Activity Based Costing

51

Activity-Based Costing

-

Upload

abdulyunus-amir -

Category

Documents

-

view

45 -

download

0

description

Activity Based Costing

Transcript of Activity Based Costing

Activity-Based Costing

How much does it cost DaimlerChrysler to manufacture a PT Cruiser?

How much does it cost PriceWaterhouseCoopers to tabulate the results of Academy Award voting?

How much does it cost Wal-Mart to sell different products from its Web site?

How much does it cost Dell Computer to assemble and sell its newest laptop computer model?

Managers ask such questions for many purposes-

Developing strategies, making pricing and cost management decisions, meeting external-reporting requirements

Job costing

Batch costing

Contract costing

Process costing

Cost object/cost unit

Direct costs of a cost object

Indirect costs of a cost object

Cost tracing

Cost allocation

Cost pool:

Grouping of individual cost items

Cost pools can range from broad, such as all costs of the manufacturing plant , to narrow, such as the costs of operating metal-cutting machines

Cost allocation base: cause-and-effect link

Plastim Corporation manufactures lenses for rear taillights of automobiles.

A lens, made from black, red, orange, white plastic, is part of the lamp visible on the automobile’s exterior.

Lenses are made by injecting molten plastic into a mold to give the lamp its desired shape.

Mold is cooled to allow the molten plastic to solidify, and the lens is removed.

Under its contract with Tata Motors Plastim makes 2 types of lenses: Complex Lens (CL) and Simple Lens (SL)

Rates offered to Tata

SL Rs.630 per lens

CL Rs.1,370 per lens

Manufacturing CL is complex and needs more resources.

SL is simpler to make and needs comparatively less resources.

Plastim is operating at capacity and incurs very low marketing costs.

Because of high quality products, it has a minimal customer service costs.

Business of SL is very competitive.

The same competitive pressures do not exist for CL.

Plastim is currently using a simple costing system and allocates all indirect costs using a single indirect-cost rate.

Step 1: Identify the cost objects:

SL plans to produce 60,000 lenses

CL plans to produce 15,000 lenses

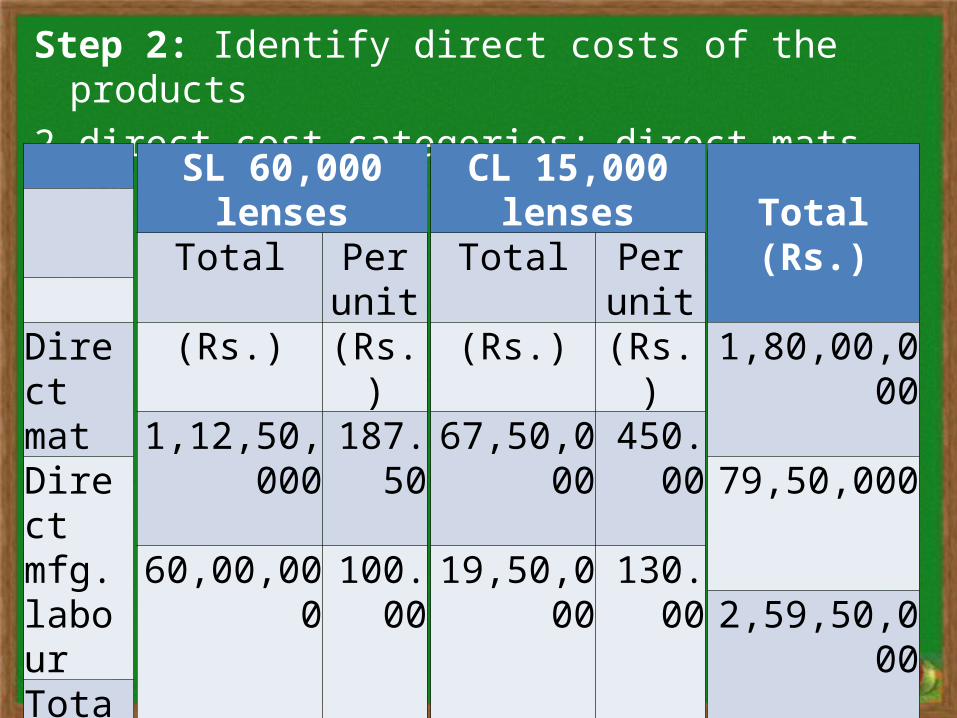

Step 2: Identify direct costs of the products

2 direct cost categories: direct mats and direct mfg. labour

Total(Rs.)

1,80,00,000

79,50,000

2,59,50,000

SL 60,000 lensesTotal Per

unit(Rs.) (Rs.)

1,12,50,000187.50

60,00,000100.00

1,72,50,000287.50

CL 15,000 lensesTotal Per

unit(Rs.) (Rs.)

67,50,000 450.00

19,50,000 130.00

87,00,000 580.00

Direct matDirect mfg. labourTotal direct cost

Step 3: Select cost-allocation bases to allocate ind. costs

Majority of indirect costs consist of salaries paid to supervisors, engineers, manufacturing support, and maintenance staff

Plastim uses direct manufacturing labour hours as the only allocation base to allocate manufacturing and non-manufacturing overheads to SL and CL

Plastim plans to use 39,750 direct mfg. labour hours for the upcoming year (30,000 for SL and 9,750 for CL)

