CMA311S – NOTES 2010. UNIT 2: ACTIVITY-BASED COSTING · PDF fileUNIT 2: ACTIVITY-BASED...

24

28 CMA311S – NOTES 2010. UNIT 2: ACTIVITY-BASED COSTING 1. Introduction Activity-based costing (ABC) is a recent development in Management Accounting which gives an alternative method of accounting for manufacturing overheads. Its development is in response to perceived limitations of the Traditional absorption costing system you learnt in Cost & Management Accounting 2A. This unit explains the techniques and rationale behind Activity-based costing. In addition, a comparison with the traditional costing method is made. 2. Traditional product costing system 2.1 Introduction In Cost & Management Accounting 2A you learned that the manufacturing (production) cost of a product is computed as follows: Direct material + Direct labour + Manufacturing overheads Direct material is the raw material that needs to be converted in order to produce a final product that can be used by consumers. For example, wood is a raw material used in the manufacturing of wooden furniture, sheet metal is a raw material used in the manufacturing of refrigerators, and paper is a raw material used in the production of newspapers, magazines, etc. The raw material changes its form and is physically consumed (incorporated) in the manufacturing process. Direct labour is the cost of wages for personnel who work directly on the manufactured products. Examples are the wages paid to cabinet-makers, welders and machine operators. Manufacturing overheads are all manufacturing costs other than direct material and direct labour cost. Manufacturing overheads include three types of cost: • Indirect material. This is the material required for the production process but which does not become an integral part of the finished product; or material consumed in production but insignificant in cost. An example is the cost of cloths and cleaning materials used in a factory. They do not become part of the product. Materials such as glue or paint do become part of the final product, but they may be so inexpensive that it is not worth tracing their costs to specific products as direct materials • Indirect labour. This is the cost of personnel who do not work directly on the product, but whose services are necessary for the manufacturing process. Factory supervisors, storekeepers, cleaners, security guards, etc. are all indirect labourers. • Other manufacturing costs. All other factory costs that are neither material nor labour costs are classified as manufacturing overheads. These costs include depreciation of plant and equipment, property taxes, insurance, electricity, etc. You also learned that it is normally quite simple to calculate the direct material and direct labour cost per unit. However, manufacturing overheads is a pool of indirect production costs and cannot easily be traced to individual units. Manufacturing overheads are therefore assigned to individual units. This process is called overheads application (absorption, recovery). Overheads are applied (absorbed, recovered) on the basis of estimates made at the beginning of the accounting period. The accounting department chooses some measure of productive activity to use as the basis for overhead absorption. In traditional product-costing

Transcript of CMA311S – NOTES 2010. UNIT 2: ACTIVITY-BASED COSTING · PDF fileUNIT 2: ACTIVITY-BASED...

28

CMA311S – NOTES 2010. UNIT 2: ACTIVITY-BASED COSTING 1. Introduction Activity-based costing (ABC) is a recent development in Management Accounting which gives an alternative method of accounting for manufacturing overheads. Its development is in response to perceived limitations of the Traditional absorption costing system you learnt in Cost & Management Accounting 2A. This unit explains the techniques and rationale behind Activity-based costing. In addition, a comparison with the traditional costing method is made. 2. Traditional product costing system 2.1 Introduction In Cost & Management Accounting 2A you learned that the manufacturing (production) cost of a product is computed as follows: Direct material + Direct labour + Manufacturing overheads Direct material is the raw material that needs to be converted in order to produce a final product that can be used by consumers. For example, wood is a raw material used in the manufacturing of wooden furniture, sheet metal is a raw material used in the manufacturing of refrigerators, and paper is a raw material used in the production of newspapers, magazines, etc. The raw material changes its form and is physically consumed (incorporated) in the manufacturing process. Direct labour is the cost of wages for personnel who work directly on the manufactured products. Examples are the wages paid to cabinet-makers, welders and machine operators. Manufacturing overheads are all manufacturing costs other than direct material and direct labour cost. Manufacturing overheads include three types of cost:

• Indirect material. This is the material required for the production process but which does not become an integral part of the finished product; or material consumed in production but insignificant in cost. An example is the cost of cloths and cleaning materials used in a factory. They do not become part of the product. Materials such as glue or paint do become part of the final product, but they may be so inexpensive that it is not worth tracing their costs to specific products as direct materials

• Indirect labour. This is the cost of personnel who do not work directly on the product, but whose services are necessary for the manufacturing process. Factory supervisors, storekeepers, cleaners, security guards, etc. are all indirect labourers.

• Other manufacturing costs. All other factory costs that are neither material nor labour costs are classified as manufacturing overheads. These costs include depreciation of plant and equipment, property taxes, insurance, electricity, etc.

You also learned that it is normally quite simple to calculate the direct material and direct labour cost per unit. However, manufacturing overheads is a pool of indirect production costs and cannot easily be traced to individual units. Manufacturing overheads are therefore assigned to individual units. This process is called overheads application (absorption, recovery). Overheads are applied (absorbed, recovered) on the basis of estimates made at the beginning of the accounting period. The accounting department chooses some measure of productive activity to use as the basis for overhead absorption. In traditional product-costing

29

systems, this measure is usually some volume-based cost driver (or activity base), such as direct labour hours, direct labour cost, machine hours, etc. An estimate is made of: 1. the amount of manufacturing overheads that will be incurred during a specified period of time and 2. the amount of the cost driver (or activity base) that will be used or incurred during the same time

period. A predetermined overhead rate is then computed as follows:

Budgeted manufacturing overhead cost Overhead absorption rate (OAR) = Budgeted amount of cost driver (or activity base)

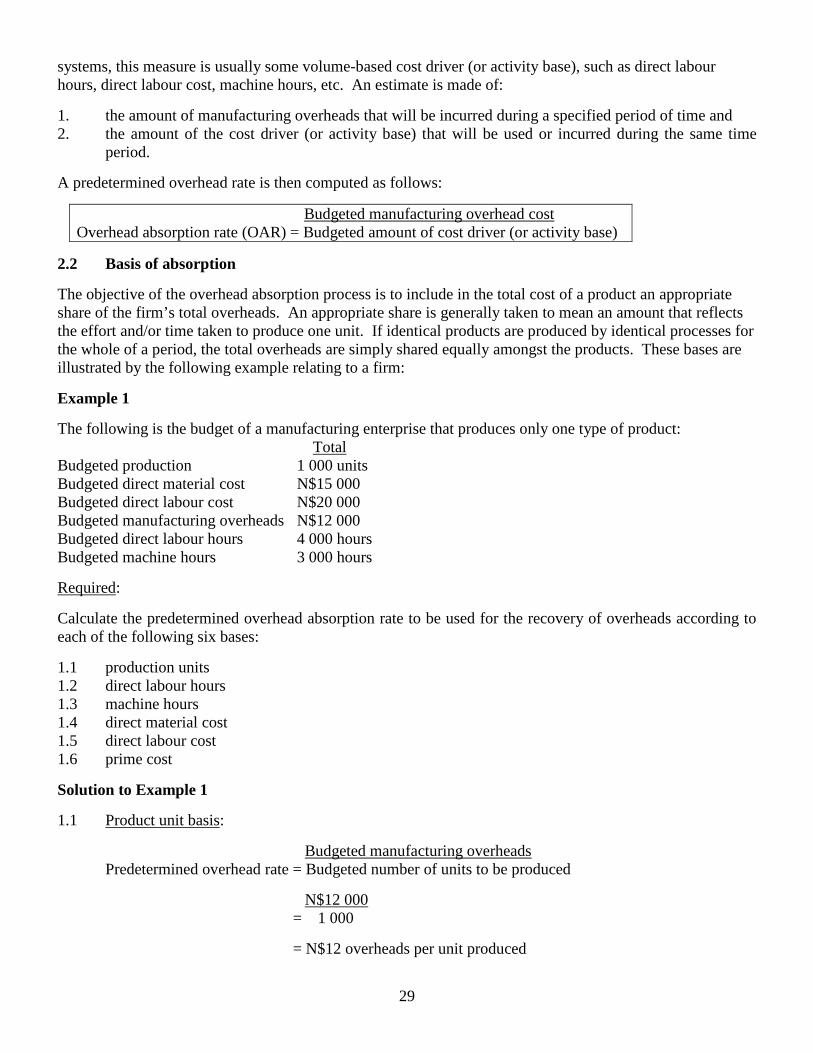

2.2 Basis of absorption The objective of the overhead absorption process is to include in the total cost of a product an appropriate share of the firm’s total overheads. An appropriate share is generally taken to mean an amount that reflects the effort and/or time taken to produce one unit. If identical products are produced by identical processes for the whole of a period, the total overheads are simply shared equally amongst the products. These bases are illustrated by the following example relating to a firm: Example 1 The following is the budget of a manufacturing enterprise that produces only one type of product: Total Budgeted production 1 000 units Budgeted direct material cost N$15 000 Budgeted direct labour cost N$20 000 Budgeted manufacturing overheads N$12 000 Budgeted direct labour hours 4 000 hours Budgeted machine hours 3 000 hours Required: Calculate the predetermined overhead absorption rate to be used for the recovery of overheads according to each of the following six bases: 1.1 production units 1.2 direct labour hours 1.3 machine hours 1.4 direct material cost 1.5 direct labour cost 1.6 prime cost Solution to Example 1 1.1 Product unit basis: Budgeted manufacturing overheads

Predetermined overhead rate = Budgeted number of units to be produced N$12 000 = 1 000 = N$12 overheads per unit produced

30

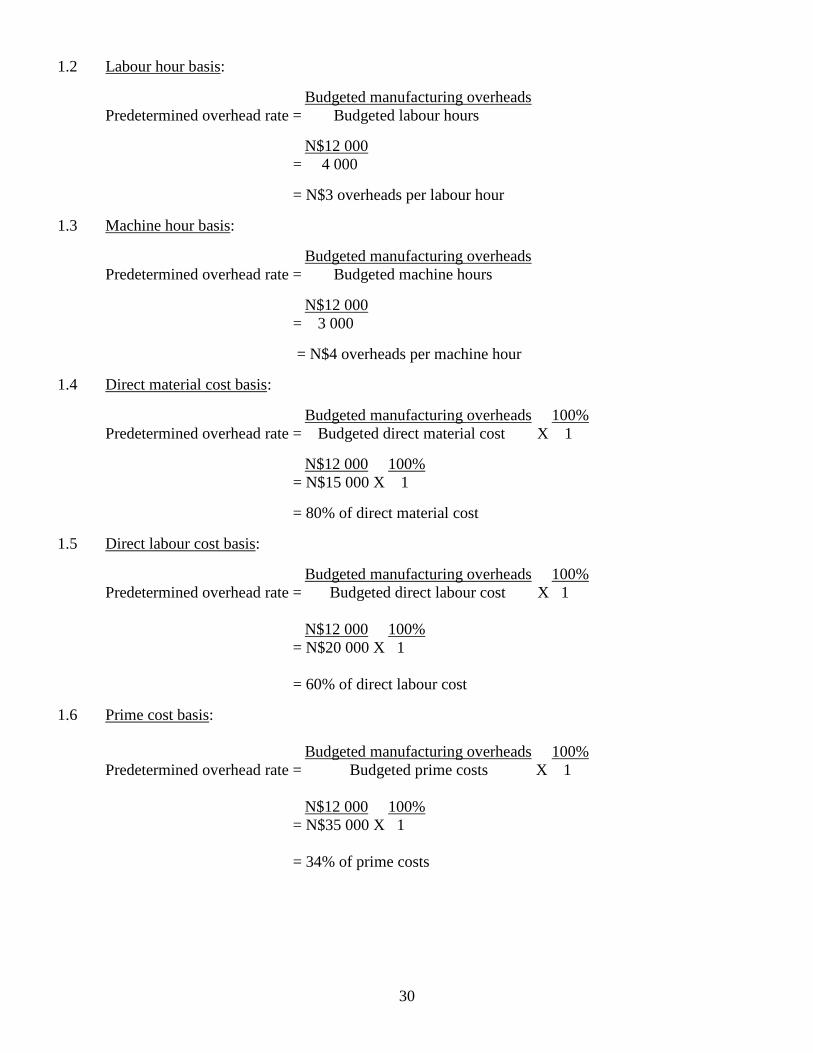

1.2 Labour hour basis: Budgeted manufacturing overheads

Predetermined overhead rate = Budgeted labour hours N$12 000 = 4 000 = N$3 overheads per labour hour 1.3 Machine hour basis: Budgeted manufacturing overheads

