Acquity group-2011-internet-retailer-top-500-commerce-audit final

35

2011 M-Commerce Audit Summary Internet Retailer 500 Q3 2011

-

Upload

e-commerce-news -

Category

Technology

-

view

737 -

download

1

Transcript of Acquity group-2011-internet-retailer-top-500-commerce-audit final

2011 M-Commerce Audit Summary Internet Retailer 500Q3 2011

© 2011 Acquity Group, LLC | Confidential & Proprietary | www.acquitygroup.com |

ACQUITY GROUP OVERVIEW

22

3

1 Top 5 independent digital agency – 2010 & 2011, Advertising Age

Who We Are

Acquity Group is a leading digital strategy, experience design, and online technology services firm.

» Headquartered in Chicago with 12 offices globally

» Over 475 experienced business, design, marketing and technology professionals

» We have been a trusted partner to more than 600 clients on thousands of projects

» One of the top five independent digital agencies in the country1

4

Partnering With The World’s Leading Brands

Acquity Group has worked with more than 600 clients over our ten year history, and is currently engaged with over 70 on a variety of initiatives.

Experience DesignHolistic site design

Ideation and concepting

Visual design

Information architecture

Usability assessments

Copywriting

Content development

Campaign dev. & execution

Mobile marketing

Content management and eCommerce platforms

Collaboration andsocial media

Mobile apps & sites

Front end development

Rich media

Digital Intelligence

Hosting & managed services

TechnologyBusiness strategy and ROI

Channel evaluation/planning

Digital marketing strategy

Web strategy

Content andcommerce strategy

Mobile & social strategy

User and market research

Measurement and analytics

Strategy

Deep Expertise Across Functions

5

© 2011 Acquity Group, LLC | Confidential & Proprietary | www.acquitygroup.com |

M-COMMERCE AUDIT OVERVIEW

66

7

The Mobile Commerce Audit. What is it?

Acquity Group performs an annual Mobile Commerce Audit in conjunction with Internet Retailer’s Top 500 and EU Top 300 guides to identify companies and industries on the leading edge of mobile initiatives, both in the US and the EU.

» Analysis of the top 500 online retailers

» Executed annually since 2009

» Also in conjunction with Internet Retailer, we perform a separate, detailed assessment of 375+ retailers, ticket sellers and travel/hospitality organizations active in the mobile channel to understand what tactics are being used: the Mobile Commerce Data Book.

2011 M-Commerce Audit: Candidate Identification

8

Selecting the pool of candidates…

» We start with the full list of 500 top online retailers, as ranked by Internet Retailer

» Multiple brands for one company were only considered in cases where two brands had significantly different desktop websites

» For companies who feature both retail and non-retail sites for their brand, only the retail sites were considered

» The final pool of candidates totaled 535 sites

2011 M-Commerce Audit: Mobile OSs

9

Six mobile operating systems were chosen to reflect the 2011 landscape:

» Each retailer’s site was tested on each of the following operating systems:

» If the retailer had a mobile specific site, it received one point

» The mobile site URL was recorded, as well as the URL extension

» Apple iPhone

» Android OS

» webOS

» Blackberry OS v. 5

» Blackberry OS v. 6

» Windows Phone 7

2011 M-Commerce Audit: Mobile Site Criteria

10

The following criteria were used as metrics for the successful adoption of an M-Commerce site:

» The checkout process cannot require any external dependencies outside of the mobile capabilities.

2011 M-Commerce Audit: App Availability

11

Testing process and scoring of mobile apps…

» Mobile Applications for each of the top 500 retailers were searched for at each of the following stores:

» Apple iTunes App Store» Google’s Android Marketplace» Blackberry App World» Palm’s App Catalog for webOS» Windows Mobile Marketplace

» Third party apps were not counted

2011 M-Commerce Audit: Final Ranking

12

» The final score for each site was calculated as the sum of both the Mobile Device Detection score and the Mobile Applications score (total of 42 points).

» Each site that registered at least one point was ranked by their final score.

» If sites had a common score, they were then ordered by their composite score breakdown: a site’s Mobile Device Detection score was given priority over their Mobile Applications score

» If sites still had a common score, they were then ordered by the following:

Devices supported > Mobile apps offered > Mobile Site Score > Redirect Score > Site Rendering Score > Optimization Score > Checkout/Booking Score » If sites still had a common score, they were finally ordered by their Top

500 rank awarded by Internet Retailer.

