ACCOUNTING PRINCIPLES and PROCESS Ricardo R. Palo, CPA, MBA.

54

ACCOUNTING PRINCIPLES and PROCESS Ricardo R. Palo, CPA, MBA

-

Upload

martin-cole -

Category

Documents

-

view

239 -

download

0

Transcript of ACCOUNTING PRINCIPLES and PROCESS Ricardo R. Palo, CPA, MBA.

ACCOUNTING PRINCIPLES and PROCESS

Ricardo R. Palo, CPA, MBA

Recognition and Measurement Concepts

ELEMENTS 1. Assets 2. Liabilities 3. Equity 4. Investment by owners 5. Distribution to owners /

dividends 6. Comprehensive

income 7. Revenues 8. Expenses 9. Gains 10. Losses

OBJECTIVES

Provide information:

1. Useful in investment and credit decisions.

2. Useful in assessing future cash flows.

3. About the financial position, performance, and changes in financial position.

PRINCIPLES

1. Historical cost 2. Revenue recognition 3. Matching 4. Full disclosure

CONSTRAINTS

1. Cost-benefit 2. Materiality 3. Industry Practice 4. Conservatism 5. Balance between Qualitative Characteristics

ASSUMPTIONS

1. Economic entity 2. Going concern 3. Monetary unit 4. Periodicity

First level: The “why” – goals and purposes of accounting.

Second level: Bridge between levels 1 and 3

Third level: The “how” – implementation

QUALITATIVE CHARACTERISTICS

1. Understandability 2. Relevance (Feedback

value, Predictive value and Materiality)

3. Reliability (Faithful Representation, Substance over Form, Neutrality, Prudence, and Completeness)

4. Comparability

Generally Accepted Accounting Principles

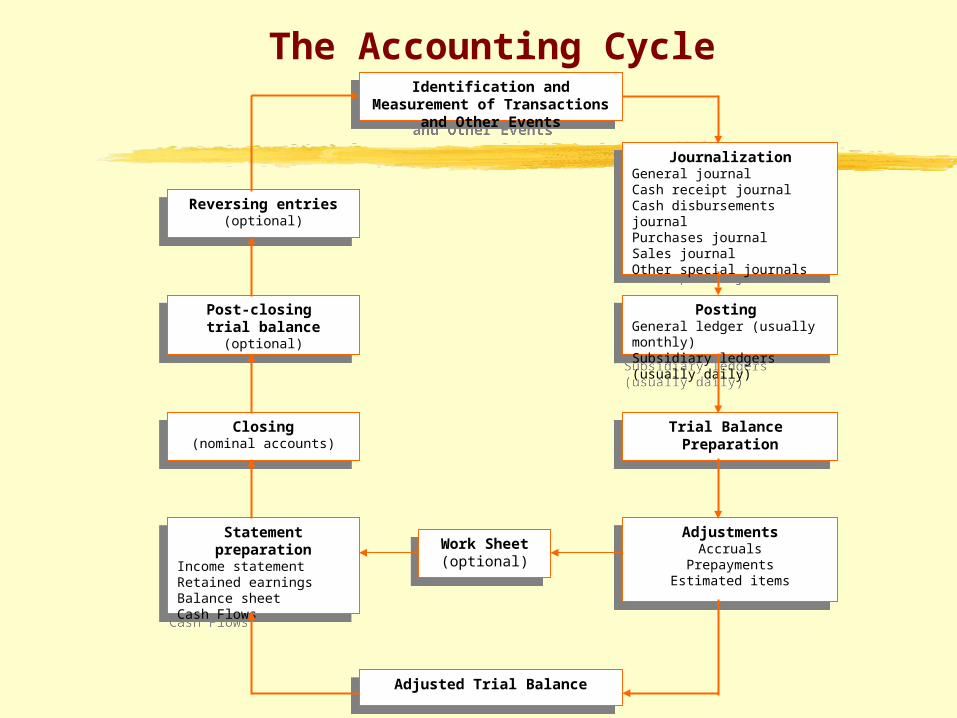

The Accounting CycleIdentification and Measurement of

Transactions and Other Events

Identification and Measurement of Transactions and Other Events

Reversing entries(optional)

Reversing entries(optional)

Post-closing trial balance

(optional)

Post-closing trial balance

(optional)

Closing(nominal accounts)

Closing(nominal accounts)

Statement preparationIncome statement Retained earnings Balance sheetCash Flows

Statement preparationIncome statement Retained earnings Balance sheetCash Flows

JournalizationGeneral journalCash receipt journalCash disbursements journalPurchases journalSales journalOther special journals

JournalizationGeneral journalCash receipt journalCash disbursements journalPurchases journalSales journalOther special journals

Posting General ledger (usually monthly)Subsidiary ledgers (usually daily)

Posting General ledger (usually monthly)Subsidiary ledgers (usually daily)