Predetermined overhead rate = Budgeted machine hours N$12 000 = 3 000 = N$4 overheads per machine hour 1.4 Direct material cost basis: Budgeted manufacturing overheads 100%

Predetermined overhead rate = Budgeted direct material cost X 1 N$12 000 100% = N$15 000 X 1 = 80% of direct material cost 1.5 Direct labour cost basis: Budgeted manufacturing overheads 100%

Predetermined overhead rate = Budgeted direct labour cost X 1 N$12 000 100% = N$20 000 X 1 = 60% of direct labour cost 1.6 Prime cost basis: Budgeted manufacturing overheads 100%

Predetermined overhead rate = Budgeted prime costs X 1 N$12 000 100% = N$35 000 X 1 = 34% of prime costs

31

Activity 1 Mouers Ltd supplied the following budgeted information for 2010: Manufacturing overheads N$60 000 Direct labour hours 8 000 hours Direct wages N$16 000 Direct material used N$30 000 Machine hours 12 000 hours Units produced 450 units Required: Use the above data to calculate six (6) different manufacturing overhead absorption rates. 2.3 Using the calculated overhead absorption rate (oar) Each firm must decide which rate will be the most appropriate to be used. It often happens that different departments (cost centres) use different overhead rates. For example, the machining department would use machine hours as the most appropriate rate whereas a department where labour is done manually would use direct labour hours or direct labour cost as the most appropriate rate for the absorption of its overheads. In example1 and activity 1 above we assumed that all the units produced were identical. However, in practical situations products are often dissimilar. Thus, although they use the same facilities, they may require different production processes or occupy the facilities for varying lengths of time. In such situations overhead absorption becomes of greater importance because the overheads absorbed into the product or job should, as far as possible reflect the load that the product or job places upon the production facilities. Example 2 Refer to example 1 above. Assume that it has been decided that direct labour hours is the most appropriate rate to use in order to absorb the manufacturing overheads in this enterprise. A cost unit X has been produced and the following details were recorded:

Cost unit X Direct material used N$100 Direct wages N$130 Direct labour hours 45 hours Machine hours 13 hours Required: Calculate the total cost of cost unit X. Solution to Example 2 Total cost of cost unit X N$ Direct material 100 Direct wages 130 Manufacturing overheads: 45 labour hours at N$3 per direct labour hour 135 365

32

Example 3 Azar Ltd supplied the following budgeted figures for 2010:

Manufacturing costs: Direct material Direct labour Indirect labour Electricity Rates and taxes Machine maintenance and repairs Indirect material Factory heat and light Depreciation on factory machinery Insurance on factory buildings Direct labour hours Machine hours Production units

N$ 200 000 600 000 100 000 140 000 22 800 115 200 6 000 34 000 130 000 172 000 N$1 520 000 200 000 90 000 100 000

Required: 3.1 Calculate three different overhead absorption rates based on each of the following: 3.1.1 Direct labour hours 3.1.2 Machine hours 3.1.3 Direct labour cost 3.2 During June 2010, Job Card no 146 showed the following particulars:

Direct material used N$4 000 Direct labour N$2 000 (800 hours) Machine hours 380 Calculate the total cost of Job No 146, using each of the overhead absorption rates calculated in 3.1 above.

Solution to Example 3 3.1.1 Direct labour hour basis: Budgeted manufacturing overheads

Predetermined overhead rate = Budgeted direct labour hours N$720 000 = 200 000 = N$3,60 per direct labour hour 3.1.2 Machine hour basis: Budgeted manufacturing overheads

Predetermined overhead rate = Budgeted machine hours

33

N$720 000 = 90 000 = N$8 per machine hour 3.1.3 Direct labour cost basis: Budgeted manufacturing overheads 100%

Predetermined overhead rate = Budgeted direct labour cost X 1 N$720 000 100% = N$600 000 X 1 = 120% of direct labour cost 3.2 Calculation of total cost of Job No 146:

Cost item

Labour hour basis

Machine hour basis

Labour cost basis

N$ N$ N$ Direct material Direct labour Manufacturing overheads: 800 labour hours x N$3,60 380 machine hours x N$8 N$2 000 labour cost x 120%

4 000 2 000 2 880

4 000 2 000 3 040

4 000 2 000 2 400

Total cost of Job No 146 8 880 9 040 8 400 Activity 2 The production manager of Poly Manufacturing Company Ltd has compiled the following budgeted figures for Cost Centre no 17 for 2010: Labour hours 1 400 hours Direct wages N$3 600 Direct material N$7 500 Machine hours 2 850 hours Production units 535 units Manufacturing overheads N$12 900 Required: 2.1 Calculate six (6) different manufacturing overhead absorption rates for Cost Centre no 17 to be used

during 2010. 2.2 During April 2010 the following details were recorded in the production of unit no 137: Direct material used N$16,50 Direct wages N$17,50 Direct labour hours 5½ hours Machine hours 8½ hours

Calculate the total cost of unit no 137, using each of the following overhead absorption rates calculated in 2.1 above:

34

1.2.1 direct labour hours 1.2.2 machine hours 1.2.3 direct material cost 1.2.4 direct labour cost 1.2.5 prime cost

2.4 Summary In this unit so far we have assumed that there is a linear relationship between the amount of manufacturing overheads and the production volume, i.e., we have assumed that the manufacturing overheads vary in direct proportion to production volume. For example, we assumed that if the number of units, labour hours, machine hours, etc. vary, the manufacturing overheads will vary in the same proportion. The approach to product costing outlined in the paragraphs above is what may be termed the traditional approach. It is widely used and must be thoroughly understood by students. However, we must appreciate that traditional product costing systems were designed decades ago, when most companies manufactured only a narrow range of products and direct labour and materials were the dominant factory costs. Overhead costs were relatively small, and if overheads were inappropriately allocated, the distortions arising as a result would be insignificant. Today companies produce a wide range of products; direct labour represents only a small fraction of total costs, and overhead costs are of considerable importance. As will be indicated in the rest of this chapter, the traditional approach to the allocation of manufacturing overheads has been based on a wrong assumption and for this reason the unit costs of products have been incorrectly calculated. Activity-based costing (ABC) is a more recent approach to product costing. ABC is an attempt to reflect more accurately the cost of products by acknowledging the fact that costs are determined by specific activities rather than production volume. 3. The emergence of activity-based costing systems It is important to note that many overhead costs consist of, and are caused by activities such as material handling, material procurement, the performing of machine set-ups, production planning and scheduling, product inspection, dispatching, etc. It is therefore incorrect to apportion all overhead costs according to one overhead rate only. Consider the following example (Example 4) where we assume that total overheads consist of two types of cost, each type driven by a specific activity, also called a cost driver. Example 4 Walton Manufacturers Ltd started business on 1 January 2010. Ever since the company has been using a single overhead rate based on machine hours. Patricia Mapedi, a newly appointed director, has noticed that Walton incurs relatively high overheads that relate to buying, receiving, storing and issuing of materials. She believes that the company could benefit if these overheads are absorbed on the basis of direct material cost. She has consequently recommended that two overhead rates be used, one based on material cost and the other on machine time. The total budgeted production overheads for 2010 have been analysed as follows: Material-related overheads N$ 48 000 Machine-related overheads N$130 000 Total overheads N$178 000 Other budgeted data for 2010 are as follows:

Cost of direct material N$160 000 Machine hours 20 000 hours

35

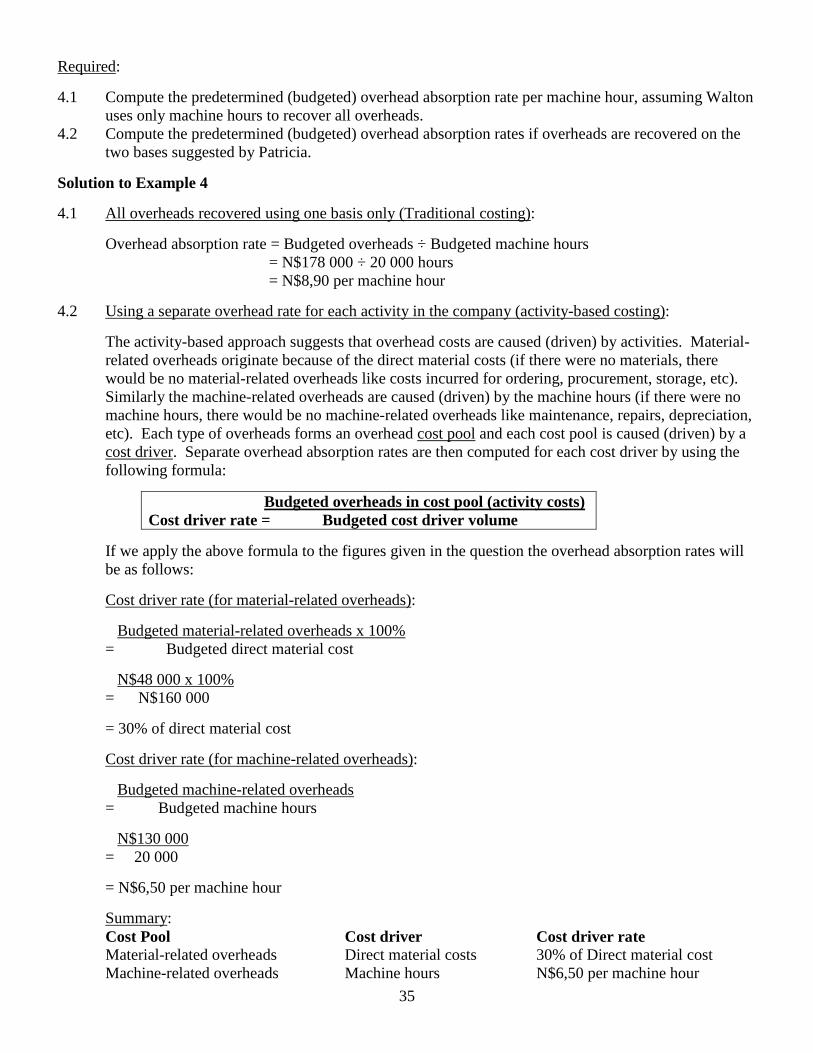

Required: 4.1 Compute the predetermined (budgeted) overhead absorption rate per machine hour, assuming Walton

uses only machine hours to recover all overheads. 4.2 Compute the predetermined (budgeted) overhead absorption rates if overheads are recovered on the

two bases suggested by Patricia. Solution to Example 4 4.1 All overheads recovered using one basis only (Traditional costing):

