Advanced Cost Management Professor William F. O’Brien, MBA, CPA Spring 2005.

21

Advanced Cost Management Professor William F. O’Brien, MBA, CPA Spring 2005

-

date post

22-Dec-2015 -

Category

Documents

-

view

214 -

download

0

Transcript of Advanced Cost Management Professor William F. O’Brien, MBA, CPA Spring 2005.

Advanced Cost Management

Professor William F. O’Brien, MBA, CPA

Spring 2005

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-2

Introduction

Cost Management Financial Non-Financial

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-3

Financial Management Evolution

DATADATA

INFORMATIONINFORMATION

ANALYSISANALYSIS

IMPLEMENTATIONIMPLEMENTATION

Today’sCorporateFocus is on

Results!

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-4

CompanyF/S

Users

EconomicDecisions

Financial Impact

(useful &relevant)

Financial Accounting Model

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-5

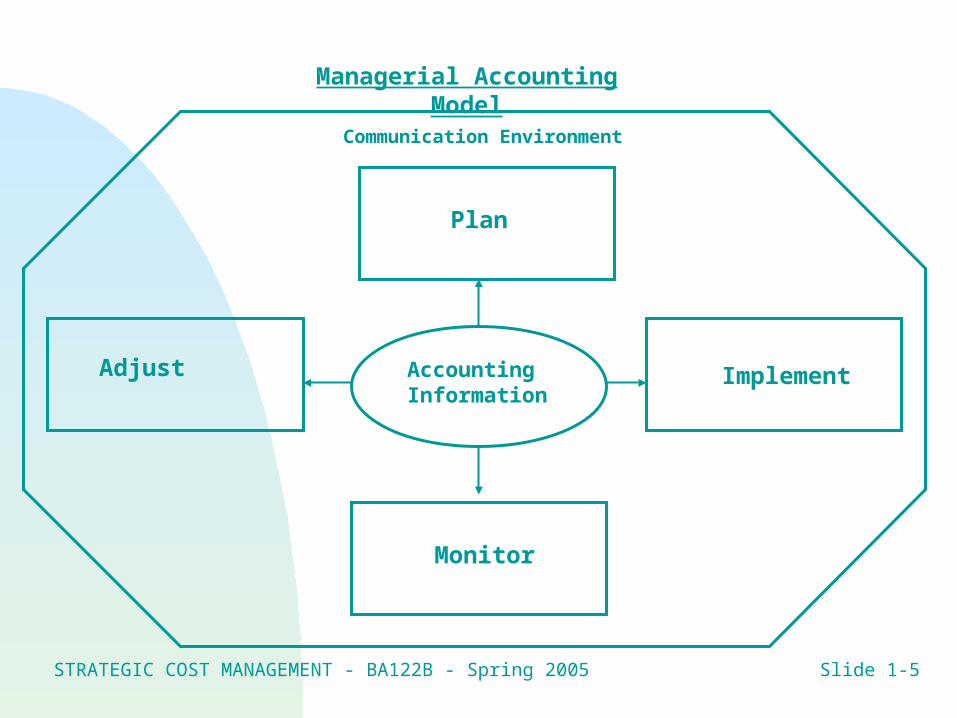

Managerial Accounting Model

Plan

Implement

Monitor

Adjust AccountingInformation

Communication Environment

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-6

Managerial vs. Financial Accounting

Managerial

Internally oriented Prospective Operational and financial focus Timely Not required Non-GAAP Relevant Sub-unit orientation

Financial

Externally oriented Historical Financial focus only Accurate Required GAAP Objective Entire entity orientation