Step 4: Identify indirect costs associated with cost-allocation base

Plastim groups all budgeted indirect costs into a single overhead cost pool

Budgeted indirect costs Rs.2,38,50,000

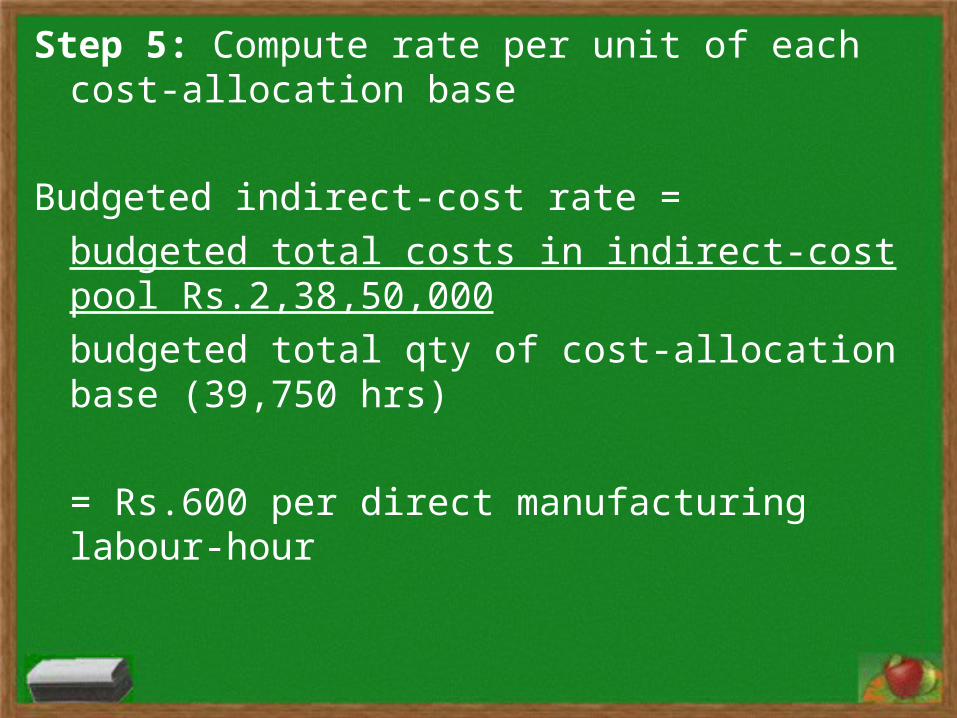

Step 5: Compute rate per unit of each cost-allocation base

Budgeted indirect-cost rate =

budgeted total costs in indirect-cost pool Rs.2,38,50,000

budgeted total qty of cost-allocation base (39,750 hrs)

= Rs.600 per direct manufacturing labour-hour

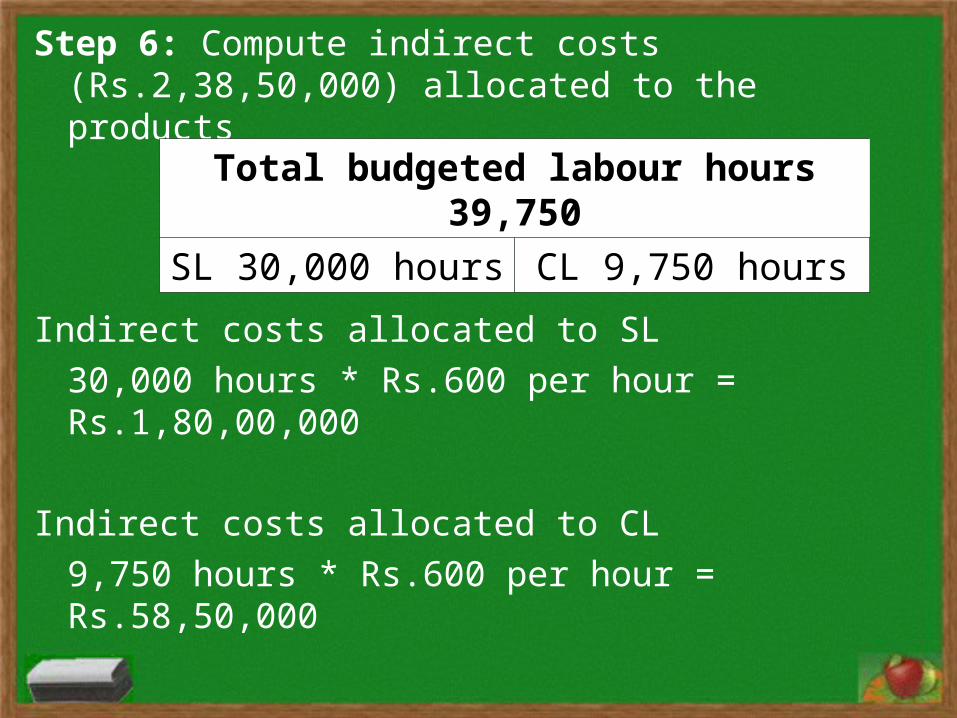

Step 6: Compute indirect costs (Rs.2,38,50,000) allocated to the products

Indirect costs allocated to SL

30,000 hours * Rs.600 per hour = Rs.1,80,00,000

Indirect costs allocated to CL

9,750 hours * Rs.600 per hour = Rs.58,50,000

Total budgeted labour hours 39,750SL 30,000 hours CL 9,750 hours

Step 7: Compute total costs of products

Total(Rs.)

1,80,00,00079,50,000

2,38,50,0004,98,00,000

SL 60,000 lensesTotal Per unit(Rs.) (Rs.)

1,12,50,000 187.5060,00,000 100.00

1,80,00,000 300.003,52,50,000 587.50

CL 15,000 lensesTotal Per unit(Rs.) (Rs.)

67,50,000 450.0019,50,000 130.00

58,50,000 390.001,45,50,000 970.00

Direct matDirect mfg. labourInd costsTotal costs

Rates offered to Tata

SL Rs.630 per lens

CL Rs.1,370 per lens

Plastim’s business for SL is very competitive.

In a recent meeting, Tata’s purchasing manager indicates that a new supplier, Jain Motors, which makes only simple lenses, is offering to supply SL to Tata at a price of Rs.530.

Unless Plastim can lower its selling price, it will lose Tata business for SL for the upcoming year

Dell Computer produces desktops, laptops and servers.

Three basic activities for manufacturing computers are:

Designing computers;

Ordering component parts; and

Assembly.

Different products require different quantities of three activities.

A server has a more complex design, many more parts, and a more complex assembly than a desktop.

Undercosting and Overcosting

Cost of a restaurant bill for 4 partners who meet monthly to discuss business developments. Each one orders separate entrees, deserts and drinks.

Restaurant bill for the most recent meeting:

EntréeDessertDrinksTotal

AnitaRs.110

040

150

AnuragRs.200

80140420

AjitRs.190

60100350

AnshulRs.140

4060

240

TotalRs.640

180340

1,160

AverageRs.160

4585

290

Undercosting and OvercostingProduct undercosting: a product consumes a high level of

resources but is reported to have a low cost per unit

Product overcosting: a product consumes a low level of resources but is reported to have a high cost per unit

What are the consequences of product undercosting and overcosting?

Five-step decision making process

Step 1: Identify the problem and uncertainties

Reduce the price and cost of SL

Five-step decision making process

Step 2: Obtain information

Asks a team of its design and process engineers to analyze and evaluate the design, manufacturing, and distribution operations for SL

The team is very confident that the technology and processes for SL are not inferior to any competitor.