Overhead absorption rate = Budgeted overheads ÷ Budgeted machine hours = N$178 000 ÷ 20 000 hours = N$8,90 per machine hour

4.2 Using a separate overhead rate for each activity in the company (activity-based costing):

The activity-based approach suggests that overhead costs are caused (driven) by activities. Material-related overheads originate because of the direct material costs (if there were no materials, there would be no material-related overheads like costs incurred for ordering, procurement, storage, etc). Similarly the machine-related overheads are caused (driven) by the machine hours (if there were no machine hours, there would be no machine-related overheads like maintenance, repairs, depreciation, etc). Each type of overheads forms an overhead cost pool and each cost pool is caused (driven) by a cost driver. Separate overhead absorption rates are then computed for each cost driver by using the following formula:

Budgeted overheads in cost pool (activity costs) Cost driver rate = Budgeted cost driver volume

If we apply the above formula to the figures given in the question the overhead absorption rates will be as follows: Cost driver rate (for material-related overheads):

Budgeted material-related overheads x 100% = Budgeted direct material cost N$48 000 x 100%

= N$160 000 = 30% of direct material cost

Cost driver rate (for machine-related overheads):

Budgeted machine-related overheads = Budgeted machine hours N$130 000

= 20 000 = N$6,50 per machine hour Summary: Cost Pool Cost driver Cost driver rate

Material-related overheads Direct material costs 30% of Direct material cost Machine-related overheads Machine hours N$6,50 per machine hour

36

4. Activity-based cost systems

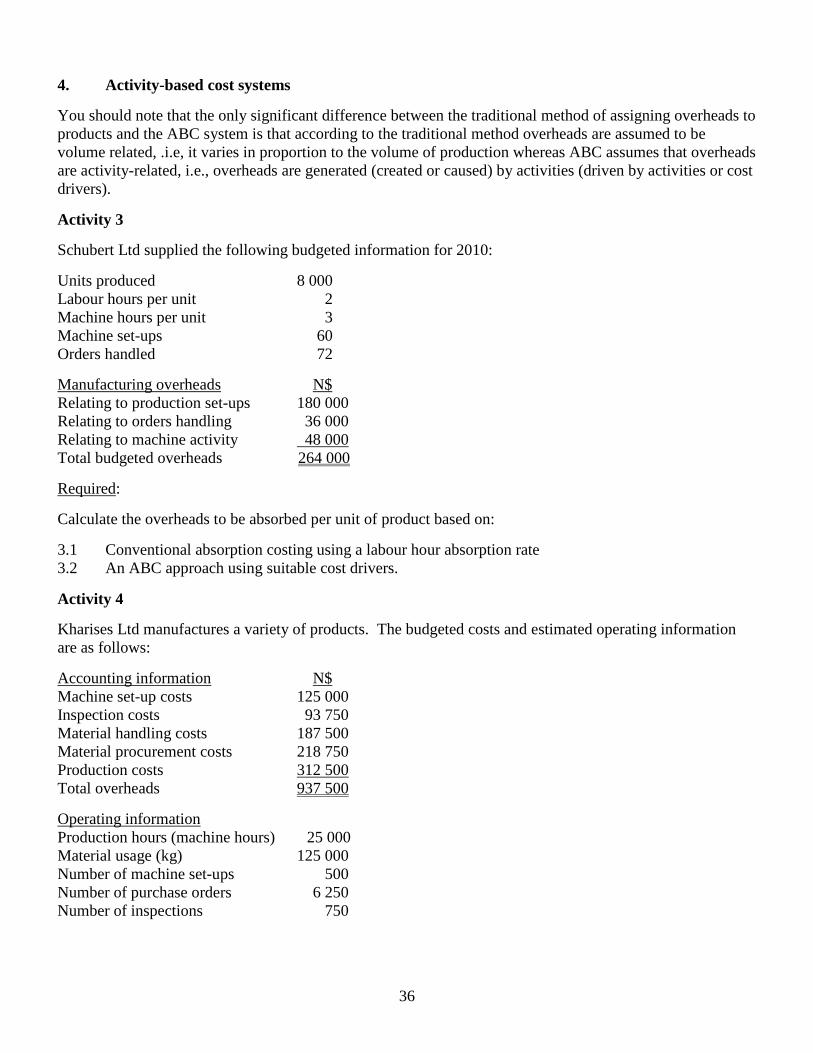

You should note that the only significant difference between the traditional method of assigning overheads to products and the ABC system is that according to the traditional method overheads are assumed to be volume related, .i.e, it varies in proportion to the volume of production whereas ABC assumes that overheads are activity-related, i.e., overheads are generated (created or caused) by activities (driven by activities or cost drivers). Activity 3 Schubert Ltd supplied the following budgeted information for 2010: Units produced 8 000 Labour hours per unit 2 Machine hours per unit 3 Machine set-ups 60 Orders handled 72 Manufacturing overheads N$ Relating to production set-ups 180 000 Relating to orders handling 36 000 Relating to machine activity 48 000 Total budgeted overheads 264 000 Required: Calculate the overheads to be absorbed per unit of product based on: 3.1 Conventional absorption costing using a labour hour absorption rate 3.2 An ABC approach using suitable cost drivers. Activity 4 Kharises Ltd manufactures a variety of products. The budgeted costs and estimated operating information are as follows: Accounting information N$ Machine set-up costs 125 000 Inspection costs 93 750 Material handling costs 187 500 Material procurement costs 218 750 Production costs 312 500 Total overheads 937 500 Operating information Production hours (machine hours) 25 000 Material usage (kg) 125 000 Number of machine set-ups 500 Number of purchase orders 6 250 Number of inspections 750

37

Required: 4.1 Calculate a single overhead absorption rate for the entire plant using machine hours as allocation

basis. 4.2 Calculate the cost centre rates which the company will use during the next financial year according to

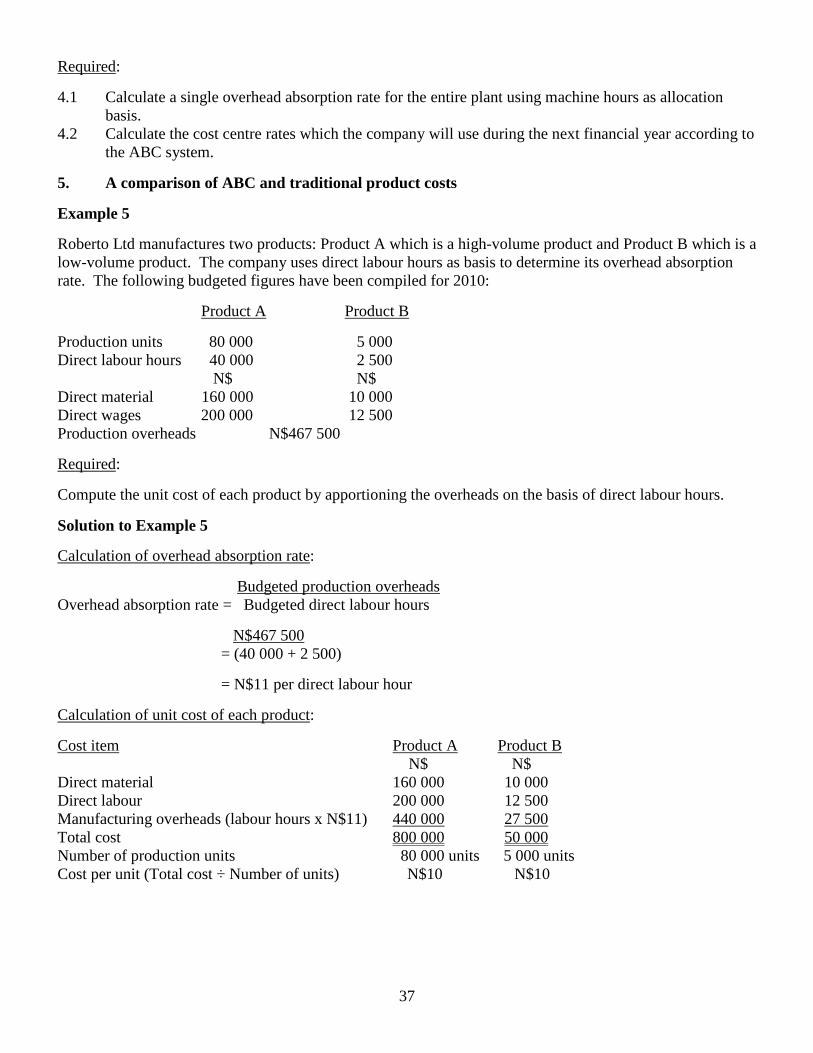

the ABC system. 5. A comparison of ABC and traditional product costs Example 5 Roberto Ltd manufactures two products: Product A which is a high-volume product and Product B which is a low-volume product. The company uses direct labour hours as basis to determine its overhead absorption rate. The following budgeted figures have been compiled for 2010:

Product A Product B Production units 80 000 5 000 Direct labour hours 40 000 2 500 N$ N$ Direct material 160 000 10 000 Direct wages 200 000 12 500 Production overheads N$467 500 Required: Compute the unit cost of each product by apportioning the overheads on the basis of direct labour hours. Solution to Example 5 Calculation of overhead absorption rate: Budgeted production overheads Overhead absorption rate = Budgeted direct labour hours

N$467 500 = (40 000 + 2 500)

= N$11 per direct labour hour Calculation of unit cost of each product: Cost item Product A Product B N$ N$ Direct material 160 000 10 000 Direct labour 200 000 12 500 Manufacturing overheads (labour hours x N$11) 440 000 27 500 Total cost 800 000 50 000 Number of production units 80 000 units 5 000 units Cost per unit (Total cost ÷ Number of units) N$10 N$10