© 2011 Acquity Group, LLC | Confidential & Proprietary | www.acquitygroup.com |

M-COMMERCE AUDIT HIGHLIGHTS

1313

Annual Comparison

14

12% of sites compatible with mobile browsers

11% of sites optimized for iPhone

7% had downloadable apps

2010 37% of sites compatible with mobile browsers

9% of sites optimized for iPhone

26% had downloadable apps

2011

Interesting Numbers

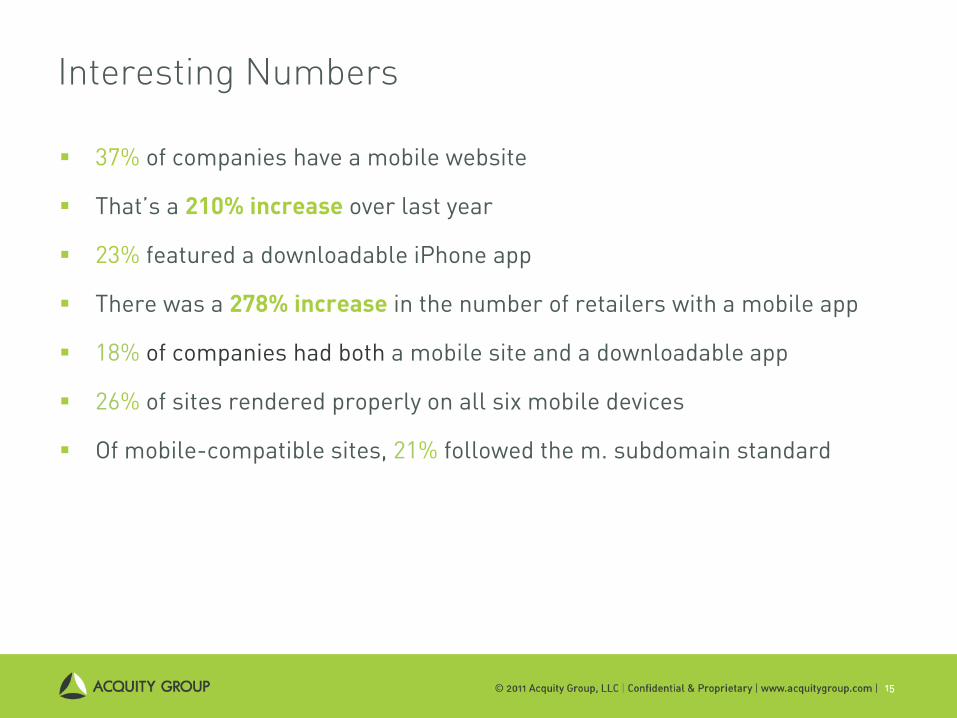

37% of companies have a mobile website

That’s a 210% increase over last year

23% featured a downloadable iPhone app

There was a 278% increase in the number of retailers with a mobile app

18% of companies had both a mobile site and a downloadable app

26% of sites rendered properly on all six mobile devices

Of mobile-compatible sites, 21% followed the m. subdomain standard

15

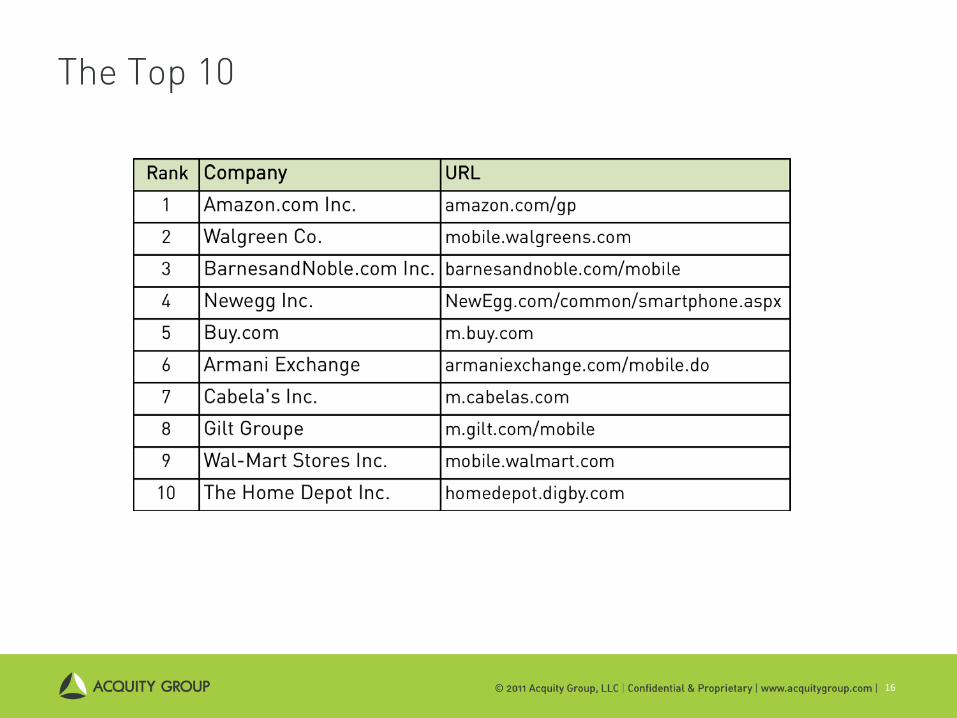

The Top 10

16

Notable Findings

17

Key Finding Conclusion

While 23% of companies featured a downloadable iPhone app, very few had Blackberry or webOS apps. Android, with 20% growth over last year, had the highest rate of growth.

There were massive gains in both the number of top retailers with a mobile site (37%, a 210% increase) and the number with a mobile app (26%, a 278% increase).

