Trend: Consolidation

AIRCRAFT OEMs

AttributesMarket Size: $100BGrowth 2012-16: 9.3%Op. Margins: 3.95%Concentration: Very HighMajor Trend: Supply Chain Optimisation

Market Size: $35BGrowth 2012-16: 7%Op. Margins:4.4%Concentration: Very Low

Major Trend: Consolidation

ENGINE OEMs

AttributesMarket Size: $34BGrowth 2012-16: 10.5%Op. Margins: 10%Concentration: Very HighMajor Trend: Aftermarket Services (MRO / FHM)

Market Size: $5BGrowth 2012-16: 6.4%Op. Margins: 11%Concentration: Mid-High

Major Trend: Expansion

Market Size: $48BGrowth 2012-16: 3.5%Op. Margins: 7%Concentration: Mid-High

Major Trend: Alliances

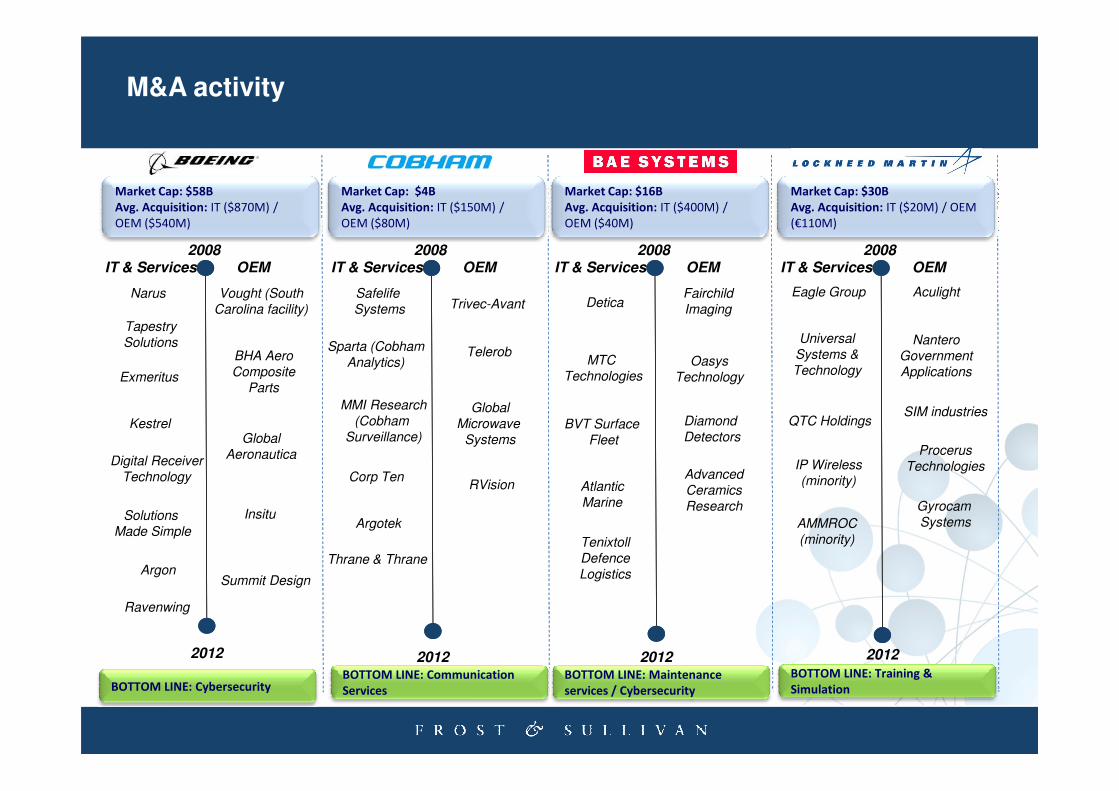

M&A activity

2008

IT & Services OEM

Narus

Tapestry

Solutions

Exmeritus

Vought (South

Carolina facility)

Market Cap: $58B

Avg. Acquisition: IT ($870M) /

OEM ($540M)

2008

IT & Services OEM

Sparta (Cobham

Analytics)

Safelife

Systems Trivec-Avant

Telerob

Market Cap: $4B

Avg. Acquisition: IT ($150M) /

OEM ($80M)

2008

IT & Services OEM

MTC

Technologies

Fairchild

Imaging

Oasys

Technology

Market Cap: $16B

Avg. Acquisition: IT ($400M) /

OEM ($40M)

2008

IT & Services OEM

Market Cap: $30B

Avg. Acquisition: IT ($20M) / OEM

(€110M)

