3PL Report - Frost & Sullivan

107

www.frost.com Strategic Analysis of the Third Party Logistics Markets in India 4C77-18

-

Upload

sugandharohira -

Category

Documents

-

view

1.079 -

download

15

Transcript of 3PL Report - Frost & Sullivan

www.frost.com

Strategic Analysis of the Third Party Logistics

Markets in India

4C77-18

#4C77-18 © 2006 Frost & Sullivan www.frost.com

Frost & Sullivan takes no responsibility for any incorrect

information supplied to us by manufacturers or users.

Quantitative market information is based primarily on

interviews and therefore is subject to fluctuation.

Frost & Sullivan reports are limited publications con-

taining valuable market information provided to a select

group of customers in response to orders. Our customers

acknowledge when ordering that Frost & Sullivan reports

are for our customers’ internal use and not for general

publication or disclosure to third parties.

No part of this report may be given, lent, resold, or

disclosed to non-customers without written permission.

Furthermore, no part may be reproduced, stored in a

retrieval system, or transmitted in any form or by any

means, electronic, mechanical, photocopying, recording,

or otherwise, without the permission of the publisher.

For information regarding permission, write:

Frost & Sullivan

2400 Geng Road, Suite 201

Palo Alto, CA 94303-3331

United States

Table of Contents

C h a p t e r 1

Executive Summary

Introduction and Overview 1-1

Introduction to Logistics Market in India 1-1

Introduction and Overview of the 3PL Market in the India 1-3

Market Overview and Research Findings 1-3

Total 3PL Market in India Size and Forecasts 1-3

Opportunities for the 3PL Service Providers in India 1-4

Competitive Analysis 1-4

Industry Challenges for the 3PL Market in India 1-4

Drivers for the 3PL Market in the India 1-5

Restraints for the 3PL Market in India 1-5

Implications of VAT on 3PL in India 1-5

Strategic Conclusions 1-6

C h a p t e r 2

Strategic Analysis of Total 3PL Market in India

Introduction 2-1

Introduction and Overview of the Indian Logistics Market 2-1

#4C77-18 © 2006 Frost & Sullivan www.frost.com iii

Introduction to 3PL in India 2-4

Evolution of 3PL Market in India 2-5

Awareness and Perception of 3PL in India 2-6

Scenario of the Indian 3PL Market 2-7

Overall 3PL Usage in the Logistics Functions 2-7

3PL Usage in Transportation 2-9

3PL Usage in Warehousing 2-10

3PL Usage in Freight Forwarding 2-12

3PL Usage in MIS and Other Value-added Services 2-12

Market Size and Revenue Forecasts 2-13

The Total Logistics Market in India 2-13

Size of the 3PL Market in the India 2-14

Growth History of 3PL Market in India 2-15

Estimated Share of the 3PL Market 2-15

Revenue Forecasts 2-16

Revenue Forecasts Breakdown by Different Logistics Functions 2-18

Revenue Forecasts for 3PL in Transportation Function 2-18

Revenue Forecasts for 3PL in Warehousing Function 2-19

Revenue Forecasts for 3PL in Freight Forwarding Function 2-21

Revenue Forecasts for 3PL in MIS and Other Value-Added Services 2-22

Industry Challenges and Market Drivers and Restraints 2-24

Industry Challenges 2-24

Geographical Size and Diversity 2-24

Stiff Competition and Pricing Strategies 2-25

Multinational 3PL Companies are at a Disadvantage Compared to the Indian Companies 2-25

Integrating Supply Chains and Providing Visibility Along the Entire Chain 2-25

Security Concern is a Critical Issue 2-25

#4C77-18 © 2006 Frost & Sullivan www.frost.com iv

Market Drivers 2-26

Growth of Multinational Operations Demand Professional Logistics Management 2-26

Growing Inclination to Outsource Logistics to Specialists 2-27

Economic Growth Across Different Sectors Necessitates Smooth Flow of Supply Chain 2-28

Infrastructure Development Facilitates Logistics 2-28

Implementation of an All India VAT System 2-29

Declining 3PL Rates is Likely to Cause More Outsourcing 2-29

Market Restraints 2-29

High Cost of Logistics in India 2-30

Existence of Infrastructure Bottlenecks 2-30

Non-Uniform Implementation of VAT,Complex Laws and Sales Tax Regulations are not Favored by Compines 2-30

Outsourcing to a 3PL Service Provider Attracts a Service Tax 2-31

Competition from the Unorganized Segment 2-31

Major End-Users of 3PL in India 2-31

Implications of VAT on 3PL 2-32

Introduction to VAT 2-32

Challenges for 3PL Service Providers due to VAT's impact 2-33

Reorganization of IT Infrastructure may be Complicated 2-34

Maintaining Large Volumes of Transactional Records Could be a Difficult Task 2-34

Nonuniformity of VAT Implementation Across the Nation and the Co-existence of VAT with the Central Sales Tax

system is Complicating 2-34

Competition from the Unorganized Segment Poses a Significant Challenge to the Growth of these Companies 2-35