Even though the overall number of sites didn’t change from our 2010 analysis, the ticket industry showed the highest percentage-changes, with the largest growth in site redirection and checkout abilities.

In the ticket industry, differentiation and market share is related to value-added services, including mobile capabilities. Simply put, a company in this industry cannot maintain a competitive edge without offering ticket purchase & management on mobiles devices.

2011 was the year that mobile truly took hold – and took off. Although there is still tremendous room for growth, retailers have accepted mobile as a key platform for growth and customer engagement.

Retailers are following the general industry trend to the two top smartphone platforms in the US: iOS and Android. Any mobile applications on the other platforms seemed to be supplementary.

Mobile App Presence

18

23%

10%

3%0%

3%

% have iPhone app

% have Android app

% have Windows Phone

7 app

% have WebOS app

% have Blackberry app

Mobile App Adoption in 2011

© 2011 Acquity Group, LLC | Confidential & Proprietary | www.acquitygroup.com |

M-COMMERCE AUDIT INDUSTRY DETAILS

1919

Apparel: Industry Usage (n=71)

20

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Industry Usage

Total Usage

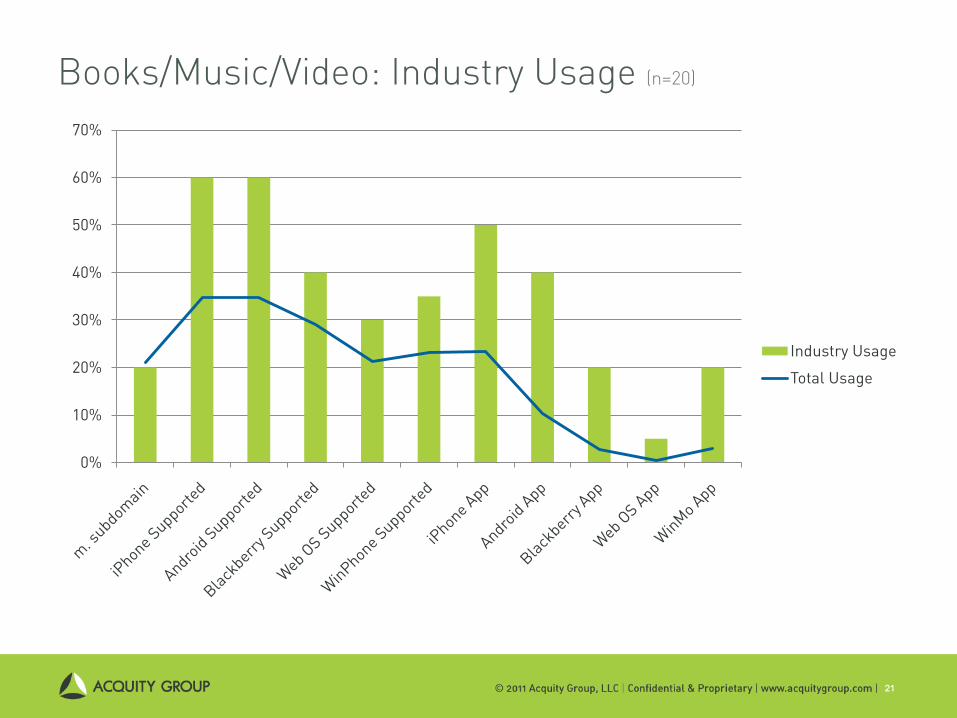

Books/Music/Video: Industry Usage (n=20)