38

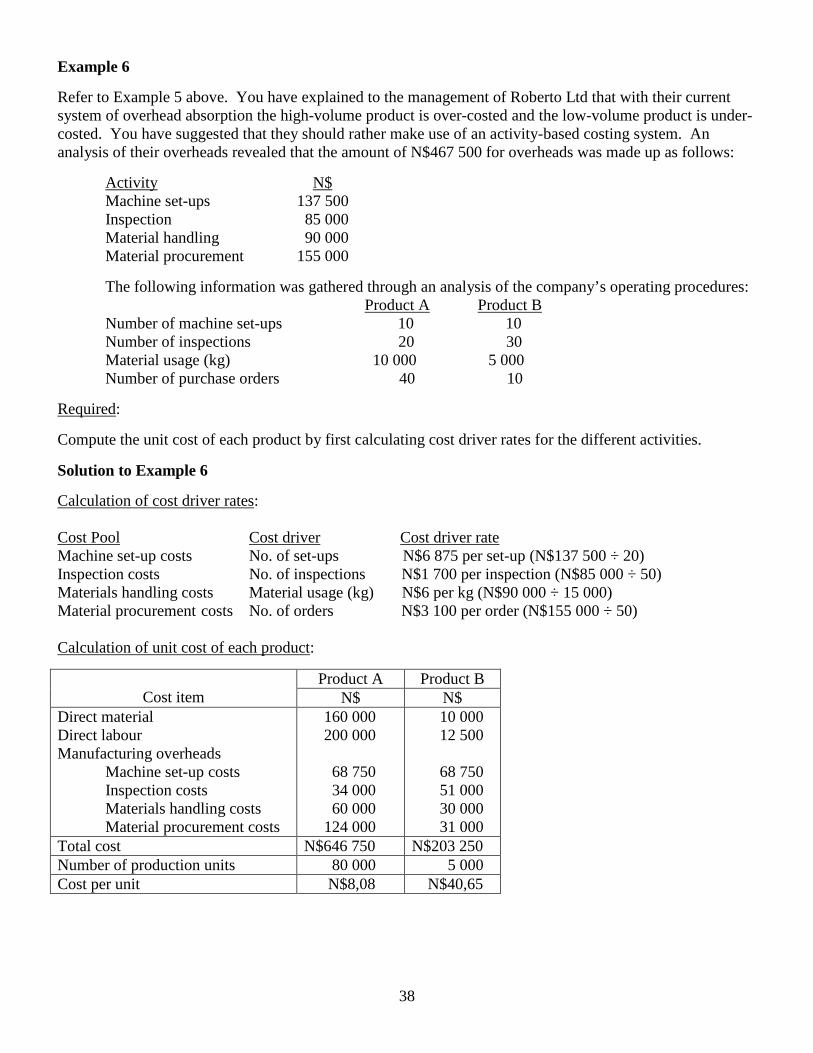

Example 6 Refer to Example 5 above. You have explained to the management of Roberto Ltd that with their current system of overhead absorption the high-volume product is over-costed and the low-volume product is under-costed. You have suggested that they should rather make use of an activity-based costing system. An analysis of their overheads revealed that the amount of N$467 500 for overheads was made up as follows:

Activity N$ Machine set-ups 137 500 Inspection 85 000 Material handling 90 000 Material procurement 155 000

The following information was gathered through an analysis of the company’s operating procedures: Product A Product B

Number of machine set-ups 10 10 Number of inspections 20 30 Material usage (kg) 10 000 5 000 Number of purchase orders 40 10 Required: Compute the unit cost of each product by first calculating cost driver rates for the different activities. Solution to Example 6

Calculation of cost driver rates: Cost Pool Cost driver Cost driver rate Machine set-up costs No. of set-ups N$6 875 per set-up (N$137 500 ÷ 20) Inspection costs No. of inspections N$1 700 per inspection (N$85 000 ÷ 50) Materials handling costs Material usage (kg) N$6 per kg (N$90 000 ÷ 15 000) Material procurement costs No. of orders N$3 100 per order (N$155 000 ÷ 50)

Calculation of unit cost of each product:

Cost item

Product A Product B N$ N$

Direct material Direct labour Manufacturing overheads

Machine set-up costs Inspection costs Materials handling costs

Material procurement costs

160 000 200 000 68 750 34 000 60 000 124 000

10 000 12 500 68 750 51 000 30 000 31 000

Total cost N$646 750 N$203 250 Number of production units 80 000 5 000 Cost per unit N$8,08 N$40,65

39

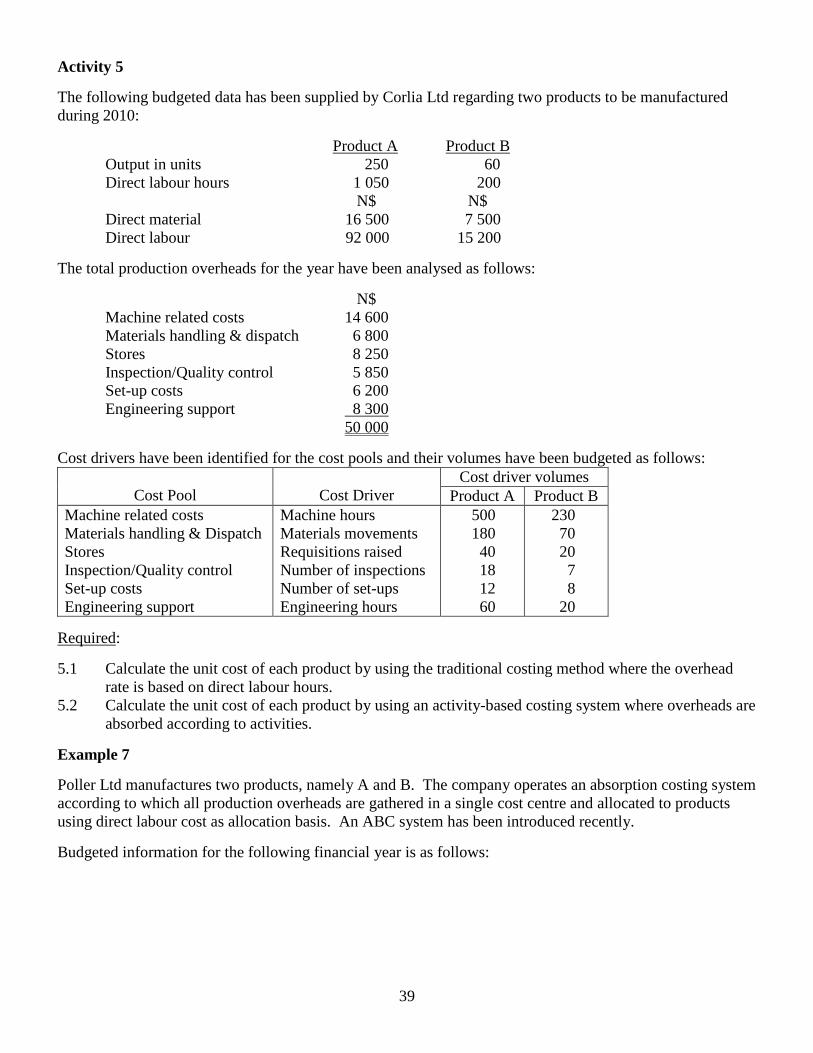

Activity 5 The following budgeted data has been supplied by Corlia Ltd regarding two products to be manufactured during 2010: Product A Product B

Output in units 250 60 Direct labour hours 1 050 200 N$ N$ Direct material 16 500 7 500 Direct labour 92 000 15 200

The total production overheads for the year have been analysed as follows: N$ Machine related costs 14 600 Materials handling & dispatch 6 800

Stores 8 250 Inspection/Quality control 5 850 Set-up costs 6 200 Engineering support 8 300 50 000

Cost drivers have been identified for the cost pools and their volumes have been budgeted as follows:

Cost Pool

Cost Driver Cost driver volumes

Product A Product B Machine related costs Materials handling & Dispatch Stores Inspection/Quality control Set-up costs Engineering support

Machine hours Materials movements Requisitions raised Number of inspections Number of set-ups Engineering hours

500 180 40 18 12 60

230 70 20 7 8 20

Required: 5.1 Calculate the unit cost of each product by using the traditional costing method where the overhead

rate is based on direct labour hours. 5.2 Calculate the unit cost of each product by using an activity-based costing system where overheads are

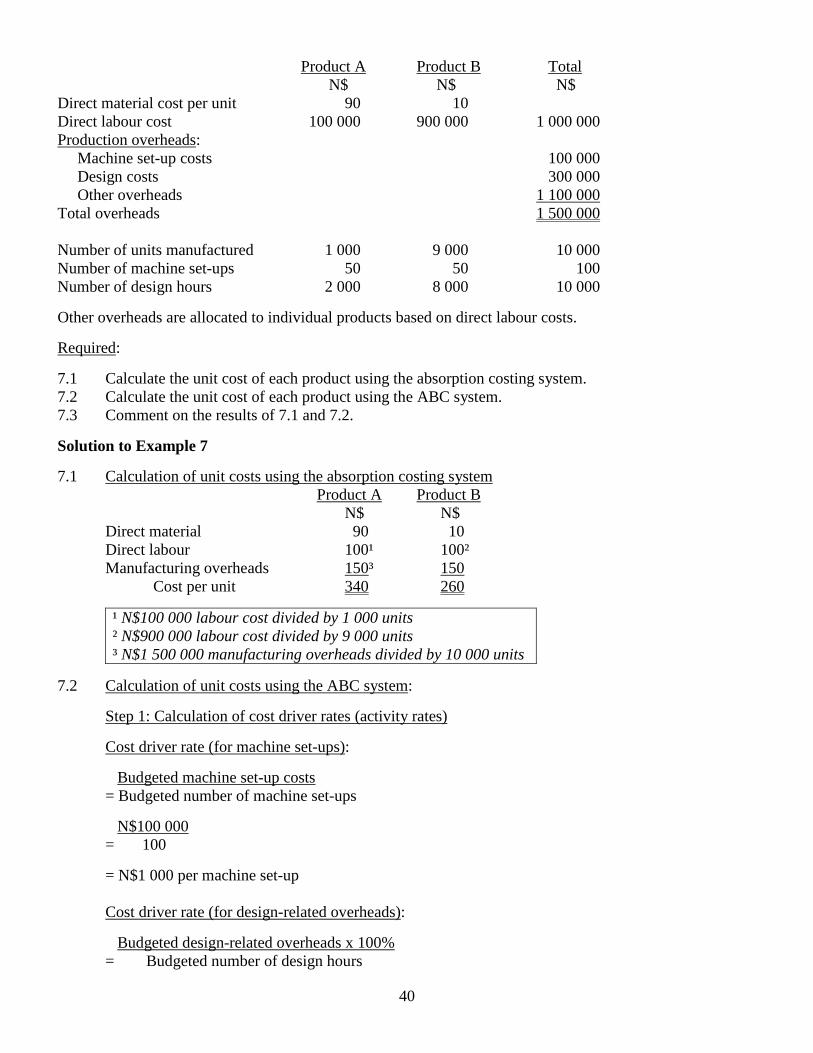

absorbed according to activities. Example 7 Poller Ltd manufactures two products, namely A and B. The company operates an absorption costing system according to which all production overheads are gathered in a single cost centre and allocated to products using direct labour cost as allocation basis. An ABC system has been introduced recently. Budgeted information for the following financial year is as follows:

40

Product A Product B Total N$ N$ N$ Direct material cost per unit 90 10 Direct labour cost 100 000 900 000 1 000 000 Production overheads: Machine set-up costs 100 000 Design costs 300 000 Other overheads 1 100 000 Total overheads 1 500 000 Number of units manufactured 1 000 9 000 10 000 Number of machine set-ups 50 50 100 Number of design hours 2 000 8 000 10 000 Other overheads are allocated to individual products based on direct labour costs. Required: 7.1 Calculate the unit cost of each product using the absorption costing system. 7.2 Calculate the unit cost of each product using the ABC system. 7.3 Comment on the results of 7.1 and 7.2. Solution to Example 7 7.1 Calculation of unit costs using the absorption costing system

Product A Product B N$ N$ Direct material 90 10 Direct labour 100¹ 100² Manufacturing overheads 150³ 150 Cost per unit 340 260

¹ N$100 000 labour cost divided by 1 000 units ² N$900 000 labour cost divided by 9 000 units ³ N$1 500 000 manufacturing overheads divided by 10 000 units