Trial Balance Preparation

Trial Balance Preparation

AdjustmentsAccruals

PrepaymentsEstimated items

AdjustmentsAccruals

PrepaymentsEstimated items

Work Sheet(optional)

Work Sheet(optional)

Adjusted Trial BalanceAdjusted Trial Balance

Accounting Process

Prepare accounting reports

Analyze and interpret for users

Record, classify, and summarize

Select economic events (transactions)

IdentificationIdentificationRecordingRecording

CommunicationCommunication

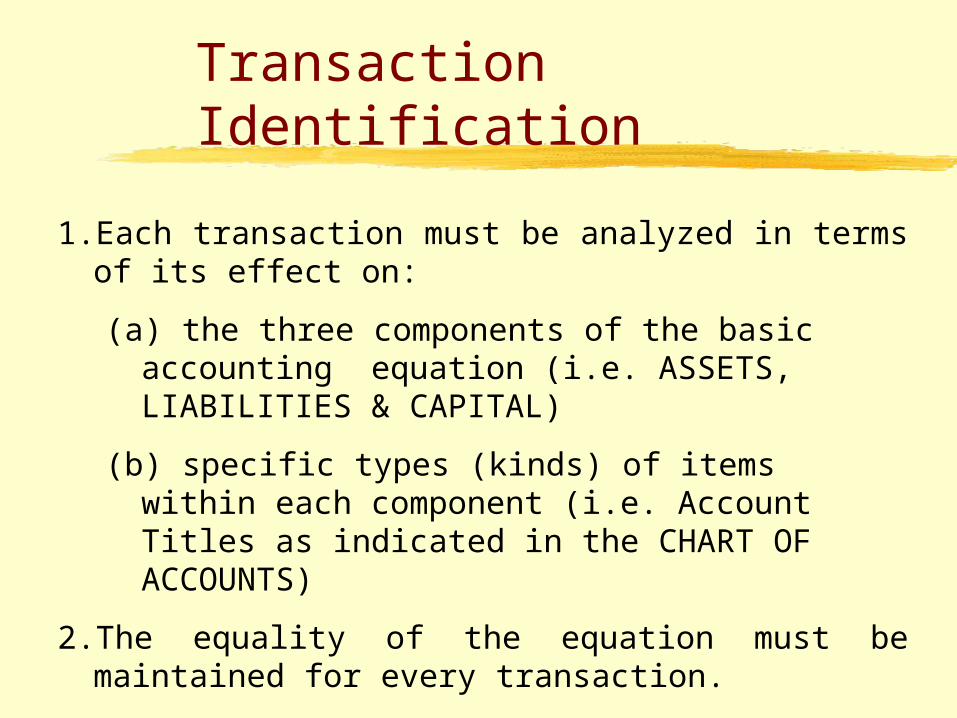

Transaction Identification

1. Each transaction must be analyzed in terms of its effect on:

(a) the three components of the basic accounting equation (i.e. ASSETS, LIABILITIES & CAPITAL)

(b) specific types (kinds) of items within each component (i.e. Account Titles as indicated in the CHART OF ACCOUNTS)

2. The equality of the equation must be maintained for every transaction.

Discuss services offered with potential client

Purchase supplies

CriterionCriterion

Pay rent

Record

EventsEvents

RecordDon’t

Record

Record/ Record/ Don’t RecordDon’t Record

Is the financial position (assets, liabilities, and owner’s equity) of the company changed?

Yes No Yes

CHART OF ACCOUNTS

Assets Owner’s Equity

101 Cash 301 E. Fernandez, Capital

112 Accounts Receivable 306 E. Fernandez, Drawing

113 Inventory 350 Income Summary

130 Prepaid Insurance

157 Equipment Revenues

158 Accumulated Depreciation—Office Equipment

400 Service Revenue

Liabilities Expenses

200 Notes Payable 501 Advertising Expense

201 Accounts Payable 502 Depreciation Expense

209 Unearned Revenue210 Accrued Revenue

503 Supplies Expense504 Insurance Expense

212 Salaries Payable 505 Salaries Expense

230 Interest Payable 506 Rent Expense

507 Utilities Expense

Revenues/Gains

Withdrawals by owner

Expenses/Losses

Investments by ownerOwner’s Equity

INCREASES DECREASES

Transaction Analysis

TRANSACTION (1). INVESTMENT BY OWNER. Eric Fernandez decides to open a clinic which he names Caring Hands. On September 1, 2007, he invests $15,000 cash in the business.