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-7

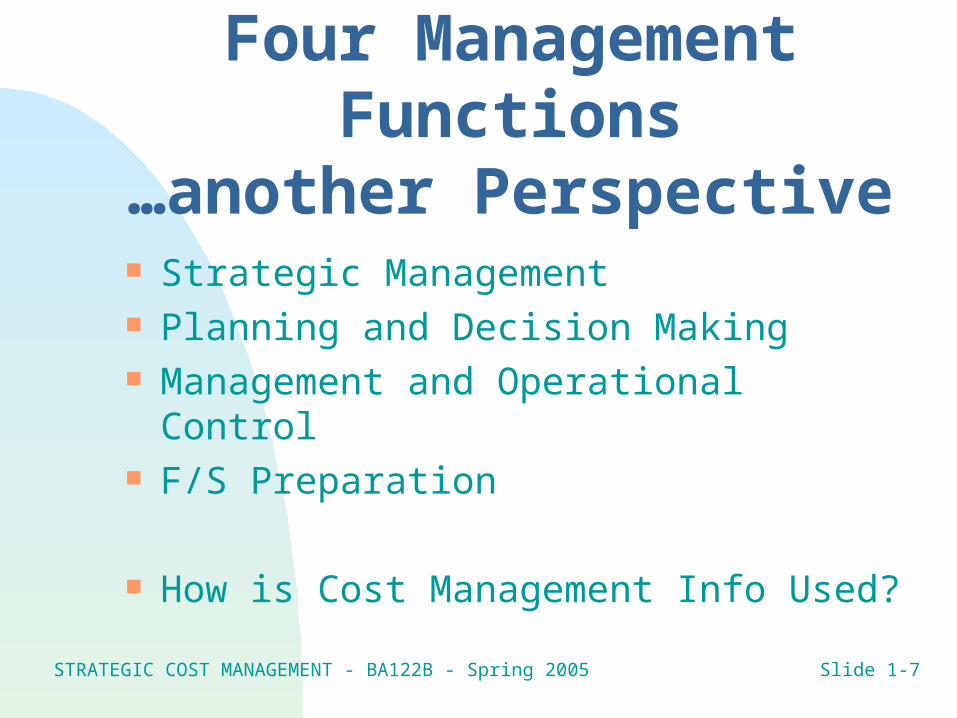

Four Management Functions

…another Perspective Strategic Management Planning and Decision Making Management and Operational Control F/S Preparation

How is Cost Management Info Used?

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-8

Strategic Cost Management

Strategic cost management is the development of cost management information to facilitate the principal management function--strategic management.

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-9

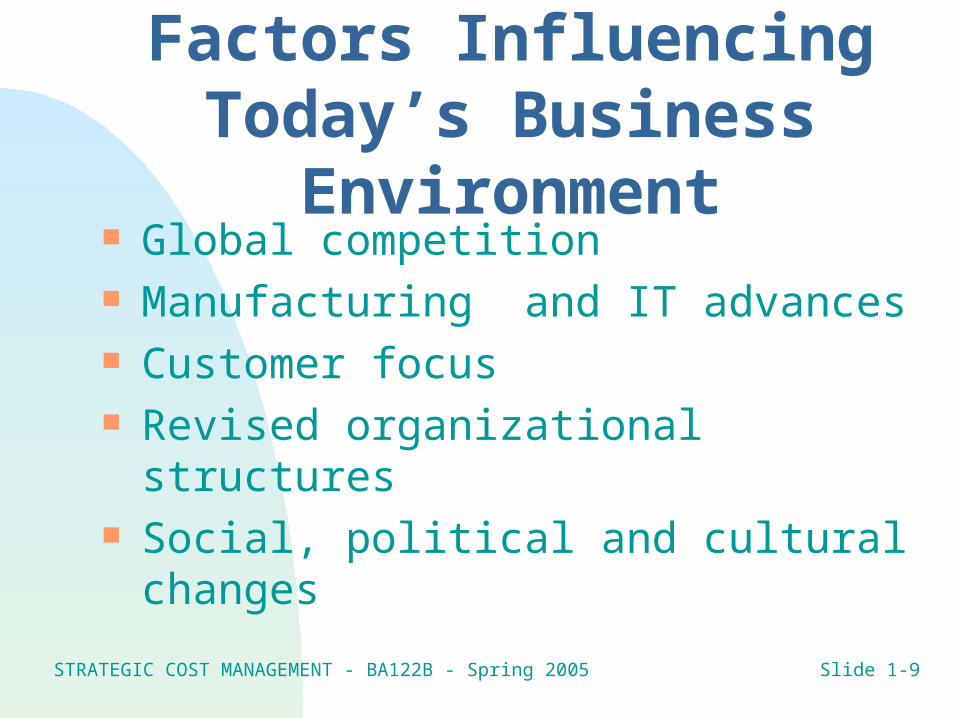

Factors Influencing Today’s Business

Environment Global competition Manufacturing and IT advances Customer focus Revised organizational structures Social, political and cultural changes