Why profit margin is low for SL, where the company has strong capabilities, but high on newer CL?

Management starts to believe that the problem lies with Plastim’s costing system.

Five-step decision making process

Step 3: Make predictions about future

Step 4: Make decisions by choosing among alternatives

Whether to bid for Tata’s SL business

and if it does bid, what price it should offer

Step 5: Implement the decision, evaluate performance, and learn

Refining a costing system

Reduces the use of broad averages for assigning the costs of resources to cost objects

Provides better measurement of costs of indirect resources used by different cost objects

Refining a costing system

Direct cost tracing: Identify as many direct costs as is economically feasible.

Reduce the amount of costs classified as indirect

Indirect-cost pools: Expand the number of indirect-cost pools

Cost-allocation bases: Use cost-driver as the cost-allocation base

Activity-Based Costing System

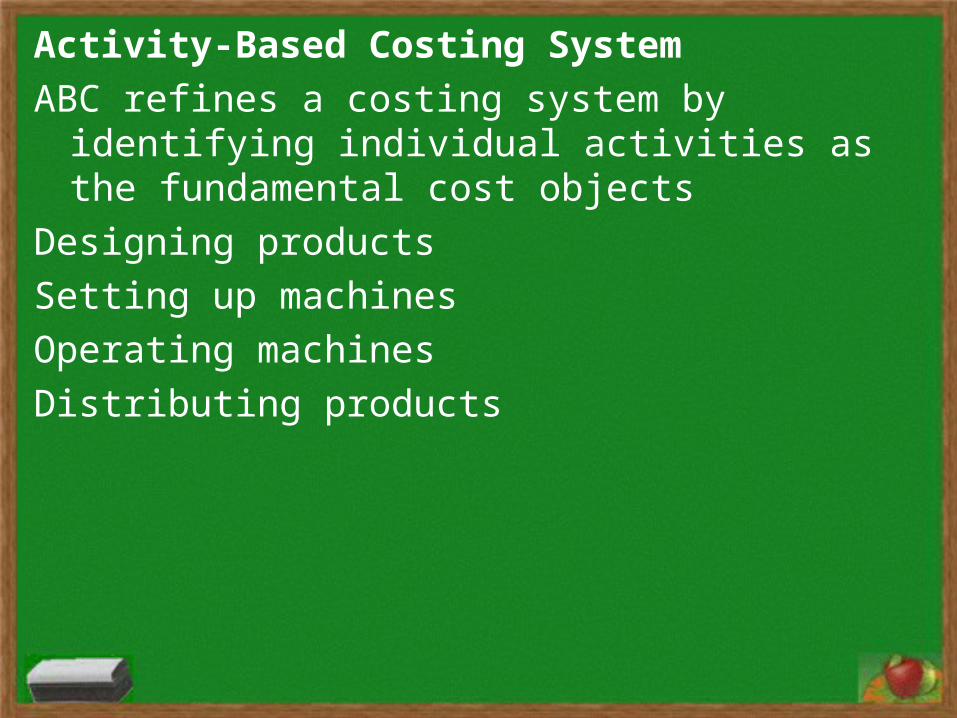

ABC refines a costing system by identifying individual activities as the fundamental cost objects

Designing products

Setting up machines

Operating machines

Distributing products

Traditional Costing System

Resource Costs

Cost Pools: Plants or Departments

Cost Objects

Activity-Based Costing System

Resource Costs

Cost Pools: Activities

Cost Objects

Activity-Based Costing System

Team identifies the following 7 activities:

1. Design products and processes

2. Set up molding machines to ensure that the molds are properly held in place and parts are properly aligned

3. Operate molding machines to manufacture lenses

4. Clean and maintain molds after lenses are manufactured

5. Prepare batches of finished lenses for shipment

6. Distribute lenses to customers

7. Administer and manage all processes

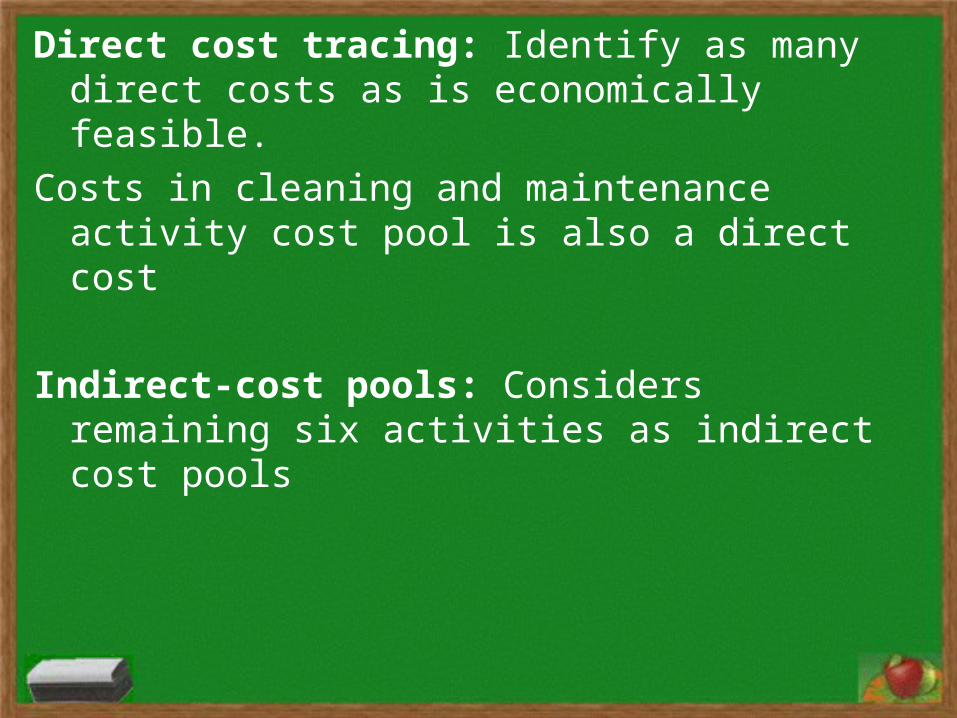

Direct cost tracing: Identify as many direct costs as is economically feasible.