Assets = Liabilities +

E. Fernandez

Capital(1) 15,000 = 15,000

Capital

Cash

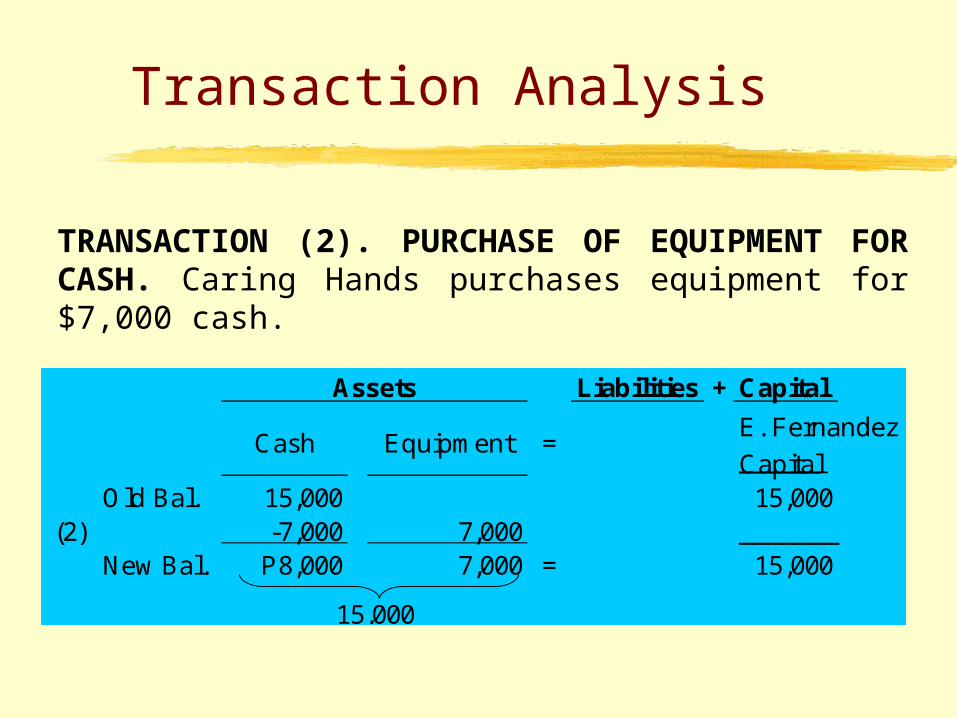

Transaction Analysis

TRANSACTION (2). PURCHASE OF EQUIPMENT FOR CASH. Caring Hands purchases equipment for $7,000 cash.

Liabilities + Capital

E. Fernandez

CapitalOld Bal. 15,000 15,000

(2) -7,000 7,000 _______New Bal. P8,000 7,000 = 15,000

15,000

=

Assets

EquipmentCash

Transaction Analysis

TRANSACTION (3). PURCHASE OF SUPPLIES ON CREDIT. Caring Hands purchases supplies for $1,600, expected to be paid next month.

Liabilities + Capital

Old Bal. 8,000 7,000 15,0001,600 -1,600

New Bal. 8,000 + 7,000 = 1,600 + 13,400

=

15,000

+

Assets

EquipmentCash

15,000

+Accounts Payable

E. Fernandez, Capital

Old Bal. 8,000 7,000 1,600 13,400(4) 1,200 1,200

New Bal. 9,200 + 7,000 = 1,600 + 14,600

Accounts Payable

E. Fernandez, Capital

=EquipmentCash + +

Transaction Analysis

TRANSACTION (4). SERVICES PROVIDED FOR CASH. Caring Hands receives $1,200 cash from customers for professional services it has provided.