Opportunities for 3PL Service Providers due to VAT's impact 2-36

C h a p t e r 3

End-User Analysis—Overview of 3PL Needs and Practices in India

Overview of 3PL Needs and Practices in India 3-1

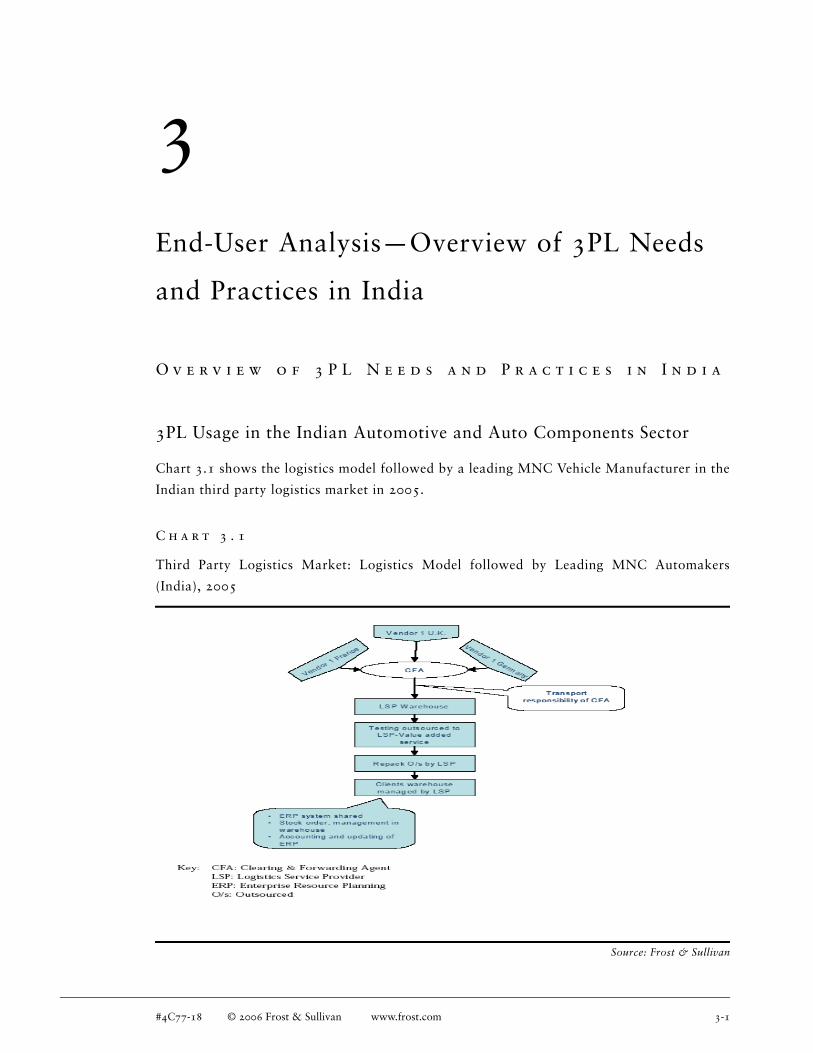

3PL Usage in the Indian Automotive and Auto Components Sector 3-1

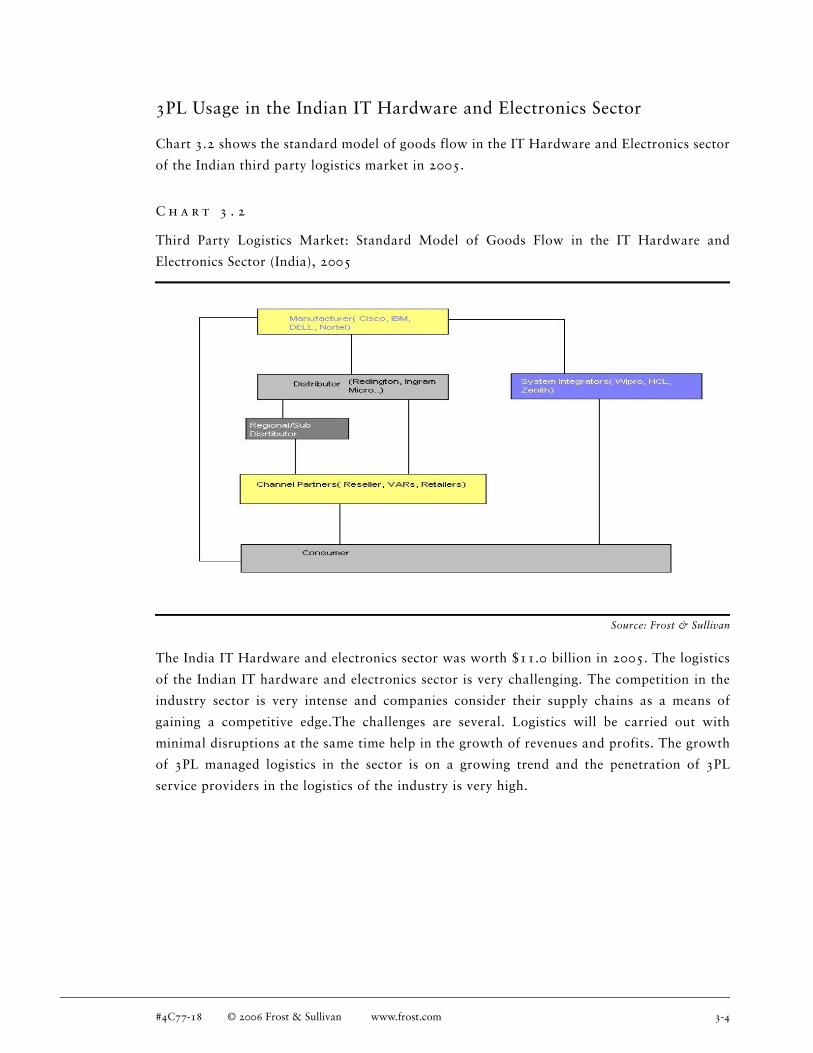

3PL Usage in the Indian IT Hardware and Electronics Sector 3-4

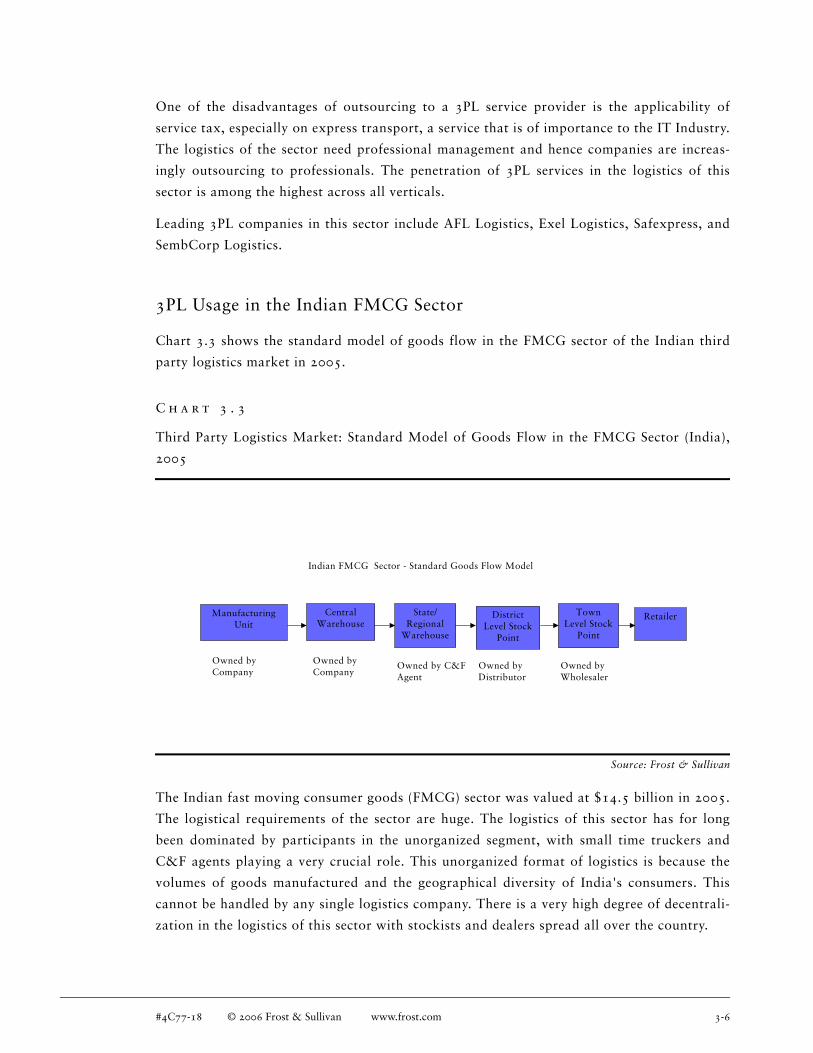

3PL Usage in the Indian FMCG Sector 3-6

3PL Usage in the Indian Pharmaceuticals Sector 3-8

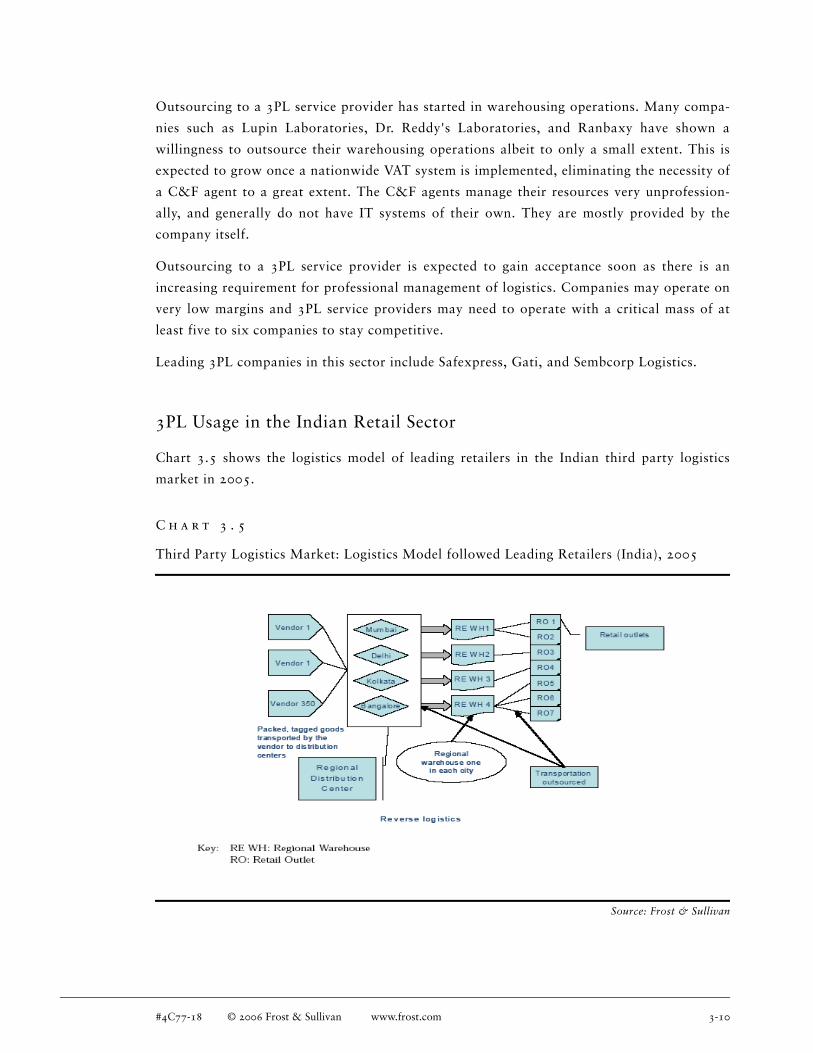

3PL Usage in the Indian Retail Sector 3-10

#4C77-18 © 2006 Frost & Sullivan www.frost.com v

C h a p t e r 4

Competitive Analysis of the 3PL Providers in Indian Market

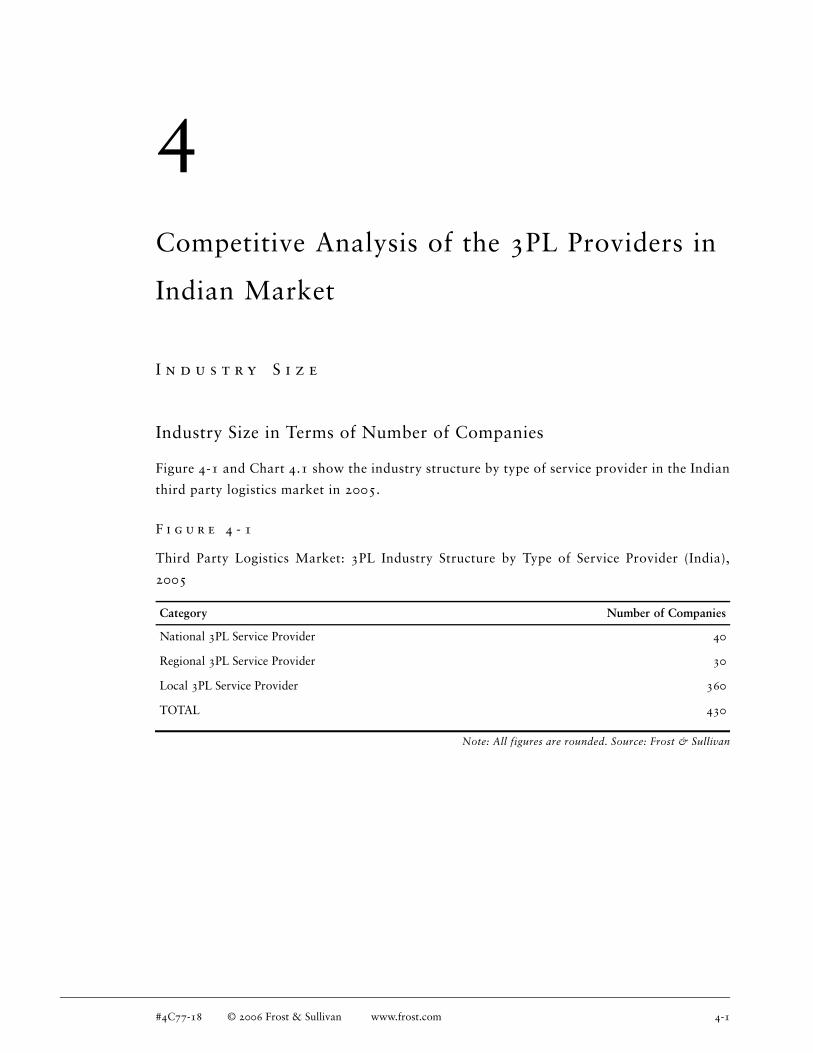

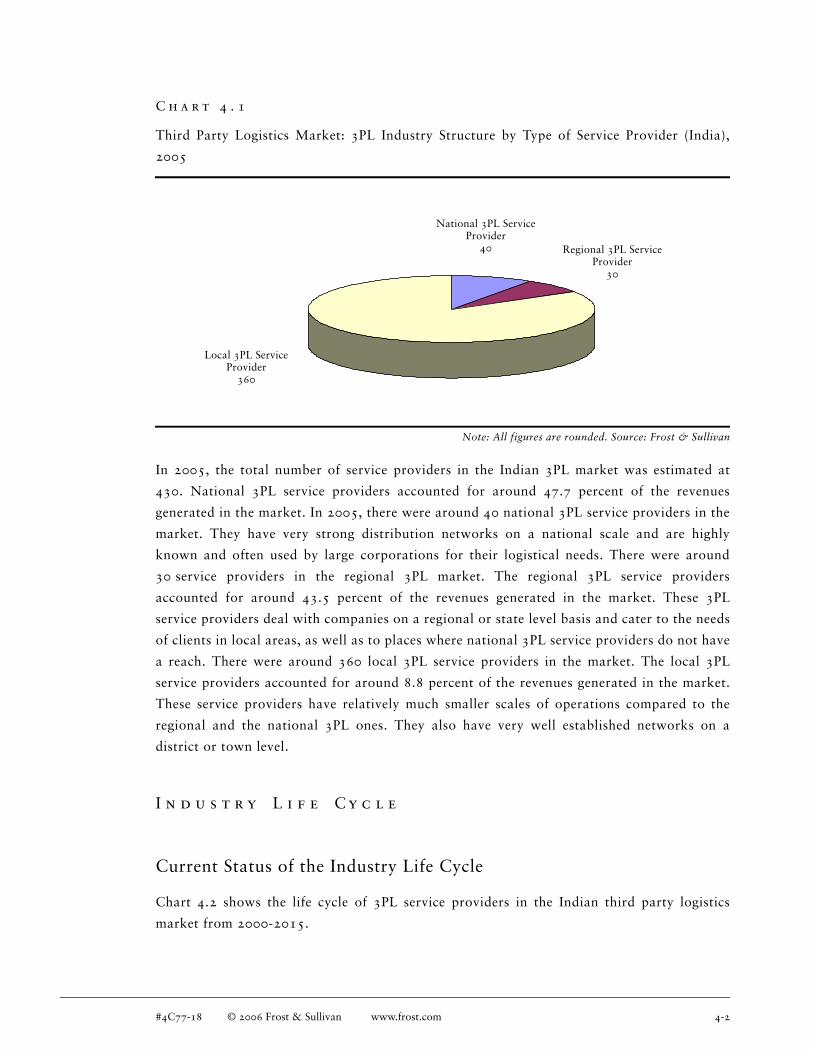

Industry Size 4-1

Industry Size in Terms of Number of Companies 4-1

Industry Life Cycle 4-2

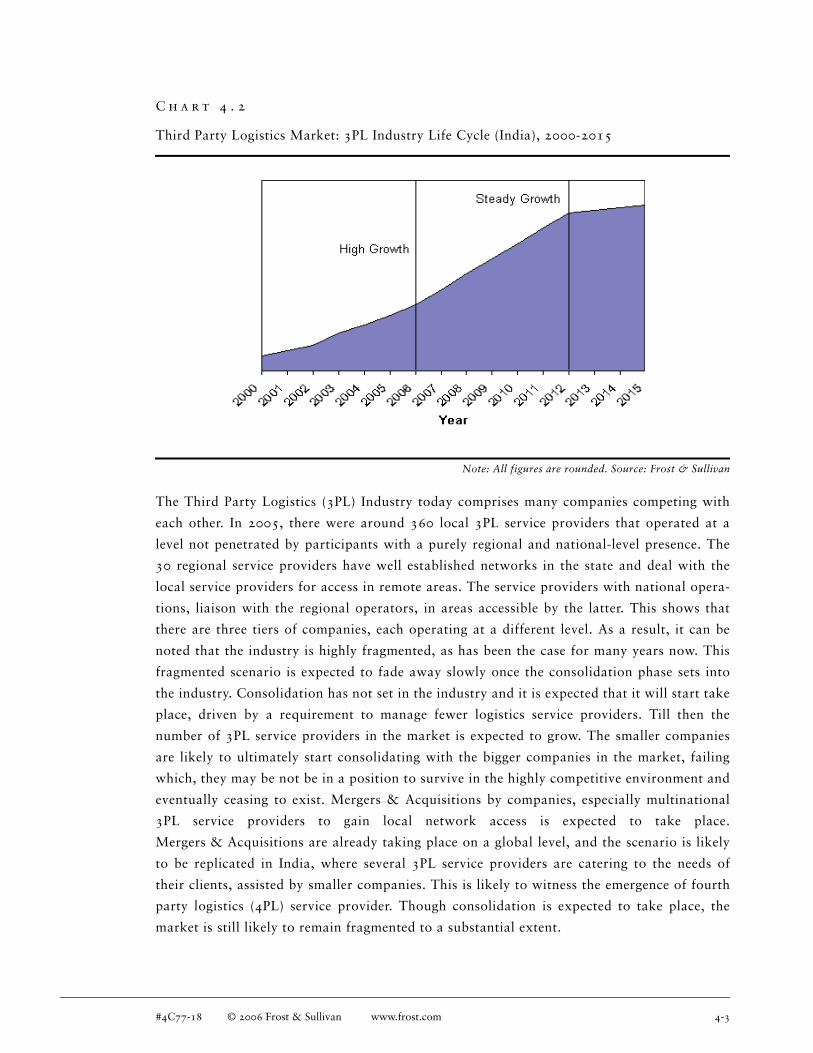

Current Status of the Industry Life Cycle 4-2

Current Status of Market Life Cycle 4-4

Market Share Comparison and Breakup 4-4

Competitive Scenario 4-4

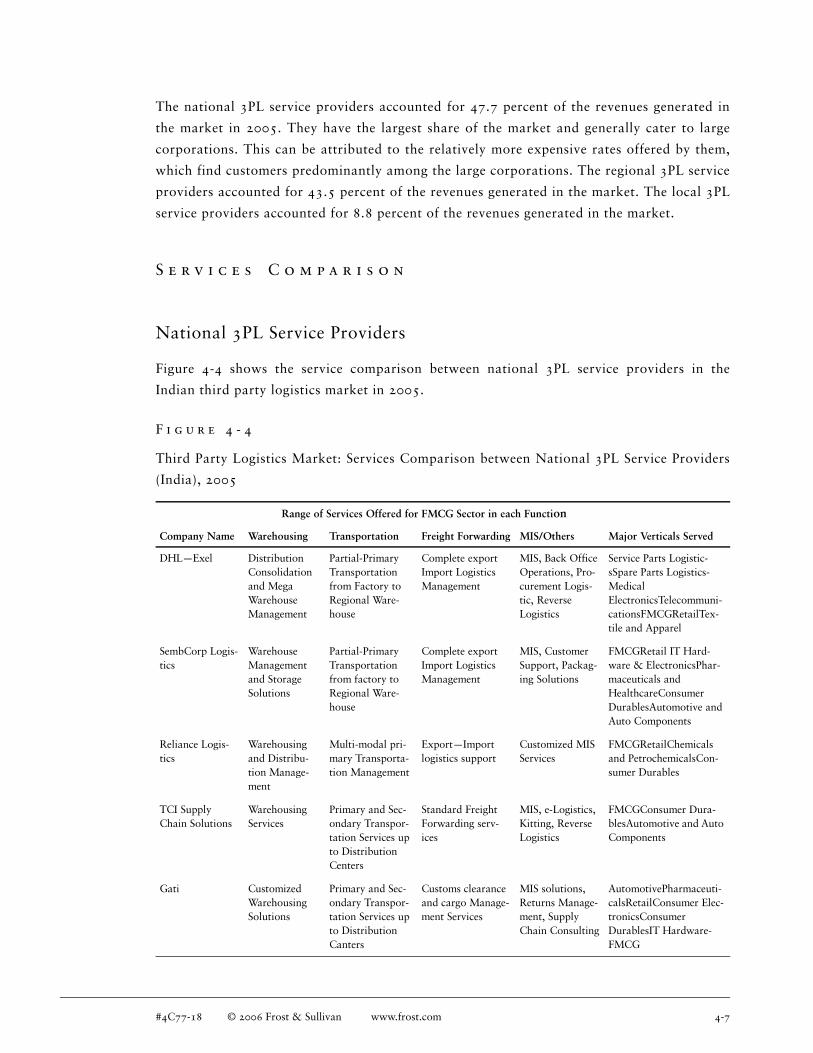

Services Comparison 4-7

National 3PL Service Providers 4-7

Regional 3PL Service Providers 4-9

Local 3PL Service Providers 4-9

Profiles of the Major 3PL Service Providers in India 4-9

AFL Logistics 4-9

DHL 4-11

Dynamic Logistics 4-12

GATI 4-14

Geo Logistics 4-15

Om Logistics 4-16

Patel Logistics 4-18

Reliance Logistics 4-19

#4C77-18 © 2006 Frost & Sullivan www.frost.com vi

Safexpress 4-20

SembCorp Logistics 4-21

Take Solutions 4-23

TCI Supply Chain Solutions 4-24

Total Logistics 4-25

Transystem Logistics International 4-26

TVS Logistics 4-27

Clientele: 4-27

C h a p t e r 5

Recommendations and Growth Strategies for 3PL Providers in India

Opportunities for 3PL Service Providers in India 5-1

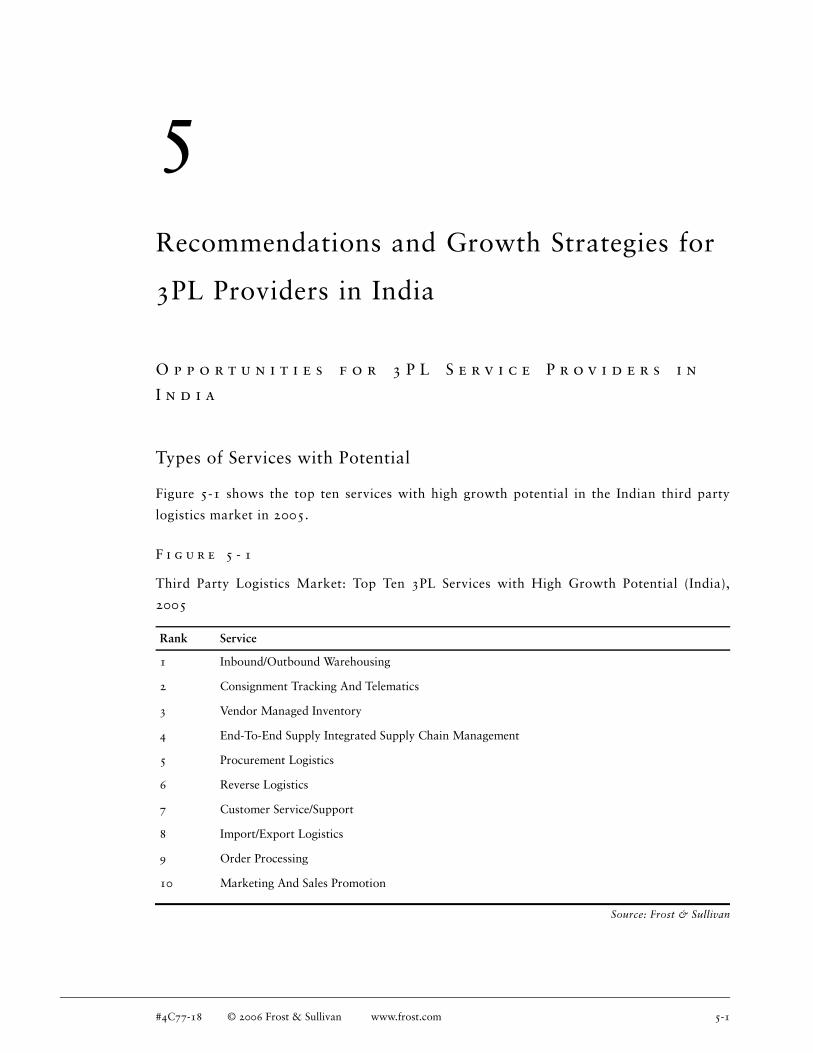

Types of Services with Potential 5-1

Potential of Services during the Forecast Period 5-2

Business Model 5-4

Suggested Business Model 5-4

Pricing and Positioning 5-4

Suggested Pricing Strategy 5-4

Suggested Positioning Strategy 5-4

Strategic Alliances Joint Ventures and Partnerships 5-5

Suggested Strategy for Forming Alliances Joint Ventures and Partnerships 5-5

#4C77-18 © 2006 Frost & Sullivan www.frost.com vii

C h a p t e r 6

Database of Key Industry Participants

Market Participants—3PL Service Providers 6-1

C h a p t e r 7

Decision Support Database

Comparitive Tabulation of Infrastructure and Industry Figures 7-1

Tabulation of Infrastructural Figures 7-1

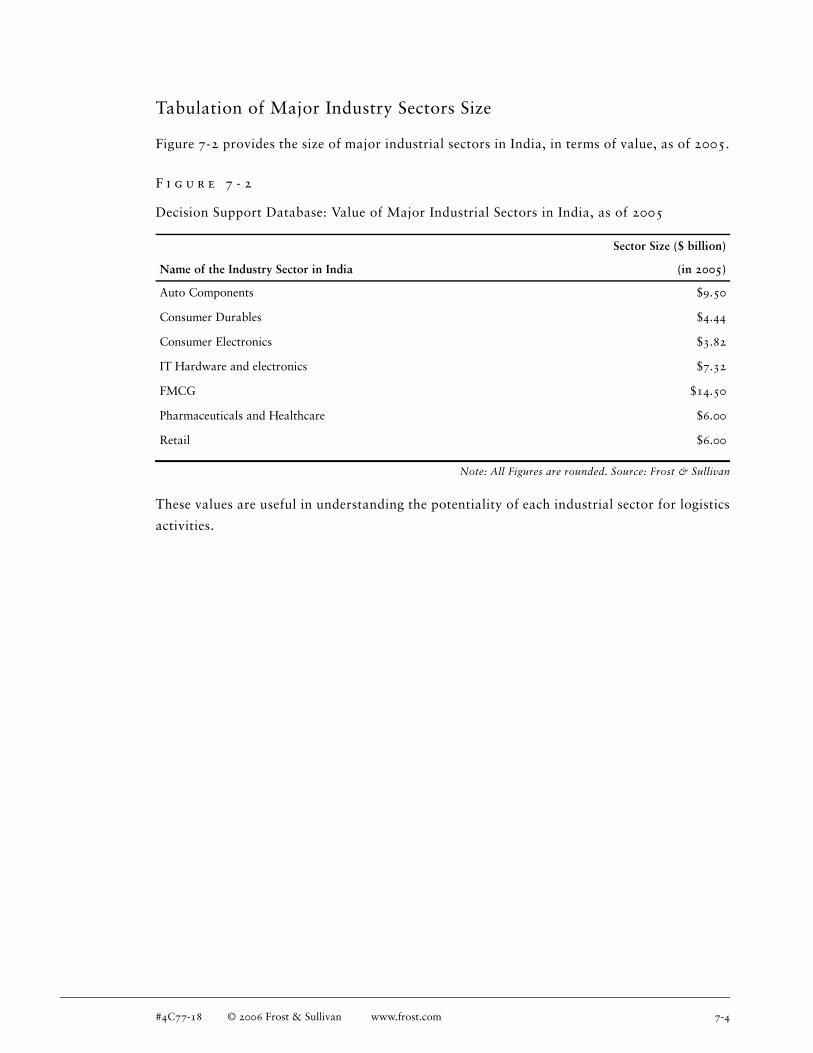

Tabulation of Major Industry Sectors Size 7-4

#4C77-18 © 2006 Frost & Sullivan www.frost.com viii

List of Figures

C h a p t e r 2

Strategic Analysis of Total 3PL Market in India

2-1 Total Third Party Logistics Market:

Breakup by Mode of Freight (India), 2005 2-1

2-2 Total Third Party Logistics Market : Penetration by Logistics Function (India), 2005 2-7

2-3 Total Third Party Logistics Market:

Revenue Breakup by Type of Logistics Function (India), 2005 2-14

2-4 Total Third Party Logistics Market:

Estimated Shares (India), 2005 2-15

2-5 Total Third Party Logistics Market:

Revenue Forecasts (India), 2002-2012 2-17

2-6 Total Third Party Logistics Market:

Revenue Forecasts for Transportation Logistics Function (India), 2002-2012 2-18

2-7 Total Third Party Logistics Market:

Revenue Forecasts for Warehousing Logistics Function (India), 2002-2012 2-20

2-8 Total Third Party Logistics Market:

Revenue Forecasts for Freight Forwarding Logistics Function (India), 2002-2012 2-21

2-9 Total Third Party Logistics Market:

Revenue Forecasts for Value-added Services and Other Services Logistics Functions

(India), 2002-2012 2-23

#4C77-18 © 2006 Frost & Sullivan www.frost.com ix

2-10 Total Third Party Logistics Market:

Impact of Top Industry Challenges (India), 2006-2012 2-24

2-11 Total Third Party Logistics Market:

Market Drivers Ranked in Order of Impact (India), 2006-2012 2-26

2-12 Total Third Party Logistics Market:

Market Restraints Ranked in Order of Impact (India), 2006-2012 2-29

2-13 Total Third Party Logistics Market:

Top End-user Sectors (India), 2005 2-31

C h a p t e r 3

End-User Analysis—Overview of 3PL Needs and Practices in India

C h a p t e r 4

Competitive Analysis of the 3PL Providers in Indian Market

4-1 Third Party Logistics Market:

3PL Industry Structure by Type of Service Provider (India), 2005 4-1

4-2 Third Party Logistics Market:

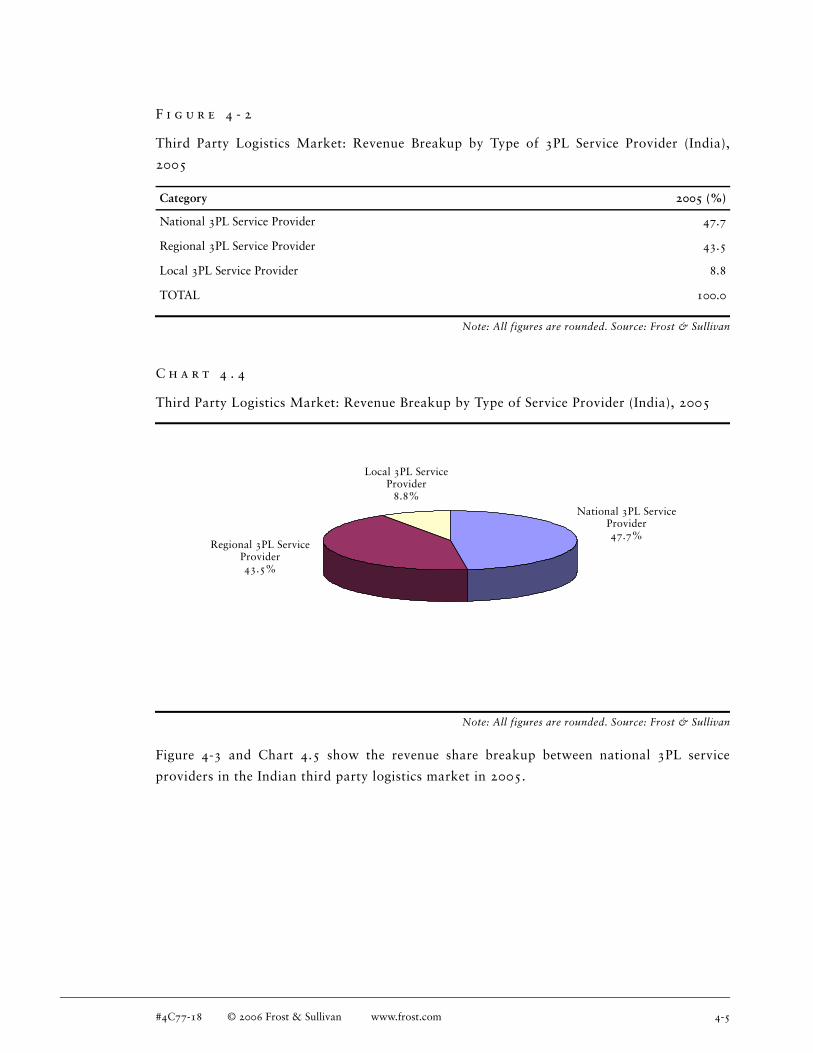

Revenue Breakup by Type of 3PL Service Provider (India), 2005 4-5

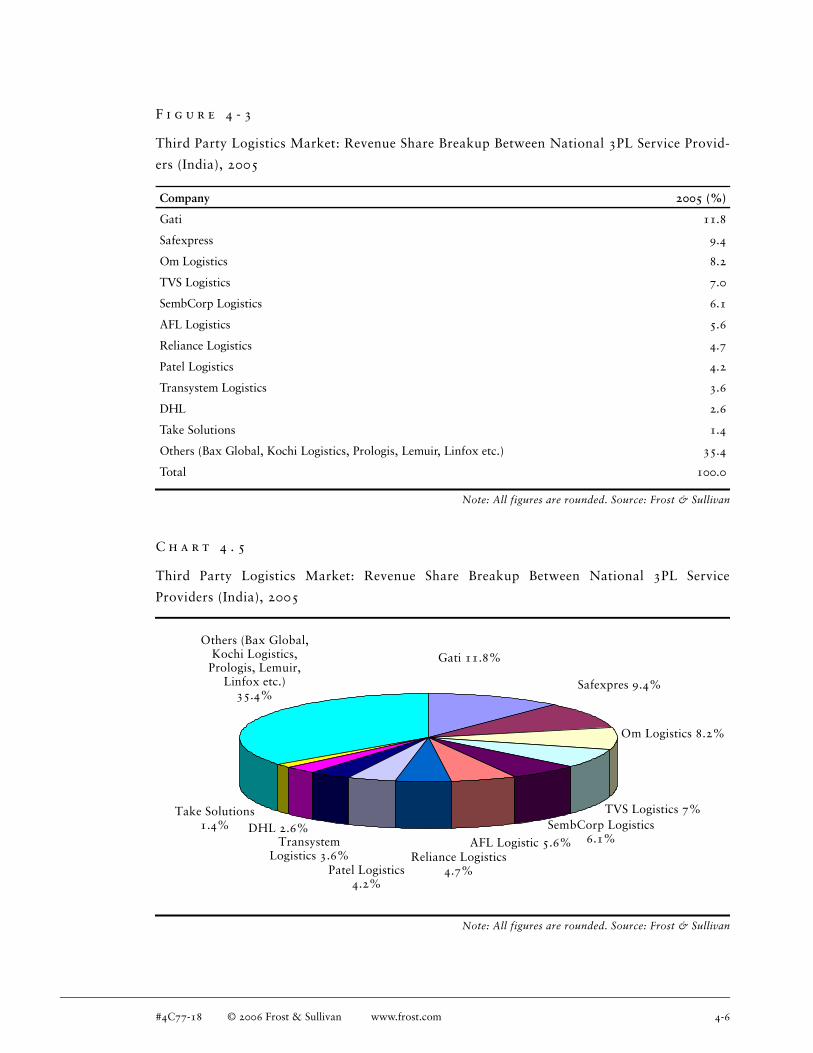

4-3 Third Party Logistics Market:

Revenue Share Breakup Between National 3PL Service Providers (India), 2005 4-6

4-4 Third Party Logistics Market:

Services Comparison between National 3PL Service Providers (India), 2005 4-7

#4C77-18 © 2006 Frost & Sullivan www.frost.com x

C h a p t e r 5

Recommendations and Growth Strategies for 3PL Providers in India

5-1 Third Party Logistics Market:

Top Ten 3PL Services with High Growth Potential (India), 2005 5-1

5-2 Third Party Logistics Market:

Top Ten 3PL Services Ranked in Order of Potential (India), 2006-2012 5-2

C h a p t e r 7

Decision Support Database

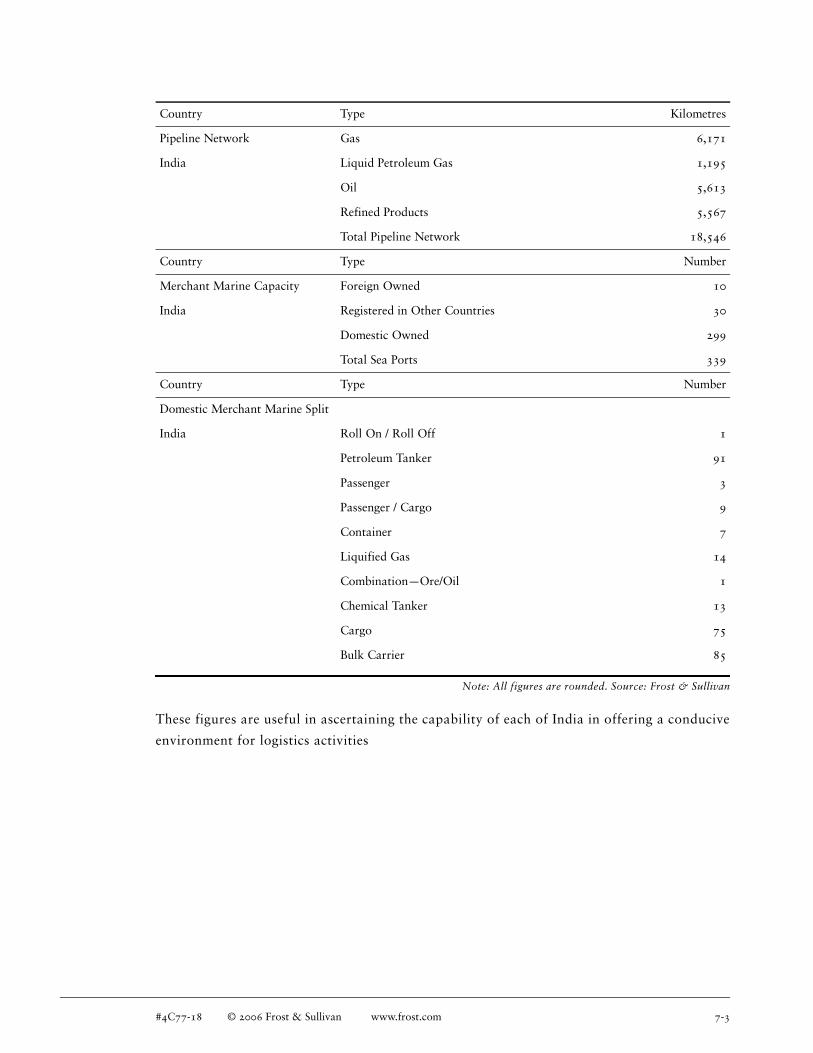

7-1 Decision Support Database:

Tabulation of Economic and Infrastructural Figures 7-2

7-2 Decision Support Database:

Value of Major Industrial Sectors in India, as of 2005 7-4

#4C77-18 © 2006 Frost & Sullivan www.frost.com xi

List of Charts

C h a p t e r 1

Executive Summary

1.1 Third Party Logistics Market:

Market Attractiveness Index by Function (India), 2005 1-2

C h a p t e r 2

Strategic Analysis of Total 3PL Market in India

2.1 Total Third Party Logistics Market:

Breakup by Mode of Freight (India), 2005 2-2

2.2 Total Third Party Logistics Market : Penetration by Logistics Function (India), 2005 2-7

2.3 Total Third Party Logistics Market:

Revenue Breakup by Type of Logistics Function (India), 2005 2-14

2.4 Total Third Party Logistics Market:

Estimated Share (India), 2005 2-16

2.5 Total Third Party Logistics Market:

Revenue Forecasts (India), 2002-2012 2-17

2.6 Total Third Party Logistics Market:

Revenue Forecasts for Transportation Logistics Function (India), 2002-2012 2-19

2.7 Total Third Party Logistics Market:

Revenue Forecasts for Warehousing Logistics Function (India), 2002-2012 2-20

#4C77-18 © 2006 Frost & Sullivan www.frost.com xiii

2.8 Total Third Party Logistics Market:

Revenue Forecasts for Freight Forwarding Logistics Function (India), 2002-2012 2-22

2.9 Total Third Party Logistics Market:

Revenue Forecasts for Value-Added Logistics Services and Other Services Logistics Functions

(India), 2002-2012 2-23

C h a p t e r 3

End-User Analysis—Overview of 3PL Needs and Practices in India

3.1 Third Party Logistics Market:

Logistics Model followed by Leading MNC Automakers (India), 2005 3-1

3.2 Third Party Logistics Market:

Standard Model of Goods Flow in the IT Hardware and Electronics Sector (India), 2005 3-4

3.3 Third Party Logistics Market:

Standard Model of Goods Flow in the FMCG Sector (India), 2005 3-6

3.4 Third Party Logistics Market:

Standard Model of Goods Flow in the Pharmaceuticals Sector (India), 2005 3-8

3.5 Third Party Logistics Market:

Logistics Model followed Leading Retailers (India), 2005 3-10

C h a p t e r 4

Competitive Analysis of the 3PL Providers in Indian Market

4.1 Third Party Logistics Market:

3PL Industry Structure by Type of Service Provider (India), 2005 4-2

4.2 Third Party Logistics Market:

3PL Industry Life Cycle (India), 2000-2015 4-3

#4C77-18 © 2006 Frost & Sullivan www.frost.com xiv

4.3 Third Party Logistics Market:

Market Life Cycle (India), 2000-2015 4-4

4.4 Third Party Logistics Market:

Revenue Breakup by Type of Service Provider (India), 2005 4-5

4.5 Third Party Logistics Market:

Revenue Share Breakup Between National 3PL Service Providers (India), 2005 4-6

#4C77-18 © 2006 Frost & Sullivan www.frost.com xv

1Executive Summary

I n t r o d u c t i o n a n d O v e r v i e w

Introduction to Logistics Market in India

The logistics market in India is fragmented predominantly due to the large presence of unor-

ganized service providers. Logistics, which is one of the lifelines of a country the size of

India, has been so far considered as a secondary activity. The industry broadly consists of

freight consolidators, transporters, warehousing specialists, and organized third party logis-

tics (3PL) service providers, in the increasing order of value addition to the service.

Roads carry the bulk of the freight in India. The roads in India have a history of being unsafe

and in very bad condition. This is likely to change with the construction of the Golden Quad-

rilateral and North-South-East-West (NSEW) highway networks, traversing the entire

country. The highway infrastructure is highly strained, comprising around 1.4 percent of the

total road network in India, carrying in excess of 50 percent of the country's total freight.