Eagle Group Aculight

Nantero

Government

Applications

Universal

Systems &

TechnologyBHA Aero

Composite

Parts

Detica

2012

Kestrel

Digital Receiver

Technology

Solutions

Made Simple

Argon

Ravenwing

Global

Aeronautica

Insitu

Summit Design

2012

MMI Research

(Cobham

Surveillance)

Corp Ten

2012

BVT Surface

Fleet

Diamond

Detectors

Advanced

Ceramics

Research

Atlantic

Marine

2012

BOTTOM LINE: CybersecurityBOTTOM LINE: Communication

Services

Argotek

Global

Microwave

Systems

Thrane & Thrane

RVision

BOTTOM LINE: Maintenance

services / Cybersecurity

Tenixtoll

Defence

Logistics

BOTTOM LINE: Training &

Simulation

QTC HoldingsSIM industries

Procerus

Technologies

Gyrocam

Systems

IP Wireless

(minority)

AMMROC

(minority)

M&A activity

2008

IT & Services OEM

L-1 Identity

Solutions

GE Homeland

Protection

Market Cap: $15.5B

Avg. Acquisition: IT (n/a) / OEM

($700M)

2008

IT & Services OEM

HARCO Labs

McKechnie

Aerospace

Telair’s Actuation

Business

Market Cap: $6.4B

Avg. Acquisition: IT (n/a) / OEM

($180M)

2008

IT & Services OEM

Kongsberg’s

Aviation Assets

B&R Machine &

Tool

Market Cap: $3B

Avg. Acquisition: IT (n/a) / OEM

($240M)

2008

IT & Services OEM

Market Cap: $16B

Avg. Acquisition: IT (n/a) / OEM

($300M)

TEAC

Aerospace

Merritt Tool

Aviation

Network

ServicesSkyline

Industries

Recon/Optical’s

2012 2012

Amsafe

Global

Holdings

2012 2012

BOTTOM LINE: Security BOTTOM LINE: Aerospace Tier 2 BOTTOM LINE: Aerostructures BOTTOM LINE: Aerospace Tier 2

SNPE Materiaux

Energetiques

SDU Identification

JV: Sagembat

Defence

JV: Snecbat

Engine

Semco

Instruments

CEF Industries

Aircraft Parts

Corporation

ACME

Schneller

Holdings

Merritt Tool

Mexmil Company

Fabritech

Saygrove

Defence &

Aerospace

Vought Aircraft

Industries

Recon/Optical’s

Assets

Cloud Cap

Technology

Crompton

Technology

Winslow

Marine Products

Microtecnica

AIS Global

Dukes Inc

MRO MRO MRO

Market Opportunities

� Electro-Mechanical Actuation

� Composites and Applications

� PMA

Manufacturing IT Aftermarket

� Business Integration

� Asset Management Solutions (Airport, MRO)

� Cloud Computing

� Asset Management (off-balance sheet)

� Equipment Condition Monitoring

� PMA

� (Welding) services

� Ground Support Equipment (scale) –buyout and roll up

� Cloud Computing

� Aircraft Connectivity (Satellite / Wireless)

� Geolocation & Airport LBS

Defence

30%

70%

Budget

allocated to

Procurement

Other

Operating

Costs

Global Defence Budget Forecast by Region (2011-2020)

0

200

400

600

800

1000

1200

1400

1600

1800

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Global Defence Expenditure (2011-2020)

Global Defence Budgets: A cost conscious approach

In U

SD

Bill

ion

• Defence budget continues to grow steadily, driven by EMs

• Cost conscious technology acquisition – focus on Equipment TLCM

• Decline in Supply R&D spending

• Suppliers increasingly looking towards new geographies and new sectors (e.g. Security due to similar customer requirements)

North America Europe APAC Middle East Latin America Africa

439 438 438444

451458

466

476

486

496

400

410

420

430

440

450

460

470

480

490

500

510

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Global Defence Procurement Spending Forecast (2011-2020)

CARG = 1.2%CARG = 1.2%

In U

SD

Bill

ion

1

3

2

High(>10%)

CA

GR

fo

r V

erti

cal M

arkets

Sectors with highest total growth potential

Unmanned Systems1

Military Airlift

2 Force Protection

3

Combat Aircraft4

5 Land Combat Systems

1

2

Key Defence Markets: Tactical Surveillance and C4ISTAR reassure their supremacy as key segments of growth Key Defence Markets

3

6

9

5

8

7

4

Small (<$2 billion)

Large(>$5 Billion)

Market Size of Vertical Markets

Low(0-5%)