Service Revenue

16,20016,200

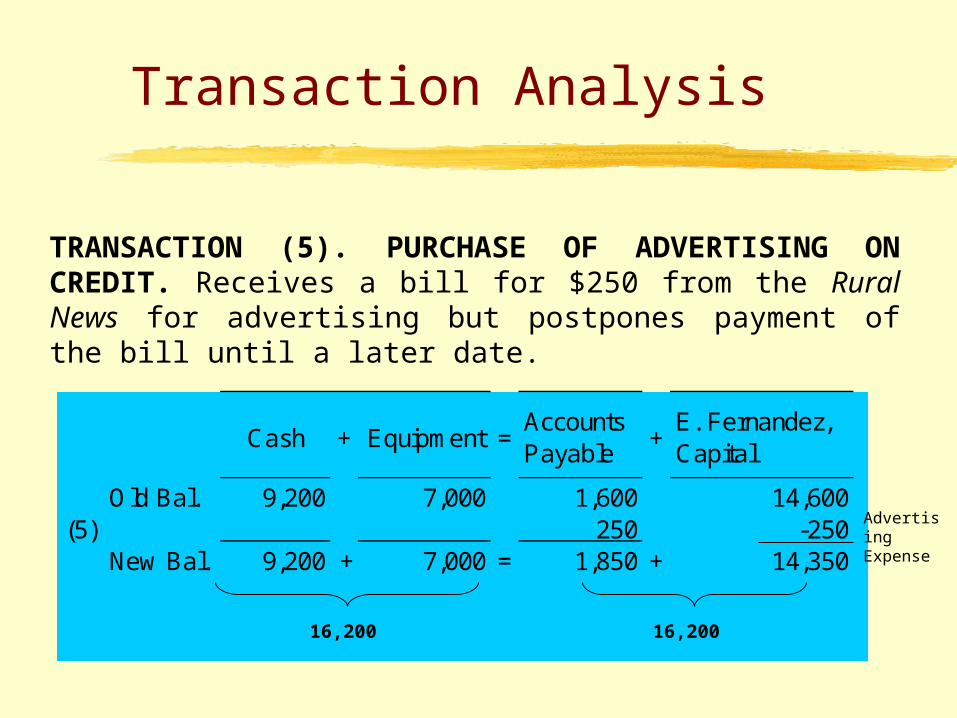

Transaction Analysis

TRANSACTION (5). PURCHASE OF ADVERTISING ON CREDIT. Receives a bill for $250 from the Rural News for advertising but postpones payment of the bill until a later date.

Old Bal. 9,200 7,000 1,600 14,600(5) 250 -250

New Bal. 9,200 + 7,000 = 1,850 + 14,350

Accounts Payable

E. Fernandez, Capital

EquipmentCash + +=

Advertising Expense

16,200 16,200

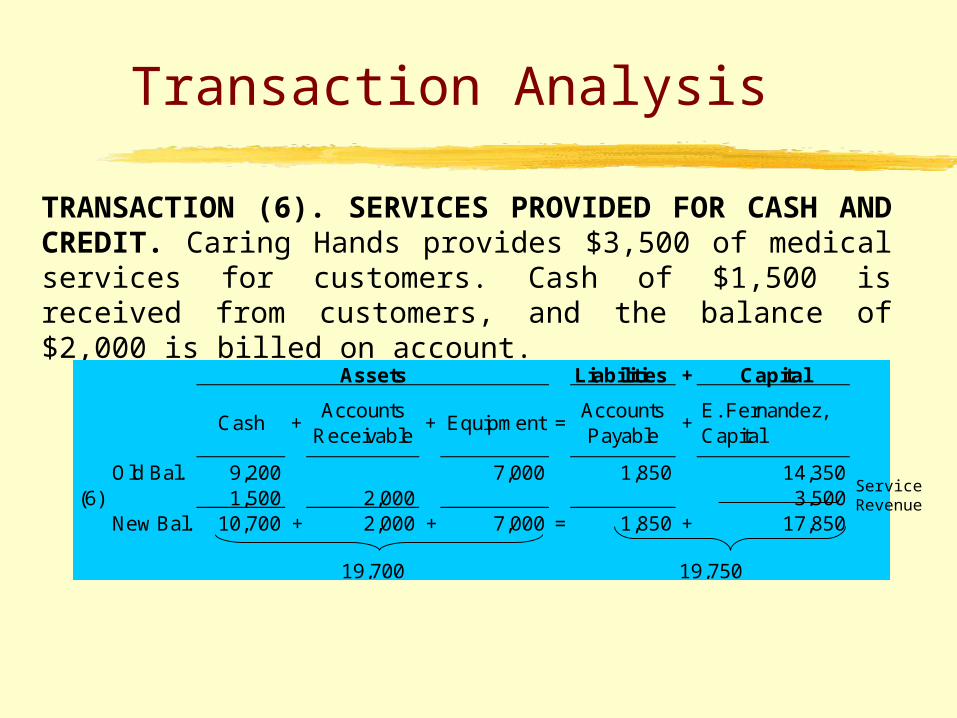

Transaction Analysis

TRANSACTION (6). SERVICES PROVIDED FOR CASH AND CREDIT. Caring Hands provides $3,500 of medical services for customers. Cash of $1,500 is received from customers, and the balance of $2,000 is billed on account.

Liabilities + Capital

Old Bal. 9,200 7,000 1,850 14,350(6) 1,500 2,000 3,500

New Bal. 10,700 + 2,000 + 7,000 = 1,850 + 17,850

19,750

Assets

EquipmentCash

19,700

+ +Accounts Payable

E. Fernandez, Capital

=+Accounts

Receivable

Service Revenue

Transaction Analysis

TRANSACTION (7). PAYMENT OF EXPENSES. Expenses paid in cash for September are rent $600, salaries of employees $900, and utilities $200.

Liabilities + Capital

Old Bal. 10,700 2,000 7,000 1,850 17,850-1,700 -600

-900(7) -200

New Bal. 9,000 + 2,000 + 7,000 = 1,850 + 16,150

Accounts Payable

E. Fernandez, Capital

=+Accounts

Receivable

18,000

Assets

EquipmentCash

18,000

+ +

Rent Expense

Salaries Expense

Utilities Expense

Transaction Analysis

TRANSACTION (8). PAYMENT OF A LIABILITY. Caring Hands pays its $250 Rural News advertising bill in cash.