Roads are flexible with easy to own assets and door-delivered consignments. Rail freight

comprises around 670 million tones, which is around 33 percent of all domestic traffic in

India. Even though rail freight is more cost effective in terms of cost per unit distance and per

unit weight, the efficiency of the rail freight system in India has for long been low and it has

been looked down upon as a secondary freight mode. With the Indian Government

announcing plans to open up the containerized rail freight sector to private operators,

companies such as APL Logistics, Maersk Logistics, Gateway Distriparks, Central Ware-

housing Corporation, JM Baxi group, Adani Logistics, and Reliance Logistics are expected to

foray into this segment. The barriers to entry for providing this service are rather low and

intense competition is likely to be witnessed.

#4C77-18 © 2006 Frost & Sullivan www.frost.com 1-1

The largely unorganized segment of the logistics industry in India poses a formidable chal-

lenge to companies in the organized segment. The unorganized segment service providers

have lesser overhead costs and are hence in a position to provide extremely competitive rates.

This is expected to have a considerably large impact in the future, posing a challenge espe-

cially to the 3PL service providers. Entry barriers too are low, leading to the possibility of

intensified competition even in the organized sector. Complex tax laws and infrastructure

bottlenecks too are challenging issues to be dealt with.

The growth of in the Indian economy, especially in the manufacturing sector is one of the key

growth drivers for the logistics industry in India. Apart from this, sincere initiatives by the

Government to iron out wrinkles in the logistics infrastructure may also drive the growth in

this sector expected to grow at a compound annual growth rate (CAGR) of 6.4 percent from

2005 to 2012.

Chart 1.1 shows the Market Attractiveness Index by Function for the Third Party Logistics

Market (India), 2005.

C h a r t 1 . 1

Third Party Logistics Market: Market Attractiveness Index by Function (India), 2005

Note: All figures are rounded. Source: Frost & Sullivan

-200.0

-100.0

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

Market Attractiveness (Based on CAGR)

Mar

ket S

tren

gth

(Bas

ed o

n M

arke

t Si

ze in

200

5) U

S $M

illio

n

Transportation

Warehousing

Freight Forwarding

MIS and Other Value-added Services

#4C77-18 © 2006 Frost & Sullivan www.frost.com 1-2

Introduction and Overview of the 3PL Market in the India

Companies in India generally outsource only a part of their supply chain requirements to a

3PL service provider. Only a small fraction of companies outsource entirely to a 3PL service

provider. Most of these companies are multinationals that entered the country and didn't

have an established network and have to outsource their logistics due to the lack of assets.

The degree and nature of outsourcing of logistics to a 3PL service provider varies signifi-

cantly between verticals and depends greatly on the nature of the company. In the automotive

sector, the trend of end-to-end outsourcing is beginning to significantly catch up as compa-

nies have realized the benefits of concentrating on core competencies and delegating the

logistics to 3PL service providers.

The penetration of 3PL is very high in the automotive sector. Likewise, the IT hardware and

electronics sectors have also begun outsourcing to 3PL service providers to a great extent. In

sectors such as Fast Moving Consumer Goods (FMCG) and pharmaceuticals, the penetration

of the 3PL concept has been fairly low, owing to already strained profit margins. Added to

this, there is a great deal of decentralization in the supply chains of these sectors, with many

stocking points and strategic distribution centers spread all over the country. This will

demand infrastructure capabilities that the 3PL service providers may not be in a position to

offer. Outsourcing in these sectors has started in warehousing operations, albeit in a small

way. Certain 3PL service providers have their own freight forwarding and customs clearance

capabilities. Those that do not have, hire the services of a local freight forwarding agent to

liaison with the required authorities to have their consignments cleared. Most 3PL service

providers offer good management of information systems (MIS) capabilities to their clients.

The provision of value-added propositions along with a 3PL contract is expected to witness a

growing trend with increasing demands from the clients and 3PL service providers that want

to gain an edge in a highly competitive marketplace.

M a r k e t O v e r v i e w a n d R e s e a r c h F i n d i n g s

Total 3PL Market in India Size and Forecasts

The market for 3PL in India was worth $890.3 million in 2005. The entire 3PL market is

expected to grow at a CAGR of 21.9 percent from 2005 to 2012 and reach $3,556.7 million

in 2012. In 2005, transportation activity outsourced to a 3PL service provider accounted for

a lion's share of the revenues in the market. However, warehousing is expected to grow the

fastest among all the logistics functions outsourced to a 3PL service provider. In 2005, it

accounted for second largest share of entire market. Revenues from MIS and Other Values

Added Services accounted for third largest share of the market revenues with freight

forwarding accounting for the lowest share.

#4C77-18 © 2006 Frost & Sullivan www.frost.com 1-3

Opportunities for the 3PL Service Providers in India

India has immense opportunities for 3PL service providers. The growth is expected to come

predominantly from warehousing, which is likely to be driven to a very great extent by the

implementation of value added tax (VAT), a uniform tax regime across the country. The

benefits are expected to be witnessed by the year 2010, when the central sales tax is likely to

be completely abolished. In the transportation function, the growth of express transport

could provide opportunities for the service providers. The growth is expected to be driven by

the betterment of infrastructure and increasing client requirements to provide committed and

time-bound services. Express transport has a very small share of the entire trucking market,

and hence presents immense potential for growth. Freight forwarding and MIS and Other

value-added services also present good opportunities in the market. The growth in

value-added services is expected to be driven by the growth in transportation and ware-

housing functions, and as a tool by 3PL service providers to gain a competitive edge in the

market. A majority of the revenues from value-added services in the market is expected to be

generated from growth in the warehousing function.

Competitive Analysis

The 3PL service providers in India are categorized into three tiers of competition namely

national, regional, and local service providers depending on their presence and reach in the

market. The major national 3PL service providers are the Tier I companies and they account

for the largest share of the revenues generated in this market. This can be attributed to the

relatively better rates and value propositions offered by them, which find customers predom-

inantly among large corporations. The regional 3PL service providers, or the Tier II

companies account for the second largest share of the revenues generated in this market.

These service providers offer basic logistics support and generally operate with corporations

and Tier I companies to provide access at a regional level. The local 3PL service providers, or

the Tier III companies that account for lowest share of the revenues generated in this market.

They have small clientele and provide logistics services that does not have a large reach.

Industry Challenges for the 3PL Market in India

Industry challenges are factors that have the potential to adversely affect the market growth

during the forecast period from 2006 to 2012. Though these may not have any direct bearing

on the growth of the market, they can be overcome using suitable strategies:

Geographical size and diversity

Stiff competition and pricing strategies

Security concern is a critical issue

#4C77-18 © 2006 Frost & Sullivan www.frost.com 1-4

Drivers for the 3PL Market in the India

Market drivers are factors that have the potential to drive the growth of the market during

the forecast period from 2006 to 2012.

Growing inclination to outsource logistics to specialists

Economic growth across all sectors necessitates smooth flow of supply chain

Implementation of an all India VAT system

Restraints for the 3PL Market in India

Market restraints are factors that have the potential to slow or retard the growth of the

market during the forecast period from 2006 to 2012.

High cost of logistics in India

Infrastructure bottlenecks still exist

Competition from the unorganized segment

Implications of VAT on 3PL in India

The implementation of a uniform VAT regime and the elimination of the sales tax model is

expected to indirectly benefit the supply chain management in the country. Previously state

borders were viewed as economic borders, as they posed hurdles to the sale of goods between

states. As a tax saving mechanism, companies operated on a highly decentralized model of

multiple warehouses spread across states. This ultimately led to management of more

resources and manpower, leading to costs that could otherwise have been avoided.

The original intention of the Indian Government behind implementation of VAT was to intro-

duce transparency into the taxation system; however, it has indirectly changed the course of

logistics in the country. The present model poses a problem of cascading taxes, which VAT is

expected to abolish.Companies are expected to move to newer and more centralized hub and

spoke distribution models that will be more convenient with lesser hassles. VAT is expected

to abolish the economic borders between states and enable sales between points with

geographic convenience in consideration, as opposed to the tax planning driven model that

was practiced earlier.

#4C77-18 © 2006 Frost & Sullivan www.frost.com 1-5

The real benefits of VAT impacting the supply chain management in India are not likely to be

witnessed until the central sales tax is eliminated. At present, VAT coexists with the central

sales tax, which is expected to be phased out by 2010. The persistence of central sales tax

defies the logic behind shifting to the new hub and spoke model, as there is no input tax

credit available against the central sales tax in the case of inter state sales. Input tax credit is

the reimbursement of tax that can be availed under the VAT system, where tax that has

already been paid is reimbursed. This ensures that taxation happens only for the value addi-

tion. The central sales tax is expected to be eliminated by 2010, after which companies are

likely to witness a drastic reorganization in the way supply chains are managed.

The service expected to benefit the most from VAT's implementation is warehousing. Once

the hub and spoke type distribution model sets in, large multi-user zonal warehousing facili-

ties could be seen mushrooming. This could see 3PL service providers operate these facilities

and leverage economies of scale. This was not observed under the earlier sales tax system,

under which the environment was not conducive for seamless logistics

The transition to VAT could pose challenges in the form of integration of IT infrastructure

and maintenance of records. There is also competition from the unorganized sector

comprising clearing and forwarding (C&F) agents, that may reinvent themselves post VAT

implementation.

Strategic Conclusions

The 3PL market in India is poised for significant growth till the year 2012. The market has

been growing steadily at an estimated Compound Annual Growth Rate of 18.3 percent since

2002 and the growth is expected to accelerate further. Changing economic and business

scenarios, along with increasing outsourcing tendencies are expected to be the drivers for the

growth in this market.

Among the services, the warehousing function is expected to witness the fastest growth.

Investing in assets could be important as owning them, could prove to be a healthy competi-

tive edge, particularly in the transportation function. In the warehousing function,

companies could build their own warehouses or operate a warehouse built by a third party to

specification. Iinvesting in new warehouses may not be advised,, considering high real estate

costs. Choice of location of warehouse is also an important factor, considering the constant

need to reduce lead and turnaround times, which will enable clients gain a competitive edge.

The growth in the transportation is expected to be driven by better infrastructure and the

constantly reducing lead times and this is likely to lead to the emergence of express transpor-

tation. Along with this growth in revenues from value-added services, driven by the

requirement of companies to gain a competitive edge, is also expected.

#4C77-18 © 2006 Frost & Sullivan www.frost.com 1-6

2Strategic Analysis of Total 3PL Market in

India

I n t r o d u c t i o n

Introduction and Overview of the Indian Logistics Market

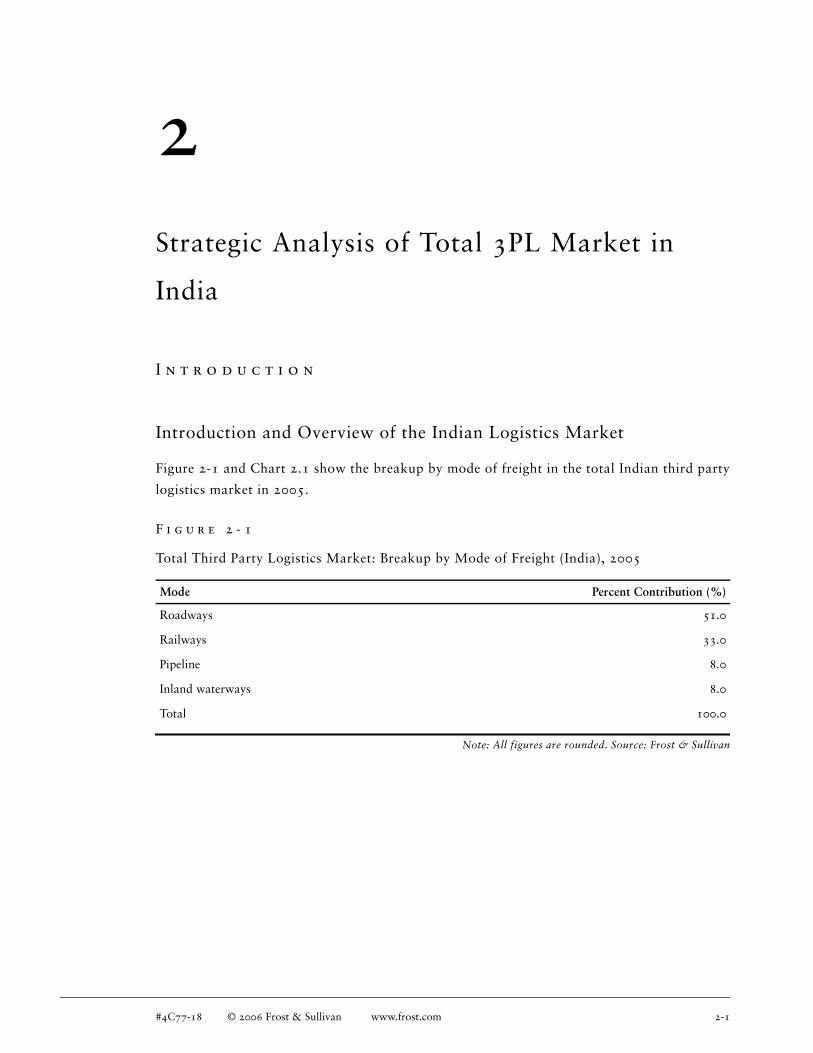

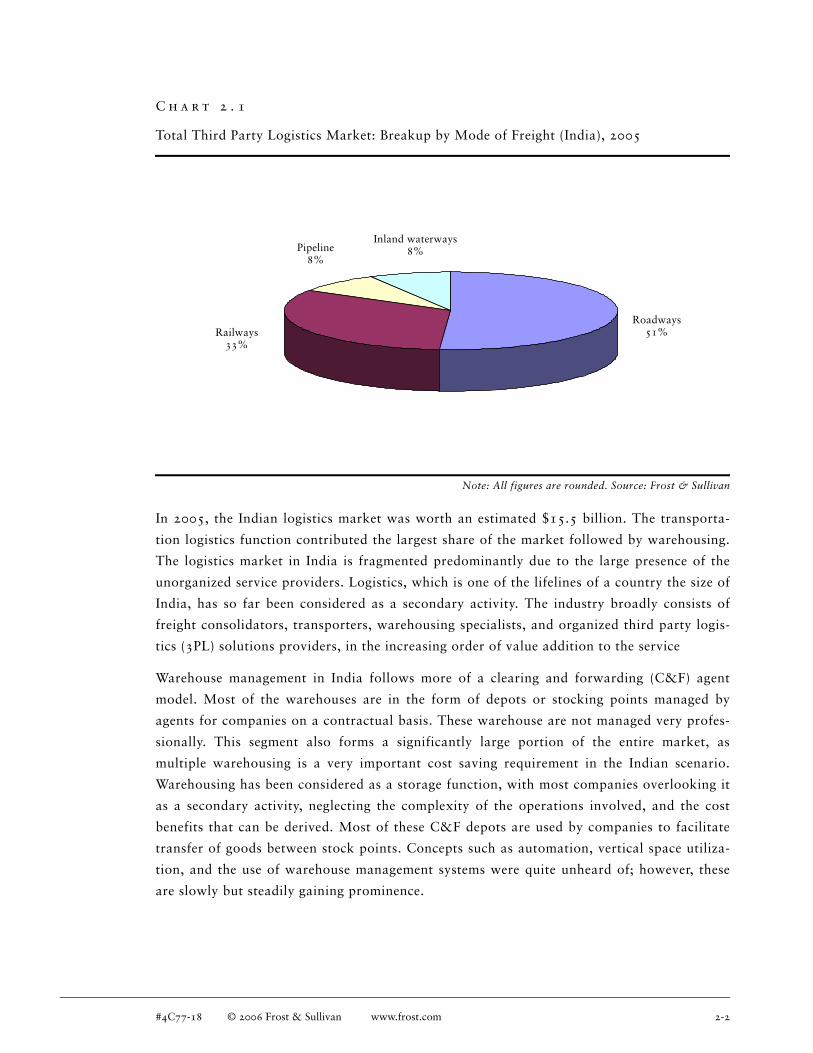

Figure 2-1 and Chart 2.1 show the breakup by mode of freight in the total Indian third party

logistics market in 2005.

Note: All figures are rounded. Source: Frost & Sullivan

F i g u r e 2 - 1

Total Third Party Logistics Market: Breakup by Mode of Freight (India), 2005

Mode Percent Contribution (%)

Roadways 51.0

Railways 33.0

Pipeline 8.0

Inland waterways 8.0

Total 100.0

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-1

C h a r t 2 . 1

Total Third Party Logistics Market: Breakup by Mode of Freight (India), 2005

Note: All figures are rounded. Source: Frost & Sullivan

In 2005, the Indian logistics market was worth an estimated $15.5 billion. The transporta-

tion logistics function contributed the largest share of the market followed by warehousing.

The logistics market in India is fragmented predominantly due to the large presence of the

unorganized service providers. Logistics, which is one of the lifelines of a country the size of

India, has so far been considered as a secondary activity. The industry broadly consists of

freight consolidators, transporters, warehousing specialists, and organized third party logis-

tics (3PL) solutions providers, in the increasing order of value addition to the service

Warehouse management in India follows more of a clearing and forwarding (C&F) agent

model. Most of the warehouses are in the form of depots or stocking points managed by

agents for companies on a contractual basis. These warehouse are not managed very profes-

sionally. This segment also forms a significantly large portion of the entire market, as

multiple warehousing is a very important cost saving requirement in the Indian scenario.