Costs in cleaning and maintenance activity cost pool is also a direct cost

Indirect-cost pools: Considers remaining six activities as indirect cost pools

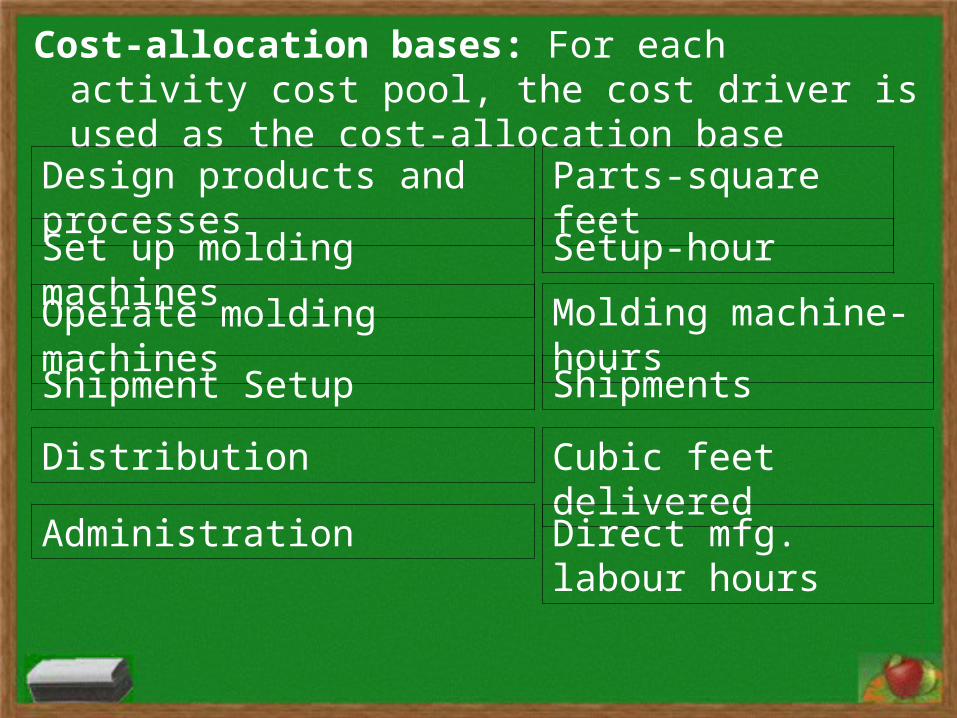

Cost-allocation bases: For each activity cost pool, the cost driver is used as the cost-allocation base

Design products and processes

Set up molding machines

Operate molding machines

Shipment Setup

Distribution

Administration

Parts-square feet

Setup-hour

Molding machine-hours

Shipments

Cubic feet delivered

Direct mfg. labour hours

Implementing ABC at Plastim

Step 1: Identify the cost objects:

SL plans to produce 60,000 lenses

CL plans to produce 15,000 lenses

Step 2: Identify direct costs of the products

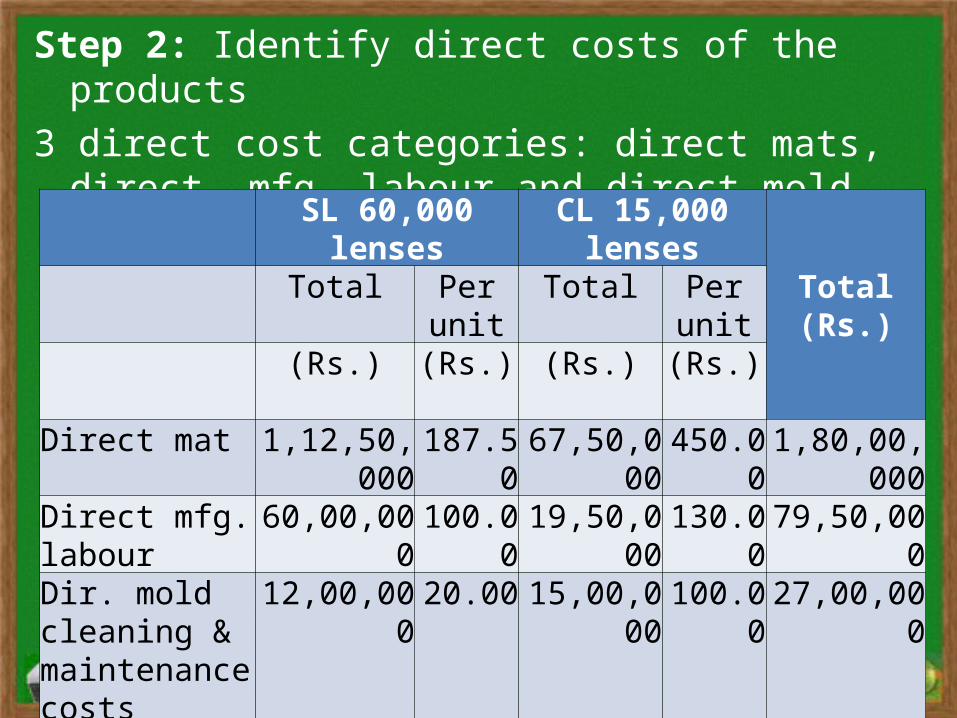

3 direct cost categories: direct mats, direct mfg. labour and direct mold cleaning and maintenance costs

SL 60,000 lenses CL 15,000 lensesTotal(Rs.)

Total Per unit Total Per unit(Rs.) (Rs.) (Rs.) (Rs.)

Direct mat 1,12,50,000 187.50 67,50,000 450.00 1,80,00,000Direct mfg. labour

60,00,000 100.00 19,50,000 130.00 79,50,000

Dir. mold cleaning & maintenance costs

12,00,000 20.00 15,00,000 100.00 27,00,000

Step 3: Select activities and cost-allocation bases

Design products and processes

Parts-square feet 100 parts-sq ft30 SL + 70 CL

Set up molding machines

Setup-hour 2,000 set-up hrs500 SL + 1,500 CL

Operate molding machines

Molding machine-hours

12,750 molding machine-hrs 9,000 SL + 3,750 CL

Shipment Setup Shipments 200 shipments100 SL + 100 CL

Distribution Cubic feet delivered 67,500 cubic ft45,000 SL + 22,500 CL

Administration Direct mfg. labour hours

39,750 mfg. lab. Hrs.30,000 SL + 9,750 CL

Step 4: Identify indirect costs associated with each cost-allocation base

Design products and processes Rs.45,00,000Set up molding machines 30,00,000Operate molding machines 63,75,000Shipment Setup 8,10,000Distribution 39,15,000Administration 25,50,000

2,11,50,000

Step 5: Compute the rate per unit of each cost-allocation base

Design products and processes

Rs.45,00,000 100 parts-sq ft 45,000/parts-sq ft

Administration 25,50,000 39,750 dir. mfg. lab. Hrs.