CA

GR

fo

r V

erti

cal M

arkets

Medium($2-$5 Billion)

Medium(5-10%) 6 Soldier Modernisation

7

8

Strategic & Tactical Comms

9

Training and Simulation

Command and Control

CAGR is calculated from 2010 - 2014

1 Tactical Surveillance

2 C4ISTAR

• Companies looking to expand their Unmanned Systems product offerings through partnering and acquisition

• The UAS industry in the U.S. is highly concentrated with approximately 80 percent of the market held by four companies (General Atomics, Northrop Grumman, Boeing and Aerovironment)

• Large UAVs are expected to see just over 2.07% CAGR between 2011-2020, whilst Small and Mini UAVs expect over 12.2%. APAC is expected to be fastest growing market in the next decade.

Unmanned

Systems

Unmanned

Systems

Key Technology FocusMarket FocusUnmanned Aerial Systems

Total Military UAS Spending Forecast – Split by Region (2011-2020)

Where to invest?

• New technologies can be found within universities and SMEs

• Companies with multi-application solutions for the civil UAS market (i.e. firefighting, border surveillance, broadcasting, agriculture)

Growth Potential of Opportunities

HighUAS

Ground Mobile

C4ISR Market: Priority Product Areas 2011-2020

C4ISR

• Estimated to be worth over $15B in 2020, C4ISR solutions continue to be priority in MoD spending due to the rapid technological developments

• Europe will grow at1.0% CAGR between 2011-2020, with APAC and ME expected to reach 7% and 6% CAGR respectively

Market FocusC4ISR

Where to Invest?

Attractiveness of Opportunities

Low Medium High

Low

Medium

Force Tracking

VehicleC2

System

Low Priority Medium Priority High Priority

SDR

Multi-bandRadar

Ground

Station

AirborneConsoles

SystemsSubmarine

SystemsCombatships

Fire ControlSystem

SATCOM

SystemsFast Jets

SystemsTransport

planesSystemsRotary Wings

SystemsPetrol ships

Datalinks MANET

R&TSystem

Soldier Device

• Focus on innovation and integration capabilities are key for suppliers. Suppliers with modular and COTS products have a competitive advantage.

• EMs with a relatively young C4ISR industry and heavy modernisation requirements in APAC, ME and LATAM (e.g. Embraer-Atechpartial acquisition)

• Tier 2 and 3 suppliers with early wins but in search of further funding

Security

Integrated Security one of the major Global Trends

Integrated

SecurityIncreasing

Innovation

Increased

Technological

Sophistication

Shift in Global

Balance of Power

Green Buildings

Top Ten Future Trends Affecting Security

$ B

illio

ns

Global Civil Security Spending by Region, 2010 - 2020

153045607590

105120135150165180195210

46 50 53 54.5 55 56 58 60 61 65 66

32 36 37 38 38.5 40 44 45 46 47 483032 33 34 36 40 42 45 47 48 50

810 11 12 14 15

17 19 20 22 25

45 6 8 9 8

88 9

1015

Top Ten Global Trends

Smart

Architecture &

Management

New Energy

Aging PopulationImproved IT

BackbonePreventative

Healthcare

�The global security market size is $140 billion and is expected to reach $200 billion by 2020.

�Growth is primarily driven by the US and EMs such as APAC and Middle East

�This excludes cyber security spending (est. $60B, to grow to $140B)