Warehousing has been considered as a storage function, with most companies overlooking it

as a secondary activity, neglecting the complexity of the operations involved, and the cost

benefits that can be derived. Most of these C&F depots are used by companies to facilitate

transfer of goods between stock points. Concepts such as automation, vertical space utiliza-

tion, and the use of warehouse management systems were quite unheard of; however, these

are slowly but steadily gaining prominence.

Railways33%

Pipeline8%

Roadways51%

Inland waterways8%

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-2

Professional management of logistics in the form of 3PL has begun being adopted since the

last decade. These 3PL service providers have the capacity to offer a wide array of services to

their clients and help them better manage their supply chains. The 3PL service providers

assume end-to-end responsibility to manage a part or the company's entire supply chain. The

growth of 3PL service providers in India has introduced the use of global supply chain

management standards in the country. However, the 3PL service providers form a very insig-

nificant part of the entire market, comprising around 3 percent of the Indian logistics.

Roads carry the bulk of the freight in India. The roads in India have a history of being unsafe

and in very bad conditions. This is changing with the construction of the Golden Quadrilat-

eral and North-South-East-West (NSEW) highway networks, traversing the entire country.

The highway infrastructure is highly strained, comprising around 1.4 percent of the total

road network in India and carries in excess of 50 percent of the country's total freight. Roads

are flexible with easy to own assets and door-delivered consignments. Even though rail

freight is more cost effective in terms of cost per unit distance and per unit weight, the effi-

ciency of the rail freight system in India has for long been low and it has also been considered

as a secondary freight mode. Previously, rail was the most preferred mode of freight;

however, bad pricing and inflexibility have resulted in the railways experiencing a downturn.

With the Indian Government announcing plans to open up the containerized rail freight

sector to private operators this is expected to change. Companies such as APL Logistics,

Maersk Logistics, Gateway Distriparks, Central Warehousing Corporation, JM Baxi group,

Adani Logistics, and Reliance Logistics are expected to enter into this segment. The barriers

of entry for providing this service are rather low. Companies need to have a minimum turn-

over of around $22 million (INR 1 billion) in India. To get a permit license for 20 years they

need to pay the Government between $1 million and $10 million, depending on whether they

want to operate on a specific route or an all India basis. Rail freight comprises around

670 million tones, which is around 33 percent of the total domestic traffic in India. Compa-

nies in the metals, heavy machinery, and engineering and cement sectors are expected to

benefit from the opening up of the railways to private participants as these carry bulky cargo

over long distances. Previously, costs of trucking were very high as the final destination could

be in a remote corner of the country, where a backhaul arrangement would be nearly impos-

sible. In sectors such as these, costs of transportation in the entire logistics spending was as

high as 75 percent. Long distance transportation by rail can help cut costs in these sectors.

With the Railways Department mulling a separate freight corridor, this sector is likely to

experience a growing trend. This is keeping in mind that passenger trains get higher priority

over goods trains and the new corridor can run parallel to existing lines to places of heavy

activity such as ports.

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-3

The large unorganized segment of the logistics industry in India poses a formidable challenge

to companies in the organized one. The unorganized segment service providers have lesser

overhead costs and are hence in a position to provide extremely competitive rates. This is

expected to have a considerably large impact in the future, posing a challenge especially to

the 3PL service providers. Entry barriers are also low, leading to the possibility of intensified

competition even in the organized sector. Complex tax laws and infrastructure bottlenecks

are also challenging issues to be dealt with.

The growth of the Indian economy, especially the rise in the manufacturing sector is one of

the key growth drivers of the logistics industry in India. Apart from this, sincere initiatives by

the Government to remove bottlenecks in the logistics infrastructure are also drivers for

growth in the sector that is expected to grow at a compound annual growth rate (CAGR) of

6.4 percent from 2005 to 2012.

Introduction to 3PL in India

3PL services in India is a relatively new concept compared to other parts of the world. The

Indian 3PL market is still in its infancy stage, though it is expected to grow at a significantly

fast pace. The major end-user verticals of 3PL services are the automotive and auto compo-

nents, machinery and heavy engineering, IT hardware and electronics, consumer durables,

pharmaceuticals, fast moving consumer goods (FMCG), and organized retailing industries.

The 3PL service providers have introduced a dimension of professionalism that was previ-

ously lacking in the industry. The Indian business houses have a better established setup in

the 3PL market. This is due to existing business relations that were there between the service

providers, an already established logistics network, and a better knowledge of the local busi-

ness environment and processes. Service providers with a prominent presence include

multinationals such as Sembcorp Logistics of Singapore, domestic service providers such as

Safexpress, GATI, Om Logistics, and TVS Logistics. Service providers such as Caterpillar

Logistics have recognized the opportunity for growth and have entered India for setting up

operations in partnership with the local service providers. Companies such as TNT, Kuehne

Nagel, Schenker, Federal Express, and Panalpina have a global presence; however, they do

not have a notable presence, or in some cases, do not operate in the Indian 3PL market, as

their main focus may be on international air express or sea freight.

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-4

Evolution of 3PL Market in India

The growth of multinational operations has been one of the key drivers in the Indian logistics

market, especially in 3PL. The 3PL services concept was originally introduced by multina-

tional 3PL service providers that entered India to manage the supply chains of their key

global clients. With the emergence of India as a global manufacturing hub, there was require-

ment for seamless supply chains with time-bound deliveries in a cost-effective manner. A

number of companies such as Transport Corporation of India, Om Logistics, Total Logistics,

and Patel Logistics that were previously pure transporters realized the opportunity for

growth in 3PL services and have included it as a part of their portfolio.

The evolution of 3PL services has not been rapid; however, the market has been growing at

an expected CAGR of 18.3 percent since 2002. The growth has been spurred on as certain

companies have had to outsource logistics to remain competitive. Warehousing, a logistics

function that was previously unprofessionally managed, has witnessed noticeable growth

since 2003. Concepts such as mechanized warehousing and vertical space utilization, which

were quite unheard of in India, have now started gaining prominence. 3PL service providers

operating such warehouses have been able to significantly reduce the number of employees

per warehouse.. The transportation logistics function is also witnessing a gradual shift from

pure trucking to containerized transport with vehicle tracking solutions such as a global posi-

tioning system (GPS) or GSM mobile telephony network. Though at present GPS is not

greatly used due to prohibitive costs of equipment, GSM mobile telephony network is being

used.

Outsourcing of integrated logistics has not happened to a very great extent in India. Instead,

companies have outsourced individual or partial services to a 3PL service provider. There are

certain companies that have outsourced their entire supply chains to a 3PL service provider;

however, these are few in number. Integrated logistics outsourcing is expected to be imple-

mented in a major manner once the demand for 3PL services grow. This is expected when key

industry verticals grow, and sourcing patterns shift from price driven sourcing to sophisti-

cated sourcing that focuses on long-term vendor relationships, larger vendor bases, and

technology-driven supply chain innovation.

At present, 3PL services have grown as capital, information, and physical movement. These

three key aspects of any supply chain are being focused on as very important. The market for

3PL services in India is still in its infancy stage. It is expected to see a strong CAGR of

21.9 percent till the year 2012. Though the unorganized segment will not be completely elim-

inated, compared to the rest of the total Indian logistics market the share of 3PL is expected

to increase as the segment is growing significantly faster.

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-5

Awareness and Perception of 3PL in India

The concept of 3PL was quite unheard of in India until the mid-1990s. It is still in its infancystage in India compared to the other parts of the world. However, at present there is anincreased awareness about 3PL services than in the past. Users of 3PL services have varyingperceptions about their service providers. Companies in the automotive sector consideroutsourcing logistics to a 3PL service provider as an important cost-saving tool. The samemay not be witnessed in the other industry verticals. FMCG companies still follow the dealer-stockist distribution model to a very large extent. Outsourcing takes place in individual logis-tics functions such as warehousing or freight forwarding but not to a very great extent intransportation. This is primarily because FMCG companies opine that for high volume,low-value goods such as FMCG such as personal care products, transportation to a 3PLservice provider may be an expensive option. Added to this, for a country as geographicallydiverse as India, with a large consumer base, companies opine that a single 3PL serviceprovider will not be able to offer an end-to-end solution. Retail firms consider working witha 3PL service provider a very viable option as the key to low cost modern retailing lies ineffective supply chain management with electronic surveillance to prevent damage andpilferage in transit. Some companies manufacturing IT hardware and electronics consideroutsourcing to a 3PL service provider a very convenient option, as prior to this quite a fewcompanies were facing problems with huge sums of money locked up in inventories andlonger lead times.

Cost and quality of service are the prime factors companies consider while choosing a 3PLservice provider. As a result of this, there tends to be a trade-off quality and cost. MostIndian companies that have started outsourcing consider cost as the primary factory, unlikemultinationals that have derived cost benefits from outsourcing. Outsourcing to a 3PLservice provider does attract a cost, which may be significantly higher than outsourcing to atrucker and C&F agent; however, companies that focus more on quality do not mind theextra spending to have quality delivered, as it can provide better margins by enabling costcutting. This is more the case with the larger companies that want to possess sophisticatedsupply chains to remain abreast with global competition. Companies may hence be willing tohire top quality services that have a commitment to deliver at the highest standards. Whilecost is a concern for outsourcers, companies, especially multinationals consider it as along-term proposition to work with a 3PL service provider, considering the total cost oflogistics in the whole product life cycle. The reputation of the 3PL serviced provider does actsignificantly on the outsourcer's choice of service provider. A known 3PL service provider ismore preferred giving importance to the requirements of the company.

Another issue of concern is the security of the supply chain of a company, considering thehigh incidences of pilferage and damage in transit in the Indian industries. An efficient supplymay in many cases be the difference between some companies being more successful than theothers. Some companies may be wary of third party intervention in their supply chain andhence be unwilling to outsource their logistics to a 3PL service provider. This though, is aconcern that is greatly unfounded. Meeting service commitments is a concern for a fewcompanies. Flexibility in services and compatibility and scalability of operations are factorsthat companies focus on when it comes to service-level determination.

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-6

S c e n a r i o o f t h e I n d i a n 3 P L M a r k e t

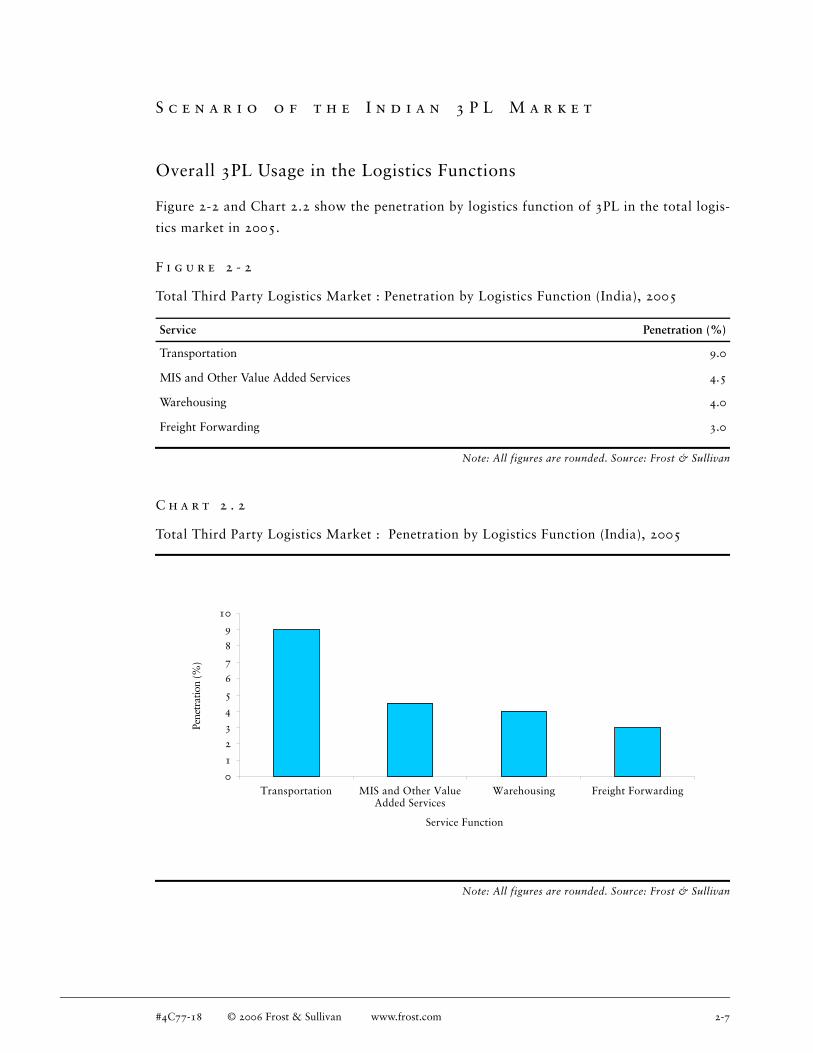

Overall 3PL Usage in the Logistics Functions

Figure 2-2 and Chart 2.2 show the penetration by logistics function of 3PL in the total logis-

tics market in 2005.

Note: All figures are rounded. Source: Frost & Sullivan

C h a r t 2 . 2

Total Third Party Logistics Market : Penetration by Logistics Function (India), 2005

Note: All figures are rounded. Source: Frost & Sullivan

F i g u r e 2 - 2

Total Third Party Logistics Market : Penetration by Logistics Function (India), 2005

Service Penetration (%)

Transportation 9.0

MIS and Other Value Added Services 4.5

Warehousing 4.0

Freight Forwarding 3.0

0

1

2

3

4

5

6

7

8

9

10

Transportation MIS and Other ValueAdded Services

Warehousing Freight Forwarding

Pene

trat

ion

(%)

Service Function

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-7

The penetration of Transportation service outsourced to a 3PL service provider is only

9.0 percent of that in the entire logistics market. This is significantly higher than the penetra-

tions in other services. The fact that transportation function outsourced to a 3PL has such a

low penetration and is still the most penetrated services shows how nascent the 3PL market

in India is. The penetration of Warehousing outsourced to a 3PL is only around 4.0 percent

of the Indian warehousing market. This is because, warehousing is still predominantly

considered a pure storage function. Organized 3PL warehousing is a concept that is new to

the Indian market, and hence the low penetration.

In India, most companies outsource only a part of their supply chain requirements to a 3PL

service provider. There may be only a small fraction of companies that outsource entirely to a

3PL service provider. Most of these companies are multinationals that have entered India and

do not have an established network and have to outsource their logistics due to the lack of

assets.

The penetration of 3PL in the total Indian market is only 5.7 percent. The degree and nature

of outsourcing of logistics to a 3PL service provider varies significantly between verticals and

depends greatly on the nature of the company. In the automotive sector, the trend of

end-to-end outsourcing is beginning to gain acceptance significantly as companies have

begun realizing the benefits of concentrating on core competencies and delegating logistics to

3PL service providers. Concepts such just-in-time (JIT) delivery to the assembly line have

gained acceptance in this sector, thereby requiring companies to hold only a few hours of

inventory. Even companies that have traditionally been known to adopt a very conservative

business outlook have started outsourcing their logistics to 3PL service providers. The pene-

tration of 3PL services is very high in the automotive sector. Likewise, the IT hardware and

electronics sector has also begun outsourcing to a 3PL service provider to a great extent. In

sectors such as FMCG and pharmaceutical industries, the penetration of the 3PL service

concept has been fairly low, owing to already strained profit margins that these companies

are experiencing. Added to this, there is a great deal of decentralization in the supply chains

of these sectors, with many stocking points and strategic distribution centers spread in

different parts of the country. This will demand infrastructure capabilities that 3PL service

providers may not be in a position to provide. Outsourcing in these sectors has started in

warehousing operations. Sector giants such as Hindustan Lever Limited, Marico Industries,

Terumo Tenpol, and Dr.Reddy's Laboratories are outsourcing their warehouse requirements

to 3PL service providers.

Certain 3PL service providers have their own freight forwarding and customs clearance capa-

bilities. Those that do not have hire the services of a local freight forwarding agent to liaison

with the required authorities in order to have their consignments cleared. Most 3PL service

providers provide good MIS capabilities to their clients. The provision of value-added propo-

sitions along with a 3PL contract is expected to witness a growing trend with clients

increasingly demanding the same.