7.2 Calculation of unit costs using the ABC system:

Step 1: Calculation of cost driver rates (activity rates)

Cost driver rate (for machine set-ups):

Budgeted machine set-up costs = Budgeted number of machine set-ups N$100 000

= 100 = N$1 000 per machine set-up

Cost driver rate (for design-related overheads):

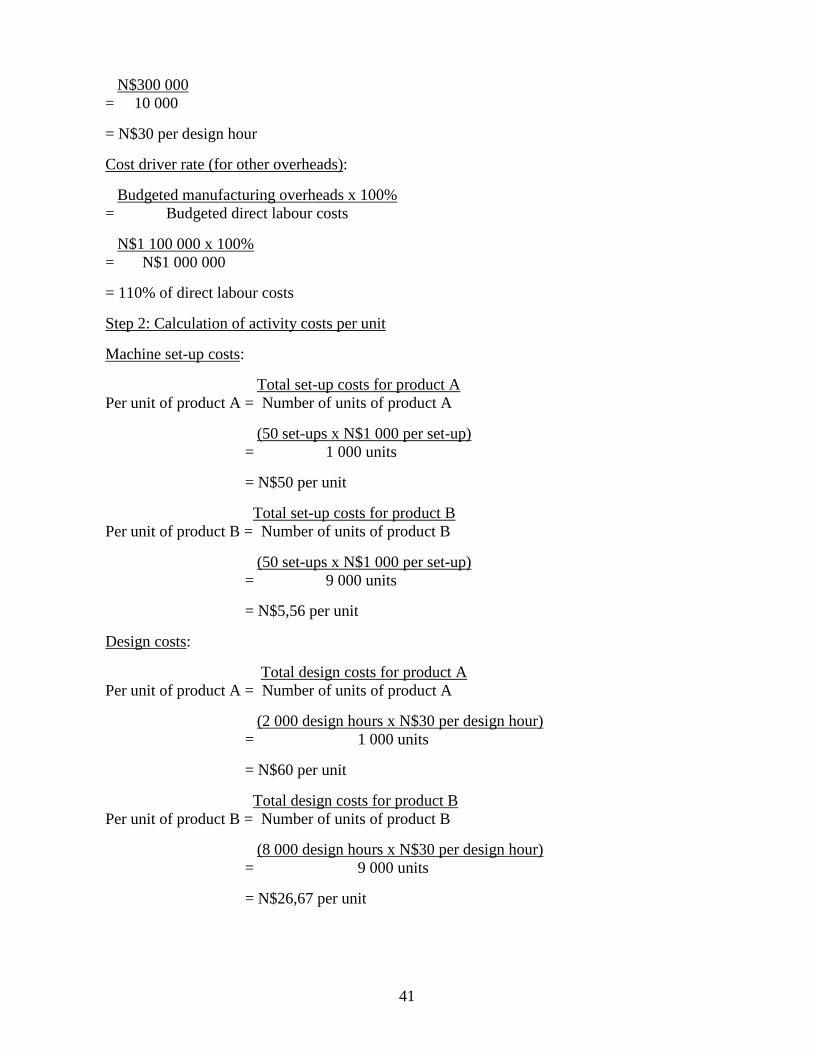

Budgeted design-related overheads x 100% = Budgeted number of design hours

41

N$300 000 = 10 000

= N$30 per design hour

Cost driver rate (for other overheads): Budgeted manufacturing overheads x 100% = Budgeted direct labour costs N$1 100 000 x 100% = N$1 000 000 = 110% of direct labour costs Step 2: Calculation of activity costs per unit Machine set-up costs: Total set-up costs for product A Per unit of product A = Number of units of product A (50 set-ups x N$1 000 per set-up) = 1 000 units = N$50 per unit Total set-up costs for product B Per unit of product B = Number of units of product B (50 set-ups x N$1 000 per set-up) = 9 000 units = N$5,56 per unit

Design costs: Total design costs for product A Per unit of product A = Number of units of product A (2 000 design hours x N$30 per design hour) = 1 000 units = N$60 per unit

Total design costs for product B Per unit of product B = Number of units of product B (8 000 design hours x N$30 per design hour) = 9 000 units = N$26,67 per unit

42

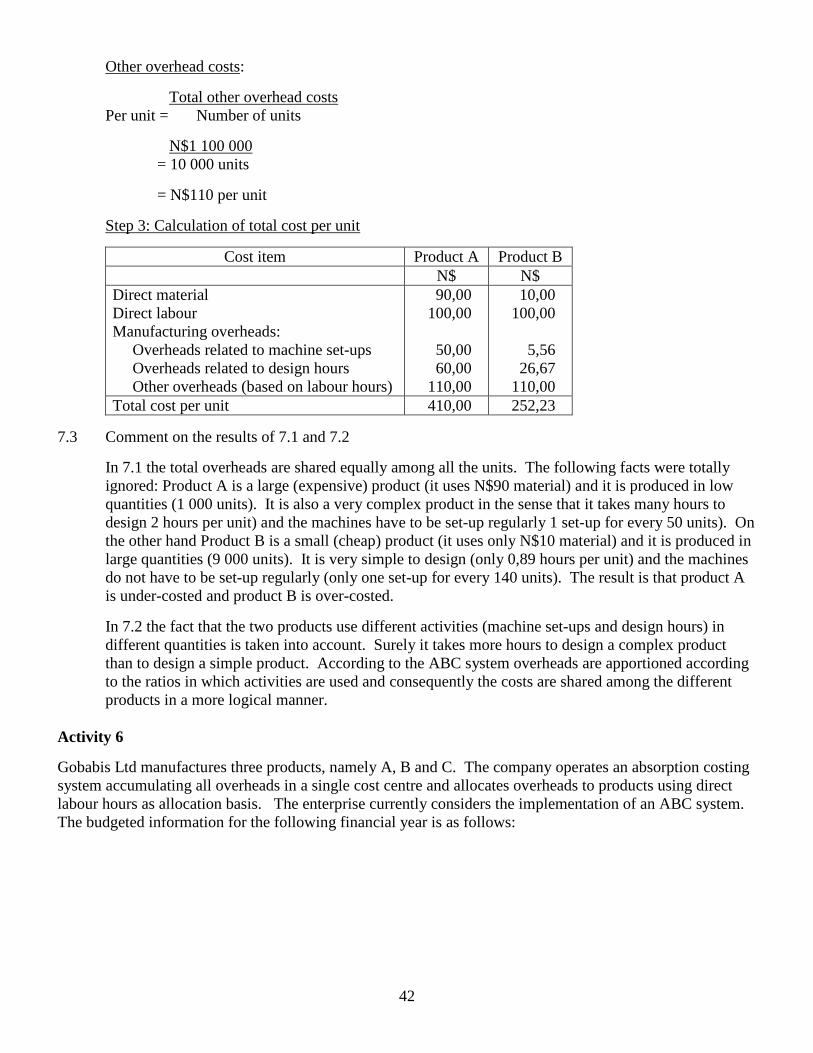

Other overhead costs:

Total other overhead costs Per unit = Number of units N$1 100 000 = 10 000 units = N$110 per unit

Step 3: Calculation of total cost per unit

Cost item Product A Product B N$ N$

Direct material Direct labour Manufacturing overheads: Overheads related to machine set-ups Overheads related to design hours Other overheads (based on labour hours)

90,00 100,00 50,00 60,00 110,00

10,00 100,00 5,56 26,67 110,00

Total cost per unit 410,00 252,23

7.3 Comment on the results of 7.1 and 7.2

In 7.1 the total overheads are shared equally among all the units. The following facts were totally ignored: Product A is a large (expensive) product (it uses N$90 material) and it is produced in low quantities (1 000 units). It is also a very complex product in the sense that it takes many hours to design 2 hours per unit) and the machines have to be set-up regularly 1 set-up for every 50 units). On the other hand Product B is a small (cheap) product (it uses only N$10 material) and it is produced in large quantities (9 000 units). It is very simple to design (only 0,89 hours per unit) and the machines do not have to be set-up regularly (only one set-up for every 140 units). The result is that product A is under-costed and product B is over-costed.

In 7.2 the fact that the two products use different activities (machine set-ups and design hours) in different quantities is taken into account. Surely it takes more hours to design a complex product than to design a simple product. According to the ABC system overheads are apportioned according to the ratios in which activities are used and consequently the costs are shared among the different products in a more logical manner.

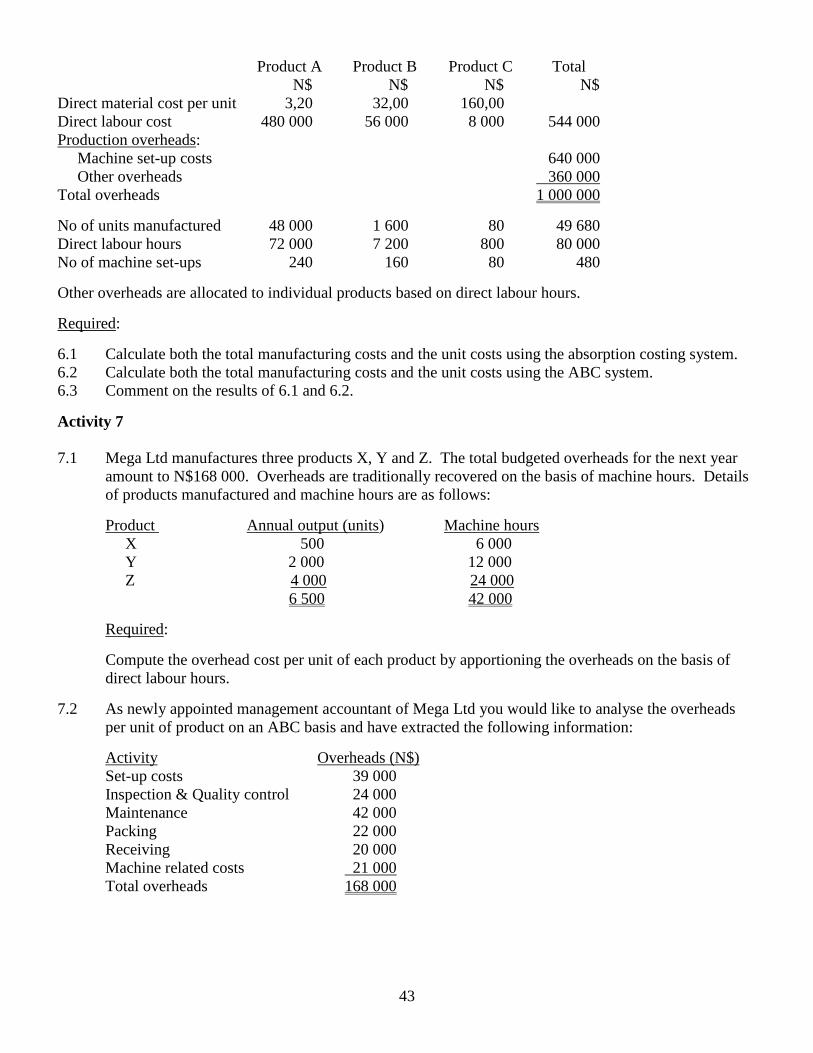

Activity 6 Gobabis Ltd manufactures three products, namely A, B and C. The company operates an absorption costing system accumulating all overheads in a single cost centre and allocates overheads to products using direct labour hours as allocation basis. The enterprise currently considers the implementation of an ABC system. The budgeted information for the following financial year is as follows:

43

Product A Product B Product C Total N$ N$ N$ N$ Direct material cost per unit 3,20 32,00 160,00 Direct labour cost 480 000 56 000 8 000 544 000 Production overheads: Machine set-up costs 640 000 Other overheads 360 000 Total overheads 1 000 000 No of units manufactured 48 000 1 600 80 49 680 Direct labour hours 72 000 7 200 800 80 000 No of machine set-ups 240 160 80 480 Other overheads are allocated to individual products based on direct labour hours. Required: 6.1 Calculate both the total manufacturing costs and the unit costs using the absorption costing system. 6.2 Calculate both the total manufacturing costs and the unit costs using the ABC system. 6.3 Comment on the results of 6.1 and 6.2. Activity 7 7.1 Mega Ltd manufactures three products X, Y and Z. The total budgeted overheads for the next year

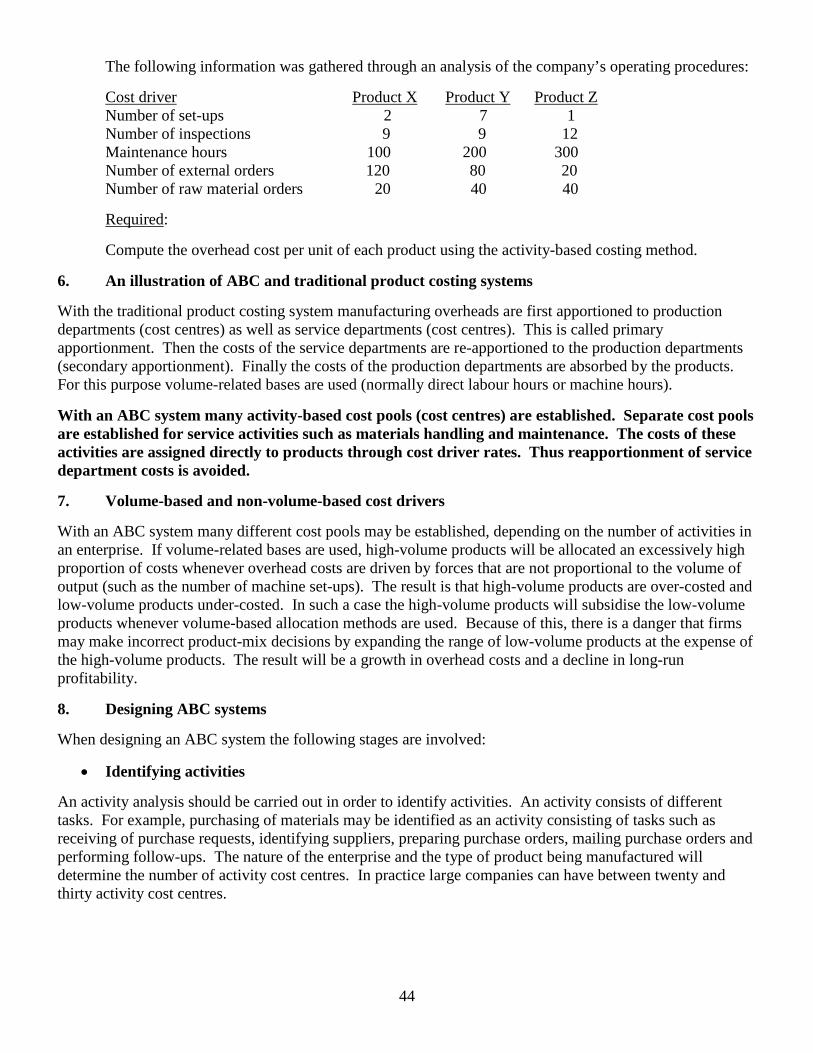

amount to N$168 000. Overheads are traditionally recovered on the basis of machine hours. Details of products manufactured and machine hours are as follows:

Product Annual output (units) Machine hours X 500 6 000 Y 2 000 12 000 Z 4 000 24 000 6 500 42 000

Required:

Compute the overhead cost per unit of each product by apportioning the overheads on the basis of direct labour hours.

7.2 As newly appointed management accountant of Mega Ltd you would like to analyse the overheads

per unit of product on an ABC basis and have extracted the following information:

Activity Overheads (N$) Set-up costs 39 000 Inspection & Quality control 24 000 Maintenance 42 000 Packing 22 000 Receiving 20 000 Machine related costs 21 000 Total overheads 168 000

44

The following information was gathered through an analysis of the company’s operating procedures: Cost driver Product X Product Y Product Z

Number of set-ups 2 7 1 Number of inspections 9 9 12 Maintenance hours 100 200 300 Number of external orders 120 80 20 Number of raw material orders 20 40 40

Required:

Compute the overhead cost per unit of each product using the activity-based costing method. 6. An illustration of ABC and traditional product costing systems With the traditional product costing system manufacturing overheads are first apportioned to production departments (cost centres) as well as service departments (cost centres). This is called primary apportionment. Then the costs of the service departments are re-apportioned to the production departments (secondary apportionment). Finally the costs of the production departments are absorbed by the products. For this purpose volume-related bases are used (normally direct labour hours or machine hours). With an ABC system many activity-based cost pools (cost centres) are established. Separate cost pools are established for service activities such as materials handling and maintenance. The costs of these activities are assigned directly to products through cost driver rates. Thus reapportionment of service department costs is avoided. 7. Volume-based and non-volume-based cost drivers With an ABC system many different cost pools may be established, depending on the number of activities in an enterprise. If volume-related bases are used, high-volume products will be allocated an excessively high proportion of costs whenever overhead costs are driven by forces that are not proportional to the volume of output (such as the number of machine set-ups). The result is that high-volume products are over-costed and low-volume products under-costed. In such a case the high-volume products will subsidise the low-volume products whenever volume-based allocation methods are used. Because of this, there is a danger that firms may make incorrect product-mix decisions by expanding the range of low-volume products at the expense of the high-volume products. The result will be a growth in overhead costs and a decline in long-run profitability. 8. Designing ABC systems When designing an ABC system the following stages are involved:

• Identifying activities An activity analysis should be carried out in order to identify activities. An activity consists of different tasks. For example, purchasing of materials may be identified as an activity consisting of tasks such as receiving of purchase requests, identifying suppliers, preparing purchase orders, mailing purchase orders and performing follow-ups. The nature of the enterprise and the type of product being manufactured will determine the number of activity cost centres. In practice large companies can have between twenty and thirty activity cost centres.

45

• Assigning costs to activity cost centres Costs are generated (created) in each activity cost centre. For example, if maintenance has been identified as an activity cost centre, all costs related to maintenance will be assigned to that activity. This may include costs such as wages, depreciation on tools, lubricating materials, cleaning materials, etc. Selecting appropriate cost drivers In order to assign the costs attached to each activity cost centre to products, a cost driver must be selected for each activity centre. A cost driver is that factor (element) that causes (drives) the costs. For example, the number of machine set-ups will be a cost driver for the activity cost centre: machine set-ups because the number of machine set-ups will determine the amount of the costs (the more the number of set-ups, the more the costs will be). A cost driver should be easily measurable; the data should be relatively easy to obtain and be identifiable with products.

• Assigning the cost of the activities to products The final stage involves applying the cost driver rates to the different products by multiplying the cost centre rate by the cost driver volume. It is therefore obvious that the cost driver must be measurable in a way that enables it to be identified with individual products. 9. Activity hierarchies A useful way to think about activities and how to combine them is to organize them into four general levels: these are unit-level activities, batch-related activities, product-sustaining activities, and facility-sustaining activities. 9.1 Unit-level activities Unit-level activities are performed each time a unit of the product or service is produced. Costs in this category vary in proportion to the number of units produced, for example direct material costs. 9.2 Batch-level activities Batch-level activities are performed each time a batch of goods is produced. The cost of these activities varies with the number of batches made but is fixed for all units within the batch. For example, for each batch the machine must be set up. The set-up costs vary in proportion to the number of set-ups, but once the machine has been set up, the cost is independent of the number of units produced. 9.3 Product-sustaining activities Product-sustaining activities are performed to support the different products manufactured, for example the development of a new production process or product testing procedures. The cost of these activities is independent of the number of units or batches produced. 9.4 Facility-sustaining activities Customer-level activities relate to specific customers and include activities such as sales calls, catalogue mailing and general technical support that are not tied to any specific product. Activity 8 Nekoto Ltd manufactures products “Nek” and “Oto”. Presently the company is operating a traditional absorption costing system based on production volume (number of production units) to allocate overheads to products. The budgeted costing information for 2010 is as follows:

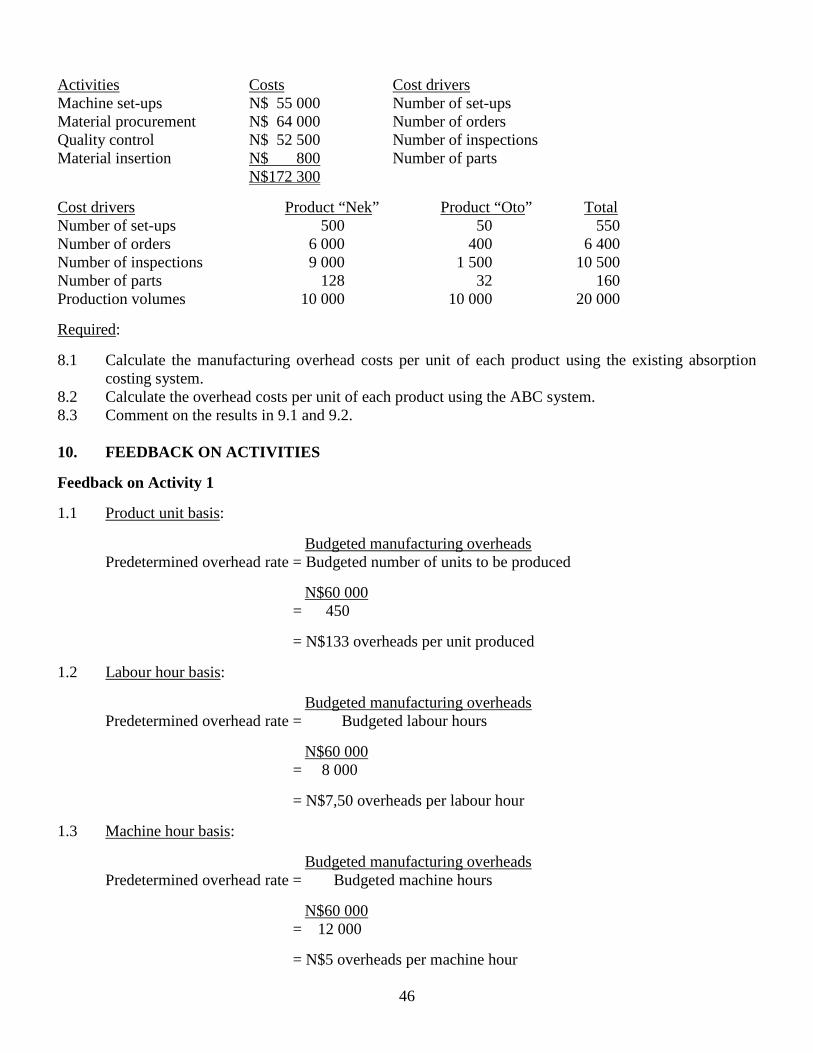

46

Activities Costs Cost drivers Machine set-ups N$ 55 000 Number of set-ups Material procurement N$ 64 000 Number of orders Quality control N$ 52 500 Number of inspections Material insertion N$ 800 Number of parts N$172 300 Cost drivers Product “Nek” Product “Oto” Total Number of set-ups 500 50 550 Number of orders 6 000 400 6 400 Number of inspections 9 000 1 500 10 500 Number of parts 128 32 160 Production volumes 10 000 10 000 20 000 Required: 8.1 Calculate the manufacturing overhead costs per unit of each product using the existing absorption

costing system. 8.2 Calculate the overhead costs per unit of each product using the ABC system. 8.3 Comment on the results in 9.1 and 9.2. 10. FEEDBACK ON ACTIVITIES Feedback on Activity 1 1.1 Product unit basis: Budgeted manufacturing overheads