Old Bal. 9,000 2,000 7,000 1,850 16,150(8) -250 -250

New Bal. 8,750 + 2,000 + 7,000 = 1,600 + 16,150

17,750

EquipmentCash

17,750

+ +Accounts Payable

E. Fernandez, Capital

=+Accounts

Receivable

Transaction Analysis

TRANSACTION (9). COLLECTION OF A RECEIVABLE. The sum of $600 in cash is received from customers who have previously been billed for services [in Transaction 6].

Old Bal. 8,750 2,000 7,000 1,600 16,150(9) 600 -600

New Bal. 9,350 + 1,400 + 7,000 = 1,600 + 16,150

Accounts Payable

E. Fernandez, Capital

=+Accounts

Receivable

17750

EquipmentCash

17,750

+ +

Transaction Analysis

TRANSACTION (10). WITHDRAWAL OF CASH BY OWNER. Erik Fernandez withdraws $1,300 in cash from the business for his personal use.

Old Bal. 9,350 1,400 7,000 1,600 16,150(10) -1,300 -1,300

New Bal. 8,050 + 1,400 + 7,000 = 1,600 + 14,850

Accounts Payable

E. Fernandez, Capital

=+Accounts

Receivable

16,450

EquipmentCash

16,450

+ +

Drawings

Liabilities +

(1) 15,000 15,000 Investment

(2) -7,000 7,0008,000 + 7,000 = 15,000

(3) 1,600 -1,600 Supplies Expense

8,000 + 7,000 = 1,600 13,400(4) 1,200 1,200 Service Revenue

9,200 + 7,000 = 1,600 14,600(5) 250 -250 Advertising Expense

9,200 + 7,000 = 1,850 14,350(6) 1,500 2,000 3,500 Service Revenue

10,700 + 2,000 + 7,000 = 1,850 17,850(7) -1,700 -600 Rent Expense

-900 Salaries Expense

-200 Utilities Expense

9,000 + 2,000 + 7,000 = 1,850 16,150(8) -250 -250

8,750 + 2,000 + 7,000 = 1,600 16,150(9) +600 -600

9,350 + 1,400 + 7,000 = 1,600 16,150(10) -1,300 -1,300 Drawings

8,050 + 1,400 + 7,000 = 1,600 + 14,850

+

Transaction

Accounts Payable

=+Accounts

Receivable

Owner's Equity

E. Fernandez, Capital

16450

Assets

EquipmentCash

16,450

+

Tabular Summary of Caring Hands Transactions

Accounting Process

Prepare accounting reports

Analyze and interpret for users

Record, classify, and summarize

Select economic events (transactions)

IdentificationIdentificationRecordingRecording

CommunicationCommunication

The Recording Process (Bookkeeping)

Transaction Identification

Enter transaction

in a JOURNAL using the rules of

DEBIT and CREDIT

Transfer journal

information to the LEDGER ACCOUNTS

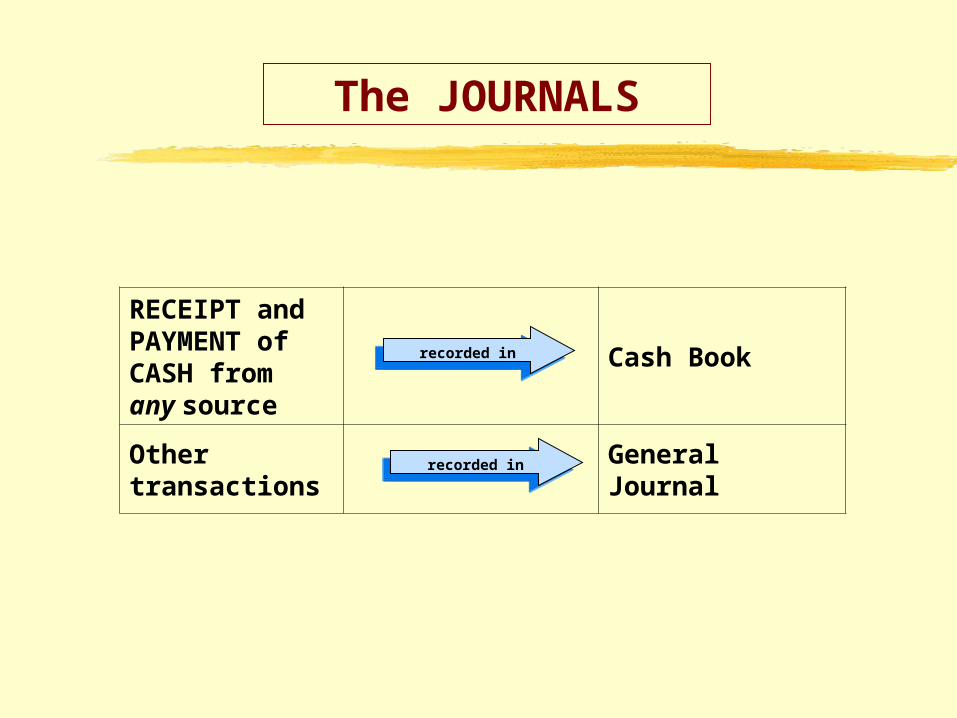

REGULAR BOOKS OF ACCOUNTS

JOURNALS Record of transactions in chronological order

Cash Book – record all receipts and payments for the period

Sales Journal – record all sales on credit Purchases Journal – record all purchases on credit General Journal – record of all transactions