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-8

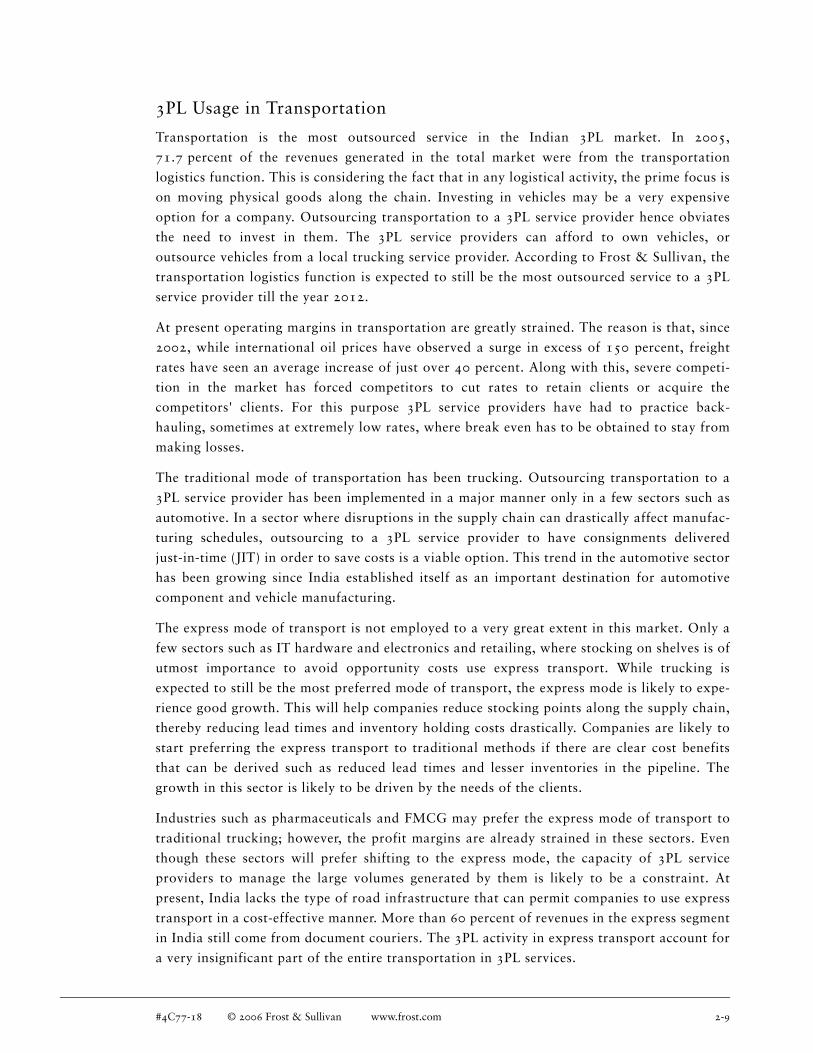

3PL Usage in Transportation

Transportation is the most outsourced service in the Indian 3PL market. In 2005,

71.7 percent of the revenues generated in the total market were from the transportation

logistics function. This is considering the fact that in any logistical activity, the prime focus is

on moving physical goods along the chain. Investing in vehicles may be a very expensive

option for a company. Outsourcing transportation to a 3PL service provider hence obviates

the need to invest in them. The 3PL service providers can afford to own vehicles, or

outsource vehicles from a local trucking service provider. According to Frost & Sullivan, the

transportation logistics function is expected to still be the most outsourced service to a 3PL

service provider till the year 2012.

At present operating margins in transportation are greatly strained. The reason is that, since

2002, while international oil prices have observed a surge in excess of 150 percent, freight

rates have seen an average increase of just over 40 percent. Along with this, severe competi-

tion in the market has forced competitors to cut rates to retain clients or acquire the

competitors' clients. For this purpose 3PL service providers have had to practice back-

hauling, sometimes at extremely low rates, where break even has to be obtained to stay from

making losses.

The traditional mode of transportation has been trucking. Outsourcing transportation to a

3PL service provider has been implemented in a major manner only in a few sectors such as

automotive. In a sector where disruptions in the supply chain can drastically affect manufac-

turing schedules, outsourcing to a 3PL service provider to have consignments delivered

just-in-time (JIT) in order to save costs is a viable option. This trend in the automotive sector

has been growing since India established itself as an important destination for automotive

component and vehicle manufacturing.

The express mode of transport is not employed to a very great extent in this market. Only a

few sectors such as IT hardware and electronics and retailing, where stocking on shelves is of

utmost importance to avoid opportunity costs use express transport. While trucking is

expected to still be the most preferred mode of transport, the express mode is likely to expe-

rience good growth. This will help companies reduce stocking points along the supply chain,

thereby reducing lead times and inventory holding costs drastically. Companies are likely to

start preferring the express transport to traditional methods if there are clear cost benefits

that can be derived such as reduced lead times and lesser inventories in the pipeline. The

growth in this sector is likely to be driven by the needs of the clients.

Industries such as pharmaceuticals and FMCG may prefer the express mode of transport to

traditional trucking; however, the profit margins are already strained in these sectors. Even

though these sectors will prefer shifting to the express mode, the capacity of 3PL service

providers to manage the large volumes generated by them is likely to be a constraint. At

present, India lacks the type of road infrastructure that can permit companies to use express

transport in a cost-effective manner. More than 60 percent of revenues in the express segment

in India still come from document couriers. The 3PL activity in express transport account for

a very insignificant part of the entire transportation in 3PL services.

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-9

Most supply chain managers in the Indian companies have to negotiate freight rates and

track a multitude of trucks from different fleets. With the emergence of lead logistics players

(LLPs), this responsibility is now gradually shifting, reducing the number of agencies to

manage and thereby saving cost and time.

The use of Global Positioning System (GPS) to track vehicles in transit is being employed by

selected companies such as Safexpress in a limited number of vehicles, as technology of this

nature is expensive. Most 3PL service providers do provide their clients with track and trace

facilities, but these are through mobile communication networks such as GSM and CDMA

networks. This requires a demonstration effect of the clear economic benefits for companies

to start using these services more. Reliance logistics has an in-house telematics division that

develops software for enabling vehicle tracking through their own CDMA network. Compa-

nies are taking initiatives in this regard; however it is in its early stages of adoption.

3PL Usage in Warehousing

Warehousing is the second most outsourced logistics function to a 3PL service provider in the

Indian market. In 2005, It accounted for 16.5 percent of the revenues generated in the Indian

3PL market. It is also expected to be the logistics function where competition. will be the

stiffest. In the past warehousing was considered as just another storage function. This is

changing with companies beginning to focus on outsourcing warehouses to a 3PL service

provider as an effective measure to handle large volumes. Companies increasingly beginning

to outsource warehouses, at an expected CAGR of 23.7 percent from 2005 to 2012. One of

the reasons companies are willing to outsource to a 3PL service provider is the need for

real-time information regarding inventories that are locked up along the supply chain and to

provide flexibility in scaling of operations.

Warehousing is not as established in India as it is in the developed economies of the west, as

each state in India has a different tax regulation. This is expected to change once a nation-

wide value added tax (VAT) system is implemented, eventually resulting in the growth of 3PL

managed warehouses. The 3PL service providers are likely to shift to a new hub and spoke

type warehouse model with regional master warehouses feeding the smaller warehouses and

depots. This will be in stark contrast to the present system of state wise C&F depots necessi-

tated as a cost saving measure due to the present sales tax system in the country, which is

expected to be replaced by a uniform VAT. Once VAT is uniformly implemented, consolida-

tion in warehousing is expected to occur, which can help 3PL service providers leverage

economies of scale. Once this takes place and consequentially warehousing costs decrease,

technological improvements such as robots and conveyor belts can be possible, resulting in

better warehousing. However, this trend is not likely to be witnessed across all sectors.

Some verticals such as FMCG operate with a mixed model, persisting with the traditionalC&F agent model, as companies they want to retain a strategic distribution hub within astate, in order to avoid opportunity costs. Ultimately, even for the C&F agents to staycompetitive, they have to upgrade existing facilities similar to 3PL warehouses.

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-10

The outsourcing of a company's warehousing logistics function to a 3PL service provider isbecoming a growing trend. This trend is expected to be a direct fallout of companies realizingthe complexity involved in a warehousing logistics function. The automotive sector has beenwitnessing outsourcing in warehousing logistics function to a great extent, where inventoriesneed to be replenished on an hourly basis than on a daily basis. Companies such as TataMotors have outsourced their warehousing logistics function to professional 3PL serviceproviders. Maintaining a large number of stock keeping units inside the warehouse, spreadover large areas is likely to lead to complexity in operations. In many cases, lead times insidethe warehouse can be very critical to a manufacturing or distribution operation, requiringquick retrieval. Moreover, investing in real estate may not be feasible for a company, andhence the best option for them to use a 3PL service. For example, Om logistics, a leading 3PLservice provider in India, is providing warehousing logistics function to a leading manufac-turer of refrigerators since 2003 at their warehouse in Mohali, in Punjab. Previously, thecompany had its warehouse in near Mumbai, with material not being able to be trackedeasily, effectively wasting around 30,000 sq. ft. of floor space.

The 3PL service providers in India have started investing on increasing warehouse capacitiesand the number of warehouses in the country. This is due to the intention to cash in on theopportunity provided by the implementation of a uniform national VAT system, where it isexpected that the present multistage warehouse model will shift to a model with fewer andlarger warehouses spread across the country. The 3PL service providers are also trying toexpand their warehouses vertically in order to increase the capacity, and hence shift to a'cubic feet' type one, as opposed to the 'square feet' type that is predominantly present inIndia. Sembcorp Logistics has four warehouses at Bhiwandi, Chennai, Pune, and Jamshedpurcatering to the needs of its clients. GATI has also announced plans to upgrade its warehousesat certain facilities. Companies such as MICO have also clearly drawn out plans for changingits supply chain structure after VAT is fully implemented.

A purely variable cost model was not considered a viable option in India when organizedwarehousing first entered the market around 2001, as manufacturing patterns were notsuited to that. In a pure variable cost model, Company 'A' managing inventory turns betterthan another Company 'B', which keeps a large inventory and tries to respond to marketdemand, should logically speaking be paying lesser for using lesser warehouse space. That iscompanies should be paying proportional to space utilization. Lack of uncertainty indemand, lack of proper forecasting, and rigid manufacturing patterns were primarily respon-sible for this costing model not doing very well. Even today, C&F agents follow acombination of a fixed and variable cost model, where companies pay for rent andmanpower at the warehousing facility even if no space is utilized. This is because many facil-ities are not shared and hence economies of scale are not being created. The 3PL serviceproviders are likely to practice a purely variable cost model once VAT is implementeduniformly.

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-11

The use of information technology has been implemented to a good extent in warehousing.

They come in the form of special application warehouse management system This is used to

get real time data about stock availability in the warehouse. Along with this 3PL service

providers are focusing on the automated storage and retrieval systems (AS/RS) to facilitate

easier handling in the warehouse premises. This helps in storage and retrieval of bins, identi-

fying them, and sorting accordingly. Along with it, usage of robots and stacker cranes that

move on rails is also expected. These are particularly useful in case of warehouses with

vertical space utilization and those that handle large volumes and many stock keeping units

such as in the FMCG, pharmaceutical, and apparel verticals.

Improvements are expected in the technology used in a warehouse that can reduce human

interference and thereby increase warehouse efficiency. At present, in India global technology

standards such as radio frequency identification (RFID) have not been implemented to a

great extent. These have a great potential to increase warehousing efficiency and security.

There is also the possibility of hi-tech automated warehouses with zero human interference in

the future, where companies are expected to save a lot in terms of reduced, or at times nil

power consumption in the form of zero air conditioning, illumination, and manpower. At

present, this is observed in extremely few companies in India, as the cost of technology of

this nature is considered to be prohibitive at the present time.

3PL Usage in Freight Forwarding

In 2005, freight forwarding logistics function accounted for 2.2 percent of the revenues

generated in the Indian 3PL market.. The 3PL service providers that offer the freight

forwarding logistics function to their clients either possess the capabilities themselves or

employ the services of an agency that liaisons with the authorities locally. There are multina-

tional freight forwarders such as Panalpina & Kuehne Nagel that offer freight forwarding

services to 3PL service providers; however, theses are far outnumbered by the local freight

forwarding agents. Complex laws and procedures and at Indian Airports and seaports often

require 3PL service providers to outsource their freight forwarding requirements to a local

service provider, who in most cases is better acquainted with local authorities and

procedures.

3PL Usage in MIS and Other Value-added Services

In 2005, MIS and other Value-added Services accounted 9.6 percent of the revenues gener-

ated in the Indian 3PL market. Since 3PL service providers offer—added services, clients can

concentrate on their competencies. The growth of these services has been mainly driven by

the growth of outsourcing to a 3PL service provider. At present, the provision of these serv-

ices has become imperative to companies considering that service differentiation is a must in

a highly competitive atmosphere.

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-12

After sales support, customs clearance, reverses logistics, kitting, packaging, repacking, labe-

ling, rate negotiation, order management, network planning, site selection, fleet

management, vendor management of inventory, and supply chain consulting are among the

many value-added services offered by 3PL service providers in India.

Vendor managed inventory (VMI) service has witnessed a strong growth in the automotive

and auto components, IT hardware, and retail sectors. Companies such as Menlo Worldwide

have set up VMI operations in the country to provide services to companies such as General

Motors. In the IT hardware sector, VMI services have helped companies decrease inventory

levels significantly, thereby helping companies cut costs. VMI provides companies with total

visibility about inventories at all points along the supply chain and help in the company

maintaining just enough merchandise required along the assembly line or by the customer.

However, not all 3PL service providers are in a position to offer all these MIS and other

value-added services, placing the ones that cannot offer them at a clear competitive disadvan-

tage when compared to companies that offer them.

M a r k e t S i z e a n d R e v e n u e F o r e c a s t s

The Total Logistics Market in India

The total logistics market in India is estimated at $15.5 billion. A vast majority of this

market is still in the unorganized segment. Companies such as VRL transporters and Navata

transporters are very good regional participants but do not have a pan-India presence. Other-

wise, the transportation is highly unorganized, with varying fleet ownership patterns. The

small fleet owners do not have operating policies and operate at extremely competitive rates.

They are generally in the form of open trucks, with no assured time schedules and improper

handling of consignments. Warehousing also has for long been in the form of C&F depots

and stocking agents, spread across the country in order to gain maximum benefit out of the

redundant sales tax system. These depots have usually been positioned more out of obtaining

tax benefits than for geographical convenience. There are a very few companies that operate

out of a single warehouse or few warehouses in the country. In the Indian warehousing

scenario, it is more of a storage function being performed and it lacks sophistication in

service.

The cost of logistics in India is very high, estimated at around 13 percent of the country's

gross domestic product (GDP). Transportation forms a predominantly large part of costs

incurred for logistics. The other two most significant cost components of logistics are ware-

housing and inventory holding costs. Together these three compose around 90 percent of the

costs incurred for logistics in the market. The other components involved are administrative

and order processing costs.

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-13

The organized 3PL service providers account for a very insignificant share of the market.

These are very professionally managed, being able to offer end-to-end logistics solutions for

their clients. The concept of a 3PL service is still in its infancy stage in India and is expected

to observe a strong growth till the year 2012.

Size of the 3PL Market in the India

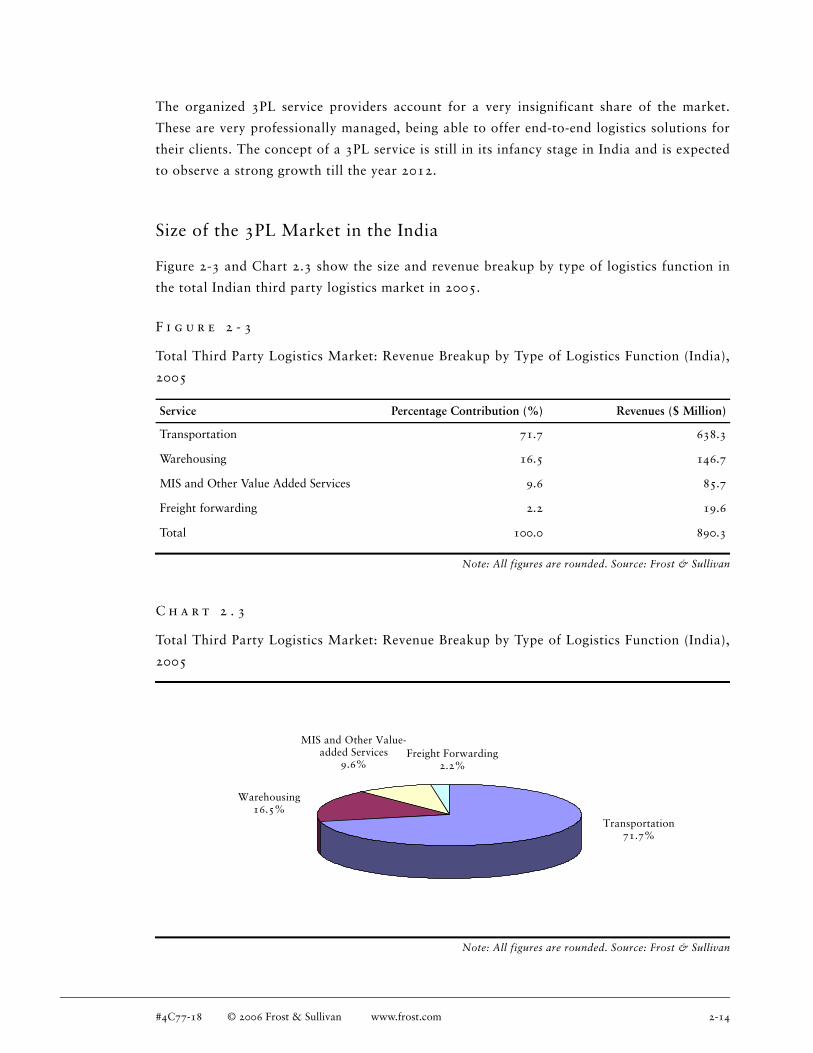

Figure 2-3 and Chart 2.3 show the size and revenue breakup by type of logistics function in

the total Indian third party logistics market in 2005.