Predetermined overhead rate = Budgeted number of units to be produced N$60 000 = 450 = N$133 overheads per unit produced 1.2 Labour hour basis: Budgeted manufacturing overheads

Predetermined overhead rate = Budgeted labour hours N$60 000 = 8 000 = N$7,50 overheads per labour hour 1.3 Machine hour basis: Budgeted manufacturing overheads

Predetermined overhead rate = Budgeted machine hours N$60 000 = 12 000 = N$5 overheads per machine hour

47

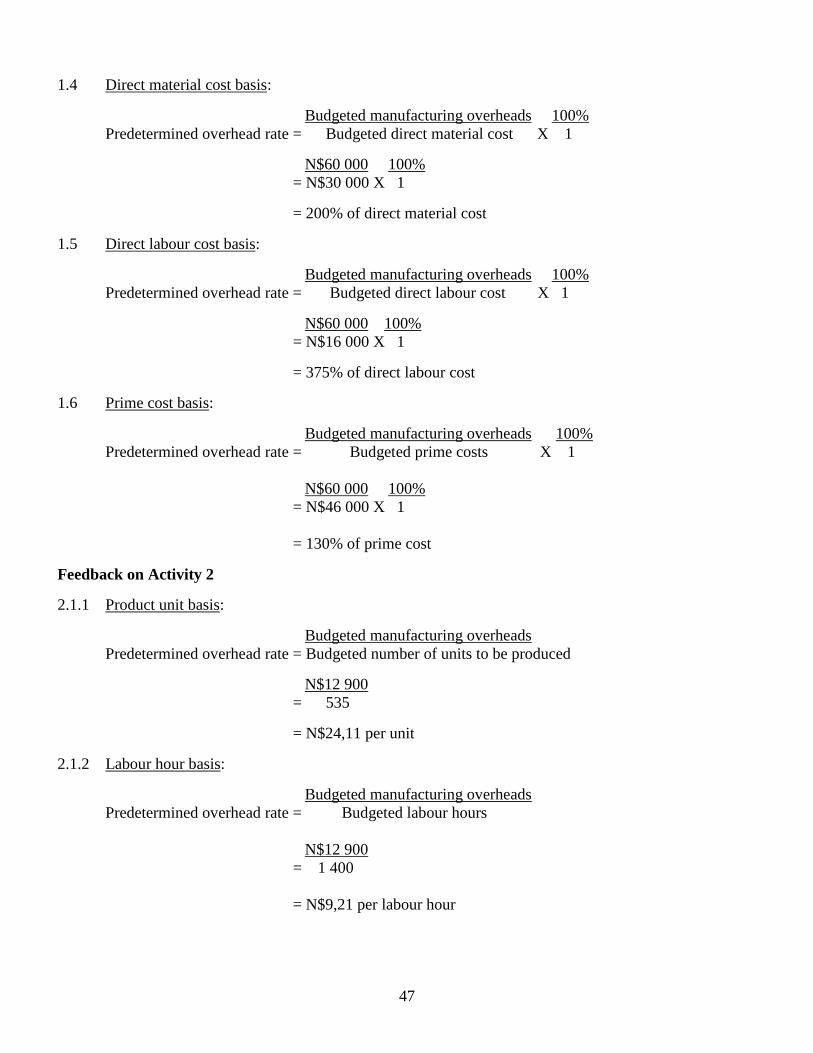

1.4 Direct material cost basis: Budgeted manufacturing overheads 100%

Predetermined overhead rate = Budgeted direct material cost X 1 N$60 000 100% = N$30 000 X 1 = 200% of direct material cost 1.5 Direct labour cost basis: Budgeted manufacturing overheads 100%

Predetermined overhead rate = Budgeted direct labour cost X 1 N$60 000 100% = N$16 000 X 1 = 375% of direct labour cost 1.6 Prime cost basis: Budgeted manufacturing overheads 100%

Predetermined overhead rate = Budgeted prime costs X 1 N$60 000 100% = N$46 000 X 1 = 130% of prime cost Feedback on Activity 2 2.1.1 Product unit basis: Budgeted manufacturing overheads

Predetermined overhead rate = Budgeted number of units to be produced N$12 900 = 535 = N$24,11 per unit 2.1.2 Labour hour basis: Budgeted manufacturing overheads

Predetermined overhead rate = Budgeted labour hours N$12 900 = 1 400 = N$9,21 per labour hour

48

2.1.3 Machine hour basis: Budgeted manufacturing overheads

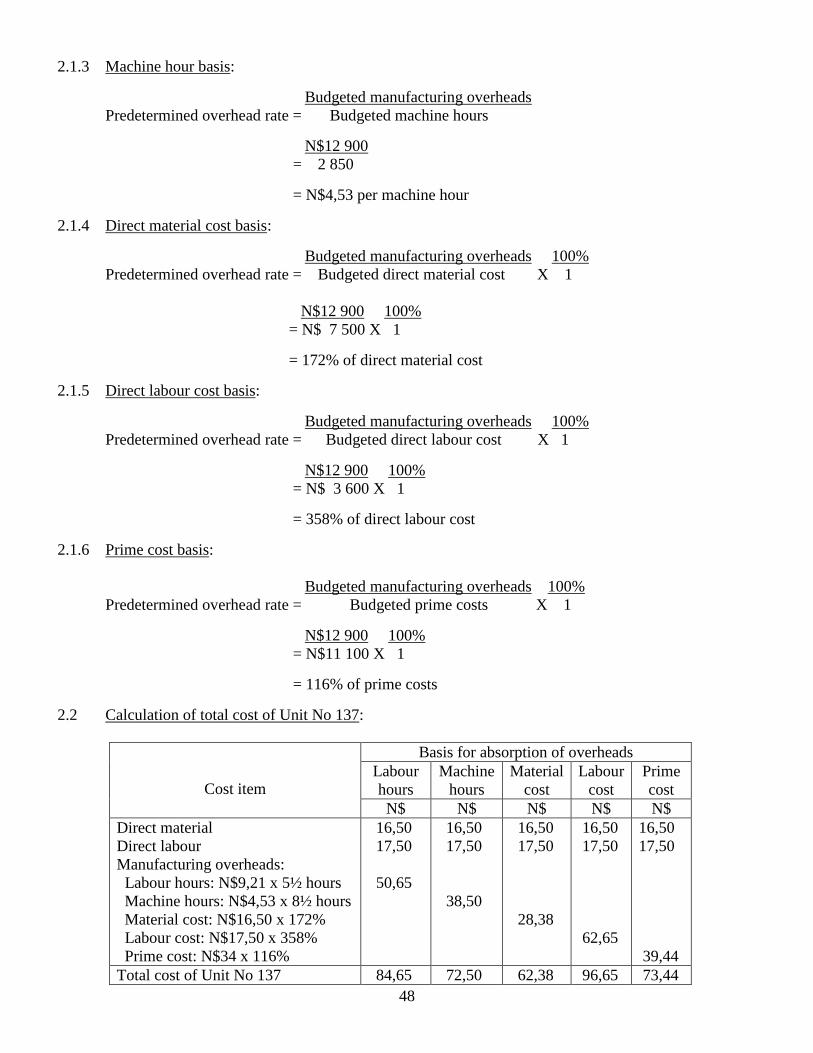

Predetermined overhead rate = Budgeted machine hours N$12 900 = 2 850 = N$4,53 per machine hour 2.1.4 Direct material cost basis: Budgeted manufacturing overheads 100%

Predetermined overhead rate = Budgeted direct material cost X 1 N$12 900 100% = N$ 7 500 X 1 = 172% of direct material cost 2.1.5 Direct labour cost basis: Budgeted manufacturing overheads 100%

Predetermined overhead rate = Budgeted direct labour cost X 1 N$12 900 100% = N$ 3 600 X 1 = 358% of direct labour cost 2.1.6 Prime cost basis: Budgeted manufacturing overheads 100%

Predetermined overhead rate = Budgeted prime costs X 1 N$12 900 100% = N$11 100 X 1 = 116% of prime costs 2.2 Calculation of total cost of Unit No 137:

Cost item

Basis for absorption of overheads Labour hours

Machine hours

Material cost

Labour cost

Prime cost

N$ N$ N$ N$ N$ Direct material Direct labour Manufacturing overheads: Labour hours: N$9,21 x 5½ hours Machine hours: N$4,53 x 8½ hours Material cost: N$16,50 x 172% Labour cost: N$17,50 x 358% Prime cost: N$34 x 116%

16,50 17,50 50,65

16,50 17,50 38,50

16,50 17,50 28,38

16,50 17,50 62,65

16,50 17,50 39,44

Total cost of Unit No 137 84,65 72,50 62,38 96,65 73,44

49

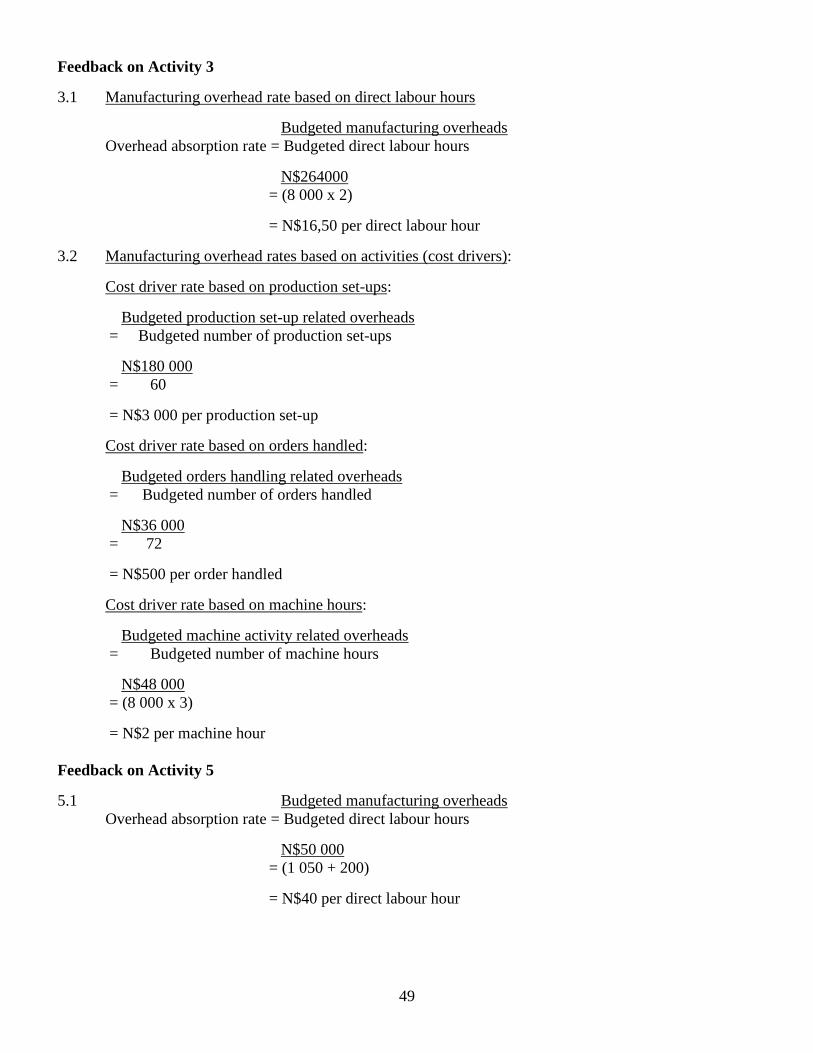

Feedback on Activity 3 3.1 Manufacturing overhead rate based on direct labour hours