GENERAL LEDGER Classifies the transactions as they affect the

different accounts for the period (usually one year)

SUBSIDIARYBOOKS OF ACCOUNTS

Receivables (Customers) Ledger Payables (Suppliers) Ledger Payroll Register Stock (Inventory) Records Equipment Ledgers or Asset

Inventory Rcords

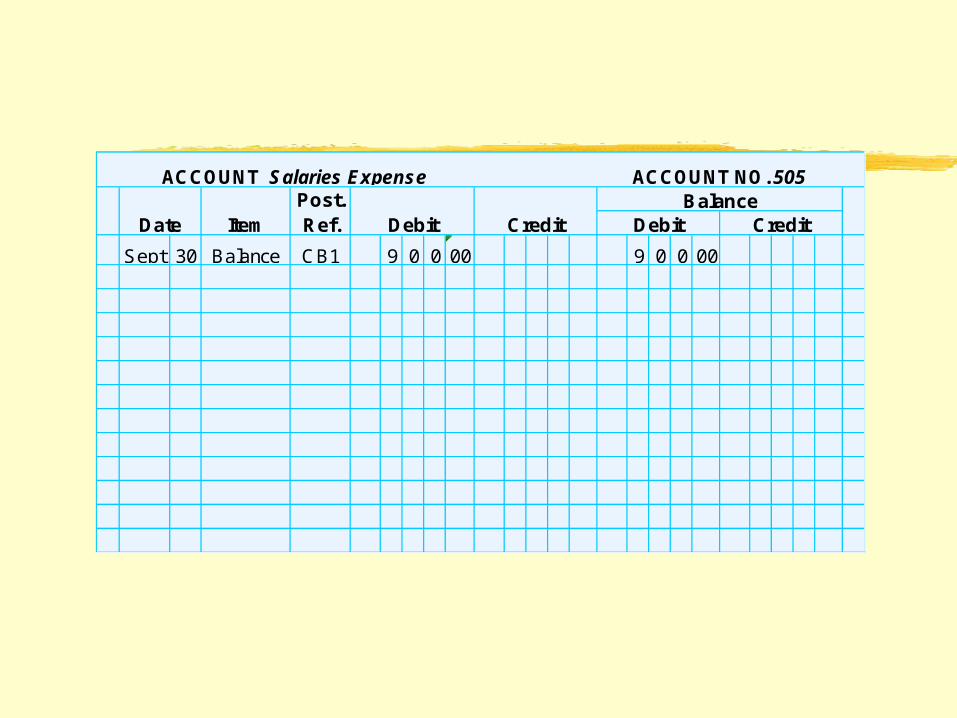

Title of Account

Left or debit sideRight or credit

side

Debit Balance Credit balance

Basic Form of Account

Debit Credit

ASSETS LIABILITIES

Withdrawals Revenue

Expenses CAPITAL

Sept 30 Balance CB1 18 3 0 0 00 18 3 0 0 0030 Balance CB1 10 2 5 0 00 8 0 5 0 00

Debit

ACCOUNT Cash ACCOUNT NO. 101

CreditPost. Ref. Debit Credit

BalanceItemDate

SAMPLE ACCOUNT

recorded inrecorded in

recorded inrecorded in

RECEIPT and PAYMENT of CASH from any source

Cash Book

Other transactions

General Journal

The JOURNALS

Account Titles F

Sept 1 15 0 0 0 00 E. Fernandez, capital 15 0 0 0 002 7 0 0 0 00 Equipment 7 0 0 0 004 1 2 0 0 00 1 2 0 0 006 1 5 0 0 00 2 0 0 0 00 3 5 0 0 007 1 7 0 0 00 9 0 0 00 2 0 0 00 Rent Expense 6 0 0 008 2 5 0 00 2 5 0 009 6 0 0 00 ( 6 0 0 00 )

10 1 3 0 0 00 E. Fernandez, drawing 1 3 0 0 0018 3 0 0 00 10 2 5 0 00 2 5 0 00 9 0 0 00 2 0 0 00 1 4 0 0 00 4 7 0 0 00 8 9 0 0 00 15 0 0 0 00

29 9 5 0 00 29 9 5 0 00Debits

ParticularsAccounts Payable

Debit

Salaries Expense

Debit

=

Cash Book page 1

Cash

Debit Credit

Utilities Expense

DebitDate

Accounts Receivable Debit (Credit)