64.151/dir mfg lab hr

Set up molding machines

30,00,000 2,000 set-up hrs

1,500/set-up hr

Operate molding machines

63,75,000 12,750 molding machine-hrs

500/molding machine-hr

Shipment Setup 8,10,000 200 shipments 4,050/ shipment

Distribution 39,15,000 67,500 cubic ft 58/cubic ft

Step 6: Compute indirect costs allocated to products

SL 60,000 lenses(Rs.)

CL 15,000 lenses(Rs.)

Total(Rs.)

DesignSL 30 parts-sq ft * Rs.45,000CL 70 parts-sq ft * Rs.45,000

13,50,00031,50,000

45,00,000

Design costs allocated under traditional costing system(on the basis of Direct Manufacturing Labour Hour)SL 30,000 and CL 9,750 labour hours

45,00,000 * 30,000 / 39,750

45,00,000 * 9,750 / 39,750

33,96,226

11,03,774

45,00,000

Step 6: Compute indirect costs allocated to productsSL 60,000

lenses(Rs.)

CL 15,000 lenses(Rs.)

Total(Rs.)

DesignSL 30 parts-sq ft * Rs.45,000CL 70 parts-sq ft * Rs.45,000

13,50,00031,50,000

45,00,000

1,15,39,530 96,10,470 2,11,50,000

Setup molding machines (500 + 1,500)(Rs.1,500 per setup hour)

7,50,000 22,50,000 30,00,000

Machine Operations(39,000 + 3,750)(Rs.500 per molding-machine hour)

45,00,000 18,75,000 63,75,000

Shipment setup (100 + 100 shipments)(Rs.4,050 per shipment)

4,05,000 4,05,000 8,10,000

Distribution (45,000 + 22,500 cubic ft)(Rs.58 per cubic foot)

26,10,000 13,05,000 39,15,000

Administration(30,000 + 9,750 mfg. lab. hours)(Rs.64.151 per direct mfg. lab. hour)

19,24,530 6,25,470 25,50,000

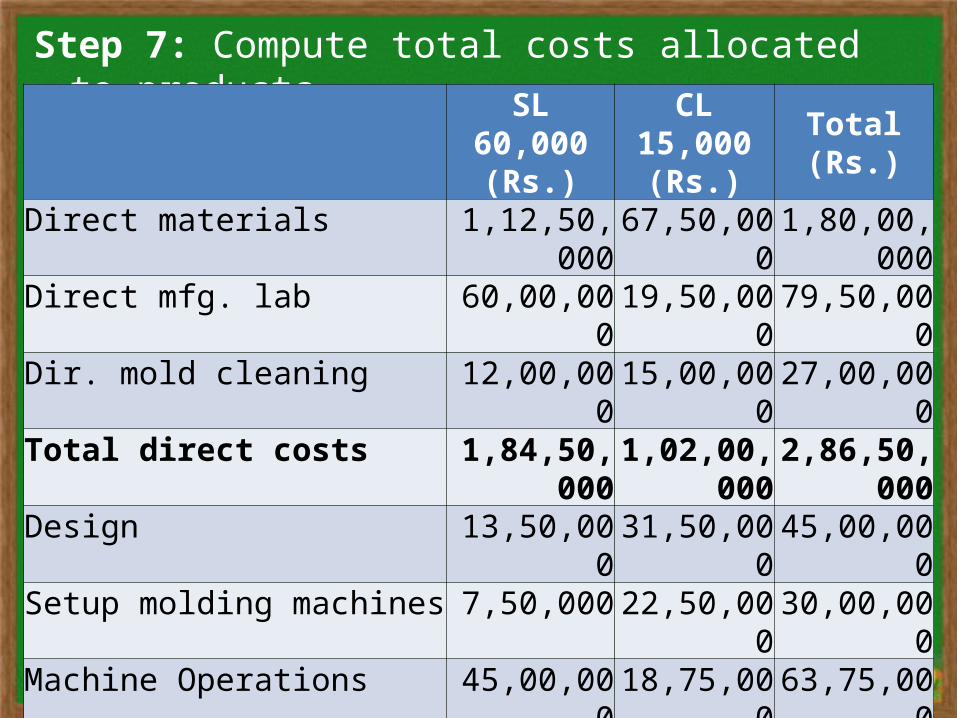

Step 7: Compute total costs allocated to products

SL 60,000(Rs.)

CL 15,000(Rs.)

Total(Rs.)

Direct materials 1,12,50,000 67,50,000 1,80,00,000Direct mfg. lab 60,00,000 19,50,000 79,50,000Dir. mold cleaning 12,00,000 15,00,000 27,00,000Total direct costs 1,84,50,000 1,02,00,000 2,86,50,000Design 13,50,000 31,50,000 45,00,000Setup molding machines 7,50,000 22,50,000 30,00,000Machine Operations 45,00,000 18,75,000 63,75,000Shipment setup 4,05,000 4,05,000 8,10,000Distribution 26,10,000 13,05,000 39,15,000Administration 19,24,530 6,25,470 25,50,000Total indirect costs 1,15,39,530 96,10,470 2,11,50,000Total costs 2,99,89,530 1,98,10,470 4,98,00,000Cost per unit Rs.499.80 Rs.1,320.70

Total costs of products under traditional costing system

Total(Rs.)

1,80,00,00079,50,000

2,59,50,000

2,38,50,0004,98,00,000

SL 60,000 lensesTotal Per unit(Rs.) (Rs.)

1,12,50,000 187.5060,00,000 100.00

1,72,50,000 287.50

1,80,00,000 300.003,52,50,000 587.50

CL 15,000 lensesTotal Per unit(Rs.) (Rs.)