Note: All figures are rounded. Source: Frost & Sullivan

C h a r t 2 . 3

Total Third Party Logistics Market: Revenue Breakup by Type of Logistics Function (India),

2005

Note: All figures are rounded. Source: Frost & Sullivan

F i g u r e 2 - 3

Total Third Party Logistics Market: Revenue Breakup by Type of Logistics Function (India),

2005

Service Percentage Contribution (%) Revenues ($ Million)

Transportation 71.7 638.3

Warehousing 16.5 146.7

MIS and Other Value Added Services 9.6 85.7

Freight forwarding 2.2 19.6

Total 100.0 890.3

Transportation71.7%

Warehousing16.5%

MIS and Other Value-added Services

9.6%Freight Forwarding

2.2%

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-14

In 2005, the 3PL market in India was worth $890.3 million. It has grown at CAGR of

18.3 percent since the year 2002. Transportation is the most outsourced service to a 3PL

service provider. It accounted for 71.7 percent of all service revenues in 2005. This is greatly

due to the fact that companies need not invest in vehicles and manage complex transporta-

tion activity. Moreover, India is geographically a very vast country with a large vendor base.

Clients are increasingly focusing on better and more secure transportation, with real-time

data availability. Soon 3PL companies are likely to witness a healthy growth in the transpor-

tation logistics function. The logistics function that contributed the next largest share after

transportation in the Indian 3PL market was warehousing, that accounted for 16.5 percent of

the revenues in 2005. The market for warehousing is not as mature as it is in the developed

economies of western Europe or North America, making the potential for growth immense.

Revenues from freight forwarding accounted for 2.2 percent of all revenues in the total

market. Value-added services and others accounted for the remaining 9.6 percent of the reve-

nues in 2005.

Growth History of 3PL Market in India

The 3PL market has been growing in India from the year 2002 to the year 2005 at a CAGR

of 18.3 percent. The market was worth $538.2 million in 2002 The growth has primarily

come from the usage of 3PL services in key industry sectors such as automotive and auto

components and IT hardware and electronics where the lead times have to be extremely short

to decrease manufacturing and opportunity costs.

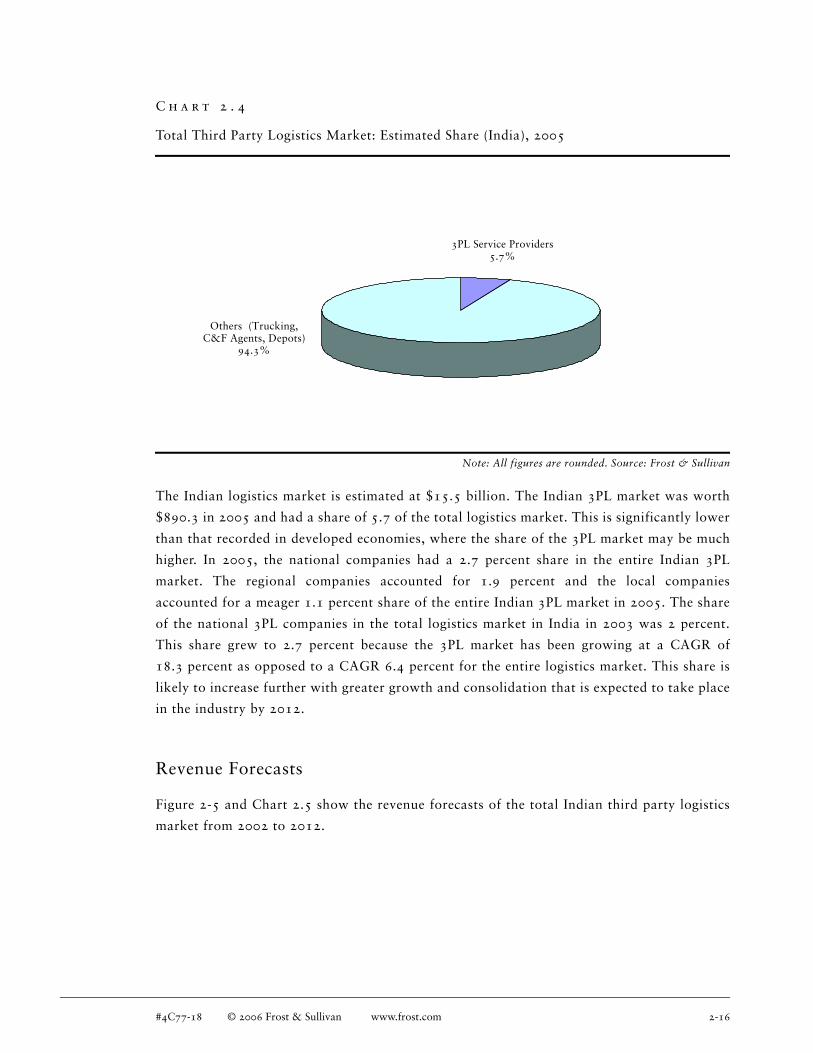

Estimated Share of the 3PL Market

Figure 2-4 and Chart 2.4 shows the estimated share of the Third Party Logistics Market in

the entire logistics market (India), 2005.

Note: All figures are rounded. Source: Frost & Sullivan

F i g u r e 2 - 4

Total Third Party Logistics Market: Estimated Shares (India), 2005

Category Market Share (%)

3PL Service Providers 5.7

Others (Trucking, C&F Agents, Depots) 94.3

Total 100.0

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-15

C h a r t 2 . 4

Total Third Party Logistics Market: Estimated Share (India), 2005

Note: All figures are rounded. Source: Frost & Sullivan

The Indian logistics market is estimated at $15.5 billion. The Indian 3PL market was worth

$890.3 in 2005 and had a share of 5.7 of the total logistics market. This is significantly lower

than that recorded in developed economies, where the share of the 3PL market may be much

higher. In 2005, the national companies had a 2.7 percent share in the entire Indian 3PL

market. The regional companies accounted for 1.9 percent and the local companies

accounted for a meager 1.1 percent share of the entire Indian 3PL market in 2005. The share

of the national 3PL companies in the total logistics market in India in 2003 was 2 percent.

This share grew to 2.7 percent because the 3PL market has been growing at a CAGR of

18.3 percent as opposed to a CAGR 6.4 percent for the entire logistics market. This share is

likely to increase further with greater growth and consolidation that is expected to take place

in the industry by 2012.

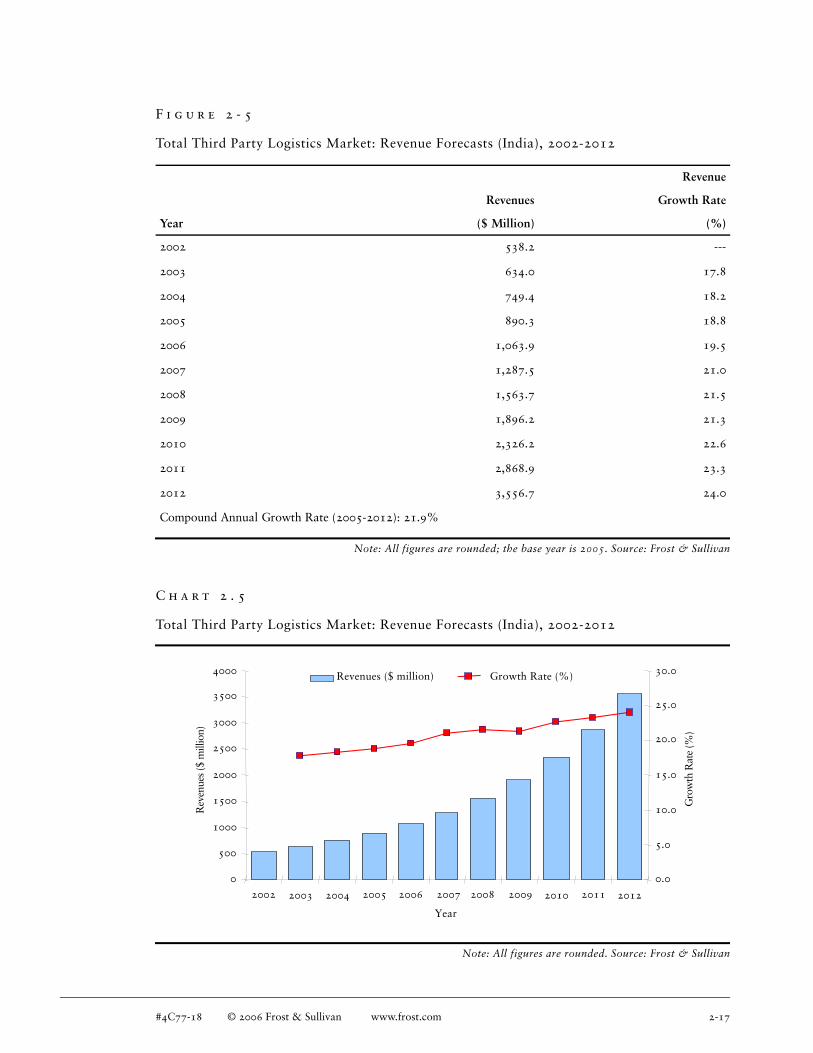

Revenue Forecasts

Figure 2-5 and Chart 2.5 show the revenue forecasts of the total Indian third party logistics

market from 2002 to 2012.

Others (Trucking, C&F Agents, Depots)

94.3%

3PL Service Providers5.7%

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-16

Note: All figures are rounded; the base year is 2005. Source: Frost & Sullivan

C h a r t 2 . 5

Total Third Party Logistics Market: Revenue Forecasts (India), 2002-2012

Note: All figures are rounded. Source: Frost & Sullivan

F i g u r e 2 - 5

Total Third Party Logistics Market: Revenue Forecasts (India), 2002-2012

Revenue

Revenues Growth Rate

Year ($ Million) (%)

2002 538.2 ---

2003 634.0 17.8

2004 749.4 18.2

2005 890.3 18.8

2006 1,063.9 19.5

2007 1,287.5 21.0

2008 1,563.7 21.5

2009 1,896.2 21.3

2010 2,326.2 22.6

2011 2,868.9 23.3

2012 3,556.7 24.0

Compound Annual Growth Rate (2005-2012): 21.9%

0

500

1000

1500

2000

2500

3000

3500

4000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Year

Rev

enue

s ($

mill

ion)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Gro

wth

Rat

e (%

)Revenues ($ million) Growth Rate (%)

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-17

In 2005, the total 3PL market in India was worth $890.3 million. It is expected to grow at a

CAGR of 21.9 percent from 2005 to 2012, and reach $3,556.7 million by 2012. The market

for 3PL is growing significantly faster than the entire Indian logistics market, which is

growing at an annual rate of 6.4 percent.

Revenue Forecasts Breakdown by Different Logistics Functions

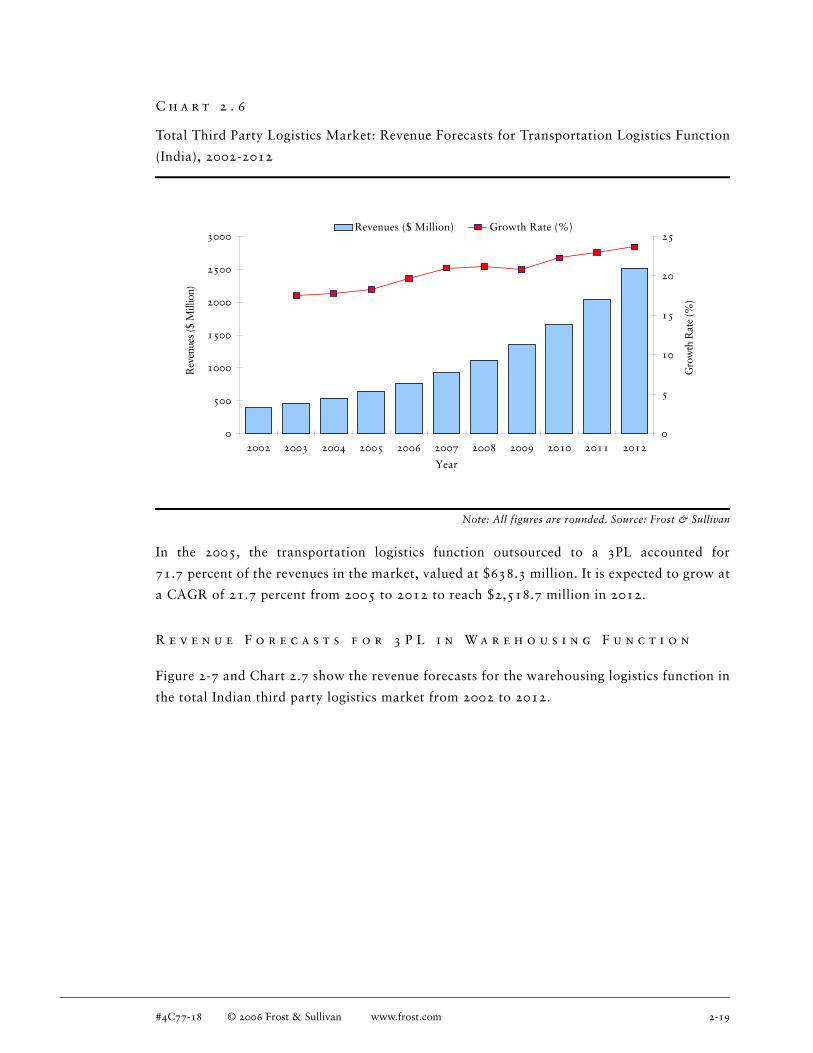

R e v e n u e F o r e c a s t s f o r 3 P L i n T r a n s p o r t a t i o n F u n c t i o n

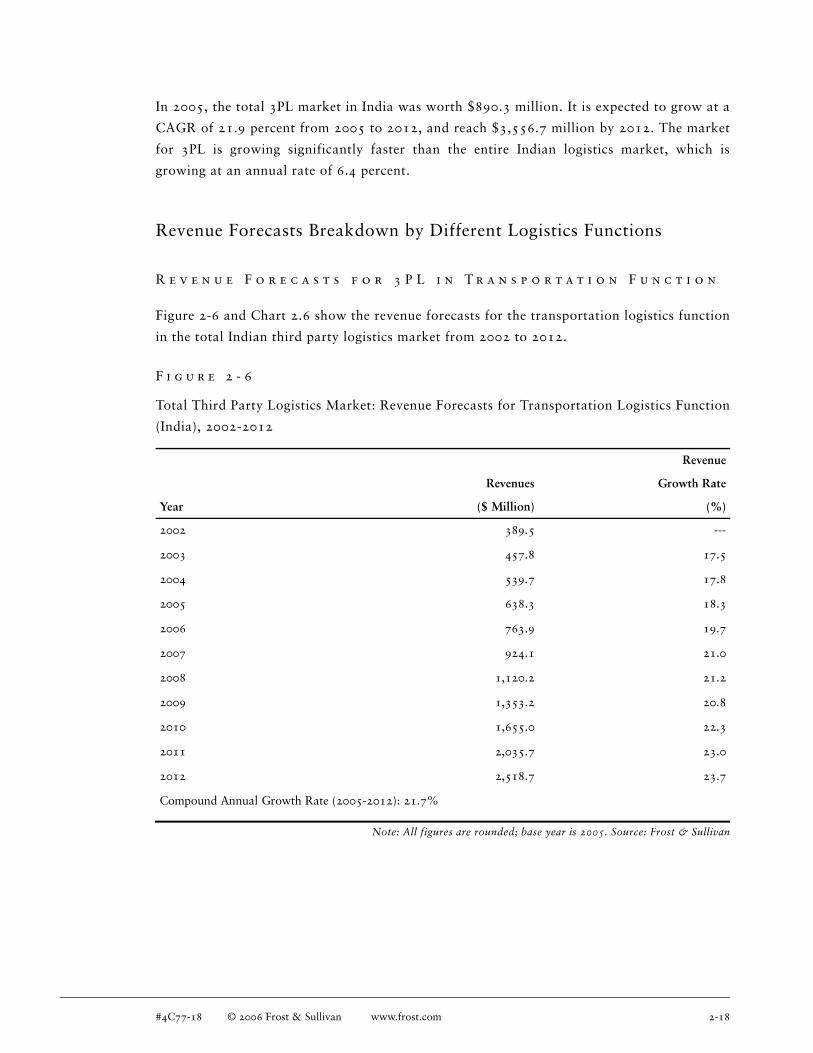

Figure 2-6 and Chart 2.6 show the revenue forecasts for the transportation logistics function

in the total Indian third party logistics market from 2002 to 2012.