Service Revenue

Credit

Credits

Debit Credit

Sundry

Description F

1 Sept 3 Supplies Expense 1 6 0 0 00 1

2 Accounts Payable 1 6 0 0 00 2

3 Purchase supplies on credit. 3

4 4

5 5 Advertising Expense 2 5 0 00 5

6 Accounts Payable 2 5 0 00 6

7 Incurred advertising expense 7

8 on credit. 8

9 9

GENERAL JOURNAL Page 1Date Debit Credit

Equipment

Supplies

The General Ledger

Individual

Assets

Accounts Receivable

Cash

Interest Payable

Salaries Payable

Individual

Liabilities

Accounts Payable

Notes Payable

Salaries Expense

Service Revenue

Individual

Owner’s Equity

E. Fernandez, Drawing

E. Fernandez, Capital

CHART OF ACCOUNTS

Assets Owner’s Equity

101 Cash 301 E. Fernandez, Capital

112 Accounts Receivable 306 E. Fernandez, Drawing

113 Inventory 350 Income Summary

130 Prepaid Insurance

157 Equipment Revenues

158 Accumulated Depreciation—Office Equipment

400 Service Revenue

Liabilities Expenses

200 Notes Payable 501 Advertising Expense

201 Accounts Payable 502 Depreciation Expense

209 Unearned Revenue210 Accrued Revenue

503 Supplies Expense504 Insurance Expense

212 Salaries Payable 505 Salaries Expense

230 Interest Payable 506 Rent Expense

507 Utilities Expense

Sept 30 Balance CB1 18 3 0 0 00 18 3 0 0 0030 Balance CB1 10 2 5 0 00 8 0 5 0 00

Debit

ACCOUNT Cash ACCOUNT NO. 101

CreditPost. Ref. Debit Credit

BalanceItemDate

Sept 6 CB1 2 0 0 0 00 2 0 0 0 009 CB1 6 0 0 00 1 4 0 0 00

Debit

ACCOUNT Accounts Receivable ACCOUNT NO. 112

CreditPost. Ref. Debit Credit

BalanceItemDate

Sept 2 CB1 7 0 0 0 00 7 0 0 0 00

Date Debit

ACCOUNT Equipment ACCOUNT NO. 157

CreditPost. Ref. Debit Credit

BalanceItem

Sept 3 GJ1 1 6 0 0 00 1 6 0 0 005 GJ1 2 5 0 00 1 8 5 0 00

30 CB1 2 5 0 00 1 6 0 0 00

Debit

ACCOUNT Accounts Payable ACCOUNT NO. 201

CreditPost. Ref. Debit Credit

BalanceItemDate

Sept 1 CB1 15 0 0 0 15 0 0 0

Debit

ACCOUNT E. Fernandez, Capital ACCOUNT NO. 301

CreditPost. Ref. Debit Credit

BalanceItemDate

Sept 10 CB1 1 3 0 0 0 1 3 0 0 00

ACCOUNT E. Fernandez, Drawing ACCOUNT NO. 306

CreditPost. Ref. Debit Credit

BalanceItemDate Debit

Sept 30 Balance CB1 4 7 0 0 4 7 0 0

Debit

ACCOUNT Service Revenue ACCOUNT NO. 400

CreditPost. Ref. Debit Credit

BalanceItemDate

Sept 5 GJ1 2 5 0 00 2 5 0 00

Debit

ACCOUNT Advertising Expense ACCOUNT NO. 501

CreditPost. Ref. Debit Credit

BalanceItemDate

Sept 3 GJ1 1 6 0 0 00 1 6 0 0 00

ACCOUNT Supplies Expense ACCOUNT NO. 503

CreditPost. Ref. Debit Credit

BalanceItemDate Debit

Sept 30 Balance CB1 9 0 0 00 9 0 0 00

ACCOUNT Salaries Expense ACCOUNT NO. 505

CreditPost. Ref. Debit Credit

BalanceItemDate Debit

Sept 6 CB1 6 0 0 00 6 0 0 00

Date Debit

ACCOUNT Rent Expense ACCOUNT NO. 506

CreditPost. Ref. Debit Credit

BalanceItem

Sept 30 CB1 2 0 0 00 2 0 0 00

Date Debit

ACCOUNT Utilities Expense ACCOUNT NO. 507

CreditPost. Ref. Debit Credit

BalanceItem

Cash 8 0 5 0 00Accounts Receivable 1 4 0 0 00Equipment 7 0 0 0 00Accounts Payable 1 6 0 0 00E. Fernandez, Capital 15 0 0 0 00E. Fernandez, Drawing 1 3 0 0 00Service Revenue 4 7 0 0 00Supplies Expense 1 6 0 0 00Advertising Expense 2 5 0 00Salaries Expense 9 0 0 00Rent Expense 6 0 0 00Utilities Expense 2 0 0 00