67,50,000 450.0019,50,000 130.00

87,00,000 580.00

58,50,000 390.001,45,50,000 970.00

Direct matDirect mfg. labourTotal direct costInd costsTotal costs

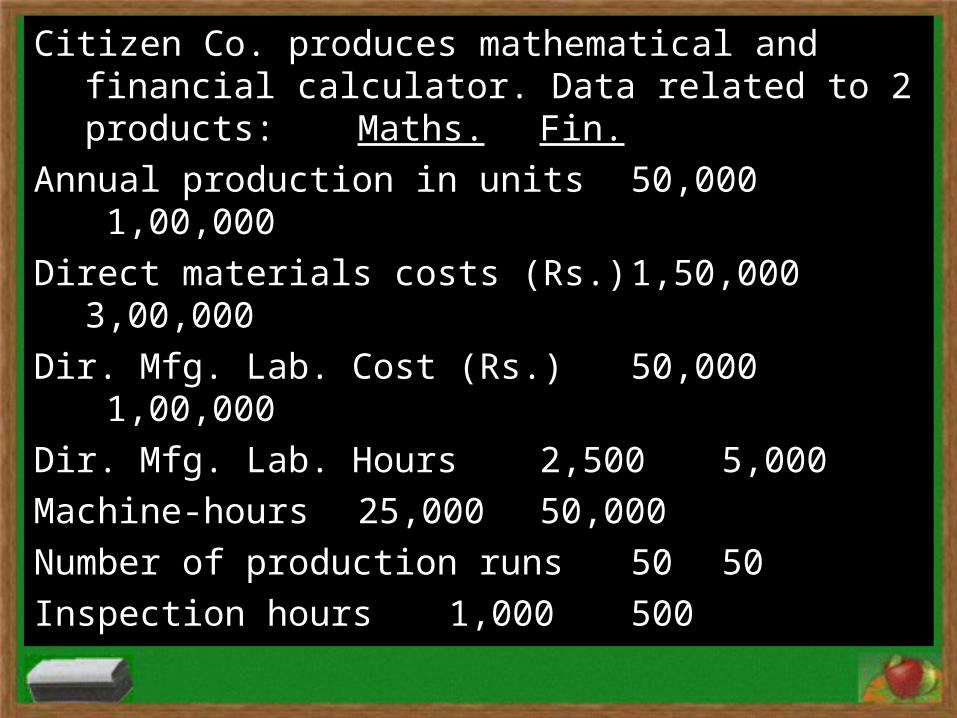

Citizen Co. produces mathematical and financial calculator. Data related to 2 products: Maths.

Fin.Annual production in units 50,000 1,00,000Direct materials costs (Rs.) 1,50,000 3,00,000Dir. Mfg. Lab. Cost (Rs.) 50,000

1,00,000Dir. Mfg. Lab. Hours 2,500 5,000Machine-hours 25,000 50,000Number of production runs 50 50Inspection hours 1,000 500

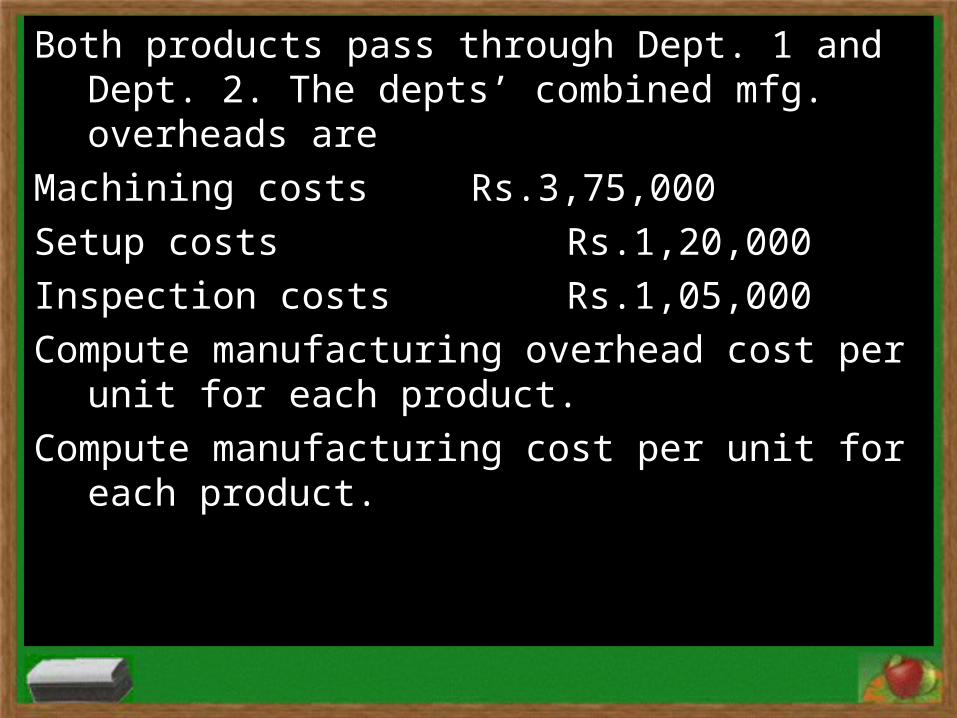

Both products pass through Dept. 1 and Dept. 2. The depts’ combined mfg. overheads are

Machining costs Rs.3,75,000Setup costs Rs.1,20,000Inspection costs Rs.1,05,000Compute manufacturing overhead cost per unit for each

product.Compute manufacturing cost per unit for each product.

GE India Ltd. has a machining facility for specializing in jobs for the aircraft-components market.

The previous job-costing system had 2 direct cost categories: direct materials and direct manufacturing labour costs and a single indirect-cost pool: manufacturing overhead, allocated using direct manufacturing labour hours

The indirect cost-allocation rate of the previous system for current year would have been Rs.230 per direct manufacturing labour hour.