Note: All figures are rounded; base year is 2005. Source: Frost & Sullivan

F i g u r e 2 - 6

Total Third Party Logistics Market: Revenue Forecasts for Transportation Logistics Function

(India), 2002-2012

Revenue

Revenues Growth Rate

Year ($ Million) (%)

2002 389.5 ---

2003 457.8 17.5

2004 539.7 17.8

2005 638.3 18.3

2006 763.9 19.7

2007 924.1 21.0

2008 1,120.2 21.2

2009 1,353.2 20.8

2010 1,655.0 22.3

2011 2,035.7 23.0

2012 2,518.7 23.7

Compound Annual Growth Rate (2005-2012): 21.7%

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-18

C h a r t 2 . 6

Total Third Party Logistics Market: Revenue Forecasts for Transportation Logistics Function

(India), 2002-2012

Note: All figures are rounded. Source: Frost & Sullivan

In the 2005, the transportation logistics function outsourced to a 3PL accounted for

71.7 percent of the revenues in the market, valued at $638.3 million. It is expected to grow at

a CAGR of 21.7 percent from 2005 to 2012 to reach $2,518.7 million in 2012.

R e v e n u e F o r e c a s t s f o r 3 P L i n W a r e h o u s i n g F u n c t i o n

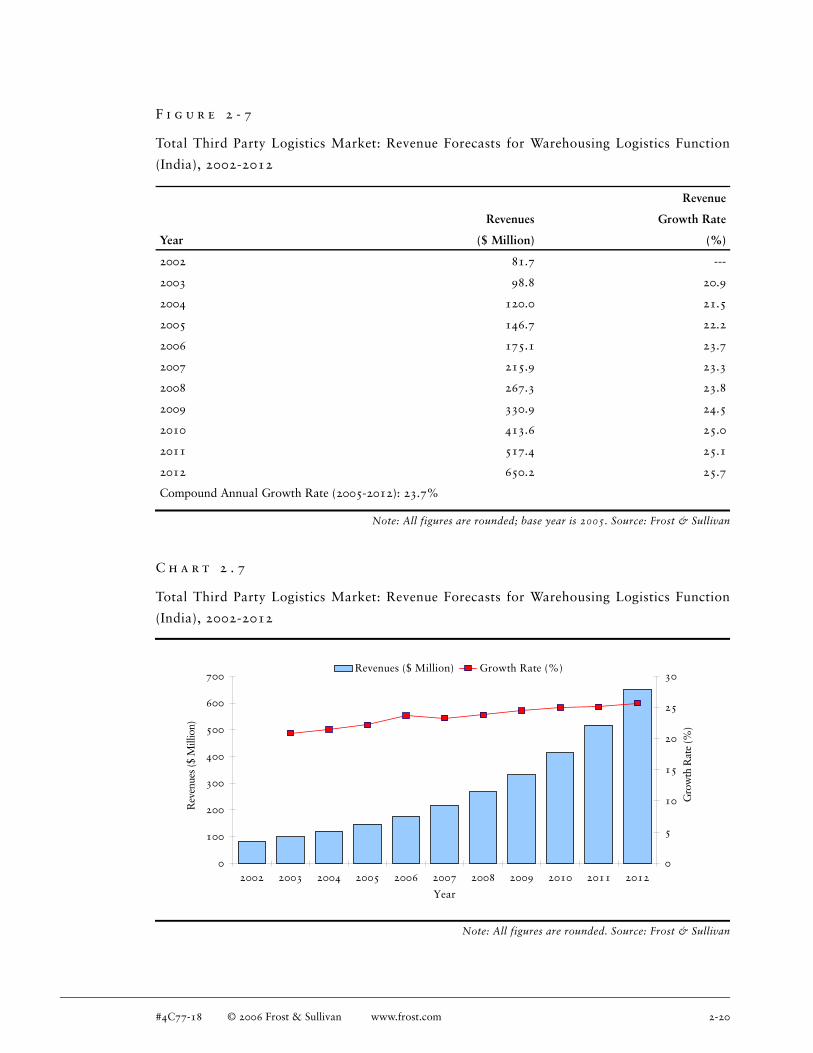

Figure 2-7 and Chart 2.7 show the revenue forecasts for the warehousing logistics function in

the total Indian third party logistics market from 2002 to 2012.

0

500

1000

1500

2000

2500

3000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Year

0

5

10

15

20

25Revenues ($ Million) Growth Rate (%)

Gro

wth

Rat

e (%

)

Rev

enue

s ($

Mill

ion)

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-19

Note: All figures are rounded; base year is 2005. Source: Frost & Sullivan

C h a r t 2 . 7

Total Third Party Logistics Market: Revenue Forecasts for Warehousing Logistics Function

(India), 2002-2012

Note: All figures are rounded. Source: Frost & Sullivan

F i g u r e 2 - 7

Total Third Party Logistics Market: Revenue Forecasts for Warehousing Logistics Function

(India), 2002-2012

Revenue

Revenues Growth Rate

Year ($ Million) (%)

2002 81.7 ---

2003 98.8 20.9

2004 120.0 21.5

2005 146.7 22.2

2006 175.1 23.7

2007 215.9 23.3

2008 267.3 23.8

2009 330.9 24.5

2010 413.6 25.0

2011 517.4 25.1

2012 650.2 25.7

Compound Annual Growth Rate (2005-2012): 23.7%

0

100

200

300

400

500

600

700

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Year

0

5

10

15

20

25

30Revenues ($ Million) Growth Rate (%)

Gro

wth

Rat

e (%

)

Rev

enue

s ($

Mill

ion)

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-20

Warehousing is expected to grow the fastest among all functions outsourced to a 3PL service

provider. In 2005, it accounted for 16.5 percent of the revenues of the entire market, that was

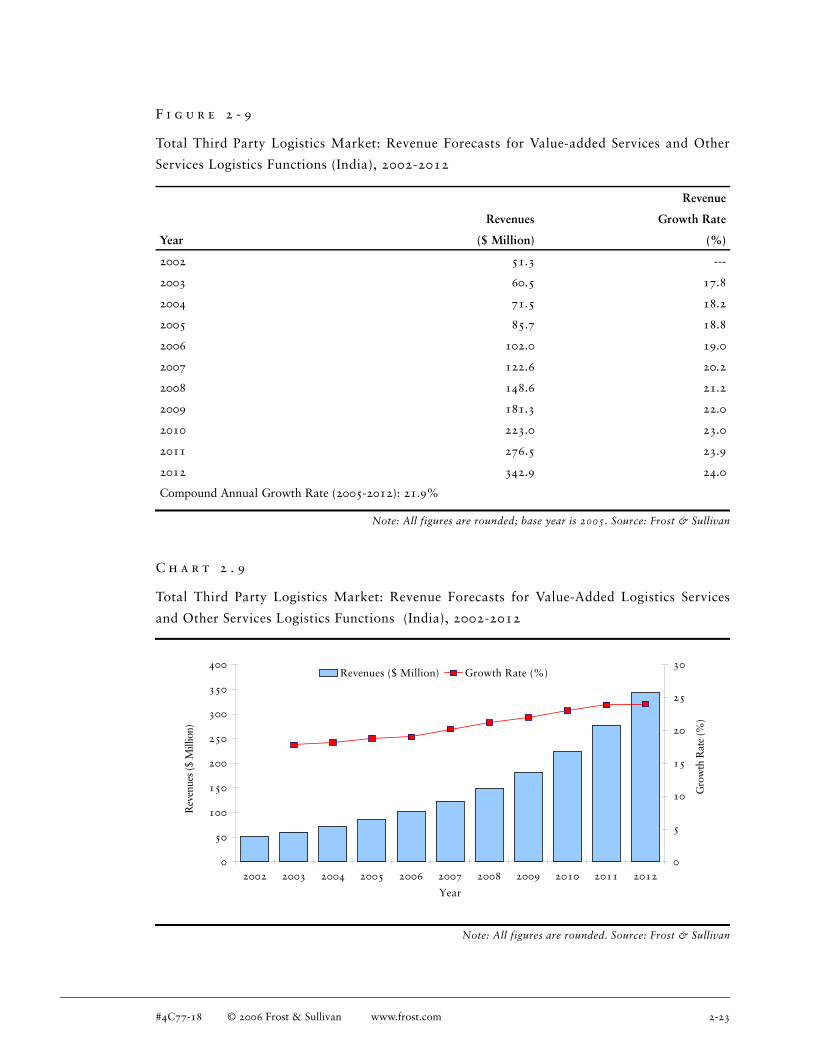

$146.7 million. The warehousing operations to a 3PL company are expected to grow at a

CAGR of 23.7 percent from 2005 to 2012, to reach $650.2 million in 2012.

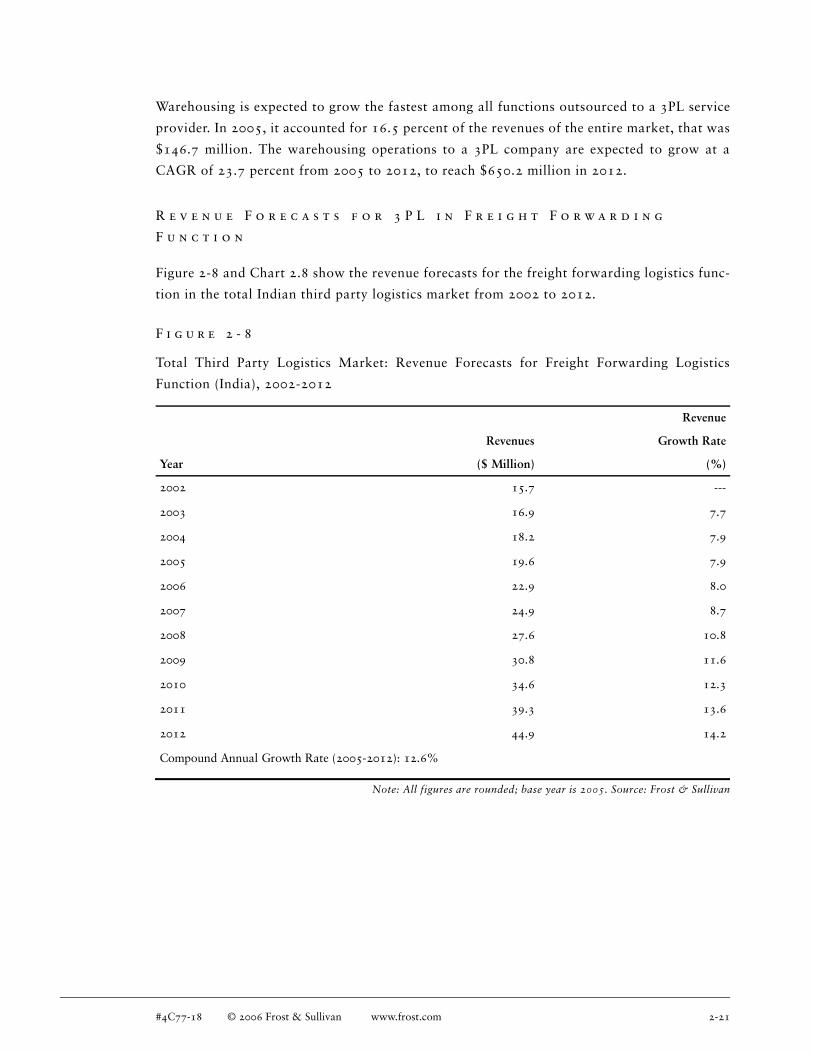

R e v e n u e F o r e c a s t s f o r 3 P L i n F r e i g h t F o r w a r d i n g

F u n c t i o n

Figure 2-8 and Chart 2.8 show the revenue forecasts for the freight forwarding logistics func-

tion in the total Indian third party logistics market from 2002 to 2012.

Note: All figures are rounded; base year is 2005. Source: Frost & Sullivan

F i g u r e 2 - 8

Total Third Party Logistics Market: Revenue Forecasts for Freight Forwarding Logistics

Function (India), 2002-2012

Revenue

Revenues Growth Rate

Year ($ Million) (%)

2002 15.7 ---

2003 16.9 7.7

2004 18.2 7.9

2005 19.6 7.9

2006 22.9 8.0

2007 24.9 8.7

2008 27.6 10.8

2009 30.8 11.6

2010 34.6 12.3

2011 39.3 13.6

2012 44.9 14.2

Compound Annual Growth Rate (2005-2012): 12.6%

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-21

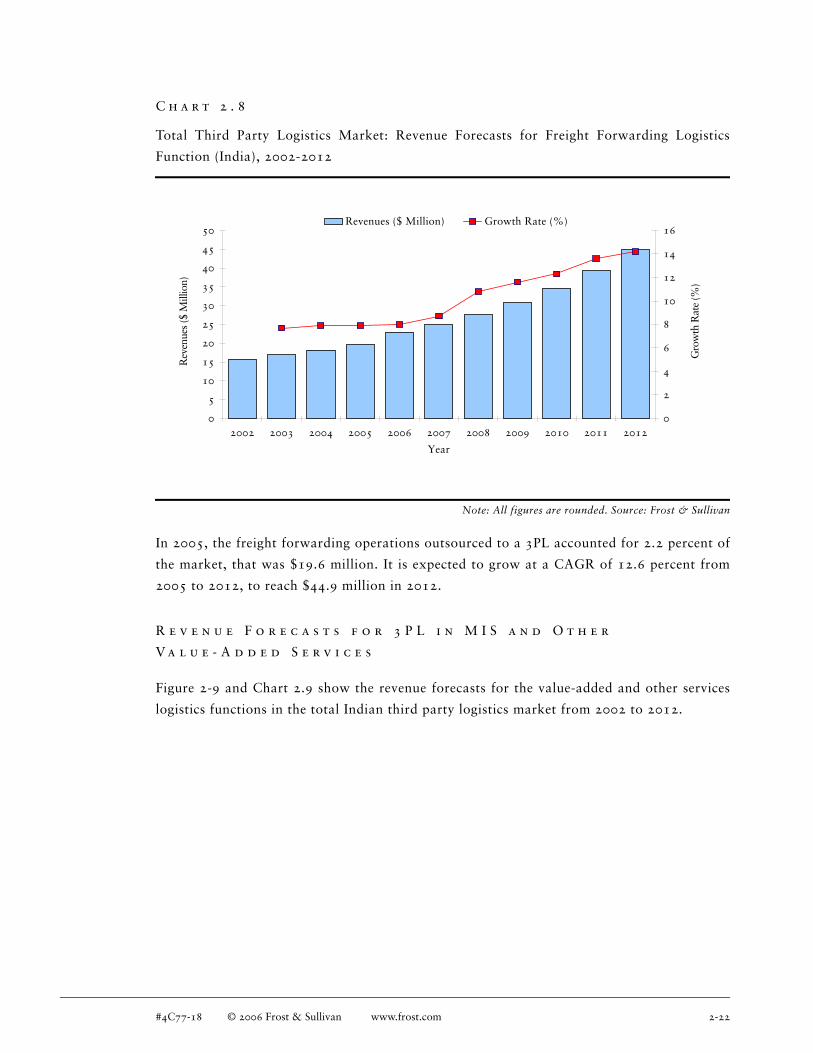

C h a r t 2 . 8

Total Third Party Logistics Market: Revenue Forecasts for Freight Forwarding Logistics

Function (India), 2002-2012

Note: All figures are rounded. Source: Frost & Sullivan

In 2005, the freight forwarding operations outsourced to a 3PL accounted for 2.2 percent of

the market, that was $19.6 million. It is expected to grow at a CAGR of 12.6 percent from

2005 to 2012, to reach $44.9 million in 2012.

R e v e n u e F o r e c a s t s f o r 3 P L i n M I S a n d O t h e r

V a l u e - A d d e d S e r v i c e s

Figure 2-9 and Chart 2.9 show the revenue forecasts for the value-added and other services

logistics functions in the total Indian third party logistics market from 2002 to 2012.

0

5

10

15

20

25

30

35

40

45

50

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Year

0

2

4

6

8

10

12

14

16Revenues ($ Million) Growth Rate (%)

Gro

wth

Rat

e (%

)

Rev

enue

s ($

Mill

ion)

#4C77-18 © 2006 Frost & Sullivan www.frost.com 2-22

Note: All figures are rounded; base year is 2005. Source: Frost & Sullivan

C h a r t 2 . 9

Total Third Party Logistics Market: Revenue Forecasts for Value-Added Logistics Services

and Other Services Logistics Functions (India), 2002-2012

Note: All figures are rounded. Source: Frost & Sullivan

F i g u r e 2 - 9