015

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

46 50

North America Europe

APAC (Including India and China) Middle East

South America

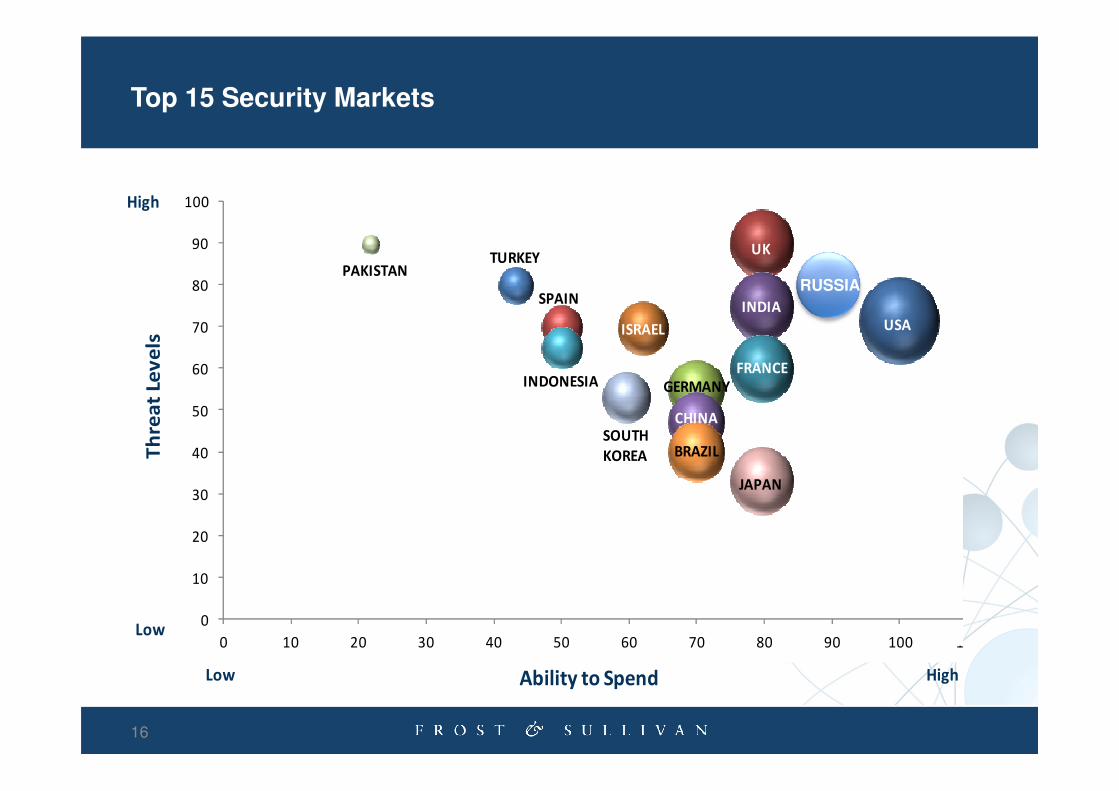

Top 15 Security Markets

High

Th

rea

t Le

ve

ls

60

70

80

90

100

USA

UK

INDIA

FRANCE

PAKISTAN

GERMANY

ISRAEL

TURKEY

INDONESIA

SPAINRUSSIA

16

Low

Th

rea

t Le

ve

ls

HighAbility to SpendLow

0

10

20

30

40

50

0 10 20 30 40 50 60 70 80 90 100 110

JAPAN

GERMANY

CHINA

BRAZILSOUTH

KOREA

Growth Segments

Infrastructure: Government-backed

projects to prove resilient to economic

recession

Education

Government: National and International

organizations (IATA, ICAO, EUROCONTROL) are

unwilling to reduce security investments in favour of

cost cutting.

High

(>10%)

CA

GR

fo

r V

ert

ica

l M

ark

ets

Healthcare

Gaming and

CasinosLow - Negative

(-5%-5%)

CA

GR

fo

r V

ert

ica

l M

ark

ets

Medium

(5-10%)

Large

Market Size of Vertical Markets

MediumSmall

billion)

Healthcare

Banking and FinanceCommercial

Residential

Emerging Technologies / Practices

Biometrics is increasingly becoming standard in Governmental

applications (e.g. e-passports etc)

The growing importance of integration of security systems with other building management systems has led to the growth of PSIM solutions. Increasingly used to protect critical infrastructure, PSIM

has gained some traction in commercial security as well.

IP-surveillance and the use of multi-mega pixel technology has driven growth for IT storage solutions (SAN/NAS/DAS), reducing the cost per GB of storage and enabling end users to record and

store more video at lower operational cost

Hig

h G

row

th

IP Storage (SAN/NAS/DAS)

High Resolution Cameras

Video Analytics

Biometrics

PSIM

Security as a Service: Following the trend of moving security systems into more IT-related

areas, vendors are focusing on providing managed services (remote monitoring/

management).

Lo

w G

row

th

Mature Technology Emerging Technology

SaaS(Security/Software as a

Service)

Electronic Access Control

IP Cameras

DVRs/NVRs

Analytics

Analogue Cameras

Intrusion Detection

Safe Cities

Integration of existing and new security infrastructure to optimise resources, reduce traffic congestion, improve services to citizens and businesses, and make the city smarter, more secure, and more efficient

New York

Los Angeles

London

TokyoShanghai

Beijing

SeoulHong Kong

Singapore

Moscow

São Paulo

Washington D.C.