Budgeted manufacturing overheads Overhead absorption rate = Budgeted direct labour hours N$264000 = (8 000 x 2) = N$16,50 per direct labour hour

3.2 Manufacturing overhead rates based on activities (cost drivers):

Cost driver rate based on production set-ups:

Budgeted production set-up related overheads = Budgeted number of production set-ups N$180 000 = 60 = N$3 000 per production set-up Cost driver rate based on orders handled:

Budgeted orders handling related overheads = Budgeted number of orders handled N$36 000 = 72 = N$500 per order handled Cost driver rate based on machine hours:

Budgeted machine activity related overheads = Budgeted number of machine hours N$48 000 = (8 000 x 3) = N$2 per machine hour

Feedback on Activity 5 5.1 Budgeted manufacturing overheads

Overhead absorption rate = Budgeted direct labour hours N$50 000 = (1 050 + 200) = N$40 per direct labour hour

50

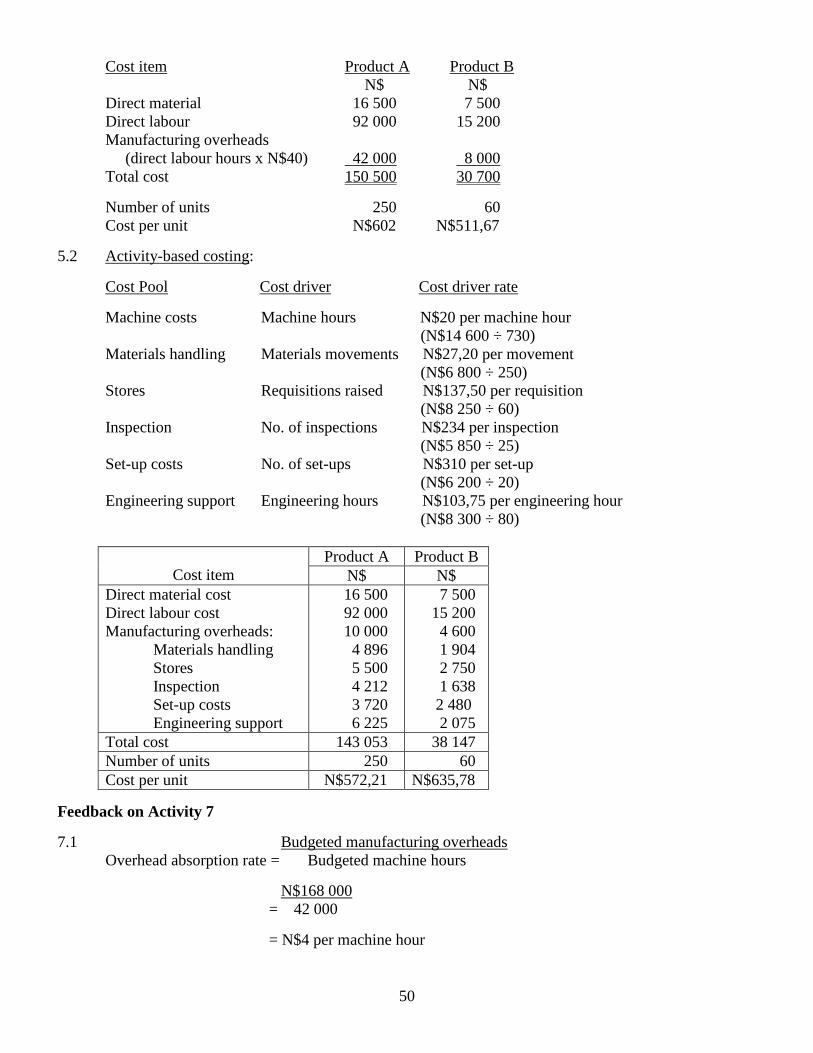

Cost item Product A Product B N$ N$ Direct material 16 500 7 500 Direct labour 92 000 15 200 Manufacturing overheads (direct labour hours x N$40) 42 000 8 000 Total cost 150 500 30 700 Number of units 250 60 Cost per unit N$602 N$511,67

5.2 Activity-based costing: Cost Pool Cost driver Cost driver rate Machine costs Machine hours N$20 per machine hour (N$14 600 ÷ 730) Materials handling Materials movements N$27,20 per movement (N$6 800 ÷ 250) Stores Requisitions raised N$137,50 per requisition (N$8 250 ÷ 60) Inspection No. of inspections N$234 per inspection (N$5 850 ÷ 25) Set-up costs No. of set-ups N$310 per set-up (N$6 200 ÷ 20) Engineering support Engineering hours N$103,75 per engineering hour (N$8 300 ÷ 80)

Cost item

Product A Product B N$ N$

Direct material cost Direct labour cost Manufacturing overheads:

Materials handling Stores Inspection Set-up costs

Engineering support

16 500 92 000 10 000 4 896 5 500 4 212 3 720 6 225

7 500 15 200 4 600 1 904 2 750 1 638 2 480 2 075

Total cost 143 053 38 147 Number of units 250 60 Cost per unit N$572,21 N$635,78

Feedback on Activity 7 7.1 Budgeted manufacturing overheads

Overhead absorption rate = Budgeted machine hours N$168 000 = 42 000 = N$4 per machine hour

51

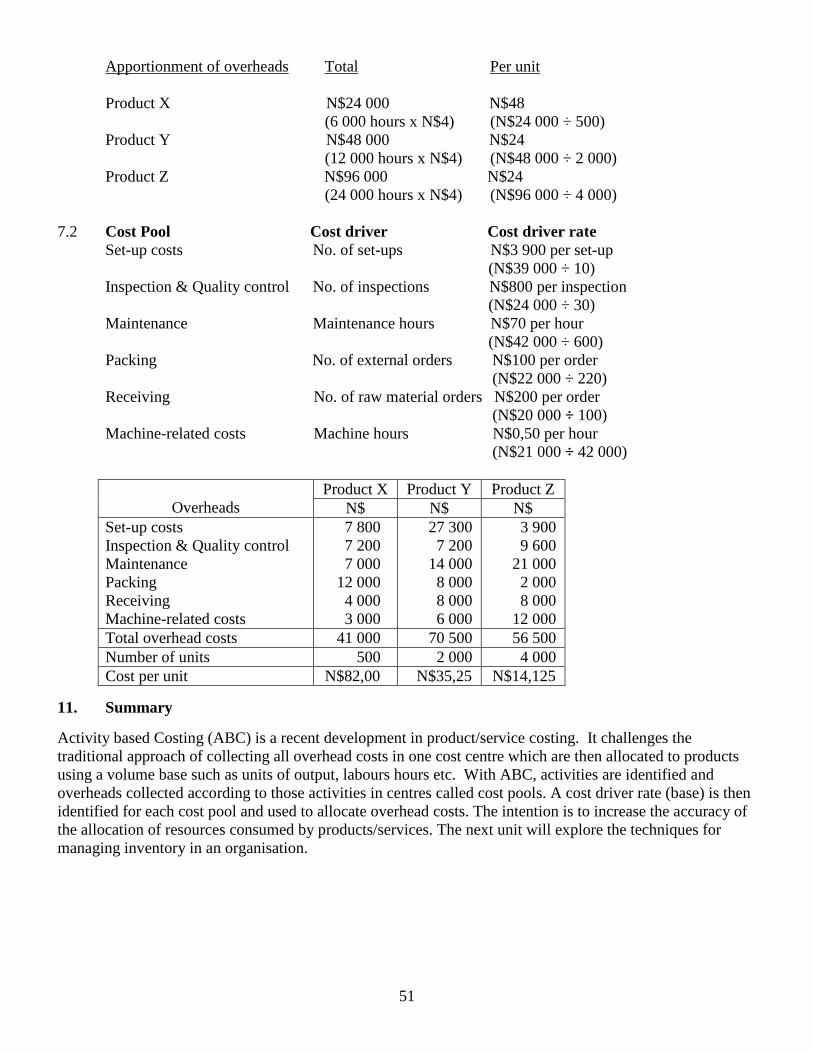

Apportionment of overheads Total Per unit Product X N$24 000 N$48 (6 000 hours x N$4) (N$24 000 ÷ 500) Product Y N$48 000 N$24 (12 000 hours x N$4) (N$48 000 ÷ 2 000) Product Z N$96 000 N$24 (24 000 hours x N$4) (N$96 000 ÷ 4 000)

7.2 Cost Pool Cost driver Cost driver rate Set-up costs No. of set-ups N$3 900 per set-up (N$39 000 ÷ 10) Inspection & Quality control No. of inspections N$800 per inspection (N$24 000 ÷ 30) Maintenance Maintenance hours N$70 per hour (N$42 000 ÷ 600) Packing No. of external orders N$100 per order (N$22 000 ÷ 220) Receiving No. of raw material orders N$200 per order

(N$20 000 ÷ 100) Machine-related costs Machine hours N$0,50 per hour

(N$21 000 ÷ 42 000)

Overheads

Product X Product Y Product Z N$ N$ N$

Set-up costs Inspection & Quality control Maintenance Packing Receiving Machine-related costs

7 800 7 200 7 000 12 000 4 000 3 000

27 300 7 200 14 000 8 000 8 000 6 000

3 900 9 600 21 000 2 000 8 000 12 000

Total overhead costs 41 000 70 500 56 500 Number of units 500 2 000 4 000 Cost per unit N$82,00 N$35,25 N$14,125

11. Summary Activity based Costing (ABC) is a recent development in product/service costing. It challenges the traditional approach of collecting all overhead costs in one cost centre which are then allocated to products using a volume base such as units of output, labours hours etc. With ABC, activities are identified and overheads collected according to those activities in centres called cost pools. A cost driver rate (base) is then identified for each cost pool and used to allocate overhead costs. The intention is to increase the accuracy of the allocation of resources consumed by products/services. The next unit will explore the techniques for managing inventory in an organisation.