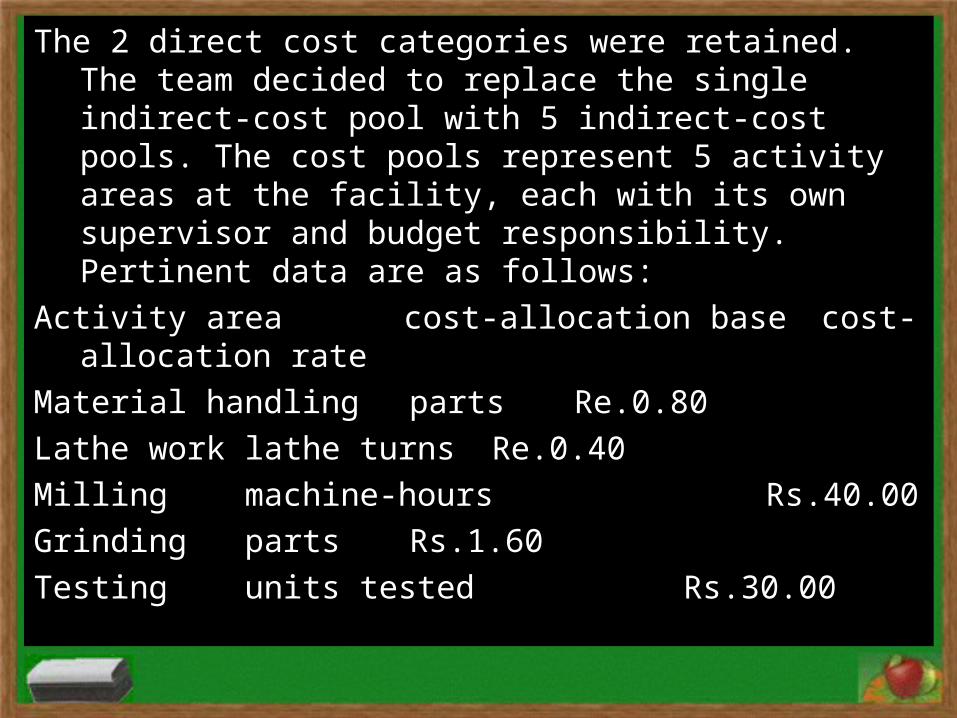

Recently a team with members from product design, manufacturing, and accounting used an ABC approach to refine its job-costing system.

The 2 direct cost categories were retained. The team decided to replace the single indirect-cost pool with 5 indirect-cost pools. The cost pools represent 5 activity areas at the facility, each with its own supervisor and budget responsibility. Pertinent data are as follows:

Activity area cost-allocation base cost-allocation rate

Material handling parts Re.0.80Lathe work lathe turns

Re.0.40Milling machine-hours Rs.40.00Grinding parts Rs.1.60Testing units tested Rs.30.00

Information gathering technology has advanced to the point at which the data necessary for budgeting in these 5 activity areas collected automatically.

2 representative jobs processed under the ABC system at the facility in the most recent period had the following characteristics:

Particulars Job 410 Job 411

Direct materials cost per job Rs.9,700 Rs.59,900Dir mfg lab cost per job Rs.750 Rs.11,250Dir mfg lab hours per job 25 375Parts per job 500 2,000Lathe turns per job 20,000 60,000Machine-hours per job 150 1,050

Units per job 10 200

Compute manufacturing cost per unit for each job under previous job-costing system.

Compute manufacturing cost per unit for each job under ABC system.

Lays Potatoes (LP) processes potatoes into potato chips at its automated Noida plant. It sells chips to retail customer market and institutional market.

LP’s existing costing system has a single direct-cost category (direct materials, raw potatoes) and a single indirect-cost pool (production support). Support costs are allocated on the basis of kgs of potato chips processed. Support costs include packaging materials. Current year total actual costs for producing 10,00,000 kgs of chips (9,00,000 for retail mkt and 1,00,000 for institutional mkt) are:

Direct materials used Rs.1,50,000Production support Rs.9,83,000

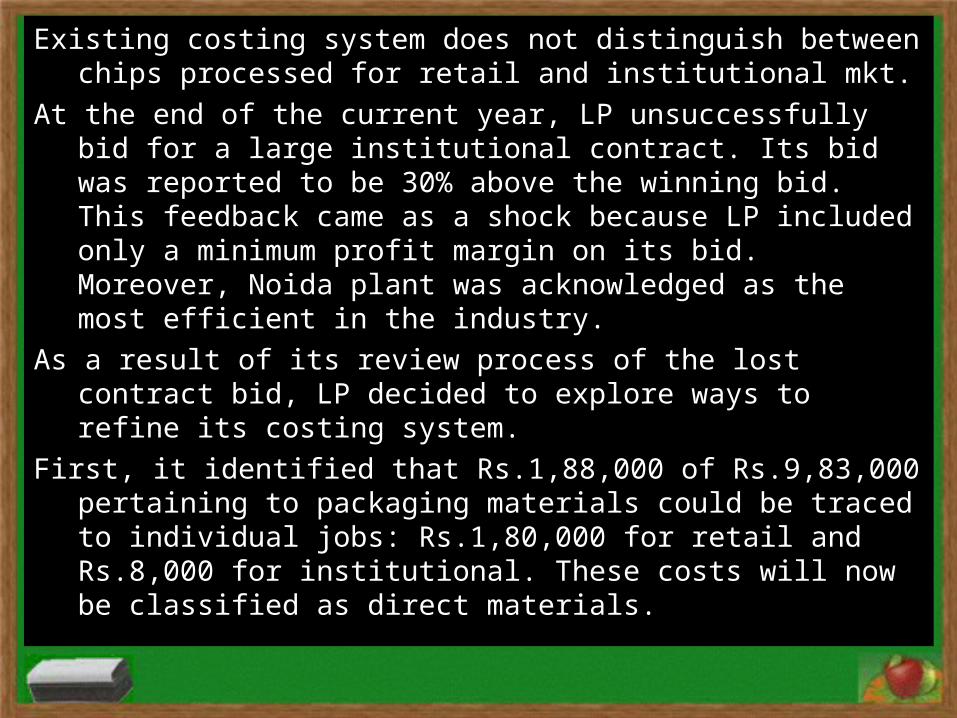

Existing costing system does not distinguish between chips processed for retail and institutional mkt.

At the end of the current year, LP unsuccessfully bid for a large institutional contract. Its bid was reported to be 30% above the winning bid. This feedback came as a shock because LP included only a minimum profit margin on its bid. Moreover, Noida plant was acknowledged as the most efficient in the industry.

As a result of its review process of the lost contract bid, LP decided to explore ways to refine its costing system.

First, it identified that Rs.1,88,000 of Rs.9,83,000 pertaining to packaging materials could be traced to individual jobs: Rs.1,80,000 for retail and Rs.8,000 for institutional. These costs will now be classified as direct materials.