Atlanta

San Francisco

Miami

Houston

Toronto

Mumbai

Sydney

PhoenixDenver

Buenos Aires Minneapolis

Madrid Busan

Metro

ChongqingJakarta

Boston

Extr

em

e

Cert

ain

tyH

igh

C

ert

ain

ty

Mexico City

19

Osaka

Chicago

GuangzhouDetroit

BangkokRio de Janeiro

Dallas

Philadelphia

Melbourne

SeattleIstanbul

Pittsburgh

San Diego

TampaTianjin

Metro Manila

Paris

Fukuoka

St. Petersburg

Milan

CairoCleveland

Manchester

St. Louis

Monterrey

Vienna

Baltimore

Basic Level of Surveillancedeployment and Integration

Healthy Economy Strong Economy Powerful Economy

Hig

h

Cert

ain

tyS

tro

ng

C

ert

ain

ty

Source: Frost & Sullivan analysis.

Deployment and Integration of Surveillance and Response

capabilities

Deployment and Integration of Detection , Response and

Mitigation capabilities

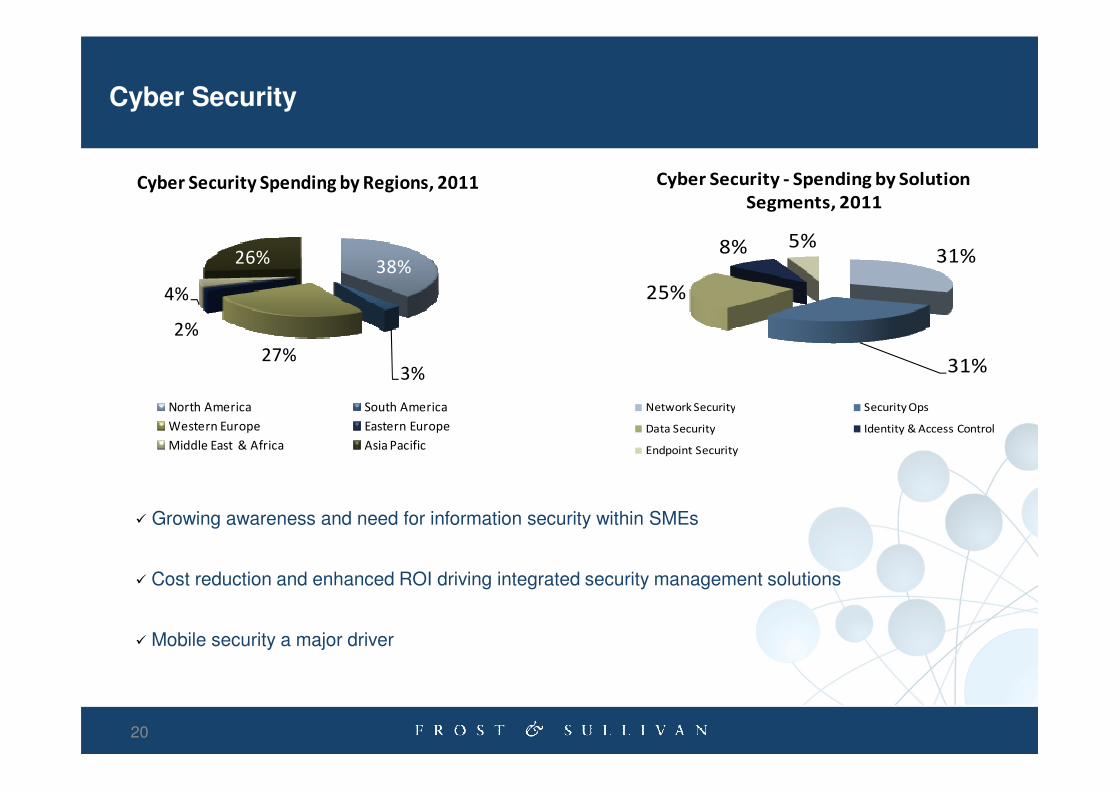

Cyber Security

38%

3%27%

2%

4%

26%

Cyber Security Spending by Regions, 2011

31%

31%

25%

8% 5%

Cyber Security - Spending by Solution

Segments, 2011

20

North America South America

Western Europe Eastern Europe

Middle East & Africa Asia Pacific

Network Security Security Ops

Data Security Identity & Access Control

Endpoint Security

� Growing awareness and need for information security within SMEs

� Cost reduction and enhanced ROI driving integrated security management solutions

� Mobile security a major driver

Conclusions

COMMERCIAL AVIATION:

� Changing business models and supply chain shifts across commercial aviation markets

� Opportunities in Services and Aftermarket

DEFENCE:

�Stable defence budgets, with focus on TLCM

21

� Opportunities in Mini UAVs and Communications

SECURITY:

� High growth market, driven by Critical Infrastructure projects and Cyber

� Opportunities in Integration and Managed Services (SaaS)