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-10

Contemporary Mgt. Techniques

Benchmarking Total Quality Management (TQM) Continuous Improvement Activity-Based Costing (ABC) and Mgt. (ABM) Reengineering Theory of Constraints (TOC) Mass Customization Target Costing Life-cycle Costing The Balanced Scorecard

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-11

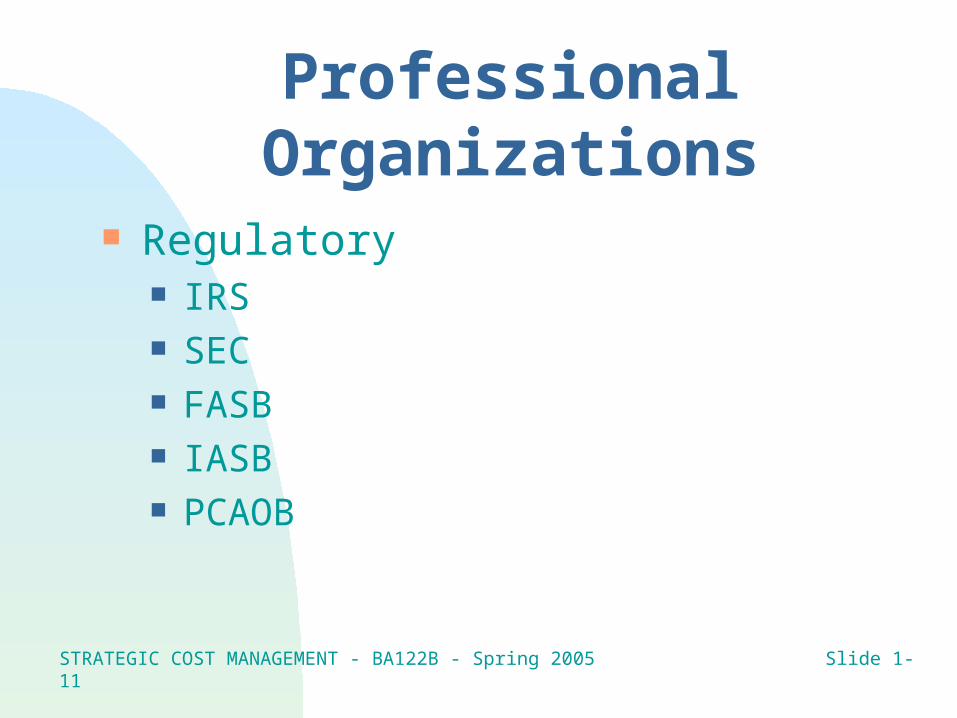

Professional Organizations

Regulatory IRS SEC FASB IASB PCAOB

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-12

Professional Organizations

Associations IMA SMA, Canada AICPA FEI IIA

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-13

Ethics

Lack of ethics--everyone loses South Florida Bermuda Triangle of

Ethics Tyco W.R. Grace Bausch and Lomb Sunbeam

Enron, World-com, Adelphia

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-14

Ethics and You

You will face an ethical challenge It could impact

Your job Your family Your relationships Your financial stability Your physical well-being

You have only ONE reputation...

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-15

Accounting Business Skills

“The What” Business Perspective Organizational Focus Bias for Action Communication Excellence People Proficiency

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-16

Financial Management Guidelines“The How”

Cc KTT MBWA R ƒ R3

responsiveness reliability relevance

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-17

Just Say “No” to...

A

B

C

Things we do to ourselves!!!

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-18

Scarlet Letter of Accounting

• Lacks Reality

• Distraction

• Lacks Cost Mgt.

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-19

Ansari: SMA

Strategic Triangle (QCT) Competition based on quality, cost & Time

Mgt. Acctg. Triangle (TBC) Impacts technical, behavioral & cultural

aspects Mgt. Acctg. Links Strategy with Action

It is not an end unto itself It is an integrating tool

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-20

SMA, cont.

The two triangles are dependent upon each other

This process is a framework to ensure that our management accounting tools possess the attributes necessary to achieve our strategic goals

STRATEGIC COST MANAGEMENT - BA122B - Spring 2005 Slide 1-21

SMA, cont.

QCT Triangle Self evident

TBC Triangle Provides Technical insight Encourages Behavioral changes Supports Cultural beliefs