21

0%

10%

20%

30%

40%

50%

60%

70%

Industry Usage

Total Usage

Computer/Electronics: Industry Usage (n=23)

22

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Industry Usage

Total Usage

Food/Drug: Industry Usage (n=16)

23

0%

10%

20%

30%

40%

50%

60%

70%

Industry Usage

Total Usage

Flowers/Gifts: Industry Usage (n=3)

24

0%

20%

40%

60%

80%

100%

120%

Industry Usage

Total Usage

Health/Beauty: Industry Usage (n=10)

25

0%

10%

20%

30%

40%

50%

60%

70%

80%

Industry Usage

Total Usage

Hardware/Home Improvement: Industry Usage (n=11)

26

0%

20%

40%

60%

80%

100%

120%

Industry Usage

Total Usage

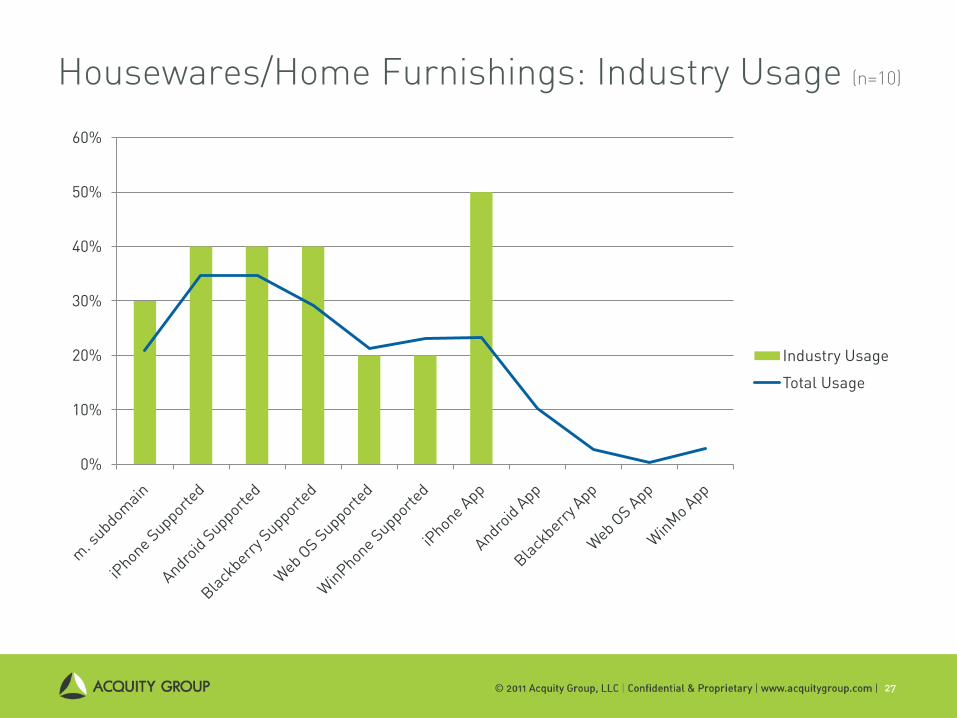

Housewares/Home Furnishings: Industry Usage (n=10)

27

0%

10%

20%

30%

40%

50%

60%

Industry Usage

Total Usage

Jewelry: Industry Usage (n=6)

28

0%

20%

40%

60%

80%

100%

120%

Industry Usage

Total Usage

Mass Merchant: Industry Usage (n=17)

29

0%

10%

20%

30%

40%

50%

60%

70%

Industry Usage

Total Usage

Office Supplies: Industry Usage (n=6)

30

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Industry Usage

Total Usage

Shoes: Industry Usage (n=13)

31

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Industry Usage

Total Usage

Sporting Goods: Industry Usage (n=8)

32

0%

20%

40%

60%

80%

100%

120%

Industry Usage

Total Usage

Specialty/Non Apparel: Industry Usage (n=18)

33

0%

10%

20%

30%

40%

50%

60%

Industry Usage

Total Usage

Toys/Hobbies: Industry Usage (n=24)

34

0%

10%

20%

30%

40%

50%

60%

70%

Industry Usage

Total Usage

Tom Nawara – VP, Digital Strategy & Design(312) 427-2058 | [email protected]

Matt Schmeltz – EVP Sales & Marketing(312) 427-2040 | [email protected]