21 3 0 0 00 21 3 0 0 00

CARING HANDSTrial Balance

30-Sep-07

Adjusting Entries

1. ACCRUALS1.1. Accruals of Expenses – expenses incurred

but not paid.Expenses

XX Payable (Accrued Expense) XX

1.2. Accruals of Revenue – revenue earned but not collected.

Receivable (Accrued Revenue) XX Revenue XX

Adjusting Entries

2. DEFERRALS2.1. Deferrals of Expenses – expenditures paid but

not incurred.ASSET METHODExpense XX Asset (Prepaid/Deferred Expense)XXEXPENSE METHODAsset (Prepaid/Deferred Expense) XX Expense

XX

Adjusting Entries

2. DEFERRALS2.2. Deferrals of Revenue – receipts collected but

not earned.LIABILITY METHODLiability (Deferred Revenue) XX Revenue XXREVENUE METHODRevenue XX Liability (Deferred Revenue)XX

Adjusting Entries

3. DEPRECIATIONDepreciation Expense – Asset XX Accumulated Depreciation – Asset

XX

Formula: Cost – Salvage Value Useful life

Adjusting Entries

4. BAD DEBTSBad Debts Expense XX Allowance for Bad Debts XX

Formula: % of Outstanding Receivables

Revenue Service revenue $4,700Expenses Supplies Expense $1,600 Salaries Expense 900 Rent Expense 600 Advertising expense 250 Utilities expense 200 Total expenses 3,550Net income $1,150

CARING HANDSIncome Statement

For the Month Ended September 30, 2007

E. Fernandez, Capital - September 1 $ --0--Add: Investments $15,000 Net income 1,150 16,150

16,150Less: Drawings 1,300E. Fernandez, Capital - September 30 $14,850

CARING HANDSOwner's Equity Statement

For the Month Ended September 30, 2007

Cash $8,050Accounts receivable 1,400Equipment 7,000 Total assets $16,450

Liabilities Accounts payable $1,600Owner's equity E. Fernadez, Capital 14,850 Total liabilities and owner's equity $16,450

Liabilities and Owner's Equity

CARING HANDSBalance Sheet

As of September 30, 2007Assets

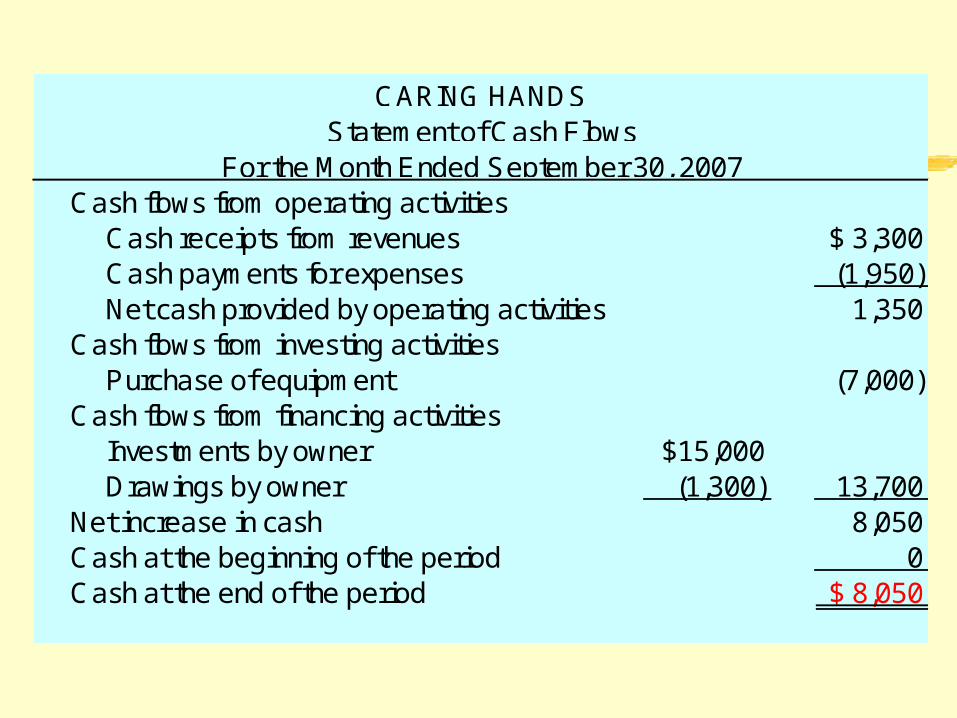

Cash flows from operating activities Cash receipts from revenues $ 3,300 Cash payments for expenses (1,950) Net cash provided by operating activities 1,350Cash flows from investing activities Purchase of equipment (7,000)Cash flows from financing activities Investments by owner $15,000 Drawings by owner (1,300) 13,700Net increase in cash 8,050Cash at the beginning of the period 0Cash at the end of the period $ 8,050

CARING HANDSStatement of Cash Flows

For the Month Ended September 30, 2007

Thank You