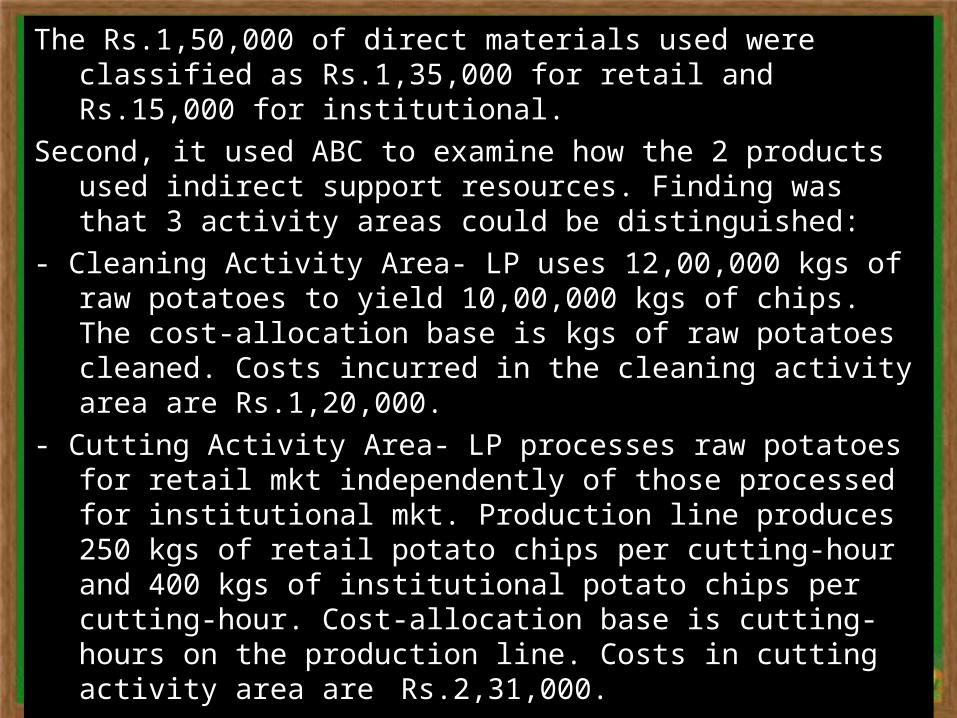

The Rs.1,50,000 of direct materials used were classified as Rs.1,35,000 for retail and Rs.15,000 for institutional.

Second, it used ABC to examine how the 2 products used indirect support resources. Finding was that 3 activity areas could be distinguished:

- Cleaning Activity Area- LP uses 12,00,000 kgs of raw potatoes to yield 10,00,000 kgs of chips. The cost-allocation base is kgs of raw potatoes cleaned. Costs incurred in the cleaning activity area are Rs.1,20,000.

- Cutting Activity Area- LP processes raw potatoes for retail mkt independently of those processed for institutional mkt. Production line produces 250 kgs of retail potato chips per cutting-hour and 400 kgs of institutional potato chips per cutting-hour. Cost-allocation base is cutting-hours on the production line. Costs in cutting activity area are

Rs.2,31,000.

- Packaging Activity Area- LP packages chips for retail mkt independently of those packaged for institutional mkt. packaging line packages 25 kgs of retail potato chips per packaging-hour and 100 kgs of institutional potato chips per packaging-hour. The cost allocation base is packaging-hours on the production line. Costs in the packaging activity area are Rs.4,44,000.

Using existing costing system, what is the cost per kg of potato chips produced by LP?

Using the ABC system, what is the cost per kg of retail potato chips and institutional potato chips?

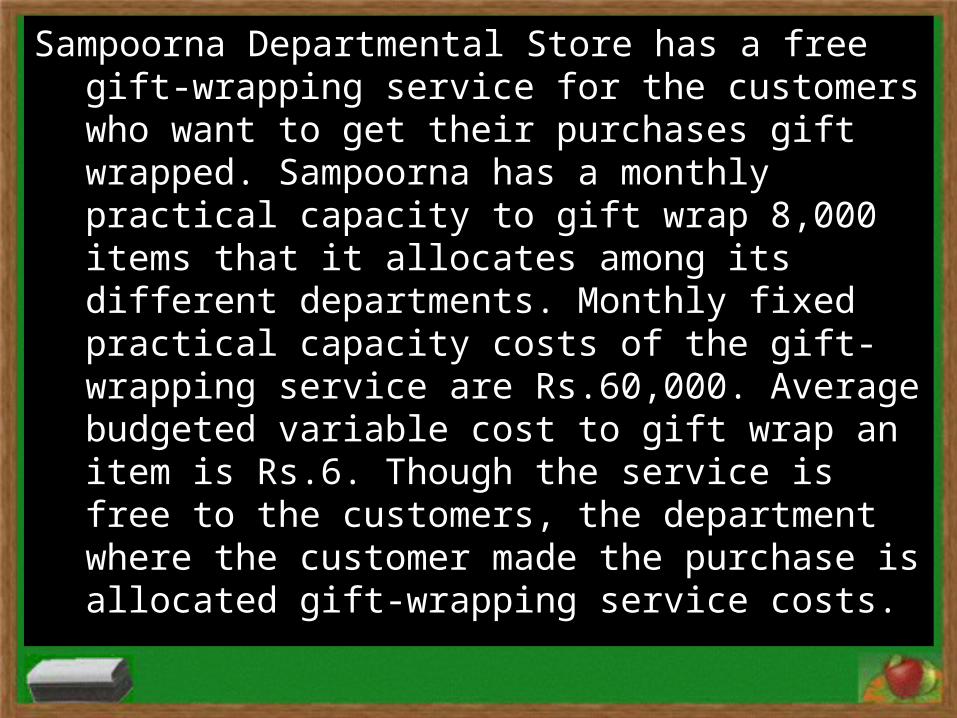

Sampoorna Departmental Store has a free gift-wrapping service for the customers who want to get their purchases gift wrapped. Sampoorna has a monthly practical capacity to gift wrap 8,000 items that it allocates among its different departments. Monthly fixed practical capacity costs of the gift-wrapping service are Rs.60,000. Average budgeted variable cost to gift wrap an item is Rs.6. Though the service is free to the customers, the department where the customer made the purchase is allocated gift-wrapping service costs.

Various departments’ actual use of the gift-wrapping service during the current month and their respective needs at practical capacity follow:

Department Actual No. of gifts

wrapped

No. of gifts that can be wrapped at practical capacity

GiftsMen’s wearWomen’s wearFootwearChinaLinen

2,2007501,600450650350

2,8001,0002,100700900500

• Allocate the costs for the gift-wrapping service to each department using a single rate method based on actual number of gifts wrapped.

• Compute the amount allocated to each department using the dual rate method when fixed costs are allocated based on practical capacity and variable costs are allocated using actual usage.